[I]t can be challenging for investors to consider how to adopt their stewardship practices to include fixed income… Yet in many areas of corporate governance, there can be a significant alignment of interest that supports engagement on behalf of all financial stakeholders, both creditors and shareholders. (George S. Dallas, Policy Director at International Corporate Governance Network, 2019)

I. Introduction

The increasing size of institutional investors, who now hold around 70% of public U.S. firms’ outstanding equity, raises questions about whether they are effective stewards for equity investors. For example, the three largest mutual fund families in total net assets (Vanguard, Fidelity, and BlackRock) hold equity positions in around 5,000 U.S. companies, casting doubt on their ability to monitor every company in their massive portfolios. Because these institutions can be influential (e.g., Appel, Gormley, and Keim (Reference Appel, Gormley and Keim2016), Gormley, Gupta, Matsa, Mortal, and Yang (Reference Gormley, Gupta, Matsa, Mortal and Yang2023)), it is essential to understand when they will be attentive owners and engaged stewards. However, the factors that affect institutional investors’ stewardship activities are poorly understood, including whether institutional investors prioritize overall portfolio returns or the returns for individual holdings (e.g., Matvos and Ostrovsky (Reference Matvos and Ostrovsky2008), Harford, Jenter, and Li (Reference Harford, Jenter and Li2011)). This article analyzes whether institutions’ corporate bond holdings affect how actively they monitor their equity positions.

Institutions offer various mutual fund and exchange-traded fund (ETF) options to investors (e.g., equity-only, bond-only, and mixed-asset), and corporate bond holdings often comprise a significant component of institutional investors’ holdings. For example, at the end of 2020, one-fourth of U.S. mutual funds and ETFs held corporate bonds, with more than half of those funds holding both equity and bonds. Moreover, 36.2% of institutions casting votes on contentious shareholder proposals between 2008 and 2020 also held a bond position in the underlying firm. That bond position accounted for, on average, 28.9% of the institution’s exposure to the firm.

Despite corporate bonds’ economic importance for institutional investors, the study of factors motivating institutional investors’ stewardship activities often ignores their bond positions. For example, proposed measures of institutional investors’ incentive to be engaged stewards tend to focus solely on institutions’ equity holdings (e.g., Chen, Harford, and Li (Reference Chen, Harford and Li2007), Fich, Harford, and Tran (Reference Fich, Harford and Tran2015), and Lewellen and Lewellen (Reference Lewellen and Lewellen2022)). And when considered, the potential importance of institutions’ bond positions is often limited to their ability to create conflicts of interest (e.g., Keswani, Tran, and Volpin (Reference Keswani, Tran and Volpin2021)).

However, there are several reasons why bond holdings might affect how actively institutions vote and monitor their equity positions, and in ways that do not necessarily conflict with shareholders’ interests. First, there are many situations where being an engaged steward can be value-enhancing for both holdings. Hence, institutions with a bond position will have a greater monitoring motive, all else equal, because engagements that improve a firm’s fundamental value will improve the value of both its bonds and equity. Second, bondholders have incentives to encourage active voting by their equity counterparts. Bond holdings are more sensitive to long-term viability risks and harder to exit, thus increasing the importance of direct engagement.Footnote 1 Third, fixed-income managers do research on companies’ default risk. If this research is shared internally within the fund family and is complementary to research conducted by equity funds, it could affect which equity positions the institution pays more attention to when voting shares.Footnote 2

On the other hand, there are also reasons why corporate bond holdings might not affect or even be detrimental to institutions’ stewardship activities. Institutions’ fiduciary duty to represent equity investors’ interests when voting their stocks could limit the extent to which institutions allow managers with a bond holding (and, hence, a potentially conflicting interest) to influence their stewardship decisions. Bond holdings could even weaken equity stewardship if fixed-income managers push their institutions to promote creditors’ interests over those of shareholders.

To assess the potential importance of bond holdings for investors’ monitoring activities, we analyze whether the size of an institution’s bond position predicts greater investor attention, which can indicate active monitoring. We start by constructing a proposal-by-institution-level data set of how institutions voted on every proposal from January 2008 to June 2020 and pair this data with institutions’ aggregated holdings at the time of the vote. We then regress a proposal-level, vote-based measure of investor attention onto the share of the fund family’s total net assets (TNA) held in that company’s bonds. Following Iliev and Lowry (Reference Iliev and Lowry2015) and Gilje, Gormley, and Levit (Reference Gilje, Gormley and Levit2020), we proxy for an institution’s attention using votes that go against the recommendation of the proxy advisory firm Institutional Shareholder Services (ISS). This investor attention proxy is theoretically motivated (Malenko, Malenko, and Spatt (Reference Malenko, Malenko and Spatt2025)), and the underlying premise is that all else equal, attentive investors are less likely to rubber-stamp ISS recommendations. Past empirical work also confirms that voting against ISS is more likely to occur among institutional investors with greater net benefits from being attentive and engaged (Iliev and Lowry (Reference Iliev and Lowry2015)).

To mitigate concerns about portfolio weights’ endogeneity, we partial out potential confounding factors that might drive differences in attention at the investor or proposal level. Specifically, we include proposal-level fixed effects in each estimation. The proposal-level fixed effects control for any proposal-level characteristics that could affect institutions’ likelihood of following ISS, including the proposal’s type and content. The proposal fixed effects also control for any firm characteristics (e.g., profitability, size, and takeover vulnerability) at the time of the vote that might matter for how institutions vote. We also include institution-by-month fixed effects to control for each institution’s overall tendency to follow ISS and the possibility that this might vary over time. In other words, we only use variation in how an institution voted across proposals each month as a function of how extensive its bond position was in each company.

Using this within-proposal and within-institution-by-month variation in votes, we find a positive association between an institution’s bond position size and the likelihood it does not follow the ISS recommendation when voting its shares. The positive association is robust to controlling for the overall importance of the institution’s equity position in that company, which also positively predicts voting against ISS (e.g., Fich et al. (Reference Fich, Harford and Tran2015), Iliev and Lowry (Reference Iliev and Lowry2015), and Gilje et al. (Reference Gilje, Gormley and Levit2020)). The association also holds for “The Big Three” indexers (BlackRock, State Street, and Vanguard), suggesting that self-selection issues are unlikely to explain the finding, given these institutions’ passive investment mandates and more limited ability to choose which stocks and bonds to hold. Moreover, the association between bond holdings and voting is economically important and similar in magnitude to that observed for equity holdings. A 1-standard-deviation increase in a bond’s share of total net assets predicts a 0.62 percentage point increase in the likelihood that the institution votes against the ISS recommendation.

We next construct an alternative proxy for investor attention, whether a fund family accesses a company’s proxy filings via EDGAR in the days before a shareholder meeting. Following Iliev, Kalodimos, and Lowry (Reference Iliev, Kalodimos and Lowry2021), we construct this governance research measure by matching the IP addresses accessing each filing on EDGAR to individual fund families. To proxy for investor attention, we create an indicator that flags whether the institution downloaded a company’s filings from 30 days before the proxy statement release and continuing through the shareholder meeting date. Iliev et al. (Reference Iliev, Kalodimos and Lowry2021) show that such downloads predict more informed voting and are more likely to occur among institutions where the value of being attentive is greater.

Providing further evidence that bond holdings might influence a fund family’s attention level, the size of an institution’s bond holdings positively predicts whether the institution views a company’s proxy filings before voting. The association is robust to controlling for the size of the institution’s equity position, meeting-level fixed effects, and institution-by-month fixed effects. The meeting-level fixed effects control for any firm characteristics at the meeting time that might affect how much research institutions conduct, and the continued inclusion of institution-by-month fixed effects controls for each institution’s overall tendency to access EDGAR filings that month. In other words, our estimates show that, within the given month, an institution is more likely to download filings before voting at companies where they hold a larger bond position. Estimates are also similar in magnitude to what we observe when using our vote-based attention proxy. A 1-standard-deviation increase in a bond’s share of total net assets is associated with a 0.26 percentage point increase in the likelihood of accessing the company’s proxy filing.

The observed association between bond holdings and voting also varies across funds in ways consistent with the influence of bond holdings on institutional investors’ attention. The positive association between portfolio weights and investor attention concentrates on bonds held in actively managed funds, where monitoring is more likely to occur (e.g., Brav, Jiang, Li, and Pinnington (Reference Brav, Jiang, Li and Pinnington2020), Iliev et al. (Reference Iliev, Kalodimos and Lowry2021)). Bonds held in mixed-asset funds are also more likely to predict institutional investors’ voting patterns. This finding is consistent with the argument that fixed-income managers’ engagement is more significant when they can leverage an equity position to exert influence (Phillips (Reference Phillips2020)). However, there is suggestive evidence that equity-only funds are also less likely to follow ISS recommendations when the institution has bond holdings in that same company, suggesting that cross-fund bond holdings also contribute to institutions’ overall engagement. Fund-level analysis confirms the importance of both within-fund and cross-fund bond holdings. Individual funds are less likely to follow ISS vote recommendations both when the fund itself holds the company’s bonds and when other funds within the larger fund family hold them.

Significantly, shareholder–creditor conflicts arising from institutions’ dual holdings do not drive our findings. The association between bond holdings and voting patterns remains unchanged when excluding firms in financial distress, where a wedge between shareholders’ and creditors’ interests is more likely. Nor do we find evidence that the association focuses only on firms with high expected default risk. Instead, the association concentrates on institutions’ investment-grade bond holdings, where default risk is low. Our findings also hold for a subset of proposals where creditor–shareholder conflicts are unlikely to be relevant. Shareholder–creditor conflicts also do not explain our findings regarding institutions’ governance research, as measured using EDGAR viewings. Our findings also hold for both highly levered and less levered firms, suggesting that they are not driven by more intense investor monitoring of levered firms (e.g., Iliev et al. (Reference Iliev, Kalodimos and Lowry2021)). Overall, the evidence suggests that bond holdings affect institutional investors’ activities more systematically than previously known. This potential influence likely reflects the alignment of interests among all financial stakeholders in many types of investor engagement.

