I. Introduction

The neoclassical theory of investment has a long history. It has been developed, tested, and refined across many decades since the seminal work of Jorgenson (Reference Jorgenson1963) and Tobin (Reference Tobin1969). The neoclassical theory suggests that the rate of investment is a function of Tobin’s q, measured by the ratio of the market value of new additional investment goods to their replacement cost, an intuition that goes back to Keynes (Reference Keynes1936). The foundation of modern q theory in Lucas and Prescott (Reference Lucas and Prescott1971) and Mussa (Reference Mussa1977) is the firm’s optimization condition—the marginal adjustment and direct purchasing costs of investment being equal to the shadow value of capital. Relatedly, Hayashi (Reference Hayashi1982) shows that marginal q equals average q under standard assumptions. Average q is the usual empirical measure of q, defined as the ratio of the valuation of the firm’s existing capital stock to its replacement cost, and it is prone to measurement issues. However, some recent studies challenge the empirical applicability of the q theory, citing difficulties in accurately measuring q, and propose alternative approaches that predict firms’ investment decisions.

In this article, we investigate the relationship between a firm’s investment and q, for which an unobserved persistent shock to the investment cost function, such as information or technology shock, is an important factor in the firm’s investment decision, derived from the firm’s optimization problem. In our dynamic investment model to motivate the empirical investment equation, both the capital and the unobserved persistent shock are dynamic state variables; risk-neutral firms choose investment each period seeking to maximize the expected present value of their continuing future profits. For example, in this setting, firms experiencing a positive technology shock may face lower investment adjustment costs. Technological advances make equipment less expensive, make the investment process more efficient, and lead to improvements in the real investment opportunity set (Greenwood, Hercowitz, and Krusell (Reference Greenwood, Hercowitz and Krusell1997), Stiroh (Reference Stiroh2002), Fisher (Reference Fisher2006), and Kogan and Papanikolaou (Reference Kogan and Papanikolaou2014)). As a result, the q-measure may become endogenous in the firm’s investment equation if the unobserved shock is not properly accounted for. Importantly, we argue that incorporating the unobserved shock into the optimal investment function is essential, as this shock may directly impact capital adjustment costs, rather than solely influencing the firm’s production function. Nonetheless, we demonstrate that this channel of dependency is not precluded by the existing classical investment theory.

The empirical concern we address here is a new challenge to the potential measurement problem of marginal q. It has been studied relatively well in the literature (e.g., Hayashi (Reference Hayashi1982), Blanchard, Rhee, and Summers (Reference Blanchard, Rhee and Summers1993), and Erickson and Whited (Reference Erickson and Whited2000)), compared to the potential omitted variable problem we focus on. Unfortunately, controlling for measurement error in marginal q alone has been proven to be a difficult problem in the literature, as different empirical approaches taken to measurement errors rendered various and even contradictory conclusions on the roles of marginal q and internal funds in investment decisions. Addressing both the unobserved persistent shock and the measurement error problem is even more challenging. If the shock is omitted, not only does q become endogenous, but other observed regressors, such as cash flow or leverage, may also become endogenous. This underscores the critical importance of controlling for the unobserved persistent shock to estimate the investment function consistently.

To this end, we develop an econometric method that handles both issues. Our approach allows for time-varying investment adjustment costs and direct investment costs in firm-level panel data. Our identification strategy is based on a set of timing and information set assumptions about changes in the unobserved shock and adjustment costs. Given these restrictions, we derive moment conditions under which we identify both investment function parameters and dynamic parameters of the unobserved shock, and propose a Generalized Method of Moments (GMM) estimator. Our approach is robust to the endogeneity concerns in estimating the investment functions, where q is correlated with the unobserved persistent shock and subject to measurement error.

Methodologically, we utilize a panel data approach, building on a similar method proposed by Blundell and Bond (Reference Blundell and Bond1998), (Reference Blundell and Bond2000) and Bajari, Fruehwirth, Kim, and Timmins (Reference Bajari, Fruehwirth, Kim and Timmins2012). Our estimation approach also generalizes differencing approaches used to control for correlated time-varying confounders. However, our context and problems are substantially different from those of existing studies. This is because, in the context of investment functions, not only is q mismeasured, but also the unobserved persistent shock is potentially correlated with other factors of investment, such as q. In standard dynamic panel models, endogeneity arises because differencing to remove a firm fixed effect induces correlation between the lagged dependent variable as a regressor and the differenced error term. In our investment equation, this endogeneity is present regardless of a firm fixed effect.

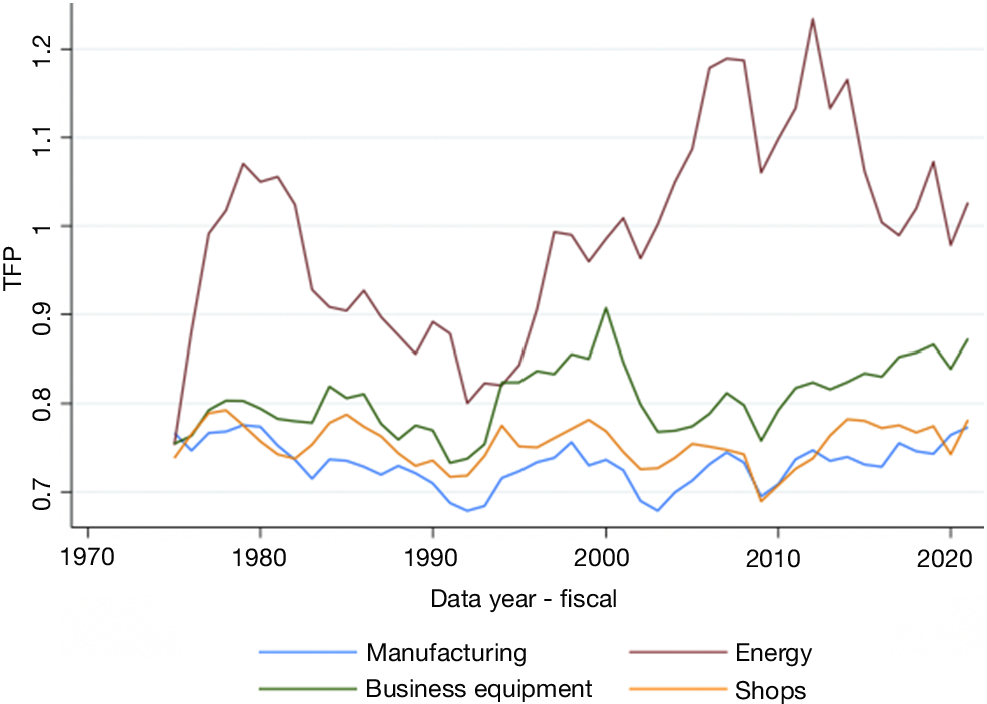

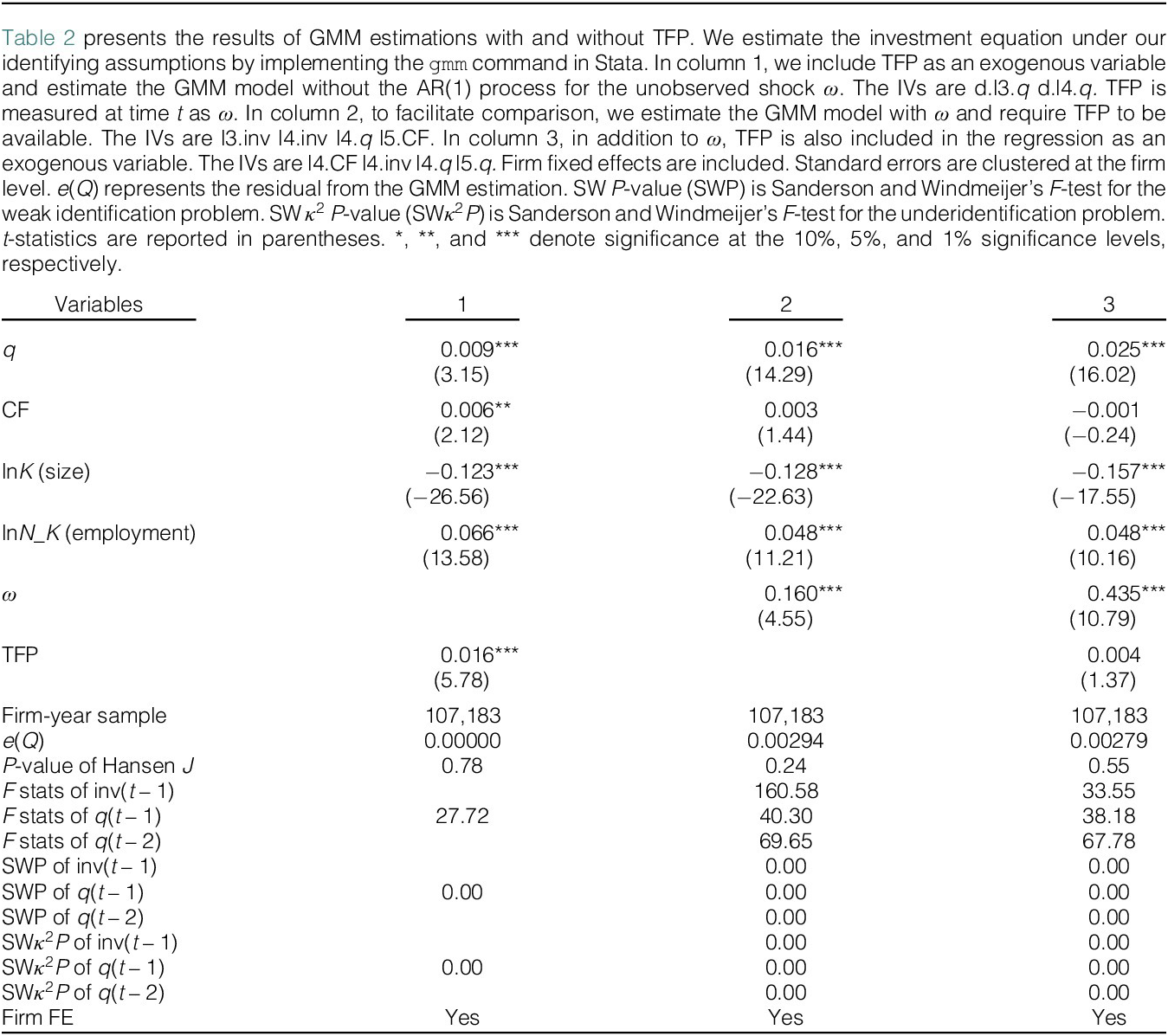

To motivate our insights on the unobserved persistent shock, we begin by incorporating the firm’s estimated total factor productivity (TFP) as an additional regressor and estimate the augmented investment equation. For this purpose, we utilize the TFP measure from İmrohoroǧlu and Tüzel (Reference İmrohoroǧlu and Tüzel2014), who estimate firm-level production functions using Olley and Pakes (Reference Olley and Pakes1996).Footnote 1 In particular, we estimate the investment equation both with and without TFP included as an additional observed state variable to assess whether our approach can effectively account for TFP when it is unobserved. We first proceed with a GMM estimator by including TFP as an additional observed state variable in place of the unobserved persistent shock. The results show that both q and TFP are statistically significant. We next estimate the investment equation using our proposed method to account for the unobserved persistent shock. It suggests that the unobserved persistent shock is significant. Importantly, q continues to be a significant factor even after the unobserved persistent shock is being controlled for. Lastly, to examine whether TFP contains information beyond that captured by the unobserved persistent shock, we include both TFP and the persistent shock in the investment function. Interestingly, once the unobserved shock is accounted for, TFP is no longer statistically significant. This suggests that our proposed method effectively captures the influence of the unobserved persistent shock, such as cost or technology shock, on investment decisions.Footnote 2

