Policy Significance Statement

This article offers a blueprint for governments and social cash policymakers for leveraging data and artificial intelligence (AI)-led targeting practices, under an organisational governance framework, in response to the limitations of data/automated (non-AI) algorithmic targeting of beneficiaries. It offers practical recommendations for increasing the enrolment of beneficiaries through improved targeting practices that lead to their greater inclusion in times of crisis. The paper also carefully evaluates the benefits and risks of AI solutions, especially how the risks can be mitigated under a governance framework that underlines responsible and ethical organisational practices. Hence, the paper contributes to the development of data and social policy directives that have the potential to positively transform digital public services and society.

1. Introduction

In recent years, the frequency, severity, and complexity of climate-induced crisis have augmented, causing escalated levels of chronic poverty and shock-related vulnerabilities among marginalised households. Climate change, in particular, is escalating risks to human and ecological systems, affecting lives and livelihoods and increasing the vulnerability of populations (World Bank, 2022b, 2023). These impacts particularly concern populations in the Global South where countries have limited capacity to manage them, resulting in increased climate vulnerability (Anschell and Tran, Reference Anschell and Tran2021). Hence, governments and international agencies around the world are investing in responses that seek to address and minimise the impacts of climate change (Sengupta and Costella, Reference Sengupta and Costella2023). Among these initiatives, adaptive social protection (ASP) has emerged as a promising policy tool to increase resilience to shocks by reducing the vulnerability of households, communities, and social-ecological systems (Costella et al., Reference Costella, van Aalst, Georgiadou, Slater, Reilly, McCord, Holmes, Ammoun and Barca2023).

Traditionally, while social cash has primarily focussed on economic risks, there is growing demand and pressure for welfare programmes to respond to social, environmental and geopolitical crisis. ASP is a response to widespread demand for the use of social cash to build the resilience of poor and vulnerable households to these kinds of covariate shocks (Bowen et al., Reference Bowen, del Ninno, Andrews, Coll-Black, Gentilini, Johnson, Kawasoe, Kryeziu, Maher and Williams2020). ASP helps to build the resilience of poor and vulnerable households by investing in their capacity to prepare for, cope with, and adapt to shocks, protecting their wellbeing to ensure that they do not fall into poverty because of the negative impacts of these shock (World Bank, 2020, 2023). This implies that social protection programmes can include a longer-term vision of resilience that builds absorptive, adaptive, and eventually transformative capacities among beneficiaries to manage the impacts of climate change.

Given the large number of decisions that need to be made efficiently by governments in times of crisis, technologies including both automated and artificial intelligence (AI) applications can play a critical role within the social cash ecosystem (World Bank, 2023). In the public and social policy sphere, some governments have successfully deployed automated and AI machine learning algorithms to enhance efficiency, improve decision accuracy or offer more personalised services to citizens. The potential of these technologies to achieve the Sustainable Development Goals (SDGs) has captured interest of the international development community (Medaglia et al., Reference Medaglia, Gil-Garcia and Pardo2021a; Aiken et al., Reference Aiken, Bedoya, Blumenstock and Coville2023). There is also much optimism about the role of AI in delivering a wide spectrum of welfare benefits, including health care, food stamps, and income assistance (World Bank, 2020; Kaun et al., Reference Kaun, Larsson and Masso2024). For instance, AI may help improve the way governments evaluate eligibility and enrolment decisions, provide benefits and monitor and manage benefit delivery (Ohlenburg, Reference Ohlenburg2020).

While technology is pivotal in adaptive social cash systems, studies evidence that AI applications may help reap greater benefits for governments (Ohlenburg, Reference Ohlenburg2020; Aiken et al., Reference Aiken, Bedoya, Blumenstock and Coville2023). While some social protection programmes have already embraced non-AI algorithmic decision-making, very few have actually harnessed the potential of AI technologies in the welfare chain. A popular example is the Novissi programme from Togo that combined AI tools with cellular and geospatial datasets to identify vulnerable populations during the pandemic (Lawson et al., Reference Lawson, Koudeka, Martínez, Encinas and Karippacheril2023). Other countries from the Democratic Republic of Congo and Nigeria have followed suit (Okamura et al., Reference Okamura, Ohlenburg and Tesliuc2024).). However, it is argued that although AI may improve efficiency and the quality of welfare delivery, technologies on its own presents its own risks and challenges to society (Eubanks, Reference Eubanks2018).

While policymakers and practitioners have recognised the benefits of data and algorithmic decision-making in boosting the efficiency in social cash disbursements during crisis (Lawson et al., Reference Lawson, Koudeka, Martínez, Encinas and Karippacheril2023; Okamura et al., Reference Okamura, Ohlenburg and Tesliuc2024), the ethical and regulatory dilemmas at the organisational, societal, and individual levels require close scrutiny (Medaglia et al., Reference Medaglia, Gianluca and Vincenzo2021b). Other studies confirm that the potentially transformative power of algorithmic decision-making risks serious harm, especially if misused, as algorithmic decisions produce biased, discriminatory and unfair outcomes in several high-stakes social spheres (Slaughter et al., Reference Slaughter, Kopec and Batal2020; Starcevic, Reference Starcevic2022). While the legitimacy of algorithmic decision-making in the public sector has been studied by scholars (Henman, Reference Henman2020; Grimmelikhuijsen and Meijer, Reference Grimmelikhuijsen and Meijer2022), issues concerning governance have problematised the social cash sector.

We witnessed how the pandemic exposed gaps and limitations in routine social protection systems, including responding quickly to vulnerable populations affected by the crisis (Barca et al., Reference Barca, Archibald, Beazley and Little2020; Barca, Reference Barca2021). Invisibility and lack of information on certain vulnerable groups, such as informal workers in urban settings was a common hindrance to adequate policy response (Bastagli and Lowe, Reference Bastagli and Lowe2021; Okamura et al., Reference Okamura, Ohlenburg and Tesliuc2024). On the other hand, the pandemic also provided opportunities to many governments to adapt their primary social protection programmes (Barca et al., Reference Barca, Archibald, Beazley and Little2020; Barca, Reference Barca2021; Bastagli and Lowe, Reference Bastagli and Lowe2021; Lowe et al., Reference Lowe, McCord and Beazley2021; Okamura et al., Reference Okamura, Ohlenburg and Tesliuc2024). In Pakistan, the flagship—Benazir Income Support Programme (BISP)—Kafaalat scaled up its social safety net to support the poorest populations during the lockdown periods of the pandemic in 2020 (Almenfi et al., Reference Almenfi, Gentilini, Orton and Dale2020). The health crisis provided the impetus for BISP to adapt its programme design and exploit the country’s extant digital identity system, social registry, and technology infrastructure through institutional partnerships.

While Pakistan was still recovering from the aftershocks of the pandemic, the monsoon floods in 2022 presented another critical climate crisis for the country. One-third of the country’s population was submerged under water, affecting lives and livelihoods of around 33 million people. An estimated 6.4 million people were in need of assistance, while approximately over 1033 lives were lost, 287,000 houses destroyed, and more than 719,000 livestock died (United Nations, 2022). Against this backdrop, the BISP Emergency Flood Cash Programme was instantly rolled out—extending its routine BISP Kafaalat programme. Similar to the pandemic, the climate crisis created novel opportunities for BISP to leverage on the country’s vast digital infrastructure, utilising digital identity, and socioeconomic data, public datasets and an array of technologies (automated algorithms/data analytics) that it had invested in over the years to build a robust ASP system.

Drawing on the case study of the BISP Emergency Flood Cash Programme in Pakistan, the aim of the paper is to critically analyse the role of data/technology in targeting citizens during a climate crisis, distil lessons from the case, and develop guidance and governance framework for leveraging AI technology in and beyond emergency settings. This is based on the research questions, RQ1) What are the limitations in programme design and data/technology applications for targeting flood-affected beneficiaries? RQ2) What opportunities does AI offer in adaptive social cash design and how can the risks be mitigated through a governance framework?

Hence, the objectives are 1) critically evaluate the data/algorithm-led targeting progress to highlight the shortcomings pertaining to programme design and data/technologies, 2) discuss a comprehensive set of recommendations, 3) present future implications in deploying AI technologies based on the findings, and 4) design an AI governance framework—outlining ethical and responsible practices to mitigate the risks. This article provides rich theoretical, empirical and practical insights for social cash policymakers and practitioners in the data, policy, and development community. It contributes to the ongoing discourse on how exclusions are embedded in data and technology in adaptive social cash systems, and aspires to make a significant impact on both policy and practice within organisations and society, nationally and globally.

