1. Introduction

In the past, as now, both rich and poor households have had to perform a number of key financial functions, including lending and borrowing.Footnote 1 While these needs remain relatively stable over time and space, and across the social spectrum, the institutional arrangements available to meet them – affected by formal or informal sets of rules, norms and conventions, and so forth – vary greatly. Existing research suggests that pre-industrial credit markets could have been able to offer several alternatives to borrowers because various lenders proposed different solutions to those in need of credit.Footnote 2 This article builds on this idea and investigates the mechanisms of this decision-making process in eighteenth-century Venice. In a nutshell: what did people in pre-industrial societies do when they needed credit and why? Could they decide between different lenders, and did they actually do so?

There is a large body of literature that examines pre-bank credit markets across Europe. It describes a complex and structured world, inhabited by various kinds of lenders who offered their services to a heterogenous group of borrowers.Footnote 3 Some of these creditors were publicly recognized and operated with the permission of local authorities, while others remained in the grey economy, offering loans in the context of private – sometimes illegal and occasional – transactions. Borrowers belonged to the whole social spectrum, including both the affluent and the poor strata of society. They had specific and often divergent needs, and they borrowed to invest, to overcome financial difficulties, to smooth consumption and so forth.

However, the interplay between the supply of and the demand for credit remains largely obscure. To what extent did people in the past evaluate their options when in need of credit, if at all? This article aims to open a discussion on this topic and contribute to filling this gap. Previous literature suggests that the credit market in early modern Venice was quite dynamic and populated by several actors. Analysis of the main features of these lenders, such as the interest rates, the average value of transactions and the characteristics of their activity, suggested that the market had a segmented structure. Indeed, it seems that the intrinsic features characterizing each creditor made them better suited to meet a specific segment of the demand, thus limiting competition.Footnote 4 The question of why such a structure existed, whether it was completely arbitrary or not, lies beyond the scope of this article. Regardless of the cause, the specific features of the Venetian credit market make it the ideal setting for this research.

The article raises significant questions: in the past, could individuals choose between different borrowing options? And, if so, how did they make their choice? Finally, was the market able to provide equally effective and comparable solutions? These are challenging questions, but we believe they are worth asking; indeed, they compel us to look at credit markets from a different angle, suggesting that the dynamics underlying them are more complex than they appear. In particular, we will focus on the borrowers’ perspective on the market: as we will see, this shift allows us to get a more comprehensive understanding of pre-industrial credit markets.

The first problem we encounter trying to answer these questions concerns the sources. Indeed, we would require access to a holistic source that describes the needs of the borrower, compares all the actors involved in the credit market, emphasizes the logic that influences the behaviour of individuals and generates a specific outcome. Unfortunately, such a source does not seem to exist. An intriguing solution comes from the use of counterfactuals applied to a microhistorical case study.Footnote 5

Critics have spread scepticism about the use of counterfactuals in the scholarly community.Footnote 6 In particular, the debate revolves around the fact that causal conditions are ‘spread out across a wide range of situations that make up a structural pattern’.Footnote 7 There is also a high degree of subjectivity involved in selecting what we consider to be the most important fact.Footnote 8 Nevertheless, counterfactuals can be extremely useful, and not only for the purpose of this study. Indeed, thinking about possible alternatives to a single fact is essential in historical research, and all historians do it, consciously or not.Footnote 9

This article uses counterfactuals to juxtapose potentially different outcomes of the same action, exploring different responses to the same need for credit. We will simulate the results of several possible choices and evaluate them against a basic cost–benefit assessment, providing an insightful picture of the credit landscape. Of course, the concepts of ‘costs’ and ‘benefits’ include many more variables than just interest rates and fees: we consider various types of transaction cost, including time, distance from the lending institution, possible social costs (such as a damaged reputation), the risks involved in the transactions (loss of pledges) and other exogenous variables. We also focus on the prerequisites that needed to be met in order to access certain credit channels, such as collateral, and access to information.

In doing so, this article adopts a ‘grounded’ counterfactual approach, supported by several types of data.Footnote 10 It draws on existing research on the Venetian credit market in the eighteenth century, complemented by new, unpublished archival sources. As mentioned earlier, in early modern Venice a multitude of lenders operated in an articulated credit market, offering both long- and short-term loans. The following sections of this article examine the borrowing options available to Venetian households, with an emphasis on consumer credit. Understanding the interplay between credit demand and supply provides insights into Venetian financial behaviour and how households coped with uncertainty.

While we fully recognize the potential of this study, we also need to consider its limitations. Specifically, not all borrowing options are included and, as in the case of peer-to-peer lending, the information is not always complete. Our understanding of the costs and benefits associated with each choice remains partial, potentially biasing the analysis. In addition, the archival nature of the research and the limited availability of the sources imply a risk of selection bias. Nevertheless, the article re-examines pre-bank credit markets from a new angle: its main contribution lies in its unique lens on pre-bank credit markets, which takes into account the coexistence of different actors. It places households at the centre of the analysis, exploring their financial needs (in this case, borrowing) and the mechanisms available to satisfy them.

This article focuses on consumer credit and delves into the everyday life in eighteenth-century Venice. By investigating the relationships between credit supply and demand, it reassesses the concept of rationality and sees the logic behind decisions that seem completely irrational from a cost–benefit perspective. The article emphasises the pivotal role of information and posits that different social strata, with different resources and access to information, are likely to have had dissimilar concepts of rationality (what is known as bounded rationality) and consequently to have behaved differently in the credit market. Conditions that might appear very unfavourable could, in fact, be quite the opposite.

This article is organized as follows: Section 2 sets the background of the research and gives a brief description of the urban economy in eighteenth-century Venice. It also presents the case study that serves as the starting point for the counterfactual analysis. Section 3 and 4 focus on borrowing opportunities in pre-bank credit markets and the merits of counterfactuals as a method of investigation. Section 5 looks at the concept of bounded rationality and highlights the role of information; it postulates potential scenarios if borrowers had approached different lenders. Finally, Section 6 summarizes the main findings.

