I. Introduction

The COVID-19 pandemic once again underscored the central role of monetary policy in stabilizing the economy, supporting consumption, investment, and production, while calming financial and credit markets. Beyond its stabilizing function, monetary policy is also a key driver of asset prices and risk premia (see, e.g., Savor and Wilson (Reference Savor and Wilson2014), Lucca and Moench (Reference Lucca and Moench2015), Neuhierl and Weber (Reference Neuhierl and Weber2018), and Ozdagli and Velikov (Reference Ozdagli and Velikov2020)). Nominal price rigidity—the inability of firms to adjust output prices immediately to nominal shocks—is the leading mechanism through which monetary policy affects the real economy. Price stickiness matters not only for aggregate transmission but also for explaining cross-sectional differences in firms’ responses to shocks. Recent studies using microdata from official price statistics show that firm-level price rigidity correlates with stock returns, leverage choices, and the transmission of fiscal and monetary policy.Footnote 1 However, little is known about how output price stickiness shapes firms’ credit risk, cash holdings, or debt structure.

We develop a capital structure model to examine how price stickiness shapes firms’ financing choices and credit risk. Firms produce differentiated goods using a risky technology, financed through short- and long-term debt, equity, and cash. They optimally choose leverage and debt maturity by balancing the tax benefits of debt against bankruptcy costs. To avoid default, firms may issue seasoned equity, subject to flotation costs, and hold cash to buffer adverse shocks, despite agency costs. Crucially, firms differ in their ability to adjust output prices. This heterogeneity in price rigidity affects operating flexibility and thereby default risk. Our model yields several testable predictions. Firms with more flexible output prices tend to have higher leverage and a greater reliance on long-term debt, while holding less precautionary cash, facing lower borrowing costs, and being subject to less stringent debt covenants. In addition, the cost of debt for sticky-price firms is more sensitive to monetary policy shocks (MPSs) and rises more sharply in response to exogenous increases in cash flow volatility, both through default risk and risk premium channels.

To test these predictions, we use micro-level data from the Bureau of Labor Statistics’ (BLS) Producer Price Index (PPI) to construct measures of nominal price rigidity. We merge these with financial data from CRSP and Compustat, cost of debt information from Mergent FISD and TRACE, and loan covenant data from Thomson Reuters LPC DealScan. We first show that firms with the stickiest prices hold significantly more precautionary cash. Inflexible-price firms, on average, maintain cash buffers about 22% larger than their flexible-price counterparts. This result remains robust after controlling for standard determinants of cash holdings, unobserved macroeconomic and financial risk factors, and industry-specific characteristics. Next, we test how debt characteristics vary with nominal output price rigidity. Sticky-price firms face higher issuance credit spreads, making debt more costly, and their bonds trade at lower prices in secondary markets. On average, these firms also have shorter debt maturity and tighter loan covenants.

