1. Introduction

We study a class of storage-type stochastic control problems with absorption risk, focusing on value maximization. The underlying state process follows a general diffusion, which is controlled in two ways: (i) by adjusting its operational scale through a scaling process that takes values in [0, 1]; and (ii) by subtracting a non-decreasing withdrawal process. The controlled process is absorbed once it reaches zero (or below). The objective is to maximize the discounted value of all withdrawals until the absorption time, or indefinitely if absorption never occurs.

This type of stochastic control problem has numerous applications across various fields, including optimal cash flow management in finance (cf. [Reference Asmussen, Højgaard and Taksar3, Reference Bai, Guo and Zhang4, Reference Cadenillas, Choulli, Taksar and Zhang6, Reference Chen, Yuen and Wang7, Reference Choulli, Taksar and Zhou10, Reference Liang and Young17, Reference Radner and Shepp22, Reference Taksar and Zhou26]), harvesting planning (cf. [Reference Alvarez2]), and reservoir management, with the latter two generally involving only the control in (ii). In these contexts, the underlying process typically represents capital or reserves in a company, fluctuating populations in harvesting problems or water levels in a reservoir. In particular, these problems are closely related to the study of optimal dynamic risk exposure control and cash flow management, where the objective is to maximize the expected firm value. Firms strategically manage their risk exposure through business activities and/or risk-sharing mechanisms to optimize various objective functions (see, for example, [Reference Choulli, Taksar and Zhou10, Reference Radner and Shepp22, Reference Wang, Chen, Chiu and Wong27, Reference Bai, Zhou, Xiao, Gao and Zhong28]). This application has attracted significant attention over the past few decades, with some of the earliest contributions dating back to [Reference Radner and Shepp22, Reference Taksar and Zhou26]. In the standard setting, a firm’s liquid reserves are modeled as a diffusion process, where the drift term represents expected profit and the diffusion coefficient reflects risk exposure. The firm controls its risk exposure by adjusting the diffusion coefficient, which simultaneously affects expected profit in the same direction. Extensive literature exists on risk exposure control, including the use of reinsurance as a risk management tool to maximize firm value (see, for example, [Reference Asmussen, Højgaard and Taksar3, Reference Bai, Guo and Zhang4, Reference Cadenillas, Choulli, Taksar and Zhang6, Reference Chen, Yuen and Wang7, Reference Choulli, Taksar and Zhou9, Reference Choulli, Taksar and Zhou10, Reference Feng, Zhu and Siu12, Reference Guo13, Reference Liang and Young17, Reference Radner and Shepp22, Reference Taksar and Zhou26, Reference Yao, Yang and Wang29, Reference Zhou and Yuen31]).

Despite the extensive attention devoted to this type of optimal control problem in the literature, much of the research concerning the controls in both (i) and (ii) above has concentrated on models driven by Brownian motion. Surprisingly, there is still a lack of theoretical studies that address the value-maximization storage-type optimal control of risk exposure/operational scale, and withdrawals in more general and realistic diffusion models that extend beyond the Brownian framework. This paper aims to fill this gap by investigating this class of optimal control problem under a general linear diffusion model, with the goal of deriving explicit theoretical optimality results within this broader setting.

While Brownian motion plays a foundational role in stochastic modeling due to its analytical tractability, it is often too restrictive to accurately capture many real-world phenomena. For example, Brownian motion-based surplus models typically neglect investment or interest income on cash reserves and fail to capture the dependence of returns and volatility on the level of available capital. Although some progress has been made, relatively few studies have explored optimal operational scale and withdrawal strategies within models that move beyond the Brownian motion assumption.

In this paper, we take a step toward addressing this gap by studying a class of optimal operational scale and withdrawal control problems within a general diffusion framework. This class of models includes the classical Brownian motion model as a special case while allowing for more general dynamics, such as state-dependent drift and volatility. We show that these problems can be solved theoretically within this more flexible framework, thereby extending the scope of optimal control results to a wider array of diffusion-based models commonly used in finance and insurance. Our analysis is built upon a general diffusion framework, where both the drift and volatility coefficients are allowed to vary as general functions of the state (or storage) process. This level of generality accommodates a variety of models and enables a unified treatment of optimal control problems across different settings. We demonstrate that, even in this broader context, the optimal control problem is solvable and that the optimal solution to the optimization problem can be obtained through a theoretical approach.

We begin by conjecturing that the positive real line can be divided into three regions: the partial-scale region, the full-scale region, and the withdrawal region. We then theoretically establish the existence of, or implicitly construct, candidate solutions to the Hamilton–Jacobi–Bellman (HJB) equation in each region for any given thresholds. Without requiring explicit closed-form solutions, we derive key theoretical properties of these solutions. A global candidate solution is constructed by smoothly pasting the local solutions across the three regions. By appropriately setting the thresholds, we prove that this global solution satisfies the necessary conditions to be the optimal solution. Our theoretical results hold in a general setting and apply to a broad class of problems. To illustrate the applicability of our approach, we provide examples where explicit solutions can be derived, as well as cases where explicit forms are unavailable within our proposed framework.

This work makes several contributions. We solve a class of value-maximizing optimal control problems involving operational scale/risk exposure, and withdrawals under a generalized diffusion framework. This framework accommodates a broad range of scenarios, including traditional Brownian motion as well as more general diffusion processes. Our approach yields either explicit or semi-explicit solutions. We develop a comprehensive and unified mathematical methodology for addressing these optimization problems. A rigorous and implementable procedure is provided for identifying solutions, whether in cases where closed-form solutions exist or where fully explicit expressions are not obtainable. In addition, we derive necessary and sufficient conditions for the existence of explicit solutions. Finally, to demonstrate the applicability of our results, we present a variety of examples, some rooted in classical settings, and others representing novel scenarios that reflect diverse business contexts for which, to the best of our knowledge, no prior solutions exist.

The remainder of the paper is organized as follows. In Section 2, we introduce the dynamic model and formulate the storage-type value-maximizing operational scale and withdrawals control problem. We divide the analysis into three scenarios based on the behavior of the drift rate: (i) when the drift rate is strictly positive for all levels of storage, (ii) when the drift rate is non-positive at zero storage, and (iii) when the drift becomes negative at some point despite being positive at the origin (zero storage level). These cases are examined in detail in Sections 3–5, where we present the mathematical derivations, optimality results, and semi-explicit forms of the solutions in the general setting. In Section 6, we identify the necessary and sufficient conditions for the availability of fully explicit solutions. Section 7 summarizes the general procedure for solving the optimal control problem. In Section 8, we illustrate the results through several examples, including cases where explicit solutions are available. We also apply the general framework and solution procedure to well-known models of practical interest, such as the Brownian motion model and the Ornstein–Uhlenbeck process. For models where explicit solutions are not tractable, we demonstrate how the same methodology can be used to derive numerical approximations, supported by examples across various scenarios. Section 10 concludes the paper. All technical proofs are provided in the Appendix.

2. Problem formulation

Let

$(\Omega, \mathcal{F}, {\mathrm{P}})$

denote a probability space, where all the random variables involved are defined. Let

$(\Omega, \mathcal{F}, {\mathrm{P}})$

denote a probability space, where all the random variables involved are defined. Let

${\mathrm{E}}$

represent the expectation associated with

${\mathrm{E}}$

represent the expectation associated with

${\mathrm{P}}$

. Define

${\mathrm{P}}$

. Define

$W=\{W_t\}_{t\ge 0}$

to be a standard Brownian motion and let

$W=\{W_t\}_{t\ge 0}$

to be a standard Brownian motion and let

$\mathcal{F}^W$

denote the augmented complete filtration generated by W. Consider the controlled stochastic process

$\mathcal{F}^W$

denote the augmented complete filtration generated by W. Consider the controlled stochastic process

$ X_t^{\pi,L}$

governed by the stochastic differential equation (SDE):

$ X_t^{\pi,L}$

governed by the stochastic differential equation (SDE):

\begin{eqnarray} {\mathrm{d}} X_t^{\pi,L}=\pi_{t} \big(\mu\big(X_{t-}^{\pi,L}\big){\mathrm{d}} t+ \sigma\big(X_{t-}^{\pi,L}\big){\mathrm{d}} W_t\big)- {\mathrm{d}} L_t,\quad t\ge 0,\end{eqnarray}

\begin{eqnarray} {\mathrm{d}} X_t^{\pi,L}=\pi_{t} \big(\mu\big(X_{t-}^{\pi,L}\big){\mathrm{d}} t+ \sigma\big(X_{t-}^{\pi,L}\big){\mathrm{d}} W_t\big)- {\mathrm{d}} L_t,\quad t\ge 0,\end{eqnarray}

where

$\pi_t$

is

$\pi_t$

is

$\mathcal{F}^W_t$

-predictable with

$\mathcal{F}^W_t$

-predictable with

$\pi_t\in[0,1]$

,

$\pi_t\in[0,1]$

,

$L_t$

is an

$L_t$

is an

$\mathcal{F}^W$

-predictable, non-decreasing, and cádlág (right-continuous with left limits) stochastic process with

$\mathcal{F}^W$

-predictable, non-decreasing, and cádlág (right-continuous with left limits) stochastic process with

$L_{0-}=0$

.

$L_{0-}=0$

.

We define the hitting time:

\begin{align}\tau^{\pi,L}=\inf \big\{t\ge 0\,:\, X^{\pi,L}_t<0 \big\}.\end{align}

\begin{align}\tau^{\pi,L}=\inf \big\{t\ge 0\,:\, X^{\pi,L}_t<0 \big\}.\end{align}

This hitting time has a natural interpretation in both harvesting planning and reservoir management problems, as it represents the time of extinction and exhaustion, respectively, naturally marking the end of the process. In financial applications, when

$ X_t $

represents cash reserves, this is the time when reserves hit zero. At this point, we assume the business ceases operations, due to forced liquidation resulting from reserve constraints, as assumed in [Reference Pierre, Villeneuve and Warin20].

$ X_t $

represents cash reserves, this is the time when reserves hit zero. At this point, we assume the business ceases operations, due to forced liquidation resulting from reserve constraints, as assumed in [Reference Pierre, Villeneuve and Warin20].

We assume the following standard conditions on

$\mu(\!\cdot\!)$

and

$\mu(\!\cdot\!)$

and

$\sigma(\!\cdot\!)$

: both

$\sigma(\!\cdot\!)$

: both

$\mu(x)$

and

$\mu(x)$

and

$\sigma(x)$

are Lipschitz continuous on

$\sigma(x)$

are Lipschitz continuous on

$[0,\infty)$

and grow no faster than linearly in x, and

$[0,\infty)$

and grow no faster than linearly in x, and

$\sigma(\!\cdot\!)$

is positive and non-vanishing on

$\sigma(\!\cdot\!)$

is positive and non-vanishing on

$[0,\infty)$

. These conditions guarantee that, for an initial state

$[0,\infty)$

. These conditions guarantee that, for an initial state

$X_{0-}=x$

, and a pair

$X_{0-}=x$

, and a pair

$(\pi,L)$

(with

$(\pi,L)$

(with

$\pi_t$

being

$\pi_t$

being

$\mathcal{F}^W$

-predictable and

$\mathcal{F}^W$

-predictable and

$L_t$

being

$L_t$

being

$\mathcal{F}^W$

-predictable, non-decreasing, and cádlág) there exists a unique strong solution to the SDE (1) on

$\mathcal{F}^W$

-predictable, non-decreasing, and cádlág) there exists a unique strong solution to the SDE (1) on

$0\le t\le \tau^{\pi,L}$

(see pp. 37–39 of [Reference Pham21]).

$0\le t\le \tau^{\pi,L}$

(see pp. 37–39 of [Reference Pham21]).

In the above setup, the pair

$(\pi,L)\,:\!=\,(\{\pi_t\}_{t\ge 0},\{L_t\}_{t\ge 0})$

is referred to as the control law, and

$(\pi,L)\,:\!=\,(\{\pi_t\}_{t\ge 0},\{L_t\}_{t\ge 0})$

is referred to as the control law, and

$X^{\pi,L}\,:\!=\,\{X_t^{\pi,L}\}_{t\ge 0}$

is called the controlled state process.

$X^{\pi,L}\,:\!=\,\{X_t^{\pi,L}\}_{t\ge 0}$

is called the controlled state process.

The formulation above describes a controlled stochastic process commonly used in financial modeling, inventory control, and reservoir management. The state variable

$X^{\pi,L}_t$

can represent the capital or reserves in a company, inventory levels, or water in a reservoir. The control variable

$X^{\pi,L}_t$

can represent the capital or reserves in a company, inventory levels, or water in a reservoir. The control variable

$\pi_t$

might represent risk exposure or business scale in problems such as consumption, cash withdrawal, or dividends distribution; the proportion of resources allocated to inventory replenishment; or the proportion of inflow directed to storage, among other interpretations. The variable

$\pi_t$

might represent risk exposure or business scale in problems such as consumption, cash withdrawal, or dividends distribution; the proportion of resources allocated to inventory replenishment; or the proportion of inflow directed to storage, among other interpretations. The variable

$L_t$

represents the cumulative amount of consumption, cash withdrawal, or dividend payments; non-decreasing adjustments due to external supply, corrections to maintain nonnegativity, or a release process.

$L_t$

represents the cumulative amount of consumption, cash withdrawal, or dividend payments; non-decreasing adjustments due to external supply, corrections to maintain nonnegativity, or a release process.

We formally define admissible control laws as follows.

Definition 1. (Admissible strategies.) Define

$\mathcal{A}$

to be the set of all admissible strategies,

$\mathcal{A}$

to be the set of all admissible strategies,

$(\pi,L)$

, that satisfy the following conditions: (a)

$(\pi,L)$

, that satisfy the following conditions: (a)

$(\pi,L)$

is

$(\pi,L)$

is

$\mathcal{F}^W$

-predictable; (b)

$\mathcal{F}^W$

-predictable; (b)

$\pi_t\in[0,1]$

; (c) L is everywhere right-continuous and has left limits everywhere (cádlág); and (d)

$\pi_t\in[0,1]$

; (c) L is everywhere right-continuous and has left limits everywhere (cádlág); and (d)

$L_{0-}=0$

, L is non-decreasing and

$L_{0-}=0$

, L is non-decreasing and

$L_t-L_{t-}\le X^{\pi,L}_{t-}$

.

$L_t-L_{t-}\le X^{\pi,L}_{t-}$

.

Item (a) indicates that decisions at any time t depend solely on historical information before time t and item (b) states that the decision-maker can adjust the business scale or exposure ratio anywhere between 0% and 100%. Item (c) implies that if there is a lump sum withdrawal at time t, this amount is treated as a deduction at time

$t-$

, which reduces the state level immediately before time t. Finally, item (d) specifies that all withdrawals must be non-negative, and the amount of each withdrawal cannot exceed the available quantity at the time of withdrawal. In other words, withdrawals cannot directly result in a deficit.

$t-$

, which reduces the state level immediately before time t. Finally, item (d) specifies that all withdrawals must be non-negative, and the amount of each withdrawal cannot exceed the available quantity at the time of withdrawal. In other words, withdrawals cannot directly result in a deficit.

