1. Introduction

Optimal investment theory is an important topic in quantitative risk management and involves determining how to allocate capital among available securities in order to maximize the expected return for a given level of risk or minimize the associated risk for a given level of return. Markowitz [Reference Markowitz13] proposed the first quantitative method for determining the optimal portfolio based on minimizing the portfolio variance for a given expectation, called mean-variance principle. In classical optimal investment theory, the distribution obeyed by the data is usually assumed to be known or an empirical distribution function is used instead of the unknown distribution, whereas in practice, the distribution obeyed by the data cannot be determined if the complete data is not available or if a small sample of data is obtained and an empirical distribution function cannot be used. This resulted in other samples performing poorly.

Motivated by this, distributionally robust optimization (DRO) has emerged as a paradigm aimed at finding a solution that is protected against sampling errors [Reference Delage and Ye6]. It seeks for a solution that performs the best with respect to the most adversarial distribution from a set of distributions, known as ambiguity set. The DRO identifies the most adversarial distribution, the worst-case distribution, from an ambiguity set, and makes an optimal decision, the optimal portfolio, which minimizes the cost induced by the worst-case distribution. The choice of a proper ambiguity set is crucial in DRO. Such DRO problem and its robust decision have been verified to exhibit some desirable properties such as finite-sample guarantee and computational tractability, which are in sharp contract with the classic stochastic optimization problem. Hence, DRO has been widely applied in data-driven problems arising from many operations research and machine learning applications. Among others, in portfolio selection, Blanchet et al. [Reference Blanchet, Chen and Zhou3] consider DRO based on mean-variance principle. The same principle is also used in Calafiore and Ghaoui [Reference Calafiore and Ghaoui4], Zhu et al. [Reference Zhu, Zhang and Ye22] and Popescu [Reference Popescu17], in which a linear-chance-constrained problem, a minimax regret objective and a portfolio optimization problem are considered, respectively. However, mean-variance principle has been criticized for that its measure of risk, variance, is not a monotone measure. Shadwick and Keating [Reference Shadwick and Keating18] introduced the Omega ratio to analyze information on the distribution of potential returns. Essentially, it is the ratio of the upside of an investment to the downside. Omega ratio has been verified to provide a new perspective in the performance evaluation of hedge funds [Reference Shadwick and Keating18] and build as a useful measure [Reference Bertrand and Prigent1]. Therefore, in this paper, we focus on DRO based on the mean-Omega ratio principle in portfolio selection. Specifically, we first calculate the worst-case Omega ratio from the ambiguity set and then find the optimal portoflio, which minimizes the worst-case Omega ratio. While the current paper focuses on mean-Omega ratio principles, we should point out that recently several other works have explored other measures such as mean-VaR and mean-CVaR in distributionally robust portfolio selection (see [Reference Kang, Li, Li and Zhu11, Reference Kang, Zhao and Sun12] and the references therein).

In addition to the principle employed in DRO, the choice of a proper ambiguity set is crucial in DRO. In particular, one common way of defining the set  ${\cal F}$ is through specifying the moments of the distribution (see, e.g., [Reference Bertsimas, Doan, Natarajan and Teo2, Reference Delage and Ye6, Reference Natarajan, Sim and Uichanco15, Reference Popescu17, Reference Wiesemann, Kuhn and Sim21]); DRO problems based on moments information has been proved to have a tractable form in applications. So we will first consider the worst-case Omega ratio based on the mean-variance information. Motivated by recent advances in data-driven DRO problem, we also consider that the uncertainty set is the Wasserstein ball centred at the empirical distribution. The Wasserstein ball that is centered at the empirical distribution has become popular as it can make full use of the data, and this ambiguity set has become an attractive ambiguity set adopted in DRO. To solve a DRO problem, identifying the most adversarial distribution, the worst-case distribution, from an ambiguity set is essential. We first study the worst-case distribution and calculate its Omega ratio. The worst-case Omega ratio is calculated under mean-variance uncertainty set and mean-Wasserstein uncertainty set, respectively. With aid of the projection result of the two ambiguity sets, we apply the results in the portfolio selection.

${\cal F}$ is through specifying the moments of the distribution (see, e.g., [Reference Bertsimas, Doan, Natarajan and Teo2, Reference Delage and Ye6, Reference Natarajan, Sim and Uichanco15, Reference Popescu17, Reference Wiesemann, Kuhn and Sim21]); DRO problems based on moments information has been proved to have a tractable form in applications. So we will first consider the worst-case Omega ratio based on the mean-variance information. Motivated by recent advances in data-driven DRO problem, we also consider that the uncertainty set is the Wasserstein ball centred at the empirical distribution. The Wasserstein ball that is centered at the empirical distribution has become popular as it can make full use of the data, and this ambiguity set has become an attractive ambiguity set adopted in DRO. To solve a DRO problem, identifying the most adversarial distribution, the worst-case distribution, from an ambiguity set is essential. We first study the worst-case distribution and calculate its Omega ratio. The worst-case Omega ratio is calculated under mean-variance uncertainty set and mean-Wasserstein uncertainty set, respectively. With aid of the projection result of the two ambiguity sets, we apply the results in the portfolio selection.

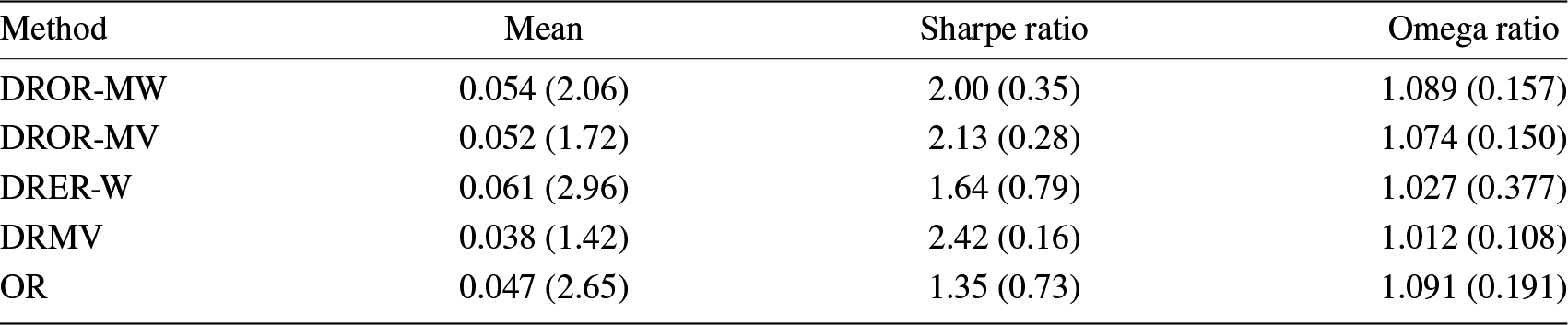

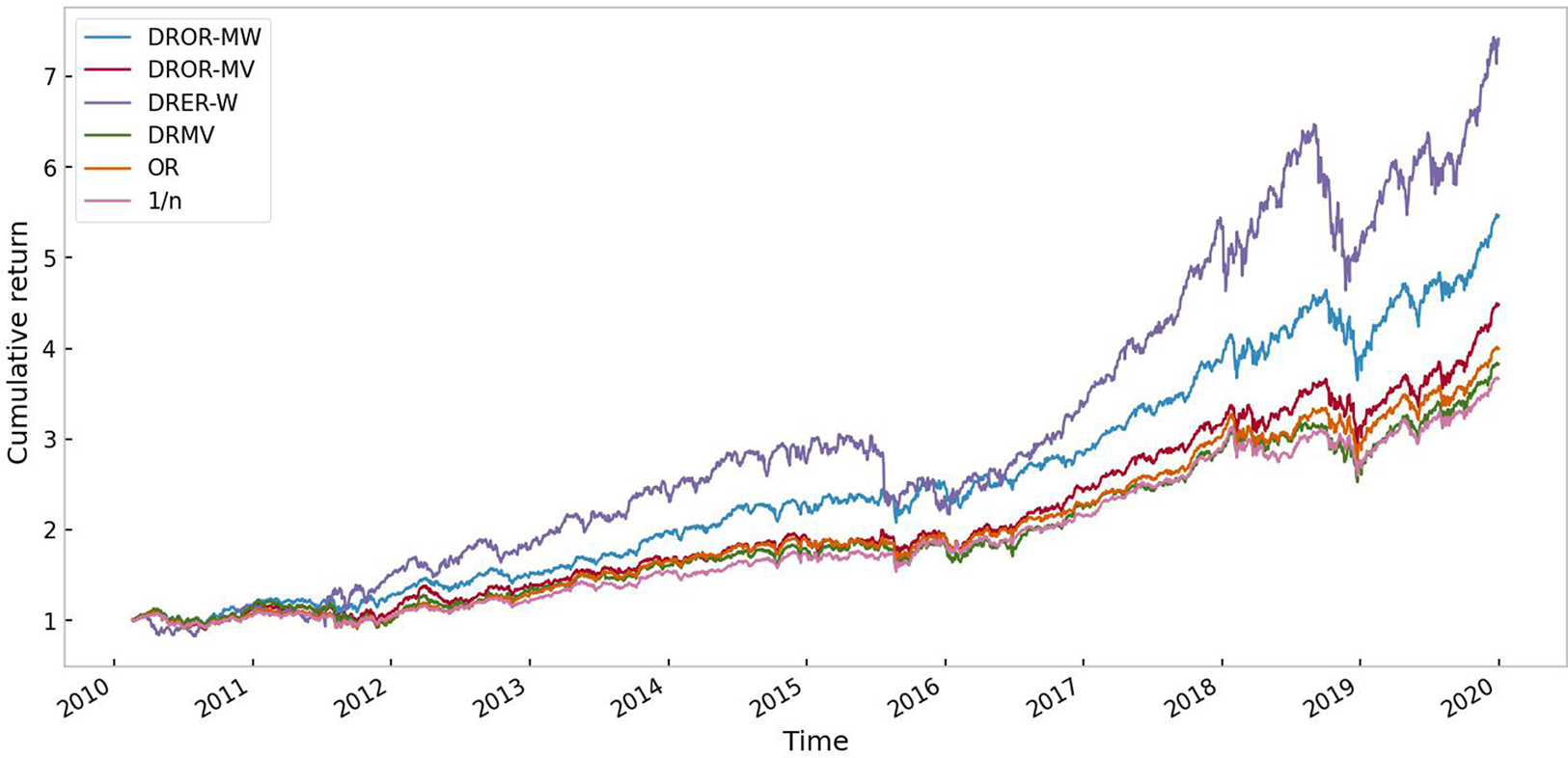

The rest of the paper is organized as follows. Section 2 presents the definition of the Omega ratio, gives explicit expression of the worst-case Omega ratio under mean-variance uncertainty set and aims to tackle the worst-case Omega ratio under mean-Wasserstein uncertainty set. Section 3 applies the worst-case Omega ratio under mean-variance uncertainty set and mean-Wasserstein uncertainty set to the portfolio. In Section 4, we present the simulation and empirical results derived from portfolios comprised of our strategies, comparing them to those of various alternative models.

Throughout the paper, let  $d \in \mathbb{N}$ and

$d \in \mathbb{N}$ and  $\mathbb{R}^d$ be the d-dimensional Euclidean space. Let

$\mathbb{R}^d$ be the d-dimensional Euclidean space. Let  $\mathcal{P}(\mathbb{R}^d)$ be the set of all distributions on

$\mathcal{P}(\mathbb{R}^d)$ be the set of all distributions on  $\mathbb{R}^d$ and denote

$\mathbb{R}^d$ and denote  $\mathcal{P}_p(\mathbb{R}^d)$ by the subset of

$\mathcal{P}_p(\mathbb{R}^d)$ by the subset of  $\mathcal{P}(\mathbb{R}^d)$ with finite pth moment for

$\mathcal{P}(\mathbb{R}^d)$ with finite pth moment for  $p \in [1,\infty)$. For a random variable (vector)

$p \in [1,\infty)$. For a random variable (vector)  $\mathbf X\in \mathcal{P}(\mathbb{R}^d)$, denote

$\mathbf X\in \mathcal{P}(\mathbb{R}^d)$, denote  $\mathbb{E}[{\mathbf X}]$ by the mean (vector) of the random variable (vector)

$\mathbb{E}[{\mathbf X}]$ by the mean (vector) of the random variable (vector)  $\mathbf X$. For a law-invariantFootnote 1 real-valued mapping ρ on

$\mathbf X$. For a law-invariantFootnote 1 real-valued mapping ρ on  $\mathcal{P}(\mathbb{R}^d)$, the notation

$\mathcal{P}(\mathbb{R}^d)$, the notation  $\rho^{F}({\mathbf X})$ means the value of

$\rho^{F}({\mathbf X})$ means the value of  $\rho({\mathbf X})$, where

$\rho({\mathbf X})$, where  ${\mathbf X}$ has the distribution F, and we omit F for simplicity. Furthermore, we denote by

${\mathbf X}$ has the distribution F, and we omit F for simplicity. Furthermore, we denote by  $x_+=\max(0,x)$ and

$x_+=\max(0,x)$ and  $x_-=\max(0,-x)$.

$x_-=\max(0,-x)$.

2. Worst-case Omega ratio

In this section, we only discuss the case of d = 1. The case of d > 1 is discussed in Section 3, where the corresponding portfolio selection problem is investigated. One popular measure of investment performance in finance is Omega ratio introduced by Shadwick and Keating [Reference Shadwick and Keating18]: the ratio of the upside of an investment to the downside.

Definition 2.1. (Shadwick and Keating [Reference Shadwick and Keating18])

For a payoff X with distribution F and a sure payoff c, Omega ratio is defined as

\begin{equation*}

\Omega_{X}(c):=\frac{\mathbb{E}\left[(X-c)_{+}\right]}{\mathbb{E}\left[(c-X)_{+}\right]}.

\end{equation*}

\begin{equation*}

\Omega_{X}(c):=\frac{\mathbb{E}\left[(X-c)_{+}\right]}{\mathbb{E}\left[(c-X)_{+}\right]}.

