Few visual models have attracted as much attention in the digital economy as the Gartner Hype Cycle Chart (HCC). With its now-familiar double curve – rising toward the ‘Peak of Inflated Expectations’ before dipping into the ‘Trough of Disillusionment’ – it offers a stylised yet compelling depiction of the volatile rhythms of technological innovation. Hailed as ‘one of the most brilliant insights in the history of technology’ (Brinker, Reference Brinker2018), its continued influence speaks not only to its visual clarity – ‘the shape just resonates’, notes its creator Jackie Fenn – but also to its ability to influence how market actors perceive and respond to technological change. Fenn insists the HCC is not a prophecy or invention but ‘a mirror held up to reality’. ‘You may hate the reality that hype cycles happen’, she quips, ‘but it is a recognition of something that occurs naturally in the wild’, pointing out that there have ‘been booms and busts for as long as history has been recorded – be it tulips, railroads, or any of the other big historical examples’. The real innovation of the HCC lies not in simply noticing these volatile rhythms, but in rendering them visible, structured, and actionable – something executives can point to in meetings, or investors can use to guide planning. By creating a recognisable curve, the HCC transformed hype from something seen as risky or even ‘dangerous’ into a calculable input for decision-making.Footnote 1

Scholars have widely explored the role of consultants and tools in market-making (Chiapello & Gilbert, Reference Chiapello and Gilbert2019; Gond & Brès, Reference Gond and Brès2020), highlighting how markets do not emerge in isolation but are actively shaped by various instruments and frameworks (Ahrne et al., Reference Ahrne, Aspers and Brunsson2015; Geiger et al., Reference Geiger, Mason, Pollock, Roscoe and Ryan2024). Research emphasises the performative effects of such tools, particularly in how they structure decision-making and influence market trajectories (Muniesa et al., Reference Muniesa, Millo and Callon2007; Callon, Reference Callon2021). One increasingly influential but underexamined force in this process is hype. Hype has become a defining feature of market-making, particularly in new technology markets, where it amplifies attention, fuels expectations, and directs investment flows (Grodal & Granqvist, Reference Grodal, Granqvist, Ashkanasy, Zerbe and Härtel2014). It channels market actors toward ‘hot markets’ (Pontikes & Barnett, Reference Pontikes and Barnett2017) – fields perceived as highly promising and potentially lucrative – while amplifying their fear of missing out (FOMO). However, while scholars have explored the role of tools in structuring markets, the specific tools designed to interpret and navigate hype – and their influence on market-making – remain largely unexamined.

Navigating hype, as Chapter 3 argued, has become a crucial yet complex challenge for market actors across industries (Garud et al., Reference Garud, Lant and Schildt2021). The difficulty stems from the rapid rise of hyped markets and their inevitable downturn, a pattern commonly referred to as a ‘hype cycle’ (van Lente et al., Reference Van Lente, Spitters and Peine2013). Moreover, hype operates at the intersection of calculative and affective dimensions, shaping decision-making by introducing new information while simultaneously triggering strong emotions such as excitement and fear – what Beckert (Reference Beckert2016), following Keynes (Reference Keynes1936), terms ‘animal spirits’. For example, a manager evaluating an emerging technology may feel exhilarated by the potential for first-mover advantage, driven by the promise of competitive gains. At the same time, the manager may hesitate, fearing premature investment in an unproven innovation (Arnold et al., Reference Arnold, Breitenmoser, Röth and Spieth2022). This tension highlights the central challenge of timing market entry. As Kumaraswamy et al. (Reference Kumaraswamy, Garud and Ansari2018, p. 1030) observe, determining when and whether to enter a hyped market requires actors to ‘cultivate the capacity’ to interpret the ‘weak signals’ embedded within hype and act ‘before it is too late’.

The growing significance of hype in market-making has led consultants and analysts to develop specialised tools – what, in this chapter, we term ‘hype tools’ – to help stakeholders navigate hype cycles and strategically respond to hype as a market-making force. These frameworks have also become commercial offerings, showing how the task of taming hype is packaged and sold as part of a business of future-oriented advice. Hype tools are an example of the kind of promissory product described in Chapter 3 – crafted frameworks that structure uncertainty and market expectations. Yet, despite their increasing influence, the design and operationalisation of these tools remain largely unexplored, particularly the tensions that arise at the intersection of hype’s calculative and affective dimensions. Existing research has examined how hype fuels market momentum, creating high-growth markets while simultaneously rendering others ‘passé’ (Pontikes & Barnett, Reference Pontikes and Barnett2017). Yet, little is known about how these cycles are actively mediated by the very tools that claim to map them. As Beckert (Reference Beckert2016) suggests, examining these tools is crucial, as they do not merely reflect hype but actively shape how it unfolds, influencing market actors’ perceptions, decisions, and strategies.

To advance this enquiry, we theorise how analysts transform hype into a structured market-shaping framework that market actors can interpret and act upon. By developing hype tools, consultants and analysts aim to strike a balance between excitement and calculation, enabling technology adopters and investors to navigate hype cycles effectively. However, in designing these tools, consultants themselves must contend with the tensions inherent in hype’s dual nature – its affective intensity and its calculative dimensions. To examine how they manage this challenge, we draw on Latour’s (2012) concept of ‘purification’, which captures the effort to reconcile and structure the interplay between hype’s emotional and more calculative aspects. This perspective leads us to ask: How do consultants design and operationalise tools to enable market actors to leverage hype in markets for novel technology?

To address this question, we conducted a qualitative study of the original design and subsequent production and maintenance of the Hype Cycle Chart (HCC), a widely recognised tool for assessing how emerging technologies progress through a hype cycle and shaping how market actors evaluate the timing of investment in new technology markets (van Lente et al., Reference Van Lente, Spitters and Peine2013). The HCC has ‘gained substantial attention from practitioners’ (Dedehayir & Steinert, Reference Dedehayir and Steinert2016, p. 34), ‘facilitated strategic investment decisions’ (van Lente et al., Reference Van Lente, Spitters and Peine2013, p. 1615), and particularly influenced ‘large companies’ R&D decisions’ (Steinert & Lefier, Reference Steinert, Leifer, Kocaoglu, Anderson, Daim and Bayus2010, p. 2). Based on this analysis, we propose a model that highlights three mechanisms – balancing, reconciling, and timing – through which analysts frame hype not as speculative noise but as a structured and staged phenomenon that market actors can engage with. We term this ‘hype purification’, illustrating how analysts manage the interplay between excitement and calculability to help market actors navigate hyped markets.

6.1 Tools and Market-Making

Scholars widely acknowledge that ‘markets do not emerge out of a vacuum’ (Ahrne et al., Reference Ahrne, Aspers and Brunsson2015, p. 9) but are actively ‘made and shaped by actors of all kinds’ (Geiger et al., Reference Geiger, Mason, Pollock, Roscoe and Ryan2024, p. 6). Specifically, research has highlighted how tools, defined broadly as ‘frameworks, concepts, models, or methods’ (Jarzabkowski & Kaplan, Reference Jarzabkowski and Kaplan2015, p. 538), often play a leading role in facilitating market-making processes through ‘equipping’ actors (Callon, Reference Callon2021) with the means to navigate markets (MacKenzie & Millo, Reference MacKenzie and Millo2003) and structuring decision-making, particular decisions aimed at the future (Miller & O’Leary, Reference Miller and O’Leary2007). Building on this foundation, several key themes have emerged. One prominent theme explores how tools do more than support rational decision-making; they engage in ‘qualculation’ (Cochoy, Reference Cochoy2008) – a process that blends qualitative judgements with numerical calculations to shape market realities (Callon & Law, Reference Callon and Law2005). Another theme has explored how tools act as ‘market devices’, defined as the ‘material and discursive assemblages that intervene in the construction of markets’ (Muniesa et al., Reference Muniesa, Millo and Callon2007, p. 2). A further theme has developed around the ‘performative’ role of market devices, where tools are not merely passive representations of markets but actively shape and influence them (Callon, 1998; Muniesa et al., Reference Muniesa, Millo and Callon2007). For example, MacKenzie and Millo (Reference MacKenzie and Millo2003) examined the mathematical models underpinning financial derivatives, demonstrating that such tools are not external to markets but fundamental to their very construction.

However, while researching tool performativity remains important, scholars caution that focusing exclusively on performative effects risks neglecting the equally critical question of how tools are initially designed and constructed in the first place. As MacKenzie and Spears (Reference MacKenzie and Spears2014) argue, prioritising performativity alone ‘occludes attention’ to the processes through which tools are developed, potentially obscuring the underlying assumptions embedded in their design and designers’ intentions in shaping market dynamics. Following this approach, Gond and Brès (Reference Gond and Brès2020), studying the development of the Corporate Social Responsibility (CSR) market, highlight consultants’ dual role as both ‘tool designers’ and ‘market builders’, demonstrating how they crafted tools to reframe concerns initially seen as ‘peripheral’ within markets and organisations (CSR products and services), ultimately transforming them into ‘mainstream’ priorities. This shift from tool deployment to tool construction is also evident in Pollock and D’Adderio’s (Reference Pollock and D’Adderio2012) examination of Gartner’s Magic Quadrant tool. While their research underscored the tool’s performative role in shaping market behaviour, it also revealed how its ‘format and furniture’ – the design principles and classificatory mechanisms embedded within it – were deliberately engineered to structure market competition from the outset.

