INTRODUCTION

As the world watched Russia launch its full-scale invasion of Ukraine on February 24, 2022, more than 40,000 foreign-invested firms were operating in the country, according to novel data introduced in this article. Almost overnight, an unprecedented array of state and non-state actors demanded answers: would these firms exit Russia? For example, we document “name, praise, and shame” lists of thousands of firms circulating online, compiled by scholar-activists and grassroots groups and with titles, such as “Boycott Russia” and “Squeezing Putin.”Footnote 1 The possibility of mass exodus of foreign direct investment (FDI) also triggered angst in Russia; anti-exit/pro-Russia lists included one titled #WeRememberEverything. Foreign-invested firms confronted a dilemma: follow pro-exit pressure and withdraw from the Russian market, or stay and weather this extraordinary realization of political risk.

Under contemporary economic globalization, capital flight has always concerned so-called hot money in short-term portfolio investment, with FDI as the stable cousin on which many developing states’ long-term economic development plans have rested (Dunning and Lundan Reference Dunning and Lundan2008). A sudden, economy-wide outflow of FDI in response to a common political shock has been thought unrealistic. Although, while FDI is often treated as an aggregate capital flow, the statistic in fact reflects the decisions of individual foreign-invested firms, each holding differentiated assets and embedded in distinct commercial and political relationships.Footnote 2 Moreover, foreign-invested firms are autonomous actors with decision-making authority over the assets they already own and operate abroad. While a coalition of states has initiated an unprecedented breadth of coordinated sanctions against Russia, pre-existing foreign investments in Russia have been predominately outside their scope, underscoring that the choice over exit is not simply a matter of legal compliance.

From the Russian point of view, that each foreign-invested firm was suddenly, simultaneously pondering exit risked deep disruptions to the highly-integrated economy. It became clear that the Putin administration was not responding with a strategy of mass expropriation, which may have risked irreparable damage to Russia’s long-term reputation. Instead, in short order, the Putin administration set up legalized, bureaucratic mechanisms that have allowed the Russian state to interfere with foreign-invested firms’ ability to voluntarily exit. Conceptually, policies that restrict FDI exit in response to the risk of widespread FDI flight are analogous to capital controls deployed in response to the risk of a sudden stop in capital markets (Edwards Reference Edwards2007).

In short, after Russia’s full-scale invasion of Ukraine foreign-invested firms faced multifaceted pressures to make the voluntary choice to exit, as well as limitations on the ability to do so. To theorize the factors at play and evaluate their net effects, we recognize that exit involves a transaction, in which a foreign-invested firm chooses to sell its assets to some buyer at some terms. In this time of war, sellers, buyers, and terms are deeply politicized. Building on the exit-as-a-transaction framework, we examine both the pressures firms face to exit and the terms under which exit occurs. All else equal, firms experiencing greater pressure to sell are more likely to do so, as are firms that can negotiate more favorable terms. We conceptualize exit pressure along political, social, and economic dimensions, including home-state pressure, exposure to activism, and dependence on consumer markets. We use factors shaping host–firm interactions to consider bargaining terms, including Russia’s ability to exert managerial control, the strategic importance of a firm’s assets, and the mobility of those assets.

This normatively consequential and theoretically unprecedented setting allows us to assess observable implications derived from our framework. We use firm registrations and official record-keeping to construct our sample of foreign-invested firms in Russia prior to the full-scale invasion (as of December 31, 2021). We then compare these firms’ pre-invasion owners to those after 18 months of conflict (as of August 31, 2023). We find that 33.3% of foreign-invested firms exited by this point, meaning that the firm was no longer in operation under the same foreign ownership.Footnote 3 This aggregate exit rate is indeed higher than historical rates, which we also compile; prior to the study period, the annual exit rate had been declining for several years to 25.3% in the immediate pre-invasion period (2020–21).Footnote 4 We construct a variety of novel measures to examine the determinants of exit in the immediate post-invasion period.

Regarding theory on sellers’ motivations, our top-line finding is that foreign-invested firms in consumer-oriented industries are more likely to exit. Whereas, our results suggest tempering expectations over the effect of generalized social backlash on exit. Specifically, we match 16.3% of pre-invasion foreign-invested firms to “name, praise, and shame” lists that circulated on the Internet, but the results show that matched firms are in fact less likely to exit Russia. Further, we find little to no evidence that home state economic statecraft vis-à-vis Russia predicts exit. On foreign-invested firms’ bargaining power, we find compelling evidence that Russian state interests influence outcomes. We expect that the Russian state is indifferent to or even supportive of exit if there is domestic Russian capacity to operate the business absent foreign ownership. We find support for the observable implication that investors in foreign-domestic joint ventures already under Russian managerial control were more likely to exit in the study period. In contrast, we expect that the Russian state is opposed to exit if and when foreign owners are instrumental to the business. We find support for the observable implication that foreign-invested firms operating in industries deemed strategic by Russia are less likely to exit in the study period.Footnote 5 Additionally, we find some evidence that the intensity of fixed assets in a firm’s industry, which theory suggests decreases the credibility of the threat of exit, also reduces the likelihood of exit.

Our study speaks to two strands of literature. First, there is renewed interest in the geopolitical implications of economic interdependence (Aggarwal and Reddie Reference Aggarwal and Reddie2021; Aiginger and Rodrik Reference Aiginger and Rodrik2020; Farrell and Newman Reference Farrell and Newman2019). A central argument is that states may leverage their positions within global economic networks in pursuit of political objectives. One point our study makes clear is that in the contemporary era of economic globalization, multinationals are, at best, unstable tools of economic statecraft, even in the midst of interstate war.

Second, our findings underscore the need for a better understanding of firm exit within the political economy of FDI. Much nuanced work examines the conditions under which MNCs enter new markets abroad (see Pandya Reference Pandya2016 for a review). In contrast, the field’s understanding of MNCs exiting markets remains deeply rooted in the classic obsolescing bargain model (Vernon Reference Vernon1971), which speaks to expropriation—a situation in which exit is not voluntary. We argue that exit should be conceptualized as a transaction through which firms seek to recover value from their invested assets. The exit-as-transaction framework can accommodate expropriation, wherein the host state coerces a sale at nonmarket terms to a non-preferred buyer (Hajzler Reference Hajzler2012; Jensen et al. Reference Jensen, Johnston, Lee and Sahin2020; Li Reference Li2009; Mahdavi Reference Mahdavi2014). Crucially, the framework can also accommodate voluntary divestment, wherein MNCs choose to sell (Boddewyn Reference Boddewyn1983; Sethuram and Gaur Reference Sethuram and Gaur2024). Our generalizable framework is even more important in light of economic statecraft efforts, demands for re-shoring, and generally shifting geopolitical dynamics, all of which have profound implications for the organization of global production (Antràs Reference Antràs2020; Baldwin and Freeman Reference Baldwin and Freeman2022).

In what follows, we situate our study in the literatures on FDI and nonmarket strategy, operationalize exit, derive hypotheses using an exit-as-a-transaction framework, and present results. We close by considering implications for both security and development.

LITERATURE

Research on the political economy of FDI has been cultivating theories that are all the more salient in these exceptional circumstances concerning a state deeply integrated into the contemporary global economy. Scholarship connects foreign investor decision-making and security, in contexts, including territorial conflict, civil unrest, and war (e.g., Braithwaite, Kucik, and Maves Reference Braithwaite, Kucik and Maves2014; Carter, Wellhausen, and Huth Reference Carter, Wellhausen and Huth2019; Lee and Mitchell Reference Lee and Mitchell2012; Pinto and Zhu Reference Pinto and Zhu2022). Much of this work examines the conditions under which MNCs make investments, although the literature teaches us to be circumspect over whether theories of entry are informative over the lifecycle of an investment (Barry Reference Barry2018; Reference Barry2025; Cefis et al. Reference Cefis, Bettinelli, Coad and Marsili2022; Farrell and Newman Reference Farrell and Newman2015; Wellhausen Reference Wellhausen2019).Footnote 6

The concept of the threat of exit, and the determinants of its credibility, is core to our understanding of foreign firm-host state relations. While the conditions at entry can privilege foreign firms in their bargains with host states, those bargains can obsolesce over time, such that power to break or renegotiate the deal shifts to the host (Vernon Reference Vernon1971). In particular, foreign firms that are reliant on fixed—alternatively known as immobile, site-specific, or non-redeployable—assets in the host state are expected to have little credibility should they threaten to exit (Frieden Reference Frieden1994; Pond and Zafeiridou Reference Pond and Zafeiridou2020; Wright and Zhu Reference Wright and Zhu2018). What has not happened in the modern era, and thus never been directly examined, is a mass of foreign-invested firms operating in many industries across a deeply integrated economy looking to make good on the threat of exit at the same time.Footnote 7 Crucially, foreign firms’ physical assets in Russia are not directly threatened by wartime violence, such that from a research design perspective we can avoid the confounding effects of war on physical assets, instead considering effects of the ex ante credibility of the threat of exit operating via a shock to political risk.Footnote 8

A growing literature identifies firm nationality as a key determinant of variation in political risk exposure. Empirical evidence suggests that dyadic political (dis)alignment between the home and host state can drive firm decision-making at entry and, by implication, host government treatment over the life of the investment (Li and Vashchilko Reference Li and Vashchilko2010; Stone, Wang, and Yu Reference Stone, Wang and Yu2022).Footnote 9 The institutional embeddedness literature suggests that emerging-market firms, most of which originate in poorly governed states, possess competitive advantages in weak institutional environments abroad (Cuervo-Cazurra and Genc Reference Cuervo-Cazurra and Genc2008), whereas firms coming from states with stronger institutions tend to favor destinations with similar legal environments (Beazer and Blake Reference Beazer and Blake2018; Reference Beazer and Blake2021). Nationality also demarcates the resources on which a firm can draw for political risk mitigation, given that diplomacy, international legal institutions, or more coercive means of investment protection are heterogeneous by national origin (Polanco Reference Polanco2019; Wellhausen Reference Wellhausen2015).

