1. Introduction

The convergence in probability is straight in the analysis tradition and can be thought of as variants of standard pointwise convergence. It is a kind of weak convergence, and it is also the basis of probability and statistics. We know that the weaker the requirements for convergence, the easier it is for a sequence of random variables to have a limit. Strong consistency or almost sure convergence is theoretically stricter and often overly stringent for empirical work. We point out that weak consistency or convergence in probability ensures that the estimator converges to the true parameter, which is sufficient for most real-world applications. This feature will be of great help for us to study some issues that we care about.

In recent years, scholars have paid more attention to computational cost and are more willing to choose estimation methods that require less computation. As we all know, the histogram plays an important role in data representation and density estimation, because it has simple calculations and a wide application. Therefore, the research and application of various estimations based on histogram technology are interesting. This paper will pay attention to the frequency polygon, which is constructed by connecting with straight lines the mid-bin values of a histogram. The calculation of constructing the frequency polygon is approximately equivalent to the histogram. Because the frequency polygon has these advantages, it is of great significance to study it deeply.

With regard to the frequency polygon density estimator, some results have been achieved. Some classic results are taken, for example, [Reference Scott8] analyzed its large sample properties for independent samples, [Reference Carbon, Garel and Tran3] extended the discussion to the strong mixing samples and showed the integrated mean squared error and uniformly strong consistency of the estimator, Besaid and Dabo-Niang [Reference Besaid and Dabo-Niang1] studied the mean square error and uniformly strong consistency for the continuous random fields and so on. Recently, the asymptotic properties of this estimator have been considered by many scholars. Let us review the asymptotic behavior of consistency, [Reference Yang12] studied the uniformly strong consistency of histogram density estimator and the convergence rate under strong mixing process, Kang et al. (2017) studied the asymptotic behavior of the uniformly strong consistency of the frequency polygon investigated by Scott (1985, 2015) under  $\phi$-mixing samples, [Reference Wu and Wang11] studied the uniformly complete consistency and the rates of uniformly complete consistency of frequency polygon estimation for widely orthant dependent samples under some general conditions and showed an application that obtained the uniformly complete consistency and the corresponding rates of hazard rate function estimator and so on. In particular, [Reference Younso13] considered a simple estimator of the density mode using the frequency polygon estimate and investigated the strong consistency of the estimator for strong mixing sequence. Let us review the asymptotic behavior of distribution, [Reference Carbon, Francq and Tran2] established the asymptotic normality of frequency polygons for random fields, [Reference Wen and Xing10] focused on the uniformly asymptotic normality of frequency polygons for

$\phi$-mixing samples, [Reference Wu and Wang11] studied the uniformly complete consistency and the rates of uniformly complete consistency of frequency polygon estimation for widely orthant dependent samples under some general conditions and showed an application that obtained the uniformly complete consistency and the corresponding rates of hazard rate function estimator and so on. In particular, [Reference Younso13] considered a simple estimator of the density mode using the frequency polygon estimate and investigated the strong consistency of the estimator for strong mixing sequence. Let us review the asymptotic behavior of distribution, [Reference Carbon, Francq and Tran2] established the asymptotic normality of frequency polygons for random fields, [Reference Wen and Xing10] focused on the uniformly asymptotic normality of frequency polygons for  $\psi$-mixing samples, [Reference Huang and Xing5] focused on the Berry–Esséen bound of frequency polygons for

$\psi$-mixing samples, [Reference Huang and Xing5] focused on the Berry–Esséen bound of frequency polygons for  $\phi$-mixing samples, and so on.

$\phi$-mixing samples, and so on.

As mentioned earlier, weak consistency plays an important role in probability limit theory. However, there is little literature on the weak consistency of the estimator under dependent samples. This paper mainly studies the weak consistency, the uniformly weak consistency, and the rate of the uniformly weak consistency for frequency polygon estimation of the density function under  $\alpha$-mixing samples, when

$\alpha$-mixing samples, when  $f(x)$ is defined on a compact subset of the real line or on the real line.

$f(x)$ is defined on a compact subset of the real line or on the real line.  $\alpha$-mixing represents a weaker and more broadly applicable dependence structure than

$\alpha$-mixing represents a weaker and more broadly applicable dependence structure than  $\psi$-mixing or

$\psi$-mixing or  $\varphi$-mixing-mixing. Notably,

$\varphi$-mixing-mixing. Notably,  $\alpha$-mixing is particularly suitable for financial applications, as the weak dependence it captures aligns well with the empirically observed dynamics in market returns, covering a wider range of realistic process categories than its stronger counterparts. Establishing convergence properties under this weaker condition is more challenging but significantly extends the proven validity of the estimator. Let us recall the following definition of

$\alpha$-mixing is particularly suitable for financial applications, as the weak dependence it captures aligns well with the empirically observed dynamics in market returns, covering a wider range of realistic process categories than its stronger counterparts. Establishing convergence properties under this weaker condition is more challenging but significantly extends the proven validity of the estimator. Let us recall the following definition of  $\alpha$-mixing random variables, which was introduced by [Reference Rosenblatt7].

$\alpha$-mixing random variables, which was introduced by [Reference Rosenblatt7].

Definition 1.1. Let  $\{X_n, n\geq1\}$ be a sequence of random variables, and let

$\{X_n, n\geq1\}$ be a sequence of random variables, and let  $\mathcal{F}_1^k=\sigma (X_j; 1 \leq j \leq k) $ and

$\mathcal{F}_1^k=\sigma (X_j; 1 \leq j \leq k) $ and  $ \mathcal{F}_{k+n}^\infty=\sigma (X_j; j \geq k+n) $ be two

$ \mathcal{F}_{k+n}^\infty=\sigma (X_j; j \geq k+n) $ be two  $\sigma$-algebras. If

$\sigma$-algebras. If

\begin{eqnarray*}\alpha(n)=\sup\limits_{k\geq 1}\sup\limits_{A \in \mathcal{F}_1^k, B \in \mathcal{F}_{k+n}^\infty} \left|P(AB )-P(A )P(B )\right|\to0,~\textrm{as}~n\to\infty,\end{eqnarray*}

\begin{eqnarray*}\alpha(n)=\sup\limits_{k\geq 1}\sup\limits_{A \in \mathcal{F}_1^k, B \in \mathcal{F}_{k+n}^\infty} \left|P(AB )-P(A )P(B )\right|\to0,~\textrm{as}~n\to\infty,\end{eqnarray*}then  $\{X_n, n\geq1\}$ is called

$\{X_n, n\geq1\}$ is called  $\alpha$-mixing.

$\alpha$-mixing.

In what follows, we will introduce the definition of frequency polygon in detail. Suppose that  $X$ is a random variable with a density function

$X$ is a random variable with a density function  $f (x)$. Let

$f (x)$. Let  $\{X_i, i\geq 1\}$ be the sample drawn from the population

$\{X_i, i\geq 1\}$ be the sample drawn from the population  $X$, which is a sequence of identically distributed random variables with common density

$X$, which is a sequence of identically distributed random variables with common density  $f(x)$ on the real line

$f(x)$ on the real line  $\mathbb{R}$. Consider a partition

$\mathbb{R}$. Consider a partition  $\cdots \lt x_{-2} \lt x_{-1} \lt x_0 \lt x_1 \lt x_2\cdots$ of the real line into equal intervals

$\cdots \lt x_{-2} \lt x_{-1} \lt x_0 \lt x_1 \lt x_2\cdots$ of the real line into equal intervals  $I_{n,j} :=[(j-1)b_n, jb_n)$ of length

$I_{n,j} :=[(j-1)b_n, jb_n)$ of length  $b_n$, where

$b_n$, where  $b_n$ is the binwidth and

$b_n$ is the binwidth and  $j = 0, \pm1, \pm2, \cdots$. For

$j = 0, \pm1, \pm2, \cdots$. For  $x \in[(j-1/2)b_n, (j+1/2)b_n)$, consider the two adjacent histogram bins

$x \in[(j-1/2)b_n, (j+1/2)b_n)$, consider the two adjacent histogram bins  $I_{n,j}$ and

$I_{n,j}$ and  $I_{n,j+1}$. Denote the number of observations falling in these intervals, respectively, by

$I_{n,j+1}$. Denote the number of observations falling in these intervals, respectively, by  $\upsilon_{n,j}$ and

$\upsilon_{n,j}$ and  $\upsilon_{n,j+1}$. Then the values of the histogram in these previous bins are given by

$\upsilon_{n,j+1}$. Then the values of the histogram in these previous bins are given by

\begin{equation}

f_{n,j}=\frac{\upsilon_{n,j}}{nb_n},~f_{n,j+1}=\frac{\upsilon_{n,j+1}}{nb_n}.

\end{equation}

\begin{equation}

f_{n,j}=\frac{\upsilon_{n,j}}{nb_n},~f_{n,j+1}=\frac{\upsilon_{n,j+1}}{nb_n}.

\end{equation} Thus the frequency polygon estimation of the density function  $f(x)$ is defined as follows

$f(x)$ is defined as follows

\begin{equation}

f_{n} (x)=\left(\frac{1}{2}+j-\frac{x}{b_n}\right) f_{n,j}+\left(\frac{1}{2}-j+\frac{x}{b_n}\right) f_{n,j+1},

\end{equation}

\begin{equation}

f_{n} (x)=\left(\frac{1}{2}+j-\frac{x}{b_n}\right) f_{n,j}+\left(\frac{1}{2}-j+\frac{x}{b_n}\right) f_{n,j+1},

\end{equation}for  $x \in[(j-1/2)b_n, (j+1/2)b_n)$. In many literatures,

$x \in[(j-1/2)b_n, (j+1/2)b_n)$. In many literatures,  $j$ is usually regarded as zero. Here it is reserved for the convenience of description later.

$j$ is usually regarded as zero. Here it is reserved for the convenience of description later.

Generally speaking, weak consistency, which ensures that the estimator converges to the true parameter value in probability, often provides a sufficient and more readily attainable guarantee of reliability for large-sample inferences. The frequency polygon, with its computational simplicity, is an attractive tool for such applications, provided its theoretical foundations under realistic dependence are firmly established. The primary contribution of this paper is to bridge this gap. We rigorously establish the weak consistency, uniformly weak consistency, and the corresponding rates of convergence for the frequency polygon density estimator under  $\alpha$-mixing samples. This work extends the theoretical justification for employing this computationally efficient nonparametric estimator to a comprehensive range of dependent data scenarios, reinforcing its utility in practical statistical analysis where complex dependence is present.

$\alpha$-mixing samples. This work extends the theoretical justification for employing this computationally efficient nonparametric estimator to a comprehensive range of dependent data scenarios, reinforcing its utility in practical statistical analysis where complex dependence is present.

The organization of this paper is as follows. Section 2 contains the assumptions and main results obtained. A divergent discussion of the main results is put in Section 3. Data examples, including a simulation study and real data analysis, are provided in Sections 4 and 5, respectively. Some important lemmas are listed in Section 6, and the corresponding proofs are detailed in Section 7.

For the sake of simplicity, let  $\lfloor x\rfloor$ stand for the integer part of

$\lfloor x\rfloor$ stand for the integer part of  $x$, let

$x$, let  $C$ and

$C$ and  $C_1$ be positive constants, whose values may be different in different places. Denote

$C_1$ be positive constants, whose values may be different in different places. Denote  $a_n =O(b_n)$ instead of

$a_n =O(b_n)$ instead of  $ a_n \leq C b_n $, and

$ a_n \leq C b_n $, and  $a_n =o(b_n)$ instead of

$a_n =o(b_n)$ instead of  $ a_n/ b_n\to 0$ as

$ a_n/ b_n\to 0$ as  $n\to\infty$, where

$n\to\infty$, where  $ \{a_n, n \geq 1\}$ and

$ \{a_n, n \geq 1\}$ and  $\{b_n, n \geq 1\}$ are both the sequences of positive numbers.

$\{b_n, n \geq 1\}$ are both the sequences of positive numbers.

2. Assumptions and main results

2.1. Assumptions

Firstly, we make some basic assumptions.

$(A1)$ As

$(A1)$ As  $n\to \infty,~b_n\to0$ and

$n\to \infty,~b_n\to0$ and  $nb_n/ \log n \to \infty$;

$nb_n/ \log n \to \infty$;

$(A2)$

$(A2)$  $\{X_i, i \geq 1\}$ is a sequence of stationary

$\{X_i, i \geq 1\}$ is a sequence of stationary  $\alpha$-mixing random variables.

$\alpha$-mixing random variables.  $X_1$ has an uniformly continuous density

$X_1$ has an uniformly continuous density  $f(x)$ on the real line

$f(x)$ on the real line  $\mathbb{R}$ and the mixing coefficient satisfies

$\mathbb{R}$ and the mixing coefficient satisfies  $\alpha(n)=O(n^{-\lambda})$ for some

$\alpha(n)=O(n^{-\lambda})$ for some  $\lambda \geq 2$;

$\lambda \geq 2$;

$(A3)$ The joint density function

$(A3)$ The joint density function  $f_{ij}(x, y)$ of

$f_{ij}(x, y)$ of  $(X_i, X_j)$ exists and for some positive constant

$(X_i, X_j)$ exists and for some positive constant  $M$, it satisfies

$M$, it satisfies

\begin{eqnarray*}

\sup\limits_{(x,y)\in \mathbb{R}^2}|f_{ij}(x, y)-f(x)f(y)| \leq M,~\textrm{for any~} i\neq j ;

\end{eqnarray*}

\begin{eqnarray*}

\sup\limits_{(x,y)\in \mathbb{R}^2}|f_{ij}(x, y)-f(x)f(y)| \leq M,~\textrm{for any~} i\neq j ;

\end{eqnarray*}  $(A4)$ The density function

$(A4)$ The density function  $f(x)$ satisfies the Lipschitz condition of order

$f(x)$ satisfies the Lipschitz condition of order  $1$, i.e., for all

$1$, i.e., for all  $x, y \in \mathbb{R}$ and some

$x, y \in \mathbb{R}$ and some  $L \gt 0$,

$L \gt 0$,

\begin{eqnarray*}|f(x)-f(y)| \leq L|x-y|;\end{eqnarray*}

\begin{eqnarray*}|f(x)-f(y)| \leq L|x-y|;\end{eqnarray*}  $(A5)$

$(A5)$  $E|X_1|^{1/T} \lt \infty$ for some

$E|X_1|^{1/T} \lt \infty$ for some  $T \gt 0$.