We quantify the performance of the control law,

$(\pi,L)$

, by the expected total discounted value

$(\pi,L)$

, by the expected total discounted value

\begin{align}\mathcal{P}(\pi,L)(x)={\mathrm{E}}_x\bigg[\int_0^{\tau^{\pi,L}}\mathrm{e}^{-\delta t}\,{\mathrm{d}} L_t\bigg],\end{align}

\begin{align}\mathcal{P}(\pi,L)(x)={\mathrm{E}}_x\bigg[\int_0^{\tau^{\pi,L}}\mathrm{e}^{-\delta t}\,{\mathrm{d}} L_t\bigg],\end{align}

where

${\mathrm{E}}_x$

represents the conditional expectation given

${\mathrm{E}}_x$

represents the conditional expectation given

$X_{0-}=x$

:

$X_{0-}=x$

:

\begin{align}{\mathrm{E}}_x[\!\cdot\!]={\mathrm{E}}[\!\cdot\!|X_{0-}=x],\end{align}

\begin{align}{\mathrm{E}}_x[\!\cdot\!]={\mathrm{E}}[\!\cdot\!|X_{0-}=x],\end{align}

and

$\delta>0$

is the discount rate used by the decision maker, reflecting their intertemporal preferences.

$\delta>0$

is the discount rate used by the decision maker, reflecting their intertemporal preferences.

The optimal control problem. The objective of the control problem is to maximize the performance functional

\begin{align}\mathcal{P}(\pi,L)(x) ={\mathrm{E}}_x\bigg[\int_0^{\tau^{\pi,L}}\mathrm{e}^{-\delta t}\,{\mathrm{d}} L_t\bigg],\end{align}

\begin{align}\mathcal{P}(\pi,L)(x) ={\mathrm{E}}_x\bigg[\int_0^{\tau^{\pi,L}}\mathrm{e}^{-\delta t}\,{\mathrm{d}} L_t\bigg],\end{align}

over all admissible strategies

$(\pi,L)\in\mathcal{A}$

, that is,

$(\pi,L)\in\mathcal{A}$

, that is,

\begin{align}V(x)\,:\!=\,\sup\nolimits_{(\pi,L)\in\mathcal{A}}{\mathrm{E}}_x\bigg[\int_0^{\tau^{\pi,L}}\mathrm{e}^{-\delta t}\,{\mathrm{d}} L_t\bigg],\end{align}

\begin{align}V(x)\,:\!=\,\sup\nolimits_{(\pi,L)\in\mathcal{A}}{\mathrm{E}}_x\bigg[\int_0^{\tau^{\pi,L}}\mathrm{e}^{-\delta t}\,{\mathrm{d}} L_t\bigg],\end{align}

subject to the system dynamics in (1) and the constraints imposed on admissible strategies as outlined in Definition 1. We refer to V as the value function. The value function, depending on the application context, can represent the maximum discounted profit, the maximum benefit, or the maximum utility of water release (e.g. for electricity generation or irrigation).

If there exists a control law, say

$(\pi^*, L^*)$

, from the set of admissible strategies that attains the maximal performance, i.e.

$(\pi^*, L^*)$

, from the set of admissible strategies that attains the maximal performance, i.e.

\begin{align}\mathcal{P}(\pi^*,L^*)(x)=\sup\nolimits_{(\pi,L)\in\mathcal{A}}{\mathrm{E}}_x\bigg[\int_0^{\tau^{\pi,L}}\mathrm{e}^{-\delta t} \, {\mathrm{d}} L_t\bigg],\end{align}

\begin{align}\mathcal{P}(\pi^*,L^*)(x)=\sup\nolimits_{(\pi,L)\in\mathcal{A}}{\mathrm{E}}_x\bigg[\int_0^{\tau^{\pi,L}}\mathrm{e}^{-\delta t} \, {\mathrm{d}} L_t\bigg],\end{align}

then

$(\pi^*, L^*)$

is the optimal control law.

$(\pi^*, L^*)$

is the optimal control law.

The model underlying the control problem discussed above is quite general. It includes the widely studied Brownian motion model, where

$\mu(\!\cdot\!)=\mathrm{constant}$

and

$\mu(\!\cdot\!)=\mathrm{constant}$

and

$\sigma(\!\cdot\!)=\mathrm{ constant}$

, as well as the less commonly explored extension, the Ornstein–Uhlenbeck process. The latter corresponds to

$\sigma(\!\cdot\!)=\mathrm{ constant}$

, as well as the less commonly explored extension, the Ornstein–Uhlenbeck process. The latter corresponds to

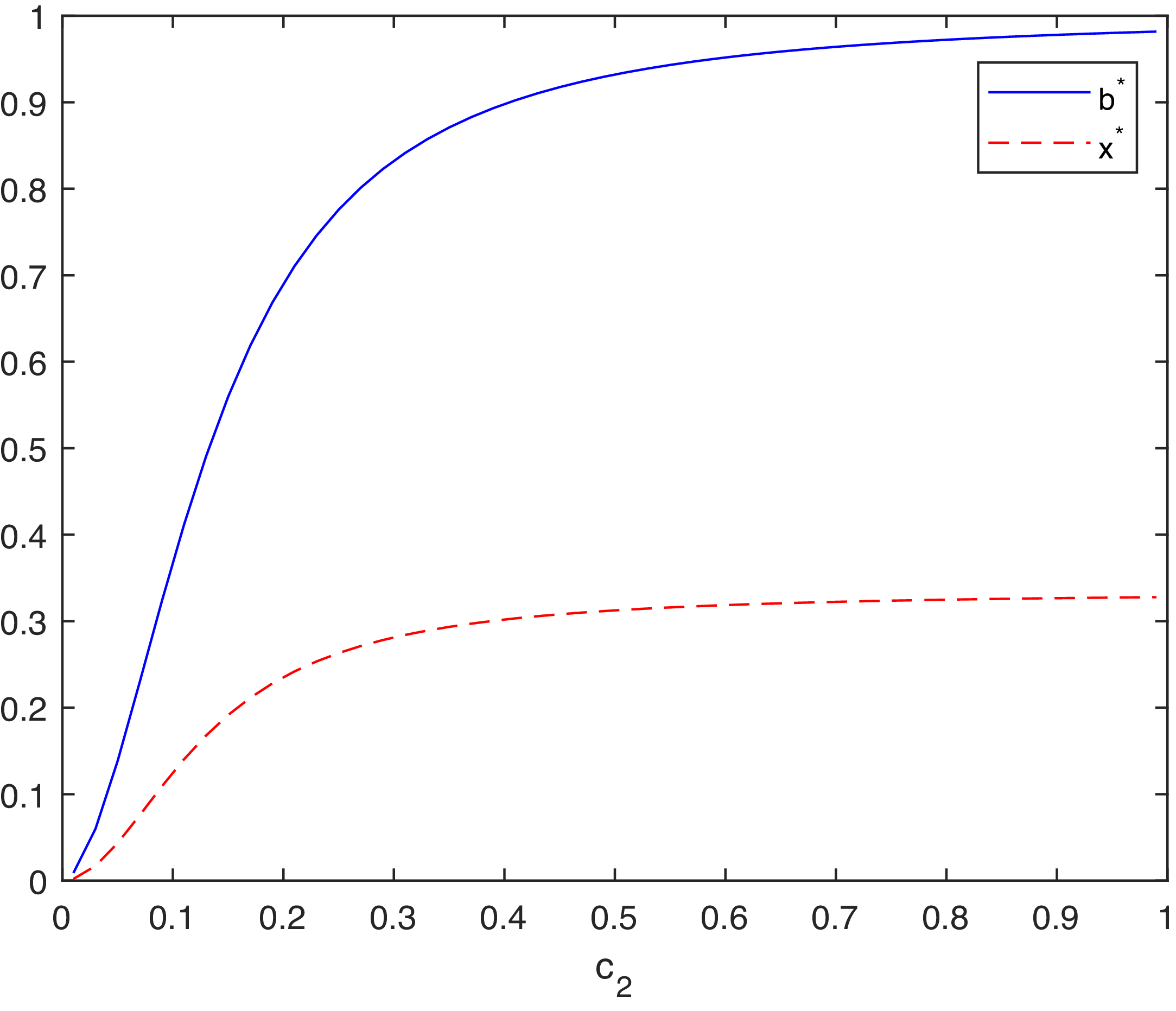

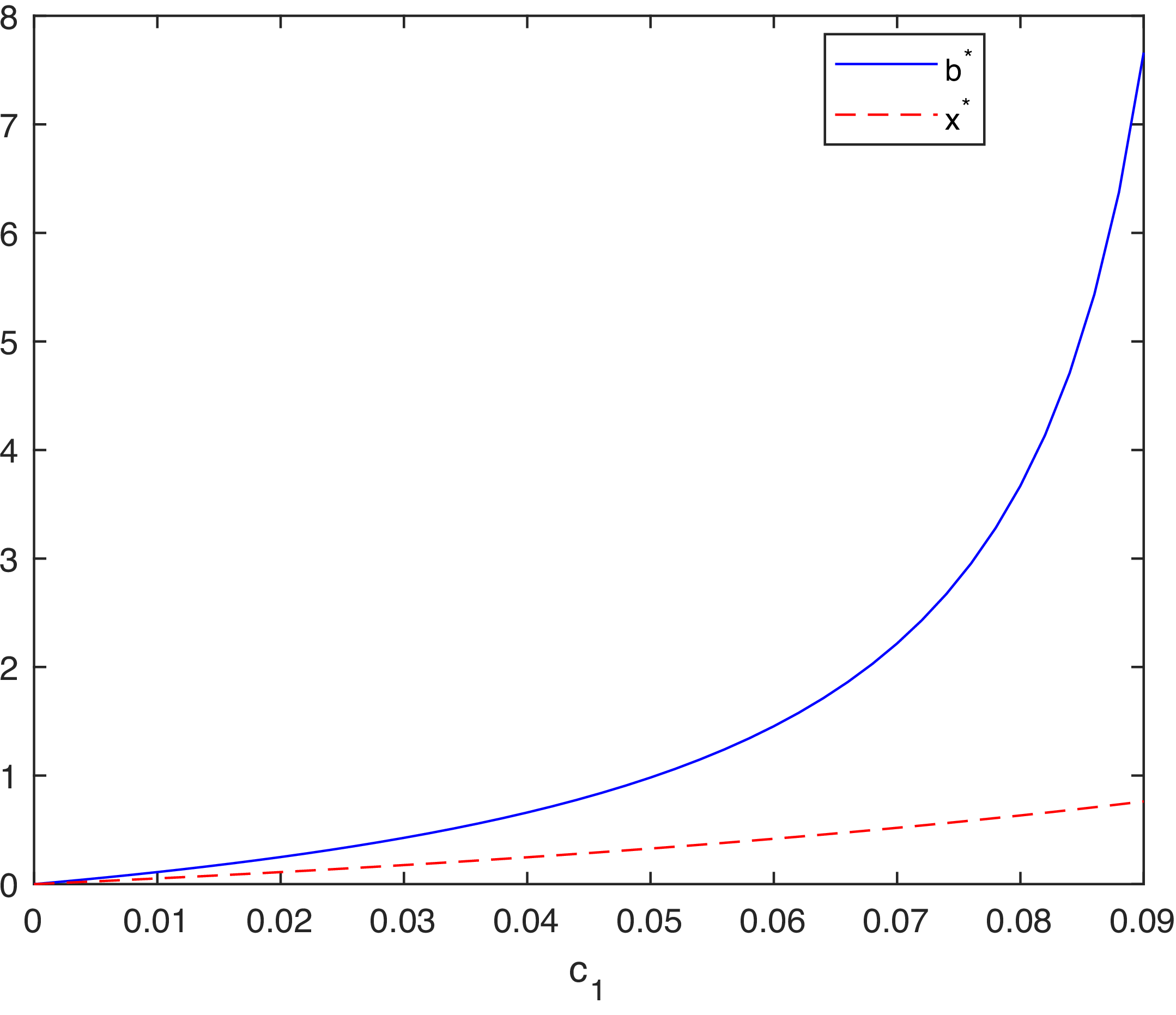

$\mu(x)=c_1 x+c_2$

for two constants

$\mu(x)=c_1 x+c_2$

for two constants

$c_1$

and

$c_1$

and

$c_2$

, which can represent more realistic dynamics in certain areas, e.g. finance and insurance, where cash reserves generate interest.

$c_2$

, which can represent more realistic dynamics in certain areas, e.g. finance and insurance, where cash reserves generate interest.

Following standard arguments in optimal control (see, for instance, [Reference Yong and Zhou30]), we derive the following HJB equation:

\begin{align}\max\left\{ \max_{a\in[0,1]}\left(\frac{1}{2}\sigma^{2}(x) a^{2}\,f^{\prime\prime}(x)+\mu(x) a\,f^\prime(x)-\delta\,f(x)\right)\!, 1-f^\prime(x)\right\}\le 0.\end{align}

\begin{align}\max\left\{ \max_{a\in[0,1]}\left(\frac{1}{2}\sigma^{2}(x) a^{2}\,f^{\prime\prime}(x)+\mu(x) a\,f^\prime(x)-\delta\,f(x)\right)\!, 1-f^\prime(x)\right\}\le 0.\end{align}

Intuitively, if the value function is sufficiently smooth, it should satisfy the above HJB equation with a corresponding to the risk exposure control

$\pi$

. Note that given

$\pi$

. Note that given

$X_{0-}=0$

, ruin occurs immediately, i.e.

$X_{0-}=0$

, ruin occurs immediately, i.e.

$ \tau^{\pi,L}=0$

conditional on

$ \tau^{\pi,L}=0$

conditional on

$X_{0-}=0$

. As a result, we have

$X_{0-}=0$

. As a result, we have

\begin{align}V(0)=\sup\nolimits_{(\pi,L)\in\mathcal{A}}{\mathrm{E}}_0\bigg[\int_0^{\tau^{\pi,L}}\mathrm{e}^{-\delta t}\,{\mathrm{d}} L_t\bigg]=0.\end{align}

\begin{align}V(0)=\sup\nolimits_{(\pi,L)\in\mathcal{A}}{\mathrm{E}}_0\bigg[\int_0^{\tau^{\pi,L}}\mathrm{e}^{-\delta t}\,{\mathrm{d}} L_t\bigg]=0.\end{align}

We conjecture that if V is sufficiently smooth, a heuristic conclusion would be that it solves the HJB equation. This motivates us to study the solution (if any) to the following initial value problem first. Applying a standard method in optimal control by using Itô lemma we can obtain the following verification theorem.

Theorem 1. (Verification theorem.) If f is a twice continuously differentiable function that satisfies:

then

$f(x)\ge V(x)$

for

$f(x)\ge V(x)$

for

$x\ge 0$

.

$x\ge 0$

.

In light of the above verification theorem, it is natural to first inquire whether such a function as described in the theorem exists. We attempt to answer this by searching for candidate solutions to the initial value HJB equation:

\begin{align} &\max\left\{ \max_{a\in[0,1]}\left(\frac{1}{2}\sigma^{2}(x) a^{2}\,f^{\prime\prime}(x)+\mu(x) a\,f^\prime(x)-\delta\,f(x)\right)\!, 1-f^\prime(x)\right\}=0, \quad& x> 0, \end{align}

\begin{align} &\max\left\{ \max_{a\in[0,1]}\left(\frac{1}{2}\sigma^{2}(x) a^{2}\,f^{\prime\prime}(x)+\mu(x) a\,f^\prime(x)-\delta\,f(x)\right)\!, 1-f^\prime(x)\right\}=0, \quad& x> 0, \end{align}

\begin{align} &f(0)=0.\end{align}

\begin{align} &f(0)=0.\end{align}

A special case where both

$\mu(x)$

and

$\mu(x)$

and

$\sigma(x)$

are constants has been solved in [Reference Højgaard and Taksar14], who studied an optimal reinsurance and dividend problem for a Brownian motion with a constant positive drift and a constant diffusion coefficient. This leads to the same mathematical problem as the special case discussed here. Further variations of the problem under the Brownian motion framework (with constant drifts and volatilities, in absence of control) have been considered in [Reference Asmussen, Højgaard and Taksar3, Reference Bai, Guo and Zhang4, Reference Cadenillas, Choulli, Taksar and Zhang6, Reference Choulli, Taksar and Zhou9–Reference Choulli, Taksar and Zhou11, Reference Højgaard and Taksar15, Reference Liang and Young17, Reference Meng and Siu18, Reference Taksar25, Reference Taksar and Zhou26], among others.

