1. Introduction

The history of banking activity within Latin American countries took a dramatic new turn in the 1880s, as a new financial transformation took place in which prize of place was taken by the ascent of national banks. Prior to the aftermath of the early panics of the 1870s, only a half dozen nations in this vast region had experienced the first stages of a banking revolution, but by the end of the 19th century, banks began to multiply in most countries, large and small.Footnote 1 At the same time, regional banks emerged in the more dynamic economic zones throughout most of South America, as well as across northern and central Mexico. However, perhaps the most striking feature in the 1880s was the consolidation of large banks that established networks of branches. These enterprises surpassed earlier financial entities in size and their greater capacity to provide credit. Their broader geographical reach was the result of the launching of numerous offices and agencies in capital cities as well as in regional centers, where the big banks were determined to force entry in order to capture clients and business of diverse types. Regardless of whether such entities were founded as private, public, or mixed companies, they generally became the largest financial organizations in nations such as Argentina, Brazil, and Chile, but also in Mexico, Colombia, and Uruguay, as well as Bolivia, Haiti, Santo Domingo, and Costa Rica, during the last decades of the century.Footnote 2

The birth and trajectory of the largest national banks took place at a series of historical crossroads that were characterized by the modernization of state administrations, in parallel to the launching of important development projects throughout Latin America and precisely at a time when national identities began to consolidate. Gradual economic integration, the reform of monetary regimes, and the shaping of financial systems went hand in hand. This essay suggests, therefore, that in the last quarter of the 19th century, there was a kind of co-evolution of state structures and banking development in much of Latin America.Footnote 3 While this process involved specific arenas of political and economic negotiation, all were part and parcel of the process of nation-building. Each of the so-called national banks emerged in a particular context and assumed specific tasks, but practically, all contributed to the extension of credit in the private sector, facilitated increased integration of payments systems, prompted the use of banknotes, and provided financial services to governments. These enterprises gained opportunities to handle public debts—domestic and external—that offered profits, but they also faced potential dangers of bankruptcy in cases of poor financial strategies and/or monetary mismanagement. It should be noted that while a given bank could acquire special privileges that offered specific advantages in the issue of banknotes, there were various circumstances in which several large financial enterprises of a similar size were competing at the same time in a given country, as will be seen in this chapter. In some cases, a given bank would be awarded a monopoly of the issue of banknotes, but, often enough, plurality of issue remained common.

National banks in Latin Americaa

Table 1 Long description

The table lists national banks in Latin America and the years each operated, generally in the late nineteenth century. Most entries begin between 1851 and 1890 and end before 1915, indicating many were short-lived or later reorganized. The earliest start is Banco do Brasil in 1851, ending in 1893 in this listing. Several banks ended around the early 1890s, including those in Chile, Argentina, Uruguay, Paraguay, and Colombia. Only two banks are shown as continuing to 2024: Banco Nacional de México, founded in 1884, and Banco de Venezuela, founded in 1890. Haiti’s national bank runs from 1880 to 1911, and Santo Domingo’s from 1889 to 1914, extending later than most others but not to the present. The date ranges reflect the specific national-bank phase or institutional continuity as recorded, and some banks later merged, renamed, or were replaced by successor institutions.

Note: A major source of the information regarding this table can be found on the academic website referenced here: https://hbancaria.org/es/inicio/.

a In this table, we include banks in Latin America that identified themselves as national banks (the majority being privately owned) toward the end of the 19th century, with the right to issue banknotes and generally maintaining close relationships with the respective governments.

b Banco do Brasil merged with other banks in 1893 and then closed its doors in 1900, reopening in 1906 and continuing to operate today as the largest commercial bank in Brazil.

c The Banco Nacional de Chile merged with two other banks in 1893 and formed Banco de Chile, which has been one of the largest in the country since then and until the present day.

d After the bankruptcy of the National Bank of Argentina in 1890, the Banco de la Nación was created in 1891, reactivating many of the old branches of its predecessor; today, Banco de la Nación remains the largest bank in Argentina.

e The Banco de la Unión de Costa Rica changed its name to Banco de Costa Rica in 1890 and has continued to operate down to the present day.

The creation of national banks in many Latin American countries during the last quarter of the 19th century raises several major questions, beginning with the issue of why there should have been such enthusiasm for the promotion of this type of financial enterprise based on official concessions that offered numerous privileges.Footnote 4 A first hypothesis concerns the interests of political and economic elites who wished to profit from taking control of the growing financial requirements of governments that were experiencing political and economic changes in the process of consolidation of nation–states. The 1880s marked the zenith of a number of strong political and military leaders in most of Latin America, figures who had the capacity to submit regional elites and integrate them into nominally liberal political projects espoused by authoritarian regimes. Forceful personalities such as General Julio Roca, who was president of Argentina in the years 1880–1886, or General Porfirio Diaz, a long-time autocratic ruler of Mexico from 1876 to 1910, stood out. However, so did the conservative, centralist politician Rafael Nuñez in Colombia (1880–1886), and the popular but highly controversial president, José Manuel Balmaceda, in Chile (1886–1891), to mention only a few of the various architects of a new political order in Latin America that was characterized by parliamentary and constitutional regimes that were emphatically conservative and oligarchic, but at the same time modernizing and increasingly capitalist.

The promotion of national banks was near the top of the list of economic priorities adopted by most of the powerful autocrats who headed parliamentary regimes bent on the modernization of their administrations as well as their societies and economies. Latin American elites looked to Europe for new models of governance.Footnote 5 They were cognizant of the fact that the consolidation of national administrations had gone hand in hand with the establishment of large banks in close relation to states. The pioneering roles of the Bank of Sweden (1668) and the Bank of England (1694) were clearly influential, being among the oldest in the world (Edvinsson et al., Reference Edvinsson, Jacobson and Waldenström2018, chapters 3 and 4). However, Latin American elites, particularly leading entrepreneurs, merchants, and private bankers, were also aware of the role of other institutions such as the Banque de France (1800) and the Oesterreische Nationalbank of Austria (1818). Equally important were examples of large banks established after 1850 in various European nations.Footnote 6 A significant example was the foundation of the Banque Nationale de Belgique (1850), which eventually became a central bank, but actually began as a firm dedicated to commercial banking operations. More imposing was the Reichsbank of Germany, created in 1875 as a consequence of the union of the German states and the launching of the first Reich by Bismarck. At the same time, news spread of the transformation of the Bank of Spain into the dominant institution within the Spanish financial system as a result of the political crisis of 1874 that inaugurated a long-lasting conservative regime (Aceña et al., Reference Aceña, Martínez-Ruiz and Nogues-Marco2013, p. 26).

In general, Latin American professional and economic elites interested in financial reform were increasingly aware of innovations in monetary and banking legislation not only in Europe but also in the United States. Not surprisingly, the concrete experiments of the diverse Latin American elites with banks reveal distinctive circumstances in the manner in which they formulated the institutional frameworks of their emerging banking systems and regimes, as well as the operational structure of the principal banking entities.

In short, the creation of national banks represented a significant innovation within the dual process of capitalist development and state modernization in Latin America. Some were public banks, but most were privately owned. Practically, all had privileges of banknote issues, and several were charged with the management of government accounts and frequently enough with the negotiation and service of public debts, but they were hard put to fulfill the role of lender of last resort, since they were not central banks. As commercial banks, they attracted numerous private clients who opened deposit accounts and took loans, but they also frequently operated as investment firms and, in some cases, carried on a significant mortgage business. In general, the national banks played an important role in expanding monetary circulation through the introduction and increasingly widespread use of banknotes, as well as by the extension of their credit facilities, stimulating the gradual integration of financial markets in various countries. Their activities were part and parcel of the economic growth generated primarily by agricultural and mining exports, accompanied by early urban and railway expansion. Nonetheless, the new national banks were not necessarily well prepared to confront local financial crises that were the result of booms and busts characteristic of the spread of capitalism almost everywhere. In fact, a good number of the larger banking enterprises that came of age in Latin America during the 1880s would face enormous stress as a result of extensive financial and debt crises in the 1890s and, in some cases, collapsed.

2. National banks and government: a two-way relationship

The emergence of increasingly complex banking systems in Latin America in the late 19th century cannot be understood without thoroughly examining the relationship between the government and one or two major banks, which occupied a most influential place within the respective banking regime of almost every nation in this era. The preeminent role of such entities was largely the result of the charters granted to them by the government as a result of complex negotiations between political and financial elites who bargained hard for privileges regarding the issue of bank notes as well as the management of fiscal and public debt accounts. We follow here the interpretations of Calomiris and Haber (Reference Calomiris and Haber2014) in their path-breaking work Fragile by Design.Footnote 7

The banks closest to the government inevitably benefited from public business, but politicians also frequently gained much from the access to credit for their own private business. As joint-stock companies, the banks sold their stock on local markets, but basically to the wealthiest members of society. In this sense, it can be argued that the high degree of banking concentration of the privileged institutions contributed to the disproportionate economic strength acquired by certain groups of the financial, mercantile, and landowning elites in Latin America during the late 19th century. In this regard, it should be borne in mind that there generally was not a strict regulation or supervision of banks at this time, although some early banking laws provided guidelines. The individual charters were firm-specific and thus largely depended on bank managers and directors to maintain observance of relatively limited sets of operating rules, especially with regard to the volume of banknote issue and capital requirements.

The influence exerted over the largest banking enterprises by political leaders and/or lobbies in most Latin American nations was a common feature of the age. As a result, opportunities to obtain large profits through non/transparent business transactions and insider lending by both financiers and politicians proved inexorable. Financial public and private affairs were mixed and symbiotic. The privileges granted to banking firms with regard to the issue of banknotes provided economic power since this allowed them to control a large share of the currency in circulation. In the pages following, we detail the relative proportions of issue of banknotes by the various larger banks in the case of Argentina, Brazil, and Chile, since in those cases, we have located statistical data from the late 1880s that allows for detailed comparison, as is shown in the brief case studies in this essay.

The creation of enterprises such as the Banco do Brasil, Banco Nacional de Argentina, Banco Nacional de Chile, or the Banco Nacional de México, among other large banking firms, propelled a downward trend in information and money costs for the respective governments, as well as for private enterprise. It should be noted, however, that the relations between large banks and governments took somewhat different paths. For instance, the Banco do Brasil (1853), the Banco Nacional de Chile (1867), and the Banco Nacional de México (1884) were private firms that managed financial operations for both the private sector and governments. In contrast, the Banco Nacional de Argentina (1872) was more of a public bank, insofar as the government had participated in its capital structure since its foundation; even so, commercial operations with private clients were a prominent feature of its activities. Evidently, the national banks exhibited distinct political and entrepreneurial components, as well as different institutional frameworks, yet they all illustrate the complex relations between capitalist development and administrative modernization, exhibiting numerous parallels and contrasts, as well as successes and failures.