6.2 Hype and Market-Making

Scholars have long linked hype to adjacent ideas – passionate interests (Hirschman, Reference Hirschman2013), fads and fashions (Abrahamson & Fairchild, Reference Abrahamson and Fairchild1999), contagious stories (Shiller, Reference Shiller2019), projective storytelling (Garud et al., Reference Garud, Gehman and Giuliani2014), speculative bubbles (Goldfarb & Kirsch, Reference Goldfarb and Kirsch2019), and fictional expectations (Beckert, Reference Beckert2016). Earlier chapters reviewed this foundational work in depth; here we focus on what that literature leaves unexplored: the role of hype in early market formation.

Recent studies highlight hype’s pervasive role as an ‘integral part of the life’ of all emerging technology markets (Rip, Reference Rip, Fisher, Jones and von Schomberg2006, p. 355) and an ‘important element’ of market emergence (Grodal & Granqvist, Reference Grodal, Granqvist, Ashkanasy, Zerbe and Härtel2014, p. 142). Innovators and entrepreneurs often employ hyperbolic claims to generate enthusiasm among investors and early adopters, with van Lente (Reference Van Lente2012) theorising hype as a ‘resource’ that legitimises emerging technology markets and justifies their support. In this sense, hype builds excitement and channels the movement of key actors – such as investors and innovators – into a market (Valliere & Peterson, Reference Valliere and Peterson2004). As Wüstenhagen et al. (Reference Wüstenhagen, Wuebker, Bürer, Goddard, Truffer, Markard, Wüstenhagen and Wiek2009, p. 123) note, ‘[a]ttracting both talent and capital seems to be easier in industries or firms where expectations are high’, a dynamic echoed by Valliere and Peterson (Reference Valliere and Peterson2004, p. 15), who found that investors are ‘drawn to where the largest growth opportunities could be found’, with ‘hype serv[ing] as an indicator of these areas’.

Hype derives its effectiveness from its ‘collective’ nature (van Lente, Reference Van Lente2012). The more diverse the stakeholders who engage with and amplify hype, the more momentum it gains as a persuasive force, shaping market perceptions and attracting investment. When hype attains widespread attention, it fosters what Grodal and Granqvist (Reference Grodal, Granqvist, Ashkanasy, Zerbe and Härtel2014, p. 143) describe as ‘collective excitement’, where self-perpetuating promissory narratives ‘give rise to fads, hypes, and bubbles’. Moreover, Pontikes, and Barnett (Reference Pontikes and Barnett2017) highlight how the rapid escalation of hype can fuel the emergence of ‘hot markets’ – nascent industries that gain widespread attention due to their perceived potential and profitability. These markets serve as ‘attractive points of entry’, drawing in market actors particularly enticed by the surrounding ‘buzz’ (Pontikes & Barnett, Reference Pontikes and Barnett2017, p. 147).

Navigating hyped markets is inherently challenging, as hype can distort decision-making by blurring the line between genuine opportunities and inflated promises. As Grodal and Granqvist (Reference Grodal, Granqvist, Ashkanasy, Zerbe and Härtel2014, p. 143) observe, hype constrains market actors’ ability to ‘make decisions’, particularly in the early stages of an emerging technology market when uncertainty is at its peak. To mitigate risk, some actors adopt a ‘waiting game’ strategy (Robinson et al., Reference Robinson, Le Masson and Weil2012; Endenich et al., Reference Endenich, Hahn, Reimsbach and Wickert2022), delaying investment to avoid what Kumaraswamy et al. (Reference Kumaraswamy, Garud and Ansari2018) term ‘errors of commission’ – prematurely investing in overhyped technologies that ultimately fail. However, while early-stage investments carry the highest risk of failure, they also offer the greatest potential for profit and growth (Knight, Reference Knight1921). To avoid ‘errors of omission’ – missing out on transformative innovations (Kumaraswamy et al., Reference Kumaraswamy, Garud and Ansari2018) – early adopters must often commit before clear evidence of a technology’s success emerges. These competing risks underscore hype’s dual role in market decision-making, raising a critical question: Does it obscure judgement or provide valuable strategic insight?

Research has begun to examine hype as a key driver of decision-making, yet its role remains highly contested. Many studies link hype to irrationality and incalculability, arguing that it distorts decision-making processes. For instance, Shi and Herniman (Reference Shi and Herniman2023, p. 6) highlight that while hype can be ‘instrumental in decision-making’, it often presents ‘less accurate information about an innovation’, making it difficult for actors to make well-informed choices. Similarly, Wüstenhagen et al. (Reference Wüstenhagen, Wuebker, Bürer, Goddard, Truffer, Markard, Wüstenhagen and Wiek2009) argue that hype fosters non-reflective thinking and ‘herd behaviour’, where actors follow market trends without rigorous evaluation. As a result, hype is frequently positioned in opposition to rational decision-making, often dismissed as ‘communications that lack factual, rational substance’ (Kiefer & Hunt, Reference Kiefer, Hunt and Laskin2017, p. 168).

Despite its association with uncertainty and speculation, a recent study in the Market Studies literature (Geiger et al., Reference Geiger, Mason, Pollock, Roscoe and Ryan2024) has highlighted the powerful affective reactions that hype can generate, demonstrating that it remains a significant force in shaping markets and driving technology investment. With its ties to passionate interests (Hirschman, Reference Hirschman2013), excitement, and future-oriented expectations rooted in technological promises, hype can be seen as a crucial yet underexplored mechanism in the ‘vascularisation’ (Gond & Brès, Reference Gond and Brès2020; Callon, Reference Callon2021) of the economy – pumping energy, attention, and resources into emerging fields. For instance, scholars argue that hype fuels economic activity by creating an ‘evocative overload’ of what Beckert (Reference Beckert2016, p. 13) terms ‘fictional expectations’ – projected futures that drive present-day investment decisions. Drawing on Keynes’ (Reference Keynes1936) concept of ‘animal spirits’, it is suggested that emotions such as ‘excitement’ and ‘fear’ can spur bold decision-making and high-stakes risk-taking in uncertain environments, even when such actions might appear irrational.

6.3 Role of Consulting Tools in Navigating Hype

Despite growing recognition that hype is not just a by-product but a crucial driver of market-making, existing research has largely overlooked how consultants actively mediate hype through specialised tools. To manage the challenge of navigating hype, market actors increasingly turn to tools like the HCC, which claim to structure hype by offering frameworks for distinguishing between exaggerated expectations and genuine opportunities. While the Sociology of Expectations has emphasised the impact of tools in shaping technological expectations (Borup et al., Reference Borup, Brown, Konrad and van Lente2006; Konrad & Alvial-Palavicino, Reference Konrad, Alvial-Palavicino, Konrad, Rohracher and von Schomberg2017), far less attention has been given to their actual design and operationalisation. Existing studies acknowledge that tools like the HCC provide structured mechanisms for action (Dedehayir & Steinert, Reference Dedehayir and Steinert2016). However, while these studies highlight the role of hype tools in shaping expectations, they do not examine how these tools are developed, maintained, and refined in response to market dynamics.

To address this gap, our research shifts the focus from merely acknowledging the existence of these tools to examining their design and operationalisation. To explore this, we draw on Latour’s (2012) concept of ‘purification’, which describes the attempt to categorise and separate domains – such as science and society, or in this case, calculation and affect – to maintain the illusion of distinct, independent spheres of action. Purification is central to how consultants frame their role in managing hype. For instance, consultants claim that the HCC can ‘separate hype from the real drivers of a technology’s commercial promise’ (Gartner, Reference Gartner2018), positioning it as an instrument of neutral evaluation.

However, Latour’s (2012) thesis is that purification is never entirely successful – in an enduringly non-modern ‘hybrid’ world, purification efforts are constantly confronted by a parallel process of ‘hybridisation’, where there is the simultaneous mixing and entanglement of domains that purification attempts to separate. Little empirical research has explored how consultants grapple with this duality – balancing the affective pull of hype with its calculative dimensions – when designing these tools. This leads us to ask: How do consultants design and operationalise tools to enable market actors to leverage hype in markets for novel technology?

6.3.1 A Note on the Hype Cycle Chart (HCC)

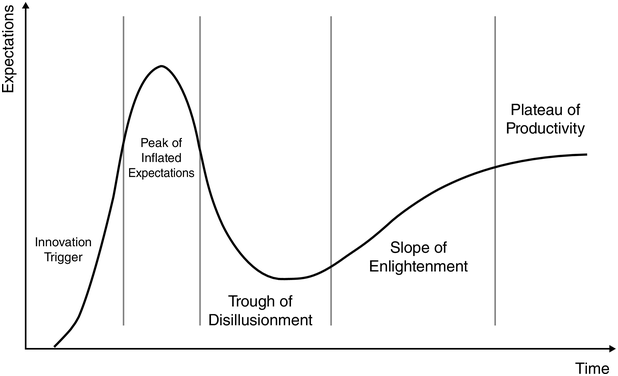

The concept of a ‘hype cycle’ is a relatively recent innovation, first introduced in 1995 by Jackie Fenn, a Gartner consultant, during her first year at the firm. Fenn coined the term and developed the tool to illustrate the dramatic rise in excitement and subsequent disillusionment surrounding emerging technologies, framing it as a predictable and repeatable process. She observed a recurring pattern among emerging technologies and ‘drew a graph illustrating the ups and downs of this cycle’ (Fenn & Raskino, Reference Fenn and Raskino2008, p. 8). She then mapped out each stage of the process and populated the curve with examples of technologies (Burkhardt, n.d.).