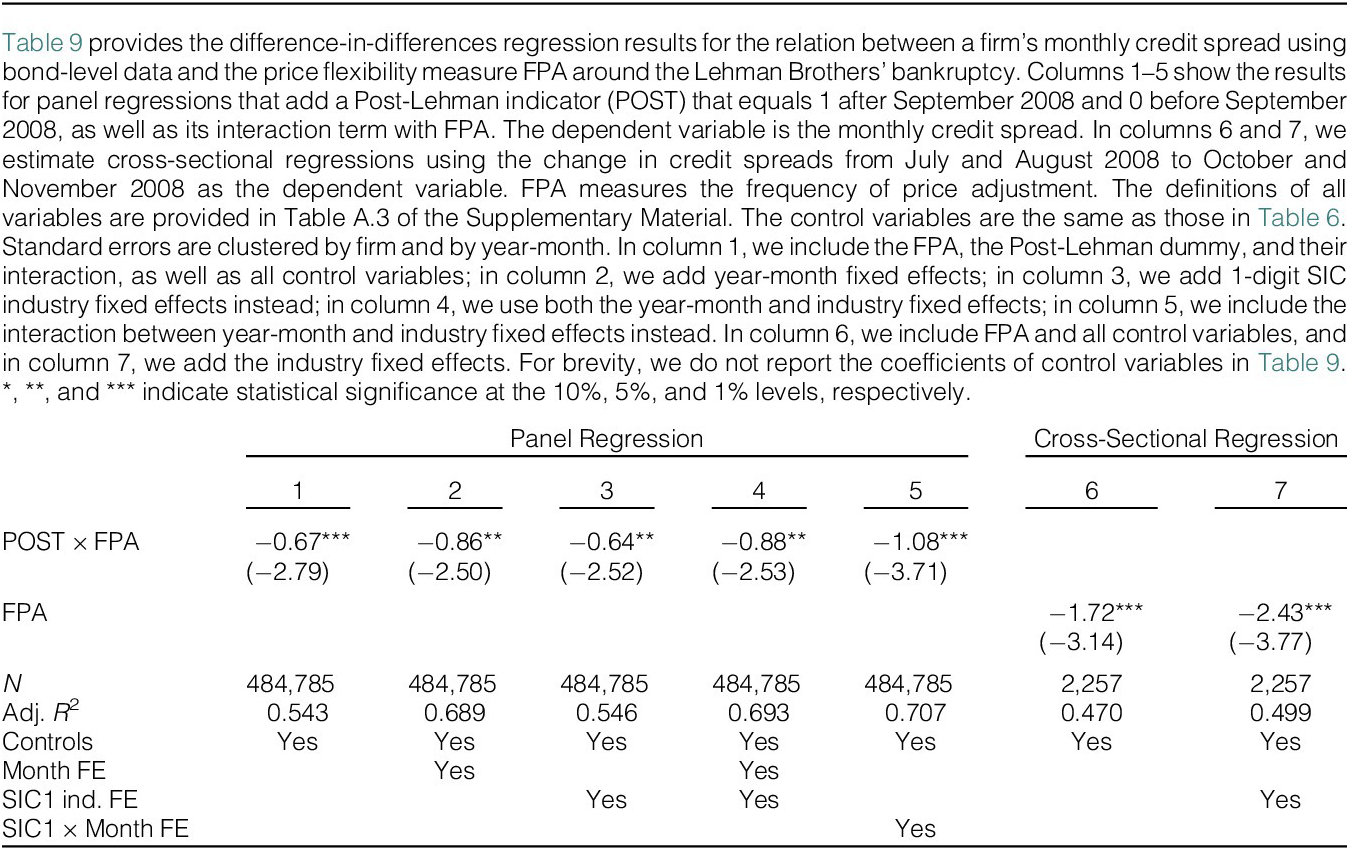

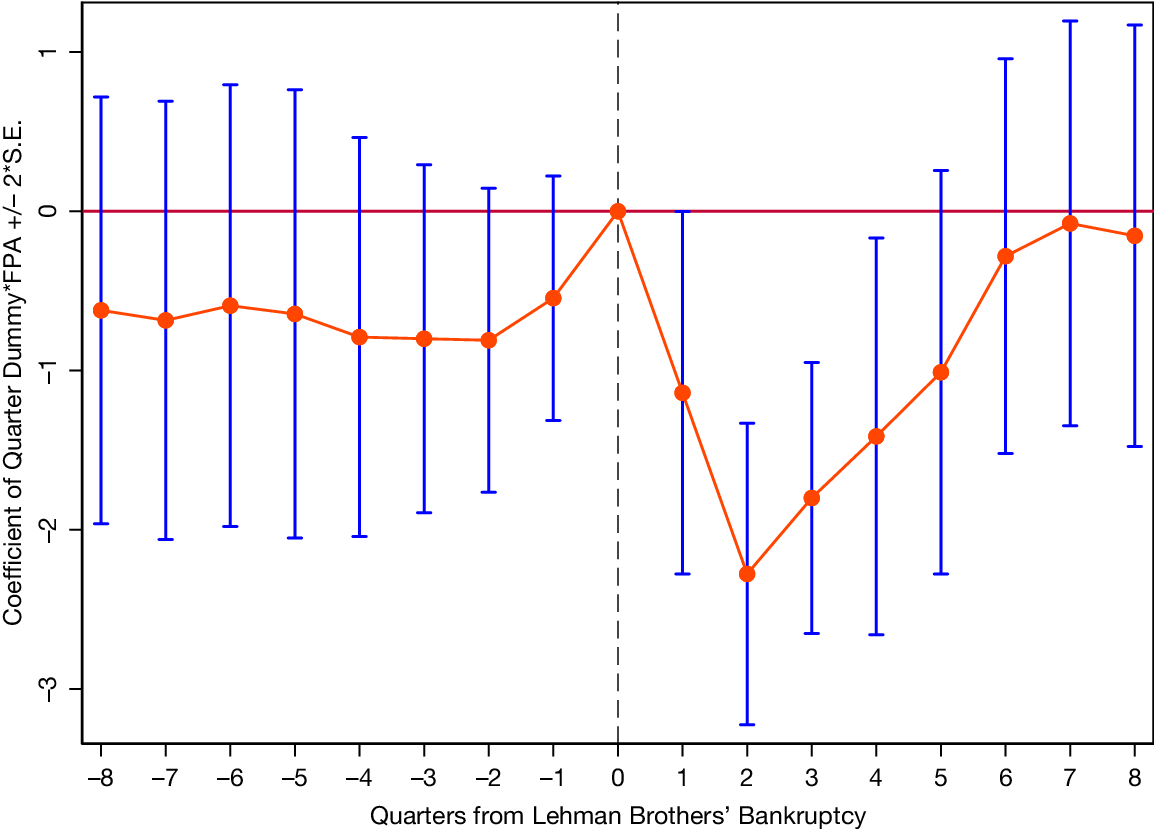

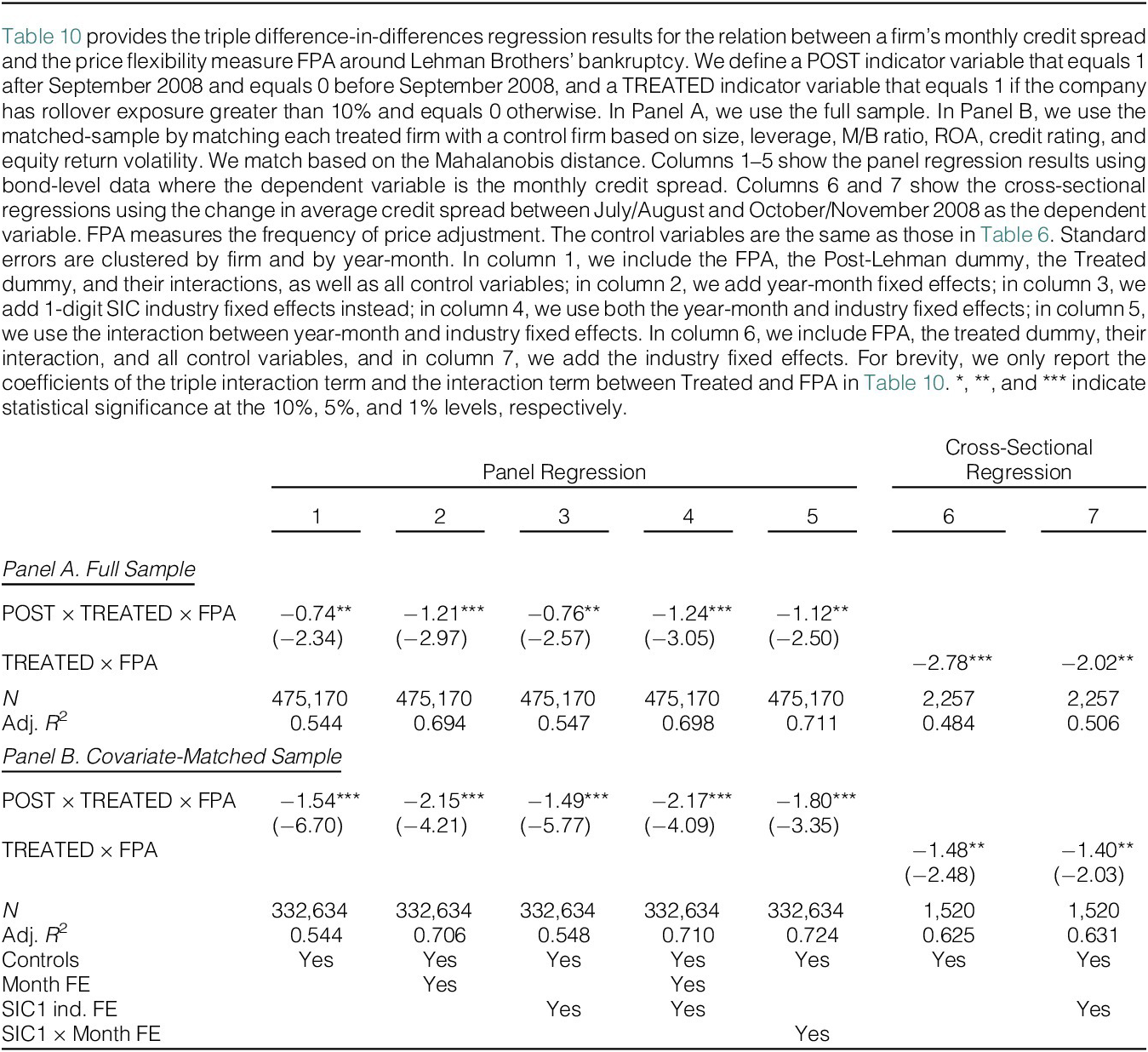

After documenting unconditional differences, we examine how firms respond to shocks. We show that nominal rigidities shape the transmission of monetary policy to asset prices and firm behavior. Using the MPS measure of Gorodnichenko and Weber (Reference Gorodnichenko and Weber2016), we analyze how squared credit spreads of flexible- and inflexible-price firms respond to monetary surprises. A hypothetical 25- basis-point (bps) shock increases conditional credit spread volatility by about 9 bps more for fully sticky-price firms than for fully flexible-price firms. Second, our framework predicts that credit spreads respond more strongly to uncertainty shocks (e.g., volatility of cash flows or profitability) for firms with greater nominal price rigidity. To test this prediction, we use the 2008 Lehman Brothers bankruptcy, an unexpected and severe uncertainty shock, as in Chodorow-Reich (Reference Chodorow-Reich2014) and Ivashina and Scharfstein (Reference Ivashina and Scharfstein2010). As the largest bankruptcy in U.S. history, it surprised market participants and triggered the Dow Jones’ biggest point drop since the Sept. 11, 2001 attacks. Consistent with the model’s predictions, credit spreads of inflexible-price firms rose significantly more than those of flexible-price firms following the Lehman Brothers collapse. Using bond-level data, the immediate differential increase, from 2 months before to 2 months after the shock, ranges from 172 to 243 bps.

Third, we refine our analysis by exploiting cross-sectional variation in firms’ financial constraints. The model predicts that sticky-price firms with higher refinancing costs should see a larger increase in credit spreads in response to uncertainty shocks. We test this prediction using exposure to rollover risk (He and Xiong (Reference He and Xiong2012)) around the Lehman Brothers bankruptcy in a triple-difference specification. All else equal, firms with refinancing needs when credit spreads spiked after the bankruptcy likely faced higher refinancing costs. Prior studies, including Almeida, Campello, Laranjeira, and Weisbenner (Reference Almeida, Campello, Laranjeira and Weisbenner2011) and Nagler (Reference Nagler2020), show that rollover risk is a predetermined channel amplifying credit risk. We measure rollover risk as the share of debt maturing in 2009. Consistent with the model, inflexible-price firms with high rollover risk experienced significantly larger increases in credit spreads following the Lehman collapse.

Taken together, the evidence supports our model’s predictions and shows that output price rigidity is a key determinant of firms’ financial policies and credit risk, as well as a central channel through which monetary policy affects asset prices.

We contribute to the literature on nominal rigidities and financial outcomes. Using PPI micro data in high-frequency event studies around Federal Open Market Committee (FOMC) announcements, Gorodnichenko and Weber (Reference Gorodnichenko and Weber2016) provide evidence consistent with a New Keynesian view of price stickiness. Weber (Reference Weber2015) shows that sticky-price firms earn a 4% return premium annually in the cross section of stock returns, while D’Acunto et al. (Reference D’Acunto, Liu, Pflueger and Weber2018) link price stickiness to persistent differences in financial leverage across firms. Our key contribution is to show that output price stickiness influences firms’ credit risk, cash holdings, and debt structure, spanning maturity, pricing, and covenants. We document a persistent wedge in issuance and secondary market credit spreads between flexible- and sticky-price firms. Sticky-price firms also exhibit greater sensitivity to uncertainty shocks. This heightened sensitivity drives higher precautionary cash holdings, prompting creditors to demand tighter covenants and shorter debt maturity.

While New Keynesian models emphasize price stickiness in transmitting nominal shocks, wage rigidities can similarly affect firms through labor costs. Recent work shows that cross-industry variation in wage rigidity and labor shares drives return predictability, credit risk, and helps explain asset pricing puzzles (Belo, Lin, and Bazdresch (Reference Belo, Lin and Bazdresch2014), Favilukis and Lin (Reference Favilukis and Lin2016a), (2016Reference Favilukis and Linb), Favilukis, Lin, and Zhao (Reference Favilukis, Lin and Zhao2020), and Belo, Donangelo, Lin, and Luo (Reference Belo, Donangelo, Lin and Luo2023)). Like these studies, we examine rigidities in financial markets, but focus on nominal frictions on the revenue side rather than real frictions on the cost side. Robustness tests confirm that wage and price stickiness are both important and complementary drivers of credit risk.Footnote 2

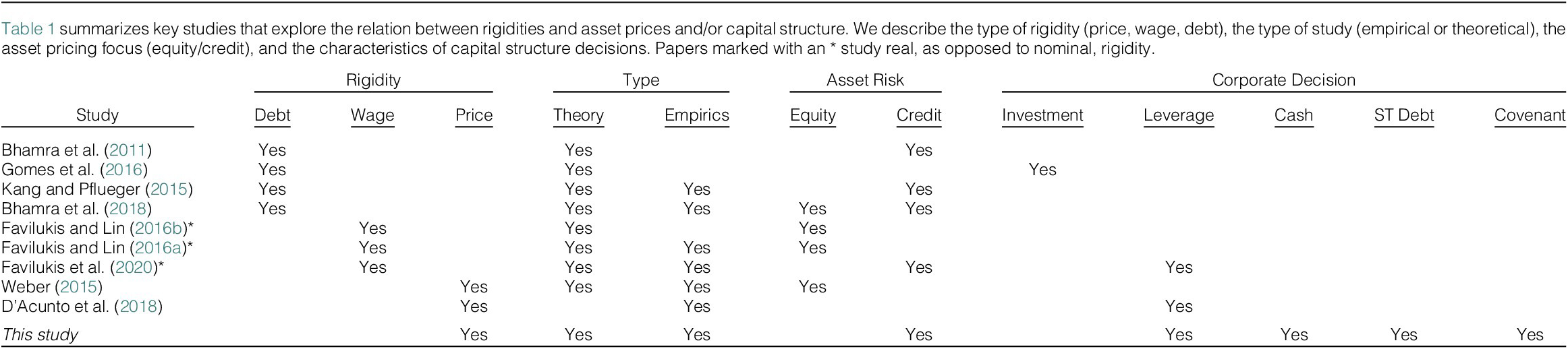

Our article also relates to studies on the role of sticky leverage in shaping credit risk. Bhamra, Fisher, and Kuehn (Reference Bhamra, Fisher and Kuehn2011), Kang and Pflueger (Reference Kang and Pflueger2015), and Gomes, Jermann, and Schmid (Reference Gomes, Jermann and Schmid2016) model how nominal debt contracts affect credit risk following unexpected price level changes. Corhay and Tong (Reference Corhay and Tong2026) show that sticky leverage can disrupt aggregate credit supply when financial intermediaries are constrained, while Bhamra, Dorion, Jeanneret, and Weber (Reference Bhamra, Dorion, Jeanneret and Weber2018) examine how sticky leverage and cash flows jointly influence credit risk and equity valuations.Footnote 3 Table 1 highlights our contribution. In contrast to these studies, we focus on how sticky output prices affect credit risk and provide new evidence on the pricing and structure of debt across firms. In related work, Gu, Hackbarth, and Johnson (Reference Gu, Hackbarth and Johnson2018) and Gu, Hackbarth, and Li (Reference Gu, Hackbarth and Li2019) examine how scale irreversibility influences firm risk and leverage. Like them, we show that firm-level frictions shape exposure to aggregate risk and influence risk pricing in financial markets.