2. Borrowing and lending in a declining economy

How did people in the past pay for food, clothing and housing? Could poor households supplement financial support from their social networks or access low-cost forms of credit? A basic economic function that households must perform is to make payments. They need to purchase goods and services, transfer money for investments, acquire assets, support other family members and so on. Scholars have often emphasized the shortage of coins that plagued pre-industrial societies. For instance, Craig Muldrew pointed out that in sixteenth-century England the supply of money ‘was always much smaller than the demand for it’, leading to inflation exacerbated by economic and demographic growth.Footnote 11 On the other hand, hoarding coins also had sometimes a negative moral connotation; it was ‘a practice considered unsociable and miserly’, and associated with avarice.Footnote 12

In the early modern period, the very act of handling coins was problematic. The small currency used for everyday transactions was constantly depreciating and prone to counterfeiting, damaging local economies – and the households that operated within them. In addition, as coins were accumulated, theft was a constant risk.Footnote 13 Thus, even if pre-industrial societies were monetized, most daily transactions bypassed silver or gold coins. Payment in kind, reciprocity and credit were paramount to facilitate and bolster exchange and ensure the fluidity of the local markets.Footnote 14 Letters of exchange provided a safer and more efficient method of transferring money over long distances. According to Muldrew, much of the wealth of English merchants did not exist in real terms, only on paper, mainly in the form of credit.Footnote 15 As a result, everyone across the social spectrum was involved in credit and debt relationships. This does not mean, however, that all strata engaged with the same lenders or had access to the same borrowing opportunities.

This research studies the functioning of the credit market and the relationship between demand and supply in eighteenth-century Venice. During this period Venice experienced a phase of significant redefinition in several respects, particularly on the international stage. After fighting the Turks in the so-called Morea wars (the first between 1684 and 1699 and the second between 1714 and 1718), the Venetian Republic entered a state of ‘forced neutrality’. This was not so much a pacifist decision as a recognition of powerlessness. The military withdrawal coincided with a decline in diplomatic relevance on the European stage and a gradual deterioration in public finances.Footnote 16 From an economic point of view, Venice remained one of the main hubs for the European nobility, renowned for its beautiful urban landscapes and home to important painters and playwrights. It was also the main port on the Adriatic Sea, acting as a link between the eastern and western shores of the Mediterranean. The Rialto Bridge was still an important commercial centre, and the volume of goods exchanged was significant.Footnote 17 However, Venice’s pre-eminence as the maritime and commercial power of the eastern Mediterranean was waning. From the early seventeenth century, Venice no longer dominated the trade routes linking the Middle East with central and northern Europe but rather acted as a regional market. Its role in global commerce dwindled, overshadowed by the more dynamic economies of the north, especially the Netherlands and England.Footnote 18

The late seventeenth and eighteenth centuries saw a decline in real wages, and the rise of costs of essential commodities like wheat and wine. This situation particularly affected the financial capabilities of the lower strata, which were also affected by the negative effects of the consumer transition.Footnote 19 Venice was the capital of a regional state, and as such it attracted a large number of poor people and vagrants who moved to the city in the hope of social support or mere sustenance through begging.Footnote 20 This situation was aggravated by economic insecurity and the increasing gap between the supply and demand for work.Footnote 21 As a result, a growing number of people needed to finance basic consumption, which is likely to have increased the demand for consumer credit and put pressure on the credit market.

The characteristic urban structure of the city invariably impacted the daily lives of its inhabitants, especially their mobility. Venice consists of a group of semi-artificial islands in the middle of a lagoon. Today, many bridges facilitate the mobility of people, both between the city and the mainland, and within the city itself. However, this was not the case in the eighteenth century: many of the bridges we can see today did not exist then and people had to walk farther to reach the nearest one, take their own boat or pay a boatman to cross a canal. Moving around the city could therefore be costly, in terms of both time and money, and even more so to move from Venice to the mainland.Footnote 22 In order to prevent fraud and speculation, the Republic of Venice implemented since at least the sixteenth century standardized tariffs for journeys within the city and from the city to the mainland.Footnote 23 However, travelling was still expensive and time-consuming, and certainly not justified by the need for small consumer loans. As we will see in the following sections, the economic background, the physical characteristics of the city and the decision of the public authorities likely affected both the structure of the credit market and the borrowing behaviour of Venetian households, making Venice a particularly interesting case study for this analysis.

3. Navigating the credit market: a matter of choices?

In the era of big data and global history, microhistory seems to be losing ground in the historical debate, apparently struggling to bridge the gap between micro and macro perspectives, linking local events to global narratives. Yet, focusing on the micro, on the everyday stories of single individuals and the ‘exceptional normal’, provides valuable insights to help us better interpret historical trends.Footnote 24 This article uses a case study related to the events characterizing an episode within a single life to explore various ‘what if?’ scenarios, examining different possible outcomes arising from the same initial conditions. This starting case study will allow us to engage in discussions about the functioning of the credit market, moving from the micro to the macro level. To this end, this study focuses on a particularly detailed court case. On 21 May 1706, Andrea Barbaro and his wife Isabetta (short for Elisabetta) filed a case with one of the Venetian civil courts, the Signori di Notte al Civil (Civil Lords of the Night). This magistracy was responsible, among other things, for settling disputes involving minor acts of violence, petty thefts and frauds. In this case, the couple reported a problem related to a credit transaction that was not going as planned. In fact, they had borrowed money against some pieces of clothing, which they were unable to redeem. The loan lasted for about three months, between February and May 1706.Footnote 25

Isabetta and her husband Andrea were addressed as Nobildonna (noble woman) and Nobilhuomo (noble man) and were part of the Venetian patriciate, the ruling class. We do not have much information about them, but they probably belonged to a minor branch of the ancient and important Barbaro family. We know they lived in the sestiere called Castello, in the eastern part of Venice, which was not the richest area of the city at the time.Footnote 26 However, they employed at least one male servant and were well known in the area, being part of a network that included the parish priest and other nobilhomeni (noblemen). It must be stressed that the main protagonist of the story is Isabetta and not her husband. Andrea Barbaro was the one who filed the case to the Signori di Notte al Civil, but it seems he only intervened when what could be considered as a ‘private’ occurrence became ‘public’ through the involvement of the court. The protagonist, the one pulling the strings, was Isabetta: it is no coincidence that she appears in all the testimonies of the various witnesses.

