‘ABC’, a software start-up from Estonia, was selected as the preferred supplier in a procurement contest in the UK for delivering a customer relationship management (CRM) system. However, it suddenly found itself ejected from the process after the adopting organisation approached an industry analyst firm for more information about the venture. An analyst reported back that they had ‘a list of some 500 vendors of CRM, many of which [the analyst] meets regularly to track the development of their products, but [ABC] is not on the list’. The analyst suggested that if the adopting organisation bought from an ‘unknown venture’, it would be ‘taking a risk’, which led one procurement team member to ask, ‘who would sign up to a company that no one has heard of?’ (Pollock & Williams, Reference Pollock and Williams2011). This interaction underscores that industry analysts act as brokers in a market of hype – their endorsements (or omissions) effectively commodify credibility, determining which innovations gain traction in the economy of expectations.

The above example reflects a pressing problem. All ventures face the difficulty that they are unknown quantities at the outset (Fisher et al., Reference Fisher, Neubert and Burnell2021). However, they can seemingly rectify this problem in part through drawing support from ‘key resource holders’ (Lounsbury et al., Reference Lounsbury, Gehman and Glynn2019, p. 1229), such as a market gatekeeper (Plummer et al., Reference Plummer, Allison and Connelly2016; Soublière & Gehman, Reference Soublière and Gehman2020). An evaluation or endorsement from an influential gatekeeper, like an industry analyst, is critical because it is ‘linked to the likelihood of firm survival and growth’ (Navis & Glynn, Reference Navis and Glynn2011, p. 479). Scholars have noted that market gatekeeper coverage can reassure audiences about investing in or purchasing from a venture lacking a proven track record (Fischer et al., Reference Fischer, Kotha and Lahiri2016). Others have provided evidence that when gatekeeper backing is not forthcoming, it can become a block or impediment to progress (Petkova et al., Reference Petkova, Rindova and Gupta2013). For instance, if a venture does not appear on a ‘recommended vendor list’, as the example of ABC above shows, the gatekeeper will caution against it (Coslor et al., Reference Coslor, Crawford and Leyshon2020). As noted in Chapter 3, digital start-ups often turn hype into a strategic asset by targeting key audiences; here, that means utilising analyst coverage to overcome being perceived as an ‘unknown quantity’.

However, the process through which ventures gain the support of a market gatekeeper has not been fully addressed (Überbacher, Reference Überbacher2014). The literature suggests a ‘screening process’ (Petkova et al., Reference Petkova, Rindova and Gupta2008, p. 327) involving abstract ‘filtering’ and ‘selecting’ mechanisms (Petkova et al., Reference Petkova, Rindova and Gupta2013, p. 866). Still, the specific evaluative processes used by gatekeepers remain poorly understood (Überbacher, Reference Überbacher2014), which highlights the need for further investigation into how, in ‘crowded locations’ (Petkova, Reference Petkova, Barnett and Pollock2012, p. 396) with numerous ventures competing for gatekeeper attention, certain ones garner support.

The challenge of drawing gatekeeper coverage appears especially acute in the context of digital entrepreneurship. There has been a recent surge in the number of new digital ventures (Nambisan, Reference Nambisan2017; Nambisan et al., Reference Nambisan, Wright and Feldman2019), defined as ventures that have ‘digital artefacts at the core of their business model for value creation and capture’ (Lin & Maruping, 2021, p. 1). How do new digital ventures engage and benefit from market gatekeeper support? Answering this research question is crucial. It is argued that the uncertainties surrounding digital ventures differ from those of non-digital enterprises (Ingram Bogusz et al., Reference Ingram Bogusz, Teigland and Vaast2018), rendering them especially reliant on gatekeeper coverage (Von Briel et al., Reference Von Briel, Recker and Davidsson2018; Elia et al., Reference Elia, Margherita and Passiante2020).

5.1 Liability of Newness

A core insight of the new venture literature is that young enterprises suffer from the ‘liability of newness’ (Stinchcombe, Reference Stinchcombe and March1965; Bruederl & Schuessler, Reference Bruederl and Schuessler1990). Scholars have given significant attention to identifying how potential customers and others, because new ventures lack a track record, could be sceptical towards their performance and whether they can deliver the required quality in a timely manner (Fischer & Reuber, Reference Fischer and Reuber2007; Fischer et al., Reference Fischer, Kotha and Lahiri2016). Recently, it has been noted that this liability is more prominent in new technology areas or what Überbacher (Reference Überbacher2014) calls ‘high velocity environments’ as there can be a ‘rapid transformation’ (p. 685) of many different aspects, including what venture performance and quality mean. We focus below on digital ventures, as the liabilities surrounding these enterprise types are especially pronounced.

5.1.1 New Digital Ventures

In the emerging field of digital entrepreneurship, attention has recently turned to differences between digital and non-digital enterprises (Nambisan, Reference Nambisan2017). An early insight of this embryonic literature is that the liability of newness may be ‘manifested differently’ in these contexts (Ingram Bogusz et al., Reference Ingram Bogusz, Teigland and Vaast2018, p. 318; see also Srinivasan & Venkatraman, Reference Srinivasan and Venkatraman2017). It is argued that digital ventures have a ‘high propensity for radical transformation’ (Von Briel et al., Reference Von Briel, Recker and Davidsson2018, p. 284) because their products can be taken in new directions by, for instance, user innovation (Nambisan et al., Reference Nambisan, Wright and Feldman2019). Other studies suggest that ‘pivoting’, where digital technologies enable a radical change in focus, goals, or strategy, is a distinguishing characteristic of digital entrepreneurship (Ghezzi & Cavallo, Reference Ghezzi and Cavallo2020; Wagner & Som, Reference Wagner, Som and Fayolle2021). Despite progress, an important issue left unaddressed concerns how digital ventures make themselves visible and understandable to potential audiences.

Scholars have drawn attention to how digital ventures uniquely rely on gatekeeper support for building market acceptance (Elia et al., Reference Elia, Margherita and Passiante2020; Von Briel et al., Reference Von Briel, Selander, Hukal, Lehmann, Rothe, Fürstenau and Wurm2021). It has been suggested that we are witnessing the emergence of ‘an increasing number of intermediaries’ who ‘play the role of brokers’ and help digital ventures ‘reach key goals’ (Von Briel et al., Reference Von Briel, Selander, Hukal, Lehmann, Rothe, Fürstenau and Wurm2021, p. 13). Some argue that winning the support of a gatekeeper will become increasingly decisive as digital entrepreneurship continues to grow (Nambisan et al., Reference Nambisan, Wright and Feldman2019). Others point out that, as the number of new digital ventures increases (Hull et al., Reference Hull, Hung, Hair, Perotti and DeMartino2007; Hair et al., Reference Hair, Wetsch, Hull, Perotti and Hung2013), competition for gatekeeper attention will become more challenging (Nambisan et al., Reference Nambisan, Wright and Feldman2019). Others still suggest that ventures failing to win gatekeeper support will become marginalised or that hierarchies could emerge between those receiving endorsement and those ignored (Dy et al., Reference Dy, Marlow and Martin2016). However, notwithstanding calls for more research on the ‘nature of intermediaries and their impact on digital entrepreneurship’ (Von Briel et al., Reference Von Briel, Selander, Hukal, Lehmann, Rothe, Fürstenau and Wurm2021, p. 13), scholars have stopped short of examining the process gatekeepers play in the formation of new digital ventures and what a venture can do to win and harness their support.