Our focus on nominal price rigidities and credit risk also contributes to the extensive literature on credit spread determinants (e.g., Merton (Reference Merton1974), Collin-Dufresne, Goldstein, and Martin (Reference Collin-Dufresne, Goldstein and Martin2001), Campbell and Taksler (Reference Campbell and Taksler2003), Blanco, Brennan, and Marsh (Reference Blanco, Brennan and Marsh2005), Chen, Lesmond, and Wei (Reference Chen, Lesmond and Wei2007), Bharath and Shumway (Reference Bharath and Shumway2008), Zhang, Zhou, and Zhu (Reference Zhang, Zhou and Zhu2009), Bongaerts, De Jong, and Driessen (Reference Bongaerts, De Jong and Driessen2011), Acharya, Amihud, and Bharath (Reference Acharya, Amihud and Bharath2013b), Corhay (Reference Corhay2017), Siriwardane (Reference Siriwardane2019), Augustin and Izhakian (Reference Augustin and Izhakian2020), and Chen, Dou, Guo, and Ji (Reference Chen, Dou, Guo and Ji2026)). We show that firms’ inability to adjust output prices creates a persistent wedge in the cost of debt between sticky- and flexible-price firms. We also find that sticky-price firms hold more cash, reflecting their heightened sensitivity to cash flow shocks. This result connects to research on precautionary savings driven by elevated credit risk (e.g., Bolton, Chen, and Wang (Reference Bolton, Chen and Wang2014)), as well as studies showing that firms facing stricter creditors (Subrahmanyam, Tang, and Wang (Reference Subrahmanyam, Tang and Wang2017)) or greater refinancing risk (Harford, Klasa, and Maxwell (Reference Harford, Klasa and Maxwell2014)) tend to hold more cash. Our findings also align with evidence that firms prefer cash to credit lines for liquidity management (Acharya, Davydenko, and Strebulaev (Reference Acharya, Davydenko and Strebulaev2012), Acharya, Almeida, and Campello (Reference Acharya, Almeida and Campello2013a)). Lin, Schmid, and Weisbach (Reference Lin, Schmid and Weisbach2021) show that greater production price risk is associated with higher cash holdings in the electricity sector. We complement their work by grounding our analysis in a theoretical framework and focusing on output-price flexibility rather than production technology. Unlike their industry-specific study, we measure price adjustment frequency across a broad set of firms and industries. In addition to cash holdings, we also examine how price stickiness relates to debt maturity, borrowing costs, and covenant tightness.

Finally, we build on a large macroeconomic literature examining the determinants and implications of output price stickiness. Zbaracki, Ritson, Levy, Dutta, and Bergen (Reference Zbaracki, Ritson, Levy, Dutta and Bergen2004) estimate that nominal price adjustments cost a major U.S. manufacturer 1.22% of total revenue and 20.03% of net profit. Using Consumer Price Index (CPI) microdata, Bils and Klenow (Reference Bils and Klenow2004) and Nakamura and Steinsson (Reference Nakamura and Steinsson2008) show that prices are typically fixed for about 6 months, with substantial cross-industry variation, findings confirmed for producer prices by Goldberg and Hellerstein (Reference Goldberg and Hellerstein2011). Other contributions include Eichenbaum, Jaimovich, and Rebelo (Reference Eichenbaum, Jaimovich and Rebelo2011), Anderson, Jaimovich, and Simester (Reference Anderson, Jaimovich and Simester2015), and Kehoe and Midrigan (Reference Kehoe and Midrigan2015). More recent work by Pasten et al. (Reference Pasten, Schoenle and Weber2020), (Reference Pasten, Schoenle and Weber2024) and Cox, Müller, Pasten, Schoenle, and Weber (Reference Cox, Müller, Pasten, Schoenle and Weber2024) explores how heterogeneity in price stickiness affects the transmission of idiosyncratic, monetary, and fiscal shocks. See Klenow and Malin (Reference Klenow, Malin, Friedman and Woodford2010) for a review of the recent literature on price rigidity using micro price data.

II. Model

This section presents a partial equilibrium model that illustrates how price stickiness shapes firms’ financing decisions and credit risk. Greater price rigidity reduces operational flexibility, making sticky-price firms more exposed to adverse shocks and thus riskier. In equilibrium, price stickiness results in lower leverage, higher precautionary cash holdings, a greater default probability, wider credit spreads, and shorter debt maturity. Because debt covenants help mitigate shareholder–creditor agency conflicts, firms with inflexible output prices face tighter covenants than those with flexible prices.

A. Economic Environment

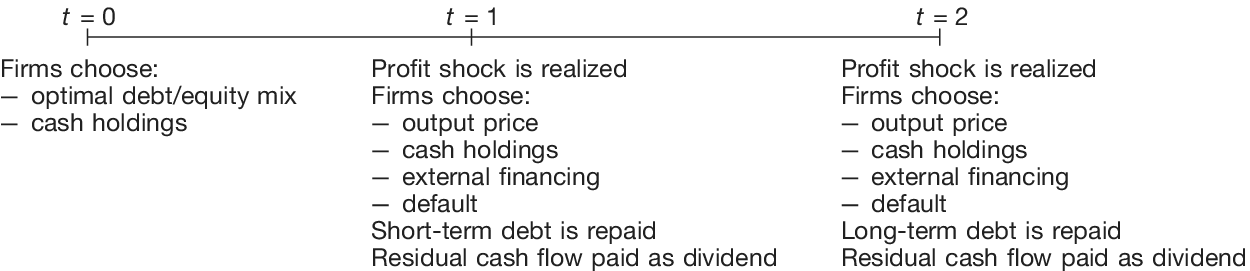

The economy consists of a continuum of firms operating a linear production technology over three periods. Firms differ in their ability to adjust nominal output prices, governed by their degree of price stickiness. A representative investor holds all claims with preferences captured by an exogenous pricing kernel. Figure 1 outlines the sequence of events.

Figure 1 illustrates the timeline of the firm’s decision-making process. At

$ t=0 $

, firms choose their optimal capital structure, including equity, debt, and precautionary cash holdings. At

$ t=0 $

, firms choose their optimal capital structure, including equity, debt, and precautionary cash holdings. At

$ t=1 $

, the first IID profit shock is realized. Firms revise output prices with probability

$ t=1 $

, the first IID profit shock is realized. Firms revise output prices with probability

$ 1-\theta $

, determine production capacity, and decide whether to adjust cash holdings, raise external equity, or default. If no default occurs, short-term debt is repaid, and residual cash flows are paid as dividends. At

$ 1-\theta $

, determine production capacity, and decide whether to adjust cash holdings, raise external equity, or default. If no default occurs, short-term debt is repaid, and residual cash flows are paid as dividends. At

$ t=2 $

, a second IID profit shock is realized. As in

$ t=2 $

, a second IID profit shock is realized. As in

$ t=1 $

, firms may revise prices with probability

$ t=1 $

, firms may revise prices with probability

$ \left(1-\theta \right) $

, set production, adjust cash, issue equity, or default. If solvent, they repay long-term debt and distribute remaining cash flows as dividends.

$ \left(1-\theta \right) $

, set production, adjust cash, issue equity, or default. If solvent, they repay long-term debt and distribute remaining cash flows as dividends.

At

$ t=0 $

, firms raise financing through equity, one-period and two-period debt, and choose precautionary cash holdings to buffer against future shocks. At

$ t=0 $

, firms raise financing through equity, one-period and two-period debt, and choose precautionary cash holdings to buffer against future shocks. At

$ t=1 $

, each firm observes its idiosyncratic productivity shock along with all aggregate shocks, then chooses its production level and nominal price. Price setting is inflexible, as firms face a positive probability of being unable to adjust prices in response to shocks. The firm repays its one-period debt, may update its cash holdings, and, if short on cash, can issue new equity or default. Any residual free cash flow is paid out as dividends to shareholders. At

$ t=1 $

, each firm observes its idiosyncratic productivity shock along with all aggregate shocks, then chooses its production level and nominal price. Price setting is inflexible, as firms face a positive probability of being unable to adjust prices in response to shocks. The firm repays its one-period debt, may update its cash holdings, and, if short on cash, can issue new equity or default. Any residual free cash flow is paid out as dividends to shareholders. At

$ t=2 $

, surviving firms experience a second idiosyncratic productivity shock together with aggregate shocks. They choose output prices (subject to price rigidity), realize profits, and decide whether to default. If solvent, the firm repays its long-term debt and distributes remaining cash flows to shareholders as dividends. The firm then exits the market.

$ t=2 $

, surviving firms experience a second idiosyncratic productivity shock together with aggregate shocks. They choose output prices (subject to price rigidity), realize profits, and decide whether to default. If solvent, the firm repays its long-term debt and distributes remaining cash flows to shareholders as dividends. The firm then exits the market.

1. Production

Each firm

$ i $

operates a linear production technology that produces output

$ i $

operates a linear production technology that produces output

$ {y}_{it}^s $

using a predetermined capital stock

$ {y}_{it}^s $

using a predetermined capital stock

$ {k}_{i0} $

and a variable input

$ {k}_{i0} $

and a variable input

$ {l}_{it} $

(e.g., labor), purchased in a competitive market at a real unit cost

$ {l}_{it} $

(e.g., labor), purchased in a competitive market at a real unit cost

$ W $

:

$ W $

:

$$ {y}_{it}^s={\tilde{X}}_{it}{k}_{i0}{l}_{it}. $$

$$ {y}_{it}^s={\tilde{X}}_{it}{k}_{i0}{l}_{it}. $$

Here,

$ {\tilde{X}}_{it} $

denotes a firm-specific IID log-normal productivity shock, with

$ {\tilde{X}}_{it} $

denotes a firm-specific IID log-normal productivity shock, with

$ \log \left({\tilde{X}}_{it}\right)\sim \mathcal{N}\left({\mu}_t,{\sigma}_t^2\right) $

. While realizations of

$ \log \left({\tilde{X}}_{it}\right)\sim \mathcal{N}\left({\mu}_t,{\sigma}_t^2\right) $

. While realizations of

$ {\tilde{X}}_{it} $

are unknown ex ante, their distribution is common knowledge and identical across firms. The conditional moments

$ {\tilde{X}}_{it} $

are unknown ex ante, their distribution is common knowledge and identical across firms. The conditional moments

$ {\mu}_t $

and

$ {\mu}_t $

and

$ {\sigma}_t $

may vary over time to capture aggregate productivity or uncertainty shocks (e.g., Bloom (Reference Bloom2009)). Let

$ {\sigma}_t $

may vary over time to capture aggregate productivity or uncertainty shocks (e.g., Bloom (Reference Bloom2009)). Let

$ \Phi \left(\cdot \right) $

and

$ \Phi \left(\cdot \right) $

and

$ \phi \left(\cdot \right) $

denote the cumulative distribution and probability density functions of the standard normal distribution, respectively.

$ \phi \left(\cdot \right) $

denote the cumulative distribution and probability density functions of the standard normal distribution, respectively.

The real demand for firm

$ i $

’s product,

$ i $

’s product,

$ {y}_{it}^d $

, depends on the nominal price

$ {y}_{it}^d $

, depends on the nominal price

$ {p}_{it} $

it charges relative to the aggregate price level

$ {p}_{it} $

it charges relative to the aggregate price level

$ {P}_t $

:

$ {P}_t $

:

$$ {y}_{it}^d={\left(\frac{p_{it}}{P_t}\right)}^{-\nu }, $$

$$ {y}_{it}^d={\left(\frac{p_{it}}{P_t}\right)}^{-\nu }, $$

where

$ \nu >1 $

denotes the elasticity of demand; higher values of

$ \nu >1 $

denotes the elasticity of demand; higher values of

$ \nu $

imply more elastic demand and thus less market power for the firm.