\end{equation*}2.1. Mean-variance uncertainty set

We assume that the distribution of X lies in a distribution set where first and second moments are fixed. Based on this assumption, we consider the following DRO problem for Omega ratio:

\begin{equation}

\underline{\Omega}_{X}(c,\mu,\sigma) = \inf_{F\in \mathcal{S}_{1}} \Omega_{X}^{F}(c),

\qquad

\overline{\Omega}_{X}(c,\mu,\sigma) = \sup_{F \in \mathcal S_{1}} \Omega_{X}^{F}(c),

\end{equation}

\begin{equation}

\underline{\Omega}_{X}(c,\mu,\sigma) = \inf_{F\in \mathcal{S}_{1}} \Omega_{X}^{F}(c),

\qquad

\overline{\Omega}_{X}(c,\mu,\sigma) = \sup_{F \in \mathcal S_{1}} \Omega_{X}^{F}(c),

\end{equation}where

\begin{align}

\mathcal S_{1}:={\cal S}(\mu,\sigma) =\left\{F\in\mathcal{P}_2(\mathbb{R}): \int_{-\infty}^\infty x\, \mathrm{d}F(x)=\mu, \int_{-\infty}^\infty x^2\, \mathrm{d}F(x)=\mu^2+\sigma^2 \right\},

\end{align}

\begin{align}

\mathcal S_{1}:={\cal S}(\mu,\sigma) =\left\{F\in\mathcal{P}_2(\mathbb{R}): \int_{-\infty}^\infty x\, \mathrm{d}F(x)=\mu, \int_{-\infty}^\infty x^2\, \mathrm{d}F(x)=\mu^2+\sigma^2 \right\},

\end{align}and  $ \Omega_{X}^{F}(c)$ represents the Omega ratio that is calculated under the constraint that the distribution of X is F. The following theorem gives the explicit solutions of the optimization problem (1).

$ \Omega_{X}^{F}(c)$ represents the Omega ratio that is calculated under the constraint that the distribution of X is F. The following theorem gives the explicit solutions of the optimization problem (1).

Theorem 2.2. Given  $\mu\in\mathbb{R}$ and σ > 0, we have

$\mu\in\mathbb{R}$ and σ > 0, we have

\begin{align}

\underline{\Omega}_{X}(c,\mu,\sigma)=

\begin{cases}

0, & \mu \lt c, \\

\frac{\sqrt{1+S^2}+S}{\sqrt{1+S^2}-S}, & \mu \geqslant c ,

\end{cases}

\end{align}

\begin{align}

\underline{\Omega}_{X}(c,\mu,\sigma)=

\begin{cases}

0, & \mu \lt c, \\

\frac{\sqrt{1+S^2}+S}{\sqrt{1+S^2}-S}, & \mu \geqslant c ,

\end{cases}

\end{align}and

\begin{align}

\overline{\Omega}_{X}(c,\mu,\sigma)=

\begin{cases}

\frac{\sqrt{1+S^2}+S}{\sqrt{1+S^2}-S}, & \mu \lt c, \\

\infty, & \mu \geqslant c,

\end{cases}

\end{align}

\begin{align}

\overline{\Omega}_{X}(c,\mu,\sigma)=

\begin{cases}

\frac{\sqrt{1+S^2}+S}{\sqrt{1+S^2}-S}, & \mu \lt c, \\

\infty, & \mu \geqslant c,

\end{cases}

\end{align}where  $S= \frac{\mu - c}{\sigma}$.

$S= \frac{\mu - c}{\sigma}$.

We first present a lemma from [Reference Jagannathan10], which is subsequently used in the proof of Theorem 2.2.

Lemma 2.3. Given  $\mu\in\mathbb{R}$ and σ > 0, we have

$\mu\in\mathbb{R}$ and σ > 0, we have

\begin{equation*}

\max_{F \in \mathcal{S}_{1}} \mathbb{E}^F[(X-c)_+]=\frac{1}{2}\left[\sqrt{\sigma^2+(\mu-c)^2}+\mu-c\right],

\end{equation*}

\begin{equation*}

\max_{F \in \mathcal{S}_{1}} \mathbb{E}^F[(X-c)_+]=\frac{1}{2}\left[\sqrt{\sigma^2+(\mu-c)^2}+\mu-c\right],

\end{equation*}where  $\mathcal S_1$ is defined by Eq. (2).

$\mathcal S_1$ is defined by Eq. (2).

Proof of Theorem 2.2

Since  $\mathbb{E}^F[X-c]=\mathbb{E}^F[(X-c)_+]-\mathbb{E}^F[(X-c)_{-}]=\mathbb{E}^F[(X-c)_+]-\mathbb{E}^F[(c-X)_{+}]$, the Omega function can be rewritten as

$\mathbb{E}^F[X-c]=\mathbb{E}^F[(X-c)_+]-\mathbb{E}^F[(X-c)_{-}]=\mathbb{E}^F[(X-c)_+]-\mathbb{E}^F[(c-X)_{+}]$, the Omega function can be rewritten as

\begin{align}

\Omega_{X}^F(c)=\frac{\mathbb{E}^F[(X-c)_+]}{\mathbb{E}^F[(c-X)_+]} =\frac{\mathbb{E}^F[(X-c)_+]}{\mathbb{E}^F[(X-c)_+]-\mathbb{E}^F[(X-c)]}

=\left\{{1-\frac{\mathbb{E}^F[X]-c}{\mathbb{E}^F[(X-c)_+]}} \right\}^{-1}.

\end{align}

\begin{align}

\Omega_{X}^F(c)=\frac{\mathbb{E}^F[(X-c)_+]}{\mathbb{E}^F[(c-X)_+]} =\frac{\mathbb{E}^F[(X-c)_+]}{\mathbb{E}^F[(X-c)_+]-\mathbb{E}^F[(X-c)]}

=\left\{{1-\frac{\mathbb{E}^F[X]-c}{\mathbb{E}^F[(X-c)_+]}} \right\}^{-1}.

\end{align} We first consider the case of  $\underline{\Omega}_{X}(c,\mu,\sigma)$. If

$\underline{\Omega}_{X}(c,\mu,\sigma)$. If  $\mu \geqslant c$, then we have

$\mu \geqslant c$, then we have

\begin{align*}

\underline{\Omega}_{X}(c,\mu,\sigma)&=\inf_{F\in \mathcal{S}_{1}} \Omega_{X}^{F}(c)

=\inf_{F\in \mathcal{S}_{1}}\left\{1-\frac{\mathbb{E}^F[X]-c}{\mathbb{E}^F[(X-c)_+]}\right\}^{-1}\\

&=\left\{1-\frac{\mu-c}{\max_{F\in\mathcal{S}_{1}}\{\mathbb{E}^F[(X-c)_+]\}}\right\}^{-1}\\

&=\left\{1-\frac{\mu-c}

{\frac12 [\sqrt{\sigma^2+(\mu-c)^2}+\mu-c]}\right\}^{-1}\\

&=\frac{\sqrt{1+S^2}+S}{\sqrt{1+S^2}-S},

\end{align*}

\begin{align*}

\underline{\Omega}_{X}(c,\mu,\sigma)&=\inf_{F\in \mathcal{S}_{1}} \Omega_{X}^{F}(c)

=\inf_{F\in \mathcal{S}_{1}}\left\{1-\frac{\mathbb{E}^F[X]-c}{\mathbb{E}^F[(X-c)_+]}\right\}^{-1}\\

&=\left\{1-\frac{\mu-c}{\max_{F\in\mathcal{S}_{1}}\{\mathbb{E}^F[(X-c)_+]\}}\right\}^{-1}\\

&=\left\{1-\frac{\mu-c}

{\frac12 [\sqrt{\sigma^2+(\mu-c)^2}+\mu-c]}\right\}^{-1}\\

&=\frac{\sqrt{1+S^2}+S}{\sqrt{1+S^2}-S},

\end{align*}where the second and fourth equalities follow from Eq. (5) and Lemma 2.3, respectively. If  $\mu \lt c$, define a discrete random variable as follows:

$\mu \lt c$, define a discrete random variable as follows:

\begin{equation}

X_\alpha=\left\{

\begin{aligned}

\mu-\sigma\sqrt{\frac{1-\alpha}{\alpha}},\quad & \textrm{with probability}\ \alpha, \\

\mu+\sigma\sqrt{\frac{\alpha}{1-\alpha}}, \quad & \textrm{with probability}\ 1-\alpha.

\end{aligned}

\right.

\end{equation}

\begin{equation}

X_\alpha=\left\{

\begin{aligned}

\mu-\sigma\sqrt{\frac{1-\alpha}{\alpha}},\quad & \textrm{with probability}\ \alpha, \\

\mu+\sigma\sqrt{\frac{\alpha}{1-\alpha}}, \quad & \textrm{with probability}\ 1-\alpha.

\end{aligned}

\right.

\end{equation} Let  $\alpha \lt \frac{(\mu-c)^2}{\sigma^2+(\mu-c)^2}$. One can check that

$\alpha \lt \frac{(\mu-c)^2}{\sigma^2+(\mu-c)^2}$. One can check that  $\mathbb{E}[X_\alpha]=\mu$,

$\mathbb{E}[X_\alpha]=\mu$,  $\mathrm{Var}(X_\alpha)=\sigma^2$, which implies that

$\mathrm{Var}(X_\alpha)=\sigma^2$, which implies that  $F_{X_\alpha}\in\mathcal S_1$. Also noting that

$F_{X_\alpha}\in\mathcal S_1$. Also noting that  $X_\alpha \lt c$ almost surely, we have

$X_\alpha \lt c$ almost surely, we have

\begin{equation*}

0\leqslant \underline{\Omega}_{X}(c,\mu,\sigma)\leqslant \Omega_{X_\alpha}(c)=0.

\end{equation*}

\begin{equation*}

0\leqslant \underline{\Omega}_{X}(c,\mu,\sigma)\leqslant \Omega_{X_\alpha}(c)=0.

\end{equation*} Hence, we conclude that  $\underline{\Omega}_{X}(c,\mu,\sigma)=0$ for

$\underline{\Omega}_{X}(c,\mu,\sigma)=0$ for  $\mu \lt c$. This completes the proof of Eq. (3).

$\mu \lt c$. This completes the proof of Eq. (3).

Next, we consider the case of  $\overline{\Omega}_{X}(c,\mu,\sigma)$. If

$\overline{\Omega}_{X}(c,\mu,\sigma)$. If  $\mu\leqslant c$, then we have

$\mu\leqslant c$, then we have

\begin{align*}

\overline{\Omega}_{X}(c,\mu,\sigma)&=\sup_{F\in \mathcal{S}_{1}} \Omega_{X}^{F}(c)

=\sup_{F\in \mathcal{S}_{1}}\left\{1-\frac{\mathbb{E}^F[X]-c}{\mathbb{E}^F[(X-c)_+]}\right\}^{-1}\\

&=\left\{1+\frac{c-\mu}{\max_{F\in\mathcal{S}_{1}}\{\mathbb{E}^F[(X-c)_+]\}}\right\}^{-1}\\

&=\left\{1+\frac{c-\mu}

{\frac12 [\sqrt{\sigma^2+(\mu-c)^2}+\mu-c]}\right\}^{-1}\\

&=\frac{\sqrt{1+S^2}+S}{\sqrt{1+S^2}-S},

\end{align*}

\begin{align*}

\overline{\Omega}_{X}(c,\mu,\sigma)&=\sup_{F\in \mathcal{S}_{1}} \Omega_{X}^{F}(c)

=\sup_{F\in \mathcal{S}_{1}}\left\{1-\frac{\mathbb{E}^F[X]-c}{\mathbb{E}^F[(X-c)_+]}\right\}^{-1}\\

&=\left\{1+\frac{c-\mu}{\max_{F\in\mathcal{S}_{1}}\{\mathbb{E}^F[(X-c)_+]\}}\right\}^{-1}\\

&=\left\{1+\frac{c-\mu}

{\frac12 [\sqrt{\sigma^2+(\mu-c)^2}+\mu-c]}\right\}^{-1}\\

&=\frac{\sqrt{1+S^2}+S}{\sqrt{1+S^2}-S},

\end{align*}where the second and fourth equalities follow from Eq. (5) and Lemma 2.3, respectively. If  $\mu \gt c$, recall the definition of Xα in Eq. (6). Let

$\mu \gt c$, recall the definition of Xα in Eq. (6). Let  $\alpha \gt \frac{(\mu-c)^2}{\sigma^2+(\mu-c)^2}$. One can check that

$\alpha \gt \frac{(\mu-c)^2}{\sigma^2+(\mu-c)^2}$. One can check that  $\mathbb{E}[X_\alpha]=\mu$,

$\mathbb{E}[X_\alpha]=\mu$,  ${\mathrm{Var}}(X_\alpha)=\sigma^2$, which implies that

${\mathrm{Var}}(X_\alpha)=\sigma^2$, which implies that  $F_{X_\alpha}\in\mathcal S_1$. Also noting that

$F_{X_\alpha}\in\mathcal S_1$. Also noting that  $X_\alpha \gt c$ almost surely, we have

$X_\alpha \gt c$ almost surely, we have

\begin{equation*}

\overline{\Omega}_{X}(c,\mu,\sigma)\geqslant \Omega_{X_\alpha}(c)=+\infty.

\end{equation*}

\begin{equation*}

\overline{\Omega}_{X}(c,\mu,\sigma)\geqslant \Omega_{X_\alpha}(c)=+\infty.

\end{equation*} Hence, we have  $\underline{\Omega}_{X}(c,\mu,\sigma)=0$ for

$\underline{\Omega}_{X}(c,\mu,\sigma)=0$ for  $\mu \gt c$. This completes the proof of (4).

$\mu \gt c$. This completes the proof of (4).

Remark 1. The slope of a straight line tangent to the efficient frontier, consisting of both risky and risk-free assets, is called the Sharpe ratio [Reference Sharpe19]. That is, for a random variable X with mean µ and standard deviation σ, Sharpe ratio is defined as  $ S_{X} = \frac{\mathbb{E}[X] - r_0}{\sqrt{\mathrm{Var}(X)}}$, where

$ S_{X} = \frac{\mathbb{E}[X] - r_0}{\sqrt{\mathrm{Var}(X)}}$, where  $\mathrm{Var}$ represents the variance and r 0 is a reference return rate, typically taken as the risk-free return rate. Theorem 2.2 implies that the upper and lower bounds of the Omega ratio can be obtained from a given Sharpe ratio, which is included by the uncertainty set (2). Observing the forms of Eqs. (3) and (4), we find that the robust value increases with the given Sharpe ratio.