5.2 Gatekeeper Screening Processes

Mainstream scholarship has made much progress in showing how new ventures attempt to remedy the liability of newness through ‘being selected for coverage by influential institutional intermediaries’ (Petkova et al., Reference Petkova, Rindova and Gupta2013, p. 866). Gatekeeper coverage provides valuable assurances because it is assumed that the gatekeeper has conducted some evaluation and made a favourable judgement about venture qualities and viability (Hsu, Reference Hsu2004). Gatekeepers are defined as neutral ‘third parties’ (Beckert & Aspers, Reference Beckert and Aspers2011) or ‘intermediaries’ (Bessy & Chauvin, Reference Bessy and Chauvin2013; Coslor et al., Reference Coslor, Crawford and Leyshon2020) who evaluate phenomena in which they have no stake or interest (Beckert & Musselin, Reference Beckert and Musselin2013; Khaire, Reference Khaire, Durrand, Granqvist and Tyllström2017). The most well-known gatekeepers include industry analysts (Pontikes & Kim, Reference Pontikes and Barnett2017), industry media (Vasterman, Reference Vasterman2005; Kennedy, Reference Kennedy2008; Byrne & Giuliani, Reference Byrne and Giuliani2025; Magalhães & Smit, Reference Magalhães and Smit2025), and critics (Coslor et al., Reference Coslor, Crawford and Leyshon2020). Research shows that the gatekeeper performs essential functions such as ‘enhancing the visibility’ of ventures and ‘mediat[ing] information flows’ between it and other stakeholders (Pollock & Gulati, Reference Pollock and Gulati2007, p. 347). Ventures that win gatekeeper attention fare better as they channel market attention to those covered (Petkova et al., Reference Petkova, Rindova and Gupta2013). Failing to attract coverage will mean ventures will ‘not only be perceived as of lower quality’, but they could also be ‘less visible’ (Pollock & Gulati, Reference Pollock and Gulati2007, p. 347) since they are not part of industry discussions. However, the fact that gatekeepers have become an important staging post for new ventures echoes the puzzle we highlighted in the previous chapter. In Chapter 4, we showed that analyst briefings are a crucial site where start-ups repair their narratives to meet analysts’ criteria. Here we pick up on that by asking how, in practice, an analyst chooses one venture over another.

Studies have noted how gatekeepers have an internal ‘screening process’ (Petkova et al., Reference Petkova, Rindova and Gupta2008, p. 327) where they figure out ‘which firms merit their attention, for what reasons and to what extent’ (Rindova et al., Reference Rindova, Petkova and Kotha2007, p. 34). Others similarly describe how gatekeepers ‘filter information about new developments’ and ‘select a relatively small subset of issues, events, and organisations to focus public attention on’ (Petkova et al., Reference Petkova, Rindova and Gupta2013, p. 866). However, beyond these abstract screening processes, the actual mechanisms and evaluation processes remain poorly understood (Überbacher, Reference Überbacher2014). How, in situations where there are hundreds or, as with digital entrepreneurship, thousands of ventures vying for attention, does the gatekeeper decide to cover one venture and not another?

5.3 Valuation Studies

To help specify the gatekeeper evaluation process, we turn to recent Valuation Studies, a body of work that has shifted conceptions of evaluation from simple outcomes based on filtering and selection to more ‘processual’ understandings (see Millo et al., Reference Millo, Power, Robson and Vollmer2021). Two key insights are relevant from this literature. First, it acknowledges that venture performance or qualities are not given. Instead, they must be enacted as part of an evaluation. This is not an abstract or cognitive evaluation but rather one that involves distinctive socio-technical evaluation processes (Helgesson & Muniesa, Reference Helgesson and Muniesa2013, p. 23). Here, we will focus on the briefings provided by new digital ventures to industry analysts and the latter’s efforts to comprehend venture viability and distinctiveness.

Second, this research also highlights how evaluation can be transformative (Antal et al., Reference Antal, Hutter, Stark, Antal, Hutter and Stark2015; Kornberger et al., Reference Kornberger, Justesen, Madsen and Mouritsen2015). In tracing the etymology of the concept of ‘value’, for instance, the French sociologist Vatin (Reference Vatin2013) distinguished between ‘evaluating’ and the more generative notion of ‘valorising’, where the latter conception captured how the work of evaluation is not merely about appraisal but can also be additive towards the phenomenon under review. To evaluate ‘corresponds with a static judgement attributing a value to a good, a thing, a person’, whereas to valorise ‘has a dynamic meaning – increasing a value, adding an increment to it, a surplus value’ (Vatin, Reference Vatin2013, p. 33). The view of evaluation as concerned with identifying and creating value has begun having currency within management scholarship and broader social sciences (Karpik, Reference Karpik2010). For instance, in their study of the evaluation of art, Plante and colleagues (Reference Plante, Free and Andon2020, p. 3) discuss how art evaluators do more than identify the value of a particular artistic asset. In defending and rationalising their assessment to others, they actively enhance its value (see also Barman, Reference Barman2015; Bidet, Reference Bidet2020; Frenzel & Frisch, Reference Frenzel and Frisch2020).

When considering how gatekeepers screen new ventures, existing scholarship describes the first conception, appraisal (Pollock & Gulati, Reference Pollock and Gulati2007; Petkova et al., Reference Petkova, Rindova and Gupta2013), but not the second, valorising. Inspired by the idea that digging further into gatekeeper screening processes reveals potentially more profound value-creating mechanisms, we highlight the role of valuation and valorisation in screening processes as new ventures brief gatekeepers to win their backing.

