1. Introduction

On 13 June 1778, the orphan Anton Brandstetter wrote a letter to his guardian, Mathias Pastanell, urging him to send him money from his parental inheritance. Brandstetter was 23 years old at the time and had been under Pastanell’s supervision since the death of his mother six years prior. At the time, Pastanell was the mayor of Brandstetter’s hometown of Eggenburg in northern Lower Austria and a parental relative of his. The minor had gone to the imperial capital of Vienna to study there, incurring many expenses for board, lodging, clothing and fees.

In the letter, Brandstetter thanked Pastanell for sending him 30 fl (gulden), but the money was barely enough to pay his outstanding bills. He had even had to pawn his pocket watch and the money was not enough to redeem it. He emphasized that his creditors were swarming and tormenting him daily, and that he did not want to arouse suspicion by constantly postponing his payments. Another letter – probably from the same year – that he wrote to his sister, Magdalena, revealed that their guardian was also helping him further his career. Anton emphasized that it was only through a recommendation letter written by Pastanell that he was able to obtain a title from the imperial government. The same letter shows that Anton tried to circumvent the tight financial restrictions under which he was placed by asking his sister for money and fabric for new clothes. The money, he insisted, was needed for a present to his professor, who would not admit anyone to exams without an appropriate gift in advance. Anton was apparently anxious to keep the whole matter secret from Pastanell as he urged his sister to remain silent about it and burn the letter. The fact that we know about this, and that the letter ended up with the rest of the documents regarding his tutelage, suggests that the whole affair did not quite go according to his plan.

This correspondence raises a number of questions about the role of guardians and their management of orphans’ assets. The fact that Pastanell appears to have been so parsimonious with his ward’s money was not owing to the siblings’ poverty. Their mother had left Anton and Magdalena an inheritance of over 4,000 gulden each, a substantial sum at the time, and the fact that Anton was able to study in Vienna was evidence of a relatively comfortable material situation, even if he did not perceive it that way.Footnote 1 However, there were restrictions in place on how their wealth could and should be used, with most of it being invested in illiquid assets by being lent to debtors with interest. This leads us to two main questions: firstly, who were the guardians and how did they manage their wards’ assets; and, secondly, what role did orphans’ assets play as a source of credit in an environment largely devoid of professional financial institutions and what position did they assume in economic networks?

It is generally accepted among historians that credit was a ubiquitous phenomenon in the early modern period. In a society where cash was chronically scarce, credit was granted for a broad range of reasons: as deferred payment for merchandise or consumption goods, or for outstanding dues and taxes. Much of this credit in circulation was small-scale, short-term and informal, serving mainly as a means of payment and relying heavily on personal trust between creditors and debtors or their intermediaries.Footnote 2 However, more large-scale and formalized credit, such as loans for productive investment and to finance property transfers, was more problematic. Specialized financial institutions were by and large sparse and inaccessible to most people outside the major cities, with savings banks only starting to appear on a large scale throughout central Europe from the 1820s.Footnote 3 Instead, other, often local sources of credit had to be found. These could include wealthy individuals, local institutions such as churches, brotherhoods or city treasuries, but also orphans who had inherited wealth that they could not administer independently before reaching adulthood. Capital that would otherwise have remained idle was lent to debtors for interest, often secured against real property. In some regions, Lower Austria among them, such heirs of minor age could emerge as prominent creditors that deserve special attention.

Being indebted was a rather ambivalent state. On the one hand, it could be a sign of poverty and economic dependence on others.Footnote 4 On the other hand, having many outstanding debts could also be a sign of social capital and trustworthiness, or of economic power, being able to force others to extend credit to them – such as business partners being owed their remuneration or employees their wages.Footnote 5 Accordingly, Sheilagh Ogilvie et al. showed that in early modern Württemberg (Germany) indebtedness was associated with a higher value of assets, while poorer people generally had lower levels of liabilities. Ulrich Pfister found that in Switzerland indebtedness through mortgage credit was positively correlated with net income since wealthier households owned more land that they could use as collateral to obtain credit.Footnote 6

In this article, we look at local credit markets in the town (‘Stadt’) of Eggenburg and the neighbouring rural seigneury (‘Grundherrschaft’) of Kattau in northern Lower Austria. The town of Eggenburg was a rather typical example of a Lower Austrian urban municipality outside of the imperial capital of Vienna with its rather small population of a few thousand inhabitants, its political self-administration led by an upper middle class of burghers which was subject directly to the archduke of Austria, and a local economy that combined craft production with agriculture – in this area most notably wine production. Kattau was a village whose inhabitants were subject to a feudal landlord, the counts of Gilleis, and was mostly dependent on arable farming and viticulture, with a small number of craftsmen who produced predominantly for everyday consumption.

Local credit markets in early modern Lower Austria have so far received little scholarly attention, despite the fact that the role of manorial lordship and the specificities of its system of property transferFootnote 7 and marital property regime make it a potentially fruitful area of research.Footnote 8 We argue that, in order to understand the particularities of Lower Austrian debt networks and credit circuits, we need to pay attention to the specifics of intergenerational property transfer and, in particular, the administration of orphans’ wealth. In order to do this, we use a broad definition of credit that encompasses not only money loans but all material claims and liabilities. These could include a broad range of obligations, such as deferred payments for consumer goods, productive materials or services, outstanding taxes and fees, but also debts stemming from wealth transfers among kin, such as inheritance shares. For an actor-centred perspective on credit, such a conceptualization makes sense because the financial planning of households or individuals had to consider their solvency in general, without necessarily differentiating between the reasons why debts were owed.Footnote 9 Liabilities accrued for various reasons and in multiple forms had to be taken into account in a household’s financial planning and could affect its ability to mobilize further funds.

Christiaan van Bochove and Jaco Zuijderduijn have argued in a recent article that rather than trying to explain the genesis of modern financial institutions such as banks retroactively, or conducting a functionalist analysis of finance applying modern standards, historians should aim to explain credit markets from contemporary demand.Footnote 10 By focusing on challenges faced by households throughout their life-course, we can understand why certain financial institutions emerged at certain times, why some survived and others vanished. We argue that one such challenge faced by most households was the transfer of property at various stages of the life-course, such as at marriage or as an inheritance after the death of a household member. These moments posed challenges for households regarding the financing of these transfers.Footnote 11 Using such a framework, the need becomes clear to examine the specifics of Lower Austrian property transmission practices and the securing of orphans’ wealth in order to understand how these credit networks functioned. While there have been a number of studies on specific orphan chambers or orphan courts, studies tracking their activities within a wider local credit network have hitherto been lacking.Footnote 12 By filling this gap, it is possible to assess the importance of orphans’ credit for local economies and place them within the context of a variety of different types of debt.

In this article, we first give a brief overview of the sources and methodologies used before providing some context on the legal and institutional background of guardianship in early modern Lower Austria. Then, we look more closely at the guardians and the administration of their wards’ wealth, discuss the importance of orphans’ assets in local credit markets and map out the networks they constituted.

2. Sources and methods

To answer the questions outlined in the previous section, the main sources used are a sample of 513 mortgage deeds (Satzbriefe) collected in book form (Satzbücher), covering the period from about 1730 to 1790 for Eggenburg and Kattau.Footnote 13 These Satzbücher (hereafter ‘mortgage books’) formally registered the hypothecation of land with a sum of money. They were a supplement to the land register (Grundbuch), which often referred to the mortgage books and vice versa. It should be noted that they do not cover all credit activities, but only those that were officially secured by land, which was a legal requirement from the seventeenth and eighteenth centuries onwards.Footnote 14 The main advantage of using this type of sources is their level of detail. They always provide information on the date, the creditor and debtor, the amount borrowed, the mortgaged properties, the number of mortgages and often the interest rate, the date of repayment and the reasons for borrowing or the type of credit (for example obligation, outstanding purchase sum or inheritance share). A disadvantage is that, like most sources on credit, they tend to record mostly formalized and therefore higher amounts of credit, although in our sample debts could be as small as 5 fl. Nevertheless, it must be recognized that many everyday informal debts are not covered by these records.

We also use documents that record the appointed guardians and their wards, as well as the accounts they were obliged to keep on their behalf. For the town of Eggenburg we have analysed a selection of guardianship accounts that record the income and expenditure of wards in great detail and provide insights into their investment and consumption behaviour as mediated by their guardians. In addition, two Pupillartabellen (‘wards tables’) for the years 1722–1735 and 1781 have survived, documenting all orphans currently under the authority of the magistrate, and the names of their appointed guardians.Footnote 15 For the village of Kattau we have used a Gerhab-Protokoll (‘guardian record’) covering the years between 1790 and 1806, which documents the income and expenditure of orphans over consecutive years, as well as their guardians, albeit in less detail than the Eggenburg sources.Footnote 16 These documents allow us to draw some conclusions about the identity of the guardians, their relationship with the wards and the administrative practices used to manage the property entrusted to them.