3. The large banks, capitalists, and financial development in the late 19th century

Apart from the role of national banks as de facto government banks, these enterprises were also profitable for the groups that controlled them, from an entrepreneurial perspective. The commercial banks offered new financial capabilities that surpassed those of traditional merchant bankers that operated domestically. The new entities contributed to the adoption of technical and organizational innovations that far exceeded the capabilities of private or family firms of bankers. Other features of the establishment of large joint-stock banks included a departmental organization, which separated functions more clearly, including the management of deposits, savings accounts, credit, loans, and reserves. In addition, the national banks were especially effective in spreading the use of fractional reserve money issue (bank bills), which some authors consider a revolution in financial markets, although it should be underlined that the banks were used mainly by economic elites and state administrations. The banknotes contributed to the creation of new forms of money and their circulation, whether as a consequence of the issuance of banknotes or from the discount facilities that expanded as deposits increased, increasing sources of credit and giving rise to broader circles of clients.

The new banking enterprises also prospered as a result of the expansion of financial markets within Latin America in the late 19th century. Stock markets experienced a golden age in several countries during the late 1880s, allowing the establishment and growth of numerous joint-stock companies, notably the large domestic banks. The new trends were mirrored by the marked improvement in the financial information provided by the local newspaper economic press in the larger nations during the 1880s.Footnote 8 These innovations in access to financial data and analysis substantially reduced the information costs related to the price of money (present and future), creating new opportunities and incentives for private economic agents with regard to decisions on credits, loans, and investments.

The establishment of large banks with numerous branches ran parallel to a series of entrepreneurial, technological, and institutional reforms in the fields of communications and transport, advancing rapidly in the larger Latin American nations during the last quarter of the 19th century. The development of branch banking systems in the last quarter of the century was usually accompanied by the introduction of telegraph networks and railroad lines. Bank offices or agencies were frequently set up in those towns or cities where there were railway stations (Gómez Galvarriato and Castañeda, Reference Gómez Galvarriato and Castañeda2024). Both the new financial and communications technologies fostered the gradual integration of regional markets and also directly influenced the integration of fiscal and military administrations.

While it is certainly possible to posit complementarity between administrative modernization, financial development, and national political integration, it should also be underlined that major economic challenges were not absent in this era. Among the most formidable challenges was the need to deal with the contradictory impact of the inflows of foreign capital that arrived on an unprecedented scale, particularly in the form of increasing government debt sold abroad in the shape of gold bonds, as well as foreign direct investments. The so-called national banks collaborated with financial ministers in negotiating large loans with European bankers, who eagerly promoted the sale of external gold bonds of Argentina, Brazil, Chile, Mexico, and many other Latin American states on the capital markets of London, Paris, Berlin, Brussels, and Amsterdam (Marichal, Reference Marichal2014, chapter 5). Nonetheless, the inflows of capital generated acute challenges for banks and governments. Foreign capital contributed to stock market booms in the late 1880s that became increasingly volatile, particularly in Argentina and Brazil, where major financial crises took place in the early 1890s, dragging many of the larger banks into bankruptcy, particularly those closely linked to state finance.

In order to unravel aspects of the complex relationships between states, economies, and national banks during this age, it is necessary to provide some concrete historical examples that can stimulate new questions and further research, particularly from a comparative perspective (Calomiris and Haber, Reference Calomiris and Haber2014; Feiertag and Margairaz, Reference Feiertag and Margairaz2016). Such an approach requires examination of some of the principal similarities as well as differences between the size and structure of the main banks in different countries. This is the purpose of the remainder of this article. We focus on the specific cases of Brazil, Chile, and Argentina, using rich comparative data found in official reports published during the 1880s, as well as a range of complementary primary and secondary sources.Footnote 9

4. The banking system of Brazil in the last quarter of the 19th century

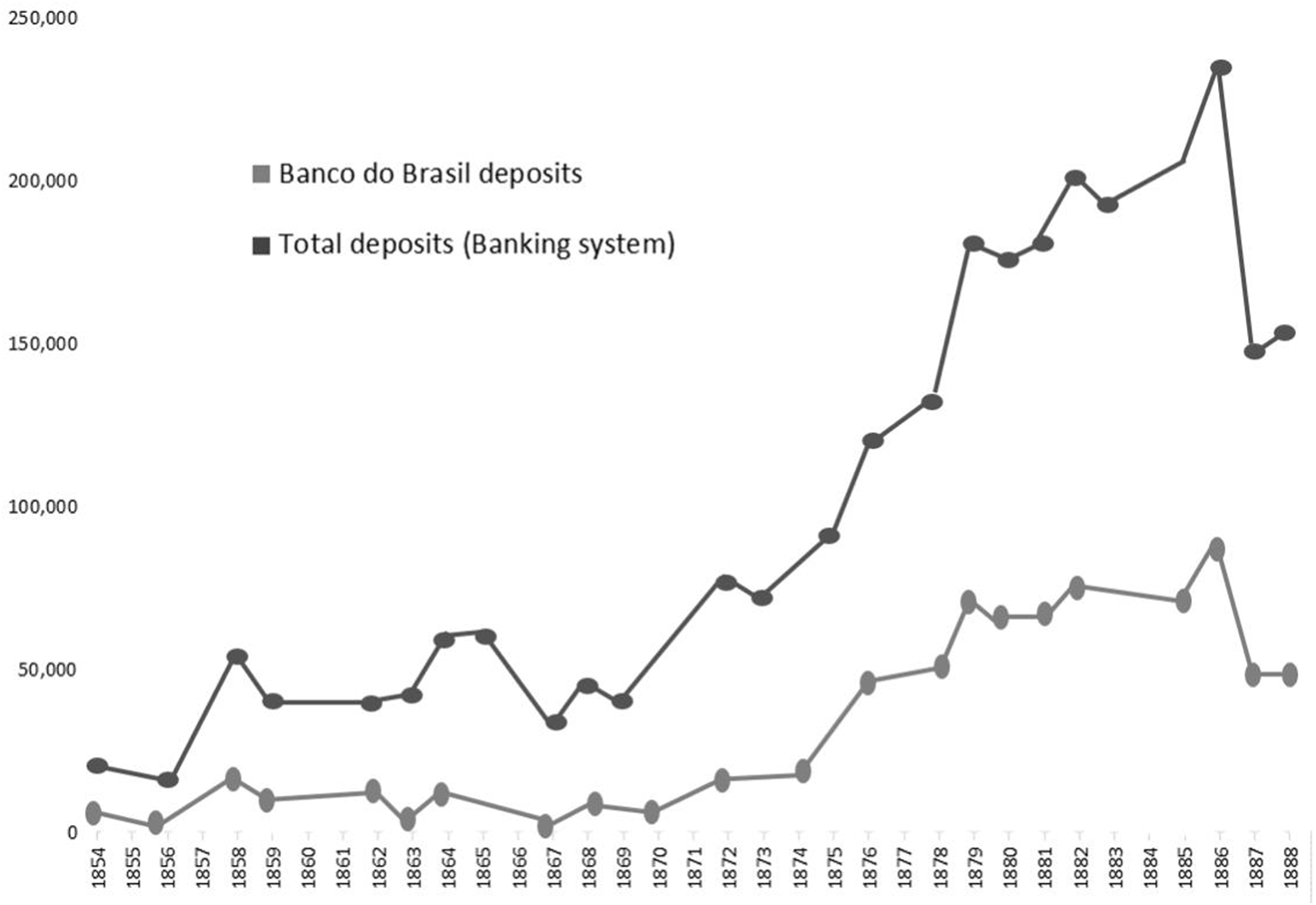

In some Latin American countries, the idea of a national bank had already led to the establishment of important institutions before the last quarter of the 19th century. In Brazil, the birth of banking had proved somewhat more precocious than in other nations of the region, with the launching of the Banco do Brasil in 1853, which became a kind of national bank from an early date (Gambi, Reference Gambi2015). In Figure 1, based on research published by the pioneering financial historian, María Barbara Levy, we can observe the trajectory of the Banco do Brasil within the banking market of the capital, Rio de Janeiro, between 1854 and 1888, in regard to deposit banking. Initially, other private banks attracted more clients, but gradually, the preeminence of Banco do Brasil became ever more notable, despite the fact that other banking enterprises emerged in both the capital and in São Paulo.

Share of Banco do Brasil in total Rio de Janeiro banking deposits, 1854–1888 (contos de réis).

1 Long description

The graph plots banking deposit amounts in contos de réis on the vertical axis, ranging from 0 to 250,000 and years on the horizontal axis, spanning from 1854 to 1888. Two lines are present, each distinguished by different markers. One line represents Banco do Brasil deposits and the other represents total deposits in the banking system. The legend labels the two series as Banco do Brasil deposits and total deposits (banking system). Throughout the entire period, the total deposits line remains well above the Banco do Brasil deposits line, indicating that Banco do Brasil accounts for a portion of the broader banking system total. Both lines begin at low values near 0 in 1854. The Banco do Brasil deposits line rises gradually and steadily, with approximate values as follows: (1854, near 0), (1860, near 5,000), (1865, near 10,000), (1870, near 20,000), (1875, near 30,000), (1880, near 50,000), (1885, near 100,000), reaching a peak near (1887, approximately 100,000), followed by a sharp decline toward (1888, approximately 30,000). The total deposits line also rises gradually but at a higher level, with approximate values: (1854, near 5,000), (1860, near 30,000), (1865, near 50,000), (1870, near 60,000), (1875, near 80,000), (1880, near 100,000), (1885, near 150,000), peaking near (1886, approximately 240,000), followed by a sharp drop toward (1888, approximately 155,000). The gap between the two lines widens noticeably from the 1870s onward, reaching its greatest extent near the peak years of the mid to late 1880s. Both lines show a sharp decline in the final recorded years.

