I. Introduction

What if laws designed to protect freedom of speech could also help protect the environment? Environmental performance, which ranges from reducing toxic emissions to enhancing green investment and strengthening governance measures for sustainability, has become a defining challenge for firms worldwide (Hsu, Li, and Pan (Reference Hsu, Li and Pan2026), Li, Mai, Wong, Yang, and Zhang (Reference Li, Mai, Wong, Yang and Zhang2026), and Li, Xu, and Zhu (Reference Li, Xu and Zhu2025)). According to the U.S. Environmental Protection Agency’s (EPA) Toxic Release Inventory (TRI), U.S. companies managed a total of 28.33 billion pounds of production-related toxic waste in 2020. Furthermore, between 2011 and 2021, EPA investigated about 200,000 noncompliance cases, imposing over US$78 billion in fines for environmental violations (see https://www.epa.gov/enforcement/environmental-enforcement-and-compliance-significant-cases/). These figures underscore both the urgency and opportunity of corporate environmental action. Prior research has examined the effects of various environmental regulations in shaping corporate sustainability (Porter and Van der Linde (Reference Porter and Van der Linde1995), Aghion, Dechezleprêtre, Hemous, Martin, and Van Reenen (Reference Aghion, Dechezleprêtre, Hemous, Martin and Van Reenen2016), and Brown, Martinsson, and Thomann (Reference Brown, Martinsson and Thomann2022)), yet a relatively less explored theme relates to how nonenvironmental legal reforms affect corporate environmental performance. Responding to calls for a broader understanding of how regulatory reforms influence firms’ green strategies (Gans (Reference Gans2012), Calel and Dechezleprêtre (Reference Calel and Dechezleprêtre2016)), we focus on anti-Strategic Lawsuit Against Public Participation (anti-SLAPP) statutes—laws originally designed to protect citizens and organizations from retaliatory lawsuits that seek to censor, intimidate, or silence public criticism. We ask whether and how these free-speech protections, though not environmental in intent, significantly affect corporate environmental outcomes.

In 1992, California enacted the nation’s first anti-SLAPP statute in response to what lawmakers described as a “disturbing increase” in lawsuits brought not to win on the merits, but to intimidate citizens who spoke out on matters of public concern. A well-known early example is Averill v. Superior Court (42 Cal. App. 4th 1170 [1996]), where a local resident who publicly opposed a proposed community project and urged their employer to withdraw support was sued for defamation and interference by the project’s sponsor, Eli Home, Inc. Although the claims by Eli Home had little chance of succeeding on the merits, the litigation itself threatened to consume the defendant’s time and resources and discouraged others from speaking out. Invoking the newly enacted anti-SLAPP statute, the court struck down Eli Home’s claims at an early stage, required the plaintiff to pay the defendant’s attorney’s fees, and reaffirmed that open debate on community projects is a form of protected public participation (see https://law.justia.com/cases/california/court-of-appeal/4th/42/1170.html). Starting with California, the adoption of anti-SLAPP statutes spreads widely across the United States, and by 2019, more than 30 states have enacted such laws (see Section A of the Supplementary Material), though their scope and strength vary considerably (Chen, Li, and Li (Reference Chen, Li and Li2025), Lee, Ng, Yoo, and Zhang (Reference Lee, Ng, Yoo and Zhang2026)). As Norman (Reference Norman2010) notes, the indirect impacts of anti-SLAPP protections are often more consequential than the direct resolution of SLAPP cases themselves. At its core, anti-SLAPP legislation operationalizes First Amendment principles in the modern legal landscape. By enabling courts to dismiss meritless claims at an early stage and awarding attorney’s fees to prevailing defendants, these statutes ensure that the constitutional right to petition and speak freely on issues of public interest, even when opposed by resourceful corporate actors.

While anti-SLAPP statutes are not environmental in nature, our study focuses on corporate environmental performance, as environmental challenges are among the most salient and publicly scrutinized aspects of firms’ social responsibility (Flammer (Reference Flammer2013), Bolton and Kacperczyk (Reference Bolton and Kacperczyk2021), and Li et al. (Reference Li, Xu and Zhu2025), (Reference Li, Mai, Wong, Yang and Zhang2026)). Because these consequences are so salient, firms face heightened reputational risk once their deficiencies in fulfilling environmental responsibility become public. We argue that anti-SLAPP statutes create an institutional setting that amplifies stakeholder voices and magnifies these reputational costs of environmental negligence and misconduct. By shielding nongovernmental organizations (NGOs) from retaliatory suits, these laws allow advocacy groups to more aggressively monitor firms and publicize environmental risks (Reid and Toffel (Reference Reid and Toffel2009)). By protecting journalists and media outlets, they foster investigative reporting that exposes harmful practices to broader audiences (Dyck, Volchkova, and Zingales (Reference Dyck, Volchkova and Zingales2008)). By safeguarding employees and community members, they encourage whistleblowing against local environmental harms (Böke, Brau, Glaeser, and Jeong (Reference Böke, Brau, Glaeser and Jeong2024)). Collectively, these protections broaden the set of stakeholders who can speak without fear of reprisal (Chen et al. (Reference Chen, Li and Li2025), Lee et al. (Reference Lee, Ng, Yoo and Zhang2026)). As firms seek to avert reputational losses from public exposure of environmental issues, the enactment of anti-SLAPP laws pressures them to adopt more substantive and credible environmental practices. Hence, even in the absence of direct environmental regulation, we expect anti-SLAPP statutes to improve firms’ environmental performance.

We further explore potential intermediary mechanisms through which firms address heightened scrutiny under anti-SLAPP laws. Specifically, we investigate environmental investment and environmental governance, two complementary mechanisms whereby the former reflects firms’ strategic resource allocation, while the latter captures the governance and incentive structures that embed sustainability considerations into corporate decision-making. We posit that through environmental investment, firms not only signal their commitment to sustainability but also achieve tangible improvements in environmental performance by reducing emissions, lowering waste, and enhancing recourse efficiency (Delmas and Toffel (Reference Delmas and Toffel2008), Aghion et al. (Reference Aghion, Dechezleprêtre, Hemous, Martin and Van Reenen2016), and Li et al. (Reference Li, Mai, Wong, Yang and Zhang2026)). In comparison, environmental governance captures organizational responses that institutionalize sustainability within corporate structures and incentive systems. Firms may strengthen governance systems by appointing sustainability directors, embedding environmental criteria in executive pay and operational partner selection, and training employees on environmental practices (Flammer (Reference Flammer2013), Hsu et al. (Reference Hsu, Li and Pan2026), and Li et al. (Reference Li, Xu and Zhu2025)). These internal governance adjustments complement firms’ operational and strategic investment efforts, jointly mitigating reputational risks magnified under anti-SLAPP protections and helping to explain the observed improvements in corporate environmental performance.

To empirically test our predictions, we apply a stacked difference-in-differences (DiD) design using a comprehensive panel data set consisting of 118,287 firm-year observations spanning 1990 to 2019. We employ toxic emissions as an objective, standardized, and quantifiable measure of corporate environmental performance (Li et al. (Reference Li, Xu and Zhu2025)). Our findings show that anti-SLAPP enactments relate to a significant reduction in corporate toxic emissions, suggesting that strong legal protections for free speech and stakeholder voice motivate firms to improve their environmental practices. We perform a series of tests to examine the robustness of our findings. To address potential endogeneity and examine the timing of the effect, we employ a dynamic DiD specification that estimates event-time coefficients relative to the anti-SLAPP enactment. We also employ alternative measures to capture toxic releases and the strength of anti-SLAPP adoptions. We further source environmental performance data from different databases, conduct falsification tests using “fake adoption treatments,” use propensity score matching (PSM), and perform entropy balancing. In all cases, we obtain consistent results.

We further examine the mechanisms through which anti-SLAPP statutes enhance corporate environmental performance. Consistent with our predictions, the results indicate that firms enhance environmental investment and strengthen environmental governance to improve their environmental outcomes following anti-SLAPP enactments. Under the investment channel, firms demonstrate greater environmental improvement through green innovation, as reflected in higher numbers of green patents, larger environmental capital spending, and stronger adoption of pollution abatement and prevention practices, including source reduction and postproduction waste management. Under the governance channel, firms implement stronger internal and external oversight by appointing sustainability directors, linking executive compensation to ESG performance, providing environmental training to employees, and integrating sustainability considerations to supply-chain partner selection. Taken together, these findings suggest that firms respond to anti-SLAPP laws by implementing operational and organizational changes that institutionalize environmental responsibility within corporate practices and governance structures.

We also conduct cross-sectional analyses to understand how firms’ characteristics shape responses to anti-SLAPP enactments. We find that the decline in toxic releases is more pronounced when firms face stronger external stakeholder pressure, such as from government clients or active environmental NGOs, and among firms whose executive compensation and investor preferences are more closely aligned with long-term sustainability objectives. These findings are in line with our propositions that enhanced legal protection for free speech strengthens stakeholder monitoring and that firms with greater exposure or stronger internal alignment are more responsive to such scrutiny. We also rule out the alternative explanation that the decline in toxic releases results from reduced economic activity.

Our study makes several contributions to the literature. First, we advance understanding of the drivers of corporate environmental performance by providing the first empirical evidence that the enactment of anti-SLAPP statutes improves outcomes such as reduced toxic releases, increased sustainability investment, and strengthened environmental governance. While prior studies have focused primarily on explicit environmental interventions, such as carbon taxes, cap-and-trade systems, or environmental disclosure mandates, in affecting firm behavior (e.g., Aghion et al. (Reference Aghion, Dechezleprêtre, Hemous, Martin and Van Reenen2016), Calel and Dechezleprêtre (Reference Calel and Dechezleprêtre2016), and Brown et al. (Reference Brown, Martinsson and Thomann2022)), we show that regulatory reforms not explicitly designed with environmental objectives in mind can nevertheless exert powerful indirect effects. In this way, our study extends sustainability research beyond compliance-based models (Porter and Van der Linde (Reference Porter and Van der Linde1995), Delmas and Toffel (Reference Delmas and Toffel2008)), and our findings on how regulatory spillovers can generate unexpected but beneficial consequences for corporate behavior bridge legal and sustainability research in a novel way. Importantly, we further show that these environmental improvements do not arise from a contraction in firms’ economic activities, indicating anti-SLAPP laws promote genuine environmental progress through greater accountability and strategic adaptation rather than operational downsizing.

