Introduction

Modern research shows that 18th and 19th centuries rural credit markets were complex, but private lenders are thought to have dominated until the late 1800s. From the late 1700s, however, institutional lenders appeared in greater numbers in Europe to meet the growing demand for capital in both urban and rural areas. Among these was the Church, whose role has probably been underestimated due to a lack of research and sources.

The aim of this article is to analyse the church as an institutional financier in 18th and 19th century rural Europe, using Sweden as a case study. In southern Europe, South America, and the Muslim world, religious institutions have long been important lenders, while in northern Europe the church’s role as a financial actor is more or less unknown. The Lutheran church of Sweden was a state church, for long the only permitted in the country, and part of the governance of the state, responsible not only for religion, morality, and education but also for censuses and some taxation. According to a mid-1800s public survey,Footnote 1 the Church was at the time one of the most important institutional lenders in Sweden, and as shown in a recently published article, around 20 per cent of households are thought to have borrowed from the church. However, almost all previous research based on probate inventories has claimed that the church had limited penetration of the local credit market.Footnote 2 It is this contradictory picture of the church as a lender that will be in focus in this article.

Rural credit markets were dominated by private loans until the second half of the 19th century, except in the more developed economies of the Netherlands and Britain. The credit system was of great importance in the growing economies of Europe, providing the necessary means for the transfer of property between generations and between farmers, improving productivity, and facilitating the consumption of goods.Footnote 3 One reason for the persistence of the private credit market was its embeddedness in society as a whole, characterised by close social interactions. Lenders and borrowers were trusted relatives and neighbours, money could be obtained at short notice, and interest rates and terms could be negotiated.Footnote 4

The emergence of institutional lenders from the late 1700s onwards was largely an urban phenomenon. As Wadhwani has pointed out, these small credit institutions – such as savings banks and credit cooperatives – were important financial intermediaries at the regional level, extending credit to borrowers whom larger institutions found unattractive.Footnote 5 Their success was often based on local knowledge where the members were part of the local network with strong liability, which reduced the costs of administration.Footnote 6 Private lenders acting like institutional lenders, before the emergence of banks, are known from several cities, where impersonal loans were given by burghers.Footnote 7 Such semi-institutional lenders were also found in the countryside, where wealthy farmers lent money systematically and on a fairly large scale.Footnote 8

Among those who have argued for the importance of rural institutional lenders are, for example, Ogilvie et al., who show that 20 per cent of loans in rural Schwarzwald in Germany were made by institutions as early as the 17th century.Footnote 9 Gradually, town burghers became more common as lenders in the countryside, and they also formalised the relationship with stronger guarantees to secure their investments.Footnote 10

Religious communities have long been known to be important lenders, but largely in urban areas. In Catholic countries, the so-called monti di pietà or mont-de-piété, which originated in Italy and Spain in the 16th and 17th centuries, offered pawning to the needy as an alternative to usury, while generating a surplus for charity, and then spread to the colonies.Footnote 11 In some of the colonial republics of Latin America, the religious funds became the core of the financial system.Footnote 12 In Spain, the Theresian Carmelites were an important credit institution, mainly lending to urban dwellers and some smaller loans to farmers.Footnote 13

In northern Europe, the church as a financial actor has been little studied. James’s 1948 study of church funds in rural Britain shows that loans were already common in the late 17th century and that almost all parishes had funds for loans by the late 1800s.Footnote 14 In France, Dermineur touches on the subject of parish vestries, which were used to lend money to parishioners when the income exceeded the expenditure.Footnote 15

The extensive research on lending in Sweden, based on probate inventories, shows, as mentioned earlier, little evidence of widespread lending from the church. However, in his study of parish granaries, Berg finds that the church was an important lender of both grain and cash in Sweden from the early 1800s.Footnote 16 The few who have used church accounts show that lending could be extensive. Aronsson shows that the church began to lend money in the 1780s, but that there was great variation among parishes in the size of their funds, and that the freehold farmers were the dominant group of borrowers.Footnote 17 In an analysis of the church’s ledgers in southern Sweden, Svensson concludes that the church was foremost an important lender to farmers aged 30 to 50 when establishing a household or taking over a farm.Footnote 18

Ulväng and Murhem, who claim that the church was an important lender, also support this with estimates of 10 to 30 per cent of rural households as borrowers. Lending was most pronounced in the wealthier parts of Sweden, particularly in the flat counties of the south. During the 19th century, funds grew, especially in poorer areas, thanks to increased lending and the creation of school funds – education became compulsory in 1842 – as well as donations by the landed gentry to fight poverty and encourage good behaviour. An important reason for the increase in assets was the need to build new church buildings in parishes with growing populations. Regardless of the size of the endowment, about 90 per cent of the capital was in the form of loans, which shows the seriousness and commitment of the parishes as lenders. Church funds in rural Sweden bear a strong resemblance to the way other institutional lenders – cooperatives, savings banks, and relief banks – were organised and operated at the time. They operated in a local market, in a strong social context, and with the flexibility to negotiate loan terms and interest rates, enabling them to reach borrowers who might otherwise have been neglected by other lenders. The lenders’ knowledge of the borrowers and the local economy kept risks and costs low.Footnote 19

In summary, it is clear that the European rural credit market consisted largely of private loans until the 19th century, with the gradual emergence of institutional and semi-institutional lenders, some with roots in urban areas. Religious communities have been common lenders since the 16th century, for both charitable and commercial purposes, and most studies have focused on communities in Catholic and Muslim countries, where they could be of great importance to the national credit system.

It is very likely that the churches in northern Europe played an important role as lenders, even if the results are contradictory, as in the Swedish case. In this article, we will explore this contradictory pattern by analysing the borrowers and loans and the changes over time from c1770 to c1900, using both probate inventories and church accounts. Was the church an important lender to households in general, compared with other institutional and private lenders? Who were the borrowers? Were they mainly from the parish, or did the church attract borrowers from other areas? What was the size, terms, and collateral of the loans, and when in life was money borrowed?

The rural credit market in Sweden in the 18th and 19th centuries

Like most western and northern European countries in the 18th and 19th centuries, Sweden underwent an agrarian revolution, followed by a financial and industrial revolution from the mid-1800s, both supported by integration into the global market. Geographically, a vast country with extensive mineral and forest resources, and one of Europe’s leading producers and exporters of iron since the 17th century, the majority of the population was still dependent on agriculture. Between 1750 and 1860, the population increased from 1.8 million to 3.5 million, excluding Finland and Pomerania, which remained part of the kingdom until the Napoleonic Wars.

Two features are worth noting: the high proportion of freehold farmers and the regulated economy. At the beginning of the 18th century, freeholders owned about a third of all land, rising to 60 per cent by the end of the 19th century.Footnote 20 The freeholders were represented in the Diet alongside the nobility, the clergy, and the burghers and gradually became more involved in politics in order to introduce reforms and strengthen their position.Footnote 21 The regulated economy was partly a consequence of population scarcity, great distances, and an in-kind economy, where the state controlled and supported vital parts of the trade and production system. A process of deregulation began at the end of the 18th century and accelerated from the 1820s and 1830s. This included an enclosure movement, road improvements, the construction of canals, the abolition of town tolls and the guild system, and, finally, the introduction of full freedom of enterprise in 1864.Footnote 22 From the 1850s, the country saw rapid industrialisation.

Deregulation and reforms spurred investment and increased credit demand, generally leaving Swedish households heavily indebted. In the 1840s, loans were equivalent to more than two years’ wages, and by the end of the century, to one year’s wages. In the first half of the century, indebtedness was most common among those aged 20–34, while in the second half of the 19th century, it became more common among older people.Footnote 23 Olsson and Svensson show that the loans were mostly used to transfer ownership, while the production surplus was used to improve production.Footnote 24

Private lenders dominated until the late 1800s, but institutional lenders gradually became more common. In addition to the Bank of Sweden (Riksbanken), founded in 1668, the main lenders were the internationally oriented trading houses, intermediaries for the iron producers and timber companies, as well as local businessmen and brokers.Footnote 25 Savings banks were established in the 1820s and 1830s, followed by commercial banks from the 1830s, all of them in towns. The founders of savings banks were often the same people who had long been active as private lenders and borrowers. In other words, in the early stages, savings banks were also semi-institutional in the sense that they simply formalised relationships in an already existing network. In a later phase, the banks became more institutional lenders as the number of borrowers increased and came from a wider geographical area, and co-signatory lending decreased in favour of mortgage lending.Footnote 26 Until the mid-19th century, both commercial and savings banks had a strong local focus. Loans against personal collateral accounted for an important share of the loans granted by both types of banks throughout the century. Such loans were particularly sought after by small farmers who had no access to mortgage loans from the mortgage societies.Footnote 27 Mortgage companies also played an important role in the 1840s and 1850s.Footnote 28

Until 1863, legislation limited the maximum interest rate on loans to 6 per cent, but institutional and semi-institutional lenders were often able to round this up and make the business profitable by charging fees and offering other services to borrowers. The introduction of free interest rates in 1863 more or less confirmed an ongoing movement and also strengthened institutional lenders at the expense of private lenders.Footnote 29

