Impact Statement

Autoregressive models often are aggregated variables from smaller scales. Of particular interest in these models is studying the impact of external perturbations on large-scale variables, which has led to numerous applications across diverse fields. Such studies mainly focus on the effects between the aggregated variables and do not consider the effects between the small-scale variables. Our work presents two contributions. First, we develop a method to quantify the effects of perturbations on small-scale variables within an aggregated autoregressive model. Second, we introduce an approach to provide uncertainty bounds for these effects. Our approach enables the estimation of the effect of an external perturbation at the level of the small-scale variable.

1. Introduction

What are the effects of increased economic activities on air pollution levels? How do different regions of the brain interact and influence one another? Can we accurately estimate the effects of these interactions with a high degree of spatial precision? Understanding the impact of external perturbations on a system is a crucial aspect of dynamic system analysis. However, in fields such as economics and climate science, direct intervention in the system to measure the impact of an external disturbance is often neither feasible nor ethical. Consequently, data-driven approaches are predominantly used to estimate the effects of perturbations on such systems.

In particular, linear time-lagged dependencies between variables are commonly estimated using autoregressive models in neuroscience (Friston, Reference Friston2009), Earth system and climate data analysis (Runge et al., Reference Runge, Bathiany, Bollt, Camps-Valls, Coumou, Deyle, Glymour, Kretschmer, Mahecha, Muñoz-Marí, van Nes, Peters, Quax, Reichstein, Scheffer, Schölkopf, Spirtes, Sugihara, Sun and Zscheischler2019), and macroeconomics (Sims, Reference Sims1980; Zha, Reference Zha, Durlauf and Blume2010). Beyond the estimation of the linear dependencies, the interest often centers on analyzing the effect of an external perturbation on the system. One frequently used quantity to estimate the effects of a shock is, for example, the impulse response. The impulse response indicates the temporal response of an exogenous shock in one of the variables on one or all the other variables. Other measures, such as the accumulated response, reveal the cumulative effect of this shock over several time steps. Finally, the long-run effects (LREs) are the total accumulated effects over all future time steps. In a linear vector autoregressive model (VAR model) (Sims, Reference Sims1980), there are explicit formulas for the impulse response, the accumulated response, and the long-term effects, which can be used to estimate the effect of a shock on the system analyzed (Pesaran and Shin, Reference Pesaran and Shin1998; Lütkepohl, Reference Lütkepohl and Lütkepohl2005). The applications of these explicit formulas are numerous in the literature, especially in macroeconomics. In addition, the estimation uncertainty of these measures can be derived from an asymptotic-based argument or using bootstrapping methods (Benkwitz et al., Reference Benkwitz, Lütkepohl and Wolters2001; Lütkepohl, Reference Lütkepohl and Lütkepohl2005).

To illustrate the range of applications, we give a non-exhaustive list of analyses in which the effects of a perturbation using a VAR model were of interest. In Lütkepohl and Wolters (Reference Lütkepohl and Wolters2003), the authors have investigated the effects of German monetary policy on the monetary sector during the pre-euro period. Blanchard and Perotti (Reference Blanchard and Perotti2002) have studied the effects of a change in government spending and taxes on Gross Domestic Product (GDP) in the United States. More recently, Prüser and Schlösser (Reference Prüser and Schlösser2020) have analyzed the effect of economic policy uncertainty on European economies. In Hayat et al. (Reference Hayat, Ghulam, Batool, Naeem, Ejaz, Spulbar and Birau2021), the relationships between inflation, interest rate, and economic growth have been the main interest. In between macroeconomic, social science, and environmental science, Khan et al. (Reference Khan, Chenggang, Bano and Hussain2020) have examined the relationships between environmental degradation, economic growth, and social well-being in the countries of the Belt and Road Initiative. More focused on public health, Jiang and Liu (Reference Jiang and Liu2022) have analyzed the effect of inflation on infant mortality. Also, in public health, Liu et al. (Reference Liu, Chang and Chen2019) have estimated the effects of economic growth and health progress in the United States. In all of these studies, the variables in the VAR model are often aggregates of smaller-scale variables. In neuroscience, Bullmore and Sporns (Reference Bullmore and Sporns2009) have used the VAR model to study the organization and interaction of different brain regions. In climate science, the interactions between climate indices and modes of variability have been studied. These modes, such as the El Niño–Southern Oscillation (Wunsch, Reference Wunsch1990), the North Atlantic Oscillation (Barnston and Livezey, Reference Barnston and Livezey1987), or the Pacific Decadal Oscillation (Mantua et al., Reference Mantua, Hare, Zhang, Wallace and Francis1997), are the main drivers of global climate from the ocean to stratospheric dynamics. To obtain time series data, modes are extracted from spatially gridded data. While some modes are defined based on expert knowledge, some require the use of dimension-reduction methods such as principal component analysis (PCA) (Storch and Zwiers, Reference Storch and Zwiers1999). The time-lagged dependencies between the modes have been analyzed using various methods (Ebert-Uphoff and Deng, Reference Ebert-Uphoff and Deng2012; Runge et al., Reference Runge, Petoukhov and Kurths2014; Runge et al., Reference Runge, Petoukhov, Donges, Hlinka, Jajcay, Vejmelka, Hartman, Marwan, Paluš and Kurths2015; Kretschmer et al., Reference Kretschmer, Coumou, Donges and Runge2016; Kretschmer et al., Reference Kretschmer, Runge and Coumou2017; Runge et al., Reference Runge, Bathiany, Bollt, Camps-Valls, Coumou, Deyle, Glymour, Kretschmer, Mahecha, Muñoz-Marí, van Nes, Peters, Quax, Reichstein, Scheffer, Schölkopf, Spirtes, Sugihara, Sun and Zscheischler2019; Nowack et al., Reference Nowack, Runge, Eyring and Haigh2020; Galytska et al., Reference Galytska, Weigel, Handorf, Jaiser, Köhler, Runge and Eyring2023; Karmouche et al., Reference Karmouche, Galytska, Runge, Meehl, Phillips, Weigel and Eyring2023).

In the aforementioned fields of study (macroeconomics, public health, environmental science, Earth data analysis, and neuroscience), large-scale variables have commonly been aggregates of smaller-scale variables. This aggregation is mostly spatial (for instance, the climate modes) but can also be an aggregation of individuals, types of products, and so forth (e.g., economic or social indices). Due to the high cross-correlations between small-scale variables and the high dimensionality of the system, it is generally not recommended to model the dependencies between small-scale variables using an autoregressive model. However, some approaches have been developed to overcome this challenge. For example, Yan et al. (Reference Yan, Huang and Genton2021) propose a VAR model where each variable represents a process in a single spatial location. To reduce the high dimensionality of the system, they enforce sparsity and coefficient homogeneity in the transition matrix. To avoid the challenge of high dimensionality, in this study, we take advantage of the time-lagged linear dependencies between large-scale variables, which reveal emergent behavior that coherently appears at the small scale, thereby leading to large-scale dependencies. As a result, we aggregate small-scale variables into large-scale variables whose dependencies can be modeled using an autoregressive model. We use the spatially aggregated VAR (SAVAR) model introduced by Tibau et al. (Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022). The SAVAR model was originally designed to benchmark causal discovery methods and was developed for spatial aggregation. In practice, however, the aggregation does not have to be spatial and can be any type of nontemporal aggregation. This model is particularly suited to represent the aggregation of the VAR processes and their linear dependencies due to its matrix of aggregation weights and a single matrix of linear dependencies.

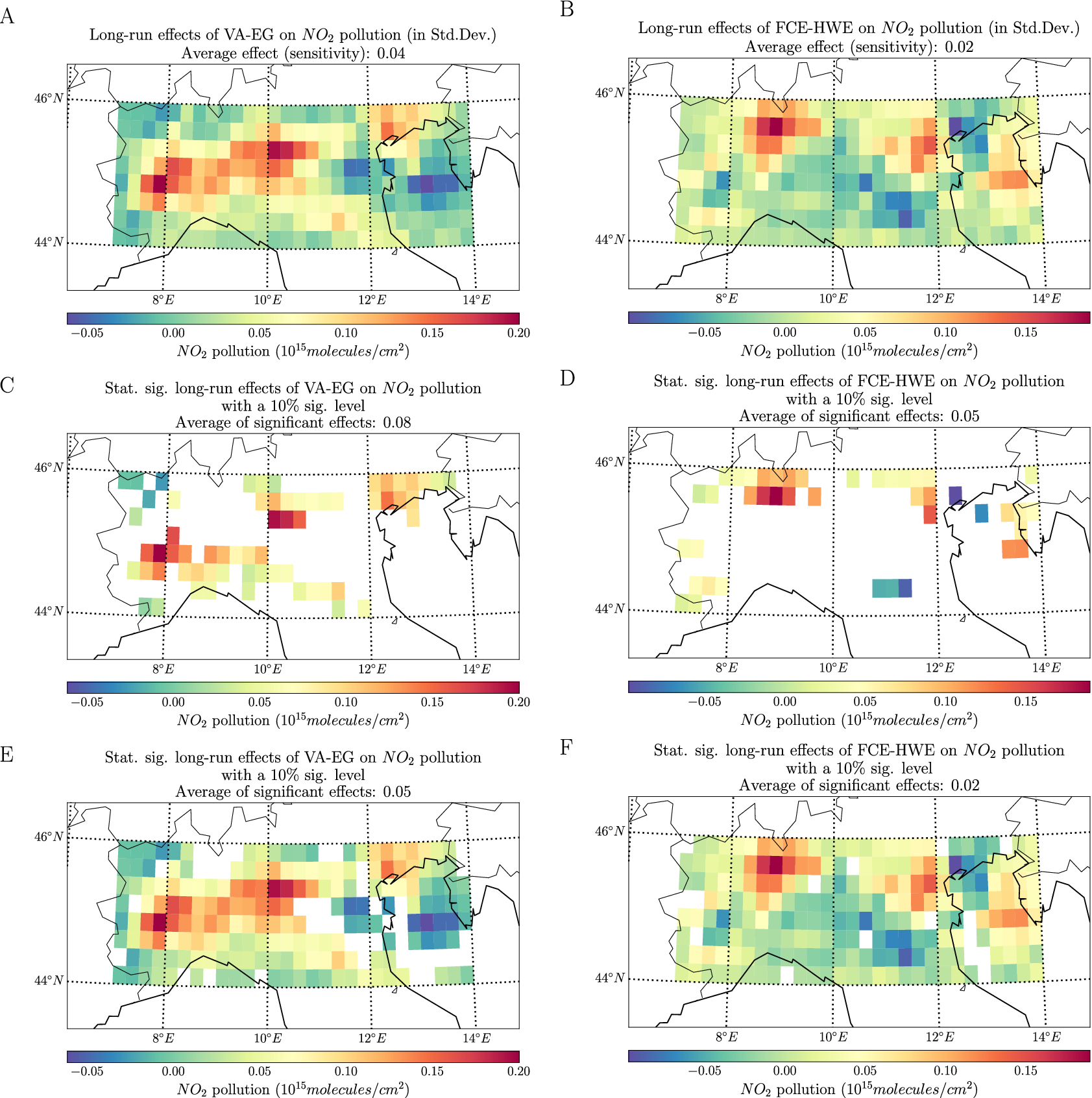

The effects of an external perturbation between large-scale variables can be explicitly calculated using formulas available in the literature. However, the effects of an external perturbation between small-scale variables need to be determined. In addition, approaches for building uncertainty bounds for small-scale effects should also be investigated. Our main contribution is in addressing those two points. We introduce LREs and sensitivity, two measures that indicate the long-term effects of an external perturbation on the small-scale variables. We derive their explicit formulas as functions of the linear coefficients and aggregation weight matrices of an SAVAR model. In addition, we derive the asymptotic distributions of the estimators for these measures under certain assumptions and show how to utilize them for uncertainty quantification. As an illustrative application, we analyze the long-term effects of economic activities on air pollution in Northern Italy, thereby demonstrating the practical utility of our approach in environmental science.

This article is divided into two sections. Section 2 provides a motivational example followed by a detailed description of materials and methods. We briefly introduce the SAVAR model along with relevant notations. We define the sensitivity and the LREs, as two measures that express the long-term effects of a perturbation in an SAVAR model. We derive their explicit formulas as follows. Assuming that the aggregation weights are known and that the underlying VAR process is stable, we derive the asymptotic distributions of their estimators. This asymptotic property can be used to build uncertainty bounds. Section 3 demonstrates the methods through several applications: two experiments with synthetic data and one real-world application. In Experiment 1, we evaluate various methods for estimating the sensitivity using synthetic data. In the second experiment, we analyze different techniques for establishing uncertainty bounds. Specifically, we assess the previously mentioned asymptotic method against multiple bootstrap methods. Finally, in the real-world application, our motivation is to quantify the long-term effects of economic activities on nitrogen dioxide (

$ {\mathrm{NO}}_2 $

) pollution in northern Italy. Our approach allows for estimating these effects at a finer resolution of a spatial grid, rather than the broader resolution of the modeled VAR processes. Additionally, we evaluate the statistical significance of these long-term effects using both bootstrap and asymptotic methods.

$ {\mathrm{NO}}_2 $

) pollution in northern Italy. Our approach allows for estimating these effects at a finer resolution of a spatial grid, rather than the broader resolution of the modeled VAR processes. Additionally, we evaluate the statistical significance of these long-term effects using both bootstrap and asymptotic methods.