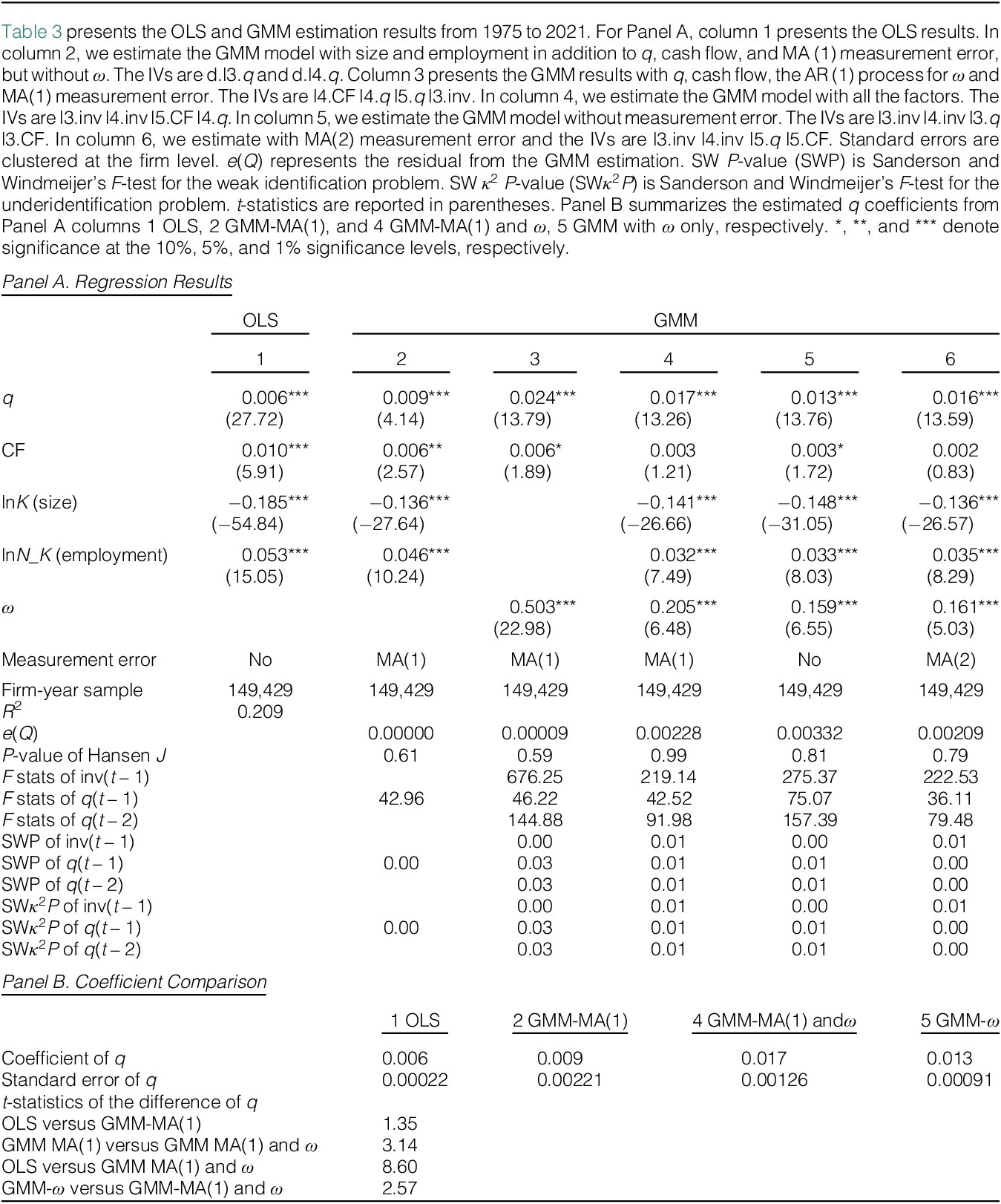

We also examine the investment equation both with and without controlling for measurement error in q. When the measurement error is ignored, the estimated coefficient on q is substantially smaller than when the error is properly accounted for. This highlights the importance and empirical relevance of addressing both the omitted persistent shock and measurement error. We also consider a case where the measurement error follows a more persistent process than the one assumed in our benchmark model. The estimation results remain very similar under this generalization, suggesting that our baseline specification performs effectively in the empirical setting.

We then conduct extensive empirical analyses, utilizing various measures of investment and q (for both physical and intangible measures) used in recent literature, for example, Peters and Taylor (Reference Peters and Taylor2017). Using 16,256 unique firms from 1975 to 2021, our empirical results indicate the importance of controlling for the unobserved persistent shock in estimating investment functions. Across all investment equations considered, we find that the unobserved persistent shock plays a significant role. Importantly, our finding indicates that q is still a significant factor in investment decisions, even after controlling for the unobserved persistent shock and measurement error in q.

We contribute to the literature on the empirics of corporate investment in several significant dimensions. First, to motivate our specification of the investment equation, we allow a firm’s adjustment cost of capital stock to depend on its unobserved persistent shock. We demonstrate that the optimal investment model is not only determined by q and other state variables but also by the unobserved persistent shock.

Second, we develop an estimation strategy for investment functions accounting for both endogeneity concerns due to the unobserved persistent shock and possibly mismeasured q. Our identifying moment conditions are derived from timing and information set assumptions that align with the firm’s optimal decision-making process and are well grounded in the principle of rational expectations. Moreover, our estimator is straightforward to implement using standard computing software. We offer a set of diagnostic tests for the moment conditions.

Third, our empirical analysis confirms that q remains an important factor of investment even when other state variables such as firm size, employment, and cash flow (or leverage) are controlled for. Furthermore, we find that investment becomes more sensitive to q after accounting for the unobserved persistent shock and the measurement error problems. This result holds for our subperiod analysis, alternative definitions of investment and q, and a variety of robustness checks.

The rest of the article proceeds as follows: Section II presents an investment model extending the models in Lucas and Prescott (Reference Lucas and Prescott1971) and Mussa (Reference Mussa1977), in which the unobserved persistent shock factors into a firm’s investment. Section III develops estimation methods. Section IV describes the data and variable construction. Section V reports the estimation results, and Section VI concludes.

II. Investment Model

To develop an empirical framework for an endogenous q model of investment in which both capital and the unobserved persistent shock are dynamic state variables, we present a simple standard dynamic investment model where risk-neutral firms choose investments each period to maximize the expected present value of continuing future profits. We use this simple dynamic investment model to motivate estimable equations and to discuss the nature of endogeneity problems in our empirical framework.

A. q Theory of Optimal Investment with Unobserved Shocks

We build on the original setting of Lucas and Prescott (Reference Lucas and Prescott1971) and Mussa (Reference Mussa1977) but, as an important point of departure, we allow for the unobserved persistent shock to enter the investment cost function. Here, we modify the dynamic investment model in Erickson and Whited (Reference Erickson and Whited2000), in which capital is the endogenous quasi-fixed factor and the unobserved persistent shock is another fixed factor that evolves exogenously following a dynamic process (e.g., a first-order Markov process). The value of the firm

$ i $

at time

$ i $

at time

$ t $

, from which the firm derives its optimal decision on investment to maximize the expected present value of the discounted flow of future profits, is given by

$ t $

, from which the firm derives its optimal decision on investment to maximize the expected present value of the discounted flow of future profits, is given by

$$ {V}_{it}=E\left[\sum \limits_{j=0}^{\infty}\left(\prod \limits_{s=1}^j{b}_{i,t+s}\right)\left[{\Pi}_{t+j}\left({K}_{i,t+j},{\varsigma}_{i,t+j}\right)-\psi \right({I}_{i,t+j},{K}_{i,t+j},{W}_{i,t+j},{\nu}_{i,t+j}\Big)|{\Omega}_{it}\right]. $$

$$ {V}_{it}=E\left[\sum \limits_{j=0}^{\infty}\left(\prod \limits_{s=1}^j{b}_{i,t+s}\right)\left[{\Pi}_{t+j}\left({K}_{i,t+j},{\varsigma}_{i,t+j}\right)-\psi \right({I}_{i,t+j},{K}_{i,t+j},{W}_{i,t+j},{\nu}_{i,t+j}\Big)|{\Omega}_{it}\right]. $$

Here,

$ E\left[\cdot |{\Omega}_{it}\right] $

is the conditional expectation operator and

$ E\left[\cdot |{\Omega}_{it}\right] $

is the conditional expectation operator and

$ {\Omega}_{it} $

denotes the information set available to firm i at time t;

$ {\Omega}_{it} $

denotes the information set available to firm i at time t;

$ {K}_{it} $

is the capital stock available at the beginning of period

$ {K}_{it} $

is the capital stock available at the beginning of period

$ t $

;

$ t $

;

$ {I}_{it} $

is the investment and

$ {I}_{it} $

is the investment and

$ {b}_{it} $

is the firm’s discount factor at time

$ {b}_{it} $

is the firm’s discount factor at time

$ t $

;

$ t $

;

$ {\Pi}_t\left({K}_{it},{\varsigma}_{it}\right) $

is the per period profit function, increasing in

$ {\Pi}_t\left({K}_{it},{\varsigma}_{it}\right) $

is the per period profit function, increasing in

$ {K}_{it} $

, with

$ {K}_{it} $

, with

$ {\varsigma}_{it} $

being the shock to the profit function;

$ {\varsigma}_{it} $

being the shock to the profit function;

$ \psi \left({I}_{it},{K}_{it},{W}_{it},{\nu}_{it}\right) $

is the investment cost function including both the cost of adjusting the stock of capital and the direct purchase or sale cost of investment, where

$ \psi \left({I}_{it},{K}_{it},{W}_{it},{\nu}_{it}\right) $

is the investment cost function including both the cost of adjusting the stock of capital and the direct purchase or sale cost of investment, where

$ {\nu}_{it} $

is an exogenous shock to adjustment cost.

$ {\nu}_{it} $

is an exogenous shock to adjustment cost.

$ {W}_{it} $

denotes the vector of state variables other than capitals, which may include technology shock, demand and cost shocks, and other aggregate shocks.

$ {W}_{it} $

denotes the vector of state variables other than capitals, which may include technology shock, demand and cost shocks, and other aggregate shocks.