These sources are analysed using quantitative and qualitative methods. Where the sources allow, we zoom in on specific individuals and the context of their actions. Additionally, we employ quantitative methods to determine the characteristics of our sample as a whole and the role of orphan credit within it in particular. Finally, social network analysis is used to map the local credit circuits discussed and highlight their structural features.

3. Guardians and guardianship

3.1 Regulation of guardianship

The legal basis for the upbringing of orphans and the administration of their wealth in the early eighteenth century was the guardianship regulation (Gerhabschaftsordnung) of 1669.Footnote 17 It specified that if no one else was named in a parent’s will, the closest blood relatives according to inheritance law should be appointed as guardians. Should they refuse, they lost any claim to the orphan’s inheritance they might have had as next of kin.Footnote 18 Guardianship law was also relevant to half-orphans. While widows retained supreme guardianship of their children, they, in contrast to men, lost the supreme guardianship of their children when they remarried. Fathers kept full legal guardianship rights of their children, while mothers did so only as long as they remained widowed. In a second marriage, they did remain acting guardians, but the authorities had to appoint a supreme guardian to keep an eye on the children’s finances and prevent the new husband from misappropriating their assets.Footnote 19 If no guardian was specified in the will and there was no suitable relative, it was the duty of the relevant authority to appoint someone who was deemed to be honest and diligent.Footnote 20

The regulation also specified that real property belonging to an orphan could only be sold with the consent of the authorities, if a surviving parent of a half-orphan agreed, or if it was stipulated in the will.Footnote 21 Despite this regulation, it was common practice to sell real estate. Helmut Feigl has argued that the long-term administration of a farm by the guardians was not feasible owing to the requirements of labour organization, as the successful running of a farm required the full effort of its holders.Footnote 22 Indeed, in our sample we have found little evidence of such a case of continued administration of a household by guardians on behalf of their wards, in either urban or rural settings. Existing cash was to be used to buy real estate or to lend it to local landowners against annual interest payments. Such loans had to be secured by a mortgage letter or ‘sufficient pledge’.Footnote 23 This is another reason why they were well documented in the mortgage books.

The guardians themselves were generally not allowed to use the funds for their own purposes. If they wished to do so, they had to seek permission from the authority.Footnote 24 However, in our sources there are numerous cases where guardians were also debtors of their wards. For example, in two mortgage deeds from Kattau from 1744, Michael Weichart and Adam Decker appear both as guardians of Hans Georg Weichart and as his debtors, owing him about 72 and 20 gulden, respectively, for money borrowed (‘baar dargelichenen gelt’).Footnote 25 In any case, the ward had a tacit mortgage on the property of his guardians, which was intended to secure the proper and careful management of his estate by making them liable should anything go wrong. Even the authorities, such as the manorial lord, were only supposed to take the money for themselves if there were no other investment opportunities. In such cases, they had to pay their ward 5 per cent interest.Footnote 26

The Codex Theresianus was drawn up by a commission in the 1760s and 1770s by order of empress Maria Theresia and contained extensive regulations on guardianship. Although this draft was never officially sanctioned, it aimed to create a uniform code of law for the Austrian lands and Bohemia, and thus reflects the legal practices and ideas of the time.Footnote 27 The Codex distinguished between four stages of youth: up to the age of 7 (Kindheit), up to 15 (Unmündigkeit), up to 20 for men and 18 for women (Unvogtbarkeit), and finally up to 24 (Minderjährigkeit), after which one was considered a full adult.Footnote 28 It was specified that supreme guardianship lay with the territorial prince, mediated by the relevant courts and local authorities, and finally with the appointed guardians. Fathers had the right to appoint guardians in their testaments, but mothers did not.Footnote 29

It was the duty of the guardianship authority to determine a level of expenditure appropriate to the social status of the ward, which was to be neither too high nor too low. The capital was to be used to cover expenses only if the income was insufficient or if it was in the long-term economic interest of the orphan.Footnote 30 To ensure this, guardians were required to keep accounts of their wards’ income and expenditure, which they had to submit to the local authority that was formally responsible for the orphans. The law did not even exempt remarried natural parents from this obligation.Footnote 31 However, the guardianship lists from Eggenburg suggest that this was not so strictly applied in practice. These documents were drawn up by the city administration to report to the state which orphans were under its authority, what property they possessed, who their parents had been and who their guardians were. The list from 1781 contains numerous entries such as ‘because the wards are still in the mother’s/stepfather’s care, no bill will be issued’.Footnote 32

The Codex Theresianus tightened the regulations on collateral. Landed property could be sold only with the knowledge of the authorities and cash or proceeds from the sale of other assets had always to be invested with interest and secured by a registered plot of land and the promissory notes deposited with the guardianship authorities.Footnote 33 It was also put into practice: the sources show that in the towns studied here, the securitization of orphans’ loans with mortgages was common practice during the eighteenth century. With increasing fiscal demands of the state, especially in the second half of the eighteenth century, the investment of orphans’ money in state funds was mandated from 1787.Footnote 34 However, this regulation did not apply to ‘the countryside’ (das flache Land), that is, rural areas outside the imperial capital of Vienna or princely towns and cities. In our case, this means that it applied to Eggenburg (a town subject directly to the archduke of Austria), but not to Kattau, which was a rural lordship. Soon after, in 1791, the regulation was abolished.Footnote 35 The impact of the restriction on the local supply of credit was potentially considerable. We will look at this in more detail.

The institutional arrangements for the administration of orphans’ wealth could vary. In many European regions, special orphan chambers or orphan courts were established to administer assets and protect their material interests. In some Italian and north-western European cities, such arrangements date back to the fourteenth century.Footnote 36 In parts of the Habsburg monarchy, such as the Lower Austrian countryside, a cumulative orphans’ fund, the so-called Waisenkasse, was usually set up by the manorial administration, into which orphans’ assets were paid. The first confirmed instances of such arrangements in Lower Austria date back at least to the sixteenth century.Footnote 37 The money was pooled in order to make larger loans and minimize risk for both lenders and borrowers. These cumulative orphans’ funds were major sources of rural credit until well into the nineteenth century and were also used as deposit banks by full-aged investors, as well as by municipalities and charitable institutions. In towns and cities, on the other hand, in contrast to rural areas, the investment of orphans’ assets was more likely to take place directly between creditors and debtors, with the intermediary of guardians and the municipal administration, which was the supreme legal custodian.

In the sources from the town of Eggenburg considered here, the term ‘Waisenkasse’ (orphans’ fund) appears from 1782 onwards, but it seems to have administered only individual orphans’ wealth. Debts were still issued directly between orphans and their debtors.Footnote 38 In Kattau the situation was different. Here the Waisenkasse acted directly as a creditor, without any reference to individual children.

The form in which orphans became creditors could vary between a mere accounting procedure where no actual cash changed hands and the actual exchange of money. A look at probate proceedings can make this clearer. Anna Maria Weinmannin from Kattau had died in 1778 and her estate was settled in early 1779. She left a husband and four children, three of which were minors. It was agreed that their maternal inheritance should be paid to them at their eighteenth birthday by depositing it in cash at the Waisenkasse.Footnote 39 Similarly, all assets of Joseph and Theresia Haydinger who had died in Eggenburg in 1799 were auctioned off. The share of their adult son was to be handed to him whereas the inheritance due to the three minor children was to be put into the Waisenkasse where it was going to earn interest.Footnote 40 By contrast, the widow of Joseph Köck who had died in Eggenburg in 1779 issued an obligation which she deposited at the Waisenkasse on behalf of his four heirs who were still minors, without any cash changing hands yet.Footnote 41

3.2 Who were the guardians?

The central government in Vienna required princely towns to keep lists of guardians. In a letter of 1759 to the mayor, judge and city council of Eggenburg, the central government reminded them of their duty to keep such records and send them to Vienna in order to improve the administration of these matters.Footnote 42 At least two such lists have survived in the archive: one from 1735 and one from 1781.Footnote 43 For Kattau, we have similar sources, called Gerhab-Protokolle (guardian protocols), from 1790 onwards.Footnote 44 The Eggenburg lists give us information about the number of children under guardianship administered by the town, as well as some details about their guardians. They show that in 1735 there were 82 children under guardianship, while in 1781 there were 127. It should be noted that not all of these children were fully orphaned. In 1781, over 70 per cent of the children on the list had at least one surviving parent or were supported by a step-parent. From this group, about 56 per cent were left with a surviving mother, 41 per cent with a father and 3 per cent with a stepfather. In these cases, the town often, but not always, appointed a guardian. However, the day-to-day administration of the half-orphans’ property was left to their parents, who were not under the same obligation to keep detailed accounts.