2. Materials and methods: Response to a forcing in a linear dynamical system

2.1. Motivating example

In the following, we illustrate the problem of estimating the effects of a particular perturbation in the SAVAR model (Tibau et al., Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022) at the level of the small-scale variables. We first present the characteristics of an SAVAR model. In this manuscript, vectors are denoted in bold (e.g.,

$ \mathbf{y} $

) while scalars remain in regular font.

$ \mathbf{y} $

) while scalars remain in regular font.

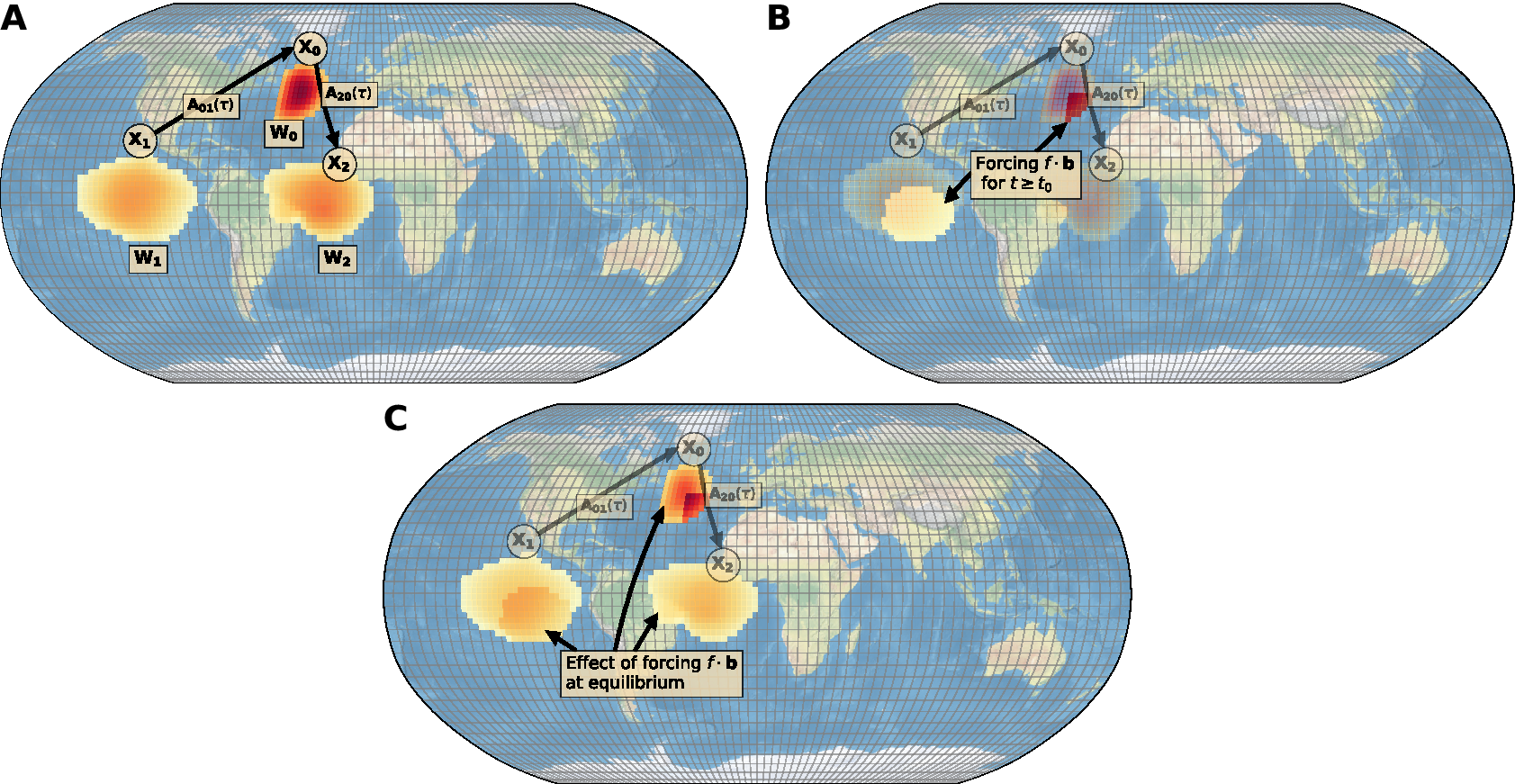

Consider, for instance, a set of three VAR processes

$ {X}_0,{X}_1,{X}_2 $

that we call modes, as depicted in Figure 1A. The

$ {X}_0,{X}_1,{X}_2 $

that we call modes, as depicted in Figure 1A. The

$ {X}_i $

are defined on the small-scale variables

$ {X}_i $

are defined on the small-scale variables

$ {y}_j $

stored in a column vector

$ {y}_j $

stored in a column vector

$ \mathbf{y} $

so that

$ \mathbf{y} $

so that

$ {X}_i={\mathbf{W}}_{\mathbf{i}}^{\prime}\;\mathbf{y} $

where

$ {X}_i={\mathbf{W}}_{\mathbf{i}}^{\prime}\;\mathbf{y} $

where

$ {\mathbf{W}}_{\mathbf{i}} $

is a weight vector. A concrete example of such modes is a set of climate modes defined as the weighted average of variables over a grid (temperature, sea level pressure, etc.). In the literature, the estimation of the VAR linear coefficients and the estimation of the effect of a perturbation on one VAR variable on the others are well documented. Diverse measures were derived to study the effect of a perturbation, shock, or impulse in a VAR model, including the impulse response analysis, forecast error variance decomposition, and accumulated response, among others (Pesaran and Shin, Reference Pesaran and Shin1998; Lütkepohl, Reference Lütkepohl and Lütkepohl2005). However, such measures describe the impact at the level of the VAR processes (in Figure 1 the

$ {\mathbf{W}}_{\mathbf{i}} $

is a weight vector. A concrete example of such modes is a set of climate modes defined as the weighted average of variables over a grid (temperature, sea level pressure, etc.). In the literature, the estimation of the VAR linear coefficients and the estimation of the effect of a perturbation on one VAR variable on the others are well documented. Diverse measures were derived to study the effect of a perturbation, shock, or impulse in a VAR model, including the impulse response analysis, forecast error variance decomposition, and accumulated response, among others (Pesaran and Shin, Reference Pesaran and Shin1998; Lütkepohl, Reference Lütkepohl and Lütkepohl2005). However, such measures describe the impact at the level of the VAR processes (in Figure 1 the

$ {X}_i $

) and not at the level of the small-scale variables (in Figure 1 the

$ {X}_i $

) and not at the level of the small-scale variables (in Figure 1 the

$ \mathbf{y} $

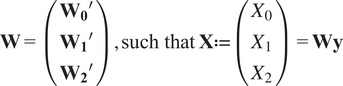

). We think it is also essential to quantify the effects of perturbing one or several small-scale variables on the other small-scale variables in such a model and to provide uncertainty bounds for these effects, as this information is crucial for a thorough understanding of the system’s behavior. We illustrate this problem in Figure 1B. The small-scale variables

$ \mathbf{y} $

). We think it is also essential to quantify the effects of perturbing one or several small-scale variables on the other small-scale variables in such a model and to provide uncertainty bounds for these effects, as this information is crucial for a thorough understanding of the system’s behavior. We illustrate this problem in Figure 1B. The small-scale variables

$ \mathbf{y} $

are subject to a particular perturbation, a forcing of intensity

$ \mathbf{y} $

are subject to a particular perturbation, a forcing of intensity

$ f $

at time

$ f $

at time

$ {t}_0 $

, where we define a forcing as follows:

$ {t}_0 $

, where we define a forcing as follows:

Definition 2.1 (Forcing). A forcing is an external perturbation of intensity

$ f $

and weights

$ f $

and weights

$ \mathbf{b}\in {\mathrm{\mathbb{R}}}^L $

, as shown in Figure 1B (where

$ \mathbf{b}\in {\mathrm{\mathbb{R}}}^L $

, as shown in Figure 1B (where

$ L $

is the total number of grid points). We assume the forcing begins at time

$ L $

is the total number of grid points). We assume the forcing begins at time

$ {t}_0 $

and remains constant after that (

$ {t}_0 $

and remains constant after that (

$ t\ge {t}_0 $

), with nonuniform weighting across the grid, specified by

$ t\ge {t}_0 $

), with nonuniform weighting across the grid, specified by

$ \mathbf{b} $

.

$ \mathbf{b} $

.

(A) Example of large-scale variables

$ {X}_0,{X}_1,{X}_2 $

following a VAR model. Arrows indicate direct linear time dependencies between the large-scale variables defined in

$ {X}_0,{X}_1,{X}_2 $

following a VAR model. Arrows indicate direct linear time dependencies between the large-scale variables defined in

$ \mathbf{A} $

, where

$ \mathbf{A} $

, where

$ {\mathbf{A}}_{ij}\left(\tau \right) $

indicates the effect of variable

$ {\mathbf{A}}_{ij}\left(\tau \right) $

indicates the effect of variable

$ {X}_j $

on variable

$ {X}_j $

on variable

$ {X}_i $

at time lag

$ {X}_i $

at time lag

$ \tau $

. The large-scale variables

$ \tau $

. The large-scale variables

$ {X}_0,{X}_1,{X}_2 $

are aggregates of the small-scale variables

$ {X}_0,{X}_1,{X}_2 $

are aggregates of the small-scale variables

$ \mathbf{y} $

defined on the spatial grid (gray grid) with weights

$ \mathbf{y} $

defined on the spatial grid (gray grid) with weights

$ {\mathbf{W}}_{\mathbf{0}},{\mathbf{W}}_{\mathbf{1}},{\mathbf{W}}_{\mathbf{2}} $

, respectively. Each large-scale variable

$ {\mathbf{W}}_{\mathbf{0}},{\mathbf{W}}_{\mathbf{1}},{\mathbf{W}}_{\mathbf{2}} $

, respectively. Each large-scale variable

$ {X}_i $

can be calculated from the small-scale variables

$ {X}_i $

can be calculated from the small-scale variables

$ \mathbf{y} $

thanks to the weights vector

$ \mathbf{y} $

thanks to the weights vector

$ {\mathbf{W}}_{\mathbf{i}} $

such that

$ {\mathbf{W}}_{\mathbf{i}} $

such that

$ {X}_i={{\mathbf{W}}_{\mathbf{i}}}^{\prime}\mathbf{y} $

. (B) An example of an external forcing of intensity

$ {X}_i={{\mathbf{W}}_{\mathbf{i}}}^{\prime}\mathbf{y} $

. (B) An example of an external forcing of intensity

$ f $

with spatial weights

$ f $

with spatial weights

$ \mathbf{b} $

is applied for all time

$ \mathbf{b} $

is applied for all time

$ t\ge {t}_0 $

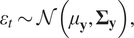

. The forcing is constant over time, but nonuniform spatially. (C) An example of the effects of the forcing once the system reaches equilibrium (LREs). Note that the aggregation weights are obtained solely via standard dimensionality reduction methods (e.g., PCA or PCA-Varimax) or prior knowledge and are not optimized based on the linear coefficient estimation. In particular, there is no feedback from the estimation of the linear coefficients to the determination of these weights.

$ t\ge {t}_0 $

. The forcing is constant over time, but nonuniform spatially. (C) An example of the effects of the forcing once the system reaches equilibrium (LREs). Note that the aggregation weights are obtained solely via standard dimensionality reduction methods (e.g., PCA or PCA-Varimax) or prior knowledge and are not optimized based on the linear coefficient estimation. In particular, there is no feedback from the estimation of the linear coefficients to the determination of these weights.

The question we want to address is: can we quantify the effects of the forcing at the small-scale level once the processes reach equilibrium? If yes, we can calculate these effects for the small-scale variables

$ \mathbf{y} $

and plot them as in Figure 1C. Answering this question is relevant as it enables the estimation of the effects of a perturbation with a higher degree of locality (at the level of the small-scale variables

$ \mathbf{y} $

and plot them as in Figure 1C. Answering this question is relevant as it enables the estimation of the effects of a perturbation with a higher degree of locality (at the level of the small-scale variables

$ {y}_i $

). A standard VAR model will provide these effects only at the coarser resolution of the VAR processes (aggregated variables

$ {y}_i $

). A standard VAR model will provide these effects only at the coarser resolution of the VAR processes (aggregated variables

$ {X}_i $

). There is a well-established body of literature on the estimation and the properties of the effects of a perturbation at the level of the VAR processes (Pesaran and Shin, Reference Pesaran and Shin1998; Lütkepohl, Reference Lütkepohl and Lütkepohl2005). However, to answer our motivational question, we have not found previous studies that derive similar measures at the small-scale level (

$ {X}_i $

). There is a well-established body of literature on the estimation and the properties of the effects of a perturbation at the level of the VAR processes (Pesaran and Shin, Reference Pesaran and Shin1998; Lütkepohl, Reference Lütkepohl and Lütkepohl2005). However, to answer our motivational question, we have not found previous studies that derive similar measures at the small-scale level (

$ \mathbf{y} $

) and provide their asymptotic properties and statistical significance.

$ \mathbf{y} $

) and provide their asymptotic properties and statistical significance.