What might the literature predict regarding Russia’s actions? The form of exit that has received the most attention is expropriation—when exit is not voluntary, but rather the result of a forced ownership transfer without due compensation (e.g., Jensen et al. Reference Jensen, Johnston, Lee and Sahin2020; Lipson Reference Lipson1985). Frankly, it came as a surprise to some observers that Russia did not engage in economy-wide expropriations in the study period, with four headline-grabbing expropriations of large foreign-invested firms serving as the exception that proved the rule (see “Bargaining over Terms” section, H2b, and Appendix 7.5 of the Supplementary Material). Instead, Russia rolled out a highly legalized set of adverse policies interfering with foreign-invested firms’ transactions (see Appendix 2 of the Supplementary Material). These are in fact reminiscent of other legalized or legal-adjacent approaches in the Russian domestic political economy (Gans-Morse Reference Gans-Morse2017; Logvinenko Reference Logvinenko2019; Reference Logvinenko2021; Szakonyi Reference Szakonyi2025). From the Russian point of view, the closest analog to the situation might be a sudden stop in capital markets (Edwards Reference Edwards2007). Here, foreign-invested firms are the first-movers in seeking exit, and Russia’s efforts to discriminate against sales of brownfield assets serve a purpose similar to capital controls.

Last, there are important literatures in the orbit of our study to which we cannot speak. Our focus is on the predictors of foreign-invested firm exit, and not the effectiveness of sanctions or any potential peace (or conflict) dividend of economic (dis)integration.Footnote 10 Scholars are also leveraging Russia to study the determinants of foreign firms’ announcements of their intentions and executives’ attitudes toward exit (Balyuk and Fedyk Reference Balyuk and Fedyk2023; Davis, Li, and Miyano Reference Davis, Li and Miyano2024; Gurkov, Filinov, and Saidov Reference Gurkov, Filinov and Saidov2024; Pham Reference Pham2025). With our study’s strong research design and comprehensive data, we push further to understand how an exogenous shock to political risk of this magnitude has, or has not, resulted in changed foreign-invested firm behavior in the form of divestment.

DATA: OPERATIONALIZING EXIT

We draw the list of foreign-invested firms in Russia as of the end of 2021. In terms of research design, at that time foreign-invested firms in Russia were operating in a “pretreatment” environment prior to the invasion that began on February 24, 2022.Footnote 11 Our sources are Bureau van Djik’s Orbis Historical Databases available from Moody’s Datahub (Bureau van Dijk Reference BureauN.d.), industry-leading products that compile company information from official and proprietary sources. What we call a foreign-invested firm is an enterprise with a unique Orbis identification number (BVD) that meets the international statistical standard for FDI. That is, foreign ownership in the enterprise meets or exceeds 10%, the agreed upon proxy to capture that foreign interests have meaningful managerial control over the enterprise. By our definition and these best-available data, there were 42,720 active foreign-invested firms in Russia on December 31, 2021; we designate this the pre-invasion sample.

Selection into the sample involves some complexities, discussed in Appendix 7.2 of the Supplementary Material. To summarize, our unit of analysis is the foreign-invested firm, which sits under a parent company.Footnote 12 Foreign-invested firms have one or more non-Russian shareholders that own at least a 10% stake. Put differently, this is a study of MNC subsidiaries, with a focus on outcomes at the subsidiary level, as subsidiaries are independent legal entities. If subsidiary-level information is insufficient, an observation is selected into the sample if its parent is not Russian. While Orbis is an industry-leading firm-level information provider, its limitations require analysts to validate rather than assume representativeness (Bajgar et al. Reference Bajgar, Berlingieri, Calligaris, Criscuolo and Timmis2020). In Appendices 8.2 and 8.3 of the Supplementary Material, we benchmark our data against figures reported by the Federal Tax Service (FTS) of Russia to demonstrate the validity and representativeness of our pre-invasion sample.Footnote 13 Replication data are available in Wellhausen and Zhu (Reference Wellhausen and Zhu2026).

Pre-Invasion Sample: Descriptive Characteristics

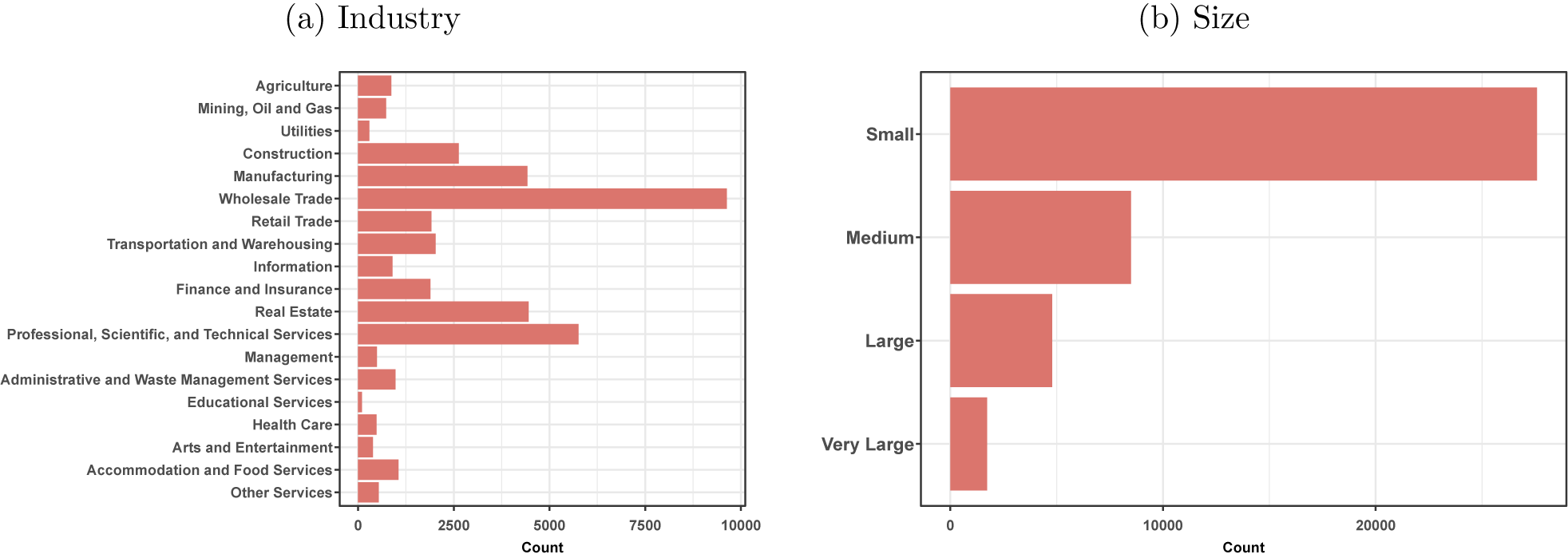

The pre-invasion sample is diverse on many metrics. Figure 1a shows that foreign-invested firms were present in all industries. On firm size, Figure 1b reveals the huge proportion of pre-invasion foreign-invested firms (64.8%) that are small, with less than one million EUR in revenue, two million EUR in assets, and/or 15 employees. Only 4.1% are very large, with over 100 million EUR in revenue, 200 million EUR in assets, and/or 1,000 employees.Footnote 14

Distribution of Foreign-Invested Firms by Industry and Size, Pre-Invasion Sample

Note: Bars indicate the count of foreign-invested firms as of the end of 2021. (a) Unique NAICS 2-digit industries. (b) Size definitions in Appendix 9 of the Supplementary Material. See Appendix 4 of the Supplementary Material for historical comparisons.

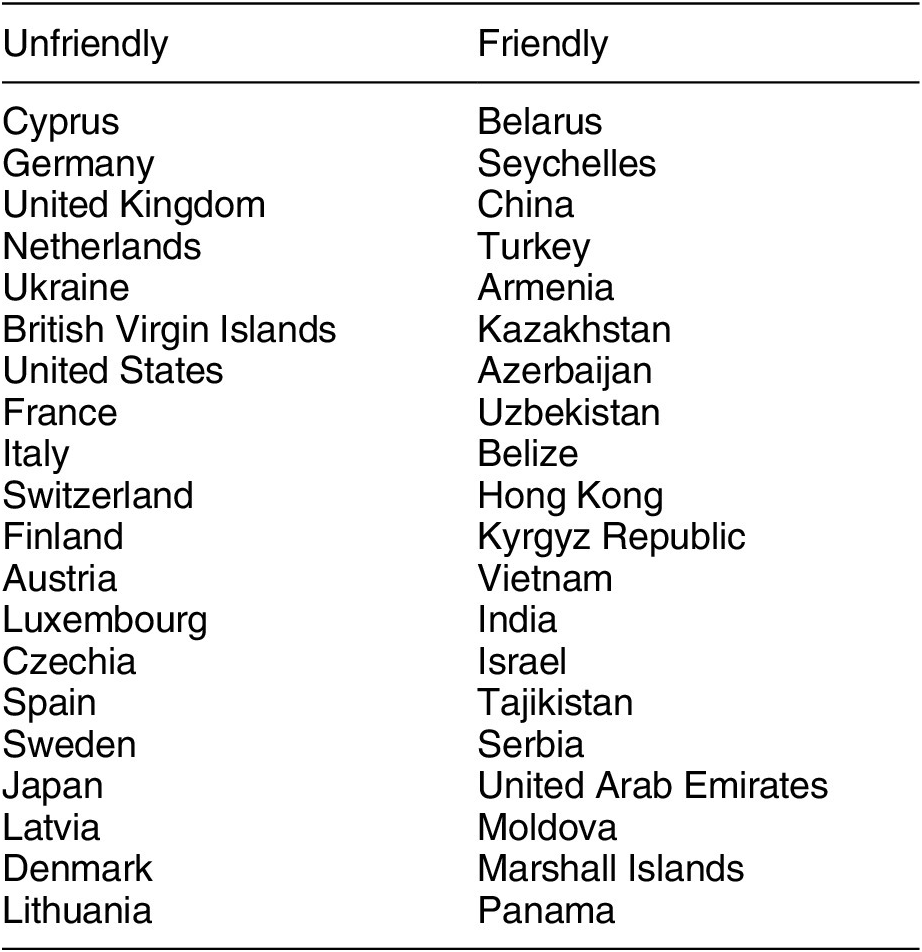

Foreign-invested firms originated from 132 jurisdictions, which we take as their nationality (see Appendix 7.4 of the Supplementary Material). To provide insight, we leverage Russia’s “Unfriendly Countries” List, which Russia began publishing 9 days after its full-scale invasion (Список недружественных стран, see Appendix 12.2 of the Supplementary Material). Jurisdictions on this list “commit unfriendly actions against Russia, its companies, and citizens.” In the data, 52 unique home jurisdictions are “unfriendly,” accounting for 75.5% of the pre-invasion sample. The remaining 24.5% comes from 80 unique “friendly” home jurisdictions. Table 1 reports the top 20 homes of each type.

