I. Introduction

Corporate diversification, with its potential impact on firm value and risk, has attracted the interest of academics and management practitioners alike.Footnote 1 A key strand of the corporate diversification literature investigates its impact on debt capacity. In particular, Galai and Masulis (Reference Galai and Masulis1976) and Lewellen (Reference Lewellen1971) claim that diversified firms can exploit the coinsurance effect across their divisions to increase their leverage, but empirical evidence in this respect is mixed (Berger and Ofek (Reference Berger and Ofek1995), Mansi and Reeb (Reference Mansi and Reeb2002)). However, leverage is only one of the channels through which corporate diversification might affect firm value via the coinsurance effect.

In this article, we are the first to investigate both theoretically and empirically the interplay between corporate diversification and debt maturity choices and their effect on firm value. Recent contributions have studied the role of debt maturity choices for investment incentives, rollover risk, and the debt overhang problem (see, e.g., Myers (Reference Myers1977), Diamond (Reference Diamond1991), Barclay and Smith (Reference Barclay and Smith1995), Cheng and Milbradt (Reference Cheng and Milbradt2012), Chen, Xu, and Yang (Reference Chen, Xu and Yang2012), Diamond and He (Reference Diamond and He2014), Gopalan, Song, and Yerramilli (Reference Gopalan, Song and Yerramilli2014), and Dangl and Zechner (2021)).Footnote 2 However, the literature has, insofar, neglected the role of corporate diversification in shaping debt maturity choices. We argue that corporate diversification allows companies to have a longer average debt maturity than stand-alone firms by alleviating the debt-overhang problem.

Our theoretical contribution consists of a simple 3-period discrete-time model and a continuous-time model based on a basket option pricing approach. The 3-period model extends Diamond and He’s (Reference Diamond and He2014) numerical example of how debt maturity can affect debt overhang to a multi-division setting.Footnote 3 Although corporate diversification reduces the conditional variance of the multi-division firm’s future payoffs (i.e., the coinsurance effect), it does not affect the value of an all-equity firm because it does not alter the expected payoffs, consistent with Mansi and Reeb’s (Reference Mansi and Reeb2002) findings. When we introduce the possibility for firms to raise debt, the coinsurance effect allows a multi-division firm to have a lower book value of debt than a comparable stand-alone firm. The lower book leverage reduces the default risk of the multi-division firm and, therefore, mitigates debt overhang in both the short and long terms. Once we allow for higher noninterest debt expenses for short-term debt (see, e.g., Acharya, Gale, and Yorulmazer (Reference Acharya, Gale and Yorulmazer2011)),Footnote 4 our model predicts that multi-division (stand-alone) firms are more likely to issue long-term (short-term) debt.

The idea that short-term debt improves investment incentives (Myers (Reference Myers1977)) originates from the Black–Scholes–Merton model, in which equity is analogous to a European call option with a strike price equal to the face value of the debt due at maturity (Diamond and He (Reference Diamond and He2014)). To further study the corporate diversification’s effect on debt maturity, we generalize our 3-period model using a Black–Scholes–Merton approach, considering the multi-division firm’s equity value as a European basket call option. We use Ju’s (Reference Ju2002) approach as an efficient closed-form approximation of the basket call option to price the equity value of the multi-division firm. This model allows us to conduct more flexible counterfactual analyses. The basket-option framework leads to the same conclusion as the 3-period model: the optimal debt maturity (i.e., the one that maximizes investment incentives) is shorter for stand-alone firms than for multi-division firms. This theoretical prediction, for which we find strong empirical support, has important implications for the diversification discount/premium measure: the presence of the coinsurance effect might lead multi-division firms to have longer debt maturity compared with stand-alone firms.Footnote 5 Longer-term debt makes the market value of equity of multi-division firms higher than that of comparable stand-alone firms. Conventional measures of excess value could be misleading because they neglect the endogenous nature of debt maturity preferences. Our model predicts that the excess value measure introduced by Berger and Ofek (Reference Berger and Ofek1995) and Mansi and Reeb (Reference Mansi and Reeb2002), which is not adjusted for debt maturity, increases with debt maturity.Footnote 6

We test the empirical predictions of our models and their assumptions on a sample of stand-alone and multi-division firms. Our main findings are as follows: First, our regression results confirm a positive association between corporate diversification and debt maturity. Multi-division firms have a debt maturity at least 1 year longer than stand-alone firms, with a median stand-alone firm increasing debt maturity by 25% through diversification. Compared with other determinants of debt maturity, corporate diversification has a larger incremental explanatory power than the debt-to-equity ratio, net income, and capital expenditures. The only variable with a larger incremental explanatory power than corporate diversification is size (market value of equity), but the positive effect of corporate diversification on debt maturity remains positive across three size-based subsamples. Thus, the positive impact of corporate diversification on debt maturity is distinct from the effect of firm size. However, the magnitude of the impact becomes smaller and less statistically significant for larger firms, plausibly because smaller firms have better growth options.

Second, we provide evidence that the positive effect of corporate diversification on debt maturity is stronger for firms with debt overhang. This finding is important because it supports the view that corporate diversification leads to longer debt maturities by mitigating the debt overhang problem, which is consistent with our model. These results are robust to using different proxies for debt overhang, including the one introduced by Alanis et al. (Reference Alanis, Chava and Kumar2018), which uses a model introduced by Chava and Jarrow (Reference Chava and Jarrow2004) to estimate the probability of default.

Third, we find a positive and statistically significant relationship between the excess value (Berger and Ofek (Reference Berger and Ofek1995), Mansi and Reeb (Reference Mansi and Reeb2002)) and debt maturity, consistent with the predictions of our basket-option model: a 1-standard-deviation increase in the natural logarithm of debt maturity leads to a 1.6% increase in the excess value.Footnote 7

In our empirical exercise, we also provide evidence supporting our models’ assumptions. Specifically, we find that a 1-standard-deviation decrease in the logarithm of debt maturity results in a 0.23-standard-deviation increase in the cost of debt, equivalent to a 4% increase. This finding supports the assumption of a negative correlation between debt maturity and the cost of debt in our theoretical models. Moreover, we provide evidence of an economically negligible difference in the leverage of the stand-alone and multi-division firms (only 40 BPS or 0.4%). This result is consistent with the setup of our basket-option model, where we require that the face value of debt for the stand-alone and multi-division firms be the same.

The central contribution of our article lies in bridging a gap between two strands of literature: one on the determinants of debt maturity and the other on corporate diversification. Debt maturity affects shareholders’ investment incentives (Myers (Reference Myers1977)), and short-term debt mitigates debt overhang. Diamond and He’s (Reference Diamond and He2014) theory offers further nuance to our understanding of the relationship between debt maturity and debt overhang. Our article contributes to the debt maturity literature by offering an analytical framework quantifying corporate diversification’s effect on lengthening debt maturity for multi-division firms due to reduced debt overhang.

From a purely theoretical perspective, there could be both costs and benefits associated with corporate diversification. From an empirical perspective, there is still a debate as to whether corporate diversification has any impact on firm value (e.g., Lang and Stulz (Reference Lang and Stulz1994), Berger and Ofek (Reference Berger and Ofek1995), Lamont and Polk (Reference Lamont and Polk2002), Rajan, Servaes, and Zingales (Reference Rajan, Servaes and Zingales2000), Denis, Denis, and Sarin (Reference Denis, Denis and Sarin1997), Levinthal and Wu (Reference Levinthal and Wu2010), and Hund et al. (Reference Hund, Monk and Tice2024)). The diversification discount could be related to endogeneity due to self-selection bias (Campa and Kedia (Reference Campa and Kedia2002), Lamont and Polk (Reference Lamont and Polk2002), Chevalier (Reference Chevalier2004), Villalonga (Reference Villalonga2004b), and Xiao and Xu (Reference Xiao and Xu2019)) or measurement error (Whited (Reference Whited2001)). After adjusting for these factors, the diversification discount tends to disappear. Moreover, focusing on establishment-level diversification, instead of business segments provided by Compustat, Villalonga (Reference Villalonga2004a) finds evidence of a diversification premium.

While most of the literature on corporate diversification tends to be empirical, recent contributions develop theoretical models allowing for endogeneity of the choice to become a diversified firm. For example, Bakke and Gu (Reference Bakke and Gu2017) focus on the relationship between corporate diversification and cash holdings. They estimate a structural model where the switch from stand-alone to multi-division firms is endogenously determined because diversifying firms tend to be larger and have better growth opportunities. Dai, Giroud, Jiang, and Wang (Reference Dai, Giroud, Jiang and Wang2024) highlight that resource allocation within the firm considers not only divisions’ productivity but also their risk, and firms may opt to spin off productive divisions voluntarily to enhance liquidity. Their results echo the mixed findings from the empirical literature and emphasize the importance of accounting for the endogenous formation of conglomerates. We contribute to this literature by providing insights into a new channel, debt maturity. Our models show that the debt maturity choices are endogenous to divisional structure. When estimating the excess value, such endogeneity cannot be resolved by matching diversified firms with a control sample of stand-alone firms. Our theoretical and empirical results suggest that the conventional excess value measure could be misleading because of the endogenous nature of debt maturity in association with corporate diversification.

II. Three-Period Model

We first study a simple 3-period model extending Diamond and He’s (Reference Diamond and He2014) 3-period numerical example of a stand-alone firm to a multi-division setting. For easy comparison, we model two firms with assets-in-place of identical size: one,

$ S $

, with a single division and the other,

$ S $

, with a single division and the other,

$ M $

, with two divisions. Each of the assets-in-place of

$ M $

, with two divisions. Each of the assets-in-place of

$ M $

,

$ M $

,

$ {F}_m $

, is one-half of the assets-in-place of

$ {F}_m $

, is one-half of the assets-in-place of

$ S $

,

$ S $

,

$ {F}_s $

.

$ {F}_s $

.

$ S $

’s (each of

$ S $

’s (each of

$ M $

’s) assets-in-place will generate three possible cash flows at

$ M $

’s) assets-in-place will generate three possible cash flows at

$ t=2 $

as {24, 12, 0} ({12, 6, 0}), with probability

$ t=2 $

as {24, 12, 0} ({12, 6, 0}), with probability

$ \frac{1}{3} $

of each scenario, conditional on the information at

$ \frac{1}{3} $

of each scenario, conditional on the information at

$ t=0 $

. The same applies to the assets-in-place of the two divisions of

$ t=0 $

. The same applies to the assets-in-place of the two divisions of

$ M $

. The distributions of

$ M $

. The distributions of

$ {F}_m $

’s two assets-in-place cash flows are independent of each other. There are no cash flows in other periods. The discount rate is 0.

$ {F}_m $

’s two assets-in-place cash flows are independent of each other. There are no cash flows in other periods. The discount rate is 0.

