I. Introduction

Given a chosen universe of

$ M $

assets, conventional wisdom argues that an unconstrained rational investor should invest in all

$ M $

assets, conventional wisdom argues that an unconstrained rational investor should invest in all

$ M $

assets to diversify idiosyncratic risk and improve the efficient frontier. However, this is at odds with the concentrated portfolios typically observed in practice among individual investors (Calvet, Campbell, and Sodini (Reference Calvet, Campbell and Sodini2007), Campbell (Reference Campbell2006), and Goetzmann and Kumar (Reference Goetzmann and Kumar2008)) and institutions (Koijen and Yogo (Reference Koijen and Yogo2019)).Footnote 1 As reviewed by Boyle, Garlappi, Uppal, and Wang (Reference Boyle, Garlappi, Uppal and Wang2012), various papers aim to rationalize the concentrated portfolios of investors or to explain them with behavioral biases. Existing explanations consider, for example, transaction costs, short-sale constraints, prospect theory, overconfidence, cost of information, geographical closeness and familiarity, private incentives, or preferences for higher-order moments.

$ M $

assets to diversify idiosyncratic risk and improve the efficient frontier. However, this is at odds with the concentrated portfolios typically observed in practice among individual investors (Calvet, Campbell, and Sodini (Reference Calvet, Campbell and Sodini2007), Campbell (Reference Campbell2006), and Goetzmann and Kumar (Reference Goetzmann and Kumar2008)) and institutions (Koijen and Yogo (Reference Koijen and Yogo2019)).Footnote 1 As reviewed by Boyle, Garlappi, Uppal, and Wang (Reference Boyle, Garlappi, Uppal and Wang2012), various papers aim to rationalize the concentrated portfolios of investors or to explain them with behavioral biases. Existing explanations consider, for example, transaction costs, short-sale constraints, prospect theory, overconfidence, cost of information, geographical closeness and familiarity, private incentives, or preferences for higher-order moments.

Besides behavioral and financial arguments, another motivation for reducing portfolio size is parameter uncertainty (i.e., the parameters governing the asset return distribution are unknown and must be estimated). In theory, the optimal portfolio can only benefit from increased investment opportunities associated with a higher portfolio size. In practice, however, more parameters and portfolio weights must be estimated, which increases estimation risk and hurts out-of-sample performance (Barroso and Saxena (Reference Barroso and Saxena2021), DeMiguel, Garlappi, and Uppal (Reference DeMiguel, Garlappi and Uppal2009b)).

Sparse portfolio selection aims at alleviating parameter uncertainty precisely by reducing the portfolio size. This is typically achieved by imposing lasso-type constraints, also known as soft-thresholding (Ao, Li, and Zheng (Reference Ao, Li and Zheng2019), DeMiguel, Garlappi, Nogales, and Uppal (Reference DeMiguel, Garlappi, Nogales and Uppal2009a), Fan, Zhang, and Yu (Reference Fan, Zhang and Yu2012), and Yen (Reference Yen2016)) or cardinality constraints (Du, Guo, and Wang (Reference Du, Guo and Wang2023), Gao and Li (Reference Gao and Li2013)). However, these methods suffer from five main drawbacks. First, the optimization programs must be solved in dimension

$ M $

and therefore face large estimation risk, even if the output portfolio is ultimately of lower dimension. Second, they can be computationally intensive in high dimension. For instance, cardinality constraints render the portfolio problem NP-hard. Third, they entangle the selection of the assets with the optimization of portfolio weights in one single step. Therefore, sparse methods do not allow for different rebalancing frequencies for portfolio weights and the asset selection, or for flexibility in the asset selection. Fourth, they generally feature hyperparameters that are often estimated by cross-validation, which is time-consuming and adds an extra layer of estimation risk. Lastly, the resulting portfolio size

$ M $

and therefore face large estimation risk, even if the output portfolio is ultimately of lower dimension. Second, they can be computationally intensive in high dimension. For instance, cardinality constraints render the portfolio problem NP-hard. Third, they entangle the selection of the assets with the optimization of portfolio weights in one single step. Therefore, sparse methods do not allow for different rebalancing frequencies for portfolio weights and the asset selection, or for flexibility in the asset selection. Fourth, they generally feature hyperparameters that are often estimated by cross-validation, which is time-consuming and adds an extra layer of estimation risk. Lastly, the resulting portfolio size

$ N $

is implicit from the portfolio weights and does not have a clear meaning.

$ N $

is implicit from the portfolio weights and does not have a clear meaning.

To address these drawbacks of sparse portfolio selection, we propose a sequential three-stage process. First, select a portfolio strategy. In this article, we consider a class of portfolio strategies that consists of different combinations of sample mean–variance (MV), global-minimum-variance (GMV), and equal-weighted (EW) portfolios. Although more sophisticated strategies exist, this class has the benefit of being simple, theoretically important, commonly considered in the literature, and allows analytical tractability in finite samples. Second, compute an optimal portfolio size

$ N\le M $

. Third, select which

$ N\le M $

. Third, select which

$ N $

assets to invest in among the

$ N $

assets to invest in among the

$ M $

available ones and optimize the weights on the

$ M $

available ones and optimize the weights on the

$ N $

assets with the strategy in step one. Interestingly, Ao et al. (Reference Ao, Li and Zheng2019) propose a similar sequential process for reasons of computational efficiency, selecting a chosen number of

$ N $

assets with the strategy in step one. Interestingly, Ao et al. (Reference Ao, Li and Zheng2019) propose a similar sequential process for reasons of computational efficiency, selecting a chosen number of

$ N $

assets to maximize the Sharpe ratio and then implementing their MAXSER strategy on this subset. Specifically, among the S&P 500 stocks, they arbitrarily select 50 of them. In contrast, we show how to select an optimal

$ N $

assets to maximize the Sharpe ratio and then implementing their MAXSER strategy on this subset. Specifically, among the S&P 500 stocks, they arbitrarily select 50 of them. In contrast, we show how to select an optimal

$ N $

for several portfolio rules based on estimation-risk considerations.

$ N $

for several portfolio rules based on estimation-risk considerations.

Two key questions remain in our three-stage process: How do we find the optimal portfolio size

$ N $

? And how do we then select the

$ N $

? And how do we then select the

$ N $

assets? We focus on the first question. Specifically, we introduce a methodology for finding the optimal

$ N $

assets? We focus on the first question. Specifically, we introduce a methodology for finding the optimal

$ N $

and leave flexibility to the investor as to the choice of the

$ N $

and leave flexibility to the investor as to the choice of the

$ N $

assets. In our empirical analysis, we evaluate the performance of our optimal

$ N $

assets. In our empirical analysis, we evaluate the performance of our optimal

$ N $

on 10 simple and sensible asset selection rules as an illustration.

$ N $

on 10 simple and sensible asset selection rules as an illustration.

To find the optimal

$ N $

, we consider a classical setting in which investors are expected-utility maximizers with MV preferences, face no investment constraints, and returns are IID multivariate elliptically distributed. In this setting, parameter uncertainty stems from the unknown mean, covariance matrix, and fat tails of returns, which we assume are constant over time. For different portfolio rules within the class of MV portfolio combination strategies we consider, we find the optimal portfolio size

$ N $

, we consider a classical setting in which investors are expected-utility maximizers with MV preferences, face no investment constraints, and returns are IID multivariate elliptically distributed. In this setting, parameter uncertainty stems from the unknown mean, covariance matrix, and fat tails of returns, which we assume are constant over time. For different portfolio rules within the class of MV portfolio combination strategies we consider, we find the optimal portfolio size

$ N $

, using a finite-sample setting that trades off between two opposite goals: increasing investment opportunities and reducing estimation risk. This

$ N $

, using a finite-sample setting that trades off between two opposite goals: increasing investment opportunities and reducing estimation risk. This

$ N $

is optimal as it maximizes the expected out-of-sample utility (EU), the standard portfolio performance measure under parameter uncertainty (Kan and Zhou (Reference Kan and Zhou2007), Kan, Wang, and Zhou (Reference Kan, Wang and Zhou2021), and Tu and Zhou (Reference Tu and Zhou2011)), and it varies across portfolio rules depending on their estimation risk. We observe empirically that determining the optimal

$ N $

is optimal as it maximizes the expected out-of-sample utility (EU), the standard portfolio performance measure under parameter uncertainty (Kan and Zhou (Reference Kan and Zhou2007), Kan, Wang, and Zhou (Reference Kan, Wang and Zhou2021), and Tu and Zhou (Reference Tu and Zhou2011)), and it varies across portfolio rules depending on their estimation risk. We observe empirically that determining the optimal

$ N $

using our theory and selecting the

$ N $

using our theory and selecting the

$ N $

assets using different selection rules significantly outperforms investing in all

$ N $

assets using different selection rules significantly outperforms investing in all

$ M $

assets in almost 90% of considered configurations.

$ M $

assets in almost 90% of considered configurations.

Our approach has five main benefits compared with the aforementioned sparse methods. First, because we derive the portfolio size before optimizing the portfolio weights, these weights depend on a more limited number of parameters and, thus, face less estimation risk. Second, our approach is computationally less expensive because our optimal

$ N $

can be found very efficiently and the portfolio weights are then optimized on a universe of smaller dimension. Third, our optimal

$ N $

can be found very efficiently and the portfolio weights are then optimized on a universe of smaller dimension. Third, our optimal

$ N $

depends on the data, the portfolio strategy, and the objective function, but is agnostic as to the selection rule determining which

$ N $

depends on the data, the portfolio strategy, and the objective function, but is agnostic as to the selection rule determining which

$ N $

assets to invest in (i.e., the investor has flexibility regarding asset selection). This allows different rebalancing frequencies for portfolio weights and asset selection, which is valuable in practice.Footnote 2 Fourth, our approach does not require the calibration of any hyperparameter such as a constraint threshold. Lastly, the optimal

$ N $

assets to invest in (i.e., the investor has flexibility regarding asset selection). This allows different rebalancing frequencies for portfolio weights and asset selection, which is valuable in practice.Footnote 2 Fourth, our approach does not require the calibration of any hyperparameter such as a constraint threshold. Lastly, the optimal

$ N $

has an intuitive meaning from trading off between investment opportunities and estimation risk when maximizing expected utility.

$ N $

has an intuitive meaning from trading off between investment opportunities and estimation risk when maximizing expected utility.

Our theoretical analysis starts with the sample MV (SMV) portfolio, which is optimal in sample, but not out of sample. Assuming that asset returns are equicorrelated as advocated by Engle and Kelly (Reference Engle and Kelly2012) and Clements, Scott, and Silvennoinen (Reference Clements, Scott and Silvennoinen2015),Footnote 3 we express the EU of this portfolio as a function of the portfolio size, the sample size, the correlation, the assets’ Sharpe ratios, and three parameters that measure the impact of fat tails.Footnote 4 We show that because SMV is highly sensitive to estimation errors, its optimal

$ N $

is typically very small. As a remedy for this large estimation risk, Kan and Zhou (Reference Kan and Zhou2007) introduce a two-fund rule (2F) that scales down the SMV portfolio by combining it with the risk-free asset to maximize the EU, which Kan and Lassance (Reference Kan and Lassance2025) extend to the case with IID multivariate elliptical returns. Building on this, we derive the optimal

$ N $

is typically very small. As a remedy for this large estimation risk, Kan and Zhou (Reference Kan and Zhou2007) introduce a two-fund rule (2F) that scales down the SMV portfolio by combining it with the risk-free asset to maximize the EU, which Kan and Lassance (Reference Kan and Lassance2025) extend to the case with IID multivariate elliptical returns. Building on this, we derive the optimal

$ N $

for the 2F. Remarkably, for typical levels of rather high correlations in equity data, this optimal

$ N $

for the 2F. Remarkably, for typical levels of rather high correlations in equity data, this optimal

$ N $

is slightly below half the sample size. Given commonly used sample sizes (e.g., 120 months), this result means that, under the 2F, a finite-sample setting, and our model assumptions, it is optimal to limit the portfolio size to optimize the out-of-sample performance.

$ N $

is slightly below half the sample size. Given commonly used sample sizes (e.g., 120 months), this result means that, under the 2F, a finite-sample setting, and our model assumptions, it is optimal to limit the portfolio size to optimize the out-of-sample performance.