The trial has been chosen as the starting point for this article for several reasons. First, it concerns a person who needed to borrow money. Second, the testimonies of Andrea Barbaro and those of the various witnesses provide us with a great deal of detail. Isabetta needed six ducats, for which she was willing to pawn two of her dressing gowns.Footnote 27 The court records confirm that the noblewoman chose (or had to turn to) pawnbroking as a source of credit, and she knew from the beginning that she would have to pawn some of her possessions in order to get what she wanted. There is also a lot of information about the quality of these pledges. One of the two gowns was of many colours, ‘beautiful and new’, and worth between 16 and 18 ducats. The other, which included a matching petticoat, was ‘the colour of lead’ and used, but was worth up to 30 ducats when new. Overall, they were both quite valuable and worth far more than the sum the noblewoman was looking for.Footnote 28

The small amount and the short duration of the loan suggest that it was probably a loan to support consumption. We can assume that Isabetta borrowed to smooth her income or to repay other small debts of the same type.Footnote 29 Despite the typically small size of the transactions, especially when compared to mortgages or commercial loans, consumer credit played a pivotal role in enabling individuals and households from all social strata to access the basic goods they needed. It is this kind of credit transaction that is at the heart of this article: focusing on consumer credit allows us to include in the analysis a range of lenders whose services covered borrowers from across the social spectrum. This is crucial for two main reasons: first, the analysis is more meaningful because it potentially includes a relevant share of the transactions that took place on a daily basis in a pre-industrial city. Second, we can exclude some sectors of the credit market, and all actors related to them, such as mortgages and notaries. In fact, notaries were costly, which made their intermediation impractical for small transactions. Therefore, the very characteristics of the case study help us to define the limits of the analysis.Footnote 30

There are two more issues we need to consider. First, it is difficult to compare Isabetta’s case with other similar ones. In fact, there are not many court cases concerning credit in the sources. All similar trials that have survived in the Signori di Notte al Civil fund can be counted on two hands.Footnote 31 We need to bear in mind that only part of the archives of the magistracy still exist today, while most of them have been lost. Furthermore, in the Venetian context, the functions of the different magistracies overlapped, and people could turn to one or another of them to file a case involving similar matters. This means that it is possible to find trials for credit in several funds, which makes it difficult to conduct a survey and estimate the volume of sources available. As a consequence, reconstructing the structure of the credit market and conducting the type of analysis proposed in this article is quite challenging. Despite extensive archival research, there will always be room for speculation.

Second, while it was not uncommon for women’s clothes and belongings to be used as pledges, it is interesting that the borrower was a woman. What implications did this have for the entire process? There is extensive literature on the limitations faced by women, especially married women, in favour of their fathers or husbands.Footnote 32 Still, women appear regularly as customers of moneylenders, in Venice and elsewhere; the literature suggests that women relied on their specific competences to evaluate second-hand objects, a critical skill when dealing with pawnbrokers.Footnote 33 Also, Isabetta had a male servant, who helped her in her daily tasks. All considered, how limited was Isabetta in her choices? While it is difficult to assess her economic agency from a single trial, the analysis will take into account as much as possible both her gender and her social status.

In the following section , we describe the borrowing options available to Isabetta Barbaro and their main features. We outline the main characteristics of consumer credit in eighteenth-century Venice. Several pawnbrokers, some officially recognized and others operating in the grey economy, played a significant socio-economic role in the city. Among the most important actors involved in this activity we can identify the Jewish moneylenders, the Monti di Pietà, and, peculiar to the Venetian case, innkeepers and wine sellers. What did borrowing from these three lenders involve? Was there a private peer-to-peer credit market and how did it work? To answer these questions, we will develop a cost–benefit model to evaluate each credit offer. Finally, we contextualize Isabetta’s decision in terms of the alternative options she had and examine them within a framework of economic rationality.

This article is based on various data collected in the Venetian State Archives. The analysis includes court cases concerning credit, including usury, theft and various frauds. These trials are interesting because they describe the mechanisms of credit transactions and the relationships between lenders and borrowers. The article also focuses on the accounting documents of the clerks working in the Jewish banchi and the reports of the authorities in charge of supervising their pawnbroking activities, as well as those of innkeepers and wine sellers (who were under the supervision of a public magistrate). These documents are crucial for measuring the volume of their transactions and for tracing the characteristics of the loans they granted. The picture is completed by normative sources, which help us define the details of the activities of each of all these lenders.