The cost function

$ \psi \left({I}_{it},{K}_{it},{W}_{it},{\nu}_{it}\right) $

is increasing in

$ \psi \left({I}_{it},{K}_{it},{W}_{it},{\nu}_{it}\right) $

is increasing in

$ {I}_{it} $

, decreasing in

$ {I}_{it} $

, decreasing in

$ {K}_{it} $

, and convex in the first two arguments. The shocks

$ {K}_{it} $

, and convex in the first two arguments. The shocks

$ \left({\varsigma}_{it},{\nu}_{it}\right) $

and state variables

$ \left({\varsigma}_{it},{\nu}_{it}\right) $

and state variables

$ {W}_{i,t} $

are observed by the firm at time

$ {W}_{i,t} $

are observed by the firm at time

$ t $

, but these shocks and some components of

$ t $

, but these shocks and some components of

$ {W}_{it} $

may not be fully observed by the econometrician. Finally, note that any other variable factors of production in the profit function (e.g., labor or materials) have already been optimized following static optimization problems by the firm. Also, for ease of notation, other observed factors are implicit and suppressed. For estimation, we will decompose

$ {W}_{it} $

may not be fully observed by the econometrician. Finally, note that any other variable factors of production in the profit function (e.g., labor or materials) have already been optimized following static optimization problems by the firm. Also, for ease of notation, other observed factors are implicit and suppressed. For estimation, we will decompose

$ {W}_{it} $

into observed factors and the unobserved persistent shock. We will add these additional factors in our empirical investment equation specifications later.

$ {W}_{it} $

into observed factors and the unobserved persistent shock. We will add these additional factors in our empirical investment equation specifications later.

The firm maximizes the expected present value of the future profits

$ {V}_{it} $

, subject to the capital stock accumulation identity

$ {V}_{it} $

, subject to the capital stock accumulation identity

$$ {K}_{i,t+1}=\left(1-{d}_i\right){K}_{it}+{I}_{it}, $$

$$ {K}_{i,t+1}=\left(1-{d}_i\right){K}_{it}+{I}_{it}, $$

where

$ {d}_i $

is the firm i’s capital depreciation. We then obtain the “marginal”

$ {d}_i $

is the firm i’s capital depreciation. We then obtain the “marginal”

$ {q}_{it} $

from

$ {q}_{it} $

from

$ \frac{\partial {V}_{it}}{\partial {K}_{it}} $

, which measures the benefit of adding an incremental unit of capital to the firm. The first-order condition for maximizing the value of the firm in equation (1), subject to equation (2), then yields

$ \frac{\partial {V}_{it}}{\partial {K}_{it}} $

, which measures the benefit of adding an incremental unit of capital to the firm. The first-order condition for maximizing the value of the firm in equation (1), subject to equation (2), then yields

$$ \frac{\partial \psi \left(\cdot \right)}{\partial {I}_{it}}\equiv {\psi}_I\left({I}_{it},{K}_{it},{W}_{it},{\nu}_{it}\right)={q}_{it}. $$

$$ \frac{\partial \psi \left(\cdot \right)}{\partial {I}_{it}}\equiv {\psi}_I\left({I}_{it},{K}_{it},{W}_{it},{\nu}_{it}\right)={q}_{it}. $$

In the original setting of Lucas and Prescott (Reference Lucas and Prescott1971) and Mussa (Reference Mussa1977) (see also Erickson and Whited (Reference Erickson and Whited2000)), which is common in the literature, a firm’s unobserved persistent shock does not enter the investment cost function. Our main innovation is to incorporate an additional source of unobserved firm heterogeneity into the firm’s investment decision problem. We develop an empirical investment equation that aligns with the theoretical model and propose a consistent estimation procedure that accounts for this unobserved factor. Importantly, our framework allows the unobserved persistent shock to influence the optimal investment decision not only through the production function but also by affecting the cost of investment. We argue that this feature remains consistent with the neoclassical theory of investment. The first-order condition above (equation (3)) highlights that incorporating the unobserved shock into the investment cost function

$ \psi \left(\cdot \right) $

is essential for the dependence of the optimal investment on the unobserved shock, given the marginal

$ \psi \left(\cdot \right) $

is essential for the dependence of the optimal investment on the unobserved shock, given the marginal

$ {q}_{it} $

. This is because the direct impact of this shock on the firm’s profit function

$ {q}_{it} $

. This is because the direct impact of this shock on the firm’s profit function

$ {\Pi}_t(\cdot ) $

through its production function is already subsumed in

$ {\Pi}_t(\cdot ) $

through its production function is already subsumed in

$ {q}_{it} $

, and the unobserved shock only shows up in the optimal investment through

$ {q}_{it} $

, and the unobserved shock only shows up in the optimal investment through

$ \psi \left(\cdot \right) $

as in equation (3).

$ \psi \left(\cdot \right) $

as in equation (3).

B. Empirical Model of Investment Equation

To develop an empirical framework, we now present an investment equation consistent with the firm’s optimal investment decision problem in equation (1). Write

$ {W}_{it}\equiv \left({Z}_{it},{\omega}_{it}\right) $

where

$ {W}_{it}\equiv \left({Z}_{it},{\omega}_{it}\right) $

where

$ {Z}_{it} $

represents the observed state variables, which may proxy for firm heterogeneity and demand factors, and

$ {Z}_{it} $

represents the observed state variables, which may proxy for firm heterogeneity and demand factors, and

$ {\omega}_{it} $

denotes the unobserved persistent shock. We consider a class of investment cost functions, including the cost of adjusting the stock of capital, as

$ {\omega}_{it} $

denotes the unobserved persistent shock. We consider a class of investment cost functions, including the cost of adjusting the stock of capital, as

$$ \psi \left({I}_{it},{K}_{it},{W}_{it},{\nu}_{it}\right)={K}_{it}\left[{\tilde{f}}_0\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right)+{\tilde{f}}_1\Big({Z}_{it},{\nu}_{it},{\omega}_{it}\Big)\frac{I_{it}}{K_{it}}+\frac{\gamma_{it}}{2}{\left(\frac{I_{it}}{K_{it}}\right)}^2\right], $$

$$ \psi \left({I}_{it},{K}_{it},{W}_{it},{\nu}_{it}\right)={K}_{it}\left[{\tilde{f}}_0\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right)+{\tilde{f}}_1\Big({Z}_{it},{\nu}_{it},{\omega}_{it}\Big)\frac{I_{it}}{K_{it}}+\frac{\gamma_{it}}{2}{\left(\frac{I_{it}}{K_{it}}\right)}^2\right], $$

where, in particular,

$ {\tilde{f}}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right) $

denotes the linear adjustment cost.

$ {\tilde{f}}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right) $

denotes the linear adjustment cost.

From equation (4), it is clear that the feature of the model that renders the investment function to depend on

$ {\omega}_{it} $

is specifically due to the linear adjustment cost

$ {\omega}_{it} $

is specifically due to the linear adjustment cost

$ {\tilde{f}}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right) $

, which is a function of the shock

$ {\tilde{f}}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right) $

, which is a function of the shock

$ {\omega}_{it} $

, not merely due to the investment cost function

$ {\omega}_{it} $

, not merely due to the investment cost function

$ \psi \left({I}_{it},{K}_{it},{W}_{it},{\nu}_{it}\right) $

depending on

$ \psi \left({I}_{it},{K}_{it},{W}_{it},{\nu}_{it}\right) $

depending on

$ {\omega}_{it} $

. For example, if we have

$ {\omega}_{it} $

. For example, if we have

$ {\tilde{f}}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right)={\tilde{f}}_1\left({Z}_{it},{\nu}_{it}\right) $

, the cost function still depends on

$ {\tilde{f}}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right)={\tilde{f}}_1\left({Z}_{it},{\nu}_{it}\right) $

, the cost function still depends on

$ {\omega}_{it} $

because of

$ {\omega}_{it} $

because of

$ {\tilde{f}}_0\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right) $

, but this additive adjustment cost does not enter the investment equation as we can see in equation (5). In the literature, it is also typically assumed that the adjustment cost parameter

$ {\tilde{f}}_0\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right) $

, but this additive adjustment cost does not enter the investment equation as we can see in equation (5). In the literature, it is also typically assumed that the adjustment cost parameter

$ {\gamma}_{it} $

is constant across firms as

$ {\gamma}_{it} $

is constant across firms as

$ \gamma $

(but it may vary by the time

$ \gamma $

(but it may vary by the time

$ t $

). Combining these, we obtain

$ t $

). Combining these, we obtain

$$ \frac{\partial \psi \left(\cdot \right)}{\partial {I}_{it}}\equiv {\psi}_I\left({I}_{it},{K}_{it},{W}_{it},{\nu}_{it}\right)={\tilde{f}}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right)+\gamma \frac{I_{it}}{K_{it}}={q}_{it}. $$

$$ \frac{\partial \psi \left(\cdot \right)}{\partial {I}_{it}}\equiv {\psi}_I\left({I}_{it},{K}_{it},{W}_{it},{\nu}_{it}\right)={\tilde{f}}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right)+\gamma \frac{I_{it}}{K_{it}}={q}_{it}. $$

This equation clearly indicates that

$ {q}_{it} $

is dependent on the unobserved persistent shock

$ {q}_{it} $

is dependent on the unobserved persistent shock

$ {\omega}_{it} $

, unless the linear adjustment cost

$ {\omega}_{it} $

, unless the linear adjustment cost

$ {\tilde{f}}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right) $

is independent of

$ {\tilde{f}}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right) $

is independent of

$ {\omega}_{it} $

. Finally, the above equation can be rewritten, as in the literature, yielding the investment equation for which now both

$ {\omega}_{it} $

. Finally, the above equation can be rewritten, as in the literature, yielding the investment equation for which now both

$ {q}_{it} $

and

$ {q}_{it} $

and

$ {\omega}_{it} $

enter as factors of investment:

$ {\omega}_{it} $

enter as factors of investment:

$$ {y}_{it}=\beta {q}_{it}-{f}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right), $$

$$ {y}_{it}=\beta {q}_{it}-{f}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right), $$

where

$ {y}_{it}=\frac{I_{it}}{K_{it}} $

,

$ {y}_{it}=\frac{I_{it}}{K_{it}} $

,

$ \beta =1/\gamma $

, and

$ \beta =1/\gamma $

, and

$ {f}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right)={\tilde{f}}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right)/\gamma $

. To develop a simple regression equation in line with the literature, we can let, for example,

$ {f}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right)={\tilde{f}}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right)/\gamma $

. To develop a simple regression equation in line with the literature, we can let, for example,

$$ {\tilde{f}}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right)=-{Z}_{it}\tilde{\theta}-\tilde{\alpha}{\omega}_{it}+{\nu}_{it}. $$

$$ {\tilde{f}}_1\left({Z}_{it},{\nu}_{it},{\omega}_{it}\right)=-{Z}_{it}\tilde{\theta}-\tilde{\alpha}{\omega}_{it}+{\nu}_{it}. $$