2. Adaptive social protection literature

A critical starting point for any ASP system is strengthening and building a routine social protection system, aiming to increase coverage and ensuring adequacy, comprehensiveness and sustainability at the policy, programme and delivery levels (Bowen et al., Reference Bowen, del Ninno, Andrews, Coll-Black, Gentilini, Johnson, Kawasoe, Kryeziu, Maher and Williams2020). The World Bank (2022b) has adopted a Global Crisis Response Framework that emphasises the importance of additional investments in ASP. Thus, ASP is viewed as a policy tool that can build climate resilience. In countries such as Honduras, Ethiopia, Madagascar and Pakistan, governments have developed their social cash infrastructure as part of their response strategy to climate-induced disasters since the early 2000s (World Bank, 2023).

2.1. Data and technology

The core component of ASP is data and technology, making social protection systems more adaptive, inclusive, resilient, and efficient. Digital identity data, registry data, and innovative technologies are crucial in ensuring that ASP programmes respond faster in times of crisis.

2.1.1. Digital identity data

Identity is a key component of the United Nations SDGs, so there is growing recognition of the importance of identity for socioeconomic development. Under SDG 16, the developmental role of identity pertains to promoting peaceful and inclusive societies for sustainable development, providing access to justice for all, and helping build effective, accountable and inclusive institutions at all levels (United Nations, 2015). Specifically, SDG 16.9 seeks to provide a legal identity for all, especially for the estimated 1 billion individuals who currently do not have access to a formal identity (World Bank, 2022a).

According to the Word Bank Identity for Development Report (ID4D, 2022a), identity refers to the combination of characteristics or attributes that make a person unique in a given context. While there are boundless personal attributes that are inherent to, chosen by, or ascribed to a person that make them unique, the particular attributes most relevant include core biographic data (e.g., name, age, address) and certain biometric features (e.g., a facial image, fingerprints, iris scans). Digital identity is a collection of electronically captured and stored identity attributes that uniquely describe a person within a given context and are used for electronic transactions (Gelb and Clark, Reference Gelb and Clark2013; World Bank, 2019). In this article, the term “digital identity” pertains to unique digital identity (ID) number conferred to citizens by government national identity management systems. These systems provide the foundational or legal biometric identity documents to citizens and manage the processes of data collection, storage and authentication of citizen’s individual identities (Whitley et al., Reference Whitley, Martin, Hosein, Boersma, Fonio and Wagenaar2014; Whitley, Reference Whitley2018).

Moreover, the increasing interest in digital ID from private/public and development sectors relates to their role in accessing a range of services, including social protection and humanitarian assistance (Whitley and Schoemaker, Reference Whitley and Schoemaker2022). Identification is fundamental to the receipt of social cash assistance, because personal details and biometric checks identify and validate citizen’s authenticity (Kemal and Shah, Reference Kemal and Shah2024). However, identity data often includes sensitive information that may put individuals at risk if accessed by unauthorised parties. In addition, digital identity systems provide a route for social and financial inclusion as gaining a legal identity is a prerequisite to access welfare services by marginalised communities (Kemal, Reference Kemal2019). Although countries like India have implemented Aadhaar-based identity verification to streamline social protection assistance, there are concerns related to data privacy, exclusion, and misuse. Masiero (Reference Masiero2020) highlights that biometric identity systems may inadvertently exclude marginalised populations, such as those lacking stable fingerprints or internet access. Additionally, the centralisation of identity data raises concerns about surveillance and data breaches (Gelb and Metz, Reference Gelb and Metz2018).

Social protection is hence at a threshold of digital change propelled by new technologies and the pressing need for adaptive and universal systems. While the use of digital technologies and identity data have characterised social protection, the integration of satellite and mobile data is developing owing to increased availability of data and evolution of computation methods and data analytics (Ohlenburg, Reference Ohlenburg2020; Okamura et al., Reference Okamura, Ohlenburg and Tesliuc2024).

2.1.2. Social registry data

Social registries play a prominent role in assessing eligibility criteria of citizens/households for social cash payments, such as welfare estimates (poverty) or demographic characteristics (Barca, Reference Barca2017; Barca and Hebbar, Reference Barca and Hebbar2020). In the context of social cash programmes, registry and databases are broadly interchangeable terms, indicating a data repository and a system to organise, store and retrieve large amounts of data (Chirchir and Barca, Reference Chirchir and Barca2020). Integrated registries combine data analytic technologies and their management information systems (MIS) across several programmes, linking data on beneficiaries into a data warehouse. Such registries provide consolidated information to support planning, coordination and monitoring (Barca, Reference Barca2017). Hence, registries serve as powerful tools to monitor and coordinate the “supply” of social programmes, particularly in identifying overlaps, gaps and duplications across multiple programmes, while supporting the consolidation of other functions along the delivery chain. They act as a nexus of information and provide interlinkages between different programme databases and other external databases, such as income tax, civil registration, and so forth (Barca et al., Reference Barca, Hebbar, Cote, Schoemaker, Enfield, Holmes and Wylde2021). Such integrated registries allow governments to identify vulnerable populations dynamically, thus improving the adaptability of social cash programmes (Chirchir and Barca, Reference Chirchir and Barca2020). Countries such as Brazil have used Cadastro Único to consolidate data across multiple programmes to enhance efficiency and reduce administrative costs (Lindert et al., Reference Lindert, George Karippacheril, Rodriguez Caillava and Nishikawa Chávez2020).

Integrated registries may be dynamic; to improve responsiveness by including real-time socioeconomic changes to the database in allowing beneficiaries to be added or removed based on evolving needs (Leite et al., Reference Leite, George, Sun, Jones and Lindert2017). Dynamic registries are extremely useful in times of economic shocks or humanitarian crisis (Barca et al., Reference Barca, Archibald, Beazley and Little2020). However, the quality of registry data depends on data collection methodologies, interoperability, and political will. Errors in data collection or outdated records may result in inclusion or exclusion errors, which reduces the effectiveness of social cash programmes (Barca, Reference Barca2017). In response to the pandemic, countries with high coverage of social registries and up-to-date information were able to deliver emergency cash to their target population more quickly and effectively, for example in Turkey, Chile, Brazil, Pakistan, and Jordan (Okamura et al., Reference Okamura, Ohlenburg and Tesliuc2024). However, those without registries were restricted in their capacity since registration and selection of new beneficiaries proved to be onerous in disbursing emergency assistance to populations not covered under basic social protection programmes that left some of the population “invisible” (Okamura et al., Reference Okamura, Ohlenburg and Tesliuc2024). Thus, for governments, it was plausible to make emergency payments to beneficiaries already present in a social registry (Gentilini et al., Reference Gentilini, Almenfi, Orton and Dale2021, 2022).

2.1.3. Automated (Non-AI) algorithms versus machine learning (AI) algorithms

An algorithm is defined as a finite series of well-defined, automated, computer implementable instructions. An automated algorithm performs simple repetitive tasks, while an AI machine learning algorithm is complex—designed to mimic humans and then performs tasks that they learn by observing patterns and outcomes through training data (OECD, 2024). According to the OECD (2024) definition, an AI system is “a machine learning-based system that (for explicit or implicit objectives) infers (from the input it receives) how to generate outputs such as predictions, content, recommendations, or decisions that can influence physical or virtual environments.” While all AI uses algorithms, not all algorithms use AI. Thus, the three main categories of machine learning algorithms vary between their training and function, comprising of supervised learning, unsupervised learning and reinforcement learning (OECD, 2024).

In the welfare sector, algorithms play a crucial role in optimising the distribution of social cash by automating eligibility assessments, predicting vulnerability, and detecting fraud payments (Ohlenburg, Reference Ohlenburg2020; Okamura et al., Reference Okamura, Ohlenburg and Tesliuc2024). Automated (non-AI) algorithms based on predictive modelling and computational statistics are typical in the social protection sector. For example, in Bangladesh, the pandemic response combined mobile phone, administrative and financial data to cover 5 million beneficiaries. In South America, the social enterprise, Prosperia.ai supported Colombia, Costa Rica, and Ecuador in the use of more effective automated predictive models for the disbursement of social cash (Okamura et al., Reference Okamura, Ohlenburg and Tesliuc2024).