$\sigma(x)$

are constants has been solved in [Reference Højgaard and Taksar14], who studied an optimal reinsurance and dividend problem for a Brownian motion with a constant positive drift and a constant diffusion coefficient. This leads to the same mathematical problem as the special case discussed here. Further variations of the problem under the Brownian motion framework (with constant drifts and volatilities, in absence of control) have been considered in [Reference Asmussen, Højgaard and Taksar3, Reference Bai, Guo and Zhang4, Reference Cadenillas, Choulli, Taksar and Zhang6, Reference Choulli, Taksar and Zhou9–Reference Choulli, Taksar and Zhou11, Reference Højgaard and Taksar15, Reference Liang and Young17, Reference Meng and Siu18, Reference Taksar25, Reference Taksar and Zhou26], among others.

We distinguish among three cases, (a)

$\mu(x)>0$

for all

$\mu(x)>0$

for all

$x\ge 0$

, (b)

$x\ge 0$

, (b)

$\mu(0)\le 0$

, and (c)

$\mu(0)\le 0$

, and (c)

$\mu(0)>0$

and

$\mu(0)>0$

and

$\mu(x) \le 0$

for some

$\mu(x) \le 0$

for some

$x>0$

, and analyze them separately. In our analysis, we also impose the following condition on the drift coefficient function.

$x>0$

, and analyze them separately. In our analysis, we also impose the following condition on the drift coefficient function.

Assumption 1. We assume

$\mu^\prime(x) < \delta$

.

$\mu^\prime(x) < \delta$

.

This assumption is introduced for mathematical tractability and is also considered natural in financial modeling, as discussed in [Reference Paulsen19] and also due to the fact that in the context of profit testing, the subjective discount rate

$\delta$

used to value future cash flows by the shareholders typically exceeds the growth rate (the force of growth) of a risk business,

$\delta$

used to value future cash flows by the shareholders typically exceeds the growth rate (the force of growth) of a risk business,

$\mu'$

, by a risk margin.

$\mu'$

, by a risk margin.

3. Optimality results when

$\boldsymbol\mu(\boldsymbol{x}) > 0$

for all

$\boldsymbol{x} \ge 0$

$\boldsymbol\mu(\boldsymbol{x}) > 0$

for all

$\boldsymbol{x} \ge 0$

We consider the case

$\mu(x)>0$

for all

$\mu(x)>0$

for all

$x\ge 0$

throughout the whole section. We start with constructing a strictly increasing and strictly concave solution to

$x\ge 0$

throughout the whole section. We start with constructing a strictly increasing and strictly concave solution to

\begin{align}&\max_{a\in[0,1]}\left(\frac{1}{2}a^2\sigma^2(x)\,f^{\prime\prime}(x)+\mu(x) a\,f^\prime(x)-\delta\,f(x)\right)=0,\quad\mbox{for $x\in (0,x_{1}]$},\quad f(0)=0, \end{align}

\begin{align}&\max_{a\in[0,1]}\left(\frac{1}{2}a^2\sigma^2(x)\,f^{\prime\prime}(x)+\mu(x) a\,f^\prime(x)-\delta\,f(x)\right)=0,\quad\mbox{for $x\in (0,x_{1}]$},\quad f(0)=0, \end{align}

where

$x_1$

is a positive constant that is determined later. Suppose the desired solution exists, denoted by f(x) here. Noting that this function, f, is strictly concave, we have

$x_1$

is a positive constant that is determined later. Suppose the desired solution exists, denoted by f(x) here. Noting that this function, f, is strictly concave, we have

$f^{\prime\prime}(x)<0$

for

$f^{\prime\prime}(x)<0$

for

$x\in (0,x_1]$

and thus we can see

$x\in (0,x_1]$

and thus we can see

\begin{align*}\arg\max_a\left(\frac{1}{2}a^{2}\sigma^{2}(x)\,f^{\prime\prime}(x)+\mu(x) a\,f^\prime(x)-\delta\,f(x))\right)=-\frac{\mu(x)}{\sigma^{2}(x)} \frac{ f^\prime(x)}{f^{\prime\prime}(x)},\quad x\in(0,x_1].\end{align*}

\begin{align*}\arg\max_a\left(\frac{1}{2}a^{2}\sigma^{2}(x)\,f^{\prime\prime}(x)+\mu(x) a\,f^\prime(x)-\delta\,f(x))\right)=-\frac{\mu(x)}{\sigma^{2}(x)} \frac{ f^\prime(x)}{f^{\prime\prime}(x)},\quad x\in(0,x_1].\end{align*}

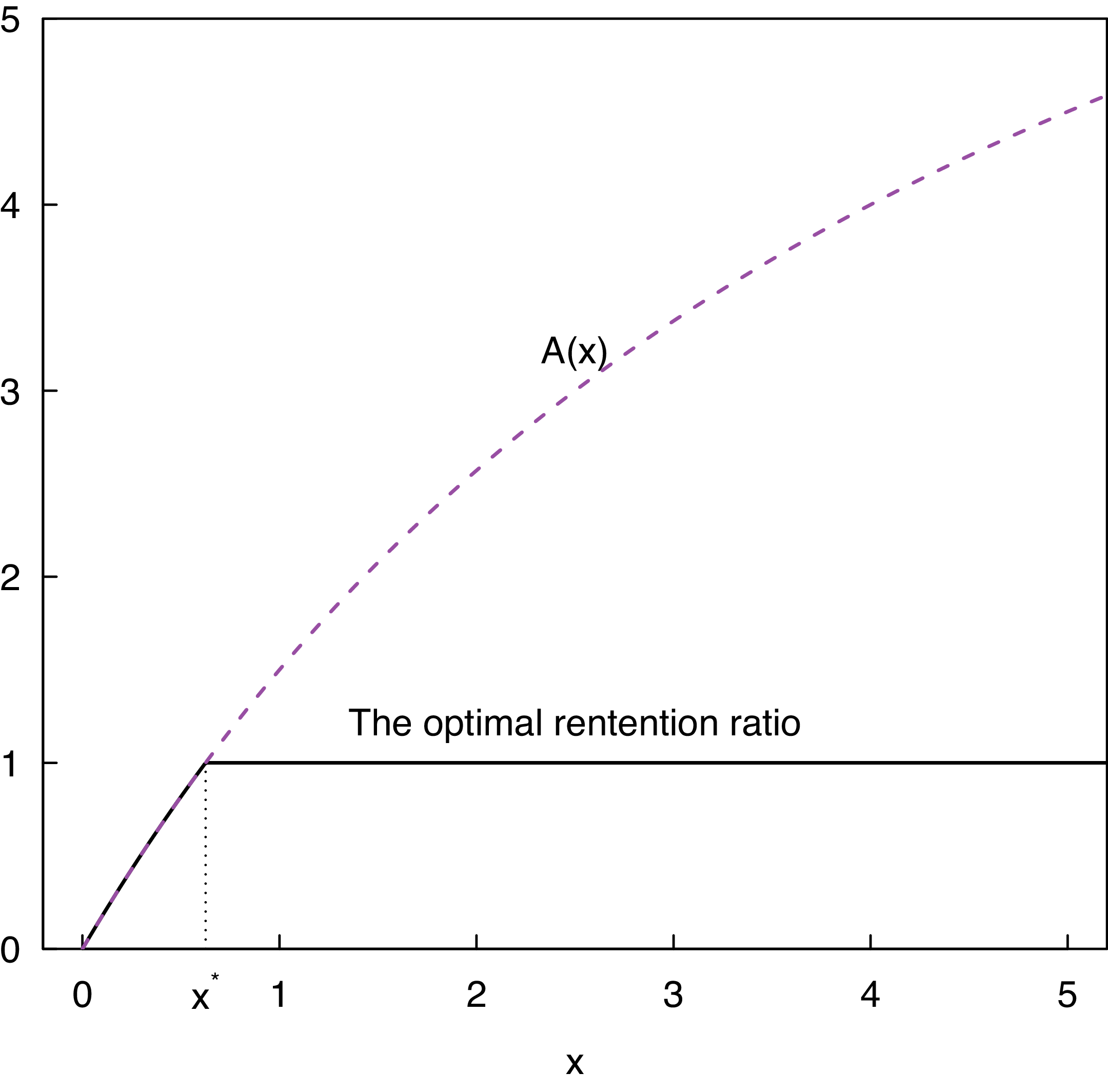

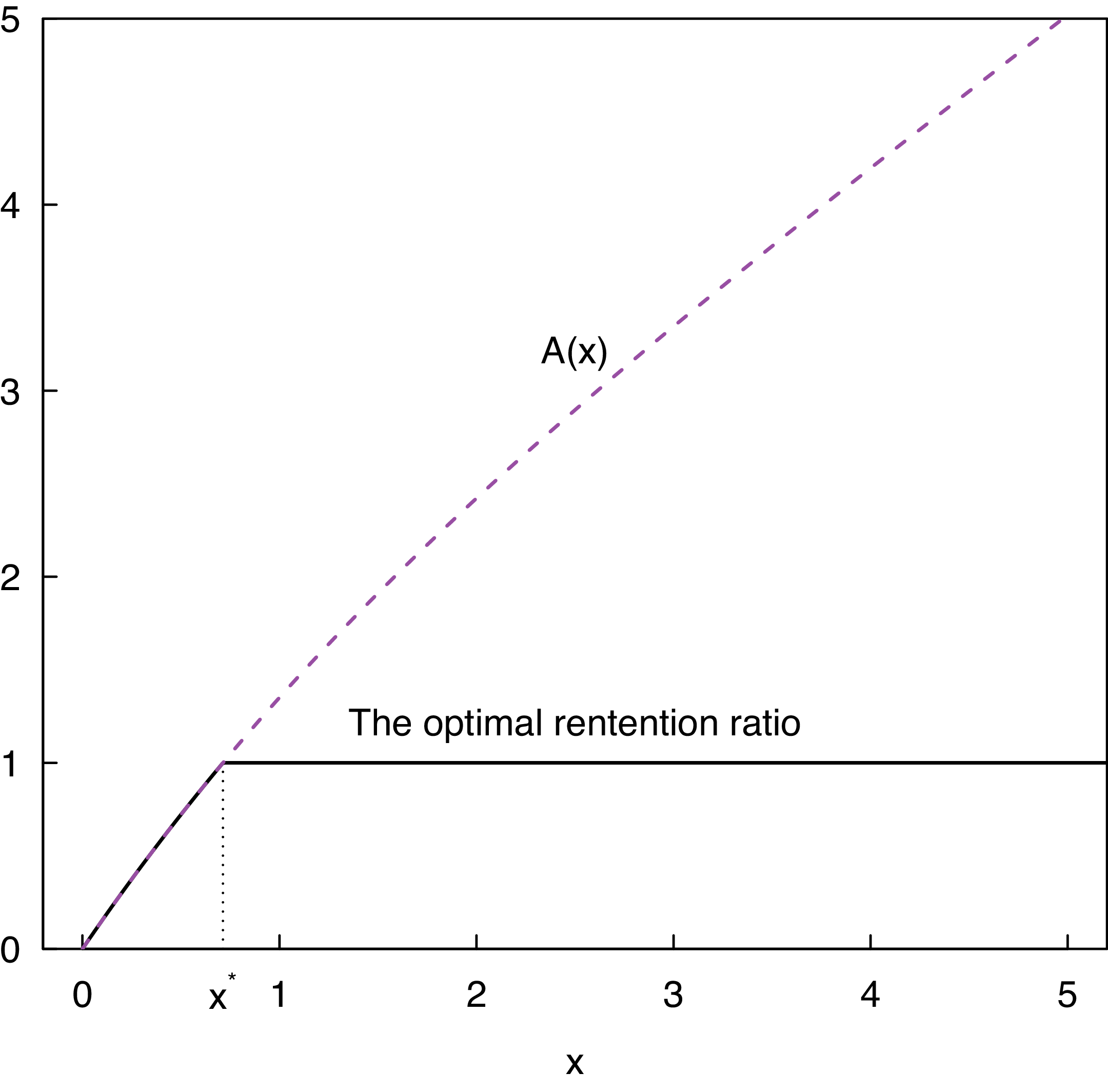

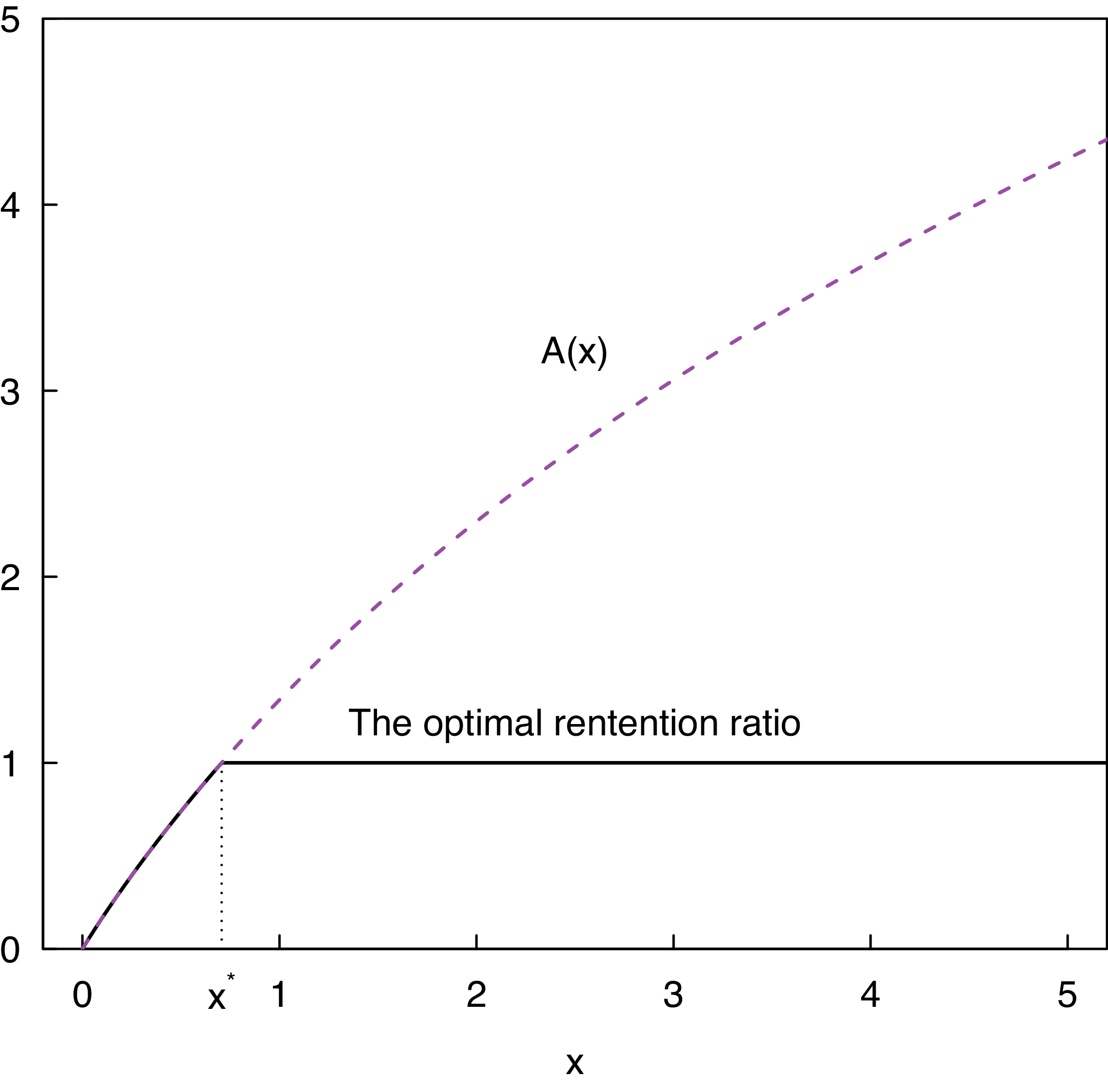

Define

\begin{align}a_{f}(x)=-\frac{\mu(x)}{\sigma^{2}(x)} \frac{ f^\prime(x)}{f^{\prime\prime}(x)}.\end{align}

\begin{align}a_{f}(x)=-\frac{\mu(x)}{\sigma^{2}(x)} \frac{ f^\prime(x)}{f^{\prime\prime}(x)}.\end{align}