We then obtain the familiar regression equation as anFootnote

3 extension of Erickson and Whited (Reference Erickson and Whited2000) (equation (6) below becomes their equation (6) if we set

$ \theta =\alpha =0 $

):

$ \theta =\alpha =0 $

):

$$ {y}_{it}=\beta {q}_{it}+{Z}_{it}\theta +{\alpha \omega}_{it}+{u}_{it}, $$

$$ {y}_{it}=\beta {q}_{it}+{Z}_{it}\theta +{\alpha \omega}_{it}+{u}_{it}, $$

where

$ \theta =\tilde{\theta}/\gamma $

,

$ \theta =\tilde{\theta}/\gamma $

,

$ \alpha =\tilde{\alpha}/\gamma $

, and

$ \alpha =\tilde{\alpha}/\gamma $

, and

$ {u}_{it}=-{\nu}_{it}/\gamma $

. An important implication of this investment equation is that, if omitted in the regression, the unobserved persistent shock

$ {u}_{it}=-{\nu}_{it}/\gamma $

. An important implication of this investment equation is that, if omitted in the regression, the unobserved persistent shock

$ {\omega}_{it} $

is a potential source of endogeneity. It can be correlated with

$ {\omega}_{it} $

is a potential source of endogeneity. It can be correlated with

$ {q}_{it} $

, while

$ {q}_{it} $

, while

$ {u}_{it} $

is the usual exogenous shock. Note that, for ease of notation, other observed factors in both the profit and cost functions are included in

$ {u}_{it} $

is the usual exogenous shock. Note that, for ease of notation, other observed factors in both the profit and cost functions are included in

$ {Z}_{it} $

. These variables can be added to the empirical investment equation and may not create additional endogeneity problems once the omitted shock

$ {Z}_{it} $

. These variables can be added to the empirical investment equation and may not create additional endogeneity problems once the omitted shock

$ {\omega}_{it} $

is controlled for.

$ {\omega}_{it} $

is controlled for.

C. Interpretation of the Persistent Shocks

In this section, we set out our interpretation of the persistent shock

$ \omega $

in the context of the firm investment, adjustment costs, and Tobin’s

$ \omega $

in the context of the firm investment, adjustment costs, and Tobin’s

$ q $

literature. Investment adjustment costs are central to dynamic models of capital accumulation, as they determine the speed and efficiency with which firms respond to changes in economic conditions. Hayashi (Reference Hayashi1982) formalized the link between

$ q $

literature. Investment adjustment costs are central to dynamic models of capital accumulation, as they determine the speed and efficiency with which firms respond to changes in economic conditions. Hayashi (Reference Hayashi1982) formalized the link between

$ q $

and investment under convex adjustment costs, showing that marginal

$ q $

and investment under convex adjustment costs, showing that marginal

$ q $

governs optimal investment decisions in the presence of installation frictions. These costs arise because capital goods cannot be instantaneously installed without incurring inefficiencies, such as production disruptions or resource misallocation.

$ q $

governs optimal investment decisions in the presence of installation frictions. These costs arise because capital goods cannot be instantaneously installed without incurring inefficiencies, such as production disruptions or resource misallocation.

In dynamic investment models, unobserved persistent shocks, such as technological advancements or improvements in information efficiency, play a critical role in shaping firms’ investment behavior by influencing adjustment costs (Greenwood et al. (Reference Greenwood, Hercowitz and Krusell1997), Stiroh (Reference Stiroh2002), Fisher (Reference Fisher2006), and Kogan and Papanikolaou (Reference Kogan and Papanikolaou2014)). These shocks affect the marginal cost of capital adjustment, thereby altering optimal investment trajectories and the speed of capital accumulation. Enhanced information efficiency, for instance, reduces informational frictions and uncertainty, enabling firms to make more accurate and timely investment decisions. This improvement mitigates costs associated with misallocation, delays, and errors, ultimately fostering a more efficient allocation of resources and, in turn, firm productivity.

Similarly, positive technology shocks can lower the costs and time required to upgrade capital equipment or adopt new production technologies. For example, the diffusion of cloud computing and automation technologies has enabled firms to scale operations rapidly without incurring the high fixed costs traditionally associated with IT infrastructure upgrades. In manufacturing, the integration of advanced robotics has streamlined production processes, reducing downtime and adjustment costs during technology transitions. In the renewable energy sector, technological improvements in battery storage and solar panel efficiency have accelerated investment cycles, making capital upgrades less costly and more frequent.

Our interpretation of

$ q $

aligns with the existing literature on measurement error in

$ q $

aligns with the existing literature on measurement error in

$ q $

. As shown in equation (5),

$ q $

. As shown in equation (5),

$ q $

is on the right-hand side of the first-order condition and, in theory, it perfectly measures the marginal benefit of adding an incremental unit of capital to the firm. However, in practice, since it is unobserved and replaced with the average

$ q $

is on the right-hand side of the first-order condition and, in theory, it perfectly measures the marginal benefit of adding an incremental unit of capital to the firm. However, in practice, since it is unobserved and replaced with the average

$ q $

, it is subject to measurement error and may not fully reflect, for example, a firm’s productivity variation stemming from intangibles, information asymmetries, or market inefficiencies.

$ q $

, it is subject to measurement error and may not fully reflect, for example, a firm’s productivity variation stemming from intangibles, information asymmetries, or market inefficiencies.

Regarding how to handle this measurement issue in

$ q $

, we depart from the existing literature by introducing unobserved persistent shocks

$ q $

, we depart from the existing literature by introducing unobserved persistent shocks

$ \omega $

that affect adjustment costs on the left-hand side and can also capture, for example, firm productivity variation if it is not fully reflected in

$ \omega $

that affect adjustment costs on the left-hand side and can also capture, for example, firm productivity variation if it is not fully reflected in

$ q $

. In our model, the unobserved persistent shocks effectively streamline the investment process and improve overall productivity. We incorporate them in the structural models for the firm’s optimization problem, but we test the theory based on the reduced-form model in equation (5). As shown in the next section, the empirical findings confirm that the unobserved persistent shocks are statistically significant and economically important in corporate investment decisions. The results stay robust even for the investment model with the total

$ q $

. In our model, the unobserved persistent shocks effectively streamline the investment process and improve overall productivity. We incorporate them in the structural models for the firm’s optimization problem, but we test the theory based on the reduced-form model in equation (5). As shown in the next section, the empirical findings confirm that the unobserved persistent shocks are statistically significant and economically important in corporate investment decisions. The results stay robust even for the investment model with the total

$ q $

that includes both physical and intangible capital. Failure to account for these unobserved persistent shocks may lead to biased estimates of investment dynamics and misinformed policy prescriptions. Incorporating such factors into investment models is therefore essential for accurately capturing the interplay between technological progress, firm behavior, and economic outcomes.

$ q $

that includes both physical and intangible capital. Failure to account for these unobserved persistent shocks may lead to biased estimates of investment dynamics and misinformed policy prescriptions. Incorporating such factors into investment models is therefore essential for accurately capturing the interplay between technological progress, firm behavior, and economic outcomes.

III. Estimation Strategy

The endogeneity of

$ {q}_{it} $

due to the unobserved persistent shock

$ {q}_{it} $

due to the unobserved persistent shock

$ {\omega}_{it} $

is another important potential confounder in the regression of the investment function, in addition to the well-noted problem of the measurement issue of the marginal q. The mismeasurement of q relevant to the neoclassical theory of optimal investment can arise from several sources (see Hayashi (Reference Hayashi1982) and Erickson and Whited (Reference Erickson and Whited2000)). Marginal q is not usually equal to average q in realistic market settings, as originally noted by Hayashi (Reference Hayashi1982), unless constant returns to scale and perfect competition conditions are all satisfied. Another source of measurement error is the divergence of average q from marginal q due to inefficiencies in financial markets, as discussed by Blanchard et al. (Reference Blanchard, Rhee and Summers1993). Besides these issues, there remain several other empirical challenges to correctly measuring q.

$ {\omega}_{it} $

is another important potential confounder in the regression of the investment function, in addition to the well-noted problem of the measurement issue of the marginal q. The mismeasurement of q relevant to the neoclassical theory of optimal investment can arise from several sources (see Hayashi (Reference Hayashi1982) and Erickson and Whited (Reference Erickson and Whited2000)). Marginal q is not usually equal to average q in realistic market settings, as originally noted by Hayashi (Reference Hayashi1982), unless constant returns to scale and perfect competition conditions are all satisfied. Another source of measurement error is the divergence of average q from marginal q due to inefficiencies in financial markets, as discussed by Blanchard et al. (Reference Blanchard, Rhee and Summers1993). Besides these issues, there remain several other empirical challenges to correctly measuring q.

Here, we develop an estimation strategy that can handle both concerns of endogeneity in estimating the investment function (6), where

$ {q}_{it} $

is measured with error and is potentially correlated with

$ {q}_{it} $

is measured with error and is potentially correlated with

$ {\omega}_{it} $

. Our purpose is two-fold. First, we test whether the unobserved

$ {\omega}_{it} $

. Our purpose is two-fold. First, we test whether the unobserved

$ {\omega}_{it} $

is a relevant factor of investment (in addition to the usual suspects, such as cash flow or leverage, firm size, etc., as considered in the literature). Second, we develop an estimation of the investment function, which is robust to the potential measurement error in q.

$ {\omega}_{it} $

is a relevant factor of investment (in addition to the usual suspects, such as cash flow or leverage, firm size, etc., as considered in the literature). Second, we develop an estimation of the investment function, which is robust to the potential measurement error in q.

Our estimation strategy is based on a set of timing and information set assumptions about changes in the unobserved persistent shock and adjustment cost. Given these assumptions, we derive moment conditions under which we identify both investment function parameters and a dynamic parameter of the persistent shock

$ {\omega}_{it} $

. Our approach to tackling both concerns of endogeneity in estimating the investment function (6) is robust, whether q is correlated with the unobserved

$ {\omega}_{it} $

. Our approach to tackling both concerns of endogeneity in estimating the investment function (6) is robust, whether q is correlated with the unobserved

$ {\omega}_{it} $

and is measured with error.

$ {\omega}_{it} $

and is measured with error.

We adopt a panel data approach, extending the methods proposed by Blundell and Bond (Reference Blundell and Bond1998), (Reference Blundell and Bond2000) in production functions and Bajari et al. (Reference Bajari, Fruehwirth, Kim and Timmins2012) in hedonic models. Our estimation approach is similar in spirit to these generalized differencing approaches used for controlling for correlated time-varying confounders. An important difference is that unobserved

$ {\omega}_{it} $

in the investment function context is potentially correlated with other factors of investment, such as q, and this q itself is also mismeasured.

$ {\omega}_{it} $

in the investment function context is potentially correlated with other factors of investment, such as q, and this q itself is also mismeasured.