These findings have important implications for corporate governance and the monitoring of companies. Institutional investors are not fully attentive (e.g., Fang, Peress, and Zheng (Reference Fang, Peress and Zheng2014), Lu, Ray, and Teo (Reference Lu, Ray and Teo2016), Ben-Rephael, Da, and Israelsen (Reference Ben-Rephael, Da and Israelsen2017), and Schmidt (Reference Schmidt2019)), particularly when it comes to their smaller equity positions (Fich et al. (Reference Fich, Harford and Tran2015), Iliev and Lowry (Reference Iliev and Lowry2015), and Iliev et al. (Reference Iliev, Kalodimos and Lowry2021)). This lack of attention affects managers’ incentives and destroys shareholder value (e.g., Kempf, Manconi, and Spalt (Reference Kempf, Manconi and Spalt2017), Liu, Low, Masulis, and Zhang (Reference Liu, Low, Masulis and Zhang2020), and Gilje et al. (Reference Gilje, Gormley and Levit2020)). Given its importance, a better understanding of what drives investor attention is needed. Our findings show that corporate bond holdings predict greater investor attention. This finding suggests that institutional investors consider their overall economic exposure when deciding where to allocate attention and that institutions prioritize total portfolio returns rather than individual stock returns. The finding also suggests that the popularity of mixed-asset funds and institutions’ tendency to hold bond positions in companies can enhance investor stewardship.

Our findings also contribute to the nascent literature that quantifies institutions’ incentive to be engaged monitors. Existing estimates of institutions’ motive to be attentive consider the relative importance of equity investors’ time horizon, position size, and concentration (Chen et al. (Reference Chen, Harford and Li2007)), the share of an institution’s equity AUM at stake in the firm (Fich et al. (Reference Fich, Harford and Tran2015)), and how improvements in the equity position’s value will increase fund fees and flows (Lewellen and Lewellen (Reference Lewellen and Lewellen2022)). However, these existing measures ignore how active monitoring can also improve the value of institutions’ bond holdings, providing many institutions with an additional economic motive to be engaged owners. Our findings suggest that institutions’ combined debt and equity holdings should be accounted for when quantifying or proxying for institutions’ overall incentive to be engaged stewards. Our findings also suggest that the type of funds holding the position—actively managed versus indexed—likely matters for investors’ stewardship activities.

The findings also highlight a key distinction between measures of investors’ potential influence and measures of their economic exposure. Having significant exposure (e.g., a large share of AUM at stake in the firm) does not necessarily mean having much influence (e.g., being among the top 5 owners of the firm). However, both economic exposure and the ability to exert influence can motivate investor engagement (e.g., Chen et al. (Reference Chen, Harford and Li2007), Fich et al. (Reference Fich, Harford and Tran2015)). Since bond holdings do not provide direct voting power, our results confirm the independent importance of economic exposures. Moreover, we present evidence that an institution’s financial exposure predicts even greater engagement when the institution is also likely to be influential, suggesting a potential complementarity between these two distinct channels.

Finally, our results contribute to the ongoing discussion regarding creditor governance and the conflicting interests of institutions holding dual debt and equity positions. Debt and equity owners can have different views regarding the value implications of dividends, equity issuances, takeover defenses, and acquisitions, which could influence how an institution that holds debt and equity votes on specific proposals. Consistent with this possibility, evidence suggests that institutions holding both debt and equity in a firm vote differently on proposed mergers (Bodnaruk and Rossi (Reference Bodnaruk and Rossi2016)) and are more likely to cast creditor-friendly votes, especially when the firm is in financial distress (Keswani et al. (Reference Keswani, Tran and Volpin2021)). Instead, we analyze the importance of debt holdings for an institution’s overall likelihood of being an engaged monitor, which can positively influence the value of both debt and equity positions. We find evidence that these dual holdings influence institutions’ stewardship more generally and in ways that do not necessarily forgo equity investors’ interests, thus providing an essential complement to the existing work on creditor governance.Footnote 3 Our findings also provide additional evidence of an indirect mechanism by which creditor governance can operate that differs from the typical focus on debt covenants and bankruptcy.

We organize the article as follows: Section II describes our data. Section III presents our empirical specification, and Section IV reports our main findings. Section V analyzes heterogeneity in our main finding across firms and funds; Section VI examines alternative explanations; and Section VII conducts additional analyses and robustness tests. Section VIII concludes.

II. Data and Summary Statistics

To assess the association between an institution’s bond holdings and its level of attention to individual companies, we combine various data sets, including mutual funds’ holdings, mutual fund voting records, and SEC log files of institutions’ EDGAR downloads.

A. Mutual Fund Holdings Data

To calculate how significant each company’s equity or bonds are in a fund family’s overall portfolio, we use the CRSP Mutual Funds Database. The SEC requires mutual funds and exchange-traded funds (ETFs) to disclose their holdings quarterly during their fiscal year using Forms N-CSR and N-Q. Many funds, however, voluntarily report holdings on other dates as well.Footnote 4 We restrict our analysis to holdings starting in 2008 because the CRSP database contains inaccurate information before that year (Schwarz and Potter (Reference Schwarz and Potter2016)).Footnote 5

To analyze how holdings correlate with subsequent institution-level measures of attention, we aggregate security holdings to the institution (i.e., fund family) level for each month. To construct this monthly measure, we aggregate all the most recent fund reports of a particular institution going back 3 months. Because funds are required to report quarterly, this 3-month window will capture each fund’s holdings within the larger fund family.

To aggregate holdings to the institution level, we manually match funds to fund families using their fund name while accounting for subsidiaries within each institution. For example, Allianz purchased both Nicholas-Applegate Capital Management and Pacific Investment Management Company (PIMCO) in 2000, and in 2008, it invested $2.5 billion in Hartford Financial Services Group. Because our sample begins in 2008, we assign all funds with names containing “Allianz,” “Nicholas-Applegate,” “PIMCO,” and “Hartford” to the Allianz fund family. When aggregating to the institution level, we exclude positions with a negative value. Our subsequent findings are similar if we instead keep these negative positions or use their absolute value when aggregating. Finally, we use WRDS’s CUSIP-PERMCO link table to assign a PERMCO to each security in our sample, where each PERMCO identifies a unique firm.

Because the CRSP database does not directly flag whether reported securities are bonds, we classify securities as bonds using two methods. First, we classify securities that report a value in the “Date of Bond Maturity” field as bonds. Because this field is missing for some bonds, we also flag a security as a bond if the security’s name includes a “%”, “.”, “-”, “/”, or any number. These symbols and numbers appear in a security name for bonds to indicate a maturity date and yield rate. For example: “RAYTHEON CO., 7.20%, 8-15-2027” has a blank maturity date in CRSP but refers to Raytheon’s 7.2% domestic bond expiring in 2027. We classify all other securities as “equity,” and a manual review of the resulting security classifications confirms that this approach accurately flags bond and equity securities. Because every security in our sample must have a CUSIP-PERMCO link, funds’ cash holdings are not included in our subsequent analysis.

Bond holdings comprise a sizable component of institutions’ portfolios. In June 2020, mutual fund families held about $1.35 trillion in corporate bonds, accounting for 10% of their total net assets.Footnote 6 Figure 1 provides a breakdown of bond holdings across fund families. Of this $1.35 trillion, Vanguard held $357 billion, while BlackRock held $161 billion.

Figure 1 plots the corporate bond holdings of the top 8 fund families in June 2020. The number next to the fund family indicates corporate bond holdings in USD billion. Total corporate bond holding by mutual fund institutions is annotated in the center.

There is also considerable variation in the importance of corporate bond holdings across fund families. Table 1, which provides a breakdown between equity and corporate bonds for some of the most prominent mutual fund families, shows this variation. For example, after excluding government bond holdings, 16.8% of Prudential’s $218 billion in assets is held in corporate bonds, compared to just 3.5% of T Rowe Price’s $474 billion in assets. There is also variation in bond holdings among The Big Three indexers. For example, BlackRock holds 13.2% of its assets in corporate bonds, while corporate bonds only account for 4.0% of State Street’s assets.

Fund-level summary statistics also show the importance of bonds for mutual fund families. Most fund families offer a range of funds, including equity-only, bond-only, and mixed-asset, which hold both debt and equity securities. Table 2, columns 1–3 provides a yearly breakdown of such funds. While bond-only funds accounted for 6% of funds in 2008, they have grown in popularity, accounting for 12% of funds by 2020. Mixed-asset funds are also relatively common, accounting for 9%–21% of mutual funds and ETFs per year between 2008 and 2020. Moreover, corporate bond holdings are an important component of mixed-asset funds. In 2020, mixed-asset funds held 50% of their assets in corporate bonds (column 4). On average, about 56%–66% of a fund family’s corporate bond holdings each year are held in mixed-asset funds (column 5).

B. Mutual Fund Voting Data

We use the ISS Voting Analytics data set to analyze how institutions’ votes vary as a function of their bond holdings. The database includes fund voting records obtained from the mandated N-PX forms that institutions file with the SEC every year. While the voting records are available from July 2003 to June 2020, we start our sample in 2008 to match the time for which we have fund holdings data and to match when the coverage of Voting Analytics is better. Before 2007, ISS collected voting records only for the top 100 fund families, but after 2007, it collected records for the top 300 (Brav et al. (Reference Brav, Jiang, Li and Pinnington2020)). The ISS data also include a description of each proposal and the ISS recommendation on how investors should vote.