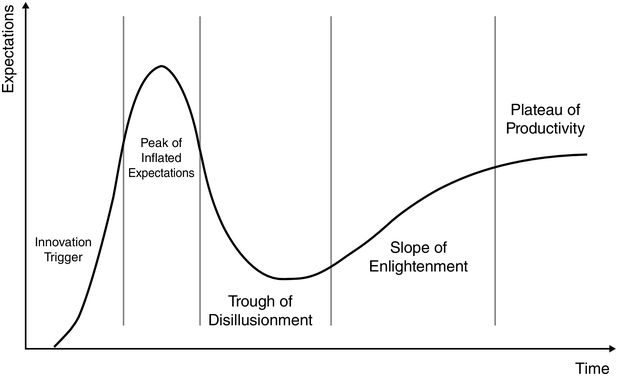

In developing the HCC, Fenn drew inspiration from two key sources. To name the cycle’s stages, she turned to theological fiction, particularly John Bunyan’s The Pilgrim’s Progress (Fenn, interview). She compared the trajectory of hype cycles to a journey, beginning with an ‘Innovation Trigger’, that sparks attention and generates hyped, often unrealistic expectations. When these expectations fail to materialise, they collapse, moving from the ‘Peak of Inflated Expectations’ into the ‘Trough of Disillusionment’.

Fenn also drew on economic theories, particularly Kondratiev Waves and Schumpeterian creative destruction (Grodal et al., Reference Grodal, Krabbe and Chang-Zunino2023). While traditional economic cycles involve a series of ‘consecutive up and down movements’ (Fenn & Raskino, Reference Fenn and Raskino2008, p. xiv), Fenn argued that hype cycles feature a distinct stabilisation phase. As technologies mature, they enter the ‘Slope of Enlightenment’, where gradual improvements accumulate through experience. Finally, when the broader benefits of these innovations become widely recognised, they achieve the ‘Plateau of Productivity’ (see Figure 6.1).

Figure 6.1 Long description

A line graph of expectations versus time plots a curve with five labelled stages. 1. Innovation trigger: marked by a steep rise terminating in a peak. 2. Peak of inflated expectations: the termination peak of innovation trigger. 3. Trough of disillusionment: the peak of inflated expectations drops to a trough. 4. Slope of enlightenment: The trough of disillusionment proceeds to a concave down increasing curve labelled slope of enlightenment. 5. Plateau of productivity: The concave down increasing curve of enlightenment plateaus.

The HCC evolved organically as other Gartner analysts ‘used the framework to put their own sets of technologies, their own domains on it’ (Fenn, interview). Its visibility surged when Alexander Droibik, a fellow Gartner analyst, incorporated the HCC into his 1999 e-business analysis to ‘predict the 2001 dotcom bust’ (Fenn, interview). Fenn describes this as a ‘really nice validation’ of the tool and a pivotal moment that propelled the HCC into global prominence (Fenn, interview).

The HCC is primarily designed for Gartner clients, particularly organisational technology adopters, who seek to navigate the evolving business solutions landscape and identify the most promising opportunities among emerging innovations that remain untested or underdeveloped. Gartner faces the challenge of effectively engaging this audience and demonstrating the value of the HCC and its advisory services in guiding strategic investment decisions. Given that Gartner’s business model relies on expanding its subscription services through personalised advisory support, client retention becomes a critical priority (Pollock & Williams, Reference Pollock and Williams2016). As a result, ensuring continued subscriptions directly influences how Gartner analysts develop and refine tools like the HCC, shaping them to align with clients’ decision-making needs and feedback, thus reinforcing the perceived value of their insights.

Today, the HCC has become one of the most recognisable and widely referenced tools in the digital economy and beyond. With over 100 distinct iterations mapping nearly 2,000 technologies (Hashemi et al., Reference Hashemi, Gallay and Hongler2021), it has evolved from a proprietary tool for Gartner’s clients into a broadly circulated and influential benchmark. As Bourne (Reference Bourne2024, p. 757) notes, the HCC is ‘now deeply embedded in promotional knowledge, reproduced in client pitches, industry presentations, and textbooks’.

Each HCC is updated annually, with new technologies added, existing ones repositioned, and others phased out. While designed for enterprise decision-makers, its online accessibility means it is used by technology vendors, venture capital investors, and other market actors seeking to position and evaluate emerging innovations. The release of a new HCC is eagerly awaited, and any adjustments send strong signals to investors, vendors, and market analysts, aligning adopter communities, vendors, and other experts, reinforcing the idea that a technology’s placement on the tool ‘can help make or break a given sector of the technology industry’ (Woodie, Reference Woodie2014).

Producing and updating an HCC involves a combination of quantitative and qualitative data, interpreted through a process that blends calculation with qualitative judgement – what Cochoy (Reference Cochoy2008) terms ‘qualculation’. Quantitative data includes financial forecasts evaluating innovations’ impact and market penetration. Meanwhile, qualitative data is drawn from vendor briefings and use cases (A1, interview). Analysts also routinely engage with clients, exploring their strategies for adopting emerging technologies and gaining insight into investment considerations. The final decision on where to position technologies within the HCC is described as a ‘judgment call’ (A1, interview) – one that reflects not only formal analysis but also the more nuanced, qualculative process of making sense of complex and often ambiguous signals. This process integrates insights from internal technology vendor assessments, media coverage, and even ‘looking at Google Trends’ (A1, interview).

6.4 Purifying Hype as a Market-Making Force

Deciding to invest in hyped markets was once a wholly unspecified process. Before the release of the HCC, no comparable tools, methodologies, or frameworks existed to help market actors navigate and interpret hype in emerging technology markets. Moreover, hype was perceived as random or relentless, moving in unpredictable waves rather than following a structured trajectory (Edgerton, Reference Edgerton1997). According to Jackie Fenn, it was disorganised ‘noise’ without much of a discernible pattern – there were merely constant ‘waves of hype’ (Fenn, interview). This situation began to change in the late 1990s. Initially published as a one-off research note, the HCC quickly gained traction with Gartner clients, who would approach Fenn during conference events to ask, ‘Hey, are you going to update that [HCC]?’ (Fenn, interview). Fenn attributes the HCC’s widespread appeal to its visual simplicity: ‘The shape just resonates.’ Once she sketched the HCC, its meaning required no extensive explanation. ‘Some models you need to present and say, “Well, this is how you use it.” But with the [HCC], people just saw it, and they get it’ (Fenn, interview).

6.5 Balancing: Bringing Together Different Rationales in One Tool

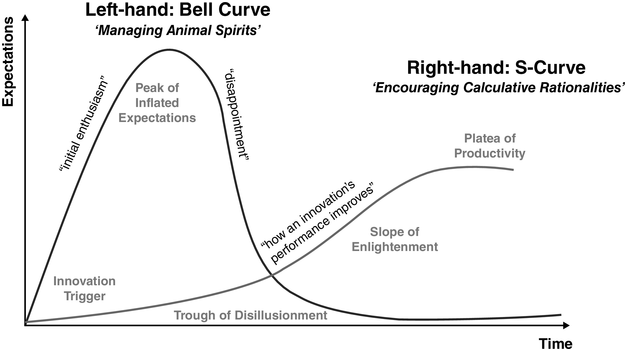

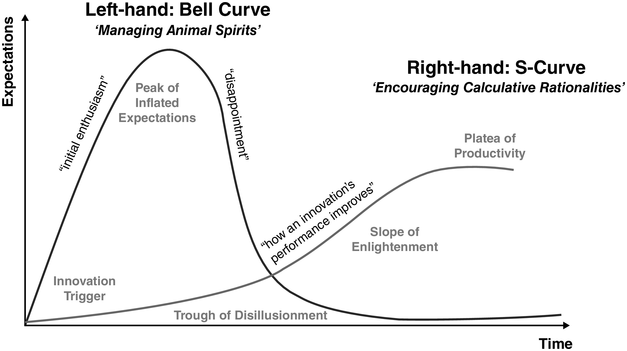

The HCC invites market actors to consider two very different curves – a process we characterise as balancing. First, a bell curve depicts ‘initial enthusiasm and disappointment driven by positive and negative hype’ (Fenn & Raskino, Reference Fenn and Raskino2008, p. 26), foregrounding how the projected claims surrounding emerging technology may not be fulfilled, which we label managing animal spirits. Then, an S-curve portrays ‘how an innovation’s performance improves slowly at first, then picks up steadily, and finally yields diminishing returns’ (Fenn & Raskino, Reference Fenn and Raskino2008, p. 26), labelled as encouraging calculative rationalities. We begin by discussing the HCC’s left-hand side (see Figure 6.2).