In addition to the 2F, we derive the optimal

$ N $

for three-fund rules combining the SMV portfolio, the sample GMV (SGMV) portfolio, and the risk-free asset as in Kan and Zhou (Reference Kan and Zhou2007), DeMiguel, Martín-Utrera, and Nogales (Reference DeMiguel, Martín-Utrera and Nogales2015), and Yuan and Zhou (Reference Yuan and Zhou2024), or combining the SMV portfolio, the EW portfolio, and the risk-free asset as in Tu and Zhou (Reference Tu and Zhou2011), Kan and Wang (Reference Kan and Wang2023), and Lassance, Vanderveken, and Vrins (Reference Lassance, Vanderveken and Vrins2024). Similar to the 2F, the optimal

$ N $

for three-fund rules combining the SMV portfolio, the sample GMV (SGMV) portfolio, and the risk-free asset as in Kan and Zhou (Reference Kan and Zhou2007), DeMiguel, Martín-Utrera, and Nogales (Reference DeMiguel, Martín-Utrera and Nogales2015), and Yuan and Zhou (Reference Yuan and Zhou2024), or combining the SMV portfolio, the EW portfolio, and the risk-free asset as in Tu and Zhou (Reference Tu and Zhou2011), Kan and Wang (Reference Kan and Wang2023), and Lassance, Vanderveken, and Vrins (Reference Lassance, Vanderveken and Vrins2024). Similar to the 2F, the optimal

$ N $

for these rules is slightly below half the sample size for typical equity–return correlations. These results extend the literature on portfolio choice with estimation risk by showing that it is beneficial to substantially reduce the portfolio size even after optimally combining the SMV portfolio with robust strategies.

$ N $

for these rules is slightly below half the sample size for typical equity–return correlations. These results extend the literature on portfolio choice with estimation risk by showing that it is beneficial to substantially reduce the portfolio size even after optimally combining the SMV portfolio with robust strategies.

We test our theory first in simulations where we assess the performance of our optimal

$ N $

when i) it is subject to estimation errors, ii) asset returns are not equicorrelated, and iii) the selection of the

$ N $

when i) it is subject to estimation errors, ii) asset returns are not equicorrelated, and iii) the selection of the

$ N $

assets out of the

$ N $

assets out of the

$ M $

available ones is random. The main conclusion is that the size-optimized two-fund and three-fund rules still deliver an EU close to the maximum and substantially larger than that when investing in all

$ M $

available ones is random. The main conclusion is that the size-optimized two-fund and three-fund rules still deliver an EU close to the maximum and substantially larger than that when investing in all

$ M $

assets or in too few assets. This shows that our method delivers a satisfying performance even when relaxing the theoretical assumptions, highlighting its practical relevance. Moreover, the simulation analysis allows us to illustrate that, for realistic values of the sample size, our size-optimized two-fund and three-fund rules can outperform more sophisticated benchmark MV portfolios that reduce the portfolio size using soft or hard-thresholding, as well as a factor-plus-alpha (F+A) strategy built on PCA (principal component analysis) and the arbitrage portfolio of Da, Nagel, and Xiu (Reference Da, Nagel and Xiu2024).

$ M $

assets or in too few assets. This shows that our method delivers a satisfying performance even when relaxing the theoretical assumptions, highlighting its practical relevance. Moreover, the simulation analysis allows us to illustrate that, for realistic values of the sample size, our size-optimized two-fund and three-fund rules can outperform more sophisticated benchmark MV portfolios that reduce the portfolio size using soft or hard-thresholding, as well as a factor-plus-alpha (F+A) strategy built on PCA (principal component analysis) and the arbitrage portfolio of Da, Nagel, and Xiu (Reference Da, Nagel and Xiu2024).