For our analysis, we follow Iliev and Lowry (Reference Iliev and Lowry2015), Gilje et al. (Reference Gilje, Gormley and Levit2020), and Gormley, Jha, and Wang (Reference Gormley, Jha and Wang2024), focusing on shareholder-sponsored proposals. During our sample, there were 11,523 proposals sponsored by shareholders, and of these, 5,944 (or 51.6%) were contentious, as defined by when ISS and management gave conflicting vote recommendations. We exclude non-contentious proposals because they are typically not well-thought-out (Gantchev and Giannetti (Reference Gantchev and Giannetti2020)) and because investors do not appear to focus on them (Iliev et al. (Reference Iliev, Kalodimos and Lowry2021)). A similar logic applies to excluding management proposals, which are primarily perfunctory and less revealing about investor attention (Iliev and Lowry (Reference Iliev and Lowry2015), Gilje et al. (Reference Gilje, Gormley and Levit2020)). However, in subsequent analysis, we also provide evidence on how institutions’ bond holdings correlate with their votes on say-on-pay and management proposals that are less likely to be perfunctory.Footnote 7

We aggregate the fund-level votes to the institution (i.e., fund family) level using the same approach to aggregate mutual fund holdings and then merge the voting data with the holdings data. When merging the holdings data for each proposal-by-institution observation, we use the aggregated holdings across all the most recent fund reports of the institution in the 3 months before the proposal vote. After this merger, we have 373 unique institutions in our sample, and, on average, 55 institutions and their funds cast votes for each proposal. In total, our sample includes 327,266 proposal-by-institution observations across 13 years.

We follow Iliev and Lowry (Reference Iliev and Lowry2015) and proxy for investor attention using an indicator for whether an institution’s votes on a proposal fail to follow the ISS recommendations. Iliev and Lowry (Reference Iliev and Lowry2015) and Malenko and Malenko (Reference Malenko and Malenko2019) posit that if fund families devote more resources toward becoming informed, they will be less likely to follow proxy advisory firm recommendations indiscriminately. Malenko et al. (Reference Malenko, Malenko and Spatt2025) also show that voting against ISS is the equilibrium outcome for more attentive investors when ISS uses its vote recommendations to create controversy. Consistent with this possibility, Iliev and Lowry (Reference Iliev and Lowry2015) observe a greater likelihood of disagreeing with ISS for mutual funds where the net benefits of being attentive are greater. Moreover, Iliev et al. (Reference Iliev, Kalodimos and Lowry2021) find that this voting behavior positively correlates with an institutional investor becoming informed before a vote.Footnote 8

To create a proposal-by-institution voting measure of investor attention, we calculate the share of an institution’s funds that do not follow the ISS recommendation, Against ISS. We start by following Gilje et al. (Reference Gilje, Gormley and Levit2020) and code fund-by-proposal vote decisions of “Against,” “Abstain,” and “Withhold” as “Against,” and “For” as “For.” We then compare how each fund voted on the ISS recommendation of either “For” or “Against” and flag those where the fund did not follow the ISS recommendation. We then calculate Against ISS as the share of an institution’s funds that did not follow the ISS recommendation for that proposal. For 83.5% of our proposal-by-institution observations, Against ISS equals either zero or one, as most funds within a fund family vote in the same direction on individual proposals.Footnote 9

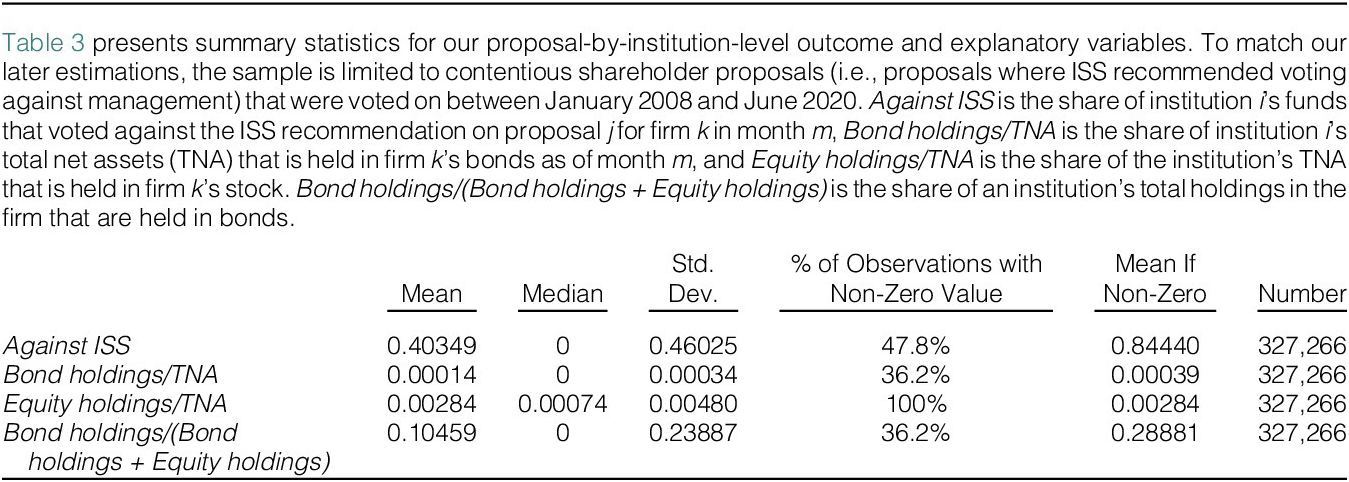

For the contentious shareholder proposals we analyze, there is considerable variation across institutions on whether they follow ISS. Table 3 provides summary statistics for our final proposal-by-institution sample. For an average proposal, 47.8% of institutions cast at least one vote that does not agree with ISS, and 40.4% of funds cast a vote that does not agree with ISS. While not tabulated, we find that the average likelihood of voting against ISS is considerably lower for management proposals (7.8%) and non-contentious shareholder proposals (10.5%), consistent with these excluded proposals being routine and less likely to require investors’ attention.

The summary statistics provided in Table 3 further highlight the potential importance of institutions’ bond holdings. In 36.2% of observations, the voting institution held a non-zero bond position in the company. On average, these bond holdings accounted for about 0.039% of the institution’s total net assets and 28.9% of its overall exposure to the firm.Footnote 10

C. Mutual Funds’ Accessing of Company Filings on EDGAR

As an additional proxy of investor attention, we use whether an institution accessed the company’s proxy filings before a shareholder meeting, which previous papers use as a measure for corporate governance research (e.g., see Loughran and McDonald (Reference Loughran and McDonald2017), Iliev et al. (Reference Iliev, Kalodimos and Lowry2021), and Bauguess, Cooney, and Hanley (Reference Bauguess, Cooney and Hanley2025)). We use the publicly available EDGAR log files to measure whether an institution accessed a company’s proxy filings. The SEC’s Division of Economic and Risk Analysis (DERA) assembles information on internet search traffic for EDGAR filings through SEC.gov, covering Feb. 14, 2003, through June 30, 2017, after which the SEC ceased providing log files. The log file contains the first three octets of the IP address accessing each filing and a time stamp on when the file was accessed. To assign these IPs to institutional investors, we use a linking table purchased from Digital Elements, an IP geolocational technology provider, containing names of the organizations registering each IP address as of Dec. 31, 2016. We then follow the approach recommended by Iliev et al. (Reference Iliev, Kalodimos and Lowry2021) to match these organization names to specific institutional investors. See the Appendix for details.

To create our second proxy for investor attention, we use an indicator for whether the institution accessed a prior or current proxy filing of the company in the days before the company’s shareholder meeting. Iliev et al. (Reference Iliev, Kalodimos and Lowry2021) show that such downloads predict more informed voting by the institution and that such downloads are more likely to occur among institutions where the value of being attentive is greater. We use accession numbers provided by the SEC to identify proxy filings, and our window includes the 30 days before the current proxy statement date and continues through the shareholder meeting date. Typically, proxy statements are released 45 days before the shareholder meeting, resulting in an average window of 75 days.

During our sample period, January 2008 to June 2017, we obtained log files for 41,996 shareholder meetings and identified 141 unique institutions. After limiting our sample to institutions with non-zero equity holdings on the meeting date, our final sample includes 1.22 million institution-by-meeting observations. On average, 8.5% of institutions with a non-zero equity position access a proxy filing before the shareholder meeting. The low percentage of institutions accessing proxy filings via EDGAR likely reflects some institutions’ use of other sources, like Bloomberg, Factset, and ISS, to access regulatory filings. For that reason, our later estimation strategy will only use within-institution variation in the accessing of filings via EDGAR. Institutions that do not use EDGAR and institutions we are unable to match to a block of IP addresses will not contribute to our subsequent point estimates.