Several conclusions can be drawn about the people who acted as guardians. While most were responsible for only one or two orphans or a group of siblings, some took care of several. In 1781, one Mathias Peyfuß had as many as ten groups of orphans under his care, amounting to 25 individual children. Many of the men who acted as guardians were local dignitaries and members of the town elite. Of the 26 guardians in 1735, 10 were addressed with the honorific ‘Herr’ and at least 4 had been mayors at some point in their lives. In 1781, at least 9 of the 30 guardians were members of the town council, including the mayor Mathias Pastanell mentioned at the beginning. In four cases, orphans shared the same surname as their guardians, suggesting some kind of kinship between them. It is difficult to say how common it was overall to have relatives as guardians, but the fact that there were no more shared surnames suggests that at least paternal uncles as guardians were not very common here.Footnote 45

In the village of Kattau, 37 persons were recorded in the orphan register in 1790. However, not all of them had appointed guardians, probably because they had already reached the age of majority and only had assets left to pay into the orphans’ fund. Excluding these cases, there remained 32 wards who were under the tutelage of at least one, and sometimes two, persons. In total, 43 different persons acted as guardians, most of them for only one child but some for two and up to eight different orphans in the case of Leopold Ludl, who was the guardian of two individuals and two groups of siblings. Of these, eight, or about 19 per cent, had the same surname as their ward, suggesting a possible kinship.

A comparison of the two places reveals some differences. In Eggenburg, a larger number of orphans were under the tutelage of a smaller number of people than in rural Kattau. The role of guardian was more often taken on by a local urban elite, whereas in the rural setting it seems to have been more often relatives.

3.3 Administration of funds

Guardians had to keep records of their wards’ assets, income and expenditure. Some of these documents, such as annual account statements or receipts for expenses, have survived and give us a glimpse of how orphans’ assets were managed. We have selected three groups of siblings from Eggenburg for whom a large number of sources have survived and whose finances we have examined in more detail.

The first group of siblings were Franziska and Anna Maria Millnerin, with accounts for the years between 1764 until 1768. After the death of their parents, Joseph and Maria Anna Millner, the estate was finally settled in 1764.Footnote 46 Together, the children inherited a sum of 1,110 gulden, which was administered by their guardian, Ignaz Haberlein, a glazier who was also a member of the town council and referred to as their Vetter, a paternal relative. For the first few years after their father’s death, however, the inheritance remained in the possession of their stepmother, for which she had to pay them between 4 and 5 per cent interest per year. It was not until 1766 that their assets were liquidated and lent to other debtors. On average, 95.6 per cent of this sum was invested in between one and six different loans. About half of their total assets was deposited with the Oberkammeramt, the municipal fiscal authority of Vienna in 1766 and about 80 per cent in 1767, generating an annual return of 4 per cent. In this case, income far exceeded expenditure, resulting in a surplus of about 140 gulden at the end of the tutelage, an increase of about 13 per cent. This was owing to the fact that both children worked as servants and therefore did not have to pay for any expenses out of their estate.Footnote 47

The second group of orphans were Anton, Rosalia and Johannes Apfeltaler.Footnote 48 When their father, a butcher, died in 1772, they were 14, 11 and 7 years old. Their mother had died a few years earlier. The three siblings had inherited 1,400 gulden each, of which on average between 94 and 98 per cent was invested in loans. If we compare income and expenditure of the three siblings, they seem to have fared rather differently. While Johannes had only about 60 per cent of his starting capital left at the end of his tutelage in 1791, Rosalia even had a slight surplus in 1781, the last year for which we have sources about her. However, this picture is misleading since some of Johannes’s capital had already been paid out to him before the accounts were finally closed in 1791. Anton’s expenses, which were slightly higher than his income, were partly owing to his apprenticeship. He trained as a barber surgeon with his guardian, mayor Mathias Pastanell, whom we have already met, and this cost Anton around 350 gulden in dues and clothing in total.

The third and final group are Anton and Magdalena Brandstetter, whose correspondence has already been mentioned.Footnote 49 After the settlement of their parents’ estate in 1772, each sibling owned a capital of 4,134 gulden.Footnote 50 Over the course of their guardianship, between 73.0 and 99.9 per cent of this capital was invested in loans. The number of individual loans varied over time, but was about three to four times higher for Magdalena than for Anton. Each of them had a large proportion of this capital invested in state funds: Magdalena slightly under and Anton over 2,000 gulden on average. The annual interest on their investments amounted to 4 per cent, resulting in a median annual income of 145 and 150 gulden, respectively. For both siblings, however, expenses exceeded income. In Anton’s case, median expenses were more than double his income. This was partly owing to his education in Vienna, with expenses for books and travel. In Magdalena’s case, they only slightly exceeded her income by about 20 gulden. Thus, at the end of the tutelage in 1779 and 1781, respectively, their wealth was lower than at the beginning. It was 3,630 gulden for Magdalena, which was about 88 per cent of her starting capital. Anton had only 2,268 gulden left, or about 55 per cent of his original assets. The records for these two siblings also give us some insight into their living arrangements by looking at their expenses for board and lodging. Anton, who was 17 years old when he was orphaned in 1772, first lived in the nearby town of Horn and later moved to Vienna to study. His sister Magdalena, two years younger, was 15 when she became an orphan. She first lived in Eggenburg and moved to Krems in 1776 when she was about 19 years old. This demonstrates that guardians were not necessarily responsible for housing and feeding their wards, which would have been quite difficult with 25 children per guardian. Instead, they served mainly an administrative purpose, an observation echoed by J. S. Schnitzeler, who noted that ‘guardianship was first and foremost concerned with assets and not with the physical well-being of the minor’.Footnote 51

We can see that the legal requirement to cover their expenses with their interest income could not always be met, even when the orphans were quite wealthy. In the case of Anton Brandstetter and Anton Apfeltaler, higher expenditure was necessary for educational purposes. Such expenditure was considered an investment – a transformation of financial into human capital. At any rate, in the case of the Brandstetter siblings, the income would not have been sufficient even to pay for board, lodging and clothing, even though they were comparatively well-off. It is clear that the requirements of social adequacy were more important here than following the law to the letter and keeping a positive balance. Whether or not expenses could be covered with their income was not necessarily determined solely by the amount inherited and the interest earnt from those assets. This is illustrated by the case of the Millner children, who were poorer than the Brandstetters and thus had a lower income. Expenses had to be in line with the social status of the wards, even if this meant that they were higher than the income from interest. In the long run, this was necessary to ensure the reproduction of their social status.

The picture we see in the Kattau guardian record for the years 1790–1806 is different. The accounts were mostly balanced, and the majority even managed to leave their wards with nominally higher wealth at the end of their tutelage than they had originally inherited, even when their capital had been quite small. This was the case, for instance, with the siblings Mathias, Johann and Ferdinand Zimmermann.Footnote 52 They had inherited modest sums from their father, their brothers Joseph and Laurenz, and their mother between 1784 and 1798, amounting to 70 gulden 48 kreuzer each. Their accounts show no expenses, so by 1806 they had an estate of over 85 gulden. The reasons why guardians in Kattau were more often able to increase their wards’ estates are less clear, as the sources are less detailed. One aspect to consider is the fact that the source lists orphans as well as half-orphans, which means that many younger children remained in the parental home without incurring additional expenses. Other possible explanations could be the more thorough integration of full orphans into rural household economies as servants, and thus lower expenditure on board, lodging and education. It is especially noteworthy that boys owned smaller sums at the end of the tutelage in Eggenburg than in the beginning. This might also have to do with higher costs for their education as students in Vienna or as apprentices to artisan masters. This probably played less of a role for girls in general, but also for boys from peasant families who needed less investment in education.

When both parents had died, the situation could be more complicated, as in the case of the siblings Rosalia and Mathias Widhalm. They had inherited the modest sum of 50 gulden from their father, a winegrower (Weinhauer) who had died in 1777, as well as 100 and 120 gulden, respectively, from their mother, who had followed in 1790.Footnote 53 However, the assets remained with their stepfather, who paid interest to his stepchildren.Footnote 54 Rosalia’s accounts show that no money was paid out to her before she reached adulthood in 1798, which led to a net wealth of 200 gulden, higher than the original 170. In contrast, Mathias’s accounts show several deductions, resulting in a slightly reduced estate of about 139 gulden, although we do not know how the money was spent. It is possible that he was an apprentice somewhere and the money was used to pay his fees.