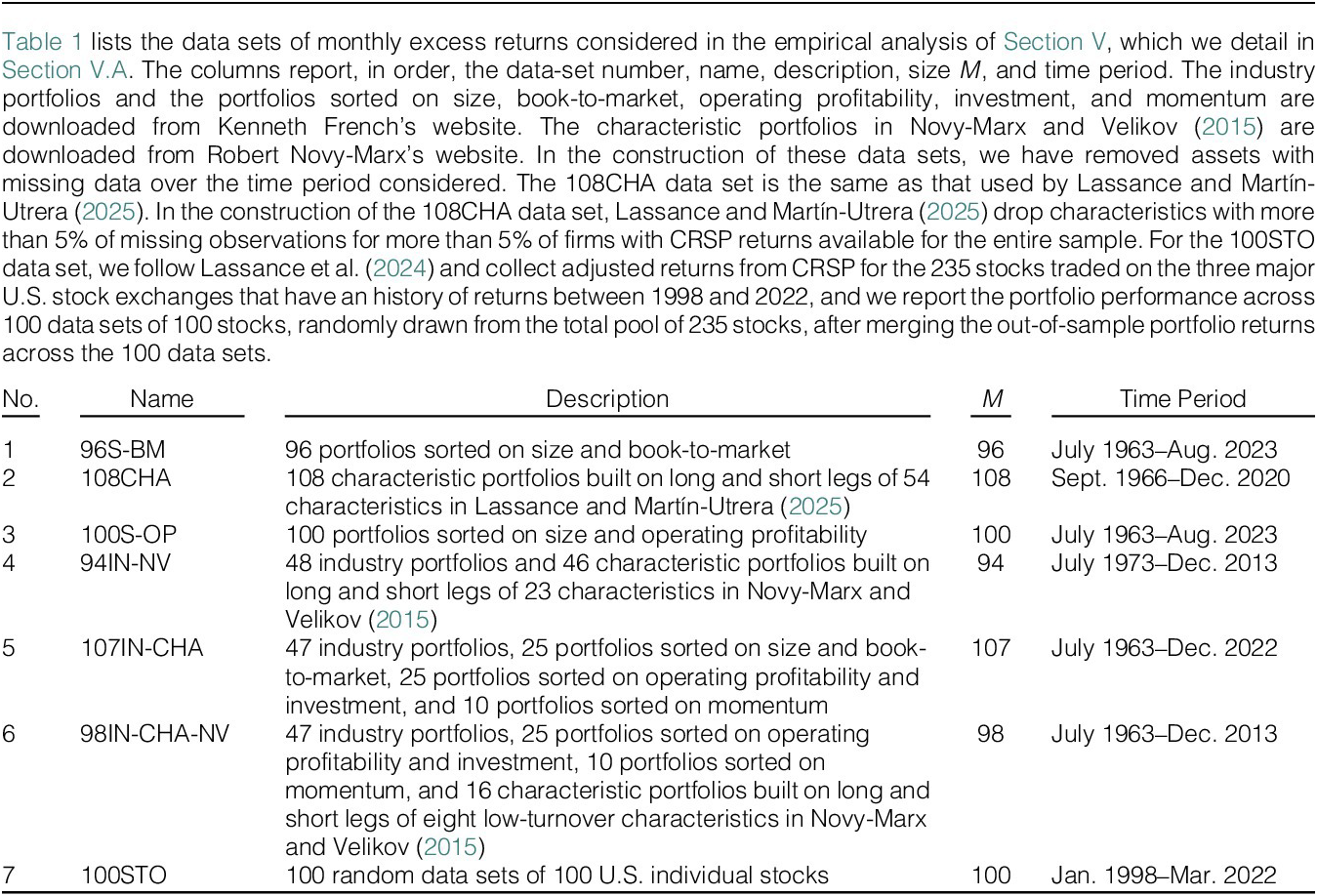

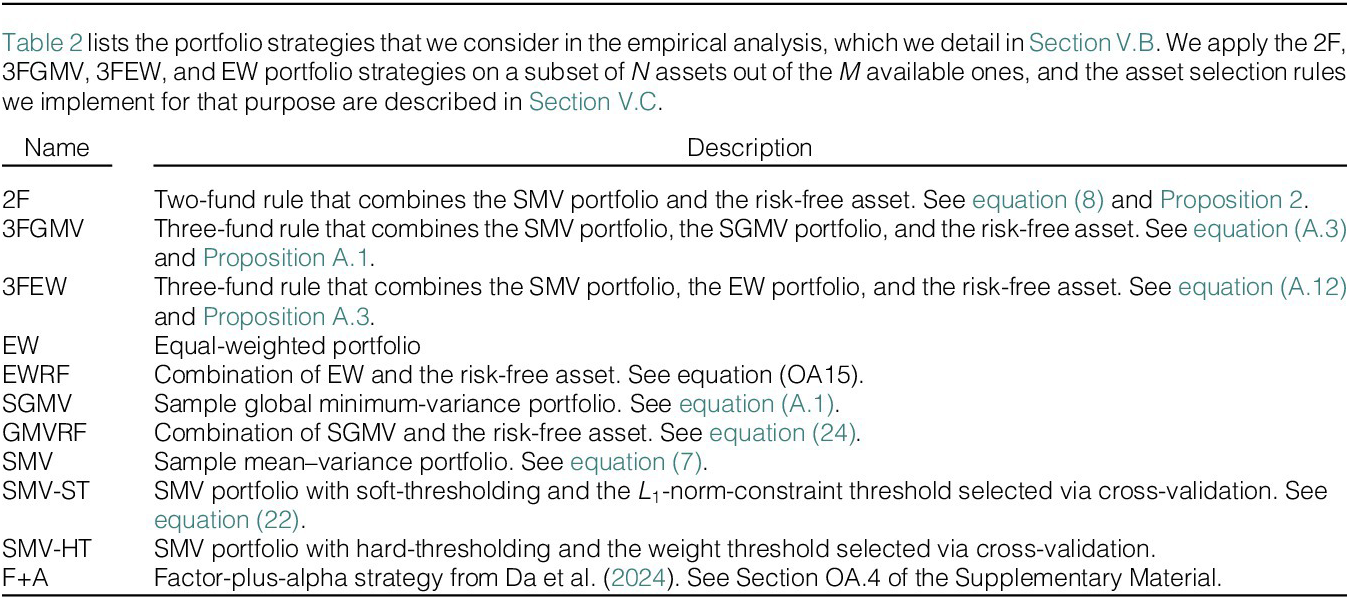

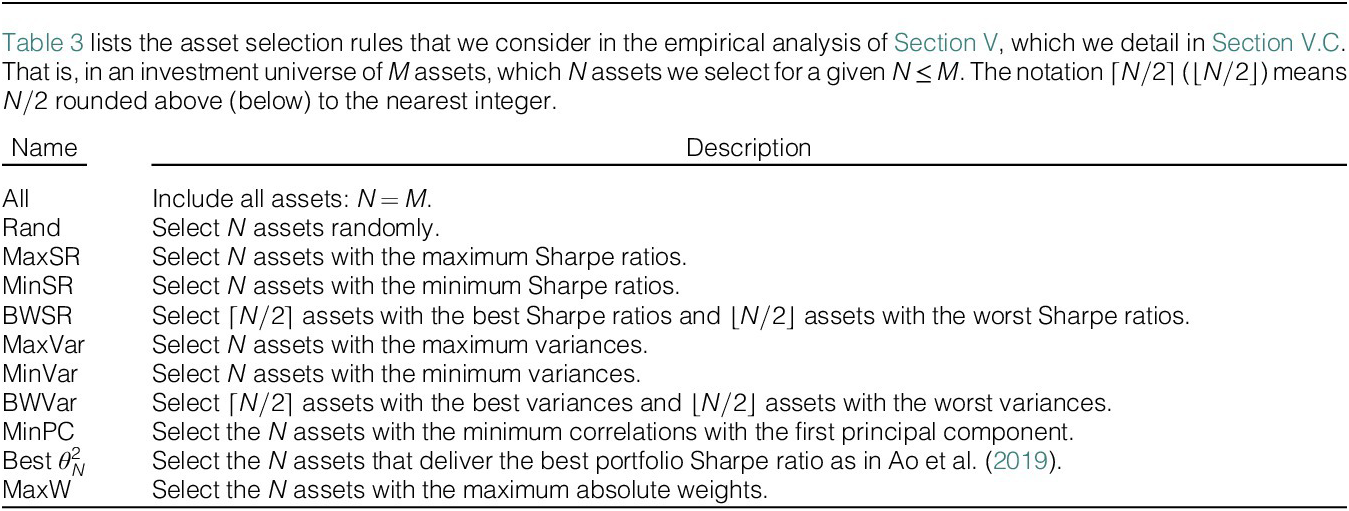

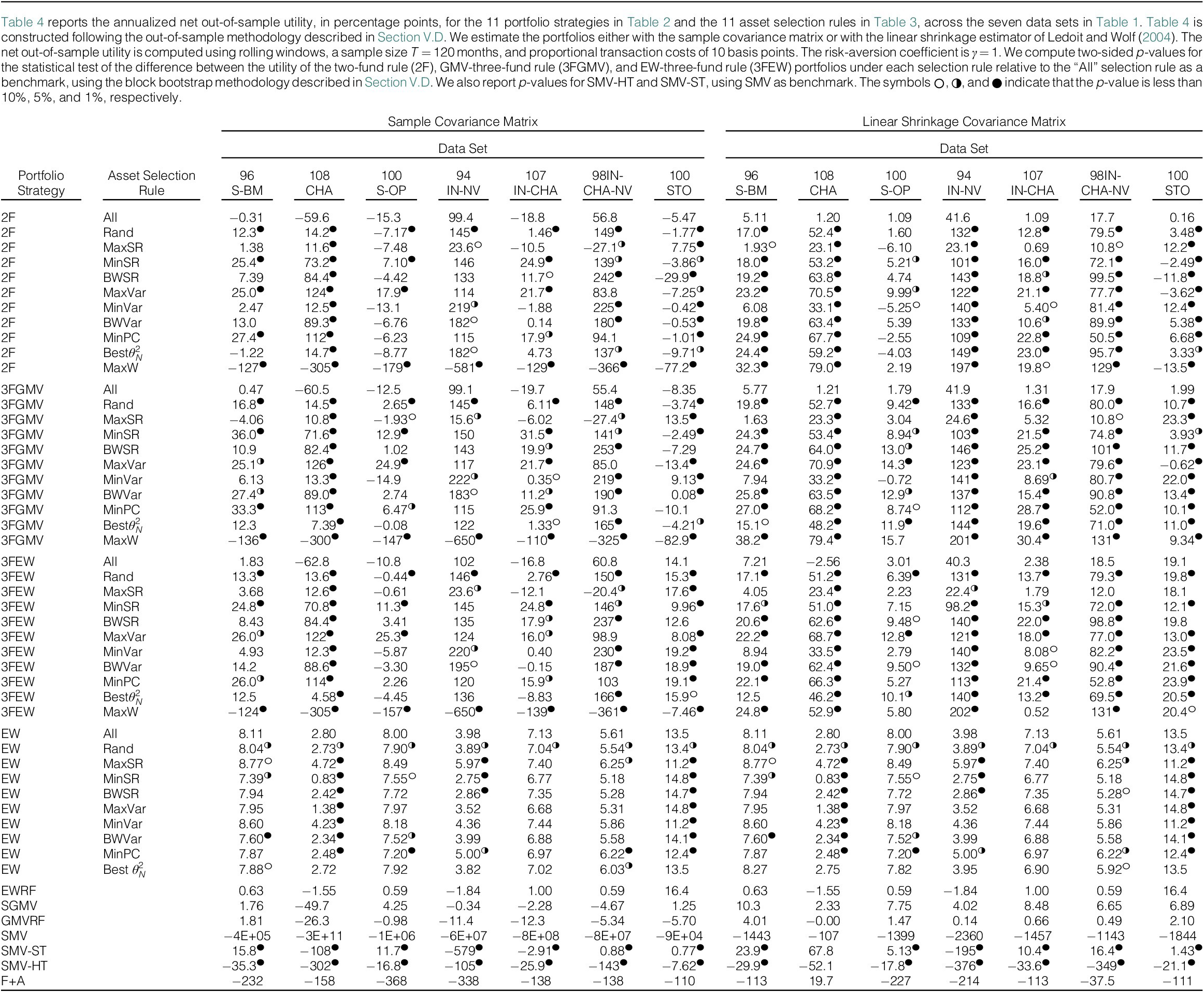

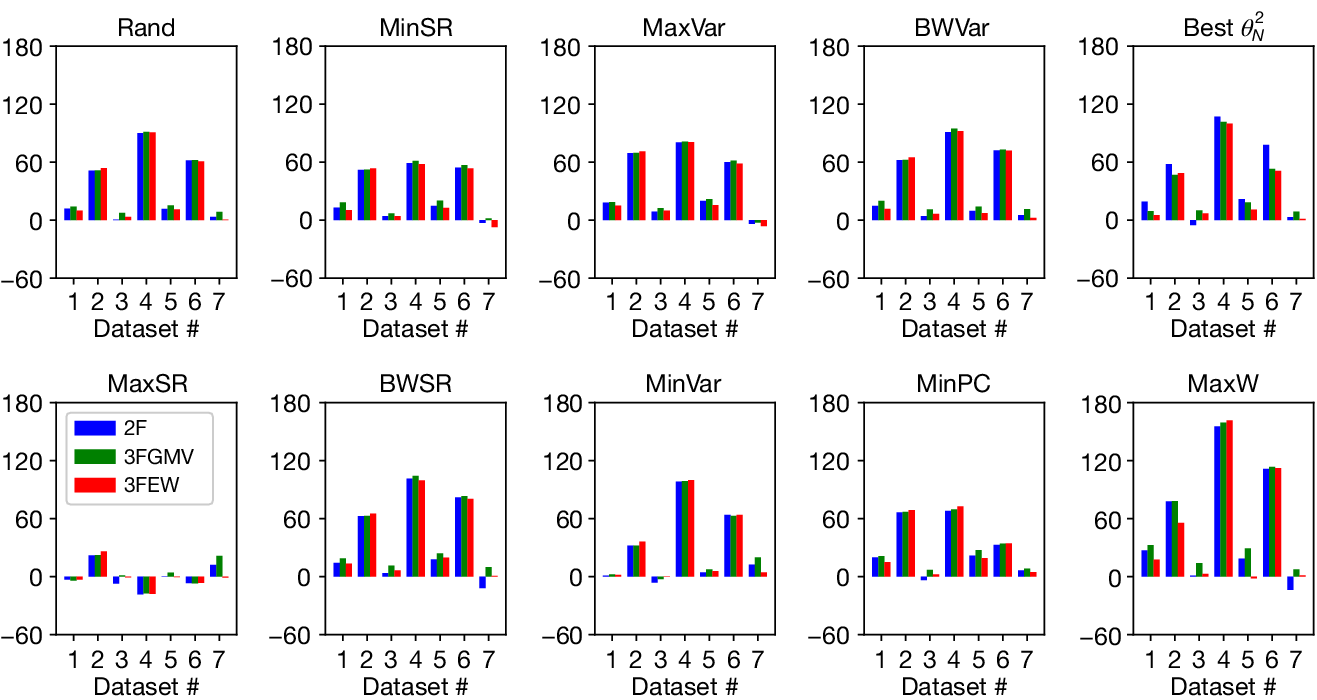

Finally, we turn to empirical data. We consider six data sets of characteristic and industry-sorted portfolios and one data set of individual stocks, with

$ M $

around 100. Using a rolling window of 120 months, we compare the net out-of-sample utility of 11 portfolio strategies, including our size-optimized two-fund and three-fund rules. For the latter, we propose 10 simple and sensible selection rules to decide which

$ M $

around 100. Using a rolling window of 120 months, we compare the net out-of-sample utility of 11 portfolio strategies, including our size-optimized two-fund and three-fund rules. For the latter, we propose 10 simple and sensible selection rules to decide which

$ N $

assets to select. We find large benefits from optimizing

$ N $

assets to select. We find large benefits from optimizing

$ N $

using our theory. In the vast majority of cases, the two-fund and three-fund rules implemented with the 10 asset selection rules outperform the same rules applied to all

$ N $

using our theory. In the vast majority of cases, the two-fund and three-fund rules implemented with the 10 asset selection rules outperform the same rules applied to all

$ M $

assets. The improvement is particularly large and statistically significant when we shrink the covariance matrix. Moreover, for some asset selection rules, our size-optimized portfolio rules consistently outperform the EW and SGMV portfolios, a notoriously difficult task when the data-set dimension

$ M $

assets. The improvement is particularly large and statistically significant when we shrink the covariance matrix. Moreover, for some asset selection rules, our size-optimized portfolio rules consistently outperform the EW and SGMV portfolios, a notoriously difficult task when the data-set dimension

$ M $

is comparable with the sample size, as well as soft and hard-thresholding MV portfolios and the F+A strategy.

$ M $

is comparable with the sample size, as well as soft and hard-thresholding MV portfolios and the F+A strategy.

Our article complements existing work that studies the effect of the portfolio size

$ N $

using asymptotic theories. In particular, Ao et al. (Reference Ao, Li and Zheng2019) and Da et al. (Reference Da, Nagel and Xiu2024) consider a class of more sophisticated portfolio strategies that treats estimation risk differently from ours via soft-thresholding and a factor model, respectively. They find, under specific assumptions, that they can asymptotically achieve the performance of the population optimal portfolio as both the portfolio size and the sample size go to infinity. That is, in their asymptotic theories, it is optimal to increase

$ N $

using asymptotic theories. In particular, Ao et al. (Reference Ao, Li and Zheng2019) and Da et al. (Reference Da, Nagel and Xiu2024) consider a class of more sophisticated portfolio strategies that treats estimation risk differently from ours via soft-thresholding and a factor model, respectively. They find, under specific assumptions, that they can asymptotically achieve the performance of the population optimal portfolio as both the portfolio size and the sample size go to infinity. That is, in their asymptotic theories, it is optimal to increase

$ N $

. We complement these results by studying a simpler, but nonetheless important, class of portfolio strategies for which we can study the out-of-sample performance analytically in a finite-sample setting. In that case, we find that it is optimal to reduce the portfolio size

$ N $

. We complement these results by studying a simpler, but nonetheless important, class of portfolio strategies for which we can study the out-of-sample performance analytically in a finite-sample setting. In that case, we find that it is optimal to reduce the portfolio size

$ N $

. Our simulation and empirical results signal that asymptotic theories like those of Ao et al. (Reference Ao, Li and Zheng2019) and Da et al. (Reference Da, Nagel and Xiu2024), which suggest that increasing

$ N $

. Our simulation and empirical results signal that asymptotic theories like those of Ao et al. (Reference Ao, Li and Zheng2019) and Da et al. (Reference Da, Nagel and Xiu2024), which suggest that increasing

$ N $

is beneficial, might not kick in for realistic sample sizes and typically deliver a performance inferior to that of our size-optimized portfolios.

$ N $

is beneficial, might not kick in for realistic sample sizes and typically deliver a performance inferior to that of our size-optimized portfolios.

This article is structured as follows: In Section II, we study the optimal portfolio size for the MV portfolio with no parameter uncertainty. In Section III, we show how to derive an optimal

$ N $

for the SMV portfolio and the 2F under parameter uncertainty. Sections IV and V contain our simulation and empirical analysis, respectively. Section VI concludes. The Appendix contains results and proofs that are central to the main text. The Supplementary Material provides additional theoretical, simulation, and empirical results.

$ N $

for the SMV portfolio and the 2F under parameter uncertainty. Sections IV and V contain our simulation and empirical analysis, respectively. Section VI concludes. The Appendix contains results and proofs that are central to the main text. The Supplementary Material provides additional theoretical, simulation, and empirical results.

II. Optimal Portfolio Size Without Parameter Uncertainty

In this section, we study the optimal portfolio size for an unconstrained MV investor who knows the parameters of asset returns without uncertainty. We suppose that the investor starts from a universe of

$ M $

assets and wishes to find an optimal number

$ M $

assets and wishes to find an optimal number

$ N\le M $

of assets.

$ N\le M $

of assets.