$T \gt 0$.

Remark 2.1. The assumptions are general and also weaker than those assumed in the literature, such as [Reference Yang12], [Reference Huang and Xing5], [Reference Kang, Abbasi, Wang, Xu, Wang and Tang6] and [Reference Younso13].  $(A1)$ ensures asymptotic unbiasedness and adequate bin occupancy for variance control;

$(A1)$ ensures asymptotic unbiasedness and adequate bin occupancy for variance control;  $(A2)$ facilitates Bernstein-type inequalities for dependent data;

$(A2)$ facilitates Bernstein-type inequalities for dependent data;  $(A3)$ restricts joint densities, which is milder than uniform boundedness often required in kernel estimation;

$(A3)$ restricts joint densities, which is milder than uniform boundedness often required in kernel estimation;  $(A4)$ is a standard Lipschitz condition;

$(A4)$ is a standard Lipschitz condition;  $(A5)$ requires a weaker moment condition, which is essential for modeling heavier-tailed data, which significantly expands applicability to real-world datasets where higher moments may not exist. This contrasts with the stronger order-

$(A5)$ requires a weaker moment condition, which is essential for modeling heavier-tailed data, which significantly expands applicability to real-world datasets where higher moments may not exist. This contrasts with the stronger order- $2/T$ moment required for strong consistency in [Reference Yang12], for instance.

$2/T$ moment required for strong consistency in [Reference Yang12], for instance.

Next, we give the main results as follows.

2.2. Main results

Theorem 2.2. Suppose that  $(A1)--(A4)$ are satisfied. If

$(A1)--(A4)$ are satisfied. If

\begin{equation}

g(n, 1) := b_n^{-1} (nb_n/ \log n)^{-\lambda} \to 0,

\end{equation}

\begin{equation}

g(n, 1) := b_n^{-1} (nb_n/ \log n)^{-\lambda} \to 0,

\end{equation}then for any  $x\in \mathbb{R}$,

$x\in \mathbb{R}$,

\begin{equation}

\left|f_{n} (x)- f(x)\right|= o(1) \textrm{~in~ probability}.

\end{equation}

\begin{equation}

\left|f_{n} (x)- f(x)\right|= o(1) \textrm{~in~ probability}.

\end{equation} Consider the optimal binwidth  $b_n = Cn^{-1/5}$ (Carbon et al. (1979)), it is clear that

$b_n = Cn^{-1/5}$ (Carbon et al. (1979)), it is clear that  $(A1)$ is satisfied. Hence, we get the following corollary.

$(A1)$ is satisfied. Hence, we get the following corollary.

Corollary 2.3. Suppose that  $b_n = Cn^{-1/5}$ and

$b_n = Cn^{-1/5}$ and  $(A2)--(A3)$ are satisfied. Then for any

$(A2)--(A3)$ are satisfied. Then for any  $x\in \mathbb{R}$, (2.2) holds.

$x\in \mathbb{R}$, (2.2) holds.

Theorem 2.4 Suppose that  $(A1)--(A5)$ are satisfied. Then we have the following two statements:

$(A1)--(A5)$ are satisfied. Then we have the following two statements:

(1) If

\begin{equation}

g(n, 2) := b_n^{-2} (nb_n/ \log n)^{-\lambda} \to 0,

\end{equation}

\begin{equation}

g(n, 2) := b_n^{-2} (nb_n/ \log n)^{-\lambda} \to 0,

\end{equation}then for any compact subset  $D$ of

$D$ of  $\mathbb{R}$,

$\mathbb{R}$,

\begin{equation}

\sup\limits_{x\in D} \left|f_{n} (x)- f(x)\right|= o(1) \textrm{~in~ probability};

\end{equation}

\begin{equation}

\sup\limits_{x\in D} \left|f_{n} (x)- f(x)\right|= o(1) \textrm{~in~ probability};

\end{equation} (2) If  $g(n, 2)n^T\to 0,$ then

$g(n, 2)n^T\to 0,$ then

\begin{equation}

\sup\limits_{x\in \mathbb{R}} \left|f_{n} (x)- f(x)\right|=o(1) \textrm{~in~ probability}.

\end{equation}

\begin{equation}

\sup\limits_{x\in \mathbb{R}} \left|f_{n} (x)- f(x)\right|=o(1) \textrm{~in~ probability}.

\end{equation}Analogously, we have the following corollary.

Corollary 2.5. Suppose that  $b_n = Cn^{-1/5}$ and

$b_n = Cn^{-1/5}$ and  $(A2)--(A5)$ are satisfied. Then for any compact subset

$(A2)--(A5)$ are satisfied. Then for any compact subset  $D$ of

$D$ of  $\mathbb{R}$, (2.4) holds. Furthermore, if

$\mathbb{R}$, (2.4) holds. Furthermore, if  $\lambda \gt \max\left\{2, \frac{2+5T}{4} \right\}$, then (2.5) holds.

$\lambda \gt \max\left\{2, \frac{2+5T}{4} \right\}$, then (2.5) holds.

Remark 2.6. The following theorem is the rate of the uniformly weak consistency for frequency polygon estimation of the density function under  $\alpha$-mixing samples.

$\alpha$-mixing samples.

Theorem 2.7. Suppose that  $(A1)--(A5)$ are satisfied. Denote

$(A1)--(A5)$ are satisfied. Denote  $R_n=\max\left\{b_n ,\left(\frac{\log n}{n b_n}\right)^{1/2}\right\}$. Then we have the following two statements:

$R_n=\max\left\{b_n ,\left(\frac{\log n}{n b_n}\right)^{1/2}\right\}$. Then we have the following two statements:

(1) If

\begin{equation}

g(n, 3) := b_n^{-2} (nb_n/ \log n)^{-\lambda/2+1/2} \to 0,

\end{equation}

\begin{equation}

g(n, 3) := b_n^{-2} (nb_n/ \log n)^{-\lambda/2+1/2} \to 0,

\end{equation}then for any compact subset  $D$ of

$D$ of  $\mathbb{R}$,

$\mathbb{R}$,

\begin{equation}

\sup\limits_{x\in D}\left| f_{n} (x)-f(x)\right|= O\left(R_n\right) {~in~ probability};

\end{equation}

\begin{equation}

\sup\limits_{x\in D}\left| f_{n} (x)-f(x)\right|= O\left(R_n\right) {~in~ probability};

\end{equation} (2) If  $g(n, 3)n^T\to 0,$ then

$g(n, 3)n^T\to 0,$ then

\begin{equation}

\sup\limits_{x\in \mathbb{R} }\left| f_{n} (x)-f(x)\right|= O\left(R_n\right) {~in~ probability}.

\end{equation}

\begin{equation}

\sup\limits_{x\in \mathbb{R} }\left| f_{n} (x)-f(x)\right|= O\left(R_n\right) {~in~ probability}.

\end{equation} Clearly, we have  $R_n\to 0$ as

$R_n\to 0$ as  $n\to \infty$, so Theorem 2.7 implies that

$n\to \infty$, so Theorem 2.7 implies that  $f_n(x)$ converges in probability to

$f_n(x)$ converges in probability to  $f (x)$ with the rate

$f (x)$ with the rate  $R_n$. Analogously, we have the following corollary.

$R_n$. Analogously, we have the following corollary.

Corollary 2.8. Suppose that  $b_n = Cn^{-1/5}$ and

$b_n = Cn^{-1/5}$ and  $(A2)--(A5)$ are satisfied. If

$(A2)--(A5)$ are satisfied. If  $\lambda \gt 2$, then for any compact subset

$\lambda \gt 2$, then for any compact subset  $D$ of

$D$ of  $\mathbb{R}$, (2.7) holds. Furthermore, if

$\mathbb{R}$, (2.7) holds. Furthermore, if  $\lambda \gt 2+\frac{5T}{2} $, then (2.8) holds.

$\lambda \gt 2+\frac{5T}{2} $, then (2.8) holds.

Remark 2.9. From Corollary 2.3, if the binwidth  $b_n = Cn^{-1/5}$, then

$b_n = Cn^{-1/5}$, then  $R_n=b_n$; if the binwidth

$R_n=b_n$; if the binwidth  $b_n = C(n^{-1} \log n)^{1/3}$, then

$b_n = C(n^{-1} \log n)^{1/3}$, then  $R_n=(n^{-1} \log n)^{1/3}$, which is the optimal rate of convergence for the histogram density estimation in the i.i.d. case.

$R_n=(n^{-1} \log n)^{1/3}$, which is the optimal rate of convergence for the histogram density estimation in the i.i.d. case.

Remark 2.10. Theorems 2.4 and 2.7 state the uniformly weak consistency for frequency polygon estimation of density function. Compared with the corresponding results of [Reference Yang12] or other related literatures establishing strong consistency under the moment condition  $E|X|^{2/T} \lt \infty$ for some

$E|X|^{2/T} \lt \infty$ for some  $T \gt 0$, it is noted that a lower moment condition is assumed here, which is

$T \gt 0$, it is noted that a lower moment condition is assumed here, which is  $E|X|^{1/T} \lt \infty$ for some

$E|X|^{1/T} \lt \infty$ for some  $T \gt 0$.

$T \gt 0$.

Remark 2.11. In fact, the weaker the requirements for convergence, the easier it is for a sequence of random variables to have a limit, we know that the existence of weak consistency can solve some issues. It is an important subject to obtain weak convergence results under weak conditions, and our results generalize and improve the existing ones in the literature.