Top 20 “Unfriendly” and “Friendly” Home States

Note: Of 52 “unfriendly” and 80 “friendly” homes in the pre-invasion sample (see Appendix 12.2 of the Supplementary Material).

In Appendix 4 of the Supplementary Material, we confirm that diversity across industry, size, and nationality has long been a hallmark of foreign-invested firms in Russia, highlighting continuity in comparison to the immediate pre-invasion period (2020) and prior to the beginning of Russian aggression against Ukraine (2013). Yes, McDonald’s in Russia has commanded attention as an FDI cultural touchstone, from queues at its opening in Moscow in 1990, to its exit via sale of its Russian operations to a domestic buyer in May 2022. Nonetheless, FDI in Russia has long concerned much more than American fast food.

Exit and Historical Context

To document exit, we compare the pre-invasion sample to its status after 18 months (August 31, 2023). Conceptually, FDI exit occurs when the foreign investor with meaningful managerial control at time t no longer exercises control at time

$ t+1 $

. Practically, that can happen in two ways: (a) the foreign-invested firm is defunct, such that its official status is “inactive” at

$ t+1 $

. Practically, that can happen in two ways: (a) the foreign-invested firm is defunct, such that its official status is “inactive” at

$ t+1 $

;Footnote

15 or, (b) the firm is active at

$ t+1 $

;Footnote

15 or, (b) the firm is active at

$ t+1 $

under different ownership. Assessing (a) is straightforward, whereas assessing (b) includes complexities, which we address in Appendix 7.3 of the Supplementary Material. In particular, to be sure we are coding meaningful exit of type (b), we compare ownership at t and

$ t+1 $

under different ownership. Assessing (a) is straightforward, whereas assessing (b) includes complexities, which we address in Appendix 7.3 of the Supplementary Material. In particular, to be sure we are coding meaningful exit of type (b), we compare ownership at t and

$ t+1 $

for both our unit of analysis and at the level of the parent. If the parent does not change, we suspect corporate reshuffling among the same owners and conservatively do not code exit.Footnote

16 Altogether, we find an aggregate exit rate of 33.3%, which is our primary dependent variable.

$ t+1 $

for both our unit of analysis and at the level of the parent. If the parent does not change, we suspect corporate reshuffling among the same owners and conservatively do not code exit.Footnote

16 Altogether, we find an aggregate exit rate of 33.3%, which is our primary dependent variable.

Before proceeding further, we adjudicate whether the 33.3% exit rate is high relative to historical rates of ownership churn in the Russian context. If it is high, we are more confident that this exogenous shock to political risk generated outcomes for which dedicated theorizing is required. We repeat the previous steps to draw samples and calculate exit rates between years t and

$ t+1 $

, for 2007–21.Footnote

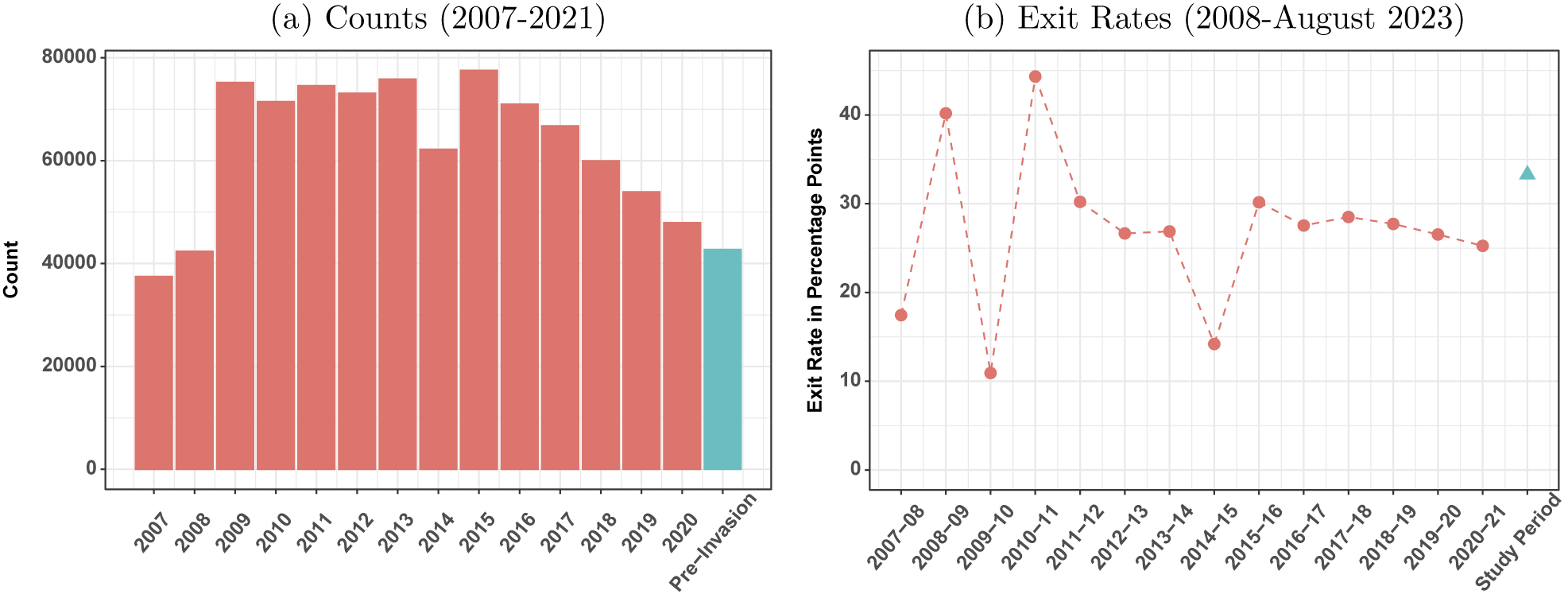

17 Figure 2a shows that the count of foreign-invested firms had declined and was relatively low pre-invasion, mitigating concern about an inflated denominator. Per Figure 2b, the annual exit rate had steadily declined, to 25.3% pre-invasion. The jump to 33.3% in the (18-month) study period is suggestive of an aberration from longer-term trends. An important point of historical comparison is to the beginning of Russian aggression against Ukraine in March 2014. The data suggest that any “exiting Russia” phenomenon was absent: although the count of firms in 2014 is conspicuously low, the 2013–14 exit rate is on par with the previous year, and the subsequent year brought a new high count and an outlier low exit rate. In combination with qualitative evidence of intense attention to firm decision-making after the full-scale invasion, this exercise leads us to conclude that the study period should be theorized in its own right. That said, we leverage data from 2020–21 and 2013–14 in placebo tests to further explore the uniqueness of the study period (see “Placebo Tests” section).

$ t+1 $

, for 2007–21.Footnote

17 Figure 2a shows that the count of foreign-invested firms had declined and was relatively low pre-invasion, mitigating concern about an inflated denominator. Per Figure 2b, the annual exit rate had steadily declined, to 25.3% pre-invasion. The jump to 33.3% in the (18-month) study period is suggestive of an aberration from longer-term trends. An important point of historical comparison is to the beginning of Russian aggression against Ukraine in March 2014. The data suggest that any “exiting Russia” phenomenon was absent: although the count of firms in 2014 is conspicuously low, the 2013–14 exit rate is on par with the previous year, and the subsequent year brought a new high count and an outlier low exit rate. In combination with qualitative evidence of intense attention to firm decision-making after the full-scale invasion, this exercise leads us to conclude that the study period should be theorized in its own right. That said, we leverage data from 2020–21 and 2013–14 in placebo tests to further explore the uniqueness of the study period (see “Placebo Tests” section).

Foreign-Invested Firms in Russia and Exit Rates

Note: (a) Bar values count active foreign-invested firms as of the end of each year. The pre-invasion sample, marked in a different color, corresponds to 2021. (b) Circles correspond to annual exit rates. The triangle indicates the exit rate for the 18-month study period (2021–August 2023).