For simplicity, we assume firm value maximization, given a firm’s divisional structure (Myers (Reference Myers1977), Damodaran (Reference Damodaran2014), and Diamond and He (Reference Diamond and He2014)).Footnote 8

A. Information Structure and Payoffs

For all three assets-in-place, there are two states: a good state and a bad state. The state of the economy is revealed at

$ t=1 $

. We use notations

$ t=1 $

. We use notations

$ G $

(good) and

$ G $

(good) and

$ B $

(bad) to represent the two states of the assets-in-place for the stand-alone firm (

$ B $

(bad) to represent the two states of the assets-in-place for the stand-alone firm (

$ {F}_s $

). For the multi-division firm, we denote the states for the assets-in-place of the first division (

$ {F}_s $

). For the multi-division firm, we denote the states for the assets-in-place of the first division (

$ {F}_m(1) $

) as

$ {F}_m(1) $

) as

$ G1 $

and

$ G1 $

and

$ B1 $

, and for the assets-in-place of the second division (

$ B1 $

, and for the assets-in-place of the second division (

$ {F}_m(2) $

) as

$ {F}_m(2) $

) as

$ G2 $

and

$ G2 $

and

$ B2 $

. The probability of each state is

$ B2 $

. The probability of each state is

$ \frac{1}{2} $

, and the outcomes are independent across all assets-in-place. For any given asset-in-place, the conditional probabilities of the cash flow at

$ \frac{1}{2} $

, and the outcomes are independent across all assets-in-place. For any given asset-in-place, the conditional probabilities of the cash flow at

$ t=2 $

are as follows: If the state at

$ t=2 $

are as follows: If the state at

$ t=1 $

is good (bad), the probabilities are

$ t=1 $

is good (bad), the probabilities are

$ \frac{1}{2} $

,

$ \frac{1}{2} $

,

$ \frac{1}{3} $

,

$ \frac{1}{3} $

,

$ \frac{1}{6} $

(

$ \frac{1}{6} $

(

$ \frac{1}{6} $

,

$ \frac{1}{6} $

,

$ \frac{1}{3} $

,

$ \frac{1}{3} $

,

$ \frac{1}{2} $

). The conditional distributions of

$ \frac{1}{2} $

). The conditional distributions of

$ {F}_s $

at

$ {F}_s $

at

$ t=2 $

, based on the information from

$ t=2 $

, based on the information from

$ t=0 $

and

$ t=0 $

and

$ t=1 $

, areFootnote 9

$ t=1 $

, areFootnote 9

$$ \underset{t=0}{\underbrace{{\left.{F}_s\right|}_{t=0}=\left\{\begin{array}{cc}24,& \mathrm{with}\hskip0.33em \mathrm{prob}=1/3,\\ {}12,& \mathrm{with}\hskip0.33em \mathrm{prob}=1/3,\\ {}0,& \mathrm{with}\hskip0.33em \mathrm{prob}=1/3,\end{array}\right.}} $$

$$ \underset{t=0}{\underbrace{{\left.{F}_s\right|}_{t=0}=\left\{\begin{array}{cc}24,& \mathrm{with}\hskip0.33em \mathrm{prob}=1/3,\\ {}12,& \mathrm{with}\hskip0.33em \mathrm{prob}=1/3,\\ {}0,& \mathrm{with}\hskip0.33em \mathrm{prob}=1/3,\end{array}\right.}} $$

$$ \underset{t=1}{\underbrace{{\left.{F}_s\right|}_{\operatorname{G},t=1}=\left\{\begin{array}{cc}24,& \mathrm{with}\ \mathrm{prob}=1/2,\\ {}12,& \mathrm{with}\ \mathrm{prob}=1/3,\\ {}0,& \mathrm{with}\ \mathrm{prob}=1/6,\end{array}\right.\hskip0.24em {\left.{F}_s\right|}_{\operatorname{B},t=1}=\left\{\begin{array}{cc}24,& \mathrm{with}\ \mathrm{prob}=1/6,\\ {}12,& \mathrm{with}\ \mathrm{prob}=1/3,\\ {}0,& \mathrm{with}\ \mathrm{prob}=1/2,\end{array}\right.}} $$

$$ \underset{t=1}{\underbrace{{\left.{F}_s\right|}_{\operatorname{G},t=1}=\left\{\begin{array}{cc}24,& \mathrm{with}\ \mathrm{prob}=1/2,\\ {}12,& \mathrm{with}\ \mathrm{prob}=1/3,\\ {}0,& \mathrm{with}\ \mathrm{prob}=1/6,\end{array}\right.\hskip0.24em {\left.{F}_s\right|}_{\operatorname{B},t=1}=\left\{\begin{array}{cc}24,& \mathrm{with}\ \mathrm{prob}=1/6,\\ {}12,& \mathrm{with}\ \mathrm{prob}=1/3,\\ {}0,& \mathrm{with}\ \mathrm{prob}=1/2,\end{array}\right.}} $$

and the conditional expectation of

$ {F}_s $

at

$ {F}_s $

at

$ t=2 $

, given the information from

$ t=2 $

, given the information from

$ t=1 $

, is

$ t=1 $

, is

$$ \unicode{x1D53C}({\left.{F}_s\right|}_{\varPi_s,t=1})=\left\{\begin{array}{cc}16,& \mathrm{with}\hskip0.33em {\Pi}_s=G,\\ {}8,& \mathrm{with}\hskip0.33em {\Pi}_s=B,\end{array}\right. $$

$$ \unicode{x1D53C}({\left.{F}_s\right|}_{\varPi_s,t=1})=\left\{\begin{array}{cc}16,& \mathrm{with}\hskip0.33em {\Pi}_s=G,\\ {}8,& \mathrm{with}\hskip0.33em {\Pi}_s=B,\end{array}\right. $$

where

$ {\Pi}_s $

is the state variable for

$ {\Pi}_s $

is the state variable for

$ {F}_s $

, which can take two realizations,

$ {F}_s $

, which can take two realizations,

$ G $

and

$ G $

and

$ B $

, with equal probability.

$ B $

, with equal probability.

Since

$ {F}_m(1) $

and

$ {F}_m(1) $

and

$ {F}_m(2) $

are independent and

$ {F}_m(2) $

are independent and

$ {F}_m={F}_m(1)+{F}_m(2) $

, we obtain

$ {F}_m={F}_m(1)+{F}_m(2) $

, we obtain

$ {F}_m $

’s conditional distribution by convolving the distributions of

$ {F}_m $

’s conditional distribution by convolving the distributions of

$ {F}_m(1) $

and

$ {F}_m(1) $

and

$ {F}_m(2) $

:

$ {F}_m(2) $

:

$$ \underset{t=0}{\underbrace{{\left.{F}_m\right|}_{t=0}=\left\{\begin{array}{cc}24,& \mathrm{with}\ \mathrm{prob}=1/9,\\ {}18,& \mathrm{with}\ \mathrm{prob}=2/9,\\ {}12,& \mathrm{with}\ \mathrm{prob}=1/3,\\ {}6,& \mathrm{with}\ \mathrm{prob}=2/9,\\ {}0,& \mathrm{with}\ \mathrm{prob}=1/9,\end{array}\right.}}\hskip1.2em \underset{t=1}{\underbrace{{\left.{F}_m\right|}_{G1G2,t=1}=\left\{\begin{array}{cc}24,& \mathrm{with}\ \mathrm{prob}=1/4,\\ {}18,& \mathrm{with}\ \mathrm{prob}=1/3,\\ {}12,& \mathrm{with}\ \mathrm{prob}=5/18,\\ {}6,& \mathrm{with}\ \mathrm{prob}=1/9,\\ {}0,& \mathrm{with}\ \mathrm{prob}=1/36,\end{array}\right.}} $$

$$ \underset{t=0}{\underbrace{{\left.{F}_m\right|}_{t=0}=\left\{\begin{array}{cc}24,& \mathrm{with}\ \mathrm{prob}=1/9,\\ {}18,& \mathrm{with}\ \mathrm{prob}=2/9,\\ {}12,& \mathrm{with}\ \mathrm{prob}=1/3,\\ {}6,& \mathrm{with}\ \mathrm{prob}=2/9,\\ {}0,& \mathrm{with}\ \mathrm{prob}=1/9,\end{array}\right.}}\hskip1.2em \underset{t=1}{\underbrace{{\left.{F}_m\right|}_{G1G2,t=1}=\left\{\begin{array}{cc}24,& \mathrm{with}\ \mathrm{prob}=1/4,\\ {}18,& \mathrm{with}\ \mathrm{prob}=1/3,\\ {}12,& \mathrm{with}\ \mathrm{prob}=5/18,\\ {}6,& \mathrm{with}\ \mathrm{prob}=1/9,\\ {}0,& \mathrm{with}\ \mathrm{prob}=1/36,\end{array}\right.}} $$

$$ \underset{t=1}{\underbrace{{\left.{F}_m\right|}_{B1B2,t=1}=\left\{\begin{array}{cc}24,& \mathrm{with}\ \mathrm{prob}=1/36,\\ {}18,& \mathrm{with}\ \mathrm{prob}=1/9,\\ {}12,& \mathrm{with}\ \mathrm{prob}=5/18,\\ {}6,& \mathrm{with}\ \mathrm{prob}=1/3,\\ {}0,& \mathrm{with}\ \mathrm{prob}=1/4,\end{array}\right.\hskip0.24em {\left.{F}_m\right|}_{G1B2\mathrm{or}B1G2,t=1}=\left\{\begin{array}{cc}24,& \mathrm{with}\ \mathrm{prob}=1/12,\\ {}18,& \mathrm{with}\ \mathrm{prob}=2/9,\\ {}12,& \mathrm{with}\ \mathrm{prob}=7/18,\\ {}6,& \mathrm{with}\ \mathrm{prob}=2/9,\\ {}0,& \mathrm{with}\ \mathrm{prob}=1/12,\end{array}\right.}} $$

$$ \underset{t=1}{\underbrace{{\left.{F}_m\right|}_{B1B2,t=1}=\left\{\begin{array}{cc}24,& \mathrm{with}\ \mathrm{prob}=1/36,\\ {}18,& \mathrm{with}\ \mathrm{prob}=1/9,\\ {}12,& \mathrm{with}\ \mathrm{prob}=5/18,\\ {}6,& \mathrm{with}\ \mathrm{prob}=1/3,\\ {}0,& \mathrm{with}\ \mathrm{prob}=1/4,\end{array}\right.\hskip0.24em {\left.{F}_m\right|}_{G1B2\mathrm{or}B1G2,t=1}=\left\{\begin{array}{cc}24,& \mathrm{with}\ \mathrm{prob}=1/12,\\ {}18,& \mathrm{with}\ \mathrm{prob}=2/9,\\ {}12,& \mathrm{with}\ \mathrm{prob}=7/18,\\ {}6,& \mathrm{with}\ \mathrm{prob}=2/9,\\ {}0,& \mathrm{with}\ \mathrm{prob}=1/12,\end{array}\right.}} $$

the conditional expectation of

$ {F}_m $

at

$ {F}_m $

at

$ t=2 $

, given the information at

$ t=2 $

, given the information at

$ t=1 $

, is

$ t=1 $

, is

$$ \unicode{x1D53C}({\left.{F}_m\right|}_{\varPi_m,t=1})=\left\{\begin{array}{cc}16,& \mathrm{with}\hskip0.33em {\Pi}_m=G1G2,\\ {}12,& \mathrm{with}\hskip0.33em {\Pi}_m=G1B2\hskip0.33em \mathrm{or}\hskip0.33em B1G2,\\ {}8,& \mathrm{with}\hskip0.33em {\Pi}_m=B1B2,\end{array}\right. $$

$$ \unicode{x1D53C}({\left.{F}_m\right|}_{\varPi_m,t=1})=\left\{\begin{array}{cc}16,& \mathrm{with}\hskip0.33em {\Pi}_m=G1G2,\\ {}12,& \mathrm{with}\hskip0.33em {\Pi}_m=G1B2\hskip0.33em \mathrm{or}\hskip0.33em B1G2,\\ {}8,& \mathrm{with}\hskip0.33em {\Pi}_m=B1B2,\end{array}\right. $$

and

$ {F}_m $

’s state variable

$ {F}_m $

’s state variable

$ {\Pi}_m $

has three realizations, and its distribution is given by

$ {\Pi}_m $

has three realizations, and its distribution is given by

$$ {\left.{\varPi}_m\right|}_{t=0}=\left\{\begin{array}{cc}G1G2,& \mathrm{with}\ \mathrm{prob}=1/4,\\ {}G1B2\hskip0.33em \mathrm{or}\hskip0.33em B1G2,& \mathrm{with}\ \mathrm{prob}=1/2,\\ {}B1B2,& \mathrm{with}\ \mathrm{prob}=1/4.\end{array}\right. $$

$$ {\left.{\varPi}_m\right|}_{t=0}=\left\{\begin{array}{cc}G1G2,& \mathrm{with}\ \mathrm{prob}=1/4,\\ {}G1B2\hskip0.33em \mathrm{or}\hskip0.33em B1G2,& \mathrm{with}\ \mathrm{prob}=1/2,\\ {}B1B2,& \mathrm{with}\ \mathrm{prob}=1/4.\end{array}\right. $$

The binomial tree representations of the possible paths of

$ {F}_s $

and

$ {F}_s $

and

$ {F}_m $

in the 2 periods are presented in Figures 1 and 2, respectively. It is worth noting that the firm value is invariant to corporate diversification when the firm is an all-equity firm, as

$ {F}_m $

in the 2 periods are presented in Figures 1 and 2, respectively. It is worth noting that the firm value is invariant to corporate diversification when the firm is an all-equity firm, as

$ \unicode{x1D53C}\left({\left.{F}_s\right|}_{t=0}\right)=\unicode{x1D53C}\left({\left.{F}_m\right|}_{t=0}\right)=12 $

. This is consistent with Mansi and Reeb (Reference Mansi and Reeb2002), in that for all-equity firms, corporate diversification is unrelated to excess total firm value. However, corporate diversification does reduce the conditional standard deviation of future firm value:

$ \unicode{x1D53C}\left({\left.{F}_s\right|}_{t=0}\right)=\unicode{x1D53C}\left({\left.{F}_m\right|}_{t=0}\right)=12 $

. This is consistent with Mansi and Reeb (Reference Mansi and Reeb2002), in that for all-equity firms, corporate diversification is unrelated to excess total firm value. However, corporate diversification does reduce the conditional standard deviation of future firm value:

$ \mathrm{Std}\left({\left.{F}_m\right|}_{t=0}\right)=6.93<9.80=\mathrm{Std}\left({\left.{F}_s\right|}_{t=0}\right) $

. This is consistent with the coinsurance effect of corporate diversification argued by Lewellen (Reference Lewellen1971), Galai and Masulis (Reference Galai and Masulis1976), and Hann et al. (Reference Hann, Ogneva and Ozbas2013).