3. Simulation study

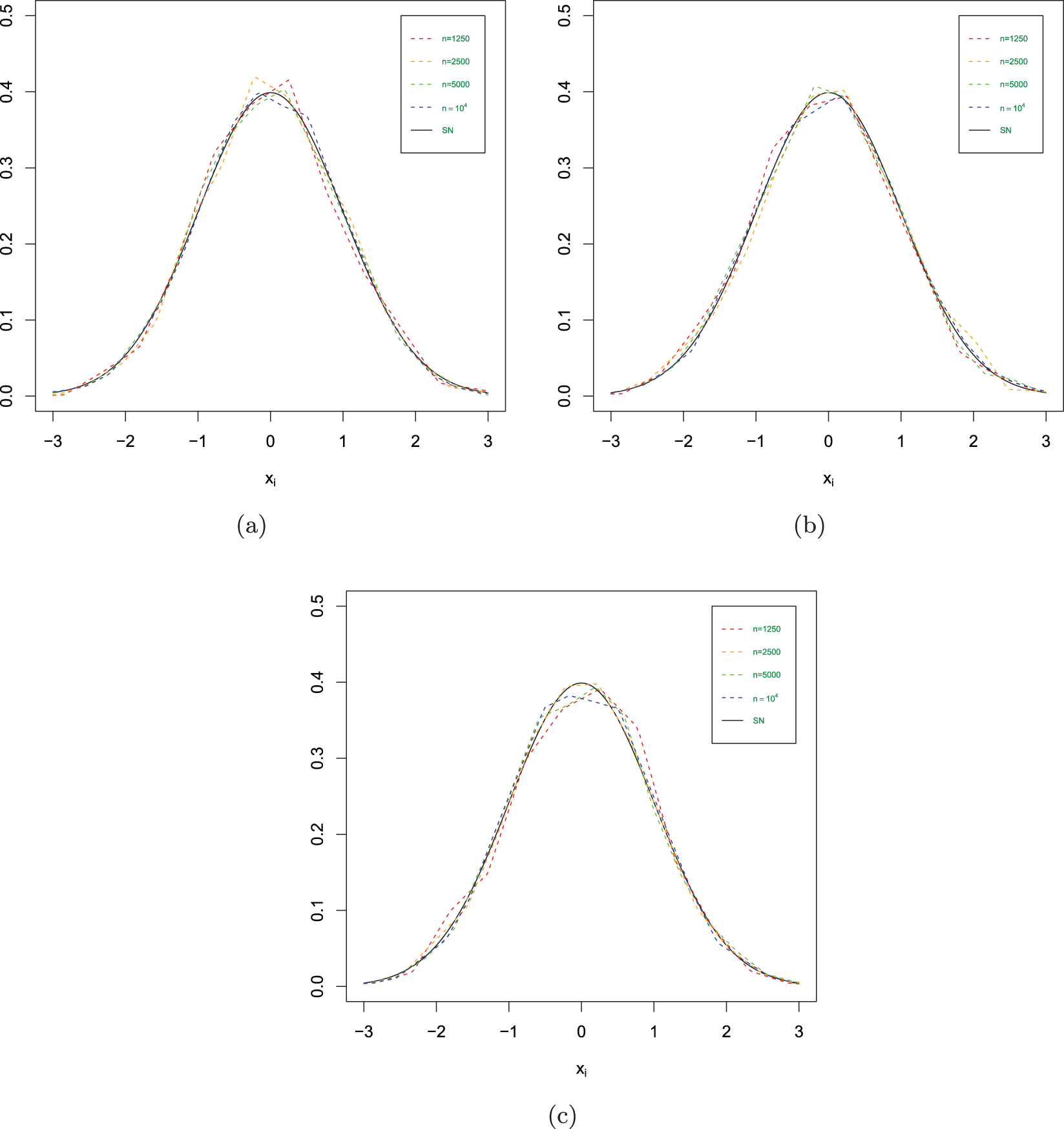

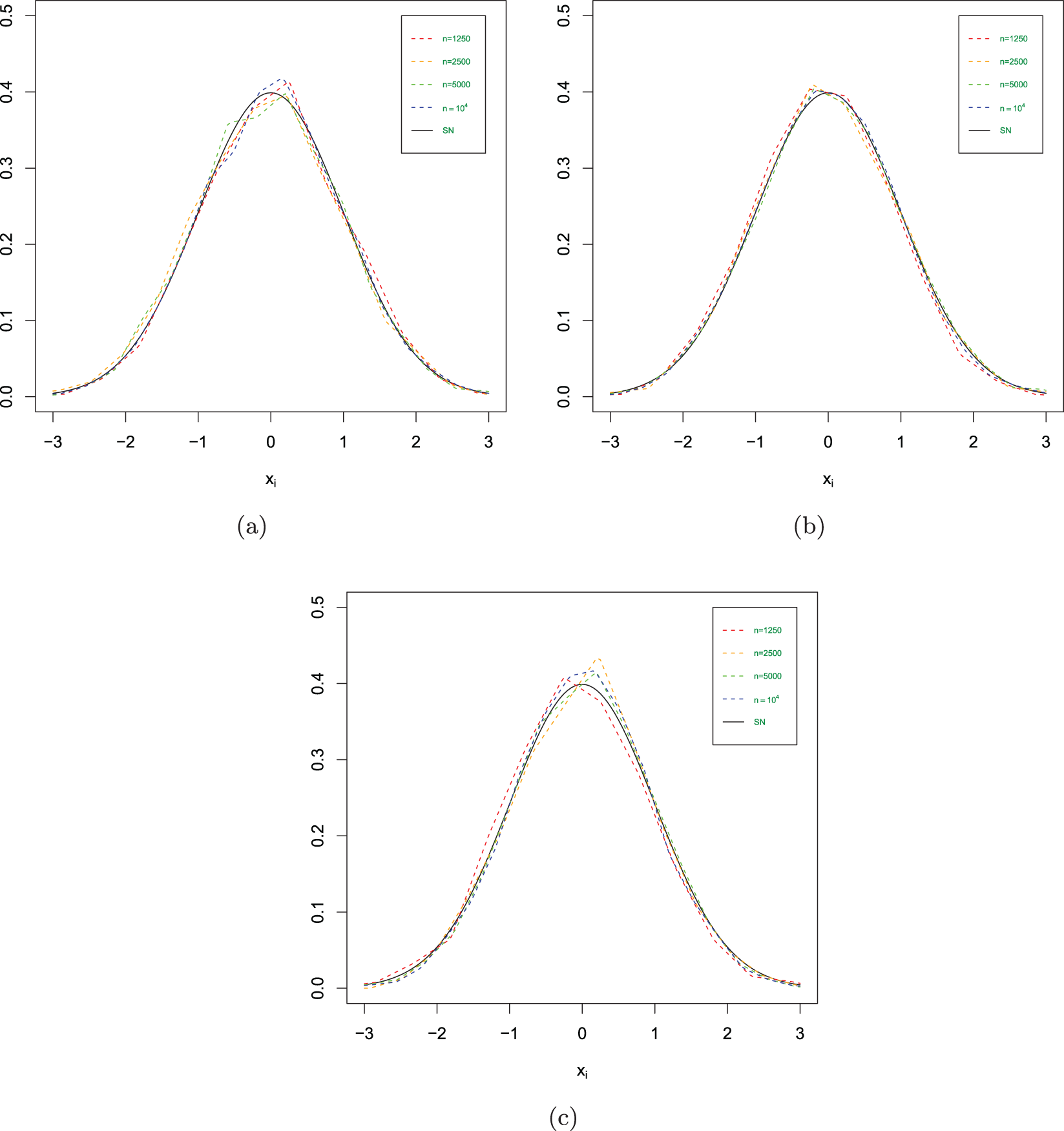

This simulation study aims to verify the theoretical consistency of the frequency polygon estimator under finite  $\alpha$-mixing samples and to examine its performance across different dependence strengths.

$\alpha$-mixing samples and to examine its performance across different dependence strengths.

We generate data from an ARMA(1,1) model, a standard framework for studying dependent processes. Consider the ARMA(1,1) model:

\begin{equation}

X_t = \phi X_{t-1} + \varepsilon_t-\theta \varepsilon_{t-1},

\end{equation}

\begin{equation}

X_t = \phi X_{t-1} + \varepsilon_t-\theta \varepsilon_{t-1},

\end{equation}where  $\{\varepsilon_t, t \geq 1\}$ are independent and identically distributed,

$\{\varepsilon_t, t \geq 1\}$ are independent and identically distributed,  $\varepsilon_i \sim N(0, \sigma_\varepsilon^2)$,

$\varepsilon_i \sim N(0, \sigma_\varepsilon^2)$,  $| \phi| \lt 1, |\theta| \lt 1$ and

$| \phi| \lt 1, |\theta| \lt 1$ and  $\sigma_\varepsilon^2= (1-\phi^2)/(1-2 \phi \theta + \theta^2)$. Obviously, we know

$\sigma_\varepsilon^2= (1-\phi^2)/(1-2 \phi \theta + \theta^2)$. Obviously, we know  $X_t \sim N(0,1)$. We know from [Reference Fan and Yao4] and Yang (2023) that

$X_t \sim N(0,1)$. We know from [Reference Fan and Yao4] and Yang (2023) that  $\{X_t, t \geq 1\}$ is an

$\{X_t, t \geq 1\}$ is an  $\alpha$-mixing and stationary time series with

$\alpha$-mixing and stationary time series with  $\alpha(k) = O(|\phi|^k)$ for the case

$\alpha(k) = O(|\phi|^k)$ for the case  $\phi\neq\theta$.

$\phi\neq\theta$.

The specific scenarios are defined by the autoregressive parameter  $\phi$, which directly controls the dependence strength. We consider

$\phi$, which directly controls the dependence strength. We consider  $\phi\in \{0,0.1,0.3,0.4,0.5,0.6,0.8\}$, covering a spectrum from independence (

$\phi\in \{0,0.1,0.3,0.4,0.5,0.6,0.8\}$, covering a spectrum from independence ( $\phi=0$) to strong positive dependence (

$\phi=0$) to strong positive dependence ( $\phi=0.8$). For each

$\phi=0.8$). For each  $\phi$, complementary moving-average parameters

$\phi$, complementary moving-average parameters  $\theta$ are selected to form distinct. Sample sizes are set to

$\theta$ are selected to form distinct. Sample sizes are set to  $n = 1250,$

$n = 1250,$  $2500$,

$2500$,  $5000$, and

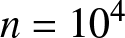

$5000$, and  $10^4$ to assess the estimator’s behavior as the sample increases.

$10^4$ to assess the estimator’s behavior as the sample increases.

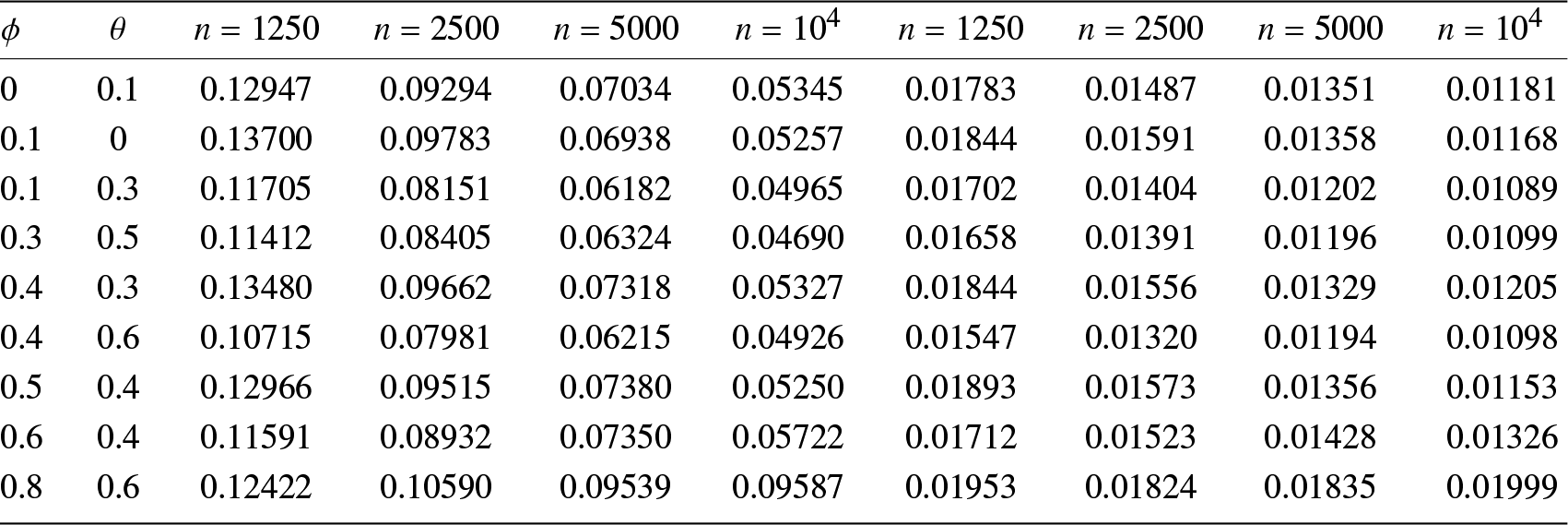

[Reference Carbon, Garel and Tran3] proved the best possible choice of the binwidth, namely  $h_{FP} =2\left(\frac{15}{49nR^{''}(f)} \right)^{1/5}$, and

$h_{FP} =2\left(\frac{15}{49nR^{''}(f)} \right)^{1/5}$, and  $R^{''}(f)=\frac{3}{8\sqrt{\pi}\sigma^5}$ can be calculated in our experiments, then optimal binwidth in our experiments is

$R^{''}(f)=\frac{3}{8\sqrt{\pi}\sigma^5}$ can be calculated in our experiments, then optimal binwidth in our experiments is  $b_{n}=h_{FP}= 2.153366 n^{-1/5}\sigma$. It is called the optimal binwidth under the integrated mean squared error. The experiment is repeated

$b_{n}=h_{FP}= 2.153366 n^{-1/5}\sigma$. It is called the optimal binwidth under the integrated mean squared error. The experiment is repeated  $N=100$ times in each scenario. For

$N=100$ times in each scenario. For  $x_i =-3 + 0.05(i -1)$ where

$x_i =-3 + 0.05(i -1)$ where  $1 \leq i \leq m$ and

$1 \leq i \leq m$ and  $m = 121$, we compute the estimates

$m = 121$, we compute the estimates  $f_n(x_i)$, the global mean absolute relative deviations

$f_n(x_i)$, the global mean absolute relative deviations

\begin{equation}

GMARD_f(n) = \frac{1}{Nm}\sum_{i=1}^{m}\sum_{k=1}^{N}\frac{| f_n(x_i,k)-f (x_i)|}{f (x_i ) },

\end{equation}

\begin{equation}

GMARD_f(n) = \frac{1}{Nm}\sum_{i=1}^{m}\sum_{k=1}^{N}\frac{| f_n(x_i,k)-f (x_i)|}{f (x_i ) },

\end{equation}and the values of

\begin{equation}

GR_f(n):= \frac{1}{Nm}\sum_{i=1}^{m}\sum_{k=1}^{N}\frac{| f_n(x_i,k)-f (x_i )|}{R_n},

\end{equation}

\begin{equation}

GR_f(n):= \frac{1}{Nm}\sum_{i=1}^{m}\sum_{k=1}^{N}\frac{| f_n(x_i,k)-f (x_i )|}{R_n},

\end{equation}where  $f (x )$ is the density function of standard normal distribution,

$f (x )$ is the density function of standard normal distribution,  $f_n(x, k)$ is the estimate of density function in

$f_n(x, k)$ is the estimate of density function in  $k$-th experiment and

$k$-th experiment and  $R_n$ takes

$R_n$ takes  $b_n$ here.

$b_n$ here.  $GMARD_f(n)$ measures the absolute estimation error

$GMARD_f(n)$ measures the absolute estimation error  $\left|f_n (\cdot)-f (\cdot)\right|$, while

$\left|f_n (\cdot)-f (\cdot)\right|$, while  $GR_f(n)$ quantifies the relative rate at which this error shrinks in comparison to the theoretical convergence rate

$GR_f(n)$ quantifies the relative rate at which this error shrinks in comparison to the theoretical convergence rate  $R_n$. Specifically, the estimates

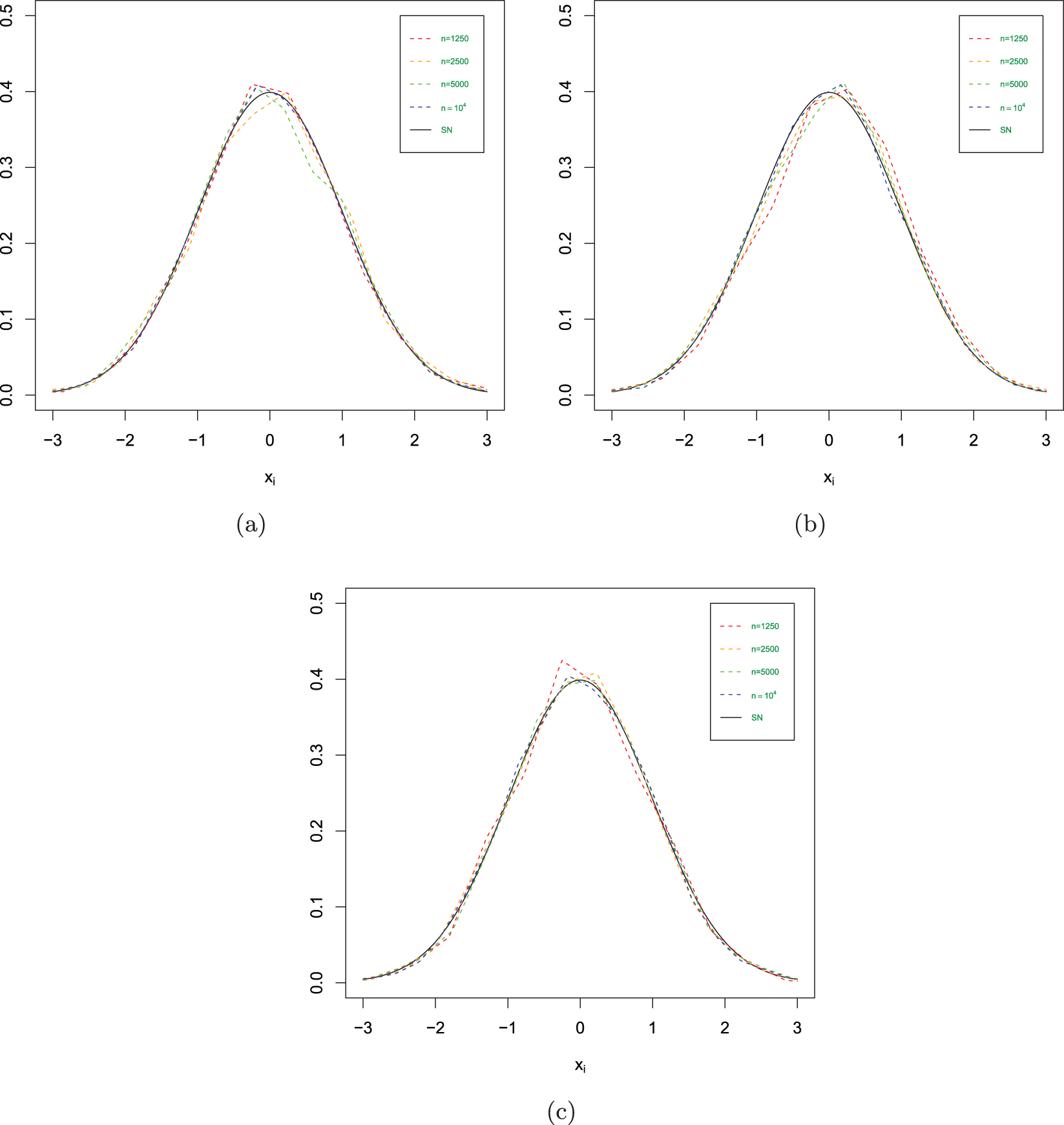

$R_n$. Specifically, the estimates  $f_n(x )$ in different scenarios are shown in Figs. 1–3, the

$f_n(x )$ in different scenarios are shown in Figs. 1–3, the  $GMARD_f(n)$ and

$GMARD_f(n)$ and  $GR_f(n)$ obtained in different scenarios are listed in Tab. 1.