$\mathrm{Var}$ represents the variance and r 0 is a reference return rate, typically taken as the risk-free return rate. Theorem 2.2 implies that the upper and lower bounds of the Omega ratio can be obtained from a given Sharpe ratio, which is included by the uncertainty set (2). Observing the forms of Eqs. (3) and (4), we find that the robust value increases with the given Sharpe ratio.

2.2. Mean-Wasserstein uncertainty set

In this section, we present the worst-case Omega ratio based on Wasserstein uncertainty set. We first give the definition of Wasserstein Distance from [Reference Villani20].

Definition 2.5. (Wasserstein Distance)

The p-Wasserstein distance  $W_{p}(G_1,G_2)$ between

$W_{p}(G_1,G_2)$ between  $G_1,G_2 \in \mathcal{P}_p(\mathbb{R}^d)$ is defined by

$G_1,G_2 \in \mathcal{P}_p(\mathbb{R}^d)$ is defined by

\begin{align*}

W_{p}(G_1,G_2) &:=\\

&\inf_{\pi \in \mathcal{P}_p(\mathbb{R}^d \times \mathbb{R}^d)} \left\{\left( \int_{\mathbb{R}^d \times \mathbb{R}^d} \left\lVert x-y \right\rVert ^p \pi({\rm d}x,{\rm d}y) \right)^{\frac{1}{p}} \Big|{\pi \in \mathcal{P}_p(\mathbb{R}^d \times \mathbb{R}^d) \ \ s.t.\ \ \atop \pi( \cdot \times \mathbb{R}^d)=G_1,\ \pi(\mathbb{R}^d \times \cdot)=G_2} \right\},

\end{align*}

\begin{align*}

W_{p}(G_1,G_2) &:=\\

&\inf_{\pi \in \mathcal{P}_p(\mathbb{R}^d \times \mathbb{R}^d)} \left\{\left( \int_{\mathbb{R}^d \times \mathbb{R}^d} \left\lVert x-y \right\rVert ^p \pi({\rm d}x,{\rm d}y) \right)^{\frac{1}{p}} \Big|{\pi \in \mathcal{P}_p(\mathbb{R}^d \times \mathbb{R}^d) \ \ s.t.\ \ \atop \pi( \cdot \times \mathbb{R}^d)=G_1,\ \pi(\mathbb{R}^d \times \cdot)=G_2} \right\},

\end{align*}where  $\left\lVert \cdot\right\rVert $ is a norm on

$\left\lVert \cdot\right\rVert $ is a norm on  $\mathbb{R}^d$, whose dual norm is defined as

$\mathbb{R}^d$, whose dual norm is defined as  $\|y\|_*:=\sup_{\left\lVert x\right\rVert \leqslant 1}x^\top y$ for

$\|y\|_*:=\sup_{\left\lVert x\right\rVert \leqslant 1}x^\top y$ for  $ y \in \mathbb{R}^d$.

$ y \in \mathbb{R}^d$.

The Wasserstein distance is a natural way to compare two distributions when one is obtained from the other by perturbation. For a fixed  $F \in \mathcal{P}_p(\mathbb{R}^d)$ and ɛ > 0, the Wasserstein ball centered on F is defined as follows:

$F \in \mathcal{P}_p(\mathbb{R}^d)$ and ɛ > 0, the Wasserstein ball centered on F is defined as follows:

\begin{align*}

\mathscr B^p_{\varepsilon}(F) :=\left\{G \in {\cal P}_p(\mathbb{R}^d) \big| W_{p}(G,F) \leqslant \varepsilon\right\}.

\end{align*}

\begin{align*}

\mathscr B^p_{\varepsilon}(F) :=\left\{G \in {\cal P}_p(\mathbb{R}^d) \big| W_{p}(G,F) \leqslant \varepsilon\right\}.

\end{align*} For d = 1, we are interested in the worst-case Omega ratio in scenarios where the expected return is greater than the risk-free return, that is,  $\mathbb{E}[X] \geqslant c$, where c is the risk-free return. Hence, we consider the worst-case Omega ratio under the mean and p-Wasserstein uncertainty set:

$\mathbb{E}[X] \geqslant c$, where c is the risk-free return. Hence, we consider the worst-case Omega ratio under the mean and p-Wasserstein uncertainty set:

\begin{equation}

\underline{\Omega}_{X}^F(c,\mu,\varepsilon)=\inf_{G \in {\mathcal S}_{2}} \Omega_{X}^G(c), \quad

\end{equation}

\begin{equation}

\underline{\Omega}_{X}^F(c,\mu,\varepsilon)=\inf_{G \in {\mathcal S}_{2}} \Omega_{X}^G(c), \quad

\end{equation}where  $F \in \mathcal{P}_p(\mathbb{R})$,

$F \in \mathcal{P}_p(\mathbb{R})$,

\begin{equation*}

{\mathcal S}_{2}:={{\cal S}_{p,\varepsilon}(\mu,F)}=\left\{G \in \mathscr B^p_{\varepsilon}(F) \big| \int x \,{\rm d}G(x)=\mu \right\}

\end{equation*}

\begin{equation*}

{\mathcal S}_{2}:={{\cal S}_{p,\varepsilon}(\mu,F)}=\left\{G \in \mathscr B^p_{\varepsilon}(F) \big| \int x \,{\rm d}G(x)=\mu \right\}

\end{equation*}and  $\Omega_{X}^G(c) $ represents the Omega ratio that is calculated under the constraint that the distribution of X is G.

$\Omega_{X}^G(c) $ represents the Omega ratio that is calculated under the constraint that the distribution of X is G.

We turn to the main result of this section, which indicates that the explicit solution of problem (7) is obtained for p = 1, and we simplify problem (7) for p > 1.

Theorem 2.6. Given c, µ, ɛ > 0,  $p \in [1,\infty)$ and

$p \in [1,\infty)$ and  $F \in \mathcal{P}_p(\mathbb{R})$, assume

$F \in \mathcal{P}_p(\mathbb{R})$, assume  $\mu \geqslant c$. Let

$\mu \geqslant c$. Let  $\underline{\Omega}_{X}^F(c,\mu,\varepsilon)$ be the optimal value of problem (7) for a given distribution F, µF denote the random variable’s mean under the distribution F. We have the following results.

$\underline{\Omega}_{X}^F(c,\mu,\varepsilon)$ be the optimal value of problem (7) for a given distribution F, µF denote the random variable’s mean under the distribution F. We have the following results.

(i) For p = 1,

$\mu_F^{c_+}:=\mathbb{E}^F[(X-c)_+]$, then

where\begin{equation*}

\underline{\Omega}_{X}^F(c,\mu,\varepsilon)=\left\{

\begin{aligned}

&1, & \textrm{if}\ \mu \in \mathcal{A}_1\cup \mathcal{B}_1, \\

&\left[1-\frac{2(\mu-c)}{\mu-\mu_F+\varepsilon}\right]^{-1}, & \textrm{if}\ \mu \in \mathcal{A}_2\cup \mathcal{B}_2,

\end{aligned}

\right.

\end{equation*}$\mathcal{A}_1=\{\mu:\mu \gt \mu_F-\mu_F^{c_+}, \mu \gt \mu_F-2\mu_F^{c_+}+\varepsilon\},$ $\mathcal{A}_2=\{\mu:\mu \gt \mu_F-\mu_F^{c_+}, \mu \leqslant \mu_F-2\mu_F^{c_+}+\varepsilon\}$, $\mathcal{B}_1=\{\mu:\mu \leqslant \mu_F-\mu_F^{c_+}, \mu \lt \mu_F-\varepsilon\}$ and $\mathcal{B}_2=\{\mu:\mu \leqslant \mu_F-\mu_F^{c_+}, \mu \geqslant \mu_F-\varepsilon\}$.

$\mu_F^{c_+}:=\mathbb{E}^F[(X-c)_+]$, then

where\begin{equation*}

\underline{\Omega}_{X}^F(c,\mu,\varepsilon)=\left\{

\begin{aligned}

&1, & \textrm{if}\ \mu \in \mathcal{A}_1\cup \mathcal{B}_1, \\

&\left[1-\frac{2(\mu-c)}{\mu-\mu_F+\varepsilon}\right]^{-1}, & \textrm{if}\ \mu \in \mathcal{A}_2\cup \mathcal{B}_2,

\end{aligned}

\right.

\end{equation*}$\mathcal{A}_1=\{\mu:\mu \gt \mu_F-\mu_F^{c_+}, \mu \gt \mu_F-2\mu_F^{c_+}+\varepsilon\},$ $\mathcal{A}_2=\{\mu:\mu \gt \mu_F-\mu_F^{c_+}, \mu \leqslant \mu_F-2\mu_F^{c_+}+\varepsilon\}$, $\mathcal{B}_1=\{\mu:\mu \leqslant \mu_F-\mu_F^{c_+}, \mu \lt \mu_F-\varepsilon\}$ and $\mathcal{B}_2=\{\mu:\mu \leqslant \mu_F-\mu_F^{c_+}, \mu \geqslant \mu_F-\varepsilon\}$.(i) Otherwise, for p > 1, we have

where\begin{equation*}

\underline{\Omega}_{X}^F(c,\mu,\varepsilon)=\left( 1- \frac{\mu-c}{T(\mu)}\right)^{-1},

\end{equation*}and\begin{equation*}

\begin{aligned}

T(\mu) := \inf_{\lambda \geqslant 0 , \gamma \in \mathbb{R}} \left\{\lambda \varepsilon^p +\gamma (\mu - \mu_F) + |\gamma| \left(1- \frac{1}{p}\right) \left( \frac{|\gamma |}{\lambda p}\right)^{\frac{1}{p-1}} + \mathbb{E}^F [ (X-c_1(\lambda,\gamma))_+]\right\} \\

\end{aligned}

\end{equation*}\begin{equation*}

\begin{aligned}

c_1(\lambda,\gamma) := c+\left(1-\frac{1}{p}\right) \left[ \left( \frac{|\gamma |}{\lambda p}\right)^{\frac{1}{p-1}} |\gamma| - \left( \frac{|1-\gamma |}{\lambda p}\right)^{\frac{1}{p-1}}|1-\gamma| \right]. \\

\end{aligned}

\end{equation*}

To simplify problem (7), we need to utilize the following lemma, the proof of which is directly derived from Theorem 1 of [Reference Gao and Kleywegt8].

Lemma 2.7. For  $p \in [1,\infty)$,

$p \in [1,\infty)$,  $ F \in \mathcal{P}_p(\mathbb{R}),$

$ F \in \mathcal{P}_p(\mathbb{R}),$  $\mu \in \mathbb{R}$, ɛ > 0 and

$\mu \in \mathbb{R}$, ɛ > 0 and  $\Psi:\mathbb{R}\to\mathbb{R}$, we have

$\Psi:\mathbb{R}\to\mathbb{R}$, we have

\begin{equation*}

\begin{aligned}

\sup_{G \in {\mathcal S}_{2}} \int_{\mathbb{R}} \Psi(\xi)\,{\rm d}G( \xi) =\inf_{\lambda \geqslant 0, \gamma \in \mathbb{R}} \left\{\lambda \varepsilon^p +\int_{\mathbb{R}} \sup_{\xi \in \mathbb{R}} [\Psi(\xi)-\gamma \xi-\lambda | \xi-\zeta | ^p ]\, {\rm d}F( \zeta) +\gamma \mu \right\}.

\end{aligned}

\end{equation*}

\begin{equation*}

\begin{aligned}

\sup_{G \in {\mathcal S}_{2}} \int_{\mathbb{R}} \Psi(\xi)\,{\rm d}G( \xi) =\inf_{\lambda \geqslant 0, \gamma \in \mathbb{R}} \left\{\lambda \varepsilon^p +\int_{\mathbb{R}} \sup_{\xi \in \mathbb{R}} [\Psi(\xi)-\gamma \xi-\lambda | \xi-\zeta | ^p ]\, {\rm d}F( \zeta) +\gamma \mu \right\}.

\end{aligned}

\end{equation*}Proof of Theorem 2.6

We know that if  $\mathbb{E}^G[X]=\mu$, Omega ratio can be expressed as

$\mathbb{E}^G[X]=\mu$, Omega ratio can be expressed as

\begin{equation*}

\Omega_{X}^G(c)=\frac{\mathbb{E}^G [(X-c)_+]}{\mathbb{E} ^G[(c-X)_+]}=\left\{{1- \frac{\mu-c}{\mathbb{E}^G [( X-c)_+]}}\right\}^{-1}.

\end{equation*}

\begin{equation*}

\Omega_{X}^G(c)=\frac{\mathbb{E}^G [(X-c)_+]}{\mathbb{E} ^G[(c-X)_+]}=\left\{{1- \frac{\mu-c}{\mathbb{E}^G [( X-c)_+]}}\right\}^{-1}.

\end{equation*} Denote  $T(\mu)= \sup_{G \in {\mathcal S}_{2}} \mathbb{E}^G [(X-c)_+]$, for

$T(\mu)= \sup_{G \in {\mathcal S}_{2}} \mathbb{E}^G [(X-c)_+]$, for  $\mu \geqslant c$, we can obtain that

$\mu \geqslant c$, we can obtain that

\begin{equation*}

\inf_{G \in {\mathcal S}_{2}} \frac{\mu-c}{\mathbb{E}^G [(X-c)_+]} =\frac{\mu-c}{T(\mu)}.

\end{equation*}

\begin{equation*}

\inf_{G \in {\mathcal S}_{2}} \frac{\mu-c}{\mathbb{E}^G [(X-c)_+]} =\frac{\mu-c}{T(\mu)}.

\end{equation*}Hence, problem (7) can be reduced as follow:

\begin{align*}

\underline{\Omega}_{X}(\mu,c,\varepsilon)&=\inf_{G \in {\mathcal S}_{2}} \Omega_{X}^G(c) = \inf_{G \in {\mathcal S}_{2}} \left\{{1- \frac{\mu-c}{\mathbb{E}^G [(X-c)_+]}}\right\}^{-1}\\

&=\left\{1-\inf_{G \in {\mathcal S}_{2}} {\frac{\mu-c}{\mathbb{E}^G [(X-c)_+]}}\right\}^{-1}\\

&=\left\{1-\frac{\mu-c}{T(\mu)}\right\}^{-1}\\

&=\frac{T(\mu)}{T(\mu)-(\mu-c)}.