5.4 New Ventures: An Unknown Quantity

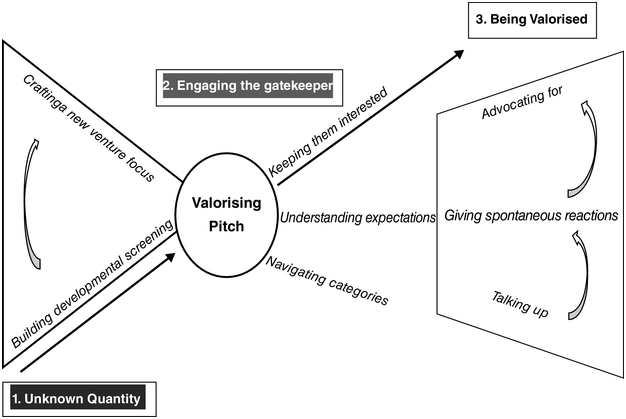

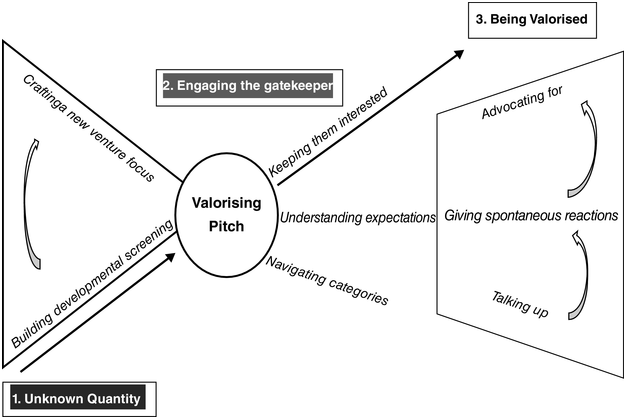

To understand how new digital ventures engaged with and benefited from gatekeeper support, we surfaced three processes that enabled ventures to move from being an unknown quantity in the eyes of the gatekeeper to engaging the gatekeeper, to being valorised by it.

We found that analyst firms are expanding their coverage as they attempt to map and categorise the start-up community. This is a significant departure point. Previously, they only focused on the more prominent and significant/established players. This shift, we found, involved them in crafting a new venture focus and building developmental screening.

5.4.1 Crafting a New Venture Focus

The interest in creating specific categories and processes for identifying new ventures started when Gartner launched its ‘Cool Vendor’ reports. Each year, this firm chooses several hundred ventures from various technology areas for coverage. An analyst specialising in the customer relationship management (CRM) area describes this focus:

We do a Cool Vendor report across the whole of Gartner where we look at Content Management, Web Analytics, and all sorts of different subjects, and we look for Cool Vendors in that area. It could be networking technologies, or mobile technologies or broadband or whatever; it doesn’t really matter. But in the area of CRM, we’ll routinely find 30 to 40 vendors easily, and we pick about 15 to write up and say that is quite cool or even different.

The analyst defines what is different about new ventures compared to the more established players usually covered:

Our Cool Vendor reports are really vendors that have been trading for three or four years, maybe five, unlisted. Most people haven’t got a clue who they are, but we know that they have got some really good customers. The customers say they are good, and that is what we think is cool about them. They have got something unique, and they got real customers.

From the earliest stages of industry analyst formation, Gartner often leads the way in developing new types of promissory products (Pollock & Williams, Reference Pollock and Williams2016). Thus, other industry analyst firms have followed suit, in many cases, borrowing and remaking the Cool Vendor appellation. For instance, the CEO of Analyst Firm B describes the provenance of his ‘Hot Vendor’ designation: ‘I was at Gartner for a long time. So, I started [Analyst Firm B] seven years ago. We said it’s not cool to be Cool, it’s cool to be “Hot”! We just took that phrasebook and reinvented it’ (A2, interview). The new venture focus was further augmented recently when another major analyst firm launched its ‘Innovators’ label. An informant from Analyst Firm C explains what they are doing to build a focus on new ventures:

We’re investing in the market around the ‘Innovators’, around the emerging vendors. We’ve got the analyst teams now supporting emerging vendors a lot more than what we’ve done in the past. We’re wanting to write about them a lot more. We want to get them visibility a lot more.

Two reasons were given for this expansion of coverage. The first point to shifts in digital innovation: ‘Most of the really innovative technologies are not coming from the big companies that always occupied [analyst research], it’s coming from the small vendors. They’re very innovative…. [And] seem to account for most of the innovation’ (A4, interview). Another cited reason was the changing interests of technology adopters, the main clients of industry analyst firms. Recent technological developments, such as Software-as-a-Service (SaaS) and cloud-based services, meant new ventures could offer attractive solutions to technology adopters:

The thing that we notice…. in SaaS software and in a lot of cloud-based applications, is you wonder if the product works and if [buyers] can sign up and they can cancel. A lot of business buyers say: ‘Look that [start-up] looks pretty good to me. I think I’m going to sign up for that’.

Analyst informants specified how clients no longer avoided new ventures. Seemingly, the buyer’s assessment is, ‘If it works, and it will help my business, then I’m going to take a chance, and I’m going to go for it’ (A2, interview). Since ensuring clients maintain subscriptions is an immediate priority, this means analyst firms are increasingly focusing on new ventures.

5.4.2. Building Developmental Screening

Building on our earlier notion of analysts crafting ‘promissory products’ (Chapter 2), Gartner launched its Cool Vendor reports to spotlight young, innovative firms. Crafting this new venture focus required the industry analysts to create different, more developmental screening processes. As existing evaluation mechanisms were geared towards assessing the larger more established players with significant and enduring market presence, they contained high ‘entry thresholds’ that new ventures could not meet: ‘[W]e do a lot of reports or syndicated research that evaluates [ventures] that cross the threshold of like four to five million [dollars] at least in revenue. So, a lot of the smaller vendors just won’t qualify to be evaluated. They don’t have enough customers and enough revenue’ (A2, interview). Another analyst describes how ‘most vendors aren’t on anything published by Gartner at all …. The small ones’ (A1, interview), which, in his view, was not necessarily a bad thing because the evaluation criteria would show them in a negative light: ‘I am a big believer that if you are small, you don’t really want to be on [a major analyst ranking] at all. You are not going to look good’ (A1, interview).Footnote 1

An analyst describes how the decision by his firm to cover new ventures required two moves. First, this was selectively drawing evaluation criteria from existing assessments: ‘We got [ranking 1] and [ranking 2], which are different market evaluations. So, when we evaluate, let’s say a product, we use some of the criteria for innovation from those reports to actually look and evaluate some of the younger, smaller vendors’ (A2, interview). Second, they developed a developmental screening process where analysts engaged with ventures in a more open and advisory manner, which included, for instance, offering ‘feedback’. Direct feedback is unusual in these settings as briefings are typically structured as a ‘one-way conversation’ (Analyst webinar). Analyst input and feedback are sold as part of a different service called ‘client inquiry’. However, analysts told us they make an exception to this rule when dealing with smaller ventures. An analyst described how:

Sometimes we give them some free feedback. The technique is called Pattern Recognition: what does the vendor have, and can they explain it. Sometimes even they can’t explain it. Like: ‘Wow! That’s great. That’s a huge capability. You should talk about that more.’