$GR_f(n)$ obtained in different scenarios are listed in Tab. 1.

The estimated values in different scenarios. (a)  $\phi= 0$ and

$\phi= 0$ and  $\theta=0.1$. (b)

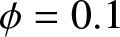

$\theta=0.1$. (b)  $\phi= 0.1$ and

$\phi= 0.1$ and  $\theta=0$. (c)

$\theta=0$. (c)  $\phi= 0.1$ and

$\phi= 0.1$ and  $\theta=0.3$.

$\theta=0.3$.

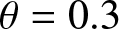

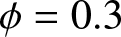

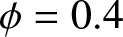

The estimated values in different scenarios. (a)  $\phi= 0.3$ and

$\phi= 0.3$ and  $\theta=0.5$. (b)

$\theta=0.5$. (b)  $\phi= 0.4$ and

$\phi= 0.4$ and  $\theta=0.3$. (c)

$\theta=0.3$. (c)  $\phi= 0.4$ and

$\phi= 0.4$ and  $\theta=0.6$.

$\theta=0.6$.

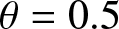

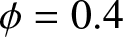

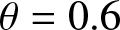

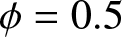

The estimated values in different scenarios. (a)  $\phi= 0.5$ and

$\phi= 0.5$ and  $\theta=0.4$. (b)

$\theta=0.4$. (b)  $\phi= 0.6$ and

$\phi= 0.6$ and  $\theta=0.4$. (c)

$\theta=0.4$. (c)  $\phi= 0.8$ and

$\phi= 0.8$ and  $\theta=0.6$.

$\theta=0.6$.

The values of  $GMARD_f(n)$ (left) and

$GMARD_f(n)$ (left) and  $GR_f(n)$ (right) in different scenarios.

$GR_f(n)$ (right) in different scenarios.

Concluding remarks

(1) Figs. 1–3 show us that when the sample size increases, the fitting effects of the three curves become better based on the same sample dependence. While the dependence enhances, the fitting effects of these three curves also become worse under the same sample size. Furthermore, as sample sizes increase, the estimation quality also correspondingly improves.

(2) Tab. 1 reveals that higher values of  $ \phi $ (e.g.,

$ \phi $ (e.g.,  $\phi = 0.8 $) introduce stronger dependence and long-range dependence in the series, leading to increased estimation errors (e.g.,

$\phi = 0.8 $) introduce stronger dependence and long-range dependence in the series, leading to increased estimation errors (e.g.,  $GMARD_f(n$) up to 0.09587 for

$GMARD_f(n$) up to 0.09587 for  $n = 10^4$).

$n = 10^4$).

(3) Increasing  $\theta$ (e.g.,

$\theta$ (e.g.,  $\theta = 0.6$ for

$\theta = 0.6$ for  $\phi = 0.4$) can counteract the dependence induced by

$\phi = 0.4$) can counteract the dependence induced by  $\phi$ to some extent, and then reduce estimation errors (e.g.,

$\phi$ to some extent, and then reduce estimation errors (e.g.,  $GMARD_f(n)$ decreases from 0.13480 to 0.10715 for

$GMARD_f(n)$ decreases from 0.13480 to 0.10715 for  $n = 1250$).

$n = 1250$).

(4) Weak dependence (e.g.,  $\phi = 0.1$ or balanced

$\phi = 0.1$ or balanced  $\phi/\theta$ pairs like

$\phi/\theta$ pairs like  $\phi = 0.3, \theta = 0.5$) yields the better performance of estimation, with lower

$\phi = 0.3, \theta = 0.5$) yields the better performance of estimation, with lower  $GMARD_f(n)$ and

$GMARD_f(n)$ and  $GR_f(n)$ values across sample sizes.

$GR_f(n)$ values across sample sizes.

(5) With the increasing of the sample size, the value of  $GR_f(n)$ decreases. Mathematically,

$GR_f(n)$ decreases. Mathematically,  $GR_f(n)$ is a representation for the convergence rate of the estimation

$GR_f(n)$ is a representation for the convergence rate of the estimation  $f_n(\cdot)$, indicating that

$f_n(\cdot)$, indicating that  $f_n(\cdot)$ either maintains the same convergence rate as

$f_n(\cdot)$ either maintains the same convergence rate as  $R_n$ or even surpasses it.

$R_n$ or even surpasses it.

In short,  $GMARD_f(n)$ decrease with the increase of sample size

$GMARD_f(n)$ decrease with the increase of sample size  $n$, which shows that the estimation is consistent based on

$n$, which shows that the estimation is consistent based on  $\alpha$-mixing samples in this case. Strong dependence reduces estimation quality, and at this time, larger samples are needed as compensation. These findings demonstrate our theoretical results.

$\alpha$-mixing samples in this case. Strong dependence reduces estimation quality, and at this time, larger samples are needed as compensation. These findings demonstrate our theoretical results.

4. Real data analysis

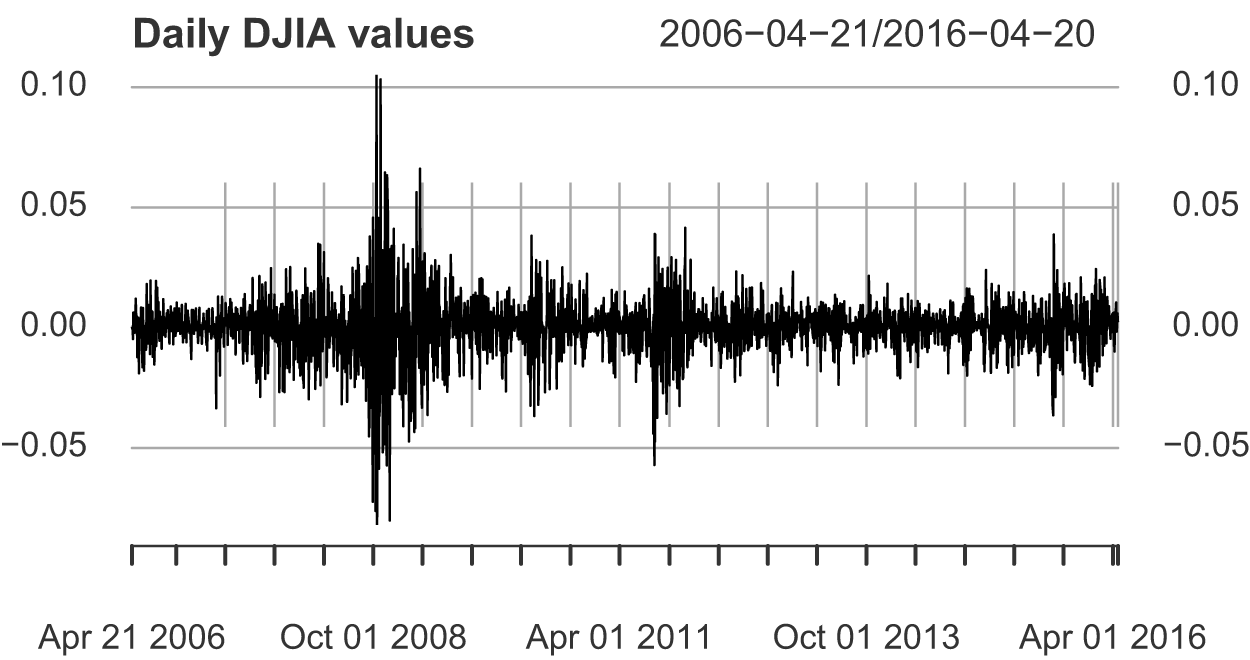

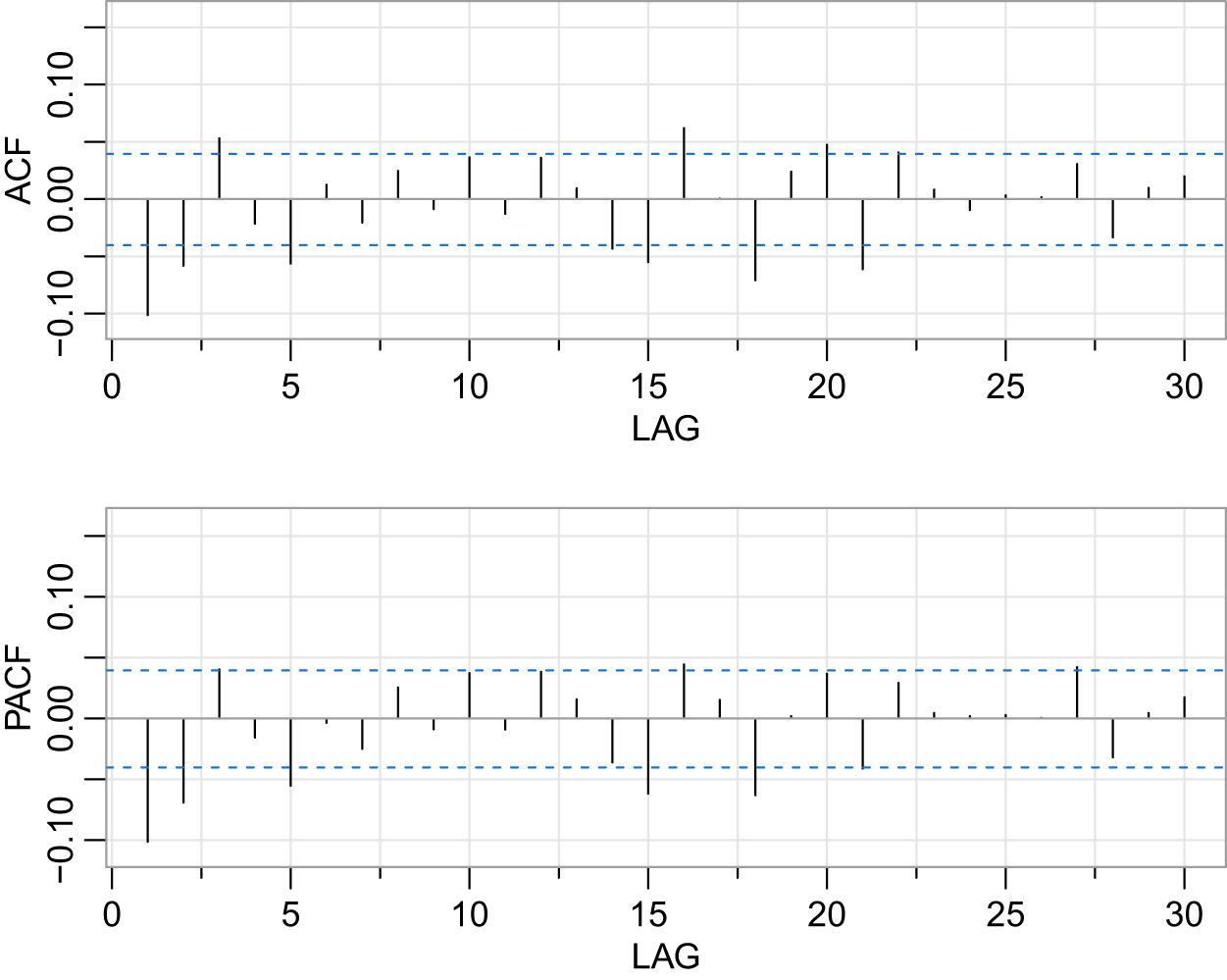

The statistical analysis of continuous data is a surprisingly recent development. The goal of this section is to demonstrate the practical applicability of the frequency polygon estimator for financial return data, which exhibits volatility clustering and heavy tails. As an example of financial time series data, Fig. 4 shows the rate of the daily return (or percentage change) of Dow Jones Industrial Average (DJIA) from April 21st, 2006 to April 20th, 2016. This is the typical rate of return data. The average value of the series seems to be stable, and the average rate of return is close to zero. However, the periods with great fluctuations (changes) tend to gather together. One problem in the analysis of these types of financial data is to estimate the density function, which is helpful to predict the volatility of future returns. Let  $d_t$ be the actual value of DJIA,

$d_t$ be the actual value of DJIA,  $r_t=(d_t-d_{t-1})/d_{t-1}$ is the rate of return, then we have

$r_t=(d_t-d_{t-1})/d_{t-1}$ is the rate of return, then we have  $1+r_t=d_t/d_{t-1}$, and

$1+r_t=d_t/d_{t-1}$, and  $\log(1+r_t)=\log(d_t/d_{t-1})=\log(d_t)-\log(d_{t-1})\approx r_t$. This data set can also be obtained in the R package (astsa).