Sources and methods

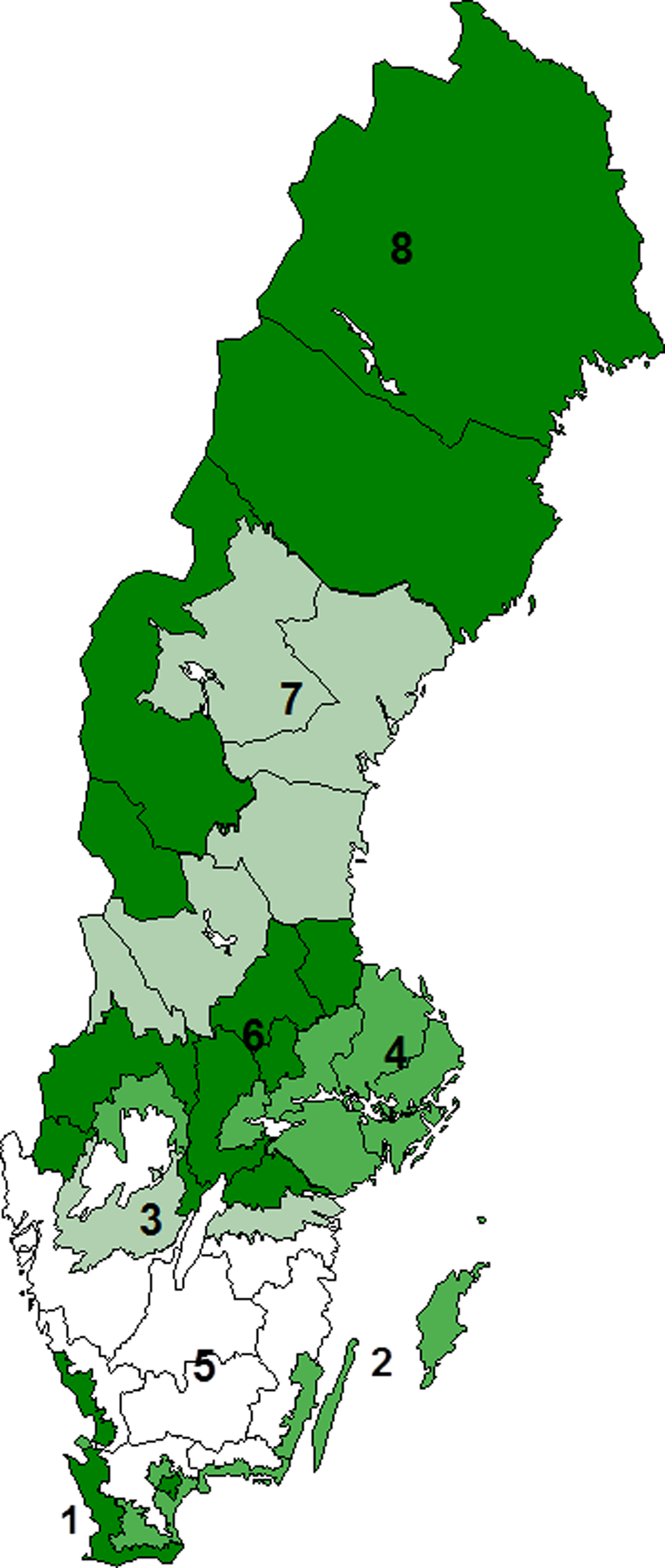

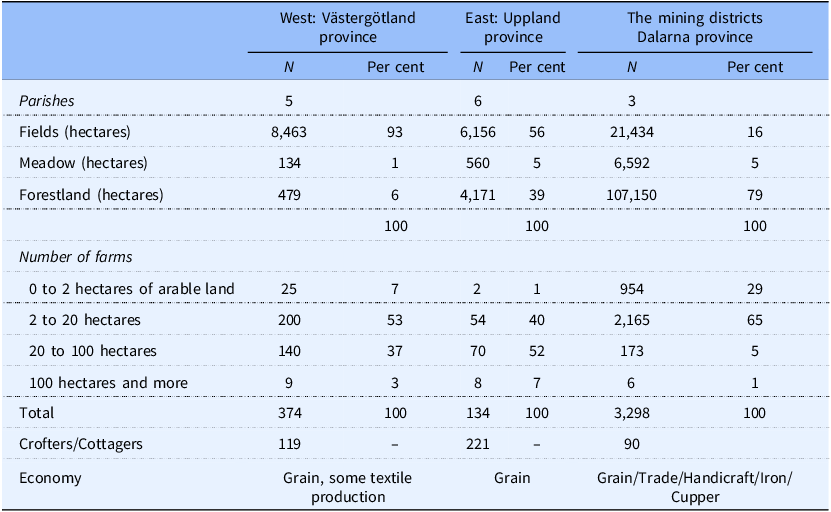

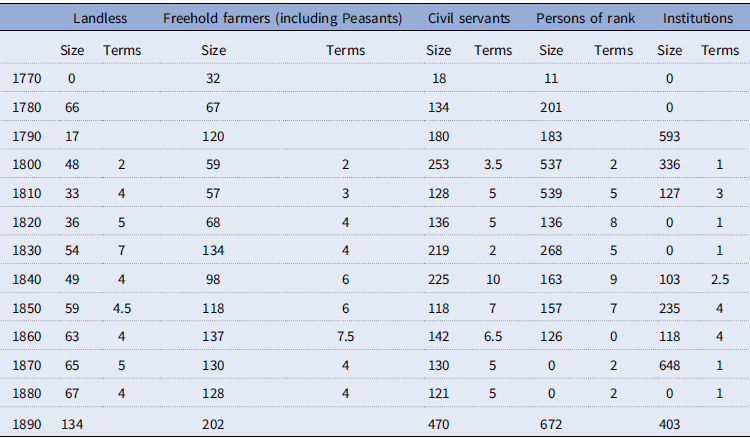

The main source for the study is the probate inventories with their information on assets, claims, and debts which have been combined with the parish account books, with detailed information on loans, borrowers, terms, and interest payments. To understand the causes of regional differences and changes over time, we have chosen to study three areas of Sweden that are well known from previous rural development studies. The selection of areas is based on farming conditions, known as natural farming areas, with area 1 having the best climate and the highest yield per hectare, and area 8 having the lowest (Map 1). Given their different geographies, economies, and agricultural practices, we might expect the church foundations to have played different roles in these areas. West Sweden (natural farming area 3) was dominated by freehold farmers; the east (4) had noble estates and urbanisation; and the mining districts (6) were characterised by small freeholder settings and proto-industrialisation (Table 1).Footnote 30

The five parishes in western Sweden, corresponding to natural farming area 3, were located in a flat, rural area with rather small forest areas.Footnote 31 The parishes experienced a population growth from the mid-1700s, from 2300 to 3500 in 1900, made possible by land reclamation with cultivation of both meadows and forests, and – in a Swedish context – early agricultural reforms that led to a large export of oats to Britain. The original small hamlets grew into villages consisting of many small farms owned by freeholders, who eventually also became owners of the small manorial estates, which were divided into farms. The economy was highly specialised in cereal production, combined with some pre-industrial textile production during the winters.Footnote 32

The six parishes in the province of Uppland, in natural farming area 4, are located near the city of Uppsala, 80 kilometres northwest of the capital, Stockholm.Footnote 33 The parishes were relatively small, both in terms of area and population, ranging in size from 1900 to 3600 hectares. In east central Sweden, the agricultural revolution took a different path. Situated in the centre of Sweden and close to the capital Stockholm, about half of the land was owned by noble families or the crown, and the other half was in the hands of freehold farmers. With the exception of the manors in the area, most of the land owned by the nobility and the Crown was farmed by tenants. The area was a major exporter of rye and wheat to the mining districts and Stockholm and maintained a traditional, though modified, two-field system until the late 19th century. Limited land reclamation and the presence of many estates in the area held back population growth, which was 2700 in 1780 and 2900 in 1900. The area was also characterised by rather large farms and the estates by capitalist agriculture, which involved a large number of landless people.Footnote 34

The three parishes in the mining district of Bergslagen, corresponding to natural farming area 6, were located 250 km northwest of Stockholm, with grain production, but above all extensive forests and mines.Footnote 35 The three parishes were huge, both geographically and in terms of population. The parishes of Stora Skedvi and By each had an area of about 30,000 hectares and a population of about 3000, while the area of Stora Tuna covered 69,000 hectares and had more than 10,000 inhabitants in the late 19th century. The freehold farmers dominated the parish, owning almost all the land, but there were also some ironworks owned by non-noble persons of rank. The 18th and 19th centuries saw rapid population growth, from 13,600 in 1780 to 25,300 in 1900, and land reclamation. In the parish of By, the arable land increased from 500 hectares at the beginning of the 18th century to 4000 hectares in 1900. The large hamlets in the parishes became even larger through the continuous division of already small farms. The economy was traditionally flexible and diversified, with a mix of landowners, farmers who worked as charcoal producers for the ironworks, craftsmen who specialised in the manufacture of iron utensils, and seasonal workers who spent months further south in land reclamation, cultivation, and construction.Footnote 36

In order to ascertain the extent to which debts were owed to individuals, the Church, or other institutional lenders, we have compiled all available probate inventories from the years 1780–1783, 1820–1823, and 1860–1863 for all parishes. The exception is Dalarna, which lacks inventories from the first period.Footnote 37 Due to the parish’s size and the large number of probates for the latter periods, however, the collection was limited to the years 1823 and 1860. A total of 507 inventories were used.

Note that we are able to trace the debts, not the loans. Debts to individuals were not necessarily the result of a real loan, as they could stem from unpaid salary, withheld guardianship funds, or a postponed inheritance. The number of preserved probate inventories is important, and to avoid misrepresentation, we have compared the number of inventories (and the deceased titles) with the number of deceased adults (and titles) in the same parishes and periods. We are fully aware that there is an under-representation of inventories from poorer, younger, and older people before the mid-1800s, as Håkan Lindgren has shown.Footnote 38 As Perlinge also has pointed out, about half of the deceased adults in his study did not leave an inventory, around 85 per cent of them due to poverty, 15 per cent because of their relatively youth, many of them still living with their parents.Footnote 39

In this particular case, the main interest is to trace the share of church fund debts in the total debts of certain social groups, not to give a complete picture of the total debts of a parish population. This means that the mean values for property, wealth, and debt are most likely above the average in each specific area, and certainly for the groups with the worst representation, but not necessary when it comes to the distribution of debts in each group.

The church account books were kept by the minister or an elected official. We have collected data from every tenth year, starting with the financial year 1770 to 1771 or 1780 to 1781 and ending with 1880 to 1881 or 1890 to 1891. The ledgers provide information on the person’s full name, title, location, loan amount, loan dates and terms, annual interest rate, and pledges. When analysing the terms of the loans, we have partly used the information on the loans that ended in the selected years and partly added information from all the loans that ended between the selected years, in order to be able to detect possible short-term loans that are not visible in the selected years. The data collected for these are limited to the size, duration, and social background of the borrowers; the duration calculations are based on data from the 10-year periods following the selected years. All sums have been converted into Riksdaler Riksgälds (Rd), the dominant Swedish currency from 1789 to 1859, and then deflated to fixed prices according to the official consumer price index (KPI 1, year 1914 = 100).Footnote 40 In total, the database consists of 4868 entries, 1119 for the five parishes in Västergötland province in the West, 1525 for the six in Uppland province in the East, and 2219 for the three in Dalarna province in the North.

The information about the borrowers, the amounts, the loan period, and the collateral can be considered adequate, but we do not know how the loan process itself worked. As Aronsson has shown, it was the parish council that decided who would be granted loans and also continuously reviewed the loan payments, sometimes with the help of the vicar.Footnote 41 For our part, no specific records have been preserved showing who applied and what decisions were made. If there was a shortage of capital, perhaps the most trusted individuals were selected, with the most trusted guarantors, which means that members of the nobility and freeholders may have been given priority at the expense of landless individuals. In Svensson’s study, men dominated as borrowers, despite the presence of female landowners in the area. Perhaps this was a consequence of informal rules that gave priority to men when granting loans, or of women actually borrowing but using men as front men.Footnote 42

West Sweden: Västergötland province

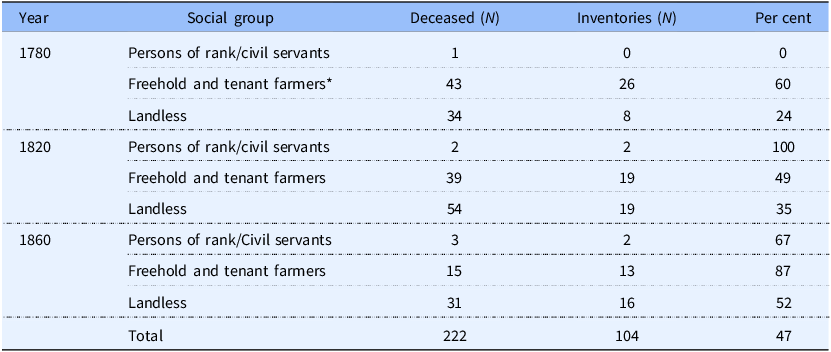

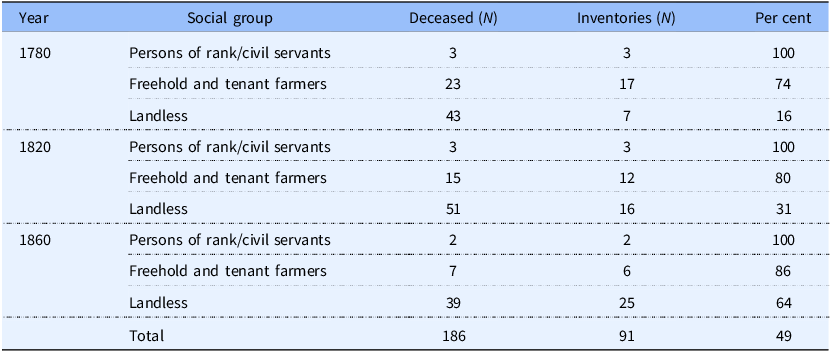

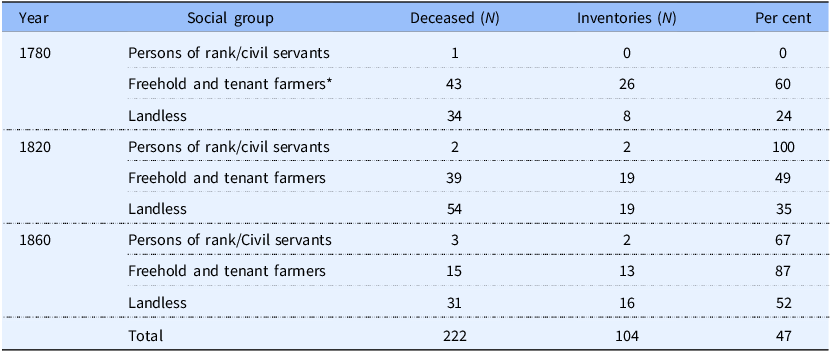

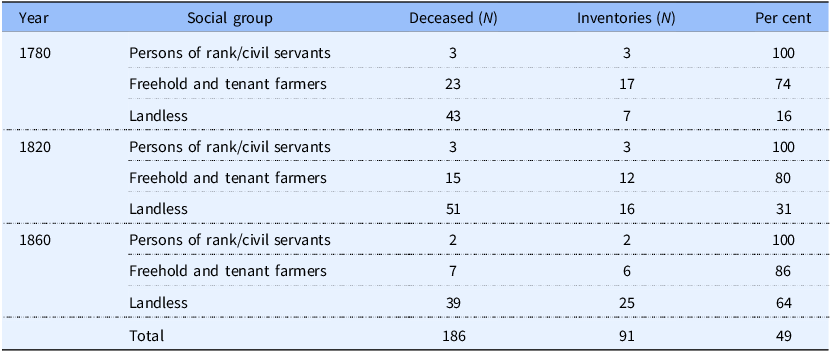

Starting with the parishes in the west, we collected 137 inventories from three of the six parishes from the periods 1780–1783, 1820–1823 and 1860–1863, of which 104 from 1780, 1820, and 1860 were used for comparison with the number of deaths in the same years (Table 2).Footnote 43 Representation is generally good, with 50 per cent or more of inventories surviving for freeholders and tenants, and even more for persons of rank, while representation for the landless is worse, only about 24 per cent in the 1780–1783 period, but then improving to over 50 per cent in the 1860–1863 period.