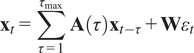

To achieve this, we model the system at the small-scale level using an SAVAR model introduced in Tibau et al. (Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022). This model is an extension of a VAR model, in which the VAR processes are mapped onto small-scale variables with a matrix of weights

$ \mathbf{W} $

. Going back to the example given in Figure 1, the matrix of weights of the SAVAR model could be, for example, the following:

$ \mathbf{W} $

. Going back to the example given in Figure 1, the matrix of weights of the SAVAR model could be, for example, the following:

$$ \mathbf{W}=\left(\begin{array}{c}{{\mathbf{W}}_{\mathbf{0}}}^{\prime}\\ {}{{\mathbf{W}}_{\mathbf{1}}}^{\prime}\\ {}{{\mathbf{W}}_{\mathbf{2}}}^{\prime}\end{array}\right),\mathrm{such}\ \mathrm{that}\hskip0.3em \mathbf{X}:= \left(\begin{array}{c}{X}_0\\ {}{X}_1\\ {}{X}_2\end{array}\right)=\mathbf{Wy} $$

$$ \mathbf{W}=\left(\begin{array}{c}{{\mathbf{W}}_{\mathbf{0}}}^{\prime}\\ {}{{\mathbf{W}}_{\mathbf{1}}}^{\prime}\\ {}{{\mathbf{W}}_{\mathbf{2}}}^{\prime}\end{array}\right),\mathrm{such}\ \mathrm{that}\hskip0.3em \mathbf{X}:= \left(\begin{array}{c}{X}_0\\ {}{X}_1\\ {}{X}_2\end{array}\right)=\mathbf{Wy} $$

We explore the impact of a unit forcing (an external factor that influences one or several small-scale variables for all future time steps) on the global mean of system variables at equilibrium, which we refer to as sensitivity. Additionally, we investigate the effects of the forcing at the level of individual small-scale variables, providing a more detailed understanding of its impacts on the

$ {y}_i $

, as opposed to the VAR processes

$ {y}_i $

, as opposed to the VAR processes

$ {X}_i $

. This is characterized by the LREs, which capture the changes induced by the external forcing on the small-scale variables at equilibrium.

$ {X}_i $

. This is characterized by the LREs, which capture the changes induced by the external forcing on the small-scale variables at equilibrium.

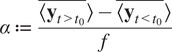

Definition 2.2 (Sensitivity). The sensitivity quantifies the equilibrium response of global means or regional averages to a forcing, capturing the magnitude of its impact. More precisely, the sensitivity,

$ \alpha $

, is defined as the ratio of the difference between the post-forcing and pre-forcing temporal averages of y over the forcing intensity f, where the temporal mean is computed over the appropriate time intervals.

$ \alpha $

, is defined as the ratio of the difference between the post-forcing and pre-forcing temporal averages of y over the forcing intensity f, where the temporal mean is computed over the appropriate time intervals.

Definition 2.3 (LREs). We define the LREs as a two-dimensional matrix, where each entry

$ ij $

represents the equilibrium response of variable

$ ij $

represents the equilibrium response of variable

$ {y}_i $

to a unit forcing applied to variable

$ {y}_i $

to a unit forcing applied to variable

$ {y}_j $

.

$ {y}_j $

.

These two measures offer quantitative information on the effects of the forcing at the level of the small-scale variables (long-term effects) or on a specific area of interest (sensitivity) in an SAVAR model. Our approach enables the practitioner to estimate the effects of a forcing with higher locality. The effects are estimated at the finer resolution (scale of the

$ {y}_i $

) rather than the coarser resolution of the VAR processes (the

$ {y}_i $

) rather than the coarser resolution of the VAR processes (the

$ {X}_i $

), which will result from a standard VAR model.

$ {X}_i $

), which will result from a standard VAR model.

The previous example has motivated the need for a model that accounts for the representation of linear dependencies at the grid level. Such a representation is possible with the SAVAR model (Tibau et al., Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022). The following sections outline the SAVAR model and derive the explicit formulas for the sensitivity and LREs. We then derive the asymptotic properties of these estimators, enabling the construction of confidence intervals (CIs) for sensitivity and LREs, which can be used to quantify uncertainty and evaluate the statistical significance of the LREs at the small-scale level.

2.2. A simple spatiotemporal stochastic model: the SAVAR model

The SAVAR model introduced by Tibau et al. (Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022) is a model that combines a VAR model with a mapping. This mapping can be spatial, as described in Tibau et al. (Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022). In general, the mapping does not have to be spatial and can be any dimension that is not temporal. The mapping

$ \mathbf{W}\in {\mathrm{\mathbb{R}}}^{N\times L} $

defines

$ \mathbf{W}\in {\mathrm{\mathbb{R}}}^{N\times L} $

defines

$ N $

modes over

$ N $

modes over

$ L $

points. The

$ L $

points. The

$ N $

modes are weighted combinations of the

$ N $

modes are weighted combinations of the

$ L $

grid points, thereby defining coarse-grained regions within the system. The

$ L $

grid points, thereby defining coarse-grained regions within the system. The

$ N $

modes correspond to the large-scale components of the system, whereas the

$ N $

modes correspond to the large-scale components of the system, whereas the

$ L $

grid points capture the small-scale features. Similar to the VAR model, the

$ L $

grid points capture the small-scale features. Similar to the VAR model, the

$ N $

modes are linearly time-dependent, which we represent with the matrices of dependencies noted

$ N $

modes are linearly time-dependent, which we represent with the matrices of dependencies noted

$ \mathbf{A}\left(\tau \right)\in {\mathrm{\mathbb{R}}}^{N\times N} $

. We note

$ \mathbf{A}\left(\tau \right)\in {\mathrm{\mathbb{R}}}^{N\times N} $

. We note

$ {\mathbf{y}}_t\in {\mathrm{\mathbb{R}}}^L $

the vector of values of the variables on the

$ {\mathbf{y}}_t\in {\mathrm{\mathbb{R}}}^L $

the vector of values of the variables on the

$ L $

points.

$ L $

points.

The SAVAR model is given in matrix notation by Tibau et al. (Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022):

$$ {\mathbf{y}}_t\hskip0.35em := \hskip0.35em {\mathbf{W}}^{+}\sum \limits_{\tau =1}^{\tau_{\mathrm{max}}}\mathbf{A}\left(\tau \right){\mathbf{W}\mathbf{y}}_{t-\tau }+{\varepsilon}_t, $$

$$ {\mathbf{y}}_t\hskip0.35em := \hskip0.35em {\mathbf{W}}^{+}\sum \limits_{\tau =1}^{\tau_{\mathrm{max}}}\mathbf{A}\left(\tau \right){\mathbf{W}\mathbf{y}}_{t-\tau }+{\varepsilon}_t, $$

$$ {\varepsilon}_t\sim \mathcal{N}\left({\mu}_{\mathbf{y}},{\boldsymbol{\Sigma}}_{\mathbf{y}}\right), $$

$$ {\varepsilon}_t\sim \mathcal{N}\left({\mu}_{\mathbf{y}},{\boldsymbol{\Sigma}}_{\mathbf{y}}\right), $$

$$ {\boldsymbol{\Sigma}}_{\mathbf{y}}=\lambda {\mathbf{W}}^{+}{\mathbf{D}}_{\mathbf{x}}{\mathbf{W}}^{+\mathbf{T}}+{\mathbf{D}}_{\mathbf{y}} $$

$$ {\boldsymbol{\Sigma}}_{\mathbf{y}}=\lambda {\mathbf{W}}^{+}{\mathbf{D}}_{\mathbf{x}}{\mathbf{W}}^{+\mathbf{T}}+{\mathbf{D}}_{\mathbf{y}} $$

Here, we note

$ {\varepsilon}_t\in {\mathrm{\mathbb{R}}}^L $

an independent noise. The noise is assumed to be independent and identically distributed. The diagonal covariance matrices

$ {\varepsilon}_t\in {\mathrm{\mathbb{R}}}^L $

an independent noise. The noise is assumed to be independent and identically distributed. The diagonal covariance matrices

$ {\mathbf{D}}_{\mathbf{x}}\in {\mathrm{\mathbb{R}}}^{N\times N} $

and

$ {\mathbf{D}}_{\mathbf{x}}\in {\mathrm{\mathbb{R}}}^{N\times N} $

and

$ {\mathbf{D}}_{\mathbf{y}}\in {\mathrm{\mathbb{R}}}^{L\times L} $

model the noise occurring at the mode level and the noise at each point, respectively. The covariant noise strength

$ {\mathbf{D}}_{\mathbf{y}}\in {\mathrm{\mathbb{R}}}^{L\times L} $

model the noise occurring at the mode level and the noise at each point, respectively. The covariant noise strength

$ \lambda $

is a coefficient that indicates the relative strength of these two noises. We denote

$ \lambda $

is a coefficient that indicates the relative strength of these two noises. We denote

$ {\mathbf{W}}^{+}\in {\mathrm{\mathbb{R}}}^{L\times N} $

the Moore–Penrose pseudoinverse of

$ {\mathbf{W}}^{+}\in {\mathrm{\mathbb{R}}}^{L\times N} $

the Moore–Penrose pseudoinverse of

$ \mathbf{W} $

. As

$ \mathbf{W} $

. As

$ \mathbf{W} $

is a mapping from the point level to the mode level,

$ \mathbf{W} $

is a mapping from the point level to the mode level,

$ {\mathbf{W}}^{+} $

is the inverse mapping that maps from the mode level to the point level. We assume that the modes are linearly independent, such that

$ {\mathbf{W}}^{+} $

is the inverse mapping that maps from the mode level to the point level. We assume that the modes are linearly independent, such that

$ \mathbf{W} $

has independent rows and is full rank. For example, a sufficient and feasible condition for linearly independent rows of

$ \mathbf{W} $

has independent rows and is full rank. For example, a sufficient and feasible condition for linearly independent rows of

$ \mathbf{W} $

would be that the modes do not overlap Tibau et al. (Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022).

$ \mathbf{W} $

would be that the modes do not overlap Tibau et al. (Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022).

Although the model initially appears to include only a single process, it can be extended to accommodate as many processes as required. For example, suppose that Figure 1A shows the temperature field on

$ {L}^{\prime } $

grid points and that the sea level pressure field is defined on

$ {L}^{\prime } $

grid points and that the sea level pressure field is defined on

$ {L}^{{\prime\prime} } $

grid points (not shown in the figure). To include both processes, we can extend the grid to

$ {L}^{{\prime\prime} } $

grid points (not shown in the figure). To include both processes, we can extend the grid to

$ L={L}^{\prime }+{L}^{{\prime\prime} } $

.

$ L={L}^{\prime }+{L}^{{\prime\prime} } $

.

The off-diagonal of

$ \lambda {\mathbf{W}}^{+}{\mathbf{D}}_{\mathbf{x}}{\mathbf{W}}^{+T} $

models the covariance structure of the fast dynamics, that is, contemporaneous dependencies. The direct time-lagged dependencies at time

$ \lambda {\mathbf{W}}^{+}{\mathbf{D}}_{\mathbf{x}}{\mathbf{W}}^{+T} $

models the covariance structure of the fast dynamics, that is, contemporaneous dependencies. The direct time-lagged dependencies at time

$ \tau >0 $

are modeled by

$ \tau >0 $

are modeled by

$ {\mathbf{W}}^{+}\mathbf{A}\left(\tau \right)\mathbf{W} $

, which represents the emergent behavior within each mode region, leading to the collective effect rather than individual effects between single points.

$ {\mathbf{W}}^{+}\mathbf{A}\left(\tau \right)\mathbf{W} $

, which represents the emergent behavior within each mode region, leading to the collective effect rather than individual effects between single points.

Tibau et al. (Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022) also give a mode-level representation of the SAVAR model. We introduce

$ {\mathbf{x}}_t\in {\mathrm{\mathbb{R}}}^N $

, such that

$ {\mathbf{x}}_t\in {\mathrm{\mathbb{R}}}^N $

, such that

$ {\mathbf{x}}_t\hskip0.35em := \hskip0.35em {\mathbf{Wy}}_t $

. After left-multiplying by

$ {\mathbf{x}}_t\hskip0.35em := \hskip0.35em {\mathbf{Wy}}_t $

. After left-multiplying by

$ \mathbf{W} $

in Equation (2.1) and using the property

$ \mathbf{W} $

in Equation (2.1) and using the property

$ {\mathbf{WW}}^{+}={I}_N $

, where we use the notation

$ {\mathbf{WW}}^{+}={I}_N $

, where we use the notation

$ {I}_n $

for the identity matrix of size

$ {I}_n $

for the identity matrix of size

$ n $

, Tibau et al. (Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022) obtained the following equation for

$ n $

, Tibau et al. (Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022) obtained the following equation for

$ {\mathbf{x}}_t $

:

$ {\mathbf{x}}_t $

:

$$ {\mathbf{x}}_t=\sum \limits_{\tau =1}^{\tau_{\mathrm{max}}}\;\mathbf{A}\left(\tau \right){\mathbf{x}}_{t-\tau }+\mathbf{W}{\varepsilon}_t $$

$$ {\mathbf{x}}_t=\sum \limits_{\tau =1}^{\tau_{\mathrm{max}}}\;\mathbf{A}\left(\tau \right){\mathbf{x}}_{t-\tau }+\mathbf{W}{\varepsilon}_t $$

The direct linear time-lagged dependencies between the modes are modeled with the

$ \mathbf{A}\left(\tau \right) $

matrices. We assume the variability at the point level to be much smaller than the mode-level variability, which is the case for the large covariant noise strength

$ \mathbf{A}\left(\tau \right) $

matrices. We assume the variability at the point level to be much smaller than the mode-level variability, which is the case for the large covariant noise strength

$ \lambda $

for which we get

$ \lambda $

for which we get

$ {\boldsymbol{\Sigma}}_{\mathbf{x}}\approx \lambda {\mathbf{D}}_{\mathbf{x}} $

. Here, model-level variability refers to the variability of the aggregated mode process (

$ {\boldsymbol{\Sigma}}_{\mathbf{x}}\approx \lambda {\mathbf{D}}_{\mathbf{x}} $

. Here, model-level variability refers to the variability of the aggregated mode process (

$ {\mathbf{x}}_t $

), which is typically larger than the variability observed at the individual grid point level (

$ {\mathbf{x}}_t $

), which is typically larger than the variability observed at the individual grid point level (

$ {\mathbf{y}}_t $

).Then the model is approximately a Markovian Structural Causal Model, here a VAR model, with independent noise terms (Tibau et al., Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022). The statistical properties of the SAVAR process, such as stationarity, stability, and identifiability, are deduced in Tibau et al. (Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022). Under the assumptions detailed in Tibau et al. (Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022), the stationarity and stability of the SAVAR process are guaranteed by the corresponding properties of the underlying mode-space VAR process. Similarly to VAR models, SAVAR models can be augmented with an exogenous term, which is particularly useful for incorporating specific characteristics of the data into the analysis. For instance, seasonal dummy variables can be added to an SAVAR model to account for periodic patterns in the data.