$\log(1+r_t)=\log(d_t/d_{t-1})=\log(d_t)-\log(d_{t-1})\approx r_t$. This data set can also be obtained in the R package (astsa).

The rate of the daily return (or percentage change) of DJIA from April 20th, 2006 to April 20th, 2016.

Observing Fig. 4, we note that the mean remains nearly constant, oscillating around 0, indicating that the series might be stationary. The PACF’s significant spike at lag 2 (exceeding the confidence band) necessitates AR(2), while the ACF’s gradual decay implies MA terms are needed. Fig. 5 suggests that the dataset could be an ARMA(2,2) process. After conducting the augmented Dickey-Fuller (ADF) unit root test, we find that the test statistic is  $-39.8484$, which is less than the critical value of

$-39.8484$, which is less than the critical value of  $-2.58$ at the 1% significance level

$-2.58$ at the 1% significance level  $(-39.8484 \lt -2.58)$. Therefore, at the 1% significance level, we reject the null hypothesis, concluding that the series is stationary. A stationary ARMA process

$(-39.8484 \lt -2.58)$. Therefore, at the 1% significance level, we reject the null hypothesis, concluding that the series is stationary. A stationary ARMA process  $\{X_t,t\geq1\}$ is

$\{X_t,t\geq1\}$ is  $\alpha$-mixing according to [Reference Fan and Yao4].

$\alpha$-mixing according to [Reference Fan and Yao4].

The ACF and PACF plots of the daily return rate of DJIA from April 20th, 2006 to April 20th, 2016.

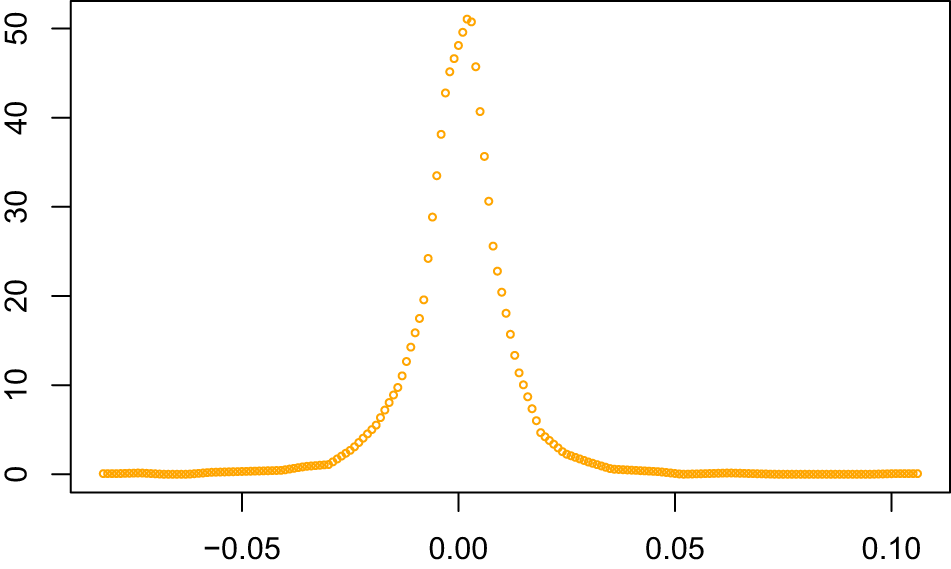

By employing the calculation method in the Simulation study section, we can derive the frequency polygon estimation of the daily return rate (or percentage change rate) of DJIA. Figure 6 shows leptokurtic features (peaked center and fat tails) compared to the red normal distribution curve, consistent with empirical finance data.

The estimated density function of daily return rate of DJIA.

In addition, the GARCH (generalized autoregressive conditional heteroskedasticity) model is particularly adept at capturing the variability of volatility in financial time series, and it can provide valuable insights for risk management and investment strategies. The frequency polygon estimator provides a complementary nonparametric approach for modeling return distributions. To delve deeper into comprehending the volatility pattern and structure specifically exhibited by the daily return rate of DJIA, we utilize the “rugarch” package in R to analyze the data set, and then derive the conditional variance equation of GARCH(1,1) model as follows:

\begin{equation*}h_t = 2.192579\times10^{-6} + 0.1209623 \varepsilon_{t-1}^2 + 0.8616528 h_{t-1}.\end{equation*}

\begin{equation*}h_t = 2.192579\times10^{-6} + 0.1209623 \varepsilon_{t-1}^2 + 0.8616528 h_{t-1}.\end{equation*} It can be noted that the aggregate value of  $\alpha_1 (0.1209623)$ and

$\alpha_1 (0.1209623)$ and  $\beta_1 (0.8616528)$ approaches unity, which strikingly emphasizes the tenacity of volatility and the significant clustering effect within the financial time series. This observation highlights the persistent nature of market turbulence, where periods of high volatility tend to be succeeded by further volatility. The data captures the essence of volatility clustering in financial data.

$\beta_1 (0.8616528)$ approaches unity, which strikingly emphasizes the tenacity of volatility and the significant clustering effect within the financial time series. This observation highlights the persistent nature of market turbulence, where periods of high volatility tend to be succeeded by further volatility. The data captures the essence of volatility clustering in financial data.

5. Lemmas

Firstly, we make some notations.

Denote  $a_{n,j;1} =\frac{1}{2}+j-\frac{x}{b_n},~a_{n,j;2} =\frac{1}{2}-j+\frac{x}{b_n}$ and

$a_{n,j;1} =\frac{1}{2}+j-\frac{x}{b_n},~a_{n,j;2} =\frac{1}{2}-j+\frac{x}{b_n}$ and  $U_{n,j} = [(j-1/2)b_n, (j+1/2)b_n), j=0,\pm1,\pm2,\cdots$. Then the frequency polygon estimator (1.2) may be rewritten as

$U_{n,j} = [(j-1/2)b_n, (j+1/2)b_n), j=0,\pm1,\pm2,\cdots$. Then the frequency polygon estimator (1.2) may be rewritten as

\begin{equation}

f_n (x) = a_{n,j;1}f_{n,j} + a_{n,j;2} f_{n,j+1}\textrm{~for~} x \in U_{n,j}.

\end{equation}

\begin{equation}

f_n (x) = a_{n,j;1}f_{n,j} + a_{n,j;2} f_{n,j+1}\textrm{~for~} x \in U_{n,j}.

\end{equation}Furthermore, let

\begin{equation}

Y_{n,j;i} = I((j-1)b_n \leq X_i \lt jb_n), Z_{n,j;i} = Y_{n,j;i} - EY_{n,j;i},~ i\geq 1.

\end{equation}

\begin{equation}

Y_{n,j;i} = I((j-1)b_n \leq X_i \lt jb_n), Z_{n,j;i} = Y_{n,j;i} - EY_{n,j;i},~ i\geq 1.

\end{equation} Then we have  $\upsilon_{n,j} =\sum\limits_{i=1}^n Y_{n,j;i}$ and

$\upsilon_{n,j} =\sum\limits_{i=1}^n Y_{n,j;i}$ and

\begin{equation}

f_n (x) = a_{n,j;1}\frac{\sum\limits_{i=1}^n Y_{n,j;i}}{nb_n}+

a_{n,j;2}\frac{\sum\limits_{i=1}^n Y_{n,j+1;i}}{nb_n}.

\end{equation}

\begin{equation}

f_n (x) = a_{n,j;1}\frac{\sum\limits_{i=1}^n Y_{n,j;i}}{nb_n}+

a_{n,j;2}\frac{\sum\limits_{i=1}^n Y_{n,j+1;i}}{nb_n}.

\end{equation} It is clear that the weights  $a_{n,j;1}$ and

$a_{n,j;1}$ and  $a_{n,j;2}$ satisfy

$a_{n,j;2}$ satisfy

\begin{equation}

0 \lt a_{n,j;1}, a_{n,j;2} \lt 1 \textrm{~and~} a_{n,j;1} + a_{n,j;2}= 1.

\end{equation}

\begin{equation}

0 \lt a_{n,j;1}, a_{n,j;2} \lt 1 \textrm{~and~} a_{n,j;1} + a_{n,j;2}= 1.

\end{equation} Denote  $p_{nj}:=EY_{n,j;i}=P((j-1)b_n \leq X_i \lt jb_n)$. It is also clear that

$p_{nj}:=EY_{n,j;i}=P((j-1)b_n \leq X_i \lt jb_n)$. It is also clear that  $EZ_{nj;i}^2=p_{nj}(1-p_{nj})$.

$EZ_{nj;i}^2=p_{nj}(1-p_{nj})$.

This section provides several important lemmas, which play vital roles and will be used in the subsequent proofs of the main results. The first one is the moment inequality on estimating the upper bound of  $2$-nd moment for the partial sums of random variables.

$2$-nd moment for the partial sums of random variables.

Lemma 5.1. (cf. Yang, 2017, Lemma 3.3)

Suppose that  $(A1)--(A3)$ hold, and the integers

$(A1)--(A3)$ hold, and the integers  $a$ and

$a$ and  $m$ satisfy

$m$ satisfy  $0\leq a \lt a+m\leq n$. Then there exists a positive constant

$0\leq a \lt a+m\leq n$. Then there exists a positive constant  $C$, which does not depend on

$C$, which does not depend on  $n,j, a$ and

$n,j, a$ and  $m$, such that

$m$, such that

\begin{equation*}E\left(\sum_{i=a+1}^{a+m}Z_{nj;i} \right)^2 \leq Cmb_n.\end{equation*}

\begin{equation*}E\left(\sum_{i=a+1}^{a+m}Z_{nj;i} \right)^2 \leq Cmb_n.\end{equation*} The following one is the probability inequality for  $\alpha$-mixing random variables, which is an important tool in the later proofs.

$\alpha$-mixing random variables, which is an important tool in the later proofs.

Lemma 5.2. (cf. Wei et al., [Reference Wei, Yang, Yu, Yang and Xing9], Lemma 3.3)

Let  $\{\xi_i, i \geq 1\}$ be a sequence of real-valued

$\{\xi_i, i \geq 1\}$ be a sequence of real-valued  $\alpha$-mixing random variables with

$\alpha$-mixing random variables with  $E\xi_i = 0$ and

$E\xi_i = 0$ and  $ |\xi_i|\leq b \lt \infty~a.s.$,

$ |\xi_i|\leq b \lt \infty~a.s.$,  $\{k_n, n \geq 1\}$ be positive integers such that

$\{k_n, n \geq 1\}$ be positive integers such that  $1\leq k_n \leq n/2$. Then for any

$1\leq k_n \leq n/2$. Then for any  $\epsilon \gt 0$,

$\epsilon \gt 0$,

\begin{eqnarray*}

P\left(\left|\sum\limits_{i=1}^{n} \xi_i\right| \gt n\epsilon \right)

\leq 4 \exp \left( -\frac{n\epsilon^2}{12(3\sigma_n^2+bk_n\epsilon)} \right) +36b\epsilon^{-1}\alpha(k_n),

\end{eqnarray*}

\begin{eqnarray*}

P\left(\left|\sum\limits_{i=1}^{n} \xi_i\right| \gt n\epsilon \right)

\leq 4 \exp \left( -\frac{n\epsilon^2}{12(3\sigma_n^2+bk_n\epsilon)} \right) +36b\epsilon^{-1}\alpha(k_n),

\end{eqnarray*}where  $\sigma_n^2=n^{-1}\sum_{j=1}^{2m_n+1}EV_j^2$,

$\sigma_n^2=n^{-1}\sum_{j=1}^{2m_n+1}EV_j^2$,  $m_n=\lfloor n/(2k_n)\rfloor$,

$m_n=\lfloor n/(2k_n)\rfloor$,  $V_j=\sum_{(j-1)k_n \lt i \leq jk_n}\xi_i~ (j=1,2,\cdots,2m_n)$ and

$V_j=\sum_{(j-1)k_n \lt i \leq jk_n}\xi_i~ (j=1,2,\cdots,2m_n)$ and  $V_{2m_n+1}=\sum_{i =2m_nk_n+1}^n\xi_i$.

$V_{2m_n+1}=\sum_{i =2m_nk_n+1}^n\xi_i$.

In order to clarify the proofs of the main results, we provide the following two lemmas. The first one is inspired by [Reference Yang12].

Lemma 5.3. If  $f(x)$ is uniformly continuous in

$f(x)$ is uniformly continuous in  $\mathbb{R}$, then

$\mathbb{R}$, then

\begin{equation}

\sup_{x\in \mathbb{R}}\left|Ef_n(x)-f(x)\right|=o(1).

\end{equation}

\begin{equation}

\sup_{x\in \mathbb{R}}\left|Ef_n(x)-f(x)\right|=o(1).

\end{equation} If  $f(x)$ satisfies the Lipschitz condition of order

$f(x)$ satisfies the Lipschitz condition of order  $1$, i.e., the condition

$1$, i.e., the condition  $(A4)$, then

$(A4)$, then

\begin{equation}

\sup_{x\in \mathbb{R}}\left|Ef_n(x)-f(x)\right|=O(b_n ).

\end{equation}

\begin{equation}

\sup_{x\in \mathbb{R}}\left|Ef_n(x)-f(x)\right|=O(b_n ).

\end{equation}Proof. It is easy to see that

\begin{eqnarray*}

\sup_{x\in \mathbb{R}}\left|Ef_n(x)-f(x)\right|=\sup_{-\infty \lt j \lt \infty}\sup_{x\in U_{nj}}\left|Ef_n(x)-f(x)\right|.

\end{eqnarray*}

\begin{eqnarray*}

\sup_{x\in \mathbb{R}}\left|Ef_n(x)-f(x)\right|=\sup_{-\infty \lt j \lt \infty}\sup_{x\in U_{nj}}\left|Ef_n(x)-f(x)\right|.