On the other hand, machine learning AI algorithms can analyse large datasets to identify vulnerable populations more accurately than traditional targeting methods (Aiken et al., Reference Aiken, Bellows, Karlan and Udry2022, Reference Aiken, Bedoya, Blumenstock and Coville2023). For instance, Togo’s Novissi Model 2 used mobile phone records, household data, nontraditional data, and AI algorithms to identify poor households affected by the pandemic (Okamura et al., Reference Okamura, Ohlenburg and Tesliuc2024). Thus, data-driven methods enabled rapid disbursement of funds to the most vulnerable groups even in the absence of comprehensive social registries (Lawson et al., Reference Lawson, Koudeka, Martínez, Encinas and Karippacheril2023).

2.2. Algorithmic bias: need for an AI governance framework

The literature highlights concerns how algorithmic decision-making in social protection addresses ethical concerns regarding transparency, accountability, and bias. Algorithms trained on biased datasets may perpetuate existing inequalities leading to unfair exclusions (Eubanks, Reference Eubanks2018). The data used to develop a machine-learning algorithm might be skewed because data points might embed human biases, or the dataset might not be adequately representative of citizens. This issue relates to the feeding of data into algorithms that generates conclusions that are inaccurate or misleading—perhaps better phrased as, data in, garbage out. Another example is the deployment of facial recognition technology that can clearly exacerbate existing racial disparities (Buolamwini and Gebru, Reference Buolamwini and Gebru2018; Fung, Reference Fung2019).

A Guardian Report (Guardian, 2024) revealed how the UK’s Department for Work and Pensions utilised AI algorithms to detect benefit frauds that were biased. The system incorrectly identified some groups over others when making recommendations of whom to investigate for fraud (Booth, Reference Booth2024). Also, the Robodebt scandal, an automated debt recovery scheme that was launched in Australia in July 2015, miscalculated overpayments and issued debt notices to welfare recipients. Eventually, the government was forced to repay when a court ruled the scheme unlawful in 2019 (Carney, Reference Carney2021). Hence, the UN Special Rapporteur has accused nations of “stumbling zombie-like into a digital welfare dystopia” in which AI technologies target, surveil, and punish the poorest people in the absence of accountability (Alston, Reference Alston2020).

Hence, concerns about the inadequacy of guardrails to mitigate the risks of AI use stands valid (WEF, 2024). The World Economic Forum’s “AI Governance Alliance Briefing Paper Series” (2024) emphasised the need for AI regulation to promote safety and ethics in protecting the interests of people, societies and organisations. Furthermore, the absence of governance frameworks for data and AI can lead to privacy violations, potential misuse of AI and missed opportunities in embracing AI for socioeconomic development (WEF, 2024).

3. Methodology

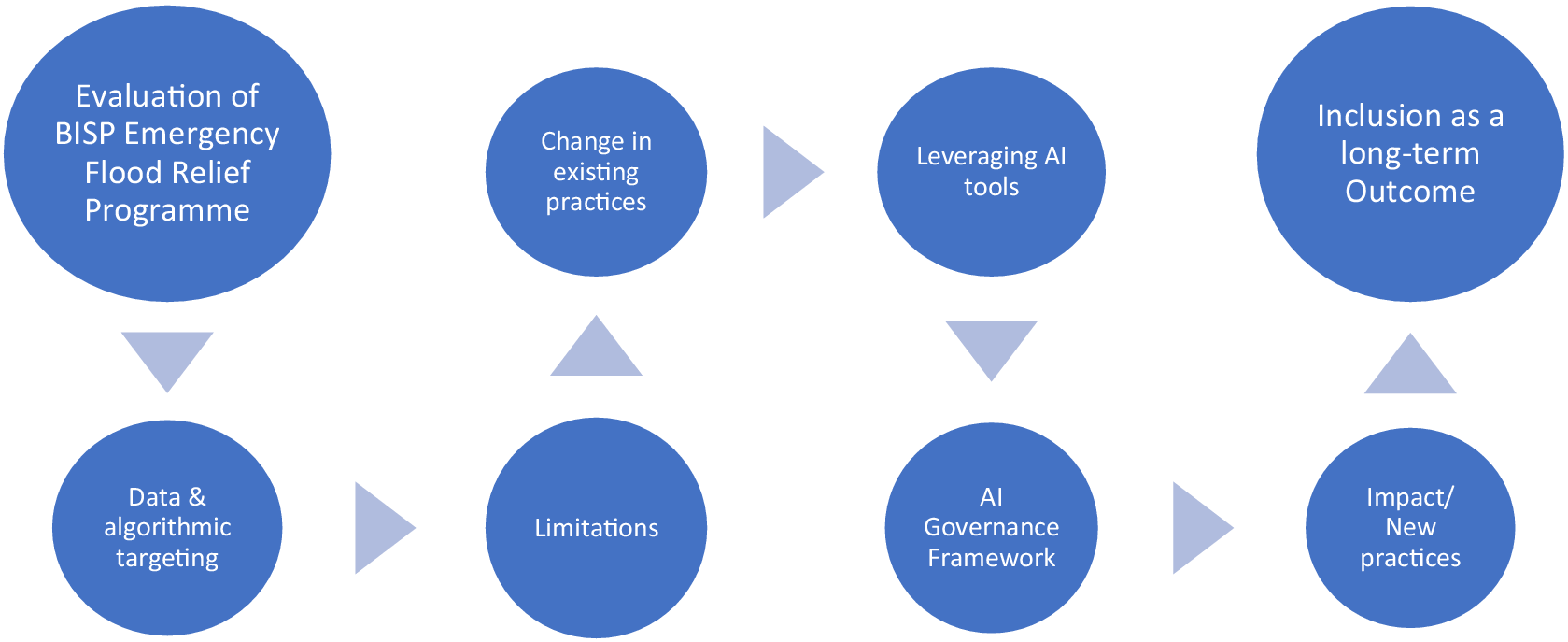

The methodology was a qualitative empirical case study of the BISP Emergency Flood Cash Programme (see Section 4). The evaluation of the case applied the Theory of Change (Weiss, Reference Weiss, Connell, Kubisch, Schorr and Weiss1995) as a methodological tool to guide the research objectives for the project (see Figure 1). It paved way in sequentially 1) critically examining the limitations in programme design and data and technology-led practices in targeting, 2) proposing recommendations, including AI interventions as remedial measures, and 3) designing a governance framework to mitigate the risks of algorithmic (non-AI or AI) decision-making. Theory of Change illustrates how BISP can direct change through modified data/technology targeting processes that will boost programme efficiency and accuracy in expanding coverage of beneficiaries in times of crisis. The theory is gaining relevance in development projects, government policy-oriented projects, and community welfare programmes.

Theory of change guiding methodology (Source: Author’s Own).

The researcher had established ties with BISP since 2014, through previous research done on the implications of the digitalisation of social cash in the BISP Kafalaat programme. Primary data were collected in November 2022 to January 2023 after the monsoon floods in Pakistan. A total of 15 semistructured interviews were conducted with officials from BISP (seven interviews), National Authority of Database Registration (NADRA; five interviews), and the provincial administration or political actors (three interviews) in Islamabad, Pakistan. Other informal and follow-up discussions were held with BISP officials until 2024. Sampling was a combination of purposeful and snow-ball, as participants were selected based on their specialist knowledge and expertise in the relevant departments at BISP and NADRA. BISP senior management officials, who possessed expertise in different functional departments were referred by each other, and were interviewed at the head office. They narrated how data/algorithms and registry data were used in identifying and enrolling beneficiaries for disbursing emergency social cash. Similarly, NADRA’s senior management officials also provided in-depth insights about the digital identity management system and their role as technical actors in supporting BISP’s targeting and disbursement processes since its inception. Finally, interviews with political actors (elected members from the provincial assembly or advisors to ministers) offered critical perspectives and some diverging viewpoints on programme design, data sharing and processes. The number of interviews were determined based on the sample reaching theoretical saturation—that is no additional interviews were required to yield new themes, concepts, or insights relevant to the research questions, as interview data adequately met the informational needs for the research questions to be answered (Patton, Reference Patton2002; Krippendorff, Reference Krippendorff2018). All themes relating to bias, exclusion, inclusion, enrolment criteria, and profiling filters were analysed exhaustively, until no new information was extracted from the interview data, and repetitive themes were recorded.