4. Orphans as creditors

4.1 Types of credit

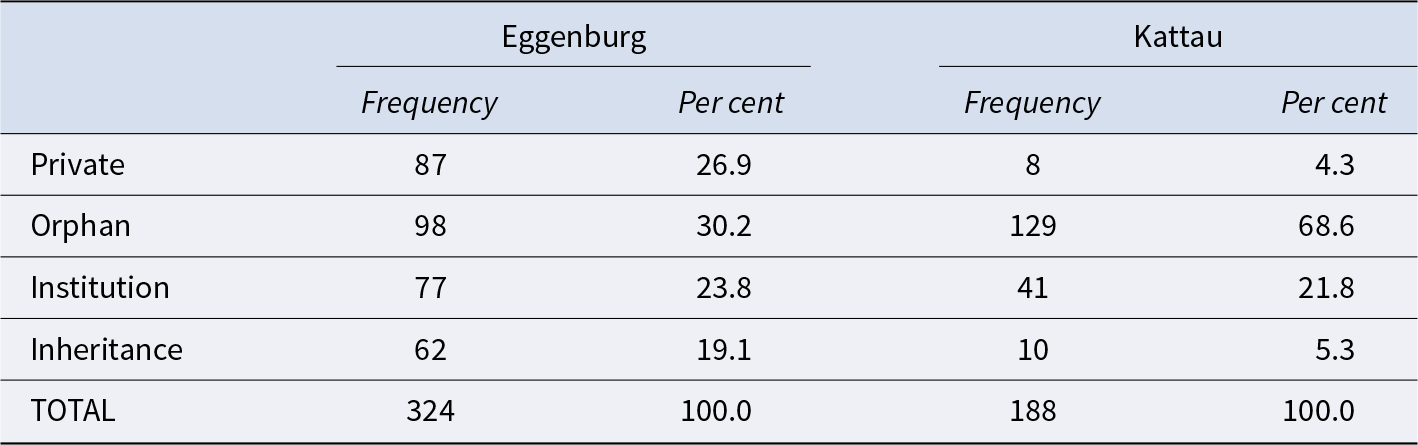

Orphans and their assets frequently appear in written records documenting the mortgaging of land, such as the Satzbücher discussed earlier. From these sources, we learn who the creditors and debtors were and some of their characteristics. For this analysis, all actors were grouped into one of four categories according to who the creditors were: orphans, institutions (such as the parish church or the municipal hospital), inheritance (debts for inheritance shares of children, which represent an accounting process and no real flow of money) and individual private adult persons (which essentially means: everyone else).Footnote 55