$ \mathrm{Std}\left({\left.{F}_m\right|}_{t=0}\right)=6.93<9.80=\mathrm{Std}\left({\left.{F}_s\right|}_{t=0}\right) $

. This is consistent with the coinsurance effect of corporate diversification argued by Lewellen (Reference Lewellen1971), Galai and Masulis (Reference Galai and Masulis1976), and Hann et al. (Reference Hann, Ogneva and Ozbas2013).

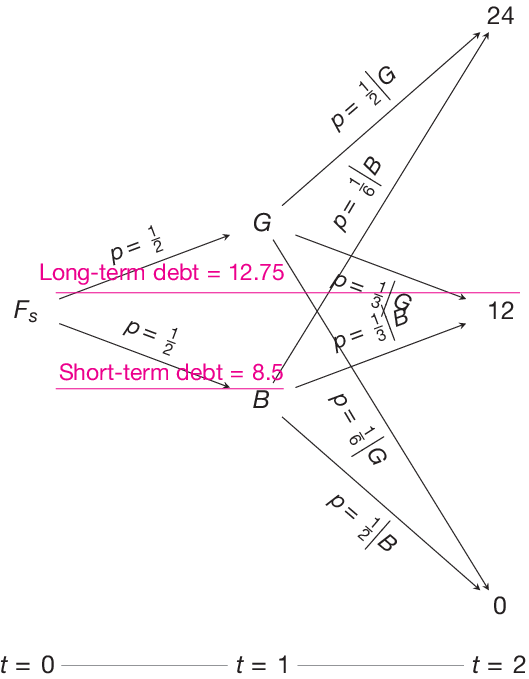

Figure 1 plots all possible values of stand-alone firm

$ S $

’s assets-in-place on

$ S $

’s assets-in-place on

$ t=2 $

and two states

$ t=2 $

and two states

$ \left\{G\hskip0.42em \mathrm{and}\hskip0.42em B\right\} $

on

$ \left\{G\hskip0.42em \mathrm{and}\hskip0.42em B\right\} $

on

$ t=1 $

. The probability of each path is shown along the path. Long-term and short-term face values of debt are indicated in the figure as long and short lines with corresponding legends.

$ t=1 $

. The probability of each path is shown along the path. Long-term and short-term face values of debt are indicated in the figure as long and short lines with corresponding legends.

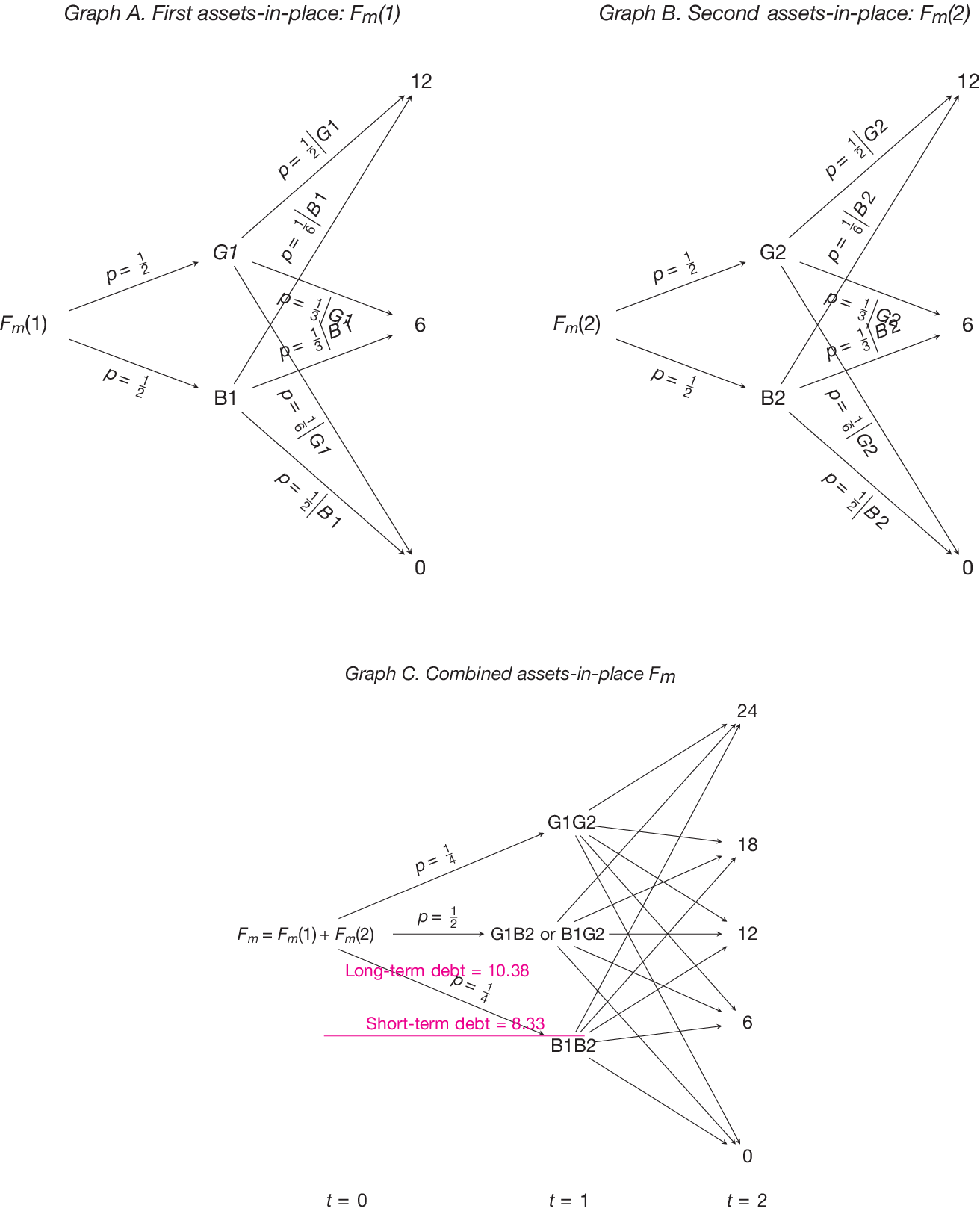

In Figure 2, Graphs A and B plot all possible values of multi-division firm

$ M $

’s two assets-in-place

$ M $

’s two assets-in-place

$ {F}_m(1) $

and

$ {F}_m(1) $

and

$ {F}_m(2) $

, respectively, on

$ {F}_m(2) $

, respectively, on

$ t=2 $

and two states

$ t=2 $

and two states

$ \left\{G\hskip0.42em \mathrm{and}\hskip0.42em B\right\} $

on

$ \left\{G\hskip0.42em \mathrm{and}\hskip0.42em B\right\} $

on

$ t=1 $

. The probability of each path is shown along the path. Graph C plots the same paths for the combined assets-in-place

$ t=1 $

. The probability of each path is shown along the path. Graph C plots the same paths for the combined assets-in-place

$ {F}_m $

for firm

$ {F}_m $

for firm

$ M $

. Long-term and short-term face values of debt are indicated in Graph C as long and short lines with corresponding legends.

$ M $

. Long-term and short-term face values of debt are indicated in Graph C as long and short lines with corresponding legends.

B. Debt Overhang and Investment Incentives

We now introduce debt into the firm value to study the effect of corporate diversification on debt overhang and shareholders’ incentives. We follow Diamond and He (Reference Diamond and He2014) and assume that both

$ S $

and

$ S $

and

$ M $

need to raise

$ M $

need to raise

$ 8.25 $

at

$ 8.25 $

at

$ t=0 $

. The debt can be either long-term (maturing at

$ t=0 $

. The debt can be either long-term (maturing at

$ t=2 $

) or short-term (maturing at

$ t=2 $

) or short-term (maturing at

$ t=1 $

). As shown in Diamond and He (Reference Diamond and He2014), given the payoffs above and the need to raise

$ t=1 $

). As shown in Diamond and He (Reference Diamond and He2014), given the payoffs above and the need to raise

$ 8.25 $

, the short-term and long-term debt’s nominal values are

$ 8.25 $

, the short-term and long-term debt’s nominal values are

$ {L}_s^{\mathrm{ST}}=8.5 $

and

$ {L}_s^{\mathrm{ST}}=8.5 $

and

$ {L}_s^{\mathrm{LT}}=12.75 $

for

$ {L}_s^{\mathrm{LT}}=12.75 $

for

$ S $

. Our model extension to the multi-division firm leads to

$ S $

. Our model extension to the multi-division firm leads to

$ {L}_m^{\mathrm{ST}}=8.33 $

and

$ {L}_m^{\mathrm{ST}}=8.33 $

and

$ {L}_m^{\mathrm{LT}}=10.38 $

for

$ {L}_m^{\mathrm{LT}}=10.38 $

for

$ M $

. Figures 1 and 2 illustrate the relationship between the payoffs and the nominal values of debt for

$ M $

. Figures 1 and 2 illustrate the relationship between the payoffs and the nominal values of debt for

$ S $

and

$ S $

and

$ M $

, respectively. The discrepancy between the nominal debt value of

$ M $

, respectively. The discrepancy between the nominal debt value of

$ S $

and that of

$ S $

and that of

$ M $

arises from the reduction in default risk due to the coinsurance effect.Footnote 10 We assume that there is no cost to raise either short-term or long-term debt.Footnote 11 For simplicity, we focus on an infinitesimal investment that only weakly increases or leaves unchanged the value of each of its debt and equity claims.Footnote 12 Such investment occurs immediately after raising the debt at

$ M $

arises from the reduction in default risk due to the coinsurance effect.Footnote 10 We assume that there is no cost to raise either short-term or long-term debt.Footnote 11 For simplicity, we focus on an infinitesimal investment that only weakly increases or leaves unchanged the value of each of its debt and equity claims.Footnote 12 Such investment occurs immediately after raising the debt at