$ {\mathbf{y}}_t $

).Then the model is approximately a Markovian Structural Causal Model, here a VAR model, with independent noise terms (Tibau et al., Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022). The statistical properties of the SAVAR process, such as stationarity, stability, and identifiability, are deduced in Tibau et al. (Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022). Under the assumptions detailed in Tibau et al. (Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022), the stationarity and stability of the SAVAR process are guaranteed by the corresponding properties of the underlying mode-space VAR process. Similarly to VAR models, SAVAR models can be augmented with an exogenous term, which is particularly useful for incorporating specific characteristics of the data into the analysis. For instance, seasonal dummy variables can be added to an SAVAR model to account for periodic patterns in the data.

2.3. Derivation of the LREs and sensitivity in an SAVAR model

In the considered framework, the introduction and the motivating example of Section 2.1 have displayed the importance of measures that identify the effects of a perturbation in a system at the small-scale level. We introduce such measures and derive their explicit formulas in an SAVAR model.

2.3.1. Sensitivity in an SAVAR model

We call a forcing of intensity

$ f $

and of weights

$ f $

and of weights

$ \mathbf{b}\in {\mathrm{\mathbb{R}}}^L $

an external perturbation that is applied to the system, as illustrated in Figure 1B. We assume that the underlying VAR process is stable before the application of the forcing, which is then introduced after the system has reached equilibrium. Without loss of generality, we assume that the forcing is applied at time

$ \mathbf{b}\in {\mathrm{\mathbb{R}}}^L $

an external perturbation that is applied to the system, as illustrated in Figure 1B. We assume that the underlying VAR process is stable before the application of the forcing, which is then introduced after the system has reached equilibrium. Without loss of generality, we assume that the forcing is applied at time

$ {t}_0 $

and that there was no forcing for

$ {t}_0 $

and that there was no forcing for

$ t<{t}_0 $

. For

$ t<{t}_0 $

. For

$ t\ge {t}_0 $

, the forcing is constant but does not have to be uniform. Each coefficient

$ t\ge {t}_0 $

, the forcing is constant but does not have to be uniform. Each coefficient

$ {\mathbf{b}}_i $

of

$ {\mathbf{b}}_i $

of

$ \mathbf{b} $

represents the weighting of the forcing at grid point

$ \mathbf{b} $

represents the weighting of the forcing at grid point

$ i $

. In this context, the sensitivity is a measure that indicates the average effect of the forcing on the system (or a custom region of interest) at equilibrium (the system reaches a stable state) normalized by the value of its intensity

$ i $

. In this context, the sensitivity is a measure that indicates the average effect of the forcing on the system (or a custom region of interest) at equilibrium (the system reaches a stable state) normalized by the value of its intensity

$ f $

. For

$ f $

. For

$ t\ge {t}_0 $

, we have:

$ t\ge {t}_0 $

, we have:

$$ {\mathbf{y}}_t\hskip0.35em := \hskip0.35em {\mathbf{W}}^{+}\sum \limits_{\tau =1}^{\tau_{\mathrm{max}}}\mathbf{A}\left(\tau \right){\mathbf{W}\mathbf{y}}_{t-\tau }+f\mathbf{b}+{\varepsilon}_t $$

$$ {\mathbf{y}}_t\hskip0.35em := \hskip0.35em {\mathbf{W}}^{+}\sum \limits_{\tau =1}^{\tau_{\mathrm{max}}}\mathbf{A}\left(\tau \right){\mathbf{W}\mathbf{y}}_{t-\tau }+f\mathbf{b}+{\varepsilon}_t $$

The forcing weights vector

$ \mathbf{b} $

is assumed to be known a priori and specifies the spatial pattern of the external perturbation. The definition of the sensitivity, denoted by

$ \mathbf{b} $

is assumed to be known a priori and specifies the spatial pattern of the external perturbation. The definition of the sensitivity, denoted by

$ \alpha $

, is given by the following formula:

$ \alpha $

, is given by the following formula:

$$ \alpha \hskip0.35em := \hskip0.35em \frac{\overline{\left\langle {\mathbf{y}}_{t>{t}_0}\right\rangle }-\overline{\left\langle {\mathbf{y}}_{t<{t}_0}\right\rangle }}{f} $$

$$ \alpha \hskip0.35em := \hskip0.35em \frac{\overline{\left\langle {\mathbf{y}}_{t>{t}_0}\right\rangle }-\overline{\left\langle {\mathbf{y}}_{t<{t}_0}\right\rangle }}{f} $$

where

$ \left\langle \mathbf{y}\right\rangle $

denotes the temporal mean of

$ \left\langle \mathbf{y}\right\rangle $

denotes the temporal mean of

$ \mathbf{y} $

. Here,

$ \mathbf{y} $

. Here,

$ \overline{\mathbf{y}} $

is the mean of

$ \overline{\mathbf{y}} $

is the mean of

$ \mathbf{y} $

over all the

$ \mathbf{y} $

over all the

$ L $

points or over a specific area of interest such that

$ L $

points or over a specific area of interest such that

$ \overline{\mathbf{y}}=\frac{1}{\parallel \mathbf{h}{\parallel}_1}{\mathbf{h}}^{\prime}\mathbf{y} $

. Here,

$ \overline{\mathbf{y}}=\frac{1}{\parallel \mathbf{h}{\parallel}_1}{\mathbf{h}}^{\prime}\mathbf{y} $

. Here,

$ \mathbf{h} $

denotes a column vector with ones for the points inside the custom region of interest and zeros otherwise.

$ \mathbf{h} $

denotes a column vector with ones for the points inside the custom region of interest and zeros otherwise.

In the following, we assume that

$ {\mathbf{x}}_t $

is a stable VAR process as defined in Equation (2.2). Then,

$ {\mathbf{x}}_t $

is a stable VAR process as defined in Equation (2.2). Then,

$ {\mathbf{y}}_t $

as defined in Equation (2.1) is also a stable SAVAR process (see proof in Tibau et al., Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022). Using the formula of the SAVAR model

$ {\mathbf{y}}_t $

as defined in Equation (2.1) is also a stable SAVAR process (see proof in Tibau et al., Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022). Using the formula of the SAVAR model

$ {\mathbf{y}}_t $

, one can derive two explicit formulas of

$ {\mathbf{y}}_t $

, one can derive two explicit formulas of

$ \alpha $

:

$ \alpha $

:

$$ \alpha =\overline{{\left({I}_L-{\mathbf{W}}^{+}\mathbf{AKW}\right)}^{-1}\mathbf{b}} $$

$$ \alpha =\overline{{\left({I}_L-{\mathbf{W}}^{+}\mathbf{AKW}\right)}^{-1}\mathbf{b}} $$

$$ \mathrm{and}\hskip0.4em \alpha =\overline{{\mathbf{W}}^{+}\left({\left({I}_N-\mathbf{AK}\right)}^{-1}-{I}_N\right)\mathbf{Wb}+\mathbf{b}} $$

$$ \mathrm{and}\hskip0.4em \alpha =\overline{{\mathbf{W}}^{+}\left({\left({I}_N-\mathbf{AK}\right)}^{-1}-{I}_N\right)\mathbf{Wb}+\mathbf{b}} $$

where we introduce the block matrices:

$ \mathbf{A}=\left(\mathbf{A}(1),\hskip0.5em \mathbf{A}(2),\hskip0.5em \dots, \hskip0.5em \mathbf{A}\left({\tau}_{\mathrm{max}}\right)\right) $

and

$ \mathbf{A}=\left(\mathbf{A}(1),\hskip0.5em \mathbf{A}(2),\hskip0.5em \dots, \hskip0.5em \mathbf{A}\left({\tau}_{\mathrm{max}}\right)\right) $

and

$ {\mathbf{K}}^{\prime }=\left(\begin{array}{cccc}{I}_N,& {I}_N,& \dots, & {I}_N\end{array}\right) $

such that the product

$ {\mathbf{K}}^{\prime }=\left(\begin{array}{cccc}{I}_N,& {I}_N,& \dots, & {I}_N\end{array}\right) $

such that the product

$ \mathbf{AK}={\sum}_{\tau =1}^{\tau_{\mathrm{max}}}\mathbf{A}\left(\tau \right) $

to facilitate future derivations. We recall that

$ \mathbf{AK}={\sum}_{\tau =1}^{\tau_{\mathrm{max}}}\mathbf{A}\left(\tau \right) $

to facilitate future derivations. We recall that

$ N $

denotes the number of modes and

$ N $

denotes the number of modes and

$ L $

is the number of points. Equations (2.3b) and (2.3c) provide two mathematically equivalent formulations for the sensitivity

$ L $

is the number of points. Equations (2.3b) and (2.3c) provide two mathematically equivalent formulations for the sensitivity

$ \alpha $

as derived from the SAVAR model. The calculations leading to the two explicit formulas are detailed in Appendix A.1.

$ \alpha $

as derived from the SAVAR model. The calculations leading to the two explicit formulas are detailed in Appendix A.1.

We notice that the value of the forcing

$ f $

does not appear in the explicit formula. However, the forcing weights

$ f $

does not appear in the explicit formula. However, the forcing weights

$ \mathbf{b} $

play a role in the calculation of the sensitivity. We also point out that the sensitivity depends on the mode weights

$ \mathbf{b} $

play a role in the calculation of the sensitivity. We also point out that the sensitivity depends on the mode weights

$ \mathbf{W} $

and on the matrices of linear time-lagged dependencies

$ \mathbf{W} $

and on the matrices of linear time-lagged dependencies

$ \mathbf{A}\left(\tau \right) $

.

$ \mathbf{A}\left(\tau \right) $

.

2.3.2. LREs in an SAVAR model

The explicit formula for sensitivity shows the role of the forcing weights

$ \mathbf{b} $

. If the forcing

$ \mathbf{b} $

. If the forcing

$ f $

involves only a single grid point, for example, grid point

$ f $

involves only a single grid point, for example, grid point

$ i $

with weight

$ i $

with weight

$ 1 $

,

$ 1 $

,

$ \mathbf{b} $

is then a vector of zeros except for

$ \mathbf{b} $

is then a vector of zeros except for

$ {b}_i=1 $

. By introducing the matrix

$ {b}_i=1 $

. By introducing the matrix

$ {\boldsymbol{\Psi}}_{\infty } $

such that

$ {\boldsymbol{\Psi}}_{\infty } $

such that

$ \alpha \hskip0.35em := \hskip0.35em \overline{{\boldsymbol{\Psi}}_{\infty}\mathbf{b}} $

, we notice that only the coefficient of the

$ \alpha \hskip0.35em := \hskip0.35em \overline{{\boldsymbol{\Psi}}_{\infty}\mathbf{b}} $

, we notice that only the coefficient of the

$ i $

th column of

$ i $

th column of

$ {\boldsymbol{\Psi}}_{\infty } $

play a role in the calculation of the sensitivity. The coefficient

$ {\boldsymbol{\Psi}}_{\infty } $

play a role in the calculation of the sensitivity. The coefficient

$ {\left({\boldsymbol{\Psi}}_{\infty}\right)}_{ij} $

indicates the effect of a unit forcing at grid point

$ {\left({\boldsymbol{\Psi}}_{\infty}\right)}_{ij} $

indicates the effect of a unit forcing at grid point

$ j $

on grid

$ j $

on grid

$ i $

at equilibrium. For this reason, we refer to

$ i $

at equilibrium. For this reason, we refer to

$ {\boldsymbol{\Psi}}_{\infty } $

as the matrix of LREs. For an SAVAR model, the LREs are given by explicit formulas:

$ {\boldsymbol{\Psi}}_{\infty } $

as the matrix of LREs. For an SAVAR model, the LREs are given by explicit formulas:

$$ {\boldsymbol{\Psi}}_{\infty }={\mathbf{W}}^{+}\left({\left({I}_N-\mathbf{AK}\right)}^{-1}-{I}_N\right)\mathbf{W}+{I}_L $$

$$ {\boldsymbol{\Psi}}_{\infty }={\mathbf{W}}^{+}\left({\left({I}_N-\mathbf{AK}\right)}^{-1}-{I}_N\right)\mathbf{W}+{I}_L $$

$$ {\boldsymbol{\Psi}}_{\infty }={\left({I}_L-{\mathbf{W}}^{+}\mathbf{AKW}\right)}^{-1} $$

$$ {\boldsymbol{\Psi}}_{\infty }={\left({I}_L-{\mathbf{W}}^{+}\mathbf{AKW}\right)}^{-1} $$

Both Expressions (2.4a) and (2.4b) provide equivalent representation under the model assumptions. The coefficient of the LREs

$ {\left({\boldsymbol{\Psi}}_{\infty}\right)}_{ij} $

indicates the long-term effect of a unit change in grid point

$ {\left({\boldsymbol{\Psi}}_{\infty}\right)}_{ij} $

indicates the long-term effect of a unit change in grid point

$ j $

on grid point

$ j $

on grid point

$ i $

. We can also interpret

$ i $

. We can also interpret

$ {\boldsymbol{\Psi}}_{\infty } $

in terms of columns. The

$ {\boldsymbol{\Psi}}_{\infty } $

in terms of columns. The

$ j $

th column of

$ j $

th column of

$ {\boldsymbol{\Psi}}_{\infty } $

contains the long-term effects of a unit change in the

$ {\boldsymbol{\Psi}}_{\infty } $

contains the long-term effects of a unit change in the

$ j $

th small-scale variable of the system. In a standard VAR model, the LREs matrix can be derived for a shock (Lütkepohl, Reference Lütkepohl and Lütkepohl2005) and has a similar form:

$ j $

th small-scale variable of the system. In a standard VAR model, the LREs matrix can be derived for a shock (Lütkepohl, Reference Lütkepohl and Lütkepohl2005) and has a similar form:

$ {\boldsymbol{\Psi}}_{\infty }={\left({I}_N-\mathbf{AK}\right)}^{-1} $

. Unlike Equations (2.4a) and (2.4b), this latter formula does not include the matrix of weights

$ {\boldsymbol{\Psi}}_{\infty }={\left({I}_N-\mathbf{AK}\right)}^{-1} $

. Unlike Equations (2.4a) and (2.4b), this latter formula does not include the matrix of weights

$ \mathbf{W} $

, which expresses the aggregation of the large-scale variables in the SAVAR model.

$ \mathbf{W} $

, which expresses the aggregation of the large-scale variables in the SAVAR model.

2.3.3. Estimation

If

$ \mathbf{W} $

is known, and

$ \mathbf{W} $

is known, and

$ \mathbf{A} $

is estimated, one can also estimate

$ \mathbf{A} $

is estimated, one can also estimate

$ \alpha $

and

$ \alpha $

and

$ {\boldsymbol{\Psi}}_{\infty } $

by plugging them in the explicit formulas of

$ {\boldsymbol{\Psi}}_{\infty } $

by plugging them in the explicit formulas of

$ \alpha $

and

$ \alpha $

and

$ {\boldsymbol{\Psi}}_{\infty } $

.

$ {\boldsymbol{\Psi}}_{\infty } $

.

Given an estimator

$ \hat{\mathbf{A}} $

of

$ \hat{\mathbf{A}} $

of

$ \mathbf{A} $

,

$ \mathbf{A} $

,

$ \hat{\alpha} $

introduced below is an estimator of

$ \hat{\alpha} $

introduced below is an estimator of

$ \alpha $

:

$ \alpha $

:

$$ \hat{\alpha}=\overline{{\mathbf{W}}^{+}\left({\left({I}_N-\hat{\mathbf{A}}\mathbf{K}\right)}^{-1}-{I}_N\right)\mathbf{Wb}+\mathbf{b}} $$

$$ \hat{\alpha}=\overline{{\mathbf{W}}^{+}\left({\left({I}_N-\hat{\mathbf{A}}\mathbf{K}\right)}^{-1}-{I}_N\right)\mathbf{Wb}+\mathbf{b}} $$

$$ \mathrm{or}\hskip0.4em \hat{\alpha}=\overline{{\left({I}_L-{\mathbf{W}}^{+}\hat{\mathbf{A}}\mathbf{KW}\right)}^{-1}\mathbf{b}} $$

$$ \mathrm{or}\hskip0.4em \hat{\alpha}=\overline{{\left({I}_L-{\mathbf{W}}^{+}\hat{\mathbf{A}}\mathbf{KW}\right)}^{-1}\mathbf{b}} $$

And an estimator

$ {\hat{\boldsymbol{\Psi}}}_{\infty } $

of

$ {\hat{\boldsymbol{\Psi}}}_{\infty } $

of

$ {\boldsymbol{\Psi}}_{\infty } $

is given by:

$ {\boldsymbol{\Psi}}_{\infty } $

is given by:

$$ {\hat{\boldsymbol{\Psi}}}_{\infty }={\left({I}_L-{\mathbf{W}}^{+}\hat{\mathbf{A}}\mathbf{KW}\right)}^{-1} $$

$$ {\hat{\boldsymbol{\Psi}}}_{\infty }={\left({I}_L-{\mathbf{W}}^{+}\hat{\mathbf{A}}\mathbf{KW}\right)}^{-1} $$

2.4. Asymptotic distribution of the LREs and sensitivity estimators

We then derive the asymptotic distributions of the estimated sensitivity and LREs. If

$ \mathbf{W} $

is known and

$ \mathbf{W} $

is known and

$ \mathbf{A} $

is estimated, then in Proposition 2.1, we give the asymptotic distributions for

$ \mathbf{A} $

is estimated, then in Proposition 2.1, we give the asymptotic distributions for

$ {\hat{\boldsymbol{\Psi}}}_{\infty } $

and

$ {\hat{\boldsymbol{\Psi}}}_{\infty } $

and

$ \hat{\alpha} $

under the assumptions.

$ \hat{\alpha} $

under the assumptions.

Proposition 2.1. (Asymptotic distribution of

$ \hat{\alpha} $

and

$ \hat{\alpha} $

and

$ {\hat{\Psi}}_{\infty } $

).

$ {\hat{\Psi}}_{\infty } $

).

Let

$ {\mathbf{x}}_t $

be a stable VAR process as defined in Equation (2.2). Then,

$ {\mathbf{x}}_t $

be a stable VAR process as defined in Equation (2.2). Then,

$ {\mathbf{y}}_t $

as defined in Equation (2.1) is also a stable SAVAR process (see proof in Tibau et al., Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022). This implies that

$ {\mathbf{y}}_t $

as defined in Equation (2.1) is also a stable SAVAR process (see proof in Tibau et al., Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022). This implies that

$ {\left({I}_L-{\mathbf{W}}^{+}\mathbf{AKW}\right)}^{-1} $

and

$ {\left({I}_L-{\mathbf{W}}^{+}\mathbf{AKW}\right)}^{-1} $

and

$ {\left({I}_N-\mathbf{AK}\right)}^{-1} $

are invertible. We note

$ {\left({I}_N-\mathbf{AK}\right)}^{-1} $

are invertible. We note

$ \hat{\beta}= vec\left(\hat{\mathbf{A}}\right) $

and

$ \hat{\beta}= vec\left(\hat{\mathbf{A}}\right) $

and

$ \beta = vec\left(\mathbf{A}\right) $

where

$ \beta = vec\left(\mathbf{A}\right) $

where

$ vec $

denotes the vectorization of a matrix (see Appendix A.2).

$ vec $

denotes the vectorization of a matrix (see Appendix A.2).

$ T $

is the sample size.

$ T $

is the sample size.

If

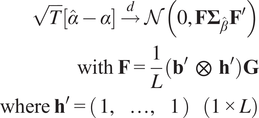

$$ \sqrt{T}\left(\hat{\beta}-\beta \right)\overset{d}{\to}\mathcal{N}\left(0,{\boldsymbol{\Sigma}}_{\hat{\beta}}\right) $$

$$ \sqrt{T}\left(\hat{\beta}-\beta \right)\overset{d}{\to}\mathcal{N}\left(0,{\boldsymbol{\Sigma}}_{\hat{\beta}}\right) $$

Then,

$$ {\displaystyle \begin{array}{r}\sqrt{T}\left[ vec\left({\hat{\boldsymbol{\Psi}}}_{\infty}\right)- vec\left({\boldsymbol{\Psi}}_{\infty}\right)\right]\overset{d}{\to}\mathcal{N}\left(0,\mathbf{G}{\boldsymbol{\Sigma}}_{\hat{\beta}}{\mathbf{G}}^{\prime}\right)\\ {}\mathrm{with}\hskip0.4em \mathbf{G}={\left(\mathbf{KW}{\boldsymbol{\Psi}}_{\infty}\right)}^{\hskip0.5em }\hskip0.4em \otimes \hskip0.7em \left({\boldsymbol{\Psi}}_{\infty }{\mathbf{W}}^{+}\right)\end{array}} $$

$$ {\displaystyle \begin{array}{r}\sqrt{T}\left[ vec\left({\hat{\boldsymbol{\Psi}}}_{\infty}\right)- vec\left({\boldsymbol{\Psi}}_{\infty}\right)\right]\overset{d}{\to}\mathcal{N}\left(0,\mathbf{G}{\boldsymbol{\Sigma}}_{\hat{\beta}}{\mathbf{G}}^{\prime}\right)\\ {}\mathrm{with}\hskip0.4em \mathbf{G}={\left(\mathbf{KW}{\boldsymbol{\Psi}}_{\infty}\right)}^{\hskip0.5em }\hskip0.4em \otimes \hskip0.7em \left({\boldsymbol{\Psi}}_{\infty }{\mathbf{W}}^{+}\right)\end{array}} $$

And

$$ {\displaystyle \begin{array}{r}\sqrt{T}\left[\hat{\alpha}-\alpha \right]\overset{d}{\to}\mathcal{N}\left(0,\mathbf{F}{\boldsymbol{\Sigma}}_{\hat{\beta}}{\mathbf{F}}^{\prime}\right)\\ {}\mathrm{with}\hskip0.32em \mathbf{F}=\frac{1}{L}\left({\mathbf{b}}^{\prime}\hskip0.5em \otimes \hskip0.5em {\mathbf{h}}^{\prime}\right)\mathbf{G}\\ {}\mathrm{where}\hskip0.32em {\mathbf{h}}^{\prime }=\left(\begin{array}{ccc}1,& \dots, & 1\end{array}\right)\hskip1em \left(1\times L\right)\end{array}} $$

$$ {\displaystyle \begin{array}{r}\sqrt{T}\left[\hat{\alpha}-\alpha \right]\overset{d}{\to}\mathcal{N}\left(0,\mathbf{F}{\boldsymbol{\Sigma}}_{\hat{\beta}}{\mathbf{F}}^{\prime}\right)\\ {}\mathrm{with}\hskip0.32em \mathbf{F}=\frac{1}{L}\left({\mathbf{b}}^{\prime}\hskip0.5em \otimes \hskip0.5em {\mathbf{h}}^{\prime}\right)\mathbf{G}\\ {}\mathrm{where}\hskip0.32em {\mathbf{h}}^{\prime }=\left(\begin{array}{ccc}1,& \dots, & 1\end{array}\right)\hskip1em \left(1\times L\right)\end{array}} $$

The normal distribution is represented by the symbol

$ \mathcal{N} $

, and the Kronecker product is denoted by the symbol

$ \mathcal{N} $

, and the Kronecker product is denoted by the symbol

$ \otimes $

. The proofs can be found in Appendix A.3.

$ \otimes $

. The proofs can be found in Appendix A.3.

2.4.1. Assumptions and estimation

Here are some important comments regarding this last proposition:

-

• Assumptions: One key assumption is that the distribution of the estimated matrix of linear coefficients is asymptotically normally distributed and that the estimator of the linear coefficient is consistent, which is the case, for instance, when

$ \mathbf{W} $

is known and

$ \mathbf{A} $

is estimated using the least-squares estimator (Lütkepohl, Reference Lütkepohl and Lütkepohl2005).

$ \mathbf{W} $

is known and

$ \mathbf{A} $

is estimated using the least-squares estimator (Lütkepohl, Reference Lütkepohl and Lütkepohl2005). -

• Implications: The proposition demonstrates that the estimators of the LREs and sensitivity are consistent. In addition, the proposition gives the asymptotic distribution of the estimators, which are normal distributions.

-

• When the sensitivity is not computed on all the

$ L $

points, one has to replace

$ \mathbf{h} $

by a vector with one coefficient for the

$ \tilde{L}\le L $

small-scale variables of interest and a zero coefficient elsewhere. Then, in the expression of

$ F $

,

$ \frac{1}{L} $

has to be replaced by

$ \frac{1}{\tilde{L}} $

. -

• To estimate the covariance matrix of the linear coefficients

$ {\boldsymbol{\Sigma}}_{\hat{\beta}} $

in practice, we use the consistent estimator provided in Lütkepohl (Reference Lütkepohl and Lütkepohl2005) for a VAR model:

$ {\hat{\boldsymbol{\Sigma}}}_{\hat{\beta}}=\frac{\mathbf{Z}{\mathbf{Z}}^{\prime }}{T}\hskip0.5em \otimes \hskip0.5em {\hat{\boldsymbol{\Sigma}}}_{\varepsilon } $

. We define

$ \mathbf{Z}\hskip0.35em := \hskip0.35em \left({\mathbf{Z}}_0,\dots, {\mathbf{Z}}_{T-1}\right) $

where

$ {\mathbf{Z}}_t^{\prime }=\left[\begin{array}{cccc}1& {\mathbf{y}}_t^{\prime }& \cdots & {\mathbf{y}}_{t-{\tau}_{\mathrm{max}}+1}^{\prime}\end{array}\right] $

. And

$ {\hat{\boldsymbol{\Sigma}}}_{\varepsilon } $

is an unbiased estimator of the covariance matrix of the residuals.