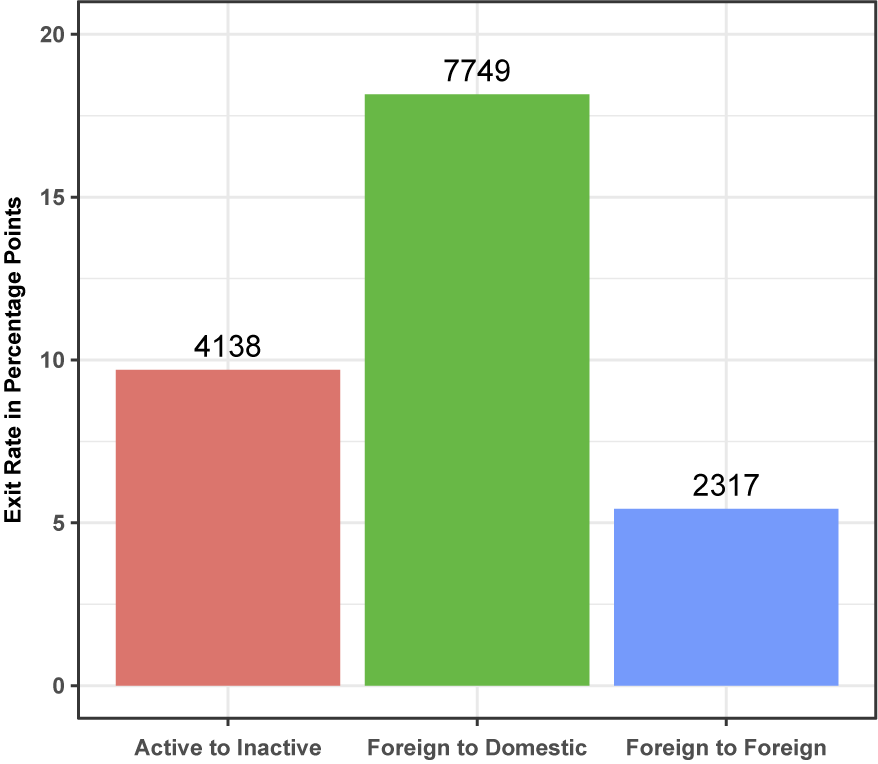

We approach exit as a transaction, which implies outcomes on both the “sell side” and the “buy side.” Our focus is on explaining the “sell side” of exit, which makes for a more analytically tractable study and is also driven by data considerations. Specifically, the dataset we build in this article is cross-sectional, as circumstances prevent us from building a time-series component. Moody’s suspended all updates to Russian data for 11 months of the 18-month study period, due to Russian policies that in Moody’s judgment significantly reduced data reliability (see Appendix 7.1 of the Supplementary Material). What we are able to do is use “buy side” data assessed at the end of the study period to validate our conceptualization of exit as a transaction, which implies that exit does not categorically mean that businesses stop operating. Indeed, of the 33.3% of the pre-invasion population that exited, only 5.4% have become inactive. The other 27.9% have exited but remain active under new ownership. Figure 3 visualizes the distribution of outcomes on the “buy side” of the transaction. Altogether, over half of the exit rate is accounted for by foreign-invested firms that have become active Russian firms. Assuming strategic non-reporting, this is a lower bound of Russian acquisitions.Footnote 18 We also identify firms operating under new foreign ownership, which in the data often consist of complex consortia and likely holding companies. We intend these data to be leveraged in future research on not just whether, but how, foreign-invested firms exit. For our purposes, we probe the robustness of results on the aggregate exit rate to these different sub-components (see “Exploring Heterogeneity” section).

Sub-Components of the Exit Rate

Note: Bars represent the exit rate in percentage points, and labels above the bars indicate the count. Our dependent variable is the aggregate exit rate summed across the three sub-components (33.3%). See the “Exploring Heterogeneity” section for exploratory analyses of sub-components.

THEORY: EXIT AS TRANSACTION

As months passed after the Russian invasion, and real-time reporting increasingly questioned why foreign-invested firms that talked about exiting Russia were still operating there, it became clear that reducing “exit” to the choice to stay-or-go is misleading. Because they are profit-motivated, foreign-invested firms choosing to exit prefer to recover value from their brownfield assets and make those assets available to be redeployed elsewhere (Kim and Kung Reference Kim and Kung2017). With this in mind, a more generalizable way to think about exit is as a transaction, which occurs between a seller and buyer at some terms. Exit-as-transaction is able to account for instances in which a firm quite literally moves physical assets abroad. In that case, the firm is engaging in intra-firm trade as both seller and buyer, transacting at a transfer price; consider, for example, relocating human capital from the Russia office to other branches. A firm could also liquidate assets by selling them to an external buyer. By approaching exit as a transaction, we can conceptualize host state interference in a foreign-invested firm’s ability to bargain over the terms of the sale. The transaction morphs into expropriation if the ownership transfer is coerced at terms to which the firm would not voluntarily have agreed.

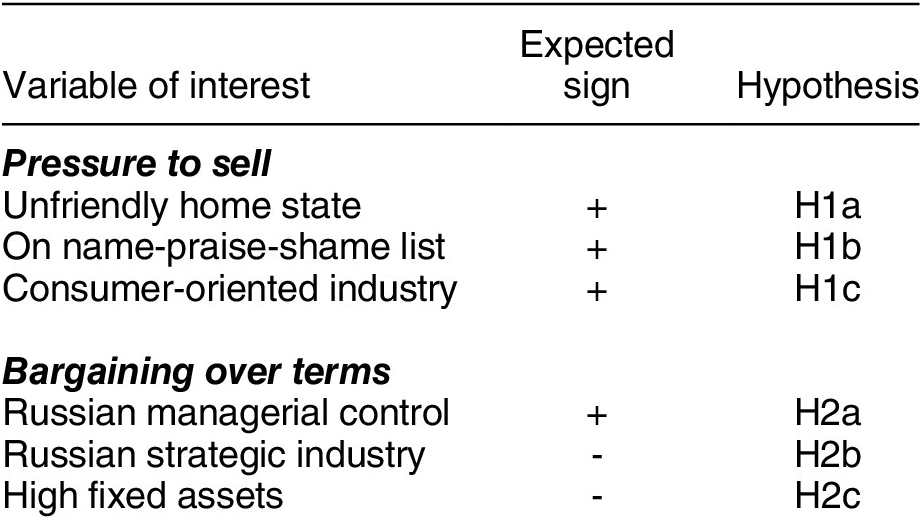

In the wake of a shock to political risk, the potential sellers, buyers, and terms of any exit transaction are deeply politicized. Our approach is to theorize foreign-invested firms’ incentives to select into seeking exit and pressures on the favorability of terms at which they can conclude sales. In so doing, we generate observable implications regarding the probability with which exit occurs, testable with our novel cross-sectional data. Importantly, this approach allows us to avoid generating some standardized measure of price, as observed prices for successful sales are not a suitable basis for inference. Table 2 summarizes how we organize the theory and hypotheses developed in the next sections.

Summary of Hypotheses: Likelihood of Exit?

Pressure to Sell

In terms of research design, one can consider every foreign-invested firm in pre-invasion Russia as “treated” with the exogenous shock of turmoil caused by its full-scale invasion of Ukraine. However, firms from only some home states have been treated with a sharp increase in political risk operating via a shock to the relationship between their home state and Russia. Russia itself provides an indicator variable in its “Unfriendly Countries” List, which it began publishing 9 days after its full-scale invasion of Ukraine (see Appendix 12.2 of the Supplementary Material). Broadly, “unfriendly” states have used their regulatory authority to engage in an unprecedented amount and variety of economic statecraft, variously stopping capital and trade flows with Russian individuals, firms, and state organs. In the 18 months post-invasion that form our study period, the European Union announced eleven “waves” of sanctions that it, the United States, the United Kingdom, and a variety of other states implemented with an unprecedented degree of coordination (Schott Reference Schott2023). As “unfriendly” states actively cut economic integration for foreign policy purposes, their firms faced pressure to reinforce home state efforts by exiting Russia of their own accord. Indeed, pre-existing foreign investments in Russia have been by and large outside of the scope of sanctions, so exit has not simply been a question of legal compliance with sanctions.Footnote 19

Although we align our prior with the expectation that foreign-invested firms from “unfriendly” homes are more likely to exit, there are several reasons to temper expectations. First, over the study period Russia implemented a series of discriminatory policies targeting asset sales by foreign firms from “unfriendly” states. As chronicled in Appendix 2 of the Supplementary Material, these have included: requiring authorization from a special government commission if transactions involve stocks, loans, or immobile “unfriendly” property; requiring nonresidents from “unfriendly” states to open special ruble bank accounts to receive transfers from Russian residents, with strict limits on repatriation; requiring government approval for profit distributions to “unfriendly” nonresidents; a requirement to sell “unfriendly” assets at a 50% discount from market value, as established by a government-approved appraiser; specific limits on “unfriendly” ownership structure changes in the energy and mining sectors; limits on “unfriendly” investors in their capacity as buyers; limits on transactions between Russian pension, insurance, and other investment funds and “unfriendly” investors; and a 10% windfall tax on the deal value of transactions resulting in companies leaving Russia. Taken as a whole, we can understand these “unfriendly”-targeted policies as a Russian effort to counteract the pressures motivating “unfriendly” foreign firms to sell. That Russia rolled out discriminatory policies across the study period suggests that the severity of Russian targeting of “unfriendly” sales is endogenous to any of a variety of dynamics—such as sanctions packages, progress in the war, increasingly scarce domestic capital, or examples of (un)successful exits.

Second, the extent to which home state foreign policy goals resulted in political pressure on foreign-invested firms to sell is also endogenous and varies over the study period. Indeed, as firms are tied to home states and not to any supra-national “unfriendly” coalition, they have distinct nationalities likely to generate heterogeneous interests and obligations (Polanco Reference Polanco2019; Wellhausen Reference Wellhausen2015). Despite the unprecedented coordination among “unfriendly” states on sanctions packages, very few home state leaders provided clear, public advice as to what their firms with pre-existing investments in Russia should (not) do. Of those that did, advice varied: in the study period official statements from the United States, United Kingdom, Canada, Estonia, and Ukraine encouraged exit, whereas France and Lithuania deferred to their companies’ judgment, and Japan made statements encouraging continued investment (see Appendix 5 of the Supplementary Material).

In short, varying and endogenous Russian efforts to counteract home state-tied pressures to sell, as well as varying and endogenous pressures to align with home state foreign policy, suggest that the net effect of “unfriendliness” on exit is an empirical question. In that way, the “Unfriendly Countries” List both presents an obvious first hypothesis and a jumping off point for theory-building.