$ t=0 $

, and results in a marginal increment of the final cash flows at

$ t=0 $

, and results in a marginal increment of the final cash flows at

$ t=2 $

equal to

$ t=2 $

equal to

$ \varepsilon >0 $

. The short-term (

$ \varepsilon >0 $

. The short-term (

$ {O}_i^{\mathrm{ST}} $

) and long-term debt overhang (

$ {O}_i^{\mathrm{ST}} $

) and long-term debt overhang (

$ {O}_i^{\mathrm{LT}} $

) are

$ {O}_i^{\mathrm{LT}} $

) are

$$ {O}_i^{\mathrm{ST}}={\unicode{x1D53C}}_0({\mathbf{1}}_{\{\unicode{x1D53C}({\operatorname{}{F}_i|}_{t=1})<{L}_i^{\mathrm{ST}}\}})\hskip0.33em \mathrm{a}\mathrm{n}\mathrm{d}\hskip0.42em {O}_i^{\mathrm{LT}}={\unicode{x1D53C}}_0({\mathbf{1}}_{\{{F}_i\ \mathrm{a}\mathrm{t}\ t=2<{L}_i^{\mathrm{LT}}\}}),\hskip0.6em \mathrm{f}\mathrm{o}\mathrm{r}\hskip0.42em i=s\hskip0.33em \mathrm{a}\mathrm{n}\mathrm{d}\hskip0.33em m, $$

$$ {O}_i^{\mathrm{ST}}={\unicode{x1D53C}}_0({\mathbf{1}}_{\{\unicode{x1D53C}({\operatorname{}{F}_i|}_{t=1})<{L}_i^{\mathrm{ST}}\}})\hskip0.33em \mathrm{a}\mathrm{n}\mathrm{d}\hskip0.42em {O}_i^{\mathrm{LT}}={\unicode{x1D53C}}_0({\mathbf{1}}_{\{{F}_i\ \mathrm{a}\mathrm{t}\ t=2<{L}_i^{\mathrm{LT}}\}}),\hskip0.6em \mathrm{f}\mathrm{o}\mathrm{r}\hskip0.42em i=s\hskip0.33em \mathrm{a}\mathrm{n}\mathrm{d}\hskip0.33em m, $$

where

$ {\mathbf{1}}_{\left\{\cdot \right\}} $

is an indicator function that equals 1 when the condition in

$ {\mathbf{1}}_{\left\{\cdot \right\}} $

is an indicator function that equals 1 when the condition in

$ \left\{\cdot \right\} $

holds, and 0 otherwise. Combining (8) with the conditional distributions of

$ \left\{\cdot \right\} $

holds, and 0 otherwise. Combining (8) with the conditional distributions of

$ {F}_s $

and

$ {F}_s $

and

$ {F}_m $

, we have

$ {F}_m $

, we have

$$ {O}_s^{\mathrm{ST}}=\frac{1}{2},\hskip1em {O}_s^{\mathrm{LT}}=\frac{2}{3},\hskip1em {O}_m^{\mathrm{ST}}=\frac{1}{4},\hskip1em \mathrm{and}\hskip1em {O}_m^{\mathrm{LT}}=\frac{1}{3}. $$

$$ {O}_s^{\mathrm{ST}}=\frac{1}{2},\hskip1em {O}_s^{\mathrm{LT}}=\frac{2}{3},\hskip1em {O}_m^{\mathrm{ST}}=\frac{1}{4},\hskip1em \mathrm{and}\hskip1em {O}_m^{\mathrm{LT}}=\frac{1}{3}. $$

Comparing

$ {O}_s^{\mathrm{ST}} $

with

$ {O}_s^{\mathrm{ST}} $

with

$ {O}_m^{\mathrm{ST}} $

and

$ {O}_m^{\mathrm{ST}} $

and

$ {O}_s^{\mathrm{LT}} $

with

$ {O}_s^{\mathrm{LT}} $

with

$ {O}_m^{\mathrm{LT}} $

shows that corporate diversification mitigates debt overhang in the short term and the long term. Moreover,

$ {O}_m^{\mathrm{LT}} $

shows that corporate diversification mitigates debt overhang in the short term and the long term. Moreover,

$ {O}_m^{\mathrm{LT}}-{O}_m^{\mathrm{ST}}<{O}_s^{\mathrm{LT}}-{O}_s^{\mathrm{ST}} $

. Thus, corporate diversification reduces the difference between long-term and short-term debt overhang (the wedge).Footnote 13

$ {O}_m^{\mathrm{LT}}-{O}_m^{\mathrm{ST}}<{O}_s^{\mathrm{LT}}-{O}_s^{\mathrm{ST}} $

. Thus, corporate diversification reduces the difference between long-term and short-term debt overhang (the wedge).Footnote 13

Now, we describe how corporate diversification affects investment incentives. Denote the percentage investment cost by

$ \lambda $

, and let

$ \lambda $

, and let

$$ \left(1-\lambda \right)>{O}_i^j, $$

$$ \left(1-\lambda \right)>{O}_i^j, $$

where

$ i\in \left\{s,m\right\} $

and

$ i\in \left\{s,m\right\} $

and

$ j\in \left\{ ST, LT\right\} $

. This condition implies that a firm invests only in projects with an NPV exceeding the debt overhang.

$ j\in \left\{ ST, LT\right\} $

. This condition implies that a firm invests only in projects with an NPV exceeding the debt overhang.

For

$ S $

’s shareholders, the condition above is satisfied if

$ S $

’s shareholders, the condition above is satisfied if

$ \lambda <1/3 $

, regardless of whether the firm raises short-term or long-term debt, implying an internal rate of return (

$ \lambda <1/3 $

, regardless of whether the firm raises short-term or long-term debt, implying an internal rate of return (

$ \mathrm{IRR}=\left(1-\lambda \right)/\lambda $

), larger than

$ \mathrm{IRR}=\left(1-\lambda \right)/\lambda $

), larger than

$ 200\% $

. For

$ 200\% $

. For

$ M $

’s shareholders, the condition becomes

$ M $

’s shareholders, the condition becomes

$ \lambda <2/3 $

, or equivalently

$ \lambda <2/3 $

, or equivalently

$ \mathrm{IRR}>50\% $

. Focusing on the optimal choice for short-term debt only, the investment condition modifies to

$ \mathrm{IRR}>50\% $

. Focusing on the optimal choice for short-term debt only, the investment condition modifies to

$ \lambda <1/2 $

(

$ \lambda <1/2 $

(

$ \mathrm{IRR}>100\% $

) for

$ \mathrm{IRR}>100\% $

) for

$ S $

’s shareholders and

$ S $

’s shareholders and

$ \lambda <3/4 $

(

$ \lambda <3/4 $

(

$ \mathrm{IRR}>33.\overline{3}\% $

) for

$ \mathrm{IRR}>33.\overline{3}\% $

) for

$ M $

’s shareholders. Therefore, all else being equal, a multi-division firm is more likely to invest in new projects than a comparable stand-alone firm. This occurs because corporate diversification mitigates debt overhang through the coinsurance effect.

$ M $

’s shareholders. Therefore, all else being equal, a multi-division firm is more likely to invest in new projects than a comparable stand-alone firm. This occurs because corporate diversification mitigates debt overhang through the coinsurance effect.

Although cash holding is not explicitly modeled here, our model implies that multi-division firms have more incentives to deploy excess cash (Opler, Pinkowitz, Stulz, and Williamson (Reference Opler, Pinkowitz, Stulz and Williamson1999)) for investment. This could result in a reduction in excess cash due to reduced debt overhang, providing an alternative explanation for Duchin (Reference Duchin2010), who finds that multi-division firms hold significantly less cash than stand-alone firms.Footnote 14

To recap, assuming that the market value of debt is the same for both

$ S $

and

$ S $

and

$ M $

, the simple model above predicts that corporate diversification mitigates the debt overhang problem by decreasing both the extent of long-term and short-term debt overhang, as well as the wedge between them. However, the simplicity of this model comes at a cost: we assume that noninterest expenses are 0, and this leads us to conclude that short-term debt is preferred to long-term debt for both single-division and multi-division firms. This confirms Myers’s (Reference Myers1977) suggestion that short-term debt is a possible solution to the debt overhang problem in a frictionless scenario.Footnote 15

$ M $

, the simple model above predicts that corporate diversification mitigates the debt overhang problem by decreasing both the extent of long-term and short-term debt overhang, as well as the wedge between them. However, the simplicity of this model comes at a cost: we assume that noninterest expenses are 0, and this leads us to conclude that short-term debt is preferred to long-term debt for both single-division and multi-division firms. This confirms Myers’s (Reference Myers1977) suggestion that short-term debt is a possible solution to the debt overhang problem in a frictionless scenario.Footnote 15

In Section II.C, we relax the assumption of zero noninterest expenses and we generalize our model to allow for a number of divisions,

$ N $

, larger than 2. In line with the results of our 3-period model with only two divisions for

$ N $

, larger than 2. In line with the results of our 3-period model with only two divisions for

$ M $

, we impose the following conditions:

$ M $

, we impose the following conditions:

$$ \frac{\partial {O}^{\mathrm{LT}}(N)}{\partial N}<0,\hskip1em \frac{\partial {O}^{\mathrm{ST}}(N)}{\partial N}<0,\hskip1em \mathrm{and}\hskip1em \frac{\partial {\Delta}_O(N)}{\partial N}<0, $$

$$ \frac{\partial {O}^{\mathrm{LT}}(N)}{\partial N}<0,\hskip1em \frac{\partial {O}^{\mathrm{ST}}(N)}{\partial N}<0,\hskip1em \mathrm{and}\hskip1em \frac{\partial {\Delta}_O(N)}{\partial N}<0, $$

where

$ 0<{O}^{\mathrm{ST}}(N)\le {O}^{\mathrm{LT}}(N)<1 $

and

$ 0<{O}^{\mathrm{ST}}(N)\le {O}^{\mathrm{LT}}(N)<1 $

and

$ {\Delta}_O(N)={O}^{\mathrm{LT}}(N)-{O}^{\mathrm{ST}}(N) $

, i.e., the wedge. Therefore, by definition,

$ {\Delta}_O(N)={O}^{\mathrm{LT}}(N)-{O}^{\mathrm{ST}}(N) $

, i.e., the wedge. Therefore, by definition,

$ {O}_s^{\mathrm{LT}}={O}^{\mathrm{LT}}(1) $

,

$ {O}_s^{\mathrm{LT}}={O}^{\mathrm{LT}}(1) $

,

$ {O}_s^{\mathrm{ST}}={O}^{\mathrm{ST}}(1) $

,

$ {O}_s^{\mathrm{ST}}={O}^{\mathrm{ST}}(1) $

,

$ {O}_m^{\mathrm{LT}}={O}^{\mathrm{LT}}(2) $

, and

$ {O}_m^{\mathrm{LT}}={O}^{\mathrm{LT}}(2) $

, and

$ {O}_m^{\mathrm{ST}}={O}^{\mathrm{ST}}(2) $

.

$ {O}_m^{\mathrm{ST}}={O}^{\mathrm{ST}}(2) $

.

C. Noninterest Debt Expenses and Debt Maturity

Short-term debt is known to have disadvantages over long-term debt. For example, short-term debt has higher issuance costs and higher rollover costs than long-term debt due to the higher frequency at which short-term debt needs to be issued or rolled over (Acharya et al. (Reference Acharya, Gale and Yorulmazer2011), He and Xiong (Reference He and Xiong2012), Cheng and Milbradt (Reference Cheng and Milbradt2012), Valenzuela (Reference Valenzuela2016)). To incorporate these additional noninterest costs in our model, we assume that the funding raised via short-term debt is proportional to investment size. Specifically, we denote such extra costs by

$ \xi \ge 0 $

and define the overhang-adjusted NPV (Chen and Manso (Reference Chen and Manso2017)) as follows:

$ \xi \ge 0 $

and define the overhang-adjusted NPV (Chen and Manso (Reference Chen and Manso2017)) as follows:

$$ {R}_i^j=\left[1-\left(1+\xi {\mathbf{1}}_{\left\{j=\mathrm{ST}\right\}}\right)\lambda \right]\varepsilon -{O}_i^j\varepsilon, $$

$$ {R}_i^j=\left[1-\left(1+\xi {\mathbf{1}}_{\left\{j=\mathrm{ST}\right\}}\right)\lambda \right]\varepsilon -{O}_i^j\varepsilon, $$

which can be used to compare the investment incentives under different scenarios. When

$ \xi =0 $

, as mentioned before, short-term debt is always preferred over long-term debt in terms of investment incentives in both

$ \xi =0 $

, as mentioned before, short-term debt is always preferred over long-term debt in terms of investment incentives in both

$ S $

and

$ S $

and

$ M $

. When

$ M $

. When

$ \xi >0 $

, however, debt maturity preferences depend on whether the firm is diversified or not. Due to the third condition in (11)—the wedge becomes smaller as

$ \xi >0 $

, however, debt maturity preferences depend on whether the firm is diversified or not. Due to the third condition in (11)—the wedge becomes smaller as

$ N $

increases—when

$ N $

increases—when

$ \xi >0 $

, the overhang-adjusted NPV for projects funded using long-term debt is more likely to be higher for

$ \xi >0 $

, the overhang-adjusted NPV for projects funded using long-term debt is more likely to be higher for

$ M $

than for

$ M $

than for

$ S $

. To formalize this intuition and generalize its validity to a broad range of realistic scenarios, we need to introduce a regularity assumption.