Suppose there exists an

$x_{1}>0$

such that

$x_{1}>0$

such that

$a_f(x)\in[0,1]$

for

$a_f(x)\in[0,1]$

for

$x\in[0,x_1]$

(the existence of such

$x\in[0,x_1]$

(the existence of such

$x_1$

will be verified later after we obtain a candidate expression for the desired f(x)). Then,

$x_1$

will be verified later after we obtain a candidate expression for the desired f(x)). Then,

\begin{align}\arg\max_{a\in[0,1]}\left(\frac{1}{2}a^{2}\sigma^{2}(x)\,f^{\prime\prime}(x)+\mu(x) a\,f^\prime(x)-\delta\,f(x)\right)=a_{f}(x), \quad x\in (0,x_{1}].\end{align}

\begin{align}\arg\max_{a\in[0,1]}\left(\frac{1}{2}a^{2}\sigma^{2}(x)\,f^{\prime\prime}(x)+\mu(x) a\,f^\prime(x)-\delta\,f(x)\right)=a_{f}(x), \quad x\in (0,x_{1}].\end{align}

Thus, by combining (15) with the assumption that f is a solution to (13) we obtain

\begin{align}\frac{1}{2}a_{f}^{2}(x)\sigma^{2}(x)\,f^{\prime\prime}(x)+\mu(x) a_{f}(x)\,f^\prime(x)-\delta\,f(x)=0,\quad x\in (0,x_{1}].\end{align}

\begin{align}\frac{1}{2}a_{f}^{2}(x)\sigma^{2}(x)\,f^{\prime\prime}(x)+\mu(x) a_{f}(x)\,f^\prime(x)-\delta\,f(x)=0,\quad x\in (0,x_{1}].\end{align}

From (14), we have

\begin{align}\sigma^{2}(x)\,f^{\prime\prime}(x)=-\frac{\mu(x)\,f^\prime(x)}{a_{f}(x)}.\end{align}

\begin{align}\sigma^{2}(x)\,f^{\prime\prime}(x)=-\frac{\mu(x)\,f^\prime(x)}{a_{f}(x)}.\end{align}

Substituting (17) into (16) yields

\begin{align}\frac{1}{2}a_{f}(x)\mu(x)\,f^\prime(x)-\delta\,f(x)=0, \quad x\in (0,x_{1}].\end{align}

\begin{align}\frac{1}{2}a_{f}(x)\mu(x)\,f^\prime(x)-\delta\,f(x)=0, \quad x\in (0,x_{1}].\end{align}

Differentiating (18) with respect to x gives

\begin{align}\frac{1}{2}a_{f}(x)\mu(x)\,f^{\prime\prime}(x)+\left(\frac{1}{2}\mu^\prime(x)a_{f}(x)+\frac12\mu(x)a_{f}^\prime(x)-\delta\right)\!f^\prime(x)=0, \quad x\in (0,x_{1}].\end{align}

\begin{align}\frac{1}{2}a_{f}(x)\mu(x)\,f^{\prime\prime}(x)+\left(\frac{1}{2}\mu^\prime(x)a_{f}(x)+\frac12\mu(x)a_{f}^\prime(x)-\delta\right)\!f^\prime(x)=0, \quad x\in (0,x_{1}].\end{align}

From (17) we get

$$a_{f}(x)\,f^{\prime\prime}(x)=-\frac{\mu(x)\,f^\prime(x)}{\sigma^{2}(x)}.$$

$$a_{f}(x)\,f^{\prime\prime}(x)=-\frac{\mu(x)\,f^\prime(x)}{\sigma^{2}(x)}.$$

By substituting this into (19) we get

\begin{align}\left(-\frac{1}{2}\frac{\mu^{2}(x)}{\sigma^{2}(x)}+\frac{1}{2}\mu^\prime(x)a_{f}(x)+\frac{1}{2}\mu(x)a_{f}^\prime(x)-\delta\right)\!f^\prime(x)=0, \quad x\in (0,x_{1}].\end{align}

\begin{align}\left(-\frac{1}{2}\frac{\mu^{2}(x)}{\sigma^{2}(x)}+\frac{1}{2}\mu^\prime(x)a_{f}(x)+\frac{1}{2}\mu(x)a_{f}^\prime(x)-\delta\right)\!f^\prime(x)=0, \quad x\in (0,x_{1}].\end{align}

Recall that f is strictly increasing on

$[0,x_1]$

and so we know

$[0,x_1]$

and so we know

$f^\prime(x)>0 $

for

$f^\prime(x)>0 $

for

$x\in (0,x_1]$

. Thus, it follows from (20) that

$x\in (0,x_1]$

. Thus, it follows from (20) that

$$-\frac{1}{2}\frac{\mu^{2}(x)}{\sigma^{2}(x)}+\frac{1}{2}\mu^\prime(x)a_{f}(x)+\frac{1}{2}\mu(x)a_{f}^\prime(x)-\delta=0, \quad x\in (0,x_{1}],$$

$$-\frac{1}{2}\frac{\mu^{2}(x)}{\sigma^{2}(x)}+\frac{1}{2}\mu^\prime(x)a_{f}(x)+\frac{1}{2}\mu(x)a_{f}^\prime(x)-\delta=0, \quad x\in (0,x_{1}],$$

which implies

$$\mu^\prime(x)a_{f}(x)+\mu(x)a_{f}^\prime(x)=2\delta+\frac{\mu^{2}(x)}{\sigma^{2}(x)},\quad \mbox{for $0< x\leq x_{1}$.}$$

$$\mu^\prime(x)a_{f}(x)+\mu(x)a_{f}^\prime(x)=2\delta+\frac{\mu^{2}(x)}{\sigma^{2}(x)},\quad \mbox{for $0< x\leq x_{1}$.}$$

That is,

$$\frac{\mathrm{d}(\mu(x)a_f(x))}{\mathrm{d} x}=2\delta+\frac{\mu^{2}(x)}{\sigma^{2}(x)}\quad \mbox{for $0< x\le x_1$.}$$

$$\frac{\mathrm{d}(\mu(x)a_f(x))}{\mathrm{d} x}=2\delta+\frac{\mu^{2}(x)}{\sigma^{2}(x)}\quad \mbox{for $0< x\le x_1$.}$$

Solving this differential equation gives

\begin{align}a_{f}(x)=\frac{1}{\mu(x)}\bigg[\int_{0}^{x}\bigg(2\delta+\frac{\mu^{2}(y)}{\sigma^{2}(y)}\bigg)\mathrm{d} y+\mu(0)a_f(0)\bigg], \quad x\in[0, x_{1}].\end{align}

\begin{align}a_{f}(x)=\frac{1}{\mu(x)}\bigg[\int_{0}^{x}\bigg(2\delta+\frac{\mu^{2}(y)}{\sigma^{2}(y)}\bigg)\mathrm{d} y+\mu(0)a_f(0)\bigg], \quad x\in[0, x_{1}].\end{align}

From (17) we know

$$\frac{f^{\prime\prime}(x)}{f^\prime(x)}=-\frac{\mu(x)}{\sigma^{2}(x)a_{f}(x)}.$$

$$\frac{f^{\prime\prime}(x)}{f^\prime(x)}=-\frac{\mu(x)}{\sigma^{2}(x)a_{f}(x)}.$$

By solving this equation we have

\begin{align}f(x)=C_{1}-C_{2}\int_{x}^{x_1}\exp\!\bigg({\int_{z}^{x_1}\frac{\mu(y)}{\sigma^{2}(y)a_{f}(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z, \quad x\in(0, x_{1}].\end{align}

\begin{align}f(x)=C_{1}-C_{2}\int_{x}^{x_1}\exp\!\bigg({\int_{z}^{x_1}\frac{\mu(y)}{\sigma^{2}(y)a_{f}(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z, \quad x\in(0, x_{1}].\end{align}

Since we want

$f(0)=0$

and so

$f(0)=0$

and so

$$C_{1}=C_{2}\int_{0}^{x_1}\exp\!\bigg({\int_{z}^{x_1}\frac{\mu(y)}{\sigma^{2}(y)a_{f}(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z$$

$$C_{1}=C_{2}\int_{0}^{x_1}\exp\!\bigg({\int_{z}^{x_1}\frac{\mu(y)}{\sigma^{2}(y)a_{f}(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z$$

and thus

\begin{align}f(x)=C_{2}\int_{0}^{x}\exp\!\bigg({\int_{z}^{x_1}\frac{\mu(y)}{\sigma^{2}(y)a_{f}(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z,\quad x\in(0, x_{1}].\end{align}

\begin{align}f(x)=C_{2}\int_{0}^{x}\exp\!\bigg({\int_{z}^{x_1}\frac{\mu(y)}{\sigma^{2}(y)a_{f}(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z,\quad x\in(0, x_{1}].\end{align}

It follows from (18) that

$\frac{1}{2}\mu(0)a_{f}(0)\,f^\prime(0+)-\delta\,f(0)=0$

. Note that

$\frac{1}{2}\mu(0)a_{f}(0)\,f^\prime(0+)-\delta\,f(0)=0$

. Note that

$f(0)=0$

,

$f(0)=0$

,

$\mu(0)>0$

, and

$\mu(0)>0$

, and

$f^\prime(0+)>0$

(as f is strictly increasing on

$f^\prime(0+)>0$

(as f is strictly increasing on

$[0,x_1]$

). Therefore, we have

$[0,x_1]$

). Therefore, we have

$\frac{1}{2}\mu(0)a_{f}(0)\,f^\prime(0+)=0$

, and thus

$\frac{1}{2}\mu(0)a_{f}(0)\,f^\prime(0+)=0$

, and thus

\begin{align}a_{f}(0)=0,\end{align}

\begin{align}a_{f}(0)=0,\end{align}

which along with (21) implies

\begin{align}a_{f}(x)=\frac{\int_{0}^{x}\left(2\delta+\frac{\mu^{2}(y)}{\sigma^{2}(y)}\right)\!\mathrm{d} y}{\mu(x)}, \quad x\in[0, x_{1}].\end{align}

\begin{align}a_{f}(x)=\frac{\int_{0}^{x}\left(2\delta+\frac{\mu^{2}(y)}{\sigma^{2}(y)}\right)\!\mathrm{d} y}{\mu(x)}, \quad x\in[0, x_{1}].\end{align}