\end{align*}

\begin{align*}

\underline{\Omega}_{X}(\mu,c,\varepsilon)&=\inf_{G \in {\mathcal S}_{2}} \Omega_{X}^G(c) = \inf_{G \in {\mathcal S}_{2}} \left\{{1- \frac{\mu-c}{\mathbb{E}^G [(X-c)_+]}}\right\}^{-1}\\

&=\left\{1-\inf_{G \in {\mathcal S}_{2}} {\frac{\mu-c}{\mathbb{E}^G [(X-c)_+]}}\right\}^{-1}\\

&=\left\{1-\frac{\mu-c}{T(\mu)}\right\}^{-1}\\

&=\frac{T(\mu)}{T(\mu)-(\mu-c)}.

\end{align*}Applying Lemma 2.7, denote by

\begin{equation*}

H_{\lambda,\gamma}(y)= \sup_{x \in \mathbb{R}} \{(x-c)_+ - \gamma x -\lambda |x-y|^p \},

\end{equation*}

\begin{equation*}

H_{\lambda,\gamma}(y)= \sup_{x \in \mathbb{R}} \{(x-c)_+ - \gamma x -\lambda |x-y|^p \},

\end{equation*}  $T(\mu)$ can be reformulated as

$T(\mu)$ can be reformulated as

\begin{equation}

T(\mu)=\sup_{G \in {\mathcal S}_{2}} \mathbb{E}^G[(X-c)_+]=\inf_{\lambda \geqslant 0, \gamma \in \mathbb{R}} \left\{\lambda \varepsilon^p + \mathbb{E}^F \left[ H_{\lambda,\gamma}(Y) \right]+\gamma \mu \right\}.

\end{equation}

\begin{equation}

T(\mu)=\sup_{G \in {\mathcal S}_{2}} \mathbb{E}^G[(X-c)_+]=\inf_{\lambda \geqslant 0, \gamma \in \mathbb{R}} \left\{\lambda \varepsilon^p + \mathbb{E}^F \left[ H_{\lambda,\gamma}(Y) \right]+\gamma \mu \right\}.

\end{equation} To simplify  $T(\mu)$, we calculate the RHS of Eq. (8) in the following steps.

$T(\mu)$, we calculate the RHS of Eq. (8) in the following steps.

1. Calculate

$H_{\lambda,\gamma}(y)$.Let

$h_y(x)=(x-c)_+ - \gamma x -\lambda |x-y|^p$. For $x \in \mathbb{R}\backslash\{c,y\}$, the derivative of $h_y(x)$ with respect to x is

\begin{equation*}

\begin{aligned}

\frac{\partial h_y(x)}{\partial x} &=I(x \gt c)-\gamma - \text{sgn}(x-y) \lambda p |x-y|^{p-1}. \\

\end{aligned}

\end{equation*}To calculate the maximum of

$h_y(x)$, we consider the case of p = 1 and p > 1, respectively.(i) If p = 1, for

$x \in \mathbb{R}\backslash\{c,y\}$, the derivative of $h_y(x)$ with respect to x can be written as

\begin{equation*}

\begin{aligned}

\frac{\partial h_y(x)}{\partial x}

&=

\begin{cases}

1-\gamma - \lambda , & x \gt \max\{c,y\}, \\

I(x \gt c)-\gamma - \text{sgn}(x-y) \lambda, &x \in (\min\{c,y\},\max\{c,y\}), \\

-\gamma +\lambda , & x \lt \min\{c,y\}. \\

\end{cases}

\end{aligned}

\end{equation*}In the case of

$\lambda \geqslant \frac{1}{2}$ and $1-\lambda \leqslant \gamma \leqslant \lambda$, if $\frac{\partial h_y(x)}{\partial x} \geqslant 0 $ for $x \lt \min\{c,y\}$ and $\frac{\partial h_y(x)}{\partial x} \leqslant 0 $ for $x \gt \max\{c,y\}$, then the maximizer to $h_y(x)$ lies in the interval $[\min\{c,y\},\max\{c,y\}]$. If y < c, as $\frac{\partial h_y(x)}{\partial x} \leqslant 0 $ for $x \in (y,c)$, the maximizer to $h_y(x)$ is $x^*=y$ and $h_y(y)=-\gamma y$. If $y \geqslant c$, as $\frac{\partial h_y(x)}{\partial x} \geqslant 0 $ for $x \in (c,y)$, the maximizer to $h_y(x)$ is $x^*=c$ and $h_y(c)=-\lambda y+(\lambda-\gamma)c$. Otherwise, it can be verified that

\begin{equation*}\sup_{x \in \mathbb{R}}h_y(x)=\max\{\lim_{x \to \infty}h_y(x),\lim_{x \to -\infty}h_y(x)\}=\infty.\end{equation*}In summary, in the case of p = 1, if

$\lambda \geqslant \frac{1}{2}$ and $1-\lambda \leqslant \gamma \leqslant \lambda$, the value of $H_{\lambda, \gamma}(y)$ is

otherwise, the value of\begin{equation*}

H_{\lambda, \gamma}(y)=\sup_{x \in \mathbb{R}} h_y(x)=

\begin{cases}

-\gamma y, & y \lt c,\\

-\lambda y+(\lambda-\gamma)c, & y \geqslant c; \\

\end{cases}

\end{equation*}$H_{\lambda, \gamma}(y)$ is $\infty$.(ii) If p > 1, for y < c, we have

\begin{equation*}

\begin{aligned}

\frac{\partial h_y(x)}{\partial x}

&=

\begin{cases}

1-\gamma - \lambda p |x-y|^{p-1}, & x \gt c, \\

-\gamma - \lambda p |x-y|^{p-1}, &x \in (y,c), \\

-\gamma +\lambda p |x-y|^{p-1}, & x \lt y. \\

\end{cases}

\end{aligned}

\end{equation*}Conversely, for

$y \geqslant c$, then

\begin{equation*}

\begin{aligned}

\frac{\partial h_y(x)}{\partial x}

&=

\begin{cases}

1-\gamma - \lambda p |x-y|^{p-1}, & x \gt y, \\

1-\gamma + \lambda p |x-y|^{p-1}, &x \in (c,y), \\

-\gamma +\lambda p |x-y|^{p-1}, & x \lt c. \\

\end{cases}

\end{aligned}

\end{equation*}Therefore, it is necessary to discuss the classification of γ. For

$\gamma \leqslant 0$, we consider the following three cases.(a) For

$y \lt c-\left(\frac{1-\gamma}{\lambda p}\right)^{\frac{1}{p-1}}$, solving $\frac{\partial h_y(x)}{\partial x} \gt 0$ yields $x \lt y+\left(\frac{-\gamma}{\lambda p}\right)^{\frac{1}{p-1}}$ and solving $\frac{\partial h_y(x)}{\partial x}\leqslant 0$ yields $x\geqslant y+\left(\frac{-\gamma}{\lambda p}\right)^{\frac{1}{p-1}}$. As a result, the maximizer to $h_y(x)$ is $x_1^*=y+\left(\frac{-\gamma}{\lambda p}\right)^{\frac{1}{p-1}}$ and

\begin{equation*}

h_y(x_1^*)=-\gamma y - \gamma \left(1- \frac{1}{p}\right) \left( \frac{- \gamma}{\lambda p}\right)^{\frac{1}{p-1}}.

\end{equation*}(b) For

$c-\left(\frac{1-\gamma}{\lambda p}\right)^{\frac{1}{p-1}} \leqslant y \leqslant c-\left(\frac{-\gamma}{\lambda p}\right)^{\frac{1}{p-1}}$, we find that $\frac{\partial h_y(x)}{\partial x} \gt 0$ in the cases that $x \lt y+\left(\frac{-\gamma}{\lambda p}\right)^{\frac{1}{p-1}}$ or $c \lt x \lt y+\left(\frac{1-\gamma}{\lambda p}\right)^{\frac{1}{p-1}}$ and $\frac{\partial h_y(x)}{\partial x}\leqslant 0$ in the cases that $y+\left(\frac{-\gamma}{\lambda p}\right)^{\frac{1}{p-1}}\leqslant x\leqslant c$ or $x \geqslant y+\left(\frac{1-\gamma}{\lambda p}\right)^{\frac{1}{p-1}}$. Hence, the local maximizers to $h_y(x)$ are

\begin{equation*}

x_1^*=y+\left( \frac{-\gamma}{\lambda p} \right)^{\frac{1}{p-1}}\quad \text{and}\quad

x_2^*=y+\left(\frac{1-\gamma}{\lambda p} \right)^{\frac{1}{p-1}} .

\end{equation*}In addition, the local maximum values of

$h_y(x)$ are

and\begin{equation*}

h_y(x_1^*)=-\gamma y - \gamma \left(1- \frac{1}{p}\right) \left( \frac{- \gamma}{\lambda p}\right)^{\frac{1}{p-1}}

\end{equation*}\begin{equation*}

h_y(x_2^*)=y- \gamma y -c + (1- \gamma) \left(1- \frac{1}{p}\right) \left( \frac{1-\gamma}{\lambda p} \right)^{\frac{1}{p-1}}.

\end{equation*}(c) For

$y \lt c-\left(\frac{-\gamma}{\lambda p}\right)^{\frac{1}{p-1}}$, solving $\frac{\partial h_y(x)}{\partial x} \gt 0$ yields $x \lt y+\left(\frac{1-\gamma}{\lambda p}\right)^{\frac{1}{p-1}}$ and solving $\frac{\partial h_y(x)}{\partial x}\leqslant 0$ yields $x\geqslant y+\left(\frac{1-\gamma}{\lambda p}\right)^{\frac{1}{p-1}}$. As a result, the maximizer to $h_y(x)$ is $x_2^*=y+\left(\frac{1-\gamma}{\lambda p}\right)^{\frac{1}{p-1}}$ and

\begin{equation*}

h_y(x_2^*)=y- \gamma y -c + (1- \gamma) \left(1-\frac{1}{p}\right) \left( \frac{1-\gamma}{\lambda p} \right)^{\frac{1}{p-1}}.

\end{equation*}Let

one can easily verify that\begin{equation*}

c_0(\lambda,\gamma)= c+\left(1-\frac{1}{p}\right) \left[ \left( \frac{-\gamma}{\lambda p}\right)^{\frac{1}{p-1}} (-\gamma) - \left( \frac{1-\gamma}{\lambda p}\right)^{\frac{1}{p-1}}(1-\gamma) \right],

\end{equation*}$c-\left(\frac{1-\gamma}{\lambda p}\right)^{\frac{1}{p-1}} \leqslant c_0(\lambda,\gamma) \leqslant c-\left(\frac{-\gamma}{\lambda p}\right)^{\frac{1}{p-1}}$ by mean value theorem. In addition, $y \lt c_0(\lambda,\gamma)$ implies $h_y(x_1) \gt h_y(x_2)$. Due to the above discussion, if $\gamma \leqslant 0$, the maximum value of $h_y(x)$ is as follows:

\begin{equation*}

H_{\lambda, \gamma}(y)=\sup_{x \in \mathbb{R}} h_y(x)=

\begin{cases}

-\gamma y - \gamma \left(1- \frac{1}{p}\right) \left( \frac{-\gamma}{\lambda p}\right)^{\frac{1}{p-1}}, & y \lt c_0(\lambda,\gamma),\\

y- \gamma y -c + (1- \gamma) \left(1-\frac{1}{p}\right) \left( \frac{1-\gamma}{\lambda p} \right)^{\frac{1}{p-1}}, & y \geqslant c_0(\lambda,\gamma). \\

\end{cases}

\end{equation*}Similarly, for

$0 \lt \gamma \lt 1$ and $\gamma \geqslant 1$, we can obtain similar results with only the difference in the sign of the open root formula. Hence, for $\gamma \in \mathbb{R}$ and $\lambda \geqslant 0$, we obtain the value of $H_{\lambda, \gamma}(y)$ as

where\begin{equation*}

H_{\lambda, \gamma}(y)=\sup_{x \in \mathbb{R}} h_y(x)=

\begin{cases}

-\gamma y + | \gamma | \left(1- \frac{1}{p}\right) \left( \frac{| \gamma |}{\lambda p}\right)^{\frac{1}{p-1}}, & y \lt c_1(\lambda,\gamma),\\

y- \gamma y -c + |1- \gamma| \left(1-\frac{1}{p}\right) \left( \frac{|1-\gamma|}{\lambda p} \right)^{\frac{1}{p-1}}, & y \geqslant c_1(\lambda,\gamma), \\

\end{cases}

\end{equation*}\begin{equation*}

c_1(\lambda,\gamma) := c+\left(1-\frac{1}{p}\right) \left[ \left( \frac{|\gamma |}{\lambda p}\right)^{\frac{1}{p-1}} |\gamma| - \left( \frac{|1-\gamma |}{\lambda p}\right)^{\frac{1}{p-1}}|1-\gamma| \right].

\end{equation*}

2. Calculate

$\mathbb{E}^F [ H_{\lambda,\gamma}(Y)]$.Denoted

$f(\lambda,\gamma)=\mathbb{E}^F [ H_{\lambda,\gamma}(Y)]$. For p = 1, if $\lambda \geqslant \frac{1}{2}$ and $1-\lambda \leqslant \gamma \leqslant \lambda$, we have

\begin{equation*}

\begin{aligned}

f(\lambda,\gamma)&=\mathbb{E}^F [ H_{\lambda,\gamma}(Y)]\\

&= \int_{-\infty}^{c}-\gamma y \,{\rm d}F(y)+\int_{c}^{+\infty}-\lambda y+(\lambda-\gamma)c \,{\rm d}F(y)\\

&=-\gamma \mu_F-(\lambda-\gamma)\int_{c}^{+\infty}(y-c)\,{\rm d}F(y) \\

&=-\gamma \mu_F-(\lambda-\gamma)\mu_F^{c_+}.