The interview questions were developed to gain a deeper understanding of the programme’s targeting mechanisms, focussing on data/technologies for the assessment and enrolment of beneficiaries onto BISP from different stakeholder perspectives. The interviews were mainly conducted in English, lasted around 40–60 minutes, and transcripts were transcribed. Prior to conducting the interviews, ethical approval was granted from the University of Essex, UK and participant information sheets and consent forms were distributed to all participants to record consent. Besides primary data, a review of the academic and grey literature on social cash programmes, policy and practitioner reports, BISP organisational documents/briefs, and social media platforms were used to analyse secondary data sources. Some of the policy/practitioner reports included, open source documents from the World Bank, international humanitarian agencies such as United Nations, and private development agencies. In general, the collation of different data sources increased depth of understanding and analysis and triangulated divergent perspectives for establishing credibility and transferability in the research.

Both interview and secondary data were analysed through content analysis, which involved organising and eliciting meaning and interpretations from the data to draw realistic conclusions. Krippendorff (Reference Krippendorff2018) defines content analysis as, “a research technique for making replicable and valid inferences from texts (or other meaningful matter) to the contexts of their use.” Inductive reasoning extracted inferences from both interview and secondary data by coding and weaving together new information under the categories of data, technologies, social registry, algorithms, bias, inclusion/exclusion in emergency cash targeting mechanisms. Content from the texts were analysed with an open mind to identify meaningful codes/categories for answering the research questions. The interpretation of interview data provided critical insights on the targeting mechanism adapted for flood-affected beneficiaries. Data were analysed to first highlight the limitations in data/algorithmic targeting of beneficiaries and then discuss the gaps to suggest recommendations. This consequently led to the proposition of AI solutions under a governance framework to mitigate the risks. This contributed to the meaningful discussion for policy and practice implications—on how leveraging AI tools may lead to the inclusion of beneficiaries, as an outcome, that can benefit both beneficiaries and BISP for positive impact.

4. Case study background

4.1. Country context

Pakistan is listed among the countries most affected by weather-related extremes in the Global Climate Risk Index’s long-term series, which records direct disaster losses rather than nonfatal exposure to heat or weather variability (The GCRI measures how countries and regions are affected by weather-related disasters, focusing only on direct losses and excluding nonfatal or gradual impacts from temperature and weather changes.). From 1992 to 2021, climate and weather-related events produced an estimated US$ 29.3 billion in damages to property, crops, and livestock, and amounted to roughly 11.1% of 2020 GDP (World Bank, 2022c) (Inflation adjusted to 2021 US dollars). Beyond these headline losses, repeated shocks threaten to reverse hard-won poverty reduction (These shocks threaten to undo Pakistan’s progress in reducing poverty over the past 20 years.) and have documented effects on health systems and disease risks (WHO, 2022) (These shocks hinder healthcare access and worsen disease outbreaks.). Such events erode living standards and households’ ability to cope over time, underscoring the role of social protection institutions, such as BISP, in strengthening resilience (PID, 2022; Costella and McCord, Reference Costella and McCord2023). It is estimated that the pandemic pushed 2 million people below the poverty line (World Bank, 2021) while the floods plunged an estimated 9.1 million people into poverty (World Bank Blog, 2023). Historically, responses in Pakistan have leaned towards post-disaster (ex post) scale-up, for example, emergency cash during COVID-19, while the case for more anticipatory, ex-ante approaches is growing.

4.2. BISP emergency flood cash programme

BISP was launched in 2008 as the Government of Pakistan’s flagship social safety net programme with the objective of cushioning poor households from chronic poverty in the aftermath of the 2007–2008 financial crisis. As the largest and most systematic unconditional cash transfer programme, it underlines the United Nations SDGs to reduce poverty in marginalised households. BISP also aims to empower women by providing cash assistance directly to the female head of the family in possession of a valid computerised national identity card (CNIC).

Over the years, since 2010 after enactment of the Benazir Income Support Programme Act (2010), the programme has evolved in terms of employing objective and digital targeting tools and disbursement channels. A poverty scorecard based on proxy-means testing (PMT) estimates households poverty levels and assigns a PMT score based on socioeconomic characteristics as poverty proxies. Households under a threshold PMT value of 32 are declared potential beneficiaries, belonging to bottom 40% of the population. To-date, there are approximately 10 million beneficiaries enrolled under BISP Kafaalat, who receive a quarterly amount of USD $52 (PKR 14500) (Exchange rate as of 25 February 2026: US $1 = PKR 279.39. Federal minimum wage in Pakistan for the fiscal year 2025‑26 is US$ 130.52 = PKR 36,465 per month.). In addition, BISP also provides conditional cash transfers under the Taleemi Wazaif (education) since 2012, and Nashonuma (health and nutrition) since 2020, to enhance investments in human capital. By 2022, the government’s budget allocation had increased to 0.58% of the country’s GDP that covers 19.84% of the country’s population (Guven et al., Reference Guven, Majoka and Jamy2024).

While BISP has contributed to significantly decrease poverty in Pakistan, the ravaging 2022 monsoon floods put enormous pressure on BISP. However, investments in technology have enhanced BISP’s basic system (BISP Kafaalat) to strengthen and adapt its regular social protection system under the flood crisis- rolling out the BISP Emergency Flood Cash Programme in 2022 (see Figure 2).

Flood 2022 damage impact and response (Source: BISP, n.d.).

The World Bank (2023) highlights four key building blocks that underpin the foundation of ASP. These include programme adjustments, data and technologies, finance, and institutional partnerships. These building blocks are analysed in the context of BISP in the next section.

4.2.1. Programme adjustments

The Emergency Flood Cash Programme was both a vertical and horizontal adaption of BISP beyond its routine beneficiary base to enrol beneficiaries from flood-affected regions. Vertical adjustments involved increasing the value of the grant, as a temporary one time top-up of USD $90 (PKR 25000), which was disbursed to 2.7 million flood-affected households. Other design parameters of the BISP Kafaalat program were adjusted for eligibility criteria and beneficiary selection (BISP, n.d.). This included having a higher cut-off in initial estimated response which was later reduced to lower PMT value due to fiscal constraints.

4.2.2. Data and technology

Digital identity data. In Pakistan, citizens’ unique digital identity (ID) number provides the enrolment of beneficiaries onto the BISP system. In order to be eligible to receive unconditional and conditional social cash, BISP has made it mandatory for beneficiaries to register with NADRA and obtain their unique 13 digital ID number through which they are identified in the social registry and other public datasets. The ID card incorporates beneficiaries’ biometric data (fingerprints, iris scans) that validates their identity—via thumbprints for disbursing grants through NADRA’s biometric verification system (BVS) at point-of-sale (POS) agent locations and automated teller machine (ATMs). The BVS is linked with the database of NADRA that enables real-time verification of beneficiaries. Identity or biometric data is encrypted within several layers of security that makes the identity platform an extremely reliable and robust system (BISP, n.d.; NADRA 2022).

National Socioeconomic Registry. Launched in 2009–2010, the National Socioeconomic Registry (NSER) started as a targeting tool for BISP unconditional cash transfer (now known as Kafaalat), but functions as the backbone of Pakistan’s social protection system, providing data to other federal and provincial programmes and institutions, including disaster response initiatives for identification and targeting. As a comprehensive database, it records socioeconomic or poverty data from over 35 million poor households that approximately covers 87% of the country’s population (Figure 3).

National socioeconomic registry coverage (Source: BISP, n.d.).

In order to register under BISP Kafaalat, and to receive regular unconditional cash payments, citizens are required to visit any BISP registration office located in their nearest district or tehsil and bring their digital ID card and family certificate issued by NADRA. They then participate in the poverty scorecard survey that relies on the use of a PMT, which calculates score based on 43 variables, comprising individual and household socioeconomic characteristics (income, assets, household size, education, etc.). Collectively, these variables proxy for household welfare and are recorded in the NSER database. The registry interacts with NADRA’s citizen registry through application programming interfaces (APIs), and more recently, BISP has established 647 facilitation centres across Pakistan (also known as Dynamic Registry Centres) where people can register and update their information in NSER (BISP, n.d.; Guven et al., Reference Guven, Majoka and Jamy2024). Thus, the NSER is a dynamic and live registry, and in case of changing circumstances, citizens may recertify their status or enrol on demand. In the aftermath of floods in 2022, BISP set up additional temporary registration desks to broaden access for people affected by floods (BMZ, 2023; GIZ, 2023).

