Introduction

Adults affected by frailty, physical or cognitive impairments, mental illness or abrupt life transitions can face difficulties in managing their finances (Bleijenberg et al. Reference Bleijenberg, Smith, Lee, Cenzer, Boscardin and Covinsky2017; Berezuk et al. Reference Berezuk, Ramirez, Black and Zakzanis2018; Li et al. Reference Li, Wang and Hersch Nicholas2022). Consequently, they can benefit from assistance with purchases, paying bills, managing a budget or navigating online banking platforms. In this sense, the Lawton Instrumental Activities of Daily Living (IADL) Scale identifies the ‘ability to handle finances’ as one of eight crucial factors in assessing the need for care (Lawton and Brody Reference Lawton, Brody and Tate2010). Third-party money management (TPMM) – the management of someone else’s assets (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005) – is thus an important part of care practice. How it is approached is essential for care recipients’ financial wellbeing, self-determination and overall quality of life.

There are several societal developments that challenge independent financial management and increase the financial assistance needs of people in need of long-term care (LTC). Firstly, the global societal tendency towards liberalized welfare-state provisions has shifted the responsibility for financial wellbeing in old age from states to individuals (e.g. increasing pressures for private funding of pensions and LTC systems). This pushes individuals to increasingly engage in long-term financial planning concerning needs in later life, health and LTC (Price Reference Price, Bennett, Avram and Austen2024). Relatedly, this prompts individuals to develop and maintain higher levels of financial capacity throughout their lifespan, including in later life. However, previous research has shown that, currently, overall levels of financial literacy are low; for example, in 2023 only 58 per cent of adults across OECD (Organisation for Economic Co-operation and Development) countries scored the minimum target financial knowledge score (Lusardi Reference Lusardi2019; OECD 2023). Secondly, declining health status and impaired cognitive functions increase the likelihood of diminished financial literacy and/or financial capacity in advanced age (Pinsker et al. Reference Pinsker, Pachana, Wilson, Tilse and Byrne2010; Finke et al. Reference Finke, Howe and Huston2017; MacLeod et al. Reference MacLeod, Musich, Hawkins and Armstrong2017; Leung et al. Reference Leung, Parial, Szeto and Koduah2022). With dementia and other cognitive impairments becoming more prevalent in societies around the globe (Karthika et al. Reference Karthika, Abraham, Kodali, Mathews and Irudaya Rajan2025; OECD 2025), care needs in general and, specifically, assistance with financial matters increase (Prince et al. Reference Prince, Bryce, Albanese, Wimo, Ribeiro and Ferri2013; Bai et al. Reference Bai, Chen, Cai, Zhang, Su, Cheung, Jackson, Sha and Xiang2022). Thirdly, digitalization affects independent as well as third-party money management. Banking services continually reduce face-to-face consultation options, prompting customers to engage in digital self-management, thereby increasing the need for assistance with operating digital devices or delegating financial matters to others (Dai et al. Reference Dai, Miedema, Hernandez, Sutton-Lalani and Moffatt2023; Sutton-Lalani et al. Reference Sutton-Lalani, Hernandez, Miedema, Dai and Omrane2023). Furthermore, certain personal banking practices, such as the use of paper cheques, have changed due to digitalization, affecting TPMM as certain modalities of payment delegation became no longer available (Vines et al. Reference Vines, Dunphy, Blythe, Lindsay, Monk and Olivier2012). Digitalization becomes challenging as certain groups face greater digital exclusion than others. People with physical or cognitive impairments can, for example, experience digital exclusion as the design of digital services and devices often disregards their needs and preferences, creating barriers to effective use (Cham et al. Reference Cham, Cheah, Cheng and Lim2022; Money et al. Reference Money, Hall, Harris, Eost-Telling, Mcdermott and Todd2024; Mubarak and Suomi Reference Mubarak and Suomi2022; Rahman et al. Reference Rahman, Kordovski, Tierney and Woods2021).

TPMM can be understood as a way to ensure that individuals receive the assistance they need to avoid falling victim to scams. On the other hand, TPMM can also be a risk factor since close others acting as carers were in some cases found to conduct financial exploitation (Karthika et al. Reference Karthika, Abraham, Kodali, Mathews and Irudaya Rajan2025). A large body of literature has discussed this sensitive issue and identified heightened risks for older adults with care needs due to higher rates of impairments as well as the occurrence of important life shifts such as the loss of a spouse or relocating to care facilities (Setterlund et al. Reference Setterlund, Tilse, Wilson, McCawley and Rosenman2007; Wood and Lichtenberg Reference Wood and Lichtenberg2017; Wood et al. Reference Wood, Lichtenberg, Purewal, Garcia, Garcia, Mccleary and Drummond2020; Jerrim et al. Reference Jerrim, Lopez-Agudo and Marcenaro-Gutierrez2022; Brancale and Blomberg Reference Brancale and Blomberg2023). Experience reports also suggest difficulties faced by informal carers including the navigation of relationship dynamics, risk management, third-party access and the need for privacy (see, for example, blog entries of support networks for informal carers: Bradley n.d.; CaringInfo n.d.; Huddleston 2024).

Although the relevance and importance of TPMM for adults with care needs and their care-givers is evident, as is the complexity of issues at stake, it remains unclear how it is being implemented in LTC as only a little research has been conducted on TPMM practices so far. Such practices seem closely entangled with personal (care) relationships, which can be shaped by situations of dependency, differing interests about financial means and spending habits, difficulties in communication and not least the respective financial resources at hand. Respecting the personal autonomy of persons receiving assistance with money management is a key challenge in this context. In line with a heightened focus on autonomy and agency in research and practice concerning later life, ageing and disabilities, substitute financial and medical decision-making underwent adaptation: In recent years, many countries updated their legislation on guardianship to enhance shared decision-making, preserve care recipients’ rights and prevent coercion (Boyle Reference Boyle2013; Then Reference Then2013; Dinerstein et al. Reference Dinerstein, Grewal and Martinis2016). However, it remains unclear to what extent this policy change to support autonomy of people in need of care has manifested and what this means for TPMM and care practice.

This scoping review aims to summarize the existing knowledge on TPMM for adults in need of LTC. It intends to (a) report on the scope and characteristics of TPMM practices; (b) identify relevant dimensions of TPMM practices to enhance understanding of TPMM and facilitate performance-evaluation; and (c) synthesize criteria for good TPMM practice to balance personal autonomy in money management and support by carers. Based on this extensive review of existing research, the findings aim to support a better understanding of current TPMM practices and their relation to laws, organizational guidelines, norms and instruments. The article identifies TPMM as highly under-researched, highlights key research gaps for future studies, and provides a conceptual framework for future studies on TPMM.

Study design and methods

We conducted a scoping review, following a systematic approach to data collection and documentation according to PRISMA-ScR (Tricco et al. Reference Tricco, Lillie, Zarin, O’Brien, Colquhoun, Levac, Moher, Peters, Horsley, Weeks, Hempel, Akl, Chang, McGowan, Stewart, Hartling, Aldcroft, Wilson, Garritty and Straus2018). The detailed protocol can be found in the appendix. We opted for a scoping review as it was better suited than systematic reviews to answer broader questions and to retrieve literature via multiple channels. The search was mainly conducted by the first and third authors.

Information sources

For the search, we used the scientific research platforms Scopus (Scopus proprietary), ProQuest (including the databases ABI/INFORM Global, International Bibliography of the Social Sciences, and Sociology Collection) and EBSCO (including the databases Library, Information Science and Technology Abstracts, PSYNDEX Literature with PSYNDEX Tests, AgeLine, Abstracts in Social Gerontology, ERIC, MEDLINE, APA PsycArticles, eBook Open Access [OA] Collection, Communication Abstracts, OpenDissertations, and Teacher Reference Center) to cover a broad basis of social scientific journals. Additional searches via Google Scholar helped in detecting further texts relevant to the search not yet included in the databases. Additionally, we used citation search via the studies’ reference lists.