A. Modeling the Unobserved Persistent Shock

We consider the empirical investment equation that generalizes equation (6) as

$$ {y}_{it}={\alpha}_i+\beta {q}_{it}+{Z}_{it}\theta +{\omega}_{it}+{u}_{it}, $$

$$ {y}_{it}={\alpha}_i+\beta {q}_{it}+{Z}_{it}\theta +{\omega}_{it}+{u}_{it}, $$

where

$ {y}_{it} $

is the investment ratio and

$ {y}_{it} $

is the investment ratio and

$ {\alpha}_i $

is the firm fixed effect. Compared to the investment equation (6), without loss of generality, we normalize the coefficient on

$ {\alpha}_i $

is the firm fixed effect. Compared to the investment equation (6), without loss of generality, we normalize the coefficient on

$ {\omega}_{it} $

to be 1 because this persistent shock is an unobserved factor.

$ {\omega}_{it} $

to be 1 because this persistent shock is an unobserved factor.

The true

$ q $

may not be directly observable and can only be measured with error as

$ q $

may not be directly observable and can only be measured with error as

$ {q}_{it}={q}_{it}^{\ast }+{e}_{it} $

, where

$ {q}_{it}={q}_{it}^{\ast }+{e}_{it} $

, where

$ {q}_{it}^{\ast } $

and

$ {q}_{it}^{\ast } $

and

$ {e}_{it} $

denote the true

$ {e}_{it} $

denote the true

$ q $

and possible measurement error, respectively. The vector of state variables,

$ q $

and possible measurement error, respectively. The vector of state variables,

$ {Z}_{it} $

, includes other potential observable factors of investment, such as cash flow (or leverage) and firm size, which proxy for firm heterogeneity and demand shocks. These variables can be incorporated into the investment equation, and their inclusion in the estimation does not introduce additional endogeneity problems once the unobserved

$ {Z}_{it} $

, includes other potential observable factors of investment, such as cash flow (or leverage) and firm size, which proxy for firm heterogeneity and demand shocks. These variables can be incorporated into the investment equation, and their inclusion in the estimation does not introduce additional endogeneity problems once the unobserved

$ {\omega}_{it} $

is controlled for. However, if

$ {\omega}_{it} $

is controlled for. However, if

$ {\omega}_{it} $

is omitted, these additional observed factors, including cash flow, can become endogenous regressors as well. This highlights the importance of controlling for the unobserved persistent shock in the investment equation to consistently estimate coefficients of both q and other observed factors.

$ {\omega}_{it} $

is omitted, these additional observed factors, including cash flow, can become endogenous regressors as well. This highlights the importance of controlling for the unobserved persistent shock in the investment equation to consistently estimate coefficients of both q and other observed factors.

The investment equation contains two unobserved shocks,

$ {\omega}_{it} $

and

$ {\omega}_{it} $

and

$ {u}_{it} $

. Motivated by equation (5), here, we allow

$ {u}_{it} $

. Motivated by equation (5), here, we allow

$ {q}_{it} $

to be correlated with

$ {q}_{it} $

to be correlated with

$ {\omega}_{it} $

. Both

$ {\omega}_{it} $

. Both

$ {q}_{it} $

and

$ {q}_{it} $

and

$ {Z}_{it} $

are not correlated with the exogenous shock

$ {Z}_{it} $

are not correlated with the exogenous shock

$ {u}_{it} $

. Following a standard setting in the literature to deal with the persistent error (Olley and Pakes (Reference Olley and Pakes1996), Blundell and Bond (Reference Blundell and Bond2000)), we assume

$ {u}_{it} $

. Following a standard setting in the literature to deal with the persistent error (Olley and Pakes (Reference Olley and Pakes1996), Blundell and Bond (Reference Blundell and Bond2000)), we assume

$ {\omega}_{it} $

follows a Markov process, such as a simple autoregressive process of order 1 (AR(1)).Footnote

4

$ {\omega}_{it} $

follows a Markov process, such as a simple autoregressive process of order 1 (AR(1)).Footnote

4

Assumption III.1 Let

$ {\omega}_{it} $

be an unobserved persistent shock, a factor of the investment cost in equation (1). We assume that

$ {\omega}_{it} $

be an unobserved persistent shock, a factor of the investment cost in equation (1). We assume that

$$ {\omega}_{it}={\rho \omega}_{i,t-1}+{\xi}_{it}, $$

$$ {\omega}_{it}={\rho \omega}_{i,t-1}+{\xi}_{it}, $$

where

$ {\xi}_{it} $

denotes the innovation term in the process, and the dynamic parameter

$ {\xi}_{it} $

denotes the innovation term in the process, and the dynamic parameter

$ \rho $

satisfies

$ \rho $

satisfies

$ \left|\rho \right|<1 $

.

$ \left|\rho \right|<1 $

.

The investment equation can be estimated with or without the firm fixed effect

$ {\alpha}_i $

. We primarily focus on the case with the fixed effect in our approach; the estimation without the fixed effect can proceed without the first-order differences to remove the fixed effect, as in Section III.B below. For the empirical implementation of the estimator, in Section V, we provide more details on the model with and/or without the firm fixed effect.

$ {\alpha}_i $

. We primarily focus on the case with the fixed effect in our approach; the estimation without the fixed effect can proceed without the first-order differences to remove the fixed effect, as in Section III.B below. For the empirical implementation of the estimator, in Section V, we provide more details on the model with and/or without the firm fixed effect.

1. Estimation without Measurement Error

We first consider the model where

$ {q}_{it} $

is measured without error and we set

$ {q}_{it} $

is measured without error and we set

$ {q}_{it}={q}_{it}^{\ast } $

where

$ {q}_{it}={q}_{it}^{\ast } $

where

$ {q}_{it}^{\ast } $

denotes the true

$ {q}_{it}^{\ast } $

denotes the true

$ q $

. Applying generalized differencing to equation (7), we obtain

$ q $

. Applying generalized differencing to equation (7), we obtain

$$ {y}_{it}=\left(1-\rho \right){\alpha}_i+\rho {y}_{i,t-1}+\beta \left({q}_{it}-\rho {q}_{i,t-1}\right)+\left({Z}_{it}-\rho {Z}_{i,t-1}\right)\theta +{u}_{i,t}-\rho {u}_{i,t-1}+{\xi}_{it}. $$

$$ {y}_{it}=\left(1-\rho \right){\alpha}_i+\rho {y}_{i,t-1}+\beta \left({q}_{it}-\rho {q}_{i,t-1}\right)+\left({Z}_{it}-\rho {Z}_{i,t-1}\right)\theta +{u}_{i,t}-\rho {u}_{i,t-1}+{\xi}_{it}. $$

By taking the first-order differences to remove the firm fixed effect, we then obtain

$$ \Delta {y}_{it}=\rho \Delta {y}_{i,t-1}+\beta \left(\Delta {q}_{it}-\rho \Delta {q}_{i,t-1}\right)+\left(\Delta {Z}_{it}-\rho \Delta {Z}_{i,t-1}\right)\theta +\Delta {u}_{it}-\rho \Delta {u}_{i,t-1}+\Delta {\xi}_{it}. $$

$$ \Delta {y}_{it}=\rho \Delta {y}_{i,t-1}+\beta \left(\Delta {q}_{it}-\rho \Delta {q}_{i,t-1}\right)+\left(\Delta {Z}_{it}-\rho \Delta {Z}_{i,t-1}\right)\theta +\Delta {u}_{it}-\rho \Delta {u}_{i,t-1}+\Delta {\xi}_{it}. $$

We now utilize a set of timing and information set assumptions as our identifying conditions. We make the following assumptions.

Assumption III.2 Let

$ {u}_{it} $

be an idiosyncratic shock in the investment equation (7) and

$ {u}_{it} $

be an idiosyncratic shock in the investment equation (7) and

$ {\xi}_{it} $

be the innovation term in the persistent shock process (8). Let

$ {\xi}_{it} $

be the innovation term in the persistent shock process (8). Let

$ {Z}_{it} $

denote other observed factors of investment, which are conditionally mean independent of the innovation

$ {Z}_{it} $

denote other observed factors of investment, which are conditionally mean independent of the innovation

$ {\xi}_{it} $

. The shocks satisfy

$ {\xi}_{it} $

. The shocks satisfy

$$ E\left[{u}_{it}|{J}_{it}\right]=0,E\left[{u}_{i{t}^{\prime }}|{Z}_{it}\right]=0 $$

$$ E\left[{u}_{it}|{J}_{it}\right]=0,E\left[{u}_{i{t}^{\prime }}|{Z}_{it}\right]=0 $$

for all

$ t $

and

$ t $

and

$ {t}^{\prime } $

and

$ {t}^{\prime } $

and

$$ E\left[{\xi}_{it}|{J}_{i,t-1},{Z}_{it}\right]=0,\mathrm{or}\;E\left[\Delta {\xi}_{it}|{J}_{i,t-2},\Delta {Z}_{it},\Delta {Z}_{i,t-1}\right]=0 $$

$$ E\left[{\xi}_{it}|{J}_{i,t-1},{Z}_{it}\right]=0,\mathrm{or}\;E\left[\Delta {\xi}_{it}|{J}_{i,t-2},\Delta {Z}_{it},\Delta {Z}_{i,t-1}\right]=0 $$

where

$ {J}_{it} $

denotes the information available to the firm i at a point in time

$ {J}_{it} $

denotes the information available to the firm i at a point in time

$ t $

when the firm makes the investment decision.

$ t $

when the firm makes the investment decision.

Note that, by construction,

$ {J}_{it} $

includes all current observables at the time of the investment decision and their lags. For example,

$ {J}_{it} $

includes all current observables at the time of the investment decision and their lags. For example,

$ {J}_{it} $

may include

$ {J}_{it} $

may include

$ {q}_{it} $

,

$ {q}_{it} $

,

$ {Z}_{it} $

, and

$ {Z}_{it} $

, and

$ {y}_{i,t-1} $

(and their respective lags). However, for estimation, the valid instruments may consist of only a subset of

$ {y}_{i,t-1} $

(and their respective lags). However, for estimation, the valid instruments may consist of only a subset of

$ {J}_{it} $

or may include additional available variables, depending on the moment conditions, as detailed in our data-driven IV selection.

$ {J}_{it} $

or may include additional available variables, depending on the moment conditions, as detailed in our data-driven IV selection.

Assumption III.2 states that i)

$ {u}_{it} $

, the exogenous shock to adjustment cost, is not systematically over or underpredicted, given the information available at time t, and this shock is also strictly exogenous with respect to

$ {u}_{it} $

, the exogenous shock to adjustment cost, is not systematically over or underpredicted, given the information available at time t, and this shock is also strictly exogenous with respect to

$ {Z}_{it} $

. It also imposes that ii) the innovation of the persistent shock process is uncorrelated with any information available at time

$ {Z}_{it} $

. It also imposes that ii) the innovation of the persistent shock process is uncorrelated with any information available at time

$ t-1 $

or other observed factors

$ t-1 $

or other observed factors

$ {Z}_{it} $

; this is reasonable since

$ {Z}_{it} $

; this is reasonable since

$ {\omega}_{it} $

follows an exogenous Markov process. Note that this assumption allows other observed factors

$ {\omega}_{it} $

follows an exogenous Markov process. Note that this assumption allows other observed factors

$ {Z}_{it} $

to be correlated with

$ {Z}_{it} $

to be correlated with

$ {\omega}_{it} $

but not with the innovation term

$ {\omega}_{it} $

but not with the innovation term

$ {\xi}_{it} $

.