Hypothesis 1a. Foreign-invested firms from home states on Russia’s “Unfriendly Countries” List are more likely to exit Russia, compared to firms from other home states.

There is a fast-growing literature on corporate social responsibility (CSR), or firm actions that consider “the triple bottom line of economic, social, and environmental performance” (Aguinis Reference Aguinis and Zedeck2011, 855). Firms engaged in CSR are expected to recognize their role in society and behave in accordance with social and ethical standards. In the event that firms’ (in)actions are in conflict with the preferences of interested stakeholders, backlash could be sufficiently motivating to change firm behavior. In the two weeks after the invasion, there was disagreement over the extent to which exiting Russia was in fact the behavior that aligned with CSR priorities. Some foreign-invested firms announced that they would stop production but continue to pay the salaries of their Russian workers as an ethical obligation, and pharmaceutical and consumer goods companies argued for the importance of continued production of essential medicines and goods in Russia. Uniqlo, a Japanese fashion company owned by Fast Retailing, announced that it would keep its 50 retail stores in Russia open, and its CEO stated that “Clothing is a necessity of life

$ \dots $

The people of Russia have the same right to live as we do.”Footnote

20 In our view, the public backlash to that international headline-making statement—and Uniqlo’s volte-face just days later, announcing that it would sell its Russian business—solidified the view among important audiences that there was little to no room for a CSR-based argument to stay.

$ \dots $

The people of Russia have the same right to live as we do.”Footnote

20 In our view, the public backlash to that international headline-making statement—and Uniqlo’s volte-face just days later, announcing that it would sell its Russian business—solidified the view among important audiences that there was little to no room for a CSR-based argument to stay.

One such audience is encapsulated in a remarkable set of grassroots, journalistic, and scholar-activist efforts to influence foreign firms with exposure to Russia, publicizing their (in)action with the intent to persuade. In Appendix 3 of the Supplementary Material, we provide detailed information on 12 lists of firms that were available on the Internet—several appearing mere days after the invasion—and actively updated as of 8-months post-invasion. Titles include “Boycott Russia,” “Squeezing Putin,” and “Don’t Fund War.” A list complied by the Kyiv School of Economics has been publicized worldwide and has had urgent value for the domestic Ukrainian audience. In the United States, a list hosted by the Yale School of Management received the endorsement of Ukrainian President Zelensky; its dedicated website describes the list as having been “widely circulated across company boardrooms, government officials, and media outlets.” These lists are an amplification of bottom-up “naming and shaming” efforts in the context of the international political economy (Barry, Clay, and Flynn Reference Barry, Chad Clay and Flynn2013; Thrall Reference Thrall2021). These lists also celebrate firms that exit, publicizing their choice as an example for others to follow. Thus, the most accurate way to describe these lists are as formalized “name, praise, and shame” lists.

Within weeks of the invasion and the first wave of lists, Russian-facing lists quickly followed. Kommersant, the Russian business newspaper of record, began hosting a list. We also document a grassroots list titled “#WeRememberEverything” (#ВСЕЗАПОМНИМ)—instructing Russian readers to boycott exiting firms should they later return to the Russian market. We suspect that at least some anti-exit counteraction has been meaningful. In a notable case, Didi, a Chinese ride-share company, immediately announced its exit from Russia but then faced social media backlash in China and reversed course. The technology company Lenovo, too, was rumored to be exiting Russia and faced Chinese social media backlash; it clarified that it too would stay.Footnote 21 Nonetheless, all firms in our sample that are on pro-exit lists are also on Russia-facing lists, and pro-exit lists are considerably more comprehensive. We presume foreign-invested firms on “name, praise, and shame” lists are facing net pro-exit pressure.

We are able to match 16.3% of foreign-invested firms in the pre-invasion sample to “name, praise, and shame” lists, and we align our priors with the expectation that matched firms are more likely to exit in the study period.Footnote 22 There are however reasons to temper expectations. First, the data generating process behind selection onto lists is nonrandom by design (Bartley and Child Reference Bartley and Child2014).Footnote 23 The kinds of firms on which activists can find information may also be the kinds of firms that have abundant resources to shield themselves, such as public relations staff or learning-by-doing experience from prior scandals. Activists may also be satisfied by firms taking actions that do not constitute exit, such as diversifying away from Russian suppliers or otherwise supporting the Ukrainian war effort. Our research design cannot test the impact of “naming, praising, and shaming” lists on outcomes other than exit.Footnote 24 That said, not only have lists been framed around exit, but a variety of commentary claims that lists have motivated exit from Russia (e.g., Sonnenfeld and Tian Reference Sonnenfeld and Tian2022; Sonnenfeld et al. Reference Sonnenfeld, Tian, Zaslavsky, Bhansali and Vakil2022). Our research design offers an opportunity to test these claims systematically.

Hypothesis 1b. Foreign-invested firms that have been named on public-facing “praise and shame” lists are more likely to exit Russia, compared to firms that have not been named.

Backlash through generalized social opprobrium might be a complement to or a substitute for a more direct pathway of consumer backlash, wherein consumers leverage their purchasing power and adopt a “vote with your dollars” strategy to influence firm behavior (Micheletti, Føllesdal, and Stolle Reference Micheletti, Føllesdal and Stolle2004; Sumner Reference Sumner2022). A consumer-backlash channel may be more important than “naming, praising, and shaming” in determining firm behavior, given the shorter causal chain linking public opinion and the risk of material costs to a firm that acts contrary to it (Pandya and Venkatesan Reference Pandya and Venkatesan2016; Vekasi Reference Vekasi2019).

To test the effects of consumer backlash, we would ideally devise a measure of consumer sentiment specific to the markets of greatest importance to each foreign-invested firm. Given that the world’s largest, richest consumer markets are in states on Russia’s “Unfriendly Countries” List, we proceed with the assumption that consumer-facing foreign-invested firms are facing net pro-exit pressure.Footnote 25 To code consumer-orientation we use advertising intensity as a proxy, an approach that has applicability to a variety of research settings (Peterson and Su Reference Peterson and Su2017). Because of the importance of the United States as a consumer market and data quality, we construct the variable using U.S. industrial advertising expenditure data, normalized by total income to measure intensity by industry (NAICS 3-digit).Footnote 26 The resulting measure makes sense intuitively: for example, motion picture and sound recording (NAICS 512) and beverage and tobacco product manufacturing (312) are among the most advertising-intensive, whereas mining (212) and heavy and civil engineering construction (237) are among the least.

Hypothesis 1c. Foreign-invested firms operating in consumer-oriented industries are more likely to exit Russia, compared to firms in other industries.

Bargaining over Terms

Whatever their motivations to sell, we assume that all foreign-invested firms are interested in maximizing the terms at which they exit. Anecdotally, this assumption is at the core of news reporting in the study period: myriad spokespeople reaffirmed companies’ intentions to exit while pointing to the difficulty of quickly closing deals.Footnote 27 We expect the Russian state to have strong preferences over the choices of foreign-invested firms, especially once it became clear that economy-wide FDI flight was a possibility. We have already considered Russia’s targeted interference with sales by foreign-invested firms from “unfriendly” home states, which is endogenous to the current political situation (see H1a and Appendix 2 of the Supplementary Material). Besides that, scholars have had much to say about ownership structures and industry as exogenous determinants of host state political interference, and these arguments carry observable implications for foreign-invested firms’ bargaining power in the current setting.

First, when the Russian state’s preferences are in fact aligned with exit, political risk is unlikely to interfere with foreign-invested firms’ ability to conclude sales. We should not lose sight of the basic explanation for why a developing state like Russia agrees to open to FDI—to benefit from longer-term domestic access to increased productive capacity, capital, and know-how that is otherwise un- or under-provided by domestic actors (Pandya Reference Pandya2016). If the Russian state has reason to believe a business could be successful absent foreign ownership, then it is likely indifferent to or even supportive of exit. How might the state differentiate between businesses in which foreign ownership is crucial or incidental? We expect that corporate structure is a guide: foreign investors operating minority stakes in joint ventures with domestic Russian partners are already operating under Russian managerial control, so it is reasonable to expect that the need for FDI has lessened. The foreign investor’s voluntary exit likely aligns with Russia’s preferences over promoting domestic ownership, and it need not doom the business, even if it disrupts productivity.Footnote 28

For a foreign investor, choosing to share ownership with a domestic partner carries implications for political risk (Zhu and Shi Reference Zhu and Shi2019). On the one hand, foreign investors in ventures with domestic partners may be shielded from host state interference. In the Russian context, a rich literature emphasizes the importance of political capital to commercial success, particularly concerning foreign and domestic shareholders (Beazer Reference Beazer2012; Markus Reference Markus2012; Reference Markus2015) and foreign minority ownership (Logvinenko Reference Logvinenko2019; Reference Logvinenko2021). On the other hand, a joint venture exposes the foreign investor to conflict with the domestic partner, including takeover attempts by the domestic partner (Earle et al. Reference Earle, Shpak, Shirikov and Gehlbach2022; Henisz Reference Henisz2000). If, however, the foreign investor is motivated to exit, then the ease of takeover may be a blessing—drastically minimizing the search costs required to find a buyer.Footnote 29 Pre-existing joint ownership could also alleviate information asymmetry issues over the quality of assets for sale, mitigating a “market for lemons” problem among potential buyers (Akerlof Reference Akerlof, Diamond and Rothschild1978). Taken together, there is reason to believe that exit by foreign minority owners is not in itself in conflict with the Russian state’s preferences, and that foreign minority ownership is conducive to striking quicker bargains.

Hypothesis 2a. Foreign-invested firms that are majority-owned by Russian shareholders are more likely to exit Russia, compared to firms that are not.