\end{aligned}

\end{equation*}Otherwise,

$f(\lambda,\gamma)=\infty$ because $H_{\lambda,\gamma}(y)=\infty$ for all $y \in \mathbb{R}$. For p > 1, we find that

\begin{equation*}

\begin{aligned}

f(\lambda,\gamma)&=\mathbb{E}^F [ H_{\lambda,\gamma}(Y)]\\

&=\int_{-\infty}^{c_1(\lambda,\gamma)} -\gamma y + | \gamma | \left(1- \frac{1}{p}\right) \left( \frac{| \gamma |}{\lambda p}\right)^{\frac{1}{p-1}}\, {\rm d}F(y) \\

&\quad+ \int_{c_1(\lambda , \gamma)}^{+\infty} y- \gamma y -c + |1- \gamma| \left(1-\frac{1}{p}\right) \left( \frac{|1-\gamma|}{\lambda p} \right)^{\frac{1}{p-1}}\, {\rm d}F(y) \\

&=-\gamma \mu_F + |\gamma| \left(1- \frac{1}{p}\right) \left( \frac{| \gamma|} {\lambda p}\right)^{\frac{1}{p-1}} +\int_{c_1(\lambda, \gamma)}^{+\infty} y-c_1(\lambda,\gamma)\,{\rm d}F(y) \\

&=-\gamma \mu_F + |\gamma| \left(1- \frac{1}{p}\right) \left( \frac{|\gamma|} {\lambda p}\right)^{\frac{1}{p-1}} + \mathbb{E}^F [ (Y-c_1(\lambda,\gamma))_+].

\end{aligned}

\end{equation*}Ultimately,

\begin{equation*}

\begin{aligned}

T(\mu)&=\sup_{G \in {\mathcal S}_{2}} \mathbb{E}^G[(X-c)_+]\\

&=\begin{cases}

\inf_{\lambda \geqslant \frac{1}{2} , 1-\lambda \leqslant \gamma \leqslant \lambda} \left\{\lambda(\varepsilon - \mu_F^{c_+})+\gamma(\mu-\mu_F+\mu_F^{c_+})\right\},\quad p=1,\\

\begin{aligned}[t]

\inf_{\lambda \geqslant 0 , \gamma \in \mathbb{R}} \Big\{&\lambda \varepsilon^p +\gamma (\mu - \mu_F) \\

& + |\gamma| \left(1- \frac{1}{p}\right) \left( \frac{|\gamma |}{\lambda p}\right)^{\frac{1}{p-1}} + \mathbb{E}^F [ (Y-c_1(\lambda,\gamma))_+]\Big\}, \ p \gt 1. \\

\end{aligned}

\end{cases}

\end{aligned}

\end{equation*}3. Calculate

$\underline{\Omega}_{X}^F(c,\mu,\varepsilon)$ in the case of p = 1.We denote

$g(\lambda,\gamma):=\lambda(\varepsilon - \mu_F^{c_+})+\gamma(\mu-\mu_F+\mu_F^{c_+})$. Fixed λ, the partial derivative of $g(\lambda,\gamma)$ with respect to γ is

\begin{equation*}

\frac{\partial g(\lambda,\gamma)}{\partial \gamma}=\mu-\mu_F+\mu_F^{c_+}.

\end{equation*}Since

$\mu \gt \mu_F-\mu_F^{c_+}$ yields $\frac{\partial g(\lambda,\gamma)}{\partial \gamma} \gt 0$, the minimizer to $g(\lambda,\gamma)$ is $\gamma^*=1-\lambda$ and

\begin{equation*}

g(\lambda,1-\lambda)=\lambda(\varepsilon+\mu_F-\mu-2\mu_F^{c_+})+(\mu-\mu_F+\mu_F^{c_+}).

\end{equation*}One can verify that

\begin{equation*}

\frac{\partial g(\lambda,1-\lambda)}{\partial \lambda}=\varepsilon+\mu_F-\mu-2\mu_F^{c_+}.

\end{equation*}Noting

$\mu \gt \varepsilon+\mu_F-2\mu_F^{c_+}$ yields $\frac{\partial g(\lambda,1-\lambda)}{\partial \lambda} \lt 0$, the minimizer to $g(\lambda,1-\lambda)$ is $\lambda^*=\infty$ and the minimum value of $g(\lambda,1-\lambda)$ is $-\infty$. Conversely, if $\mu \leqslant \varepsilon+\mu_F-2\mu_F^{c_+}$, as $\frac{\partial g(\lambda,1-\lambda)}{\partial \lambda} \geqslant 0$, the minimizer to $g(\lambda,1-\lambda)$ is $\lambda^*=\frac{1}{2}$ and $g\left(\frac{1}{2},\frac{1}{2}\right)=\frac{1}{2}(\mu-\mu_F+\varepsilon)$. On the other hand, if $\mu \leqslant \mu_F-\mu_F^{c_+}$, as $\frac{\partial g(\lambda,\gamma)}{\partial \gamma} \leqslant 0$, the minimizer to $g(\lambda,\gamma)$ is $\gamma^*=\lambda$ and

\begin{equation*}

g(\lambda,\lambda)=\lambda(\mu-\mu_F+\varepsilon).

\end{equation*}In addition, we have

\begin{equation*}

\frac{\partial g(\lambda,\lambda)}{\partial \lambda}=\mu-\mu_F+\varepsilon.

\end{equation*}Then

$\mu \geqslant \mu_F-\varepsilon$ yields $\frac{\partial g(\lambda,\lambda)}{\partial \lambda} \geqslant 0$ and the minimizer to $g(\lambda,\lambda)$ is $\lambda^*=\frac{1}{2}$ and $g\left(\frac{1}{2},\frac{1}{2}\right)=\frac{1}{2}(\mu-\mu_F+\varepsilon)$. If $\mu \lt \mu_F-\varepsilon$, we have $\frac{\partial g(\lambda,\lambda)}{\partial \lambda} \lt 0$, then the minimizer to $g(\lambda,\lambda)$ is $\lambda^*=\infty$ and the minimum value of $g(\lambda,\lambda)$ is $-\infty$. To sum up,

where\begin{equation*}

T(\mu)=\inf_{\lambda \geqslant \frac{1}{2} , 1-\lambda \leqslant \gamma \leqslant \lambda}g(\lambda,\gamma)=\begin{cases}

-\infty, & \textrm{if}\ \mu \in \mathcal{A}_1\cup \mathcal{B}_1,\\

\frac{1}{2}(\mu-\mu_F+\varepsilon), & \textrm{if}\ \mu \in \mathcal{A}_2\cup \mathcal{B}_2, \\

\end{cases}

\end{equation*}$\mathcal{A}_1$, $\mathcal{A}_2$, $\mathcal{B}_1$ and $\mathcal{B}_2$ are defined in Theorem 2.6. As a result,

\begin{equation*}

\underline{\Omega}_{X}^F(c,\mu,\varepsilon)=\left( 1- \frac{\mu-c}{T(\mu)}\right)^{-1}

=\begin{cases}

1, & \textrm{if}\ \mu \in \mathcal{A}_1\cup \mathcal{B}_1,\\

\left[ 1- \frac{2(\mu-c)}{\mu-\mu_F+\varepsilon}\right]^{-1}, & \textrm{if}\ \mu \in \mathcal{A}_2\cup \mathcal{B}_2. \\

\end{cases}

\end{equation*}

In Theorem 2.6, we provide an explicit solution to problem (7) and derive a more concise optimization problem for p > 1. In the next section, we will apply problems (1) and (7) in portfolio selection.

3. Application in portfolio selection

In this section, we explore interesting properties of the distributionally robust portfolio optimization problem under the mean-variance and Wasserstein uncertainty sets. Throughout this section, suppose that  $\mathbb{W} $ is a subset of

$\mathbb{W} $ is a subset of  $\mathbb{R}^d$. Let

$\mathbb{R}^d$. Let  $\mathbf {X}=( X_1,\ldots, X_d)^\top \in \mathcal{P}(\mathbb{R}^d)$ and

$\mathbf {X}=( X_1,\ldots, X_d)^\top \in \mathcal{P}(\mathbb{R}^d)$ and  $\mathbf {w}=(w_1,\ldots,w_d)^\top \in \mathbb{W}$, where Xi represents the return of the ith asset, wi represents the investment weight of the ith asset. The distribution of

$\mathbf {w}=(w_1,\ldots,w_d)^\top \in \mathbb{W}$, where Xi represents the return of the ith asset, wi represents the investment weight of the ith asset. The distribution of  $\mathbf {w}^\top\mathbf {X}$ is denoted by

$\mathbf {w}^\top\mathbf {X}$ is denoted by  $F_{\mathbf {w}}$ when the distribution of

$F_{\mathbf {w}}$ when the distribution of  $\mathbf {X}$ is F.

$\mathbf {X}$ is F.

3.1. Mean-variance uncertainty set

We consider the distributionally robust portfolio optimization problem under mean-variance uncertainty set:

\begin{equation}

\sup_{\mathbf{w}\in \mathbb{W}} \inf_{F \in {\cal S}(\bf{\mu},\Sigma)} \Omega_{\mathbf{w}^\top \mathbf {X}}^{F}(c),

\end{equation}

\begin{equation}

\sup_{\mathbf{w}\in \mathbb{W}} \inf_{F \in {\cal S}(\bf{\mu},\Sigma)} \Omega_{\mathbf{w}^\top \mathbf {X}}^{F}(c),

\end{equation}where

\begin{equation*}

\begin{aligned}

{\cal S}(\bf{\mu},\Sigma)

:=\{F\in \mathcal{P}_2(\mathbb{R}^d): \mathbb{E}^F[\mathbf{X}]=\mathbf{\bf{\mu}},\ \mathrm{Var}^F(\mathbf{X}) = \Sigma \},

\end{aligned}

\end{equation*}

\begin{equation*}

\begin{aligned}

{\cal S}(\bf{\mu},\Sigma)

:=\{F\in \mathcal{P}_2(\mathbb{R}^d): \mathbb{E}^F[\mathbf{X}]=\mathbf{\bf{\mu}},\ \mathrm{Var}^F(\mathbf{X}) = \Sigma \},

\end{aligned}

\end{equation*}and  $ \Omega_{\mathbf{w}^\top \mathbf{X}}^{F}(c)$ represents the Omega ratio of

$ \Omega_{\mathbf{w}^\top \mathbf{X}}^{F}(c)$ represents the Omega ratio of  $\mathbf{w}^\top \mathbf{X}$ that is calculated under the constraint that the distribution of

$\mathbf{w}^\top \mathbf{X}$ that is calculated under the constraint that the distribution of  $\mathbf {X}$ is F.

$\mathbf {X}$ is F.

In the following theorem, we solve the inner problem of (9) and give an equivalent optimization problem with the same optimal solution as problem (9).

Theorem 3.1. Given  $c\in\mathbb{R}$,

$c\in\mathbb{R}$,  $\bf{\mu} \in \mathbb{R}^d$ and Σ, a positive semidefinite matrix of

$\bf{\mu} \in \mathbb{R}^d$ and Σ, a positive semidefinite matrix of  $\mathbb{R}^{d \times d}$, assuming

$\mathbb{R}^{d \times d}$, assuming  $\mathbf {w}^\top \bf{\mu} \geqslant c$ for

$\mathbf {w}^\top \bf{\mu} \geqslant c$ for  $\mathbf {w} \in \mathbb{W}$, problem (9) is equivalent to the following optimization problem:

$\mathbf {w} \in \mathbb{W}$, problem (9) is equivalent to the following optimization problem:

\begin{equation}

\sup_{\mathbf {w} \in \mathbb{W}} \frac{\mathbf {w} ^\top \bf{\mu}-c}{\sqrt{\mathbf {w}^\top \Sigma \mathbf {w}}},

\end{equation}

\begin{equation}

\sup_{\mathbf {w} \in \mathbb{W}} \frac{\mathbf {w} ^\top \bf{\mu}-c}{\sqrt{\mathbf {w}^\top \Sigma \mathbf {w}}},

\end{equation}in the sense that two problems have the same optimal solution.

To prove Theorem  $3.1$, we need the following lemma from [Reference Chen, He and Zhang5].

$3.1$, we need the following lemma from [Reference Chen, He and Zhang5].

Lemma 3.2. For  $ \mathbf{w} \in \mathbb{R}^d$, it holds that

$ \mathbf{w} \in \mathbb{R}^d$, it holds that

\begin{equation*}

{\cal S}(\mathbf{w},\bf{\mu},\Sigma) ={\cal S}_{\mathbf {w}}(\bf{\mu},\Sigma),

\end{equation*}

\begin{equation*}

{\cal S}(\mathbf{w},\bf{\mu},\Sigma) ={\cal S}_{\mathbf {w}}(\bf{\mu},\Sigma),

\end{equation*}where

\begin{align*}

{\cal S}(\mathbf{w},\bf{\mu},\Sigma)=\{&F_{\mathbf {w}} \in \mathcal{P}_2(\mathbb{R}):F \in {\cal S}(\bf{\mu},\Sigma)\\

& F_{\mathbf {w}}\ \textrm{is the distribution of}\ \mathbf {w}^\top\mathbf {X}\ \textrm{when the distribution of}\ \mathbf {X}\ \textrm{is}\ F \}

\end{align*}

\begin{align*}

{\cal S}(\mathbf{w},\bf{\mu},\Sigma)=\{&F_{\mathbf {w}} \in \mathcal{P}_2(\mathbb{R}):F \in {\cal S}(\bf{\mu},\Sigma)\\

& F_{\mathbf {w}}\ \textrm{is the distribution of}\ \mathbf {w}^\top\mathbf {X}\ \textrm{when the distribution of}\ \mathbf {X}\ \textrm{is}\ F \}

\end{align*}and

\begin{equation*}

{\cal S}_{\mathbf {w}}(\bf{\mu},\Sigma)=\{F \in \mathcal{P}_2(\mathbb{R}): \mathbb{E}^F[\mathbf{X}]=\mathbf{w}^\top\mathbf{\bf{\mu}}, \mathrm{Var}^F(\mathbf{X}) = \mathbf{w}^\top\Sigma \mathbf{w} \}.

\end{equation*}

\begin{equation*}

{\cal S}_{\mathbf {w}}(\bf{\mu},\Sigma)=\{F \in \mathcal{P}_2(\mathbb{R}): \mathbb{E}^F[\mathbf{X}]=\mathbf{w}^\top\mathbf{\bf{\mu}}, \mathrm{Var}^F(\mathbf{X}) = \mathbf{w}^\top\Sigma \mathbf{w} \}.