$ {\xi}_{it} $

.

In the dynamic panel literature, Assumption III.2 is often referred to as

$ {J}_{i,t-1} $

including “predetermined” variables. Our identifying conditions are also motivated by rational expectations in the sense that, given available information, a firm does not over or underinvest on average. In other words, from the available information, we cannot predict systematic over or underinvestment by firms. Ackerberg (Reference Ackerberg2023) further provides details on how these assumptions can be strengthened or relaxed. An important point he elaborates is that what matters is not only the timing of when firms choose the “predetermined” variables but also what they know at that time. In this sense, these restrictions are referred to as the timing and information set assumptions, not only timing assumptions.

$ {J}_{i,t-1} $

including “predetermined” variables. Our identifying conditions are also motivated by rational expectations in the sense that, given available information, a firm does not over or underinvest on average. In other words, from the available information, we cannot predict systematic over or underinvestment by firms. Ackerberg (Reference Ackerberg2023) further provides details on how these assumptions can be strengthened or relaxed. An important point he elaborates is that what matters is not only the timing of when firms choose the “predetermined” variables but also what they know at that time. In this sense, these restrictions are referred to as the timing and information set assumptions, not only timing assumptions.

These assumptions allow that

$ {q}_{it} $

is potentially endogenous, even being free of measurement error. Under Assumptions III.1 and III.2, we then obtain the moment condition

$ {q}_{it} $

is potentially endogenous, even being free of measurement error. Under Assumptions III.1 and III.2, we then obtain the moment condition

$$ E\left[\Delta {u}_{it}-\rho \Delta {u}_{i,t-1}+\Delta {\xi}_{it}|{J}_{i,t-2},\Delta {Z}_{it},\Delta {Z}_{i,t-1}\right]=0, $$

$$ E\left[\Delta {u}_{it}-\rho \Delta {u}_{i,t-1}+\Delta {\xi}_{it}|{J}_{i,t-2},\Delta {Z}_{it},\Delta {Z}_{i,t-1}\right]=0, $$

from which we obtain the moment condition for GMM estimation

$$ E\left[\Delta {y}_{it}-\left\{\rho \Delta {y}_{i,t-1}+\beta \left(\Delta {q}_{it}-\rho \Delta {q}_{i,t-1}\right)+\left(\Delta {Z}_{it}-\rho \Delta {Z}_{i,t-1}\right)\theta \right\}|{J}_{i,t-2},\Delta {Z}_{it},\Delta {Z}_{i,t-1}\right]=0. $$

$$ E\left[\Delta {y}_{it}-\left\{\rho \Delta {y}_{i,t-1}+\beta \left(\Delta {q}_{it}-\rho \Delta {q}_{i,t-1}\right)+\left(\Delta {Z}_{it}-\rho \Delta {Z}_{i,t-1}\right)\theta \right\}|{J}_{i,t-2},\Delta {Z}_{it},\Delta {Z}_{i,t-1}\right]=0. $$

2. Estimation with Measurement Error

Next, we consider the measurement error in

$ {q}_{it}={q}_{it}^{\ast }+{e}_{it} $

. The regression equation derived from equation (7) becomes

$ {q}_{it}={q}_{it}^{\ast }+{e}_{it} $

. The regression equation derived from equation (7) becomes

$$ {\displaystyle \begin{array}{c}\Delta {y}_{it}=\rho \Delta {y}_{i,t-1}+\beta \left(\Delta {q}_{it}-\rho \Delta {q}_{i,t-1}\right)+\left(\Delta {Z}_{it}-\rho \Delta {Z}_{i,t-1}\right)\theta \\ {}+\Delta {u}_{it}-\rho \Delta {u}_{i,t-1}+\Delta {\xi}_{it}-\beta \left(\Delta {e}_{it}-\rho \Delta {e}_{i,t-1}\right).\end{array}} $$

$$ {\displaystyle \begin{array}{c}\Delta {y}_{it}=\rho \Delta {y}_{i,t-1}+\beta \left(\Delta {q}_{it}-\rho \Delta {q}_{i,t-1}\right)+\left(\Delta {Z}_{it}-\rho \Delta {Z}_{i,t-1}\right)\theta \\ {}+\Delta {u}_{it}-\rho \Delta {u}_{i,t-1}+\Delta {\xi}_{it}-\beta \left(\Delta {e}_{it}-\rho \Delta {e}_{i,t-1}\right).\end{array}} $$

We further assume that the measurement error is not persistent in the sense that it is not correlated with lagged information

$ {J}_{i,t-1} $

, and is also not correlated with other observable factors of the investment

$ {J}_{i,t-1} $

, and is also not correlated with other observable factors of the investment

$ {Z}_{it} $

, as follows:

$ {Z}_{it} $

, as follows:

Assumption III.3 Let

$ {q}_{it}={q}_{it}^{\ast }+{e}_{it} $

, where

$ {q}_{it}={q}_{it}^{\ast }+{e}_{it} $

, where

$ {q}_{it}^{\ast } $

denotes the true q and

$ {q}_{it}^{\ast } $

denotes the true q and

$ {e}_{it} $

denotes its measurement error. The measurement error satisfies for all

$ {e}_{it} $

denotes its measurement error. The measurement error satisfies for all

$ t $

and

$ t $

and

$ {t}^{\prime } $

,

$ {t}^{\prime } $

,

$$ E\left[{e}_{it}|{J}_{i,t-1}\right]=0\hskip1em \mathrm{and}\hskip1.12em E\left[{e}_{i{t}^{\prime }}|{Z}_{it}\right]=0. $$

$$ E\left[{e}_{it}|{J}_{i,t-1}\right]=0\hskip1em \mathrm{and}\hskip1.12em E\left[{e}_{i{t}^{\prime }}|{Z}_{it}\right]=0. $$

This assumption about the measurement error commonly appears in the literature, which rules out

$ q $

being systematically mismeasured. This is a reasonable condition since the market’s perception of the firm’s true q is continuously updated by rationally incorporating information available at the market up to the current date. The assumption of the measurement error being uncorrelated with the first-order lagged information,

$ q $

being systematically mismeasured. This is a reasonable condition since the market’s perception of the firm’s true q is continuously updated by rationally incorporating information available at the market up to the current date. The assumption of the measurement error being uncorrelated with the first-order lagged information,

$ {J}_{i,t-1} $

, is plausible, given the annual frequency of the data that is empirically used to estimate the investment equation. For instance, if the measurement error follows a moving average process of order 1 (MA(1)), the assumption is satisfied. It follows from this assumption that

$ {J}_{i,t-1} $

, is plausible, given the annual frequency of the data that is empirically used to estimate the investment equation. For instance, if the measurement error follows a moving average process of order 1 (MA(1)), the assumption is satisfied. It follows from this assumption that

$$ E\left[\Delta {e}_{it}|{J}_{i,t-2},{Z}_{it}\right]=0\hskip1.12em \mathrm{and}\hskip1.12em E\left[\Delta {e}_{i,t-1}|{J}_{i,t-3},{Z}_{it}\right]=0. $$

$$ E\left[\Delta {e}_{it}|{J}_{i,t-2},{Z}_{it}\right]=0\hskip1.12em \mathrm{and}\hskip1.12em E\left[\Delta {e}_{i,t-1}|{J}_{i,t-3},{Z}_{it}\right]=0. $$

By combining these conditional moment conditions, we then obtain

$$ E\left[\Delta {e}_{it}-\rho \Delta {e}_{i,t-1}|{J}_{i,t-3},\Delta {Z}_{it},\Delta {Z}_{i,t-1}\right]=0. $$

$$ E\left[\Delta {e}_{it}-\rho \Delta {e}_{i,t-1}|{J}_{i,t-3},\Delta {Z}_{it},\Delta {Z}_{i,t-1}\right]=0. $$

From this result, it is clear that, given Assumption III.3, the moment condition (9) can be made robust to the measurement error of

$ {q}_{it} $

by using the following moment condition:Footnote

5

$ {q}_{it} $

by using the following moment condition:Footnote

5

$$ E\left[\Delta {y}_{it}-\left\{\rho \Delta {y}_{i,t-1}+\beta \left(\Delta {q}_{it}-\rho \Delta {q}_{i,t-1}\right)+\left(\Delta {Z}_{it}-\rho \Delta {Z}_{i,t-1}\right)\theta \right\}|{J}_{i,t-3},\Delta {Z}_{it},\Delta {Z}_{i,t-1}\right]=0. $$

$$ E\left[\Delta {y}_{it}-\left\{\rho \Delta {y}_{i,t-1}+\beta \left(\Delta {q}_{it}-\rho \Delta {q}_{i,t-1}\right)+\left(\Delta {Z}_{it}-\rho \Delta {Z}_{i,t-1}\right)\theta \right\}|{J}_{i,t-3},\Delta {Z}_{it},\Delta {Z}_{i,t-1}\right]=0. $$

It is worth mentioning that most studies assume the classical measurement error in

$ q $

and do not allow for a persistent measurement error. Nevertheless, Assumption III.3 can be modified to allow for a more persistent measurement error; this would require changing the conditioning variables in the moment condition. In our empirical applications (Section V), we examine this scenario using a more persistent process and find that the measurement error process outlined in Assumption III.3 aligns more appropriately with the empirical settings.

$ q $

and do not allow for a persistent measurement error. Nevertheless, Assumption III.3 can be modified to allow for a more persistent measurement error; this would require changing the conditioning variables in the moment condition. In our empirical applications (Section V), we examine this scenario using a more persistent process and find that the measurement error process outlined in Assumption III.3 aligns more appropriately with the empirical settings.

With the use of additional notation, we can also allow the coefficients

$ \beta $

and

$ \beta $

and

$ \gamma $

to vary by time or period. In Section V, we provide further details on how to choose instruments to implement GMM estimation, based on these timing and information set assumptions.

$ \gamma $

to vary by time or period. In Section V, we provide further details on how to choose instruments to implement GMM estimation, based on these timing and information set assumptions.