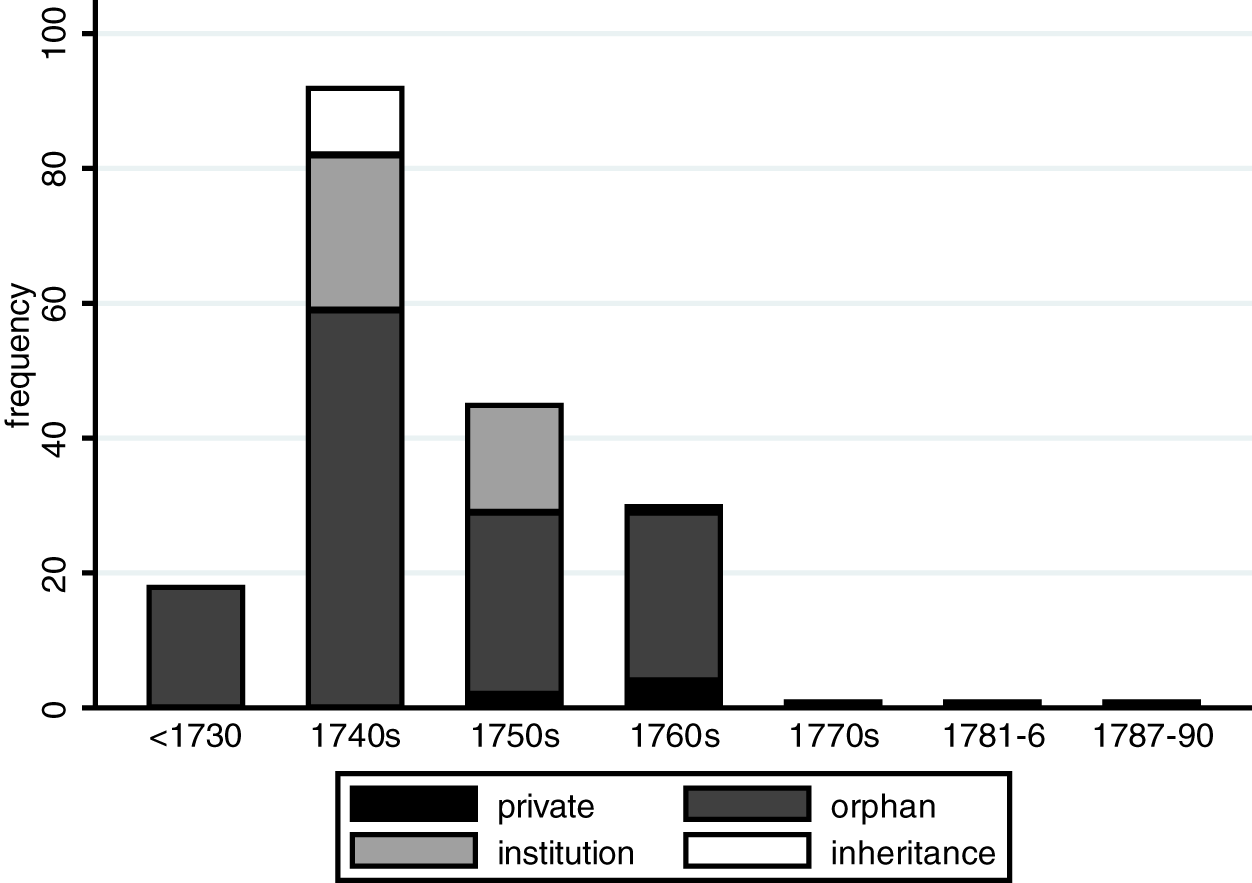

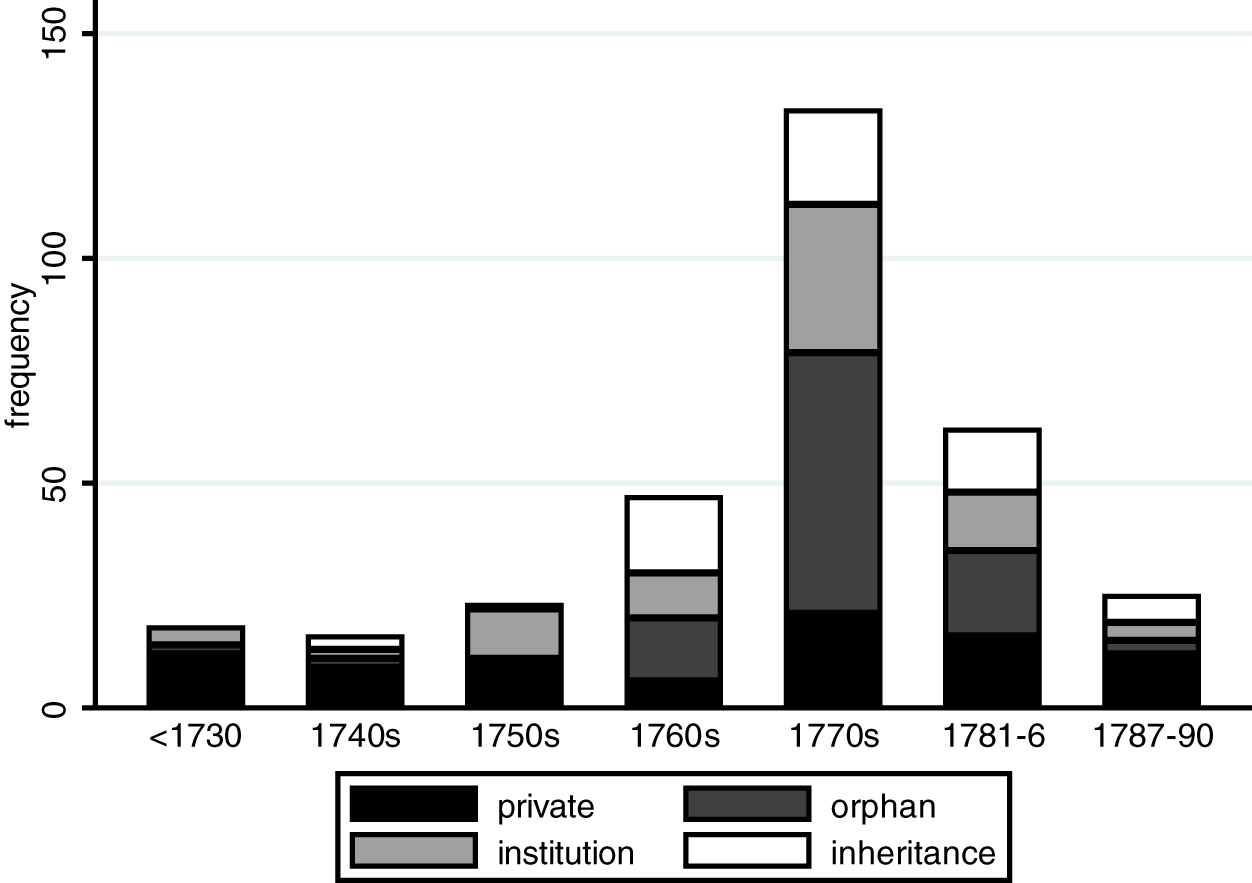

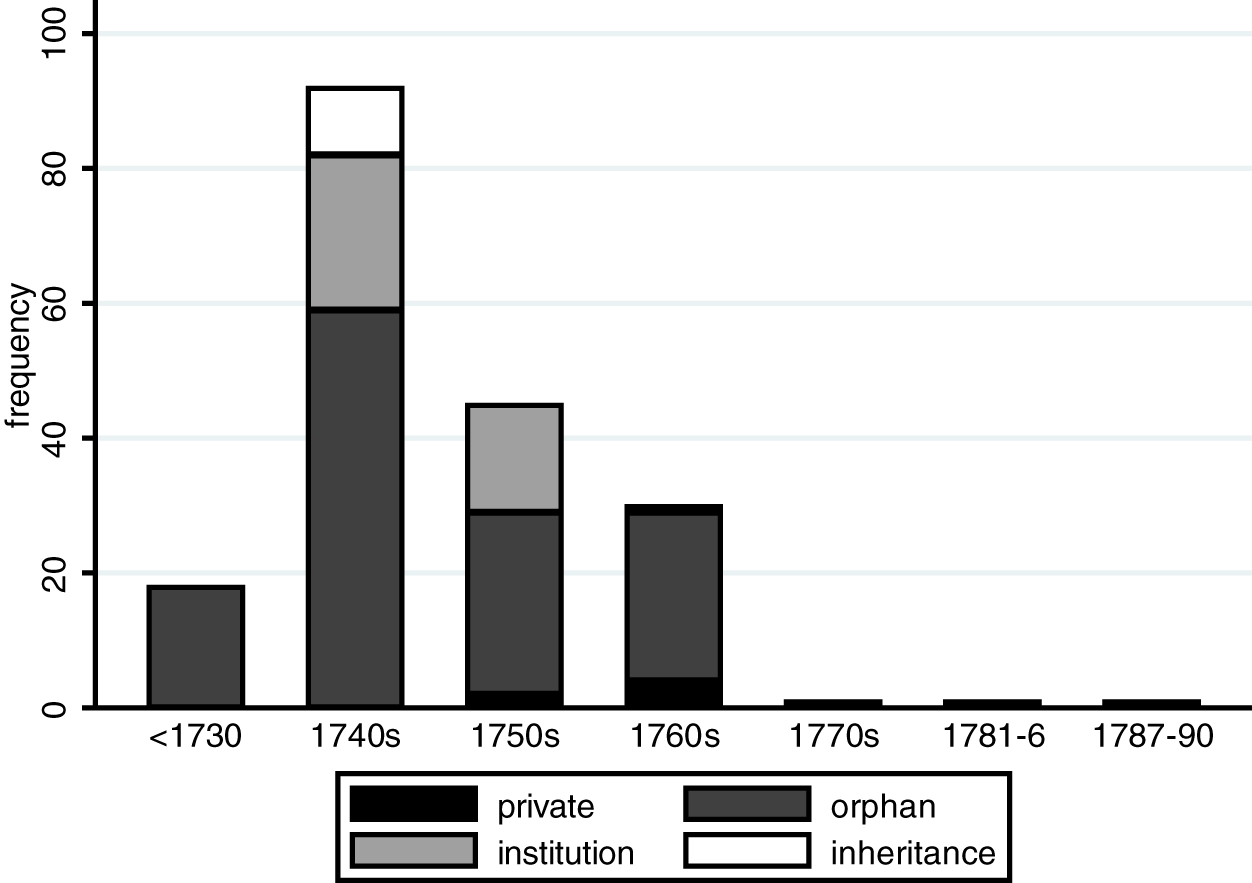

Figures 1 and 2 show the amount of individual loans per period for Eggenburg and Kattau. Note that the number of records for Kattau drops drastically after the 1760s, which is unlikely to be caused by a corresponding disappearance of credit activity. We can thus make only limited statements here for the latter period. Table 1 displays the total number of mortgage loans in each category from 1725 to 1790. We can see that in both Eggenburg and Kattau orphan loans were the most common type, although in Kattau they appear to have been even more important. Institutions were also very common creditors, with a share of more than 20 per cent in both places. However, the importance of loans from private persons differed drastically. In Eggenburg, they accounted for 26.9 per cent of all loans, whereas in Kattau they were of minor importance.

Amount of mortgage credit in Eggenburg – 1725–1790.

Amount of mortgage credit in Kattau – 1725–1790.

Frequency of credits by category – 1725–1790

Source: Mortgage deeds – NÖLA, BG Eggenburg 04/05, Satzprotokoll 1734–1792; NÖLA, BG Eggenburg 11/08, Satzbuch 1740–1824.

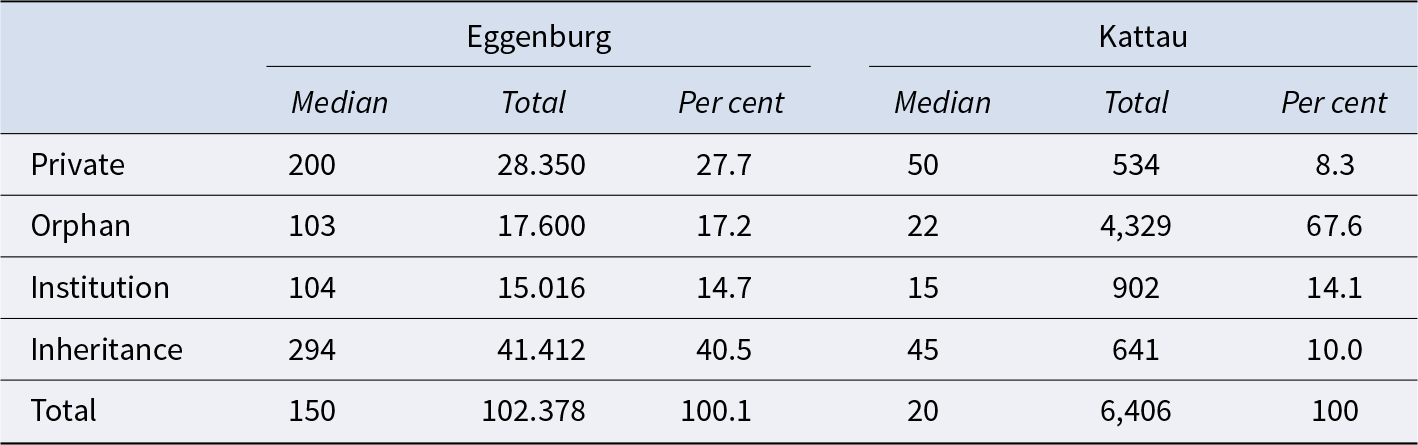

In Kattau, for example, loans to private persons only accounted for 8.3 per cent of total (mortgage) credit volume, compared to 27.7 per cent in Eggenburg (Table 2). However, in both places, these loans tended to be larger than either orphan or institutional credits on average. The median volume of orphan loans was slightly lower in both places, comparable to that of institutional credit, resulting in a smaller share of the total volume than their frequency would suggest. Particularly striking, however, is the much lower volume of credit in Kattau compared to Eggenburg, with the median amount in Kattau being only about 14 per cent of that in Eggenburg. Mortgages for securing inheritance shares were the largest category by volume in Eggenburg with over 40 per cent of all mortgaged debt falling into this group. In Kattau, by contrast, they made up only about 10 per cent of mortgage credit volume.

Median and total volume of credits in gulden (fl) – 1725–1790

Note: percentage totals in this and subsequent tables do not all add up to 100.0 owing to rounding.

Source: Mortgage deeds – NÖLA, BG Eggenburg 04/05, Satzprotokoll 1734–1792; NÖLA, BG Eggenburg 11/08, Satzbuch 1740–1824.

The bar for the last period in Figure 1 has been divided into a part for 1781 to 1786 and one for 1787 to 1790 in order to be able to assess the impact of the above-mentioned edicts, which required orphans’ assets to be invested in state funds. As we can see, the issue of new orphan credits declined sharply, but did not disappear completely after this point. Two mortgages were for obligations issued in early 1787, possibly before the edict was fully implemented. Only one source tells us about a loan made by orphans from as late as 1790. In it, one Angelus Johann Tischler and his wife Maria Anna pawned an acre of land and a wine cellar for a debt of 210 gulden 32 kreuzer that they had issued to three different groups of orphans in 1790. It is difficult to say whether this reduction was an effect of state policy, given the general drop in source records around this time, but it seems very likely that it was not simply an artefact of source availability and instead represents a real decline in orphan credit.