The three areas in Sweden. Land and number of farms in 1885

Source: BiSOS 1885. Västergötland province parishes: Härjevad, Rackeby, Skalunda, Saleby, Trässberg, Uppland province parishes: Balingsta, Fittja, Fröslunda, Giresta, Gryta och Hagby. Dalarna province parishes: By Stora Tuna and Västra Skedvi.

The number of preserved probate inventories in relation to the number of deceased after social group, in three parishes in Västergötland province 1780, 1820, and 1860

Source: Inventories in Kållands and Skånings häradsrätt, F II, information on the number of deceased in Härjevad C:1, Rackeby C:1 and F:1, Saleby C:2 and F:1.

* The title ‘farmer’ used in the death rolls does not distinguish freeholders from tenant farmers, but they were probably in most cases freeholders, given the fact that most of the land was in the hands of freeholders.

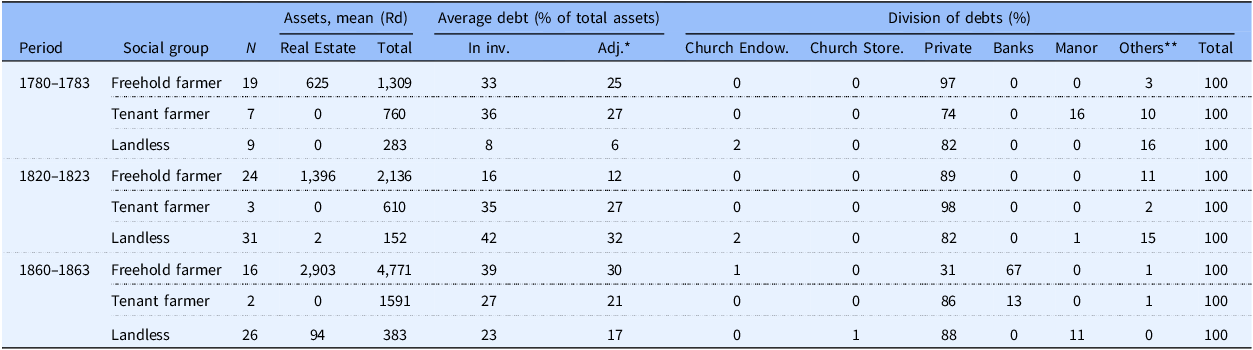

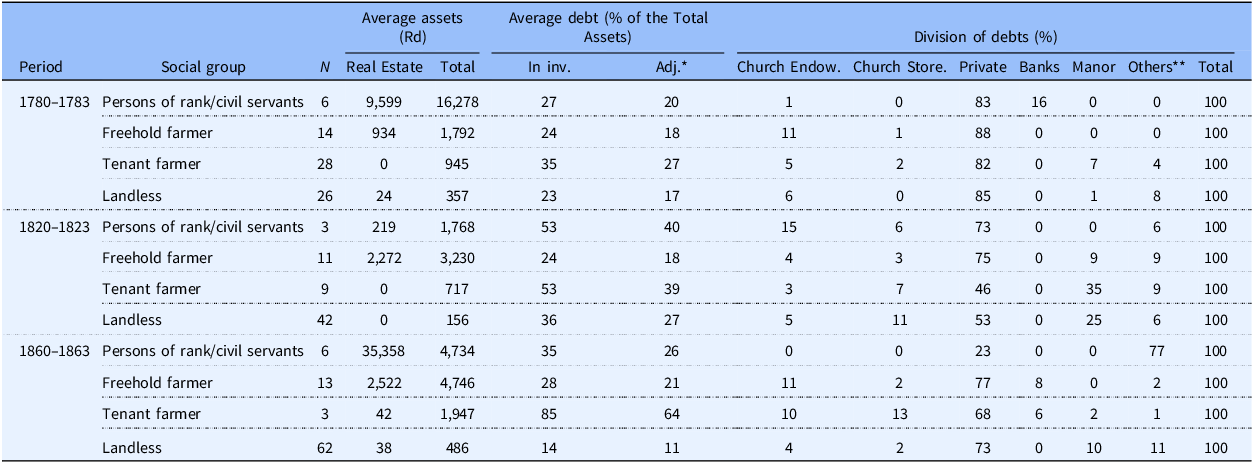

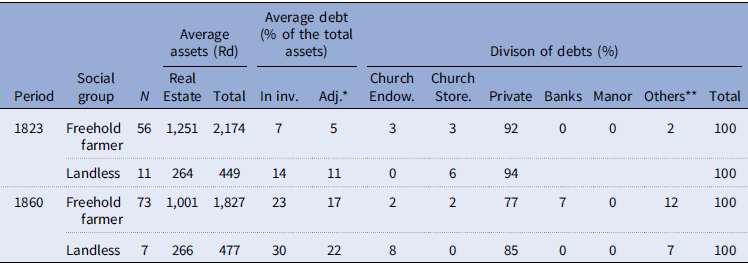

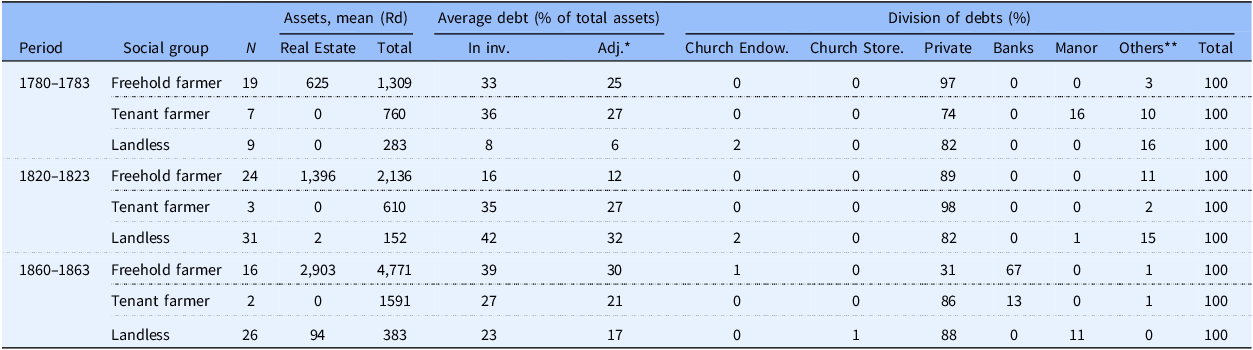

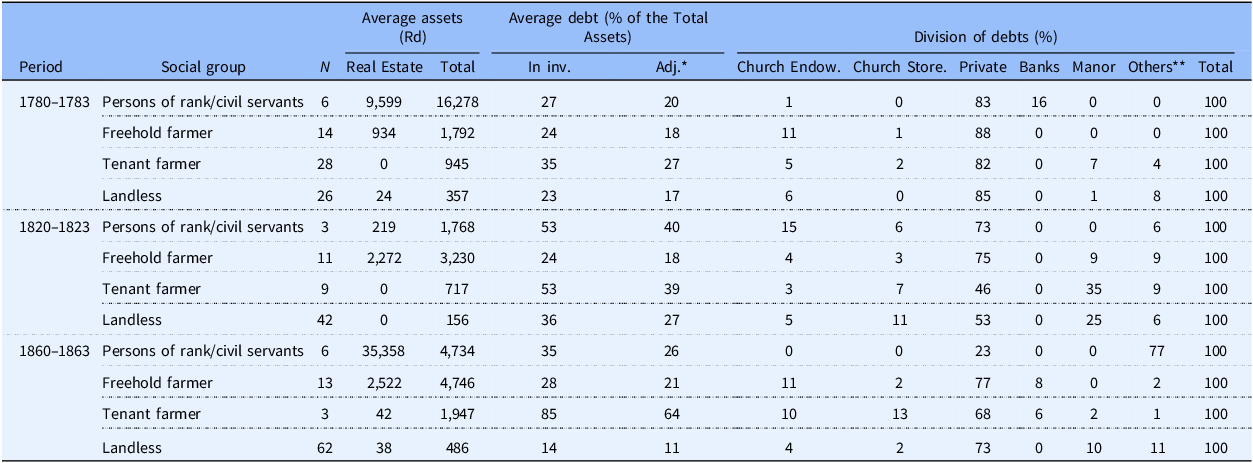

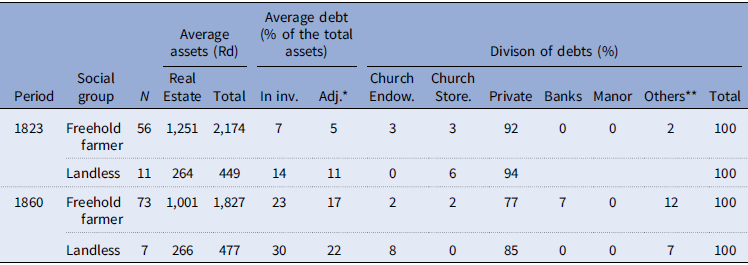

Table 3 shows the assets, debts, and debt distribution of freeholders, tenant farmers, and the landless. The group of persons of rank/civil servants is excluded because of its small number. The column Average debt also includes figures for an adjusted percentage of debt, since it is known that the assets in the Swedish probate inventories were generally undervalued, real estates in particular, by about 33 per cent and the size of debts therefore overestimated.Footnote 44 Households generally had debts of around 20–30 per cent. It is the distribution of debt that interests us most. The credit market was dominated by private loans across all groups, particularly among freeholders, while some tenant farmers and landless people were indebted to their lords. Institutional loans were rare, but became more common in the mid-nineteenth century among freeholders, who had 67 per cent of their loans from banks in 1860–1863. The Landshypotek (Farmers’ Mortgage Bank) dominated among them, accounting for 92 per cent of the debt, ahead of the savings banks with 7 per cent. Tenant farmers used private banks or the Swedish National Bank. This rapid transition to institutional lenders was a result of the commercialisation of agriculture in the area, where farmers became involved in exporting grain to Britain.Footnote 45 The church played a minor role, both as a lender of capital and grain, and was used almost exclusively by the landless – the funds seem to be more or less a poor relief fund.

The average assets and debts in Rd for freehold farmers, tenants, and landless, and the distribution of debts in per cent, in three parishes in Västergötland province 1780–1783, 1820–1823, and 1860–1863, in fixed prices (Swedish Consumer Price Index (CPI), 1914 = 100)

Source: Inventories in Kållands and Skånings häradsrätt, F II

* Adjusted proportion of debts, because of a 33 per cent undervaluation of the assets.