Geospatial/Satellite Data. BISP incorporated geospatial data from the United Nations Institute for Training and Research (UNITAR) through satellite-based assessments (UNISAT VIIRS) and combined it with GPS data from NSER identified flood stricken households in areas of high vulnerability (Guven et al., Reference Guven, Majoka and Jamy2024). Satellite images showed localities submerged under water and households located 5 km on either side of the riverbanks were included in the assessment. The maps provided valuable insights to allocate resources in disaster struck areas (BISP, n.d.). A similar exercise was carried out in aftermath of Harnai Earthquake response (Figure 4).

Depiction of NSER household data coordinates from the epicentre of Harnai Earthquake (Source: BISP, n.d.).

4.2.3. Institutional partnerships

National Disaster Management Authority. The National Disaster Management Authority (NDMA) is a federal lead and coordinating agency. It frames national policy and standards, runs national-level risk monitoring and early warning, and acts as the secretariat to the National Disaster Management Commission (chaired by the Prime Minister). Four Provincial Disaster Management Agencies (PDMAs) including State Disaster Management Authority (for Azad Jammu and Kashmir) and Gilgit-Baltistan Disaster Management Authority prepare provincial disaster plans, coordinate line departments and run provincial Emergency Operations Centres. The provincial and regional authorities work with NDMA when events exceed provincial capacity or require national/international coordination, but PDMAs are constituted under law with their own mandates. At the district level, District Disaster Management Authorities execute plans on the ground (often chaired by the Deputy Commissioner) in assessing local risks, coordinating departments and partners, and implementing evacuations, relief and early recovery, in line with provincial guidance and national standard (BISP, n.d.).

National Database Regulation Authority (NADRA). Since the inception of BISP in 2008, the collaboration between BISP and NADRA has been critical for the effective execution of the programme. NADRA’s provision of identity documents (computerised national ID card) to beneficiaries assists BISP in identity verification for targeting and disbursing social cash. NADRA also provided technical assistance in designing and conducting the door-to-door poverty scorecard survey in 2010. Additionally, it supported the development of BISPs information system that manages and monitors data related to BISP beneficiaries, and payments for all programmes. Both BISP and NADRA closely collaborate to ensure that the NSER is dynamic in nature (NADRA, 2022). This involves a desk-based data collection initiative in registering households excluded in previous surveys, updating household information, removing discrepancies such as missing CNICs, change in marital status, age and gender, disability status, and so forth and beneficiaries’ recertification after every 3 years. According to BISP (n.d.), so far 23 million beneficiaries have registered and updated their information via the desk-based collection centres.

4.2.4. Finance

Over time, in the face of increased shocks, the budget and coverage of BISP Kafaalat expanded, reflecting a policy shift away from reactive measures towards providing long-term safety nets. The total budget allocation for flood relief assistance by the Government of Pakistan was USD $250,556,180 (PKR 70 billion) to cover approximately 2.7 million families, out of which approximately 2.65 million, were beneficiaries receiving regular cash transfers, while 106,000 were non beneficiaries recorded in the system (BISP, n.d.). It was recorded that BISP provided a one-time lump sum payment of USD $90 (PKR 25,000) to the eligible families under flood relief assistance. Besides financial support from the World Bank of USD $150 million, and funding of USD $178,968,700 (PKR 5 billion) released by the Government to the NDMA, a relief fund was also established for people to donate to the flood relief efforts (United Nations Report, 2022).

5. Analysis of data and algorithmic targeting processes

Data and algorithmic targeting process that identified and enrolled beneficiaries under the BISP Emergency Flood Cash Programme is analysed to present the findings in Section 6.

5.1. Initial disaster assessment: NSER data mapping

The initial assessment of flood stricken areas was undertaken by NDMA and PDMA—starting from the district, tehsil, union council, and moving to village level. The information was shared through NDMA’s notification to BISP/NSER section. Some of the notifications were also shared by Relief Commissioners, who work in collaboration with PDMAs and NDMA, and other provincial/regional institutions (see Figure 5).

BISP’s flood 2022 response and backend design (Source: BISP, n.d.).

Once the NSER team received information of the regions affected by flooding, they mapped it against households falling under the conditions based on PMT scores. As validated by a BISP official, “we relaxed the PMT cut off score in some tehsils to 35 in order to cover more households…so beneficiaries hailing from flood affected regions with PMT scores under 35 were identified through their digital IDs” (BISP Official 1).

As part of the data cleaning exercise (Figure 6), “the beneficiary had to be an ‘ever married female’ ….married, divorced, or widowed, but if there were no ‘ever married female’ present in the household, then an ‘ever married male’ from the same household qualified to receive the grant” (BISP Official 1).

NSER data collection, validation, and scoring process (Source: BISP, n.d.).

This initial assessment involved cross-checking NSER data against the NADRA database for family/spouse verification. Thus, profiling filters helped to avoid duplication of the grant in case the beneficiary resided in a different household.

Although field level assessments and notification of flooded areas were responsibility of NDMA, BISP internally did an analysis using the GIS coordinates of the households (as per NSER data against satellite/geospatial data) to cross-check localities of flood stricken households. As stated by another BISP official, “satellite maps illustrated household GPS coordinates to plot vulnerable households located within a distance of 5 km along the sides of flooded river banks…..such images may not have necessarily captured flooding in real-time, as flood water tends to flow from higher to lower regions” (BISP Official 3).

5.2. Enrolment: algorithmic decision-making

The final stage in targeting involved BISP sharing potential beneficiaries’ digital ID data with the identity provider NADRA. Utilising computerised algorithms designed by BISP, NADRA executed a series of successive data analytics across several datasets, including the Federal Board of Revenue, mobile phone databases, and Government Employee Database (Integrated Border Management System) as depicted in Figure 7.

Integration of systems for social protection—interplay of social and beneficiary registries with administrative datasets (Source: BISP, n.d.).

A BISP official remarked, “algorithms served as exclusion filters or proxies for wealth and disqualified beneficiaries if their IDs matched their profile in the databases. The exclusion criteria comprised of possession of a passport for international travel, ownership/registration of a new vehicle, telephone and/or mobile phone bill exceeding PKR 1000/month (USD $3.5) processing of three or more family members’ ID documents through NADRA’s executive service and being in government employment or recipient of government pension” (BISP Official 2).

Hence, this depicts that algorithmic decision-making validated beneficiaries enrolment onto the BISP Flood Emergency Cash Programme. Eligible beneficiaries received a text message, informing them to cash-out their one-time payment through BVSs at POSs and ATMs, as illustrated in Figure 5. However, the targeting process for beneficiary enrolment is summarised in Figure 7.

6. Findings: shortcomings and recommendations

The study has identified several shortcomings pertaining to data/algorithmic-led targeting of beneficiaries in assessment and enrolment stages that led to their exclusion, either through programme design or data and technology constraints. The recommendations proposed, based on the limitations (findings), underline “change in existing practices”—drawing on the Theory of Change (see Figure 1).

6.1. Communication challenges

The findings suggest that there were communication challenges within channels of communication between BISP and beneficiaries. A BISP official exclaimed, “extensive flooding affected the technology communication channels, damaging network cables and impacting mobile phone services in some regions….it became challenging for BISP to communicate with existing or new beneficiaries, notifying them of the one-time benefits they were eligible to receive” (BISP Official 1).

Hence, communicating social cash provision to a new set of beneficiaries was extremely difficult as their contact information was unavailable in the social registry. This suggests that it is pertinent to create a database to include contact information (registered against family member’s CNIC) of vulnerable households exposed to natural risks (floods and earthquake) in order to build an effective communication strategy and launch an early public information campaign.

Another BISP official remarked, “locating and tracking displaced people, who had migrated to safer havens, due to houses being destroyed or damaged from excessive flooding was another difficult task for BISP…. where beneficiaries migrated to other districts, BISP had to manually unlock their location data, on a case to case basis” (BISP Official 4).