Figure 6.2 Long description

A 2-line graph of expectations versus time plots a left hand bell curve and a right hand S curve. The left hand bell curve, subtitled, managing animal spirits, shows initial enthusiasm peaking, and declining after, to a trough of disillusionment. The peak is labelled, peak of inflated expectations. The right hand S curve subtitled, encouraging calculative rationalities, shows a gradually rising innovation trigger indicated by a concave up rising curve, that inflects to a concave down increasing curve showing how the innnovation's performance improves, and subsequently plateaus. The plateau is labelled, plateau of productivity. The trough of disillusionment in the bell curve meets the improving performance of the innovation at a certain point.

6.5.1 Left-Hand Side: Managing Animal Spirits

When analysts first assess a newly released innovation, they adopt a cautious stance, working under the assumption that hype is widespread. They frequently warn market actors about a recurring pattern in which technology vendors and other stakeholders exaggerate the potential and applicability of innovations – describing the HCC as being ‘judgmental against [this] trend’ (A3, interview). As Jackie Fenn herself explained, ‘these very large waves of hype that move quite rapidly’ can lead some adopter organisations ‘to move in before all the lessons have been learnt’ (Fenn, interview). As Fenn explained, ‘[w]hen it first came out, it was more of a statement, the recognition that this is a pattern that happens … an adopter beware type of message’ (Fenn, interview). Organisations were warned not to ‘fall victim to the hype cycle’, as premature adoption of unproven technologies could result in catastrophic failure.

Analysts frequently use cautionary language, warning market actors about the risks of premature investment. One described the tendency as ‘bright shiny object syndrome’, advising clients to ‘beware’ of its pull (A1, interview). Another noted that ‘the vendors are always trying to manipulate you into thinking that everything is wonderful, which of course it isn’t’ (A2, interview). A third emphasised that ‘[a]t the end of the day, it’s all about dispelling the enthusiasm that is not justified’ (A3, interview). The same analyst explained that ‘the primary purpose of [HCCs] is to remind people that early-stage investments carry significant risks’ (A3, interview). He continues:

You’re potentially buying into a technology and probably companies, many of whom are probably start-ups, who simply are probably not going to be around to see that technology come to a mutual market sense. So, I think there is a bit of a caveat emptor intention in [HCCs], not necessarily to scare people away but certainly to remind them to do their due diligence very carefully.

According to this informant, analysts aim to temper expectations, advising market actors: ‘“Don’t necessarily get your hopes up too high about this.” I think that’s probably the number one message that any analyst would want … if you’re a buyer, to walk away with’ (A3, interview). For example, when discussing the current excitement surrounding Blockchain technologies, another analyst illustrates this cautionary approach by saying:

There’s all types of hype around Blockchain…. Hard to tell which is true and which is not true unless you actually get hands-on with stuff…. Once a vendor or a concept or space gets past The Peak, then, because the journalists and all the trades are all hyping up, ‘Oh man, this is going to solve everything. Blockchain is the answer to every problem we ever have in IT. You know culpability is not a problem, we’ve got Blockchain.’

This scepticism is frequently a result of their extensive familiarity with new successive technologies over a lengthy period. Based on their experience, analysts advise market actors to exercise caution to avoid disappointment, noting that:

6.5.2 Right-Hand Side: Encouraging Calculative Rationalities

Now, we turn to the right-hand curve, where the objective shifts. While analysts use the left-hand side to highlight risks, they are careful not to discourage market actors from engaging altogether. Jackie Fenn warned against the dangers of excessive caution. Waiting too long can be just as consequential as acting too early. ‘Serious threats to survival’, she stressed, ‘are probably cases when companies don’t move soon enough’ – leading to irrelevance or missed opportunity. As Fenn explained, some market actors may dismiss a technology as ‘no good’ or fail to recognise that competitors are already adopting it (Fenn, interview).

The right side signals when benefits can be gained from investing and adopting early. As Fenn points out, ‘so when something’s Peaking, adopters could say, ‘Ok, this may be of interest, and we should look at it, but let’s not invest at all costs just because everybody else is. Let’s really understand what it means for us’ (Fenn, interview). Her message to market actors is to capitalise on the opportunities presented within the HCC, even when things turn sour: ‘And then when the issues hit, and things start to be difficult, and people are telling you all the times it didn’t work, if it’s valuable to you, then you can and should pursue it anyway, even while it’s in The Trough’ (Fenn, interview).

Furthermore, drawing on well-established criteria for stock market orientation (Chiapello, Reference Chiapello2015; Birch & Muniesa, Reference Birch and Muniesa2020), the internal HCC methodology encourages analysts to categorise market actors as ‘Type A, B, or C’ based on their risk tolerance. A central message of the HCC is that entering a market should align with the adopter’s risk profile. ‘Aggressive’ adopters may explore and adopt emerging technologies earlier, as they are more willing to take risks, whereas ‘conservative’ adopters are advised to adopt early only if the potential benefits outweigh the uncertainties. Jackie Fenn explains the reasoning behind these classifications:

I found it in talking with companies to be a very simple way that organisations are prepared to self-identify. So, if you say, ‘well, you do think you’re Type A, B, C, you’re aggressive, moderate, conservative?’, they can immediately say, ‘Oh, yes, we’re definitely a Type C’. Or, ‘well, our Product Department is a Type A, but in IT we’re Type B or C’ or vice versa. So, it’s a very simple way that people identify where they are in terms of how willing they are to take the risk of new technologies and also the mismatches within their own companies.

Another analyst describes how he needs to find the correct balance between optimism and caution when providing recommendations to different market actors. As they see it, some should expect to reap significant rewards, whilst others should stay in line with best practices:

[I]f you’re Type A, stuff that’s early in the [HCC], that’s the kind of stuff you might want to be an early adopter of to create competitive advantage. But, if you’re Type B or Type C, we would probably say, ‘You want to stay away from that unless it’s absolutely transformational, and you’re going to lose out by not being part of it.’

For instance, Type Bs are told to invest at ‘The Trigger mid-point, right before it quite reaches The Peak’ (A1, interview). Investing after The Peak is considered a safer investment because,

We’re going to look at something as it’s fed out of the hype, so it’s made it through that. But we know now it’s going to be refined [and] bugs are going to be fixed as it goes down through The Trough of Disillusionment - maybe that’s where some companies want to invest.

Another analyst uses the example of Software-as-a-Service (SaaS), an emerging phenomenon at the time, to talk us through the way he advises market actors:

When you talk to a client, the Type B and Type C will say, ‘Should we go SaaS?’ And you can go, ‘No, it’s not for you, yet’. But for the Type As, you might say, ‘Yes, SaaS Financial Management or SaaS HR, it’s over The Peak, it’s going into The Trough of Disillusionment, so if you know what to watch out for then, yes, you can be an early adopter.’

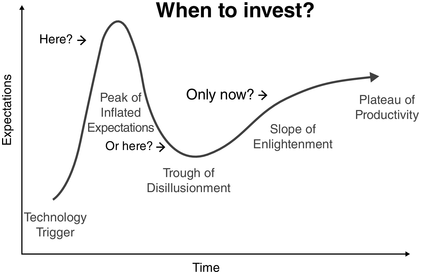

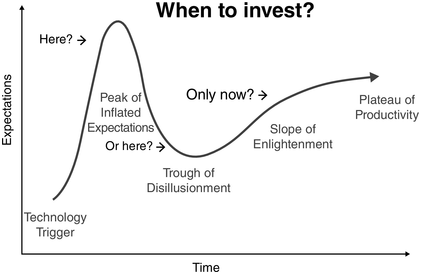

The image above, widely disseminated in industry circles, illustrates this segmentation of market actors based on their capacity/willingness to support risk (see Figure 6.3).

Figure 6.3 Long description

The Hype Cycle Chart titled, When to Invest?, with the five stages labelled. A label reads, here? with a right arrow pointing to the peak of inflated expectations, followed by another one, that reads, or here? with an arrow pointing to the trough of disillusionment, and yet another one that reads, only now? with a n arrow pointing to the slope of enlightenment,

6.6 Reconciling: Engaging Hype without Succumbing to It

We now examine how analysts determine when technologies enter, progress through, or exit a hype cycle. A key challenge for analysts in constructing the tool is engaging with hype without becoming over-influenced by it. To maintain critical distance, they must engage in a reconciliation process, where, to avoid falling prey to hype, analysts balance individual judgement with collective peer review. This process, which we theorise as negotiating where the dots go, ensures that decisions are not solely driven by speculative enthusiasm but are instead tempered through structured evaluation and collective deliberation.

6.6.1 Falling Prey to Hype

Individual analysts devote much effort to investigating technology sectors, but it is recognised that they struggle to maintain analytical distance. Before commencing this role, many were seasoned technology specialists, meaning they had extensive professional experience and had often made time and personal/emotional investments in the specific fields covered. However, they face the challenge of becoming overexcited by technology. Informants told us that one of the most damaging errors an analyst can make is to fail to see through overstated vendor promises and to produce a ‘vendor puff piece’ that is ‘too biased in one direction’ (interview, A2). In other words, analysts must counter the overenthusiasm of innovation actors and communities by ‘not falling prey to … the vendor hype’ (A4, interview). According to one analyst’s description,

It is a hype cycle, and the vendors tend to define markets by virtue of their own strength. And some of them are very good at it: very good marketing material, very good at supporting arguments they want to support, rather than looking where the evidence is taking you. So, you have to resist that.