** Other debts were in almost all cases tax debts to the state or the church.

The endowments of the five parishes in Västergötland were quite small. At the end of the eighteenth century, the funds contained about 1300 Rd (deflated, CPI = 1914), which increased to 3000 Rd around 1860 thanks to extensive lending. The funds were then depleted by the construction of a new church building but were replenished until another church needed renovation in the 1890s. The rather small funds limited the ability to borrow money.Footnote 46

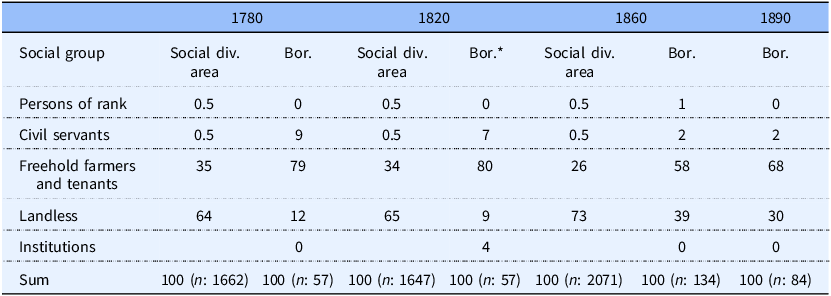

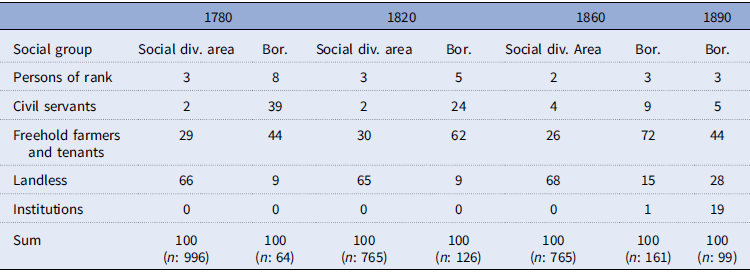

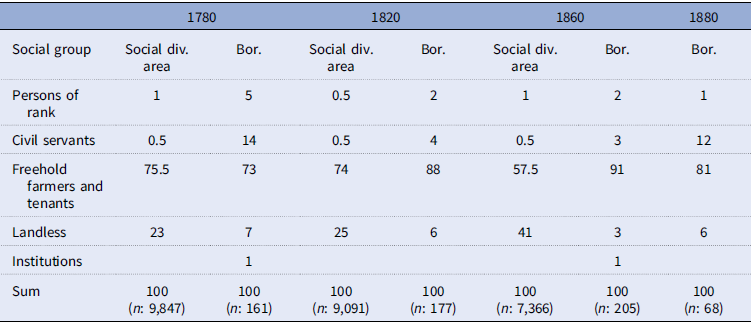

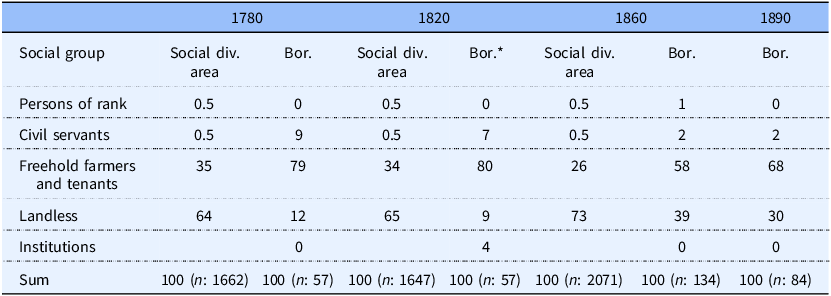

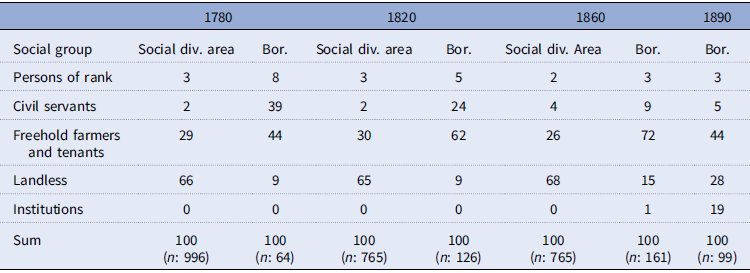

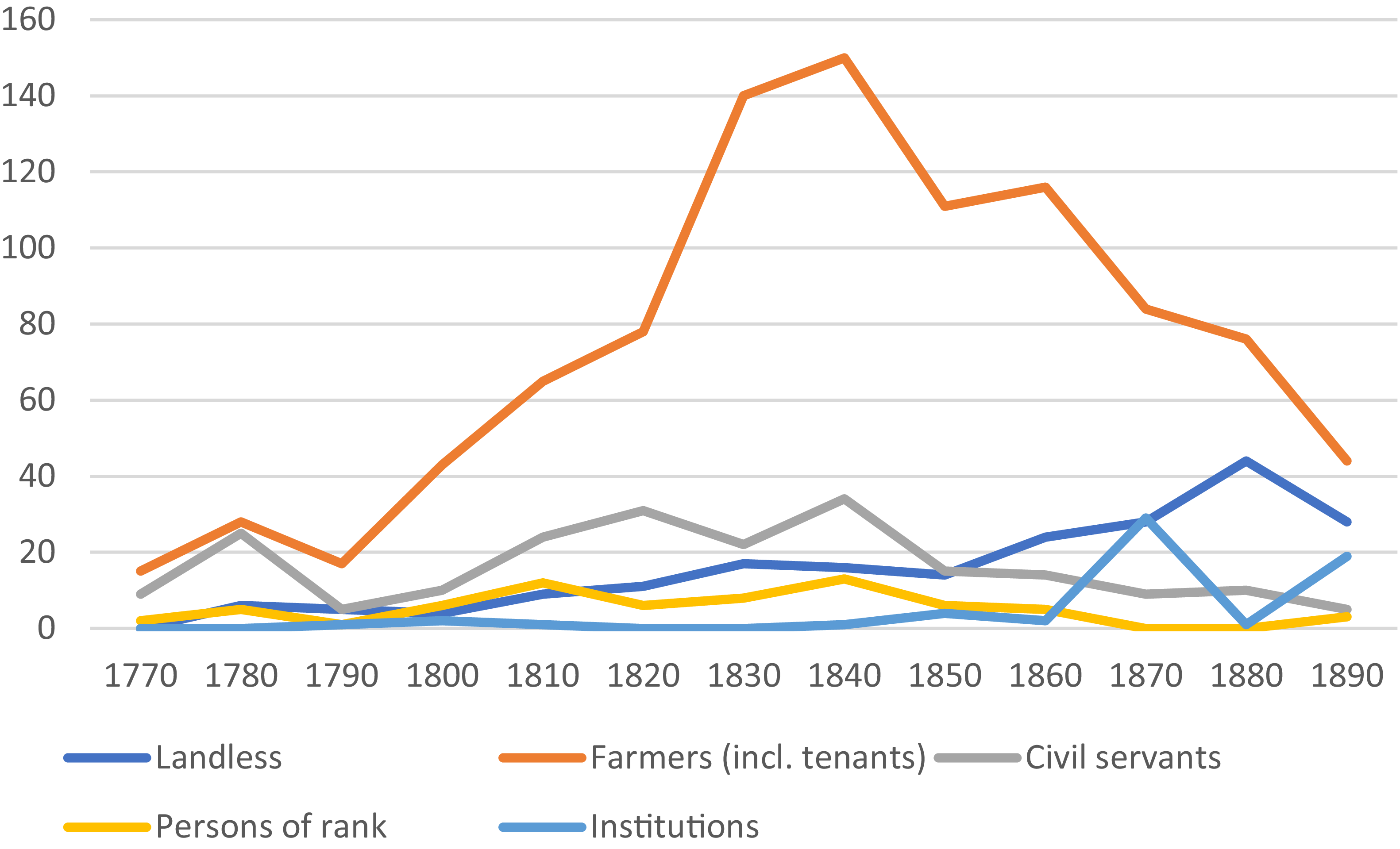

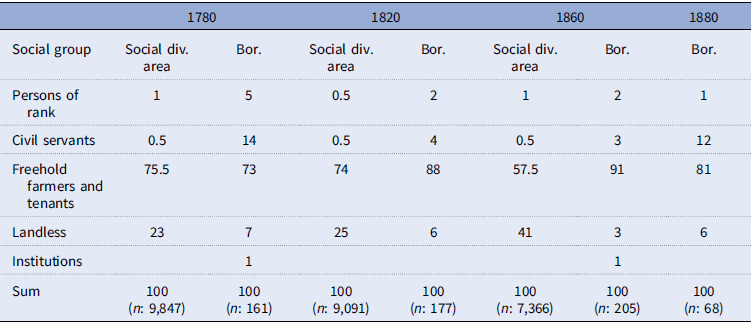

The land in the parishes of Västergötland was owned by freehold farmers, but it was socially divided, with farmers making up about one-third of the population and the landless – crofters, farm hands, and cottagers – making up two-thirds. The freeholders and the few tenant farmers dominated as borrowers. In both 1780 and 1820, they held around 80 per cent of the capital in loans, while the remaining 20 per cent was divided between the landless and the civil servants. The growing funds enabled increased lending, and by 1840, about 200 farmers were borrowing, about a third of all farmers (Table 4, Figure 1).

The social division of borrowers compared with the social strata in the Västergötland province in per cent in 1780, 1820, 1860, and 1890

Source: Calculations of social structure based on the statistical forms in Riksarkivet, Parish archives, ser. G:1. Social structure = the number of people of age in each social group.

* The social division of borrowers from 1810, since the lending was paused around 1820.