A further analyst made a similar point about how, when he found ‘confusing’ the material a new venture had sent him, he provided them with direction:

I had to admit, the first time I read [new venture’s] material, I said, ‘Well, this is really interesting’. And my second question was, ‘What do you do? What’s your deliverable? What’s your service?’ So I’m big on the economy of words or phrase. Tell me what you do in as few words as possible. And they found out that using my research was easier to explain what they did.

As analysts expand their coverage to include newer ventures, this provides opportunities for these ventures to engage more and benefit from the attention.

5.5 Engaging Gatekeeper Screening Processes

Our analysis identified a second process whereby the venture engaged with gatekeeper screening processes through a briefing. Our investigation captured how the briefing involved a series of mechanisms that included keeping them interested, understanding expectations, and navigating categories.

5.5.1 Keeping the Gatekeeper Interested

As noted in the previous chapter, briefing industry analysts is not easy – it is marked by several hurdles. The first is finding an analyst. Because of the ‘volume of vendors participating in the marketplace’ (Analyst webinar), these experts are inundated with requests from promising ventures. Thus, there was a need for a venture to be proactive and to set out to ‘win analyst attention’ (V1, interview). Some ventures reported that they ‘didn’t have a targeted approach to the analysts’, and they ‘would bump into them at conferences’ (V1, interview). Others talked of more directed strategies: ‘We targeted specific analysts that we felt were commentating on the space to tell them about who we were and what we did and our points of view about how we felt that this market space was evolving’ (V2, interview).

A second hurdle is finding the analysts who cover a venture’s product area. These experts are divided into ‘primary’ or ‘referral’ analysts. The former is the analyst who directly covers the area and ‘who knows you the best’, while the latter is the analyst more on the periphery but who could potentially ‘make mention of you’ (Analyst webinar). Working out primary from referral analysts was complex (for reasons we unpack more fully below) and often required multiple briefings. One venture describes how: ‘I have probably spoken with 20 analysts at Gartner, some of them more than others. Most of them, multiple times…. You either have 15- or 30-minute calls or one-hour calls. I bet we’ve had 100 hours of analyst interaction calls’ (V3, interview). Another described how they approached cohorts of analysts at a time: ‘You start with about six [analysts]…. You see how it’s going. And then you start with the next six. So, we have talked to probably close to 18 or 20 analysts, maybe 24, over the course of the two years’ (V4, interview).

Once identified, the next significant hurdle is keeping the analyst interested. These briefings are not a one-off event but a process where ventures must brief the analysts continuously – ‘maybe every quarter’ (Analyst webinar). Ventures are thus encouraged to build a ‘relationship’ with the analyst. This is to avoid their losing interest but also to move the affiliation to the next level. Specifically, a particular informant, having already ‘worked with analysts’ in a previous role, knew it was about ‘developing relationships of trust and collaboration’ (V4, interview). She describes how: ‘[W]e found a few who were interested in us quite early and having an internal analyst champion is absolutely critical’ (V4, interview). The ‘analyst champion’ is described as the ‘set of analysts who will then start talking about you and take the big leap to starting to write about you’ (V4, interview).

5.5.2 Understanding Gatekeeper Expectations

What do these briefings look like? How should the venture approach them? Ventures learnt that gaining industry analyst attention required assembling more than one set of skills; it was not just a matter of pitching but also understanding what analysts wanted. In thinking about the briefing, a venture CEO asks, ‘[w]hat’s the hook that most analysts are interested in? Is it because … it’s their space, and they’re interested in all the vendors and all the technologies? Is it because they want to understand what’s happening at the lower end, the earlier stage?’ (V6, prep). Ventures were often unsure why analysts had suddenly become interested in them. For instance, the same CEO asks:

Why would they care about what we’re doing? I’d get why they would care if we’d launched in January and we now had 50 customers, and we were beating [rival 1] and [rival 2] out of customers. You know, there’s certain start-up companies that get on a path and a traction where it’s like you can’t not care. But ones like us where it’s sort of that early stage.

Ventures worked hard to understand how to present themselves, that is to say, construct their ‘stories’ and ‘pitch deck’ to make themselves attractive to the analyst. AR experts would prep ventures on how the analyst is a ‘different audience’, that the process was unlike ‘pitching to clients’, and thus required ventures to ‘switch their tone from a pitch tone to an analyst focused tone’ (V7, prep). This echoes Chapter 4’s finding that start-ups must tailor their stories specifically for analysts.

During briefings, ventures tended to highlight technical features and had more difficulty conveying their products in a way that analysts understood. For instance, an analyst explained the briefing structure: ‘[i]t’s a pretty tight story, it follows a pretty visible logic structure: what does the marketplace look like, what are the complications affecting that market, and how can your solution solve it or undo this complicating factor’ (Analyst webinar). Ventures were advised to focus on how their product resolved significant customer problems (V7, prep). An AR expert explains to a venture:

So, [explain] what is [the venture], what does it do and how does it solve these [customer] issues. So, if we think of the lion’s share of our expository, right, I think…. We should just get [the analyst] to start thinking about, ‘Wow, this is something that I didn’t pay attention to, and I should be paying attention to. I would like to land that as the primary thing, right? I want [the analyst] to go, ‘Wow, I didn’t know this was that big of an issue’.

5.5.3 Navigating Gatekeeper Categories

Pitching also required periods of socialisation, whereby ventures would learn about these experts and, as one informant described it, ‘analyst curiosities’ (V2, interview). As this venture CEO saw, the critical aspect of developing and improving a briefing was to understand how:

[Analysts] have [an] established market model…. If you don’t necessarily fit…. Within an established category of business or activity…. They can be a bit resistant…. Because they are ‘Are you … this? Or a[re] you … that?’ … And if the answer is ‘Well, we’re neither of those things’…. Then [there] can be a little bit of difficulty in the conversation.

Failing to present the venture in a way the analysts recognised was risky. An AR expert recounts how analysts were reluctant to schedule further briefings with a venture as they found its product challenging to understand: ‘They haven’t used Gartner’s language to describe the market category that they were in. And so, [the analysts have] misunderstood what the company does. And they’ve responded to say, “I don’t follow you”’ (V6, prep). Ventures were advised to ‘create alignment’ with the analyst, which means thinking about ‘how you speak to them’ and responding in ‘the same tone and the same way to these people’ (V5, prep). A venture informant describes how ‘[y]ou can look at what each analyst is writing about, and the sort of terminologies and the models and so on that [they] have developed…. And in that way, you can sort of align language’ (V8, interview). Contained in analyst research would often be explicit mention of entry criteria: ‘[A]nd the trick’, one venture described, ‘is to be able to customise your brief request to show that you know the analysts’ research, that you understand how far you meet their criteria, so that you can show relevance, and you can show that you are helpful’ (V6, prep) – a point we emphasised in Chapter 4 when discussing how entrepreneurs must align their pitches to analysts’ frameworks.