\end{eqnarray*} Note that for  $ x\in U_{nj}$,

$ x\in U_{nj}$,

\begin{equation*}\left|Ef_n(x)-f(x)\right|\leq \frac{1}{b_n}\int_{(j-1)b_n}^{jb_n}\left| f (y)-f(x)\right|dy\textrm{~and~}b_n\to 0.\end{equation*}

\begin{equation*}\left|Ef_n(x)-f(x)\right|\leq \frac{1}{b_n}\int_{(j-1)b_n}^{jb_n}\left| f (y)-f(x)\right|dy\textrm{~and~}b_n\to 0.\end{equation*} If  $f (x)$ is uniformly continuous in

$f (x)$ is uniformly continuous in  $\mathbb{R}$, then for

$\mathbb{R}$, then for  $\epsilon \gt 0$, as

$\epsilon \gt 0$, as  $n$ sufficiently large,

$n$ sufficiently large,

\begin{equation*} \int_{(j-1)b_n}^{jb_n}\left| f (y)-f(x)\right|dy\leq \epsilon b_n.\end{equation*}

\begin{equation*} \int_{(j-1)b_n}^{jb_n}\left| f (y)-f(x)\right|dy\leq \epsilon b_n.\end{equation*}Hence, the desired result (5.5) is derived.

If  $f(x)$ satisfies the condition

$f(x)$ satisfies the condition  $(A4)$, then as

$(A4)$, then as  $n$ sufficiently large, we have

$n$ sufficiently large, we have

\begin{equation*} \int_{(j-1)b_n}^{jb_n}\left| f (y)-f(x)\right|dy\leq C b_n^2.\end{equation*}

\begin{equation*} \int_{(j-1)b_n}^{jb_n}\left| f (y)-f(x)\right|dy\leq C b_n^2.\end{equation*}Hence, the desired result (5.6) is derived.

Lemma 5.4. Suppose that there exists some  $T \gt 0$ such that

$T \gt 0$ such that  $E|X|^{1/T} \lt \infty$. Denote

$E|X|^{1/T} \lt \infty$. Denote  $T_n=(-\infty,-n^T)\bigcup(n^T,\infty)$ and

$T_n=(-\infty,-n^T)\bigcup(n^T,\infty)$ and  $R_n=\max\left\{b_n,\left(\frac{\log n}{n b_n}\right)^{1/2}\right\}$. Then we have

$R_n=\max\left\{b_n,\left(\frac{\log n}{n b_n}\right)^{1/2}\right\}$. Then we have

\begin{equation}

\sup_{x\in T_n} f_n(x)=O_P\left( R_n\right).

\end{equation}

\begin{equation}

\sup_{x\in T_n} f_n(x)=O_P\left( R_n\right).

\end{equation} Furthermore, suppose that the density function  $f(x)$ is continuous. Then we have

$f(x)$ is continuous. Then we have

\begin{equation}

\sup_{x\in T_n} f (x)=O\left( n^{-(1+T)}\right).

\end{equation}

\begin{equation}

\sup_{x\in T_n} f (x)=O\left( n^{-(1+T)}\right).

\end{equation}Proof. In fact, if we want to get (5.7), we only need to prove that for every  $\epsilon \gt 0$, there exist

$\epsilon \gt 0$, there exist  $M_\epsilon$ and

$M_\epsilon$ and  $N_\epsilon$ such that for all

$N_\epsilon$ such that for all  $n \gt N_\epsilon$

$n \gt N_\epsilon$

\begin{equation}

P\left(\frac{\sup_{x\in T_n} f_n(x)}{R_n} \gt M_\epsilon \right) \lt \epsilon.

\end{equation}

\begin{equation}

P\left(\frac{\sup_{x\in T_n} f_n(x)}{R_n} \gt M_\epsilon \right) \lt \epsilon.

\end{equation}Note that

\begin{equation}

\sum_{k=1}^\infty kP\left(k^T \lt |X|\leq (k+1)^T\right)

\leq CE|X|^{1/T} \lt \infty.

\end{equation}

\begin{equation}

\sum_{k=1}^\infty kP\left(k^T \lt |X|\leq (k+1)^T\right)

\leq CE|X|^{1/T} \lt \infty.

\end{equation} We can obtain by (5.10) that for sufficiently large  $n$

$n$

\begin{eqnarray}P\left(\frac{\sup_{x\in T_n} f_n(x)}{R_n} \gt M_\epsilon \right)&\leq & P\left( \sup_{x\in T_n} f_n(x) \gt 0\right)\nonumber\\

&\leq& nP\left(X\in T_n\right)=nP\left(|X| \gt n^T\right)\nonumber\\

&=&\sum_{k=n}^\infty nP\left(k^T \lt |X|\leq (k+1)^T\right)\nonumber\\

&\leq&\sum_{k=n}^\infty kP\left(k^T \lt |X|\leq (k+1)^T\right) \lt \epsilon.\end{eqnarray}

\begin{eqnarray}P\left(\frac{\sup_{x\in T_n} f_n(x)}{R_n} \gt M_\epsilon \right)&\leq & P\left( \sup_{x\in T_n} f_n(x) \gt 0\right)\nonumber\\

&\leq& nP\left(X\in T_n\right)=nP\left(|X| \gt n^T\right)\nonumber\\

&=&\sum_{k=n}^\infty nP\left(k^T \lt |X|\leq (k+1)^T\right)\nonumber\\

&\leq&\sum_{k=n}^\infty kP\left(k^T \lt |X|\leq (k+1)^T\right) \lt \epsilon.\end{eqnarray} Since  $E|X|^{1/T} \lt \infty$ and the density function

$E|X|^{1/T} \lt \infty$ and the density function  $f (x)$ is continuous, we obtain

$f (x)$ is continuous, we obtain  $f (x) = o\left(|x|^{-(1/T+1)}\right)$ as

$f (x) = o\left(|x|^{-(1/T+1)}\right)$ as  $|x|\to \infty$. Therefore, for sufficiently large

$|x|\to \infty$. Therefore, for sufficiently large  $n$, we have

$n$, we have

\begin{eqnarray}\sup_{x\in T_n}f (x)&=&\sup_{|x| \gt n^T}f (x) \leq \sup_{|x| \gt n^T} \left(\frac{|x|}{n^T} \right)^{1/T+1} f (x) \nonumber\\

&=& n^{-(1+T)} \sup_{|x| \gt n^T} |x|^{1/T+1} f (x) \leq Cn^{-(1+T)}.\end{eqnarray}

\begin{eqnarray}\sup_{x\in T_n}f (x)&=&\sup_{|x| \gt n^T}f (x) \leq \sup_{|x| \gt n^T} \left(\frac{|x|}{n^T} \right)^{1/T+1} f (x) \nonumber\\

&=& n^{-(1+T)} \sup_{|x| \gt n^T} |x|^{1/T+1} f (x) \leq Cn^{-(1+T)}.\end{eqnarray}Hence, the proof of Lemma 5.4 is completed.

6. Proofs of main results

6.1. Proof of Theorem 2.2

Recall that the partition  $\cdots \lt x_{-2} \lt x_{-1} \lt x_0 \lt x_1 \lt x_2\cdots$ of the real line

$\cdots \lt x_{-2} \lt x_{-1} \lt x_0 \lt x_1 \lt x_2\cdots$ of the real line  $\mathbb{R}$ and equal intervals

$\mathbb{R}$ and equal intervals  $I_{n,j} :=[(j-1)b_n, jb_n)$ of length

$I_{n,j} :=[(j-1)b_n, jb_n)$ of length  $b_n$, where

$b_n$, where  $b_n$ is the binwidth and

$b_n$ is the binwidth and  $j = 0, \pm1, \pm2, \cdots$,

$j = 0, \pm1, \pm2, \cdots$,  $U_{nj}=\left[(j-1/2)b_n, (j+1/2)b_n\right)$. From Lemma 5.3, we only need to prove that for each

$U_{nj}=\left[(j-1/2)b_n, (j+1/2)b_n\right)$. From Lemma 5.3, we only need to prove that for each  $j$ and any

$j$ and any  $x\in U_{nj}$,

$x\in U_{nj}$,

\begin{equation}

\left|f_n(x)- Ef_n(x)\right|=o(1) \textrm{~in~ probability.}

\end{equation}

\begin{equation}

\left|f_n(x)- Ef_n(x)\right|=o(1) \textrm{~in~ probability.}

\end{equation} Noting that  $EZ_{nj;i}=0$ and

$EZ_{nj;i}=0$ and  $|Z_{nj;i}|\leq 1$, we get by Lemma 5.1 that

$|Z_{nj;i}|\leq 1$, we get by Lemma 5.1 that

\begin{eqnarray*}

E V_j^2=E\left( \sum\limits_{(j-1) k_n \lt i \leq j k_n}Z_{nj;i} \right)^2

\leq Ck_nb_n,

\end{eqnarray*}

\begin{eqnarray*}

E V_j^2=E\left( \sum\limits_{(j-1) k_n \lt i \leq j k_n}Z_{nj;i} \right)^2

\leq Ck_nb_n,

\end{eqnarray*}and thus

\begin{eqnarray*}

\sigma_n^2=n^{-1}\sum_{j=1}^{2m_n+1}EV_j^2\leq Cn^{-1}k_n (2m_n+1)b_n\leq Cb_n.

\end{eqnarray*}

\begin{eqnarray*}

\sigma_n^2=n^{-1}\sum_{j=1}^{2m_n+1}EV_j^2\leq Cn^{-1}k_n (2m_n+1)b_n\leq Cb_n.

\end{eqnarray*} Hence, we have that for any  $\varepsilon \gt 0$ and

$\varepsilon \gt 0$ and  $x\in U_{nj}$

$x\in U_{nj}$

\begin{align}&P\left( \left|f_n(x)- Ef_n(x)\right| \gt \varepsilon\right)\nonumber\\

&= P\left( \left|a_{n,j;1}\sum\limits_{i=1}^{n}\left(Y_{n,j;i} -E Y_{n,j;i} \right)+a_{n,j;2}\sum\limits_{i=1}^{n}\left(Y_{n,j+1;i} -E Y_{n,j+1;i} \right) \right| \gt nb_n\varepsilon\right) \nonumber\\

&= P\left( \left|a_{n,j;1}\sum\limits_{i=1}^{n}Z_{n,j;i}+a_{n,j;2}\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt nb_n\varepsilon\right) \nonumber\\

&\leq P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_n\varepsilon}{2a_{n,j;1}}\right) +P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_n\varepsilon}{2a_{n,j;2}}\right) .\end{align}

\begin{align}&P\left( \left|f_n(x)- Ef_n(x)\right| \gt \varepsilon\right)\nonumber\\

&= P\left( \left|a_{n,j;1}\sum\limits_{i=1}^{n}\left(Y_{n,j;i} -E Y_{n,j;i} \right)+a_{n,j;2}\sum\limits_{i=1}^{n}\left(Y_{n,j+1;i} -E Y_{n,j+1;i} \right) \right| \gt nb_n\varepsilon\right) \nonumber\\

&= P\left( \left|a_{n,j;1}\sum\limits_{i=1}^{n}Z_{n,j;i}+a_{n,j;2}\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt nb_n\varepsilon\right) \nonumber\\

&\leq P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_n\varepsilon}{2a_{n,j;1}}\right) +P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_n\varepsilon}{2a_{n,j;2}}\right) .\end{align}Note by Lemma 5.2 that

\begin{align}P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_n\varepsilon}{2a_{n,j;1}}\right)&\leq P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_n\varepsilon}{2}\right)\nonumber\\

&\leq 4\exp\left\{ -\frac{nb_n^2 \varepsilon^2}{24(6\sigma_n^2+k_nb_n\varepsilon)}\right\}+72\varepsilon^{-1}b_n^{-1}\alpha(k_n) \nonumber\\

&\leq 4\exp\left\{ -\frac{nb_n \varepsilon^2}{24( C+k_n \varepsilon)}\right\}+72\varepsilon^{-1}b_n^{-1}\alpha(k_n) \nonumber\\

&\leq C\exp\left\{ -\frac{ \varepsilon^2}{24\left( \frac{C}{nb_n} +\frac{k_n}{nb_n} \varepsilon\right)}\right\}+C b_n^{-1} k_n^{-\lambda}.\end{align}

\begin{align}P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_n\varepsilon}{2a_{n,j;1}}\right)&\leq P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_n\varepsilon}{2}\right)\nonumber\\

&\leq 4\exp\left\{ -\frac{nb_n^2 \varepsilon^2}{24(6\sigma_n^2+k_nb_n\varepsilon)}\right\}+72\varepsilon^{-1}b_n^{-1}\alpha(k_n) \nonumber\\

&\leq 4\exp\left\{ -\frac{nb_n \varepsilon^2}{24( C+k_n \varepsilon)}\right\}+72\varepsilon^{-1}b_n^{-1}\alpha(k_n) \nonumber\\

&\leq C\exp\left\{ -\frac{ \varepsilon^2}{24\left( \frac{C}{nb_n} +\frac{k_n}{nb_n} \varepsilon\right)}\right\}+C b_n^{-1} k_n^{-\lambda}.\end{align} Taking  $k_n=\frac{nb_n \varepsilon}{48\log n}$, we can get by (2.1) that the RHS of above inequality is less than

$k_n=\frac{nb_n \varepsilon}{48\log n}$, we can get by (2.1) that the RHS of above inequality is less than

\begin{align}

C\exp\left\{ -\frac{\varepsilon^2 \log n}{24\left( \frac{\varepsilon^2}{48} +\frac{\varepsilon^2}{48}\right)}\right\}+C b_n^{-1} \left(\frac{nb_n }{\log n}\right)^{-\lambda}

&\leq C\exp\left\{-\log n\right\}+C b_n^{-(1+\lambda)} n^{-\lambda} \left( \log n\right)^{\lambda}\nonumber\\

&\leq C n^{-1} +C b_n^{-(1+\lambda)} n^{-\lambda} \left( \log n\right)^{\lambda}\nonumber\\

&= C n^{-1} +C g(n, 1)=o(1).

\end{align}

\begin{align}

C\exp\left\{ -\frac{\varepsilon^2 \log n}{24\left( \frac{\varepsilon^2}{48} +\frac{\varepsilon^2}{48}\right)}\right\}+C b_n^{-1} \left(\frac{nb_n }{\log n}\right)^{-\lambda}

&\leq C\exp\left\{-\log n\right\}+C b_n^{-(1+\lambda)} n^{-\lambda} \left( \log n\right)^{\lambda}\nonumber\\

&\leq C n^{-1} +C b_n^{-(1+\lambda)} n^{-\lambda} \left( \log n\right)^{\lambda}\nonumber\\

&= C n^{-1} +C g(n, 1)=o(1).