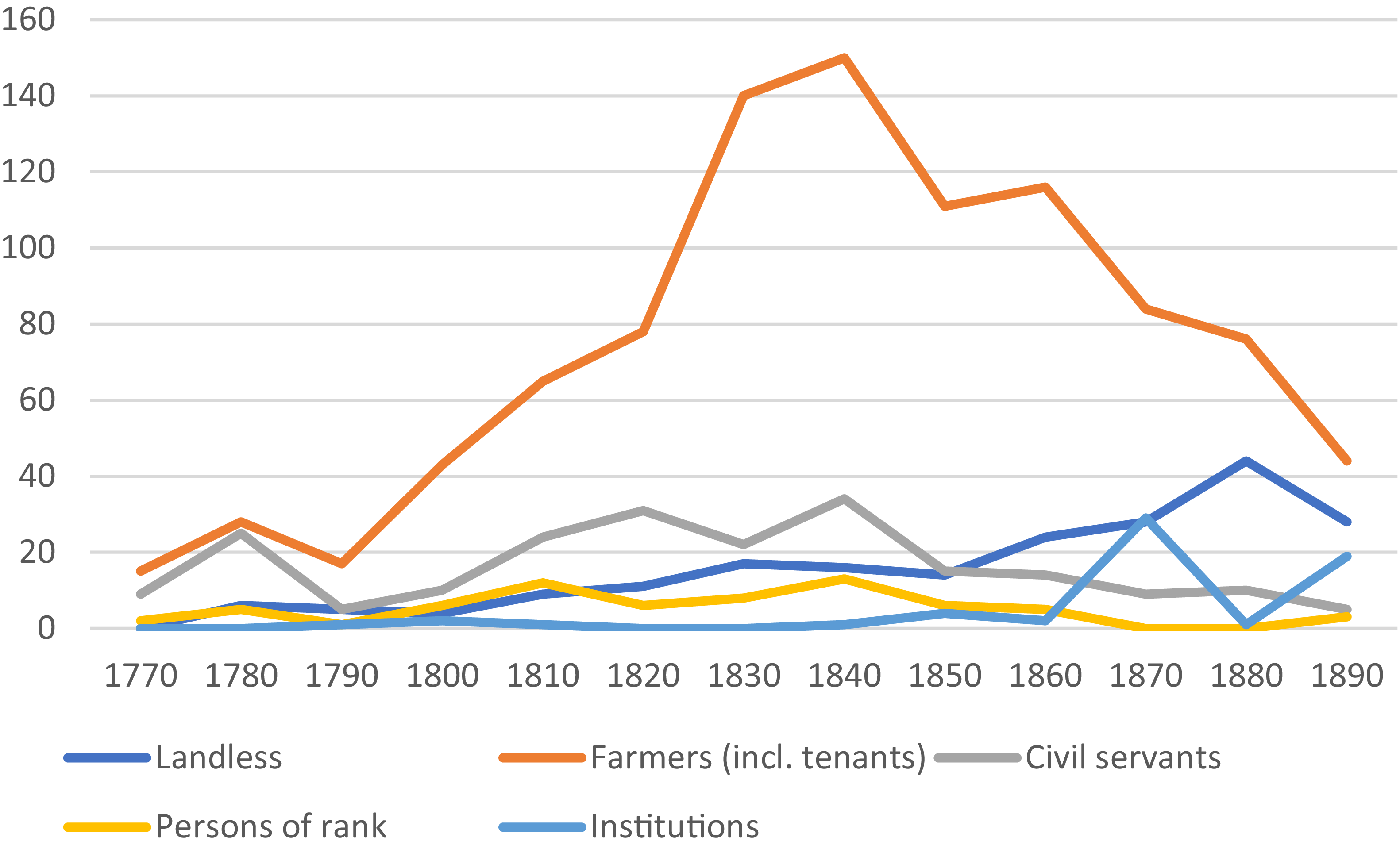

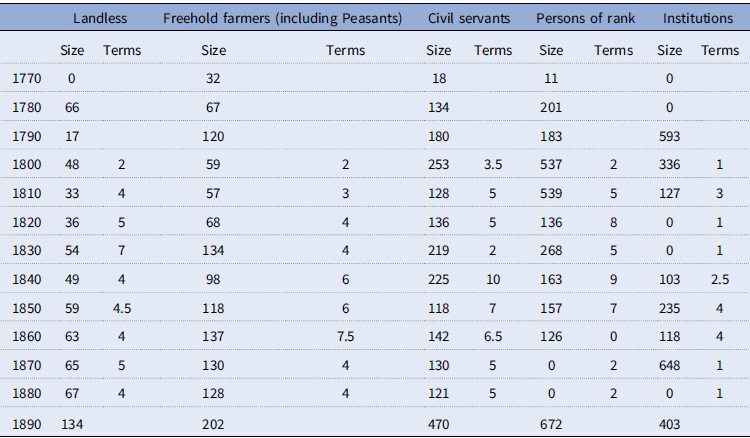

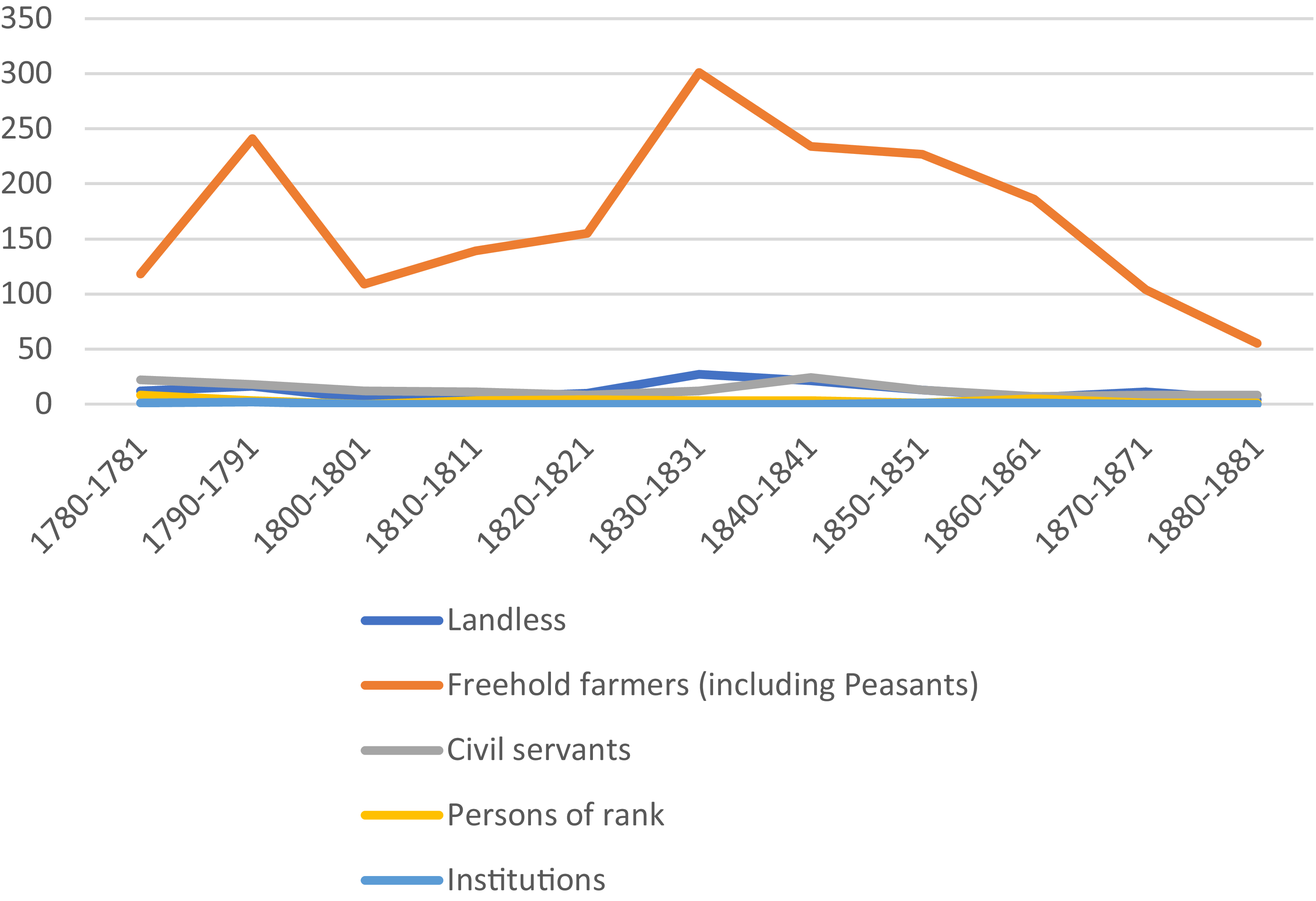

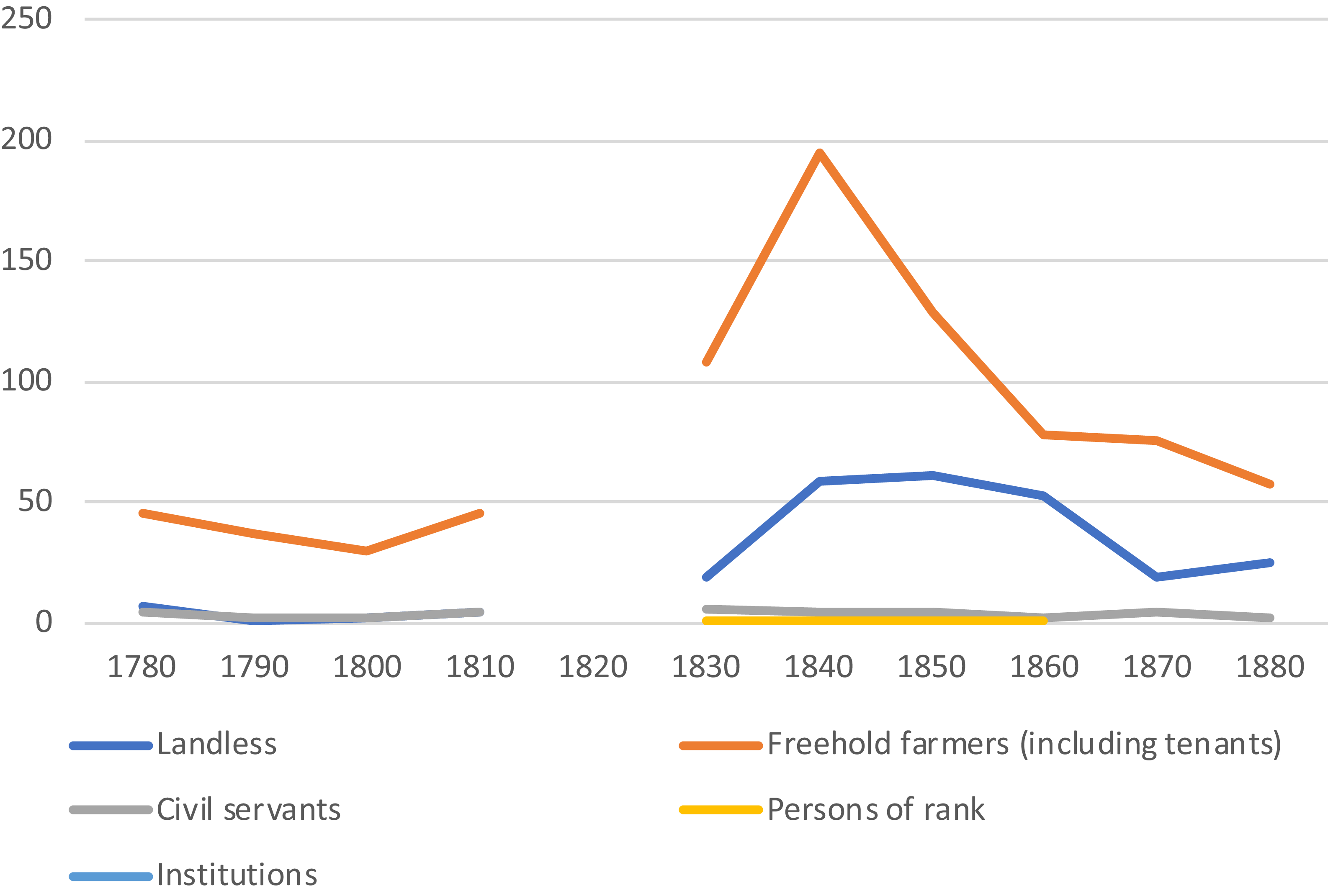

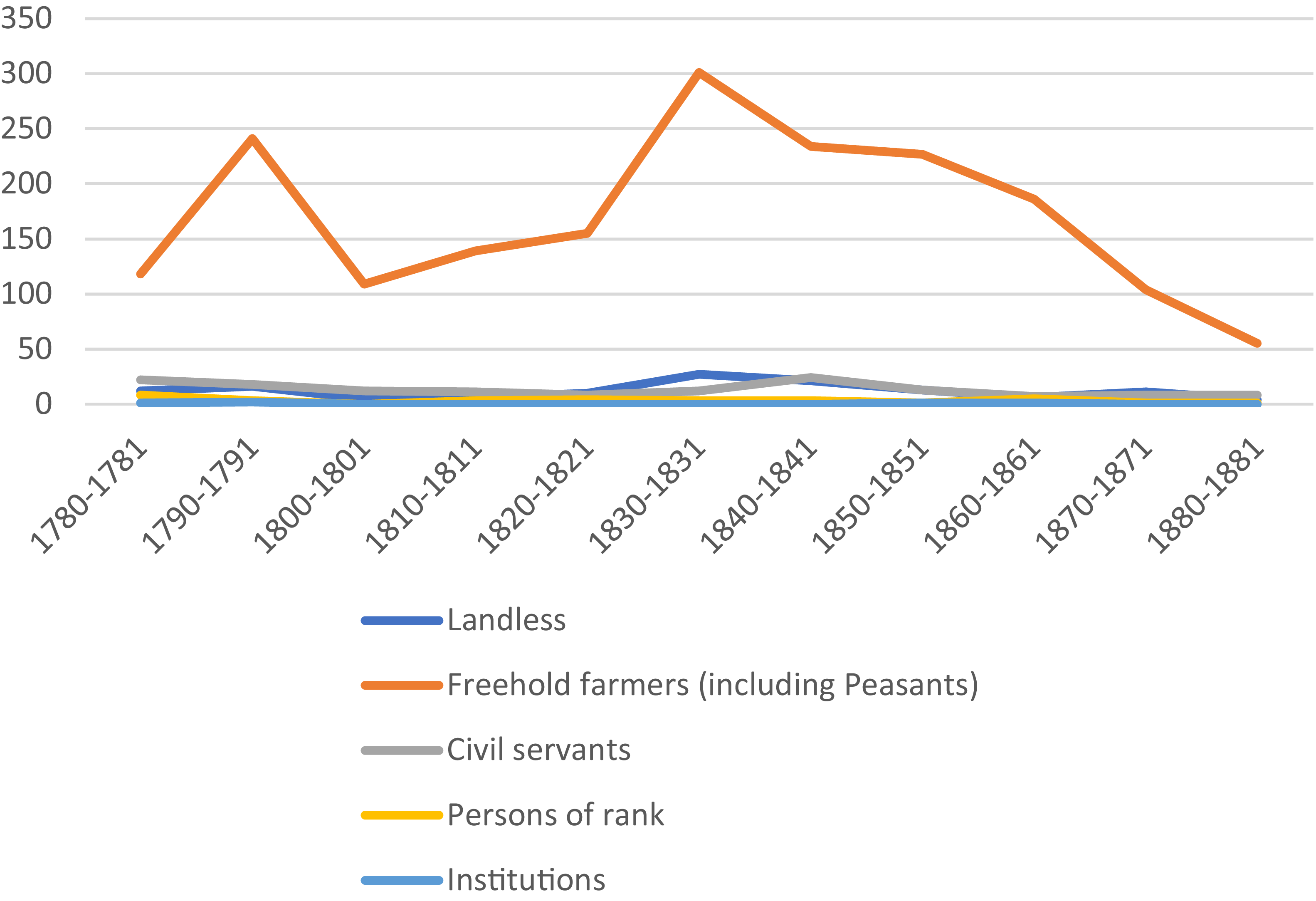

The number of borrowers by social group between 1770 and 1880 in five parishes in Västergötland province.

Farmers remained the main borrowers in the second half of the nineteenth century, but many turned to other institutional lenders during this period. Instead, the landless became borrowers from the 1820s onwards, with about a third of capital in loans by the end of the century.