Second, we shed light on the mechanisms through which heightened stakeholder scrutiny translates into substantive corporate responses. We show that firms adapt both strategically, by increasing green investments, and organizationally, by strengthening governance structures for sustainability. Our findings thus clarify the channels through which anti-SLAPP protections promote corporate sustainability. We also show that the impact of anti-SLAPP statutes is stronger among firms subject to greater stakeholder scrutiny from government clients and NGOs, but weaker when executives receive more compensation with short-term targets attached or when the firm is less exposed to ESG-oriented investors. These findings contribute to debates about the conditional effectiveness of legal reforms and suggest that the ability of civil rights-based legal protections to advance corporate sustainability depends on the surrounding stakeholder environment and firms’ internal governance.

Third, we add to the emerging empirical work on the corporate consequences of anti-SLAPP statutes. Recent studies show that anti-SLAPP adoption leads firms to expand CSR disclosure (Griffin, Hong, Jung, and Moon (Reference Griffin, Hong, Jung and Moon2024)) and disclose bad news more promptly (Chen et al. (Reference Chen, Li and Li2025), Lee et al. (Reference Lee, Ng, Yoo and Zhang2026)). Relatedly, stronger speech protections promote more candid employee disclosures on workplace issues (Böke et al. (Reference Böke, Brau, Glaeser and Jeong2024)), and the improved transparency helps lower firms’ cost of equity (Guernsey, Serfling, and Yan (Reference Guernsey, Serfling and Yan2025)) and enhance investment efficiency in both labor (Jung, Wang, Wei, and Zhang (Reference Jung, Wang, Wei and Zhang2021)) and capital allocation (Guernsey et al. (Reference Guernsey, Serfling and Yan2025)). By linking anti-SLAPP statutes to environmental performance, we extend this growing line of research to a domain where stakeholder scrutiny and reputational accountability are particularly pronounced (Flammer (Reference Flammer2013), Bolton and Kacperczyk (Reference Bolton and Kacperczyk2021), and Li et al. (Reference Li, Xu and Zhu2025)). Our evidence shows how firms respond to heightened stakeholder scrutiny by implementing operational and structural adaptations that have concrete environmental performance consequences. Although the reputational mechanism we study may also influence firms’ broader social performance (Li et al. (Reference Li, Mai, Wong, Yang and Zhang2026)), our focus on environmental outcomes is conceptually salient and empirically distinct, given their high visibility, regulatory verification, and close connection to firms’ operations and investments. Our findings therefore offer a complementary perspective to emerging work on the social dimension of corporate responsibility.

Finally, we contribute to the law and political economy literature by showing how legal institutions designed to protect civil liberties can shape corporate behavior in areas beyond their original intent. We provide empirical evidence relevant to ongoing debates surrounding speech-related reforms, such as the U.S. Executive Order 14149 and the proposed Free Speech Protection Act (Heese and Pérez-Cavazos (Reference Heese and Pérez-Cavazos2021), Chen et al. (Reference Chen, Li and Li2025)). While enhanced free-speech protections are typically evaluated in terms of civic or political disclosure, our findings reveal a previously underexplored channel through which acts aiming to promote civil rights may also advance corporate sustainability (Norman (Reference Norman2010)). This insight complements traditional environmental policy research and is particularly relevant in settings where direct environmental regulation is weak, stalled, or politically contested (Xu and Kim (Reference Xu and Kim2022)).

II. Institutional Background and Theoretical Predictions

A. Stakeholder Pressure and Reputational Costs

A large body of research highlights that firms face powerful incentives to respond to stakeholder pressure because of the substantial reputational costs associated with failing to meet societal expectations (Fombrun (Reference Fombrun1996), Delmas and Toffel (Reference Delmas and Toffel2008)). Evidence shows that sanctions through market and nonmarket channels may be initiated by diverse stakeholders, such as investors, journalists, NGOs, employees, and communities (Klassen and McLaughlin (Reference Klassen and McLaughlin1996), Dyck et al. (Reference Dyck, Volchkova and Zingales2008), and Krüger (Reference Krüger2015)). When corporate practices are exposed as socially or environmentally irresponsible, firms tend to suffer a loss of legitimacy and trust in the eyes of key stakeholders, evidenced by declines in market value (Klassen and McLaughlin (Reference Klassen and McLaughlin1996), Bolton and Kacperczyk (Reference Bolton and Kacperczyk2021)) and heightened vulnerability to regulatory scrutiny or activist campaigns (King and Lenox (Reference King and Lenox2000), Christensen, Hail, and Leuz (Reference Christensen, Hail and Leuz2021)). Firms are therefore motivated to undertake measures, such as enhancing transparency, adopting governance reforms, or investing in sustainability initiatives to address these reputational concerns (Delmas and Toffel (Reference Delmas and Toffel2008), Flammer (Reference Flammer2013)).

Reputational pressures are particularly salient when the issues involve environmental consequences. Studies show that activist groups and NGOs play an important role in uncovering harmful corporate environmental practices and mobilizing pressure that compels firms to adjust their policies and strategies (Reid and Toffel (Reference Reid and Toffel2009)). Journalists and media coverage further magnify these effects by broadcasting environmental controversies to wider audiences (Dyck et al. (Reference Dyck, Volchkova and Zingales2008)). Employees may also act as whistleblowers when internal practices conflict with sustainability commitments (Böke et al. (Reference Böke, Brau, Glaeser and Jeong2024)). In addition, firms tend to be penalized in capital markets when controversies arise (Krüger (Reference Krüger2015), Krueger, Sautner, and Starks (Reference Krueger, Sautner and Starks2020), and Bolton and Kacperczyk (Reference Bolton and Kacperczyk2021)), while being rewarded when they proactively adopt environmental initiatives (Flammer (Reference Flammer2013)). Recent studies demonstrate that stakeholder monitoring helps enhance firm social performance (Li et al. (Reference Li, Mai, Wong, Yang and Zhang2026)) and that individual characteristics of CEOs and board directors significantly affect corporate environmental outcomes (Hsu et al. (Reference Hsu, Li and Pan2026), Li et al. (Reference Li, Xu and Zhu2025)). Taken together, this literature suggests that reputational concerns amplified by diverse stakeholders have significant implications for corporate environmental practices and outcomes.

B. Institutional Background

The adoption of anti-SLAPP statutes empowers stakeholders to voice their concerns more freely (Pring and Canan (Reference Pring and Canan1996), Norman (Reference Norman2010)). What distinguishes these laws is their procedural design, which directly reduces the legal and financial burdens of public participation. First, anti-SLAPP statutes typically authorize the early dismissal of meritless lawsuits via special motions to strike, preventing drawn-out legal battles that might otherwise drain defendants’ time and resources. This safeguard directly addresses the kind of protracted litigation faced by organizations such as Greenpeace International, which has repeatedly been targeted by energy firms seeking to silence environmental campaigns—cases later dismissed as baseless but costly to defend (see https://www.greenpeace.org.au/news/greenpeace-international-begins-groundbreaking-anti-slapp-case-to-protect-freedom-of-speech/). Second, anti-SLAPP laws deter frivolous litigation by requiring losing plaintiffs to cover defendants’ legal fees upon a successful motion (e.g., California’s CCP §425.16(c)). Third, they generally pause discovery proceedings while a motion is pending, preventing plaintiffs from strategically inflating litigation expenses to pressure a settlement. This measure strikes at the core coercive tactics of SLAPP suits, where plaintiffs exploit procedural costs, financially and emotionally, to punish critics.Footnote 1 Finally, anti-SLAPP protections are intentionally broad, covering a wide range of public expression, including traditional speech, online commentary, activism, and other civic discourse, thereby reinforcing their continued relevance in today’s communication landscape.

The contemporary legal framework addressing SLAPP lawsuits originates from California’s pioneering anti-SLAPP statute, codified as California Code of Civil Procedure §425.16 in 1992. Since then, similar anti-SLAPP provisions have been enacted across various jurisdictions, including Texas (Texas Civil Practice & Remedies Code §27.001 et seq.), New York (N.Y. Civ. Rights Law §70-a), and Washington (RCW 4.24.510). As of 2019, over 30 states in the U.S. have adopted such statutes. However, the scope of these laws varies widely: some protect only speech directed at government entities, while others extend coverage to any expression concerning matters of public interest. This variation has prompted considerable legal debate, with courts frequently testing the boundaries of what qualifies as protected speech (Chen et al. (Reference Chen, Li and Li2025)). The controversy has become especially pronounced in the environmental context. Major oil and agribusiness firms, for instance, file defamation and racketeering claims against environmental NGOs and media outlets reporting on climate concerns (see https://www.nytimes.com/2025/06/22/climate/oil-industry-anti-slapp-climate-lawsuits.html/). Parallel developments in Europe, such as litigation between Energy Transfer and Greenpeace, highlight the global resonance of these disputes and the growing international discussions on anti-SLAPP protections (see https://verfassungsblog.de/greenpeace-slapp-energy-transfer/).

From an institutional perspective, the common thread of these anti-SLAPP efforts is clear. That is, anti-SLAPP statutes recalibrate the legal balance of power, reducing the ability of well-resourced plaintiffs to suppress criticism through litigation tactics. The widespread adoption of anti-SLAPP statutes reflects their institutional significance in safeguarding constitutionally protected speech from coercive litigation practices. By embedding free-speech protections into civil procedure, anti-SLAPP laws fundamentally reduce the real and perceived costs of public criticism. These protections are particularly relevant in environmental contexts, where stakeholders, such as NGOs and journalists, often rely on legal protections for free speech to investigate and publicize issues such as corporate pollution and greenwashing (Pring and Canan (Reference Pring and Canan1996)). A direct implication is that, as discussed in Norman (Reference Norman2010), these statutes encourage more open dialogue and create a durable infrastructure for stakeholder oversight. Recent empirical evidence confirms these effects by showing that anti-SLAPP laws significantly amplify stakeholder voice in the corporate domain and elicit meaningful corporate responses in disclosure (Chen et al. (Reference Chen, Li and Li2025), Lee et al. (Reference Lee, Ng, Yoo and Zhang2026)), allocating resources at the workforce and capital markets (Jung et al. (Reference Jung, Wang, Wei and Zhang2021), Griffin et al. (Reference Griffin, Hong, Jung and Moon2024)), and improving transparency (Griffin et al. (Reference Griffin, Hong, Jung and Moon2024), Guernsey et al. (Reference Guernsey, Serfling and Yan2025)).