$ {\hat{\boldsymbol{\Sigma}}}_{\varepsilon }=\frac{\hat{\varepsilon}{\hat{\varepsilon}}^{\prime }}{T-P} $

, here

$ \hat{\varepsilon} $

are the estimated residuals and

$ P $

is the total number of parameters of the VAR model embedded in the SAVAR model.

2.4.2. CI and statistical significance

If the actual asymptotic distributions of the LREs and sensitivity are not degenerate, we can derive asymptotic CIs from the asymptotic variance of the sensitivity and covariance matrix of the LREs (Benkwitz et al., Reference Benkwitz, Lutkepohl and Neumann1997; Lütkepohl, Reference Lütkepohl and Lütkepohl2005). For example, to obtain the

$ \omega $

% CI of a specific LRE

$ \omega $

% CI of a specific LRE

$ {\left({\boldsymbol{\Psi}}_{\infty}\right)}_{ij} $

, we first retrieve the associated diagonal element of the covariance matrix of the LREs. This gives us

$ {\left({\boldsymbol{\Psi}}_{\infty}\right)}_{ij} $

, we first retrieve the associated diagonal element of the covariance matrix of the LREs. This gives us

$ {\hat{\sigma}}_{{\left({\boldsymbol{\Psi}}_{\infty}\right)}_{ij}}^2 $

, an estimate of the asymptotic variance of the LREs

$ {\hat{\sigma}}_{{\left({\boldsymbol{\Psi}}_{\infty}\right)}_{ij}}^2 $

, an estimate of the asymptotic variance of the LREs

$ {\left({\boldsymbol{\Psi}}_{\infty}\right)}_{ij} $

. Then, the asymptotic CI is given by the interval between the

$ {\left({\boldsymbol{\Psi}}_{\infty}\right)}_{ij} $

. Then, the asymptotic CI is given by the interval between the

$ \frac{\omega }{2} $

quantile and

$ \frac{\omega }{2} $

quantile and

$ 1-\frac{\omega }{2} $

quantile of a normal distribution with mean

$ 1-\frac{\omega }{2} $

quantile of a normal distribution with mean

$ {\left({\hat{\boldsymbol{\Psi}}}_{\infty}\right)}_{ij} $

and variance

$ {\left({\hat{\boldsymbol{\Psi}}}_{\infty}\right)}_{ij} $

and variance

$ {\hat{\sigma}}_{{\left({\boldsymbol{\Psi}}_{\infty}\right)}_{ij}}^2 $

. Furthermore, the estimated LRE

$ {\hat{\sigma}}_{{\left({\boldsymbol{\Psi}}_{\infty}\right)}_{ij}}^2 $

. Furthermore, the estimated LRE

$ {\left({\hat{\boldsymbol{\Psi}}}_{\infty}\right)}_{ij} $

is significantly different from zero at an asymptotic

$ {\left({\hat{\boldsymbol{\Psi}}}_{\infty}\right)}_{ij} $

is significantly different from zero at an asymptotic

$ \frac{\omega }{2} $

level if the latter CI does not contain the value zero. The proposed asymptotic-based CIs can be used to assess significance at the level of the small-scale variables, allowing for a more localized assessment of the effects of a perturbation.

$ \frac{\omega }{2} $

level if the latter CI does not contain the value zero. The proposed asymptotic-based CIs can be used to assess significance at the level of the small-scale variables, allowing for a more localized assessment of the effects of a perturbation.

3. Numerical results

We have introduced materials and methods to estimate the sensitivity and LREs in an SAVAR model. In the next section, we numerically estimate these measures from synthetic data and real-world data while providing uncertainty ranges.

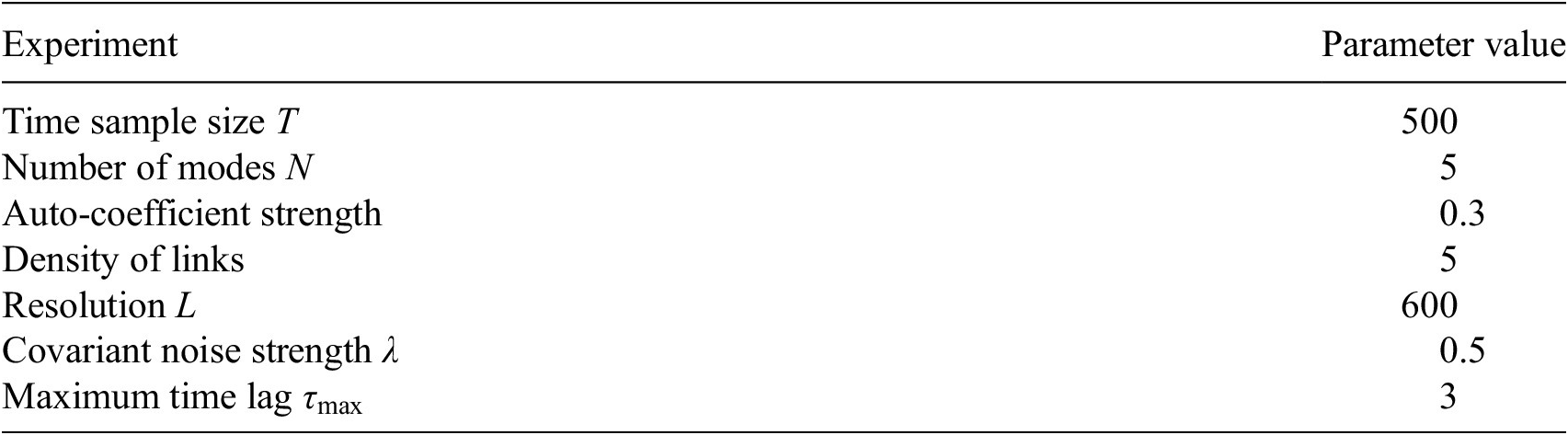

3.1. Synthetic data experiments

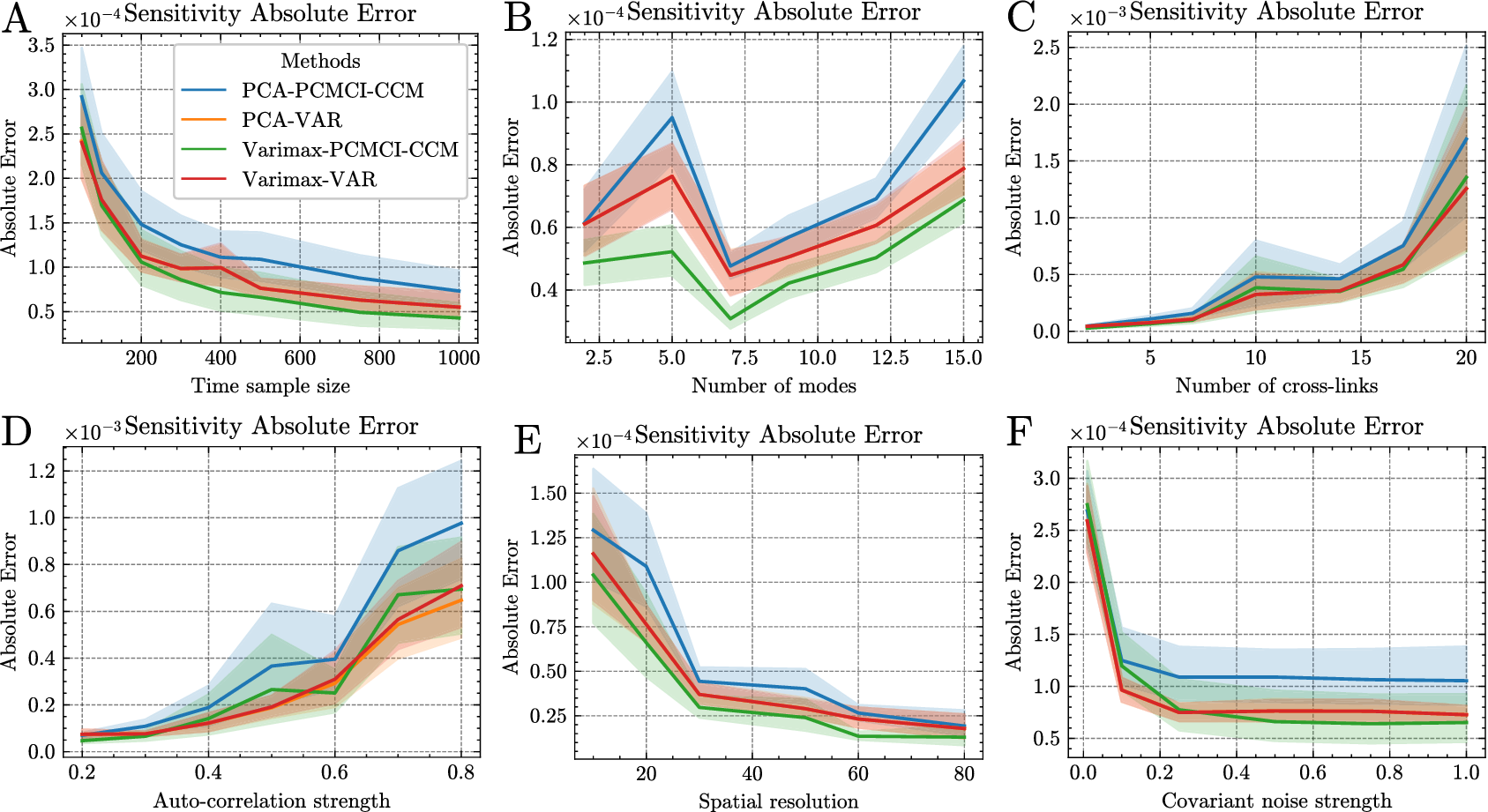

We designed two experiments with synthetic data summarized in Table 1. In Experiment 1, we carried out a benchmark analysis of four methods to estimate the sensitivity for varying SAVAR parameters. The synthetic data are generated from an SAVAR model. The sensitivity values are calculated from the explicit formulas with the estimated weights and linear coefficients. We included two methods to estimate the weights and two methods to estimate the linear coefficients. This gave us four combinations of methods to estimate the sensitivity. In Experiment 2, we compared five methods to obtain an uncertainty estimation of the sensitivity with CIs. In Experiment 1, both the aggregation weights W and the linear coefficient matrix A are estimated to assess the full estimation pipeline, whereas in Experiment 2, we assume that

$ W $

is known in order to isolate the effect of

$ W $

is known in order to isolate the effect of

$ A $

estimation on the uncertainty quantification.

$ A $

estimation on the uncertainty quantification.

Summary of the synthetic data experiments

3.1.1. Methods to estimate the sensitivity and LREs

The goal of Experiment 1 is to evaluate which estimation methods are best for estimating sensitivity and LREs from data. For this, we compared four methods to estimate sensitivity from SAVAR-generated data in the case where the weight matrix

$ \mathbf{W} $

is unknown. Each method consists of two distinct steps: the weight matrix estimation and the linear coefficients estimation. We estimated and evaluated the sensitivity from these estimated weights and linear coefficient matrices. In the main body of this article, we chose to evaluate the sensitivity, as the evaluation of this one-dimensional measure is more interpretable. We conducted separate benchmarks for the LREs, and the results are presented in the Appendix. We included the following methods in the benchmark analysis:

$ \mathbf{W} $

is unknown. Each method consists of two distinct steps: the weight matrix estimation and the linear coefficients estimation. We estimated and evaluated the sensitivity from these estimated weights and linear coefficient matrices. In the main body of this article, we chose to evaluate the sensitivity, as the evaluation of this one-dimensional measure is more interpretable. We conducted separate benchmarks for the LREs, and the results are presented in the Appendix. We included the following methods in the benchmark analysis:

-

• PCA followed by a VAR estimation

-

• PCA followed by Peter and Clark Momentary Conditional Independence (PCMCI) and a Causal Coefficient Matrix (CCM) estimation

-

• PCA-Varimax followed by a VAR estimation

-

• PCA-Varimax followed by PCMCI and a CCM estimation

To estimate the weights, two methods are compared: the PCA and the PCA-Varimax. PCA is a dimension-reduction technique that aims to maximize the variance of the components (Shaffer, Reference Shaffer2002). Additionally, PCA components must satisfy a constraint of orthogonality. Varimax is another dimension-reduction technique that builds on PCA. In the Varimax method, the PCA components are first calculated, and then these components are Varimax-rotated. The Varimax rotation follows a specific criterion (Kaiser, Reference Kaiser1958; Vautard and Ghil, Reference Vautard and Ghil1989), which makes the large PCA loadings larger and the small loadings smaller. This rotation allows the original PCA components to become non-orthogonal and more regionally confined, thereby generally enhancing the interpretability of the components (Rohe and Zeng, Reference Rohe and Zeng2023).