Given a fixed number

$ N $

of assets, let

$ N $

of assets, let

$ {\boldsymbol{r}}_t $

be the

$ {\boldsymbol{r}}_t $

be the

$ N\times 1 $

vector of asset excess returns at time

$ N\times 1 $

vector of asset excess returns at time

$ t $

, which has a mean

$ t $

, which has a mean

$ {\boldsymbol{\mu}}_N $

and a positive-definite covariance matrix

$ {\boldsymbol{\mu}}_N $

and a positive-definite covariance matrix

$ {\boldsymbol{\Sigma}}_N $

. We denote by

$ {\boldsymbol{\Sigma}}_N $

. We denote by

$ {\mu}_i $

,

$ {\mu}_i $

,

$ {\sigma}_i^2 $

, and

$ {\sigma}_i^2 $

, and

$ {s}_i={\mu}_i/{\sigma}_i $

the mean excess return, variance, and Sharpe ratio of asset

$ {s}_i={\mu}_i/{\sigma}_i $

the mean excess return, variance, and Sharpe ratio of asset

$ i $

. An MV investor with risk-aversion coefficient

$ i $

. An MV investor with risk-aversion coefficient

$ \gamma >0 $

selects the portfolio weights on the risky assets as

$ \gamma >0 $

selects the portfolio weights on the risky assets as

$$ {\boldsymbol{w}}^{\star }=\underset{\boldsymbol{w}\in {\mathrm{\mathbb{R}}}^N}{\arg \max }U\left(\boldsymbol{w}\right)=\underset{\boldsymbol{w}\in {\mathrm{\mathbb{R}}}^N}{\arg \max }{\boldsymbol{w}}^{\prime }{\boldsymbol{\mu}}_N-\frac{\gamma }{2}{\boldsymbol{w}}^{\prime }{\boldsymbol{\Sigma}}_N\boldsymbol{w}, $$

$$ {\boldsymbol{w}}^{\star }=\underset{\boldsymbol{w}\in {\mathrm{\mathbb{R}}}^N}{\arg \max }U\left(\boldsymbol{w}\right)=\underset{\boldsymbol{w}\in {\mathrm{\mathbb{R}}}^N}{\arg \max }{\boldsymbol{w}}^{\prime }{\boldsymbol{\mu}}_N-\frac{\gamma }{2}{\boldsymbol{w}}^{\prime }{\boldsymbol{\Sigma}}_N\boldsymbol{w}, $$

where

$ U\left(\boldsymbol{w}\right) $

is the MV utility of portfolio

$ U\left(\boldsymbol{w}\right) $

is the MV utility of portfolio

$ \boldsymbol{w} $

. Solving (1) yields the MV portfolio satisfying

$ \boldsymbol{w} $

. Solving (1) yields the MV portfolio satisfying

$$ {\boldsymbol{w}}^{\star }=\frac{1}{\gamma }{\boldsymbol{\Sigma}}_N^{-1}{\boldsymbol{\mu}}_N\hskip1em \mathrm{and}\hskip1em U\left({\boldsymbol{w}}^{\star}\right)=\frac{\theta_N^2}{2\gamma}\hskip1em \mathrm{with}\hskip1em {\theta}_N^2={\boldsymbol{\mu}}_N^{\prime }{\boldsymbol{\Sigma}}_N^{-1}{\boldsymbol{\mu}}_N, $$

$$ {\boldsymbol{w}}^{\star }=\frac{1}{\gamma }{\boldsymbol{\Sigma}}_N^{-1}{\boldsymbol{\mu}}_N\hskip1em \mathrm{and}\hskip1em U\left({\boldsymbol{w}}^{\star}\right)=\frac{\theta_N^2}{2\gamma}\hskip1em \mathrm{with}\hskip1em {\theta}_N^2={\boldsymbol{\mu}}_N^{\prime }{\boldsymbol{\Sigma}}_N^{-1}{\boldsymbol{\mu}}_N, $$

where

$ {\theta}_N $

is the maximum Sharpe ratio. We have that

$ {\theta}_N $

is the maximum Sharpe ratio. We have that

$ {\boldsymbol{w}}^{\star } $

combines two funds: the fully invested tangency portfolio,

$ {\boldsymbol{w}}^{\star } $

combines two funds: the fully invested tangency portfolio,

$ \boldsymbol{w}={\left({\mathbf{1}}_N^{\prime }{\boldsymbol{\Sigma}}_N^{-1}{\boldsymbol{\mu}}_N\right)}^{-1}{\boldsymbol{\Sigma}}_N^{-1}{\boldsymbol{\mu}}_N $

, and the risk-free asset,

$ \boldsymbol{w}={\left({\mathbf{1}}_N^{\prime }{\boldsymbol{\Sigma}}_N^{-1}{\boldsymbol{\mu}}_N\right)}^{-1}{\boldsymbol{\Sigma}}_N^{-1}{\boldsymbol{\mu}}_N $

, and the risk-free asset,

$ \boldsymbol{w}={\mathbf{0}}_N $

.

$ \boldsymbol{w}={\mathbf{0}}_N $

.

Clearly,

$ U\left({\boldsymbol{w}}^{\star}\right) $

is nondecreasing with

$ U\left({\boldsymbol{w}}^{\star}\right) $

is nondecreasing with

$ N $

because one can set the weight of an additional asset to 0 and keep the same utility. Thus, without parameter uncertainty, it is optimal to consider the whole investment universe and set

$ N $

because one can set the weight of an additional asset to 0 and keep the same utility. Thus, without parameter uncertainty, it is optimal to consider the whole investment universe and set

$ N=M $

. To relate

$ N=M $

. To relate

$ U\left({\boldsymbol{w}}^{\star}\right) $

and

$ U\left({\boldsymbol{w}}^{\star}\right) $

and

$ N $

explicitly, we assume the following about

$ N $

explicitly, we assume the following about

$ {\boldsymbol{\Sigma}}_M $

:

$ {\boldsymbol{\Sigma}}_M $

:

Assumption 1. The covariance matrix

$ {\boldsymbol{\Sigma}}_M $

takes the form

$ {\boldsymbol{\Sigma}}_M $

takes the form

$ {\boldsymbol{\Sigma}}_M\left(\rho \right)={\boldsymbol{D}}_M{\boldsymbol{P}}_M\left(\rho \right){\boldsymbol{D}}_M $

with

$ {\boldsymbol{\Sigma}}_M\left(\rho \right)={\boldsymbol{D}}_M{\boldsymbol{P}}_M\left(\rho \right){\boldsymbol{D}}_M $

with

$ {\boldsymbol{D}}_M $

the diagonal matrix of standard deviations and

$ {\boldsymbol{D}}_M $

the diagonal matrix of standard deviations and

$ {\boldsymbol{P}}_M\left(\rho \right) $

the equicorrelation matrix,

$ {\boldsymbol{P}}_M\left(\rho \right) $

the equicorrelation matrix,

$$ {\boldsymbol{P}}_M\left(\rho \right)=\left(1-\rho \right){\boldsymbol{I}}_M+\rho {\mathbf{1}}_M{\mathbf{1}}_M^{\prime }, $$

$$ {\boldsymbol{P}}_M\left(\rho \right)=\left(1-\rho \right){\boldsymbol{I}}_M+\rho {\mathbf{1}}_M{\mathbf{1}}_M^{\prime }, $$

where

$ {\mathbf{1}}_M $

and

$ {\mathbf{1}}_M $

and

$ {\boldsymbol{I}}_M $

are the unit vector and matrix, and

$ {\boldsymbol{I}}_M $

are the unit vector and matrix, and

$ \rho \in \left(-\frac{1}{M-1},1\right) $

so that

$ \rho \in \left(-\frac{1}{M-1},1\right) $

so that

$ {\boldsymbol{\Sigma}}_M $

is invertible.

$ {\boldsymbol{\Sigma}}_M $

is invertible.

Under Assumption 1, the dependence structure depends on a single parameter,

$ \rho $

. It follows that for any

$ \rho $

. It follows that for any

$ N\le M $

,

$ N\le M $

,

$ {\boldsymbol{\Sigma}}_N $

has the same form as in Assumption 1. This assumption is commonly used in portfolio selection to trade off between specification and estimation error.Footnote 5 We use Assumption 1 only as a way to express the EU of our portfolio rules as an explicit function of

$ {\boldsymbol{\Sigma}}_N $

has the same form as in Assumption 1. This assumption is commonly used in portfolio selection to trade off between specification and estimation error.Footnote 5 We use Assumption 1 only as a way to express the EU of our portfolio rules as an explicit function of

$ N $

, which will allow us to find the optimal

$ N $

, which will allow us to find the optimal

$ N $

. We do not need this assumption for the portfolio weights. In Section OA.1 of the Supplementary Material, we find the optimal

$ N $

. We do not need this assumption for the portfolio weights. In Section OA.1 of the Supplementary Material, we find the optimal

$ N $

under another commonly used approximation, the single-factor model, which we show is essentially equivalent to that under equicorrelation.

$ N $

under another commonly used approximation, the single-factor model, which we show is essentially equivalent to that under equicorrelation.

In the next proposition, we provide the analytical expression of

$ U\left({\boldsymbol{w}}^{\star}\right) $

under Assumption 1.Footnote 6 This is a novel result to the best of our knowledge.

$ U\left({\boldsymbol{w}}^{\star}\right) $

under Assumption 1.Footnote 6 This is a novel result to the best of our knowledge.

Proposition 1. Under Assumption 1, the utility of the MV portfolio is

$ U\left({\boldsymbol{w}}^{\star}\right)={\theta}_N^2/\left(2\gamma \right) $

with

$ U\left({\boldsymbol{w}}^{\star}\right)={\theta}_N^2/\left(2\gamma \right) $

with

$$ {\theta}_N^2=\frac{N}{1-\rho }{\delta}_N\left({\overline{\boldsymbol{\theta}}}_N\right),\hskip1em {\delta}_N\left({\overline{\boldsymbol{\theta}}}_N\right)={\overline{\theta}}_{N,2}-\frac{N\rho}{1-\rho + N\rho}{\overline{\theta}}_{N,1}^2\ge 0, $$

$$ {\theta}_N^2=\frac{N}{1-\rho }{\delta}_N\left({\overline{\boldsymbol{\theta}}}_N\right),\hskip1em {\delta}_N\left({\overline{\boldsymbol{\theta}}}_N\right)={\overline{\theta}}_{N,2}-\frac{N\rho}{1-\rho + N\rho}{\overline{\theta}}_{N,1}^2\ge 0, $$

where

$ {\overline{\boldsymbol{\theta}}}_N=\left({\overline{\theta}}_{N,1},{\overline{\theta}}_{N,2}\right) $

and

$ {\overline{\boldsymbol{\theta}}}_N=\left({\overline{\theta}}_{N,1},{\overline{\theta}}_{N,2}\right) $

and

$ {\overline{\theta}}_{N,k}=\frac{1}{N}{\sum}_{i=1}^N{s}_i^k $

. Moreover,

$ {\overline{\theta}}_{N,k}=\frac{1}{N}{\sum}_{i=1}^N{s}_i^k $

. Moreover,

$ U\left({\boldsymbol{w}}^{\star}\right) $

is nondecreasing in

$ U\left({\boldsymbol{w}}^{\star}\right) $

is nondecreasing in

$ N $

and is strictly increasing from

$ N $

and is strictly increasing from

$ N $

to

$ N $

to

$ N+1 $

whenever

$ N+1 $

whenever

$ {s}_{N+1}\ne \rho N{\overline{\theta}}_{N,1}/\left(1-\rho + N\rho \right) $

.

$ {s}_{N+1}\ne \rho N{\overline{\theta}}_{N,1}/\left(1-\rho + N\rho \right) $

.

Proposition 1 shows that the maximum utility is nondecreasing in

$ N $

. In Figure 1, we depict

$ N $

. In Figure 1, we depict

$ U\left({\boldsymbol{w}}^{\star}\right) $

as a function of

$ U\left({\boldsymbol{w}}^{\star}\right) $

as a function of

$ N\in \left\{1,\dots, M\right\} $

for

$ N\in \left\{1,\dots, M\right\} $

for

$ \rho \in \left\{\mathrm{0.2,0.5,0.8}\right\} $

and assets’ monthly Sharpe ratios

$ \rho \in \left\{\mathrm{0.2,0.5,0.8}\right\} $

and assets’ monthly Sharpe ratios

$ {s}_i $

calibrated to a data set of

$ {s}_i $

calibrated to a data set of

$ M=96 $

decile portfoliosFootnote 7 sorted on size and book-to-market (96S-BM) spanning July 1963 to August 2023.Footnote 8

$ M=96 $

decile portfoliosFootnote 7 sorted on size and book-to-market (96S-BM) spanning July 1963 to August 2023.Footnote 8

Figure 1 depicts

$ U\left({\boldsymbol{w}}^{\star}\right) $

in equation (4) as a function of the portfolio size

$ U\left({\boldsymbol{w}}^{\star}\right) $

in equation (4) as a function of the portfolio size

$ N $

under the assumption that asset returns are equicorrelated with a correlation

$ N $

under the assumption that asset returns are equicorrelated with a correlation

$ \rho \in \left\{\mathrm{0.2,0.5,0.8}\right\} $

. We calibrate the assets’ monthly Sharpe ratios to a data set of

$ \rho \in \left\{\mathrm{0.2,0.5,0.8}\right\} $

. We calibrate the assets’ monthly Sharpe ratios to a data set of

$ M=96 $

portfolios sorted on size and book-to-market spanning July 1963 to August 2023. Starting with

$ M=96 $

portfolios sorted on size and book-to-market spanning July 1963 to August 2023. Starting with

$ N=1 $

asset chosen randomly, we compute

$ N=1 $

asset chosen randomly, we compute

$ U\left({\boldsymbol{w}}^{\star}\right) $

. Then, we add a randomly selected asset not previously selected and compute

$ U\left({\boldsymbol{w}}^{\star}\right) $

. Then, we add a randomly selected asset not previously selected and compute

$ U\left({\boldsymbol{w}}^{\star}\right) $

again. We continue this procedure until

$ U\left({\boldsymbol{w}}^{\star}\right) $

again. We continue this procedure until

$ N=M $

. We repeat this procedure

$ N=M $

. We repeat this procedure

$ \mathrm{10,000} $

times and depict the average

$ \mathrm{10,000} $

times and depict the average

$ U\left({\boldsymbol{w}}^{\star}\right) $

over all draws. We consider a risk-aversion coefficient

$ U\left({\boldsymbol{w}}^{\star}\right) $

over all draws. We consider a risk-aversion coefficient

$ \gamma =1 $

.