The decline in the number of borrowers after 1860 was an effect of the decline in the size of the endowments. The majority of borrowers appear to have had only one loan at the time, and if we assume that they each represented a household, then about 20 per cent of all households in the parishes borrowed from the funds.Footnote 47

Of the 1124 borrowers, only 49 (4 per cent) were women, almost all of them widows of freehold farmers, who, under Swedish law, were considered of age and able to run a business. Men also dominated as landowners in the area because male ownership was prioritised in inheritance divisions.Footnote 48

The overwhelming majority of borrowers came from within the parish. Only 4 per cent lived outside the parish, in a neighbouring parish or in another parish, but of the latter almost all lived in the vicinity. When the borrower came from a more distant parish, he was in most cases a vicar. None of the borrowers came from an urban area.

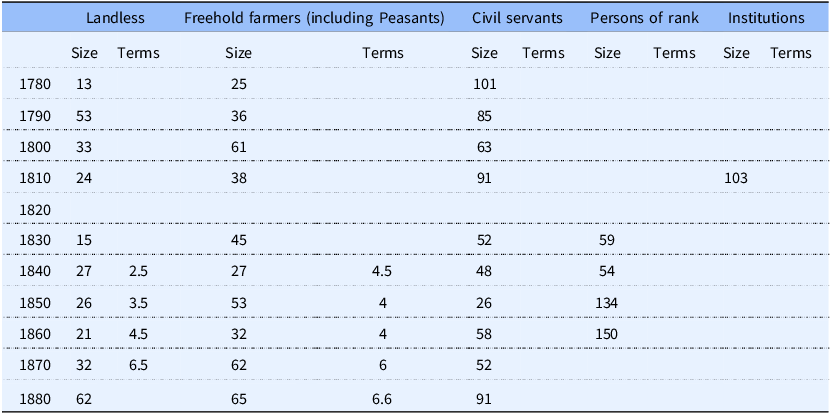

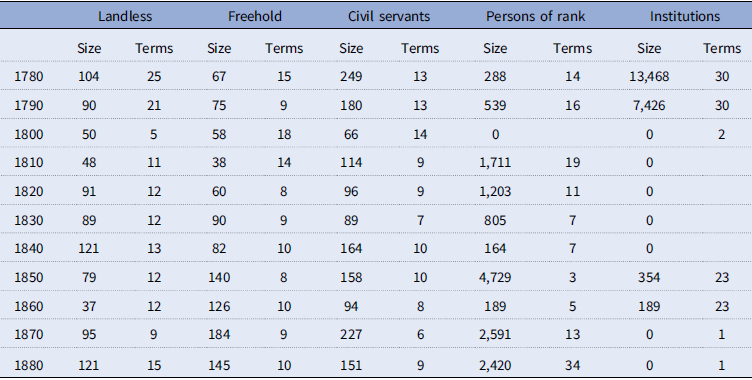

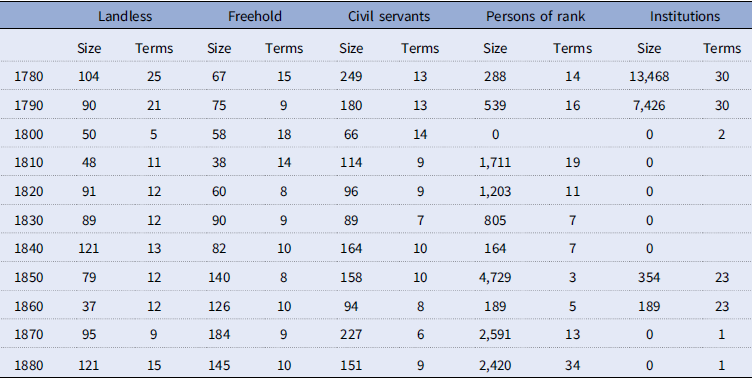

As mentioned above, loan sizes were quite small. The loans of the freeholders rarely exceeded 50 Rd, the average size, and for the landless, most loans were even smaller, only around 20 to 30 Rd. The 50 Rd was the value of a couple of cows or a horse, and 20 Rd could buy a heifer or an ox but could not be used for property purchases; a normal-sized farm in the area was valued at 600 Rd in 1780 and 2900 Rd in 1860. Larger loans were made only to the few civil servants and persons of rank, and in one case to an institution. But even their loans must be considered small, with a median size of around 80 Rd for officials and just over 120 for persons of rank (Table 5). In Svensson’s study of church finances in southern Sweden, most loans ranged from 100 to 200 riksdaler.Footnote 49 By comparison, the average size of a savings bank account in Sweden was 130 Rd in 1850, 162 in 1870, and 256 in 1890.Footnote 50

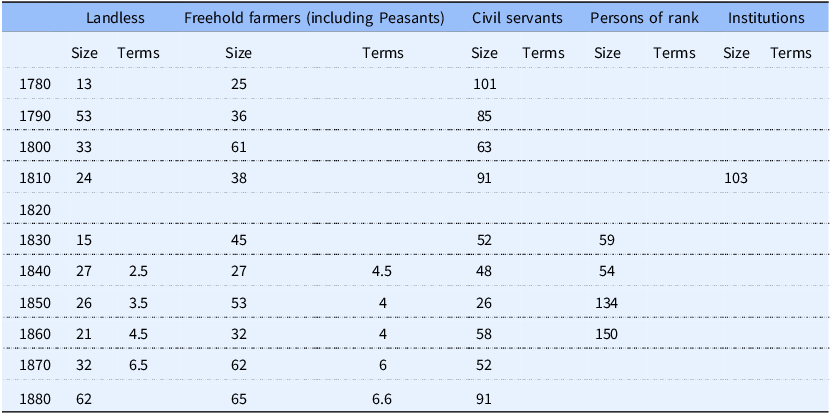

The median size of the loans by social group between 1780 and 1880 and the terms of the loans, median, 1840 to 1880, in five parishes in west Sweden, in fixed prices (Swedish Consumer Price Index (CPI), 1914 = 100)

Source: Härjevad, Rackeby, Skalunda, Saleby, and Trässberg church records, volumes L I:1–12.

Unfortunately, it was difficult to obtain information on the terms prior to 1840, as this information was missing from both the church accounts and the ledgers. The data are based on a rather small sample of only 146 loans and should therefore be treated with some caution, although the average size of the loans appears to be similar to loans in general. The terms of the loans were in most cases short, with a median term of between 2.5 and 6.5 years, most with a mean of around 4.5 years. This is slightly longer than Perlinge’s figure for the duration of private loans in southern Sweden, which is 3.4 years.Footnote 51 After 1870, the terms increased to over 6 years, perhaps as a result of the economic decline that hit farmers in this grain-exporting area in the 1870s. Due to the rather small sample size, it is somewhat risky to discuss any relationships between terms and loan size, but some of the smaller loans taken by the landless tended to have very short terms of around two or three years.

Of the 1119 borrowers listed, information on the type of collateral used is available for 840 cases. Guarantees from neighbours, relatives, and friends dominated, with only two of the 840 borrowers using other types of collateral. 95 per cent of all loans had two freehold farmers as guarantors, and they were also used by the landless and even by civil servants and persons of rank, which may not be so strange since freeholders were the dominant landowners. Three per cent of the loans had persons of rank and civil servants as guarantors, others of their social standing, and, in some cases, landless people in their service.

Central Sweden: Uppland province

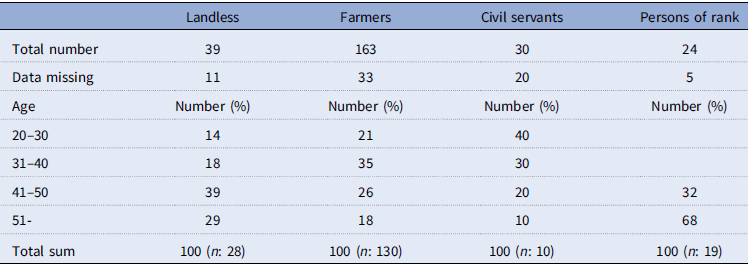

The 223 probate inventories collected from three parishes in Uppland show a very different pattern from the western area.Footnote 52 The comparison between the number of deceased and the number of surviving inventories for 1780, 1820, and 1860 (91 inventories) shows a better representation of persons of rank/civil servants and farmers. The situation was worse for the landless in the late 18th century, but then improved, and by 1860, some 64 per cent of the deceased left an inventory (Table 6).

The number of preserved probate inventories in relation to the number of deceased, after social group, in six parishes in Uppland province 1780, 1820, and 1860

Source: Inventories in Hagunda and Lagunda häradsrätt, F II, information on the number of deceased in Balingsta F:1–2, Fröslunda C:1–3 and F:1, and Giresta C:3 and F:1.

As in the west of Sweden, all households were indebted, but generally with lower debts, around 20 per cent (Table 7). The exception was the 1820s, a period known to be difficult for farmers in eastern Sweden, who had suffered several years of price falls following the Napoleonic wars, bad harvests, and famine in the 1810s. The hard times hit those most dependent on wage labour, the estate owners, but also their subordinates, the tenant farmers and the landless.Footnote 53 Personal loans dominated and, as in the West, institutional lenders became more common in the mid-18th century among freeholders and tenants, but also among persons of rank.Footnote 54 For the latter group, there were several options. The 77 per cent of debt under ‘others’ was mainly owed to institutional lenders such as the House of Nobility, the Army Retirement Fund, and a saltpetre fund. The most important institutional lender in general was the Church, which accounted for between three and 15 per cent of loans to farmers and landless people, or between six and 23 per cent of loans if grain loans from the parish storehouse are included.

The average assets and debts in Rd for persons of rank/civil servants, freehold farmers, tenants, and landless, and the distribution of debts in per cent, in three parishes in Uppland province 1780–1783, 1820–1823, and 1860–1863, in fixed prices (Swedish Consumer Price Index (CPI), 1914 = 100)

Source: Inventories in Hagunda and Lagunda häradsrätt, F II.

*Adjusted proportion of debts, because of a 33 per cent undervaluation of the assets. **Other debts were in almost all cases tax debts to the state or the church.

The endowments of the six parishes in Uppland province had considerable capital to lend. A capital of a full 10,000 Rd (deflated, CPI index 1914) in the 1770s grew to almost 55,000 in the 1830s, which then fell to around 30,000 and after 1880 to just 12,000. The reason for the decline was the building of two churches.Footnote 55

The combination of a rich endowment and the presence of both estate owners and civil servants, as well as many landless people, led to a very different pattern of lending (Table 8, Figure 2). As in the West, freehold farmers dominated as borrowers, constituting about 30 per cent of the households in the area, but about 50 per cent of the borrowers, as high as 72 per cent in 1860. What’s striking is the number of borrowers from the upper classes, who made up around 5 to 6 per cent of the population, but were frequent borrowers. In 1780, they accounted for 47 per cent of borrowers, in 1820 for 29 per cent and in 1860 for 12 per cent. The most eager borrowers were the civil servants, many of them vicars or officers. The landless, who made up about 65 to 68 per cent of the population, took few loans, but they became more common as borrowers towards the end of the 19th century. Some of the loans taken by the landed gentry were in fact donations. The noble families of Tersmeden at Hässle manor, and Spens at Salnecke and Höja manors, donated capital which they then borrowed themselves, with the obligation to pay interest for several decades and eventually pay it off.

The social division of borrowers compared with the social strata in six parishes in east Sweden in per cent in 1780, 1820, 1860 and 1890

Source: Calculations of social structure based on the statistical forms in Riksarkivet, Parish archives, ser. G:1. Social structure = the number of people of age in each social group.

The number of borrowers by social group between 1770 and 1891 in six parishes in Uppland province.

In 1850, there were 588 households in the area and 161 borrowers, which means that almost a third of the households borrowed money from the church funds in the mid-18th century. In the parish of Hagby, which had the most intensive lending activity, more than 50 people paid annual interest, or half the households in the parish.Footnote 56

A strange phenomenon is the presence of institutional borrowers in a few years around 1870 and in 1889-1890, when several savings banks and commercial banks started to borrow large amounts of money from some foundations. The commercial bank Uplands Enskilda bank had around 1870 28 different loans to the Balingsta foundation, ranging from 100 to 2400 Rd, all for very short terms, just one month. At the time, Sweden was going through a financial crisis and the borrowing was probably done to secure capital.Footnote 57

The importance of church funds seems to have declined by the end of the century. One reason for this is that the funds were depleted as new church buildings were built. Farmers also turned to savings banks or private banks instead, as the probate inventories show, but this change was slower in this area than in the west.