4. Lending opportunities and borrowing practices in eighteenth-century Venice

Jewish moneylenders, initially also Lombards and Tuscans, were authorized to settle down in Venice and open their banchi (lit. bench) in 1382. Three years later, the Republic signed the first condotta with the Jewish community, an agreement that granted them exclusive rights to this lending activity and established some basic rules for its management.Footnote 34 In the following years, the relations between the Venetian authorities and the Jewish community were tense, and they were expelled from Venice in 1397. They could reopen their banchi in 1509, finally settling down in the Ghetto in 1516.Footnote 35 By 1558, there were three banchi operating in the Ghetto, lending at an annual interest rate of 12 per cent.Footnote 36 In 1573, the Republic intervened, reducing their interest to 5 per cent a year and limiting the maximum amount of each loan to three ducats.Footnote 37

By the time Isabetta Barbaro tried to pawn her dresses, Jewish moneylenders had been active in Venice for around 200 years. It is plausible that she knew about their existence. The noblewoman lived in Castello, which means that she, or more likely her servant, would have had to travel to the other side of the city. The loan conditions imposed by the Republic on Jewish moneylenders at the beginning of the eighteenth century set an interest rate of 5 per cent annually. Each transaction, limited to three ducats, was subject to a tax of one soldo (1/20th of a lira). This cost was proportional to the amount lent, but considering an equal valuation of the two dresses at 3 ducats, Isabetta would have paid an effective interest rate of 5.27 per cent in the first year. The Jewish moneylenders were a cost-effective option for the noblewoman. The stricter conditions of the banchi (loans limited to three ducats) would not have been a problem in this case, since the loan was within the parameters set by the Republic. The only downside was that to borrow six ducats she would have had to pledge the two dresses into two separate banchi.

There are also exogenous variables that we need to consider. At the beginning of the eighteenth century, the Jewish community was experiencing serious financial troubles. This certainly had an impact on their ability to operate. The Republic wanted to make sure that the social purpose of this lending activity always took precedence over the financial needs and the greed of the lenders.Footnote 38 For this reason, the Jewish moneylenders in Venice were subjected since 1573 to stricter lending conditions that reduced the profits from lending. At the same time, the Republic repeatedly requested the Jewish community to increase the total amount invested in such activity.Footnote 39 In order to keep up with all these requests, the Jewish community accumulated a huge debt that undermined their activity and jeopardized their own existence.

In 1732, the community had a total debt of more than 1,200,000 ducats.Footnote 40 Even if part of the amount was due because of rising interest rates, the enormous sum gives us a particularly vivid idea of the importance of the Jewish banchi for the local population. The Republic created a specific magistracy to support and coordinate the financial recovery of the Jewish community (the Provveditori sopra ai Banchi), but it was not until the 1770s, almost a century later, that the banchi started to make some profits, albeit minimal.Footnote 41 We can therefore imagine that the activity of the Jewish lenders could have been undermined, at least cyclically, by a critical lack of liquidity.

Alongside the Jewish moneylenders, there were other actors offering small loans to the lower strata, secured by low-value pledges of everyday use. This applied to Venetian innkeepers and bastioneri – managers of the bastioni, warehouses where wine was sold. They assumed the dual role of supplier of primary goods – especially wine – and moneylender, becoming central figures in Venice’s urban context. Venice was not the only place where innkeepers and, more generally, wine sellers were involved in the credit market, but the Venetian authorities made it formal and ‘public’.Footnote 42 It was placed under the supervision of a specific magistracy, the Provveditori and Sopraprovveditori alla Giustizia Nuova, which regulated the whole activity and monitored the protection of private property.Footnote 43

While inns were located exclusively around St Mark’s Square and the Rialto Bridge, there was at least one bastione in each of the 70 parishes into which the city was divided. It is therefore likely that Isabetta had access to one or more bastioni near her home. The authorities portrayed the bastioni as dangerous places where all kinds of people met to drink and indulge in vice and immorality.Footnote 44 Moreover, Isabetta was a woman and entering a bastione alone would probably have damaged her reputation. Again, she had a servant who could have taken care of such a matter.

The advantage of the pawnbroking activity of bastioni and inns was its ‘mixed’ nature, given that objects were pawned in exchange for cash and wine, or to pay for the purchase of wine and food, to be either taken away or consumed on site. Loans were formally interest-free, and borrowers had to pay only a small tax of one soldo on each pledge. However, lenders provided at least a third of each loan in wine, profiting from the difference between the price of wine bought and sold and its quality – the wine used for this kind of operation was usually very poor.Footnote 45 If Isabetta had gone to a bastione to pledge her dresses, she would have received at least a third of the value of the loan in wine, about 50 litres. This is a considerable amount: although it was a fundamental part of people’s daily diet, it was a product that deteriorated rather quickly.Footnote 46