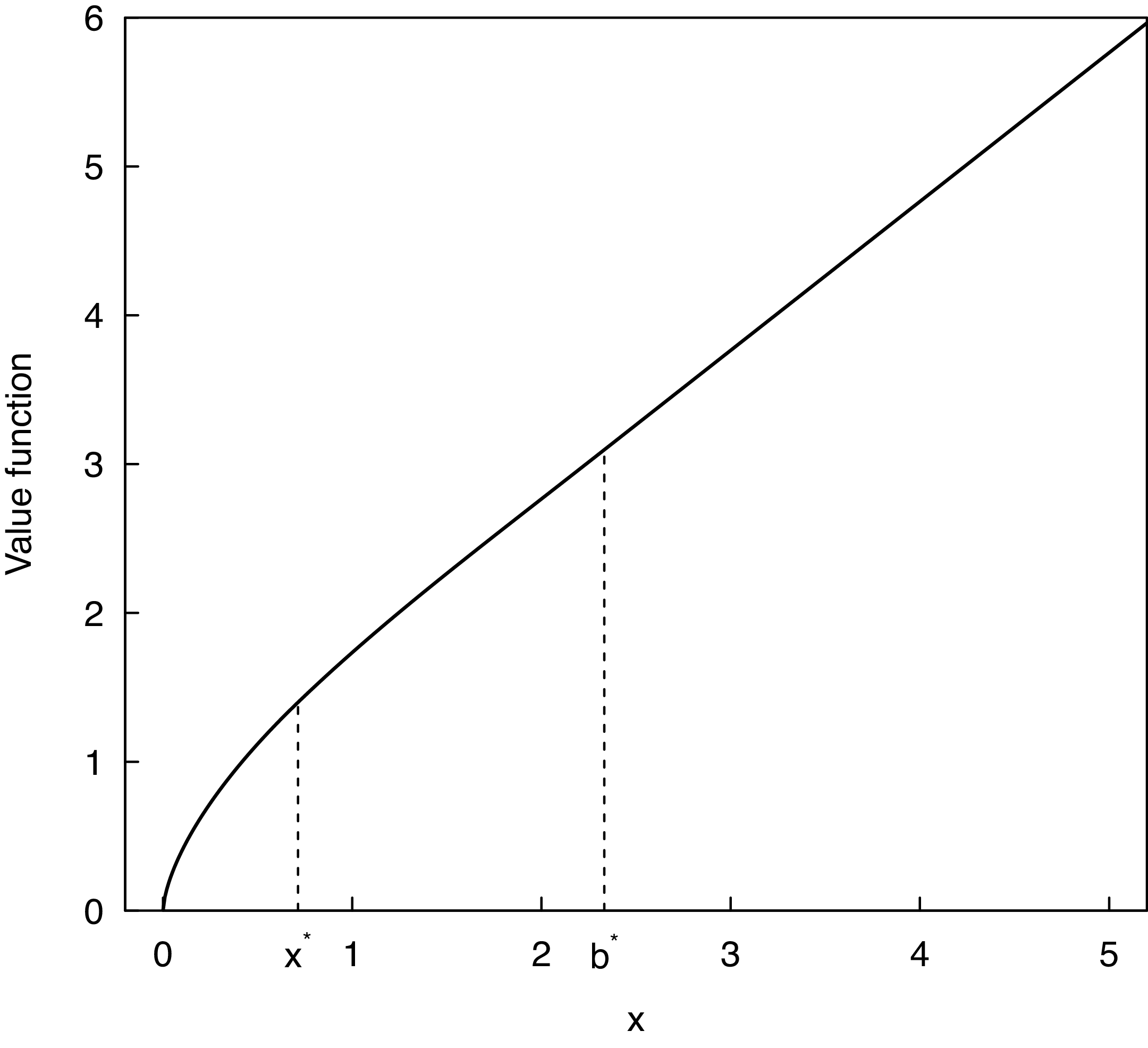

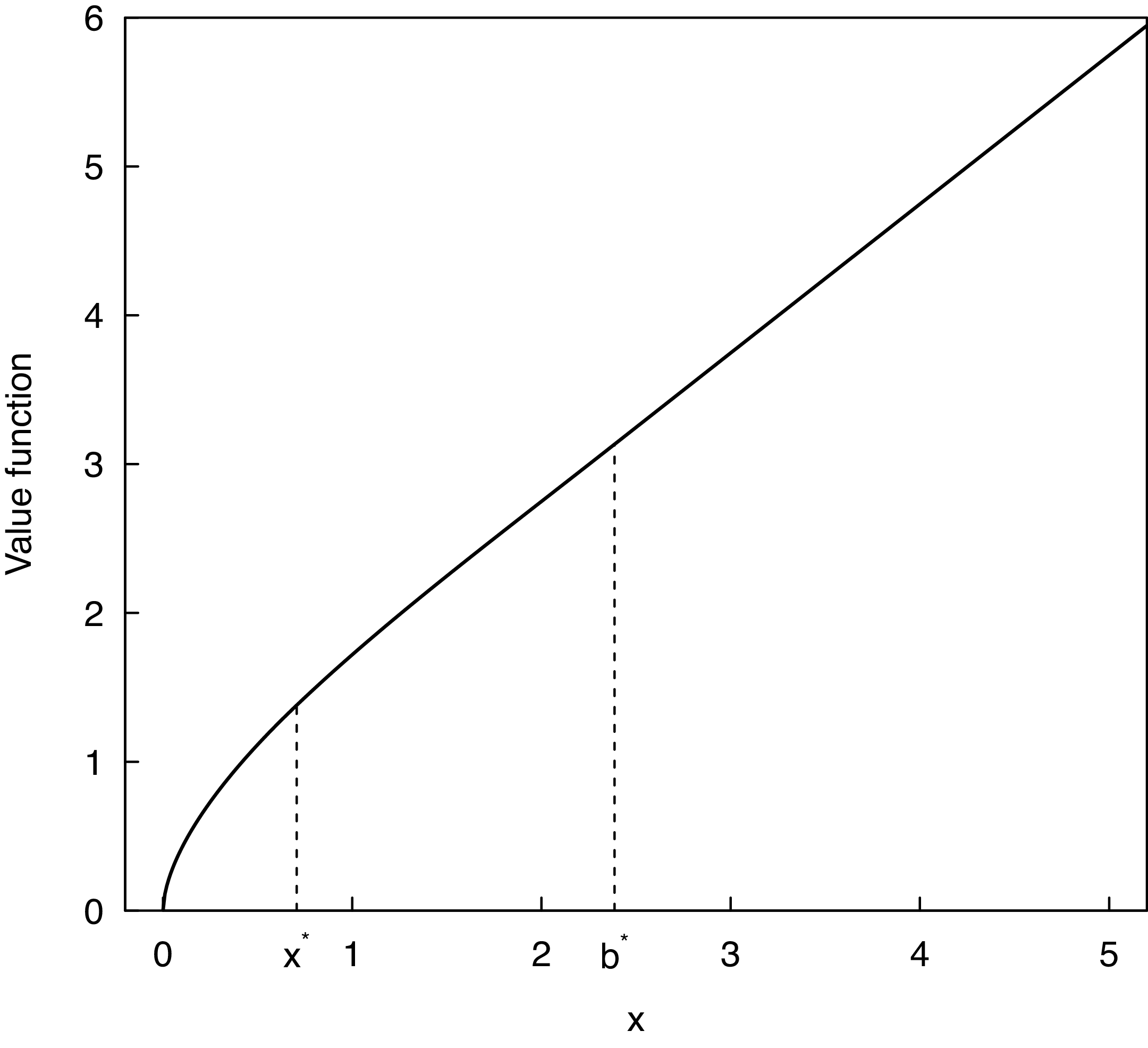

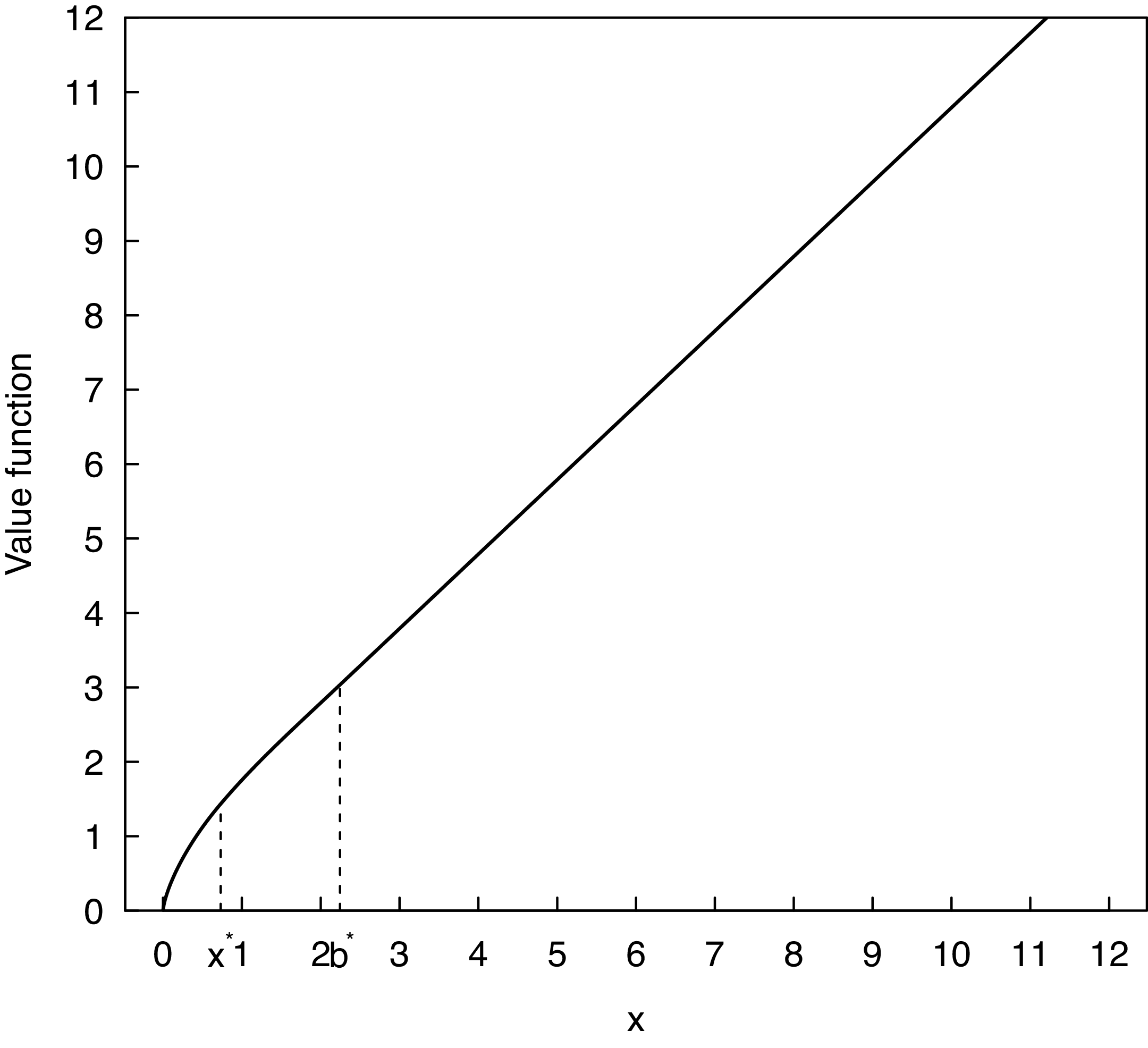

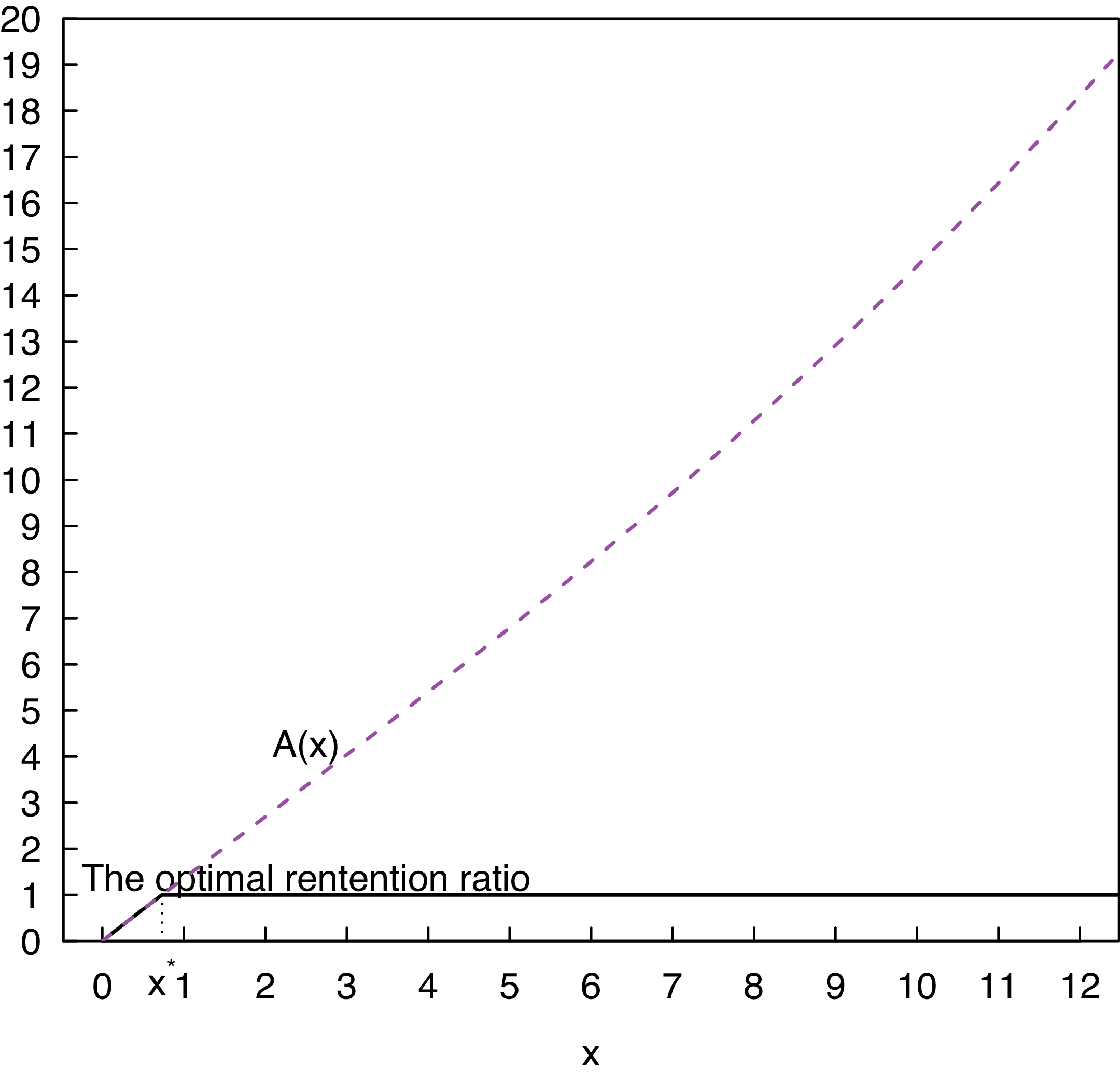

Before we proceed with further derivation, let us define two quantities.

Notation 2. Define the following function and quantity:

Those quantities possess the following properties.

Lemma 1. Let A(x) and

$x^*$

be defined in (26), respectively. The function A(x) is increasing on

$x^*$

be defined in (26), respectively. The function A(x) is increasing on

$[0,x^*]$

and the following hold:

$[0,x^*]$

and the following hold:

\begin{align}&0 < x^{*}< \frac{\mu(0)}{\delta}, \end{align}

\begin{align}&0 < x^{*}< \frac{\mu(0)}{\delta}, \end{align}

\begin{align}&0\leq A(x)\leq 1,\quad x\in[0,x^{*}],\end{align}

\begin{align}&0\leq A(x)\leq 1,\quad x\in[0,x^{*}],\end{align}

\begin{align}&A(0)=0,\quad A(x^*)=1.\end{align}

\begin{align}&A(0)=0,\quad A(x^*)=1.\end{align}

Now let us resume our analysis on the desired solution to (11) and (12) for

$x\in [0, x^*]$

. From the above analysis we can see that for the candidate solution f given in (23),

$x\in [0, x^*]$

. From the above analysis we can see that for the candidate solution f given in (23),

$a_f(x)=A(x)\in[0, 1]$

for

$a_f(x)=A(x)\in[0, 1]$

for

$0\le x\le x^*$

. Thus, we have

$0\le x\le x^*$

. Thus, we have

$x_1=x^*$

. Thus, by (23), (25), and (26) it follows that

$x_1=x^*$

. Thus, by (23), (25), and (26) it follows that

\begin{align}f(x)=C_{2}\int_{0}^{x}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z, \quad x\in[0, x^*].\end{align}

\begin{align}f(x)=C_{2}\int_{0}^{x}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z, \quad x\in[0, x^*].\end{align}

Note that A(x) is increasing and

$A(0)=0$

. Thus,

$A(0)=0$

. Thus,

$ \int_{z}^{x^*}({\mu(y)}/{\sigma^{2}(y)A(y)})\mathrm{d} y$

is finite for any fixed

$ \int_{z}^{x^*}({\mu(y)}/{\sigma^{2}(y)A(y)})\mathrm{d} y$

is finite for any fixed

$z>0$

. However, as z approaches zero, this integral may diverge to infinity. Therefore, ensuring the well-definedness of f in (30), which is equivalent to the well-definedness of the integral

$z>0$

. However, as z approaches zero, this integral may diverge to infinity. Therefore, ensuring the well-definedness of f in (30), which is equivalent to the well-definedness of the integral

$$ \int_{0}^{x}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z, $$

$$ \int_{0}^{x}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z, $$

becomes crucial. This important aspect has been established in Lemma 9 in the Appendix.

From the previous derivation we know that f defined in (30) satisfies the following equation:

\begin{align}\frac{1}{2}\sigma^{2}(x)A^2(x)\,f^{\prime\prime}(x)+\mu(x) A(x)\,f^\prime(x)-\delta\,f(x)=0,\quad x\in (0,x^*].\end{align}

\begin{align}\frac{1}{2}\sigma^{2}(x)A^2(x)\,f^{\prime\prime}(x)+\mu(x) A(x)\,f^\prime(x)-\delta\,f(x)=0,\quad x\in (0,x^*].\end{align}

Furthermore, it follows directly from (22) that for any strictly negative

$C_2$

,

$C_2$

,

\begin{align}f^{\prime\prime}(x)< 0, \quad x\in[0, x^*]. \end{align}

\begin{align}f^{\prime\prime}(x)< 0, \quad x\in[0, x^*]. \end{align}

We show later that f(x) defined in (30) with

$C_2$

being a positive constant is indeed the strictly increasing and strictly concave solution to (13) on

$C_2$

being a positive constant is indeed the strictly increasing and strictly concave solution to (13) on

$[0,x^{*}]$

.

$[0,x^{*}]$

.

We now proceed to construct an increasing and concave solution to (13) for

$x\in (x^*,b]$

, where b (

$x\in (x^*,b]$

, where b (

$b>x^*$

) is a constant to be specified later. We conjecture that if f is such solution then

$b>x^*$

) is a constant to be specified later. We conjecture that if f is such solution then

$a_f(x)\ge 1$

for

$a_f(x)\ge 1$

for

$x\in [x^*,b)$

. Based on this conjecture we can show that

$x\in [x^*,b)$

. Based on this conjecture we can show that

$${\max_{a\in[0,1]}}\left(\frac{1}{2}\sigma^{2}(x) a^{2}\,f^{\prime\prime}(x)+\mu(x) a\,f^\prime(x)-\delta\,f(x)\right)=\frac{1}{2}\sigma^{2}(x)\,f^{\prime\prime}(x)+\mu(x)\,f^\prime(x)-\delta\,f(x)$$

$${\max_{a\in[0,1]}}\left(\frac{1}{2}\sigma^{2}(x) a^{2}\,f^{\prime\prime}(x)+\mu(x) a\,f^\prime(x)-\delta\,f(x)\right)=\frac{1}{2}\sigma^{2}(x)\,f^{\prime\prime}(x)+\mu(x)\,f^\prime(x)-\delta\,f(x)$$

for

$x\in [x^*,b)$

. We start by defining two functions.