However, our empirical data show that aligning with a specific analyst category could be problematic for many ventures. For instance, when an AR expert asked a venture CEO to tell him which analyst category his ‘platform’ belonged to, he responded that he no longer knew. This was because the platform had become something of a ‘Swiss army knife’ (V6, prep) – that is, something that can be used in multiple different ways by customers – and thus did not easily fit into one analyst category:

Part of the challenge I think we have…. You can do a multitude of things with [the platform]…. So, the use cases we’re finding actually in the market tends to be actually cross organisation data sharing… And it’s a totally side use case we hadn’t really thought of when we first started building the platform.

5.6 Being Valorised by the Gatekeeper

Those ventures that successfully proceed through the screening process would expect to benefit from gatekeeper attention in some way. In our analysis, we identified a third process that included giving spontaneous reactions, talking up, and advocating for.

5.6.1 Giving Spontaneous Reactions

In the briefing, many ventures hoped to provoke ‘feedback’. Whilst we heard above how ‘comment’ and ‘input’ is not formally a part of these settings, we also saw that analysts might provide ‘a little bit of feedback’ (A1, interview), especially if the venture briefing is a start-up. For instance, one venture CEO told us that he approached the briefing with the explicit aim of provoking a reaction:

What I wanted to do was approach it from the standpoint of: is my idea, is this product that the three of us have dreamed up great? Is it truly unique? Or is it my own naivety because it’s the first time I’ve thought of it, but surely someone else has thought about tackling the problem this way.

This informant particularly appreciated the analysts’ broader perspective: ‘[Analysts] see all the technology. They understand it way better than I do. And where [the briefing] was beneficial was, as a learning experience for me, because as I’m verbalising what my thoughts are, they’re giving me feedback, which is making me smarter, right’ (V10, interview).

Indeed, during debriefing sessions, it is customary for venture staff and AR experts to spend time reviewing the analysts’ comments and questions to identify what can be gleaned. After one briefing, for instance, an analyst’s remark about a venture’s product being the ‘holy grail’ was latched onto. This was first welcomed, then, a few moments later, discussed, as doubt began to creep in about whether the comment was positive or negative: ‘[The analyst] did mention that the metric piece was the “holy grail.” Does that mean that she doesn’t believe it or that we’re really onto something?’ (V11, debrief).

Analyst comments – even if spontaneous and cryptic – were seen as crucial for a developing venture. For instance, one informant told us how after being briefed by a particular analyst, he suggested they rethink their entire identity, which seemingly provided a breakthrough in their development. As we saw in the previous chapter, the analyst told them:

‘Look, you’re not a networking company. You do networking, but you want to be a security company And it took us over a year to really appreciate what he meant. But he’s absolutely right, and we are a security company now. What we say is ‘security is what we do, and networking is how we do it’…. Suffice to say, it was the most important advice this company has ever gotten.

5.6.2 Talking Up Ventures

Industry analyst coverage was viewed as a positive development. In some cases, a very good thing: ‘It was a great honour to be named a Cool Vendor’ (V12, interview) said one venture; it ‘helped in building our credibility’ (V2, interview) described another; it was ‘very powerful; it’s probably one of the best awards we’ve ever received’ (V13, interview), said a third. For some, this initial analyst attention is viewed as a stepping stone to further, perhaps more substantial, analyst coverage. One venture told us how there was talk ‘potentially of Gartner moving us up into a [major analyst ranking] this year’ (V14, interview). Direct acknowledgement of the coverage received was common among informants: ‘It’s like a stamp of quality that we are not just another product but a product who is in the right space’ (V15, interview). Some described having achieved ‘industry acceptance’:

As you build a business, particularly in tech environments, you know…. That people want to have a sense that…. There is a technology which is kind of going in the right direction…. And has an industry acceptance…. So that kind of associational branding…. brings that endorsement to you.

Industry analyst coverage was seen to allow entry into a market that was otherwise obstructed: ‘When you’re trying to break into the enterprise market, it’s very important to be recognised by an enterprise analyst firm’ (V16, interview). Informants discussed using this coverage to attract buyers and secure funding. A venture covered by an analyst firm very quickly received further attention from others, including investment analysts:

451 … covered us, Forrester covered us…. First Analysts have covered us, and then you know JP Morgan and Goldman have both covered us and so forth… I think that you know the fact that we’ve had that … coverage by Gartner has helped you know, putting us on their radar.

Many reported increased numbers of venture capitalists (VCs) cold calling them: ‘We got all these VCs calling us, and I kept saying, “Well, where have you heard about us?” … “You’re on the Gartner’s Cool Vendor list”’ (V1, interview). Another analyst informant described examples of ventures he had covered that secured further investment: ‘We know one from a couple of years ago, that no-one knew, who was from Australia, they said it helped them get some major deals because [Analyst Firm B] research thought that they were innovative, and that was enough to convince some big banks to invest in them’ (A2, interview).

It is analysts who open doors for new ventures. Analysts achieve this indirectly by serving as a source of relevant information. They could provide advice to a new venture on how to approach prospects. One venture describes how: ‘So, I’m trying to leverage other Gartner analysts so that they can give me insight so I can make better-informed sales calls on my prospects by knowing more of my competition in those individual industry verticals’ (V14, interview). They may do this more directly through, for example, facilitating critical introductions for ventures:

I would say there were a couple of analysts that did approach us that way, and what’s interesting is that while they didn’t specifically reach out to me in advance of me saying making an enquiry into them, what they did do, was take it upon themselves to go above and beyond the call and introduce me to people in the industry that would be important to the success of my company.

Alongside gatekeeping, analysts also provide the all-important introductions to potential customers. These direct recommendations influenced bottom-line decisions:

They would use their position, and they say, ‘Oh, this company is struggling with something like this, why don’t you reach out to, you know, their head of technology or their CEO or whatever? Use my name, tell them I said it might be worth a phone call and see what you can do’. And they’ve done that. There’s probably been a handful, three or four analysts that have done that multiple times for me.