The Banco do Brasil was not a public bank but rather owned by the principal merchants and financiers of Rio, as well as by important sectors of the coffee fazenda (plantation) owners. Its ties to the government were severely weakened during the Paraguayan War (1865–1870), when the Ministry of Finance rescinded the bank’s right to issue banknotes, which then became a monopoly of the State Treasury, which took over the issue of convertible paper money. Nonetheless, from 1879, relations between the government and the Banco do Brasil improved. The latter collaborated increasingly with the Ministry of Finance, opening an account for the Treasury with credits for large sums. Reciprocally, the government now began to deposit all surplus balances of the General Treasury in an account at the bank, as also did the principal customs offices. At the same time, the bank began to operate as an agent for the state in negotiating loans on European markets, several of which were used to improve the exchange operations of the imperial government of Brazil. These were key functions carried out by the bank, which still had a small staff of barely 47 functionaries at the head office as of 1880. Despite the small size of this financial enterprise, it played a crucial role in the economy (Banco do Brasil, 2010).

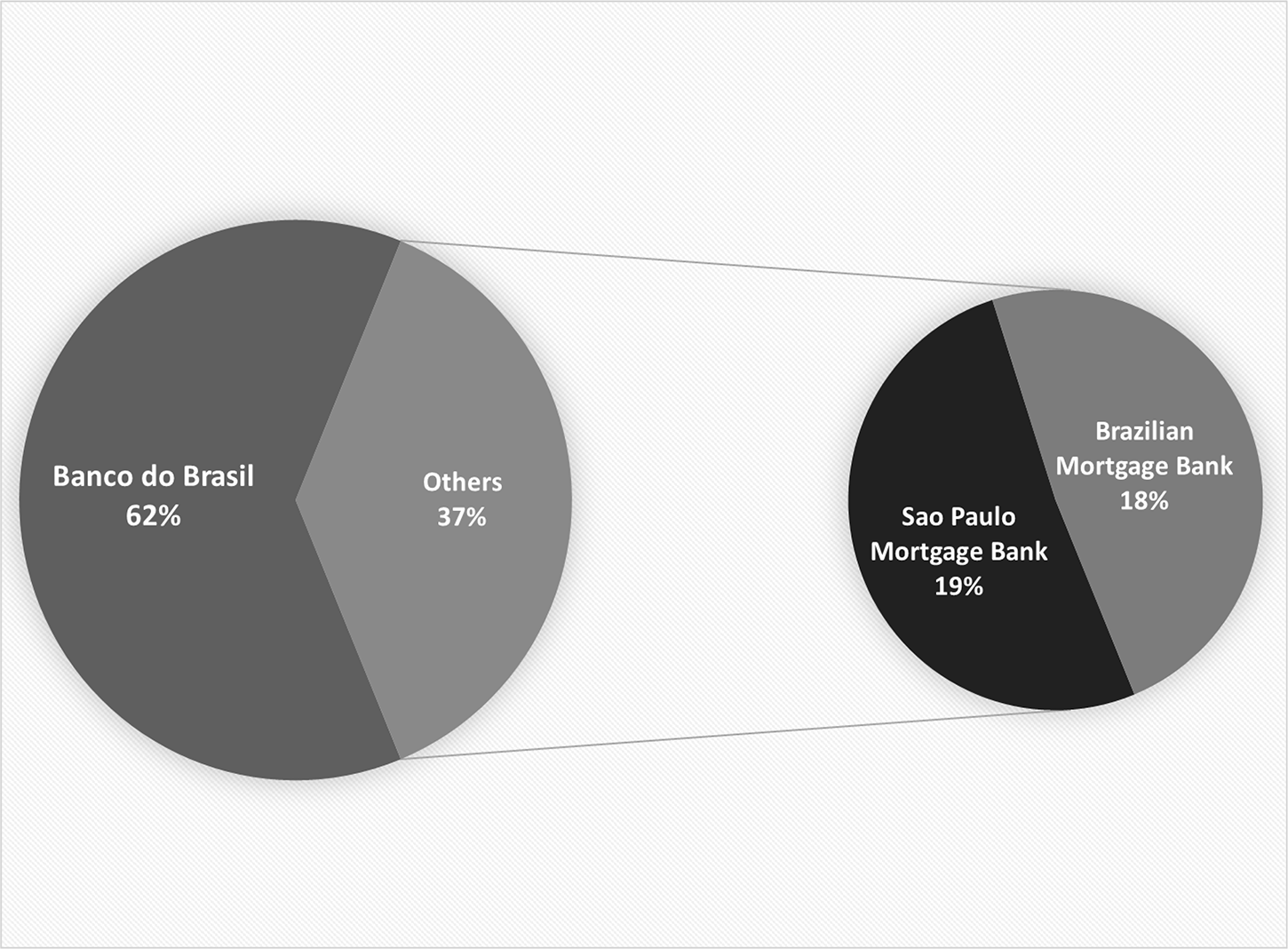

The Brazilian government gradually adopted more flexible policies to allow for a small increase in monetary circulation, but until 1887, only three banks, the Banco do Brasil and two mortgage banks, circulated banknotes widely in financial markets, a fact that clearly gave these entities special advantages (see Figure 2). Nonetheless, it should be mentioned that there were another 15 commercial banks in Río de Janeiro and several more in cities such as Bahía and Sao Paulo. These entities carried on much business based essentially on the discount of commercial paper on a short-term basis, using the rising volume of such bills to sustain credit operations, while they invested some of their capital in a variety of investments. However, such banks faced limits to their expansion because of the lack of capacity to issue banknotes (Summerhill, Reference Summerhill2015, chapter 7).

Share of total banknote issues in Brazil, 1887.

Figure 2 Long description

Two pie charts connected by a tapered shape. Left pie chart labels: Banco do Brasil 62 percent. Others 37 percent. Right pie chart labels: Sao Paulo Mortgage Bank 19 percent. Brazilian Mortgage Bank 18 percent.

It may be concluded that the banking system in Brazil had a basically conservative and oligopolistic character that was bound to be modified as a result of the major socio/economic developments that were taking place in the 1880s.Footnote 10 These changes were driven most forcefully by the rapid expansion of coffee production and exports in the provinces of Sao Paulo and Minas that became the new locomotives of the Brazilian economy, replacing the declining coffee plantations of the great Paraíba valley, proximate to Río de Janeiro. As a result, the emerging mercantile and coffee oligarchies of Sao Paulo and Minas began to challenge the elites of Río and pressed for financial reforms. However, there was another equally important process that was taking place, namely, the burgeoning of a series of movements in favor of the abolition of slavery. In fact, manumission proved inevitable as a result of the ageing of the clave population and the virtual end of the internal slave trade that had transferred tens of thousands of slaves from the old sugar plantations of the Northeast to the coffee plantations of central south Brazil during several decades.

Despite the growing force of abolition, the Banco do Brasil, itself, remained heavily engaged in mortgages of old plantations, using slaves as collateral until the year 1884. According to William Summerhill, in 1880, this large bank held mortgages on 346 plantations (fazendas) in the classic coffee districts of the province of Río de Janeiro, the collateral of which included nearly 19,000 slaves (Summerhill, Reference Summerhill2015, p. 206). The Banco do Brasil was, therefore, overloaded with mortgages on large but declining rural properties, although it also held dozens of mortgages in the more dynamic provinces of São Paulo and Minas. Nonetheless, plantations confronted acute problems as slaves began to be freed in the 1880s. Nonetheless, it should also be noted that the bank continued to benefit from a large volume of deposits provided by the mercantile and professional classes of the capital at Río and continued to be a close ally of the imperial government. The abundance of deposits allowed the bank to carry on an important discount business for commercial and early industrial firms, for some railways, as well as for agricultural companies.Footnote 11 Nonetheless, Banco do Brasil was a staid organization that some foreign observers considered inefficient, especially considering its dominant role in the issue of banknotes.

Rivals to the Banco do Brasil began to appear in the late 1880s and built up special relations with the government One of the first was the Banco Internacional do Brazil, founded in 1886 in Rio de Janeiro by the influential entrepreneur, Vicount Francisco Figuereido, who soon came to be a key partner of European banks in the negotiation of foreign investments as well as public debts of Brazil (Summerhill, Reference Summerhill2015, pp. 210–211). Figueiredo was a leading coffee export merchant, president of a major water works company in Río, and director of important railroad enterprises, such as the Estrada de Ferro Dom Pedro II. He is remembered as a promoter of the abolition of slavery but also as a monarchist. In the last years of the Empire, Figuereido helped to ratify an important financial reform that allowed for the concession of short-term loans to the government and the reduction of the external debt service, in good measure as a result of his close relations with leading Paris investment banks as well as with London merchant banks, including the firms of N.M. Rothschild and Morton Rose, who were involved in the placement and service of Brazilian external debts.

Figuereido pressed for the creation of a kind of private central bank, based on European models, to act as lender of last resort and to serve as an agency for the Treasury and regulator of the money market. In June 1889, the Minister of Finance, Viscount Ouro Preto, promoted the reform of the banking law of 1888 with regulations that allowed for the creation of a new issuing bank to be called the Banco Nacional do Brasil, whose banknotes were to be backed by government currency and bonds. At the same time, Treasury promised to provide loans to major landowners at a relatively modest rate of 6% per year.Footnote 12 The new bank was to absorb the Banco Internacional, headed by Figuereido, and soon opened offices in both Río de Janeiro and Paris. The powerful Banque de Paris et Bays Bas (Paribas) was charged with issuing half of the huge original capital of 10 million pounds sterling on European capital markets.Footnote 13 The new “Banco Nacional do Brasil” was to hold the gold and hard currency reserves of the Brazilian government and was charged with retiring the bulk of Treasury notes in circulation. In order to do so, it received a huge block of domestic bonds of the Brazilian government that paid 4% interest and was instructed to organize a financial syndicate to place these bonds on the local financial market and whatever could be sold abroad.

The objective of Prime Minister Ouro Preto in granting such important financial concessions to Figuereido was part of his strategy to assure the continued inflow of European capital, following the successful restructuring in 1888 of the Brazilian external debt of 20 million pounds sterling, carried out in an operation headed by the London firm of N.M. Rothschilds. At the same time, Ouro Preto also decided to carry out a series of domestic financial reforms as a result of the abolition of slavery, which had been ratified in 1888. According to Summerhill, the prime minister put in motion a “large subsidy program to encourage banks to engage in mortgage lending to rural producers, concentrated heavily in coffee-growing regions where the wealth of planters had been most adversely impacted by the abolition of slavery” (Summerhill, Reference Summerhill2015, p. 190). The plan was negotiated with the millionaire entrepreneur and banker Francisco de Paula Mayrink, who helped negotiate contracts with 17 banks from various regions of Brazil that were signed between June and October 1889. In toto, Ouro Preto authorized the treasury to transfer bonds from the Treasury worth 172 million contos to the banks on condition that they would also contribute part of their capital for the provision of credits to landowners who were willing to mortgage their properties to get the funds necessary to expand operations (Schulz, Reference Schulz1996, p. 159). Among the favored entities was the Banco do Crédito Real, owned by Mayrinck, which made huge profits in this public/private business that involved no risks for this powerful banker, who invested in a great number of new entrepreneurial ventures.