$ \gamma =1 $

.

III. Optimal Portfolio Size Under Parameter Uncertainty

In this section, we show that it is no longer optimal for an MV investor to invest in all

$ M $

assets when the assets’ parameters are unknown and the investor relies on sample estimates.

$ M $

assets when the assets’ parameters are unknown and the investor relies on sample estimates.

A. Sample Estimates and Distributional Assumption

Given a sample of asset excess returns of size

$ T $

,

$ T $

,

$ \left({\boldsymbol{r}}_1,\dots, {\boldsymbol{r}}_T\right) $

, let

$ \left({\boldsymbol{r}}_1,\dots, {\boldsymbol{r}}_T\right) $

, let

$$ {\hat{\boldsymbol{\mu}}}_N=\frac{1}{T}\sum \limits_{t=1}^T{\boldsymbol{r}}_t\hskip1em \mathrm{and}\hskip1em {\hat{\boldsymbol{\Sigma}}}_N=\frac{1}{T}\sum \limits_{t=1}^T\left({\boldsymbol{r}}_t-{\hat{\boldsymbol{\mu}}}_N\right){\left({\boldsymbol{r}}_t-{\hat{\boldsymbol{\mu}}}_N\right)}^{\prime } $$

$$ {\hat{\boldsymbol{\mu}}}_N=\frac{1}{T}\sum \limits_{t=1}^T{\boldsymbol{r}}_t\hskip1em \mathrm{and}\hskip1em {\hat{\boldsymbol{\Sigma}}}_N=\frac{1}{T}\sum \limits_{t=1}^T\left({\boldsymbol{r}}_t-{\hat{\boldsymbol{\mu}}}_N\right){\left({\boldsymbol{r}}_t-{\hat{\boldsymbol{\mu}}}_N\right)}^{\prime } $$

be the sample estimates of

$ {\boldsymbol{\mu}}_N $

and

$ {\boldsymbol{\mu}}_N $

and

$ {\boldsymbol{\Sigma}}_N $

, and we require

$ {\boldsymbol{\Sigma}}_N $

, and we require

$ T>N $

so that

$ T>N $

so that

$ {\hat{\boldsymbol{\Sigma}}}_N $

is almost surely invertible. Given a sample portfolio

$ {\hat{\boldsymbol{\Sigma}}}_N $

is almost surely invertible. Given a sample portfolio

$ \hat{\boldsymbol{w}} $

estimated with

$ \hat{\boldsymbol{w}} $

estimated with

$ {\hat{\boldsymbol{\mu}}}_N $

and

$ {\hat{\boldsymbol{\mu}}}_N $

and

$ {\hat{\boldsymbol{\Sigma}}}_N $

, we measure its performance with the EU pioneered by Kan and Zhou (Reference Kan and Zhou2007),

$ {\hat{\boldsymbol{\Sigma}}}_N $

, we measure its performance with the EU pioneered by Kan and Zhou (Reference Kan and Zhou2007),

$$ EU\left(\hat{\boldsymbol{w}}\right)=\unicode{x1D53C}\left[U\left(\hat{\boldsymbol{w}}\right)\right]=\unicode{x1D53C}\left[{\hat{\boldsymbol{w}}}^{\prime }{\boldsymbol{\mu}}_N-\frac{\gamma }{2}{\hat{\boldsymbol{w}}}^{\prime }{\boldsymbol{\Sigma}}_N\hat{\boldsymbol{w}}\right]. $$

$$ EU\left(\hat{\boldsymbol{w}}\right)=\unicode{x1D53C}\left[U\left(\hat{\boldsymbol{w}}\right)\right]=\unicode{x1D53C}\left[{\hat{\boldsymbol{w}}}^{\prime }{\boldsymbol{\mu}}_N-\frac{\gamma }{2}{\hat{\boldsymbol{w}}}^{\prime }{\boldsymbol{\Sigma}}_N\hat{\boldsymbol{w}}\right]. $$

We then define

$ {N}^{\star } $

as the optimal portfolio size

$ {N}^{\star } $

as the optimal portfolio size

$ N $

maximizing the EU of

$ N $

maximizing the EU of

$ \hat{\boldsymbol{w}} $

.

$ \hat{\boldsymbol{w}} $

.

Kan and Zhou (Reference Kan and Zhou2007) and follow-up papers, such as Tu and Zhou (Reference Tu and Zhou2011), Kan et al. (Reference Kan, Wang and Zhou2021), Lassance et al. (Reference Lassance, Vanderveken and Vrins2024), Lassance, Martín-Utrera, and Simaan (Reference Lassance, Martín-Utrera and Simaan2024), and Yuan and Zhou (Reference Yuan and Zhou2024), evaluate (6) under the IID multivariate normal distributional assumption. Instead, we follow Kan and Lassance (Reference Kan and Lassance2025), who study the EU of various sample portfolios under the IID multivariate elliptical distribution. Like them, we use the stochastic representation of the elliptical distribution in El Karoui (Reference El Karoui2010), (Reference El Karoui2013).

Assumption 2. Asset returns

$ {\boldsymbol{r}}_t $

are IID over time and follow a multivariate elliptical distribution. That is,

$ {\boldsymbol{r}}_t $

are IID over time and follow a multivariate elliptical distribution. That is,

$ {\boldsymbol{r}}_{t_1}\perp {\boldsymbol{r}}_{t_2} $

for

$ {\boldsymbol{r}}_{t_1}\perp {\boldsymbol{r}}_{t_2} $

for

$ {t}_1\ne {t}_2 $

and

$ {t}_1\ne {t}_2 $

and

$ {\boldsymbol{r}}_t\overset{d}{=}{\boldsymbol{\mu}}_M+{\left(\tau {\boldsymbol{\Sigma}}_M\right)}^{\frac{1}{2}}{\mathbf{z}}_M $

, where

$ {\boldsymbol{r}}_t\overset{d}{=}{\boldsymbol{\mu}}_M+{\left(\tau {\boldsymbol{\Sigma}}_M\right)}^{\frac{1}{2}}{\mathbf{z}}_M $

, where

$ {\mathbf{z}}_M\sim \mathcal{N}\left({\mathbf{0}}_M,{\boldsymbol{I}}_M\right) $

,

$ {\mathbf{z}}_M\sim \mathcal{N}\left({\mathbf{0}}_M,{\boldsymbol{I}}_M\right) $

,

$ \tau $

is a positive random variable satisfying

$ \tau $

is a positive random variable satisfying

$ \unicode{x1D53C}\left[\tau \right]=1 $

, and

$ \unicode{x1D53C}\left[\tau \right]=1 $

, and

$ {\mathbf{z}}_M\perp \tau $

. In particular,

$ {\mathbf{z}}_M\perp \tau $

. In particular,

$ {\boldsymbol{\mu}}_M $

and

$ {\boldsymbol{\mu}}_M $

and

$ {\boldsymbol{\Sigma}}_M $

are constant over time.

$ {\boldsymbol{\Sigma}}_M $

are constant over time.

We recover the normal distribution when

$ \tau =1 $

and the

$ \tau =1 $

and the

$ t $

-distribution when

$ t $

-distribution when

$ \tau \sim \left(\nu -2\right)/{\chi}_{\nu}^2 $

, where

$ \tau \sim \left(\nu -2\right)/{\chi}_{\nu}^2 $

, where

$ {\chi}_{\nu}^2 $

is a chi-square distribution with

$ {\chi}_{\nu}^2 $

is a chi-square distribution with

$ \nu >2 $

degrees of freedom. We focus on the elliptical distribution because it is consistent with MV portfolios (Chamberlain (Reference Chamberlain1983), Schuhmacher, Kohrs, and Auer (Reference Schuhmacher, Kohrs and Auer2021)). Specifically, since the multivariate elliptical distribution is closed under linear transformations, all portfolios have the same higher moments and only differ in their mean return and variance. Therefore, for all increasing and concave utility functions, the optimal portfolio under expected utility is MV efficient. We also opt for the elliptical distribution because Kan and Lassance (Reference Kan and Lassance2025) show that accounting for fat tails is crucial in determining optimal portfolio combination rules.

$ \nu >2 $

degrees of freedom. We focus on the elliptical distribution because it is consistent with MV portfolios (Chamberlain (Reference Chamberlain1983), Schuhmacher, Kohrs, and Auer (Reference Schuhmacher, Kohrs and Auer2021)). Specifically, since the multivariate elliptical distribution is closed under linear transformations, all portfolios have the same higher moments and only differ in their mean return and variance. Therefore, for all increasing and concave utility functions, the optimal portfolio under expected utility is MV efficient. We also opt for the elliptical distribution because Kan and Lassance (Reference Kan and Lassance2025) show that accounting for fat tails is crucial in determining optimal portfolio combination rules.

B. Optimal Portfolio Size for Sample Portfolios

The first strategy we consider is the sample counterpart of the MV portfolio in (2), that is,

$$ {\hat{\boldsymbol{w}}}^{\star }=\frac{1}{\gamma }{\hat{\boldsymbol{\Sigma}}}_N^{-1}{\hat{\boldsymbol{\mu}}}_N. $$

$$ {\hat{\boldsymbol{w}}}^{\star }=\frac{1}{\gamma }{\hat{\boldsymbol{\Sigma}}}_N^{-1}{\hat{\boldsymbol{\mu}}}_N. $$

The SMV portfolio is not robust to parameter uncertainty because it is only optimal in sample. Therefore, we also consider the 2F of Kan and Zhou (Reference Kan and Zhou2007) that scales down the SMV portfolio to maximize its EU. This 2F is of the form

$$ \hat{\boldsymbol{w}}\left(\alpha \right)=\alpha {\hat{\boldsymbol{w}}}^{\star }=\frac{\alpha }{\gamma }{\hat{\boldsymbol{\Sigma}}}_N^{-1}{\hat{\boldsymbol{\mu}}}_N, $$

$$ \hat{\boldsymbol{w}}\left(\alpha \right)=\alpha {\hat{\boldsymbol{w}}}^{\star }=\frac{\alpha }{\gamma }{\hat{\boldsymbol{\Sigma}}}_N^{-1}{\hat{\boldsymbol{\mu}}}_N, $$

where

$ \alpha \in \mathrm{\mathbb{R}} $

is the combination coefficient. The SMV in (7) corresponds to

$ \alpha \in \mathrm{\mathbb{R}} $

is the combination coefficient. The SMV in (7) corresponds to

$ {\hat{\boldsymbol{w}}}^{\star }=\overset{}{\hat{\boldsymbol{w}}}(\alpha =1) $

.

$ {\hat{\boldsymbol{w}}}^{\star }=\overset{}{\hat{\boldsymbol{w}}}(\alpha =1) $

.

In the next proposition, we derive the EU of the 2F and, thus, also the SMV portfolio, the optimal combination coefficient

$ {\alpha}^{\star } $

, and which EU it delivers, when asset returns are elliptically distributed. These results then allow us to determine the optimal portfolio size

$ {\alpha}^{\star } $

, and which EU it delivers, when asset returns are elliptically distributed. These results then allow us to determine the optimal portfolio size

$ N $

. This proposition follows, with minor adjustments, from Kan and Lassance ((Reference Kan and Lassance2025), Propositions 7 and 8). In Appendix A.I, we follow the same approach for three-fund rules that extend the 2F by incorporating a third fully invested fund that is either the GMV or the EW portfolio. We refer to these as the GMV-three-fund rule (3FGMV) and the EW-three-fund rule (3FEW), respectively.