Database search: keywords and time frame

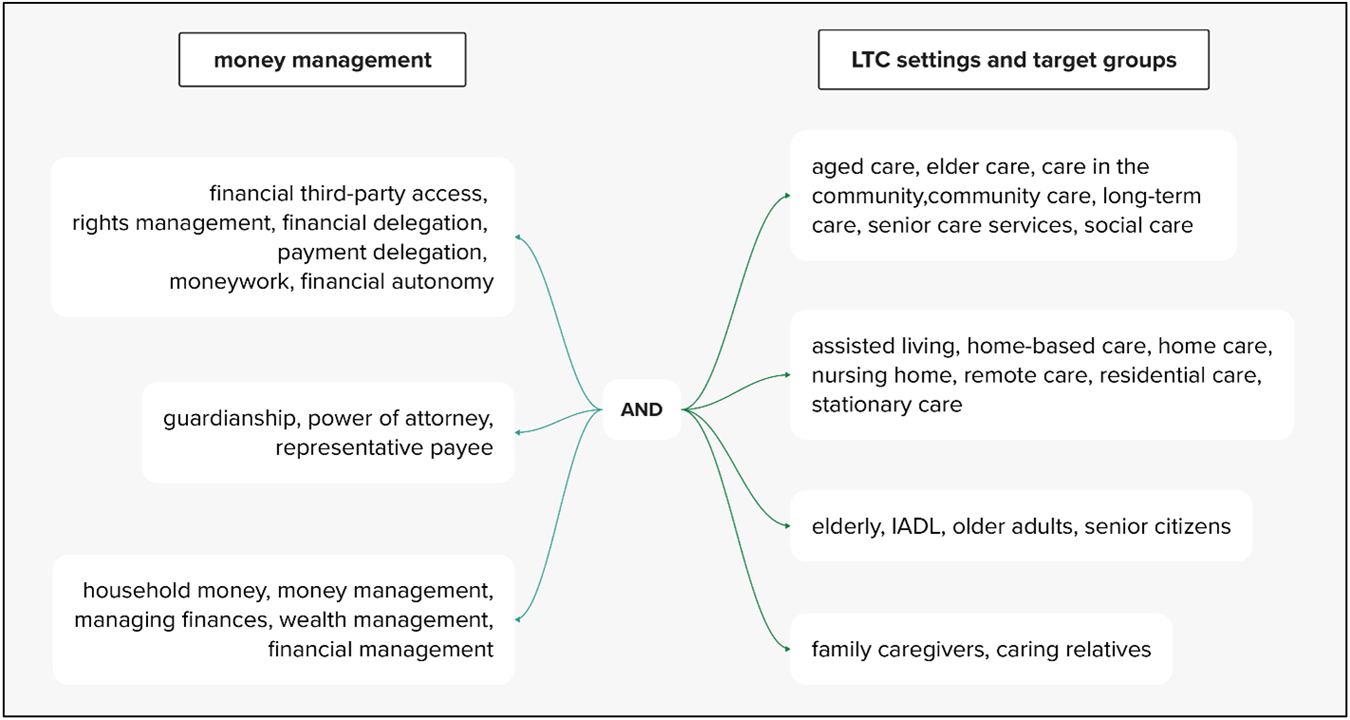

In developing our search strategy, we tested the specificity and sensitivity of the descriptors in preliminary searches. This was done by the first author with feedback from the second and third authors. Identifying the most relevant keywords took several attempts and adaptations as there are many different expressions used for TPMM (see Fig. 1). These concepts were grouped by the Boolean operator OR. As displayed in Figure 1, we additionally used broader terms for money management and used the Boolean operator AND to link them with a second group of concepts (again linked with OR) describing the different LTC settings and target groups (elderly care recipients and family care-givers).

Keyword combination used in the TPMM literature search.

We considered publications in English and German, published between 2000 and 2024. The search string used for the database search can be found in the Appendix.

Screening and selection strategy

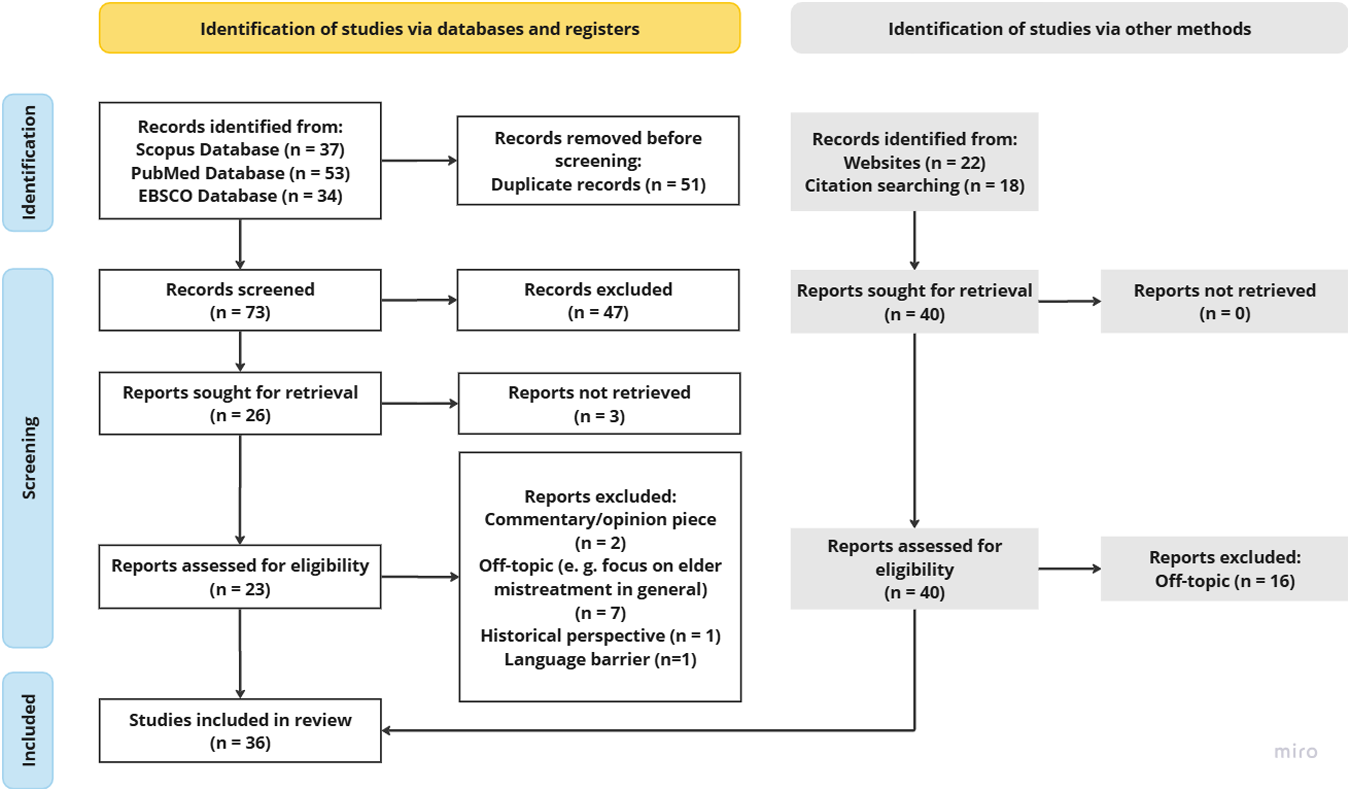

The database search yielded 124 results; 51 duplicates were removed. The first author screened 73 records (titles and abstracts) and excluded 47 articles based on predefined inclusion and exclusion criteria. Further articles were collected through websites and citation search by the first author and the third author (n = 39). This was done separately and then the results were compared. To be selected for the analysis, articles had to deal with money management in the context of LTC or TPMM in other contexts. The publications had to refer to certain groups: older adults, persons experiencing IADL impairments and/or their carers. Related topics, such as digital banking practices or financial capacity measurement, were considered only if they provided insights into the money management practices, needs and specific requirements of carers or care recipients.

In total, 55 articles were sought for retrieval, three of which could not be retrieved. Thus, 52 papers underwent full-text screening, of which 27 were excluded because their thematic focus was too wide (e.g. digitalization in the care home sector), too narrow or off-topic (e.g. medical assessments of financial capacity). Papers were also excluded in case (a) the type of text was neither scientific nor empirical, but represented the authors’ opinion only; (b) the paper’s focus was on older adults only without discussing any sort of care context; (c) the text applied a strictly historical perspective; or (d) the text was in a language other than English or German. Figure 2 shows the progression of the paper selection.

Selection of records following .Haddaway et al. (Reference Haddaway, Page, Pritchard and McGuinness2022).

Synthesis of results

The studies included in the review were analysed via qualitative content analysis. We used both deductive and inductive coding according to Mayring and Fenzl (Reference Mayring, Fenzl, Baur and Blasius2019). First, broad categories were used for the initial coding including ‘practices of third-party money management’, ‘formalised v. non-formalized arrangements’, ‘banking modalities’, ‘care settings’ and ‘solutions’. Second, open coding helped in differentiating the results and considering additional categories and aspects such as ‘substitute v. supported decision-making’. The synthesis was first done by the first author, with the third author providing feedback. Then the results were discussed, refined and edited collaboratively by all authors in a series of workshops.

Results

The search yielded 36 articles for the final review. Table 1 gives an overview of the studies selected for the analysis.