$x\in [x^*,b)$

. We start by defining two functions.

Notation 3. Let

$g_{1}$

and

$g_{1}$

and

$g_{2}$

denote the unique solutions to the equation

$g_{2}$

denote the unique solutions to the equation

\begin{align}\frac{1}{2}\sigma^{2}(x)g^{\prime\prime}(x)+\mu(x)g^\prime(x)-\delta g(x)=0, \quad x > x^*, \end{align}

\begin{align}\frac{1}{2}\sigma^{2}(x)g^{\prime\prime}(x)+\mu(x)g^\prime(x)-\delta g(x)=0, \quad x > x^*, \end{align}

respectively, with the following two sets of initial values:

\begin{align}g_{1}(x^{*})&=0, \quad g_{1}^\prime (x^{*})=1,\end{align}

\begin{align}g_{1}(x^{*})&=0, \quad g_{1}^\prime (x^{*})=1,\end{align}

\begin{align}g_{2}(x^{*})&=1, \quad g_{2}^\prime (x^{*})=0.\end{align}

\begin{align}g_{2}(x^{*})&=1, \quad g_{2}^\prime (x^{*})=0.\end{align}

The existence and uniqueness of

$g_1$

and

$g_1$

and

$g_2$

to the initial value problems are proven in Theorem 5.4.2 of [Reference Krylov16]. Due to the continuity of

$g_2$

to the initial value problems are proven in Theorem 5.4.2 of [Reference Krylov16]. Due to the continuity of

$\mu(\!\cdot\!)$

and

$\mu(\!\cdot\!)$

and

$\sigma(\!\cdot\!)$

, it is not hard to see that

$\sigma(\!\cdot\!)$

, it is not hard to see that

$g_1^{\prime\prime}$

and

$g_1^{\prime\prime}$

and

$g_2^{\prime\prime}$

are continuous.

$g_2^{\prime\prime}$

are continuous.

We can see that

$g_{1}$

and

$g_{1}$

and

$g_{2}$

form a set of fundamental solutions to (33) and therefore, the function defined below is a general solution to (33),

$g_{2}$

form a set of fundamental solutions to (33) and therefore, the function defined below is a general solution to (33),

\begin{align}g(x)=C_{4}g_{1}(x)+C_{5}g_{2}(x), \quad x\geq x^{*},\end{align}

\begin{align}g(x)=C_{4}g_{1}(x)+C_{5}g_{2}(x), \quad x\geq x^{*},\end{align}

where

$C_{4}$

and

$C_{4}$

and

$C_{5}$

are constants. Let f be the function specified in (30). We now determine

$C_{5}$

are constants. Let f be the function specified in (30). We now determine

$C_{2}$

,

$C_{2}$

,

$C_{4}$

, and

$C_{4}$

, and

$C_{5}$

by letting

$C_{5}$

by letting

$f(x^{*})=g(x^{*})$

,

$f(x^{*})=g(x^{*})$

,

$f^\prime(x^{*})=g^\prime(x^{*})$

, and

$f^\prime(x^{*})=g^\prime(x^{*})$

, and

$g^\prime(b)=1$

, where b (

$g^\prime(b)=1$

, where b (

$b\ge x^{*})$

is a constant to be specified later. These equations amount to

$b\ge x^{*})$

is a constant to be specified later. These equations amount to

\begin{align*}&C_{2}\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^{*}}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z=C_{4}g_{1}(x^{*})+C_{5}g_{2}(x^{*})=C_{5},\\&C_{2}=C_{4}g^\prime_{1}(x^{*})+C_{5}g^\prime_{2}(x^{*}) =C_{4}, \quad C_{4}g^\prime_{1}(b)+C_{5}g^\prime_{2}(b)=1.\end{align*}

\begin{align*}&C_{2}\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^{*}}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z=C_{4}g_{1}(x^{*})+C_{5}g_{2}(x^{*})=C_{5},\\&C_{2}=C_{4}g^\prime_{1}(x^{*})+C_{5}g^\prime_{2}(x^{*}) =C_{4}, \quad C_{4}g^\prime_{1}(b)+C_{5}g^\prime_{2}(b)=1.\end{align*}

We can see that for any

$b>x^{*}$

,

$b>x^{*}$

,

$C_{2}$

,

$C_{2}$

,

$C_{4}$

, and

$C_{4}$

, and

$C_{5}$

fulfilling the above equations, denoted by

$C_{5}$

fulfilling the above equations, denoted by

$C_{2}(b)$

,

$C_{2}(b)$

,

$C_{4}(b)$

, and

$C_{4}(b)$

, and

$C_{5}(b)$

here, have the following representations:

$C_{5}(b)$

here, have the following representations:

\begin{align}&C_5(b)=\frac{\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^{*}}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z}{g_1^\prime(b)+g_2^\prime(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^{*}}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z},\end{align}

\begin{align}&C_5(b)=\frac{\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^{*}}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z}{g_1^\prime(b)+g_2^\prime(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^{*}}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z},\end{align}

\begin{align}&C_2(b)=C_4(b)=\frac{1}{g_1^\prime(b)+g_2^\prime(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^{*}}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z}.\end{align}

\begin{align}&C_2(b)=C_4(b)=\frac{1}{g_1^\prime(b)+g_2^\prime(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^{*}}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z}.\end{align}

As discussed earlier,

$$\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^{*}}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z$$

$$\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^{*}}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z$$

is well defined and finite and so are

$C_2(b)$

,

$C_2(b)$

,

$C_4(b)$

, and

$C_4(b)$

, and

$C_5(b)$

.

$C_5(b)$

.

We extend the definitions of

$C_2(b)$

,

$C_2(b)$

,

$C_4(b)$

, and

$C_4(b)$

, and

$C_5(b)$

to

$C_5(b)$

to

$b=x^*$

by using the same expressions above. Then,

$b=x^*$

by using the same expressions above. Then,

\begin{align}C_2(x^*)=\lim_{b\downarrow x^*} C_2(b),\quad C_4(x^*)=\lim_{b\downarrow x^*}C_4(b), \quad C_5(x^*)=\lim_{b\downarrow x^*}C_5(b).\end{align}

\begin{align}C_2(x^*)=\lim_{b\downarrow x^*} C_2(b),\quad C_4(x^*)=\lim_{b\downarrow x^*}C_4(b), \quad C_5(x^*)=\lim_{b\downarrow x^*}C_5(b).\end{align}

The following properties for

$g_1$

,

$g_1$

,

$g_2$

, and

$g_2$

, and

$C_2(\!\cdot\!)$

,

$C_2(\!\cdot\!)$

,

$C_4(\!\cdot\!)$

, and

$C_4(\!\cdot\!)$

, and

$C_5(\!\cdot\!)$

can be derived (and are proved in the Appendix), and they prove useful in the subsequent analysis.

$C_5(\!\cdot\!)$

can be derived (and are proved in the Appendix), and they prove useful in the subsequent analysis.

Lemma 2. (i) We have

$g_1^\prime(x)>0$

and

$g_1^\prime(x)>0$

and

$g_2^\prime(x)\ge 0$

for

$g_2^\prime(x)\ge 0$

for

$x\ge x^*$

.

$x\ge x^*$

.

(ii) Let

$C_2(b)$

,

$C_2(b)$

,

$C_4(b)$

and

$C_4(b)$

and

$C_5(b)$

be specified in (37)–(39), respectively, for

$C_5(b)$

be specified in (37)–(39), respectively, for

$b\ge x^*$

, and A(x) and

$b\ge x^*$

, and A(x) and

$x^*$

be defined in (26), respectively. For any

$x^*$

be defined in (26), respectively. For any

$b\ge x^*$

, all

$b\ge x^*$

, all

$C_2(b)$

,

$C_2(b)$

,

$C_4(b)$

, and

$C_4(b)$

, and

$C_5(b)$

are strictly positive.

$C_5(b)$

are strictly positive.

For any

$b\ge x^*$

, now write

$b\ge x^*$

, now write

\begin{align}f_{b}(x)&=C_{2}(b)\int_{0}^{x}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu^{2}(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z,\quad {x}\in[0, x^*],\end{align}

\begin{align}f_{b}(x)&=C_{2}(b)\int_{0}^{x}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu^{2}(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z,\quad {x}\in[0, x^*],\end{align}

\begin{align}g_{b}(x)&=C_{4}(b)g_{1}(x)+C_{5}(b)g_{2}(x), \quad {x}\in[x^*,\infty).\end{align}

\begin{align}g_{b}(x)&=C_{4}(b)g_{1}(x)+C_{5}(b)g_{2}(x), \quad {x}\in[x^*,\infty).\end{align}

From the above derivation we know that

$g_{b}$

is a solution to (33) on

$g_{b}$

is a solution to (33) on

$[ x^{*},+\infty)$

and satisfies

$[ x^{*},+\infty)$

and satisfies

\begin{eqnarray} g_{b}^\prime(b)=1, \quad f_{b}(x^*)=g_{b}(x^*), \quad \mbox{and} \quad f_{b}^\prime(x^*-\!)=g_{b}^\prime(x^*+).\end{eqnarray}

\begin{eqnarray} g_{b}^\prime(b)=1, \quad f_{b}(x^*)=g_{b}(x^*), \quad \mbox{and} \quad f_{b}^\prime(x^*-\!)=g_{b}^\prime(x^*+).\end{eqnarray}

Thus,

\begin{align}g_{ b}^{\prime\prime}(x^{*}+)= \frac{2 (\delta g_{b}(x^{*})-\mu(x^{*})g_{b}^\prime(x^{*}+))}{\sigma^{2}(x^{*})}= \frac{2 (\delta g_{b}(x^{*})-\mu(x^{*})A(x^{*})g_{b}^\prime(x^{*}+))}{A^{2}(x^{*})\sigma^{2}(x^{*})},\end{align}

\begin{align}g_{ b}^{\prime\prime}(x^{*}+)= \frac{2 (\delta g_{b}(x^{*})-\mu(x^{*})g_{b}^\prime(x^{*}+))}{\sigma^{2}(x^{*})}= \frac{2 (\delta g_{b}(x^{*})-\mu(x^{*})A(x^{*})g_{b}^\prime(x^{*}+))}{A^{2}(x^{*})\sigma^{2}(x^{*})},\end{align}

where the last equality follows from noting

$A(x^*)=1$

(by Lemma 1). From previous derivations we know that

$A(x^*)=1$

(by Lemma 1). From previous derivations we know that

$f_b(x)$

is a solution to (31) and, thus,

$f_b(x)$

is a solution to (31) and, thus,

\begin{align}f_{b}^{\prime\prime}(x^{*}-\!)= \frac{2 (\delta\,f_{b}(x^{*})-\mu(x^{*})A(x^{*})\,f_{b}^\prime(x^{*}-\!))}{A^{2}(x^{*})\sigma^{2}(x^{*})}=g_{b}^{\prime\prime}(x^{*}+),\end{align}

\begin{align}f_{b}^{\prime\prime}(x^{*}-\!)= \frac{2 (\delta\,f_{b}(x^{*})-\mu(x^{*})A(x^{*})\,f_{b}^\prime(x^{*}-\!))}{A^{2}(x^{*})\sigma^{2}(x^{*})}=g_{b}^{\prime\prime}(x^{*}+),\end{align}

where the last equality follows from (43).

For any

$b>x^*$

, define

$b>x^*$

, define

\begin{align}v_{ b}(x)\,:\!=\,\begin{cases}f_{ b}(x)\,:\!=\,C_{2}( b)\int_{0}^{x}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z \quad& x\in[0, x^{*}),\\g_{ b}(x)\,:\!=\,C_{4}( b)g_{1}(x)+C_{5}( b)g_{2}(x)&x\in[x^{*},b],\\v_{ b}(b)+x-b& x\in(b,\infty).\end{cases}\end{align}

\begin{align}v_{ b}(x)\,:\!=\,\begin{cases}f_{ b}(x)\,:\!=\,C_{2}( b)\int_{0}^{x}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z \quad& x\in[0, x^{*}),\\g_{ b}(x)\,:\!=\,C_{4}( b)g_{1}(x)+C_{5}( b)g_{2}(x)&x\in[x^{*},b],\\v_{ b}(b)+x-b& x\in(b,\infty).\end{cases}\end{align}

Define

\begin{align}{\mathcal L}_{g}(a,x)=\frac{1}{2}\sigma^{2}(x) a^{2}g^{\prime\prime}(x)+\mu(x) a g^\prime(x)-\delta g(x). \end{align}

\begin{align}{\mathcal L}_{g}(a,x)=\frac{1}{2}\sigma^{2}(x) a^{2}g^{\prime\prime}(x)+\mu(x) a g^\prime(x)-\delta g(x). \end{align}

The following properties for

$v_b$

will prove useful.

$v_b$

will prove useful.

Theorem 2. Let A(x) and

$x^{*}$

be defined in (26), respectively. Let

$x^{*}$

be defined in (26), respectively. Let

$v_{ b}(x)$

be defined in (45). For any

$v_{ b}(x)$

be defined in (45). For any

$b>x^*$

:

$b>x^*$

:

-

(i) the function

$v_{ b}(x)$

is continuously differentiable on

$[0,+\infty)$

and twice continuously differentiable except at the point,

$x=b$

,

$v_{ b}^\prime(x)>0$

for

$x\ge 0$

and

$v_{ b}^\prime(b)=1$

; -

(ii)

$v_{ b}^{\prime\prime}(x)<0$

and

$\max_{a\in[0,1]}{\mathcal L}_{v_{ b}}(a,x)={\mathcal L}_{v_{ b}}(A(x),x)=0$

for

$x\in[0,x^{*}]$

; -

(iii)

${\mathcal L}_{v_{ b}}(1,x)=0$

for

$x\in( x^*, b)$

; -

(iv) if

$v_{ b}^{\prime\prime}(b-\!)\le 0$

then

$v_{ b}^{\prime\prime}(x)\le 0$

and

$\max_{a\in[0,1]}{\mathcal L}_{v_{ b}}(a,x)={\mathcal L}_{v_{ b}}(1,x)=0$

for

$x\in( x^*, b)$

.

Theorem 3. Let

$A(\!\cdot\!)$

and

$A(\!\cdot\!)$

and

$x^*$

be defined as in Notation 2. For

$x^*$

be defined as in Notation 2. For

$b>x^*$

, define the pair:

$b>x^*$

, define the pair:

$(\pi^*,L^b) =\{(\pi^*_t,L^b_t);\;t\ge 0\}$

where

$(\pi^*,L^b) =\{(\pi^*_t,L^b_t);\;t\ge 0\}$

where

$$\pi^*_t=\begin{cases}A(X^{\pi^*,L^b}_{t-}),&0\le X^{\pi^*,L^b}_{t-}\le x^*,\\1, & X^{\pi^*,L^b}_{t-}>x^*,\end{cases}$$

$$\pi^*_t=\begin{cases}A(X^{\pi^*,L^b}_{t-}),&0\le X^{\pi^*,L^b}_{t-}\le x^*,\\1, & X^{\pi^*,L^b}_{t-}>x^*,\end{cases}$$

and

$L^b_t$

is the function which causes the controlled process to be reflected downward at the boundary b (that is,

$L^b_t$

is the function which causes the controlled process to be reflected downward at the boundary b (that is,

$L^b$

is the policy that withdraws all storage in excess of b as and keeps the controlled process reflected at b). Let

$L^b$

is the policy that withdraws all storage in excess of b as and keeps the controlled process reflected at b). Let

$v_b(x)$

be defined in (45). For any

$v_b(x)$

be defined in (45). For any

$b>x^*$

,

$b>x^*$

,

$v_b(x)=\mathcal{P}(\pi^*,L^b)(x)$

for

$v_b(x)=\mathcal{P}(\pi^*,L^b)(x)$

for

$x\ge 0$

.