C. Theoretical Predictions

We contend that the institutional design of anti-SLAPP statutes carries significant implications for corporate environmental performance. By reducing the legal and financial risks associated with public participation and strengthening the voices of stakeholders, these laws raise the reputational costs of environmental negligence. Environmental issues differ from other areas of corporate responsibility in their visibility, long-term social impact, and often irreversible consequences for affected communities and ecosystems (Flammer (Reference Flammer2013), Bolton and Kacperczyk (Reference Bolton and Kacperczyk2021), and Li et al. (Reference Li, Xu and Zhu2025), (Reference Li, Mai, Wong, Yang and Zhang2026)). Events such as pollution incidents, toxic releases, and climate-related harms frequently trigger intensive attention from stakeholders (Dyck et al. (Reference Dyck, Volchkova and Zingales2008), Krüger (Reference Krüger2015), Krueger et al. (Reference Krueger, Sautner and Starks2020)). Under anti-SLAPP protections, these concerns can be raised with less fear of retaliation (Pring and Canan (Reference Pring and Canan1996), Norman (Reference Norman2010)), thereby increasing the likelihood that harmful practices will be publicly exposed. Anticipating this scrutiny and the reputational damage it may entail, firms are more likely to proactively improve their environmental practices. We therefore expect that the enactment of anti-SLAPP statutes is associated with improvements in corporate environmental performance.

We further argue that two complementary channels help explain how firms adapt to amplified stakeholder voice under anti-SLAPP laws. First, they may increase investment in environmental initiatives within operations as a forward-looking strategy. By allocating more financial and technological resources to green innovation, pollution abatement, and waste management, firms can credibly signal their long-term commitment to sustainability in alignment with stakeholders’ expectations (Aghion et al. (Reference Aghion, Dechezleprêtre, Hemous, Martin and Van Reenen2016)). Although such investments typically involve significant cost and uncertain returns (Xu and Kim (Reference Xu and Kim2022)), they often deliver substantive improvements in corporate environmental outcomes (King and Lenox (Reference King and Lenox2000), Berrone and Gomez-Mejia (Reference Berrone and Gomez-Mejia2009)). In this sense, green investments represent both a signal of commitment and an operational shift toward more robust environmental risk mitigation strategies in response to greater transparency and stakeholder monitoring.

Second, firms may reinforce environmental governance to institutionalize and sustain their sustainability efforts. As the foundation for lasting change, governance embeds environmental accountability into decision-making processes and aligns managerial incentives and organizational routines with long-term sustainability objectives (Delmas and Toffel (Reference Delmas and Toffel2008), Berrone and Gomez-Mejia (Reference Berrone and Gomez-Mejia2009)). In response to intensified stakeholder scrutiny under anti-SLAPP statutes, firms may adopt governance mechanisms that support more disciplined and forward-looking environmental strategies. Such mechanisms include improving board oversight of sustainability issues, embedding ESG criteria in executive compensation and supply-chain partner selection, and enhancing employee environmental training (Berrone and Gomez-Mejia (Reference Berrone and Gomez-Mejia2009), Li et al. (Reference Li, Xu and Zhu2025), (Reference Li, Mai, Wong, Yang and Zhang2026)). We contend that these governance measures help integrate environmental considerations into corporate decision-making and establish accountability systems that sustain the firm’s environmental effort. Together, environmental investment and governance represent strategic and structural adaptations for firms to respond effectively to heightened stakeholder scrutiny arising from anti-SLAPP protections (Porter and Van der Linde (Reference Porter and Van der Linde1995)).

III. Research Design

A. Toxic Release Data

We measure corporate environmental performance using toxic chemical release, a direct and objective indicator for firms’ environmental footprint (Delmas and Toffel (Reference Delmas and Toffel2008), Akey and Appel (Reference Akey and Appel2021), Xu and Kim (Reference Xu and Kim2022), Duchin, Gao, and Xu (Reference Duchin, Gao and Xu2025), and Hsu et al. (Reference Hsu, Li and Pan2026)). Facility-level toxic release data are acquired from the EPA’s TRI, established under Section 313 of the Emergency Planning and Community Right-to-Know Act (EPCRA) (https://www.epa.gov/toxics-release-inventory-tri-program). The TRI covers chemicals that meet at least one of the following criteria: i) linked to cancer or other chronic human health effects, ii) associated with significant adverse acute human health effects, or iii) expected to cause significant adverse environmental effects. The covered list currently includes around 799 individually listed chemicals and 33 chemical categories (see https://www.epa.gov/toxics-release-inventory-tri-program/tri-listed-chemicals). Facilities that emit such chemicals are required to report their annual release quantities to the TRI. Since its inception in 1987, this reporting obligation has applied to facilities that i) employ at least 10 workers, ii) operate in specific 6-digit NAICS sectors, and iii) handle listed chemicals above defined threshold levels.Footnote 2 From the TRI data set, we acquire comprehensive information on reporting facilities, including facility and parent company identifiers (e.g., names and DUNS number), reporting year, and the quantity of each listed chemical released into air, water, or land.

We next merge the TRI data with financial information on U.S. public firms from Compustat. Because the two databases lack a common identifier or linking tables, we rely on name-based matching combined with manual verification, following Akey and Appel (Reference Akey and Appel2021), Chen, Jing, Keasey, and Xu (Reference Chen, Jing, Keasey and Xu2026), Jing, Keasey, Lim, and Xu (Reference Jing, Keasey, Lim and Xu2024), and Li et al. (Reference Li, Xu and Zhu2025). Our matching procedure proceeds in three steps. First, we standardize firm names by removing common suffixes (e.g., “Corp,” “Limited,” “Ltd.”). We then apply a fuzzy string-matching algorithm based on the Levenshtein distance to link TRI parent names to Compustat firm names.Footnote 3 This approach measures the minimum number of single-character edits required to transform one string into another, allowing us to identify matches even when firm names differ slightly due to abbreviations, typographical errors, or formatting inconsistencies. Second, to address time-varying names in both data sources, we incorporate historical names from CRSP and extract historical names and addresses from 10-K, 10-Q, and 8-K filings using the SEC Analytics Suite available through WRDS and Loughran–McDonal database (https://sraf.nd.edu/sec-edgar-data/) (e.g., Loughran and McDonald (Reference Loughran and McDonald2014)). Third, we manually check every algorithmic match.Footnote 4 As an additional check, we compare headquarters locations, official company websites, and DUNS numbers to confirm each link.Footnote 5

TRI reports emissions at the facility-chemical–year level. We construct a firm-year measure of total toxic release by aggregating facility-level emissions across chemicals and facilities owned by the same firm in a given year. Our primary variable is total toxic pollution, defined as the sum of on-site releases (to air, water, and land) and off-site transfers for further treatment, disposal, or release (Jing et al. (Reference Jing, Keasey, Lim and Xu2024), Li et al. (Reference Li, Xu and Zhu2025), (Reference Li, Mai, Wong, Yang and Zhang2026)). Following Jing et al. (Reference Jing, Keasey, Lim and Xu2024) and Li et al. (Reference Li, Xu and Zhu2025), we exclude facilities that report zero toxic emissions throughout the 1990–2019 period.Footnote 6 This procedure leaves us with 20,150 facilities affiliated with 2,135 distinct publicly listed firms.

B. Sample Selection

The primary source for identifying the timing of each state’s anti-SLAPP adoption is the Reporters Committee for Freedom of the Press (RCFP) (https://www.rcfp.org/), which tracks the passage and statutory coverage of anti-SLAPP laws nationwide. To ensure accuracy, we cross-validate the enactment years with prior academic literature, including Chen et al. (Reference Chen, Jing, Keasey and Xu2026) and Li et al. (Reference Li, Xu and Zhu2025), who provide comprehensive timelines of anti-SLAPP implementation suitable for empirical research.

Our initial sample comprises all U.S. firms included in the merged Compustat and CRSP database from 1990 to 2019. We merge these firm-level records with the aggregated toxic release data and exclude firms that operate no reporting facilities. Each firm is then linked to the anti-SLAPP statute of its headquarters state (Chen et al. (Reference Chen, Li and Li2025)). We match the statute with firms’ headquarters for two main reasons. First, anti-SLAPP laws are enacted and enforced at the state level, and courts typically apply the statute of the state where the plaintiff’s principal place of business or domicile is located in defamation or related tort actions. According to the Restatement (Second) of Conflict of Laws (Sections 145 and 150.1), the state of the plaintiff’s principal place of business has the “most significant relationship” in determining the applicable law.Footnote 7 Consequently, when a firm faces public, media, and civil criticism, the applicable anti-SLAPP protections are generally determined by the headquarters state, and the headquarters state thus best captures the firm’s jurisdictional exposure to speech-related legal protections. Second, from an economic standpoint, a firm’s headquarters is the core of strategic decision-making and external communication. It hosts senior management, investor relations, and legal teams, and serves as the primary contact point for analysts, media, and regulators. Local media and residents in the headquarters state often have greater access to firm-specific information and stronger monitoring capacity, making them more responsive to changes in local speech protections. Thus, anti-SLAPP statutes in the headquarters state influence the likelihood that negative environmental information (e.g., pollution events or breaches of environmental regulation) is detected, reported, and disseminated.