Studies on third-party money management selected for the analysis (sorted by the first author A–Z)

* Papers related to results sections 1–3 (see below)

Characteristics and thematic emphases of the included studies

Distribution over time and locations

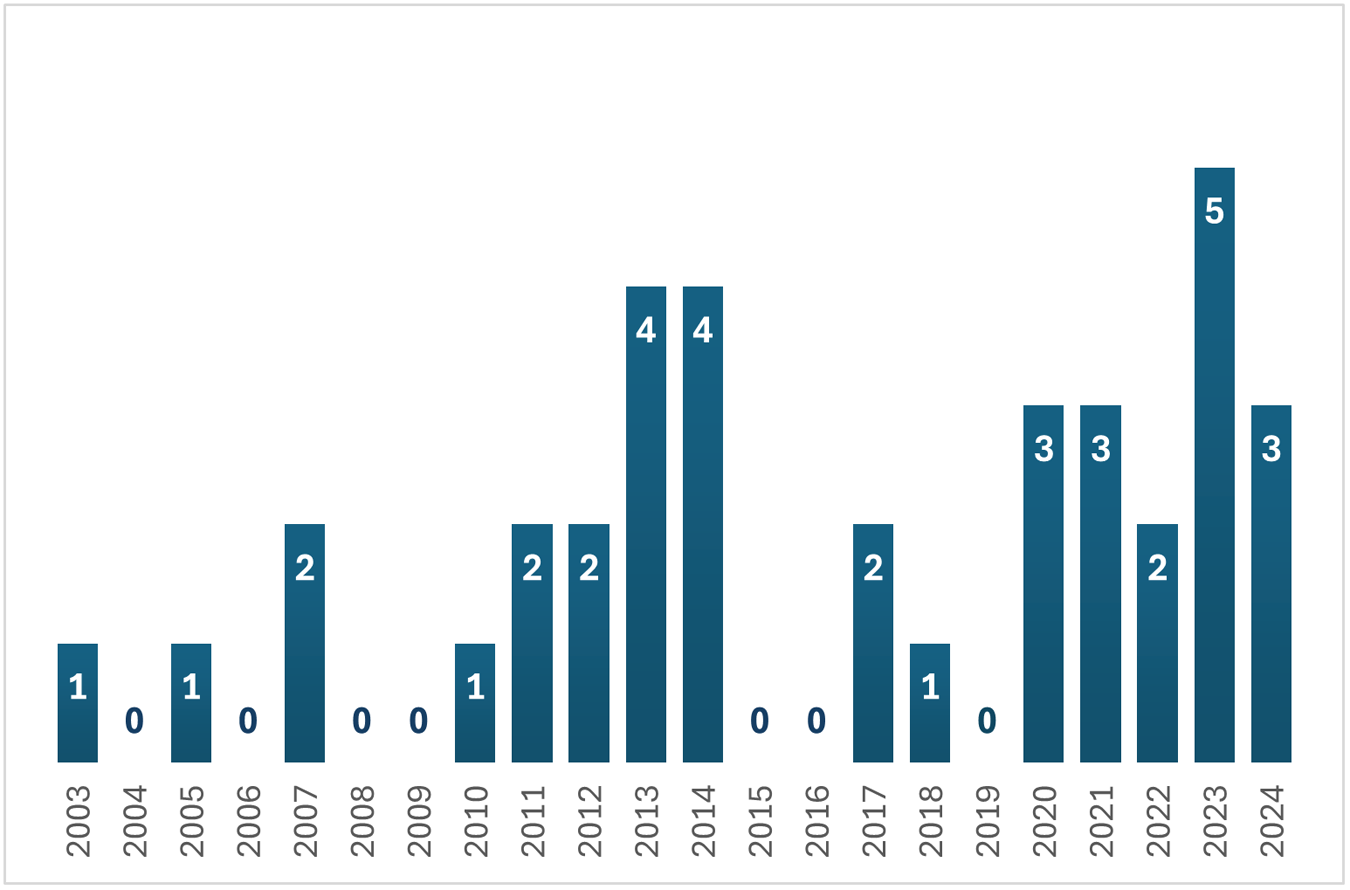

The studies included were published between 2003 and 2024. Most of them (n = 19) were published from 2017 to 2024, with more than a quarter of all studies (n = 10) released between 2022 and 2024 (see Figure 3). Most of the empirical studies assessed in this article were conducted in the United States (US) (n = 13), the United Kingdom (UK) (n = 10) and Australia (n = 6). A few studies were based in Canada (n = 2), Germany (n = 1) and the US and Canada (n = 1).

Number of publications per year.

Methods

Generally, a mixed set of methods was applied to the study of TPMM and related issues (see Table 1). Among the empirical studies, the majority (n = 24) conducted qualitative studies (interviews and focus groups, qualitative case studies, document analyses or qualitative prototype evaluations). Four studies reviewed and discussed previous research findings (Mitchell et al. Reference Mitchell, Pachana, Wilson, Vearncombe, Massavelli, Byrne and Tilse2014; Wood et al. Reference Wood, Lichtenberg, Purewal, Garcia, Garcia, Mccleary and Drummond2020; Dai et al. Reference Dai, Miedema, Hernandez, Sutton-Lalani and Moffatt2023; Price Reference Price, Bennett, Avram and Austen2024). Seven studies applied quantitative methods (Elbogen et al. Reference Elbogen, Swanson, Swartz and Wagner2003; Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005, Reference Tilse, Setterlund, Wilson and Rosenman2007; Rosen et al. Reference Rosen, Ablondi, Black, Serowik and Rowe2014; Tillmann et al. Reference Tillmann, Schnakenberg, Weckbecker, Just, Weltermann and Münster2020; Latulipe et al. Reference Latulipe, Dsouza and Cumbers2022; Wang et al. Reference Wang, Morphew, Vitale, Mullan and Zietlow2023), most of which, however, used small samples or open-ended questions. Only two studies (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005; Belbase et al. Reference Belbase, Sanzenbacher and Walters2020) referred to national surveys. The Australian study by Tilse et al. (Reference Tilse, Setterlund, Wilson and Rosenman2005) is the only one from our sample working with a sound body of data on the prevalence and characteristics of non-professional TPMM. However, this is also the second oldest study in our sample, meaning that its results may be outdated. Due to the dominance of small-scale studies and qualitative methods, our synthesis relies largely on highly localized empirical results.

Thematic clusters

Among the analysed studies, we identified two larger and six smaller thematic clusters. The first cluster is closest to our research interest. It explicitly dealt with practices and experiences of persons engaging in TPMM as a part of care practice, mostly within informal care contexts (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005, Reference Tilse, Setterlund, Wilson and Rosenman2007, Reference Tilse, Wilson, Rosenman, Morrison and McCawley2011; Plander Reference Plander2013; Dunphy et al. Reference Dunphy, Monk, Vines, Blythe and Olivier2014; McLoughlin and Stern Reference McLoughlin and Stern2017; Labrum Reference Labrum2018; Latulipe et al. Reference Latulipe, Dsouza and Cumbers2022; Qiu et al. Reference Qiu, Blair and Abdullah2024). Two studies within this first cluster also consulted staff members or managers of care organizations (Dunphy et al. Reference Dunphy, Monk, Vines, Blythe and Olivier2014; Latulipe et al. Reference Latulipe, Dsouza and Cumbers2022), and only one paper focused exclusively on a formal care setting (Tilse et al. Reference Tilse, Wilson, Rosenman, Morrison and McCawley2011).

The second, slightly larger cluster discussed formalized arrangements of TPMM such as guardianship, power of attorney (PoA) or representative payee systems (specific to Medicare beneficiaries in the US). The studies were concerned with the application processes (Elbogen et al. Reference Elbogen, Swanson, Swartz and Wagner2003; Mitchell et al. Reference Mitchell, Pachana, Wilson, Vearncombe, Massavelli, Byrne and Tilse2014; Rosen et al. Reference Rosen, Ablondi, Black, Serowik and Rowe2014; Mills Reference Mills2017; Tillmann et al. Reference Tillmann, Schnakenberg, Weckbecker, Just, Weltermann and Münster2020; Connolly and Peisah Reference Connolly and Peisah2023; Wang et al. Reference Wang, Morphew, Vitale, Mullan and Zietlow2023) experiences or (best) practices (Serowik et al. Reference Serowik, Bellamy, Rowe and Rosen2013; Creasy et al. Reference Creasy, Olaniyan, Davis and Hawk2021; Nwakasi and Roberts Reference Nwakasi and Roberts2022; Giebel et al. Reference Giebel, Halpin, O’Connell and Carton2023a).

Six smaller clusters addressed the modalities of digital banking for TPMM (Barros Pena et al. Reference Barros Pena, Kursar, Clarke, Alpin, Holkar and Vines2021; Dai et al. Reference Dai, Miedema, Hernandez, Sutton-Lalani and Moffatt2023; Giebel, Halpin, O’Connell et al. Reference Giebel, Halpin, O’Connell and Carton2023; Havens and Latulipe Reference Havens and Latulipe2024), financial exploitation of older adults (Setterlund et al. Reference Setterlund, Tilse, Wilson, McCawley and Rosenman2007; Wood et al. Reference Wood, Lichtenberg, Purewal, Garcia, Garcia, Mccleary and Drummond2020; Schmidt et al. Reference Schmidt, Stowell, Pacini and Patterson2022), personal banking practices in relation to TPMM more broadly (Vines et al. Reference Vines, Blythe, Dunphy and Monk2011, Reference Vines, Dunphy, Blythe, Lindsay, Monk and Olivier2012; Kaye et al. Reference Kaye, McCuistion, Gulotta and Shamma2014), effects of TPMM on financial wellbeing and quality of life (Svare and Anngela-Cole Reference Svare and Anngela-Cole2010; Belbase et al. Reference Belbase, Sanzenbacher and Walters2020), the gendered dynamics of money management among (care-giving) spouses (Bisdee et al. Reference Bisdee, Daly and Price2013; Boyle Reference Boyle2013; Price Reference Price, Bennett, Avram and Austen2024) and a specific service programme for money management assistance (Sacks et al. Reference Sacks, Das, Romanick, Caron, Morano and Fahs2012).