III. Estimation Strategy

To analyze the association between an institution’s level of attention and the importance of a particular bond position in an institution’s overall portfolio, we start by estimating

$$ {\displaystyle \begin{array}{c}\hskip0.24em Against\;{ISS}_{ijkm}=\beta {\left(\frac{Bond\ holdings}{TNA}\right)}_{ikm}+\gamma {\left(\frac{Equity\ holdings}{TNA}\right)}_{ikm}\\ {}\hskip-10em +{\alpha}_j+{\delta}_{im}+{\varepsilon}_{ijkm},\end{array}} $$

$$ {\displaystyle \begin{array}{c}\hskip0.24em Against\;{ISS}_{ijkm}=\beta {\left(\frac{Bond\ holdings}{TNA}\right)}_{ikm}+\gamma {\left(\frac{Equity\ holdings}{TNA}\right)}_{ikm}\\ {}\hskip-10em +{\alpha}_j+{\delta}_{im}+{\varepsilon}_{ijkm},\end{array}} $$

where Against ISS is the share of institution i’s funds that voted against the ISS recommendation on proposal j for firm k in month m, Bond holdings/TNA and Equity holdings/TNA are the proportion of institution i’s total net assets (TNA) held in firm k’s bonds and equity as of month m,

$ \mathrm{and}\hskip0.45em {\alpha}_j $

and

$ \mathrm{and}\hskip0.45em {\alpha}_j $

and

$ {\delta}_{im} $

are proposal and institution-by-month fixed effects, respectively. To ensure outliers do not unduly influence our findings, we winsorize Bond holdings/TNA and Equity holdings/TNA at the 1% level.Footnote

11 Furthermore, to ease the estimates’ interpretation, we scale both variables (and subsequent explanatory variables) by their sample standard deviation. Thus, each variable’s coefficient reflects the change in the outcome for a 1-standard-deviation increase in that variable. Because the estimation errors,

$ {\delta}_{im} $

are proposal and institution-by-month fixed effects, respectively. To ensure outliers do not unduly influence our findings, we winsorize Bond holdings/TNA and Equity holdings/TNA at the 1% level.Footnote

11 Furthermore, to ease the estimates’ interpretation, we scale both variables (and subsequent explanatory variables) by their sample standard deviation. Thus, each variable’s coefficient reflects the change in the outcome for a 1-standard-deviation increase in that variable. Because the estimation errors,

$ \varepsilon $

, might exhibit serial correlation and be correlated within institutions and years, we double-cluster the standard errors at the institution and year level.

$ \varepsilon $

, might exhibit serial correlation and be correlated within institutions and years, we double-cluster the standard errors at the institution and year level.

Our main identification concern is that of omitted variables. Suppose Bond holdings/TNA correlates with proposal-, firm-, or institution-level characteristics that affect an institution’s likelihood of actively voting its shares (i.e., not blindly following the ISS recommendation). In that case, our estimate of interest,

$ \beta $

, could reflect these omitted variables rather than an effect of bond holdings on investor attention. For example, if institutions tend to hold larger bond positions in better-run companies and such companies are also those where institutions are more likely to vote against ISS recommendations, a positive correlation between Bond holdings/TNA and Against ISS could exist even if bond holdings do not affect institutions’ attention.

$ \beta $

, could reflect these omitted variables rather than an effect of bond holdings on investor attention. For example, if institutions tend to hold larger bond positions in better-run companies and such companies are also those where institutions are more likely to vote against ISS recommendations, a positive correlation between Bond holdings/TNA and Against ISS could exist even if bond holdings do not affect institutions’ attention.

However, including proposal and institution-by-month fixed effects allows us to control for a number of these potential omitted factors. The proposal-level fixed effects control for any proposal-level characteristics that could affect institutions’ likelihood of following ISS, including the proposal’s type and content. The proposal fixed effects also control for any firm characteristics (e.g., profitability, size, and takeover vulnerability) at the time of the vote that might matter for how institutions vote on a particular proposal. The institution-by-month fixed effects control for any differences in an institution’s overall tendency to be “pro-management” (e.g., Brav et al. (Reference Brav, Jiang, Li and Pinnington2020), Kedia, Starks, and Wang (Reference Kedia, Starks and Wang2020)), while allowing for this tendency to change over time. Hence, our coefficient of interest,

$ \beta $

, is identified using variation in how votes for a given proposal vary as a function of each institution’s bond holdings in each month. Institutions with no within-month variation in their tendency to follow ISS (e.g., institutions that always follow ISS or institutions that always vote for management) will not contribute to our estimates.

$ \beta $

, is identified using variation in how votes for a given proposal vary as a function of each institution’s bond holdings in each month. Institutions with no within-month variation in their tendency to follow ISS (e.g., institutions that always follow ISS or institutions that always vote for management) will not contribute to our estimates.

These fixed effects do not control for other factors that might exhibit cross-sectional variation across an institution’s holdings at a particular point in time, affect the likelihood of an institution voting against ISS, and correlate with Bond holdings/TNA. One possible such factor is how significant that firm’s equity is in the institution’s overall portfolio, which affects institutions’ attention (e.g., Fich et al. (Reference Fich, Harford and Tran2015), Iliev and Lowry (Reference Iliev and Lowry2015)) and could correlate with Bond holdings/TNA. For this reason, we also include the proportion of an institution i’s TNA held in firm k’s equity as of month m, Equity holdings/TNA, as an additional control.Footnote 12

IV. Baseline Results

This section analyzes the association between bond holdings and institutions’ voting using the specification in equation (1). We also test our findings’ robustness by using an alternative proxy for investor attention—whether an institution accesses the company’s proxy filings via EDGAR.

A. Voting Against ISS

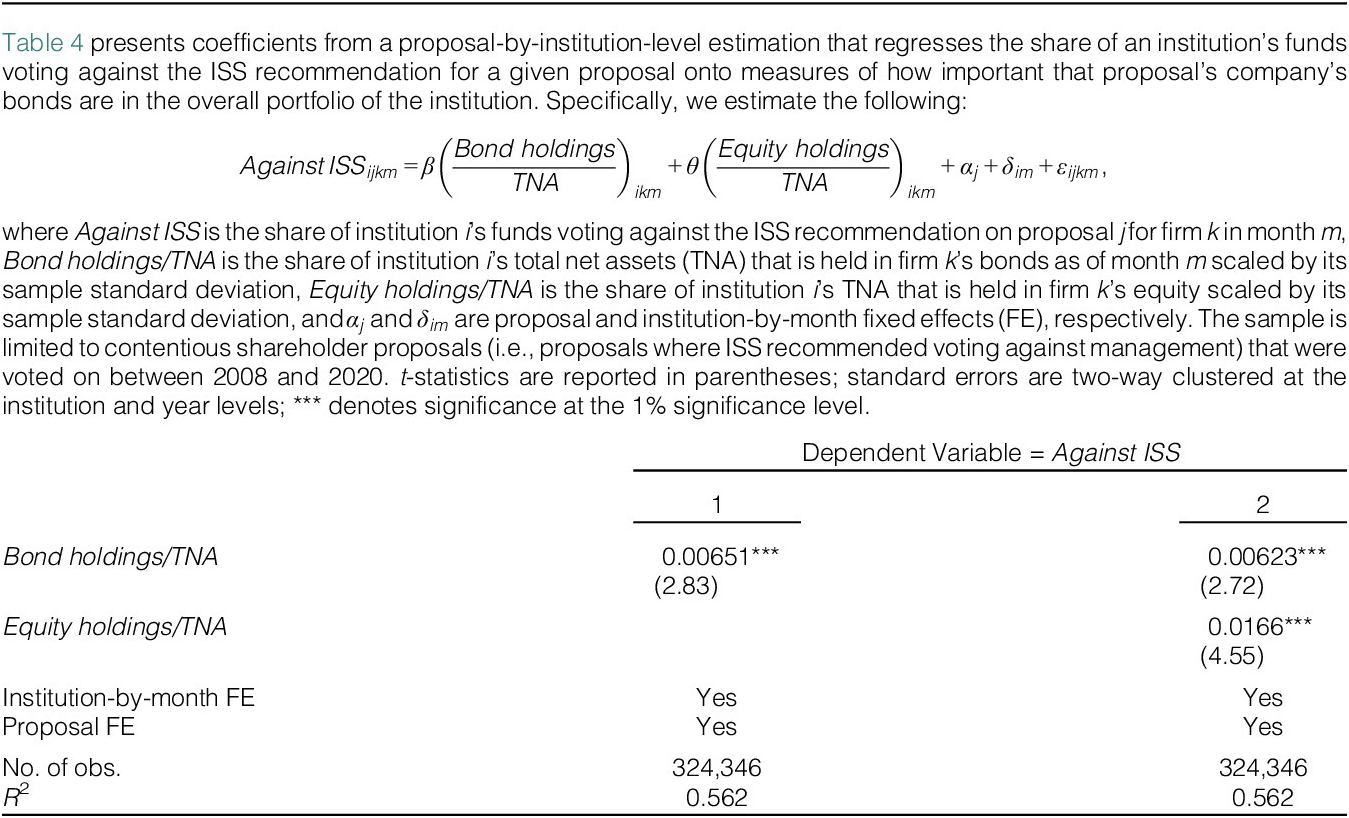

To assess how bond holdings might influence institutions’ level of attention, we start by estimating a version of equation (1) that excludes the Equity holdings/TNA control. This estimation determines the baseline association between an institution’s bond holdings in a company and the share of an institution’s funds that vote against ISS for a company’s proposals after controlling for proposal and institution-by-month fixed effects. Table 4, column 1 reports the findings.

We find that institutions where a firm’s bonds represent a larger proportion of their portfolio are more likely to vote against the ISS recommendation. Specifically, a 1-standard-deviation increase in the share of an institution’s portfolio held in a firm’s bonds (0.034%) is associated with a 0.651 percentage point increase in the likelihood of voting against ISS (Table 4, column 1). This estimate corresponds to a 1.41% increase relative to the sample standard deviation.

Like prior work analyzing how investors’ attention varies with their equity holdings, the positive association between bond holdings and institutions’ votes against ISS is concave. To illustrate this, we follow Gilje et al. (Reference Gilje, Gormley and Levit2020) and plot the point estimates from a regression of Against ISS onto dummy variables for each quintile of Bond holdings/TNA, proposal fixed effects, and institution-by-month fixed effects. Figure 2 reports the findings using a linear extrapolation between point estimates. The likelihood of voting against ISS increases with bond position size, particularly for increases within the lowest two quintiles of the overall distribution. However, the observed concavity indicates that the potential increase in attention per unit of bond holdings diminishes as the portfolio weight increases, especially for bond positions in the top quintile.