To link corporate headquarters to states, we rely on firms’ historical headquarters locations. We first identify each firm’s headquarters state from the 10-K header files using the Loughran–McDonald database (e.g., Loughran and McDonald (Reference Loughran and McDonald2014)), which provides information between 1994 and 2019. We then supplement this information with data from Heider and Ljungqvist (Reference Heider and Ljungqvist2015) and the company header history file in the legacy Compustat/CRSP merged database, as compiled by Bena, Ortiz-Molina, and Simintzi (Reference Bena, Ortiz-Molina and Simintzi2022). Finally, we exclude firms in the financial and utility sectors and remove observations with missing control variables.

Recent finance and econometrics literature indicates that traditional two-way fixed effects Difference-in-Difference (TWFE-DiD) models can produce biased estimates when treatment effects vary across groups or overtime (Goodman-Bacon (Reference Goodman-Bacon2021)). In our setting, this bias may arise because firms in early-treated states can serve as controls for those in later-treated states, causing negative weighting and biasing the estimation of dynamic treatment effects (Goodman-Bacon (Reference Goodman-Bacon2021)). To mitigate this concern, we employ a stacked event-study design (Sun and Abraham (Reference Sun and Abraham2021), Barrios (Reference Barrios2022), and Wing, Freedman, and Hollingsworth (Reference Wing, Freedman and Hollingsworth2024)), which estimates treatment effects relative to adoption cohorts while avoiding comparisons between previously and newly treated units. Specifically, for each treatment year c in which at least one state enacted an anti-SLAPP statute, we form a separate cohort. The treatment sample for cohort c includes firm-year observations within the window [c − 5, c + 5] for firms headquartered in states that enacted anti-SLAPP statutes in year c. The control sample includes firm-year observations within the same window for firms headquartered in states that have not adopted an anti-SLAPP statute by year c + 5. We then stack all cohorts into a single panel for estimation, ensuring that identification relies solely on not-yet-treated states as controls.

In this way, after stacking observations of all cohorts, our final regression sample for the main analysis contains 118,287 cohort-firm-year observations from 1,600 unique firms between 1990 and 2019. We winsorize all continuous variables in each cohort at the 1st and 99th percentiles to mitigate the influence of outliers.

C. Empirical Design

We estimate the following cohort DiD regression using the stacked cohort sample constructed above to test the effect of the anti-SLAPP statutes on corporate toxic release:

$$ {\displaystyle \begin{array}{c}{RELEASE}_{c,i,t}={\beta}_0+{\beta}_1 ANTI\_{SLAPP}_{c,s,t}+\sum {\beta}_k{controls}_{c,i,t}\\ {}+{\gamma}_{c,i}+{\rho}_{c,s}+{\delta}_{c,j,t}+{\varepsilon}_{c,i,t}\end{array}} $$

$$ {\displaystyle \begin{array}{c}{RELEASE}_{c,i,t}={\beta}_0+{\beta}_1 ANTI\_{SLAPP}_{c,s,t}+\sum {\beta}_k{controls}_{c,i,t}\\ {}+{\gamma}_{c,i}+{\rho}_{c,s}+{\delta}_{c,j,t}+{\varepsilon}_{c,i,t}\end{array}} $$

where c denotes the cohort, i the firm, t the year, s the firm’s headquarters state at year t, and j the 48-Fama French code for firm i at year t. In addition,

$ {\gamma}_{c,i} $

,

$ {\gamma}_{c,i} $

,

$ {\rho}_{c,s} $

, and

$ {\rho}_{c,s} $

, and

$ {\delta}_{c,j,t} $

represent cohort–firm, cohort–state, and cohort–industry–year fixed effects, respectively. These fixed effects control for unobserved heterogeneity at the firm, state, and industry–year levels within each anti-SLAPP cohort. Specifically, cohort–firm fixed effects (

$ {\delta}_{c,j,t} $

represent cohort–firm, cohort–state, and cohort–industry–year fixed effects, respectively. These fixed effects control for unobserved heterogeneity at the firm, state, and industry–year levels within each anti-SLAPP cohort. Specifically, cohort–firm fixed effects (

$ {\gamma}_{c,i} $

) absorb time-invariant firm-level characteristics such as baseline environmental practices, managerial culture, and strategic orientation; cohort–state fixed effects (

$ {\gamma}_{c,i} $

) absorb time-invariant firm-level characteristics such as baseline environmental practices, managerial culture, and strategic orientation; cohort–state fixed effects (

$ {\rho}_{c,s} $

) account for persistent differences across states, including civil litigation norms, political climates, and economic conditions that may influence both the adoption and impact of anti-SLAPP laws; cohort–industry–year fixed effects (

$ {\rho}_{c,s} $

) account for persistent differences across states, including civil litigation norms, political climates, and economic conditions that may influence both the adoption and impact of anti-SLAPP laws; cohort–industry–year fixed effects (

$ {\delta}_{c,j,t} $

) capture common shocks or trends affecting firms within the same industry and year, such as sector-wide technological changes or macroeconomic fluctuations. Since the treatment in our setting varies by state, we cluster standard errors at the headquarters-state level, allowing for within-state correlation in the error terms and ensuring valid statistical inference (Imbens and Wooldridge (Reference Imbens and Wooldridge2009)).

$ {\delta}_{c,j,t} $

) capture common shocks or trends affecting firms within the same industry and year, such as sector-wide technological changes or macroeconomic fluctuations. Since the treatment in our setting varies by state, we cluster standard errors at the headquarters-state level, allowing for within-state correlation in the error terms and ensuring valid statistical inference (Imbens and Wooldridge (Reference Imbens and Wooldridge2009)).

Following Akey and Appel (Reference Akey and Appel2021), Chen et al. (Reference Chen, Jing, Keasey and Xu2026), Duchin et al. (Reference Duchin, Gao and Xu2025), Jing et al. (Reference Jing, Keasey, Lim and Xu2024), and Li et al. (Reference Li, Xu and Zhu2025), the dependent variable in equation (1),

$ RELEASE $

, captures corporate environmental policies, proxied by total toxic pollution, including LOG(RELEASE) and sale-adjusted toxic emissions LOG(RELEASE/SALE), where LOG(RELEASE) is the natural logarithm of the amounts of total toxic pollution, and LOG(RELEASE/SALE) is the natural logarithm of sales-adjusted toxic pollution.

$ RELEASE $

, captures corporate environmental policies, proxied by total toxic pollution, including LOG(RELEASE) and sale-adjusted toxic emissions LOG(RELEASE/SALE), where LOG(RELEASE) is the natural logarithm of the amounts of total toxic pollution, and LOG(RELEASE/SALE) is the natural logarithm of sales-adjusted toxic pollution.

$ ANTI\_ SLAPP $

is an indicator that equals to 1 if firm i is headquartered in state s that enacts an anti-SLAPP law in year t, and in all subsequent years. That said, zero values of

$ ANTI\_ SLAPP $

is an indicator that equals to 1 if firm i is headquartered in state s that enacts an anti-SLAPP law in year t, and in all subsequent years. That said, zero values of

$ ANTI\_ SLAPP $

indicate nonadopters or adopters’ preadoption years. A significantly negative coefficient on

$ ANTI\_ SLAPP $

indicate nonadopters or adopters’ preadoption years. A significantly negative coefficient on

$ {\beta}_1 $

would indicate that the adoption of anti-SLAPP laws is associated with a reduction in corporate toxic emissions, consistent with our prediction that amplified stakeholder voice under anti-SLAPP motivates firms to improve their environmental performance.

$ {\beta}_1 $

would indicate that the adoption of anti-SLAPP laws is associated with a reduction in corporate toxic emissions, consistent with our prediction that amplified stakeholder voice under anti-SLAPP motivates firms to improve their environmental performance.

The inclusion of control variables follows prior literature (Akey and Appel (Reference Akey and Appel2021), Jing et al. (Reference Jing, Keasey, Lim and Xu2024), Chen et al. (Reference Chen, Jing, Keasey and Xu2026), and Li et al. (Reference Li, Xu and Zhu2025)). Specifically, we include the logarithm of total assets (SIZE), return on assets (ROA), leverage ratio (LEV), firm age (AGE), cash holdings (CASH), cost of goods sold (COG), selling, general and administrative expense (SG&A), asset tangibility (PPE), research and development expenditure intensity (R&D/AT), an indicator for missing R&D data (MISSINGR&D), dividend payments (DIVIDEND), analysts coverage (ANALYST), and institutional ownership (INS). The definitions of all variables and data sources are summarized in Section A of the Supplementary Material.

D. Descriptive Statistics

Panel A of Table 1 summarizes the descriptive statistics of the variables used in equation (1), derived from the cohort-matched sample.Footnote 8 Firms report an average pollution level of 889.6 thousand pounds with a standard deviation of 3,127 thousand pounds. The log-transformed, sales-scaled measure of pollution (LOG(RELEASE/SALE)) has a mean of 2.997 and a standard deviation of 2.853. The mean value of ANTI_SLAPP is 0.035, comparable to Lee et al. (Reference Lee, Ng, Yoo and Zhang2026). Panel B presents the distribution of pollution by year. Average firm-level emissions, measured in thousands of pounds, decline steadily from the early 1990s to the late 2010s. Specifically, mean releases fall from about 1,130 thousand pounds in 1990 to 750 thousand pounds in 2019, indicating marked improvements in environmental efficacy. The log-transformed measures, both unscaled and sales-scaled, exhibit a similar downward trend.

TABLE 1 Descriptive Statistics and Sample Distribution

Panel C of Table 1 presents the breakdown of pollution by industry (Fama–French 48 industry groups). The data reveal substantial cross-industry heterogeneity. Toxic emissions are highly concentrated in a few resource- and energy-intensive sectors, such as Precious Metals, Steel Works, Petroleum and Natural Gas, Chemicals, and Business Supplies, where average emissions exceed 2,400 thousand pounds. In contrast, sectors such as Agriculture, Construction, and Candy & Soda record relatively lower emissions. The log-scaled measures (LOG(RELEASE/SALE)) further confirm that heavy manufacturing and extraction industries, as well as material-intensive sectors, dominate total reported releases.