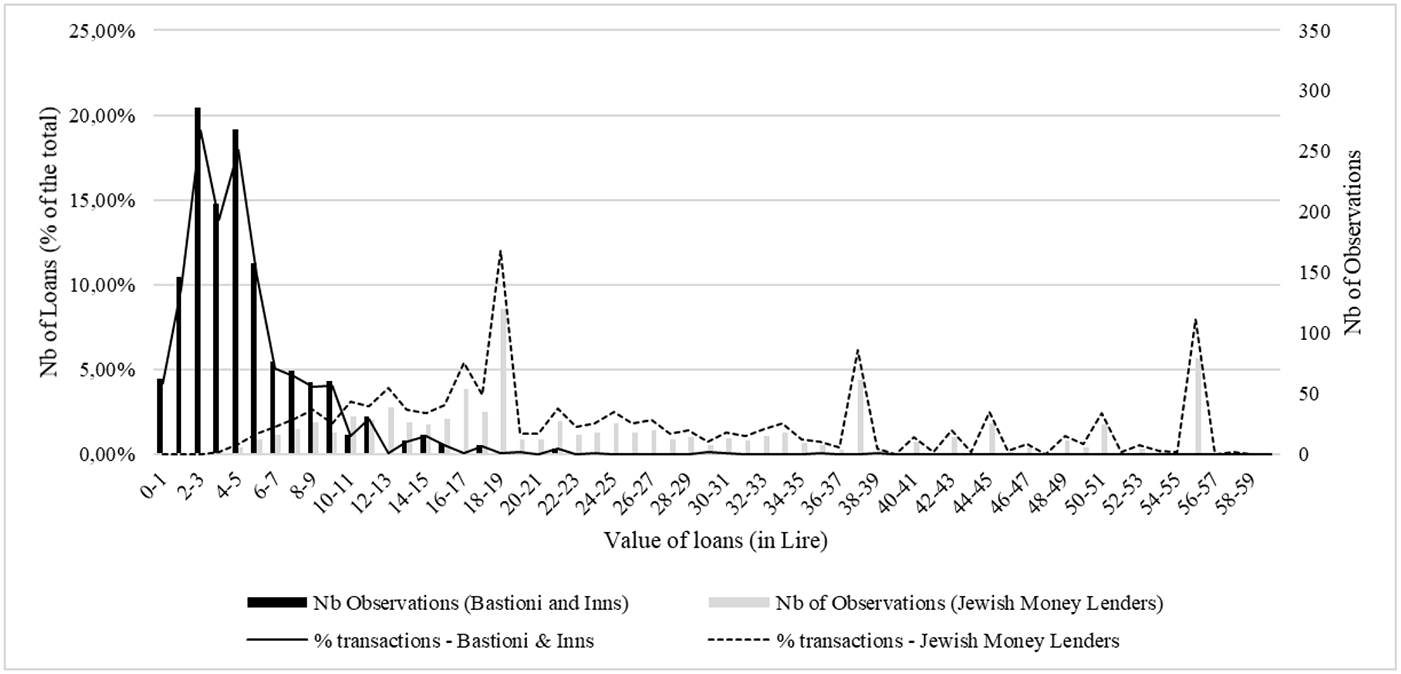

This brief description clearly suggests that the lending activities of Jewish moneylenders and innkeepers and bastioneri were different in nature. It seems that they addressed different needs for credit. Objects were mainly pawned into inns and bastioni in order to pay for food and wine, while this was not the case with the Jewish banchi. All these features are reflected in the quantitative analysis of the value of the loans. Figure 1 compares the value of loans supplied by the bastioneri and the Jewish moneylenders at the beginning of the 1790s (percentage of loans per range of value). The data we used for this comparison come from a ledger of a Jewish banco dated 1790, and a series of accounting books and inventories related to the activity of several bastioni in 1792. This comparison is particularly relevant for two main reasons. First of all, information on the daily activity of Jewish moneylenders in Venice is sparse at best. We were able to find information on approximately 1,000 loans supplied by the Jewish moneylenders, including both new loans and repayments, which remains a unique finding in the Venetian archives. For bastioni and inns, our database includes roughly 1,200 transactions. Second, while the value of loans is not directly correlated to the quality of the borrowers, it is at least a sign of the kinds of transaction that took place in the specific context. As we can see in Figure 1, there is limited overlap between the two lines, indicating that the values of loans supplied were quite different. This suggests that the two lenders were involved in different kinds of transaction and likely served different kinds of borrower.Footnote 47

Number of loans by value (deflated, as % of total) and number of observations: inns and bastioni (1792) compared to one of the Jewish banchi (1790).

Besides Jewish banchi and bastioni, another option available to Isabetta Barbaro would have been the municipal pawnshops. The Monti di Pietà were first established in the late fifteenth century to support the lower strata, in ideological opposition to the ‘Jewish usury’.Footnote 49 There was a well-developed network of Monti in central and northern Italy, as well as in northern France, Belgium and Spain. Originally designed to provide small loans to the lower strata, the range of services they offered to their clients expanded rapidly. In fact, they soon began accepting deposits and making significant loans to local communities and wealthy families – which was more profitable, but also riskier.Footnote 50

The process of establishing a Monte in Venice was a long one, marked by many setbacks, and only officially ended in 1829, 32 years after the fall of the Republic.Footnote 51 Initial attempts to establish a municipal pawnshop in Venice date back to the first half of the sixteenth century, but they were never successful owing to the firm opposition of the authorities. Specifically, in 1523, the Consilio dei Dieci (the Council of the Ten), one of the most important magistracies of the Republic with a mandate for state security, decreed a ‘death sentence to any nobleman [who] dared to propose something new in the matter of pledges’.Footnote 52 The exact motives behind such a strong stance are unclear, but probably it was intended to protect the activity of the Jewish moneylenders, who had proved to be a useful economic asset that Venice was reluctant to jeopardize. The establishment of the Monte could have damaged the source of revenue of the Jewish community, a significant concern given their historical role in supporting the Republic financially.Footnote 53

Nevertheless, the absence of a Monte in Venice did not prevent its inhabitants from having recourse to those located on the Venetian mainland, especially in Treviso and Padua. Sources testify that many Venetians, usually from the wealthier strata, went there to pawn their goods.Footnote 54 However, travelling was costly and made the Monti on the mainland a cost-effective alternative only if the sum required limited the incidence of such costs. The decision to include the Monti in our analysis is therefore important, particularly in a context where extra-urban mobility seemed to be costly but well developed. Since we do not have any information about possible connections between Isabetta or her husband in any of the cities on the Venetian mainland, we must assume that the most logical choice for her was to cut costs as much as possible and turn to the nearest Monte, that in Treviso. In this case, the literature on the subject proves to be lacking in technical details, since we know only that between the seventeenth and eighteenth centuries the interest on loans ranged between 3 and 5 per cent.Footnote 55 We must also take into account the cost of crossing the lagoon, in terms of both money (if she did not have a boat) and time. The conditions linked to the loan were similar to those offered by the Jewish moneylenders, but moving to Treviso was relatively expensive in relation to the loan Isabetta Barbaro wanted to obtain. In the cities of the mainland, the Monti played an important social role in sustaining the lower strata, at least those who possessed objects of some value that could be used as collateral.Footnote 56 This was certainly not the case for those living in Venice.