The financial reforms are considered to have been responsible for stimulating a sudden and spectacular boom on the Rio de Janeiro stock exchange that began in late 1889 and was to continue for 2 years, which soon became known as the Encilhamento. The political and financial complexity of the last months of the long-lasting Imperial regime in Brazil was notable. It had begun with the abolition of slavery in May of 1888, followed a year later by the financial furor, but it was also the result of rising political instability. The Empire ended as a result of a military coup, headed by Marsall Deodoro da Fonseca that instituted the Republic on November 15, 1889. Two months later, on January 17, 1890, the new Brazilian government decreed the abandonment of the gold standard, a measure that caused a marked decline in the stock market boom. As a result, the new Finance Minister of the young Republic, Rui Barbosa, a famous abolitionist, decided to counter the temporary crisis by adopting a loose and inconvertible monetary regime that would provoke rampant speculation as well as a new surge in the stock exchange. The minister ratified a banking law in January 1890 that created three new banks of issue in the North, Center, and Northeast of Brazil, which were authorized to issue up to 450,000 contos de réis, doubling the paper currency in circulation at that time, presumably to meet the demands of landowners in a number of Brazilian provinces.Footnote 14 Furthermore, Rui Barbosa ratified a series of decrees facilitating the formation of new companies and allowed them to register on the Rio de Janeiro Stock Exchange and to issue shares with the paid-in subscription of only 10% of nominal capital. The stock market boom again regained strength.

In these circumstances, Rui Barbosa adopted additional measures that contributed to the intensification of the banking frenzy. He reinforced his personal alliance with his friend, Francisco de Paula Mayrink, the most powerful entrepreneur of the Republican regime, and requested him to organize a new banking colossus, the Banco dos Estados Unidos do Brasil, in January of 1890. The finance minister awarded this new bank the right to issue a huge sum of 200,000 contos of banknotes, guaranteed by Brazilian domestic debt. Nonetheless, criticisms of these exclusive privileges mounted, and by early March 1890, Rui Barbosa was forced by other bankers to reduce the monopoly privileges extended to Mayrink and to share the rights to issue banknotes with rival entities, to be backed up with public debt instruments which could be acquired at rock bottom prices.Footnote 15 With these additional funds, the Banco do Brasil, as well as the Banco Nacional, also entered the financial fray on the stock market. According to a detailed financial report, the Banco do Brasil came to hold on account of its clients a huge volume of stocks and debentures of more than 250 companies registered on the stock exchange by 1893, including dozens of banks, 15 railway companies, over a hundred commercial and manufacturing firms, numerous real estate enterprises, and many public works and construction firms.Footnote 16 How many of these entities were solid and how many fraudulent is open to question. Contemporary critics argued that many were only speculative ventures, but the financial furor was impressive.

By September 1890, three banks, the Banco dos Estados Unidos do Brasil, the Banco Nacional, and the Banco do Brasil, controlled 95% of all banknotes in circulation by means of their privileges and those of other banks which they controlled (Topik, Reference Topik1987). In this way, a surprisingly rapid change took place in the Brazilian banking system that had long been very conservative and dominated by the Banco do Brasil, transmuting into a system with three very large competing banks. The expansion of the money powers of these banks tended to introduce a series of potentially dangerous elements for the financial system as a whole, since they engaged increasingly in the stock market binge. To reduce potential problems, the finance minister, Rui Barbosa, pushed for the creation of a new, giant entity that was named the Banco da República dos Estados Unidos do Brasil (BREUB), as a result of the merger between the Banco dos Estados Unidos do Brasil and the Banco Nacional in December 1890. The government gave the BREUB a monopoly on the issue of banknotes, as well as numerous privileges related to the management of public finance, including the negotiation of foreign loans. However, severe problems began to emerge since this bank pursued a course of increasing circulation of banknotes with insufficient metallic reserves.

Confidence in the new bank also began to falter as news came of the Argentine financial crash, the Baring crisis that took place in November 1890, being largely the consequence of the excessive commitments of the prestigious London merchant bank in Argentina and Uruguay with government debt, and particularly with local companies that were on the verge of bankruptcy. Nonetheless, and simultaneously, the furor on the Río stock exchange continued for several more months, until the finance minister lost favor and resigned in January 1891.

After February 1891, the government headed by President Manuel Deodoro da Fonseca, the general who had headed the new Brazilian Republic from its inception, attempted to moderate the financial boom, but was largely unsuccessful. Fonseca resigned from office after a coup orchestrated by his own vice president, General Floriano Peixoto, on November 28, 1891. The financial situation became increasingly unstable as international investors began to abandon Brazilian government debt, traditionally highly regarded on the London Stock Exchange. According to one incisive quantitative study, it is clear that the decline of the prices of Brazilian gold bonds on foreign capital markets was not only caused by the domestic financial and political unrest in Brazil but also by contagion as a result of the formidable collapse of Argentine banks and state finance in 1891 (Triner and Wandschneider, Reference Triner and Wandschneider2005). In December 1892, the finance ministry pressed the directors and shareholders of the Banco do Brasil (which remained the strongest bank) to merge with the Banco da República in January 1893, despite considerable internal opposition by leading shareholders.Footnote 17

The creation of the new and massive banking entity marked a move toward extreme concentration in the banking system. As historian Gale Triner has stated:

By 1893 the Banco da República concentrated note-issuing rights within one organization and expanded its capital to accommodate public-sector financial needs, while still maintaining its reach into the private sector … The Banco da República also provided a net to other banks and often acquired assets of failing smaller organizations. (Triner, Reference Triner2000, pp. 45–46)

Nonetheless, for several years, the Brazilian banking system was obliged to restructure and attempt to cover the huge losses stemming from the crash, following the end of the stock market boom known as the Encilhamento. In any case, there is debate among historians as to the circumstances that later led to the virtual collapse of both the Banco da República and most commercial banks in 1900, at which date the government intervened forcefully to reorganize the banking system. This also implied paying off foreign investors.Footnote 18 In fact, it would not be until 1906 that the state authorities were finally able to clean up the financial mess and launch a new Banco do Brasil as a public bank, essentially under government control, but also dealing with a great range of private clients. This large financial entity continued to operate as the leading commercial bank in Brazil, as well as the dominant government bank for much of the rest of the 20th century.

5. Banks in Argentina: rivalries between two major state banks

In the case of Argentina, after the election of Julio Roca as president of Argentina in 1880, the new head of state began to press for the expansion of the Banco Nacional (1872) in order to compete with the older and larger Banco de la Provincia de Buenos Aires (1854) in both operations of public and private finance and in the issue of banknotes, with the aime of making the Banco Nacional the preeminent monetary authority in the country. Nonetheless, rivalry with the rich provincial bank continued with regard to banknote issue down to 1890. During the decade of the 1880s, the Banco Nacional established branches in the capitals of all the Argentine provinces, as well as a growing number of agencies in secondary cities. The capital of the bank was held by several hundred shareholders, mainly wealthy individuals from the city and province of Buenos Aires, although the state also held a varying percentage of the stock.Footnote 19 In 1883, the national government approved a new charter for the bank, increased its capital from 8 to 20 million pesos, and took half of the new shares. The charter also established that the bank would open an account for the government and would fulfill important functions for the national Treasury, including the reception of taxes and payments of salaries of public employees.Footnote 20 The intention was explicitly to promote a unified, national monetary and credit system. The statutes indicated that it had the legal capacity:

to issue notes payable to the bearer and at sight, and to carry out all kinds of banking operations, including the faculty of making loans to the national and provincial governments and to extend open credits to municipalities and individuals with the guarantee of public funds and shares of companies traded on the Stock Exchange. (Argentina, 1890, pp. 26–27)

Existing records in the historical archive of the present-day Banco de la Nación provide information on the loans advanced by the Banco Nacional to a great number of clients but have not been studied in detail by historians.Footnote 21 By 1884, this bank had 27 provincial branches, which were quite profitable.Footnote 22 The minutes of the weekly meetings of the directors make it clear that the majority of loans went to large landowners and leading merchant houses, but in addition, they indicate that there was frequent insider trading since credits were extended regularly to select directors, who were themselves owners of major trading firms.Footnote 23 The concession of loans increased year by year, in most cases with simple promissory notes as guarantees, although a large number were also backed up by deposit accounts. The loans were often renewed, including a good number of the largest credits that had been awarded to important landowners or to politically influential entrepreneurs.