Another analyst makes a similar argument: ‘[y]ou need a certain amount of cynicism and experience, essentially, to be able to cut through vendor claims’ (A1, interview). Indeed, according to this analyst, it is through their long-term career and emotional investments in learning about the technology and trends that they can see through vendor hype:

This does require folks who have some experience and background [and] understand the application of the technology, and can do their own research, right, in terms of [developing a] better understanding [about] these technologies and how they’re applied. Where the experience comes in is, really, being able to look at all the current information about something like that and be able to not just plot it on a [HCC] … but be able to say, ‘And this is the impact it’s going to have.’

However, more seasoned analysts would admit that this closeness and familiarity could also make it difficult to stay impartial: ‘It’s human nature to think that the things that you’re studying are more advanced than they really are, and you have a tendency to move those dots quicker than they should’ (interview, A4). As another informant saw it, neophyte analysts have the propensity to become ‘enamoured’ with technology:

The biggest thing we [tell] our analysts … is ‘not to get enamoured with the technology. Don’t admire the technology. Understand it so that you can help the client to understand whether it’s relevant or not’. And that’s probably the reason … a lot of … inexperienced people … don’t work on these [HCCs] … it’s not just a function of age, right? It can be just the interest in technology. We can get blinded … by what is described with the technology itself and … be so enamoured with it that we lose sight of what its real impact is going to be.

A direct consequence of becoming enamoured is prematurely moving technologies forward in the HCC, regardless of whether there is evidence to support the move:

As an experienced analyst, I’ve been doing this a long time, I can resist those urges. The younger, the less experienced analysts have a tendency to feel like they need to move the dots year every year – some without real evidence that there’s actually increased adoption or a more vibrant vendor community. So, I check all those things out. So, I make sure I’m not falling prey to those proclivities that you tend to do.

6.6.2 Negotiating Where the Dots Go

Because individual knowledge and judgement are inherently limited and prone to error, the development of HCCs is not the responsibility of a single analyst but the result of a collective process. HCCs are shaped through collaboration among multiple contributors. As one informant explains, HCCs typically ‘go out of the door with maybe three or four [author] names’ (interview, A6). However, these authors ‘don’t own all the dots in the [HCC]’ (A7, interview). Instead, ‘every single one of those dots would have possibly a separate owner’ (A3, interview), reflecting the highly distributed nature of the process. Creating an HCC requires synthesising and aligning the perspectives of dozens – and, in some cases, hundreds – of dot owners, a task one author described as a ‘pain to do’ (A6, interview) and another likened to ‘herding cats’. (A2, interview)

An analyst explains a characteristic example: ‘So, I do the [HCC] for [tech area 1], so I need the dot from the guy who does [tech area 2], and I need the dot from the guy who does [tech area 3]. I need the stuff from the [tech area 4] guy’ (A6, interview), and so on. Moreover, they must coordinate with them about where their dot should appear and whether it has moved since the previous year. For some HCCs, this coordination effort could be massively expanded: ‘400 people would play a role in really negotiating where these different dots go and creating the document that gets published’ (A3, interview). The process of bringing these actors together is described by the same analyst as follows:

So in a typical year when the [specific HCC] relevant to me was being produced, I would be in this periodic phone, WebEx conversation, providing my point of view of what I think this should be here and that should be there, and these are the anecdotal reasons why I think so, typically based upon the ongoing conversations you’re having with end-users and vendors and balancing the two, and in a [HCC] that may have had 25 dots, I would probably end up being the [dot owner] for about four or five of them.

However, there is more to these events than mere coordination of actions. For example, during meetings, analysts vigorously dispute and occasionally ‘fight’ with each other: ‘If you look at any [HCC], it’s the result of probably 50 or 60 analysts debating and infighting to position where those various dots live’, says one analyst (A3, interview). The HCC, according to this informant, is a ‘methodology’ for encouraging debate and negotiation:

Negotiate is a good word. I would have to basically haggle with all of these other people in terms of why I think it should be towards the bottom of ‘The Trough’ or wherever I’ve decided it ought to be. So, [the HCC], to me, is the rather important methodology for the internal negotiating and debating that takes place within the analysts. And a [HCC] which finally sees the light of day … can be seen to represent a very broad quern of opinion.

Placing dots required extensive collaboration and ‘a lot of arguing’ among community members:

You try to get consensus from your peers … they demand evidence even though it’s difficult to find. They want you to launch a good argument, and they want you to defend your placement of that dot. It’s a lot of collaboration, a lot of communication, a lot of arguing, [and] a lot of meetings before everyone feels comfortable that, if challenged, they can defend it.

By, for example, pushing analysts to not only crystallise and polish opinions but also ‘defend’ them, the frequent (and at times intense) conversations that ensue aided the production and testing of judgements. As another analyst characterises, ‘if you can convince somebody that this [dot] deserves to be right up on the right-hand side of that [HCC], then [the innovation] has truly arrived, and it’s ready to be a mainstream product’ (A3, interview).

6.7 Timing: Shaping Market Actors’ Investment Decisions

A final challenge for analysts is positioning technologies within the HCC in a way that aligns with evolving market dynamics – a process we term timing. However, this plotting process involves an ongoing balancing act as analysts navigate the risks of responding too quickly to speculative enthusiasm or delaying recognition of technological shifts. When hindsight reveals misjudgements, analysts must be adept at addressing missteps and performing repair acts.

6.7.1 Addressing Missteps

6.7.1.1 Too Late: Overlooking Transformative Technologies

The placement of technologies on the HCC has wide-ranging consequences, structuring vendor strategies and technology adoption rates and influencing broader industry expectations. Analysts recognise that adjustments to the HCC are not just descriptive but actively shape how market actors engage with new technologies. The idea that tools like the HCC actively influence market dynamics has become so deeply embedded in their practice that it is now ‘not much of a discussion point’ nor considered ‘controversial’ within the analyst community (interview, A2). This recognition reinforces their awareness that misjudgements in plotting HCCs are not merely analytical errors but can have significant implications for market dynamics.

As one analyst observed, while their primary goal is ‘trying to measure and get a sense of an emerging technology,’ they also acknowledge they have a ‘certain amount of influence’ over which technologies make it onto the [HCC]’ (A3, interview). The plotting process is not neutral; it involves deliberate ‘filtering’, where only a select group of technologies – those considered most ‘relevant to [their] audience’ (A3, interview) – are included. Rather than attempting to map all innovations, analysts prioritise those they believe will resonate with their clients.

A key risk in this filtering process is that analysts may overlook or underestimate the importance of specific vendor claims. This can result in the omission or delayed recognition of technologies that later prove to be critical, ultimately causing their clients to miss out on emerging opportunities. For instance, an informant recalls how they initially dismissed the ‘smartphone’s’ potential and consequently did not include it in the HCC at all:

Did anybody really assess [the smartphone] correctly? I mean the smartphone starting with what Nokia came out with, with the N95s and whatnot back in the late ’90s, early 2000? See, that’s an interesting example. Did we or anybody actually call [out] how important or significant that was?… When the iPhone got introduced … did anybody really go ‘this is going to change the world?’ …Well yeah, it did. And I honestly … can’t remember if we or anybody actually called out … how much impact the smartphone was going to have on consumers, marketing [and] society.

Another factor that shapes how technologies appear on the HCC is the persistence of certain long-standing entries – what analysts refer to as ‘perennial favourites’. Analysts invest considerable time and effort in establishing themselves as recognised experts in the field – making a personal investment in their status. The high standing of a specialist analyst depends on their ability to identify and position themselves as a leading authority. Thus, because analysts invest time and professional credibility in evaluating specific technologies, there can be a reluctance to remove or downgrade those which have been prominently featured for extended periods. As one analyst noted, this reluctance can lead to stagnation in the HCC’s representation of emerging technologies, preventing clients from being informed about the full spectrum of potential opportunities:

In terms of the [HCC] for [technology area, we] saw that there were a number of technologies that had become ‘perennial favourites’…. So, right at the beginning, I could not actually go for emerging technologies for 13 years, and because, you know, others have been on for long periods of time as well, and because we have limited ‘real estate’ on the [HCC].

6.7.1.2 Too Early: Advancing Technologies Prematurely

Conversely, there is also the challenge of positioning a technology too early within the HCC, signalling that it is more advanced than market evidence suggests. Premature repositioning can shape vendors’ allocation of resources and influence how market actors perceive a technology’s trajectory. Analysts acknowledged that ‘sometimes the vendors … will change what they’re doing to adapt to the [HCC]’ (A4, interview). For example, vendors may prioritise certain technologies over others, accelerate development efforts, or scale back investment based on their placement within the tool (A4, interview).

Another consequence of premature repositioning is that it can generate excessive market optimism. One analyst described how market actors like technology adopters primarily use the tool to compare their current strategies with projected technology trajectories: ‘[they] compare what [they’re] currently doing to what is in the [HCC] to see if [they] can do a kind of current and future gap study’ (A3, interview). This includes determining: ‘What do [they] need to decommission? What do [they] keep? And what others should [they] look at?’ (A3, interview). Another informant describes how he worked with ‘big banks in the US’ who ‘would spend their innovation budget based on some of the [HCCs] they saw out there for their specific industry or for specific technology’ (webinar 1).