Scholars have much to say about industry as an exogenous determinant of host state political interference, and risks of interference are higher for foreign-invested firms operating in industries considered strategic, in or out of wartime (Lipson Reference Lipson1985). Insofar as a host state allows foreign-invested firms to operate in strategic industries, we can infer that domestic alternatives or replacements are scarce, and foreign-invested firms are likely providing crucial know-how to which the host state does not want to lose access (Johns and Wellhausen Reference Johns and Wellhausen2021). For these reasons, we expect that, post-invasion, voluntary exit by foreign-invested firms in strategic industries is contrary to the Russian state’s preferences. We expect the Russian state’s incentives to interfere act as a drag on foreign investors’ ability to negotiate and conclude sales.

To test whether exit varies with the strategic importance of an industry, we need to devise a list of Russian strategic industries exogenous to the conflict with Ukraine. Russia does not maintain such a list, but in 2008 amid the Global Financial Crisis, Russia released a list of “systemically important organizations” (Johnson Reference Johnson1997). Russia proposed that it would prioritize economic stabilization efforts for the 295 firms on that list if the need were to arise. Firms come from 84 disaggregated industries (4-digit NAICS), which we code as strategic (see Appendix 6 of the Supplementary Material). We infer that foreign-invested firms operating in these industries are exposed to systematically high risks of Russian state interference, by virtue of the kinds of goods and services they provide and/or by operating in competition with important domestic commercial actors.

As validation, we consider the four large foreign-invested firms that Russia did directly expropriate in the study period: Uniper SE (Germany, operating in the industry NAICS 2211); Fortum (Finland, 5416); Carlsberg (Denmark, 3121); and Danone (France, 3115). Each of these foreign-invested firms had announced their intention to exit and been publicly negotiating voluntary sales when the Russian state intervened. In each case, Russia signaled dissatisfaction with the terms being negotiated and forced a transfer of operations to preferred buyers at nonmarket terms.Footnote 30 Three out of four of these firms’ NAICS codes are indeed on the strategic industry list we devise. While Danone’s code is not on the list, all other 4-digit NAICS under the 3-digit 311, “Food manufacturing,” are included.Footnote 31 These facts give us confidence that our measure captures industries in which the Russian state is especially likely to constrain foreign-invested firms’ ability to bargain, and further that our measure is an under-count. We expect that foreign-invested firms operating in strategic industries are less likely to pursue voluntary exit, lest the Russian state interfere and even go so far as to expropriate (i.e., cause an involuntary exit).Footnote 32

Hypothesis 2b. Foreign-invested firms operating in industries considered strategic by Russia are less likely to exit Russia, compared to firms operating in other industries.

Another reason industry plays a large role in political economy theory is because of its impact on a firm’s exit options. Industries vary in fixed asset intensity, or the fixed assets like physical property, plant, and equipment required to produce each unit of output. By definition, fixed assets are those that cannot be quickly converted into cash. So, for a foreign-invested firm considering exit, more fixed assets implies lower quickly recoverable value and worse bargaining power over terms.

The current setting makes it crucial for us to innovate a means of testing the fixed asset intensity mechanism in isolation, distinguishing it from other characteristics associated with industry. For example, mining and oil and gas are the go to archetypes of highly fixed-asset intensive industries (Vernon Reference Vernon1971), but in resource-rich Russia these are also among Russia’s strategic industries (H2b). Therefore, it was perhaps theoretically overdetermined that Russia severely restricted assets sales of foreign-invested firms in mining and oil and gas (see Appendix 2 of the Supplementary Material).

We hone in on the fact that industry characteristics are largely determined by technology, and certain industries are always more fixed-asset intensive than others (Nunn and Trefler Reference Nunn, Trefler, Gita, Elhanan and Rogoff2014, 274). However, it would be naive to take fixed asset intensity as fully exogenous; foreign-invested firms in Russia have surely strategically adjusted their investments in response to political risk and uncertainty, both pre- and post-invasion. We therefore use U.S. data, as the U.S. market is arguably the most competitive in the world, leaving its industry characteristics primarily shaped by technology rather than nonmarket factors (Wright and Zhu Reference Wright and Zhu2018; Zhu and Deng Reference Zhu and Deng2022). We scale industry fixed asset stocks by gross output and average over the five-year span prior to our study period (2017–21).Footnote 33 The resulting measure makes sense intuitively—for example, oil and gas (NAICS 211) and mining (212) are among the most fixed asset-intensive. Additionally, the measure reveals variation within 2-digit industries in line with our primary identification strategy that relies on 2-digit industry fixed effects. For example, within transportation and warehousing (48), pipeline transportation (486) are high in fixed assets, whereas support activities (488) are not. Still, it is possible that this strategy goes too far in expecting nuanced fixed asset differences to predict variation in the dichotomous exit outcome. To preview, we find stronger results when adjusting our strategy to leverage variation at higher levels of industry aggregation.

Hypothesis 2c. Foreign-invested firms operating in industries intensive in fixed assets are less likely to exit Russia, compared to firms in other industries.

SPECIFICATION

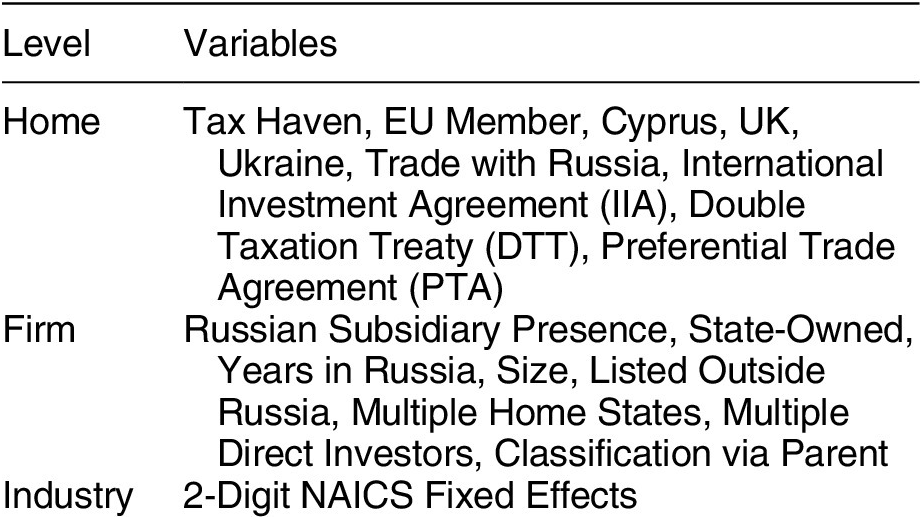

In the estimations, we control for a battery of home- and firm-level variables, summarized in Table 3. Coding involves a number of complexities; in the interest of space, we discuss a subset of controls here and point the reader to Appendix 9 of the Supplementary Material for full information.

Summary of Control Variables

On home-level controls, the prominence of known strategic jurisdictions in Table 1 reinforces the importance of controlling for Tax Haven, which we do with the European Union’s list of noncooperative tax jurisdictions while additionally controlling for EU Member (see Appendix 9.2 of the Supplementary Material). We control for Cyprus separately for several reasons: it is a prominent host to Russian capital that is round-tripped through foreign-invested firms back into Russia; it is considered by many to be a tax haven; and it is simultaneously an EU member state on Russia’s “Unfriendly Countries” List (Gonchar and Greve Reference Gonchar and Greve2022; Linsi and Mügge Reference Linsi and Mügge2019; Logvinenko Reference Logvinenko2019). Trade with Russia is the five-year average over the immediate pre-invasion period (2017–21). We also control for economic treaties in force between the home and Russia as of the invasion. Ex ante treaty protections might temper a foreign-invested firm’s post-invasion shock (Peinhardt and Zhang Reference Peinhardt and Zhang2024). Still, Russian treaty commitments may be endogenous; inter alia, in the study period Russia officially suspended Double Taxation Treaties (DTTs) with a wide swath of “unfriendly” states (Wellhausen and Peinhardt Reference Wellhausen and Peinhardt2025; Appendix 9.3 of the Supplementary Material).

At the firm level, we account for the importance of the Russian market by looking up the corporate ladder to the parent company. Russian Subsidiary Presence is the proportion of the parent’s corporate family located in Russia.Footnote 34 State-Owned indicates that the firm has at least one (non-Russian) state shareholder. Data-related variables include Multiple Home States, if a foreign-invested firm’s nationality is different from its parent; Multiple Direct Investors, if more than one foreign shareholder passes the FDI threshold; and Classification via Parent, if an observation enters the dataset based on parent company information.

As industry-level variation is of theoretical interest, the most conservative approach is to test sub-industry variation while controlling for aggregate industry categories (NAICS 2-digit fixed effects). This approach also accounts for exposure to industry-linked sanctions packages imposed on Russia (Schott Reference Schott2023). In Appendix 12.1 of the Supplementary Material, we use a different approach to industry inspired by the finance literature (Fama and French Reference Fama and French1996), which leverages more aggregate sectoral variation. We demonstrate robust, and in some cases stronger, results, which suggest limits to hyper-specific industry designations as a means of operationalizing political-economic concepts.

We fit simple linear probability models to provide a straightforward interpretation of substantive effects; results are robust to estimating nonlinear probit models (see Table 12.18 in the Supplementary Material). Standard errors are clustered at the 2-digit NAICS industry level to adjust for heteroskedasticity and within-group dependence.

RESULTS

Table 4 reports our main results. On pressure to sell, in all specifications Unfriendly Home State is negative—opposite to expectations—though only marginally significant in the most parsimonious model (contra H1a). Null results highlight that exit choices have been about more than economic statecraft by “unfriendly” countries. In what advocates of pro-exit “name, praise, and shame” lists might see as disappointing, the coefficient of On Name-Praise-Shame List is consistently negative and significant (contra H1b). One concern is that the observed negative association reflects reverse causation: firms that had already exited would no longer be targets of shaming. Although, when considering the data-generating process, it is reasonable to assume that firms that had already exited or taken meaningful steps in that direction are likely to be named and praised. In fact, praising is a widespread practice: 56.8% of named firms are praised on at least one list (see Appendix 3 of the Supplementary Material). Still, after disaggregating lists and re-estimating models, results are contrary to expectations: naming–praising is unrelated to exit, whereas naming–shaming is significantly associated with less exit (see Table 12.21 in the Supplementary Material).