The fourth borrowing option we consider in this analysis is that of private lenders. It is well known that interpersonal networks, embedded in social relationships, play a pivotal role in facilitating and encouraging credit transactions. Laurence Fontaine and Craig Muldrew have delved deeply into the nature of the relationships that bind the individuals involved in this type of credit, in order to understand the mechanisms and preconditions necessary for one person to decide to lend money to another. In particular, the literature emphasizes the role of trust in maintaining financial networks.Footnote 57

The circle of credit, including family and friends, was extremely important in past societies, acting as a safety net for individuals and a way of managing risk and uncertainty. It was a kind of pre-industrial welfare system.Footnote 58 Family and friends provided a way to raise funds and a safety net to deal with coin shortages or other financial difficulties. It was often impossible to refuse a loan to a family member even if the chances of repayment were bleak, which was probably a burden on the wealthiest line of a family.Footnote 59

The trial demonstrates that Isabetta did not borrow from a family member or a friend. She might have tried; after all, she did not need a large sum. But, for some reason, she opted for another solution. Her request was maybe declined by her family; maybe she deliberately chose not to turn to her family in order to maintain secrecy and borrow without letting other people, perhaps her husband, know. We do not aim to underestimate the role of family networks in providing access to credit.Footnote 60 At the same time, it is undeniable that in the Venetian context they seemed not to be enough: for some reason, Venetians looked outside of their family when they needed credit. Indeed, there were other alternatives: sources confirm that innkeepers and bastioneri granted tens of thousands of small loans every year, and the same applies to the Monti on the mainland. There is not much quantitative evidence about Jewish moneylenders in Venice, other than the data for the early 1790s shown in Figure 1; however, we do know, for instance, that in 1792 the banco nero and the banco rosso granted 887 and 932 loans per month, respectively.Footnote 61

Moreover, there was also a vivid interpersonal market populated by private lenders. Court records are the only source that allows us to look at interpersonal credit. In the sample at the heart of this article, there seem to be common features that characterize this kind of transaction. First, they usually involved movable collateral. Having something to pledge was so critical in early modern Venice that individuals even rented out objects to be used as collateral in credit transactions.Footnote 62 Second, borrowers and lenders came into contact through one or more intermediaries. For instance, in 1706 Pietro Vespasiani borrowed 20 ducati from Sebastian Rizzo, using a silver coaster as collateral. Vespasiani repaid his debt, but he was unable to retrieve his collateral from Rizzo. He was only an intermediary who spent the money he received from the borrowers instead of repaying the original lender. What is interesting here is that the lender is not even mentioned; he is only a terza persona (a third person). His identity remains unknown to us, and probably to the borrower as well.Footnote 63 Third, interest rates were often very high compared to the rest of the market. Andrea Lorenzetti lent 60 florins to Francesco Cecchetti (who gave as collateral four crimson velvet tapestries worth a total of 460 ducats). When Cecchetti repaid his debt, he had to add an usura of ten ducati, one-sixth of the full amount.Footnote 64

In general, interpersonal transactions are more flexible and less homogeneous, which makes them more difficult to categorize and more challenging to compare with the other options considered here. Moreover, the only sources available are a few court records, which are partly biased because they describe only cases where something went wrong. Also, it is not likely that family members turned to courts when there were problems within the family, which means that all these cases could escape the analysis. However, the inclusion of the interpersonal private market allows us to answer another important question that goes beyond the Venetian case. The family was probably a cheap and quite logical option to look to for support. But why did individuals decide to get involved in transactions that included other private lenders and often several intermediaries, characterized by a high risk of losing their collateral and high interest rates? This is even more puzzling when we consider that there were other, perhaps more convenient, alternatives.

5. Information, opportunities and choice

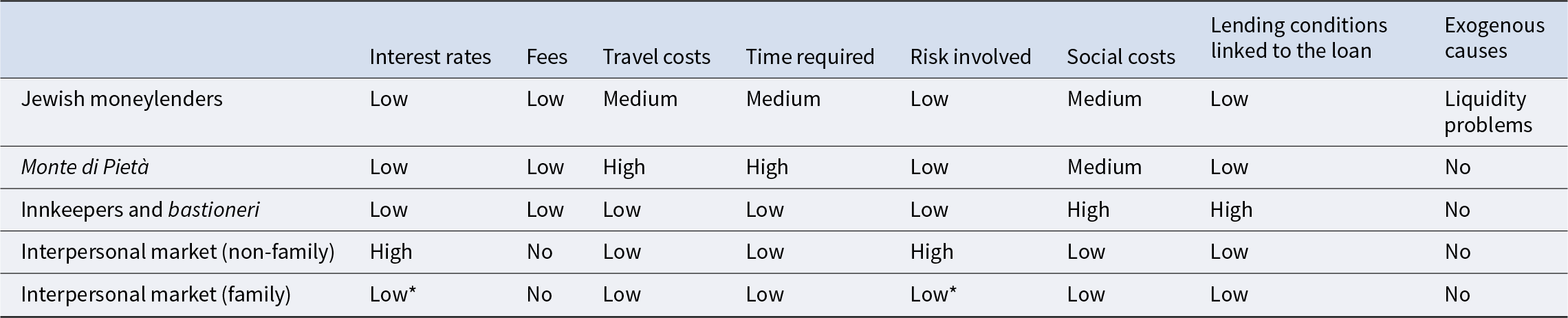

Table 1 summarizes the results of the comparison of the four different borrowing options we have discussed so far, all of which were available to Isabetta Barbaro in 1706 Venice. These options can be characterized using a few simple variables to indicate whether they are low, medium or high cost.

Cost–benefit analysis of all borrowing options considered in the research (consumer credit); elaborated by the author

Table 1 fails to summarize convincingly all the transactions that took place on the interpersonal market (this explains the *). This is owing to the above-mentioned lack of sources and the flexibility of the conditions that characterize private transactions. However, the model certainly includes some of them and, as we will see, it works convincingly well in the context of this analysis.