In some cases, market actors have interpreted premature movements in the HCC as confirmation that a specific technology was ready for large-scale adoption, leading to investment decisions that later proved problematic. One analyst recounted an instance where premature movement within the HCC created unintended market effects:

I’ve had clients say…. ‘You said this would move at a certain speed, and it’s languished, and we bought into it early, and we haven’t been able to deploy that as a result’. That’s happened, but earlier in my career. As I got wiser, with a little more diligence and a lot more trying to figure [out] whether or not that movement was real or imagined.

6.7.2 Performing Repair Acts

6.7.2.1 Too Late: Correcting Oversights and Rebuilding Credibility

As market observers and interpreters, analysts rely on the perceived reliability of the HCC to maintain their credibility. This credibility can be undermined when they overlook important technologies. For instance, when they failed to anticipate the rise of the smartphone, one industry commentator dismissed the HCC as a ‘complete waste of time’ (Goodwin, Reference Goodwin2023). Another noted that ‘every single truly transformative technology wasn’t ever tracked by the [HCC]’ (Molander, Reference Molander2023).

To mitigate the impact of such omissions, analysts engage in repair acts, adjusting the tool to account for past oversights. A key strategy involves incorporating previous misjudgements, such as missing the smartphone, into internal training, using these cases as cautionary lessons for newer analysts:

One of the things we kind of try to inculcate and kind of beat into our … new analysts’ heads is … ‘remember the smartphone’. Because I will tell you … a lot of people made fun of them: ‘Who’s going to pay [for] that; Who needs that?; I just want to make a phone call; ‘I just want to text; Who cares’? And well … almost 15 years later, we’ve seen what the impact has been of that. And so that’s the example I use a lot with our newer analysts: ‘Don’t look past that … keep an eye on that’…. You’re never going to be right with the [HCC] 100%.’

To prevent the HCC from becoming overly static with ‘perennial favourites’, analysts introduced a ‘shelf life’ rule, capping the duration a technology can remain on the tool before being removed. One analyst explained that this change aimed to prevent outdated entries from dominating the tool: ‘Technologies now have a maximum three-year shelf life on the [HCC]’ whereafter they are removed ‘and that is to free up real estate to introduce more technologies that our clients should be aware of’ (A3, interview). However, removing a technology from the HCC can create confusion – or even signal concerns – about its trajectory to the broader market. When, for example, the ‘Big Data’ dot was abruptly dropped from the HCC, many in the specific industry were ‘mortified’ (Ellis, Reference Ellis2015), and market commentators speculated whether this indicated that ‘the technology has not progressed as fast as initially expected’ (Woodie, Reference Woodie2014) and that its projected market potential was not being realised (Ellis, Reference Ellis2015).

6.7.2.2 Too Early: Managing Premature Advancements without Undermining Trust

What happens when analysts realise – or are informed – that they have prematurely advanced a technology, misrepresenting its maturity beyond what market evidence supports? As one analyst explains, ‘You don’t move [the technology] forward unless there’s real evidence of market changes, increased adoption, or other clear indicators’ (A4, interview). However, one rule remains firm if this misjudgement occurs: while a dot can progress along the curve, it cannot be moved to an earlier point. ‘We never go backwards’, the analyst stated. ‘You might let the market catch up, but you don’t move anything backwards’ (A4, interview). This practice aims to maintain the credibility of the HCC by creating the illusion of forward momentum, ensuring that every placement appears deliberate and informed. As the analyst elaborates:

You don’t move anything backwards. That’s admitting you’re wrong, I guess. Since you spent so much time putting it in the right place to begin with, and there’s so few new ones introduced every year – usually two every year – you spend so much time getting consensus about where to put it.

Yet, in practice, this rule is not consistently upheld. Our research reveals instances where technologies have indeed been moved backwards. In the HCC for artificial intelligence (AI), for example, Edge AI and Cloud AI Services advanced in 2023, creating some excitement, but were repositioned backwards in 2024, leading to some confusion in the market (Ramel, Reference Ramel2024). However, when challenged, analysts rely on narrative adjustments rather than explicitly acknowledging errors, strategically framing these movements as refinements rather than reversals (Jaffri & Khandabattu, Reference Jaffri and Khandabattu2024). By incorporating additional commentary and new insights into subsequent iterations, they subtly recalibrate expectations while maintaining the perception of methodological rigour.

6.8 Discussion: Towards a Processual Understanding of Hype Purification

How analysts create tools to help market actors interpret and respond to hyped markets plays a vital role in emerging new technology industries. Yet the extant literature on market-making has paid scant attention to how analysts construct and operationalise these tools. We conducted a qualitative study of the original design and subsequent production and maintenance process for the HCC, where our findings show that analysts attempt to transform hype from unstructured noise into an interpretable market force, theorised as a process of ‘hype purification’. This new understanding contributes to research on tools and market-making, adds to the hype literature, and extends the emerging concept of hype management.

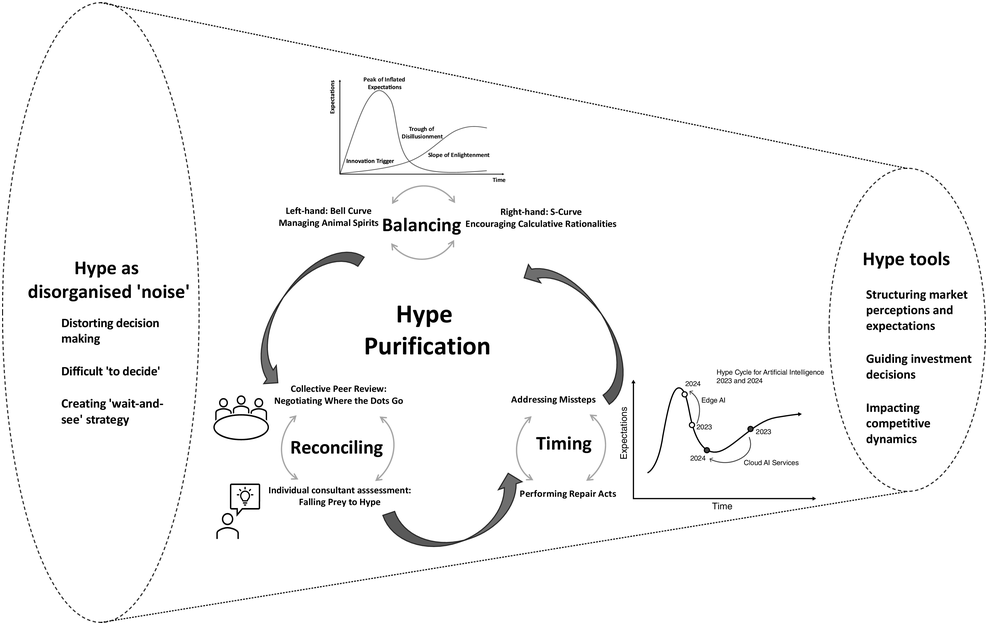

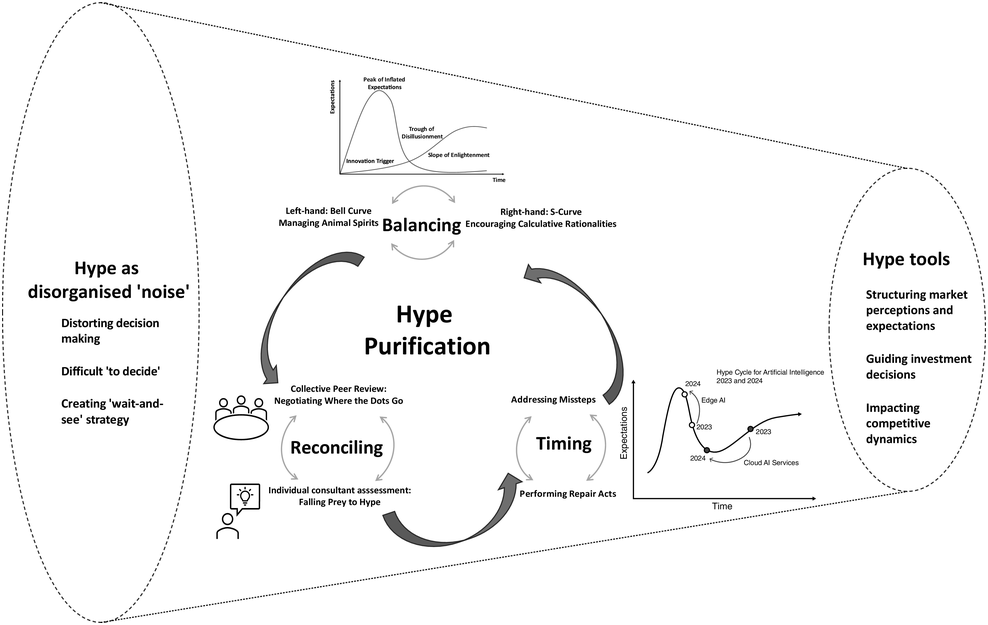

Our notion of hype purification refers to analysts’ attempts to distinguish between hype’s affective and calculative dimensions when creating tools like the HCC. We identify three mechanisms that help analysts contend with the complexities, tensions, and contradictions of purifying hype – balancing, reconciling, and timing (see Figure 6.4).