\end{equation*}Proof of Theorem 3.1

The core of the robust optimization problem in portfolio is solving for the internal worst-case Omega ratio under the uncertainty set  ${\cal S}(\bf{\mu},\Sigma)$. By Lemma 3.2, we have

${\cal S}(\bf{\mu},\Sigma)$. By Lemma 3.2, we have

\begin{equation*}

\inf_{F \in {\cal S}(\bf{\mu},\Sigma)} \Omega_{\mathbf{w}^\top \mathbf {X}}^{F}(c)=\inf_{F_{\mathbf {w}} \in {\cal S}(\mathbf{w},\bf{\mu},\Sigma)} \Omega_{\mathbf{w}^\top\mathbf {X}}^{F_{\mathbf {w}}}(c)=\inf_{G \in {\cal S}_{\mathbf {w}}(\bf{\mu},\Sigma)} \Omega_{Y}^G(c).

\end{equation*}

\begin{equation*}

\inf_{F \in {\cal S}(\bf{\mu},\Sigma)} \Omega_{\mathbf{w}^\top \mathbf {X}}^{F}(c)=\inf_{F_{\mathbf {w}} \in {\cal S}(\mathbf{w},\bf{\mu},\Sigma)} \Omega_{\mathbf{w}^\top\mathbf {X}}^{F_{\mathbf {w}}}(c)=\inf_{G \in {\cal S}_{\mathbf {w}}(\bf{\mu},\Sigma)} \Omega_{Y}^G(c).

\end{equation*} Hence, for  $\mathbf{w}^\top \bf{\mu} \geqslant c$, one can verify that

$\mathbf{w}^\top \bf{\mu} \geqslant c$, one can verify that

\begin{equation*}

\underline{\Omega}_{\mathbf X}(\mathbf{w},c,\bf{\mu},\Sigma):=\inf_{F \in {\cal S}(\bf{\mu},\Sigma)} \Omega_{\mathbf{w}^\top \mathbf {X}}^{F}(c)=

\inf_{G \in {\cal S}_{\mathbf {w}}(\bf{\mu},\Sigma)} \Omega_{Y}^G(c)=\min_{G \in {\cal S}_{\mathbf {w}}(\bf{\mu},\Sigma)} \Omega_{Y}^G(c) = \frac{\sqrt{1+S_{\mathbf {w}}^2}+S_{\mathbf {w}}}{\sqrt{1+S_{\mathbf {w}}^2}-S_{\mathbf {w}}}

\end{equation*}

\begin{equation*}

\underline{\Omega}_{\mathbf X}(\mathbf{w},c,\bf{\mu},\Sigma):=\inf_{F \in {\cal S}(\bf{\mu},\Sigma)} \Omega_{\mathbf{w}^\top \mathbf {X}}^{F}(c)=

\inf_{G \in {\cal S}_{\mathbf {w}}(\bf{\mu},\Sigma)} \Omega_{Y}^G(c)=\min_{G \in {\cal S}_{\mathbf {w}}(\bf{\mu},\Sigma)} \Omega_{Y}^G(c) = \frac{\sqrt{1+S_{\mathbf {w}}^2}+S_{\mathbf {w}}}{\sqrt{1+S_{\mathbf {w}}^2}-S_{\mathbf {w}}}

\end{equation*}directly by Theorem  $2.2$, where

$2.2$, where  $S_{\mathbf {w}}= \frac{\mathbf{w}^\top \bf{\mu} - c} {\sqrt{\mathbf{w}^\top \Sigma \mathbf{w}}}$. The above conclusion gives the worst-case Omega ratio with respect to the weight w. The monotonic progression of

$S_{\mathbf {w}}= \frac{\mathbf{w}^\top \bf{\mu} - c} {\sqrt{\mathbf{w}^\top \Sigma \mathbf{w}}}$. The above conclusion gives the worst-case Omega ratio with respect to the weight w. The monotonic progression of  $\underline{\Omega}_{\mathbf X}(\mathbf{w},c,\bf{\mu},\Sigma)$ with respect to

$\underline{\Omega}_{\mathbf X}(\mathbf{w},c,\bf{\mu},\Sigma)$ with respect to  $S_{\mathbf {w}}$ is obvious, implying that the worst-case Omega ratio problem in the portfolio is equivalent to the supremum of the Sharpe ratio

$S_{\mathbf {w}}$ is obvious, implying that the worst-case Omega ratio problem in the portfolio is equivalent to the supremum of the Sharpe ratio  $S_{\mathbf{w}}$. Thus, we complete the proof.

$S_{\mathbf{w}}$. Thus, we complete the proof.

Remark 2. We consider the situation where the expected return is greater than the risk-free return, that is,  $\mathbf {w}^\top\bf{\mu} \geqslant c$. Therefore, in Theorem 3.1, we simplify problem (9) in the case of

$\mathbf {w}^\top\bf{\mu} \geqslant c$. Therefore, in Theorem 3.1, we simplify problem (9) in the case of  $\mathbf {w}^\top\bf{\mu} \geqslant c$. For

$\mathbf {w}^\top\bf{\mu} \geqslant c$. For  $\mathbf {w}^\top\bf{\mu} \lt c$, by Theorem 2.2,

$\mathbf {w}^\top\bf{\mu} \lt c$, by Theorem 2.2,  $\underline{\Omega}_{\mathbf{X}}(\mathbf{w},c,\bf{\mu},\Sigma)=0$, and thus the optimal value of problem (9) is 0.

$\underline{\Omega}_{\mathbf{X}}(\mathbf{w},c,\bf{\mu},\Sigma)=0$, and thus the optimal value of problem (9) is 0.

Remark 3. Given  $c\in \mathbb{R}$,

$c\in \mathbb{R}$,  $\bf{\mu}_1$,

$\bf{\mu}_1$,  $\bf{\mu}_2\in \mathbb{R}^d$ and two positive semidefinite matrices Σ1,

$\bf{\mu}_2\in \mathbb{R}^d$ and two positive semidefinite matrices Σ1,  $\Sigma_2 \in \mathbb{R}^{d \times d}$, assume

$\Sigma_2 \in \mathbb{R}^{d \times d}$, assume  $\bf{\mu}_1 \preceq \bf{\mu}_2$ ,

$\bf{\mu}_1 \preceq \bf{\mu}_2$ ,  $\Sigma_1 \preceq \Sigma_2$ Footnote 2 and

$\Sigma_1 \preceq \Sigma_2$ Footnote 2 and  $\mathbf {w}^\top\bf{\mu}_1 \geqslant c$ for

$\mathbf {w}^\top\bf{\mu}_1 \geqslant c$ for  $\mathbf {w} \in \mathbb{W}$. If both the mean and covariance matrix are included in the box uncertainty set, that is,

$\mathbf {w} \in \mathbb{W}$. If both the mean and covariance matrix are included in the box uncertainty set, that is,

\begin{align*}

{\cal S}_1(\bf{\mu}_1,\bf{\mu}_2,\Sigma_1,\Sigma_2)

:=\{F\in \mathcal{P}_2(\mathbb{R}^d): \bf{\mu}_1\preceq \mathbb{E}^F[\mathbf{X}] \preceq \bf{\mu}_2,

\Sigma_1\preceq \mathrm{Var}^F(\mathbf{X}) \preceq \Sigma_2 \},

\end{align*}

\begin{align*}

{\cal S}_1(\bf{\mu}_1,\bf{\mu}_2,\Sigma_1,\Sigma_2)

:=\{F\in \mathcal{P}_2(\mathbb{R}^d): \bf{\mu}_1\preceq \mathbb{E}^F[\mathbf{X}] \preceq \bf{\mu}_2,

\Sigma_1\preceq \mathrm{Var}^F(\mathbf{X}) \preceq \Sigma_2 \},

\end{align*}then we can obtain similar results by applying the result in Theorem 3.1. We consider the distributionally robust portfolio optimization problem under the new mean-variance uncertainty set:

\begin{equation}

\sup_{\mathbf{w}\in \mathbb{W}} \inf_{F \in {\cal S}_1(\bf{\mu}_1,\bf{\mu}_2,\Sigma_1,\Sigma_2)} \Omega_{\mathbf{w}^\top \mathbf{X}}^{F}(c),

\end{equation}

\begin{equation}

\sup_{\mathbf{w}\in \mathbb{W}} \inf_{F \in {\cal S}_1(\bf{\mu}_1,\bf{\mu}_2,\Sigma_1,\Sigma_2)} \Omega_{\mathbf{w}^\top \mathbf{X}}^{F}(c),

\end{equation}where  $ \Omega_{\mathbf{w}^\top \mathbf{X}}^{F}(c)$ represents the Omega ratio of

$ \Omega_{\mathbf{w}^\top \mathbf{X}}^{F}(c)$ represents the Omega ratio of  $\mathbf{w}^\top \mathbf{X}$ that is calculated under the constraint that the distribution of X is F. One can verify that

$\mathbf{w}^\top \mathbf{X}$ that is calculated under the constraint that the distribution of X is F. One can verify that

\begin{align*}

\inf_{F \in {\cal S}_1(\bf{\mu}_1,\bf{\mu}_2,\Sigma_1,\Sigma_2)} \Omega_{\mathbf{w}^\top \mathbf{X}}^{F}(c)=\inf_{\bf{\mu}_1\preceq \bf{\mu} \preceq \bf{\mu}_2 \atop

\Sigma_1\preceq \Sigma \preceq \Sigma_2}\inf_{F \in {\cal S}(\bf{\mu},\Sigma)} \Omega_{\mathbf{w}^\top \mathbf{X}}^{F}(c)=\inf_{\bf{\mu}_1\preceq \bf{\mu} \preceq \bf{\mu}_2 \atop

\Sigma_1\preceq \Sigma \preceq \Sigma_2}\frac{\sqrt{1+S_{\mathbf {w}}^2}+S_{\mathbf {w}}}{\sqrt{1+S_{\mathbf {w}}^2}-S_{\mathbf {w}}},

\end{align*}

\begin{align*}

\inf_{F \in {\cal S}_1(\bf{\mu}_1,\bf{\mu}_2,\Sigma_1,\Sigma_2)} \Omega_{\mathbf{w}^\top \mathbf{X}}^{F}(c)=\inf_{\bf{\mu}_1\preceq \bf{\mu} \preceq \bf{\mu}_2 \atop

\Sigma_1\preceq \Sigma \preceq \Sigma_2}\inf_{F \in {\cal S}(\bf{\mu},\Sigma)} \Omega_{\mathbf{w}^\top \mathbf{X}}^{F}(c)=\inf_{\bf{\mu}_1\preceq \bf{\mu} \preceq \bf{\mu}_2 \atop

\Sigma_1\preceq \Sigma \preceq \Sigma_2}\frac{\sqrt{1+S_{\mathbf {w}}^2}+S_{\mathbf {w}}}{\sqrt{1+S_{\mathbf {w}}^2}-S_{\mathbf {w}}},

\end{align*}where  $S_{\mathbf {w}}= \frac{\mathbf{w}^\top \bf{\mu} - c} {\sqrt{\mathbf{w}^\top \Sigma \mathbf{w}}}$. Note that

$S_{\mathbf {w}}= \frac{\mathbf{w}^\top \bf{\mu} - c} {\sqrt{\mathbf{w}^\top \Sigma \mathbf{w}}}$. Note that  $S_{\mathbf {w}}$ is increasing with respect to µ and decreasing with respect to Σ. Furthermore,

$S_{\mathbf {w}}$ is increasing with respect to µ and decreasing with respect to Σ. Furthermore,  $\frac{\sqrt{1+S_{\mathbf {w}}^2}+S_{\mathbf {w}}}{\sqrt{1+S_{\mathbf {w}}^2}-S_{\mathbf {w}}}$ is increasing with respect to

$\frac{\sqrt{1+S_{\mathbf {w}}^2}+S_{\mathbf {w}}}{\sqrt{1+S_{\mathbf {w}}^2}-S_{\mathbf {w}}}$ is increasing with respect to  $S_{\mathbf {w}}$. Thus, problem (11) is equivalent to the following optimization problem:

$S_{\mathbf {w}}$. Thus, problem (11) is equivalent to the following optimization problem:

\begin{equation}

\sup_{\mathbf {w} \in \mathbb{W}} \frac{\mathbf {w} ^\top \bf{\mu}_1-c}{\sqrt{\mathbf {w}^\top \Sigma_2 \mathbf {w}}},

\end{equation}

\begin{equation}

\sup_{\mathbf {w} \in \mathbb{W}} \frac{\mathbf {w} ^\top \bf{\mu}_1-c}{\sqrt{\mathbf {w}^\top \Sigma_2 \mathbf {w}}},

\end{equation}in the sense that two problems have the same optimal solution.