For obvious reasons, travel costs and time are partly correlated. ‘Risk involved’ refers to the likelihood of being cheated or robbed and losing the collateral (from the borrower’s perspective). Property rights were protected by the law, and courts seemed to take those cases very seriously. At the same time, we do not know how effective they were, or how likely it was that defrauded borrowers were able to recover their collateral. ‘Social costs’ describes how a specific choice could potentially damage one’s reputation (such as a woman entering an inn alone). ‘Lending conditions’ indicates that there were specific conditions linked to a loan, such as one-third of any loan being supplied in wine by innkeepers and bastioneri. Finally, ‘exogenous causes’ is a general category that includes various external factors that may discourage a transaction or render it less attractive. The features related to family credit transactions are based on what the literature suggests since we do not have specific information on this sector of the credit market.

Now that we have compared all the options we identified in this research, we can go back to the central question: what did Isabetta do and why? Looking at Table 1, the Jewish moneylenders were the best option available in the institutional market to meet the demand for consumer credit. Nonetheless, Isabetta did not pledge her dresses to the Jewish banchi. Instead, she got in touch via her servant with two women, Gerolima Minelli and Cecilia Mola, who lived not far from her house, in the parish of San Martin, one of the poorest of the city.Footnote 65 The two women acted as intermediaries, pledged the two dresses and took the agreed sum to the noblewoman.Footnote 66 The loan was issued at the beginning of February and, considering that the trial is dated 22 May – with Isabetta attempting to redeem the dresses some 20 days earlier – had a duration of about three months (beginning of February–beginning of May). The interest rate she had to pay was about 70 per cent per annum.

Upon repayment, Isabetta learnt that it was impossible to retrieve her items. The sources testify that she tried several times to settle the matter privately, before turning to the Signori di Notte al Civil. More specifically, she sent four different people to try to recover the objects. The first was a man called Marco Scandagio, priest of the church of San Trovaso. He talked to the two women, but all he got was a vague promise to return the objects as soon as possible – which did not happen. Subsequently, Isabetta asked a friend of hers, a woman called Betta Moresini, to contact the two women. Betta Moresini claimed that she was able to track down only Gerolima Minelli, who was then taken to the Barbaro residence and met with Isabetta. Unfortunately, the witness did not know what the two women talked about, but Gerolima claimed that the ‘things [the pledges] were safe’, and that ‘only one man has them’, meaning that the two dressing gowns were in the hands of a single lender.

This meeting failed to resolve the issueand Isabetta sent a third person, her servant Giacomo Castellazzi, to plead her case: he was probably more determined than the previous two mediators and was able to get a better understanding of the situation. The women were part of a chain of intermediaries: they got in touch with a man who worked as an apprentice in a barber shop in the sestiere of Castello. The servant described in his testimony that he was able to find out who the man was and to talk to him. The apprentice admitted that he had played a role in the transaction, but that he was only an intermediary and that the pledges were in the hands of another man who lived in the Ghetto. Eventually, the servant went to the barber shop ‘10 or 12 times’ to ask about the pledges, until the owner, angry, sent him away, explaining that ‘he [the apprentice] only has business with the women who received the pledges [Gerolima Minelli and Cecilia Mola] and he does not want to deal with anyone else’.Footnote 67 This is an interesting statement about the limits of individual responsibility, which we will hear again later.

The last person Isabetta sent to talk to the two women was Gasparo Diedo, who claimed to be a family friend.Footnote 68 He spoke to the two women and found out that the lender was due to be in Rialto that very day. He hurried there and was able to track him down and talk to him. Gasparo tried in vain to get the two dressing gowns back. He explained that when he became angry (‘scaldato in questo interesse’) the mysterious man immediately ran away, declaring that he had no business with him. After collecting these testimonies, the Signori di Notte al Civil summoned Cecilia Mola and Gerolima Minelli for questioning: at first, they avoided answering, and then they asked for more time to prepare for their defence. Eventually, they simply ignored the orders and did not appear in court. This is how the trial ended on 12 July 1706, and we do not know what happened after that.

The trial certainly highlights the importance of social networks in resolving conflicts: before turning to the court of the Signori di Notte al Civil, Isabetta asked four different people to contact the two women and persuade them to return her objects. The case study also reveals a fascinating strategy used by intermediaries when faced with complications in the credit transaction. They simply emphasized their specific role in the deal, stressing that they were accountable only to the intermediary immediately before or after them, and to no one else. This approach appears to be effective, as evidenced by the fact that only the two women were summoned and held accountable by the authorities, and no other individuals (including intermediaries or the lender) were directly involved in the legal proceedings. Remarkably, it was the intermediary closest to the borrower who bore the brunt of the risks involved.

The court case confirms two more things: interpersonal credit transactions could be risky and very costly – an interest rate of 70 per cent a year, not to mention the risk of losing the pledges. It seems strange, we could say not rational, that anyone would voluntarily choose to take out a loan with such characteristics. The neoclassical interpretation of individual behaviour postulates global consistency and objective rationality on the part of the economic actors, who make their decisions according to a utility function.Footnote 69 This implies that, in similar circumstances, all individuals would uniformly choose the same lender, the one offering the best conditions in terms of the cost of the transaction (interest rates and fees). But this is clearly not the case.

Behavioural economists have adopted a broader definition of rationality that includes not only outcomes but also the processes that lead to decisions.Footnote 70 They introduced the concept of bounded rationality, which encompasses the limits of rationality and takes into account the human nature of the objects of study. This idea was driven by the need to develop a theory that was more consistent with the results observed in empirical studies in social and behavioural sciences.Footnote 71 Bounded rationality means

that the choices people make are determined not only by some consistent overall goal and the properties of the external world, but also by the knowledge that decision makers do and don’t have of the world, their ability to evoke that knowledge … to work out the consequences of their action … to cope with uncertainty.Footnote 72

Rational behaviour is subjective and linked to a person’s specific interpretation of the world in which they live, as well as their gender, age, social status, density and type of social networks, affiliation, citizenship, legal situation and other personal characteristics. Rationality is bounded because the abilities of individuals and their means of computation are limited, and information is imperfect. What people knew about the structure of the credit market varied according to social networks, peer influences, expectations and past experiences. The very concept of rationality is distorted by our own ideas of what is rational. We might think that 70 per cent a year is an astonishing interest rate, that it is irrational to accept such loan conditions, and immoral to propose them. While this may be true to some extent, Isabetta’s case and others found in the sources demonstrate that it is not entirely accurate.