In order to overcome this challenge, time-based satellite maps and sophisticated GIS/geospatial informatics could be utilised to target vulnerable populations for designing any shock response initiative by federal or provincial institutions. In addition, the use of mobile data to track and locate displaced beneficiaries and disburse grants through mobile money/digital wallets, especially in remote districts can prove to be favourable.

6.2. Data mismatches

Digital identification systems can inadvertently exclude eligible beneficiaries due to biometric data mismatches or other information inaccuracies. As disclosed by a NADRA Official, “there have been times when beneficiaries’ fingerprints are faint, or do not match our records, especially common in case of elderly women…we are aware of this issue” (NADRA Official 4).

This was also echoed by BISP officials,

“at times, identified beneficiaries cannot withdraw their payment due to unavailability of their matching fingerprints in NADRA’s database….alternate method of disbursement, non-BVS payments, often takes time and special arrangements at BISP offices creates further hurdle for beneficiaries” (BISP Official 5).

“another problem which links to having commonly agreed digital address libraries created issues during identification of flood affected areas during the targeting process….the NSER and NDMA (including disaster management authorities) had different address libraries, due to which some identified areas by NDMA were not located in the NSER record” (BISP Official 1).

It is noted how this issue was prevalent for Union Councils because in Pakistan (approximately over 10,000 Union Councils in the country) a consistent naming system is absent at the Union Council level that leads to data discrepancy. It was found that the same issue exists at the Tehsil level too, but since there are approximately 650 tehsils, string matching is relatively easier and less error-prone. Sometimes, beneficiaries’ ID card had expired that led to complexities around the biometric disbursement of funds. This suggests that while CNIC possession remains a core eligibility criterion to access emergency funds, it may also exclude those who need support the most (BISP, n.d.).

Therefore, it is recommended that extension of digital ID coverage to marginalised populations may help increase registration and access in remote sites, particularly extending NADRA registration camps or mobile registration vehicles. Additionally, there should be a commonly agreed address library, which has same spellings across all the registries at least at the Province, District, Tehsil, and Union Council levels. Further down at the Village level, digital IDs or numbers should be given which are referred in the administrative data. This suggests that regular data auditing may improve the quality and accuracy of the NSER dynamic database.

6.3. NSER data: proxy bias

BISP’s mandate is to provide quick cash assistance to support marginalised segments during any shock for consumption smoothing. A BISP official proclaimed, “in times of crisis, damage assessment is neither the responsibility of BISP, nor can BISP wait for such an assessment to identify eligible beneficiaries, as it is a cumbersome process and takes a long time” (BISP Official 4).

This narrative implies that initial assessment is the prime responsibility of NDMA/PDMA- to provide data to BISP for identifying affected populations already present in the social registry. Hence, households only in the flood stricken tehsils/districts, with a PMT score under 32 in the NSER, qualified in the early stage of assessment, considering the financial constraints at the Government side. This alludes that the needs assessment primarily relied on poverty scores, irrespective of asset assessment for damage. While PMT score relies on household/asset information that is fairly static under normal conditions, and being less susceptible to shocks, it is less suitable as a proxy to evaluate asset damage in times of shock. For instance, citizens with damaged houses, crops, or livestock loss may not have been included in the emergency cash system. Hence, this indicates that targeting was centred on poverty as “proxy,” omitting asset damage that pushed households into further poverty during climate shocks. Although BISP expanded horizontally in design, this was confined to the cap on PMT score, which may have left out some vulnerable households. This form of proxy selection may have contributed to under-coverage among affected groups from the receipt of emergency funds.

Furthermore, at the time of floods in 2022, the social registry was not fully inclusive of data from transgender groups, disabled households, and single “not ever married” women/orphans as household heads. This was confirmed by a NADRA official, “although data registration at that time for certain demographic groups was being collected by NADRA, this meant some eligible individuals may not have been included in the citizen registry….neither in the validation exercises between NSER and NADRA….targeting data primarily drew from households in the social registry only” (NADRA Official 2).

Moreover, assessment could, where feasible, complement NSER data with light-touch assessments to capture asset/livelihood damage—including housing type (katcha/pakka), crops and livestock loss. As recommended by a provincial actor, “employing hybrid processes, both in-person and digital, to evaluate damage assessment…and where appropriate, geo-tagging those households and assigning QR codes for targeting and monitoring may provide more precise and accurate targeting” (Provincial Actor 1). Also, in times of future crisis, timely and clear communication to beneficiaries for eligibility criteria updates (PMT threshold) would be extremely advantageous and productive.

6.4. Geospatial targeting

The triangulation of NSER data with other sources—for example, GPS data in combination with flood exposure data from the UNITAR was not part of the formal targeting strategy, nor implemented as a standard operating procedure (SOP) and shared with other departments. A BISP official proclaimed, “more extensive and effective GIS satellite data/geospatial imagery may illustrate a comprehensive picture of pre-post flooding localities in real-time” (BISP Official 3). This finding proposes the use of hazard risk assessment maps that evaluate the impact of shocks to help formulate a targeted crisis response strategy as a remedial measure.

6.5. Algorithmic (non-AI) bias

While recognising BISP’s intent to ensure prudent targeting, the study indicated that proxy-based algorithms for wealth indicators of beneficiaries’ poverty status may have introduced unintended exclusion risks in times of climate shock. This was stated by a NADRA official, “disqualifying a beneficiary from the system on the basis of international travel may not always accurately represent their economic status…as some travel for a religious pilgrimage (Umra/Hajj/ziarat) utilising their life long savings or loans from family members” (NADRA Official 1). Another NADRA official reiterated, “mobile phone bills, exceeding a certain threshold value, may also not be a reliable proxy for wealth, as mobile phones are sometimes a shared utility among several family members” (NADRA Official 3).

This insinuates that algorithmic decision-making may, in some instances, contribute to under-coverage or unintended exclusion. Therefore, designing and executing algorithms based on the exclusion criteria can be error-prone in certain contexts—that is it could be temporarily paused or complemented especially during a crisis. Algorithmic decision-making may not always fully capture beneficiaries’ true economic status. Thus, the consideration of periodic validation of datasets against other economic/financial behaviours, such as patterns of consumption (buying/spending) of beneficiaries (where feasible and appropriate) while respecting privacy and programme policies may prove to be a valuable exercise in future.

6.6. Lack of institutional coordination

While BISP enjoys high levels of support at the national level, it is important that any shock response effort by BISP is implemented in tandem with existing national disaster relief management frameworks and protocols to avoid duplication and enhance complementarity with provincial programmes. The study noted opportunities to further strengthen institutional coordination between BISP and the disaster management system, extending to PDMAs, and relevant federal counterparts. From the perspective of provincial political actors, collaboration with BISP presented some practical challenges, especially pertaining to data sharing from the provincial administration to BISP. This was validated by a BISP official, “NSER data was generally not shared with other provincial databases from public/private institutions, including the Pakistan Poverty Alleviation Fund, Pakistan Bait-ul-Maal and Zakat programmes (Provincial Bait-ul-Mal), during the period under review, to avoid duplication of flood relief efforts and to align with prevailing governance protocols” (BISP Official 1).

While separate budgets for flood relief assistance were allocated by the federal government to provincial administrations, some provinces, like Punjab and KPK, designed and executed independent flood relief systems in parallel—that may have led to benefit duplication in some instances. However, through a power lens, a provincial actor remarked, “the disbursement of emergency social cash was perceived as a politically sensitive act that may have heightened sensitivities and existing power tussles between the federal and provincial administrations” (Provincial Actor 3).

Another provincial actor remarked, “Punjab administration conducted their own in-person digital survey to assess household damage, geo-tagged households with a unique QR code, and developed their own technology infrastructure….this comprised of independent databases and interactive dashboards seeking assistance from local IT Boards” (Provincial Actor 2). This validates that the assessment and enrolment exercise at the provincial level was a hybrid digital system, underlining asset-damage assessment relative to the federal approach that relied more on poverty scores—the approaches could be viewed as complementary.