\end{align}Similarly, we have

\begin{equation}

P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_n\varepsilon}{2a_{n,j;2}}\right)=o(1),

\end{equation}

\begin{equation}

P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_n\varepsilon}{2a_{n,j;2}}\right)=o(1),

\end{equation}which together with (6.2)–(6.4) yields (6.1).

Therefore, the proof of Theorem 2.2 is completed.

6.2. Proof of Theorem 2.4

Firstly, we prove (2.4). From Lemma 5.3, we only need to show that

\begin{equation}

\sup_{x\in D}\left|f_n(x)- Ef_n(x)\right|=o(1) \textrm{~in~ probability.}

\end{equation}

\begin{equation}

\sup_{x\in D}\left|f_n(x)- Ef_n(x)\right|=o(1) \textrm{~in~ probability.}

\end{equation} Since  $D$ is a compact subset of

$D$ is a compact subset of  $\mathbb{R}$, we may denote

$\mathbb{R}$, we may denote  $D=[-d, d]$ for some constant

$D=[-d, d]$ for some constant  $d \gt 0$. Let

$d \gt 0$. Let  $r_n=\lfloor d/b_n\rfloor+1$. Since

$r_n=\lfloor d/b_n\rfloor+1$. Since  $U_{nj}=\left[(j-1/2)b_n, (j+1/2)b_n\right)$, we have

$U_{nj}=\left[(j-1/2)b_n, (j+1/2)b_n\right)$, we have  $D\subseteq \bigcup_{j=-r_n}^{r_n}U_{nj}$.

$D\subseteq \bigcup_{j=-r_n}^{r_n}U_{nj}$.

Similar to the proof of Theorem 2.2, we obtain that  $EV_j^2\leq Ck_nb_n $ and

$EV_j^2\leq Ck_nb_n $ and  $ \sigma_n^2 \leq C b_n$, and thus for any

$ \sigma_n^2 \leq C b_n$, and thus for any  $\varepsilon \gt 0$,

$\varepsilon \gt 0$,

\begin{align}&P\left(\sup_{x\in D} \left|f_n(x)- Ef_n(x)\right| \gt \varepsilon\right)\nonumber\\

&\leq P\left(\max_{-r_n\leq j\leq r_n}\sup_{x\in U_{nj}} \left|f_n(x)- Ef_n(x)\right| \gt \varepsilon\right)\nonumber\\

&\leq \sum_{j= -r_n}^{r_n}P\left(\sup_{x\in U_{nj}} \left|f_n(x)- Ef_n(x)\right| \gt \varepsilon\right)\nonumber\\

&=\sum_{j= -r_n}^{r_n} P\left( \sup_{x\in U_{nj}} \left|a_{n,j;1}\sum\limits_{i=1}^{n}Z_{n,j;i}+a_{n,j;2}\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt nb_n\varepsilon\right) \nonumber\\

&\leq\sum_{j= -r_n}^{r_n}P\left( \sup_{x\in U_{nj}} \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_n\varepsilon}{2a_{n,j;1}}\right) +\sum_{j= -r_n}^{r_n}P\left( \sup_{x\in U_{nj}} \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_n\varepsilon}{2a_{n,j;2}}\right)\nonumber\\

&\leq\sum_{j= -r_n}^{r_n}P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_n\varepsilon}{2 }\right) +\sum_{j= -r_n}^{r_n}P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_n\varepsilon}{2 }\right)\end{align}

\begin{align}&P\left(\sup_{x\in D} \left|f_n(x)- Ef_n(x)\right| \gt \varepsilon\right)\nonumber\\

&\leq P\left(\max_{-r_n\leq j\leq r_n}\sup_{x\in U_{nj}} \left|f_n(x)- Ef_n(x)\right| \gt \varepsilon\right)\nonumber\\

&\leq \sum_{j= -r_n}^{r_n}P\left(\sup_{x\in U_{nj}} \left|f_n(x)- Ef_n(x)\right| \gt \varepsilon\right)\nonumber\\

&=\sum_{j= -r_n}^{r_n} P\left( \sup_{x\in U_{nj}} \left|a_{n,j;1}\sum\limits_{i=1}^{n}Z_{n,j;i}+a_{n,j;2}\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt nb_n\varepsilon\right) \nonumber\\

&\leq\sum_{j= -r_n}^{r_n}P\left( \sup_{x\in U_{nj}} \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_n\varepsilon}{2a_{n,j;1}}\right) +\sum_{j= -r_n}^{r_n}P\left( \sup_{x\in U_{nj}} \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_n\varepsilon}{2a_{n,j;2}}\right)\nonumber\\

&\leq\sum_{j= -r_n}^{r_n}P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_n\varepsilon}{2 }\right) +\sum_{j= -r_n}^{r_n}P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_n\varepsilon}{2 }\right)\end{align}and

\begin{eqnarray}\sum_{j= -r_n}^{r_n}P\left( \left|\sum\limits_{i=1}^{n}Z_{nj;i} \right| \gt \frac{nb_n\varepsilon}{2 }\right) &\leq& C\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ -\frac{ \varepsilon^2}{24\left( \frac{C}{nb_n} +\frac{k_n}{nb_n} \varepsilon\right)}\right\}+C b_n^{-1} k_n^{-\lambda}\right\}.\end{eqnarray}

\begin{eqnarray}\sum_{j= -r_n}^{r_n}P\left( \left|\sum\limits_{i=1}^{n}Z_{nj;i} \right| \gt \frac{nb_n\varepsilon}{2 }\right) &\leq& C\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ -\frac{ \varepsilon^2}{24\left( \frac{C}{nb_n} +\frac{k_n}{nb_n} \varepsilon\right)}\right\}+C b_n^{-1} k_n^{-\lambda}\right\}.\end{eqnarray} It is clear that  $r_n=\left\lfloor d/b_n\right\rfloor+1\leq Cb_n^{-1}$ and

$r_n=\left\lfloor d/b_n\right\rfloor+1\leq Cb_n^{-1}$ and  $nb_n\to \infty$ as

$nb_n\to \infty$ as  $n\to \infty$. Taking

$n\to \infty$. Taking  $k_n=\frac{nb_n \varepsilon}{48\log n}$, we can obtain by (2.3) that the RHS of (6.8) is less than

$k_n=\frac{nb_n \varepsilon}{48\log n}$, we can obtain by (2.3) that the RHS of (6.8) is less than

\begin{align}

Cr_n \exp\left\{ -\frac{ \varepsilon^2\log n}{24\left(\frac{\varepsilon^2}{48} +\frac{\varepsilon^2}{48}\right)}\right\}+Cr_n b_n^{-1} k_n^{-\lambda}

&\leq Cr_n\exp\left\{-\log n\right\}+Cr_n b_n^{-1} k_n^{-\lambda}\nonumber\\

&\leq Cr_nn^{-1}+Cr_n b_n^{-1}(nb_n )^{-\lambda} (\log n)^{\lambda}\nonumber\\

&\leq Cb_n^{-1} n^{-1} +C g(n, 2)=o(1).

\end{align}

\begin{align}

Cr_n \exp\left\{ -\frac{ \varepsilon^2\log n}{24\left(\frac{\varepsilon^2}{48} +\frac{\varepsilon^2}{48}\right)}\right\}+Cr_n b_n^{-1} k_n^{-\lambda}

&\leq Cr_n\exp\left\{-\log n\right\}+Cr_n b_n^{-1} k_n^{-\lambda}\nonumber\\

&\leq Cr_nn^{-1}+Cr_n b_n^{-1}(nb_n )^{-\lambda} (\log n)^{\lambda}\nonumber\\

&\leq Cb_n^{-1} n^{-1} +C g(n, 2)=o(1).

\end{align}Similarly, we have

\begin{equation}

\sum_{j= -r_n}^{r_n}P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_n\varepsilon}{2 }\right) =o(1),

\end{equation}

\begin{equation}

\sum_{j= -r_n}^{r_n}P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_n\varepsilon}{2 }\right) =o(1),

\end{equation}which together with (6.7)–(6.9) yields (6.6).

Next, we prove (2.5). Recalling that  $T_{n}=(-\infty,-n^T)\bigcup (n^T,\infty)$, we have

$T_{n}=(-\infty,-n^T)\bigcup (n^T,\infty)$, we have

\begin{align}\sup_{x\in \mathbb{R}} \left|f_n(x)- f(x)\right|&\leq \sup_{x\in [-n^T,n^T]} \left|f_n(x)- Ef_n(x)\right|+\sup_{x\in [-n^T,n^T]} \left|Ef_n(x)- f(x)\right|\nonumber\\

&\quad +\sup_{x\in T_n} \left|f_n(x)- f(x)\right|.\end{align}

\begin{align}\sup_{x\in \mathbb{R}} \left|f_n(x)- f(x)\right|&\leq \sup_{x\in [-n^T,n^T]} \left|f_n(x)- Ef_n(x)\right|+\sup_{x\in [-n^T,n^T]} \left|Ef_n(x)- f(x)\right|\nonumber\\

&\quad +\sup_{x\in T_n} \left|f_n(x)- f(x)\right|.\end{align}Lemma 5.3 yields that

\begin{equation}

\sup_{x\in [-n^T,n^T]} \left|Ef_n(x)- f(x)\right|=O\left(b_n \right)=o(1).

\end{equation}

\begin{equation}

\sup_{x\in [-n^T,n^T]} \left|Ef_n(x)- f(x)\right|=O\left(b_n \right)=o(1).

\end{equation}It follows from Lemma 5.4 that

\begin{align}\sup_{x\in T_n} \left|f_n(x)- f(x)\right|&\leq \sup_{x\in T_n}f_n(x)+\sup_{x\in T_n}f (x)=O_P\left(R_n\right)+O\left( n^{-(1+T)}\right)\nonumber\\

&=o(1),\textrm{~in~ probability}.\end{align}

\begin{align}\sup_{x\in T_n} \left|f_n(x)- f(x)\right|&\leq \sup_{x\in T_n}f_n(x)+\sup_{x\in T_n}f (x)=O_P\left(R_n\right)+O\left( n^{-(1+T)}\right)\nonumber\\

&=o(1),\textrm{~in~ probability}.\end{align}So if we want to prove

\begin{equation}

\lim_{n\to \infty}P\left(\sup_{x\in \mathbb{R}} \left|f_n(x)- Ef_n(x)\right| \gt 3\varepsilon\right)=0,

\end{equation}

\begin{equation}

\lim_{n\to \infty}P\left(\sup_{x\in \mathbb{R}} \left|f_n(x)- Ef_n(x)\right| \gt 3\varepsilon\right)=0,

\end{equation}it suffices to prove

\begin{equation}

\lim_{n\to \infty}P\left( \sup_{x\in [-n^T,n^T]} \left|f_n(x)- Ef_n(x)\right| \gt \varepsilon\right)=0.

\end{equation}

\begin{equation}

\lim_{n\to \infty}P\left( \sup_{x\in [-n^T,n^T]} \left|f_n(x)- Ef_n(x)\right| \gt \varepsilon\right)=0.

\end{equation} Let  $D=[-n^T, n^T]$ and

$D=[-n^T, n^T]$ and  $r_n=\left\lfloor n^T/b_n\right\rfloor+1\leq Cn^T b_n^{-1}$. Similar to (6.7)–(6.8), we obtain

$r_n=\left\lfloor n^T/b_n\right\rfloor+1\leq Cn^T b_n^{-1}$. Similar to (6.7)–(6.8), we obtain

\begin{align}

&P\left( \sup_{x\in [-n^T,n^T]} \left|f_n(x)- Ef_n(x)\right| \gt \varepsilon\right)\nonumber\\

&\leq P\left(\max_{-r_n\leq j\leq r_n}\sup_{x\in U_{nj}} \left|f_n(x)- Ef_n(x)\right| \gt \varepsilon\right)\nonumber\\

&\leq \sum_{j= -r_n}^{r_n}P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_n\varepsilon}{2 }\right) +\sum_{j= -r_n}^{r_n}P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_n\varepsilon}{2 }\right)

\end{align}

\begin{align}

&P\left( \sup_{x\in [-n^T,n^T]} \left|f_n(x)- Ef_n(x)\right| \gt \varepsilon\right)\nonumber\\

&\leq P\left(\max_{-r_n\leq j\leq r_n}\sup_{x\in U_{nj}} \left|f_n(x)- Ef_n(x)\right| \gt \varepsilon\right)\nonumber\\

&\leq \sum_{j= -r_n}^{r_n}P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_n\varepsilon}{2 }\right) +\sum_{j= -r_n}^{r_n}P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_n\varepsilon}{2 }\right)

\end{align}and

\begin{align}\sum_{j= -r_n}^{r_n} P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_n\varepsilon}{2 }\right)

&\leq C\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ -\frac{ \varepsilon^2}{24\left( \frac{C}{nb_n} +\frac{k_n}{nb_n} \varepsilon\right)}\right\}+C b_n^{-1} k_n^{-\lambda}\right\}.\nonumber\\\end{align}

\begin{align}\sum_{j= -r_n}^{r_n} P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_n\varepsilon}{2 }\right)

&\leq C\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ -\frac{ \varepsilon^2}{24\left( \frac{C}{nb_n} +\frac{k_n}{nb_n} \varepsilon\right)}\right\}+C b_n^{-1} k_n^{-\lambda}\right\}.\nonumber\\\end{align} Taking  $k_n=\frac{nb_n \varepsilon}{48(T+1)\log n}$, the RHS of (6.17) is less than

$k_n=\frac{nb_n \varepsilon}{48(T+1)\log n}$, the RHS of (6.17) is less than

\begin{align}

Cr_n \exp\left\{ -\frac{ \varepsilon^2 (T+1)\log n}{24\left(\frac{\varepsilon^2}{48} +\frac{\varepsilon^2}{48}\right)}\right\}+Cr_n b_n^{-1} k_n^{-\lambda}

&\leq Cr_n\exp\left\{-(T+1)\log n\right\}+Cr_n b_n^{-1} k_n^{-\lambda}\nonumber\\

&\leq Cn^Tb_n^{-1} n^{-(T+1)} +C n^T b_n^{-(2+\lambda)} n^{-\lambda} \left( \log n\right)^{\lambda}\nonumber\\

&\leq Cn^Tb_n^{-1} n^{-(T+1)} +Cn^T g(n, 2)=o(1).