Figure 2 plots the point estimates from the proposal-by-institution-level regression of the share of an institution’s funds voting against the ISS recommendation for a given proposal, Against ISS, onto indicators for Bond holdings/TNA. The indicators are represented by five dummy variables, each assigned a value of 1 if the Bond holdings/TNA falls within the specific quintile range. The regression includes proposal and institution-by-month fixed effects, and a linear extrapolation is applied between point estimates to construct the figure, where Against ISS is centered at zero for Bond holdings/TNA = 0. The vertical lines indicate 95% confidence intervals.

The positive association between bond holdings and voting is robust to controlling for the proportion of institutions’ portfolios held in the firm’s equity (Table 4, column 2). Consistent with the prior literature, we find a positive association between the importance of a stock in an institution’s portfolio and the likelihood of that institution disagreeing with ISS (e.g., Iliev and Lowry (Reference Iliev and Lowry2015), Gilje et al. (Reference Gilje, Gormley and Levit2020)). A 1-standard-deviation increase in Equity holdings/TNA (0.48%) predicts a 1.66 percentage point increase in the likelihood of voting against ISS. However, the coefficient on Bond holdings/TNA remains mostly unchanged and is still statistically significant at the one percent level. In other words, after controlling for proposal and firm characteristics at the time of the vote (as done by including the proposal fixed effects), an institution’s overall tendency to disagree with ISS (as done by including institution-by-month fixed effects), and the institution’s equity position size, institutions are more likely to vote against ISS when that firm’s bonds represent a larger proportion of the institution’s portfolio.

The association between bond holdings and voting is also economically significant and similar in magnitude to that of equity holdings for comparable changes in institutions’ financial exposure to the firm. Controlling for Equity holdings/TNA, a 0.1 percentage point increase in a bond’s share of TNA is associated with a 1.8 percentage point increase in the share of an institution’s funds voting against ISS. Institutions are 0.4 percentage points more likely to vote against ISS for a comparable shift in their financial exposure via equity.

One should not interpret the larger magnitude for bond holdings as evidence that investors pay more attention to bond positions. The larger magnitude instead reflects differences in the average size of each position type and the concavity of the association between position sizes and voting against ISS. Bond positions tend to be smaller, with the average equity position being 10 times larger than the average bond position (see Table 3). Because the association between position sizes and voting is concave (e.g., see Figure 2 and Figure 6 of Gilje et al. (Reference Gilje, Gormley and Levit2020)), the increase in voting against ISS that occurs for larger holdings is diminishing as the portfolio weight increases. This combination of concavity and smaller positions for bonds will tend to make the relative importance of bond positions appear larger when linearity is assumed. However, if we instead employ an estimation that accounts for this concavity (e.g., by instead using (Bond holdings/TNA)0.5 and (Equity holdings/TNA)0.5 as the explanatory variables), we do not reject the null hypothesis that the coefficients on the two types of holdings are of the same magnitude.

B. An Institution’s EDGAR Viewings of Company Filings

Because voting against ISS need not always indicate an attentive investor, we also assess the association between bond holdings and an alternative proxy for investor attention—whether an institution accesses the company’s proxy filings via EDGAR. Because we measure this proxy at the meeting—rather than proposal-level, we estimate

$$ Non- zero\hskip0.45em {EDGAR\ views}_{iklm}={\displaystyle \begin{array}{l}\beta {\left(\frac{Bond\ holdings}{TNA}\right)}_{ikm}\\ {}+\hskip2px \gamma {\left(\frac{Equity\ holdings}{TNA}\right)}_{ikm}+{\alpha}_l+{\delta}_{im}+{\varepsilon}_{iklm},\end{array}} $$

$$ Non- zero\hskip0.45em {EDGAR\ views}_{iklm}={\displaystyle \begin{array}{l}\beta {\left(\frac{Bond\ holdings}{TNA}\right)}_{ikm}\\ {}+\hskip2px \gamma {\left(\frac{Equity\ holdings}{TNA}\right)}_{ikm}+{\alpha}_l+{\delta}_{im}+{\varepsilon}_{iklm},\end{array}} $$

where Non-zero EDGAR views is an indicator equal to 1 if institution i accessed a proxy filing of firm k before shareholder meeting l held in month m (see Section II.C and the Appendix for more details on how we construct this variable), a

$ \mathrm{nd}\hskip0.45em {\alpha}_l $

and

$ \mathrm{nd}\hskip0.45em {\alpha}_l $

and

$ {\delta}_{im} $

are meeting and institution-by-month fixed effects, respectively. The meeting fixed effects control for any firm characteristics (e.g., profitability, size, and takeover vulnerability) at the time of the meeting that might matter for how likely institutions are to access a firm’s SEC filings. The institution-by-month fixed effects control for any differences in an institution’s overall tendency to access EDGAR filings, while allowing for this tendency to change over time. Hence, our coefficient of interest,

$ {\delta}_{im} $

are meeting and institution-by-month fixed effects, respectively. The meeting fixed effects control for any firm characteristics (e.g., profitability, size, and takeover vulnerability) at the time of the meeting that might matter for how likely institutions are to access a firm’s SEC filings. The institution-by-month fixed effects control for any differences in an institution’s overall tendency to access EDGAR filings, while allowing for this tendency to change over time. Hence, our coefficient of interest,

$ \beta $

, is identified using variation in EDGAR viewings that vary as a function of each institution’s bond holdings in each month. Institutions with no within-month variation in their downloading of filings will not contribute to our estimates. We continue to double-cluster the standard errors at the institution and year level.

$ \beta $

, is identified using variation in EDGAR viewings that vary as a function of each institution’s bond holdings in each month. Institutions with no within-month variation in their downloading of filings will not contribute to our estimates. We continue to double-cluster the standard errors at the institution and year level.

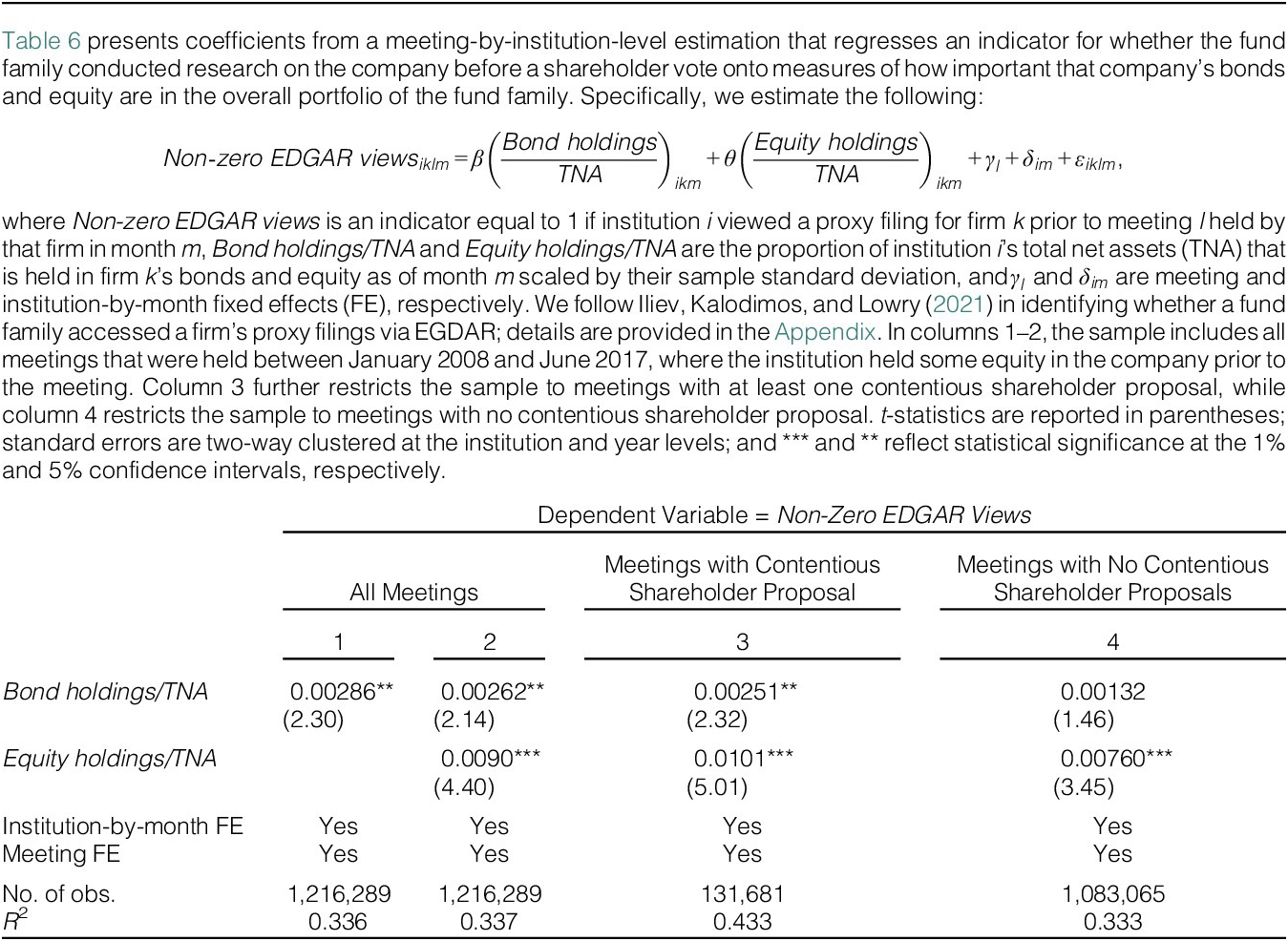

Table 5 provides summary statistics for our meeting-by-institution-level sample. The sample includes all institutions with a non-zero equity position in the company in the month of the meeting. In 10.1% of our meeting-by-institution observations, an institution also holds a bond position in the company. That bond position accounts for, on average, 0.015% of the institution’s overall portfolio and 29.9% of the fund family’s overall position in that company.Footnote 13

Bond holdings also positively predict whether an institution will view a company’s proxy filing in the days before the meeting. Table 6 reports our estimates. When excluding the control for Equity holdings/TNA, a 1-standard-deviation increase in the share of an institution’s overall portfolio held in a particular firm’s bonds is associated with a 0.286 percentage point increase in the likelihood of accessing the proxy filing (column 1). The point estimate remains mostly unchanged when including Equity holdings/TNA as a control (column 2). Moreover, like Iliev et al. (Reference Iliev, Kalodimos and Lowry2021), we find a positive association between institutions’ equity holdings and accessing a firm’s SEC filings, consistent with institutions conducting more governance research on stocks that account for a larger proportion of their portfolio.