Determinants of Foreign-Invested Firm Exit

Note: Robust standard errors in parentheses, clustered at the 2-digit NAICS level; * p < 0.10, ** p < 0.05, *** p < 0.01. Suppressed for presentation: aDTT, PTA, UK, Ukraine, bSize categories, Multiple homes, Multiple direct investors, and Classification via parent. Full results are shown in Table 12.17 in the Supplementary Material.

Does this mean that social pressure backfired? We do not think that is a fair interpretation, given nonrandom selection onto lists, our inability to adjudicate the effect of lists on other outcomes, and the additional reasons discussed above that led us to temper expectations over H1b. Further, the absence of a positive aggregate-level, average effect does not mean that “name, praise, and shame” efforts never worked; case study process tracing might uncover specific instances in which lists motivated exit. That said, our results do throw cold water on the strongest defenders of “name, praise, and shame” lists as having robust effects on foreign investor exit or the Russian political economy writ large (Sonnenfeld and Tian Reference Sonnenfeld and Tian2022; Sonnenfeld et al. Reference Sonnenfeld, Tian, Zaslavsky, Bhansali and Vakil2022).

In contrast, Consumer-Oriented Industry is positive and significant across all models, as expected (H1c). In sum, on pressure to sell we have the most confidence that consumer orientation meaningfully differentiates which foreign-invested firms actually complete exit within the 18 months following the invasion.

On firms’ bargaining power over the terms of exit, we find compelling evidence that firm behavior is shaped by Russian state interests. The coefficient on Russian Managerial Control is consistently positive and significant: foreign-invested firms in ventures already under Russian majority ownership were more likely to conclude exit (H2a). Russian Strategic Industry is consistently negative and significant: foreign-invested firms operating in industries of strategic importance to Russia were less likely to exit, consistent with the Russian state’s disinterest in these firms’ exit (H2b). Substantively, take results in the fully specified Model 5 as an example of the importance of these factors. All else equal, foreign-invested firms under pre-existing Russian managerial control are 5.9 percentage points more likely to exit, while foreign-invested firms in Russian strategic industries are 4.1 percentage points less likely to exit.

Regarding H2c, the coefficient for High Fixed Assets is negative as expected, but statistically insignificant. These results suggest that when controlling for 2-digit NAICS via fixed effects, relative levels of fixed asset intensity at the 3-digit NAICS level are not meaningful predictors of exit. We revisit H2c in Appendix 12.1 of the Supplementary Material, in which we adjust our fixed effects strategy and measure fixed assets at an aggregate level, based on 12 sector categories commonly used in the finance literature (Fama and French Reference Fama and French1996). There, we do find statistically significant evidence consistent with H2c that firms in high fixed asset industries are less likely to exit—specifically, firms in oil, gas, and coal, utilities, and telecommunications. Taken together, the null results in Table 4 and the significant results in Appendix 12.1 of the Supplementary Material provide some support for H2c and also point to the limits of data disaggregation in applications of the classic obsolescing bargain literature.

For presentation purposes, Table 4 reports coefficients for only a subset of controls; full results are available in Table 12.17 in the Supplementary Material. On home-level controls, we highlight the consistently negative and significant sign on IIA, which corresponds to these treaties’ intentions: given that IIAs protect foreign-invested firms’ property rights, those covered by IIAs would be less likely to exit due to realized political risk. At the firm level, the coefficient on Russian Subsidiary Presence is consistently positive and significant, but we caution against over-interpretation. While the suggestion that firms more dependent on Russia are more likely to exit is surprising, it might simply be easier for these corporate families to consolidate operations into fewer Russian subsidiaries, a conjecture we cannot validate with our data.

To probe robustness, we confirm that results in Table 4 are consistent when a minimal set of data-related firm level controls are included (see Table 12.16 in the Supplementary Material), and when home-level controls are replaced with home fixed effects (see Table 12.19 in the Supplementary Material). We also confirm robustness to dropping foreign-invested firms in the corporate families of those Russia did expropriate in the study period, as well as dropping observations for which parent information is unavailable (see Table 12.19 in the Supplementary Material). When dropping rather than controlling for foreign-invested firms registered in tax havens and Cyprus, results are robust except that the coefficient on Russian Managerial Control remains positive but loses significance, which makes sense given the concentration of Russian round-tripping through Cyprus. We also add a slate of additional home state variables: GDP per Capita, Liberal Democracy (V-Dem), and UN General Assembly (UNGA) Voting Similarity capturing foreign policy alignment between the firm’s home and Russia (average 2017–21; Bailey, Strezhnev, and Voeten Reference Bailey, Strezhnev and Voeten2017). While this specification drops home jurisdictions in the sample that are non-sovereign and not UN members, results on covariates of interest are robust. Additionally, firms from home states that had been politically aligned with Russia at the UNGA were less likely to exit, notable despite overwhelming UNGA condemnation in the immediate aftermath of the invasion (see Appendix 10 of the Supplementary Material).

Placebo Tests

We return to historical data to conduct placebo tests: do the dynamics of foreign-invested firm exit in the study period differ from those in earlier years? Knowing this will allow us more insight into whether, and in what ways, the post-invasion context is associated with different behavior. We replicate Table 4 using data from immediately pre-invasion (2020–21) and the beginning of Russian aggression against Ukraine (2013–14). We decline to interpret placebo results concerning Unfriendly Home State (H1a) and On Name-Praise-Shame List (H1b), as those covariates are by definition anachronistic in earlier periods. Usefully, in all cases other results of interest are robust to their inclusion or exclusion.Footnote 35

In 2020–21, the Russian occupation of Crimea and militarized conflict in eastern Ukraine had been ongoing since 2014, but the status quo intensity and scope of the conflict was stable for many years. We presume that foreign-invested firms at the time operated in a most-similar environment, except for factors related to Russia’s escalation to its full-scale invasion of Ukraine. Table 11.10 in the Supplementary Material reports that coefficients on Consumer-Oriented Industry (H1c) and Russian Strategic Industry (H2b) are insignificant, consistent with the theoretical intuition that the shock of Russia’s dramatic escalation was crucial to turning on these mechanisms. Notably, the sign on Russian Managerial Control flips in the immediate pre-invasion placebo period: foreign-invested firms in ventures with controlling domestic partners were less (rather than more) likely to exit. This result aligns with literature on the strategic usefulness of engaging in joint ventures with domestic firms—in normal times, when the goal is to stay in the market (Henisz Reference Henisz2000; Zhu and Shi Reference Zhu and Shi2019).

In 2013–14, the research design captures exit after nine months of armed conflict as the Russian occupation of Crimea began in March 2014. As in the post-invasion study period, foreign-invested firms operating in Russia at this time found themselves in a state that was the aggressor in a militarized interstate conflict, and subsequent sanctions impaired Russia’s domestic investment environment. As reported in Table 11.11 in the Supplementary Material, the positive and significant coefficient on Russian Managerial Control (H2a) replicates at the beginning of Russian aggression—sharing ownership with a domestic partner is useful in exceptional times of realized political risk, if the goal is to leave the market. In contrast to the study period, after March 2014 pre-existing FDI in Russia was not suddenly the subject of intense scrutiny. Nothing on the order of the study period’s “name, praise, and shame” efforts emerged; indeed, the coefficient Consumer-Oriented Industry (H1c) is insignificant. Absent the threat of mass FDI exit, it follows that Russia did not step up interference, reflected in the insignificant coefficient on Russian Strategic Industry.