$x\ge 0$

.

The proof is omitted here, a similar proof procedure can be found in [Reference Yao, Yang and Wang29]. Here,

$X^{\pi^*,L^b}$

is a stochastic process reflected at the upper boundary, b, and

$X^{\pi^*,L^b}$

is a stochastic process reflected at the upper boundary, b, and

$L^b$

is a non-decreasing process, subtracting which from

$L^b$

is a non-decreasing process, subtracting which from

$X^{\pi^*,L^b}$

results in the reflection of

$X^{\pi^*,L^b}$

results in the reflection of

$X^{\pi^*,L^b}$

from b. The existence of the classes of strategy

$X^{\pi^*,L^b}$

from b. The existence of the classes of strategy

$L^b$

has been confirmed in [Reference Shreve, Lehoczky and Gaver24, Section 2] and [Reference Choulli, Taksar and Zhou10, Section 5].

$L^b$

has been confirmed in [Reference Shreve, Lehoczky and Gaver24, Section 2] and [Reference Choulli, Taksar and Zhou10, Section 5].

Notation 4. Let

$g_1$

and

$g_1$

and

$g_2$

be the fundamental solutions defined in Notation 3. Define

$g_2$

be the fundamental solutions defined in Notation 3. Define

\begin{align}\xi(b)&={g^{\prime\prime}_{1}(b)+g^{\prime\prime}_{2}(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z},\quad b\in[x^*,\infty),\end{align}

\begin{align}\xi(b)&={g^{\prime\prime}_{1}(b)+g^{\prime\prime}_{2}(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z},\quad b\in[x^*,\infty),\end{align}

\begin{align}b^{*}&=\inf \{b> x^{*}: \xi(b)\geq0\},\quad \mbox{and}\quad b^{*}= +\infty\ \mbox{if } \xi(b)< 0\ \mbox{for all $b\in[x^{*},\infty)$}.\end{align}

\begin{align}b^{*}&=\inf \{b> x^{*}: \xi(b)\geq0\},\quad \mbox{and}\quad b^{*}= +\infty\ \mbox{if } \xi(b)< 0\ \mbox{for all $b\in[x^{*},\infty)$}.\end{align}

If we differentiate the expression for

$v_b(x)$

(see (45)) twice we can see that the function

$v_b(x)$

(see (45)) twice we can see that the function

$\xi(b)$

basically is

$\xi(b)$

basically is

$$v_b^{\prime\prime}(b-\!)\bigg({g^\prime_{1}(b)+g^\prime_{2}(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^{*}}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z}\bigg).$$

$$v_b^{\prime\prime}(b-\!)\bigg({g^\prime_{1}(b)+g^\prime_{2}(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^{*}}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z}\bigg).$$

As has already been shown in Lemma 2 that

$g_1^\prime>0$

and

$g_1^\prime>0$

and

$g_2^\prime\ge 0$

, then

$g_2^\prime\ge 0$

, then

$\xi(b)\ge 0$

is equivalent to

$\xi(b)\ge 0$

is equivalent to

$ v_b^{\prime\prime}(b-\!)\ge 0$

. Thus,

$ v_b^{\prime\prime}(b-\!)\ge 0$

. Thus,

\begin{align}b^*=\inf \{b> x^{*}\,:\, v_b^{\prime\prime}(b-\!)\geq0 \}.\end{align}

\begin{align}b^*=\inf \{b> x^{*}\,:\, v_b^{\prime\prime}(b-\!)\geq0 \}.\end{align}

Due to the continuity of

$\mu(\!\cdot\!)$

and

$\mu(\!\cdot\!)$

and

$\sigma(\!\cdot\!)$

, we know

$\sigma(\!\cdot\!)$

, we know

$g_1^{\prime\prime}$

and

$g_1^{\prime\prime}$

and

$g_2^{\prime\prime}$

are also continuous and thus

$g_2^{\prime\prime}$

are also continuous and thus

$\xi(b)$

is continuous. Obviously,

$\xi(b)$

is continuous. Obviously,

$b^*$

is greater than or equal to

$b^*$

is greater than or equal to

$x^*$

. We first show in the following that

$x^*$

. We first show in the following that

$b^*$

is strictly greater than

$b^*$

is strictly greater than

$x^*$

.

$x^*$

.

Lemma 3. The following holds:

$b^*>x^*$

.

$b^*>x^*$

.

There is a chance that

$b^*$

is infinitely large. To explore when

$b^*$

is infinitely large. To explore when

$b^*$

is not finite, we first examine the monotonicity and concavity of the two fundamental functions,

$b^*$

is not finite, we first examine the monotonicity and concavity of the two fundamental functions,

$g_1$

and

$g_1$

and

$g_2$

. We can show that for any solution, g, to

$g_2$

. We can show that for any solution, g, to

$({\sigma^2(x)}/{2})g^{\prime\prime}(x)+\mu(x) g^{\prime}(x) -\delta g(x)=0$

, if for some point

$({\sigma^2(x)}/{2})g^{\prime\prime}(x)+\mu(x) g^{\prime}(x) -\delta g(x)=0$

, if for some point

$x_0$

such that

$x_0$

such that

$g^{\prime\prime}(x_0)>0$

and

$g^{\prime\prime}(x_0)>0$

and

$g^\prime (x_0)\ge 0$

, then

$g^\prime (x_0)\ge 0$

, then

\begin{align}g^{\prime\prime}(x)>0,\quad x\in(x_0,\infty).\end{align}

\begin{align}g^{\prime\prime}(x)>0,\quad x\in(x_0,\infty).\end{align}

This can be proven by a proof by contradiction. Suppose the above claim (50) is not true. Considering the continuity of

$g^{\prime\prime}$

, the quantity,

$g^{\prime\prime}$

, the quantity,

$x_1$

, defined by

$x_1$

, defined by

$x_1\;=\!:\;\inf\{x>x_0:g^{\prime\prime}(x)=0\}$

, will be finite with

$x_1\;=\!:\;\inf\{x>x_0:g^{\prime\prime}(x)=0\}$

, will be finite with

\begin{align}g^{\prime\prime}(x_1)=0.\end{align}

\begin{align}g^{\prime\prime}(x_1)=0.\end{align}

We can further see

\begin{align}g^{\prime\prime}(x)>0,\quad x\in (x_0,x_1),\end{align}

\begin{align}g^{\prime\prime}(x)>0,\quad x\in (x_0,x_1),\end{align}

and, as a result,

\begin{align}g^{\prime}(x_1)>g^{\prime}(x_0)\ge 0.\end{align}

\begin{align}g^{\prime}(x_1)>g^{\prime}(x_0)\ge 0.\end{align}

Note

$g^{\prime\prime}(x)= (2/{\sigma^{2}(x)}) (\!-\mu(x) g^\prime(x)+\delta g(x)).$

Hence,

$g^{\prime\prime}(x)= (2/{\sigma^{2}(x)}) (\!-\mu(x) g^\prime(x)+\delta g(x)).$

Hence,

$-\mu(x) g^\prime(x)+\delta g(x)>0$

for

$-\mu(x) g^\prime(x)+\delta g(x)>0$

for

$x\in(x_0,x_1)$

, and

$x\in(x_0,x_1)$

, and

$-\mu(x_1) g^\prime(x_1)+\delta g(x_1)=0.$

As a result,

$-\mu(x_1) g^\prime(x_1)+\delta g(x_1)=0.$

As a result,

$(\!-\mu(x) g^\prime(x)+\delta g(x))-(\!-\mu(x_1) g^\prime(x_1)+\delta g(x_1))>0,\ x\in(x_0,x_1).$

Dividing both sides of the above equation by

$(\!-\mu(x) g^\prime(x)+\delta g(x))-(\!-\mu(x_1) g^\prime(x_1)+\delta g(x_1))>0,\ x\in(x_0,x_1).$

Dividing both sides of the above equation by

$x-x_1$

and then letting

$x-x_1$

and then letting

$x\uparrow x_1$

lead to

$x\uparrow x_1$

lead to

$(\delta-\mu^\prime(x_1) ) g^\prime(x_1)-\mu(x_1)g^{\prime\prime}(x_1)\le 0.$

Noting

$(\delta-\mu^\prime(x_1) ) g^\prime(x_1)-\mu(x_1)g^{\prime\prime}(x_1)\le 0.$

Noting

$g^{\prime\prime}(x_1)=0$

(see (51)), we have

$g^{\prime\prime}(x_1)=0$

(see (51)), we have

$(\delta-\mu^\prime(x_1) ) g^\prime(x_1)\le 0.$

By noting

$(\delta-\mu^\prime(x_1) ) g^\prime(x_1)\le 0.$

By noting

$g^\prime(x_1)>0$

(see (53)), we conclude

$g^\prime(x_1)>0$

(see (53)), we conclude

$\mu^\prime(x_1)\ge \delta$

, which contradicts the condition that

$\mu^\prime(x_1)\ge \delta$

, which contradicts the condition that

$\mu^\prime(x)<\delta$

for

$\mu^\prime(x)<\delta$

for

$x>0$

. This implies that (50) is indeed true.

$x>0$

. This implies that (50) is indeed true.

Note

$$g_2^{\prime\prime}(x^*)=\frac{2(\delta g_2(x^*)-\mu(x^*)g_2^\prime(x^*))}{\sigma^2(x^*)}=\frac{2\delta}{\sigma^2(x^*)}> 0$$

$$g_2^{\prime\prime}(x^*)=\frac{2(\delta g_2(x^*)-\mu(x^*)g_2^\prime(x^*))}{\sigma^2(x^*)}=\frac{2\delta}{\sigma^2(x^*)}> 0$$

and

$g_2^{\prime}(x^*)=0$

, it follows from (50) that

$g_2^{\prime}(x^*)=0$

, it follows from (50) that

\begin{align}g_2^{\prime\prime}(b) > 0,\quad \mbox{for all $b > x^*$}.\end{align}

\begin{align}g_2^{\prime\prime}(b) > 0,\quad \mbox{for all $b > x^*$}.\end{align}

It follows from (49) that

\begin{align}b^*=+\infty\quad \mbox{if and only if } g^{\prime\prime}_{1}(b)<-g^{\prime\prime}_{2}(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z,\quad \mbox{for all $b > x^*$.}\end{align}

\begin{align}b^*=+\infty\quad \mbox{if and only if } g^{\prime\prime}_{1}(b)<-g^{\prime\prime}_{2}(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z,\quad \mbox{for all $b > x^*$.}\end{align}

We now consider the following partition and distinguish two cases:

$$\textrm{(I)}\quad g^{\prime\prime}_{1}(b) +g^{\prime\prime}_{2}(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z\ge 0\quad \mbox{for some $b > x^*$;}$$

$$\textrm{(I)}\quad g^{\prime\prime}_{1}(b) +g^{\prime\prime}_{2}(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z\ge 0\quad \mbox{for some $b > x^*$;}$$

and

$$\textrm{(II)}\quad g^{\prime\prime}_{1}(b)+g^{\prime\prime}_{2}(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z<0\quad \mbox{for all $b > x^*$.}$$

$$\textrm{(II)}\quad g^{\prime\prime}_{1}(b)+g^{\prime\prime}_{2}(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z<0\quad \mbox{for all $b > x^*$.}$$

3.1. Case (I)

We investigate the case where the following condition holds:

$$g^{\prime\prime}_{1}(b) +g^{\prime\prime}_{2}(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z\ge 0\quad \mbox{for some $b > x^*$;}$$

$$g^{\prime\prime}_{1}(b) +g^{\prime\prime}_{2}(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z\ge 0\quad \mbox{for some $b > x^*$;}$$

From the previous discussion we know that in this case,

$x^* < b^* < +\infty$

. We show that in this case the function

$x^* < b^* < +\infty$

. We show that in this case the function

$v_{b^*}$

is a solution to the initial value HJB equation and therefore equals the value function. By using Theorem 2 and the definition of

$v_{b^*}$

is a solution to the initial value HJB equation and therefore equals the value function. By using Theorem 2 and the definition of

$b^*$

, we can obtain the following results for

$b^*$

, we can obtain the following results for

$v_{b^*}(x)$

, which are crucial for deriving the optimality results.

$v_{b^*}(x)$

, which are crucial for deriving the optimality results.

Lemma 4. Assume

Let A(x),

$x^{*}$

, and

$x^{*}$

, and

${b^*}$

be defined in (26) and (48), respectively. Let

${b^*}$

be defined in (26) and (48), respectively. Let

$v_{b^*}(x)$

be defined in (45). Then:

$v_{b^*}(x)$

be defined in (45). Then:

-

(i)

$v_{b^*}(x)$

is twice continuously differentiable,

$v^\prime_{b^*}(x)>0$

for

$x\ge 0$

, and

$v_{b^*}^{\prime\prime}(x)\le 0$

for

$x\ge 0$

; -

(ii)

$\max_{a\in[0,1]}{\mathcal L}_{v_{b^*}}(a,x)={\mathcal L}_{v_{b^*}}(A(x),x)=0$

for

$x\in[0,x^{*}]$

; -

(iii)

$\max_{a\in[0,1]}{\mathcal L}_{v_{b^*}}(a,x)={\mathcal L}_{v_{b^*}}(1,x)=0$

for

$x\in(x^{*},b^*]$

; and -

(iv)

$\max_{a\in[0,1]}{\mathcal L}_{v_{b^*}}(a,x)={\mathcal L}_{v_{b^*}}(1,x)\le 0$

for

$x\in(b^*,\infty)$

.

Consequently, we can derive the following optimality results.