For comparable changes in institutions’ financial exposure to the firm, the association between bond holdings and the proxy for investor attention is again similar in magnitude to that of equity holdings. Controlling for Equity holdings/TNA, a 0.1 percentage point increase in a bond’s share of TNA is associated with a 3.5 percentage point increase in accessing the proxy filing. For equity, the comparable increase is 0.6 percentage points.Footnote 14

A drawback of using EDGAR views as our outcome variable is that it does not allow us to focus on the shareholder proposals that are more likely to require investor attention. The sample in columns 1 and 2 of Table 6 includes many meetings with only routine proposals. To mitigate this weakness, we assess whether the observed association varies when a meeting includes a contentious shareholder proposal. Table 6, columns 3 and 4, conducts this test.

Meetings that include a contentious shareholder proposal drive the association between bond holdings and EDGAR views. When restricting the sample to meetings with a contentious shareholder proposal (which accounts for about 11% of all observations), we find a large and positive coefficient on Bond holdings/TNA (column 3; p < 0.05). When using meetings without a contentious shareholder proposal, the point estimate is almost 50% smaller and no longer statistically significant (column 4). A similar pattern emerges if we instead use the presence of a say-on-pay proposal to proxy for the shareholder meeting having a contentious proposal. Bond holdings are predictive of EDGAR views for meetings with say-on-pay proposals, but not other meetings (Table A1 in the Supplementary Material). The lack of a statistically significant association between bond holdings and EDGAR views for meetings without a contentious proposal is consistent with such meetings including only routine proposals that require less attention.Footnote 15

V. Heterogeneity Across Funds

Overall, the above findings are consistent with bond holdings influencing institutions’ level of attention. Larger equity and bond positions both predict an increased likelihood of observing behaviors indicating greater investor attention: voting against ISS and downloading SEC filings. These findings suggest that while only equity investors vote, an institution’s holding of bonds might increase its attention to individual companies. This increased attention might occur for a variety of reasons. For example, there are many situations where being an engaged steward can be value-enhancing for both holdings. Hence, institutions with a bond position will have a greater monitoring motive, all else equal, because engagements that improve a firm’s fundamental value will enhance the value of both its bonds and equity. Moreover, bond managers might possess additional information that influences an institution’s decision on how to vote their shares.

We next assess whether bond holdings’ importance varies based on the type of fund holding the bond and whether those bonds are held in the same fund or at another fund in the larger fund family. For this analysis, we focus exclusively on our first proxy for attention, disagreeing with ISS, because it allows us to limit our sample to contentious shareholder proposals, where we observe more meaningful variation in attention, and because the ISS-based measure of attention covers a significantly larger sample of years and institutions, especially for institutions that tend to hold both an equity and bond position.

A. Heterogeneity by Type of Fund

We first assess whether the positive association between how important a firm’s bonds are in an institution’s overall portfolio and that institution’s voting behavior depends on which type of funds hold those bonds. As Table 2 shows, an institution might have a bond position due to holdings in bond-only funds or mixed-asset funds.

It is unclear whether we should observe heterogeneity across fund types. One possibility is that the location of bond positions does not matter for an institution’s overall stewardship activities. This irrelevance might occur if the institution centralizes proxy voting decisions in a way that treats individual fund managers equally or if the centralized process allocates attention and governance resources based solely on the institution’s overall economic exposures to individual companies. On the other hand, the type of fund that holds the bonds might matter if there are differences in the relative influence of different manager types within the institution. For example, if only funds with an equity position have a “seat at the table” when making institution-level vote decisions, positions in bond-only funds might matter less for an institution’s stewardship activities. Alternatively, if voting is not centralized by the institution, it might only be mixed-asset fund manager teams that consider their bond positions when voting.

To test for heterogeneity across fund types, we repeat our estimation of equation (1) after replacing Bond holdings/TNA with two measures of how important a company’s bonds are in the institution’s portfolio. The first, Bond holdings [in bond-only funds]/TNA, measures the proportion of an institution’s overall TNA held in the company’s bonds using bond-only funds. The second, Bond holdings [in mixed-asset funds]/TNA, reflects the share of an institution’s TNA held in the company’s bonds, using only mixed-asset funds. By construction, the sum of these two bond measures equals the original Bond holdings/TNA for each observation.

We find limited evidence that bond positions held in mixed-asset funds are more predictive of institutions’ voting decisions than those held in bond-only funds. Table 7 shows this finding. A 1-standard-deviation increase in Bond holdings [in mixed-asset funds]/TNA (0.13%) predicts a 0.516 percentage point increase in the likelihood of the institution voting against ISS (p-value < 0.01). We find less evidence that holdings in bond-only funds predict institutional investors’ voting patterns. The coefficient on Bond holdings [in bond-only funds]/TNA is 33% smaller and not statistically significant at conventional levels (p-value = 0.20). However, the two coefficients are not statistically different, suggesting that both holding types might be important.

The importance of bond holdings for institutions’ voting might also depend on the type of mixed-asset fund—indexed or actively managed—that holds the bonds. Suppose institutions are more attentive to their actively managed holdings. In that case, bonds held in indexed mixed-asset funds (e.g., target-date funds that include both bond and equity holdings) could matter less for institutions’ attention than bonds held in actively managed, mixed-asset funds.

To assess this possibility, we further subdivide institutions’ mixed-asset holdings into bonds held in index funds and bonds held in actively managed funds. To assign a mixed-asset fund as either indexed or actively managed, we follow Appel, Gormley, and Keim (Reference Appel, Gormley and Keim2016), (Reference Appel, Gormley and Keim2019) and classify a fund as “index” if either CRSP classifies the fund as indexed or if the fund name contains words that would indicate an index fund. All other funds are classified as actively managed. About 85% of the mixed-asset funds in our sample are actively managed.

Consistent with actively managed funds being more attentive to shareholder proposals (or institutions tending to give more weight to the views of their non-index fund managers), we find that the positive association between bond holdings and the likelihood of voting against ISS is limited to actively managed mixed-asset funds (Table 7, column 2). The size of bond holdings held in actively managed, mixed-asset funds is positively associated with the likelihood of disagreeing with ISS (p-value < 0.01). The amount of bonds held in mixed-asset index funds exhibits no association with whether an institution is likely to vote against ISS.

Combined, the heterogeneity across fund types suggests that a combination of factors contributes to institutional investors’ attention and stewardship activities. Not only does an institution’s total economic exposure across asset classes seem to matter, but how the views of individual fund managers are represented internally in stewardship choices also seems to matter.

B. Within-Fund Versus Cross-Fund Bond Holdings

The previous analysis suggests there may be differences in the relative importance of an institution’s within-fund versus cross-fund bond holdings. To investigate this possibility, we next re-estimate our baseline specification at the fund level instead of the fund-family level.

To develop a fund-level data set of votes and holdings, we follow the methodology outlined in Peter Iliev’s guidance note for Iliev and Lowry (Reference Iliev and Lowry2015). Specifically, we used the NPX filing IDs provided by ISS to retrieve NPX text files from EDGAR and manually extracted mutual fund tickers disclosed in each filing. We then matched these tickers to CRSP portfolio numbers to identify individual funds. This manual matching process resulted in a substantial reduction in sample size due to non-standardized reporting formats across filings. Nonetheless, we managed to create a final matched sample of 4,426 unique tickers voting on 5,421 contentious proposals.

Using this fund-level data set, we re-estimated our equation (1) specification with fund-by-month and proposal fixed effects. By including fund-by-month fixed effects (which mirror the institution-by-month fixed effects in our institution-level analysis), the specification examines whether voting by the same fund within the same month varies depending on whether that fund also holds a bond position in the underlying company. Specifically, the test determines if within-fund holdings are significant independently of cross-fund holdings. To assess the potential importance of cross-fund holdings, we calculate the amount of bonds held in other funds at the same institution and include that as an additional control. Table 8 reports the findings.

Both within-fund and within-family cross-fund bond holdings appear to drive our results. The baseline estimation shows a positive and suggestive link between a fund’s bond holdings in a firm and its probability of voting against the ISS recommendation (Table 8, column 1; p-value = 0.11). Furthermore, when we include cross-fund bond holdings in the specification (column 2), we find evidence that both types of holdings predict the observed voting pattern. The significance of cross-fund holdings is consistent with institutions centralizing their voting decisions after consulting with individual fund managers.Footnote 16

VI. Analysis of Alternative Mechanisms

We next assess whether alternative mechanisms might drive the association between bond holdings and investor attention. First, we assess whether creditor–shareholder conflicts can explain our findings. Next, we assess the potential importance of reverse causality and self-selection.