Informants explained that analysts would help ventures stand out from the crowd, but this was only part of it. For instance, an analyst explains to a group of ventures how they will ‘talk them up’ if they win their backing:

We will talk about you if we think you’ve got an interesting story. We will speak of you with clients. We’ll talk about you in presentations. We’ll present case studies of what your clients are doing because that solves the need of our end-user organisations our end-user clients to understand the marketplace and to understand where their solutions are coming from…. There are different ways of getting to us so that we are as passionate about your solutions and capabilities as you are.

5.6.3 Advocating for Ventures

In the vernacular of these settings, analysts provide ‘lead generation’. Although ventures could achieve these leads themselves, it was widely recognised that contacting the lead ‘cold’ would have been of little use. The analyst not only provided them with an introduction but also crucial information regarding the specific problem they faced. Another informant gives a similar example where it was the analyst who provided the break needed, pointing them to a particular client problem and then smoothing over reservations they had of working with a start-up:

Gartner has been very influential to us…. One of the big things that happened to our company is we have a relationship with a security company called [Big Vendor], one of the biggest security companies…. And [Big Vendor] had a problem… But we could fix that problem with them. But, you know, they didn’t really want to work with a start-up. The problem is they couldn’t find anybody else who could solve their problem.

While reluctant to go with a new venture, the more prominent vendor agreed because the industry analyst’s recommendation provided this possibility. She recounts how the conversation between Big Vendor and the analyst firm went:

But, you know, [Big Vendor] is a big customer of Gartner, and I’m sure it helped when [Big Vendor] talked to Gartner about us and said, ‘Hey, can we work with these people or are they going to be total flakes?’ And Gartner said, ‘Well, you know, they have this weakness and this weakness. But, yeah, they do what they say they do, and we know a lot about them’, and so on and so forth…. So, it helped us establish the most important partner relationship that this company has had, and it was a turning point for us because once we could say that we worked with [Big Vendor], then we were real.

Above, we heard about the ‘analyst champion’. Others used similar terms. For instance, an AR expert explained how analysts could become ‘advocates’. Moreover, once enrolled as an advocate, the person could be ‘leveraged’:

What you can do with an analyst who is an advocate for you, in a lot of ways, is more valuable than being written in a report or being in a [ranking]…. Once we have them as an advocate, what strategies can we use to better leverage that advocacy in sales, marketing, product development.

The language of ‘championing’ and ‘advocacy’ appeared no overstatement. It was routine to hear analysts speak enthusiastically about ventures covered. Some even used words like ‘my’ venture and ‘buy-in’. For instance, we heard how analysts would compete internally to write about selected ventures. An analyst informant describes the selection process for ventures defined as ‘Cool Vendors’: ‘Let’s say there are ten analysts on a team and there are only five vendors that are going to be written about, and everybody is encouraged to submit a Cool Vendor’ (analyst webinar). The results are ‘some back and forth saying my Cool Vendor is different and more unique or impactful than yours’ (Analyst webinar). Once included in the research, it was common for analysts to talk about the ventures with clients and others: ‘So an analyst nominates and successfully publishes a vendor as a Cool Vendor. Well, then there is a psychological buy-in to the business problem that they are trying to solve and the uniqueness that they bring. So they would come to the lips of the analyst a little more’ (Analyst webinar).

These effects exemplify the shift we describe in Chapter 1 from ‘hype in the wild’ to more institutionalised, expert-mediated hype – or ‘tamed hype’. The case of Cool Vendor demonstrates how hype is being integrated into formal market structures.

5.7 Discussion: Model of the Gatekeeper Evaluation Process

This chapter sought to answer how new digital ventures engage a market gatekeeper and benefit from its coverage in helping solve a critical problem, being an unknown quantity. In doing so, we develop a process model of gatekeeper evaluation, revealing how ventures were required to perform a new kind of pitch, theorised as a valorising pitch, to move from being an unknown quantity to engaging the gatekeeper and being valorised. Figure 5.1 illustrates the mechanisms and challenges associated with briefing the gatekeeper and securing its support.

From Unknown Quantity to Engaging the Gatekeeper: The starting point for our process model is how, identifying the growing significance of new digital ventures (Nambisan et al., Reference Nambisan, Wright and Feldman2019), the gatekeeper went about crafting a new venture focus and, because these ventures rarely met ‘established scales of evaluation’ (Aspers, Reference Aspers2018), ‘building developmental screening’. We show that to move from being an unknown quantity to engaging the gatekeeper required ventures to mobilise three mechanisms: keeping them interested, where, similar to ‘entrepreneurial storytelling’ (Lounsbury et al., Reference Lounsbury, Gehman and Glynn2019), ventures attempted to convince why gatekeeper coverage was warranted; understanding expectations, whereby ventures become socialised in gatekeeper practices and worldview; navigating categories, where ventures needed to consider and take into account gatekeeper categorisations (see Chapter 7). While these mechanisms helped ventures progress to the next phase of gatekeeper evaluation, we emphasise that this was far from inevitable, given high levels of competition for analyst coverage and exacting briefing demands.

From Engaging the Gatekeeper to Being Valorised: If successful in briefing, a venture may potentially receive more detailed consideration, perhaps making it onto a ranking or procurement list. However, the nub of our argument is that the briefing triggered more than inclusion in the formal gatekeeper evaluation system. Specifically, it led to being valorised, which comprised the gatekeeper talking up, where it explained and justified to gatekeeper clients and others why certain ventures received coverage, including providing further detailed evidence of positive attributes and innovative characteristics; advocating for, where, having discovered a promising venture, gatekeeper staff might then enthuse about it during client meetings, on stage when making a presentation, or when writing up a case study; giving spontaneous reactions, where advice was offered to a venture struggling to spell out its more innovative attributes or identity. These were typically not deep reflections but unprompted and knee-jerk.

However, this raises the puzzling question of why the gatekeeper might support or promote a venture, especially considering its role as an ‘impartial’ assessor (Beckert & Musselin, Reference Beckert and Musselin2013; Pollock & Williams, Reference Pollock and Williams2016; Khaire, Reference Khaire, Durrand, Granqvist and Tyllström2017). As we see it, the gatekeeper promoted ventures not in a prescribed or designed way but as a ‘consequence’ of its evaluation process (Kruger & Reinhart, Reference Krüger and Reinhart2017; Frenzel & Frisch, Reference Frenzel and Frisch2020). This interpretation is reinforced by Valuation Studies scholarship, which views gatekeeper screening as involving evaluation and a more generative process of ‘valorising’ (Kornberger et al., Reference Kornberger, Justesen, Madsen and Mouritsen2015; Aspers, Reference Aspers2018). As Vatin (Reference Vatin2013) theorises, evaluators play an active role in not just identifying but ‘enhancing’ value through explaining and justifying assessments (see also Bidet, Reference Bidet2020). However, in our case, the gatekeeper did more than elaborate and define a venture position – what we theorise as talking up – it also sought to ‘improve’ that position through advocating for and giving spontaneous reactions.