Only about 4 per cent of borrowers were women (57 in 1525), three-quarters of them widows after freeholders and civil servants, and a few unmarried women in the 1880s, a time when unmarried women could finally claim legal age and thus borrow money. As in western Sweden, male heirs were given priority when it came to inheriting land.Footnote 58

The final quarter of borrowers are two noblewomen who have been paying interest for decades as part of a donation made in the late 1700s.

The borrowers came mainly (71 per cent) from the parishes, but 25 per cent had their roots in a neighbouring or more distant parish. One exception is Hagby parish, which, with its expanding credit business in the early 19th century, attracted quite a few people of rank, civil servants, and even citizens from the city of Uppsala to borrow capital (5 per cent). The prevailing view is that credit went the other way. Farmers went to the cities to get loans, mainly institutional loans, that were not available in their own or neighbouring parishes.Footnote 59 Rarely do we find examples of burghers travelling to rural areas to obtain (institutional) credit, but this is obviously the case here.

The median size of the loans by social group between 1770 and 1890 in six parishes in east Sweden, and the terms of the loans, median 1800-1880, in fixed prices (Swedish Consumer Price Index (CPI), 1914=100)

Source: Balingsta, Fittja, Fröslunda, Giresta, Gryta and Hagby church records, volumes L I:1-12.

In general, the loans granted were larger than in western Sweden. Loans to the landless were about twice as large as those in the west, at around 30 to 70 Rd (Table 9). The dominant borrowers were crofters and soldiers, who were also part-time crofters-the Swedish army was based on an in-kind economy where soldiers were paid from agriculture. Farmers’ loans were larger, averaging between 100 and 200 Rd. The loans taken out by civil servants and persons of rank ranged from over 100 to 200 Rd and in some years over 500 Rd. The loans were probably used to invest in cattle or tools, given that an ordinary farmstead in this area was worth 900 Rd in 1780 and 2500 Rd in 1860. It is clear that the foundations were an important lender to the upper classes in the late 1700s and early 1800s, both in terms of the number of borrowers and the size of the loans. The terms of the loans were generally between two and six years. From 1820 to 1839 and from 1840 to 1849, the terms were longer, probably as a result of the hard years of the 1820s and the crises of 1845, when the area was hit by bad harvests and famine, followed by bankruptcies.Footnote 60 In the very few studies that exist on this specific topic, the terms seem to be almost the same as in the private market. As Perlinge shows in his study of a municipality in southern Sweden, most loans had terms of two and six years, with an average of around 3.5 years.Footnote 61 The period from 1860 to 1869 was also characterised by several famines, which may have affected the ability to repay the loans. The shortest terms are found among institutional borrowers, who repaid their loans within one or two years.

The endowments of the six parishes in Uppland province had considerable capital to lend. A capital of a full 10,000 Rd (deflated, CPI index 1914) in the 1770s grew to almost 55,000 in the 1830s, which then fell to around 30,000 and after 1880 to just 12,000. The reason for the decline was the building of two churches.Footnote 62

The combination of a rich endowment and the presence of both estate owners and civil servants, as well as many landless people, led to a very different pattern of lending (Table 8, Figure 2). As in the West, freehold farmers dominated as borrowers, constituting about 30 per cent of the households in the area, but about 50 per cent of the borrowers, as high as 72 per cent in 1860. What’s striking is the number of borrowers from the upper classes, who made up around 5 to 6 per cent of the population, but were frequent borrowers. In 1780, they accounted for 47 per cent of borrowers, in 1820 for 29 per cent, and in 1860 for 12 per cent. The most eager borrowers were the civil servants, many of them vicars or officers. The landless, who made up about 65 to 68 per cent of the population, took few loans, but they became more common as borrowers towards the end of the 19th century. Some of the loans taken by the landed gentry were in fact donations. The noble families of Tersmeden at Hässle manor, and Spens at Salnecke and Höja manors, donated capital which they then borrowed themselves, with the obligation to pay interest for several decades and eventually pay it off.

In 1850, there were 588 households in the area and 161 borrowers, which means that almost a third of the households borrowed money from the church funds in the mid-18th century. In the parish of Hagby, which had the most intensive lending activity, more than 50 people paid annual interest or half the households in the parish.Footnote 63

A strange phenomenon is the presence of institutional borrowers in a few years around 1870 and in 1889-1890, when several savings banks and commercial banks started to borrow large amounts of money from some foundations. The commercial bank Uplands Enskilda bank had around 1870 28 different loans to the Balingsta foundation, ranging from 100 to 2400 Rd, all for very short terms, just one month. At the time, Sweden was going through a financial crisis and the borrowing was probably done to secure capital.Footnote 64

The importance of church funds seems to have declined by the end of the century. One reason for this is that the funds were depleted as new church buildings were built. Farmers also turned to savings banks or private banks instead, as the probate inventories show, but this change was slower in this area than in the west.

Only about four per cent of borrowers were women (57 in 1525), three-quarters of them widows after freeholders and civil servants, and a few unmarried women in the 1880s, a time when unmarried women could finally claim legal age and thus borrow money. As in western Sweden, male heirs were given priority when it came to inheriting land.Footnote 65

The final quarter of borrowers are two noblewomen who have been paying interest for decades as part of a donation made in the late 1700s.

The borrowers came mainly (71 per cent) from the parishes, but 25 per cent had their roots in a neighbouring or more distant parish. One exception is Hagby parish, which, with its expanding credit business in the early 19th century, attracted quite a few people of rank, civil servants, and even citizens from the city of Uppsala to borrow capital (five per cent). The prevailing view is that credit went the other way. Farmers went to the cities to get loans, mainly institutional loans, that were not available in their own or neighbouring parishes.Footnote 66 Rarely do we find examples of burghers travelling to rural areas to obtain (institutional) credit, but this is obviously the case here.

In general, the loans granted were larger than in western Sweden. Loans to the landless were about twice as large as those in the west, at around 30 to 70 Rd (Table 9). The dominant borrowers were crofters and soldiers, who were also part-time crofters – the Swedish army was based on an in-kind economy where soldiers were paid from agriculture. Farmers’ loans were larger, averaging between 100 and 200 Rd. The loans taken out by civil servants and persons of rank ranged from over 100 to 200 Rd and in some years over 500 Rd. The loans were probably used to invest in cattle or tools, given that an ordinary farmstead in this area was worth 900 Rd in 1780 and 2500 Rd in 1860. It is clear that the foundations were an important lender to the upper classes in the late 1700s and early 1800s, both in terms of the number of borrowers and the size of the loans. The terms of the loans were generally between two and six years. From 1820 to 1839 and from 1840 to 1849, the terms were longer, probably as a result of the hard years of the 1820s and the crises of 1845, when the area was hit by bad harvests and famine, followed by bankruptcies.Footnote 67 In the very few studies that exist on this specific topic, the terms seem to be almost the same as in the private market. As Perlinge shows in his study of a municipality in southern Sweden, most loans had terms of two and six years, with an average of around 3.5 years.Footnote 68 The period from 1860 to 1869 was also characterised by several famines, which may have affected the ability to repay the loans. The shortest terms are found among institutional borrowers, who repaid their loans within one or two years.

Of the 1525 entries, we have information on the collaterals for 1250, but there is no bias, as information on the collaterals is lacking across all social groups and loan sizes. Seventy-nine per cent of the borrowers used farmers as creditors, the freeholders themselves, and crofters and tenants. Judging from the surnames, most of the creditors were relatives or neighbours. It is clear that the Church’s requirement for security was a reality: very few of the loans granted lacked security. Crofters and tenants could sometimes get their patron as a creditor. Some landless had other landless as guarantors (14 per cent), and some of them used silver or gold objects as collateral (5 per cent). Very few farmers used mortgages as security (0.5 per cent), probably because the loans were so small that it was easier and cheaper to use creditors. Mortgages became more common in the second half of the 19th century and appear to be related to the size of loans. The average size of loans secured by mortgages was 836 Rd.

The civil servants and persons of rank borrowed money under different conditions. The demand for collateral was lower because they were members of the upper classes, gentlemen with reputations to defend and sometimes even some wealth. Most civil servants and persons of rank had friends and relatives as creditors (40 per cent), but surprisingly many used freeholders as sureties (48 per cent). This is interesting because the opposite – freeholders having persons of rank as creditors – was extremely rare. Being a creditor to a landowner or official could be a great advantage. As a creditor, you had some insight into the borrower’s business, and if the borrower went bankrupt, the creditor could be paid in land. Borrowing against mortgages was more common in this higher strata (8 per cent).

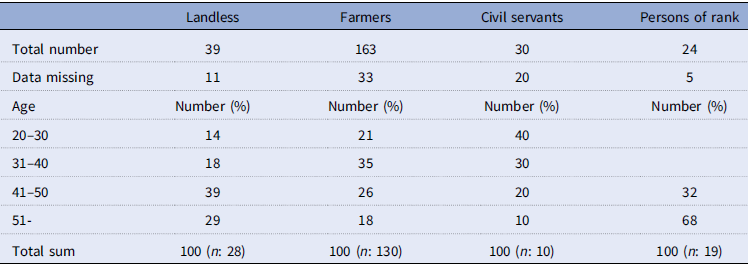

Because the Hagby endowment had such extensive lending and very well-kept records, we have chosen to use Hagby to investigate the age of the borrowers (Table 10). This is possible thanks to information on each borrower’s name, title, and residence, and to the church records, which provide very detailed information on every parishioner’s life, with notices issued annually by the pastors. Of the 270 borrowers from 1770 to 1850, we have data on 201. This includes their age at the time they borrowed money and their marital status. Of the remaining 69, most of them were from other parishes or towns, and therefore, it was harder to find information on them.

Age of the borrowers when borrowing money in Hagby church fund 1770 to 1850

Source: Hagby church records, volumes A I: 1–7 and L I:1–12.

As seen, most of the loans were taken quite early in life, before age 50, which coincides with what Svensson has shown for church funds lending in southern Sweden.Footnote 69 The only exception to this is the persons of rank, who were generally over 50. In Hagby parish, borrowing often coincided with when the household took over a croft or a farm. Five out of nine crofters under the age of 40, 15 out of 20 tenants, 44 out of 72 freeholders, and 6 out of 11 civil servants took a loan when they moved in. After age 50, loans were taken for a variety of reasons, including the death of a spouse or children moving out of the household. This pattern of borrowing to start a household, which in many cases led to over-indebtedness, is confirmed by several studies covering the early and mid-1800s.Footnote 70

The mining districts: Dalarna province

In the mining district of Dalarna, the number of inventories was relatively small compared to the number of deceased, which is also recognised in earlier works.Footnote 71 The lack of preserved inventories from the 18th century has forced us to limit the years to around 1820 and 1860 (Table 11).

The number of preserved probate inventories in relation to the number of deceased, after social group, in two parishes in Dalarna province 1823 and 1860

Source: Inventories in Stora Skedvi and Stora Tuna häradsrätt, F II, information on the number of deceased in Stora Skedvi F:14 and 17 and Stora Tuna F:3:and F:5.

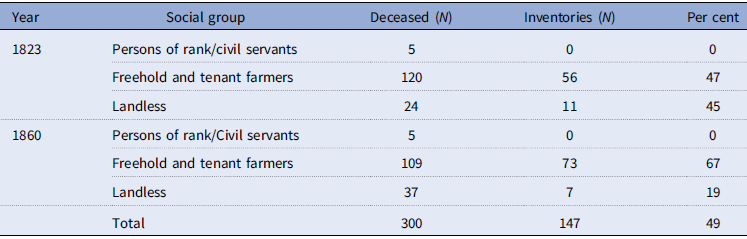

The poverty of the area is quite obvious when compared with the counties of Västergötland and Uppland, with generally lower assets and lower farm values (Table 12). Land was more evenly distributed in Dalarna, and soldiers and craftsmen, who would have been among the landless in the grain-producing west and central Sweden, were in many cases landowners, owning small shares in the hamlets. Widows and unmarried women were also more likely to be landowners. Debt was generally lower than in the west and centre, but private loans dominated both in 1823 and in 1860. The church played a minor role as a lender.

The average assets and debts in Rd for freehold farmers and landless, and the distribution of debts in per cent, in two parishes in Dalarna province c1820 and c1860, in fixed prices (Swedish Consumer Price Index (CPI), 1914 = 100)

Inventories in Stora Skedvi and Stora Tuna häradsrätt, F II.

* Adjusted proportion of debts, because of a 33 per cent undervaluation of the assets.

** Other debts were in almost all cases tax debts to the state or the church.

The parishes in the mining district were very different from the grain-producing west and central Sweden, with a flexible and diversified economy dominated by freeholders on small self-supporting farms, with some farmers working as charcoal producers for the ironworks, craftsmen specialising in the manufacture of iron utensils and tools, and many supporting themselves as seasonal workers in the south.