Figure 6.4 Long description

The diagram depicts a process called Hype Purification involving two main elements: Hype as disorganized noise and Hype tools. The central process involves a cycle with the following stages:

Balancing: Connects the left-hand Bell Curve (Managing Animal Spirits) and the right-hand S-Curve (Encouraging Calculative Rationalities). Hype Purification: The central concept of the diagram. Reconciling: Includes Collective Peer Review: Negotiating Where the Dots Go and Individual consultant assessment: Falling Prey to Hype. Timing: Includes Addressing Missteps and Performing Repair Acts.

The Hype as disorganized noise lists the following: Distorting decision making Difficult to decide Creating wait-and-see strategy

The Hype tools are as follows: Structuring market perceptions and expectations Guiding investment decisions Impacting competitive dynamics

There are two graphs: Top Graph: A typical hype cycle graph with Innovation Trigger, Peak of Inflated Expectations, Trough of Disillusionment, and Slope of Enlightenment labeled on the curve. Bottom Graph: A hype cycle for Artificial Intelligence 2023 and 2024, showing Edge A I in 2024 and Cloud A I Services in 2024.

The first mechanism, balancing, refers to how analysts structure the relationship between hype’s emotional (excitement, speculation) and calculative (evidence, feasibility) dimensions in a two-sided graph. Rather than fully separating these elements, they seek to balance two rationales – what we label ‘animal spirits’ and ‘calculative rationalities’ (Beckert, Reference Beckert2016) – and navigate the tension that arises from their interaction. The left-hand side of the tool is dominated by animal spirits – the surge of excitement and speculation accompanying emerging technologies. This curve indicates the volatility of early-stage hype and the potential risks associated with premature investment. As enthusiasm and attention build, market actors are prompted to view emerging technologies as ‘hopeful monstrosities’ (Mokyr, Reference Mokyr1990) and reflect on the risks and consequences of entering a market too soon.

Conversely, the right-hand side of the tool illustrates the transition to calculative rationalities as more evidence accumulates regarding a technology’s feasibility and commercial potential. This shift encourages market actors to adopt an investor mindset (Chiapello, Reference Chiapello2015; Birch & Muniesa, Reference Birch and Muniesa2020), weighing risks and opportunities in a more structured manner. By visually distinguishing between these two dimensions, the tool does not eliminate hype but reframes it as an interpretable and structured phenomenon.

However, as Latour (2012) argues, purification efforts are always associated with multiple hybrids – messy interconnected realities that require management by deploying several complementary mechanisms.

The second mechanism, reconciling, shows that analysts are embedded in the promissory forces they seek to manage and could, for instance, become emotionally ‘attached’ (Hochschild, Reference Hochschild2011) to technologies, which we label as falling prey to hype. For example, analysts consistently retained specific technologies in the tool year after year (‘perennial favourites’), thereby delaying the recognition of newer innovations and leading to ‘errors of omission’ (Kumaraswamy et al., Reference Kumaraswamy, Garud and Ansari2018), which caused market actors to overlook emerging opportunities. To remedy this, the analysts’ judgements were subjected to collective scrutiny – a process we label as negotiating where the dots go.

The final mechanism, timing, involves moving technologies strategically from left to right on the tool, flagging technologies that may be transitioning between phases. However, while analysts sought to reinforce the idea that there are more and less favourable moments to invest, they could sometimes advance technologies through the tool too soon, contributing to ‘errors of commission’ (Kumaraswamy et al., Reference Kumaraswamy, Garud and Ansari2018), which encouraged market actors to enter markets prematurely.

We show that addressing missteps was critical as errors could become visible and consequential. Supporting prior findings that the tool’s ‘plausibility’ (Rindova & Martins, Reference Rindova and Martins2022) is essential for sustaining legitimacy, analysts engaged in repair acts, which involved codifying and refining ‘tool-based practices’ (Gond & Brés, Reference Gond and Brès2020). This suggests that while the HCC presents itself as a structured forecasting tool, it is, in reality, an evolving framework – one that adjusts to market shifts but does so silently and selectively, ensuring that its authority remains intact.

6.9 Theorising Hype Tools as a Market-Making Force

Our chapter contributes to the Market Studies literature (Geiger et al., Reference Geiger, Mason, Pollock, Roscoe and Ryan2024) by introducing a distinct and previously unexplored category of market device (Muniesa et al., Reference Muniesa, Millo and Callon2007) – ‘hype tools’. We defined hype tools in Chapter 2 as material and technical frameworks that shape hyped markets by guiding the timing of decision-making processes and market actions. Prior research has established that markets do not emerge autonomously (Ahrne et al., Reference Ahrne, Aspers and Brunsson2015; Geiger et al., Reference Geiger, Mason, Pollock, Roscoe and Ryan2024) but are actively constructed by various actors, including consultants and their tools, which play a pivotal role in organising and structuring markets (Pollock & D’Adderio, Reference Pollock and D’Adderio2012; Gond & Brès, Reference Gond and Brès2020).

However, while scholars have explored how tools shape market emergence and organisation, far less attention has been paid to how hype – an important market force – is structured, mediated, and sustained through tools. Specifically, we examine the HCC, one of the most influential and widely referenced tools in technology markets, which Beckert (Reference Beckert2016, p. 12) suggests is a ‘constitutive element of capitalist dynamics’. While previous studies have acknowledged the HCC’s role in shaping how market actors engage with and respond to hype (Pontikes & Barnett, Reference Pontikes and Barnett2017; Logue & Grimes, Reference Logue and Grimes2022; Wadhwani & Lubinski, Reference Wadhwani and Lubinski2025), the tool itself has yet to be systematically examined in terms of how it is constructed, maintained, and adjusted over time. In this chapter, we address these gaps by providing an in-depth analysis of the HCC, shedding light on its development, adaptation, and influence on market dynamics.

Moreover, prior research has pointed to the performativity of tools, suggesting that they do not merely describe market trends but actively produce and reinforce them (Callon, 1998; MacKenzie & Millo, Reference MacKenzie and Millo2003). However, rather than focusing solely on their performative effects, we have argued for a closer examination of how hype tools are designed and operationalised to exert influence in the market. As MacKenzie and Spears (Reference MacKenzie and Spears2014, p. 394) suggest, ‘[tools] do indeed have effects, but … exclusive attention to their effects occludes attention to the processes that shape [tools] and their development’. We extend this argument by shifting attention from the presumed performativity of hype tools to examining how they are continuously redesigned, thus offering one of the first empirical studies to capture the iterative, negotiated, and often contested processes involved in embedding, shaping, and reconfiguring a key tool to ensure that it remains performative by sustaining the attention of market players.

Scholars have highlighted that hype – and its institutionalisation through structured hype cycles – is expanding (Garud et al., Reference Garud, Snihur, Thomas and Phillips2023), creating a pressing need to understand better the mechanisms that govern how market actors navigate hyped markets (Pontikes & Barnett, Reference Pontikes and Barnett2017; Garud et al., Reference Garud, Lant and Schildt2021; Logue & Grimes, Reference Logue and Grimes2022). While existing research has explored how hype acts as an engine of economic dynamism (Beckert, Reference Beckert2016), a critical unanswered question remains: how do market actors interpret the ‘high hopes’ (Beckert, Reference Beckert2016) surrounding new markets and determine when they are ‘hot’ and when they are ‘passé’ (Pontikes & Barnett, Reference Pontikes and Barnett2017)? Previous studies have primarily explained these dynamics through ‘herding behaviour’ (Wüstenhagen et al., Reference Wüstenhagen, Wuebker, Bürer, Goddard, Truffer, Markard, Wüstenhagen and Wiek2009) or ‘self-perpetuating’ promissory narratives (Grodal & Granqvist, Reference Grodal, Granqvist, Ashkanasy, Zerbe and Härtel2014; Beckert, Reference Beckert2016).

However, these perspectives largely overlook the critical role of hype tools in structuring market perceptions. They do not fully account for how analysts actively monitor, categorise, and selectively amplify hype, shaping expectations, guiding investment decisions, and constructing trajectories of market development. Our chapter shows how the HCC introduces a shared language, framing hyped technologies within a structured trajectory that encourages early-stage caution while positioning later phases as business opportunities. Through directing attention and expectations, the HCC actively helps market participants navigate hyped markets by getting actors to consider their risk appetite in judging when to respond to market signals.

Finally, we highlight that, rather than a neutral mapping of technological trends, the HCC operates as a selective and highly curated tool, in which analysts deliberately ‘filter’ and ‘prioritise’ which technologies to include (Pollock & D’Adderio, Reference Pollock and D’Adderio2012). This filtering process ensures that only technologies deemed strategically relevant to clients are included. In other words, we show that hype is a ‘business issue’ that analysts actively manage and monetise, transforming the tool into a ‘sellable product’ that sustains client engagement and advisory services (Gond & Brès, Reference Gond and Brès2020, p. 721).