$ N $

. This proposition follows, with minor adjustments, from Kan and Lassance ((Reference Kan and Lassance2025), Propositions 7 and 8). In Appendix A.I, we follow the same approach for three-fund rules that extend the 2F by incorporating a third fully invested fund that is either the GMV or the EW portfolio. We refer to these as the GMV-three-fund rule (3FGMV) and the EW-three-fund rule (3FEW), respectively.

Proposition 2. Let

$ T>N+4 $

,

$ T>N+4 $

,

$ \boldsymbol{M}={\boldsymbol{I}}_T-{\mathbf{1}}_T{\mathbf{1}}_T^{\prime }/T $

,

$ \boldsymbol{M}={\boldsymbol{I}}_T-{\mathbf{1}}_T{\mathbf{1}}_T^{\prime }/T $

,

$ {\boldsymbol{Z}}_N $

be a

$ {\boldsymbol{Z}}_N $

be a

$ T\times N $

matrix of independent standard normal variables,

$ T\times N $

matrix of independent standard normal variables,

$ \boldsymbol{\Lambda} $

be a diagonal matrix of

$ \boldsymbol{\Lambda} $

be a diagonal matrix of

$ T $

independent copies of

$ T $

independent copies of

$ {\tau}^{1/2} $

, and

$ {\tau}^{1/2} $

, and

$ \boldsymbol{\Lambda} \perp {\boldsymbol{Z}}_N $

. Then, under Assumption 2, the EU of the 2F

$ \boldsymbol{\Lambda} \perp {\boldsymbol{Z}}_N $

. Then, under Assumption 2, the EU of the 2F

$ \hat{\boldsymbol{w}}\left(\alpha \right) $

in (8) is

$ \hat{\boldsymbol{w}}\left(\alpha \right) $

in (8) is

$$ EU\left(\hat{\boldsymbol{w}}\left(\alpha \right)\right)=\frac{T}{2\gamma \left(T-N-2\right)}\left[\left(2{\alpha \kappa}_{N,1}-\frac{c_N{\alpha}^2{\kappa}_{N,2}T}{T-N-2}\right){\theta}_N^2-\frac{c_N{\alpha}^2{\kappa}_{N,3}N}{T-N-2}\right], $$

$$ EU\left(\hat{\boldsymbol{w}}\left(\alpha \right)\right)=\frac{T}{2\gamma \left(T-N-2\right)}\left[\left(2{\alpha \kappa}_{N,1}-\frac{c_N{\alpha}^2{\kappa}_{N,2}T}{T-N-2}\right){\theta}_N^2-\frac{c_N{\alpha}^2{\kappa}_{N,3}N}{T-N-2}\right], $$

where

$ {\theta}_N^2 $

is the maximum squared Sharpe ratio given in (4),

$ {\theta}_N^2 $

is the maximum squared Sharpe ratio given in (4),

$ {c}_N=\frac{\left(T-2\right)\left(T-N-2\right)}{\left(T-N-1\right)\left(T-N-4\right)} $

, and

$ {c}_N=\frac{\left(T-2\right)\left(T-N-2\right)}{\left(T-N-1\right)\left(T-N-4\right)} $

, and

$ {\kappa}_{N,1} $

,

$ {\kappa}_{N,1} $

,

$ {\kappa}_{N,2} $

, and

$ {\kappa}_{N,2} $

, and

$ {\kappa}_{N,3} $

, which we assume exist, are the functions of only

$ {\kappa}_{N,3} $

, which we assume exist, are the functions of only

$ N $

,

$ N $

,

$ T $

, and the distribution of

$ T $

, and the distribution of

$ \tau $

:

$ \tau $

:

$$ {\kappa}_{N,1}=\frac{T-N-2}{N}\unicode{x1D53C}\left[\mathrm{tr}\left({\left({\boldsymbol{Z}}_N^{\prime}\boldsymbol{\Lambda} \boldsymbol{M}\boldsymbol{\Lambda } {\boldsymbol{Z}}_N\right)}^{-1}\right)\right], $$

$$ {\kappa}_{N,1}=\frac{T-N-2}{N}\unicode{x1D53C}\left[\mathrm{tr}\left({\left({\boldsymbol{Z}}_N^{\prime}\boldsymbol{\Lambda} \boldsymbol{M}\boldsymbol{\Lambda } {\boldsymbol{Z}}_N\right)}^{-1}\right)\right], $$

$$ {\kappa}_{N,2}=\frac{{\left(T-N-2\right)}^2}{c_NN}\unicode{x1D53C}\left[\mathrm{tr}\left({\left({\boldsymbol{Z}}_N^{\prime}\boldsymbol{\Lambda} \boldsymbol{M}\boldsymbol{\Lambda } {\boldsymbol{Z}}_N\right)}^{-2}\right)\right], $$

$$ {\kappa}_{N,2}=\frac{{\left(T-N-2\right)}^2}{c_NN}\unicode{x1D53C}\left[\mathrm{tr}\left({\left({\boldsymbol{Z}}_N^{\prime}\boldsymbol{\Lambda} \boldsymbol{M}\boldsymbol{\Lambda } {\boldsymbol{Z}}_N\right)}^{-2}\right)\right], $$

$$ {\kappa}_{N,3}=\frac{{\left(T-N-2\right)}^2}{c_N NT}\unicode{x1D53C}\left[{\mathbf{1}}_T^{\prime}\boldsymbol{\Lambda} {\boldsymbol{Z}}_N{\left({\boldsymbol{Z}}_N^{\prime}\boldsymbol{\Lambda} \boldsymbol{M}\boldsymbol{\Lambda } {\boldsymbol{Z}}_N\right)}^{-2}{\boldsymbol{Z}}_N^{\prime}\boldsymbol{\Lambda} {\mathbf{1}}_T\right]. $$

$$ {\kappa}_{N,3}=\frac{{\left(T-N-2\right)}^2}{c_N NT}\unicode{x1D53C}\left[{\mathbf{1}}_T^{\prime}\boldsymbol{\Lambda} {\boldsymbol{Z}}_N{\left({\boldsymbol{Z}}_N^{\prime}\boldsymbol{\Lambda} \boldsymbol{M}\boldsymbol{\Lambda } {\boldsymbol{Z}}_N\right)}^{-2}{\boldsymbol{Z}}_N^{\prime}\boldsymbol{\Lambda} {\mathbf{1}}_T\right]. $$

Moreover, the optimal combination coefficient

$ {\alpha}^{\star } $

maximizing (9) and the resulting EU are

$ {\alpha}^{\star } $

maximizing (9) and the resulting EU are

$$ {\alpha}^{\star }=\frac{T-N-2}{c_NT}\left(\frac{\kappa_{N,1}{\theta}_N^2}{\kappa_{N,2}{\theta}_N^2+{\kappa}_{N,3}\frac{N}{T}}\right)\hskip0.66em \mathrm{and}\hskip0.66em EU\left(\hat{\boldsymbol{w}}\left({\alpha}^{\star}\right)\right)=\frac{1}{2\gamma {c}_N}\left(\frac{\kappa_{N,1}^2{\theta}_N^4}{\kappa_{N,2}{\theta}_N^2+{\kappa}_{N,3}\frac{N}{T}}\right). $$

$$ {\alpha}^{\star }=\frac{T-N-2}{c_NT}\left(\frac{\kappa_{N,1}{\theta}_N^2}{\kappa_{N,2}{\theta}_N^2+{\kappa}_{N,3}\frac{N}{T}}\right)\hskip0.66em \mathrm{and}\hskip0.66em EU\left(\hat{\boldsymbol{w}}\left({\alpha}^{\star}\right)\right)=\frac{1}{2\gamma {c}_N}\left(\frac{\kappa_{N,1}^2{\theta}_N^4}{\kappa_{N,2}{\theta}_N^2+{\kappa}_{N,3}\frac{N}{T}}\right). $$

Three comments are in order. First, Proposition 2 is valid for any

$ {\boldsymbol{\Sigma}}_N $

, not only those of the form

$ {\boldsymbol{\Sigma}}_N $

, not only those of the form

$ {\boldsymbol{\Sigma}}_N\left(\rho \right) $

. Second,

$ {\boldsymbol{\Sigma}}_N\left(\rho \right) $

. Second,

$ {\kappa}_{N,1} $

,

$ {\kappa}_{N,1} $

,

$ {\kappa}_{N,2} $

, and

$ {\kappa}_{N,2} $

, and

$ {\kappa}_{N,3} $

do not have a closed-form expression, but can be evaluated via Monte Carlo simulations given the distribution of

$ {\kappa}_{N,3} $

do not have a closed-form expression, but can be evaluated via Monte Carlo simulations given the distribution of

$ \tau $

. We explain how we estimate them in Appendix A.II. Kan and Lassance (Reference Kan and Lassance2025) show that they increase with estimation risk

$ \tau $

. We explain how we estimate them in Appendix A.II. Kan and Lassance (Reference Kan and Lassance2025) show that they increase with estimation risk

$ N/T $

and tail heaviness. Third, under parameter uncertainty in

$ N/T $

and tail heaviness. Third, under parameter uncertainty in

$ {\boldsymbol{\mu}}_N $

and

$ {\boldsymbol{\mu}}_N $

and

$ {\boldsymbol{\Sigma}}_N $

, a larger

$ {\boldsymbol{\Sigma}}_N $

, a larger

$ N $

may not always be favorable. Instead, the

$ N $

may not always be favorable. Instead, the

$ N $

maximizing (9) trades off between improving the population performance (i.e., increasing

$ N $

maximizing (9) trades off between improving the population performance (i.e., increasing

$ {\theta}_N^2 $

) and limiting estimation risk (i.e., decreasing

$ {\theta}_N^2 $

) and limiting estimation risk (i.e., decreasing

$ N/T $

).

$ N/T $

).

Next, we proceed as in Section II and relate the EU with

$ N $

more explicitly by assuming that the covariance matrix

$ N $

more explicitly by assuming that the covariance matrix

$ {\boldsymbol{\Sigma}}_N $

complies with Assumption 1 (i.e.,

$ {\boldsymbol{\Sigma}}_N $

complies with Assumption 1 (i.e.,

$ {\boldsymbol{\Sigma}}_N={\boldsymbol{\Sigma}}_N\left(\rho \right) $

). We obtain this novel result by plugging the expression for

$ {\boldsymbol{\Sigma}}_N={\boldsymbol{\Sigma}}_N\left(\rho \right) $

). We obtain this novel result by plugging the expression for

$ {\theta}_N^2 $

under equicorrelation in (4) into equations (9) and (13).

$ {\theta}_N^2 $

under equicorrelation in (4) into equations (9) and (13).