$ \nu $

imply more elastic demand and thus less market power for the firm.

Imposing the equilibrium condition

$ {y}_{it}^d={y}_{it}^s={y}_{it} $

, the firm’s real profit (normalized by

$ {y}_{it}^d={y}_{it}^s={y}_{it} $

, the firm’s real profit (normalized by

$ {P}_t $

) is defined as revenue net of operating costs:

$ {P}_t $

) is defined as revenue net of operating costs:

$$ {h}_{it}=\left(\frac{p_{it}}{P_t}\right){y}_{it}-{Wl}_{it}-{fk}_{i0}\times {\unicode{x1D7D9}}_{t=1}, $$

$$ {h}_{it}=\left(\frac{p_{it}}{P_t}\right){y}_{it}-{Wl}_{it}-{fk}_{i0}\times {\unicode{x1D7D9}}_{t=1}, $$

where

$ {p}_{it} $

is firm

$ {p}_{it} $

is firm

$ i $

’s nominal output price and

$ i $

’s nominal output price and

$ {P}_t $

is the aggregate price level. The term

$ {P}_t $

is the aggregate price level. The term

$ f $

denotes a fixed cost of maintaining the capital stock for the next period, incurred only in periods 0 and 1, since the firm operates for three periods. Without loss of generality, we normalize the initial capital stock

$ f $

denotes a fixed cost of maintaining the capital stock for the next period, incurred only in periods 0 and 1, since the firm operates for three periods. Without loss of generality, we normalize the initial capital stock

$ {k}_{i0} $

to one.

$ {k}_{i0} $

to one.

2. Price Stickiness

Following Calvo (Reference Calvo1983), we assume that at the start of each period, after all relevant shocks are realized, each firm faces an idiosyncratic shock

$ {\zeta}_{it}\in \left\{0,1\right\} $

that determines its ability to adjust output prices. If

$ {\zeta}_{it}\in \left\{0,1\right\} $

that determines its ability to adjust output prices. If

$ {\zeta}_{it}=1 $

, the firm can freely reoptimize and set a new price. If

$ {\zeta}_{it}=1 $

, the firm can freely reoptimize and set a new price. If

$ {\zeta}_{it}=0 $

, the firm must continue selling at the previous period’s price

$ {\zeta}_{it}=0 $

, the firm must continue selling at the previous period’s price

$ {p}_{it-1} $

. The conditional probability of not adjusting prices is denoted by

$ {p}_{it-1} $

. The conditional probability of not adjusting prices is denoted by

$ \theta \in \left[0,1\right] $

, which captures the degree of price rigidity. The limiting case

$ \theta \in \left[0,1\right] $

, which captures the degree of price rigidity. The limiting case

$ \theta =0 $

corresponds to fully flexible prices.

$ \theta =0 $

corresponds to fully flexible prices.

3. Financing

Debt: At

$ t=0 $

, the firm chooses its issuance of short- and long-term real debt. Short-term debt matures at

$ t=0 $

, the firm chooses its issuance of short- and long-term real debt. Short-term debt matures at

$ t=1 $

, whereas long-term debt matures at

$ t=1 $

, whereas long-term debt matures at

$ t=2 $

. Following Leland (Reference Leland1994), (Reference Leland1998), the firm commits to this initial debt schedule but may issue new equity in future periods. Equity holders retain the option to default when the equity value turns negative, with zero recovery for creditors.Footnote

4 These deadweight default costs raise the effective cost of debt financing relative to equity.

$ t=2 $

. Following Leland (Reference Leland1994), (Reference Leland1998), the firm commits to this initial debt schedule but may issue new equity in future periods. Equity holders retain the option to default when the equity value turns negative, with zero recovery for creditors.Footnote

4 These deadweight default costs raise the effective cost of debt financing relative to equity.

To ensure an interior solution for the optimal debt-equity mix at

$ t=0 $

, we assume that debt provides benefits to shareholders. For instance, interest payments are tax-deductible, offering an advantage over equity. However, tax benefits alone cannot fully explain observed leverage levels (e.g., Graham (Reference Graham2000)). More broadly, debt may also help mitigate agency and informational frictions, as argued by Myers and Majluf (Reference Myers and Majluf1984) and Jensen (Reference Jensen1986).

$ t=0 $

, we assume that debt provides benefits to shareholders. For instance, interest payments are tax-deductible, offering an advantage over equity. However, tax benefits alone cannot fully explain observed leverage levels (e.g., Graham (Reference Graham2000)). More broadly, debt may also help mitigate agency and informational frictions, as argued by Myers and Majluf (Reference Myers and Majluf1984) and Jensen (Reference Jensen1986).

Following Gourio (Reference Gourio2013) and Kang and Pflueger (Reference Kang and Pflueger2015), we capture the present value of debt benefits in reduced form by assuming that the firm receives

$ \left(1+{\chi}^S\right)>1 $

and

$ \left(1+{\chi}^S\right)>1 $

and

$ \left(1+{\chi}^L\right)>1 $

for each dollar of short- and long-term debt issued, respectively. Higher values of

$ \left(1+{\chi}^L\right)>1 $

for each dollar of short- and long-term debt issued, respectively. Higher values of

$ {\chi}^S $

and

$ {\chi}^S $

and

$ {\chi}^L $

increase the appeal of debt, raising leverage. Their difference determines the relative attractiveness of short- versus long-term debt and thus shapes the firm’s optimal maturity structure. In our numerical analysis, we calibrate these parameters jointly to match observed firm-level leverage and the ratio of long- to short-term debt.

$ {\chi}^L $

increase the appeal of debt, raising leverage. Their difference determines the relative attractiveness of short- versus long-term debt and thus shapes the firm’s optimal maturity structure. In our numerical analysis, we calibrate these parameters jointly to match observed firm-level leverage and the ratio of long- to short-term debt.

The total proceeds from debt issuance at time

$ t=0 $

are given by:

$ t=0 $

are given by:

$$ \left(1+{\chi}^S\right)\;{q}_{i0}^S{b}_i^S+\left(1+{\chi}^L\right)\;{q}_{i0}^L{b}_i^L, $$

$$ \left(1+{\chi}^S\right)\;{q}_{i0}^S{b}_i^S+\left(1+{\chi}^L\right)\;{q}_{i0}^L{b}_i^L, $$

where

$ {b}_i^S $

(

$ {b}_i^S $

(

$ {b}_i^L $

) is the amount of short-term (long-term) real debt issued, and

$ {b}_i^L $

) is the amount of short-term (long-term) real debt issued, and

$ {q}_{i0}^S $

(

$ {q}_{i0}^S $

(

$ {q}_{i0}^L $

) denotes its market price at

$ {q}_{i0}^L $

) denotes its market price at

$ t=0 $

.Footnote

5

$ t=0 $

.Footnote

5

Debt is issued in a competitive, rational lending market. Let

$ {\unicode{x1D7D9}}_{it}^{\mathrm{survival}} $

denote a survival indicator equal to 1 if firm

$ {\unicode{x1D7D9}}_{it}^{\mathrm{survival}} $

denote a survival indicator equal to 1 if firm

$ i $

does not default in period

$ i $

does not default in period

$ t $

, and 0 otherwise. The market value of debt equals the expected present value of future cash flows:

$ t $

, and 0 otherwise. The market value of debt equals the expected present value of future cash flows:

$$ {q}_{it}^S={\unicode{x1D53C}}_t\left[{M}_{t+1}\times {\unicode{x1D7D9}}_{it+1}^{\mathrm{survival}}\right],\hskip1em \mathrm{for}\;t=0,1, $$

$$ {q}_{it}^S={\unicode{x1D53C}}_t\left[{M}_{t+1}\times {\unicode{x1D7D9}}_{it+1}^{\mathrm{survival}}\right],\hskip1em \mathrm{for}\;t=0,1, $$

$$ {q}_{i0}^L={\unicode{x1D53C}}_0\left[{M}_1\times {q}_{i1}^S\right], $$

$$ {q}_{i0}^L={\unicode{x1D53C}}_0\left[{M}_1\times {q}_{i1}^S\right], $$

where

$ {M}_t $

denotes the real stochastic discount factor. The firm’s default decision is endogenous and determined by equity holders’ optimization problem, discussed in Section II.C.

$ {M}_t $

denotes the real stochastic discount factor. The firm’s default decision is endogenous and determined by equity holders’ optimization problem, discussed in Section II.C.

Equity: At time

$ t=0 $

, the firm can issue equity without cost. In subsequent periods, it may raise external equity at a cost

$ t=0 $

, the firm can issue equity without cost. In subsequent periods, it may raise external equity at a cost

$ \lambda $

per dollar issued (e.g., Jermann and Quadrini (Reference Jermann and Quadrini2012), Eisfeldt and Muir (Reference Eisfeldt and Muir2016)), capturing flotation costs or agency frictions (Hennessy and Whited (Reference Hennessy and Whited2007)). As shown in Section II.E, costly external financing creates a wedge between the shadow value of internal and external funds, inducing effective risk aversion and making precautionary cash holdings a key tool for mitigating financing frictions. Unlike debt holders, equity holders are entitled to residual cash flows and benefit from limited liability, allowing them to walk away with zero payout in the event of default.

$ \lambda $

per dollar issued (e.g., Jermann and Quadrini (Reference Jermann and Quadrini2012), Eisfeldt and Muir (Reference Eisfeldt and Muir2016)), capturing flotation costs or agency frictions (Hennessy and Whited (Reference Hennessy and Whited2007)). As shown in Section II.E, costly external financing creates a wedge between the shadow value of internal and external funds, inducing effective risk aversion and making precautionary cash holdings a key tool for mitigating financing frictions. Unlike debt holders, equity holders are entitled to residual cash flows and benefit from limited liability, allowing them to walk away with zero payout in the event of default.

Cash: Each period, firms decide whether to hold cash as a precaution against future productivity shocks. Holding cash can reduce future financing costs. To prevent firms from relying excessively on cash and thereby neutralizing financing frictions, we introduce an agency problem following Nikolov and Whited (Reference Nikolov and Whited2014), in which managers may divert free cash flows for private benefit. We model these agency costs in reduced form, similar to our treatment of debt benefits. Let

$ {x}_{it} $

denote the firm’s real cash balance at the end of period

$ {x}_{it} $

denote the firm’s real cash balance at the end of period

$ t $

. We assume the firm incurs a cost of

$ t $

. We assume the firm incurs a cost of

$ \frac{\psi {x}_{it}}{2} $

per dollar of cash held, where

$ \frac{\psi {x}_{it}}{2} $

per dollar of cash held, where

$ \psi >0 $

. The net cash flow associated with cash balances is then given by:

$ \psi >0 $

. The net cash flow associated with cash balances is then given by:

$$ {x}_{it-1}-{x}_{it}\left(1+\frac{\psi }{2}{x}_{it}\right). $$

$$ {x}_{it-1}-{x}_{it}\left(1+\frac{\psi }{2}{x}_{it}\right). $$

This specification implies a quadratic cost of holding cash, governed by the parameter

$ \psi $

. In our numerical analysis, we calibrate

$ \psi $

. In our numerical analysis, we calibrate

$ \psi $

to match the average cash holdings observed in the data.