Next, we included two methods to estimate the linear coefficients of an SAVAR model. First, a simple least-squares VAR estimation, which we refer to as VAR estimation, is performed on the estimated components’ time series. We use the VAR estimation (Johansen, Reference Johansen and Johansen1995; Lütkepohl, Reference Lütkepohl and Lütkepohl2005), implemented in the statsmodel Python package (Seabold and Perktold, Reference Seabold and Perktold2010). The second method we include, referred to as PCMCI–CCM, exploits causality to constrain the linear coefficients to only causal dependencies in a two-step procedure. In the first step, we use a time series causal discovery algorithm, here PCMCI (Runge et al., Reference Runge, Petoukhov, Donges, Hlinka, Jajcay, Vejmelka, Hartman, Marwan, Paluš and Kurths2015; Runge et al., Reference Runge, Nowack, Kretschmer, Flaxman and Sejdinovic2019), to estimate the causal parents of each mode from the time series data. By causal parent, we refer to a direct cause of the specific variable in question. PCMCI is fundamentally different from PCA, which is used only for dimensionality reduction. PCMCI uses conditional independence tests to infer causal relationships between variables. In the second step, called CCM estimation, we estimate the linear coefficients solely for the causal dependencies identified in the previous step. PCMCI is a causal discovery algorithm adapted for time series, which estimates the time-lagged dependencies from input time series data. The PCMCI is available in the tigramite Python package at https://github.com/jakobrunge/tigramite. The CCM is estimated by performing a linear regression with ordinary least squares on the estimated causal parents. Note that the use of PCMCI comes with certain assumptions such as causal sufficiency, acyclicity, causal stationarity, causal faithfulness, and the causal Markov condition (Spirtes et al., Reference Spirtes, Glymour and Scheines1993; Runge et al., Reference Runge, Gerhardus, Varando, Eyring and Camps-Valls2023). Causal sufficiency requires the absence of unobserved variables. Causal stationarity assumes that the causal relationships and noise distributions are invariant in time. The causal faithfulness assumption and the causal Markov condition are necessary to establish the equivalence between the connectivity of causal graphs (precisely, d-separation) and conditional independence in the distribution (Runge et al., Reference Runge, Gerhardus, Varando, Eyring and Camps-Valls2023). PCMCI utilizes this property to perform statistical tests of independence from observational data. These tests provide insights that refine the structure of causal graphs. To test the conditional independence, we employ the linear partial correlation test of PCMCI. Throughout all numerical experiments, including both synthetic and real-world data, the PCMCI parameter

$ {\alpha}_{PC} $

is internally optimized. The reader can refer to (Runge et al., Reference Runge, Nowack, Kretschmer, Flaxman and Sejdinovic2019) for an in-depth explanation of PCMCI.

$ {\alpha}_{PC} $

is internally optimized. The reader can refer to (Runge et al., Reference Runge, Nowack, Kretschmer, Flaxman and Sejdinovic2019) for an in-depth explanation of PCMCI.

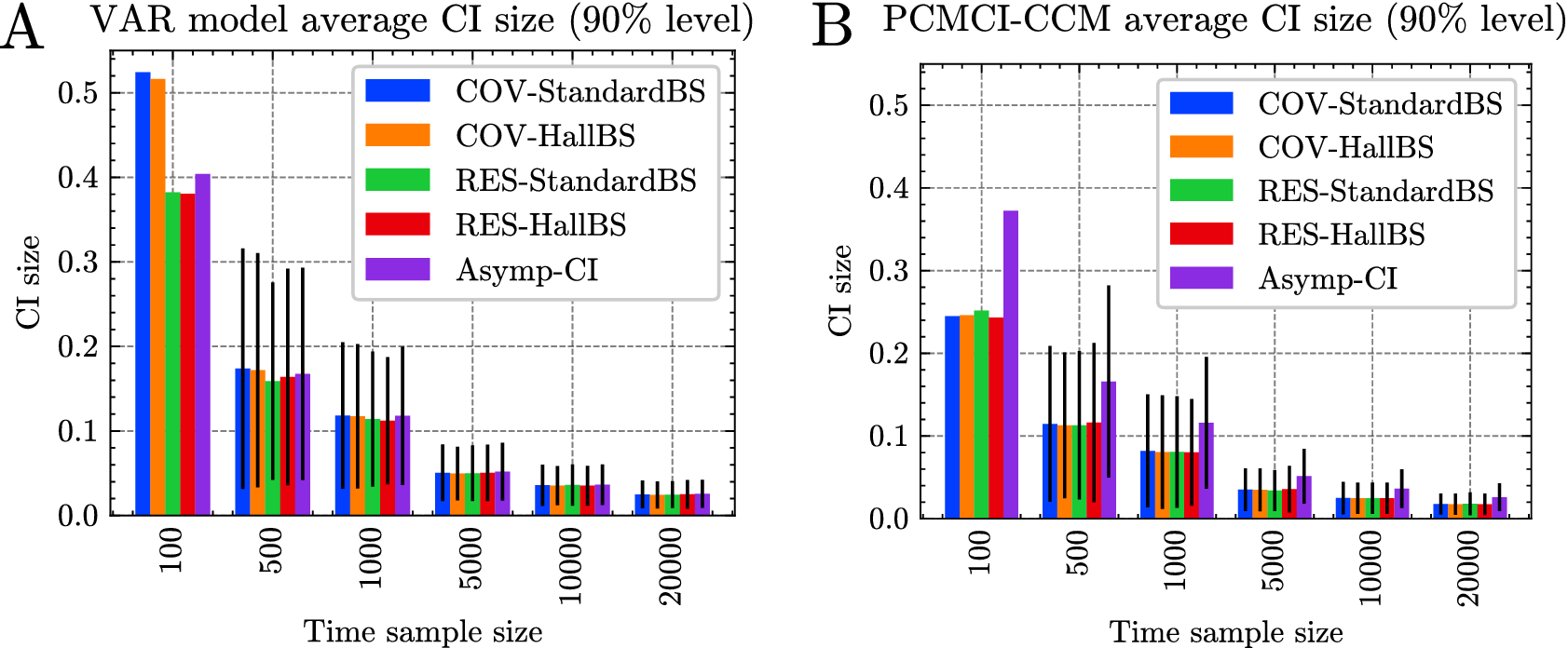

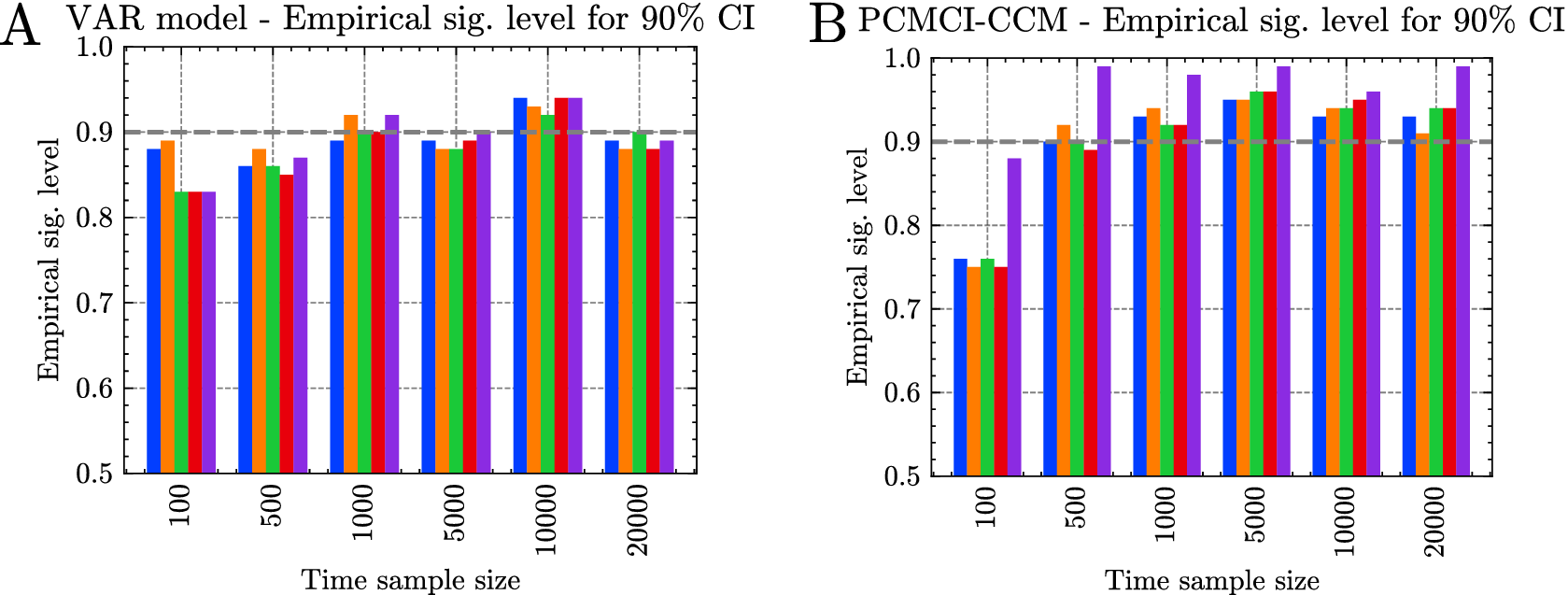

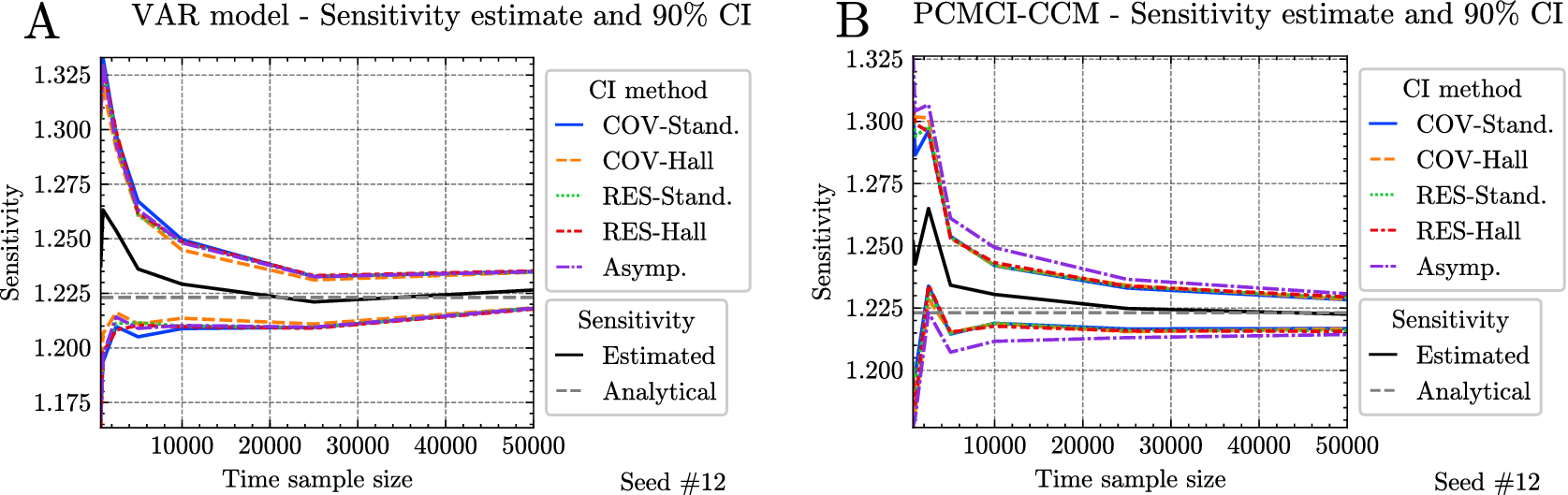

3.1.2. Methods to quantify uncertainties of the estimates (CIs)

In Experiment 2, we explored various methods for establishing CIs around sensitivity estimates. Several techniques exist for deriving CIs. In our study, we examined four bootstrap methods, which involved resampling residuals similar to techniques used in impulse response analysis (Benkwitz et al., Reference Benkwitz, Lütkepohl and Wolters2001; Lütkepohl, Reference Lütkepohl and Lütkepohl2005), along with the asymptotic-based CI outlined in Section 2.4.2. This resulted in a total of five distinct methods, listed below:

-

• Bootstrapping with resampling of the residuals (Efron and Tibshirani, Reference Efron and Tibshirani1995) and standard percentile interval (abbreviated to Res-Standard),

-

• Bootstrapping with resampling of the residuals and with Hall’s percentile interval (Hall, Reference Hall1992) (abbreviated to Res-Hall),

-

• Bootstrapping with sampling from the covariance of the residuals (Efron and Tibshirani, Reference Efron and Tibshirani1995) and standard percentile interval (abbreviated to Cov-Standard),

-

• Bootstrapping with sampling from the covariance of the residuals and with Hall’s percentile interval (Hall, Reference Hall1992) (abbreviated to Cov-Hall),

-

• CI based on the asymptotic normal distribution of the estimator we have derived in Section 2.4.2 (abbreviated to Asymp.).

Throughout the rest of this article, we refer to confidence interval as CI. For further information on the various bootstrap procedures, please refer to Appendix A.4. In this experiment, we assumed that the true weights, denoted as

$ \mathbf{W} $

, are known. However, only the linear coefficients, represented by

$ \mathbf{W} $

, are known. However, only the linear coefficients, represented by

$ \mathbf{A} $

, are estimated. This estimation is performed using either the PCMCI–CCM method or the VAR estimation.