These findings resemble Karpik’s (Reference Karpik2010) analysis of the competition between evaluators, where, because evaluators vie with others for the attention of audiences, they strive to make the things they assess ‘more visible and more desirable than their competitors’ (p. 46). Hence, as shown in our case, the gatekeeper devoted considerable effort to help ventures prosper in the market, that is, going as far as to provide suggestions (‘You want to be a security company’), introductions (‘We will speak of you with clients’), and even affective responses (‘We are as passionate about your solutions and capabilities as you are’). We suggest that valorisation should be conceptualised as involving both these aspects (justifying and advocating), which brings together what the extant literature treats as separate or does not account for. It also allows us to theorise another aspect in our study – how ventures sought to trigger and leverage this broader gatekeeper role.

Valorising Pitch: The notion of the valorisation pitch should capture the idea that ventures were often mindful that, underlying the gatekeeper evaluation system, there were other mechanisms to be leveraged. This aspect resembles the ‘strategic valorisation’ described by Plante and colleagues (Reference Plante, Free and Andon2020, p. 3), showing how actors, often purposefully and expertly, exploit the connection between evaluation and valorisation. For instance, some ventures viewed briefing not simply as a means to enter a ranking but as a way to elicit spontaneous feedback, which could then have an ‘editing’ effect (Überbacher et al., Reference Überbacher, Jacobs and Cornelissen2015, p. 943) on their venture. Others realised the potential for the briefing to build more significant gatekeeper engagement – similar to the ‘soft power tactics’ described by Santos and Eisenhardt (Reference Santos and Eisenhardt2009, p. 663) – which could then be subtly exploited. Others still saw the potential for a venture to enter a ranking but then for the two processes – evaluation and valorisation – to shape each other in a ‘bootstrapping manner’ (Plante et al., Reference Plante, Free and Andon2020, p. 15) where, because of gatekeeper coverage, it receives further valorisation, which enables entrance to other higher prestige rankings.

These insights illuminate how ventures could engage the gatekeeper to overcome some of the damaging aspects of being an unknown quantity. Valorisation appeared as powerful as other influences that stem from the formal gatekeeper evaluation system. Indeed, for some, gatekeeper valorisation was thought to be more powerful. Ventures that proactively leverage gatekeeper valorisation appear more likely to build market acceptance, that is, successfully engage with potential customers and other resource providers. Our analysis suggests that leveraging gatekeeper valorisation requires all three mechanisms – keeping them interested, understanding expectations, and navigating categories. We, therefore, reveal and theorise an enhanced model of gatekeeper evaluation that offers ventures the potential to mitigate some of the liabilities of venture adolescence (Stinchcombe, Reference Stinchcombe and March1965; Bruederl & Schuessler, Reference Bruederl and Schuessler1990).

We now discuss how this new theorisation of the gatekeeper evaluation process and valorising pitch contributes to research on new venture development, gatekeepers, and digital entrepreneurship.

5.8 How New Ventures Brief Market Gatekeepers for Endorsements

There is broad recognition of the importance of gatekeepers in the development of new ventures (Navis & Glynn, Reference Navis and Glynn2011). They can perform a significant role for ventures that find it challenging to gain a foothold in the marketplace (Überbacher, Reference Überbacher2014). Our chapter thus directly responds to Petkova’s (Reference Petkova, Barnett and Pollock2012) call to build conceptions of ‘what exactly a young firm can do to become selected by prestigious affiliates’ (Petkova, Reference Petkova, Barnett and Pollock2012, p. 394) by offering a rare empirical study of interactions between gatekeepers and ventures at the moment when they become more structured and formalised around a briefing. Our exploration of relationships forming around this distinct briefing type is novel; to our knowledge, we are the first to study and establish the importance of these valorising pitches and the micro-processes enacting them.

It is widely recognised that pitching is a core ‘cultural competence’ (Überbacher et al., Reference Überbacher, Jacobs and Cornelissen2015). However, most attention has been given hitherto to pitches related to starting and financing (Clarke et al., Reference Clarke, Cornelissen and Healey2019) rather than to audiences, such as gatekeepers, for broader assets, such as an endorsement (Fischer et al., Reference Fischer, Kotha and Lahiri2016). Scholars posit that it is necessary to distinguish between pitches to early- and later-stage audiences as the challenges will likely differ (Lounsbury & Glynn, Reference Lounsbury and Glynn2019). Fisher and colleagues (Reference Fisher, Neubert and Burnell2021) identified six pitch types with unique features and functions, but none directly reflect the dynamics and audience identified in this chapter. Our account complements the above studies by revealing a further pitch – the valorising pitch – which we have defined as a device to enrol a market gatekeeper to help build market presence. For instance, while investment pitches are characterised as a ‘singular transaction-based exchange’ (Teague et al., Reference Teague, Gorton and Liu2020, p. 336) involving ‘simple relationship[s]’ (p. 334), the valorisation pitch requires longer-term interactions where ventures must not only ‘engage the gatekeeper’ but ‘keep them interested’ over many years, which requires new skills and expertise. Furthermore, our theorisation of the valorising pitch would seem to complement Überbacher and colleagues’ (Reference Überbacher, Jacobs and Cornelissen2015) call for further research on the ‘strategic cultural actions’ those in new ventures must engage in when ‘legitimising their ventures’ (p. 947).

5.9 Gatekeeper Evaluation Processes Are Value-Creating

Our theorisation of the market gatekeeper evaluation process is also novel. Despite being theorised as ‘expert evaluators’ (Hsu, Reference Hsu2004), ‘evaluative institutions’ (Überbacher, Reference Überbacher2014), and ‘evaluators’ (Bessy & Chauvin, Reference Bessy and Chauvin2013), there are as yet no fine-grained models (Überbacher, Reference Überbacher2014) that tell us how gatekeepers evaluate ventures vying for their attention and what influence this has on their development. This chapter provides this more granular analysis in the form of an enhanced theoretical model of gatekeeper evaluation, which depicts evaluation processes as not simply ‘value-identifying’ but also value-creating. To date, researchers have advanced the debate by examining the ‘screening processes’ (Petkova et al., Reference Petkova, Rindova and Gupta2008, p. 327) used by gatekeepers to help figure out ‘which firms merit their attention, for what reasons and to what extent’ (Rindova et al., Reference Rindova, Petkova and Kotha2007, p. 34), where gatekeepers are depicted as making ‘judgments about the presence and level of specific [venture] attributes’ (Petkova et al., Reference Petkova, Rindova and Gupta2013, p. 866). However, this focuses on static value-identifying processes, the first part of our model, but not the second. The more value-creating mechanisms we reveal here are important because they are fundamentally generative of venture attributes and capabilities. Our enhanced theorisation, therefore, articulates mechanisms not fully accounted for in the existing concept of gatekeeper screening. It also deepens our understanding of how gatekeepers influence the development of new ventures.