$ \psi $

to match the average cash holdings observed in the data.

B. Objective Function

The firm’s objective is to maximize equity value by making a sequence of financing and production decisions, subject to product demand and fair debt pricing. For simplicity, we omit the

$ i $

-subscript unless needed for clarity.

$ i $

-subscript unless needed for clarity.

In period

$ t=0 $

, the entrepreneur is unlevered and does not produce. The problem reduces to choosing short- and long-term debt levels,

$ t=0 $

, the entrepreneur is unlevered and does not produce. The problem reduces to choosing short- and long-term debt levels,

$ {b}^S $

and

$ {b}^S $

and

$ {b}^L $

, and initial cash holdings

$ {b}^L $

, and initial cash holdings

$ {x}_0 $

, to maximize total proceeds from debt and equity issuanceFootnote

6:

$ {x}_0 $

, to maximize total proceeds from debt and equity issuanceFootnote

6:

$$ {\displaystyle \begin{array}{l}\underset{b^S,{b}^L,{x}_0}{\max}\left\{{\unicode{x1D53C}}_0\left[{M}_1{V}_1\left({\tilde{\zeta}}_1,{\tilde{X}}_1,{z}_1,{\Upsilon}_1\right)\right]-{x}_0-\frac{\psi }{2}{\left({x}_0\right)}^2\right.\\ {}\left.\hskip2em +\left(1+{\chi}^S\right){q}_0^S\Big({\tilde{\zeta}}_1,{\tilde{X}}_1,{z}_1,{\Upsilon}_1\left)\times {b}^S+\left(1+{\chi}^L\right){q}_0^L\right({\tilde{\zeta}}_1,{\tilde{X}}_1,{z}_1,{\Upsilon}_1\Big)\times {b}^L-f\right\},\end{array}} $$

$$ {\displaystyle \begin{array}{l}\underset{b^S,{b}^L,{x}_0}{\max}\left\{{\unicode{x1D53C}}_0\left[{M}_1{V}_1\left({\tilde{\zeta}}_1,{\tilde{X}}_1,{z}_1,{\Upsilon}_1\right)\right]-{x}_0-\frac{\psi }{2}{\left({x}_0\right)}^2\right.\\ {}\left.\hskip2em +\left(1+{\chi}^S\right){q}_0^S\Big({\tilde{\zeta}}_1,{\tilde{X}}_1,{z}_1,{\Upsilon}_1\left)\times {b}^S+\left(1+{\chi}^L\right){q}_0^L\right({\tilde{\zeta}}_1,{\tilde{X}}_1,{z}_1,{\Upsilon}_1\Big)\times {b}^L-f\right\},\end{array}} $$

subject to the breakeven conditions (5) and (6), which determine the equilibrium prices of short- and long-term debt, respectively.

The value of equity

$ {V}_1 $

and the debt prices

$ {V}_1 $

and the debt prices

$ {q}_0^S $

and

$ {q}_0^S $

and

$ {q}_0^L $

depend on a set of state variables summarized by the vector

$ {q}_0^L $

depend on a set of state variables summarized by the vector

$ \left({\tilde{\zeta}}_t,{\tilde{X}}_t,{z}_t,{\Upsilon}_t\right) $

. Here,

$ \left({\tilde{\zeta}}_t,{\tilde{X}}_t,{z}_t,{\Upsilon}_t\right) $

. Here,

$ {z}_t\equiv \left({b}^S,{b}^L,{x}_{t-1},{p}_{t-1}\right) $

captures firm-specific states, while

$ {z}_t\equiv \left({b}^S,{b}^L,{x}_{t-1},{p}_{t-1}\right) $

captures firm-specific states, while

$ {\Upsilon}_t $

denotes aggregate state variables. Accordingly, the firm internalizes how its financing decisions affect the market values of both equity and debt.

$ {\Upsilon}_t $

denotes aggregate state variables. Accordingly, the firm internalizes how its financing decisions affect the market values of both equity and debt.

In periods

$ t>0 $

, the firm chooses its production quantity, output price, and cash holdings

$ t>0 $

, the firm chooses its production quantity, output price, and cash holdings

$ {x}_t $

to maximize equity value. If the dividend is negative, the firm may issue seasoned equity, incurring a flotation cost

$ {x}_t $

to maximize equity value. If the dividend is negative, the firm may issue seasoned equity, incurring a flotation cost

$ \lambda $

. Alternatively, it declares bankruptcy when the firm value is negative. The firm faces two types of idiosyncratic uncertainty: A productivity shock

$ \lambda $

. Alternatively, it declares bankruptcy when the firm value is negative. The firm faces two types of idiosyncratic uncertainty: A productivity shock

$ {\tilde{X}}_t\in \left[0,+\infty \right) $

and a pricing shock

$ {\tilde{X}}_t\in \left[0,+\infty \right) $

and a pricing shock

$ {\zeta}_t\in \left\{0,1\right\} $

, along with a sequence of aggregate shocks. The real market value of equity satisfies the following recursive formulation for

$ {\zeta}_t\in \left\{0,1\right\} $

, along with a sequence of aggregate shocks. The real market value of equity satisfies the following recursive formulation for

$ t=1,2 $

:

$ t=1,2 $

:

$$ {\displaystyle \begin{array}{l}{V}_t\left({\Xi}_t\right)=\underset{x_t,{p}_t\left({\tilde{\zeta}}_t=1\right),{l}_t}{\max}\left\{\max \left({d}_t\left({\Xi}_t\right)+{\mathrm{E}}_t\left[{M}_{t+1}{V}_{t+1}\left({\Xi}_{t+1}\right)\right],0\right)\right\},\\ {}\hskip5.7em \mathrm{subject}\ \mathrm{to}:\hskip1em {y}_t\left({\tilde{\zeta}}_t\right)={\left(\frac{p_t\left({\tilde{\zeta}}_t\right)}{P_t}\right)}^{-\nu}\end{array}} $$

$$ {\displaystyle \begin{array}{l}{V}_t\left({\Xi}_t\right)=\underset{x_t,{p}_t\left({\tilde{\zeta}}_t=1\right),{l}_t}{\max}\left\{\max \left({d}_t\left({\Xi}_t\right)+{\mathrm{E}}_t\left[{M}_{t+1}{V}_{t+1}\left({\Xi}_{t+1}\right)\right],0\right)\right\},\\ {}\hskip5.7em \mathrm{subject}\ \mathrm{to}:\hskip1em {y}_t\left({\tilde{\zeta}}_t\right)={\left(\frac{p_t\left({\tilde{\zeta}}_t\right)}{P_t}\right)}^{-\nu}\end{array}} $$

where

$ {p}_t\left({\tilde{\zeta}}_t\right)={\unicode{x1D7D9}}_{\left\{{\tilde{\zeta}}_t=0\right\}}\times {p}_{t-1}+{\unicode{x1D7D9}}_{\left\{{\tilde{\zeta}}_t=1\right\}}\times {p}_t $

captures the fact that the firm can only optimize its nominal output price when

$ {p}_t\left({\tilde{\zeta}}_t\right)={\unicode{x1D7D9}}_{\left\{{\tilde{\zeta}}_t=0\right\}}\times {p}_{t-1}+{\unicode{x1D7D9}}_{\left\{{\tilde{\zeta}}_t=1\right\}}\times {p}_t $

captures the fact that the firm can only optimize its nominal output price when

$ {\tilde{\zeta}}_t=1 $

and

$ {\tilde{\zeta}}_t=1 $

and

$ {\Xi}_t\equiv \left({\tilde{\zeta}}_t,{\tilde{X}}_t,{z}_t,{\Upsilon}_t\right) $

summarizes the set of state variables. The real dividends (i.e., normalized by

$ {\Xi}_t\equiv \left({\tilde{\zeta}}_t,{\tilde{X}}_t,{z}_t,{\Upsilon}_t\right) $

summarizes the set of state variables. The real dividends (i.e., normalized by

$ {P}_t $

) paid by the firm at

$ {P}_t $

) paid by the firm at

$ t=1,2 $

are:

$ t=1,2 $

are:

$$ {d}_1\left({\Xi}_1\right)=\frac{h_1\left({\tilde{\zeta}}_1,{\tilde{X}}_1,{z}_1,{\Upsilon}_1\right)+{x}_0-{x}_1\left(1+\psi \right)-{b}^S-f}{1-\lambda \times {\unicode{x1D7D9}}_{\left\{{d}_1<0\right\}}}, $$

$$ {d}_1\left({\Xi}_1\right)=\frac{h_1\left({\tilde{\zeta}}_1,{\tilde{X}}_1,{z}_1,{\Upsilon}_1\right)+{x}_0-{x}_1\left(1+\psi \right)-{b}^S-f}{1-\lambda \times {\unicode{x1D7D9}}_{\left\{{d}_1<0\right\}}}, $$

$$ {d}_2\left({\Xi}_2\right)=\frac{h_2\left({\tilde{\zeta}}_2,{\tilde{X}}_2,{z}_2,{\Upsilon}_2\right)+{x}_1-{x}_2\left(1+\psi \right)-{b}^L}{1-\lambda \times {\unicode{x1D7D9}}_{\left\{{d}_2<0\right\}}}. $$

$$ {d}_2\left({\Xi}_2\right)=\frac{h_2\left({\tilde{\zeta}}_2,{\tilde{X}}_2,{z}_2,{\Upsilon}_2\right)+{x}_1-{x}_2\left(1+\psi \right)-{b}^L}{1-\lambda \times {\unicode{x1D7D9}}_{\left\{{d}_2<0\right\}}}. $$

C. Optimal Policies

We now describe the firm’s optimal policies. Since the firm’s labor decision is static, the model can be solved in two steps.

First, we solve the firm’s cost-minimization problem: Given a target output level, the firm chooses labor to minimize production costs, yielding the marginal cost

$ {\tilde{c}}_t $

as a function of firm-level productivity:

$ {\tilde{c}}_t $

as a function of firm-level productivity:

$$ {\tilde{c}}_t=\frac{W}{{\tilde{X}}_t}. $$

$$ {\tilde{c}}_t=\frac{W}{{\tilde{X}}_t}. $$

The log marginal cost inherits the log-normal distribution of

$ {\tilde{X}}_t $

; specifically,

$ {\tilde{X}}_t $

; specifically,

$ \log \left({\tilde{c}}_t\right)\sim \mathcal{N}\left(\log (W)-{\mu}_t,{\sigma}_t^2\right) $

. For clarity, we refer to marginal cost rather than productivity throughout the remainder of the draft, noting their inverse relationship: Lower productivity implies higher marginal cost.