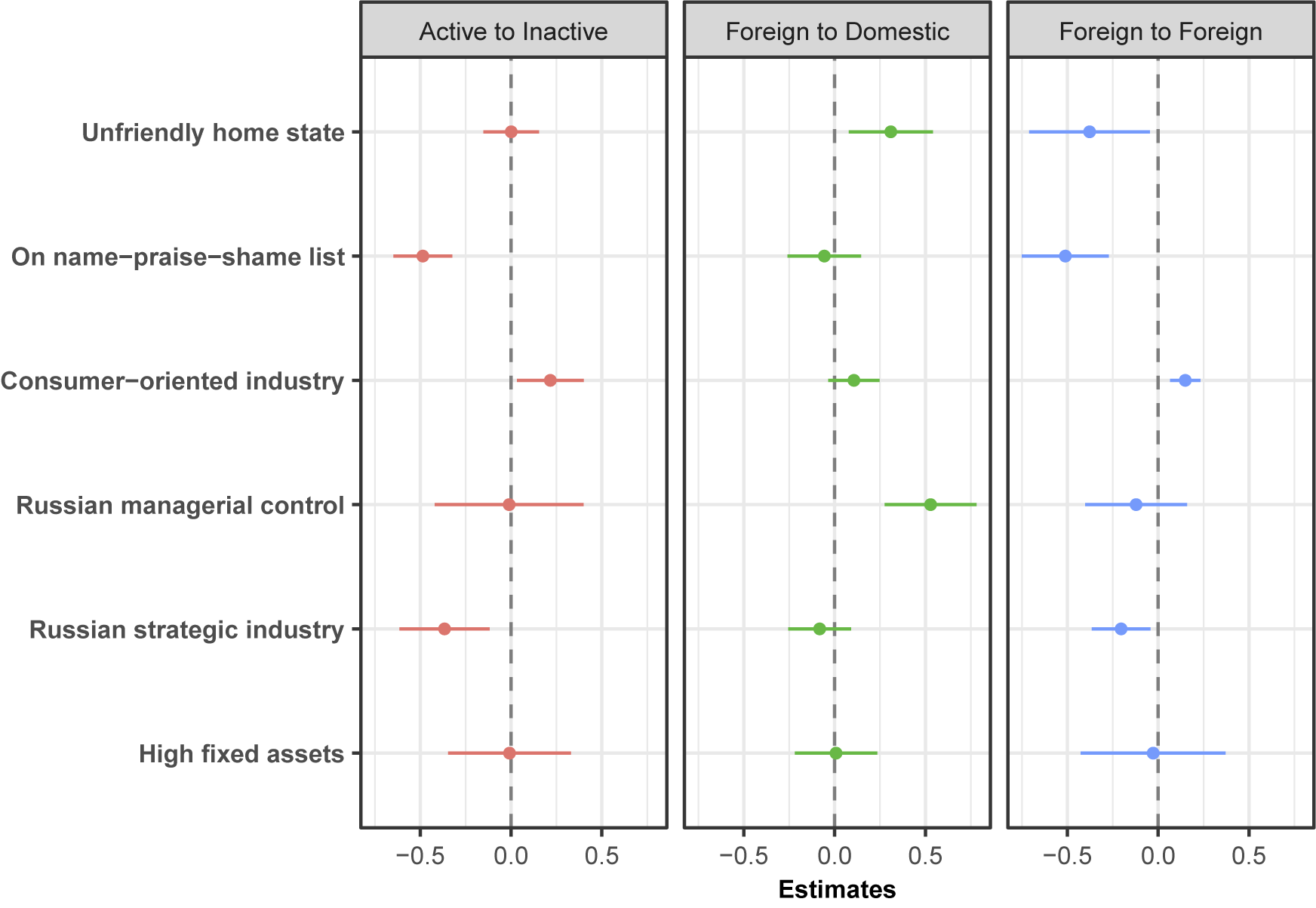

Exploring Heterogeneity

In Appendix 12.2 of the Supplementary Material, we explore potential heterogeneity between foreign-invested firms from home states labeled “unfriendly” or “friendly” by Russia. On state-ownership, we find that “unfriendly” (and not “friendly”) state-owned foreign-invested firms are more likely to exit—suggesting that leveraging exit for foreign policy purposes is easiest when the state is a decision-maker (H1a). In Appendix 12.3 of the Supplementary Material, we explore heterogeneity by size. Notably, among very large foreign-invested firms, those from “unfriendly” states are significantly more likely to exit—the closest evidence we find in support of “unfriendly” economic statecraft driving exit by private firms (H1a). Results also suggest that very large foreign-invested firms are especially constrained by consumer pressure (H1c) but not by more generalized social backlash (contra H1b), suggesting that financial risks mattered more than reputational ones.

Next, we consider heterogeneity across the three “buy side” sub-components: whether a foreign-invested firm becomes inactive, whether we can confirm that it has become a domestic (Russian) firm, or whether it remains a foreign-invested firm but under new ownership (see again Figure 3). While sub-components are mutually exclusive, endogenous discrepancies in Russian wartime data reporting suggest that we may underestimate foreign-to-domestic and thus overestimate one or both of the other sub-components (see Appendix 7.1 of the Supplementary Material). Accepting data shortcomings, we estimate a multinomial logit model; full results are in Table 12.22 in the Supplementary Material and key results are visualized in Figure 4. It is sensible that Russian Managerial Control predicts exit via an ownership transfer to a domestic (Russian) firm (H2a). It is also consistent with our theory that foreign-invested firms operating in a Russian Strategic Industry are unlikely to become inactive, as such an outcome would likely be counter to the Russian state’s interests (H2b).

Extension: Considering Different “Buy Side” Outcomes within the Aggregate Exit Rate

Note: Plot of point estimates and 95% confidence intervals from multinomial logit results on a 3-category dependent variable. See full results in Table 12.22 in the Supplementary Material. Controls omitted for presentation.

What we want to emphasize from Figure 4 is heterogeneity on the “unfriendly” home state result, and specifically a positive and significant coefficient for the foreign-to-domestic exit outcome. This is evidence that foreign-invested firms from “unfriendly” homes disproportionately transferred their businesses to Russian buyers—likely at fire sale prices. It is an open question whether this outcome is consistent with “unfriendly” economic statecraft goals (Gaur, Settles, and Väätänen Reference Gaur, Settles and Väätänen2023; Schott Reference Schott2023).

At the time of writing, neither the “exiting Russia” phenomenon nor economic sanctions have exerted so much stress on the Russian economy as to undermine its ability to wage war. We hope results in Figure 4 motivate future analyses of “buy side” outcomes, as well as their political-economic consequences.Footnote 36

CONCLUSION

In this setting of an exceptional shock to political risk, sellers, buyers, and prices of brownfield foreign-owned assets have been deeply politicized. We document that 33.3% of foreign-invested firms present in our pre-invasion sample had exited as of 18 months into the war, with most continuing operations as either domestic Russian or other-foreign firms and a small percentage becoming inactive. To explain exit patterns, we approach exit as a transaction and theorize how foreign-invested firms vary in their motivations to sell and the ease with which they can come to terms with buyers. We find mixed evidence on several hypotheses, themselves closely linked to the literature, which open up a variety of new lines of inquiry. On pressures to sell, our findings are strongest on consumer pressure as a motivation for exit, with little to no evidence of home state foreign policy or prominent social backlash as significant predictors of exit. On the ease of coming to terms in voluntary exit transactions, we find that foreign-invested firms with pre-existing Russian majority ownership were significantly more likely to exit, and were especially likely to become domestic Russian firms instead. Foreign-invested firms operating in strategic Russian industries were significantly less likely to exit, consistent with the expectation that the Russian state is disinclined to let these firms leave. Last, we find only some evidence that foreign-invested firms operating in industries intensive in fixed assets are less likely to exit, which suggests revisiting the centrality of asset immobility in vast literatures on foreign investor-host state relations.

We hope our nuanced results, data, novel measures, and general approach to exit as a transaction enables examination of a rich set of timely questions on the nonmarket determinants of firm behavior. At the same time, our study raises important questions at the nexus of international political economy and security. Is it net beneficial to geostrategic goals to encourage quick exit, especially as the identities of buyers might disrupt other geostrategic goals? Also, recall that in our pre-invasion sample, 75.5% of foreign-invested firms originate from “unfriendly” states. This high percentage is consistent with 1990s–2000s efforts by many of today’s “unfriendly” states to promote FDI into what some short-handed the “Wild East” (Gans-Morse Reference Gans-Morse2017; Grittersová Reference Grittersová2014; Szakonyi Reference Szakonyi2020). It also reflects “unfriendly” states’ long-time acceptance if not encouragement of FDI, even as violent Russian aggression against Ukraine has been ongoing since 2014. In historical perspective, pressure to exit Russia constitutes a volte face in “unfriendly” economic statecraft. Scholars would do well to consider the potentially disorienting effect of changeable home state foreign policy on MNCs’ investment decisions and forward-planning.

For now, we conclude by considering what all this exit means for Russia or, indeed, other developing states that are host to FDI. For a state deeply integrated into the global economy, we know that capital flight can spark any of a multitude of politically and economically destabilizing effects. For decades, such detrimental outcomes have been clearly, repeatedly demonstrated by so-called hot money, or short-term portfolio investment. The possibility of a “sudden stop” in FDI is new. FDI has been thought to be something different—investments by foreign owners that are reliably long-term enough to further industrial and economic development goals. We wonder whether FDI flight from Russia has brought to light risks relevant to other host states relying on FDI as a pillar of their development strategies. Our findings throw cold water on presumptions that firms’ choices over investment destinations are readily swayed by home state foreign policy or acute social backlash, suggesting that FDI is at best an imperfect tool of economic statecraft. Nevertheless, economic statecraft approaches that incentivize firms to become more “footloose” and capable of quick exit could reduce host states’ perceptions of FDI as a reliable tool for employment and economic growth. The consequence of the “exiting Russia” phenomenon for development strategies and attitudes toward economic integration, especially in politically risky host states, is an open question.

SUPPLEMENTARY MATERIAL

The supplementary material for this article can be found at https://doi.org/10.1017/S000305542610152X.

DATA AVAILABILITY STATEMENT

Research documentation and data that support the findings of this study are openly available at the American Political Science Review Dataverse: https://doi.org/10.7910/DVN/GTUD8P.

ACKNOWLEDGEMENTS

We thank Christina Davis, Clint Peinhardt, In Song Kim, Eddy Malesky, David Szakonyi, Yue Lin, Julia Morse, Victoria Liu, Bumba Mukherjee, Joe Wright, Lukas Linsi, Natalia Lamberova, Hayley Pring, and audiences at the International Political Economy Society (2023), International Studies Association (2023), the American Political Science Association (2023), the PSU-Pitt Joint IR Workshop (2024), and the London School of Economics (2024). For excellent research assistance, we thank teams of student researchers from Innovations for Peace and Development at UT Austin led by Rachel Jeon, with special thanks to Artem Kvartalnov, Vedanth Ramabhadran, Emily Doan, Yunyi Huang, and AJ Torok. At Penn State, we thank Lingbo Zhao, Tuba Sendinc, Tyler Suman, and Angel Villegas-Cruz and a team of graduate and undergraduate research assistants: Sam Bilotta, Shyam KC, Veronika Miskowiec, David Morgan, Savannah Morris, Chris Thomas, Alexandra Ward, and Lisi Wei. All errors are our own. Authors are listed alphabetically, indicating equal contributions.

FUNDING STATEMENT

This research was funded by the National Science Foundation RAPID Grant No. 2234188/9.

CONFLICT OF INTEREST

The authors declare no ethical issues or conflicts of interest in this research.

ETHICAL STANDARDS

The authors affirm this research did not involve human participants.

Open access

Open access

Comments

No Comments have been published for this article.