$ S $

. To formalize this intuition and generalize its validity to a broad range of realistic scenarios, we need to introduce a regularity assumption.

Assumption 1. The short-term debt expense

$ \xi $

and the investment cost

$ \xi $

and the investment cost

$ \lambda $

are independently and uniformly distributed on

$ \lambda $

are independently and uniformly distributed on

$ \left[0,\overline{\xi}\right] $

and

$ \left[0,\overline{\xi}\right] $

and

$ \left[\underline{\lambda},1\right] $

, respectively.

$ \left[\underline{\lambda},1\right] $

, respectively.

$ \overline{\xi} $

and

$ \overline{\xi} $

and

$ \underline{\lambda} $

satisfy the following constraintsFootnote 16:

$ \underline{\lambda} $

satisfy the following constraintsFootnote 16:

$$ \frac{O_s^{LT}-{O}_s^{ST}}{1-{O}_s^{LT}}+\log \left(\frac{1-{O}_s^{ST}}{1-{O}_s^{LT}}\right)<\overline{\xi}\le \frac{2\left({O}_s^{LT}-{O}_s^{ST}\right)}{1-{O}_s^{LT}}, $$

$$ \frac{O_s^{LT}-{O}_s^{ST}}{1-{O}_s^{LT}}+\log \left(\frac{1-{O}_s^{ST}}{1-{O}_s^{LT}}\right)<\overline{\xi}\le \frac{2\left({O}_s^{LT}-{O}_s^{ST}\right)}{1-{O}_s^{LT}}, $$

$$ 0<\underline{\lambda}<1-{O}_s^{LT}. $$

$$ 0<\underline{\lambda}<1-{O}_s^{LT}. $$

The uniform distribution assumption is common in the asset-pricing literature (Oehmke and Zawadowski (Reference Oehmke and Zawadowski2015), Glode and Opp (Reference Glode and Opp2016), Hollifield, Neklyudov, and Spatt (Reference Hollifield, Neklyudov and Spatt2017)). Both (13) and (14) are sufficient (albeit not necessary) conditions for the proposition we introduce below. Given reasonable values of

$ {O}_s^{\mathrm{ST}} $

and

$ {O}_s^{\mathrm{ST}} $

and

$ {O}_s^{\mathrm{LT}} $

, equation (13) ensures

$ {O}_s^{\mathrm{LT}} $

, equation (13) ensures

$ \overline{\xi}>0 $

with a bounded upper limit, and equation (14) rise in plausible IRR scenarios.

$ \overline{\xi}>0 $

with a bounded upper limit, and equation (14) rise in plausible IRR scenarios.

Now, we use

$ {R}^{ST} $

and

$ {R}^{ST} $

and

$ {R}^{LT} $

to denote the NPV of projects funded with short-term debt and long-term debt, respectively. Moreover,

$ {R}^{LT} $

to denote the NPV of projects funded with short-term debt and long-term debt, respectively. Moreover,

$ {P}^{\mathrm{ST}} $

is the probability of raising short-term debt instead of long-term debt to invest in projects with a positive NPV:

$ {P}^{\mathrm{ST}} $

is the probability of raising short-term debt instead of long-term debt to invest in projects with a positive NPV:

$ {P}^{\mathrm{ST}}=\unicode{x1D53C}\left({\mathbf{1}}_{\left\{{R}^{\mathrm{ST}}>\max \left(0,{R}^{\mathrm{LT}}\right)\right\}}\right) $

. Similarly, the probability of raising long-term debt instead of short-term debt is defined as

$ {P}^{\mathrm{ST}}=\unicode{x1D53C}\left({\mathbf{1}}_{\left\{{R}^{\mathrm{ST}}>\max \left(0,{R}^{\mathrm{LT}}\right)\right\}}\right) $

. Similarly, the probability of raising long-term debt instead of short-term debt is defined as

$ {P}^{\mathrm{LT}}=\unicode{x1D53C}\left({\mathbf{1}}_{\left\{{R}^{\mathrm{LT}}>\max \left(0,{R}^{\mathrm{ST}}\right)\right\}}\right) $

. To understand the impact of corporate diversification, we use the subscript

$ {P}^{\mathrm{LT}}=\unicode{x1D53C}\left({\mathbf{1}}_{\left\{{R}^{\mathrm{LT}}>\max \left(0,{R}^{\mathrm{ST}}\right)\right\}}\right) $

. To understand the impact of corporate diversification, we use the subscript

$ N $

, denoting the number of segments. Thus,

$ N $

, denoting the number of segments. Thus,

$ {P}_N^{ST} $

and

$ {P}_N^{ST} $

and

$ {P}_N^{LT} $

are the probabilities of investing using short-term and long-term debt, respectively, for a firm with

$ {P}_N^{LT} $

are the probabilities of investing using short-term and long-term debt, respectively, for a firm with

$ N $

segments.Footnote 17

$ N $

segments.Footnote 17

Given these definitions, we can now introduce Proposition 1, which is proved in Appendix A.

Proposition 1. Given a fixed market value of debt and conditions in (11) and Assumption 1, there exists a threshold

$ {N}^{\ast } $

such that firms with more than

$ {N}^{\ast } $

such that firms with more than

$ {N}^{\ast } $

segments are more likely to invest using long-term debt, whereas those with fewer than

$ {N}^{\ast } $

segments are more likely to invest using long-term debt, whereas those with fewer than

$ {N}^{\ast } $

segments are more likely to invest using short-term debt. More formally:

$ {N}^{\ast } $

segments are more likely to invest using short-term debt. More formally:

$$ \mathrm{\exists}{N}^{\ast }:\{\begin{array}{cc}{P}^{LT}<{P}^{ST},& if\;N<{N}^{\ast },\\ {}{P}^{LT}\ge {P}^{ST},& if\;N\ge {N}^{\ast }.\end{array}\operatorname{} $$

$$ \mathrm{\exists}{N}^{\ast }:\{\begin{array}{cc}{P}^{LT}<{P}^{ST},& if\;N<{N}^{\ast },\\ {}{P}^{LT}\ge {P}^{ST},& if\;N\ge {N}^{\ast }.\end{array}\operatorname{} $$

Given the values of

$ {O}_s^{\mathrm{LT}} $

and

$ {O}_s^{\mathrm{LT}} $

and

$ {O}_s^{\mathrm{ST}} $

in (9), the constraints in Assumption 1 for

$ {O}_s^{\mathrm{ST}} $

in (9), the constraints in Assumption 1 for

$ \overline{\xi} $

and

$ \overline{\xi} $

and

$ \underline{\lambda} $

are

$ \underline{\lambda} $

are

$$ 0.91<\overline{\xi}\le 1\hskip0.62em \mathrm{and}\hskip0.62em 0<\underline{\lambda}<1/3. $$

$$ 0.91<\overline{\xi}\le 1\hskip0.62em \mathrm{and}\hskip0.62em 0<\underline{\lambda}<1/3. $$

For numerical illustration, we set

$ \overline{\xi}=1 $

, which means the short-term debt expense is shared by each investment up to the total size of the initial investment outlay before the short-term debt expense;

$ \overline{\xi}=1 $

, which means the short-term debt expense is shared by each investment up to the total size of the initial investment outlay before the short-term debt expense;

$ \underline{\lambda}=0.25 $

, which means

$ \underline{\lambda}=0.25 $

, which means

$ \lambda \in \left[\mathrm{0.25,1}\right] $

, so that each investment’s IRR before the short-term debt expense is positive and no more than

$ \lambda \in \left[\mathrm{0.25,1}\right] $

, so that each investment’s IRR before the short-term debt expense is positive and no more than

$ 300\% $

.Footnote 18 Given these settings and the values of

$ 300\% $

.Footnote 18 Given these settings and the values of

$ {O}^{\mathrm{LT}} $

and

$ {O}^{\mathrm{LT}} $

and

$ {O}^{\mathrm{ST}} $

in (9), we have

$ {O}^{\mathrm{ST}} $

in (9), we have

$$ {P}_s^{\mathrm{ST}}=0.112>0.047={P}_s^{\mathrm{LT}}, $$

$$ {P}_s^{\mathrm{ST}}=0.112>0.047={P}_s^{\mathrm{LT}}, $$

$$ {P}_m^{\mathrm{ST}}=0.116<0.447={P}_m^{\mathrm{LT}}, $$

$$ {P}_m^{\mathrm{ST}}=0.116<0.447={P}_m^{\mathrm{LT}}, $$

where

$ {P}_s^{ST} $

and

$ {P}_s^{ST} $

and

$ {P}_m^{ST} $

are

$ {P}_m^{ST} $

are

$ {P}^{ST} $

for the stand-alone and multi-division firms, respectively, and

$ {P}^{ST} $

for the stand-alone and multi-division firms, respectively, and

$ {P}_s^{LT} $

and

$ {P}_s^{LT} $

and

$ {P}_m^{LT} $

are

$ {P}_m^{LT} $

are

$ {P}^{LT} $

for the stand-alone and multi-division firms, respectively.

$ {P}^{LT} $

for the stand-alone and multi-division firms, respectively.

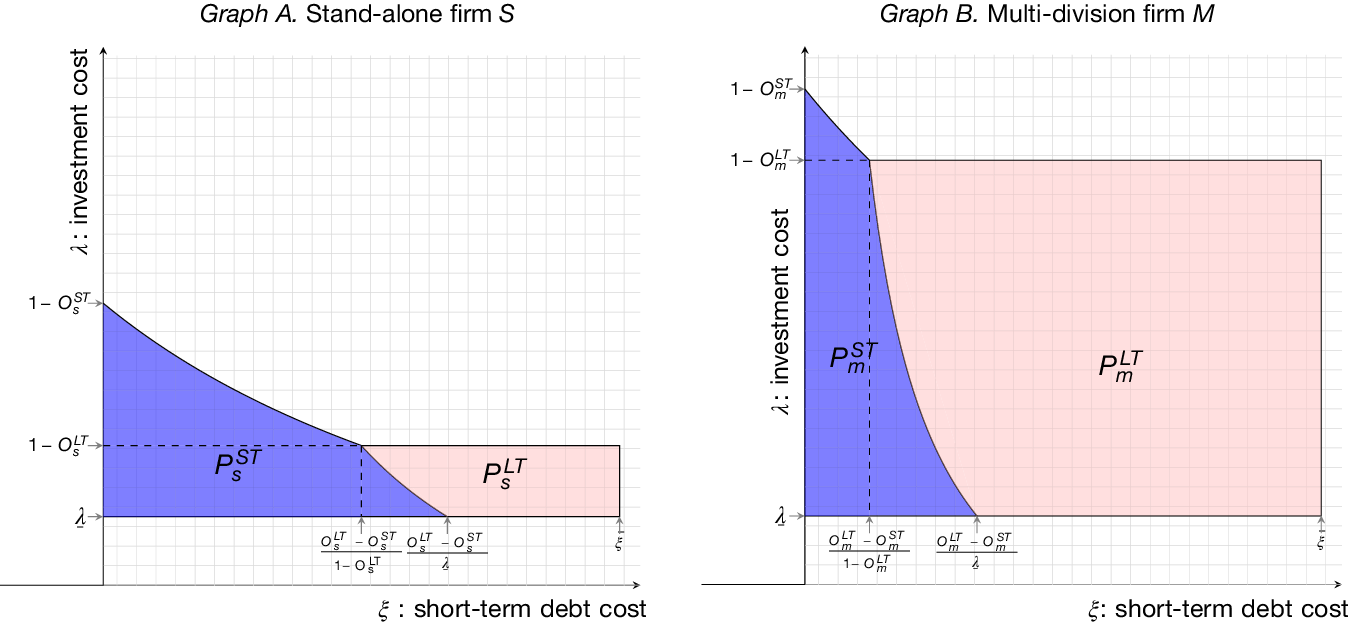

To see the above intuition more clearly, we plot in Figure 3 the probabilities of investing with short-term debt

$ {P}_i^{\mathrm{ST}} $

and long-term debt

$ {P}_i^{\mathrm{ST}} $

and long-term debt

$ {P}_i^{\mathrm{LT}} $

defined in Proposition 1, which are derived in Appendix A. The area of the different shapes represents the probability values.