4.2 Purposes of lending and kinship relations

In an economy where trust and moral considerations played an important part, as in early modern Europe, relatives were often mentioned as important creditors and debtors. Laurence Fontaine has argued that family and kin were the first group of potential creditors to turn to because they had a strong moral obligation that made it more difficult to refuse a loan, even if one’s creditworthiness was questionable.Footnote 56 Besides cash loans, another important reason for indebtedness among relatives was the securitization of inheritance shares and other claims. Depending on the laws governing inheritance and marital property, property transfer between generations or between spouses could give rise to a series of debt relations between different groups of people.Footnote 57 The economic consequences of this were discussed as early as the nineteenth century, with critics of partible succession arguing that it would lead to a fragmentation of land and hinder capital accumulation.Footnote 58 Land-hungry smallholders would drive up land prices and burden their land with mortgages, preventing productive investment. Defenders of partible succession argued that undivided property transfers could have equally negative effects. Principal heirs had to pay off other claimants, often resulting in similarly heavy debt burden on the land and discouraging productive investments. While credit relations between relatives were widespread, their extent could vary greatly from region to region. Sheilagh Ogilvie, Markus Küpker and Janine Maegraith found for the town of Wildberg in Württemberg (nowadays Germany) during the seventeenth century that only about 22 per cent of all debts were owed to relatives.Footnote 59 Andreas Maisch has shown that in rural Württemberg in the early modern period, money lent to relatives accounted for up to 46 per cent, while debts owed to kin were between 10 and 16 per cent, comparable to Wildberg.Footnote 60 For the seigneurie of Florimont in southern Alsace (France) during the late eighteenth century, Elise Dermineur found that about 11 per cent of borrowing took place within the same family.Footnote 61 On the other hand, B. A. Holderness concluded that relatives accounted for up to 40 per cent of creditors in early modern Lincolnshire (England).Footnote 62

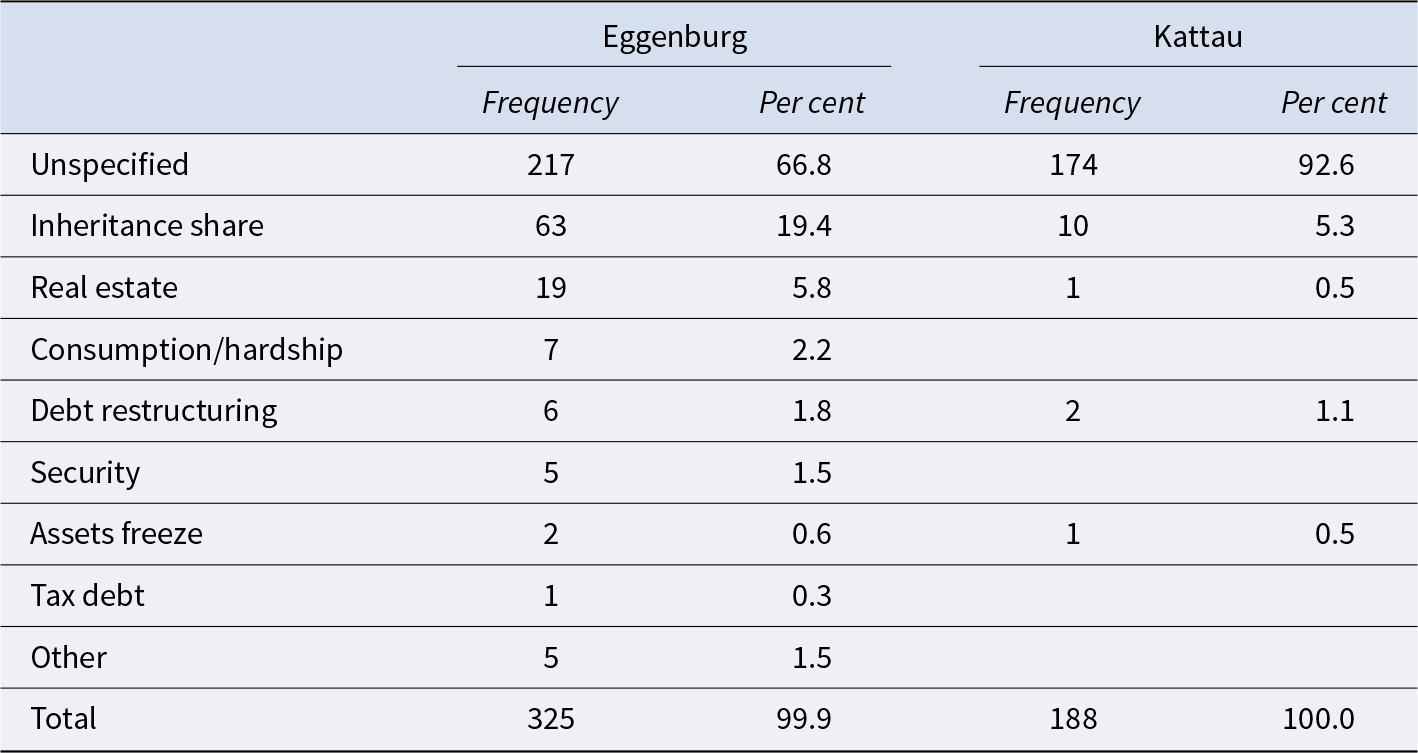

Historians have identified a number of common reasons for borrowing, including the payment of rents and taxes, wages for workers, the purchase of land, business and consumption expenses, compensation for ceding heirs or as a result of crises such as crop failures, epidemics and wars.Footnote 63 In most sources, these specific reasons are often difficult to discern as it is not always clear what a sum of money borrowed was used for. In some cases, however, the mortgage books do provide information that makes it possible to identify the reasons for borrowing and lending (Table 3).

Purpose of lending – 1725–1790

Source: Mortgage deeds – NÖLA, BG Eggenburg 04/05, Satzprotokoll 1734–1792; NÖLA, BG Eggenburg 11/08, Satzbuch 1740–1824.

For Kattau, this information is relatively sparse, with over 92 per cent of cases not specifying the reason for the debt, instead giving such general descriptions as ‘capital’ (Kapital), ‘money’ (Geld) or ‘cash’ (Bares Geld). The only other reason that could be reconstructed more than sporadically was outstanding inheritance shares in just over 5 per cent of cases. In Eggenburg, although the majority of mortgage deeds were similarly vague, about 30 per cent did state more specific purposes. Here, too, inheritance shares were the most important group with over 19 per cent. Other reasons were the purchase of real estate, the restructuring or transfer of debts and loans for consumption or to mitigate hardship. However, it is very likely that many of the debts in the unspecified category were also used to purchase land or for consumption in times of economic distress, which ultimately makes it difficult to comment on its relative importance.

It is necessary, however, to take a closer look at the largest group and to clarify what is meant by ‘inheritance shares’. These were not payments of money, but relationships of indebtedness that arose from the inheritance practices and marital property regime in Lower Austria. In this region, husband and wife typically owned their property jointly as a community of property. This meant that they were legally equal co-owners of most, if not all, of the possessions they owned. On the death of one of them, between half and two-thirds of these assets went to the surviving spouse, with only the remainder going to the actual heirs, often the children. However, since the widow or widower was usually entitled to the largest share of the estate and since succession in Lower Austria was usually undivided, they typically took over the entire estate. The inheritance shares of the children of the deceased remained, in this very common scenario, as a debt secured on the house or the farm. These debts usually only began to accrue interest once the children reached adulthood, left home or married. When they were still dependent children in the household, the cost of their upbringing was considered as interest. A similar scenario could arise if children inherited a house or a farm from their parents, in which case they usually had to pay off their siblings, often on a deferred basis. However, such cases were not very numerous as the preferred mode of property transmission was inter vivos, similar to the context described by Hermann Zeitlhofer for southern Bohemia.Footnote 64 While these debts were of social rather than economic origin, they also dictated the ways in which the property could be used. A property that was already overburdened with debts to kin as a result of succession practices was of limited use in acquiring further credit for other things, such as productive investment.Footnote 65

Information about kinship in our sample can often be deduced from the sources themselves, or by linking them to other evidence such as parish records or purchase contracts (Table 4). Such information is necessarily incomplete in the absence of a full family reconstitution, but can highlight some of the patterns of kinship credit that exist.Footnote 66 An important marker of kinship was the surnames adopted by wives from their husbands on marriage. Where it was not possible to discern the exact relationship between two persons, but they shared the same surname, we also recorded this as a marker for high probability of relatedness. Thus, in almost 22 per cent of cases in Eggenburg and over 16 per cent in Kattau, some kind of kinship between creditor and debtor could be identified. In the latter case, the majority could not be specifically identified. The rest consisted of constellations with parents or at least one step-parent. Groups of debtors with at least one step-parent made up the majority of the identifiable relationships in Eggenburg, followed by biological parents. Some were non-specifiable relationships and others were debts between siblings or from children to their parents.