IV. Main Results and Discussions

A. Does the Adoption of Anti-SLAPP Laws Relate to Decreases in Toxic Releases?

We predict firms to improve environmental performance by engaging in lower toxic releases following the enactment of anti-SLAPP laws. Table 2 reports the estimation results of equation (1), which examines the association between anti-SLAPP enactments and firms’ toxic emissions.

TABLE 2 The Effect of Anti-SLAPP Laws on Corporate Toxic Emissions

Across all specifications, the coefficients on ANTI_SLAPP are significant and negative, suggesting that firms significantly reduce toxic pollution after the enactment of anti-SLAPP laws. This finding is consistent with our conjecture that stronger free-speech protection amplifies stakeholder voice related to environmental issues, and firms are motivated to improve corporate environmental performance. We find that the effect is also economically significant. In column 2, the coefficient on ANTI_SLAPP (i.e., −0.5308) implies that for an average firm in our sample, total toxic releases decrease by approximately 41% following anti-SLAPP adoption; in column 4, the corresponding coefficient (i.e., −0.2017) suggests that the firm’s sales-adjusted pollution intensity declines by about 18%.Footnote 9 Therefore, the implementation of anti-SLAPP statutes leads to a significant and economically meaningful improvement in corporate environmental performance, reducing both the absolute and relative levels of toxic emissions.Footnote 10

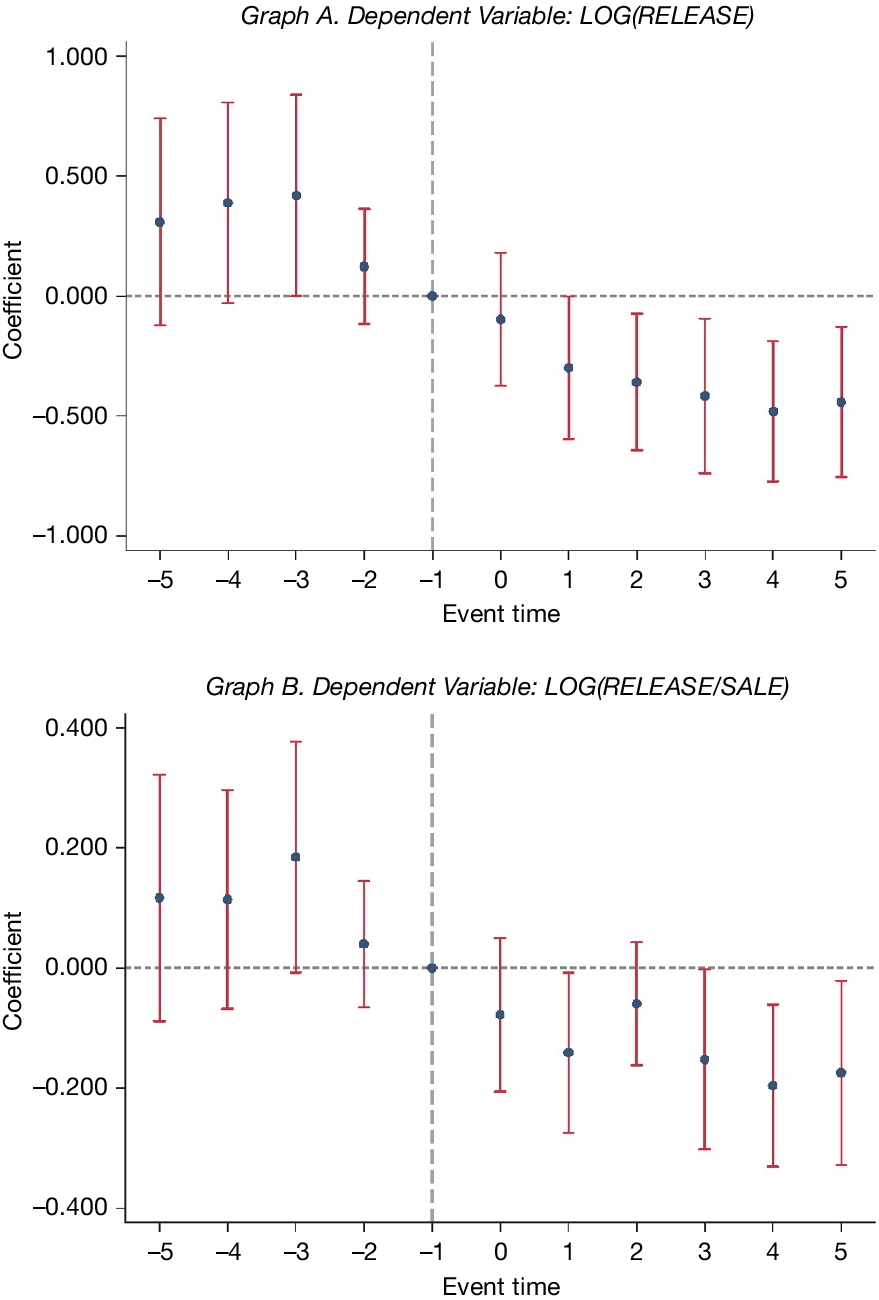

B. Dynamic Treatment Effects of Anti-SLAPP on Toxic Releases

To satisfy the DiD identification requirement, we assume that, in the absence of anti-SLAPP laws, firms in the treatment and control groups would have followed parallel trends in toxic emissions over time. To assess this assumption, we estimate dynamic treatment effects by replacing the anti-SLAPP indicator in equation (1) with a set of event-year dummies for treatment firms, spanning 5 years before to 5 years after adoption (t = −5 to t = 5), excluding year t = −1 as the reference period. The event-study specification, as shown in equation (2), provides both a visual and statistical test of the parallel-trend assumption and allows us to examine the timing of anti-SLAPP law effects on toxic emissions.

$$ {\displaystyle \begin{array}{c}{RELEASE}_{c,i,t}={\beta}_0+\sum \limits_{l=-5,l\ne -1}^{l=5}{\beta}_l\times {Treat}_{i,c}\times {Year}_l+\sum {\beta}_k{controls}_{c,i,t}\\ {}\hskip-9em +\hskip0.35em {\gamma}_{c,i}+\hskip0.35em {\rho}_{c,s}+\hskip0.35em {\delta}_{c,j,t}+\hskip0.35em {\varepsilon}_{c,i,t}\end{array}} $$

$$ {\displaystyle \begin{array}{c}{RELEASE}_{c,i,t}={\beta}_0+\sum \limits_{l=-5,l\ne -1}^{l=5}{\beta}_l\times {Treat}_{i,c}\times {Year}_l+\sum {\beta}_k{controls}_{c,i,t}\\ {}\hskip-9em +\hskip0.35em {\gamma}_{c,i}+\hskip0.35em {\rho}_{c,s}+\hskip0.35em {\delta}_{c,j,t}+\hskip0.35em {\varepsilon}_{c,i,t}\end{array}} $$

Graphs A and B of Figure 1 present the dynamic treatment effects of anti-SLAPP enactments on LOG(RELEASE) and LOG(RELEASE/SALE) for a [c − 5, c + 5] window. The results suggest that trends for the treatment and control firms remain fairly parallel during the pre-event period, consistent with the parallel-trend assumption, while in the postevent period following anti-SLAPP enactment, firm toxic release decreases visibly.

FIGURE 1 Dynamics of the Changes in Toxic Release Around the Anti-SLAPP Enactment Years

Figure 1 shows the dynamic treatment effects (5-year lag and 5-year lead) of anti-SLAPP and time trends on annual toxic emissions. In Graph A, the dependent variable is LOG(RELEASE), while the dependent variable is LOG(RELEASE/SALE) in Graph B. Variables are defined in Appendix A.

C. Robustness Checks

1. Alternative Measurements

To mitigate potential measurement errors of our key constructs, we examine the robustness of our findings using alternatively defined measurements for toxic emissions and anti-SLAPP enactments.

Specifically, we follow Chen et al. (Reference Chen, Jing, Keasey and Xu2026) and Naaraayanan, Sachdeva, and Sharma (Reference Naaraayanan, Sachdeva and Sharma2021) and employ two alternative output-adjusted measures of toxic emissions, namely LOG(REVENUE_ADJ) and LOG(ASSET_ADJ). Furthermore, following Li et al. (Reference Li, Xu and Zhu2025), we construct another four alternative measures of this construct: i) on-site releases only, LOG(ONSITE); ii) releases covered by the Clean Air Act (air pollutants), LOG(CAA); iii) persistent bioaccumulative toxic (PBT) chemicals release, LOG(PBT) (https://www.epa.gov/toxics-release-inventory-tri-program/persistent-bioaccumulative-toxic-pbt-chemicals-rules-under-tri); and iv) total releases weighted by the EPA’s Risk-Screening Environmental Indicators (RSEI) hazard score, LOG(RSEI) (https://www.epa.gov/sites/default/files/2015-08/documents/rsei_methodology_v2_3_3_0.pdf). We use each of these measures as the dependent variable in equation (1). Panel B of Table 2 presents the regression results. The coefficients on ANTI_SLAPP are significantly negative across all columns, indicating that the documented reduction in toxic emissions under anti-SLAPP laws is robust to alternative measures of environmental performance.

Next, we test the robustness of our findings using alternative data sources to measure firms’ environmental performance. First, following Li et al. (Reference Li, Mai, Wong, Yang and Zhang2026), we draw on Refinitiv’s ESG database (formerly Thomson Reuters ASSET4) and use E_SCORE and E_GRADE as alternative dependent variables for corporate environmental performance. Second, following Sautner, van Lent, Vilkov, and Zhang (Reference Sautner, van Lent, Vilkov and Zhang2023) and Li et al. (Reference Li, Mai, Wong, Yang and Zhang2026), we source carbon emissions from S&P Global Trucost. Because pollution may reflect an unavoidable by-product of production, such as carbon dioxide (CO2) emissions in cement manufacturing (Jaffe, Newell, and Stavins (Reference Jaffe, Newell, Stavins, Mäler and Vincent2003)), we interpret emissions measures with this nuance in mind. We use LOG(CO2), the natural logarithm of direct (Scope 1) and indirect (Scope 2) emissions, and LOG(CO2/SALE), sales-adjusted carbon emissions.Footnote 11 Third, consistent with Li et al. (Reference Li, Mai, Wong, Yang and Zhang2026), we use environmental scores from RiskMetrics KLD database (ENV_KLD). We re-estimate equation (1) using each alternative dependent variable. Panel C of Table 2 shows that the main results on anti-SLAPP enactment remain consistent.