3.2. Mean-Wasserstein uncertainty set

We consider a distributionally robust portfolio optimization problem based on Omega ratio in the portfolio under the mean-Wasserstein uncertainty set. Let  $F \in {\cal P}_p(\mathbb{R}^d)$ be a prespecified distribution used as a benchmark. Assume the distribution of

$F \in {\cal P}_p(\mathbb{R}^d)$ be a prespecified distribution used as a benchmark. Assume the distribution of  $\mathbf {X}$, defined at the beginning of Section 3, is G, which satisfies

$\mathbf {X}$, defined at the beginning of Section 3, is G, which satisfies  $W_{p} (F,G)\leqslant \varepsilon$. The distribution of

$W_{p} (F,G)\leqslant \varepsilon$. The distribution of  $\mathbf {w}^\top\mathbf {X}$ is denoted by

$\mathbf {w}^\top\mathbf {X}$ is denoted by  $G_{\mathbf {w}}$ when the distribution of

$G_{\mathbf {w}}$ when the distribution of  $\mathbf {X}$ is G. Then, we propose the distributionally robust portfolio optimization problem under mean-Wasserstein uncertainty set:

$\mathbf {X}$ is G. Then, we propose the distributionally robust portfolio optimization problem under mean-Wasserstein uncertainty set:

\begin{equation}

\sup_{\mathbf{w}\in \mathbb{W}} \inf_{G \in {\mathcal S}^d_{p,\varepsilon}(\bf{\mu},F)}

\Omega_{\mathbf {w}^\top \mathbf {X}}^{G}(c)

\end{equation}

\begin{equation}

\sup_{\mathbf{w}\in \mathbb{W}} \inf_{G \in {\mathcal S}^d_{p,\varepsilon}(\bf{\mu},F)}

\Omega_{\mathbf {w}^\top \mathbf {X}}^{G}(c)

\end{equation}where ɛ > 0,  $F \in {\cal P}_p(\mathbb{R}^d)$,

$F \in {\cal P}_p(\mathbb{R}^d)$,

\begin{equation*}

\begin{aligned}

{\mathcal S}^d_{p,\varepsilon}(\bf{\mu},F): =\{G \in \mathscr B^p_{\varepsilon}(F) : \mathbb{E}^G[\mathbf {X}]=\bf{\mu}\},

\end{aligned}

\end{equation*}

\begin{equation*}

\begin{aligned}

{\mathcal S}^d_{p,\varepsilon}(\bf{\mu},F): =\{G \in \mathscr B^p_{\varepsilon}(F) : \mathbb{E}^G[\mathbf {X}]=\bf{\mu}\},

\end{aligned}

\end{equation*}and  $\Omega_{\mathbf {w} ^\top \mathbf {X}}^{G}(c)$ represents the Omega ratio of

$\Omega_{\mathbf {w} ^\top \mathbf {X}}^{G}(c)$ represents the Omega ratio of  $\mathbf {w}^\top\mathbf {X}$ that is calculated under the constraint that the distribution of X is G.

$\mathbf {w}^\top\mathbf {X}$ that is calculated under the constraint that the distribution of X is G.

In the following theorem, we give the explicit solution to the inner problem of Eq. (13) for p = 1 and simplify the inner problem of Eq. (13) for p > 1.

Theorem 3.5. For  $p \geqslant 1$, let

$p \geqslant 1$, let  $F \in {\cal P} _p(\mathbb{R}^d)$ be a benchmark distribution,

$F \in {\cal P} _p(\mathbb{R}^d)$ be a benchmark distribution,  $\mathbb{E}^F[\mathbf {X}]=\bf{\mu}$ and c be a sure payoff. Suppose

$\mathbb{E}^F[\mathbf {X}]=\bf{\mu}$ and c be a sure payoff. Suppose  $\mathbf {w}^\top \bf{\mu} \geqslant c$ for

$\mathbf {w}^\top \bf{\mu} \geqslant c$ for  $\mathbf {w} \in \mathbb{W}$, and denote

$\mathbf {w} \in \mathbb{W}$, and denote

\begin{equation}

\begin{aligned}

\sup_{\mathbf{w}\in \mathbb{W}} \inf_{G \in {\mathcal S}^d_{p,\varepsilon}(\bf{\mu},F)}

\Omega_{\mathbf {w}^\top \mathbf {X}}^{G}(c):=\sup_{\mathbf{w}\in \mathbb{W}}\underline{\Omega}_{\mathbf {X}}^{F}(\mathbf {w},c,\bf{\mu},\varepsilon).

\end{aligned}

\end{equation}

\begin{equation}

\begin{aligned}

\sup_{\mathbf{w}\in \mathbb{W}} \inf_{G \in {\mathcal S}^d_{p,\varepsilon}(\bf{\mu},F)}

\Omega_{\mathbf {w}^\top \mathbf {X}}^{G}(c):=\sup_{\mathbf{w}\in \mathbb{W}}\underline{\Omega}_{\mathbf {X}}^{F}(\mathbf {w},c,\bf{\mu},\varepsilon).

\end{aligned}

\end{equation}(i) If p = 1, then we have

where\begin{equation*}

\begin{aligned}

\underline{\Omega}_{\mathbf {X}}^{F}(\mathbf {w},c,\bf{\mu},\varepsilon)=\left\{

\begin{aligned}

&1, & \textrm{if}\ \mathbf {w}^\top\bf{\mu} \in \mathcal{A}_1^* \cup \mathcal{B}_1^*, \\

&\left[1-\frac{2(\mathbf {w}^\top\bf{\mu}-c)}{\mathbf {w}^\top\bf{\mu}-\mu_{F_{\mathbf {w}}}+\varepsilon}\right]^{-1}, & \textrm{if}\ \mathbf {w}^\top\bf{\mu} \in \mathcal{A}_2^* \cup \mathcal{B}_2^*,

\end{aligned}

\right.

\end{aligned}

\end{equation*}$\mathcal{A}_1^*=\{\mu:\mu \gt \mu_{F_{\mathbf {w}}}-\mu_{F_{\mathbf {w}}}^{c_+}, \mu \gt \mu_{F_{\mathbf {w}}}-2\mu_{F_{\mathbf {w}}}^{c_+}+\varepsilon\},$ $\mathcal{A}_2^*=\{\mu:\mu \gt \mu_{F_{\mathbf {w}}}-\mu_{F_{\mathbf {w}}}^{c_+}, \mu \leqslant \mu_{F_{\mathbf {w}}}-2\mu_{F_{\mathbf {w}}}^{c_+}+\varepsilon\}$, $\mathcal{B}_1^*=\{\mu:\mu \leqslant \mu_{F_{\mathbf {w}}}-\mu_{F_{\mathbf {w}}}^{c_+}, \mu \lt \mu_{F_{\mathbf {w}}}-\varepsilon\}$ and $\mathcal{B}_2^*=\{\mu:\mu \leqslant \mu_{F_{\mathbf {w}}}-\mu_{F_{\mathbf {w}}}^{c_+}, \mu \geqslant \mu_{F_{\mathbf {w}}}-\varepsilon\}$.

(ii) If p > 1, then we have

where\begin{equation*}

\underline{\Omega}_{\mathbf {X}}^{F}(\mathbf {w},c,\bf{\mu},\varepsilon)=\left[ 1-\frac{\mathbf {w}^\top\bf{\mu}-c}{T(\mathbf {w}^\top\bf{\mu})}\right]^{-1},

\end{equation*}and\begin{align*}

T(\mathbf {w}^\top \bf{\mu})=\inf_{\lambda \geqslant 0 , \gamma \in \mathbb{R}} \bigg\{&\lambda ( \left\lVert \mathbf {w} \right\rVert_* \varepsilon)^p +\gamma (\mathbf {w}^\top \bf{\mu} - \mu_{F_{\mathbf {w}}}) \\

&+ |\gamma| \left(1- \frac{1}{p}\right) \left( \frac{|\gamma |}{\lambda p}\right)^{\frac{1}{p-1}} + \mathbb{E}^{F} [ (\mathbf {w}^\top \mathbf {X}-c_1(\lambda,\gamma))_+]\bigg\},

\end{align*}$c_1(\lambda,\gamma)$ is defined in Theorem $2.6$.

For the benchmark distribution F, define

\begin{align*}

{\mathcal F}_{\mathbf {w},p,\varepsilon}(F) =\{& G_{\mathbf {w}^\top\mathbf {X}} \in {\cal P}_p(\mathbb{R}):G\in \mathscr B^p_{\varepsilon}(F),\\

& G_{\mathbf {w}}\ \textrm{is the distribution of}\ \mathbf {w}^\top\mathbf {X}\ \textrm{when the distribution of}\ \mathbf {X}\ \textrm{is}\ G\}.

\end{align*}

\begin{align*}

{\mathcal F}_{\mathbf {w},p,\varepsilon}(F) =\{& G_{\mathbf {w}^\top\mathbf {X}} \in {\cal P}_p(\mathbb{R}):G\in \mathscr B^p_{\varepsilon}(F),\\

& G_{\mathbf {w}}\ \textrm{is the distribution of}\ \mathbf {w}^\top\mathbf {X}\ \textrm{when the distribution of}\ \mathbf {X}\ \textrm{is}\ G\}.

\end{align*} The following lemma can be found in [Reference Mao, Wang and Wu14], which will be used in the proof of Theorem  $3.5$.

$3.5$.

Lemma 3.6. For  $\varepsilon \geqslant 0$,

$\varepsilon \geqslant 0$,  $p \geqslant 1$ and

$p \geqslant 1$ and  $ \mathbf{w} \neq \bf{0}$, assume a prespecified distribution

$ \mathbf{w} \neq \bf{0}$, assume a prespecified distribution  $F \in {\cal P}_p(\mathbb{R}^d)$, it holds that

$F \in {\cal P}_p(\mathbb{R}^d)$, it holds that

\begin{equation*}

{\mathcal{F}}_{\mathbf {w},p,\varepsilon}(F) =\mathscr B^p_{\left\lVert \mathbf {w} \right\rVert _* \varepsilon}(F_{\mathbf {w}}),

\end{equation*}

\begin{equation*}

{\mathcal{F}}_{\mathbf {w},p,\varepsilon}(F) =\mathscr B^p_{\left\lVert \mathbf {w} \right\rVert _* \varepsilon}(F_{\mathbf {w}}),

\end{equation*}where  $\left\lVert \cdot \right\rVert _*$ is the dual norm of

$\left\lVert \cdot \right\rVert _*$ is the dual norm of  $\left\lVert \cdot \right\rVert $.

$\left\lVert \cdot \right\rVert $.

Now we use the projection result in Lemma 3.6 to prove Theorem 3.5.

Proof of Theorem 3.5

We focus on a portfolio selection problem where the unknown distribution of  $\mathbf {X}$ is in the uncertainty set

$\mathbf {X}$ is in the uncertainty set  ${\mathcal S}_4$. For

${\mathcal S}_4$. For  $F \in {\cal P} _p(\mathbb{R}^d)$, let

$F \in {\cal P} _p(\mathbb{R}^d)$, let

\begin{align*}

{\mathcal S}_{p,\varepsilon}(\mathbf {w},\bf{\mu},F)=\{&G_{\mathbf {w}} \in {\cal P}_p(\mathbb{R}):G\in {\mathcal S}^d_{p,\varepsilon}(\bf{\mu},F),\\

& G_{\mathbf {w}}\ \textrm{is the distribution of}\ \mathbf {w}^\top\mathbf {X}\ \textrm{when the distribution of}\ \mathbf {X}\ \textrm{is}\ G\}.

\end{align*}

\begin{align*}

{\mathcal S}_{p,\varepsilon}(\mathbf {w},\bf{\mu},F)=\{&G_{\mathbf {w}} \in {\cal P}_p(\mathbb{R}):G\in {\mathcal S}^d_{p,\varepsilon}(\bf{\mu},F),\\

& G_{\mathbf {w}}\ \textrm{is the distribution of}\ \mathbf {w}^\top\mathbf {X}\ \textrm{when the distribution of}\ \mathbf {X}\ \textrm{is}\ G\}.

\end{align*} By the Lemma 3.6, we have  ${\mathcal{F}}_{\mathbf {w},p,\varepsilon}(F)=\mathscr B^p_{\left\lVert \mathbf {w} \right\rVert _* \varepsilon}(F_{\mathbf {w}})$. It directly applies that

${\mathcal{F}}_{\mathbf {w},p,\varepsilon}(F)=\mathscr B^p_{\left\lVert \mathbf {w} \right\rVert _* \varepsilon}(F_{\mathbf {w}})$. It directly applies that  ${\mathcal S}_{p,\varepsilon}(\mathbf {w},\bf{\mu},F)=\mathcal{S}^1_{p, \left\lVert \mathbf {w} \right\rVert _* \varepsilon}(\mathbf {w}^\top \bf{\mu},F_{\mathbf {w}})$. As a result,

${\mathcal S}_{p,\varepsilon}(\mathbf {w},\bf{\mu},F)=\mathcal{S}^1_{p, \left\lVert \mathbf {w} \right\rVert _* \varepsilon}(\mathbf {w}^\top \bf{\mu},F_{\mathbf {w}})$. As a result,

\begin{equation*}

\inf_{G \in {\mathcal S}^d_{p,\varepsilon}(\bf{\mu},F)}

\Omega_{\mathbf {w}^\top \mathbf {X}}^{G}(c)=\inf_{G_{\mathbf {w}} \in {\mathcal S}_{p,\varepsilon}(\mathbf {w},\bf{\mu},F)}

\Omega_{\mathbf {w}^\top \mathbf {X}}^{G_{\mathbf {w}}}(c)=\inf_{H \in \mathcal{S}^1_{p, \left\lVert \mathbf {w} \right\rVert _* \varepsilon}(\mathbf {w}^\top \bf{\mu},F_{\mathbf {w}})}

\Omega_{Y}^{H}(c).

\end{equation*}

\begin{equation*}

\inf_{G \in {\mathcal S}^d_{p,\varepsilon}(\bf{\mu},F)}

\Omega_{\mathbf {w}^\top \mathbf {X}}^{G}(c)=\inf_{G_{\mathbf {w}} \in {\mathcal S}_{p,\varepsilon}(\mathbf {w},\bf{\mu},F)}

\Omega_{\mathbf {w}^\top \mathbf {X}}^{G_{\mathbf {w}}}(c)=\inf_{H \in \mathcal{S}^1_{p, \left\lVert \mathbf {w} \right\rVert _* \varepsilon}(\mathbf {w}^\top \bf{\mu},F_{\mathbf {w}})}

\Omega_{Y}^{H}(c).

\end{equation*} Hence, for  $ \mathbf {w}^\top \bf{\mu} \geqslant c$, applying Theorem

$ \mathbf {w}^\top \bf{\mu} \geqslant c$, applying Theorem  $2.6$ to

$2.6$ to  $\mathbf {w}^\top \mathbf {X}$, the result follows immediately.

$\mathbf {w}^\top \mathbf {X}$, the result follows immediately.

In Theorem 3.5, we apply problem (7) in portfolio selection. In Section 3.3, we will discuss finite sample guarantee based on Wasserstein ball.

3.3. Finite sample guarantee based on Wasserstein ball

In portfolio simulation, the distribution of portfolio assets is unknown, and we often use an empirical distribution function  $\hat{F}_N$ to approximate the true distribution of assets. This uncertainty set provides attractive performance guarantees under the common light tail assumption of generating a distribution F over unknown data.

$\hat{F}_N$ to approximate the true distribution of assets. This uncertainty set provides attractive performance guarantees under the common light tail assumption of generating a distribution F over unknown data.