Kinship relations of debtors – 1725–1790

* Step-parent here means that there was at least one step-parent, often together with a biological parent.

Source: Mortgage deeds – NÖLA, BG Eggenburg 04/05, Satzprotokoll 1734–1792; NÖLA, BG Eggenburg 11/08, Satzbuch 1740–1824.

If we look at the specific purposes of loans between relatives in Table 5, we can see that the vast majority of these were for inheritance shares. A number of debts were for unspecified sums of money, but some of these debts could also have been for inheritance shares.Footnote 67 The frequency with which stepfathers were involved in debts specifying inheritance shares is particularly striking. Among debts for inheritance shares between relatives, stepfathers were debtors in more than 34 per cent of cases, whereas stepmothers were present in only about 27 per cent of cases. Similarly, mothers were debtors in 57 per cent of such cases and fathers in 28 per cent. The constellation of mothers and stepfathers was more often found in mortgage deeds than that of fathers and stepmothers.

Purpose of lending among relatives – 1725–1790

Source: Mortgage deeds – NÖLA, BG Eggenburg 04/05, Satzprotokoll 1734–1792; NÖLA, BG Eggenburg 11/08, Satzbuch 1740–1824.

These cases illustrate that kinship could be a facilitator of trust, but also had the potential for competing claims, interests and disputes. The strong presence of step-families, especially in constellations of biological mothers and stepfathers, indicates that such situations were seen as particularly in need of regulation and protection, and thus frequently found their way into mortgage deeds. The Guardianship Regulation of 1669 decreed that widowed women, in contrast to men, lost supreme guardianship over their children when they remarried. Thus, the law suspected women in particular of neglecting their children’s best interests in favour of their new husbands and stepfathers, who might jeopardize the claims of their stepchildren.Footnote 68 This observation fits into a broader European pattern of distrust of remarried parents and step-parents, reflected in the law and in legal practice, but also present in the common trope of the ‘evil stepmother’.Footnote 69

In the context of marital community of property, as was common in Lower Austria, there was indeed a potential tension between the inheritance claims of children from previous marriages and the continued power of disposition over the household assets of the surviving parent and the new stepmother or stepfather.Footnote 70 In areas with separation of marital property, the matrimonial property law provided a better protection for the assets of half-orphans.Footnote 71 In Lower Austria, claims of heirs were especially vulnerable where step-parents brought only little wealth into the marriage.Footnote 72 If, for example, a poorer man married a wealthier widow, the marital fund from which her children’s inheritance would be calculated was diminished by being divided between two people. Formalized securitization through mortgages mitigated this tension by securing the children’s claim on the paternal inheritance. This specific constellation is also reflected in the higher number of mothers/stepfathers being debtors than fathers/stepmothers.

Another strategy sometimes used in Lower Austria to ensure equity between children from different marriages was the so-called Einkindschaft (from German ‘ein Kind’ – ‘one child’), which was also found in other European regions in similar form. In this ‘one-child’ union, occasionally found in marriage contracts, children from previous marriages waived their claims to the inheritance of their deceased parent in favour of their new step-parent. In return, they acquired a claim to the inheritance of the second spouse, effectively giving children from both first and second marriages equal inheritance rights. Similarly, children from a previous marriage could be given by a groom to his new bride as a Morgengabe (‘morning gift’), who effectively adopted them as her own.Footnote 73 As Gertrude Langer-Ostrawsky has pointed out, this could indeed be equivalent to a material morning gift, as the new wife’s access to her husband’s property was not diminished by the child’s inheritance claims, and she could even inherit from the child should it die before her.Footnote 74 Furthermore, this construction could ease the financial burden on the husband by postponing the payment to the child until a later date. However, the processes of legal codification, culminating in the Codex Theresianus of 1766, attempted to move away from both Einkindschaft and Morgengabskinder, eventually abolishing the institution in the Allgemeines Bürgerliches Gesetzbuch (Austrian Civil Code) of 1811.

5. Credit networks

While credit relations have long been described as networks, it is only in recent years that historians have started to use the formal methods of social network analysis (SNA) as a tool for analysing them.Footnote 75 Social network analysis can help us look at credit relationships not only in isolation or as aggregates but also to establish connections between observations and the structures of those relationships. As such, it is ideally suited to the study of credit networks. In particular, our mortgage book data are well suited to such a study as they contain information on both debtor(s) and creditor(s) as well as some more contextual information that allows us to identify and distinguish specific individuals in our database. In SNA terminology, individual people or institutions are nodes and their credit relations form the edges between them. Since debts are asymmetrical in nature, it makes sense to model the graph as a directed network, with edges running from creditors to debtors, parallel to the flow of money or other assets they often represent.

Figure 3 shows a graph of the (mortgage) credit networks in both Eggenburg and Kattau. Owing to their highly localized nature, they are mostly separate entities. At first glance the graph suggests that institutions were very well connected and acted as central creditors. The size of the nodes reflects their out-degree, here the number of loans granted. Especially the municipal hospital (Bürgerspital) in Eggenburg, the parish church in Kattau and the orphans’ fund (Waisenkasse) were major lenders. However, it also seems that certain orphan creditors, especially in Eggenburg, were very well connected. Comparing the two parts, it seems that credit relations in Kattau were much more centred on the two institutional creditors, which probably became even more pronounced later, as the Waisenkasse was only introduced around 1765 and subsequently subsumed all orphan credit. In Eggenburg, the credit network seems to have been more complex and multi-centred. In both places, however, there were many isolated components that were not connected to the wider network through mortgage credit (albeit possibly through more informal means).

Credit network in Eggenburg and Kattau – 1725–1790.

We can test some of these findings using different metrics (Table 6). Degree tells us how many connections a node (here: a person or institution) has had. It is possible to further break this down into in-degree (incoming connections – here: number of credits borrowed) and out-degree (outgoing connections – here: number of credits lent). Looking at the averages for the three categories established earlier, a clear picture emerges. Institutions were much better connected than both private individuals and orphans, with degrees ranging from 10.7 to 21.3, all of which came from outward connections. Institutions did not borrow here – at least not in a way that was reflected in the sources used.Footnote 76 Orphans almost never borrowed either.

Node metrics (mean of values > 0)

Source: Mortgage deeds – NÖLA, BG Eggenburg 04/05, Satzprotokoll 1734–1792; NÖLA, BG Eggenburg 11/08, Satzbuch 1740–1824.

To get a more nuanced view of the position of individuals in these networks, we can use the metric of eigenvector centrality, which considers not only their direct connections but also how well these were connected in an iterative process where ‘a high score means that an actor is connected to many nodes that also have high scores’.Footnote 77 Thus, it can give us a measure of a node’s embeddedness in a network that goes beyond its direct links. By looking at how well connected a node’s connection is, we can more meaningfully gauge the density of its personal network. Again, we see that institutions were better connected than both individuals and orphans. In Eggenburg, orphans and individuals were roughly similar in terms of eigenvector centrality, whereas in Kattau orphans were less well connected.

A similar picture emerges when looking at the top ten creditors by out-degree (Tables 7 and 8) and debtors by in-degree (Tables 9 and 10). In both Eggenburg and Kattau, the most active lenders over the whole period were institutions (partly owing to their theoretically unlimited lifespan). However, there were also a number of orphans with a high level of outgoing debt, while private persons were completely absent. In contrast, all of the nodes with the highest debts incurred were private adult individuals. It is noteworthy that for both categories, the number of debts per person and the eigenvector centrality were lower in Kattau than in Eggenburg, suggesting an overall less dense credit network in the more rural community.