We further test the robustness of our findings using alternative measures of anti-SLAPP law strength. Based on information available on the EPA website (https://www.epa.gov/assessing-and-managing-chemicals-under-tsca/persistent-bioaccumulative-and-toxic-pbt-chemicals (PBT chemicals), https://www.epa.gov/rsei/rsei-results-definitions (RSEI Score)), we use COVERED SPEECH SCORE, which reflects the extent of protected speech under each state’s law; PROCEDURES SCORE, which measures the comprehensiveness of procedural protections for defendants; and ANTI_SLAPP SCORE, a composite measure derived from COVERED SPEECH SCORE and PROCEDURES SCORE. These scores capture the breadth of protection, procedural rigor in filing and adjudicating motions to dismiss, and the evidentiary burden required for dismissal. For preenactment years and states where the law has not been enacted, we assign a score of zero. Each score is divided by 100 and used to re-estimate equation (1). Panel D of Table 2 presents the regression results. In all columns, the alternative anti-SLAPP measurements remain negative and statistically significant, suggesting that stronger legal protections for speech are consistently associated with lower levels of toxic emissions, which confirms our main results and indicates that greater free-speech protections strengthen stakeholder monitoring and corporate environmental accountability.

2. Other Robustness Checks

We conduct several additional robustness tests. First, we validate our setting by examining whether strengthened protection of free speech encourages the media to report more extensively on corporate environmental issues. We obtain data from RavenPack to measure the number of environmentally related news articles, that is, LOG(ENV_NEWS), and their sentiment, that is, ENV_NEWS_SENTI. We also follow Li et al. (Reference Li, Mai, Wong, Yang and Zhang2026) and use RepRisk incident-level data, where we retain only environmental- and social-related incidents to capture the number of negative environmental news items in a given year, that is, LOG(ENV_INCIDENTS). We re-estimate equation (1) using each of these variables as the dependent variable. Table 1 in the Supplementary Material reports the results. The coefficients on ANTI_SLAPP are significantly positive in columns 1 and 3, and significantly negative in column 2, which indicates that, consistent with our proposition, the enactment of anti-SLAPP laws significantly increases the media coverage of corporate environmental performance, especially negative news.

Next, following Li et al. (Reference Li, Xu and Zhu2025), we rerun equation (1) using RELEASE as the dependent variable in a Poisson model within the cohort DiD framework. Column 1 of Table 2 in the Supplementary Material reports the results, showing that the coefficient on ANTI_SLAPP remains significantly negative. We also obtain consistent findings when applying alternative event windows, that is, [−3, +3] and [−7, +7], before and after the law’s enactment, as shown in columns 2–5.

To address potential nonrandom selection into the treatment group, we implement a PSM approach. Specifically, we construct matched samples using 1:1 nearest neighbor matching and radius caliper matching, respectively.Footnote 12 In addition, we create weighted samples based on inverse probability weighting (IPW) and entropy balancing to further ensure covariate balance between treated and control firms. Table 3 in the Supplementary Material reports the results. Across all specifications, the coefficients on ANTI_SLAPP remain negative and statistically significant, which suggests that the positive association between anti-SLAPP laws and corporate toxic release is robust after controlling for potential sample selection bias.

We further conduct a placebo test to check if our findings are driven by spurious correlations. Specifically, we generate a series of placebo events, where we repeatedly draw a random subset of firms 2,000 times without replacement as “fake treated units.” Each is assigned a randomly chosen common “fake treated year.” We then re-estimate equation (1) using these simulated placebo treatments. This procedure produces a distribution of placebo effects against which the actual treatment effect can be benchmarked. Figure 1 in the Supplementary Material plots the coefficients on ANTI_SLAPP using LOG(RELEASE) and LOG(RELEASE/SALE) as the dependent variable, respectively; both coefficients are not significantly different from zero, consistent with our main findings.

V. Mechanism Analyses

Our findings thus far indicate that the enactment of anti-SLAPP statutes is associated with significant reductions in corporate toxic emissions. In this section, we investigate the underlying mechanisms through which these free-speech protections influence firms’ environmental performance.

A. Environmental Investment

Under amplified stakeholder voice following the anti-SLAPP laws, firms may increase investment in cleaner technologies, innovation, and pollution control initiatives to mitigate reputational and regulatory risks. We explore this mechanism along four dimensions: green innovation, environmental investment spending, pollution source reduction, and waste management activities.

1. Green Innovation

We begin by examining whether anti-SLAPP statutes promote corporate green innovation. To measure innovation outcomes, we use firm-level patent data compiled by Kogan, Papanikolaou, Seru, and Stoffman (Reference Kogan, Papanikolaou, Seru and Stoffman2017) (KPSS).Footnote 13 Green patents are identified based on classifications provided by Haščič and Migotto (Reference Haščič and Migotto2015), using the International Patent Classification (IPC) system maintained by the World Intellectual Property Organization (WIPO).Footnote 14 The dependent variable, GREEN_PATENT, measures the number of green patents that firm i applies in year t and are ultimately granted. We estimate equation (1) using a Poisson model.Footnote 15 Column 1 of Table 3 shows that firms affected by anti-SLAPP laws produce significantly more green patents. This result suggests that enhanced stakeholder voice and public accountability foster the development of cleaner technologies and environmental innovation.

TABLE 3 Mechanism Analysis Results: Environmental Investment

2. Environmental Capital Spending

Next, we examine whether anti-SLAPP legislation motivates firms to allocate more financial resources toward pollution abatement. Following Fiechter, Hitz, and Lehmann (Reference Fiechter, Hitz and Lehmann2022) and Li et al. (Reference Li, Mai, Wong, Yang and Zhang2026), we use Refinitiv data that captures firms’ investment in cleaner technologies designed to reduce future environmental risks. We construct a dummy variable, ENV_INV, equal to 1 if a firm reports such initiatives, and 0 otherwise.Footnote 16 As reported in column 2 of Table 3, firms subject to anti-SLAPP laws are significantly more likely to engage in pollution abatement and prevention spending. This finding supports the view that stronger public oversight motivates firms to invest in environmental improvements.

3. Source Reduction Practices

We further assess whether firms respond to anti-SLAPP laws by adopting more pollution prevention practices. Drawing on the U.S. EPA Pollution Prevention (P2) database (https://www.epa.gov/toxics-release-inventory-tri-program/pollution-prevention-p2-and-tri), we identify initiatives that reduce, eliminate, or prevent pollution at its source, before recycling, treatment, or disposal. The P2 database distinguishes between operations-related and production-related activities. Operations-related practices aim to reduce toxic emissions and waste through improvements in operating processes and procedures. Examples include enhanced maintenance scheduling and record-keeping, improved inventory control through efficient storage and handling of chemicals and materials, and more effective spill and leak prevention through monitoring programs and equipment inspections. Production-related practices focus on improving the techniques, materials, and equipment used in manufacturing. Such practices involve process modifications, surface preparation and finishing, cleaning and degreasing methods, product redesign, and adjustments in raw material usage.

Following Li et al. (Reference Li, Xu and Zhu2025), we count the total number of newly initiated source reduction activities at the facility level in a given year and aggregate them to the firm level to construct LOG(SOURCE_REDUC). We then examine whether the enactment of anti-SLAPP laws leads firms to adopt more pollution source reduction activities. The results are presented in column 3 of Table 3. Consistent with our expectation, the coefficient on ANTI_SLAPP is significantly positive, indicating that firms located in states with stronger free-speech protections are more proactive in implementing pollution prevention practices. This evidence suggests that amplified stakeholder voice encourages firms to take more preventive approaches to environmental management.

4. Waste Management Activities

We further examine firms’ postproduction waste management efforts, which mitigate environmental harms after pollutants are generated and help minimize their ultimate release into the environment. These activities include recycling (the reuse of discarded materials in producing new products) and combustion for energy recovery and treatment processes, such as incineration and oxidation, that destroy or neutralize toxic chemicals. To capture the effectiveness of these practices, we calculate WASTE_MGNT, the fraction of waste reduced through postproduction waste management approaches relative to total generated waste. The results, reported in column 4 of Table 3, show that the coefficient on ANTI_SLAPP is significantly positive, which suggests that firms in treated states eliminate a larger proportion of toxic chemicals through postproduction waste management.

In sum, the collective results indicate that firms respond to anti-SLAPP laws by undertaking a broad spectrum of environmental investments and deploying financial and technological resources to improve environmental performance, thereby driving the significant reduction in toxic emissions documented earlier.