We could not identify any definitive thematic trends among the TPMM studies in our review over the study period. However, our findings suggest an increased focus on digitalization and its impact on TPMM in recent years. Recently, more attention has also been paid to topics related to preventive measures in dementia care and the role of medical personnel in TPMM processes. Additionally, recent research indicates an increase in nuanced reports on TPMM practices within guardianship and representative payee service provision.

Adding to the descriptive analysis of the body of studies we retrieved, the subsequent sections of the paper will present findings from the content analysis. The findings are organized in three results sections according to the research interests outlined in the introduction.

Results 1: scope and characteristics of TPMM

One representative study in our sample (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005) and information from 22 further studies referring to the variety of circumstances, causes and care arrangements of TPMM were included. (Elbogen et al. Reference Elbogen, Swanson, Swartz and Wagner2003; Setterlund et al. Reference Setterlund, Tilse, Wilson, McCawley and Rosenman2007; Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2007; Sacks et al. Reference Sacks, Das, Romanick, Caron, Morano and Fahs2012; Bisdee et al. Reference Bisdee, Daly and Price2013; Serowik et al. Reference Serowik, Bellamy, Rowe and Rosen2013; Boyle Reference Boyle2013; Plander Reference Plander2013; Rosen et al. Reference Rosen, Ablondi, Black, Serowik and Rowe2014; Kaye et al. Reference Kaye, McCuistion, Gulotta and Shamma2014; Dunphy et al. Reference Dunphy, Monk, Vines, Blythe and Olivier2014; McLoughlin and Stern Reference McLoughlin and Stern2017; Labrum Reference Labrum2018; Belbase et al. Reference Belbase, Sanzenbacher and Walters2020; Barros Pena et al. Reference Barros Pena, Kursar, Clarke, Alpin, Holkar and Vines2021; Creasy et al. Reference Creasy, Olaniyan, Davis and Hawk2021; Latulipe et al. Reference Latulipe, Dsouza and Cumbers2022; Nwakasi and Roberts Reference Nwakasi and Roberts2022; Connolly and Peisah Reference Connolly and Peisah2023; Giebel, Halpin, Tottie et al. Reference Giebel, Halpin, Tottie, O’Connell and Carton2023; Price Reference Price, Bennett, Avram and Austen2024; Qiu et al. Reference Qiu, Blair and Abdullah2024).

A national representative survey conducted in Australia in 2002 found that 71 per cent of the persons receiving help with money matters were 65 or older (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005). Further research shows that help with managing finances is mostly related to experiencing limited decision-making capacity due to physical health-care needs, frailty or dementia (Setterlund et al. Reference Setterlund, Tilse, Wilson, McCawley and Rosenman2007; Belbase et al. Reference Belbase, Sanzenbacher and Walters2020), the experience of digital financial exclusion (Giebel, Halpin, Tottie et al. Reference Giebel, Halpin, Tottie, O’Connell and Carton2023), social isolation or abrupt changes such as the loss of a partner who used to manage household finances, or a sudden financial or health-related problem (Setterlund et al. Reference Setterlund, Tilse, Wilson, McCawley and Rosenman2007; Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2007; McLoughlin and Stern Reference McLoughlin and Stern2017; Sacks et al. Reference Sacks, Das, Romanick, Caron, Morano and Fahs2012; Plander Reference Plander2013; Connolly and Peisah Reference Connolly and Peisah2023; Qiu et al. Reference Qiu, Blair and Abdullah2024). Some studies suggest that among older adults, women more often need assistance with money management due to traditional gender roles prescribing the roles of breadwinner and household money manager to male partners (Bisdee et al. Reference Bisdee, Daly and Price2013; Boyle Reference Boyle2013; Price Reference Price, Bennett, Avram and Austen2024).

Core dimensions characterizing TPMM practices.

The most common tasks that individuals receive help with are paperwork (e.g. filing health insurance claims), paying bills, making transfers, budgeting, monitoring balances, accessing money, dealing with pension matters and managing retirement savings, property, insurance or mortgage (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005; Sacks et al. Reference Sacks, Das, Romanick, Caron, Morano and Fahs2012; Latulipe et al. Reference Latulipe, Dsouza and Cumbers2022). It is important to consider, however, that personal care needs are highly diverse due to differences in health status, personal experience, financial situation, available assets, values, habits, beliefs as well as societal institutions including social security systems (Bisdee et al. Reference Bisdee, Daly and Price2013; Boyle Reference Boyle2013; Price Reference Price, Bennett, Avram and Austen2024).

For adults with mental health conditions, help with money management is often an important care requirement and well-recognized as part of treatment and care plans (Elbogen et al. Reference Elbogen, Swanson, Swartz and Wagner2003; Serowik et al. Reference Serowik, Bellamy, Rowe and Rosen2013; Labrum Reference Labrum2018; Creasy et al. Reference Creasy, Olaniyan, Davis and Hawk2021). Experiencing compulsory overspending in this context can result in requiring assistance with limit-setting and budgeting (Labrum Reference Labrum2018; Barros Pena et al. Reference Barros Pena, Kursar, Clarke, Alpin, Holkar and Vines2021). Affected persons face heightened risks of financial hardship, which further enhances assistance needs, for example to prevent homelessness (Elbogen et al. Reference Elbogen, Swanson, Swartz and Wagner2003; Rosen et al. Reference Rosen, Ablondi, Black, Serowik and Rowe2014).

Among informal carers, helping with money management is a highly prevalent task (Kaye et al. Reference Kaye, McCuistion, Gulotta and Shamma2014). Financial care-giving is mostly provided by family members, in some cases also by neighbours, friends or formal care workers (Elbogen et al. Reference Elbogen, Swanson, Swartz and Wagner2003; Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005; Dunphy et al. Reference Dunphy, Monk, Vines, Blythe and Olivier2014; Belbase et al. Reference Belbase, Sanzenbacher and Walters2020) and professional or volunteer guardians (or representative payees) (Creasy et al. Reference Creasy, Olaniyan, Davis and Hawk2021; Nwakasi and Roberts Reference Nwakasi and Roberts2022).

Results 2: practices and mechanisms of TPMM – formal schemes and grey areas

In this section, we report on 28 studies discussing practices relating to TPMM (Elbogen et al. Reference Elbogen, Swanson, Swartz and Wagner2003; Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005, Reference Tilse, Setterlund, Wilson and Rosenman2007, Reference Tilse, Wilson, Rosenman, Morrison and McCawley2011; Setterlund et al. Reference Setterlund, Tilse, Wilson, McCawley and Rosenman2007; Vines et al. Reference Vines, Blythe, Dunphy and Monk2011, Reference Vines, Dunphy, Blythe, Lindsay, Monk and Olivier2012; Boyle Reference Boyle2013; Serowik et al. Reference Serowik, Bellamy, Rowe and Rosen2013; Dunphy et al. Reference Dunphy, Monk, Vines, Blythe and Olivier2014; Rosen et al. Reference Rosen, Ablondi, Black, Serowik and Rowe2014; Kaye et al. Reference Kaye, McCuistion, Gulotta and Shamma2014; McLoughlin and Stern Reference McLoughlin and Stern2017; Mills Reference Mills2017; Labrum Reference Labrum2018; Belbase et al. Reference Belbase, Sanzenbacher and Walters2020; Wood et al. Reference Wood, Lichtenberg, Purewal, Garcia, Garcia, Mccleary and Drummond2020; Barros Pena et al. Reference Barros Pena, Kursar, Clarke, Alpin, Holkar and Vines2021; Creasy et al. Reference Creasy, Olaniyan, Davis and Hawk2021; Schmidt et al. Reference Schmidt, Stowell, Pacini and Patterson2022; Nwakasi and Roberts Reference Nwakasi and Roberts2022; Latulipe et al. Reference Latulipe, Dsouza and Cumbers2022; Connolly and Peisah Reference Connolly and Peisah2023; Dai et al. Reference Dai, Miedema, Hernandez, Sutton-Lalani and Moffatt2023; Giebel, Halpin, O’Connell et al. Reference Giebel, Halpin, O’Connell and Carton2023, Giebel, Halpin, Tottie et al. Reference Giebel, Halpin, Tottie, O’Connell and Carton2023; Havens and Latulipe Reference Havens and Latulipe2024; Qiu et al. Reference Qiu, Blair and Abdullah2024).

The studies investigating the state-of-the-art practices and mechanisms of TPMM showed substantial variation in TPMM practices resulting from care settings, legal and bureaucratic formalities, personal preferences and stakeholder perspective. Grouping the findings allowed us to define four dimensions of TPMM: (a) degree of formalization, (b) degree of collaboration, (b) type of care provision and (d) digitalization. Figure 4 shows the four dimensions of TPMM practices and their dichotomous characteristics. These four dimensions will now be explained in more detail.