$ \log \left({\tilde{c}}_t\right)\sim \mathcal{N}\left(\log (W)-{\mu}_t,{\sigma}_t^2\right) $

. For clarity, we refer to marginal cost rather than productivity throughout the remainder of the draft, noting their inverse relationship: Lower productivity implies higher marginal cost.

In the second step, we solve jointly for the firm’s optimal pricing, financing, and default decisions. Given the finite horizon, this step is solved recursively. We summarize the resulting policy functions, provide economic intuition, and leave full derivations to Section A.1 of the Supplementary Material.

Pricing policy: We first solve for the optimal output price in each period, after substituting in the demand schedule. At

$ t=2 $

, a flexible-price firm, knowing it will cease operations, sets its nominal price to maximize current profits. This yields a pricing policy with a constant markup of

$ t=2 $

, a flexible-price firm, knowing it will cease operations, sets its nominal price to maximize current profits. This yields a pricing policy with a constant markup of

$ \nu /\left(\nu -1\right) $

over nominal marginal cost

$ \nu /\left(\nu -1\right) $

over nominal marginal cost

$ {\tilde{c}}_2{P}_2 $

, that is,

$ {\tilde{c}}_2{P}_2 $

, that is,

$$ {p}_2^{\star}\left({\tilde{c}}_2\right)=\frac{\nu }{\nu -1}{\tilde{c}}_2{P}_2. $$

$$ {p}_2^{\star}\left({\tilde{c}}_2\right)=\frac{\nu }{\nu -1}{\tilde{c}}_2{P}_2. $$

In contrast, if the firm cannot adjust its output price due to price rigidity, it must continue selling at the previously set nominal price

$ {p}_1 $

. This price may be suboptimal if either the marginal cost

$ {p}_1 $

. This price may be suboptimal if either the marginal cost

$ {\tilde{c}}_2 $

or the aggregate price level

$ {\tilde{c}}_2 $

or the aggregate price level

$ {P}_2 $

changes, exposing the firm to real and nominal risk.

$ {P}_2 $

changes, exposing the firm to real and nominal risk.

At

$ t=1 $

, a flexible-price firm sets its output price to maximize the present discounted value of dividends, resulting in the following optimal pricing policy:

$ t=1 $

, a flexible-price firm sets its output price to maximize the present discounted value of dividends, resulting in the following optimal pricing policy:

$$ \frac{p_1^{\star}\left({\tilde{c}}_1\right)}{P_1}=\left(\frac{\nu }{\nu -1}\right)\frac{{\tilde{c}}_1+\theta \left(1-\lambda \times {\unicode{x1D7D9}}_{\left\{{d}_1<0\right\}}\right){\unicode{x1D53C}}_1\left[{M}_2\left({\int}_0^{c_{\zeta_2=0}^d}{\tilde{c}}_2d\Phi \left({\tilde{c}}_2\right)\right){\left({\Pi}_2\right)}^{\nu}\right]}{1+\theta \left(1-\lambda \times {\unicode{x1D7D9}}_{\left\{{d}_1<0\right\}}\right){\unicode{x1D53C}}_1\left[{M}_2\left(\Phi \left({c}_{\zeta_2=0}^d\right){\left({\Pi}_2\right)}^{\nu -1}\right)\right]}, $$

$$ \frac{p_1^{\star}\left({\tilde{c}}_1\right)}{P_1}=\left(\frac{\nu }{\nu -1}\right)\frac{{\tilde{c}}_1+\theta \left(1-\lambda \times {\unicode{x1D7D9}}_{\left\{{d}_1<0\right\}}\right){\unicode{x1D53C}}_1\left[{M}_2\left({\int}_0^{c_{\zeta_2=0}^d}{\tilde{c}}_2d\Phi \left({\tilde{c}}_2\right)\right){\left({\Pi}_2\right)}^{\nu}\right]}{1+\theta \left(1-\lambda \times {\unicode{x1D7D9}}_{\left\{{d}_1<0\right\}}\right){\unicode{x1D53C}}_1\left[{M}_2\left(\Phi \left({c}_{\zeta_2=0}^d\right){\left({\Pi}_2\right)}^{\nu -1}\right)\right]}, $$

where

$ {\Pi}_2\equiv {P}_2/{P}_1 $

is the gross inflation rate between

$ {\Pi}_2\equiv {P}_2/{P}_1 $

is the gross inflation rate between

$ t=1 $

and

$ t=1 $

and

$ t=2 $

.

$ t=2 $

.

As in the case of

$ {p}_2^{\star } $

, the optimal price at

$ {p}_2^{\star } $

, the optimal price at

$ t=1 $

consists of a markup over the nominal marginal cost of production. However, because of potential price rigidity in the next period, the firm now takes into account the possibility that the price it sets today may remain fixed at

$ t=1 $

consists of a markup over the nominal marginal cost of production. However, because of potential price rigidity in the next period, the firm now takes into account the possibility that the price it sets today may remain fixed at

$ t=2 $

. This exposes the firm to both real marginal cost risk, via changes in

$ t=2 $

. This exposes the firm to both real marginal cost risk, via changes in

$ {\tilde{c}}_2 $

, and nominal risk, via inflation

$ {\tilde{c}}_2 $

, and nominal risk, via inflation

$ {\Pi}_2 $

. The extent to which the firm incorporates these future risks into its pricing decision depends on two key forces, both ultimately shaped by the degree of price rigidity. First, a higher value of

$ {\Pi}_2 $

. The extent to which the firm incorporates these future risks into its pricing decision depends on two key forces, both ultimately shaped by the degree of price rigidity. First, a higher value of

$ \theta $

increases the likelihood that the firm will be unable to adjust its price in the future, making it more forward-looking in its pricing strategy today. Second, if the firm requires external equity financing (i.e.,

$ \theta $

increases the likelihood that the firm will be unable to adjust its price in the future, making it more forward-looking in its pricing strategy today. Second, if the firm requires external equity financing (i.e.,

$ {d}_1<0 $

) or faces a higher probability of default, it shifts its focus toward maximizing immediate cash flows, becoming more myopic.

$ {d}_1<0 $

) or faces a higher probability of default, it shifts its focus toward maximizing immediate cash flows, becoming more myopic.

In short, price inflexibility influences the firm’s pricing behavior both directly, through the risk of being stuck with today’s price, and indirectly, by shaping its financing and default decisions. Absent price rigidity (i.e.,

$ \theta =0 $

) or real and nominal risk (i.e.,

$ \theta =0 $

) or real and nominal risk (i.e.,

$ {\tilde{c}}_1={\tilde{c}}_2 $

and

$ {\tilde{c}}_1={\tilde{c}}_2 $

and

$ {\Pi}_2={\Pi}_1 $

), the firm would simply set:

$ {\Pi}_2={\Pi}_1 $

), the firm would simply set:

$$ {p}_1^{flex}=\frac{\nu }{\nu -1}{\tilde{c}}_1{P}_1. $$

$$ {p}_1^{flex}=\frac{\nu }{\nu -1}{\tilde{c}}_1{P}_1. $$

In contrast, a non-price-optimizing firm sells its output at a nominal price

$ {\overline{p}}_0 $

, which we normalize to 1.

$ {\overline{p}}_0 $

, which we normalize to 1.

Default and financing policy: In each period

$ t>0 $

, the firm defaults if the marginal cost shock

$ t>0 $

, the firm defaults if the marginal cost shock

$ {\tilde{c}}_t $

is high enough to result in a negative equity value. The firm continues operating as long as

$ {\tilde{c}}_t $

is high enough to result in a negative equity value. The firm continues operating as long as

$ {\tilde{c}}_t $

remains below the default threshold

$ {\tilde{c}}_t $

remains below the default threshold

$ {c}_t^d\left({\tilde{\zeta}}_t,{z}_t,{\Upsilon}_t\right) $

. If the shock causes a liquidity shortfall, that is, a negative dividend, the firm raises funds via costly external equity issuance. These financing decisions can be summarized as follows:

$ {c}_t^d\left({\tilde{\zeta}}_t,{z}_t,{\Upsilon}_t\right) $

. If the shock causes a liquidity shortfall, that is, a negative dividend, the firm raises funds via costly external equity issuance. These financing decisions can be summarized as follows:

$$ \left\{\begin{array}{ll}\mathrm{default}\hskip0.24em & \mathrm{if}\;{\tilde{c}}_t\ge {c}_t^d\left({\tilde{\zeta}}_t,{z}_t,{\Upsilon}_t\right)\\ {}\mathrm{issue}\;\mathrm{new}\;\mathrm{equity}\hskip0.24em & \mathrm{if}\;{c}_t^d\left({\tilde{\zeta}}_t,{z}_t,{\Upsilon}_t\right)>{\tilde{c}}_t\ge {c}_t^e\left({\tilde{\zeta}}_t,{z}_t,{\Upsilon}_t\right)\\ {}\mathrm{no}\;\mathrm{financing}\hskip0.24em & \mathrm{if}\;{\tilde{c}}_t<{c}_t^e\left({\tilde{\zeta}}_t,{z}_t,{\Upsilon}_t\right),\end{array}\right. $$

$$ \left\{\begin{array}{ll}\mathrm{default}\hskip0.24em & \mathrm{if}\;{\tilde{c}}_t\ge {c}_t^d\left({\tilde{\zeta}}_t,{z}_t,{\Upsilon}_t\right)\\ {}\mathrm{issue}\;\mathrm{new}\;\mathrm{equity}\hskip0.24em & \mathrm{if}\;{c}_t^d\left({\tilde{\zeta}}_t,{z}_t,{\Upsilon}_t\right)>{\tilde{c}}_t\ge {c}_t^e\left({\tilde{\zeta}}_t,{z}_t,{\Upsilon}_t\right)\\ {}\mathrm{no}\;\mathrm{financing}\hskip0.24em & \mathrm{if}\;{\tilde{c}}_t<{c}_t^e\left({\tilde{\zeta}}_t,{z}_t,{\Upsilon}_t\right),\end{array}\right. $$

where the equity issuance threshold

$ {c}_t^e\left(\cdot \right) $

and the default threshold

$ {c}_t^e\left(\cdot \right) $

and the default threshold

$ {c}_t^d\left(\cdot \right) $

are implicitly defined by the following conditions (see Section 1 of the Supplementary Material for a detailed derivation):