$ \mathbf{A} $

, are estimated. This estimation is performed using either the PCMCI–CCM method or the VAR estimation.

3.1.3. Setup of Experiment 1

In Experiment 1, we performed a benchmark analysis of the methods introduced in Section 3.1.1 to estimate the sensitivity from synthetic data. In particular, we considered the global sensitivity (i.e., the global effects over all small-scale variables) for a uniform and constant unit forcing.

Similar to the numerical experiments in Tibau et al. (Reference Tibau, Reimers, Gerhardus, Denzler, Eyring and Runge2022), the synthetic data are generated from an SAVAR model (see Equation (2.1)). The weights of the

$ N $

modes

$ N $

modes

$ \mathbf{W} $

are generated randomly from nonoverlapping boxes in a space of size

$ \mathbf{W} $

are generated randomly from nonoverlapping boxes in a space of size

$ 20\times 30 $

(called resolution). Their shape is that of a bivariate Gaussian distribution computed from a random positive-definite covariance matrix. The underlying causal dependencies among these modes are modeled by the matrix

$ 20\times 30 $

(called resolution). Their shape is that of a bivariate Gaussian distribution computed from a random positive-definite covariance matrix. The underlying causal dependencies among these modes are modeled by the matrix

$ \mathbf{A} $

given in Equation (2.1). All modes are autocorrelated and have coefficients drawn from a truncated Gaussian distribution with a mean of 0.3 (called auto-coefficient strength) and a variance of 0.2. The coefficients have an absolute value greater than 0.2 and have a probability of 0.5 to be negative or positive. Furthermore, five (called density of links) cross-dependencies are randomly chosen with a random time lag of between 1 and 3 and a coefficient drawn from the same distribution as the autocorrelation coefficients but with a probability of 0.2 to be negative. By default, the covariance noise strength

$ \mathbf{A} $

given in Equation (2.1). All modes are autocorrelated and have coefficients drawn from a truncated Gaussian distribution with a mean of 0.3 (called auto-coefficient strength) and a variance of 0.2. The coefficients have an absolute value greater than 0.2 and have a probability of 0.5 to be negative or positive. Furthermore, five (called density of links) cross-dependencies are randomly chosen with a random time lag of between 1 and 3 and a coefficient drawn from the same distribution as the autocorrelation coefficients but with a probability of 0.2 to be negative. By default, the covariance noise strength

$ \lambda =0.5 $

. We fixed

$ \lambda =0.5 $

. We fixed

$ {\mathbf{D}}_{\mathbf{x}} $

and

$ {\mathbf{D}}_{\mathbf{x}} $

and

$ {\mathbf{D}}_{\mathbf{y}} $

as identity matrices and consider zero means

$ {\mathbf{D}}_{\mathbf{y}} $

as identity matrices and consider zero means

$ {\mu}_{\mathbf{y}} $

= 0. The generated time series have a default time sample size of 500. Only stationary models are considered.

$ {\mu}_{\mathbf{y}} $

= 0. The generated time series have a default time sample size of 500. Only stationary models are considered.

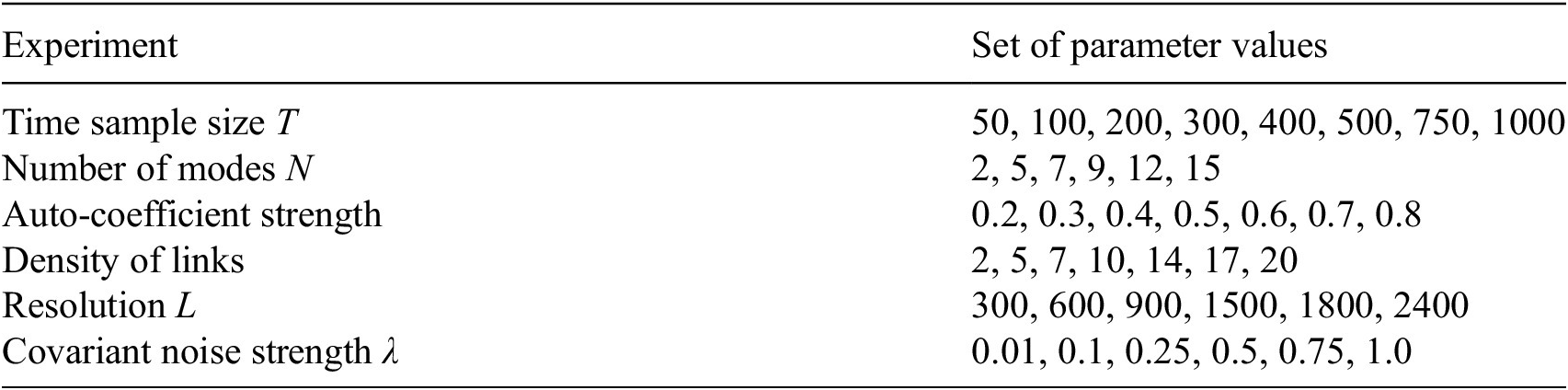

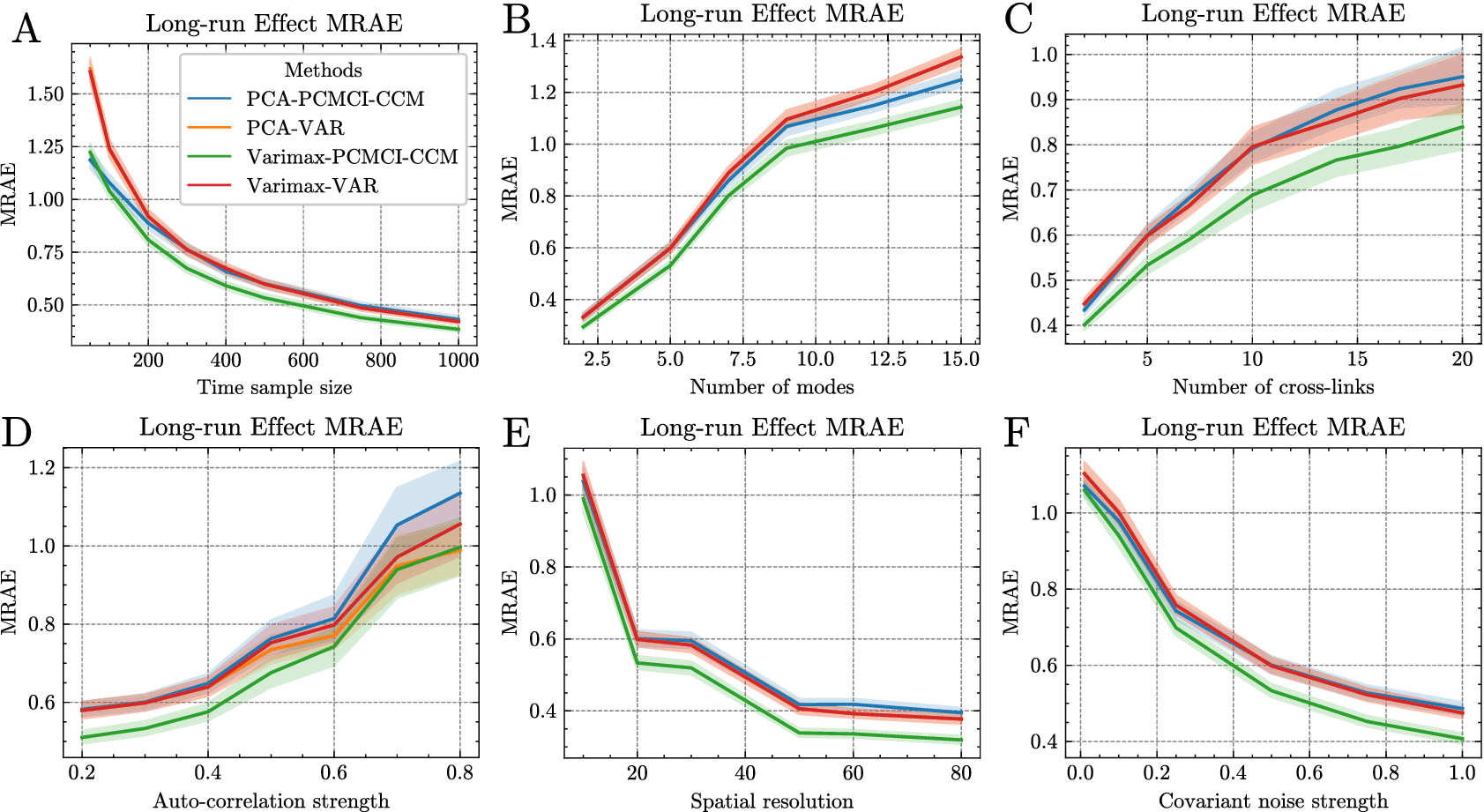

To compare the different methods, we designed a set of experiments in which we vary one of the following parameters:

-

• Time sample size: the number of data samples available. This will reveal the impact of sample size on the error of the LREs estimated with different dimension-reduction methods and linear coefficient estimation methods.

-

• Number of modes: the number of large-scale variables in the SAVAR model. The number of cross-links is also set to the number of modes, such that the average cross-in-degree is 1 for all models. This ensures consistent sparsity levels across the models. We study the impact of an increasing number of modes on the performance of the dimension reduction method and the estimation of the linear coefficients.

-

• Auto-coefficient strength: the strength of time-lagged dependencies of one mode with itself. Studies have shown that high auto-dependencies can lead to the detection of spurious links (zero linear coefficients that are estimated to be statistically different from zero). This experiment unveils if the method to estimate the linear coefficients can cope with the high auto-dependencies of the modes.

-

• Density of links: the number of time-lagged dependencies between the different modes. The methods will be faced with increasing complexity (number of dependencies across the modes).

-

• Resolution: the number of points on which the modes are defined. These will reveal the performance of the methods for an increasing number of points.

-

• Covariance noise strength: the importance of the variability of the modes relative to the variability of each point. This experiment will highlight the impact of each noise term on the estimation of the LREs and sensitivity.

All experiments followed the same default parameters setup. The parameter values of the default setup are given in Table 2. For each experiment, we varied only one of the described parameters of the default setup. The set of values of the varying parameters of each sub-experiment is shown in Table 3. For each sub-experiment, we generated and evaluated 250 SAVAR realizations to obtain a CI of the evaluation metric. To evaluate the estimated sensitivity in each SAVAR realization, the absolute error (AE) is calculated as the absolute difference between the actual sensitivity (

$ \alpha $

) and the estimated sensitivity (

$ \alpha $

) and the estimated sensitivity (

$ \hat{\alpha} $

):

$ \hat{\alpha} $

):

$ AE\left(\alpha, \hat{\alpha}\right)=\mid \alpha -\hat{\alpha}\mid $

. The final evaluation metric is the mean absolute error (MAE) which is obtained by averaging the AEs across the 250 SAVAR realizations.

$ AE\left(\alpha, \hat{\alpha}\right)=\mid \alpha -\hat{\alpha}\mid $

. The final evaluation metric is the mean absolute error (MAE) which is obtained by averaging the AEs across the 250 SAVAR realizations.

Numerical experiments’ default setup

Parameters values for Experiment 1

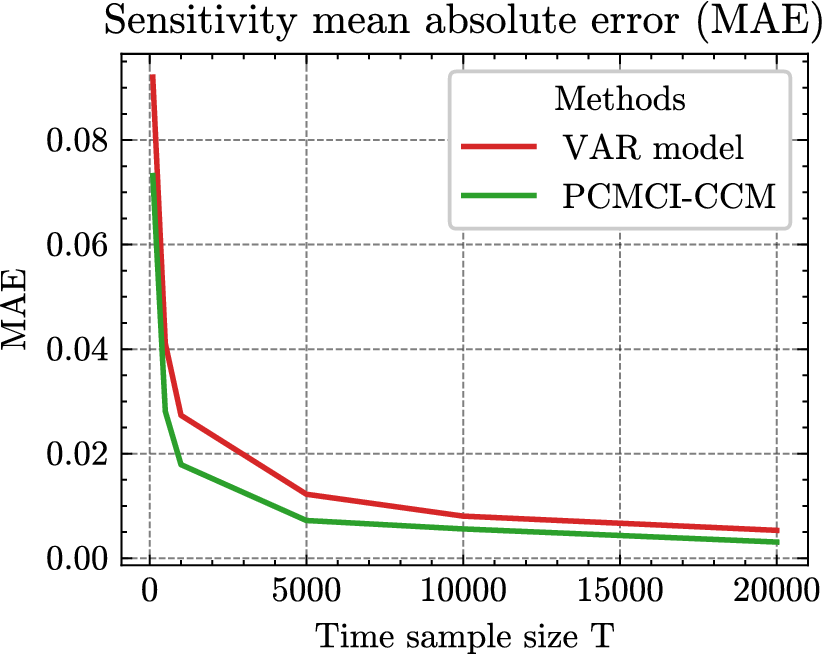

3.1.4. Experimental setup for Experiment 2

In Experiment 2, we compared the different CI methods introduced in Section 3.1.2 for the sensitivity. In addition, to study the effect of the sample size on the different CI methods, we conducted an experiment that follows the default setup of Experiment 1, described in Table 2, in which the sample size varies from

$ 100 $

to

$ 100 $

to

$ 20000 $

. We generated the synthetic data using 100 random stationary SAVAR models following Equation (2.1). We assumed the true weights

$ 20000 $