B. Implementation of Estimation

We discuss here how to implement the GMM estimation for the investment equation (7), with measurement error in the measured

$ {q}_{it}={q}_{it}^{\ast }+{e}_{it} $

, where

$ {q}_{it}={q}_{it}^{\ast }+{e}_{it} $

, where

$ {q}_{it}^{\ast } $

denotes the true q. We consider two cases: the model without and with the firm fixed effect, respectively:

$ {q}_{it}^{\ast } $

denotes the true q. We consider two cases: the model without and with the firm fixed effect, respectively:

$$ {\iota}_{it}=\alpha +\beta {q}_{it}+{Z}_{it}\theta +{\omega}_{it}+{u}_{it}-\beta {e}_{it}, $$

$$ {\iota}_{it}=\alpha +\beta {q}_{it}+{Z}_{it}\theta +{\omega}_{it}+{u}_{it}-\beta {e}_{it}, $$

and

$$ {\iota}_{it}={\alpha}_i+\beta {q}_{it}+{Z}_{it}\theta +{\omega}_{it}+{u}_{it}-\beta {e}_{it}, $$

$$ {\iota}_{it}={\alpha}_i+\beta {q}_{it}+{Z}_{it}\theta +{\omega}_{it}+{u}_{it}-\beta {e}_{it}, $$

where we now use the notation

$ {\iota}_{it} $

, instead of

$ {\iota}_{it} $

, instead of

$ {y}_{it} $

, to denote various investment measures in our analyses.Footnote

6 Here

$ {y}_{it} $

, to denote various investment measures in our analyses.Footnote

6 Here

$ {\alpha}_i $

denotes the firm fixed effect;

$ {\alpha}_i $

denotes the firm fixed effect;

$ {\omega}_{it} $

denotes the unobserved persistent shock;

$ {\omega}_{it} $

denotes the unobserved persistent shock;

$ {u}_{it} $

is an exogenous shock to the adjustment cost;

$ {u}_{it} $

is an exogenous shock to the adjustment cost;

$ {e}_{it} $

is the measurement error in

$ {e}_{it} $

is the measurement error in

$ {q}_{it}^{\ast } $

.

$ {q}_{it}^{\ast } $

.

The model without the firm fixed effect, after applying the generalized differencing due to the AR(1) process of the persistent shock (8), yields

$$ {\displaystyle \begin{array}{c}{\iota}_{it}=\alpha \left(1-\rho \right)+{\rho \iota}_{i,t-1}+\beta \left({q}_{it}-\rho {q}_{i,t-1}\right)+\left({Z}_{it}-\rho {Z}_{i,t-1}\right)\theta \\ {}+{u}_{it}-\rho {u}_{i,t-1}+{\xi}_{it}-\beta \left({e}_{it}-\rho {e}_{i,t-1}\right).\end{array}} $$

$$ {\displaystyle \begin{array}{c}{\iota}_{it}=\alpha \left(1-\rho \right)+{\rho \iota}_{i,t-1}+\beta \left({q}_{it}-\rho {q}_{i,t-1}\right)+\left({Z}_{it}-\rho {Z}_{i,t-1}\right)\theta \\ {}+{u}_{it}-\rho {u}_{i,t-1}+{\xi}_{it}-\beta \left({e}_{it}-\rho {e}_{i,t-1}\right).\end{array}} $$

We note that the variables

$ \left\{{Z}_{it},{Z}_{i,t-1}\right\} $

satisfy the moment condition and serve as instruments for themselves, while the variables

$ \left\{{Z}_{it},{Z}_{i,t-1}\right\} $

satisfy the moment condition and serve as instruments for themselves, while the variables

$ \left\{{\iota}_{i,t-1},{q}_{it},{q}_{i,t-1}\right\} $

do not. Therefore, we can use the following set of further lagged variables as excluded instrumental variables (IVs), because they are not correlated with the error terms

$ \left\{{\iota}_{i,t-1},{q}_{it},{q}_{i,t-1}\right\} $

do not. Therefore, we can use the following set of further lagged variables as excluded instrumental variables (IVs), because they are not correlated with the error terms

$ \left[{u}_{it}-\rho {u}_{i,t-1}+{\xi}_{it}-\beta \left({e}_{it}-\rho {e}_{i,t-1}\right)\right]: $

$ \left[{u}_{it}-\rho {u}_{i,t-1}+{\xi}_{it}-\beta \left({e}_{it}-\rho {e}_{i,t-1}\right)\right]: $

$$ \left\{\begin{array}{c}{\iota}_{i,t-2},{\iota}_{i,t-3},{\iota}_{i,t-4},\dots \\ {}{q}_{i,t-2},{q}_{i,t-3},{q}_{i,t-4},\dots \\ {}{Z}_{i,t-2},{Z}_{i,t-3},{Z}_{i,t-4},\dots \end{array}\right\} $$

$$ \left\{\begin{array}{c}{\iota}_{i,t-2},{\iota}_{i,t-3},{\iota}_{i,t-4},\dots \\ {}{q}_{i,t-2},{q}_{i,t-3},{q}_{i,t-4},\dots \\ {}{Z}_{i,t-2},{Z}_{i,t-3},{Z}_{i,t-4},\dots \end{array}\right\} $$

We justify these IVs based on the assumptions about timing and information set, as discussed in the previous section, and we adopt data-driven criteria to select IVs among this set of variables, as we detail in Section III.C.

Define the vector of parameters

$ \vartheta \equiv {\left(\alpha, \beta, {\theta}^{\prime },\rho \right)}^{\prime } $

. Let

$ \vartheta \equiv {\left(\alpha, \beta, {\theta}^{\prime },\rho \right)}^{\prime } $

. Let

$ {H}_{it} $

be a

$ {H}_{it} $

be a

$ K\times 1 $

vector that stacks the IVs we select, given firm i and time t. Let

$ K\times 1 $

vector that stacks the IVs we select, given firm i and time t. Let

$ \hat{W} $

be a

$ \hat{W} $

be a

$ K\times K $

weighting matrix satisfying the

$ K\times K $

weighting matrix satisfying the

$ \hat{W}{\to}_pW $

condition, with a symmetric positive definite matrix W. The GMM estimator of

$ \hat{W}{\to}_pW $

condition, with a symmetric positive definite matrix W. The GMM estimator of

$ \vartheta $

is defined as

$ \vartheta $

is defined as

$$ \hat{\vartheta}\equiv {\mathrm{argmin}}_{\theta}\;{g}_n{\left(\vartheta \right)}^{\prime}\hat{W}{g}_n\left(\vartheta \right), $$

$$ \hat{\vartheta}\equiv {\mathrm{argmin}}_{\theta}\;{g}_n{\left(\vartheta \right)}^{\prime}\hat{W}{g}_n\left(\vartheta \right), $$

with

$$ {g}_n\left(\vartheta \right)\equiv \frac{1}{n}\sum \limits_{i=1}^n\sum \limits_{t={t}_0}^{T_i}{H}_{it}\cdot \left({\iota}_{it}-\alpha \left(1-\rho \right)-{\rho \iota}_{i,t-1}-\beta \left({q}_{it}-\rho {q}_{i,t-1}\right)-\left({Z}_{it}-\rho {Z}_{i,t-1}\right)\theta \right), $$

$$ {g}_n\left(\vartheta \right)\equiv \frac{1}{n}\sum \limits_{i=1}^n\sum \limits_{t={t}_0}^{T_i}{H}_{it}\cdot \left({\iota}_{it}-\alpha \left(1-\rho \right)-{\rho \iota}_{i,t-1}-\beta \left({q}_{it}-\rho {q}_{i,t-1}\right)-\left({Z}_{it}-\rho {Z}_{i,t-1}\right)\theta \right), $$

where

$ {t}_0 $

is determined by the availability of lagged variables in the instruments

$ {t}_0 $

is determined by the availability of lagged variables in the instruments

$ {H}_{it} $

, depending on the choice of lags in the instruments. Under standard regularity conditions for GMM, the estimator achieves consistency and asymptotic normality:

$ {H}_{it} $

, depending on the choice of lags in the instruments. Under standard regularity conditions for GMM, the estimator achieves consistency and asymptotic normality:

$$ \sqrt{n}\left(\hat{\vartheta}-\vartheta \right){\to}_dN\left(0,{V}_{\vartheta}\right), $$

$$ \sqrt{n}\left(\hat{\vartheta}-\vartheta \right){\to}_dN\left(0,{V}_{\vartheta}\right), $$

with the asymptotic variance–covariance matrix

$ {V}_{\vartheta } $

.

$ {V}_{\vartheta } $

.

Similarly, for the model with the firm fixed effect, after applying the generalized differencing to the first-differenced equation, we obtain

$$ {\displaystyle \begin{array}{c}\Delta {\iota}_{it}=\rho \Delta {\iota}_{i,t-1}+\beta \left(\Delta {q}_{it}-\rho \Delta {q}_{i,t-1}\right)+\left(\Delta {Z}_{it}-\rho \Delta {Z}_{i,t-1}\right)\theta \\ {}+\Delta {u}_{it}-\rho \Delta {u}_{i,t-1}+\Delta {\xi}_{it}-\beta \left(\Delta {e}_{it}-\rho \Delta {e}_{i,t-1}\right).\end{array}} $$

$$ {\displaystyle \begin{array}{c}\Delta {\iota}_{it}=\rho \Delta {\iota}_{i,t-1}+\beta \left(\Delta {q}_{it}-\rho \Delta {q}_{i,t-1}\right)+\left(\Delta {Z}_{it}-\rho \Delta {Z}_{i,t-1}\right)\theta \\ {}+\Delta {u}_{it}-\rho \Delta {u}_{i,t-1}+\Delta {\xi}_{it}-\beta \left(\Delta {e}_{it}-\rho \Delta {e}_{i,t-1}\right).\end{array}} $$

In this case, the variables

$ \left\{\Delta {Z}_{it},\Delta {Z}_{i,t-1}\right\} $

satisfy the moment condition, while the variables

$ \left\{\Delta {Z}_{it},\Delta {Z}_{i,t-1}\right\} $

satisfy the moment condition, while the variables

$ \left\{\Delta {\iota}_{i,t-1},\Delta {q}_{it},\Delta {q}_{i,t-1}\right\} $

do not. Then the following set of further lagged variables can be used as excluded IVs, because they are orthogonal to the error terms

$ \left\{\Delta {\iota}_{i,t-1},\Delta {q}_{it},\Delta {q}_{i,t-1}\right\} $

do not. Then the following set of further lagged variables can be used as excluded IVs, because they are orthogonal to the error terms

$ \left[\Delta {u}_{it}-\rho \Delta {u}_{i,t-1}+\Delta {\xi}_{it}-\beta \left(\Delta {e}_{it}-\rho \Delta {e}_{i,t-1}\right)\right] $

:

$ \left[\Delta {u}_{it}-\rho \Delta {u}_{i,t-1}+\Delta {\xi}_{it}-\beta \left(\Delta {e}_{it}-\rho \Delta {e}_{i,t-1}\right)\right] $

:

$$ \left\{\begin{array}{l}{\iota}_{i,t-3},{\iota}_{i,t-4},{\iota}_{i,t-5},\dots \\ {}{q}_{i,t-3},{q}_{i,t-4},{q}_{i,t-5},\dots \\ {}{Z}_{i,t-3},{Z}_{i,t-4},{Z}_{i,t-5},\dots \end{array}\right\}. $$

$$ \left\{\begin{array}{l}{\iota}_{i,t-3},{\iota}_{i,t-4},{\iota}_{i,t-5},\dots \\ {}{q}_{i,t-3},{q}_{i,t-4},{q}_{i,t-5},\dots \\ {}{Z}_{i,t-3},{Z}_{i,t-4},{Z}_{i,t-5},\dots \end{array}\right\}. $$