Assumption 3.7. (Light-tailed distribution)

For  $F \in {\cal P}_p(\mathbb{R}^d)$, there exists an exponent a > p such that

$F \in {\cal P}_p(\mathbb{R}^d)$, there exists an exponent a > p such that

\begin{equation*}

A:=\mathbb{E}^{F} [\exp(\left\lVert X \right\rVert^a)]=\int_{\mathbb{R}^d} \exp (\left\lVert \xi\right\rVert ^a) {F} (d \xi) \lt +\infty.

\end{equation*}

\begin{equation*}

A:=\mathbb{E}^{F} [\exp(\left\lVert X \right\rVert^a)]=\int_{\mathbb{R}^d} \exp (\left\lVert \xi\right\rVert ^a) {F} (d \xi) \lt +\infty.

\end{equation*} Assumption 3.7 essentially requires that the tails of the distribution F decay at an exponential rate. Let  $\mathbb{W}_1=\{\mathbf {w}\in \mathbb{R}^d: w_i \geqslant 0 ,\ i=1,\ldots,d,\ \sum_{i=1}^{d}w_i=1\}$ and

$\mathbb{W}_1=\{\mathbf {w}\in \mathbb{R}^d: w_i \geqslant 0 ,\ i=1,\ldots,d,\ \sum_{i=1}^{d}w_i=1\}$ and  $\mathbf{e}_{1/d}=(1/d,\ldots,1/d)^\top$. We have

$\mathbf{e}_{1/d}=(1/d,\ldots,1/d)^\top$. We have  $U_{\mathbb{W}_1}:=\sup_{\mathbf {w} \in \mathbb{W}_1}\left\lVert\mathbf {w}\right\rVert_*=1 \lt \infty$ and

$U_{\mathbb{W}_1}:=\sup_{\mathbf {w} \in \mathbb{W}_1}\left\lVert\mathbf {w}\right\rVert_*=1 \lt \infty$ and  $L_{\mathbb{W}_1}:=\inf_{\mathbf {w} \in \mathbb{W}_1}\left\lVert\mathbf {w}\right\rVert_*=\left\lVert\mathbf{e}_{1/d}\right\rVert_* \gt 0$. For

$L_{\mathbb{W}_1}:=\inf_{\mathbf {w} \in \mathbb{W}_1}\left\lVert\mathbf {w}\right\rVert_*=\left\lVert\mathbf{e}_{1/d}\right\rVert_* \gt 0$. For  $\mathbf {w} \in \mathbb{W}_1$,

$\mathbf {w} \in \mathbb{W}_1$,  $\hat{F}_{\mathbf {w},N}$ is constructed with i.i.d samples in the population whose true distribution is

$\hat{F}_{\mathbf {w},N}$ is constructed with i.i.d samples in the population whose true distribution is  $F_{\mathbf {w}}$. We have the following lemma from Theorem 2 of Fournier and Guillin [Reference Fournier and Guillin7].

$F_{\mathbf {w}}$. We have the following lemma from Theorem 2 of Fournier and Guillin [Reference Fournier and Guillin7].

Lemma 3.8. If Assumption 3.7 holds, then for any  $\mathbf {w} \in \mathbb{W}_1$,

$\mathbf {w} \in \mathbb{W}_1$,  $N \geqslant 1$ and ɛ > 0, we have

$N \geqslant 1$ and ɛ > 0, we have

\begin{equation}

\mathbb{P}^N \left(W_{p}\left(F_{\mathbf {w}},\hat{F}_{\mathbf {w},N}\right) \geqslant \varepsilon\right) \leqslant

\begin{cases}

c_1\, \exp\left(-c_2 N \varepsilon^2 \right), & {\rm if}\ \varepsilon \leqslant 1, \\

c_1\, \exp\left(-c_2 N \varepsilon^{a/p} \right), & {\rm if}\ \varepsilon \gt 1 ,\\

\end{cases}

\end{equation}

\begin{equation}

\mathbb{P}^N \left(W_{p}\left(F_{\mathbf {w}},\hat{F}_{\mathbf {w},N}\right) \geqslant \varepsilon\right) \leqslant

\begin{cases}

c_1\, \exp\left(-c_2 N \varepsilon^2 \right), & {\rm if}\ \varepsilon \leqslant 1, \\

c_1\, \exp\left(-c_2 N \varepsilon^{a/p} \right), & {\rm if}\ \varepsilon \gt 1 ,\\

\end{cases}

\end{equation}where c 1, c 2 are positive constants that only depend on a, A and p.

For fixed  $\mathbf {w} \in \mathbb{W}_1$, Lemma 3.8 provides an a priori estimate of the probability that the unknown data generating distribution

$\mathbf {w} \in \mathbb{W}_1$, Lemma 3.8 provides an a priori estimate of the probability that the unknown data generating distribution  $F_{\mathbf {w}}$ lies outside the Wasserstein ball

$F_{\mathbf {w}}$ lies outside the Wasserstein ball  $\mathscr B^p_{\varepsilon}(\hat{F}_{\mathbf {w},N})$. Equating the RHS of Eq. (15) to β and solving for ɛ yields

$\mathscr B^p_{\varepsilon}(\hat{F}_{\mathbf {w},N})$. Equating the RHS of Eq. (15) to β and solving for ɛ yields

\begin{equation}

\varepsilon_{p,N}(\beta) :=

\begin{cases}

\left( \frac{\log (c_1 \beta^{-1})}{c_2 N} \right)^{1/2}, & {\rm if}\ N \geqslant \frac{\log (c_1 \beta^{-1})}{c_2}, \\

\left( \frac{\log (c_1 \beta^{-1})}{c_2 N} \right)^{p/a}, & {\rm if}\ N \lt \frac{\log (c_1 \beta^{-1})}{c_2}. \\

\end{cases}

\end{equation}

\begin{equation}

\varepsilon_{p,N}(\beta) :=

\begin{cases}

\left( \frac{\log (c_1 \beta^{-1})}{c_2 N} \right)^{1/2}, & {\rm if}\ N \geqslant \frac{\log (c_1 \beta^{-1})}{c_2}, \\

\left( \frac{\log (c_1 \beta^{-1})}{c_2 N} \right)^{p/a}, & {\rm if}\ N \lt \frac{\log (c_1 \beta^{-1})}{c_2}. \\

\end{cases}

\end{equation} Thus, we can use Lemma 3.8 to estimate the radius of the smallest Wasserstein ball containing distribution  $F_{\mathbf {w}}$ with

$F_{\mathbf {w}}$ with  $1-\beta$ confidence for

$1-\beta$ confidence for  $\beta \in (0,1)$. Specifically, if Assumption 3.7 holds, then for any

$\beta \in (0,1)$. Specifically, if Assumption 3.7 holds, then for any  $\mathbf {w} \in \mathbb{W}_1$,

$\mathbf {w} \in \mathbb{W}_1$,  $N \geqslant 1$ and

$N \geqslant 1$ and  $\beta \in (0,1)$, we have

$\beta \in (0,1)$, we have

\begin{equation}

\mathbb{P}^N \left(W_{p}\left(F_{\mathbf {w}},\hat{F}_{\mathbf {w},N}\right) \leqslant \varepsilon_{p,N}(\beta)\right) \geqslant 1-\beta,

\end{equation}

\begin{equation}

\mathbb{P}^N \left(W_{p}\left(F_{\mathbf {w}},\hat{F}_{\mathbf {w},N}\right) \leqslant \varepsilon_{p,N}(\beta)\right) \geqslant 1-\beta,

\end{equation}where  $\varepsilon_{p,N}(\beta)$ is defined in Eq. (16). Then the concentration inequality gives rise to the following finite sample guarantee.

$\varepsilon_{p,N}(\beta)$ is defined in Eq. (16). Then the concentration inequality gives rise to the following finite sample guarantee.

Theorem 3.9. (Finite sample guarantee)

Suppose Assumption 3.7 holds. For  $\beta \in (0,1)$, let

$\beta \in (0,1)$, let  $\varepsilon_{p,N}(\beta)$ be defined in (16). Then we have

$\varepsilon_{p,N}(\beta)$ be defined in (16). Then we have

\begin{align*}

\mathbb{P}^N\left(\Omega_{\mathbf{w}^\top\mathbf {X}}^F(c)\geqslant \inf_{G \in \mathscr B^p_{\varepsilon_{p,N}(\beta)/L_{\mathbb{W}_1}}(\hat{F}_N)}\Omega_{\mathbf{w}^\top\mathbf {X}}^G(c)\right)\geqslant 1-\beta,\ \forall\mathbf {w} \in \mathbb{W}_1.

\end{align*}

\begin{align*}

\mathbb{P}^N\left(\Omega_{\mathbf{w}^\top\mathbf {X}}^F(c)\geqslant \inf_{G \in \mathscr B^p_{\varepsilon_{p,N}(\beta)/L_{\mathbb{W}_1}}(\hat{F}_N)}\Omega_{\mathbf{w}^\top\mathbf {X}}^G(c)\right)\geqslant 1-\beta,\ \forall\mathbf {w} \in \mathbb{W}_1.

\end{align*}Proof. Denoted by  $\varepsilon^*:=\varepsilon_{p,N}(\beta)/L_{\mathbb{W}_1}$. One can verify that

$\varepsilon^*:=\varepsilon_{p,N}(\beta)/L_{\mathbb{W}_1}$. One can verify that  $F_{\mathbf {w}} \in {\mathcal{F}}_{\mathbf {w},p,\varepsilon^*}(\hat{F}_N)$ implies that

$F_{\mathbf {w}} \in {\mathcal{F}}_{\mathbf {w},p,\varepsilon^*}(\hat{F}_N)$ implies that

\begin{align*}

\Omega_{\mathbf{w}^\top\mathbf {X}}^F(c)\geqslant \inf_{G \in \mathscr B^p_{\varepsilon^*}(\hat{F}_N)}\Omega_{\mathbf{w}^\top\mathbf {X}}^G(c).

\end{align*}

\begin{align*}

\Omega_{\mathbf{w}^\top\mathbf {X}}^F(c)\geqslant \inf_{G \in \mathscr B^p_{\varepsilon^*}(\hat{F}_N)}\Omega_{\mathbf{w}^\top\mathbf {X}}^G(c).

\end{align*}Then, we have

\begin{align*}

\mathbb{P}^N\left(\Omega_{\mathbf{w}^\top\mathbf {X}}^F(c)\geqslant \inf_{G \in \mathscr B^p_{\varepsilon^*}(\hat{F}_N)}\Omega_{\mathbf{w}^\top\mathbf {X}}^G(c)\right) \geqslant \mathbb{P}^N\left(F_{\mathbf {w}} \in {\mathcal{F}}_{\mathbf {w},p,\varepsilon^*}(\hat{F}_N)\right).

\end{align*}

\begin{align*}

\mathbb{P}^N\left(\Omega_{\mathbf{w}^\top\mathbf {X}}^F(c)\geqslant \inf_{G \in \mathscr B^p_{\varepsilon^*}(\hat{F}_N)}\Omega_{\mathbf{w}^\top\mathbf {X}}^G(c)\right) \geqslant \mathbb{P}^N\left(F_{\mathbf {w}} \in {\mathcal{F}}_{\mathbf {w},p,\varepsilon^*}(\hat{F}_N)\right).

\end{align*}By Lemma 3.6, we obtain

\begin{align*}

\mathbb{P}^N\left(F_{\mathbf {w}} \in {\mathcal{F}}_{\mathbf {w},p,\varepsilon^*}(\hat{F}_N)\right)=\mathbb{P}^N\left(F_{\mathbf {w}} \in \mathscr B^p_{\left\lVert \mathbf {w} \right\rVert _* \varepsilon^*}(\hat{F}_{\mathbf {w},N})\right)=\mathbb{P}^N \left(W_{p}\left(F_{\mathbf {w}},\hat{F}_{\mathbf {w},N}\right) \leqslant \left\lVert \mathbf {w} \right\rVert _* \varepsilon^*\right).

\end{align*}

\begin{align*}

\mathbb{P}^N\left(F_{\mathbf {w}} \in {\mathcal{F}}_{\mathbf {w},p,\varepsilon^*}(\hat{F}_N)\right)=\mathbb{P}^N\left(F_{\mathbf {w}} \in \mathscr B^p_{\left\lVert \mathbf {w} \right\rVert _* \varepsilon^*}(\hat{F}_{\mathbf {w},N})\right)=\mathbb{P}^N \left(W_{p}\left(F_{\mathbf {w}},\hat{F}_{\mathbf {w},N}\right) \leqslant \left\lVert \mathbf {w} \right\rVert _* \varepsilon^*\right).

\end{align*} Since  $\varepsilon^*=\varepsilon_{p,N}(\beta)/L_{\mathbb{W}_1}$, we have

$\varepsilon^*=\varepsilon_{p,N}(\beta)/L_{\mathbb{W}_1}$, we have

\begin{align*}

\mathbb{P}^N \left(W_{p}\left(F_{\mathbf {w}},\hat{F}_{\mathbf {w},N}\right) \leqslant \left\lVert \mathbf {w} \right\rVert _* \varepsilon^*\right) \geqslant \mathbb{P}^N \left(W_{p}\left(F_{\mathbf {w}},\hat{F}_{\mathbf {w},N}\right) \leqslant \varepsilon_{p,N}(\beta)\right).

\end{align*}

\begin{align*}

\mathbb{P}^N \left(W_{p}\left(F_{\mathbf {w}},\hat{F}_{\mathbf {w},N}\right) \leqslant \left\lVert \mathbf {w} \right\rVert _* \varepsilon^*\right) \geqslant \mathbb{P}^N \left(W_{p}\left(F_{\mathbf {w}},\hat{F}_{\mathbf {w},N}\right) \leqslant \varepsilon_{p,N}(\beta)\right).

\end{align*}Thus, one can verify that

\begin{align*}

\mathbb{P}^N\left(\Omega_{\mathbf{w}^\top\mathbf {X}}^F(c)\geqslant \inf_{G \in \mathscr B^p_{\varepsilon_{p,N}(\beta)/L_{\mathbb{W}_1}}(\hat{F}_N)}\Omega_{\mathbf{w}^\top\mathbf {X}}^G(c)\right) \geqslant 1-\beta

\end{align*}

\begin{align*}