\end{align}

\begin{align}

Cr_n \exp\left\{ -\frac{ \varepsilon^2 (T+1)\log n}{24\left(\frac{\varepsilon^2}{48} +\frac{\varepsilon^2}{48}\right)}\right\}+Cr_n b_n^{-1} k_n^{-\lambda}

&\leq Cr_n\exp\left\{-(T+1)\log n\right\}+Cr_n b_n^{-1} k_n^{-\lambda}\nonumber\\

&\leq Cn^Tb_n^{-1} n^{-(T+1)} +C n^T b_n^{-(2+\lambda)} n^{-\lambda} \left( \log n\right)^{\lambda}\nonumber\\

&\leq Cn^Tb_n^{-1} n^{-(T+1)} +Cn^T g(n, 2)=o(1).

\end{align}Similarly, we have

\begin{equation}

\sum_{j= -r_n}^{r_n}P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_n\varepsilon}{2 }\right) =o(1),

\end{equation}

\begin{equation}

\sum_{j= -r_n}^{r_n}P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_n\varepsilon}{2 }\right) =o(1),

\end{equation}which together with (6.16)–(6.18) yields (6.15).

Therefore, the proof of Theorem 2.4 is completed.

6.3. Proof of Theorem 2.7

Firstly, we prove (2.7). From Lemma 5.3, it suffices to show that

\begin{equation}

\sup_{x\in D}\left|f_n(x)- Ef_n(x)\right|=O(R_n) \textrm{~in~ probability.}

\end{equation}

\begin{equation}

\sup_{x\in D}\left|f_n(x)- Ef_n(x)\right|=O(R_n) \textrm{~in~ probability.}

\end{equation} Recall that we denoted  $D=[-d, d]$ for some constant

$D=[-d, d]$ for some constant  $d \gt 0$ and set

$d \gt 0$ and set  $r_n=\lfloor d/b_n\rfloor+1$. It is easy to see that

$r_n=\lfloor d/b_n\rfloor+1$. It is easy to see that  $r_n=\lfloor d/b_n\rfloor+1\leq Cb_n^{-1}$ and

$r_n=\lfloor d/b_n\rfloor+1\leq Cb_n^{-1}$ and  $nb_n/ \log n\to \infty$ as

$nb_n/ \log n\to \infty$ as  $n\to \infty$. Let

$n\to \infty$. Let  $C_0$ be a positive constant, which will be specified later. Similar to (6.8), taking

$C_0$ be a positive constant, which will be specified later. Similar to (6.8), taking  $k_n=C_0^{-1} C_1\left(\frac{nb_n }{\log n}\right)^{1/2}$ and

$k_n=C_0^{-1} C_1\left(\frac{nb_n }{\log n}\right)^{1/2}$ and  $C_0=\sqrt{24\times7 C_1 } $, we obtain by (6.8) and (2.6) that

$C_0=\sqrt{24\times7 C_1 } $, we obtain by (6.8) and (2.6) that

\begin{align}&P\left( \sup_{x\in D} \left|f_n(x)- Ef_n(x)\right| \gt C_0R_n\right)

\leq P\left(\max_{-r_n\leq j\leq r_n}\sup_{x\in U_{nj}} \left|f_n(x)- Ef_n(x)\right| \gt C_0R_n\right)\nonumber\\

&\leq \sum_{j= -r_n}^{r_n} P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_nC_0R_n}{2 }\right) +\sum_{j= -r_n}^{r_n} P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_nC_0R_n}{2 }\right),\end{align}

\begin{align}&P\left( \sup_{x\in D} \left|f_n(x)- Ef_n(x)\right| \gt C_0R_n\right)

\leq P\left(\max_{-r_n\leq j\leq r_n}\sup_{x\in U_{nj}} \left|f_n(x)- Ef_n(x)\right| \gt C_0R_n\right)\nonumber\\

&\leq \sum_{j= -r_n}^{r_n} P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_nC_0R_n}{2 }\right) +\sum_{j= -r_n}^{r_n} P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_nC_0R_n}{2 }\right),\end{align}and the former of the RHS of (6.21) is less than

\begin{align}& 4\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ -\frac{ n b_n^2C_0^2R_n^2}{24\left(6\sigma_n^2 + k_n b_n C_0R_n\right)}\right\}+72 C_0^{-1}R_n^{-1}b_n^{-1} k_n^{-\lambda}\right\}\nonumber\\

&\leq 4\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ -\frac{ n b_nC_0^2R_n^2 }{24\left(6C_1 + k_n C_0R_n\right)}\right\}+CR_n^{-1}b_n^{-1} k_n^{-\lambda}\right\}\nonumber\\

&\leq 4\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ -\frac{C_0^2R_n^2 \log n }{24\left[6C_1 \frac{\log n}{n b_n} + C_1 \left(\frac{\log n}{n b_n}\right)^{1/2}R_n\right]}\right\}+CR_n^{-1}b_n^{-1} k_n^{-\lambda}\right\}\nonumber\\

&= 4\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ -\frac{ C_0^2R_n^2 \log n }{24\left[6C_1 R_n^2 + C_1 R_n^2\right] }\right\}+CR_n^{-1}b_n^{-1} k_n^{-\lambda}\right\}\nonumber\\

&\leq 4\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ - \log n \right\}+C\left(\frac{\log n}{n b_n}\right)^{-1/2} b_n^{-1} \left(\frac{n b_n}{\log n}\right)^{-\lambda/2} \right\}\nonumber\\

&\leq C n^{-1}b_n^{-1} + C b_n^{-2} \left(\frac{n b_n}{\log n}\right)^{-\lambda/2+1/2}=C n^{-1}b_n^{-1}+C g(n, 3)=o(1).\end{align}

\begin{align}& 4\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ -\frac{ n b_n^2C_0^2R_n^2}{24\left(6\sigma_n^2 + k_n b_n C_0R_n\right)}\right\}+72 C_0^{-1}R_n^{-1}b_n^{-1} k_n^{-\lambda}\right\}\nonumber\\

&\leq 4\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ -\frac{ n b_nC_0^2R_n^2 }{24\left(6C_1 + k_n C_0R_n\right)}\right\}+CR_n^{-1}b_n^{-1} k_n^{-\lambda}\right\}\nonumber\\

&\leq 4\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ -\frac{C_0^2R_n^2 \log n }{24\left[6C_1 \frac{\log n}{n b_n} + C_1 \left(\frac{\log n}{n b_n}\right)^{1/2}R_n\right]}\right\}+CR_n^{-1}b_n^{-1} k_n^{-\lambda}\right\}\nonumber\\

&= 4\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ -\frac{ C_0^2R_n^2 \log n }{24\left[6C_1 R_n^2 + C_1 R_n^2\right] }\right\}+CR_n^{-1}b_n^{-1} k_n^{-\lambda}\right\}\nonumber\\

&\leq 4\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ - \log n \right\}+C\left(\frac{\log n}{n b_n}\right)^{-1/2} b_n^{-1} \left(\frac{n b_n}{\log n}\right)^{-\lambda/2} \right\}\nonumber\\

&\leq C n^{-1}b_n^{-1} + C b_n^{-2} \left(\frac{n b_n}{\log n}\right)^{-\lambda/2+1/2}=C n^{-1}b_n^{-1}+C g(n, 3)=o(1).\end{align} Similarly, the latter of the RHS of (6.21) tends to zero as  $n$ tends to infinity, that is,

$n$ tends to infinity, that is,

\begin{equation}

\sum_{j= -r_n}^{r_n} P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_nC_0R_n}{2 }\right)=o(1),

\end{equation}

\begin{equation}

\sum_{j= -r_n}^{r_n} P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_nC_0R_n}{2 }\right)=o(1),

\end{equation}which together with (6.21)–(6.22) yields (6.20).

Next, we prove (2.8). Recall that  $T_{n}=(-\infty,-n^T)\bigcup (n^T,\infty)$ and

$T_{n}=(-\infty,-n^T)\bigcup (n^T,\infty)$ and

\begin{eqnarray}\sup_{x\in \mathbb{R}} \left|f_n(x)- f(x)\right|&\leq& \sup_{x\in [-n^T,n^T]} \left|f_n(x)- Ef_n(x)\right|+\sup_{x\in [-n^T,n^T]} \left|Ef_n(x)- f(x)\right|\nonumber\\

&&+\sup_{x\in T_n} \left|f_n(x)- f(x)\right|.\end{eqnarray}

\begin{eqnarray}\sup_{x\in \mathbb{R}} \left|f_n(x)- f(x)\right|&\leq& \sup_{x\in [-n^T,n^T]} \left|f_n(x)- Ef_n(x)\right|+\sup_{x\in [-n^T,n^T]} \left|Ef_n(x)- f(x)\right|\nonumber\\

&&+\sup_{x\in T_n} \left|f_n(x)- f(x)\right|.\end{eqnarray}Similar to (6.12)–(6.13) in the proof of Theorem 2.4(2), if we want to prove

\begin{equation}

\lim_{n\to \infty}P\left(\sup_{x\in \mathbb{R}} \left|f_n(x)- Ef_n(x)\right| \gt 3C_0R_n\right)=0,

\end{equation}

\begin{equation}

\lim_{n\to \infty}P\left(\sup_{x\in \mathbb{R}} \left|f_n(x)- Ef_n(x)\right| \gt 3C_0R_n\right)=0,

\end{equation}it suffices to prove

\begin{equation}

\lim_{n\to \infty}P\left( \sup_{x\in [-n^T,n^T]} \left|f_n(x)- Ef_n(x)\right| \gt C_0R_n\right)=0.

\end{equation}

\begin{equation}

\lim_{n\to \infty}P\left( \sup_{x\in [-n^T,n^T]} \left|f_n(x)- Ef_n(x)\right| \gt C_0R_n\right)=0.

\end{equation} Let  $D=[-n^T, n^T]$ and

$D=[-n^T, n^T]$ and  $r_n=\left\lfloor n^T/b_n\right\rfloor+1\leq Cn^T b_n^{-1}$. Similar to (6.21)–(6.22), we obtain by taking

$r_n=\left\lfloor n^T/b_n\right\rfloor+1\leq Cn^T b_n^{-1}$. Similar to (6.21)–(6.22), we obtain by taking  $k_n=C_0^{-1} C_1\left(\frac{nb_n }{\log n}\right)^{1/2}$ and

$k_n=C_0^{-1} C_1\left(\frac{nb_n }{\log n}\right)^{1/2}$ and  $C_0=\sqrt{24\times7(T+1) C_1 } $ that

$C_0=\sqrt{24\times7(T+1) C_1 } $ that

\begin{align}&P\left( \sup_{x\in [-n^T,n^T]} \left|f_n(x)- Ef_n(x)\right| \gt C_0R_n\right)\nonumber\\

&\leq \sum_{j= -r_n}^{r_n} P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_nC_0R_n}{2 }\right)+ \sum_{j= -r_n}^{r_n} P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_nC_0R_n}{2 }\right),\end{align}

\begin{align}&P\left( \sup_{x\in [-n^T,n^T]} \left|f_n(x)- Ef_n(x)\right| \gt C_0R_n\right)\nonumber\\

&\leq \sum_{j= -r_n}^{r_n} P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_nC_0R_n}{2 }\right)+ \sum_{j= -r_n}^{r_n} P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_nC_0R_n}{2 }\right),\end{align}and

\begin{align}

\sum_{j= -r_n}^{r_n} P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_nC_0R_n}{2 }\right)

&\leq 4\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ -\frac{ C_0^2R_n^2 \log n }{24\left[6 C_1 R_n^2 + C_1R_n^2\right] }\right\}+CR_n^{-1}b_n^{-1} k_n^{-\lambda}\right\}\nonumber\\

&\leq 4\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ -(T+1) \log n \right\}+C b_n^{-1} \left(\frac{n b_n}{\log n}\right)^{-\lambda/2+1/2} \right\}\nonumber\\

&\leq Cn^Tb_n^{-1} n^{-(T+1)} +Cn^T g(n, 3)=o(1).

\end{align}

\begin{align}

\sum_{j= -r_n}^{r_n} P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j;i} \right| \gt \frac{nb_nC_0R_n}{2 }\right)

&\leq 4\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ -\frac{ C_0^2R_n^2 \log n }{24\left[6 C_1 R_n^2 + C_1R_n^2\right] }\right\}+CR_n^{-1}b_n^{-1} k_n^{-\lambda}\right\}\nonumber\\

&\leq 4\sum_{j= -r_n}^{r_n} \left\{\exp\left\{ -(T+1) \log n \right\}+C b_n^{-1} \left(\frac{n b_n}{\log n}\right)^{-\lambda/2+1/2} \right\}\nonumber\\

&\leq Cn^Tb_n^{-1} n^{-(T+1)} +Cn^T g(n, 3)=o(1).

\end{align}Analogously, we have

\begin{equation}

\sum_{j= -r_n}^{r_n} P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_nC_0R_n}{2 }\right)=o(1),

\end{equation}

\begin{equation}

\sum_{j= -r_n}^{r_n} P\left( \left|\sum\limits_{i=1}^{n}Z_{n,j+1;i} \right| \gt \frac{nb_nC_0R_n}{2 }\right)=o(1),

\end{equation}which together with (6.27)–(6.28) yields (6.26).

Therefore, the proof of Theorem 2.7 is completed.

Acknowledgements

The authors are most grateful to the Editor and anonymous referees for carefully reading the manuscript and for valuable suggestions, which helped in improving an earlier version of this paper.

Funding

This work was supported by the National Natural Science Foundation of China (12471248, 12301181, 12361031, 12201600), the Natural Science Youth Project of Anhui Provincial Department of Education (2025AHGXZK40092), and the Chizhou University High-Level Talent Research Start-up Fund (CZ2024YJRC05).

Conflict of interest statement

We declare that we have no conflict of interest.

Open access

Open access