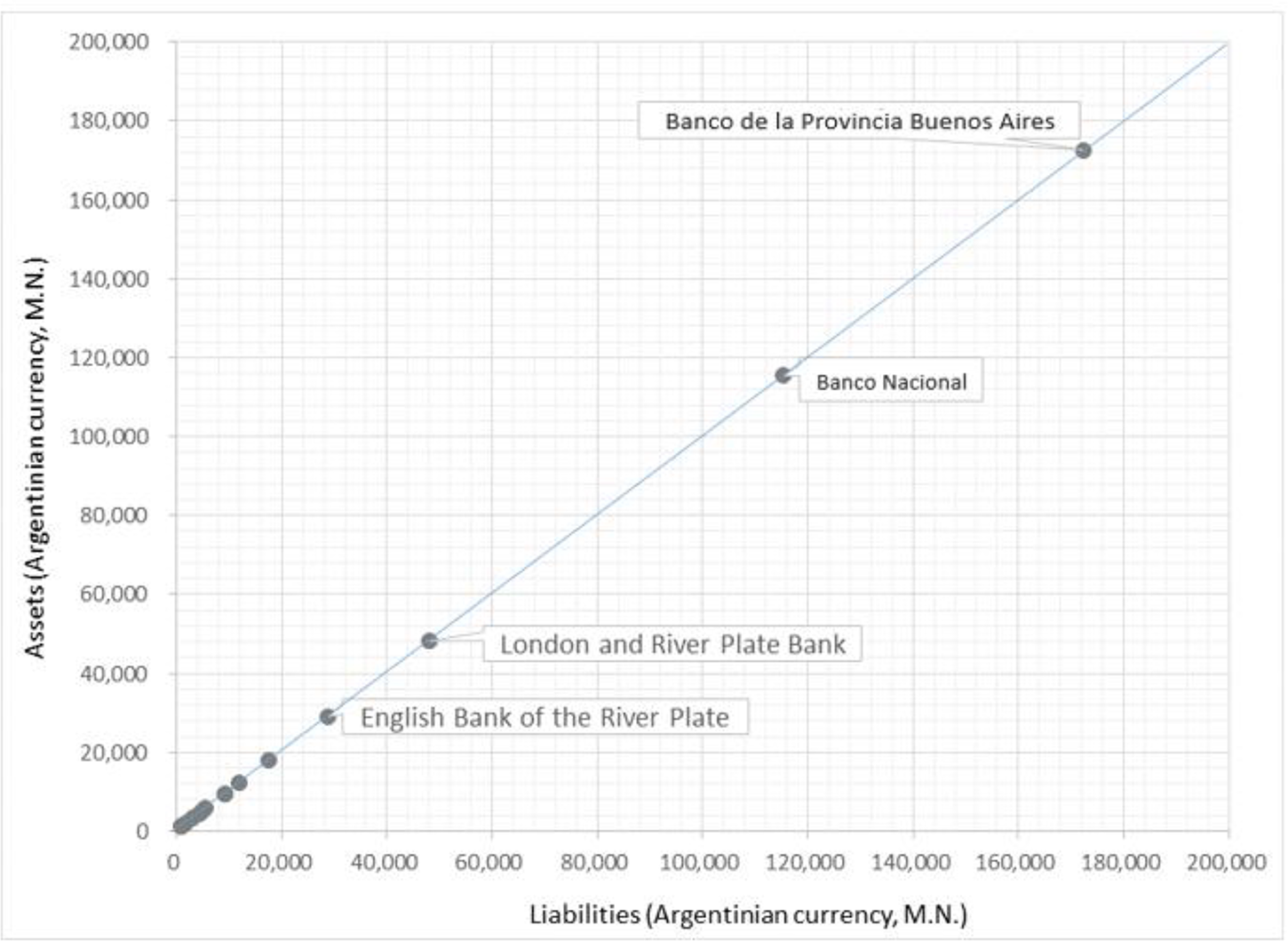

Special challenges for all of the players in the Argentine money markets were caused by shifts in monetary regimes. During the years 1881–1884, all banks were obliged to maintain gold reserves for the privilege of issuing banknotes, but this was followed by a subsequent regime of inconvertibility between 1885 and 1890. In a detailed study of Argentine finance at the time, the economic historian Roberto Cortes Conde demonstrated that the Banco Nacional began to expand its credit operations on considerable scale during the years 1885 and 1886, but that even so, the public continued to trust its management insofar as the bank received large injections of public debt securities to bolster its reserves (Cortés Conde, Reference Cortés Conde1989, p. 166). The confidence in the performance of the bank and of state finance was a reflection of the optimism that had been generated among domestic entrepreneurs and investors by the rapid growth of the economy, reinforced by the enormous increase in foreign direct investments, as well as a result of the successful negotiation of a string of foreign loans issued on European capital markets. Nonetheless, the head of the Argentine Office of Public Credit, Pedro Agote, a specialist in banking statistics, argued that after 1887 the Banco Nacional had exceeded prudent levels in its concession of loans to private clients as calculated in relation to reserves (Agote, Reference Agote1881–1888, IV, pp. 132–133). See Figure 3.

Bank assets and liabilities in Argentina, 1887 (thousands of pesos, moneda nacional).

Figure 3 Long description

The horizontal axis label is Liabilities (Argentinian currency, M.N.). The tick labels run from 0 to 200,000. The vertical axis label is Assets (Argentinian currency, M.N.). The tick labels run from 0 to 200,000. Text labels next to plotted points include: English Bank of the River Plate; London and River Plate Bank; Banco Nacional; Banco de la Provincia Buenos Aires. A diagonal reference line runs from near (0, 0) toward (200,000, 200,000). The plotted points form an upward pattern from lower left toward upper right. Several points are clustered near the lower left at low liabilities and low assets. One labeled point, Banco de la Provincia Buenos Aires, appears near the upper right around 180,000 liabilities and 180,000 assets. Another labeled point, Banco Nacional, appears around 120,000 liabilities and 110,000 assets. London and River Plate Bank appears around 50,000 liabilities and 50,000 assets. English Bank of the River Plate appears around 30,000 liabilities and 25,000 assets.

Official reports on the banks and on public debt of Argentina demonstrated that as of 1887, the two large government banks, the Bank of the Province of Buenos Aires and the National Bank, were clearly dominant in the local banking system, controlling together 67% of the capital of all commercial banks, 41% of cash, 59% of deposits, 64% of loans, and 89% of banknotes.Footnote 24

The Banco Nacional’s expansion was not only based on domestic growth, since it also relied increasingly on foreign business.Footnote 25 It became the main international financial agent for the government, taking charge of the external debt service and the negotiation of new loans of Europe. In 1886, for example, the directors took a bold step by issuing 10 million gold peso bonds of the bank in Europe, in collaboration with a syndicate of German bankers, and subsequently expanded its operations in the international loan business.

In 1887, the law of national guaranteed banks was ratified, authorizing provincial banks to issue banknotes, provided they purchase government gold bonds to the full amount of the notes to be issued. As a result of this law, seven provinces that had no banks (Santiago del Estero, La Rioja, Mendoza, San Juan, Catamarca, San Luis, and Corrientes) set up new banking enterprises with public support. In addition, 13 previously existing financial institutions also took advantage of the law to increase their issue; among these were the official banks of Cordoba, Santa Fe, Entre Rios, and Buenos Aires, as well as several private banks (Marichal, Reference Marichal1984). The new legislation was, with some modifications, an attempt to emulate the National Bank system (1864) of the United States. Argentine businessmen and politicians were aware of the enormous expansion and multiplication of banks in North America and of the decisive contribution they had made to economic development there. Nonetheless, it should be observed that several important differences existed between the basic guidelines used in the Argentine and the United States banking systems. One common point consisted in assuring that, like the American national banks, each of the official provincial banks of Argentina would guarantee its note issue with the acquisition of negotiable government bonds to be held as a reserve fund. However, the provincial governments that owned the banks were then obliged to look for the financial resources to be able to buy the bonds, and all of them sought foreign gold loans for this purpose. The gold was deposited in the coffers of the Banco Nacional as safekeeping to back up the issue of the provincial banknotes. But in contrast to the United States, where the banknotes could be exchanged for gold, in Argentina, convertibility had been suspended.Footnote 26 Moreover, another major difference in Argentina was that in this period of plurality of issues, the Banco Nacional stood behind all the provincial banks, whereas in the United States, the Treasury was the ultimate guarantor of the public debt held on account of the national banks.

In Argentina, the greatest financial challenge in the late 1880s was the growing dependence on foreign loans. The regional banks actually raised most of their capital through the sale of foreign bonds—payable in gold—that were nominally guaranteed by state revenues. The banks could issue banknotes (see Figure 4) by buying national government bonds payable in gold that would become their reserve funds, but simultaneously, they had to deposit the gold obtained through foreign loans in accounts of the Banco Nacional in order to pay for the domestic bonds. In theory, the bulk of these funds was to be used to strengthen the capital base of more than a dozen provincial banks, but this depended on a prudent management of the gold reserves held by Banco Nacional in order to assure solvency. The risks involved in this complicated financial mechanism were great and soon began to create significant financial problems.

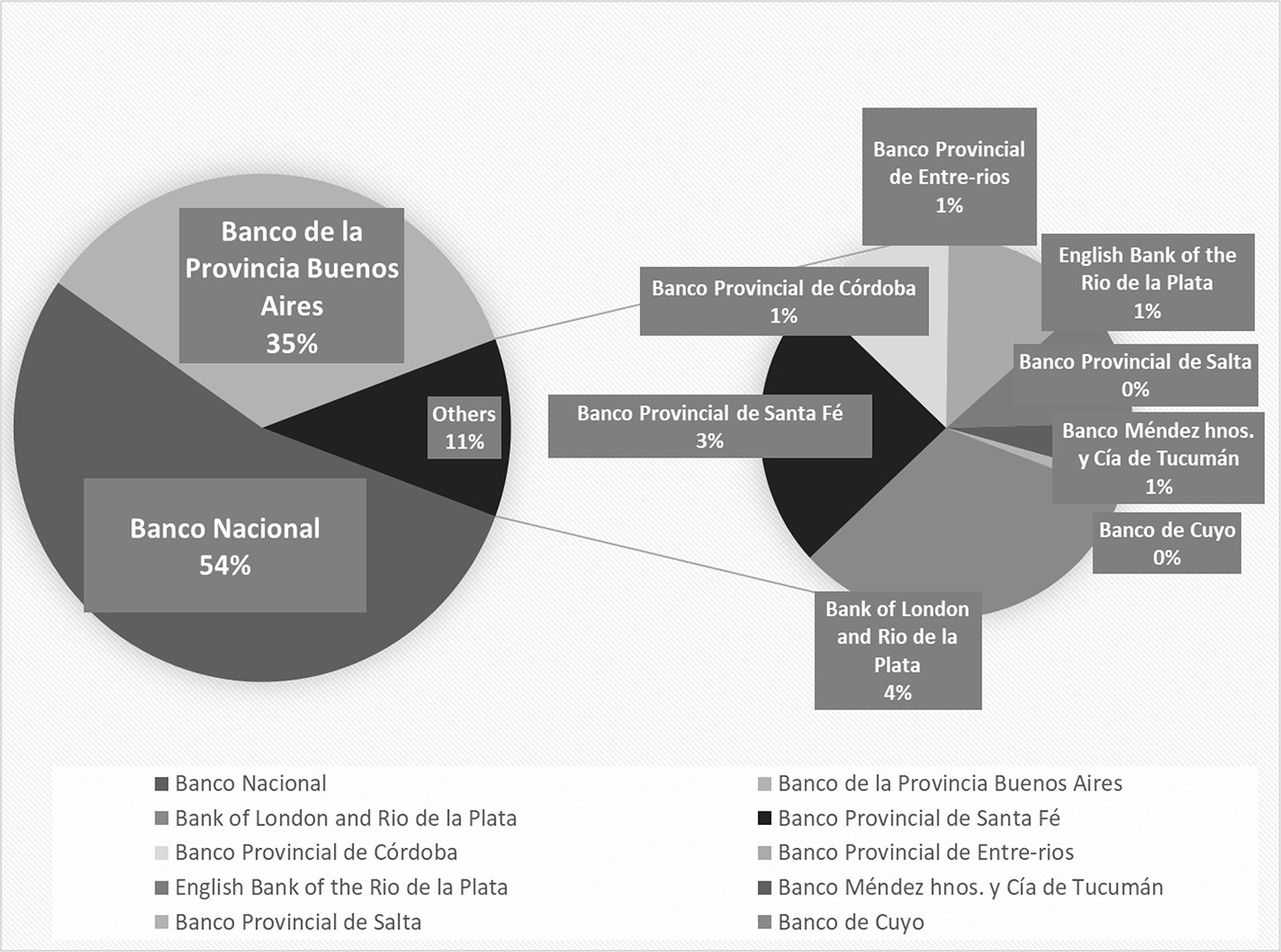

Share of banknote issues in the total, Argentina, 1887.