Furthermore, we reveal how analysts themselves are not immune to the forces of hype and may prematurely advance certain technologies, reinforcing promissory cycles or developing attachments to ‘perennial favourites’, keeping them on the tool well beyond their relevance. These tendencies can lead to feedback loops that shape investor sentiment and technological momentum, fostering what Patvardhan and Ramachandran (Reference Patvardhan and Ramachandran2020) term ‘artificial evolution’ – a process that propels market trajectories in unexpected, sometimes contradictory, directions. By conceptualising these dynamics, our chapter responds directly to Gond & Brès’ (Reference Gond and Brès2020, p. 721) call for deeper engagement with how consultants and their tools actively structure and recalibrate the ‘trajectory of markets’.

6.10 Hype Tools Balance Calculative and Affective Aspects

Our concept of hype tools advances existing research on hype by showing that it is not solely an emotionally charged phenomenon but also one in which distinct ‘calculative’ dimensions are constructed and enacted. Existing literature has prioritised accounts of hype’s affective dimensions, mainly the excitement and speculative fervour surrounding emerging technology markets (Grodal & Granqvist, Reference Grodal, Granqvist, Ashkanasy, Zerbe and Härtel2014; Geiger & Gross, Reference Geiger and Gross2017). For instance, Beckert (Reference Beckert2016, p. 32) describes hyped expectations as a ‘cognitive and emotional force that helps orient and animate the capitalist economy’, while Geiger and Gross (Reference Geiger and Gross2017, p. 451) highlight the ‘strong affective valence of hype’, noting how it fosters ‘feverish anticipation, expectations, and hope’. Yet, other research points to the tension between speculative enthusiasm (animal spirits) and structured decision-making (calculative rationalities) (Hirschman, Reference Hirschman2013). For instance, as Zaloom (Reference Zaloom2009, p. 246) argues, much contemporary business knowledge is organised around the dual influences of calculation and affect. However, existing research offers limited insight into how these two influences are managed and mediated in practice.

Our chapter addresses this gap by examining how analysts actively construct, operationalise, and sustain the interplay between affect and calculation – not as opposing forces but as co-constitutive elements that shape market dynamics. Rather than merely visualising hype cycles, the tool creates a negotiation space where affective excitement and calculative assessments are present and strategically balanced. By visually separating and contrasting hype’s emotional and calculative aspects in a structured framework such as a two-sided graph, the hype tool studied plays a critical role in framing hyped technology markets as viable spaces for intervention and investment. While the emotive dimension of hype fuels enthusiasm, it could also generate scepticism among decision-makers, perhaps leading to a wait-and-see approach (Endenich et al., Reference Endenich, Hahn, Reimsbach and Wickert2022).

However, the hype tool does not simply reflect this tension but actively shapes it by introducing a structured distinction between affect and calculability, which serves a dual rhetorical function. First, hype tools establish ‘affective credibility’ (Comer, Reference Comer2024) by recognising the emotional force of hype as a key driver of engagement with emerging technologies. Excitement, anticipation, and the imaginative dimensions of technological futures are crucial for resonance. A hype tool may struggle to connect with its audience without these elements. It risks losing relevance and credibility among market participants if analysts ‘over-purify’ their tools – stripping away speculative energy in favour of pure calculability. Second, it confers ‘calculative legitimacy’ (Doganova, Reference Doganova2024) by incorporating structured, measurable, and commensurable elements that frame hype as a navigable and structured phenomenon. By introducing notions of calculability, these tools reframe hype from speculative noise into an organised and interpretable process that market actors can strategically engage with.

6.11 Hype Tools Extend Processes of Hype Management

Scholars typically characterise hype and hype cycles as ‘unbounded’ and emerging spontaneously and unfiltered from within innovation communities (Garud et al., 2014). However, recent scholarship has introduced the concepts of ‘expectations management’ (Konrad & Alvial-Palavicino, Reference Konrad, Alvial-Palavicino, Konrad, Rohracher and von Schomberg2017) and ‘hype management’ (Logue & Grimes, Reference Logue and Grimes2022), reflecting a shift in how hype is understood – not merely as a destabilising influence but as a force that, under certain conditions, can be shaped and leveraged. As research on hype management gains prominence (Ometto et al., Reference Ometto, Lounsbury, Gehman, Felin, Foss and Zenger2023; Heupel et al., Reference Heupel, Fonseca, Rutherford and Edwards2024; Wood et al., Reference Wood, Dwyer and Scheaf2024; Wadhwani & Lubinski, Reference Wadhwani and Lubinski2025), scholars increasingly recognise the need to examine how market actors engage with hype and channel it as a strategic resource. While existing studies primarily focus on entrepreneurs as primary articulators of hyped expectations (Logue & Grimes, Reference Logue and Grimes2022), our chapter broadens this perspective by examining analysts and their role in designing tools that actively structure hype trajectories. This shifts the focus of hype management beyond individual and organisational actors to the industry-wide tools that sustain, regulate, and legitimise hype.

Our chapter builds on the hype management perspective by examining how analysts develop tools and practices that provide a ‘threshold of institutionalisation’ (Power, Reference Power2015, p. 48) to hype cycles. By framing hype as a staged and repeatable process, these tools embed a prevailing interpretation of hype cycles into market discourse, shaping how market actors perceive, engage with, and respond to hype, reinforcing expectations that hype cycles follow a structured trajectory – even though, in practice, technological developments remain contingent and uncertain (see van Lente et al., Reference Van Lente, Spitters and Peine2013).

However, while analysts seek to impose structure on hype, our findings reveal that hype management is anything but straightforward. Rather than working as authoritative guides (Porter, Reference Porter2004), hype tools are precarious instruments (Jackson, Reference Jackson, Wajcman and Dodd2017). Errors, misjudgements, and ‘discrepancies’ (Dedehayir & Steinert, Reference Dedehayir and Steinert2016) frequently emerge in the classification and positioning of technologies, requiring ongoing adjustments to sustain their credibility. This aligns with research on ‘invisible work’ (Justesen & Plesner, Reference Justesen and Plesner2024), highlighting how seemingly stable systems and frameworks rely on continuous, often unseen maintenance work. Our findings suggest that hype management is not solely about predicting technological trajectories; it is equally about repairing and recalibrating expectations to sustain the ‘plausibility’ of these tools (Rindova & Martins, Reference Rindova and Martins2022). (We return to the hype management concept in Chapter 9.)

6.12 Research Opportunities for Studying Hype Tools

We have only begun to scrape the surface of hype cycles and their role in market-making. While this chapter and book expand our understanding of how analysts and their tools actively shape the trajectory of hype in new technology markets, they also reveal opportunities for further research. Future studies could investigate further how hype tools actively shape competitive dynamics by channelling attention and investment into specific areas while marginalising others. This asymmetry in speculative interest warrants closer scrutiny, particularly in its role in market structuring. Research should more fully explore the extent to which those who judge the timing of a technology’s entry or exit from a hype cycle wield significant influence over industry resource allocation. Future work might examine in more detail how powerful consultants, in constructing and disseminating a ‘coherent field frame’ (Lo & Rhee, Reference Lo, Rhee, Lo and Rhee2022), strategically amplify or suppress innovations – decisions that can have far-reaching consequences. Studies might throw more light on whether analysts, by prematurely promoting a technology in a tool like the HCC, may fuel excitement and drive speculative investment, or by quietly ‘removing’ it, might introduce doubts about its viability – potentially leading to its ‘stigmatisation’ (Garud et al., Reference Garud, Snihur, Thomas and Phillips2023).

Future research could expand the scope of enquiry to encompass the broader ecosystem of actors and mechanisms involved in generating, filtering, and evaluating hype. A key area of interest is the role of other hype tools that shape organisational decision-making in uncertain technological landscapes. While the HCC remains the most prominent, other influential tools – such as McKinsey’s Tech Trends, WEF’s Top Ten Emerging Technologies, and Forrester’s Top Emerging Trends to Watch, to name a few – may also play a crucial role in shaping market expectations. Digitalisation has also given rise to algorithmic tools that track and quantify hype in real-time, including Google Trends, Brand24, HypeIndex, and Buzz.

Our study only had limited engagement with market players regarding how they utilise these tools. We explored how vendors respond to these tools but have not yet studied extensively how technology adopters act on them. Future research might address an intriguing range of issues. For example, how do these tools shape adopters’ perceptions of opportunities for action? What new practices and strategies emerge as market actors develop more sophisticated responses to hype? Exploring the extent to which the development of hype tools encourages market actors to build proactive or reactive approaches to hype would offer valuable insights into the evolving dynamics of hype tools and market-making.

The HCC is just one example of how analysts attempt to reshape market actors’ disposition towards hype. Chapter 7 builds directly on the above analysis by turning to another critical dimension of this taming process: the categorisation of emerging technological trends. If Chapter 6 demonstrated how analysts guide market actors on when to act, Chapter 7 addresses how they help them decide what to act upon. Analysts provide a structured map of the innovation landscape by developing, revising, and retiring technology categories. These category frameworks, much like the HCC, are not passive reflections of technological developments but active devices for shaping market attention and organising vendor narratives.

Open access

Open access