Specifically, existing research has highlighted two prominent roles the gatekeeper plays towards new ventures. First, this is Pollock and Gulati’s (Reference Pollock and Gulati2007) suggestion that it ‘enhance[s] the visibility’ of ventures (p. 347). Second, it is Petkova and colleagues’ (Reference Petkova, Rindova and Gupta2013) finding that gatekeepers funnel ‘public attention toward some [ventures] and away from others’ (p. 866). However, by revealing how gatekeepers have value-creating and not just value-identifying mechanisms, we theorise them as more than simply amplifying pre-existing venture characteristics or popularising ventures with audiences. For instance, we show that the gatekeeper can shape the narrative surrounding venture identity and attributes (‘That’s a huge capability, you should talk about that more’). This insight that the gatekeeper can make ventures more understandable and attractive aligns with Überbacher’s (Reference Überbacher2014) call for research on the evaluative institutions that enable ventures to become ‘comprehensible and meaningful in the first place’ (p. 688). It also complements Lounsbury and colleagues’ (Reference Lounsbury, Gehman and Glynn2019) discussion of the ‘judgement processes’ surrounding new ventures and how it is these that drive the activity whereby ventures ‘acquire their attributes’ rather than simply residing in the ‘hands of the entrepreneur’ (p. 1225).

5.10 Gatekeepers Are Central in Realising Digital Entrepreneurship

Our chapter fosters an understanding of digital entrepreneurship by examining the unique role gatekeepers play in digital ventures (Elia et al., Reference Elia, Margherita and Passiante2020; Von Briel et al., Reference Von Briel, Selander, Hukal, Lehmann, Rothe, Fürstenau and Wurm2021). Scholars suggest the liability of newness is revealed differently in digital entrepreneurship (Srinivasan & Venkatraman, Reference Srinivasan and Venkatraman2017; Ingram Bogusz et al., Reference Ingram Bogusz, Teigland and Vaast2018). Specifically, this is because digital technologies embody ‘traits that allow [ventures] to evolve their identity’ (Recker & Von Briel, Reference Recker and Von Briel2019, p. 2). While the process of transforming identity through a ‘pivot’ (Ghezzi & Cavallo, Reference Ghezzi and Cavallo2020; Wagner & Som, Reference Wagner, Som and Fayolle2021) can help survival and growth (Von Briel et al., Reference Von Briel, Selander, Hukal, Lehmann, Rothe, Fürstenau and Wurm2021), it can also make it difficult for ventures to be clear about questions relating to ‘who [they] are’ and ‘what [they] do’ (Navis & Glynn, Reference Navis and Glynn2011, p. 479), which can be damaging when approaching resource providers.

Our generative model of gatekeeper evaluation complements existing research by showing how industry analysts are crucial actors in realising and shaping digital entrepreneurship, working as both ‘evaluators’ and ‘valorisers’. Our chapter suggests they play an especially significant role for some ventures more than others – specifically, those still developing significant aspects such as identity. Surprisingly, it did not seem to be the case that confusion around identity was wholly damaging in these settings (see McDonald & Gao, Reference McDonald and Gao2019; Fisher, Reference Fisher2020). Indeed, the gatekeeper took a ‘developmental’ rather than policing (Zuckerman, Reference Zuckerman1999) approach. However, this finding does not sit easily with mainstream gatekeeper literature. Scholars suggest that a venture lacking clarity around identity would be ‘screened out’ (Zuckerman, Reference Zuckerman1999, p. 1415). Yet, our chapter showed this was not always or inevitably the case (Durand & Paolella, Reference Durand and Paolella2013). We thus complement the body of scholarship that seeks to move beyond the depiction of ventures as either ‘screened in’ or ‘screened out’ (McDonald & Gao, Reference McDonald and Gao2019; Fisher, Reference Fisher2020). This is particularly important, given that we show that the gatekeeper adopted more ‘developmental screening’ and ventures themselves appear more expert and strategic in leveraging such coverage.

5.11 Research Opportunities for Studying Valorisation

Our chapter points to further research opportunities. We investigated how the valorising pitch benefits new digital venture development, but we glossed over whether this is a ‘tide that lifts all boats’ (Lounsbury et al., Reference Lounsbury, Gehman and Glynn2019, p. 1226). An essential vein of research would highlight the differences between those receiving gatekeeper coverage and those failing to win such endorsements. It is also necessary to identify the adverse consequences surrounding these briefings, including aspects such as what happens if the gatekeeper develops a negative assessment and how the venture might ‘shield’ (Überbacher et al., Reference Überbacher, Jacobs and Cornelissen2015, p. 945) if valorisation turns out to be ‘reductive’ instead of additive.

A further aspect for future research would be capturing the tension in our model between ‘value-identifying’ and ‘value-creating’ mechanisms. Both are important in supporting new ventures, but each works differently. Scholars may develop a richer understanding of how these mechanisms interrelate and whether there can be clashes, such as when one mechanism overrides or subsumes the other. For instance, further research might seek to understand whether there are limits to valorisation and any measures evaluators must take to ensure their evaluation systems and outputs continue to be seen as ‘impartial’ rather than ‘puff pieces’ (Silberstein-Loeb, Reference Silberstein-Loeb2011).

Finally, we suspect that our insights surrounding the valorising pitch could be further elaborated upon and incorporated into Valuation Studies (Kornberger et al., Reference Kornberger, Justesen, Madsen and Mouritsen2015; Aspers, Reference Aspers2018; Plante et al., Reference Plante, Free and Andon2020). Studying these briefings suggests a new type of evaluation practice – a ‘valorisation practice’ – that captures actors’ strategies and tactics to leverage the valorisation mechanisms underlying evaluation systems. Further research could investigate practical techniques as well as challenges across a variety of settings – rankings (Ringel et al., Reference Ringel, Espeland, Sauder and Werron2021), third-party certifiers (Gehman et al., Reference Gehman, Grimes and Cao2019), investment analysts (Arjaliès et al., Reference Arjaliès, Grant, Hardie, MacKenzie and Svetlova2017), auditing firms (Power, Reference Power2021), rating agencies (Rona-Tas & Hiss, Reference Rona-Tas, Hiss, Lounsbury and Hirsch2010) – as actors seek to benefit from this not much studied but fundamental evaluator role.

Open access

Open access