Research shows that context matters. Still today, people sometimes accept paying even higher interest rates when they are really in need. This happens in imperfect markets characterized by a lack of alternative sources of credit. At the same time, such loans tend to be very small and very short term (a few days), which substantially reduces the incidence of interest. It is not possible to generalize, but in some cases such unfair and immoral loans – which, of course, bear no fees besides interest rates – allow borrowers to access the resources they need to earn enough money to repay the loan, the interest and to cover their daily expenses – which makes them perfectly rational.Footnote 73

Individual rationality is intrinsically linked to access to (quality) information. We expect that the lower, middle and higher strata – with Isabetta probably belonging to the last of these – had access to different information. The upper and the lower social groups occupied different positions within society that either facilitated or hindered their access to specific economic opportunities, which in turn shaped their economic behavior. Also, they had different collateral to rely on, which gave them access to different credit circuits; they had access to different social networks, which meant different intermediaries and lenders. This indicates that some credit offers available to the lower strata might have appeared irrational to the upper strata and vice versa. But it also confirms the idea that pre-bank credit markets offered various alternatives and that people were likely to make different choices according to their financial means and their bounded rationality.

Some of the reasons that might have led Isabetta Barbaro to turn to a private lender, despite the seeming inconvenience of doing so, are now much clearer. The Monti and the bastioni were certainly not attractive options for her because of the costs and the conditions linked to the loans. On the other hand, the Jewish moneylenders could have been a good choice, but probably ‘external’ causes took over and led the noblewoman to the informal alternative. It is very unlikely that she followed the same process we have traced in this article, comparing the various options available to her in the Venetian market: she probably just turned to those lenders who seemed more suited to her specific needs at the time. The most rational choice for her.

6. Concluding remarks

Pre-industrial credit markets seem to have been complex and characterized by a diversity that no longer exists in modern developed countries. They were flexible and multifaceted, and probably able to offer suitable solutions to a variety of different actors. Counterfactuals helped us to go deeper, to observe more closely the mechanisms that organized the Venetian credit market, and to highlight what distinguished all of the credit offers. Through a methodological exercise, we simulated a decision-making process: starting from a trial, we then traced the structure of the consumer credit offer based on data collected from different sources. After all of this, what do we now know about the Venetian credit market – and more generally about pre-industrial credit markets – that we did not know before?

First, different actors were offering different services to their clients, and we better understand the importance of looking at the bigger picture. Whether in competition or not, this implies considering that there was some kind of relationship between the actors available on the market. Second, we know that the Venetian authorities shaped the activity of the Jewish moneylenders, making it similar to that of a municipal pawnshop. This is also a plausible explanation for their refusal to establish a Monte in the capital. This was a political decision that could have led to a mismatch between the supply and the demand of credit: the episodes of Venetians pledging their objects in the Monti on the mainland seem to confirm the existence of a spill-over between different markets.Footnote 74 However, further research is needed to prove this hypothesis. Third, we did not find any information on credit within the family and among friends, but we do know that there was a vibrant interpersonal market, characterized by the presence of many intermediaries – many of which were women—and operating according to roughly the same features as the ‘institutional’ market (for instance, the use of collateral).Footnote 75 We have also gained useful insights into the importance of social networks and the mechanisms regulating interpersonal transactions. All of this adds to our understanding of pre-bank credit markets.

The decision-making process we tried to replicate involved a woman needing to borrow a relatively small amount of money. This is not exceptional, as the literature reports many similar cases. Isabetta was a woman surrounded by men, some of whom held inferior hierarchical positions relative to her. What can we say about her economic agency? This is an intriguing issue that could not be fully explored within the scope of this article.Footnote 76 The trial suggests that she acted alone when she decided to borrow money, and managed autonomously the entire process. The complex web of relationships does not seem to have constrained her economic agency; rather, it may have enhanced it.

The case study of Isabetta Barbaro also confirms that the neoclassical concept of rationality is not appropriate to analysing and understanding pre-industrial economies. Indeed, conditions initially perceived as unfavourable can in fact be competitive. High interest rates were offset by the absence of fees, the relatively small amounts and the typically short duration of the loan. On the other hand, interpersonal loans could also be risky. The private lenders could withhold the collateral and run away with it, which would not have been possible in the context of a Monte, a Jewish banco, an inn or a bastione. In fact, the authorities strictly controlled their activities and could require immediate and full refund. In Isabetta’s case, the loss of her collateral would have meant a huge loss and a great risk for her.Footnote 77

This article focuses on a very specific urban context (Venice) and on a case study, and the results cannot be generalized. We expect the picture to be quite different in other contexts, especially in rural areas. Nonetheless, it proves that such an approach can be useful to deepen our understanding of the structure of the credit market and to help us investigate its underlying mechanisms. Finally, has the market been able to provide equally effective and comparable solutions to borrowers? Yes and no. All credit offers proved to be somehow different. However, the market was undoubtedly able to meet different needs, which should not be taken for granted.

Acknowledgements

The ways in which households have dealt with financial needs in the past was the focus of a workshop that the author co-organized in Antwerp with Oscar Gelderblom and Nelleke Thanis. I would like to thank my co-organizers and all the participants for the stimulating discussions, some of which are summarized in this article. I would also like to thank Martin Dackling for revising the article and all the participants of the workshop ‘Debt: the good, the bad and the hidden – bringing family, kin, commerce and consumption debts together’, organized in Vienna by Janine Maegraith, Margareth Lanzinger and Matthias Donabaum.

Competing interests

The author declares none.

Open access

Open access