Degree of formalization in TPMM: formalized and non-formalized mechanisms

Guardianship, power of attorney (PoA) (UK, Australia) or representative payee schemes (US) are formalized mechanisms for TPMM. These schemes can be either voluntary or mandatory. The latter result from a medical assessment of financial capacity. Guardians, attorneys or payees can be close others, lawyers, professionals or volunteers appointed by court. Appointed persons gain access to the care recipients’ funds and are authorized to make decisions on their behalf. On the one hand, these systems set clear boundaries and rules offering peace of mind to those who need it (Elbogen et al. Reference Elbogen, Swanson, Swartz and Wagner2003; McLoughlin and Stern Reference McLoughlin and Stern2017). On the other hand, care recipients’ personal autonomy is severely reduced (Belbase et al. Reference Belbase, Sanzenbacher and Walters2020). In 2005, 17 per cent of Australians aged 65+ had a guardian or PoA with higher prevalence in the older age group (80+) (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005; see also Setterlund et al. Reference Setterlund, Tilse, Wilson, McCawley and Rosenman2007; Latulipe et al. Reference Latulipe, Dsouza and Cumbers2022). Evidence suggests that demand for payees is rising (McLoughlin and Stern Reference McLoughlin and Stern2017). Despite the growing demand, it was found that awareness and knowledge of the legal mechanisms and their implications was low (Rosen et al. Reference Rosen, Ablondi, Black, Serowik and Rowe2014; Belbase et al. Reference Belbase, Sanzenbacher and Walters2020). Reaching out to people in need of assistance has proven difficult, and some may be left without the formal mechanism and support they need (Elbogen et al. Reference Elbogen, Swanson, Swartz and Wagner2003; Rosen et al. Reference Rosen, Ablondi, Black, Serowik and Rowe2014).

Further mechanisms for gaining third-party access are joint accounts (also called joint signatories or nominees) (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005; Setterlund et al. Reference Setterlund, Tilse, Wilson, McCawley and Rosenman2007; Havens and Latulipe Reference Havens and Latulipe2024) or third-party mandates (UK) (McLoughlin and Stern Reference McLoughlin and Stern2017). In these cases, designated persons are authorized to make certain financial decisions. Prerequisite for this arrangement is a trusted relationship between carers and care recipients.

Apart from these formalized mechanisms, the literature sketches the following non-formalized practices. First, according to several studies, credential sharing (sharing PINs or passwords) is common practice with family care-givers (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005; Setterlund et al. Reference Setterlund, Tilse, Wilson, McCawley and Rosenman2007; Havens and Latulipe Reference Havens and Latulipe2024) as well as care workers (Dunphy et al. Reference Dunphy, Monk, Vines, Blythe and Olivier2014). Sometimes, family care-givers even impersonate the care recipient by setting up an online banking account in their name. They then use the care recipients’ email address or phone number to communicate with the bank, thus avoiding compliance issues (Havens and Latulipe Reference Havens and Latulipe2024). In any case, credential sharing poses a substantial safety threat, as carers could easily exploit the situation, and care recipients would not be compensated by insurance (Dunphy et al. Reference Dunphy, Monk, Vines, Blythe and Olivier2014). Second, more recent studies found that assisting with online banking is among the most prevalent forms of help provided (Latulipe et al. Reference Latulipe, Dsouza and Cumbers2022; Havens and Latulipe Reference Havens and Latulipe2024). Third, furthermore, non-professional carers often engaged in advancing money to pay bills and getting reimbursed or reimbursing themselves afterwards (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005; Latulipe et al. Reference Latulipe, Dsouza and Cumbers2022). Dunphy et al. (Reference Dunphy, Monk, Vines, Blythe and Olivier2014) also found this to be the case for formal care workers. Fourth, some informal carers merged the accounts of those they cared for into their own to simplify their caring tasks and manage TPMM via online banking (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005; Kaye et al. Reference Kaye, McCuistion, Gulotta and Shamma2014). Alarmingly, the intermingling of accounts is difficult to audit and blurs the boundaries between personal transactions and transactions made on behalf of someone else (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005; Setterlund et al. Reference Setterlund, Tilse, Wilson, McCawley and Rosenman2007). Fifth, some carers made individual arrangements with local shops allowing the care recipients to keep running shopping errands without having to care about money (Boyle Reference Boyle2013). Later the carers would pay the bills. Sixth, in many cases, carers installed automatized bill payments (direct debits) to simplify regular bill payments for the care recipients (Boyle Reference Boyle2013; Wood et al. Reference Wood, Lichtenberg, Purewal, Garcia, Garcia, Mccleary and Drummond2020; Latulipe et al. Reference Latulipe, Dsouza and Cumbers2022). Seventh, finally, many carers accompany care recipients to a local bank branch and help with in-person banking (Latulipe et al. Reference Latulipe, Dsouza and Cumbers2022).

Both formalized and non-formalized mechanisms bear risks of potential misconduct and financial exploitation. Non-formalized arrangements often operate in legal grey areas, providing opportunities for misuse. Formalized mechanisms, on the other hand, give carers substantial decision-making power, which could lead to exploitation. While the threat of financial exploitation by guardians is high and some cases have been recorded (e.g. misappropriation of finances or neglect of the care recipient’s needs), this form of abuse is difficult to detect (Nwakasi and Roberts Reference Nwakasi and Roberts2022; Schmidt et al. Reference Schmidt, Stowell, Pacini and Patterson2022).

Degree of collaboration in TPMM: substitute v. supported decision-making

Practices of TPMM can be differentiated by the degree of collaboration encouraged in the care relationship, for example whether care recipients receive support with money management tasks or whether the carers carry out banking tasks on behalf of care recipients. Generally, providing support is considered more demanding and time-consuming for carers than substitute decision-making (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2007). Latulipe et al. (Reference Latulipe, Dsouza and Cumbers2022), for example, reported only one among the interviewed family care-givers made the effort to navigate the person they care for through the online banking processes to retain their independence instead of merely acting on their behalf (Havens and Latulipe Reference Havens and Latulipe2024). The tendency towards delegation in these cases was closely related to a lack of practical solutions for assistance, in particular concerning bank policies: only if a joint account was put in place or if the older adult was declared incompetent did the bank provide the carer with a proxy account. In-person banking was the only alternative for helping with money management without having to declare the care recipient incompetent, which most carers deemed inconvenient.

Guardianship and PoA schemes have generally been criticized for prompting an all-or-nothing decision that fails to recognize the continuum of care needs between requiring help and lacking decision-making capacity (Latulipe et al. Reference Latulipe, Dsouza and Cumbers2022). Connolly and Peisah (Reference Connolly and Peisah2023) found that, too often, guardianship was appointed without considering alternatives to substitute decision-making. Overall, scholars suggested that substitute decision-making is over-emphasized, with the result that care recipients’ wishes are easily overruled (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005; Boyle Reference Boyle2013; Belbase et al. Reference Belbase, Sanzenbacher and Walters2020; Latulipe et al. Reference Latulipe, Dsouza and Cumbers2022). However, guardianship or PoA does not necessarily imply a loss of all decision-making power. Instead, individual arrangements can be made to allow shared decision-making, helping care recipients to set priorities and negotiate control mechanisms (Serowik et al. Reference Serowik, Bellamy, Rowe and Rosen2013; Creasy et al. Reference Creasy, Olaniyan, Davis and Hawk2021; see section 'Results 3: ensuring good TPMM practice to balance autonomy and care').

Type of care provision in TPMM: financial care-giving through formal and informal carers

Only a small number of publications discussed how TPMM was conducted in formal care settings. These studies found that care organizations operated in highly diverse ways: for example, some care homes set up little shops for their residents; others collected money from their residents before running errands; and some managed a pool of money handed out to residents upon request (Vines et al. Reference Vines, Blythe, Dunphy and Monk2011, Reference Vines, Dunphy, Blythe, Lindsay, Monk and Olivier2012; Dunphy et al. Reference Dunphy, Monk, Vines, Blythe and Olivier2014). They all had one thing in common: high levels of responsibility. Care home managers had to keep track of residents’ spending and make sure that their valuables were safe (Vines et al. Reference Vines, Dunphy, Blythe, Lindsay, Monk and Olivier2012). In certain cases, they were responsible for handling allegations of theft against staff members (Tilse et al. Reference Tilse, Wilson, Rosenman, Morrison and McCawley2011). Therefore, risk minimization was in some cases favoured over assistance with personal money management (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005, Reference Tilse, Wilson, Rosenman, Morrison and McCawley2011). Relatedly, a lack of well-established guidelines and training in TPMM for care staff resulted in insecurity and avoidance to engage in TPMM (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005; Dunphy et al. Reference Dunphy, Monk, Vines, Blythe and Olivier2014). Similarly, resource constraints caused care organizations to abstain from assisted decision-making, which was seen as resource-intensive and difficult to facilitate (Tilse et al. Reference Tilse, Wilson, Rosenman, Morrison and McCawley2011). Furthermore, not all care organizations viewed money management as their responsibility but instead considered it a family matter and automatically referred to substitute decision-makers (PoAs) (Tilse et al. Reference Tilse, Wilson, Rosenman, Morrison and McCawley2011).