The endowments of the three parishes were substantial in the late 18th century but declined in the early 19th century due to the construction of new church buildings and the effects of the Napoleonic Wars. Reduced church funds limited lending, and interest on loans was a minor source of income. As in the parishes further south, lending increased from the 1820s, especially in Stora Skedvi, which had a more agricultural economy than the other parishes.Footnote 72

As can be seen from the probate inventories, church endowments were of much less importance. There were 3106 households in the area in the mid-1800s, and 205 borrowers (representing one household), indicating that only 7 per cent of households used the endowments.Footnote 73

Freeholders dominated as borrowers (Table 13, Figure 3), accounting for 88 per cent of borrowers in 1820, while constituting 74 per cent of the population. The landless, who made up between 23 and 41 per cent of the population, accounted for only six to seven per cent of the borrowers. As in central Sweden, persons of rank and civil servants were borrowers, but here during the whole 19th century. They represented only about 1 to 1.5 per cent of the population, but 19 per cent of the borrowers in 1820, six in 1820, five in 1860, and 13 in 1880. Among them we find ironwork owners, officers, and vicars. This popularity could be due to the limited opportunities for borrowing money in this area, with few and small towns.

The social division of borrowers compared with the social strata in six parishes in east Sweden in per cent, and the median size of the loans in 1780, 1820, 1860, and 1880

Source: Calculations of social structure based on the statistical forms in Riksarkivet, Parish archives, ser. G:1. Social structure = the number of people of age in each social group.

The number of borrowers by social group between 1780 and 1880 in three parishes in Dalarna province.

The loan sizes were similar to those in Uppland, ranging from 100 to 200 Rd. These could be used to purchase smaller farms, as they were cheaper at around 600 Rd in 1820. The loans of the few ironworks owners, officers, and civil servants were considerably larger, in some cases over 2000 Rd (Table 14). Women were more frequent borrowers in this area, accounting for eight per cent (228 out of 2807). This is probably due to the area’s more equal socio-economic nature, with more women being landowners than in eastern and western Sweden.

The median size of the loans by social group between 1770 and 1891 and the terms of the loans, median, in three parishes in the mining districts, mean, in fixed prices (Swedish Consumer Price Index (CPI), 1914 = 100)

Source: By Stora Skedvi and Stora Tuna church records, volumes L I:1–12.

Many of the borrowers were widows, but we also found wives, daughters, and landless women among them. The borrowers all came from the parishes, except for two. The parishes were all huge, covering 101,000 hectares of land (compared to the five parishes in the west together covering 9000 hectares and the six in Central Sweden covering 10,000 hectares), which meant that several borrowers came from rather long distances.

Here, the average loan was repaid after around 15 years. At the end of the 18th century, the average term could reach 20 to 25 years. In the course of the 19th century, the terms decreased but were still around 10 years at the end of the century. Around 300 of the loans had terms of 20 to 30 years, 120 of 30 to 40 years, and 80 of 40 to 65 years! Those with terms of 30 years or more were often inherited in the family and paid off by a grandchild or great-grandchild. Each time a debtor died, the heir made a new arrangement with the creditors or, if the creditors had also died, found a new pair. If the debtor couldn’t pay the interest, the creditors had to step in, and sometimes they had to borrow money themselves, a debt that could be passed on to a younger generation. The landowner Johan Persson’s loan of 25 Rd in 1772 was in 1830. The only borrowers on more normal terms were the very few persons of rank, a few officers, and the owners of ironworks. inherited by his sons’ widow, Anna Ersdotter, in 1804 and, after her death in 1815, by her son, Samuel Persson, who went bankrupt in 1820 and was finally paid off by his guarantors

The predominant form of security in Stora Tuna was co-signatory notes. Freehold farmers had relatives and neighbours as creditors. About 14 of the loans had a larger group of borrowers and guarantors, called ‘one for all, all for one’, a type of collateral that also occasionally appeared in Central Sweden. As in east Sweden, the persons of rank and civil servants had friends and relatives as guarantors (26 per cent), but freeholders also dominated here (62 per cent). Loans against mortgages were used primarily by the upper classes.

The natural farming areas of Sweden.

Conclusions

The Swedish Lutheran Church was one of the largest institutional lenders in Sweden until the mid-18th century, while on the other hand, according to previous studies in this field, loans from the church funds are rarely found in 18th and 19th-century probate inventories.

In this paper, we have combined information from church account books and probate inventories across three geographical areas, spanning ca. 1770 to ca. 1900, to gain a deeper understanding of the church’s role as a lender. The study was based on five parishes in the grain-producing, freeholder-dominated western Sweden, six in the grain-producing, more feudal and urbanised eastern Sweden, and three in the mining district in the north, combined with 507 probate inventories from all areas.

As shown here, the church’s success as a lender was due to its strong local presence, with parishioners both controlling the church’s funds and serving as the main borrowers. Most loans were relatively small and were repaid after a few years. As both Aronsson and Svensson have pointed out, the relatively small loans and relatively short loan periods meant that the church might have been used in cases of urgent capital needs.Footnote 74 Co-signatory loans totally dominated, for instance. Only a few per cent of the loans used mortgages as security, most commonly in the latter half of the 19th century and when larger loans were borrowed. The church funds had many similarities with contemporary institutional lenders in both urban and rural societies, consisting of local networks with strong liability, which reduced administrative costs.Footnote 75 It is also obvious that the church funds should be recognised as a semi-institutional lender, similar to the functioning of the private credit market, embedded in a peasant society and just one aspect of all social interactions in society.Footnote 76 The interest also went to a good cause, ensuring the presence of the church.

The freeholders, the dominant landowners in all three areas, were also the main borrowers, generally with around 70 to 80 per cent of the loans. Until the mid-1800s, the nobility and civil servants were also common borrowers, especially in feudal Central Sweden, and often used freehold farmers as co-signatories. However, as mentioned earlier, if there was a shortage of capital, the most trusted individuals may have been selected, which means that members of the nobility and freeholders may have been given priority at the expense of landless individuals.

In both western and eastern Sweden, landless people became more common as borrowers in the last decades of the 19th century, partly because they were becoming more numerous and partly because landowners and members of the upper classes may have turned to other institutional lenders offering lower interest rates. Farming also became more capital-intensive in the second half of the nineteenth century, and the church funds may have been too small to meet this demand for larger loans. Almost all borrowers came from the parishes or neighbouring parishes, with the exception of eastern Sweden, where 10 per cent of borrowers came from more distant parishes. The church funds of East Sweden also attracted borrowers from the city of Uppsala, a phenomenon rarely noted in previous studies; the reverse was well known, rural dwellers borrowing urban capital.

The role of church funds was different in the three areas, but by no means insignificant. In mid-1800s, an estimated one-fifth of all households borrowed from the church funds, if we assume that each loan represented a household, 20 per cent in the West, 30 per cent in the East, and around 5 per cent up north.

However, the probate inventories analysed here contain rather few loans from church funds, which partly confirms the results of previous studies that private loans dominated until the late 19th century. In western Sweden, only 1 per cent of the debts were owed to the church, in the mining district around two to 3 per cent, while in eastern Sweden the share of debts owed to freehold farmers and landless people was up to 15 per cent. Since the general terms of church loans seem to be similar to private loans, church loans shouldn’t be underrepresented in the inventories. However, the majority of church loans seem to be taken early in the household cycle, before the age of 40, and since the number of inventories after younger people is quite low, this may be one explanation why church loans are rarely visible in the inventories.

The Lutheran Church in Sweden was obviously an important institutional lender, or more precisely a semi-institutional lender, as it operated in a strong social context. The church is probably an underestimated lender in northern Europe, but we still lack knowledge about its role in the credit market as a whole. Was the decline in lending from the mid-18th century a result of increased competition from other institutional lenders, or was the reduced funds, due to increased investment in church buildings, which limited lending?

Printed

BiSOS (Bidrag till Sveriges Officiella Statistik) 1885, ser. N. Jordbruk och boskapsskötsel.

BiSOS (Bidrag till Sveriges Officiella Statistik) 1880 ser. A. Befolkning

Acknowledgements

This work was financed by a three-year grant from the Jan Wallander and Tom Hedelius Foundation and the Tore Browaldh Foundation (P2015-0094:1). We would like to thank Stefan Andersson for his assistance with the excerpt and Lars Fälting and Måns Jansson for their generous help with comments. We would also like to thank Sarah Linden-Passay for her proofreading assistance.

Archives

Riksarkivet i Uppsala

Balingsta kyrkoarkiv

F:1 – F:2 Död och begravningsbok 1780–1861.

G:1 Redogörelser för folkmängden

L Ia:4 – L Ia:13 Huvudräkning och skuldbok 1787–1942.

By kyrkoarkiv

G:1 Redogörelser för folkmängden (Tabellverket).

L Ia:2 – L Ic:12 Kyrkoräkenskaper och skuldbok 1778–1881.

Fittja kyrkoarkiv

G:1 Redogörelser för folkmängden (Tabellverket).

L Ia:3 – L Ia:12 Kyrkoräkenskaper och skuldbok 1737–1932.

Fröslunda kyrkoarkiv

C:1 – C:3 Död och begravningsbok 1743–1893.

G:1 Redogörelser för folkmängden (Tabellverket).

L Ia:1 – L Ia:12 Huvudräkenskaper och skuldbok 1727–1946.

Giresta kyrkoarkiv

C:3 and F:1 Död och begravningsbok 1741–1861.

G:1 Redogörelser för folkmängden (Tabellverket).

L Ia:2 – LIa:6 Huvudräkenskaper och skuldbok 1740–1900.

Gryta kyrkoarkiv

G:1 Redogörelser för folkmängden (Tabellverket).

L Ia:5 – L Ia:9 Huvudräkenskaper och skuldbok 1777–1924.

Hagby kyrkoarkiv

G:1 Redogörelser för folkmängden (Tabellverket).

A I Husförhörslängder

L Ia:3 – L Ia: 7, Kyrkoräkenskaper och skuldbok 1771–1944.

Stora Skedvi kyrkoarkiv

F:14 – F:17 Död och begravningsbok 1803–1861.

G:1 Redogörelser för folkmängden (Tabellverket).

L Ia:8 – L Ic:3 Kyrkoräkenskaper och utlåningsbok 1758–1897.

Stora Tuna kyrkoarkiv

F:3 – F:5 Död och begravningsbok 1813–1860.

G:1 Redogörelser för folkmängden (Tabellverket).

L 1a:2 – L 1e:5 Kyrkoräkenskaper och skuldbok 1778–1909.

Hagunda häradsrätt

FI:4 – FI:18, Bouppteckningar 1781–1864

Lagunda häradsrätt

FII:8 – FII:23, Bouppteckningar 1780–1866

Stora Skedvi tingslags häradsrätt

F2:13 – F2:22, Bouppteckningar 1821–1860

Stora Tuna tingslags häradsrätt

Stora Tuna FII:2, F II:37, Bouppteckningar 1823 and 1860

Riksarkivet i Göteborg

Härjevad kyrkoarkiv

C:2 död och begravning 1755–1836

G:1 Redogörelser för folkmängden (Tabellverket).

L I:2 – L I:5 Specialräkenskaper 1756–1864

Rackeby kyrkoarkiv

C:1 Födelse och dopbok 1691–1787.

F:1 Död och begravningsbok 1861–1894.

G:1 Redogörelser för folkmängden (Tabellverket).

E:2 – E:3, Lysnings och vigselboken 1834–1894.

L I:1 – L I:4 Huvudräkenskaper och skuldbok 1758–1894.

Saleby kyrkoarkiv

C:2 Födelse och dopbok 1741–1790.

F:1 Död och begravningsbok 1851–1874.

G:1 Redogörelser för folkmängden (Tabellverket).

L I:3 – L I:12 Huvudräkenskaper och skuldbok 1755–1887.

Skalunda kyrkoarkiv

G:1 Redogörelser för folkmängden (Tabellverket).

L I:1 – L I:4 Huvudräkenskaper och skuldbok 1758–1918.

Trässberg kyrkoarkiv

G:1 Redogörelser för folkmängden (Tabellverket).

L I:2 – L I:6 Huvudräkenskaper och skuldbok 1758–1877.

Kållands häradsrätt

FII:10 – F II:36, bouppteckningar 1779–1862

Skånings häradsrätt

FII:13 – FII:36, bouppteckningar 1780–1867

Open access

Open access