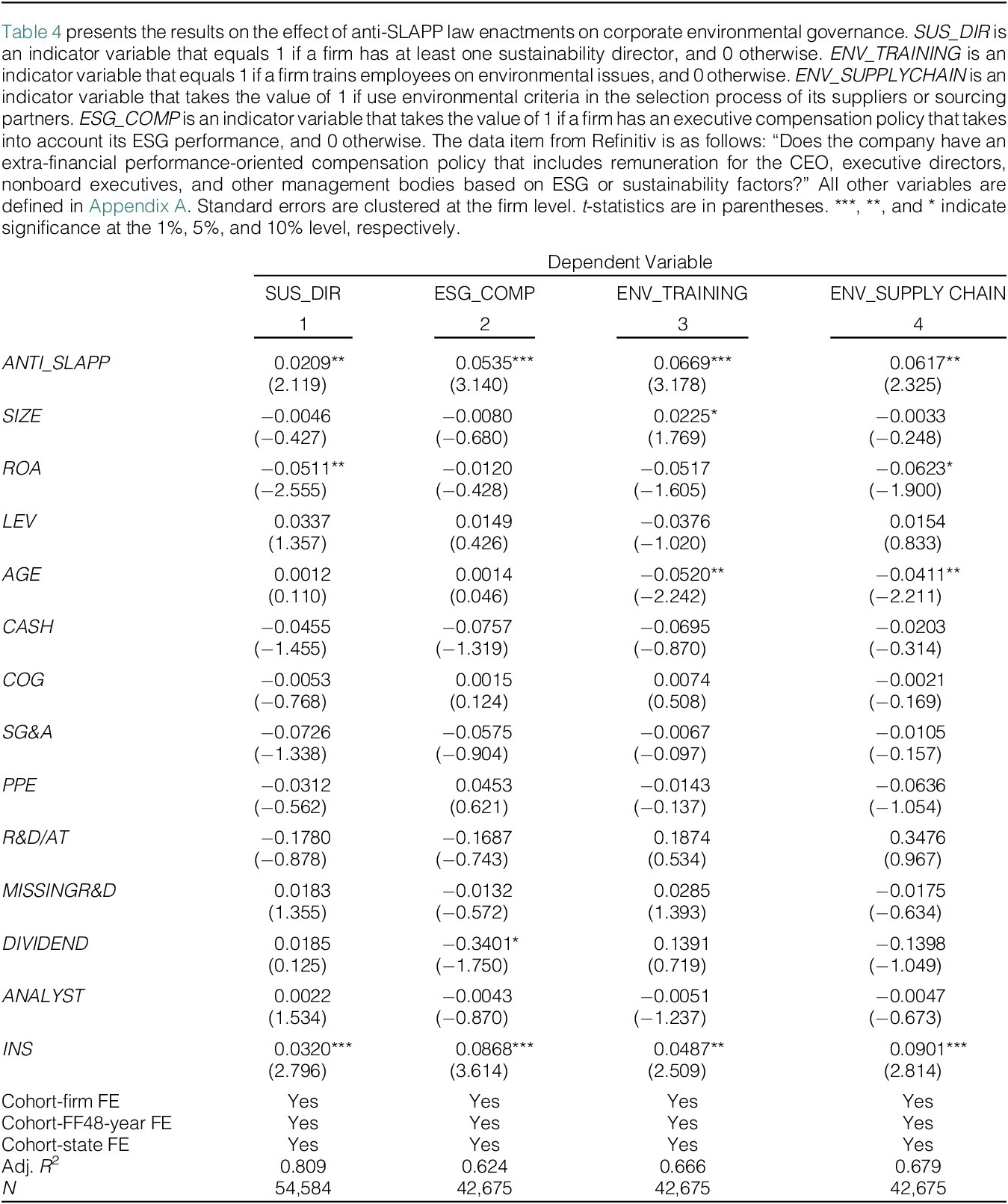

B. Environmental Governance

Our second mechanism focuses on environmental governance, which reflects the organizational structures and managerial systems through which firms integrate environmental considerations into corporate decision-making, aimed at improved environmental performance. We examine this mechanism across four dimensions, including the appointment of sustainability-related directors on the board, ESG-linked executive compensation, employee environmental training, and environmentally responsible supply chain management.

1. Sustainability Directors

We first examine whether treated firms are more likely to appoint a sustainability director. Appointing a sustainability director embeds accountability and expertise in environmental oversight, helping ensure sustainability goals are integrated into both strategic and operational decisions.

Director information is obtained from BoardEx. Following Chen et al. (Reference Chen, Jing, Keasey and Xu2026) and Fu, Tang, and Chen (Reference Fu, Tang and Chen2020), we classify a director as sustainability-related if their job title or description includes the terms of sustainability, sustainable, responsibility, ethics, or environment. We then create an indicator variable, SUS_DIR, which equals 1 for firm-years with at least one such director, and 0 otherwise. Column 1 of Table 4 shows a positive and statistically significant association between anti-SLAPP enactment and the likelihood of appointing a sustainability director. This result suggests that firms operating under stronger free-speech protection allocate more internal governance resources to environmental and ethical oversight. It also indicates that heightened stakeholder scrutiny encourages firms to formalize sustainability leadership roles, thereby signaling a stronger commitment to responsible management.

TABLE 4 Mechanism Analysis Results: Environmental Governance

2. Executive Compensation Linked to ESG

We next examine whether firms incorporate ESG performance metrics into executive compensation to encourage improved environmental performance. Using data from Refinitiv ESG, we construct a firm-year indicator equal to 1 if a firm’s compensation policy explicitly links executive remuneration to ESG or sustainability performance, and 0 otherwise.Footnote 17 Column 2 of Table 4 reports a positive and statistically significant association between the adoption of anti-SLAPP statutes and the likelihood of implementing ESG-linked compensation, consistent with the view that great public accountability encourages firms to align managerial incentives with environmental goals.

3. Environmental Training

We then examine whether firms improve environmental performance by strengthening employee environmental training programs in response to anti-SLAPP laws. Using Refinitiv data and following Fiechter et al. (Reference Fiechter, Hitz and Lehmann2022), we construct ENV_TRAINING, an indicator equal to 1 if a firm provides employees with training on environmental issues (e.g., resource conservation, emission reduction, or environmental codes of conduct), and 0 otherwise.

As shown in column 3 of Table 4, the coefficient on ANTI_SLAPP is positive and statistically significant, suggesting that treated firms are more likely to adopt employee training initiatives. So, our finding indicates that anti-SLAPP legislation fosters greater internal environmental awareness and capability building through workforce education.

4. Environmental Supply Chain Management

Supply chains represent a substantial portion of a firm’s environmental footprint. The governance of up and downstream partners is a critical aspect of firms’ internal environmental governance. Incorporating environmental criteria into supplier selection and monitoring enables firms to extend sustainability standards beyond their own operations. We next examine whether firms implement environmental management practices within their supply chains.

Sourcing data from Refinitiv, we identify two relevant items: i) whether the company applies environmental criteria (e.g., ISO 14000 certification, energy consumption standards, etc.) in the selection of suppliers or sourcing partners; and ii) whether it conducts surveys assessing the environmental performance of its suppliers. We construct an indicator variable, ENV_SUPPLYCHAIN, which equals 1 if a firm engages in either of these practices, and 0 otherwise. Column 4 of Table 4 shows a significantly positive relationship between anti-SLAPP adoption and the likelihood of implementing green supply chain practices, reflecting broader diffusion of environmental governance throughout the corporate value chain.

Together, these results indicate that anti-SLAPP laws strengthen corporate environmental governance and that such governance enhancements provide a credible mechanism through which legal protections for free speech translate into improved corporate environmental performance.

VI. Additional Analyses

A. Cross-Sectional Analyses

In this section, we examine whether the effect of anti-SLAPP statutes on firms’ toxic emissions varies across firms with different levels of stakeholder scrutiny and managerial incentive alignment. We argue that while enhanced protection of free speech amplifies public oversight, the extent to which firms respond depends on their external exposure to stakeholder pressure and internal incentive to pursue sustainable practices.

1. External Stakeholder Pressure

We first examine whether the effect is more pronounced among firms subject to greater external stakeholder pressure. Firms that rely heavily on government clients or operate in regions with active environmental NGOs arguably face stronger reputational and regulatory monitoring, making them more responsive to public criticism under anti-SLAPP protections.

To test this prediction, we employ two proxies for external stakeholder pressure: GOV_CUS is an indicator equal to 1 if the firm has government customers, and 0 otherwise, which captures exposure to government procurement oversight and the reputational constraints associated with serving public clients; ENV_EGO measures the average intensity of environmental NGOs in a firm’s headquarters state, reflecting the strength of local activist and advocacy monitoring. Both variables are measured before anti-SLAPP law adoption to mitigate endogeneity concerns related to concurrent institutional changes.

We interact these variables with the anti-SLAPP indicator and re-estimate equation (1) with these interaction terms included. Panel A of Table 5 presents the results. Columns 1 and 2 report regressions interacting ANTI_SLAPP with GOV_CUS, while columns 3 and 4 use ENV_EGO as the moderating variable. Across all specifications, the coefficients on the interaction terms are significantly negative, suggesting that, in line with our prediction, the reduction in firms’ toxic emissions following the enactment of anti-SLAPP laws is more pronounced among firms facing greater stakeholder exposure.

TABLE 5 Cross-Sectional Analysis Results

2. Managerial Incentive Alignment

Next, we explore whether firms’ responses to anti-SLAPP laws vary with managerial incentives from compensation design and investors’ sustainability preferences. Managerial compensation design guides executives’ behavior by aligning rewards with performance objectives (Meckling and Jensen (Reference Meckling and Jensen1976), Core, Guay, and Verrecchia (Reference Core, Guay and Verrecchia2003)), and investor ownership shapes managerial incentives through monitoring and preference transmission (Fiechter et al. (Reference Fiechter, Hitz and Lehmann2022), Heath et al. (Reference Heath, Ringgenberg, Samadi and Werner2023b)). We contend that firms whose managerial incentives are more attuned to long-term environmental goals are more responsive to heightened stakeholder scrutiny under anti-SLAPP laws. However, when executives are rewarded primarily for short-term performance, and investors emphasize near-term financial returns over sustainability goals, the effect of anti-SLAPP protections on improving corporate environmental performance is expected to weaken.

We use two variables to capture these dimensions. SHORT_COMP is the average ratio of short-term to total executive compensation in the pretreatment period. A higher value of SHORT_COMP indicates a compensation structure that incentivizes a reduced tendency to focus on long-term sustainability outcomes. ESG_FUND measures the average pretreatment ownership by ESG-oriented institutional investors (Krueger et al. (Reference Krueger, Sautner and Starks2020), Heath et al. (Reference Heath, Macciocchi, Michaely and Ringgenberg2023a)), reflecting the intensity of monitoring by socially responsible investors who prioritize environmental stewardship.

Panel B of Table 5 presents the results. Columns 1 and 2 examine the moderating role of short-term compensation incentives, while columns 3 and 4 focus on ESG-oriented institutional ownership. The results show that the effects of anti-SLAPP are weaker for firms with higher SHORT_COMP and stronger for those with greater ESG_FUND, suggesting that managerial myopia derived from compensation design constraints, whereas ESG-oriented investors enhance firms’ environmental responses to heightened stakeholder scrutiny.