Figure 4 Long description

Share of banknote issues in the total, Argentina 1887. A pie chart with labeled slices and a legend listing: Banco Nacional; Bank of London and Rio de la Plata; Banco Provincial de Córdoba; English Bank of the Rio de la Plata; Banco Provincial de Santa Fe; Banco de la Provincia Buenos Aires; Banco Provincial de Entre-rios; Banco Provincial de Salta; Banco Mender hnos. y Cia de Tucuman; Banco de Cuyo. Slice labels shown on the chart: Banco Nacional 54 percent. Banco de la Provincia Buenos Aires 35 percent. Others 11 percent. Banco Provincial de Córdoba 1 percent. Banco Provincial de Santa Fe 3 percent. Banco Provincial de Entre-rios 1 percent. English Bank of the Rio de la Plata 1 percent. Banco Provincial de Salta 1 percent. Banco Mender hnos. y Cia de Tucuman 1 percent. Banco de Cuyo 0 percent. Bank of London and Rio de la Plata 4 percent. Range of labeled percentages shown on slices: 0 percent to 54 percent.

By the end of the 1880s, the number of public entities competing for loans on European financial markets had surpassed all expectations. Apart from the federal government and provincial governments, all the banks sought money abroad, including the Banco de la Provincia de Buenos Aires and the Banco Nacional, as well as the provincial banks in Catamarca, Córdoba, Corrientes, Entre Ríos, Mendoza, San Luis, Santa Fe, and Tucuman. Between 1880 and 1890, the diverse Argentine public entities had issued foreign bonds that had a total nominal worth close to 400 million gold pesos, approximately 80 million pounds sterling. The issue of international bonds was quite evenly split between the national and provincial governments, with a marked peak in the years 1887–1889. But the Argentine financial frenzy went far beyond, since large quantities of bonds were also sold in Europe by 10 municipal governments, to which must be added the role of the state mortgage banks that succeeded in selling huge quantities of mortgage bonds (known as cédulas) in European secondary markets.Footnote 27 One detailed source calculated that the value of the Argentine mortgage banks placed in Europe between 1886 and 1890 reached the enormous sum of 170 million gold pesos (Williams, Reference Williams1920, p. 85).Footnote 28

In summary, the legislation to create provincial banks as well as mortgage banks did not strengthen the autonomy of the Argentine banking system but rather weakened it by accentuating dependency on foreign money markets. At the same time, the finances of the national government were compromised by the irresponsible policies of the bank directors. All told, the national government delivered 200 million gold pesos of bonds to the banks as a guarantee for a similar quantity of banknotes. But the latter actually paid less than 80 million gold pesos for these securities. The national treasury thus found itself in the position of having to guarantee a huge domestic debt with metallic reserves equivalent to less than 40% of that sum. Not surprisingly, depreciation of the paper money began almost at once, driving the gold premium upward from 35 in 1887 to 48 in 1888, 91 in 1889, 151 in early 1890, and, finally, 310 by April 1890. The Minister of Finance, Rufino Varela, authorized the Banco Nacional to begin selling its gold reserves to calm the markets, but as the inflation accelerated, gold speculators in Buenos Aires added fuel to the fire, causing havoc in currency markets, the stock exchange, and the real estate market.Footnote 29

As early as March 1890, it was suspected that the most important financial institutions, the Provincial Bank of Buenos Aires and the Banco Nacional, were on the verge of bankruptcy. In order to avoid the collapse of the provincial bank, the governor of the province of Buenos Aires ordered that the funds obtained from the sale to British investors of the Ferrocarril Oeste, a profitable railway company owned by the provincial government, be deposited in the coffers of the bank, which was able to avoid collapse for another year. In the case of the Banco Nacional, the situation was much graver as it had debts to the national government and to foreign creditors that eventually surpassed the huge figure of 50 million gold pesos. Furthermore, its commercial business was deep in the red as most of its clients were not fulfilling payments on their credits. To make matters worse, the issue of banknotes by the Banco Nacional surpassed all reasonable limits. This could be seen in the contrast between the ratio of total loans to reserves, equal to 90/100, as opposed to the ratio of reserves and banknote issues, which was barely 12/100. The extremely high risks taken by the bank could be attributed to the fact that it was supported by the state, but in fact, it had weakened severely, as several bank runs demonstrated.

In June, the directors of the Banco Nacional notified Baring Brothers & Co. of London, Argentina’s main creditor, that it would be forced to suspend payment of the quarterly debt service of government gold bonds. This announcement was followed by a second run on the deposits of the official banks. The government tried to continue with its policies of rediscounts and fiscal deficits despite the default on foreign loans, but Congress did not support it, triggering a political crisis (Paolera and Taylor, Reference Paolera and Taylor2003, pp. 84–85). A military rebellion with considerable popular support took place in Buenos Aires (Sommi, Reference Sommi1948; Rojkind, Reference Rojkind2012). Almost 4 years after his assumption as president of the Nation, Juárez Celman presented his resignation on August 5, 1890. Carlos Pellegrini, the vice president, took charge of the Executive Branch.

After the ouster of Juárez Celman, the new president, Pellegrini, and his finance minister, Vicente López, once again confronted the prospect of an imminent collapse by the National and Provincial banks. Pellegrini decided to issue 60 million pesos in treasury bills to bolster bank reserves. This stabilized public finance for several months, but in November, news of the collapse of the firm of Baring Brothers shook the London market to its foundations. The Governor of the Bank of England pressed the Argentine government to transfer 43 million pesos of treasury notes held by the Banco Nacional to pay short-term debts in Europe, a large portion consisting of acceptances due to Barings.Footnote 30 The result was that the leading Argentine bank was even more seriously debilitated. In early January of 1891, Pellegrini received news of an imminent run by depositors on the provincial bank of Buenos Aires. In response, he instructed the already weak Banco Nacional to transfer a part of its reserves to the former institution. To raise additional funds, he imposed a 2% tax on all deposits held by foreign-owned banks as well as a 7% tax on their profits.

On March 6, having been informed that the leading state institutions were once again on the verge of suspending payments, Pellegrini and López declared a banking holiday and asked the financial and merchant community of Buenos Aires to save the public banks by subscribing to a “patriotic loan” of 100 million pesos. Domestic investors took 40 million pesos of the bonds, but this was not enough. On April 4, the National Mortgage Bank suspended payments on its cédulas (mortgage bonds), and on April 7, both the National Bank and the Provincial Bank announced a 90-day moratorium on all transactions. The Buenos Aires newspaper, El Diario noted:

While the news [of the bank moratorium] has made a large impression on commercial circles, it has provoked great alarm among the working classes and the small depositors subject to the impact of street rumors… On Florida Street the agitation was intense among the circle of stockbrokers and merchants. (El Diario, April 8, 1891, p. 1)

At this point, it became clear that the entire public banking system would have to be dismantled. Pellegrini’s close friend, Vicente Casares, who had been conducting an investigation of the financial state of the Banco Nacional, issued a withering report on the extraordinary degree of corruption in this banking institution.Footnote 31 He did not mention, however, that at the start of the crisis, while he was a director of the bank, he had received a huge loan of half a million pesos to finance one of his various private companies.Footnote 32 Evidently, the collusion and corruption were so widespread among entrepreneurs and politicians that there was no way of establishing legal responsibilities.

In any case, Pellegrini and López had no alternative but to close both the Banco Nacional and the Banco de la Provincia de Buenos Aires. As a result, the government declared a moratorium of 5 years to allow the provincial bank to reorganize and attempt to collect outstanding debts. On the other hand, the Banco Nacional was summarily closed, and a financial investigation was initiated to determine what real assets it still retained. Simultaneously, the government authorized the creation of an exchange commission (Caja de conversion) that would take charge of the supervision of operations on the monetary market. More fundamentally, in October 1891, the National Congress ratified the creation of a new national bank, to be called the Banco de la Nación Argentina (BNA), which became the centerpiece of the financial system thereafter. It inherited all the branches of the old Banco Nacional, which were solvent, and was authorized to operate those offices in most of the provinces. Subsequently, the BNA maintained close relations with the government while simultaneously becoming the largest commercial bank in the country, continuing to be so down to the present day (Rougier and Regalsky, Reference Rougier and Regalsky2023).

6. The banking system in Chile and the role of the Banco Nacional

The initial development of banking in Chile was legally structured as a free banking system from 1860, when the first banking law was ratified. This law authorized the establishment of a plurality of banks of issue, marking the triumph of the school of “free banking” (Marichal, Reference Marichal2021, chapter 4). In this sense, this early banking regime developed in a somewhat different direction from that of Argentina and Brazil. While a considerable number of private banks were authorized to issue banknotes during the 1860s, quite soon this privilege was dominated by two privately owned firms, namely the Banco Nacional and the Banco de Valparaíso, although the Edwards private banking firm also participated in varying proportions. Despite the legal framework of free banking, one well-capitalized private commercial bank, the National Bank of Chile, came to assume a position as the largest financial institution from 1865 onward, with certain fiscal privileges as well as a preponderance in the issue of banknotes. It provided important loans to the government in 1865 during wartime, and 4 years later, it provided a credit of one million pesos to finance a state-owned railroad, as well as receiving the privilege of opening a regular checking account for the Ministry of Finance, after which it became the main government bank.Footnote 33

Throughout the 1860s and the 1870s, the National Bank of Chile exerted a clear leadership within the banking structure, providing finance to private clients, the government, and public railroads. The main funds used to construct the state railroads came from three foreign loans negotiated with the London merchant bankers, J.S. Morgan and Co, in the years 1866, 1867, and 1870, and it may be presumed that much of the money from the public debt operations passed through the coffers of the Banco Nacional, providing support for its issue of banknotes, although it also counted on funds from the formidable rise in deposits in its accounts and a large credit business.