$ {c}_t^d\left(\cdot \right) $

are implicitly defined by the following conditions (see Section 1 of the Supplementary Material for a detailed derivation):

$$ {c}_t^e:= {d}_t\left({\tilde{\zeta}}_t,{c}_t^e,{z}_t,{\Upsilon}_t\right)=0, $$

$$ {c}_t^e:= {d}_t\left({\tilde{\zeta}}_t,{c}_t^e,{z}_t,{\Upsilon}_t\right)=0, $$

$$ {c}_t^d:= {V}_t\left({\tilde{\zeta}}_t,{c}_t^d,{z}_t,{\Upsilon}_t\right)=0. $$

$$ {c}_t^d:= {V}_t\left({\tilde{\zeta}}_t,{c}_t^d,{z}_t,{\Upsilon}_t\right)=0. $$

The endogenous thresholds in equations (17) and (18) determine the default probability,

$ 1-\Phi \left({c}_t^d\right) $

, and the probability of external equity issuance,

$ 1-\Phi \left({c}_t^d\right) $

, and the probability of external equity issuance,

$ 1-\Phi \left({c}_t^e\right) $

. Both depend on the full set of state variables

$ 1-\Phi \left({c}_t^e\right) $

. Both depend on the full set of state variables

$ \left({\tilde{\zeta}}_t,{z}_t,{\Upsilon}_t\right) $

. The degree of price inflexibility

$ \left({\tilde{\zeta}}_t,{z}_t,{\Upsilon}_t\right) $

. The degree of price inflexibility

$ \theta $

plays a central role in shaping these probabilities. Firms with sticky prices cannot adjust output prices in response to real or nominal shocks, increasing their risk exposure. For instance, in the face of an adverse cost shock, they cannot raise prices to offset losses; under favorable conditions, they cannot lower prices to boost demand. As a result, sticky-price firms are endogenously riskier, all else equal.

$ \theta $

plays a central role in shaping these probabilities. Firms with sticky prices cannot adjust output prices in response to real or nominal shocks, increasing their risk exposure. For instance, in the face of an adverse cost shock, they cannot raise prices to offset losses; under favorable conditions, they cannot lower prices to boost demand. As a result, sticky-price firms are endogenously riskier, all else equal.

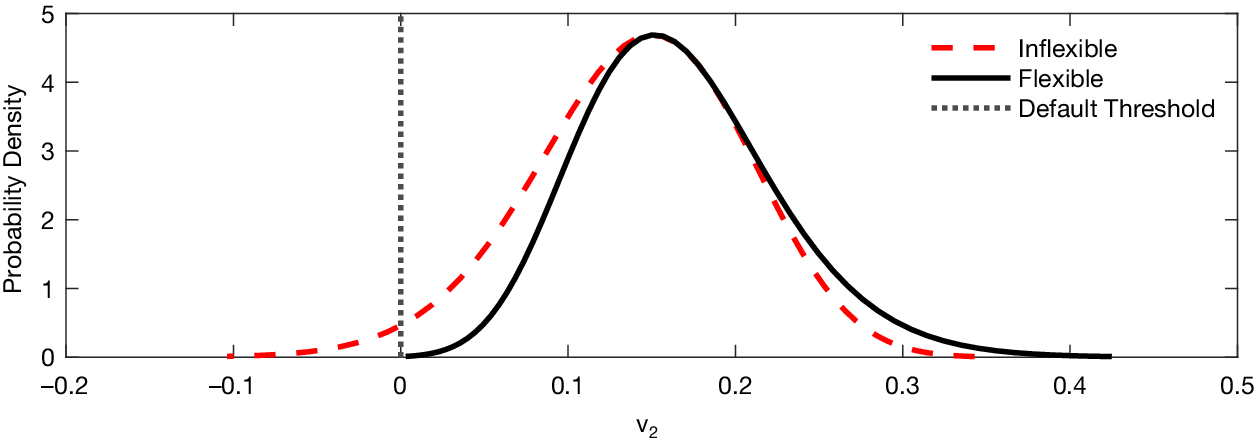

Figure 2 illustrates this mechanism by comparing the probability density function (pdf) of equity at

$ t=2 $

for a perfectly flexible firm (solid black line) and a perfectly inflexible firm (dashed red line). The vertical line indicates the default threshold. The inflexible firm’s pdf is left-skewed and exhibits a higher default probability, demonstrating how price stickiness increases default risk and liquidity needs, thereby shaping optimal financing decisions, such as leverage and cash holdings, and ultimately affecting the equilibrium price of debt, as we show next.

$ t=2 $

for a perfectly flexible firm (solid black line) and a perfectly inflexible firm (dashed red line). The vertical line indicates the default threshold. The inflexible firm’s pdf is left-skewed and exhibits a higher default probability, demonstrating how price stickiness increases default risk and liquidity needs, thereby shaping optimal financing decisions, such as leverage and cash holdings, and ultimately affecting the equilibrium price of debt, as we show next.

Figure 2 compares the probability density function of the equity value

$ {V}_2 $

at time

$ {V}_2 $

at time

$ t=2 $

, for a perfectly flexible firm (solid black line) and a perfectly inflexible firm (dashed red). The vertical dotted line represents the default threshold, that is,

$ t=2 $

, for a perfectly flexible firm (solid black line) and a perfectly inflexible firm (dashed red). The vertical dotted line represents the default threshold, that is,

$ {V}_2=0 $

. The calibration used to obtain these graphs is summarized in Section II.E.

$ {V}_2=0 $

. The calibration used to obtain these graphs is summarized in Section II.E.

Debt policy: We now turn to the firm’s optimal choice of long-term debt

$ {b}^L $

, derived from the first-order condition with respect to

$ {b}^L $

, derived from the first-order condition with respect to

$ {b}^L $

at time

$ {b}^L $

at time

$ t=0 $

:

$ t=0 $

:

$$ {\chi}^L{q}_0^L=-\left(1+{\chi}^L\right)\frac{\partial {q}_0^L}{\partial {b}^L}{b}^L-\left(1+{\chi}^S\right)\frac{\partial {q}_0^S}{\partial {b}^L}{b}^S. $$

$$ {\chi}^L{q}_0^L=-\left(1+{\chi}^L\right)\frac{\partial {q}_0^L}{\partial {b}^L}{b}^L-\left(1+{\chi}^S\right)\frac{\partial {q}_0^S}{\partial {b}^L}{b}^S. $$

Equation (19) shows that optimal leverage is determined through the condition that marginal benefits equal marginal costs of issuing long-term debt. The marginal benefit is the additional proceeds per dollar raised,

$ {\chi}^L{q}_0^L $

. The marginal cost reflects increased default risk, which lowers the market value of both long- and short-term debt, as indicated by

$ {\chi}^L{q}_0^L $

. The marginal cost reflects increased default risk, which lowers the market value of both long- and short-term debt, as indicated by

$ \partial {q}_0^H/\partial {b}^L<0 $

for

$ \partial {q}_0^H/\partial {b}^L<0 $

for

$ H=L,S $

.

$ H=L,S $

.

The optimal decision for short-term debt,

$ {b}^S $

, is given by:

$ {b}^S $

, is given by:

$$ \hskip1em {\chi}^S{q}_0^S=-\left(1+{\chi}^L\right)\frac{\partial {q}_0^L}{\partial {b}^S}{b}^L-\left(1+{\chi}^S\right)\frac{\partial {q}_0^S}{\partial {b}^S}{b}^S+\underset{\mathrm{rollover}\ \mathrm{cost}}{\underbrace{\left[\frac{\lambda }{1-\lambda}\left({\mathrm{\mathbb{P}}}_1\left(\mathrm{FIN}\right)-{\mathrm{\mathbb{P}}}_1\left(\mathrm{DEF}\right)\right)\right]}}, $$

$$ \hskip1em {\chi}^S{q}_0^S=-\left(1+{\chi}^L\right)\frac{\partial {q}_0^L}{\partial {b}^S}{b}^L-\left(1+{\chi}^S\right)\frac{\partial {q}_0^S}{\partial {b}^S}{b}^S+\underset{\mathrm{rollover}\ \mathrm{cost}}{\underbrace{\left[\frac{\lambda }{1-\lambda}\left({\mathrm{\mathbb{P}}}_1\left(\mathrm{FIN}\right)-{\mathrm{\mathbb{P}}}_1\left(\mathrm{DEF}\right)\right)\right]}}, $$

where the probabilities of raising external financing and defaulting are given by

$ {\mathrm{\mathbb{P}}}_1\left(\mathrm{FIN}\right)=1-{\unicode{x1D53C}}_0\Phi \left({c}_1^e\left({\tilde{\zeta}}_1,{z}_1,{\Upsilon}_1\right)\right) $

and

$ {\mathrm{\mathbb{P}}}_1\left(\mathrm{FIN}\right)=1-{\unicode{x1D53C}}_0\Phi \left({c}_1^e\left({\tilde{\zeta}}_1,{z}_1,{\Upsilon}_1\right)\right) $

and

$ {\mathrm{\mathbb{P}}}_1\left(\mathrm{DEF}\right)=1-{\unicode{x1D53C}}_0\Phi \left({c}_1^d\left({\tilde{\zeta}}_1,{z}_1,{\Upsilon}_1\right)\right) $

, respectively.

$ {\mathrm{\mathbb{P}}}_1\left(\mathrm{DEF}\right)=1-{\unicode{x1D53C}}_0\Phi \left({c}_1^d\left({\tilde{\zeta}}_1,{z}_1,{\Upsilon}_1\right)\right) $

, respectively.

As with long-term debt, the marginal benefit of issuing an additional dollar of short-term debt is the extra inflow,

$ {\chi}^S{q}_0^S $

. The marginal cost consists of two components. The first two terms reflect default-related costs, mirroring the deterioration in debt prices from increased default risk. The third term—the rollover cost—captures the heightened risk of a liquidity shortfall in the next period, which may force the firm to raise costly external equity. Thus, issuing more short-term debt today increases both default risk and the likelihood of relying on external financing.

$ {\chi}^S{q}_0^S $

. The marginal cost consists of two components. The first two terms reflect default-related costs, mirroring the deterioration in debt prices from increased default risk. The third term—the rollover cost—captures the heightened risk of a liquidity shortfall in the next period, which may force the firm to raise costly external equity. Thus, issuing more short-term debt today increases both default risk and the likelihood of relying on external financing.

The degree of price stickiness plays a central role in shaping both the level and composition of corporate debt. Firms with higher price rigidity (e.g., higher

$ \theta $

) are endogenously riskier, reducing the net benefits of both short- and long-term debt, leading to lower leverage, higher default risk, and wider credit spreads. Moreover, since long-term debt is repaid only if the firm survives two periods, it is more sensitive to credit risk than short-term debt. As a result, and as we show later, firms with greater price stickiness tend to choose shorter average debt maturity.