In informal care contexts, help with money management was mostly expected and carried out by care recipients’ kids or spouses (Havens and Latulipe Reference Havens and Latulipe2024). In many cases, this was found to benefit care recipients as family members can be close, provide comfort, take good care of their relatives and help them out financially if need be (Elbogen et al. Reference Elbogen, Swanson, Swartz and Wagner2003; Labrum Reference Labrum2018; Belbase et al. Reference Belbase, Sanzenbacher and Walters2020; Barros Pena et al. Reference Barros Pena, Kursar, Clarke, Alpin, Holkar and Vines2021). However, there were several risk factors associated with informal financial care-giving. Firstly, many carers experienced it as burdensome and emotionally stressful (Labrum Reference Labrum2018; Mills Reference Mills2017; Giebel, Halpin, Tottie et al. Reference Giebel, Halpin, Tottie, O’Connell and Carton2023; Qiu et al. Reference Qiu, Blair and Abdullah2024). This especially accounted for primary care-givers acting as guardians (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2007; Nwakasi and Roberts Reference Nwakasi and Roberts2022). In turn, care recipients felt pressured as they were aware of the distress they caused their carers (Barros Pena et al. Reference Barros Pena, Kursar, Clarke, Alpin, Holkar and Vines2021). Secondly, care recipients risked uncritically trusting their carers or prioritizing the social relationship over independence or accountability of their carers’ actions (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005; Giebel, Halpin, O’Connell et al. Reference Giebel, Halpin, O’Connell and Carton2023). Thirdly, external authorities did not always scrutinize money and asset management within family care-giving, although carers disregarded the stipulation to keep records and/or put their own interests before the care recipient’s (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005; Setterlund et al. Reference Setterlund, Tilse, Wilson, McCawley and Rosenman2007). Hence, financial misconduct by family asset managers often remained undetected (Elbogen et al. Reference Elbogen, Swanson, Swartz and Wagner2003; Setterlund et al. Reference Setterlund, Tilse, Wilson, McCawley and Rosenman2007; Havens and Latulipe Reference Havens and Latulipe2024). Some scholars suggested allocating TPMM responsibilities to multiple family care-givers to increase social control. However, this could potentially result in increased conflicts and care-giving burdens (Giebel, Halpin, Tottie et al. Reference Giebel, Halpin, Tottie, O’Connell and Carton2023; Qiu et al. Reference Qiu, Blair and Abdullah2024).

Digitalization in TPMM: from haptic to digital money management

Design barriers in digital financial services arise due to age- or impairment-related changes in vision, hearing, tactile functions, memory and psychological challenges or low financial capacity. According to Latulipe et al. (Reference Latulipe, Dsouza and Cumbers2022), especially mobility, memory and hearing impairments negatively affect users’ experience with online banking. For persons with dementia, digital banking and online shopping can be challenging, and unwise purchases or financial investments can easily be done without immediately evident consequences (Giebel, Halpin, Tottie et al. Reference Giebel, Halpin, Tottie, O’Connell and Carton2023). Some scholars pointed out that not only personal banking but also TPMM was complicated by digital banking modalities (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005; Giebel, Halpin, Tottie et al. Reference Giebel, Halpin, Tottie, O’Connell and Carton2023). Vines et al. (Reference Vines, Dunphy, Blythe, Lindsay, Monk and Olivier2012), for example, discussed how paper cheques provided a mechanism for spontaneous and relatively secure payment delegation and found that there is no digital substitute for them. In this sense, digital banking services were criticized for failing to consider care(-giving) and assistance needs (Dunphy et al. Reference Dunphy, Monk, Vines, Blythe and Olivier2014; Barros Pena et al. Reference Barros Pena, Kursar, Clarke, Alpin, Holkar and Vines2021; Dai et al. Reference Dai, Miedema, Hernandez, Sutton-Lalani and Moffatt2023; Havens and Latulipe Reference Havens and Latulipe2024).

Results 3: ensuring good TPMM practice to balance autonomy and care

28 studies in our scoping review expressed some kind of policy recommendation or need for change (see Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005, Reference Tilse, Setterlund, Wilson and Rosenman2007, Reference Tilse, Wilson, Rosenman, Morrison and McCawley2011; Svare and Anngela-Cole Reference Svare and Anngela-Cole2010; Sacks et al. Reference Sacks, Das, Romanick, Caron, Morano and Fahs2012; Boyle Reference Boyle2013; Plander Reference Plander2013; Serowik et al. Reference Serowik, Bellamy, Rowe and Rosen2013; Dunphy et al. Reference Dunphy, Monk, Vines, Blythe and Olivier2014; Kaye et al. Reference Kaye, McCuistion, Gulotta and Shamma2014; Mitchell et al. Reference Mitchell, Pachana, Wilson, Vearncombe, Massavelli, Byrne and Tilse2014; Rosen et al. Reference Rosen, Ablondi, Black, Serowik and Rowe2014; McLoughlin and Stern Reference McLoughlin and Stern2017; Mills Reference Mills2017; Tillmann et al. Reference Tillmann, Schnakenberg, Weckbecker, Just, Weltermann and Münster2020; Wood et al. Reference Wood, Lichtenberg, Purewal, Garcia, Garcia, Mccleary and Drummond2020; Barros Pena et al. Reference Barros Pena, Kursar, Clarke, Alpin, Holkar and Vines2021; Creasy et al. Reference Creasy, Olaniyan, Davis and Hawk2021; Latulipe et al. Reference Latulipe, Dsouza and Cumbers2022; Nwakasi and Roberts Reference Nwakasi and Roberts2022; Schmidt et al. Reference Schmidt, Stowell, Pacini and Patterson2022; Wang et al. Reference Wang, Morphew, Vitale, Mullan and Zietlow2023; Dai et al. Reference Dai, Miedema, Hernandez, Sutton-Lalani and Moffatt2023; Connolly and Peisah Reference Connolly and Peisah2023; Giebel, Halpin, O’Connell et al. Reference Giebel, Halpin, O’Connell and Carton2023, Giebel, Halpin, Tottie et al. Reference Giebel, Halpin, Tottie, O’Connell and Carton2023; Havens and Latulipe Reference Havens and Latulipe2024; Qiu et al. Reference Qiu, Blair and Abdullah2024).

Among possible ways to improve TPMM practices, the issue of preserving care recipients’ autonomy stood out as a particular matter of concern. Care recipients were often found to associate keeping control over their finances and the privacy of their financial information with independence and a sense of self-worth (Latulipe et al. Reference Latulipe, Dsouza and Cumbers2022; Giebel, Halpin, Tottie et al. Reference Giebel, Halpin, Tottie, O’Connell and Carton2023). For many care recipients, it was thus important to have their choice honoured and to exercise some kind of control, even though they required assistance (Svare and Anngela-Cole Reference Svare and Anngela-Cole2010; Wood et al. Reference Wood, Lichtenberg, Purewal, Garcia, Garcia, Mccleary and Drummond2020). Striking a balance between autonomy and care (or between privacy and support) proved essential for adequate financial care practice. On an interpersonal level, this requires establishing a trusted and non-coercive care relationship in which privacy boundaries are renegotiated, for example through individual agreements on the amount and kinds of information shared (Plander Reference Plander2013; Serowik et al. Reference Serowik, Bellamy, Rowe and Rosen2013; Wood et al. Reference Wood, Lichtenberg, Purewal, Garcia, Garcia, Mccleary and Drummond2020; Barros Pena et al. Reference Barros Pena, Kursar, Clarke, Alpin, Holkar and Vines2021; Qiu et al. Reference Qiu, Blair and Abdullah2024; Havens and Latulipe Reference Havens and Latulipe2024).

Based on this notion, we found six suggestions to ensure good TPMM practice to balance autonomy and care that have been put forward by the reviewed papers.

1. Ensuring collaborative decision-making and security in TPMM and professional guardianship/PoA arrangements

Within formalized money management arrangements such as guardianship, possible solutions should emphasize collaboration and shared decision-making (Mills Reference Mills2017; Creasy et al. Reference Creasy, Olaniyan, Davis and Hawk2021; Nwakasi and Roberts Reference Nwakasi and Roberts2022). This includes deciding together with care recipients on the purchases, saving plans, priorities, restrictions and control mechanisms applied (Creasy et al. Reference Creasy, Olaniyan, Davis and Hawk2021). To identify personal care needs, guardians should get to know the individuals as persons (Svare and Anngela-Cole Reference Svare and Anngela-Cole2010). Evidence suggests that these practices enhance trust, increase care recipients’ agency and improve financial literacy and management skills (Serowik et al. Reference Serowik, Bellamy, Rowe and Rosen2013; Creasy et al. Reference Creasy, Olaniyan, Davis and Hawk2021). Implementing such practices requires extensive and more standardized staff training and a sensitive approach to reaching out to clients (in the PoA context) to foster acceptance (Serowik et al. Reference Serowik, Bellamy, Rowe and Rosen2013; Schmidt et al. Reference Schmidt, Stowell, Pacini and Patterson2022).

To prevent exploitation through guardianship, some authors call for stricter reviews and more control over representative payees and guardians (Belbase et al. Reference Belbase, Sanzenbacher and Walters2020; Nwakasi and Roberts Reference Nwakasi and Roberts2022; Schmidt et al. Reference Schmidt, Stowell, Pacini and Patterson2022). This includes improved mechanisms to identify fraud, for example monitoring programmes that assess the wellbeing of persons under guardianship and perform random home visits (Nwakasi and Roberts Reference Nwakasi and Roberts2022). Schmidt et al. (Reference Schmidt, Stowell, Pacini and Patterson2022) suggest enforcing the duty to report activities, peer review processes for guardians and reporting of guardianship fraud data to improve learning about these cases. The authors also suggest an integrated approach to law enforcement through inter-institutional cooperation (Nwakasi and Roberts Reference Nwakasi and Roberts2022; Schmidt et al. Reference Schmidt, Stowell, Pacini and Patterson2022).