$ {P}_i^{\mathrm{LT}} $

defined in Proposition 1, which are derived in Appendix A. The area of the different shapes represents the probability values.

$ {P}^{\mathrm{ST}} $

’s area clearly diminishes with

$ {P}^{\mathrm{ST}} $

’s area clearly diminishes with

$ {O}^{\mathrm{LT}}-{O}^{\mathrm{ST}} $

getting smaller, especially

$ {O}^{\mathrm{LT}}-{O}^{\mathrm{ST}} $

getting smaller, especially

$ {P}_2^{\mathrm{ST}} $

, which has an upper bound of

$ {P}_2^{\mathrm{ST}} $

, which has an upper bound of

$ \frac{{\left({O}^{\mathrm{LT}}-{O}^{\mathrm{ST}}\right)}^2}{2\left(1-{O}^{\mathrm{LT}}\right)} $

.

$ \frac{{\left({O}^{\mathrm{LT}}-{O}^{\mathrm{ST}}\right)}^2}{2\left(1-{O}^{\mathrm{LT}}\right)} $

.

In Figure 3, the areas of the different shapes represent probability values. Graphs A and B, respectively, plot stand-alone firm

$ S $

and multi-division firm

$ S $

and multi-division firm

$ M $

’s probabilities of investing with short-term debt

$ M $

’s probabilities of investing with short-term debt

$ {P}_i^{\mathrm{ST}} $

and long-term debt

$ {P}_i^{\mathrm{ST}} $

and long-term debt

$ {P}_i^{\mathrm{LT}} $

defined in Proposition 1. The formulae of different areas are presented in Appendix A. The numerical values of parameters are set as follows:

$ {P}_i^{\mathrm{LT}} $

defined in Proposition 1. The formulae of different areas are presented in Appendix A. The numerical values of parameters are set as follows:

$ {O}_s^{\mathrm{ST}}=\frac{1}{2},{O}_s^{\mathrm{LT}}=\frac{2}{3},{O}_m^{\mathrm{ST}}=\frac{1}{4},\mathrm{and}\;{O}_m^{\mathrm{LT}}=\frac{1}{3} $

;

$ {O}_s^{\mathrm{ST}}=\frac{1}{2},{O}_s^{\mathrm{LT}}=\frac{2}{3},{O}_m^{\mathrm{ST}}=\frac{1}{4},\mathrm{and}\;{O}_m^{\mathrm{LT}}=\frac{1}{3} $

;

$ \overline{\xi}=1 $

and

$ \overline{\xi}=1 $

and

$ \underline{\lambda}=0.25 $

.

$ \underline{\lambda}=0.25 $

.

With this simple 3-period model, we gain valuable insights into how Hann et al.’s (Reference Hann, Ogneva and Ozbas2013) coinsurance effect of corporate diversification alleviates debt overhang and enhances investment incentives. This model elucidates a novel prediction accounting for higher noninterest expenses for short-term debt: a positive association between corporate diversification and debt maturity. However, this 3-period model is unable to incorporate more nuanced features for further analysis, such as the possibility of size heterogeneity for the segments of a multi-division firm, correlated payoffs for different segments, and continuous debt maturity. To offer further insights, in Section III, we develop a continuous-time structural model using option pricing.

III. A Black–Scholes–Merton Model Variant for Corporate Diversification

In a typical setting regarding pricing the equity of a levered firm, the market value of equity at time

$ 0 $

with debt maturity of

$ 0 $

with debt maturity of

$ t $

can be found using standard pricing models for call options, since equity is the residual claimant at time

$ t $

can be found using standard pricing models for call options, since equity is the residual claimant at time

$ t $

(Merton (Reference Merton1974)). Under certain assumptions, the equity of a levered firm is essentially a European call option with the strike price equal to the face value of debt to be repaid at time

$ t $

(Merton (Reference Merton1974)). Under certain assumptions, the equity of a levered firm is essentially a European call option with the strike price equal to the face value of debt to be repaid at time

$ t $

.

$ t $

.

To parsimoniously capture the impact of corporate diversification on investment incentive and debt maturity choice, we follow Diamond and He’s (Reference Diamond and He2014) analysis based on the Black–Scholes–Merton setting and assume that the firm’s only debt is a zero-coupon debt maturing at time

$ t $

with a face value

$ t $

with a face value

$ L $

and set the risk-free rate to

$ L $

and set the risk-free rate to

$ r $

.Footnote 19

$ r $

.Footnote 19

Accordingly, our structural model assumes that a diversified firm with

$ N $

divisions has

$ N $

divisions has

$ N $

existing assets-in-place. We denote the risk-neutral measure by

$ N $

existing assets-in-place. We denote the risk-neutral measure by

$ \mathrm{\mathbb{Q}} $

(Arnold, Hackbarth, and Xenia Puhan (Reference Arnold, Hackbarth and Puhan2017)). The total value of a levered firm is

$ \mathrm{\mathbb{Q}} $

(Arnold, Hackbarth, and Xenia Puhan (Reference Arnold, Hackbarth and Puhan2017)). The total value of a levered firm is

$ {V}_t={\sum}_{i=1}^N{v}_{i,t} $

, where the distribution of the value of each of the assets-in-place follows a geometric Brownian motion (GBM) under the

$ {V}_t={\sum}_{i=1}^N{v}_{i,t} $

, where the distribution of the value of each of the assets-in-place follows a geometric Brownian motion (GBM) under the

$ \mathrm{\mathbb{Q}} $

measure:

$ \mathrm{\mathbb{Q}} $

measure:

$$ \frac{dv_{i,t}}{v_{i,t}}={g}_i dt+{\sigma}_i{dw}_{i,t},\hskip1em i=1,\cdots, N, $$

$$ \frac{dv_{i,t}}{v_{i,t}}={g}_i dt+{\sigma}_i{dw}_{i,t},\hskip1em i=1,\cdots, N, $$

where

$ {g}_i $

is the growth rate of

$ {g}_i $

is the growth rate of

$ {v}_{i,t} $

under the

$ {v}_{i,t} $

under the

$ \mathrm{\mathbb{Q}} $

measure,

$ \mathrm{\mathbb{Q}} $

measure,

$ {w}_{i,t} $

is a Wiener process under the

$ {w}_{i,t} $

is a Wiener process under the

$ \mathrm{\mathbb{Q}} $

measure, and

$ \mathrm{\mathbb{Q}} $

measure, and

$ {\rho}_{ij} $

is the pairwise correlation between

$ {\rho}_{ij} $

is the pairwise correlation between

$ {w}_i $

and

$ {w}_i $

and

$ {w}_j $

. Given this setting, since the sum of GBM is not itself a GBM, the standard Black–Scholes option pricing formula cannot be used. This means that we need to depart from the assumptions in Diamond and He’s (Reference Diamond and He2014) model, since, in their model,

$ {w}_j $

. Given this setting, since the sum of GBM is not itself a GBM, the standard Black–Scholes option pricing formula cannot be used. This means that we need to depart from the assumptions in Diamond and He’s (Reference Diamond and He2014) model, since, in their model,

$ {V}_t $

is assumed to be log-normally distributed. However, we can still make use of option pricing techniques. Specifically, we argue that the equity of a levered multi-division firm can be priced according to the models developed for pricing basket options (i.e., options whose underlying consists of two or more securities). For convenience, the detailed descriptions of model parameters and functions used in this section are presented in Table 1.

$ {V}_t $

is assumed to be log-normally distributed. However, we can still make use of option pricing techniques. Specifically, we argue that the equity of a levered multi-division firm can be priced according to the models developed for pricing basket options (i.e., options whose underlying consists of two or more securities). For convenience, the detailed descriptions of model parameters and functions used in this section are presented in Table 1.

A. A Basket Option Approach for Modeling Corporate Diversification

At time

$ t $

, we have two potential outcomes for shareholders: if

$ t $

, we have two potential outcomes for shareholders: if

$ {V}_t<L $

, debt holders take over the defaulted firm and shareholders receive 0; if

$ {V}_t<L $

, debt holders take over the defaulted firm and shareholders receive 0; if

$ {V}_t\ge L $

, debt holders are repaid the full amount

$ {V}_t\ge L $

, debt holders are repaid the full amount

$ L $

and shareholders receive the residual value

$ L $

and shareholders receive the residual value

$ {V}_t-L $

. Thus, at time

$ {V}_t-L $

. Thus, at time

$ 0 $

, the market equity value of a levered firm with

$ 0 $

, the market equity value of a levered firm with

$ N $

divisions is

$ N $

divisions is

$$ E\left(L,t\right)={\unicode{x1D53C}}_0^{\mathrm{\mathbb{Q}}}\left[{\left(\sum \limits_{i=1}^N{v}_{i,t}-L\right)}^{+}\right], $$

$$ E\left(L,t\right)={\unicode{x1D53C}}_0^{\mathrm{\mathbb{Q}}}\left[{\left(\sum \limits_{i=1}^N{v}_{i,t}-L\right)}^{+}\right], $$

and the corresponding market value of debt is

$ D\left(L,t\right)={V}_0-E\left(L,t\right) $

. Although the exact closed-form solution of the basket option is unavailable—to the best of our knowledge—highly accurate approximations exist. Here, we use Ju’s (Reference Ju2002) Taylor expansion approximation as the solution to equation (19)

Footnote 20:

$ D\left(L,t\right)={V}_0-E\left(L,t\right) $

. Although the exact closed-form solution of the basket option is unavailable—to the best of our knowledge—highly accurate approximations exist. Here, we use Ju’s (Reference Ju2002) Taylor expansion approximation as the solution to equation (19)

Footnote 20:

$$ E\left(L,t\right)=\left[{U}_1N\left({y}_1\right)- LN\left({y}_2\right)\right]+L\left({z}_1p(y)+{z}_2\frac{dp(y)}{dy}+{z}_3\frac{d^2p(y)}{dy^2}\right), $$

$$ E\left(L,t\right)=\left[{U}_1N\left({y}_1\right)- LN\left({y}_2\right)\right]+L\left({z}_1p(y)+{z}_2\frac{dp(y)}{dy}+{z}_3\frac{d^2p(y)}{dy^2}\right), $$

where

$ N\left(\cdot \right) $

is the standard normal CDF and

$ N\left(\cdot \right) $

is the standard normal CDF and

$ p\left(\cdot \right) $

is the normal PDF with mean

$ p\left(\cdot \right) $

is the normal PDF with mean

$ \mu (1) $

and variance

$ \mu (1) $

and variance

$ \nu (1) $

,

$ \nu (1) $

,

$$ y=\mathit{\log}(L),{y}_1=\frac{\mu (1)-y}{\sqrt{\nu (1)}}+\sqrt{\nu (1)},\hskip1em {y}_2={y}_1-\sqrt{\nu (1)}. $$

$$ y=\mathit{\log}(L),{y}_1=\frac{\mu (1)-y}{\sqrt{\nu (1)}}+\sqrt{\nu (1)},\hskip1em {y}_2={y}_1-\sqrt{\nu (1)}. $$

Closed-form expressions for

$ \mu (x) $

,

$ \mu (x) $

,

$ \nu (x) $

,

$ \nu (x) $

,

$ {z}_1 $

,

$ {z}_1 $

,

$ {z}_2 $

, and

$ {z}_2 $

, and

$ {z}_3 $

are provided in Appendix B.