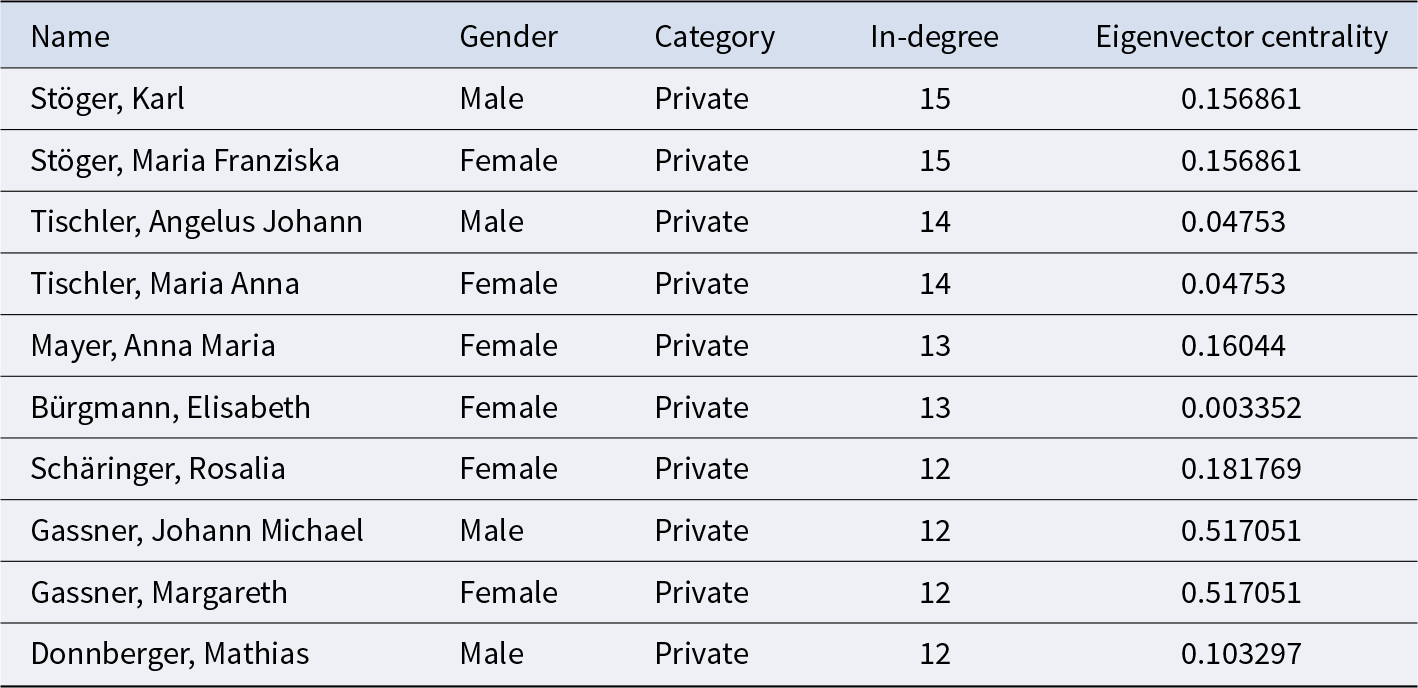

Eggenburg: top ten creditors by out-degree – 1725–1790

Source: Mortgage deeds – NÖLA, BG Eggenburg 04/05, Satzprotokoll 1734–1792.

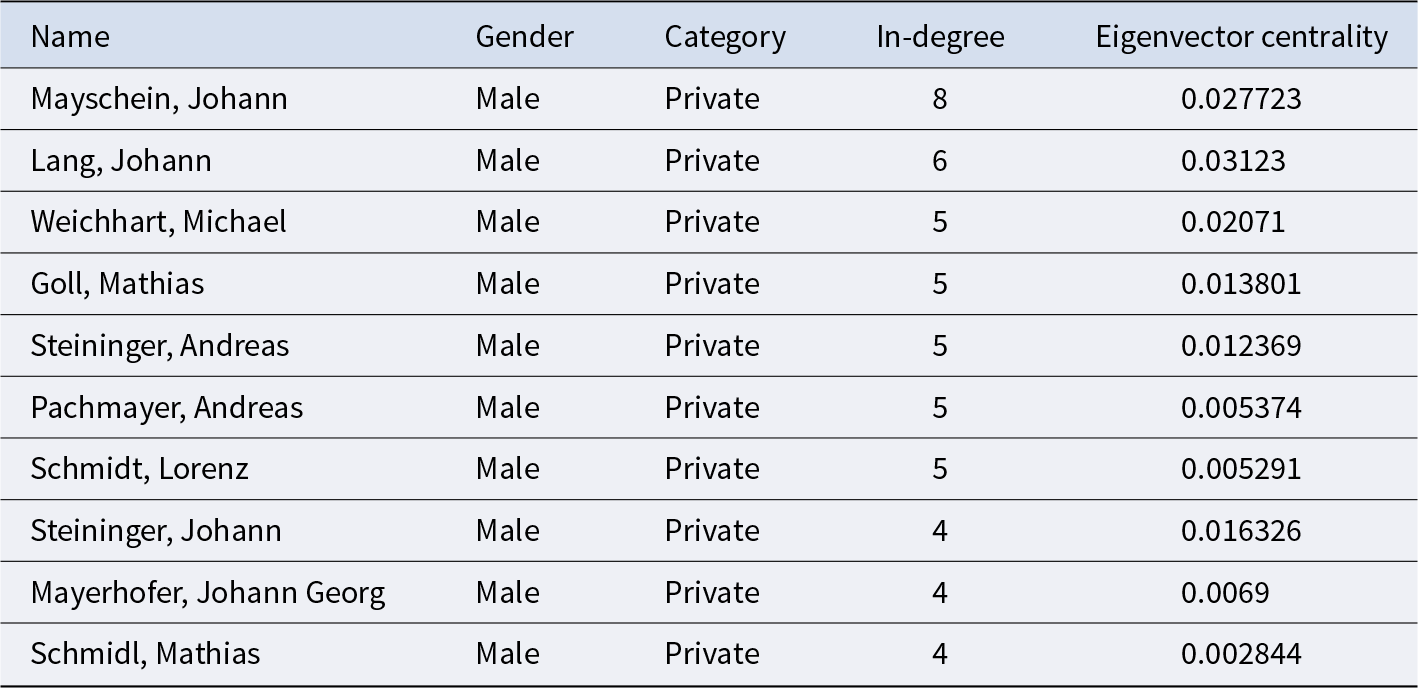

Kattau: top ten creditors by out-degree – 1725–1790

Source: Mortgage deeds – NÖLA, BG Eggenburg 11/08, Satzbuch 1740–1824.

Eggenburg: top ten debtors by in-degree – 1725–1790

Source: Mortgage deeds – NÖLA, BG Eggenburg 04/05, Satzprotokoll 1734–1792.

Kattau: top ten debtors by in-degree – 1725–1790

Source: Mortgage deeds – NÖLA, BG Eggenburg 11/08, Satzbuch 1740–1824.

In both places the top creditors had a higher degree than the top debtors, suggesting a limit to the amount of credit that could be mobilized with limited property, while a much higher number of loans could be granted if sufficient funds were available. Both the Brandstetter and the Apfeltaler children were among the creditors with the most loans extended. As we have seen, it was possible (and often advantageous) for orphans to have almost all of their wealth invested in interest-bearing loans, while most adults had to have a substantial part of their capital tied up in productive assets such as land, buildings, tools, materials or merchandise and household movables. Thus, the liquidation of orphans’ assets provided a substantial influx of capital into local credit markets, and at the same time mobilized land (a topic beyond the scope of this article), with a potentially stimulating effect on the local economy.

6. Conclusion

Authors such as David Sabean and Giovanni Levi have questioned the strong distinction between the family and the market. Transactions between family members were often remunerated and valued in monetary terms, but they did not usually follow a market logic.Footnote 78 Instead, mutual obligations and reciprocity were central. While Sabean and others were primarily concerned with property and labour, we have shown that a similar logic holds true for debt and credit in terms of transactions. Local debt relations and credit markets were intertwined with systems of intergenerational property transmission and demographic events.

In Lower Austria, debts in connection with inheritance and succession were particularly noteworthy. On the one hand, a large number of debts was generated as a result of death and remarriage in combination with the common practice of marital community of property and succession by the spouse. These were the result not of a credit market in the narrower sense but of a transfer of wealth as a purely accounting process. Nevertheless, this undoubtedly had an impact on the market by limiting the possibility of generating further credit for other purposes.

On the other hand, the administration of orphans’ wealth mobilized a supply of relatively cheap, accessible and secure credit that could provide liquidity in an economic environment of limited financial markets. In both Eggenburg and Kattau, credit provided by orphans was larger both in number of debts and by monetary volume than that extended by either institutional or private lenders. Wealthy orphans were important, well-connected local suppliers of credit and often earnt a substantial return on their assets. Our network analysis has shown that they were more active lenders in the mortgage credit markets than adult lenders and competing institutions as sources of capital. We have shown that institutions that were not primarily financial, such as the orphans’ funds but also hospitals and parish churches, were central players in the local credit markets of Lower Austria and need to be taken seriously. Guardians, who often belonged to the local elite, and their social and professional networks probably played a crucial role as intermediaries, but further research on their concrete activities is needed. Such contexts, which were often very specific regionally and even locally, shaped the functioning of these markets and thus economic activity.

Funding

This research was funded in whole or in part by the Austrian Science Fund (FWF) 10.55776/P33348.

Competing interests

The author declares none.

Open access

Open access