2. Allocating resources to care organizations to improve TPMM

In care homes, assistance with money management often depends on the goodwill and extra efforts of staff members as care organizations tend to discourage money management assistance and have few resources available for it (Tilse et al. Reference Tilse, Wilson, Rosenman, Morrison and McCawley2011). If they had the necessary resources, staff could take residents to the bank and assess their individual capacity and personal preferences, making support arrangements accordingly. The same accounts for professional and voluntary guardians, who experience high workloads due to rising demand and scarcity of guardians. Mobilizing financial resources for guardian programmes is thus essential for implementing good practice and ensuring that trained guardians are available and affordable (Creasy et al. Reference Creasy, Olaniyan, Davis and Hawk2021; Nwakasi and Roberts Reference Nwakasi and Roberts2022). Nwakasi and Roberts (Reference Nwakasi and Roberts2022) argue that such resources could be secured through community support and collaboration with public entities.

3. Providing TPMM support for planning ahead and improved appointment procedures of guardians/PoAs

Planning care arrangements in advance is important for good practice tailored to care recipients’ needs and carers’ capacities. Patients with dementia, for example, might not be able to communicate their preferences at a late stage of the disease. Therefore, preferences and modalities should be decided beforehand; for example, this could include setting up a PoA before it is acutely needed (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005; Boyle Reference Boyle2013; McLoughlin and Stern Reference McLoughlin and Stern2017; Wood et al. Reference Wood, Lichtenberg, Purewal, Garcia, Garcia, Mccleary and Drummond2020; Giebel, Halpin, O’Connell et al. Reference Giebel, Halpin, O’Connell and Carton2023; Qiu et al. Reference Qiu, Blair and Abdullah2024). For this purpose, carers and care recipients require more information, education and training offers, such as structured education sessions at community level (Mitchell et al. Reference Mitchell, Pachana, Wilson, Vearncombe, Massavelli, Byrne and Tilse2014). In this context, some authors discussed the benefits of voluntary money management training programmes including enhanced financial literacy, increased trust in money managers (helpers) and client empowerment (Rosen et al. Reference Rosen, Ablondi, Black, Serowik and Rowe2014; Serowik et al. Reference Serowik, Bellamy, Rowe and Rosen2013; Creasy et al. Reference Creasy, Olaniyan, Davis and Hawk2021).

Some scholars hold social workers, legal advisers and health professionals responsible for addressing the issue of TPMM and discussing options with clients (Mitchell et al. Reference Mitchell, Pachana, Wilson, Vearncombe, Massavelli, Byrne and Tilse2014; Mills Reference Mills2017; Tillmann et al. Reference Tillmann, Schnakenberg, Weckbecker, Just, Weltermann and Münster2020; Wang et al. Reference Wang, Morphew, Vitale, Mullan and Zietlow2023; Connolly and Peisah Reference Connolly and Peisah2023). Through interventions (family counselling, mediation, advocacy), social workers can play an important role in ensuring that older adults and their carers make informed choices. General practitioners (GPs) are crucial agents for early intervention and supporting patients in making arrangements that will later be needed. However, GPs were found to lack knowledge and training on the requirements of dementia patients, local support infrastructures and the skills to interact with affected persons. Also, assessments of patients’ capacity should be improved to ensure adequate treatment and care (Connolly and Peisah Reference Connolly and Peisah2023; Wang et al. Reference Wang, Morphew, Vitale, Mullan and Zietlow2023).

4. Providing TPMM support and guidelines for informal carers and care recipients

For informal carers, financial literacy, information and guidelines about finance management and care systems, including available benefits and financial support, are often lacking or not easily accessible (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2005; Giebel, Halpin, O’Connell et al. Reference Giebel, Halpin, O’Connell and Carton2023). Additionally, informal as well as formal care-givers were often found to be ill-equipped to help with bureaucracy and finances (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2007; Giebel, Halpin, O’Connell et al. Reference Giebel, Halpin, O’Connell and Carton2023, Giebel, Halpin, Tottie et al. Reference Giebel, Halpin, Tottie, O’Connell and Carton2023). This also accounts for care recipients, especially for those who lack financial care-givers and/or the financial means to consult legal representatives for advice (Giebel, Halpin, O’Connell et al. Reference Giebel, Halpin, O’Connell and Carton2023). Giebel, Halpin, O’Connell et al. (Reference Giebel, Halpin, O’Connell and Carton2023) found that care organizations (charities, nurses), although reluctant to do so, would rather help with money matters than banks. Some scholars argued that financial institutions should close this service provision gap, provide straightforward information and improve customer journeys (McLoughlin and Stern Reference McLoughlin and Stern2017; Giebel, Halpin, O’Connell et al. Reference Giebel, Halpin, O’Connell and Carton2023, Giebel, Halpin, Tottie et al. Reference Giebel, Halpin, Tottie, O’Connell and Carton2023). McLoughlin and Stern (Reference McLoughlin and Stern2017) see it as a government responsibility to improve services and support care recipients and carers with setting up and understanding PoAs (or guardianship).

Generally, care recipients, informal and formal carers require clear guidelines and targeted support including programmes to enhance financial and digital literacy (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2007; Giebel, Halpin, Tottie et al. Reference Giebel, Halpin, Tottie, O’Connell and Carton2023; Qiu et al. Reference Qiu, Blair and Abdullah2024). Policy measures also need to address prevention of financial abuse in this context, for example through awareness and education programmes by accountants, lawyers and financial institutions, as well as access to mediation and affordable financial advice.

5. Creating targeted services for TPMM

Sacks et al. (Reference Sacks, Das, Romanick, Caron, Morano and Fahs2012) discuss daily money management (DMM) programmes, a targeted service programme for TPMM. The study estimated that DMM as a core component of case management (an integrated system in the US managing the delivery of health-care services for persons living at home) is less costly and more efficient compared to care home placement. The results challenge the common assumption that, on a macro-scale, care home placement is more cost-effective than community-based care. In this sense, DMM could help in supporting care recipients’ independence and prevent financial abuse. Similarly, Serowik et al. (Reference Serowik, Bellamy, Rowe and Rosen2013) promote the implementation of money management intervention programmes for persons with mental health issues as an important tool to support care recipients.

6. Designing fintech to support collaboration in TPMM

Through inclusive design, fintech can have an enabling effect and support social participation (Dai et al. Reference Dai, Miedema, Hernandez, Sutton-Lalani and Moffatt2023; Giebel, Halpin, O’Connell et al. Reference Giebel, Halpin, O’Connell and Carton2023). However, this presupposes certain usability requirements, such as a higher contrast ratio, resizable text and non-text options on bank and finance websites (Dai et al. Reference Dai, Miedema, Hernandez, Sutton-Lalani and Moffatt2023). Furthermore, user interfaces should be simplified by providing relevant information at prominent places, avoiding distractors and using clean visual elements. Given the diverse needs of users, a holistic approach is required that involves affected persons in the design process (Dai et al. Reference Dai, Miedema, Hernandez, Sutton-Lalani and Moffatt2023; Giebel, Halpin, O’Connell et al. Reference Giebel, Halpin, O’Connell and Carton2023).

Several authors discussed the need to update bank account management so as to consider care-taking needs: Kaye et al. (Reference Kaye, McCuistion, Gulotta and Shamma2014), for example, argued for enhanced privacy provisions for individuals using joint accounts. Dunphy et al. (Reference Dunphy, Monk, Vines, Blythe and Olivier2014) suggested prepaid debit cards assigned to care recipients’ bank accounts allowing for the secure delegation of payments to carers. Furthermore, a few publications addressed the benefits of collaborative payments and assisted monitoring of balances (Barros Pena et al. Reference Barros Pena, Kursar, Clarke, Alpin, Holkar and Vines2021; Dai et al. Reference Dai, Miedema, Hernandez, Sutton-Lalani and Moffatt2023; Havens and Latulipe Reference Havens and Latulipe2024; Qiu et al. Reference Qiu, Blair and Abdullah2024). Barros Pena et al. (Reference Barros Pena, Kursar, Clarke, Alpin, Holkar and Vines2021), for instance, tested an app that notified designated helpers in case unusual transactions took place in care recipients’ bank accounts, allowing them to intervene. Havens and Latulipe (Reference Havens and Latulipe2024) discussed proxy accounts, which allow trusted individuals to gain legitimate access to the care recipient’s accounts. A proxy account is accessed through a separate log-in and features limitations on what can or should be done and seen by the carer. Qiu et al. (Reference Qiu, Blair and Abdullah2024) proposed the implementation of multi-agent cooperation in (digital) financial management systems through role-based permissions. Essentially, all these prototypes aim to ensure that support and care can be provided without forcing the care recipient to give up all privacy and autonomy.