In order to alleviate these limitations, building and progressively strengthening systemic linkages with the NDRM for the co-development of a fit for purpose disaster risk strategy- spanning preparedness through recovery and reconstruction, with clear roles, timelines, and review mechanisms may be the way forward. Additionally, to continue to foster and (where helpful) formalise institutional cooperation between BISP, provincial systems, and social protection institutes for coordinated collaboration and (where appropriate) share strategic resources and data in times of shock, with agreed governance, privacy, and security safeguards can prove mutually beneficial for all stakeholders. Finally, exploring a phased, secure interoperability and bi-directional/two-way data sharing protocols or APIs (where appropriate)—for example, NSER could provide organisations with valuable data after removing/anonymising sensitive data under appropriate data-sharing agreements and, in turn benefit from receiving well-defined, consented data from other organisations, consistent with legal and regulatory requirements, can enhance institutional strengthening and corporation (BISP, n.d.).

6.7. Financial constraints

The budget allocation of USD $250,556,180 (PKR 70 billion) from the Government of Pakistan and donor funding was insufficient to extend support to all beneficiaries affected by the devasting floods. A BISP official advised, “in times of crisis it would be feasible to pool all financial resources from public/private institutions, NGOs and civil society into a combined transparent digital fund to eliminate duplication in disbursements and maximise resource allocation (BISP Official 4). Also building trust and investing in the long-term resilience of vulnerable populations, through the provision of saving schemes, micro-credit, and mobile accounts can proactively prepare vulnerable populations from future shocks. The monitoring of funds with clear instructions to beneficiaries on the purpose and aims of the grant use in times of crisis should be a continuous communication process.

6.8. Data governance concerns

6.8.1. Ethical, diversity, and inclusion concerns

A key governance aspect in digital AI solutions is to move beyond distributional, macro-level considerations of programme design to micro-level fairness. Programme managers and policymakers need to define principles of fairness in algorithmic decision-making and how they can be institutionalised. From the findings, ethical principles may be formalised to counter bias embedded in data/technology to ensure fairness in representation of beneficiaries within datasets, building on existing organisational controls for access, approvals and audit. Hence, ethical considerations need to be factored into regulatory frameworks in adaptive social cash systems, alongside technical safeguards such as role-based access, least-privilege, and audit trails.

An organisational governance framework, specific to the adaptive social cash sector, may help inform other institutions—drawing on the recently approved national AI policy in July 2025. Currently, the “National Commission for Data Protection” under the Personal Data Protection Act awaits approval by the Senate. A BISP official clarified, “in the interim, at the social protection front, BISP’s Technology Wing governance (centralised planning/oversight, change control, periodic audits) offers a platform to anchor such principles in practice and existing security controls, such as network segregation, least-privilege storage/sharing…to reinforce responsible handling” (BISP Official 6).

In light of this, an ethical regulatory framework for fair principles and practices, aligned with current approval, logging and audit processes is proposed for BISP in this study. Also, it is pertinent to expand the coverage of beneficiaries beyond the social registry, and possession of digital IDs for greater inclusion, with consent and purpose-limitation safeguards when ingesting external datasets. By instituting algorithmic development, teams (AI and non-AI) that are diverse and multi-disciplinary can help better understand the representation of beneficiaries for greater diversity.

6.8.2. Data privacy and security concerns

Although data collection and data sharing in welfare programmes can be positioned within a legal framework, the ethical dilemma always remains. A BISP official earlier claimed, “while efforts in Pakistan are directed towards the approval of the Data Protection Bill, a National AI policy cannot be framed without the implementation of the prior” (BISP Official 7). However, this stance does not stand true with the implementation of the policy.

Operationally, BISP’s SOPs already mandate secure environments, encryption, role-based access, formal approvals, and monthly audits for any data sharing—with records of recipients, purpose and verification- and network-level controls (no internet on secure VLAN machines, segregated laptops, least-privilege Z-drive, encryption) further reduce exposure. Also, NADRA’s requirements add purpose limitation, storage minimisation, audit trails, and incident reporting within 24 hours and right-to-audit (BISP, n.d.).

It can be recommended that the data protection clause can be strengthened and standardised in order to seek informed consent for data usage and sharing from beneficiaries at the time of data collection/registration in the NSER at NADRA registration centres. Consistent with NADRA’s end-user visibility, consent, purpose-limitation, and logging expectations is of prime importance. However, broader national legislation should advocate robust data security with stringent protocols complementing existing organisational SOPs on encryption, approvals, audits and incident response.

6.8.3. Lack of transparency, trust, and accountability

Data-driven and algorithmic decision-making processes for the provision of social welfare have been found to marginalise beneficiaries during a climate crisis. Beneficiaries were not always fully aware how decisions were made, or what criteria were used to determine their eligibility that led to unintentional exclusions. Such lack of transparency in algorithmic targeting models may potentially erode beneficiaries trust in social cash systems. Hence, advocating transparency in data-driven systems accentuate that algorithmic targeting processes should become visible and accountable in order to build trust among beneficiaries and other stakeholders.

As stated by a BISP official, “While technology cannot rationally explain to beneficiaries why they were excluded from emergency cash enrolment, pathways for feedback and communication can be established to remove this obstacle….noting that NADRA explicitly requires complete end-user visibility and auditable purpose records for online verifications…..BISP SOPs provide channels for formal communication, verification and reporting” (BISP Official 1). Hence, based on these initiatives, transparent interactive communication channels can be deployed to build trust among beneficiaries to communicate enrolment decisions. Leveraging existing verification workflows, communication channels and audit logs can enhance accountability and redress.

7. Discussion and future implications

7.1. Data and AI technology

The study has invited attention to data governance and ethical issues concerning the use of data and non-AI algorithmic decision-making in the context of the BISP Emergency Flood Cash Programme. This is a critical finding as it implies that any future consideration of harnessing AI solutions, in response to the limitations (highlighted in the previous section) may further augment the magnitude of risks in the absence of certain guardrails. While there is potential for adaptive social cash organisations, like BISP, to exploit a range of AI tools for underpinning targeting decisions, especially in crisis situations, these technologies need to be carefully planned and managed. Here, the Theory of Change is relevant to postulate how future change in organisational practices may result from the deployment of AI technologies.

In the previous section, we disclosed how registry data embedded proxy bias in the identification and enrolment of beneficiaries—that is the use of poverty indicators in times of crisis limits the coverage of beneficiaries in damage assessment exercises. Building on this finding, we evaluate the use of AI tools can help in automated data collection and offer personalised support to beneficiaries. Machine learning applications can evaluate the quality of registry data, identify anomalies, and flag up inaccurate or incomplete entries. In addition, Natural Language Processing (NLP) applications can collate data from various prefetched data sources, and thereby reduce manual effort and minimise errors in data collection (Ohlenburg, Reference Ohlenburg2020). Data collected through chatbots, or AI-administered interviews from beneficiaries can utilise NLP tools to analyse unstructured responses, and chatbots can also facilitate personalised real-time support to beneficiaries based on specific needs to foster trust and increase transparency between BISP and beneficiaries While conversational agents can offer guidance in applying for social cash, self-service portals can support beneficiaries to check and update their eligibility status (Ohlenburg, Reference Ohlenburg2020). However, while AI-driven chatbots offer the potential to transform public delivery interactions in an effective manner (Wirtz et al., Reference Wirtz, Weyerer and Geyerer2019; Vogl et al., Reference Vogl, Seidelin, Ganesh and Bright2020), there are concerns related to the privacy paradox (Willems et al., Reference Willems, Schmid, Vanderelst, Vogel and Ebinger2022). To overcome privacy issues for BISP beneficiaries, informed consent can be recorded at the time of data collection/registration. Moreover, findings revealed that some data-sharing protocols with stakeholders have already been established.

Another finding was how algorithm decision-making design could be made more inclusive and diverse across beneficiary targeting exercises rather than based on exclusionary algorithmic filters. Machine learning algorithms and predictive analytics can pool registration and assessment data from different sources and analyse large datasets from other registries (Bertsimas et al., Reference Bertsimas, Pawlowski and Zhuo2018; Ohlenburg, Reference Ohlenburg2020). In the case of BISP, data from excise, land ownership, and health systems may be pooled together to determine eligibility criteria. Supervised AI models can use labelled data for training that can help adjust eligibility thresholds, based on real-time data to ensure reliability in the targeting process even during changing economic conditions.