We note that the set of instruments consisting of the differenced version of the IVs can also be used in place of the IVs above:

$$ \left\{\begin{array}{l}\Delta {\iota}_{i,t-3},\Delta {\iota}_{i,t-4},\Delta {\iota}_{i,t-5},\dots \\ {}\Delta {q}_{i,t-3},\Delta {q}_{i,t-4},\Delta {q}_{i,t-5},\dots \\ {}\Delta {Z}_{i,t-3},\Delta {Z}_{i,t-4},\Delta {Z}_{i,t-5},\dots \end{array}\right\}. $$

$$ \left\{\begin{array}{l}\Delta {\iota}_{i,t-3},\Delta {\iota}_{i,t-4},\Delta {\iota}_{i,t-5},\dots \\ {}\Delta {q}_{i,t-3},\Delta {q}_{i,t-4},\Delta {q}_{i,t-5},\dots \\ {}\Delta {Z}_{i,t-3},\Delta {Z}_{i,t-4},\Delta {Z}_{i,t-5},\dots \end{array}\right\}. $$

Define the vector of parameters

$ \tilde{\vartheta}\equiv {\left(\beta, {\theta}^{\prime },\rho \right)}^{\prime } $

. Then, the GMM estimator of

$ \tilde{\vartheta}\equiv {\left(\beta, {\theta}^{\prime },\rho \right)}^{\prime } $

. Then, the GMM estimator of

$ \tilde{\vartheta} $

is defined as in equation (11):

$ \tilde{\vartheta} $

is defined as in equation (11):

$$ \hat{\tilde{\vartheta}}\equiv {\mathrm{argmin}}_{\tilde{\vartheta}}\;{\tilde{g}}_n{\left(\tilde{\vartheta}\right)}^{\prime}\hat{W}{\tilde{g}}_n\left(\tilde{\vartheta}\right), $$

$$ \hat{\tilde{\vartheta}}\equiv {\mathrm{argmin}}_{\tilde{\vartheta}}\;{\tilde{g}}_n{\left(\tilde{\vartheta}\right)}^{\prime}\hat{W}{\tilde{g}}_n\left(\tilde{\vartheta}\right), $$

with

$$ {\tilde{g}}_n\left(\tilde{\vartheta}\right)\equiv \frac{1}{n}\sum \limits_{i=1}^n\sum \limits_{t={t}_1}^{T_i}{\tilde{H}}_{it}\cdot \left(\Delta {\iota}_{it}-\rho \Delta {\iota}_{i,t-1}-\beta \left(\Delta {q}_{it}-\rho \Delta {q}_{i,t-1}\right)-\left(\Delta {Z}_{it}-\rho \Delta {Z}_{i,t-1}\right)\theta \right). $$

$$ {\tilde{g}}_n\left(\tilde{\vartheta}\right)\equiv \frac{1}{n}\sum \limits_{i=1}^n\sum \limits_{t={t}_1}^{T_i}{\tilde{H}}_{it}\cdot \left(\Delta {\iota}_{it}-\rho \Delta {\iota}_{i,t-1}-\beta \left(\Delta {q}_{it}-\rho \Delta {q}_{i,t-1}\right)-\left(\Delta {Z}_{it}-\rho \Delta {Z}_{i,t-1}\right)\theta \right). $$

$ {\tilde{H}}_{it} $

denotes the vector that stacks the instruments equation (12) or equation (13), and

$ {\tilde{H}}_{it} $

denotes the vector that stacks the instruments equation (12) or equation (13), and

$ {t}_1 $

is determined by the availability of lagged variables in the instruments

$ {t}_1 $

is determined by the availability of lagged variables in the instruments

$ {\tilde{H}}_{it} $

, depending on the choice of lags in the instruments. We discuss our criteria for selecting instruments and provide some practical guidelines in Section III.C.

$ {\tilde{H}}_{it} $

, depending on the choice of lags in the instruments. We discuss our criteria for selecting instruments and provide some practical guidelines in Section III.C.

In practice, the proposed estimator is easy to implement in standard computing software. For illustrative purposes, we utilize the Stata command, gmm, to implement the proposed estimator in the empirical estimation. We use the robust option for the weighting matrix and cluster the standard errors of the parameter estimates at the firm level.

C. Selection of Instrumental Variables

We adopt data-driven criteria to select IVs that satisfy legitimate instrumental variable conditions. Since the number of IVs can be more than the number of endogenous variables as long as the moment condition is satisfied, in principle, the model can be overidentified. So, our first criterion is Hansen’s J-test for overidentification. To ensure consistency of the estimator and its desirable finite sample performance, IVs should not suffer from weak instrument problems. The second criterion is strong instrument tests. In particular, we consider Sanderson and Windmeijer’s F-tests for weak identification and underidentification since multiple endogenous variables exist at the moment condition for the investment equation. Third, we select the specification that minimizes the residual of the GMM objective function (11) or (14) as small as possible. This guarantees that the estimates are the global minimizers of the optimization problem. Lastly, we conduct AR(1) and AR(2) diagnostic tests on the regression residuals obtained from our estimation (using, e.g., Stata’s arima command). These tests examine whether the residuals exhibit first- or second-order serial correlation. The absence of significant higher-order autocorrelation provides additional support that our moment conditions are not misspecified and that the GMM framework is appropriately designed. These practical criteria guarantee that the selected instruments are valid and relevant for the moment conditions.

IV. Data and Construction of Variables

In this section, we describe the construction of the sample and the main variables. We construct the key variables of interest, following Peters and Taylor (Reference Peters and Taylor2017), Erickson and Whited (Reference Erickson and Whited2000), Hadlock and Pierce (Reference Hadlock and Pierce2010), and Gala, Gomes, and Liu (Reference Gala, Gomes and Liu2020).

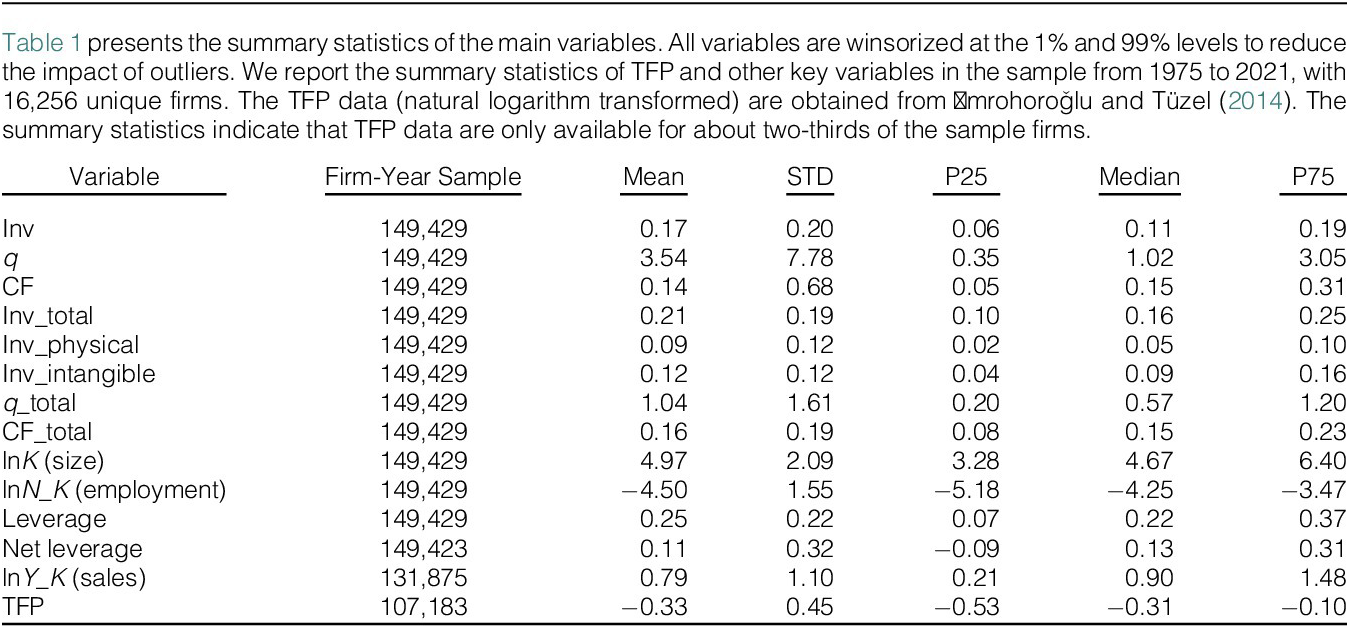

Our sample ranges from 1975 to 2021. The sample contains all Compustat North American firms, except for utility firms (SIC codes 4900–4999), financial firms (6000–6999), and firms identified as public service, international affairs, or nonoperating establishments (9000+). Using the standard procedure from the literature, we only include firms with nonmissing or non-negative book values of assets or sales and firms with at least $5 million in physical capital. The sample has 16,256 unique firms and 149,429 observations. We winsorize all regression variables at the 1% level to reduce the impact of outliers.

In the following, we describe our construction of the variables—investment, q, cash flow, firm size, employment-to-capital ratio, leverage, and sales—for our analysis. Standard investment is defined as capital expenditures (Compustat item capex) scaled by the replacement cost of physical capital (Compustat item ppegt). q is constructed as the firm’s market value scaled by the replacement of physical capital. The market value of a firm is defined as the market value of outstanding equity (Compustat items prcc_c times csho), plus the book value of debt (Compustat items dltt + dlc), minus the firm’s current assets (Compustat item act), which include cash, marketable securities, and inventory. Cash flow is the sum of income before extraordinary items (ib) and depreciation expense (dp) scaled by the replacement cost of physical capital. Firm size is the natural logarithm of physical capital stock, and employment-to-capital ratio is the natural logarithm of the number of employees scaled by the physical capital stock. We define leverage as the sum of long-term and short-term debt scaled by total assets, and net leverage as the total debt minus cash and short-term investments, scaled by total assets. We construct sales as sales normalized by physical capital. Table 1 reports summary statistics of the key variables. Detailed definitions of the firm’s physical, intangible, and total investment rates are provided in Appendix A.

V. Empirical Results

This section outlines our approach to estimating the empirical investment function and presents the results. Our primary objective is to investigate the well-established relationship between a firm’s investment and q, accounting for firm heterogeneity and the unobserved persistent shock. Specifically, we focus on standard investment, defined as capital expenditure scaled by physical capital, and later extend the analysis to other types of investment, including total, physical, and intangible investments.

A. Motivating Preliminary Analyses

We first estimate the investment equation using a higher-order polynomial OLS model, where a nonlinear function of the state variables, such as cash flow (CF), firm size (lnK), and employment (lnN_K), is considered as a benchmark drawn from the recent literature. In this literature, Gala et al. (Reference Gala, Gomes and Liu2020) argue that observed state variables explain corporate investment better than q and propose a flexible polynomial regression approach to avoid model misspecification, while Song and Wee (Reference Song and Wee2026) document heterogeneity in the investment-q relation, using nonlinear investment equations. The results are reported in Appendix B.