Beyond collaborative account management, Dai et al. (Reference Dai, Miedema, Hernandez, Sutton-Lalani and Moffatt2023) refer to the potential of emerging technologies such as AI in the context of banking and accessibility. Intelligent voice assistants or social support chatbots could, for example, help with online or local information search, or help in realizing payment innovation and the above-outlined third-party access tools. Schmidt et al. (Reference Schmidt, Stowell, Pacini and Patterson2022) find that technology could also be used to prevent financial exploitation by detecting suspicious activities.

Discussion

The aim of this scoping review was to cluster TPMM practices, and describe associated risks and barriers in the context of LTC. Such practices are highly varied and cannot be reduced to a clear-cut number of distinct practices. However, we identified four important dimensions that characterize these practices: (a) the degree of formalization of TPMM; (b) the level of cooperation; (c) the type of care provision in TPMM; and (d) the level of digitalization of TPMM. These criteria may be useful for future researchers and care organizations as they help in understanding the different and intersecting circumstantial factors. Our study further contributes to existing literature by supporting the notion that help with money management is not an all-or-nothing decision but rather operates on a broad spectrum ranging from need for occasional assistance to complete inability to manage one’s finances independently.

Our findings suggest that there may currently be too much emphasis on substitute decision-making in research and practice, while strategies to promote supported decision-making remain underdeveloped (Quinn et al. Reference Quinn, Gur, Watson, Doron and Georgantzi2018). In care organizations, this resulted in risk mitigation strategies being favoured over supporting self-efficacy (Tilse et al. Reference Tilse, Setterlund, Wilson and Rosenman2007, Reference Tilse, Wilson, Rosenman, Morrison and McCawley2011). With regard to the practical modalities of TPMM, formal and informal care-givers faced a lack of convenient ways to provide support without having to operate in legal grey areas (Latulipe et al. Reference Latulipe, Dsouza and Cumbers2022; Connolly and Peisah Reference Connolly and Peisah2023). Concerning the technological modalities of monetary transactions, substitute decision-making is prompted by the absence of fintech for TPMM that would facilitate collaboration, for example through forms of mutually agreed control and intervention (Havens and Latulipe Reference Havens and Latulipe2024; Qiu et al. Reference Qiu, Blair and Abdullah2024). Consequently, it is evident that merely focusing on enhancing the autonomy and self-determination of care recipients is insufficient to ensure adequate care and financial management assistance (Price Reference Price, Bennett, Avram and Austen2024; Wright Reference Wright2019). Rather, it is important to reduce the institutional barriers that hinder effective assistance by carers and reduce care recipients in their agency (see similar findings in other contexts: Hawkins et al. Reference Hawkins, Redley and Holland2011; Jacobs Reference Jacobs2019). Carers require solid organizational and technological infrastructure to securely perform TPMM. They also need time and space to act in the best interests of care recipients. In the context of TPMM, autonomy cannot be understood as merely the absence of coercion, but rather as a relational circumstance closely tied to adequate assistance (Verkerk Reference Verkerk1999).

In our review, we synthesized a range of policy and practice measures to improve TPMM practice and promote supported decision-making. These include broader strategies, such as providing more funding and establishing better guidelines for TPMM in formal care provision. Ideally, these measures could help in building personal and trusting relationships between formal carers (including care workers and professional guardians) and care recipients. Care organizations that are less constrained by heavy workloads, staff shortages and the rationalization of care practices are more able to foster such care relationships, in which personal preferences, modes of care and interventions can be negotiated (Stone Reference Stone and Harrington Meyer2000; Boumans et al. Reference Boumans, van Boekel, Baan and Luijkx2019; Moilanen et al. Reference Moilanen, Suhonen and Kangasniemi2022; Armstrong et al. Reference Armstrong, Armstrong and Choiniere2024). In line with our findings, Schmidhuber et al. (Reference Schmidhuber, Haeupler, Marinova-Schmidt, Frewer and Kolominsky-Rabas2017) emphasized the need for improved structures to provide public information and raise awareness of advance care planning, as well as education and support, to ensure good care for informal carers and care recipients. Our findings also stress the need to improve application processes for guardians, and information and training for physicians regarding TPMM options and requirements. Other straightforward measures include creating targeted services for care recipients (Sacks et al. Reference Sacks, Das, Romanick, Caron, Morano and Fahs2012) and new fintech solutions, such as digital proxy accounts that enable flexible collaboration and support with money management (Havens and Latulipe Reference Havens and Latulipe2024). Synthesizing the literature thus highlighted that there is substantial room for improvement. A plethora of policy-related and practical measures is required to facilitate change in favour of improving the quality of life of care recipients and informal carers, as well as providing better working conditions for formal care workers and guardians. Implementing such policy measures will require cooperation from multiple stakeholders, including lawyers, law enforcement, public administration and financial institutions.

There are several research gaps that need to be addressed. First, so far, there has been almost no systematic collection of data on the scope of assistance needed and the types of assistance tasks required and carried out. Of the few quantitative studies on the subject, most have used small samples. Second, TPMM in formal care settings has not yet been widely explored. Of the studies included in this review, only three addressed formal care contexts and the difficulties they experience (for a recent study touching on this subject see Bilgrami et al. Reference Bilgrami, Cutler, Gu, Aghdaee and Gu2025). Third, only three studies in our sample (Vines et al. Reference Vines, Blythe, Dunphy and Monk2011; Dunphy et al. Reference Dunphy, Monk, Vines, Blythe and Olivier2014; Havens and Latulipe Reference Havens and Latulipe2024) consulted representatives of financial institutions. This points to a lack of awareness and understanding of the role that such institutions can or should play in facilitating TPMM. Fourth, future research should also pay attention to the burdens faced by informal carers, the extent to which they provide adequate TPMM assistance, the kinds of support they require and how to prevent financial exploitation and coercive influence (Orfila et al. Reference Orfila, Coma-Solé, Cabanas, Cegri-Lombardo, Moleras-Serra and Pujol-Ribera2018; Puga et al. Reference Puga, Wang, Rafford, Poe and Pickering2023). In this sense, future research should emphasize interdependence and the collaborative nature of financial care-giving rather than individualizing financial wellbeing. Fifth, at a macro-level, cross-national comparisons and best practices are lacking entirely. Furthermore, the existing literature has not yet addressed the relationship between an increased prevalence of requiring TPMM and the economic shift towards downscaled welfare states, including financialized pension systems and increasing precariousness among older adults. Finally, more evidence is needed on the adoption of fintech applications to improve TPMM in LTC settings.

Limitations

The research findings we synthesized were largely made of specialized, located and small-scale studies. Therefore, it was difficult to compare the results or make out distinctive research trends or disruptions. The observations made and recommendations proposed warrant further investigation in future research to enhance their robustness and applicability. Further limitations of our study are language- and source-related. As we conducted the search in German and English, the findings relate to the specific legal, social and economic circumstances in the countries where the studies were carried out and published. Thus, the results mainly relate to the societal, legal and economic contexts of the USA, the UK and Australia. Even among these countries, TPMM differs in terms of national regulations, which we were unable to address in greater detail. Additionally, non-scientific publications, such as policy papers, brochures or job instructions, may have slipped our attention. Such additional sources and documents could be insightful for further investigation. As the terminology surrounding TPMM proved inconsistent, some important terms may have been overlooked.

Conclusion

In this scoping review, we synthesized existing scientific findings on TPMM for care-dependent adults. Research covers its practices, challenges and solutions. It became clear that apart from formalized ways of ensuring third-party access, for example through guardianship arrangements, there are many ways in which people with care needs receive help with managing money. However, supported decision-making in financial matters is often neglected in favour of substitute decision-making due to time-related and circumstantial constraints. The studies analysed, therefore, propose a variety of ways to improve the framework conditions for TPMM practice comprising policy-related and practical measures. A key focus of these measures is safeguarding good financial care-giving and care recipients’ self-determination, by providing sensitive care and services that can adapt to the individual needs and circumstances of care recipients. This includes creating digital financial services that reflect care-giving needs, such as proxy accounts; allocating resources to care organizations; providing clear guidelines for informal carers; and improving support for carers and care recipients through social and medical services. However, TPMM remains under-researched and offers a range of key subjects for future research. Several research gaps remain, particularly regarding TPMM in formal care service organizations, the role of financial institutions in TPMM, support for informal carers, adequate design of fintech and the influence of social policy on financial assistance needs.

Financial support

This scoping review was carried out as part of the research project ‘Social Coin’, a collaboration involving the Research Institute for Economics of Aging, the Austrian Blockchain Center (ABC), TwoNext and OeNPay. Financial support for the underlying research was provided by the Erste Foundation and via the programme ‘COMET’ (Competence Centers for Excellent Technologies). COMET is funded by the Austrian Federal Ministries BMK and BMAW, the Austrian Länder Vienna, Lower Austria and Vorarlberg and managed by the Austrian Research Promotion Agency (FFG). The WU Research Institute for Economics of Aging received funds from the Vienna Social Fund (Fonds Soziales Wien). The views expressed are not necessarily those of the funders.

Competing interests

The author(s) declare none.

Ethical standards

DeepL Team was used for language editing.

Appendix

PRISMA-ScR Checklist

Open access

Open access