Corollary 1. Under Assumptions 1 and 2, the EU of the SMV portfolio

$ {\hat{\boldsymbol{w}}}^{\star } $

and the optimal 2F

$ {\hat{\boldsymbol{w}}}^{\star } $

and the optimal 2F

$ \hat{\boldsymbol{w}}\left({\alpha}^{\star}\right) $

are given by

$ \hat{\boldsymbol{w}}\left({\alpha}^{\star}\right) $

are given by

$$ EU\left({\hat{\boldsymbol{w}}}^{\star}\right)=\frac{NT}{2\gamma \left(T-N-2\right)}\left[\frac{\delta_N\left({\overline{\boldsymbol{\theta}}}_N\right)}{1-\rho}\left(2{\kappa}_{N,1}-\frac{c_N{\kappa}_{N,2}T}{T-N-2}\right)-\frac{c_N{\kappa}_{N,3}}{T-N-2}\right] $$

$$ EU\left({\hat{\boldsymbol{w}}}^{\star}\right)=\frac{NT}{2\gamma \left(T-N-2\right)}\left[\frac{\delta_N\left({\overline{\boldsymbol{\theta}}}_N\right)}{1-\rho}\left(2{\kappa}_{N,1}-\frac{c_N{\kappa}_{N,2}T}{T-N-2}\right)-\frac{c_N{\kappa}_{N,3}}{T-N-2}\right] $$

$$ =: E{U}_{smv}\left(N,T,\rho, \tau, {\bar{\theta}}_N\right),\hskip0.33em \mathrm{and} $$

$$ =: E{U}_{smv}\left(N,T,\rho, \tau, {\bar{\theta}}_N\right),\hskip0.33em \mathrm{and} $$

$$ EU\left(\hat{\boldsymbol{w}}\left({\alpha}^{\star}\right)\right)=\frac{N}{2\gamma {c}_N\left(1-\rho \right)}\times \frac{\kappa_{N,1}^2{\delta}_N{\left({\overline{\boldsymbol{\theta}}}_N\right)}^2}{\kappa_{N,2}{\delta}_N\left({\overline{\boldsymbol{\theta}}}_N\right)+{\kappa}_{N,3}\frac{1-\rho }{T}}=: {EU}_{2f}\left(N,T,\rho, \tau, {\overline{\boldsymbol{\theta}}}_N\right). $$

$$ EU\left(\hat{\boldsymbol{w}}\left({\alpha}^{\star}\right)\right)=\frac{N}{2\gamma {c}_N\left(1-\rho \right)}\times \frac{\kappa_{N,1}^2{\delta}_N{\left({\overline{\boldsymbol{\theta}}}_N\right)}^2}{\kappa_{N,2}{\delta}_N\left({\overline{\boldsymbol{\theta}}}_N\right)+{\kappa}_{N,3}\frac{1-\rho }{T}}=: {EU}_{2f}\left(N,T,\rho, \tau, {\overline{\boldsymbol{\theta}}}_N\right). $$

$ {EU}_{smv} $

and

$ {EU}_{smv} $

and

$ {EU}_{2f} $

depend on several parameters.Footnote 9 First, the sample size

$ {EU}_{2f} $

depend on several parameters.Footnote 9 First, the sample size

$ T $

, directly but also via

$ T $

, directly but also via

$ {c}_N $

and

$ {c}_N $

and

$ \left({\kappa}_{N,1},{\kappa}_{N,2},{\kappa}_{N,3}\right) $

. Second, the portfolio size

$ \left({\kappa}_{N,1},{\kappa}_{N,2},{\kappa}_{N,3}\right) $

. Second, the portfolio size

$ N $

, directly but also via

$ N $

, directly but also via

$ {c}_N $

, the function

$ {c}_N $

, the function

$ {\delta}_N $

, and

$ {\delta}_N $

, and

$ \left({\kappa}_{N,1},{\kappa}_{N,2},{\kappa}_{N,3}\right) $

. Third, which

$ \left({\kappa}_{N,1},{\kappa}_{N,2},{\kappa}_{N,3}\right) $

. Third, which

$ N $

assets are selected via

$ N $

assets are selected via

$ {\overline{\boldsymbol{\theta}}}_N=\left({\overline{\theta}}_{N,1},{\overline{\theta}}_{N,2}\right) $

.

$ {\overline{\boldsymbol{\theta}}}_N=\left({\overline{\theta}}_{N,1},{\overline{\theta}}_{N,2}\right) $

.

Now, to maximize

$ {EU}_{smv}\left(N,T,\rho, \tau, {\overline{\boldsymbol{\theta}}}_N\right) $

or

$ {EU}_{smv}\left(N,T,\rho, \tau, {\overline{\boldsymbol{\theta}}}_N\right) $

or

$ {EU}_{2f}\left(N,T,\rho, \tau, {\overline{\boldsymbol{\theta}}}_N\right) $

with respect to

$ {EU}_{2f}\left(N,T,\rho, \tau, {\overline{\boldsymbol{\theta}}}_N\right) $

with respect to

$ N $

, one would also need to optimize the selection of assets because

$ N $

, one would also need to optimize the selection of assets because

$ {\overline{\boldsymbol{\theta}}}_N $

depends on

$ {\overline{\boldsymbol{\theta}}}_N $

depends on

$ N $

via the chosen subset of assets. This is a difficult optimization problem because the number of possible subsets of

$ N $

via the chosen subset of assets. This is a difficult optimization problem because the number of possible subsets of

$ N $

assets with

$ N $

assets with

$ N $

going from 1 to

$ N $

going from 1 to

$ M $

grows very quickly with

$ M $

grows very quickly with

$ M $

.Footnote 10 Moreover, this would introduce potentially severe estimation risk and time instability in the selection of assets, which is undesirable. This is why, to disentangle the determination of the optimal

$ M $

.Footnote 10 Moreover, this would introduce potentially severe estimation risk and time instability in the selection of assets, which is undesirable. This is why, to disentangle the determination of the optimal

$ N $

from the asset selection, we replace

$ N $

from the asset selection, we replace

$ {\overline{\boldsymbol{\theta}}}_N $

by its counterpart for the whole investment universe (i.e.,

$ {\overline{\boldsymbol{\theta}}}_N $

by its counterpart for the whole investment universe (i.e.,

$ {\overline{\boldsymbol{\theta}}}_M $

). This approximation may not be accurate when

$ {\overline{\boldsymbol{\theta}}}_M $

). This approximation may not be accurate when

$ N $

is small relative to

$ N $

is small relative to

$ M $

.Footnote 11 In this case, however, the estimated

$ M $

.Footnote 11 In this case, however, the estimated

$ {\overline{\boldsymbol{\theta}}}_N $

will be particularly noisy, and thus estimating it from

$ {\overline{\boldsymbol{\theta}}}_N $

will be particularly noisy, and thus estimating it from

$ {\overline{\boldsymbol{\theta}}}_M $

can help too. All in all, the way we determine the optimal portfolio size

$ {\overline{\boldsymbol{\theta}}}_M $

can help too. All in all, the way we determine the optimal portfolio size

$ N $

for the SMV portfolio and the optimal 2F becomesFootnote 12

$ N $

for the SMV portfolio and the optimal 2F becomesFootnote 12

$$ {N}_{smv}^{\star }=\underset{N\in \left\{1,\dots, \min \left(M,T-5\right)\right\}}{\arg \max }{EU}_{smv}\left(N,T,\rho, \tau, {\overline{\boldsymbol{\theta}}}_M\right),\mathrm{and} $$

$$ {N}_{smv}^{\star }=\underset{N\in \left\{1,\dots, \min \left(M,T-5\right)\right\}}{\arg \max }{EU}_{smv}\left(N,T,\rho, \tau, {\overline{\boldsymbol{\theta}}}_M\right),\mathrm{and} $$

$$ {N}_{2f}^{\star }=\underset{N\in \left\{1,\dots, \min \left(M,T-5\right)\right\}}{\arg \max }{EU}_{2f}\left(N,T,\rho, \tau, {\overline{\boldsymbol{\theta}}}_M\right). $$

$$ {N}_{2f}^{\star }=\underset{N\in \left\{1,\dots, \min \left(M,T-5\right)\right\}}{\arg \max }{EU}_{2f}\left(N,T,\rho, \tau, {\overline{\boldsymbol{\theta}}}_M\right). $$

We now illustrate

$ {N}_{smv}^{\star } $

and

$ {N}_{smv}^{\star } $

and

$ {N}_{2f}^{\star } $

. Using the full sample of the 96S-BM data set introduced in Section II, we obtain

$ {N}_{2f}^{\star } $

. Using the full sample of the 96S-BM data set introduced in Section II, we obtain

$ {\hat{\boldsymbol{\mu}}}_{96} $

and

$ {\hat{\boldsymbol{\mu}}}_{96} $

and

$ {\hat{\boldsymbol{\Sigma}}}_{96} $

using (5). Then, we set the population mean

$ {\hat{\boldsymbol{\Sigma}}}_{96} $

using (5). Then, we set the population mean

$ {\mu}_M={\hat{\mu}}_{96} $

and the population covariance matrix

$ {\mu}_M={\hat{\mu}}_{96} $

and the population covariance matrix

$ {\boldsymbol{\Sigma}}_M={\hat{\boldsymbol{\Sigma}}}_{96}\left(\rho \right)={\hat{\boldsymbol{D}}}_{96}{\boldsymbol{P}}_{96}\left(\rho \right){\hat{\boldsymbol{D}}}_{96} $

with

$ {\boldsymbol{\Sigma}}_M={\hat{\boldsymbol{\Sigma}}}_{96}\left(\rho \right)={\hat{\boldsymbol{D}}}_{96}{\boldsymbol{P}}_{96}\left(\rho \right){\hat{\boldsymbol{D}}}_{96} $

with

$ {\hat{\boldsymbol{D}}}_{96}=\operatorname{diag}{\left({\hat{\boldsymbol{\Sigma}}}_{96}\right)}^{1/2} $

, which yields

$ {\hat{\boldsymbol{D}}}_{96}=\operatorname{diag}{\left({\hat{\boldsymbol{\Sigma}}}_{96}\right)}^{1/2} $

, which yields

$ {\overline{\boldsymbol{\theta}}}_{96}=\left(\mathrm{0.125,0.0169}\right) $

, and we take

$ {\overline{\boldsymbol{\theta}}}_{96}=\left(\mathrm{0.125,0.0169}\right) $

, and we take

$ \rho \in \left\{\mathrm{0.2,0.5,0.8}\right\} $

. We consider either the normal distribution (i.e.,

$ \rho \in \left\{\mathrm{0.2,0.5,0.8}\right\} $

. We consider either the normal distribution (i.e.,

$ \tau =1 $

and

$ \tau =1 $

and

$ {\kappa}_{N,1}={\kappa}_{N,2}={\kappa}_{N,3}=1 $

) or the

$ {\kappa}_{N,1}={\kappa}_{N,2}={\kappa}_{N,3}=1 $

) or the

$ t $

-distribution (i.e.,

$ t $

-distribution (i.e.,

$ \tau \sim \left(\nu -2\right)/{\chi}_{\nu}^2 $

, with

$ \tau \sim \left(\nu -2\right)/{\chi}_{\nu}^2 $

, with

$ \nu =6) $

. Figure 2 depicts

$ \nu =6) $

. Figure 2 depicts

$ {N}_{smv}^{\star } $

and

$ {N}_{smv}^{\star } $

and

$ {N}_{2f}^{\star } $

as a function of

$ {N}_{2f}^{\star } $

as a function of

$ T $

. We make several observations. First,

$ T $

. We make several observations. First,

$ {N}_{smv}^{\star } $

and

$ {N}_{smv}^{\star } $

and

$ {N}_{2f}^{\star } $

increase with

$ {N}_{2f}^{\star } $

increase with

$ T $

because, as

$ T $

because, as

$ T $

increases, the estimated portfolios become better estimates of the true MV portfolio for which the optimal

$ T $

increases, the estimated portfolios become better estimates of the true MV portfolio for which the optimal

$ N=M $

.

$ N=M $

.

Figure 2 depicts the optimal portfolio size for the SMV portfolio,

$ {N}_{smv}^{\star } $

in (17) (Graph A), and for the optimal 2F,

$ {N}_{smv}^{\star } $

in (17) (Graph A), and for the optimal 2F,

$ {N}_{2f}^{\star } $

in (18) (Graph B), as a function of the sample size

$ {N}_{2f}^{\star } $

in (18) (Graph B), as a function of the sample size

$ T $

. Each line represents a different choice of the correlation,

$ T $

. Each line represents a different choice of the correlation,

$ \rho =\left\{\mathrm{0.2,0.5,0.8}\right\} $

, and the degrees of freedom of the

$ \rho =\left\{\mathrm{0.2,0.5,0.8}\right\} $

, and the degrees of freedom of the

$ t $

-distribution,

$ t $

-distribution,

$ \nu =\left\{6,\infty \right\} $

. We calibrate

$ \nu =\left\{6,\infty \right\} $

. We calibrate

$ {\overline{\boldsymbol{\theta}}}_M=\left(\mathrm{0.125,0.0169}\right) $

to a data set of

$ {\overline{\boldsymbol{\theta}}}_M=\left(\mathrm{0.125,0.0169}\right) $

to a data set of

$ M=96 $

portfolios sorted on size and book-to-market spanning July 1963 to August 2023.

$ M=96 $

portfolios sorted on size and book-to-market spanning July 1963 to August 2023.