In the 1870s, the Banco Nacional tended to be profligate in the expansion of loans to its many clients, but also due to insider lending by directors. The balance sheets of the three leading banks indicate that the Edwards financial firm and the Bank of Valparaíso maintained higher reserves, including bullion as well as solid securities, and were less liberal in the issue of their banknotes, but maintained a dynamic business in commercial loans (Ross, Reference Ross2003, Appendix). On the other hand, the Banco Nacional increased its loans enormously from 1871 onward, a fact that may be attributed to the increase in its deposits that advanced very rapidly, probably derived from close links to government finance. For example, in 1873, the state financial authorities requested the bank to organize an international syndicate of banks to issue Chilean gold bonds in London to the tune of 2,278,000 pounds sterling, and it did so in combination with two British banks, the Oriental Bank Corporation and the City Bank. This demonstrated that the Chilean bank had finally been recognized as a relevant actor on international markets. Two years later, in 1875, the government again requested the Banco Nacional to negotiate a foreign loan of one million pounds sterling on the London capital market to convert domestic debt into foreign gold bonds and to cover interest payments on the outstanding foreign loan of 1867 (Cavieres, Reference Cavieres and Liehr1995, p. 207).

All of this business placed the Banco Nacional in a class of its own in Valparaíso, where it had its main offices, and made it equivalent in importance to the leading national banks in other Latin American countries. By 1877, however, the directors of the bank went overboard with speculative operations. According to the leading Chilean financial historian of that era, “the directors of the bank supplied themselves abundantly” with loans which totaled more than 7 million pesos (Santelices, Reference Santelices1893, p. 4). The same author stated the Law of Inconvertibility was promulgated (1878) at a most critical moment since the directors had already loaned to themselves half the capital of the bank. This circumstance marked the apex of the crisis of 1878 and almost led to the bankruptcy of the Banco Nacional. In the middle of the financial collapse of the stock market and of various smaller banks, capital flight became so intense that metallic reserves were all but exhausted, and the government was forced to declare the banknotes of the leading financial entity inconvertible, as well as those of its rivals, despite many protests.Footnote 34

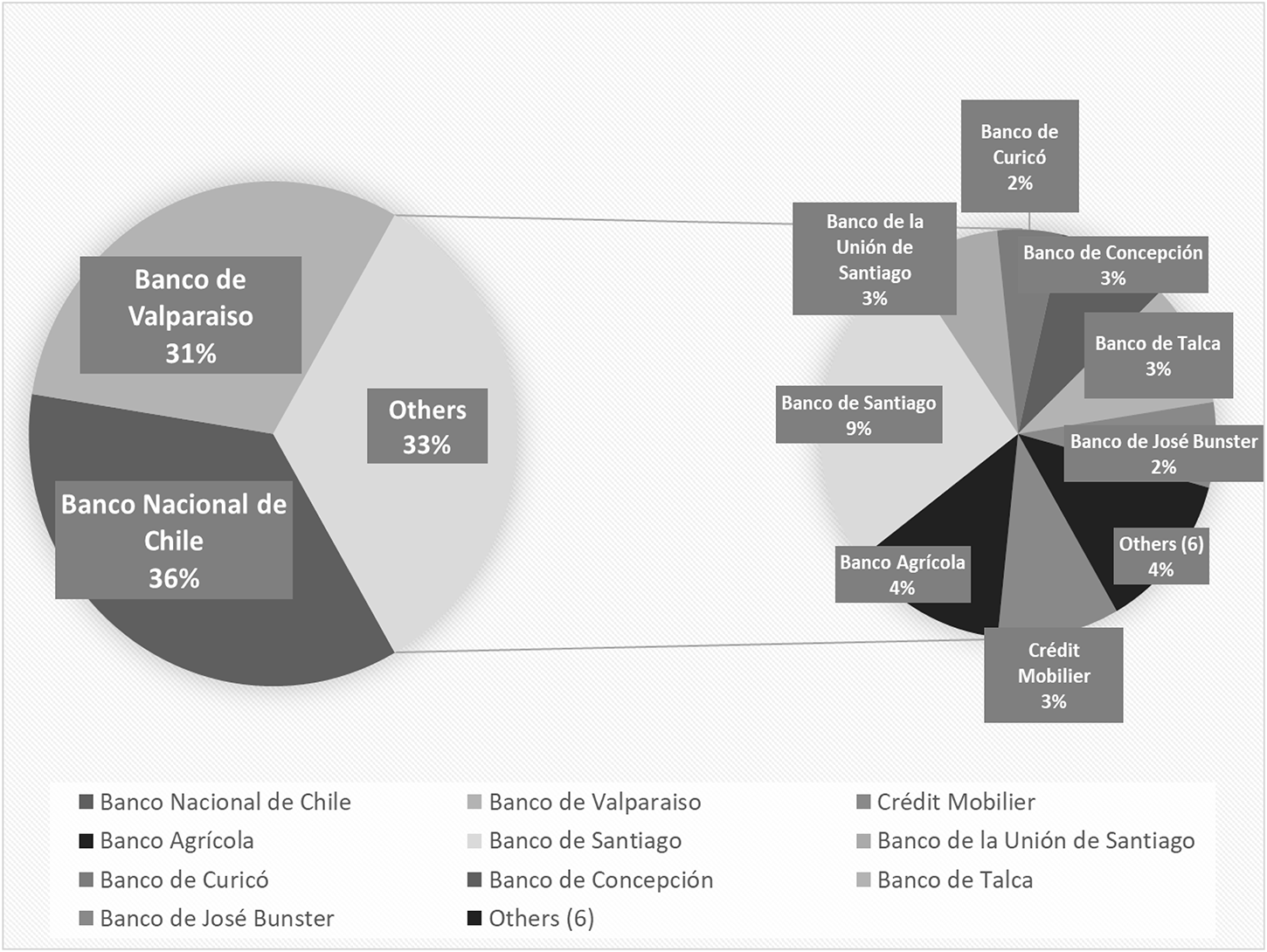

The Banco Nacional did not go under because it received substantial support from the state, which benefited from the war with Peru (1879–1883), permitting Chile to acquire an enormous number of valuable nitrate fields in the northern Atacama Desert. However, in the meantime, the government was obliged to seek new sources of finance in order to cover the war expenses, given the weakness of the banking system following the panic of 1878. Fiscal certificates were issued by the national Treasury and guaranteed by the nitrate taxes, and in this way, the state became responsible for the circulation of a large volume of paper money that competed with the notes issued by the private banks. The Treasury certificates were accepted because they were backed up by the notable increase in public revenues during the 1880s. The Banco Nacional gradually recovered and remained quite powerful since it remained the main entity in which the Treasury deposited its surplus funds. Furthermore, the bank continued to be the leading issuer of banknotes, as can be seen in the data from 1887 registered in Figure 5.

Share by banks of the total banknote issues by Chilean banks in the year 1887.

Figure 5 Long description

Share by banks of total of banknote issues by Chilean banks in the year 1887. A pie chart with labeled segments and a legend listing the banks. The segments and values shown are: Banco Nacional de Chile, 36 percent. Others, 33 percent. Banco de Valparaiso, 31 percent. A connected breakdown for Others 33 percent shows: Banco de Santiago, 9 percent. Banco de la Union de Santiago, 3 percent. Banco de Concepcion, 2 percent. Banco Agricola, 2 percent. Credit Mobilier, 3 percent. Banco de Curico, 2 percent. Banco de Talca, 2 percent. Banco de Iquique, 2 percent. Banco de los Bustos, 4 percent. Others (6), 4 percent. Legend text shown: Banco Nacional de Chile. Banco Agricola. Banco de Curico. Banco de los Bustos. Banco de Valparaiso. Banco de Santiago. Banco de Concepcion. Others (6). Credit Mobilier. Banco de la Union de Santiago. Banco de Talca.

From the mid-century, during an early boom phase of the Chilean economy, the Banco Nacional de Chile managed to maintain predominance in the financial sector, at least down to 1875. This private enterprise concentrated more than 40% of the total deposits in the banking system in the years 1870–1875, which was not surprising, taking into account its role as fiscal agent of the government and manager of a large part of the domestic and foreign debt (Ross, Reference Ross2003, p. 163). Indeed, most of the inflow of pounds sterling on account of borrowings was deposited in the accounts of the Banco Nacional. In turn, the firm dominated the total issue of banknotes, a fact that calls into question some of the arguments about competitiveness in this era of plurality of issue, although there is no doubt that the normative principles established by the very liberal banking law of 1860 remained in force, at least until 1878.