A. Creditor–Shareholder Conflicts

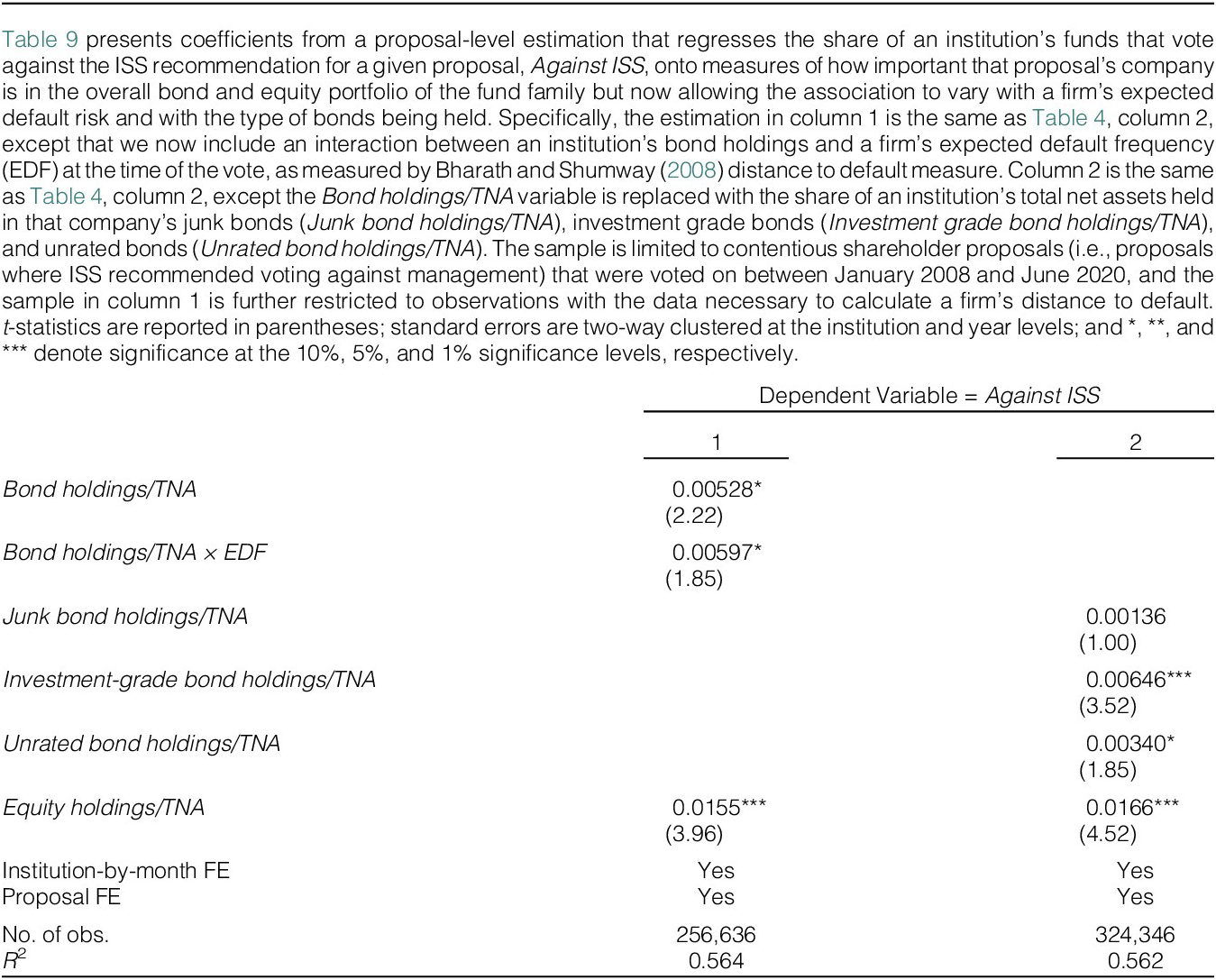

Keswani et al. (Reference Keswani, Tran and Volpin2021) find that institutions with dual debt and equity holdings are more likely to cast votes favorable to creditors, mainly when a firm is in financial distress. Because ISS recommendations reflect equity holders’ interests, debt-holding institutions’ conflicting interests provide an alternative explanation for why such institutions are less likely to follow ISS recommendations. If creditor–shareholder conflicts explain our findings, then the importance of bond holdings for voting should concentrate on firms in financial distress.

However, firms in financial distress do not drive our findings. The importance of institutions’ bond holdings does not concentrate only on firms with a high expected default frequency (EDF), as measured using the approach of Bharath and Shumway (Reference Bharath and Shumway2008). Table 9 reports these estimates. The coefficient on the interaction between Bond holdings/TNA and the issuing firm’s EDF is positive and marginally significant, but the coefficient on Bond holdings/TNA remains positive and statistically significant (Table 9, column 1).Footnote 17 In further support that creditor–shareholder conflicts do not drive our findings, we also find no evidence that institutions’ junk bond holdings drive the association between bond holdings and voting against ISS. Larger holdings in a firm’s investment-grade bonds (where default risk is less) positively predict voting against ISS, while larger holdings in junk bonds (where default risk is greater) do not (Table 9, column 2). Moreover, if we repeat our earlier estimations but exclude firms that Keswani et al. (Reference Keswani, Tran and Volpin2021) define as distressed, we find similar results (Table A3 in the Supplementary Material). We also find no evidence that our findings differ for firms with above or below median leverage (Table A4 in the Supplementary Material).Footnote 18

Our findings also hold for a subset of shareholder proposals where creditor–shareholder conflicts are unlikely to be relevant. Table 10 reports these estimates. Keswani et al. (Reference Keswani, Tran and Volpin2021) find evidence that the influence of creditor–shareholder conflicts on institutional voting is present for proposals with clear implications for creditors but not for proposals related to director elections, where the implications for creditors are typically less clear. However, we find that a larger bond position predicts an increased likelihood of casting votes against ISS for both proposals related to director elections (Table 10, column 1) and all other proposals (column 2). These findings suggest that bond holdings are affecting institutions’ votes more generally.Footnote 19

Creditor–shareholder conflicts also cannot easily explain our findings for EDGAR viewings. While creditor–shareholder conflicts might induce a shift in voting, especially for firms in financial distress, it is unclear why it would explain the amount of governance research conducted by an institution. Consistent with this, our earlier findings for EDGAR viewings are nearly unchanged when excluding firms in financial distress (Table A6 in the Supplementary Material).

Overall, the evidence suggests that our findings are not merely the result of creditor–shareholder conflicts and that institutions are more engaged monitors of their equity positions when they also hold a debt position. This finding provides an essential complement to the existing work on creditor governance and creditor–shareholder conflicts. While such conflicts and creditor influence might lead to votes that fail to maximize shareholder value when companies are distressed, creditor governance can positively influence the value of both a firm’s debt and equity positions at other times. As noted by Dallas (Reference Dallas2019), there can be a significant alignment of interest between creditors and shareholders in many areas of corporate governance. For example, better risk management, a common goal of fixed-income managers, can reduce default risk and increase bond values while simultaneously improving equity value. Our findings suggest this alignment of interest is economically important and contributes to institutional investors’ stewardship.

B. Reverse Causality

Another possible concern with our findings is reverse causality, which could occur if knowledge of how an institution will vote influences its level of bond holdings. For example, suppose institutions planning to vote against ISS tend to think their vote will enhance the value of a firm’s overall assets (increasing both equity and debt values). In that case, those institutions might seek to increase both their equity and bond holdings prior to the vote. If true, institutions’ votes could influence their holdings of equity and bonds rather than vice versa.

However, reverse causality cannot easily explain our findings. First, our findings regarding institutions voting against ISS are nearly unchanged when we instead use holdings that are lagged by 6 months (see Table A7 in the Supplementary Material). Because investors typically do not know shareholder proposals and ISS recommendations that many months in advance of a meeting, it seems unlikely that such an estimation could suffer from simultaneity bias. Second, it is unclear how our findings regarding EDGAR viewings would also be subject to concerns regarding reverse causality.

C. Self-Selection Concerns

While our inclusion of granular fixed effects mitigates omitted variable concerns, one might still worry about potential self-selection concerns. If institutions self-select into holding both the debt and equity of certain companies based on unobservable characteristics that also affect institutions’ monitoring behavior, the interpretation of our findings would change.

To assess this possibility, we analyze whether bond holdings predict how the three largest index fund families—Vanguard, BlackRock, and State Street (the “Big Three”) vote their shares. If self-selection drives our findings, we might expect our findings to be weaker for The Big Three, whose holdings are primarily determined by index benchmarks due to their passive investment mandates. In Table A8 in the Supplementary Material, we repeat our estimation of equation (1) but allow the importance of bonds to differ for The Big Three by including an interaction between Bond holdings/TNA and an indicator that equals 1 if the voting institution is one of The Big Three institutions, Big Three. We also include an interaction term for Equity holdings/TNA and Big Three for completeness. We do not include Big Three on its own as it is collinear with our institution-by-month fixed effects.

Our main findings remain robust for the Big Three, suggesting that selection issues are unlikely to drive the observed patterns. In fact, the proportion of an institution’s overall portfolio held in bonds is an even stronger predictor of voting against ISS for the Big Three. For all other institutions, a 1-standard-deviation increase in Bond holdings/TNA predicts a 0.525 percentage point increase in the likelihood of voting against ISS recommendations (Table A8 in the Supplementary Material; p < 0.05). For the Big Three, the same change predicts a significantly larger 3.125 (0.525 + 2.600) percentage point increase, with the incremental effect being statistically significant at the 1% level.