Theorem 4. Let A(x),

$x^{*}$

,

$x^{*}$

,

${b^*}$

, and

${b^*}$

, and

$C_2(\!\cdot\!)-C_5(\!\cdot\!)$

be defined in (26), (48), and (37)–(38), respectively. Suppose

$C_2(\!\cdot\!)-C_5(\!\cdot\!)$

be defined in (26), (48), and (37)–(38), respectively. Suppose

${b^*}<+\infty$

and let

${b^*}<+\infty$

and let

$v_{b^*}(x)$

be defined in (45). Then,

$v_{b^*}(x)$

be defined in (45). Then,

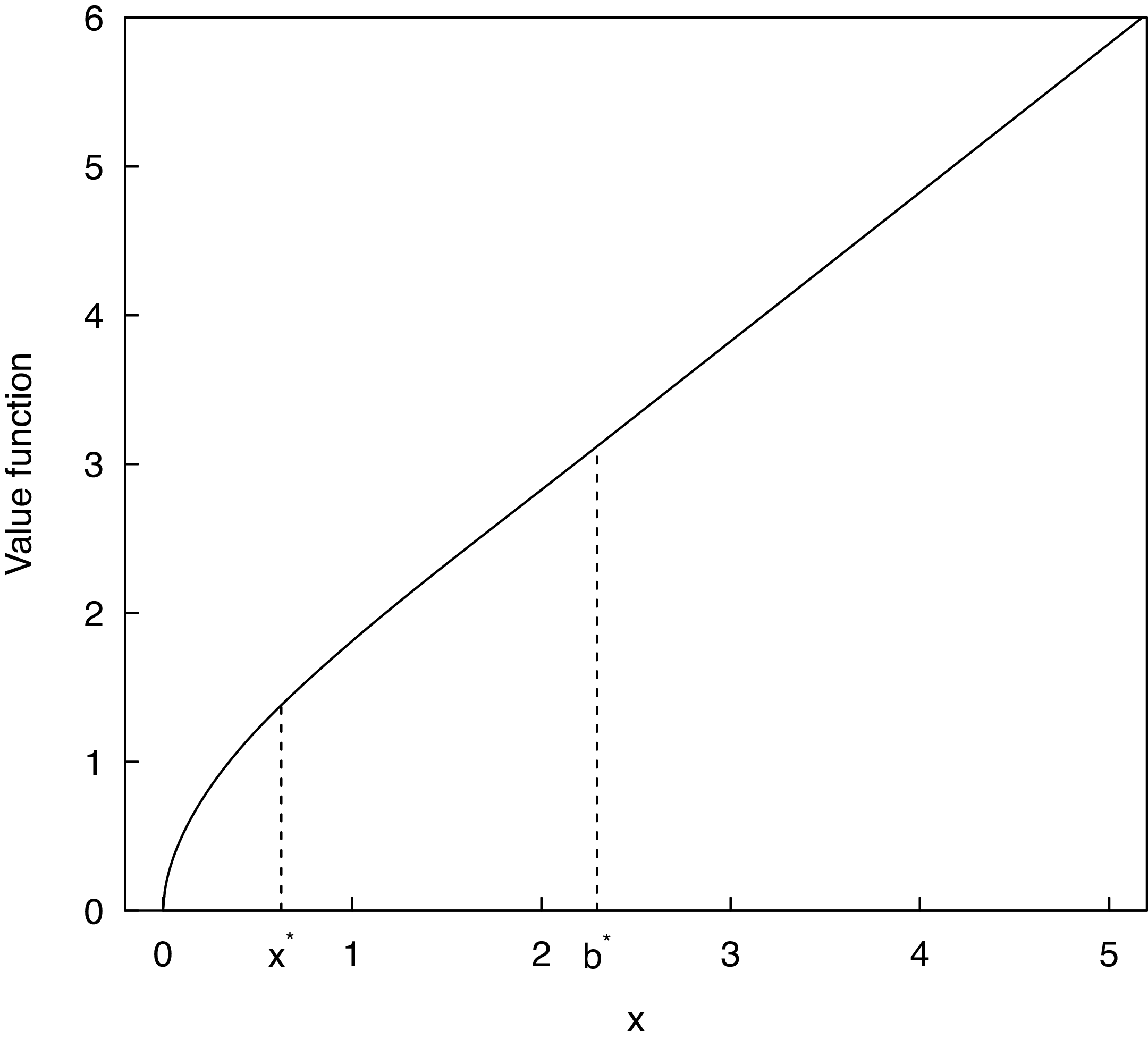

\begin{align}V(x)=v_{b^*}(x)=\begin{cases}\displaystyle C_2(b^*)\int_{0}^{x}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z,\quad &{x\in[0,x^{*})},\\C_4(b^*)g_{1}(x)+C_5(b^*)g_2(x),\quad & x\in[x^{*},b^*],\\v_{b^*}(b^*)+x-b^*,\quad & x\in(b^*,\infty) {,}\end{cases}\end{align}

\begin{align}V(x)=v_{b^*}(x)=\begin{cases}\displaystyle C_2(b^*)\int_{0}^{x}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z,\quad &{x\in[0,x^{*})},\\C_4(b^*)g_{1}(x)+C_5(b^*)g_2(x),\quad & x\in[x^{*},b^*],\\v_{b^*}(b^*)+x-b^*,\quad & x\in(b^*,\infty) {,}\end{cases}\end{align}

and the optimal strategy is

$(\pi^*,L^{b^*})=\{(\pi^*_t,L^{b^*}_t);\;t\ge 0\}$

, where

$(\pi^*,L^{b^*})=\{(\pi^*_t,L^{b^*}_t);\;t\ge 0\}$

, where

$$\pi^*_t=\begin{cases}A(X^{\pi^*,L^{b^*}}_{t-}) & 0\le X^{\pi^*,L^{b^*}}_{t-}\le x^*,\\1 & X^{\pi^*,L^{b^*}}_{t-}>x^*,\end{cases}$$

$$\pi^*_t=\begin{cases}A(X^{\pi^*,L^{b^*}}_{t-}) & 0\le X^{\pi^*,L^{b^*}}_{t-}\le x^*,\\1 & X^{\pi^*,L^{b^*}}_{t-}>x^*,\end{cases}$$

and

$L^{b^*}_t$

is the functional which causes the controlled process to be reflected downward at the boundary

$L^{b^*}_t$

is the functional which causes the controlled process to be reflected downward at the boundary

$b^*$

.

$b^*$

.

The above theorem proves the existence of an optimal solution and provides a semi-explicit method for finding the optimal solutions. Explicit solutions are available if we can find explicit expressions for

$g_1$

and

$g_1$

and

$g_2$

, which is feasible if and only if we can find explicit expressions for the solutions to the following second-order ordinary differential equation (ODE):

$g_2$

, which is feasible if and only if we can find explicit expressions for the solutions to the following second-order ordinary differential equation (ODE):

$\frac{1}{2}\sigma^{2}(x)g^{\prime\prime}(x)+\mu(x)g^\prime(x)-\delta g(x)=0$

.

$\frac{1}{2}\sigma^{2}(x)g^{\prime\prime}(x)+\mu(x)g^\prime(x)-\delta g(x)=0$

.

If the underlying diffusion models are such that it is not possible to solve

$\frac{1}{2}\sigma^{2}(x)g^{\prime\prime}(x)+\mu(x)g^\prime(x)-\delta g(x)=0$

explicitly. Then we can use numerical methods to find

$\frac{1}{2}\sigma^{2}(x)g^{\prime\prime}(x)+\mu(x)g^\prime(x)-\delta g(x)=0$

explicitly. Then we can use numerical methods to find

$g_1$

and

$g_1$

and

$g_2$

and then apply the results in Theorem 4 to compute the optimal solutions and find the optimal strategies.

$g_2$

and then apply the results in Theorem 4 to compute the optimal solutions and find the optimal strategies.

3.2. Case (II)

We now consider case (II) where the following condition holds:

$$g^{\prime\prime}_{1}(b)+g^{\prime\prime}_{2}(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z<0\quad \mbox{for all $b>x^*$.}$$

$$g^{\prime\prime}_{1}(b)+g^{\prime\prime}_{2}(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z<0\quad \mbox{for all $b>x^*$.}$$

From the early discussions before Section 3.1 we know that in this case

$b^*=+\infty$

. We first derive some analytical properties that

$b^*=+\infty$

. We first derive some analytical properties that

$v_b(x)$

and some associated quantities possess, which play an important role in solving the optimization problem in such case.

$v_b(x)$

and some associated quantities possess, which play an important role in solving the optimization problem in such case.

Lemma 5. Consider case (II). Let A(x),

$x^{*}$

, and

$x^{*}$

, and

$v_b(x)$

be defined in (26) and (45), respectively. Then, for any

$v_b(x)$

be defined in (26) and (45), respectively. Then, for any

$b>x^*$

, the function

$b>x^*$

, the function

$v_b(x)$

is continuously differentiable on

$v_b(x)$

is continuously differentiable on

$[0,+\infty)$

and twice continuously differentiable except at

$[0,+\infty)$

and twice continuously differentiable except at

$x=b$

,

$x=b$

,

$ v_b^\prime(x)\ge 1$

for

$ v_b^\prime(x)\ge 1$

for

$x\ge 0$

,

$x\ge 0$

,

$v_b^{\prime\prime}(b-\!)<0$

, and

$v_b^{\prime\prime}(b-\!)<0$

, and

$\max_{a\in[0,1]}{\mathcal L}_{v_b}(a,x)={\mathcal L}_{v_b}(A(x),x)=0$

for

$\max_{a\in[0,1]}{\mathcal L}_{v_b}(a,x)={\mathcal L}_{v_b}(A(x),x)=0$

for

$x\in[0, x^{*}]$

and

$x\in[0, x^{*}]$

and

$\max_{a\in[0,1]}{\mathcal L}_{v_b}(a,x)={\mathcal L}_{v_b}(1,x)=0$

for

$\max_{a\in[0,1]}{\mathcal L}_{v_b}(a,x)={\mathcal L}_{v_b}(1,x)=0$

for

$x\in(x^{*},b)$

.

$x\in(x^{*},b)$

.

We show that the quantities

$C_2(b)$

,

$C_2(b)$

,

$C_4(b)$

, and

$C_4(b)$

, and

$C_5(b)$

are still finite when b converges to

$C_5(b)$

are still finite when b converges to

$+\infty$

, which then guarantees the existence of the limit of

$+\infty$

, which then guarantees the existence of the limit of

$v_b(x)$

when b converges to

$v_b(x)$

when b converges to

$+\infty$

.

$+\infty$

.

Lemma 6. If

$b^*=+\infty$

, then

$b^*=+\infty$

, then

$C_2(b)$

,

$C_2(b)$

,

$C_4(b)$

, and

$C_4(b)$

, and

$C_5(b)$

converge to finite quantities as b goes toward

$C_5(b)$

converge to finite quantities as b goes toward

$+\infty$

.

$+\infty$

.

As a result, the following optimality results can be derived.

Theorem 5. Consider case (II). Let A(x),

$x^{*}$

,

$x^{*}$

,

${b^*}$

,

${b^*}$

,

$C_2(\!\cdot\!)$

,

$C_2(\!\cdot\!)$

,

$C_2(\!\cdot\!)$

, and

$C_2(\!\cdot\!)$

, and

$C_5(\!\cdot\!)$

be defined in (26), (48), and (37)–(38), respectively. Let

$C_5(\!\cdot\!)$

be defined in (26), (48), and (37)–(38), respectively. Let

$v_b(x)$

be defined same as in (45) for

$v_b(x)$

be defined same as in (45) for

$b>x^*$

:

$b>x^*$

:

\begin{align*}v_b(x)=\begin{cases}\displaystyle C_{2}(b)\int_{0}^{x}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z,\quad & x\in[0, x^{*}),\\C_{4}(b)g_{1}(x)+C_{5}(b)g_{2}(x),\quad& x\in[x^{*}, b],\\v_b(b)+x-b,\quad & x\in(b,\infty).\end{cases}\end{align*}

\begin{align*}v_b(x)=\begin{cases}\displaystyle C_{2}(b)\int_{0}^{x}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z,\quad & x\in[0, x^{*}),\\C_{4}(b)g_{1}(x)+C_{5}(b)g_{2}(x),\quad& x\in[x^{*}, b],\\v_b(b)+x-b,\quad & x\in(b,\infty).\end{cases}\end{align*}

Then: (i)

$V(x)=\lim_{b\uparrow +\infty}v_b(x)$

for

$V(x)=\lim_{b\uparrow +\infty}v_b(x)$

for

$x\ge 0$

; and (ii) no optimal strategy exists.

$x\ge 0$

; and (ii) no optimal strategy exists.

4. Optimality results when

$\mu(0) \le 0$

We show in the following that if

$\mu(0) \le 0$

, it is optimal to withdraw the full storage, which leads to immediate absorption.

$\mu(0) \le 0$

, it is optimal to withdraw the full storage, which leads to immediate absorption.

Theorem 6. Assume

$\mu(0)\le 0$

. It holds that

$\mu(0)\le 0$

. It holds that

$V(x)=x$

for

$V(x)=x$

for

$x\ge 0$

, and that the optimal strategy is given by

$x\ge 0$

, and that the optimal strategy is given by

$(\pi^0,L^0)$

, where

$(\pi^0,L^0)$

, where

$\pi^0(t)\equiv 0$

and

$\pi^0(t)\equiv 0$

and

$L^0$

represents the strategy that entails withdrawing all available reserves immediately at time 0.

$L^0$

represents the strategy that entails withdrawing all available reserves immediately at time 0.

If this is viewed as a control problem in finance, the above optimality results suggest the following intuition. Recall that

$\sigma(\!\cdot\!)$

is non-vanishing. If

$\sigma(\!\cdot\!)$

is non-vanishing. If

$\mu(0)\le 0$

, then when the state is at 0, the instantaneous return rate is zero or negative, while there remains a non-zero risk. This calls for an immediate withdrawal from the risky business.

$\mu(0)\le 0$

, then when the state is at 0, the instantaneous return rate is zero or negative, while there remains a non-zero risk. This calls for an immediate withdrawal from the risky business.

5. Optimality results when

$\mu(0) > 0$

and

$\boldsymbol\mu(\boldsymbol{x}) \le 0$

for some

$\boldsymbol{x} > 0$

We now consider the case where

$\mu(0)> 0$

and

$\mu(0)> 0$

and

$\mu(x)\le 0$

for some

$\mu(x)\le 0$

for some

$x>0$

. Define

$x>0$

. Define

\begin{align}x_0=\inf\{x>0\,:\, \mu(x)\le 0\}.\end{align}

\begin{align}x_0=\inf\{x>0\,:\, \mu(x)\le 0\}.\end{align}

Then

$0 < x_0 < \infty$

and

$0 < x_0 < \infty$

and

$\mu(x)>0$

for

$\mu(x)>0$

for

$0\le x < x_0$

. Define A(x) and

$0\le x < x_0$

. Define A(x) and

$x^*$

as in (26):

$x^*$

as in (26):

\begin{align}A(x)=\frac{\int_{0}^{x}(2\delta+\frac{\mu^{2}(y)}{\sigma^{2}(y)})\mathrm{d} y}{\mu(x)} \quad \mbox{for $x\geq0$}\quad \mbox{and} \quad x^{*}=\inf\{x\geq0\,:\, A(x)>1\}. \end{align}

\begin{align}A(x)=\frac{\int_{0}^{x}(2\delta+\frac{\mu^{2}(y)}{\sigma^{2}(y)})\mathrm{d} y}{\mu(x)} \quad \mbox{for $x\geq0$}\quad \mbox{and} \quad x^{*}=\inf\{x\geq0\,:\, A(x)>1\}. \end{align}

We can obtain the following properties in this case.

Lemma 7. The function A(x) is increasing on

$[0,x^*]$

and the following hold:

$[0,x^*]$

and the following hold:

\begin{align}&0 < x^{*}< \min\left(\frac{\mu(0)}{\delta},x_0\right)\!, \end{align}

\begin{align}&0 < x^{*}< \min\left(\frac{\mu(0)}{\delta},x_0\right)\!, \end{align}

\begin{align}&0\leq A(x)\leq 1,\quad x\in[0,x^{*}],\end{align}

\begin{align}&0\leq A(x)\leq 1,\quad x\in[0,x^{*}],\end{align}

\begin{align}&A(0)=0,\quad A(x^*)=1.\end{align}

\begin{align}&A(0)=0,\quad A(x^*)=1.\end{align}

Define

$\xi(b)$

and

$\xi(b)$

and

$b^*$

as previously (in (48)):

$b^*$

as previously (in (48)):

\begin{align}\xi(b)&\,:\!=\,{g^{\prime\prime}_{1}(b)+g^{\prime\prime}_{2}(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z},\quad b\in[x^*,\infty),\end{align}

\begin{align}\xi(b)&\,:\!=\,{g^{\prime\prime}_{1}(b)+g^{\prime\prime}_{2}(b)\int_{0}^{x^{*}}\exp\!\bigg({\int_{z}^{x^*}\frac{\mu(y)}{\sigma^{2}(y)A(y)}\,\mathrm{d} y}\bigg)\mathrm{d} z},\quad b\in[x^*,\infty),\end{align}

\begin{align}b^{*}&=\inf\{b> x^{*}\;:\; \xi(b)\geq0\}\quad\mbox{and}\quad b^{*}= +\infty\ \mbox{if } \xi(b)< 0\ \mbox{for all $b\in[x^{*},\infty)$},\end{align}

\begin{align}b^{*}&=\inf\{b> x^{*}\;:\; \xi(b)\geq0\}\quad\mbox{and}\quad b^{*}= +\infty\ \mbox{if } \xi(b)< 0\ \mbox{for all $b\in[x^{*},\infty)$},\end{align}

where