$ {z}_3 $

are provided in Appendix B.

B. Revisiting the Corporate Diversification’s Effect on Debt Maturity and Overhang

Since we focus on debt overhang from infinitesimal investments, we define the debt overhang measure as follows:

$$ O\left(N,t,W\right)=\sum \limits_{i=1}^N{W}_i\frac{\partial D\left(L,t\right)}{\partial {v}_{i,0}}=1-\sum \limits_{i=1}^N{W}_i\frac{\partial E\left(L,t\right)}{\partial {v}_{i,0}}, $$

$$ O\left(N,t,W\right)=\sum \limits_{i=1}^N{W}_i\frac{\partial D\left(L,t\right)}{\partial {v}_{i,0}}=1-\sum \limits_{i=1}^N{W}_i\frac{\partial E\left(L,t\right)}{\partial {v}_{i,0}}, $$

where

$ {W}_i $

is the

$ {W}_i $

is the

$ i $

th element of the

$ i $

th element of the

$ N\times 1 $

weighting vector

$ N\times 1 $

weighting vector

$ W $

and

$ W $

and

$ {\sum}_i^N{W}_i=1 $

. The debt overhang measure defined by Diamond and He (Reference Diamond and He2014) under their Black–Scholes–Merton setting is a special case of equation (21) when

$ {\sum}_i^N{W}_i=1 $

. The debt overhang measure defined by Diamond and He (Reference Diamond and He2014) under their Black–Scholes–Merton setting is a special case of equation (21) when

$ N=1 $

. As argued by Galai and Masulis (Reference Galai and Masulis1976), corporate diversification increases firms’ debt capacity, which could result in higher leverage and/or longer debt maturity. Since the evidence on the relationship between corporate diversification and leverage is weak (see Berger and Ofek (Reference Berger and Ofek1995), Mansi and Reeb (Reference Mansi and Reeb2002), and Section IV), and our empirical results in Section IV provide strong evidence on the positive association between corporate diversification on debt maturity, we focus on a counterfactual analysis for debt maturity while constraining the face value of debt

$ N=1 $

. As argued by Galai and Masulis (Reference Galai and Masulis1976), corporate diversification increases firms’ debt capacity, which could result in higher leverage and/or longer debt maturity. Since the evidence on the relationship between corporate diversification and leverage is weak (see Berger and Ofek (Reference Berger and Ofek1995), Mansi and Reeb (Reference Mansi and Reeb2002), and Section IV), and our empirical results in Section IV provide strong evidence on the positive association between corporate diversification on debt maturity, we focus on a counterfactual analysis for debt maturity while constraining the face value of debt

$ L $

to be the same for both

$ L $

to be the same for both

$ S $

and

$ S $

and

$ M $

.Footnote 21

$ M $

.Footnote 21

We use the Black–Scholes formula to price

$ S $

’s equity value, and we allow the debt maturity of

$ S $

’s equity value, and we allow the debt maturity of

$ M $

to vary until its equity value matches that of

$ M $

to vary until its equity value matches that of

$ S $

. This enables us to calculate the implied debt maturity for

$ S $

. This enables us to calculate the implied debt maturity for

$ M $

(i.e., implied by its equity value). Shareholders maximize the firm value by choosing the optimal debt maturity, conditional on their firm’s divisional structure. In other words, shareholders choose the optimal debt maturity with the minimal investment cost and debt overhang to achieve a given level of firm value and growth.

$ M $

(i.e., implied by its equity value). Shareholders maximize the firm value by choosing the optimal debt maturity, conditional on their firm’s divisional structure. In other words, shareholders choose the optimal debt maturity with the minimal investment cost and debt overhang to achieve a given level of firm value and growth.

We impose conditions to ensure that

$ M $

and

$ M $

and

$ S $

are strictly comparable. Specifically, we constrain

$ S $

are strictly comparable. Specifically, we constrain

$ M $

to have the same total assets-in-place, growth rate, market value of equity, and face value of debt as

$ M $

to have the same total assets-in-place, growth rate, market value of equity, and face value of debt as

$ S $

. For simplicity, we also set each division’s assets-in-place within

$ S $

. For simplicity, we also set each division’s assets-in-place within

$ M $

to have equal weights and with the same volatility as

$ M $

to have equal weights and with the same volatility as

$ S $

. To price

$ S $

. To price

$ M $

’s equity value, we also need the pairwise correlation

$ M $

’s equity value, we also need the pairwise correlation

$ \rho $

between any two divisions, which negatively affects corporate diversification’s coinsurance effect. We set the pairwise correlation coefficient to three different levels: {0, 0.1, 0.3}. Thanks to the analytical formula in equation (20), we can easily solve for the value of debt maturity by equating

$ \rho $

between any two divisions, which negatively affects corporate diversification’s coinsurance effect. We set the pairwise correlation coefficient to three different levels: {0, 0.1, 0.3}. Thanks to the analytical formula in equation (20), we can easily solve for the value of debt maturity by equating

$ M $

’s equity value to that of

$ M $

’s equity value to that of

$ S $

.

$ S $

.

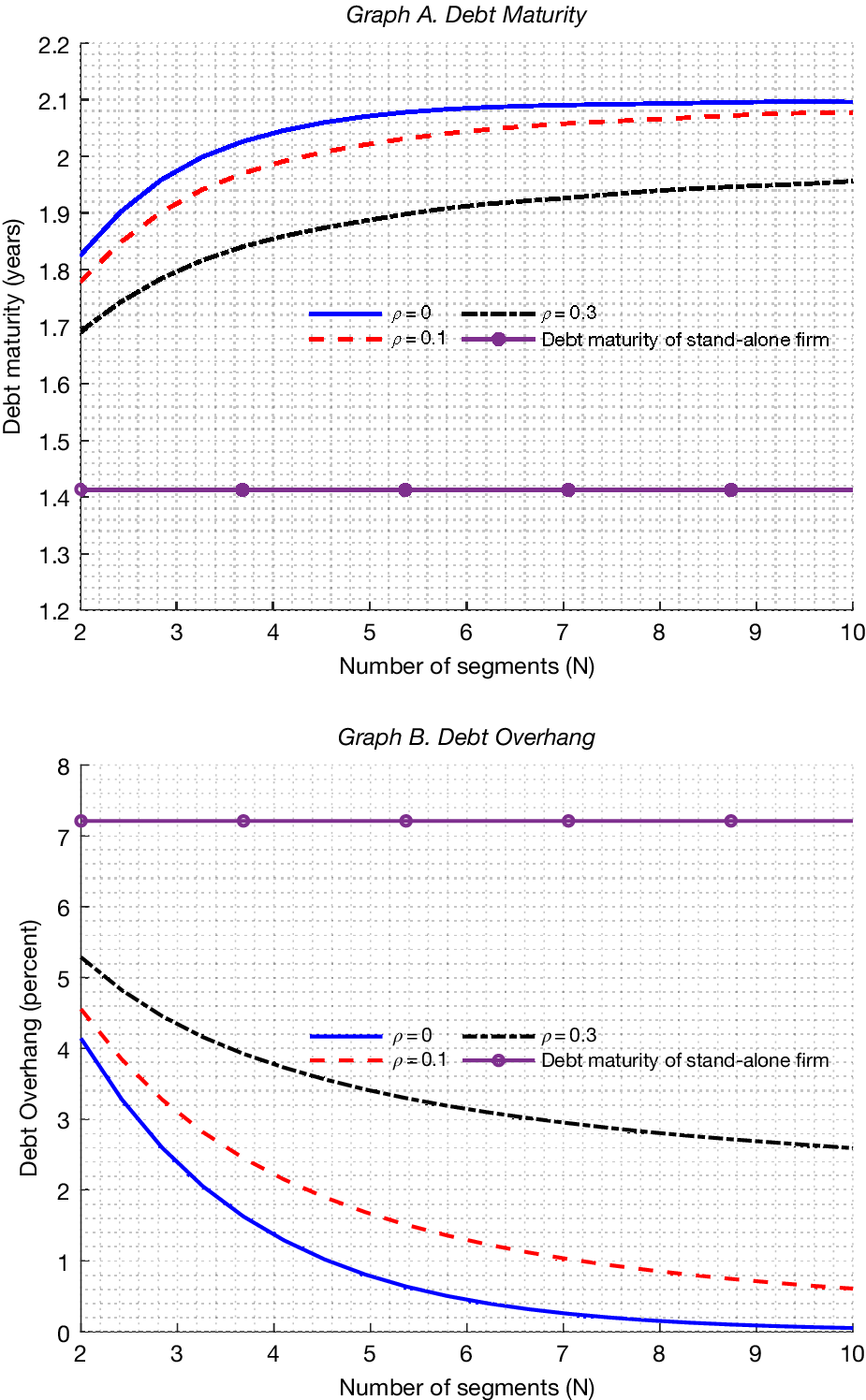

The numerical results are shown in Figure 4. From Graph A of Figure 4, we can clearly see that, given the same values of total assets-in-place, face value of debt, growth rate, and market value of equity,

$ M $

’s debt maturity is longer than that of

$ M $

’s debt maturity is longer than that of

$ S $

and increases with the number of segments, confirming the notion stated in Proposition 1 that

$ S $

and increases with the number of segments, confirming the notion stated in Proposition 1 that

$ M $

tend to issue long-term debt relative to

$ M $

tend to issue long-term debt relative to

$ S $

. This tendency becomes stronger as the number of segments grows. Graph B of Figure 4 shows the changing pattern of debt overhang with the increasing number of segments. The pattern matches nicely with the results in Section II that corporate diversification reduces debt overhang. We also find that as the average pairwise correlation between divisions decreases, the debt maturity increases and the debt overhang decreases even further. This observation reinforces the idea from Section II that corporate diversification increases debt maturity and mitigates debt overhang via the coinsurance effect.

$ S $

. This tendency becomes stronger as the number of segments grows. Graph B of Figure 4 shows the changing pattern of debt overhang with the increasing number of segments. The pattern matches nicely with the results in Section II that corporate diversification reduces debt overhang. We also find that as the average pairwise correlation between divisions decreases, the debt maturity increases and the debt overhang decreases even further. This observation reinforces the idea from Section II that corporate diversification increases debt maturity and mitigates debt overhang via the coinsurance effect.

Graph A (Graph B) of Figure 4 plots debt maturity (debt overhang) against the number of segments. The numerical values for the parameters are set as follows:

$ {g}_i=r=5\% $

,

$ {g}_i=r=5\% $

,

$ {\sigma}_i=0.4 $

,

$ {\sigma}_i=0.4 $

,

$ V=100 $

,

$ V=100 $

,

$ {v}_i=\frac{100}{N} $

, and

$ {v}_i=\frac{100}{N} $

, and

$ L=60 $

. The three curves in Graph A (Graph B) represent debt maturity (debt overhang) with three pairwise correlation levels (

$ L=60 $

. The three curves in Graph A (Graph B) represent debt maturity (debt overhang) with three pairwise correlation levels (

$ \rho =0,\ 0.1, $

and

$ \rho =0,\ 0.1, $

and

$ 0.3 $

). The debt maturity and overhang of the comparable stand-alone firm are also plotted for reference purposes.

$ 0.3 $

). The debt maturity and overhang of the comparable stand-alone firm are also plotted for reference purposes.