The greater importance of Bond holdings/TNA and Equity holdings/TNA for The Big Three’s voting could reflect their portfolios’ relative size and diversity. Because of their greater focus on indexed investment strategies, these institutions tend to hold more securities overall, and each security typically represents a relatively small proportion of their overall portfolio. Absent complete economies of scale in monitoring, these institutions might focus their limited resources on monitoring companies representing the largest proportion of their portfolio.Footnote 20

VII. Additional Analysis and Robustness Tests

We next assess whether the importance of economic exposures for monitoring motives might differ when the institution is likely to be an influential owner of the company. Finally, we analyze the robustness of our findings to non-linearities, outliers, and winsorization choices.

A. Heterogeneity Based on the Institution’s Likely Ability to Exert Influence

Our analysis focuses on whether institutions’ economic exposure across asset classes affects their monitoring incentives and attention. While greater economic exposure and monitoring incentives should contribute to greater influence, our share of TNA measures does not directly map into that potential influence because they do not factor in the size or concentration of the ownership stake. For example, an institution might have a large economic exposure and incentive to monitor (because the stock and bonds are a large share of their portfolio), but their level of influence might be small if their equity stake is not among the stock’s largest investors. Moreover, unlike equity, the economic exposure arising from bonds yields no direct influence via voting power.

However, an investor’s ability to exert influence can also drive monitoring motives. For example, Chen et al. (Reference Chen, Harford and Li2007) show that the size of institutional ownership stakes can also affect monitoring incentives. As they note, monitoring motives will likely be greater when institutions have larger ownership stakes because there are greater benefits to increasing the stock’s value. And if there are some fixed costs associated with monitoring technologies, the per-unit cost of monitoring will also be lower, further increasing the institution’s motive to monitor.

We next investigate whether the significance of economic exposure (what we measure) influences outcomes independently of ownership stake size and whether this varies among institutions with larger overall ownership stakes. To conduct this analysis, we follow Chen et al. (Reference Chen, Harford and Li2007) and construct an indicator for whether the institution’s total stock holdings place it in the Top 5 of a company’s institutional investors. Such investors are more able to exert influence. We then included this indicator as a control in our baseline estimation, along with its interactions with our main explanatory variables. Table A9 in the Supplementary Material presents the results.

The findings confirm that economic exposure reflects a dimension of monitoring motive distinct from those arising from the ability to exert influence. Both the Top 5 indicator and the two economic exposure measures (Bond holdings/TNA and Equity holdings/TNA) positively associate with voting against ISS (Table A9 in the Supplementary Material). The findings also provide additional evidence against self-selection concerns stemming from the possibility that investors might increase their economic exposure to companies they can actively monitor and exert greater influence over. Even after controlling for an investor’s likely influence, the findings remain similar.

The estimates also suggest a potential complementarity between an institution’s economic exposure and its ability to exert influence. An institution’s economic exposure via bonds is even more predictive of voting patterns when the institution holds a Top 5 equity position; the interaction between Bond Holdings/TNA and the Top 5 holding indicator is positive and statistically significant. The same is true for the interaction with Equity Holdings/TNA. The findings suggest that monitoring motives arising from economic exposures is amplified when that institution also holds a substantial equity position that likely gives it greater influence.

B. Nonlinearity and Winsorization

Our key explanatory variables, Bond holdings/TNA and Equity holdings/TNA, exhibit significant skewness due to outliers. For example, despite a natural bounding between 0 and 1, the skewness of Bond holdings/TNA is 32, and the kurtosis is 2,067. A handful of unrepresentative, outlier observations above the 99th percentile (0.0014) drive these high values.Footnote 21

To ensure outliers do not drive our findings, we winsorize Bond holdings/TNA and Equity holdings/TNA at the 1% level. This winsorization is important because the relationship between portfolio weight (Bond holdings/TNA or Equity holdings/TNA) and the likelihood of voting against ISS is concave (see Figure 2). This nonlinearity means that extreme values—especially large positions—can exert outsized influence on estimates and obscure more general patterns.

An alternative way to mitigate the influence of outliers would be to estimate a specification that directly captures the concavity of the association between holdings and voting. Such a concave specification will better fit the underlying data, thus reducing the importance of outliers. For example, one could instead use (Bond holdings/TNA)0.5 and (Equity holdings/TNA)0.5 as the explanatory variables, as discussed in Gilje et al. (Reference Gilje, Gormley and Levit2020).

When we use an estimation that accounts for that concavity, we obtain similar results even without winsorization. Moreover, the point estimates and their economic magnitudes are strikingly similar to what we find in the linear estimation. Table A10 in the Supplementary Material presents these findings for our baseline estimation in Table 4 when we instead use (Bond holdings/TNA)0.5 and (Equity holdings/TNA)0.5. These alternative estimates confirm that our reported findings, which include winsorization, accurately capture the underlying associations in the data. All our other main findings also hold when using this alternative specification without winsorization.

VIII. Conclusion

Investors influence governance through a combination of voice (managerial engagement and voting; e.g., Shleifer and Vishny (Reference Shleifer and Vishny1986), Admati, Pfleiderer, and Zechner (Reference Admati, Pfleiderer and Zechner1994)) and exit (selling one’s position; e.g., Admati and Pfleiderer (Reference Admati and Pfleiderer2009), Edmans (Reference Edmans2009), and Edmans, Levit, and Reilly (Reference Edmans, Levit and Reilly2019)). Lacking the ability to participate in shareholder votes, bond investors are typically not thought to play an important governance role, and commonly used measures of institutional investors’ incentive to be engaged stewards focus solely on their equity positions (e.g., Fich et al. (Reference Fich, Harford and Tran2015), Lewellen and Lewellen (Reference Lewellen and Lewellen2022)). However, bond investors have many reasons to be concerned about firms’ governance structures, which can influence bond values (via increased firm value), credit ratings, and the likelihood of repayment. Moreover, bonds represent a large proportion of institutional investors’ portfolios, and institutional investors’ stewardship activities are often centralized, providing their bond managers a potential way to influence how actively the institution monitors and votes its equity positions.

We find evidence that institutions’ bond holdings predict their stewardship activities. Institutions are more likely to vote against ISS, an indication of greater attention, and more likely to access a company’s SEC filings before a shareholder meeting, an indication of governance research, when they have a larger equity position in that company, and importantly, when they have a larger bond position. Comparing the importance of equity and bond holdings, an increase in the size of an institution’s bond position predicts a similar increase in active voting and governance research to what we observe for increases in an institution’s equity position.

Our findings highlight how the determinants of institutional investor attention are more complicated than typically assumed. Intuitively, institutions’ combined equity and bond holdings appear to play a factor in where institutions allocate their limited attention and resources, suggesting that measures of investors’ incentive to be engaged stewards should account for institutions’ total economic exposure to a firm rather than just their exposure via equity. Our findings also suggest that the type of funds that hold these investments matters, as does the internal process by which institutions carry out their stewardship activities. For example, bond positions are more correlated with institutional voting when they are part of an actively managed, mixed-asset fund. And consistent with some institutions’ decision to centralize vote decisions, we find that both within-fund and within-family cross-fund bond holdings drive our results.

Overall, our findings suggest that institutions’ bond holdings increase their incentives to be engaged monitors, providing an important counterpoint to recent concerns about how institutions’ dual ownership might affect equity investors. While dual ownership of a company’s bonds and equity could increase the potential for voting decisions that benefit debt holders at the expense of equity investors (e.g., Bodnaruk and Rossi (Reference Bodnaruk and Rossi2016), Keswani et al. (Reference Keswani, Tran and Volpin2021)), an overall increase in active monitoring and engagement could improve value for both investors. How these dual holdings and their increasing frequency among firms’ largest institutional investors ultimately affect firms’ governance structures is an important topic for future research.

Appendix. Processing Fund’s Information Acquisition via EDGAR

The search traffic data for SEC.gov cover the period from February 2003 through June 2017. EDGAR log file data set includes information on the visitor’s Internet Protocol (IP) address, date, timestamp, CIK, and filing document’s accession number. The IP address in the data set is in version 4 (IPv4) format, which defines an IP address as a 32-bit number separated into four 8-bit numbers. A dot separates each 8-bit number, and the number between the dots could be between 0 and 255 (28 – 1). So, a specific IP address, let us say BlackRock’s, looks like 199.253.64.128. However, the last octet of the IP addresses in the EDGAR log files is replaced with alphabets. The replacement is done to preserve the uniqueness of the IP address and not reveal the visitor’s full identity. Thus, if BlackRock accesses the SEC.gov website from the IP address, the log file will show an entry 199.253.64.gjs. In essence, the EDGAR log file data set has a 24-bit (IP3) address for each EDGAR server activity. Fortunately, most fund families register large blocks of IP addresses; for example, BlackRock owns IP addresses ranging from 199.242.6.0 to 199.242.6.255. As such, the IP3 address is a sufficiently precise representative of IPv4 addresses.

Loughran and McDonald (Reference Loughran and McDonald2017) suggest separating EDGAR requests generated by robots from server requests by regular investors. We classify an IP address as a robot if it requests more than a thousand filings in a day. We remove IP addresses classified as robots for that day. To include only valid EDGAR activities, we follow Drake, Roulstone, and Thornock (Reference Drake, Roulstone and Thornock2015) and exclude activities not related to governance research. We remove index pages (index.htm), icons (.ico), XML filings (.xml), and filings that are under 500 bytes in size. We also combine views by an IP address if they are less than 5 minutes apart and for the same filing.