Second,

$ {N}_{smv}^{\star } $

is very small compared with

$ {N}_{smv}^{\star } $

is very small compared with

$ T $

and

$ T $

and

$ M $

. For instance, with

$ M $

. For instance, with

$ T=240 $

and

$ T=240 $

and

$ \rho =0.5 $

,

$ \rho =0.5 $

,

$ {N}_{smv}^{\star }=3 $

both for the normal and

$ {N}_{smv}^{\star }=3 $

both for the normal and

$ t $

-distributions. For a larger

$ t $

-distributions. For a larger

$ \rho =0.8 $

,

$ \rho =0.8 $

,

$ {N}_{smv}^{\star } $

gets larger but is still small. For example, when

$ {N}_{smv}^{\star } $

gets larger but is still small. For example, when

$ \rho =0.8 $

and

$ \rho =0.8 $

and

$ T=120 $

, 180, and 240, we have

$ T=120 $

, 180, and 240, we have

$ {N}_{smv}^{\star }=1 $

,

$ {N}_{smv}^{\star }=1 $

,

$ 3 $

, and 10 for the normal distribution, and

$ 3 $

, and 10 for the normal distribution, and

$ {N}_{smv}^{\star }=1 $

,

$ {N}_{smv}^{\star }=1 $

,

$ 2 $

, and 7 for the

$ 2 $

, and 7 for the

$ t $

-distribution, respectively.

$ t $

-distribution, respectively.

Third,

$ {N}_{smv}^{\star } $

and

$ {N}_{smv}^{\star } $

and

$ {N}_{2f}^{\star } $

tend to increase with

$ {N}_{2f}^{\star } $

tend to increase with

$ \rho $

. This is because, as we show in Section OA.2 of the Supplementary Material, the maximum utility without parameter uncertainty,

$ \rho $

. This is because, as we show in Section OA.2 of the Supplementary Material, the maximum utility without parameter uncertainty,

$ U\left({\boldsymbol{w}}^{\star}\right) $

, is a convex function of

$ U\left({\boldsymbol{w}}^{\star}\right) $

, is a convex function of

$ \rho $

and, thus, is increasing in

$ \rho $

and, thus, is increasing in

$ \rho $

for

$ \rho $

for

$ \rho $

large enough. Therefore, given that

$ \rho $

large enough. Therefore, given that

$ U\left({\boldsymbol{w}}^{\star}\right) $

is an increasing function of

$ U\left({\boldsymbol{w}}^{\star}\right) $

is an increasing function of

$ N $

, a larger

$ N $

, a larger

$ \rho $

tends to increase the optimal

$ \rho $

tends to increase the optimal

$ N $

.

$ N $

.

Fourth,

$ {N}_{2f}^{\star } $

is higher than

$ {N}_{2f}^{\star } $

is higher than

$ {N}_{smv}^{\star } $

, below

$ {N}_{smv}^{\star } $

, below

$ T/2 $

, equal to

$ T/2 $

, equal to

$ M $

if

$ M $

if

$ T/2 $

is enough above

$ T/2 $

is enough above

$ M $

, and gets closer to

$ M $

, and gets closer to

$ T/2 $

as

$ T/2 $

as

$ \rho $

increases. These results can be explained based on (16) and (18). Specifically, we can show that in the normal case, that is,

$ \rho $

increases. These results can be explained based on (16) and (18). Specifically, we can show that in the normal case, that is,

$ {\kappa}_{N,1}={\kappa}_{N,2}={\kappa}_{N,3}=1 $

,

$ {\kappa}_{N,1}={\kappa}_{N,2}={\kappa}_{N,3}=1 $

,

$ {N}_{2f}^{\star } $

is below

$ {N}_{2f}^{\star } $

is below

$ T/2 $

(and equal to

$ T/2 $

(and equal to

$ M $

if

$ M $

if

$ M $

is sufficiently below

$ M $

is sufficiently below

$ T/2 $

), and close to

$ T/2 $

), and close to

$ T/2 $

when

$ T/2 $

when

$ \rho $

is close to 0 or 1. To see this, consider the

$ \rho $

is close to 0 or 1. To see this, consider the

$ N $

maximizing the first term of

$ N $

maximizing the first term of

$ {EU}_{2f} $

(i.e.,

$ {EU}_{2f} $

(i.e.,

$ N/{c}_N $

). We have

$ N/{c}_N $

). We have

$$ \frac{N}{c_N}=\frac{N\left(T-N-1\right)\left(T-N-4\right)}{\left(T-2\right)\left(T-N-2\right)}\approx \frac{N\left(T-N-4\right)}{\left(T-2\right)}, $$

$$ \frac{N}{c_N}=\frac{N\left(T-N-1\right)\left(T-N-4\right)}{\left(T-2\right)\left(T-N-2\right)}\approx \frac{N\left(T-N-4\right)}{\left(T-2\right)}, $$

and the latter is maximized by

$$ \underset{N\in \left\{1,\dots, \min \left(M,T-5\right)\right\}}{\arg \max}\frac{N\left(T-N-4\right)}{\left(T-2\right)}=\min \left(\left[T/2-2\right],M\right). $$

$$ \underset{N\in \left\{1,\dots, \min \left(M,T-5\right)\right\}}{\arg \max}\frac{N\left(T-N-4\right)}{\left(T-2\right)}=\min \left(\left[T/2-2\right],M\right). $$

Moreover, when

$ {\kappa}_{N,1}={\kappa}_{N,2}={\kappa}_{N,3}=1 $

, the second term of

$ {\kappa}_{N,1}={\kappa}_{N,2}={\kappa}_{N,3}=1 $

, the second term of

$ {EU}_{2f} $

in (16) decreases with

$ {EU}_{2f} $

in (16) decreases with

$ N $

and is maximized by

$ N $

and is maximized by

$ N=1 $

, which moves

$ N=1 $

, which moves

$ {N}_{2f}^{\star } $

below (20). However, the sensitivity of this second term to

$ {N}_{2f}^{\star } $

below (20). However, the sensitivity of this second term to

$ N $

depends on how sensitive

$ N $

depends on how sensitive

$ N\rho /\left(1-\rho + N\rho \right) $

is to

$ N\rho /\left(1-\rho + N\rho \right) $

is to

$ N $

, and it is less so as

$ N $

, and it is less so as

$ \rho $

approaches 0 or 1. In equity data where

$ \rho $

approaches 0 or 1. In equity data where

$ \rho $

is typically large, we thus expect

$ \rho $

is typically large, we thus expect

$ {N}_{2f}^{\star } $

to stay close to (20). Finally, in the elliptical case,

$ {N}_{2f}^{\star } $

to stay close to (20). Finally, in the elliptical case,

$ {\kappa}_{N,1} $

,

$ {\kappa}_{N,1} $

,

$ {\kappa}_{N,2} $

, and

$ {\kappa}_{N,2} $

, and

$ {\kappa}_{N,3} $

also depend on

$ {\kappa}_{N,3} $

also depend on

$ N $

, but Figure 2 and later simulations suggest that

$ N $

, but Figure 2 and later simulations suggest that

$ {N}_{2f}^{\star } $

still remains close to that under normality.

$ {N}_{2f}^{\star } $

still remains close to that under normality.

Finally, fat tails positively impact

$ {N}_{2f}^{\star } $

, whereas we observe the opposite for

$ {N}_{2f}^{\star } $

, whereas we observe the opposite for

$ {N}_{smv}^{\star } $

. This can be explained because the 2F optimally scales down the SMV portfolio according to tail heaviness via

$ {N}_{smv}^{\star } $

. This can be explained because the 2F optimally scales down the SMV portfolio according to tail heaviness via

$ {\kappa}_{N,1} $

,

$ {\kappa}_{N,1} $

,

$ {\kappa}_{N,2} $

, and

$ {\kappa}_{N,2} $

, and

$ {\kappa}_{N,3} $

. Therefore, as shown by Kan and Lassance ((Reference Kan and Lassance2025), Proposition 5), the 2F often performs better when asset returns are elliptically instead of normally distributed, and thus we find a larger

$ {\kappa}_{N,3} $

. Therefore, as shown by Kan and Lassance ((Reference Kan and Lassance2025), Proposition 5), the 2F often performs better when asset returns are elliptically instead of normally distributed, and thus we find a larger

$ {N}_{2f}^{\star } $

under elliptical returns.

$ {N}_{2f}^{\star } $

under elliptical returns.

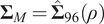

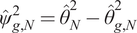

IV. Simulation Analysis

In Section IV.A, we study the estimated optimal

$ N $

for the SMV portfolio and two-fund and three-fund rules. In Section IV.B, we test whether the EU is close to optimal under the estimated optimal

$ N $

for the SMV portfolio and two-fund and three-fund rules. In Section IV.B, we test whether the EU is close to optimal under the estimated optimal

$ N $

and when Assumption 1 (i.e., equicorrelation) is not satisfied. In Section IV.C, we analyze the effect of

$ N $

and when Assumption 1 (i.e., equicorrelation) is not satisfied. In Section IV.C, we analyze the effect of

$ N $

on the EU delivered by alternative benchmark portfolio strategies.

$ N $

on the EU delivered by alternative benchmark portfolio strategies.

To run this analysis, we draw monthly excess returns from a

$ t $

-distribution (i.e.,

$ t $

-distribution (i.e.,

$ \tau \sim \left(\nu -2\right)/{\chi}_{\nu}^2 $

), with

$ \tau \sim \left(\nu -2\right)/{\chi}_{\nu}^2 $

), with

$ \nu \in \left\{6,\infty \right\} $

. As in Section III.B, we calibrate the mean and covariance matrix to the full sample of 96S-BM data set introduced in Section II. Specifically, we set

$ \nu \in \left\{6,\infty \right\} $

. As in Section III.B, we calibrate the mean and covariance matrix to the full sample of 96S-BM data set introduced in Section II. Specifically, we set

$ {\boldsymbol{\mu}}_M={\hat{\boldsymbol{\mu}}}_{96} $

and consider

$ {\boldsymbol{\mu}}_M={\hat{\boldsymbol{\mu}}}_{96} $

and consider

$ {\boldsymbol{\Sigma}}_M\in \left\{{\hat{\boldsymbol{\Sigma}}}_{96},{\hat{\boldsymbol{\Sigma}}}_{96}\left(\overline{\rho}\right)\right\} $

, where

$ {\boldsymbol{\Sigma}}_M\in \left\{{\hat{\boldsymbol{\Sigma}}}_{96},{\hat{\boldsymbol{\Sigma}}}_{96}\left(\overline{\rho}\right)\right\} $

, where

$ \overline{\rho}=0.74 $

is the average of the correlations in

$ \overline{\rho}=0.74 $

is the average of the correlations in

$ {\hat{\boldsymbol{\Sigma}}}_{96} $

. We also consider varying

$ {\hat{\boldsymbol{\Sigma}}}_{96} $

. We also consider varying

$ \rho $

. Setting

$ \rho $

. Setting

$ {\boldsymbol{\Sigma}}_M={\hat{\boldsymbol{\Sigma}}}_{96}\left(\overline{\rho}\right) $

allows us to compare the estimated optimal values of

$ {\boldsymbol{\Sigma}}_M={\hat{\boldsymbol{\Sigma}}}_{96}\left(\overline{\rho}\right) $

allows us to compare the estimated optimal values of

$ N $

with the oracle optimal one that, for the SMV portfolio and the two-fund and three-fund rules, is known theoretically under Assumption 1 (i.e., when

$ N $

with the oracle optimal one that, for the SMV portfolio and the two-fund and three-fund rules, is known theoretically under Assumption 1 (i.e., when

$ {\boldsymbol{\Sigma}}_M $

is of the form

$ {\boldsymbol{\Sigma}}_M $

is of the form

$ {\boldsymbol{\Sigma}}_M\left(\rho \right) $

).

$ {\boldsymbol{\Sigma}}_M\left(\rho \right) $

).

Throughout this simulation analysis, the EU gains from reducing portfolio size originate from the benefits of a reduction in parameter dimensionality on out-of-sample performance. In-sample, with

$ {\boldsymbol{\mu}}_M $

and

$ {\boldsymbol{\mu}}_M $

and

$ {\boldsymbol{\Sigma}}_M $

being known, it is optimal to have

$ {\boldsymbol{\Sigma}}_M $

being known, it is optimal to have

$ N=M $

.

$ N=M $

.

A. Estimated Optimal Portfolio Size

We now analyze the estimated optimal portfolio size for the SMV portfolio

$ \left({\hat{N}}_{smv}^{\star}\right) $

, the 2F

$ \left({\hat{N}}_{smv}^{\star}\right) $

, the 2F

$ \left({\hat{N}}_{2f}^{\star}\right) $

, the 3FGMV

$ \left({\hat{N}}_{2f}^{\star}\right) $

, the 3FGMV

$ \left({\hat{N}}_{3f,g}^{\star}\right) $

, and the 3FEW

$ \left({\hat{N}}_{3f,g}^{\star}\right) $

, and the 3FEW