So far, the analysis using the basket option approach mirrors Section II.B with enhanced flexibility in modeling. However, we have not taken into account the maturity-sensitive noninterest debt expenses. Next, we consider the costs (analogous to Section II.C) and demonstrate that the intuition of Proposition 1 on the long-term debt and short-term debt separation in multi-division firms and stand-alone firms can also be shown under the basket option approach. Specifically, we use an exponential function to capture the maturity-sensitive noninterest debt expenses and extend the overhang-adjusted NPV in equation (12) to the following overhang and cost-adjusted NPVFootnote 22:

$$ R\left(N,t\right)=\left\{1-O\left(N,t,W\right)-\left[1+\exp \left(- bt\right)\right]\lambda \right\}\varepsilon, $$

$$ R\left(N,t\right)=\left\{1-O\left(N,t,W\right)-\left[1+\exp \left(- bt\right)\right]\lambda \right\}\varepsilon, $$

where the cost function

$ \exp \left(- bt\right) $

, with the maturity-sensitivity parameter

$ \exp \left(- bt\right) $

, with the maturity-sensitivity parameter

$ b>0 $

, captures the negative correlation between noninterest debt expenses and maturity. Setting

$ b>0 $

, captures the negative correlation between noninterest debt expenses and maturity. Setting

$ b=2.4 $

,

$ b=2.4 $

,

$ \lambda =0.4 $

,

$ \lambda =0.4 $

,

$ \rho =0 $

, and

$ \rho =0 $

, and

$ N=6 $

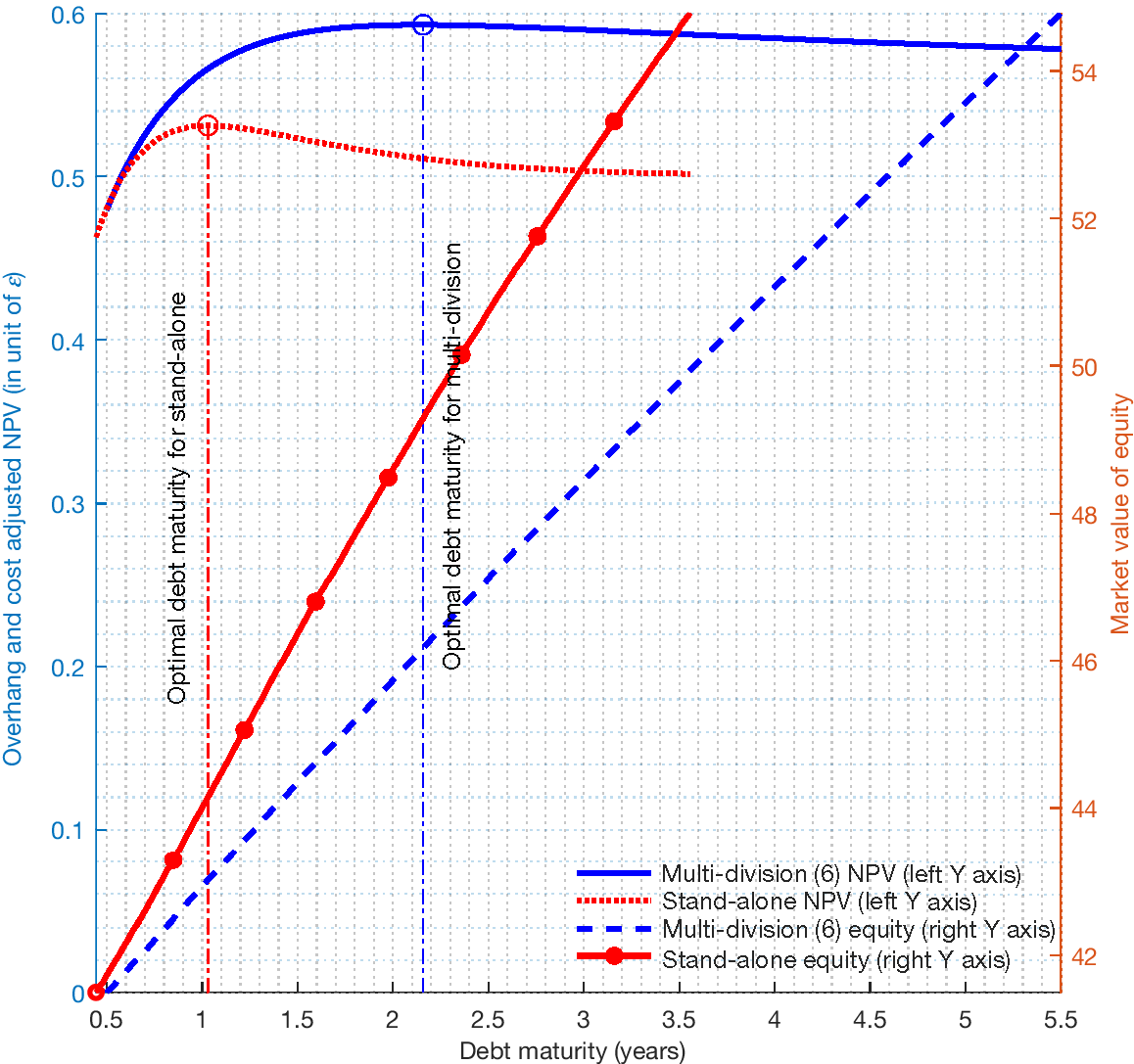

alongside other numerical values already set in Figure 4, we present in Figure 5 an example of long-term debt and short-term debt separation consistent with Proposition 1. Maximizing the overhang-adjusted NPV in equation (22), there are cases where stand-alone firms’ optimal debt maturity is shorter than that of multi-division firms, when all else is equal. Figure 5 (x-axis and left y-axis) presents an example of such cases.

$ N=6 $

alongside other numerical values already set in Figure 4, we present in Figure 5 an example of long-term debt and short-term debt separation consistent with Proposition 1. Maximizing the overhang-adjusted NPV in equation (22), there are cases where stand-alone firms’ optimal debt maturity is shorter than that of multi-division firms, when all else is equal. Figure 5 (x-axis and left y-axis) presents an example of such cases.

The left y-axis in Figure 5 visually compares the overhang and cost-adjusted NPVs, given various debt maturities of the multi-division firm with those of the comparable stand-alone firm. The right y-axis visually compares the corresponding market values of equity of the multi-division firm with those of the comparable stand-alone firm. The numerical values for the parameters are set as follows:

$ {g}_i=r=5\% $

,

$ {g}_i=r=5\% $

,

$ {\sigma}_i=0.4 $

,

$ {\sigma}_i=0.4 $

,

$ N=6 $

,

$ N=6 $

,

$ V=100 $

,

$ V=100 $

,

$ {v}_i=\frac{100}{6} $

,

$ {v}_i=\frac{100}{6} $

,

$ L=60 $

, and

$ L=60 $

, and

$ {\rho}_{i,j}=0 $

.

$ {\rho}_{i,j}=0 $

.

C. Endogenous Debt Maturity in Corporate Diversification

We investigate how corporate diversification affects debt maturity and overhang by constraining the multi-division firm’s book value of debt to be the same as that of the stand-alone firm. This is intentional and consistent with Admati et al.’s (Reference Admati, DeMarzo, Hellwig and Pfleiderer2018) leverage ratchet effect—where shareholders resist book leverage reductions—and is confirmed empirically by Berger and Ofek (Reference Berger and Ofek1995), who document that there is no economically significant difference between the book leverage of multi-division and stand-alone firms. This controlled setting allows us to isolate the impact of corporate diversification on debt maturity and overhang while holding other determinants of firm value constant.

The coinsurance effect of corporate diversification on firm risk is well understood in the corporate diversification discount literature, but there is currently no formal investigation of its potential effects on debt maturity and overhang. There is, however, some evidence suggesting that corporate diversification might benefit debt holders relative to shareholders in levered firms. Specifically, Mansi and Reeb (Reference Mansi and Reeb2002) study the risk effects of corporate diversification and its impact on firm value in levered and all-equity firms. In all-equity firms, there is no corporate diversification discount, while in levered firms, shareholders’ losses due to corporate diversification increase with leverage. Moreover, the overall impact of corporate diversification on excess firm value tends to be negligible in levered firms. Thus, these results suggest that the coinsurance effect reduces the market value of equity and enhances the market value of debt in levered firms. Mansi and Reeb’s (Reference Mansi and Reeb2002) argument is essentially a restatement of a potential consequence of corporate diversification that has been put forward in earlier contributions, such as Higgins and Schall (Reference Higgins and Schall1975), Galai and Masulis (Reference Galai and Masulis1976), and Kim and McConnell (Reference Kim and McConnell1977). The coinsurance effect of corporate diversification may result in a wealth transfer from shareholders to debt holders. However, the implicit assumption in Mansi and Reeb (Reference Mansi and Reeb2002) is that when firms diversify, they maintain the same maturity and face value of debt. This is not necessarily the case in real capital markets.

Figure 5 illustrates the effect of corporate diversification on the market value of debt and equity for a given value of debt maturity. Specifically, the right y-axis in Figure 5 shows the market values of the stand-alone firm and the comparable multi-division firm. Assuming a debt maturity of 1 year for both firms, the market equity value of the multi-division firm is about 43, whereas that of the stand-alone firm is about 44. This result verifies Mansi and Reeb’s (Reference Mansi and Reeb2002) hypothesis: conditional on the assumption of the same debt maturity, the market value of equity for a stand-alone firm (red straight line in the graph) is higher than that of a multi-division firm (blue dashed straight line in the graph). However, this is a strong assumption in a world of imperfect ‘me-first’ rules where the shareholders control the investment decision (Galai and Masulis (Reference Galai and Masulis1976), Kim and McConnell (Reference Kim and McConnell1977)).

Now, let us consider what happens if we relax the assumption of constant debt maturity. The shareholders of the multi-division firm can increase the NPV of their investments (adjusted for debt overhang and investment cost) by choosing a longer debt maturity, as shown on the left y-axis of Figure 5. For example, choosing a debt maturity of 2.2 years—the optimal debt maturity maximizing the adjusted NPV for the multi-division firm in Figure 5—increases the market value of equity from about 43 (for 1-year maturity) to over 46. The optimal debt maturity (i.e., the debt maturity that maximizes the adjusted NPV) for the stand-alone firm is 1 year, which corresponds to a market value of equity of about 44. If both firms can choose their optimal debt maturity to maximize the adjusted NPV of their investments, diversifying can actually result in a premium. In other words, corporate diversification does not necessarily lead to a lower equity value if firms can increase their debt maturity when they decide to diversify, and increasing the debt maturity could lead to a diversification premium.

D. Implications for Corporate Diversification Discount and Premium

These results bear major implications on the interpretation of previous findings related to the existence of a diversification discount: if multi-division firms tend to have longer debt maturity than stand-alone firms—as we show below in our empirical exercise—due to the coinsurance effect, traditional measures of corporate diversification discount (Berger and Ofek (Reference Berger and Ofek1995), Mansi and Reeb (Reference Mansi and Reeb2002)) could be misleading. Our analysis here predicts that the debt maturity of multi-division firms can explain the traditional excess value measures (see Mansi and Reeb ((Reference Mansi and Reeb2002), equation (1))). Specifically, the benchmark used in conventional excess value measures is the sum of the market values of median stand-alone firms in each relevant industry segment. That is, for a multi-division firm

$ i $

with

$ i $

with

$ m $

divisions, conventional excess value is measured as follows:

$ m $

divisions, conventional excess value is measured as follows:

$$ {V}_i^m-\sum \limits_{j=1}^m\mathrm{M}\mathrm{d}\mathrm{n}\{{V}_k^s,k\in j\mathrm{t}\mathrm{h}\ \mathrm{s}\mathrm{e}\mathrm{c}\mathrm{t}\mathrm{o}\mathrm{r}\}, $$

$$ {V}_i^m-\sum \limits_{j=1}^m\mathrm{M}\mathrm{d}\mathrm{n}\{{V}_k^s,k\in j\mathrm{t}\mathrm{h}\ \mathrm{s}\mathrm{e}\mathrm{c}\mathrm{t}\mathrm{o}\mathrm{r}\}, $$

where

$ {V}_i^m $

is the value of firm

$ {V}_i^m $