However, studies unveil that decisions made by AI algorithms can influence input data they subsequently process that reinforces and amplifies existing biases (Booth, Reference Booth2024). Often skewed training data reflect historical and enduring patterns of prejudice or inequality, and when it does, the faulty inputs create biased algorithms that exacerbate injustice (Slaughter et al., Reference Slaughter, Kopec and Batal2020). Thus, it is argued that algorithms trained on historical, real-world training data may inherit existing societal biases, with the common phrase, “garbage in, garbage out” (Ohlenburg, Reference Ohlenburg2020). While machine learning algorithms seem to create an “illusion of objectivity,” inequality may be coded into systems to further marginalise disadvantaged groups. Hence, AI tools may encode biases by representing the assumptions and interests of its developers (Buolamwini and Gebru, Reference Buolamwini and Gebru2018; Fung, Reference Fung2019). To address this issue of discrimination, while it is difficult to define and measure fairness through any singular data justice framework, efforts to code fairness can be attempted through having a heterogeneous and diverse team of algorithmic designers.

The findings evidenced that there was limited use of geospatial mapping; hence, AI can play a proactive role in making climate predictions to enhance a social cash systems ability to respond efficiently and effectively to crisis situations. By utilising crisis predictive algorithms and data analytics, technology can track and analyse metrology or climate data, such as abnormal weather patterns, and economic indicators to predict a crisis, and identify and warn associated populations at risk (Ohlenburg, Reference Ohlenburg2020). For BISP, Geographic Information Systems can combine GPS and climate data to identify vulnerable households based on demographic profiles and climate risks. Geospatial analysis can display the socioeconomic dynamics of different regions by correlating data with geographic locations that can identify households based on regional patterns and resource allocation (Ohlenburg, Reference Ohlenburg2020). For example in Nigeria, machine learning algorithms predicted wealth indicators based on high-resolution satellite imagery data to identify marginalised groups for welfare delivery during the pandemic. By utilising geospatial and mobile phone data, combined with machine learning algorithms, the country effectively delivered emergency cash (Okamura et al., Reference Okamura, Ohlenburg and Tesliuc2024). Other countries, including Ecuador and Costa Rica, utilised machine learning AI algorithms and combined registry data with satellite images to create maps for identifying vulnerable households (Aiken and Ohlenburg, Reference Aiken and Ohlenburg2023). Although we can argue that such interventions may lead to biased predictions given that eligibility decisions before/during a crisis are time sensitive, the benefits of AI-led decision-making outweighs the risks of delayed assessments.

Another critical finding related to data mismatches—that sometimes excluded beneficiaries despite robust anti-fraud controls in place was rather frustrating for genuine beneficiaries. Hence, it may be worth for BISP to deploy AI applications, replacing traditional manual systems that detect patterns of misuse. Predictive AI modelling can predict fraudulent activities before they occur by analysing historical data that can flag suspicious behaviours, detect anomalies in data, and monitor large volumes of transactions in real time to identify discrepancies, duplicate claims or unusual trends (Ohlenburg, Reference Ohlenburg2020). Biometric data glitches (e.g., thumbprint verification, or expiration of ID cards) can be validated through AI image recognition or facial recognition software. However, this may need to be deployed responsibly, as differences in accuracy rates relating to skin complexion maybe concerning, besides other concerns of biometric mass surveillance (Ohlenburg, Reference Ohlenburg2020). On the contrary, the example of the Dutch Tax Authority Fraud in 2013 and lesson from the UK Universal Credit system that used AI-driven tools to detect fraudulent claims showed that user behaviour patterns can be sometimes biased, leading to outcome disparities towards certain population groups, disabilities, marital status, and nationality (Guardian, 2024). This accentuates the need for conducting regular audits, as part of documentation and fraud reporting systems for enhancing accountability in organisations.

We mentioned how communication challenges excluded some beneficiaries. NLP tools can be used to ensure that marginalised groups residing in remote regions have better access to social cash. AI systems being user-friendly through voice recognition, language translation and other assistive technologies (Sezgin et al., Reference Sezgin, Kocaballi, Dolce, Skeens, Militello, Huang, Stevens and Kemper2024) can help beneficiaries with limited literacy or physical disabilities to access and apply for benefits. Since NLP tools can offer multilingual support, this can increase engagement and real-time assistance, via language translations, for beneficiaries from diverse ethnic and linguistic backgrounds (Yang et al., Reference Yang, Ng, Lei, Tan, Wang, Yan, Pargi, Zhang, Lim, Gunasekeran, Tan, Lee, Yeo, Tan, Ho, Tan, Wong, Kwek, Goh, Liu and Ting2023). This would not only increase inclusion of beneficiaries of all abilities, but also provide complaint redressal—to foster transparency and trust between BISP, beneficiaries and stakeholders. Such applications demonstrate how AI technologies can promote principles of fairness and diversity across marginalised population segments. Also, in line with Sen’s capability approach, transparency empowers beneficiaries’ agency and the opportunities for greater freedom and inclusion.

7.2. Implications for policy and practice: AI governance framework

Table 1 displays the AI governance framework outlining the principles (fairness, diversity, inclusion, transparency, accountability, trust, data security, and privacy), practices, actions, type of AI technologies, and ethical and responsible processes that can mitigate some of the potential risks we discussed above for BISP. Such a framework can be used as a blue print for the wider social cash sector in the Global South. This framework aims to address some concerns of the wider global community related to AI usage in organisations to frame social policy (Vredenburgh, Reference Vredenburgh2024; WEF, 2024).

AI governance framework for BISP (Source: Author’s Own)

8. Conclusion and contributions

The study underlines areas for enhancement in programme design and data/automated targeting processes of the BISP Emergency Flood Cash Programme in Pakistan. By using the Theory of Change as a methodological tool to guide the research strategy, we proposed policy and practice recommendations, including the incorporation of responsible AI tools for ethical and inclusive outcomes for the wider enrolment of beneficiaries in times of crisis. Hence, the study makes several novel contributions. First, it highlights the kinds of exclusions inherent in different data sets (social registry, geospatial data, identity data) exacerbated by communication issues, and financial constraints that affected the initial assessment stage. Another layer of exclusion is augmented by algorithmic-decision-making, executed through profiling filters, through institutional partnerships that can be enhanced. Second, we discuss recommendations for BISP, extending into future opportunities of AI technologies in response to the current limitations posed by data/algorithmic-led targeting. Third, the study proposes an AI governance framework for implementing responsible and ethical AI applications to mitigate the identified risks. Hence, the study empirically contributes to the data and policy literature in the adaptive social cash context, while informing policy change and related practice for development practitioners.

Furthermore, the study informs theoretical discourses on data/algorithmic decision-making in the social cash sector, data, and policy literature. It provides rich evidence-based practical insights for social cash practitioners to institute change, encountering the biases innate in different kinds of data and technologies—starting from digital ID data, social registry data, and algorithm/data analytic design (non-AI) for making beneficiary enrolment decisions. Contrary to the popular assumption that AI-algorithmic targeting removes human intervention in the enrolment of beneficiaries, the study recognises that the decision-making power still lies in the hands of AI technology designers, so some form of human mediation exists. Whether it is the case of automated (non-AI) or AI algorithms, if not responsibly designed and governed, they both pose danger in generating undesirable exclusionary outcomes ensuing from bias, so there needs to be a robust governance framework to safeguard the risks for both BISP and beneficiaries.

Hence, at the policy level, while embracing AI practices, there is a need for vigilance, sensitivity and empathy to guardrail the challenges and risks for BISP, stakeholders, and beneficiaries. Responsible AI innovation, guided by a governance framework, steers ethical principles (fairness, diversity, inclusion, transparency, accountability, trust, data security, and privacy) in targeting practices that challenge bias and opaque decision-making. This policy change emphasises the significance of regulatory frameworks for BISP policymakers before embarking on premature decisions to implement AI solutions.

To conclude, the study underscores the theoretical, empirical, and practical contributions for scholars, policymakers, and practitioners working in the data and social policy domains in the social protection sector. It provides a blue print for policy redesign and new practices that are applicable to other social cash organisations, particularly in the Global South. While the study recognises the limitations of drawing on qualitative insights only, future research can employ a mixed method design to evaluate change, resulting from new data/AI-led targeting processes at BISP and other global social cash systems. The study advocates for adopting data and AI-led targeting solutions that can benefit the adaptive social cash sector in predictive forecasting, and more accurate and transparent targeting processes to increase the inclusion of beneficiaries in times of crisis.