Taken together, these cross-sectional findings suggest that stakeholder pressure and managerial incentive alignment jointly affect firms’ responses to enhanced speech protections for stakeholders, as reflected in their environmental performance. Overall, the results highlight that stronger external oversight and closer alignment of managerial incentive to ESG goals enhance the effectiveness of anti-SLAPP statutes in promoting corporate environmental improvement.

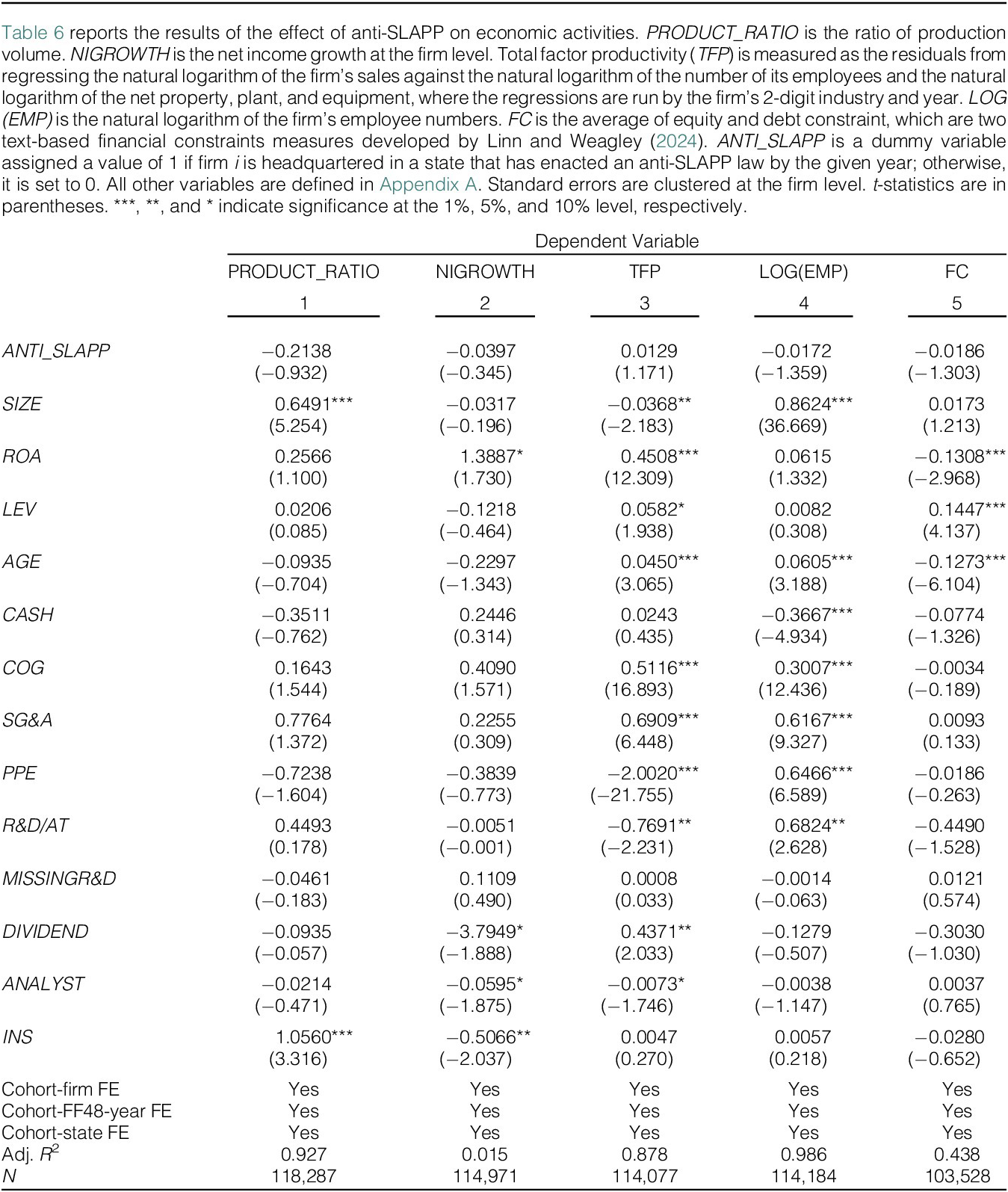

B. Does Anti-SLAPP Reduce Toxic Releases by Shrinking Firms’ Economic Activities?

We have by far documented that anti-SLAPP statutes are associated with lower toxic releases and improved environmental practices. However, a potential concern is that the observed decline in emissions could stem from reduced economic activity rather than genuine environmental improvement. As noted by Akey and Appel (Reference Akey and Appel2021), firms may lower reported emissions simply by scaling down production or operations. To address this concern, we test whether the enactment of anti-SLAPP laws leads to a significant decline in firms’ economic activities.

We employ five proxies to capture firm-level economic performance. First, we use the current-year production ratio from the TRI database. We aggregate facility-level ratios to the firm-year level to obtain PRODUCT_RATIO. Footnote 18 Second, NIGROWTH measures a firm’s annual growth rate of net income. Third, TFP stands for total factor productivity, which captures a firm’s efficiency in generating output given its labor and capital inputs. Specifically, we estimate TFP as the residual from regressing the natural logarithm of firm sales on the logarithms of the number of employees and net property, plant, and equipment, with regressions conducted separately by 2-digit industry and year. Fourth, we measure firm size by the number of employees (i.e., LOG(EMP)) to capture firms’ production scale and operational activity. Finally, FC, a financial-constraint index (Linn and Weagley (Reference Linn and Weagley2024)), reflects firms’ capability to sustain investment and operations—a decline in financial flexibility would indicate economic slowdown.

The results, reported in columns 1–5 of Table 6, consistently show that the coefficients on the anti-SLAPP indicator are statistically insignificant. These findings suggest that the implementation of anti-SLAPP laws does not significantly affect firms’ production activities or overall economic operations. Therefore, the observed reduction in toxic emissions likely reflects genuine environmental improvement rather than a contraction in firm scale.

TABLE 6 Do Anti-SLAPP Laws Shrink Economic Activities?

VII. Conclusion

This study documents a theoretical and empirical link between stronger speech protections and corporate environmental performance. Utilizing an asynchronous, state-by-state rollout of U.S. anti-SLAPP statutes, we apply a stacked DiD design and analyze 118,287 firm-year observations from 1990 to 2019. We find that the enactment of anti-SLAPP laws relates to a significant reduction in toxic emissions. Further, these effects are not driven by a contraction in firms’ economic activities. Instead, firms tend to increase their environmental investment, as evidenced by greater green patenting, higher environmental spending, and more extensive source reduction and waste management efforts. They also strengthen their environmental governance by appointing sustainability directors, linking executive pay to ESG performance, providing employees with environmental training, and incorporating environmental responsibility into supply chain management, following anti-SLAPP adoption. Cross-sectional analyses show that the effect of anti-SLAPP laws is more pronounced among firms exposed to greater stakeholder oversight and those with stronger managerial incentive alignment toward long-term ESG goals.

Taken together, our findings suggest that legal reforms unrelated to the environment can nonetheless steer firms toward substantive sustainability improvements through accountability and stakeholder voice. Our study also yields valuable regulatory implications, as our findings suggest that strengthening speech protections can serve as a cost-effective complement to traditional environmental regulation to ensure that heightened scrutiny translates into improved corporate commitment to sustainable practices.

Appendix A. Variable Definitions

Main Analysis

- RELEASE:

-

Total quantity of emissions at the firm level. Source: TRI.

- LOG(RELEASE):

-

Natural logarithm of the amounts of total toxic pollution. Source: TRI.

- LOG(RELEASE/SALE):

-

Natural logarithm of sales-adjusted toxic pollution. Source: TRI.

- ANTI_SLAPP:

-

Indicator equal to 1 if firm i is headquartered in a state that has enacted an anti-SLAPP law by the given year; 0 otherwise. Source: IFS.

- SIZE:

-

Natural logarithm of total assets. Source: Compustat.

- ROA:

-

Net income scaled by total assets. Source: Compustat.

- LEV:

-

(long-term debt + debt in current liabilities) scaled by total assets. Source: Compustat.

- AGE:

-

Natural logarithm 1 plus years since a firm first appears in Compustat. Source: Compustat.

- CASH:

-

Cash holding scaled by year-end total assets. Source: Compustat.

- COG:

-

Cost of goods sold scaled by year-end total assets. Source: Compustat.

- SG&A:

-

Selling, general, and administrative expenses scaled by year-end total assets. Source: Compustat.

- PPE:

-

Property, plant, and equipment scaled by year-end total assets. Source: Compustat.

- R&D/AT:

-

R&D expense scaled by year-end total asset. Source: Compustat.

- MISSINGR&D:

-

Indicator equal to 1 if R&D expense is missing values, and 0 otherwise. Source: Compustat.

- DIVIDEND:

-

(Common dividends + preferred dividends) scaled by total assets. Source: Compustat.

- ANALYST:

-

Natural logarithm of 1 plus the arithmetic mean of the 12 monthly number of earnings forecasts for a firm. Source: IBES.

- INS:

-

Percentage of institutional shareholdings. Source: LSEG.

Robustness Tests

- LOG(ONSITE):

-

Natural logarithm of 1 plus the amount of firms’ onsite release. Source: TRI.

- LOG(CAA):

-

Natural logarithm of 1 plus the amount of toxic release under the Clean Air Act (CAA). Source: TRI.

- LOG(RSEI):

-

Natural logarithm of 1 plus the amount of total release weighted by EPA’s Risk-Screening Environmental Indicators (RSEI) hazard score. Source: TRI.

- LOG(REVENUE_ADJ):

-

Natural logarithm of 1 plus revenue-adjusted toxic pollution. Source: TRI.

- LOG(ASSET_ADJ):

-

Natural logarithm of 1 plus asset-adjusted toxic pollution. Source: TRI.

- E_SCORE:

-

Environmental score, ranging from 0 to 1. Source: Refinitiv.

- E_GRADE:

-

Environmental rating, ranging from D– (assign 1) to A+ (assign 11). Source: Refinitiv.

- LOG(CO2):