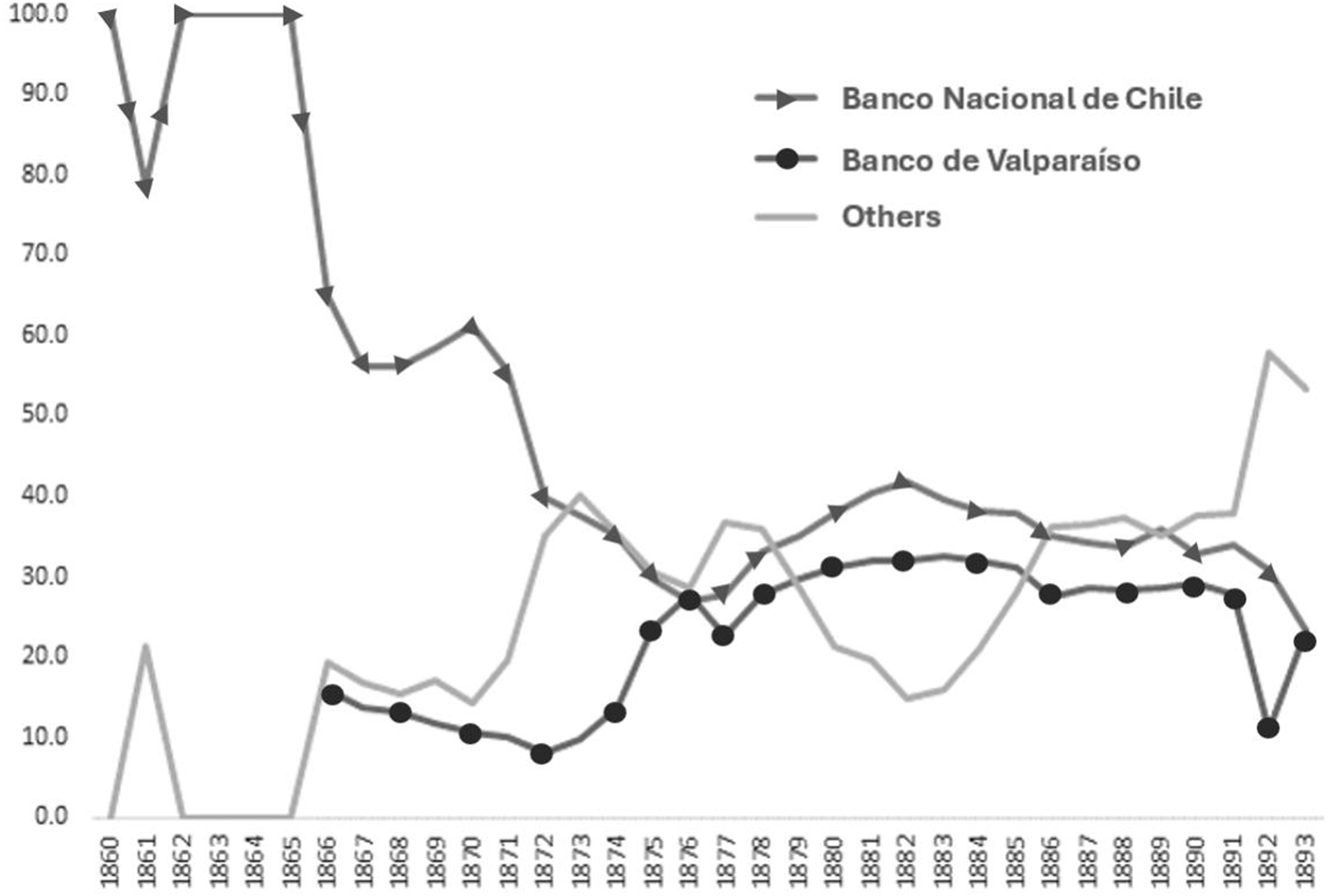

In overall commercial terms, however, the Banco Nacional was soon matched and even surpassed in some years by the Banco de Valparaíso in capital, reserves, deposits, and loans (See Figure 6). Although both were privately owned banks with many shareholders, most of whom were relatively large property owners and merchants, the two entities had different business strategies. The directors of the Valparaíso bank were more conservative in their loan business and prudent in accumulating large bullion reserves, both factors that allowed them to attract deposits on a large scale.Footnote 35 But much remains unknown about the internal strategies and decisions adopted by the directors of each of these banks. In a word, there is a need for more detailed research on the history of these two leading banking enterprises, the Banco Nacional and the Banco de Valparaíso, particularly during the 1880s. Nonetheless, there is considerable difficulty in reconstructing their precise trajectories because of the lack of surviving historical archives of these firms, as well as of practically all 19th-century Chilean banks.Footnote 36 Fortunately, there remains a considerable volume of legal documents regarding the banks on the website of a Chilean monetary agency, which provides complementary information.Footnote 37 In the event, a few economic historians have done major spadework bringing together documentary sources to begin to put together a coherent analysis of some key facets of their history (Ross, Reference Ross2003; Briones, Reference Briones2004, Reference Briones2016; Briones and Rockoff, Reference Briones and Rockoff2005; Brock, Reference Brock2016).

Shares of National Bank of Chile, Valparaiso Bank, and other banks in currency issue, 1860–1893.

Figure 6 Long description

The graph displays shares in currency issue from 1860 to 1893. The x-axis represents years from 1860 to 1893. The y-axis represents percentage values from 0 to 100. Three lines are shown: Banco Nacional de Chile, Banco de Valparaiso and Others. Banco Nacional de Chile starts high at 90 percent in 1860, drops sharply by 1865 and fluctuates around 20 percent thereafter. Banco de Valparaiso begins at 0 percent, rises steadily to around 30 percent by 1875 and remains stable. Others start at 0 percent, rise to 50 percent by 1865 and fluctuate between 30 and 60 percent. Banco Nacional de Chile initially dominates, but shares converge around 1875. Major fluctuations occur for Banco Nacional de Chile between 1860 and 1865. Lines are distinguished by different markers: Banco Nacional de Chile uses triangles, Banco de Valparaiso uses circles and Others use a solid line. The graph illustrates changes in dominance among the banks over time.

Another important feature of the Chilean banking system was that it was highly politicized. On the basis of an extensive database of the Chilean deputies and senators between 1876 and 1882, historian César Ross has established that of 156 deputies, 50% were closely linked or directly engaged in banking business, while of a total of 43 senators, 60% had close links to banks. Of the total 199 members of Congress registered in the database, 89 were actually stockholders in different banks. Among important bankers in the Chamber of Deputies were José Nicolás Hurtado, director general of the Banco Chileno Garantizador de Valores, Agustín Edwards Ross, director of the Banco A. Edwards, Pedro Lucio Cuadra, manager of the Banco de Valparaíso in its Santiago offices, as well as four directors of the Banco Mobiliario. Among the leading Senators were such figures as Pedro Marcoleta, a director of the Banco Nacional de Chile, Rafael Larraín, president of the Banco de Valparaíso, José Besa, president of Banco Nacional de Chile, and Agustín Edwards Ossandón, president of the Edwards bank, as well as owner of the Banco de Ossa y Cia (Ross, Reference Ross2003, p. 117).

The astoundingly high participation of bankers in politics did not diminish over time, as is shown by similar data from 1885 to 1888, when a total of 121 deputies were closely linked to banks (51% of the Chamber of Deputies), and 77 senators, representing 58% of the total members of the Senate (Ross, Reference Ross2003, pp. 118–119). While this close interface between political and financial elites has been studied for Chile at the end of the 19th century, deeper research is required to explore the real influence of the bankers on public policies. The information available on Chile also suggests possibilities for comparison with other Latin American countries, but research in this specific field of the historical sociology of the ties between political elites and banking directors is yet in its infancy.

The entire Chilean banking system was deeply affected by the civil war of 1891, when the majority of the Congressional deputies allied with the Navy in a movement determined to oust the head of the government, José Manuel Balmaceda (1886–1891). As president, he had used the nitrate revenues to push forward an ambitious public works program as well as expand public education. But the religious tolerance espoused by the head of state garnered the opposition of the Catholic Church, as well as of many new deputies. Perhaps most importantly, the private nitrate companies considered that the government threatened their interests, and they were backed up by leading bankers and powerful British interests. A decisive moment came when the majority of Congress refused to ratify the budget and drove the executive branch into an impossible situation. During the year 1890, as various rebellions broke out, most bankers came to favor the rebels, especially after the president began to impose a series of emergency measures that were intended to increase the issuance of a large volume of fiscal certificates to cover both administrative and military expenses. The Army supported the executive branch but was defeated by troops of the Navy in a series of pitched battles that led to the fall of the government and eventually to the suicide of Balmaceda.

The civil war of 1891 inevitably led to growing fears that both the monetary system and the banks were headed toward collapse. As a result, the leading bank directors began to discuss future reforms to bolster the financial system. Toward the end of 1893, an important event occurred in the country’s banking development with the merger of three of the leading commercial banks: the Banco Nacional, the Bank of Valparaíso, and the Banco Agrícola. Their entire commercial business passed to a new entity that was baptized as the Banco de Chile. The capital of the new entity was 40 million pesos, with contributions of 50% from the shareholders of the Banco de Valparaíso, 40% from the owners of the Banco Nacional, and 10% from the shareholders of the Banco Agrícola. At the same time, there was created a new mortgage company denominated the Banco Hipotecario de Chile, which brought together all the mortgage resources of the three banks and had a capital of 10 million pesos. For decades, these entities would dominate the Chilean financial system.Footnote 38

7. Epilogue

Our summary review of the cases of Argentina, Brazil, and Chile suggests that in the late 1880s, there was a high level of banking concentration in all cases, explained by the notable predominance of the largest banks. These entities dominated the issue of banknotes in each country, although it is clear that in each case, the plurality of issue continued to exist down to the end of the century. A quantitative comparison of the banking systems of Argentina, Brazil, and Chile indicates that the Argentine system was the largest and had the highest level of concentration. There were, however, many latent risks in the establishment of large private banks with extensive monetary privileges and close ties to their respective governments. These materialized during the financial crises that shook each nation during the early 1890s, when most of the national banks collapsed or were transformed due to close linkages with unstable public finances. In 1890 in Argentina, the two leading banks went under in the midst of a huge financial debacle marked by various bank panics, a stock market collapse, a real estate crash, and a debt crisis. This debacle ricocheted across the Atlantic, causing considerable havoc in the money market of London and being known subsequently as the Baring Panic. This was largely due to the excessive commitments of the famous British merchant bank with investments and loans in Argentina and Uruguay.

The financial crisis in the River Plate simultaneously shook the Brazilian markets (Triner and Wandschneider, Reference Triner and Wandschneider2005). First came the reaction of foreign investors who saw increased risk in the acquisition of Argentine and Brazilian gold bonds, causing steep drops in quotations and curtailing new loans. Second was the monetary and banking contagion that spread outward from the financial collapse in Buenos Aires, spurring a currency crisis in Brazil. The latter led to chaos in the domestic banking and equity markets in Rio de Janeiro and contributed to the end of the financial boom known as the Encilhamento in 1892. That the leading banks were in deep trouble was confirmed by the decision of the Brazilian Finance Ministry to force the shareholders of the strongest entity, the Banco do Brasil, to merge with the Banco da República in January 1893, despite considerable opposition. During the following decade, the Brazilian banking system would suffer from the legacy of the crisis. In Chile, both the National Bank of Chile and the Bank of Valparaiso, dominant entities within the local banking system, were brought to their knees by the civil war of 1891 rather than by financial volatility and contagion as had been the case in Argentina and Brazil. In the event, in 1893, the two largest banking entities in Chile were forced to merge with the smaller Banco Agrícola to form a much larger enterprise, the Bank of Chile, that came to be the dominant financial enterprise in the nation for decades. In sum, the 1890s were witness to major banking and financial upheavals in three of the largest Latin American economies and also led to a profound restructuring of their leading banks and banking systems, with long-lasting consequences.