$ \theta $

) are endogenously riskier, reducing the net benefits of both short- and long-term debt, leading to lower leverage, higher default risk, and wider credit spreads. Moreover, since long-term debt is repaid only if the firm survives two periods, it is more sensitive to credit risk than short-term debt. As a result, and as we show later, firms with greater price stickiness tend to choose shorter average debt maturity.

Cash-holdings: The firm’s optimal cash holding is determined by equating the marginal benefit of holding an additional dollar in cash with its marginal cost:

$$ \hskip1em \frac{\lambda }{1-\lambda}\times {\mathrm{\mathbb{P}}}_1\left(\mathrm{FIN}\right)+\left(1+{\chi}^L\right)\frac{\partial {q}_0^L}{\partial {x}_0}{b}^L+\left(1+{\chi}^S\right)\frac{\partial {q}_0^S}{\partial {x}_0}{b}^S=\psi {x}_0+{\mathrm{\mathbb{P}}}_1\left(\mathrm{DEF}\right)\times \frac{1}{1-\lambda }. $$

$$ \hskip1em \frac{\lambda }{1-\lambda}\times {\mathrm{\mathbb{P}}}_1\left(\mathrm{FIN}\right)+\left(1+{\chi}^L\right)\frac{\partial {q}_0^L}{\partial {x}_0}{b}^L+\left(1+{\chi}^S\right)\frac{\partial {q}_0^S}{\partial {x}_0}{b}^S=\psi {x}_0+{\mathrm{\mathbb{P}}}_1\left(\mathrm{DEF}\right)\times \frac{1}{1-\lambda }. $$

Holding an additional unit of cash provides two main benefits. First, it reduces the likelihood of costly external equity issuance. Second, it lowers default risk, thereby increasing the market value of both short- and long-term debt and raising total debt proceeds. However, cash holdings also involve costs: They intensify agency frictions, captured by

$ \psi {x}_0 $

, and the cash may be lost in the event of default.

$ \psi {x}_0 $

, and the cash may be lost in the event of default.

Because sticky-price firms are endogenously riskier, they face a higher likelihood of both default and external financing. Consequently, they optimally hold more precautionary cash in equilibrium to ease future financing constraints.

D. Monetary Policy, SDF, and Aggregate Processes

We close the model by specifying the monetary policy rule and the stochastic discount factor (SDF), and by introducing aggregate processes that help generate further predictions on the relation between price flexibility and credit risk.

Monetary policy: Following the New Keynesian literature, we specify a Taylor rule for the nominal short-term interest rate:

$$ {r}_t^{\$}={\overline{r}}^{\$}+{\phi}_{\pi}\left(\log {\Pi}_t-\log \overline{\Pi}\right)+{x}_{rt}, $$

$$ {r}_t^{\$}={\overline{r}}^{\$}+{\phi}_{\pi}\left(\log {\Pi}_t-\log \overline{\Pi}\right)+{x}_{rt}, $$

Here,

$ {\overline{r}}^{\$} $

is the long-run log-nominal interest rate,

$ {\overline{r}}^{\$} $

is the long-run log-nominal interest rate,

$ {\phi}_{\pi }>0 $

captures the sensitivity of the policy rate to deviations of inflation from its target

$ {\phi}_{\pi }>0 $

captures the sensitivity of the policy rate to deviations of inflation from its target

$ \overline{\Pi} $

, and

$ \overline{\Pi} $

, and

$ {x}_{rt} $

denotes an exogenous MPS. The Taylor rule allows monetary shocks to generate unexpected changes in inflation.

$ {x}_{rt} $

denotes an exogenous MPS. The Taylor rule allows monetary shocks to generate unexpected changes in inflation.

Aggregate processes: Our economy includes three exogenous aggregate processes:

$ {\mu}_t $

,

$ {\mu}_t $

,

$ {\sigma}_t $

, and

$ {\sigma}_t $

, and

$ {x}_{rt} $

. Each follows a persistent AR(1) process:

$ {x}_{rt} $

. Each follows a persistent AR(1) process:

$$ {\mu}_t=\left(1-{\rho}_{\mu}\right)\overline{\mu}+{\rho}_{\mu }{\mu}_{t-1}+{\sigma}_{\mu }{\varepsilon}_{\mu t}, $$

$$ {\mu}_t=\left(1-{\rho}_{\mu}\right)\overline{\mu}+{\rho}_{\mu }{\mu}_{t-1}+{\sigma}_{\mu }{\varepsilon}_{\mu t}, $$

$$ \log {\sigma}_t=\left(1-{\rho}_{\sigma}\right)\log \overline{\sigma}+{\rho}_{\sigma}\log {\sigma}_{t-1}-{\rho}_{\mu \sigma}{\varepsilon}_{\mu t}+{\sigma}_{\sigma }{\varepsilon}_{\sigma t}, $$

$$ \log {\sigma}_t=\left(1-{\rho}_{\sigma}\right)\log \overline{\sigma}+{\rho}_{\sigma}\log {\sigma}_{t-1}-{\rho}_{\mu \sigma}{\varepsilon}_{\mu t}+{\sigma}_{\sigma }{\varepsilon}_{\sigma t}, $$

$$ {x}_{rt}={\rho}_r{x}_{rt-1}+{\sigma}_r{\varepsilon}_{rt}, $$

$$ {x}_{rt}={\rho}_r{x}_{rt-1}+{\sigma}_r{\varepsilon}_{rt}, $$

where

$ {\rho}_m $

and

$ {\rho}_m $

and

$ {\sigma}_m $

denote the persistence and conditional volatility of each process, for

$ {\sigma}_m $

denote the persistence and conditional volatility of each process, for

$ m=\mu, \sigma, $

and

$ m=\mu, \sigma, $

and

$ r $

, respectively.

$ r $

, respectively.

The parameter

$ {\rho}_{\mu \sigma}>0 $

introduces a countercyclical component to volatility by allowing adverse productivity shocks (i.e., negative

$ {\rho}_{\mu \sigma}>0 $

introduces a countercyclical component to volatility by allowing adverse productivity shocks (i.e., negative

$ {\varepsilon}_{\mu t} $

) to raise uncertainty. This reduced-form specification captures the well-documented empirical pattern that uncertainty rises during recessions (Bloom (Reference Bloom2014)). Moreover, Chen (Reference Chen2010) and Bhamra et al. (Reference Bhamra, Kuehn and Strebulaev2010a) show that this channel helps generate a sizable credit risk premium.Footnote

7

$ {\varepsilon}_{\mu t} $

) to raise uncertainty. This reduced-form specification captures the well-documented empirical pattern that uncertainty rises during recessions (Bloom (Reference Bloom2014)). Moreover, Chen (Reference Chen2010) and Bhamra et al. (Reference Bhamra, Kuehn and Strebulaev2010a) show that this channel helps generate a sizable credit risk premium.Footnote

7

Stochastic discount factor: Because we focus on how price inflexibility affects the cross section of credit spreads, we specify an exogenous SDF process with inflation nonneutrality, following Bansal and Shaliastovich (Reference Bansal and Shaliastovich2013):

$$ \ln \left({M}_t\right)=-\overline{r}-{\gamma}_{\mu}\hskip0.1em {\sigma}_{\mu}\hskip0.1em {\varepsilon}_{\mu t}-{\gamma}_{\pi}\hskip0.1em \Delta {\pi}_t-{\gamma}_{\sigma}\hskip0.1em {\sigma}_{\sigma}\hskip0.1em {\varepsilon}_{\sigma t}, $$

$$ \ln \left({M}_t\right)=-\overline{r}-{\gamma}_{\mu}\hskip0.1em {\sigma}_{\mu}\hskip0.1em {\varepsilon}_{\mu t}-{\gamma}_{\pi}\hskip0.1em \Delta {\pi}_t-{\gamma}_{\sigma}\hskip0.1em {\sigma}_{\sigma}\hskip0.1em {\varepsilon}_{\sigma t}, $$

where

$ \overline{r} $

is the steady-state real risk-free rate,

$ \overline{r} $

is the steady-state real risk-free rate,

$ \Delta {\pi}_t\equiv \log \left({\Pi}_t\right)-{\mathrm{E}}_{t-1}\log \left({\Pi}_t\right) $

denotes the log-inflation surprise, and

$ \Delta {\pi}_t\equiv \log \left({\Pi}_t\right)-{\mathrm{E}}_{t-1}\log \left({\Pi}_t\right) $

denotes the log-inflation surprise, and

$ {\gamma}_{\mu } $

,

$ {\gamma}_{\mu } $

,

$ {\gamma}_{\pi } $

, and

$ {\gamma}_{\pi } $

, and

$ {\gamma}_{\sigma } $

are the prices of risk associated with productivity, nominal, and uncertainty shocks, respectively. We set

$ {\gamma}_{\sigma } $

are the prices of risk associated with productivity, nominal, and uncertainty shocks, respectively. We set

$ {\gamma}_{\mu }>0 $

, consistent with the idea that positive productivity shocks correspond to good states of the world, and

$ {\gamma}_{\mu }>0 $

, consistent with the idea that positive productivity shocks correspond to good states of the world, and

$ {\gamma}_{\sigma }<0 $

, meaning that higher uncertainty is considered bad news for investors and increases the SDF (e.g., Bansal and Yaron (Reference Bansal and Yaron2004)). We assume

$ {\gamma}_{\sigma }<0 $

, meaning that higher uncertainty is considered bad news for investors and increases the SDF (e.g., Bansal and Yaron (Reference Bansal and Yaron2004)). We assume

$ {\gamma}_{\pi }<0 $

, reflecting evidence that unexpected increases in inflation are bad news for future consumption, as documented by Piazzesi, Schneider, Benigno, and Campbell (Reference Piazzesi, Schneider, Benigno and Campbell2006). Inflation nonneutrality ensures that MPSs, our sole source of inflation news, are priced by the representative investor.

$ {\gamma}_{\pi }<0 $

, reflecting evidence that unexpected increases in inflation are bad news for future consumption, as documented by Piazzesi, Schneider, Benigno, and Campbell (Reference Piazzesi, Schneider, Benigno and Campbell2006). Inflation nonneutrality ensures that MPSs, our sole source of inflation news, are priced by the representative investor.

E. Numerical Exercise and Empirical Predictions

We solve the model numerically using a second-order perturbation method. We provide details on the solution strategy, parameter calibration, and model fit in Section A.2 of the Supplementary Material. Our primary objective is to generate qualitative, testable predictions about how price rigidity affects firms’ financing decisions and credit risk in the cross section.

First, we examine how price rigidity affects firm-level risk by analyzing the response of credit spreads, after financing decisions are made, to a surprise increase in aggregate marginal costs, which is equivalent to a negative productivity shock

$ {\varepsilon}_{\mu t}<0 $

. All impulse responses are averaged across the distribution of idiosyncratic shocks.

$ {\varepsilon}_{\mu t}<0 $

. All impulse responses are averaged across the distribution of idiosyncratic shocks.

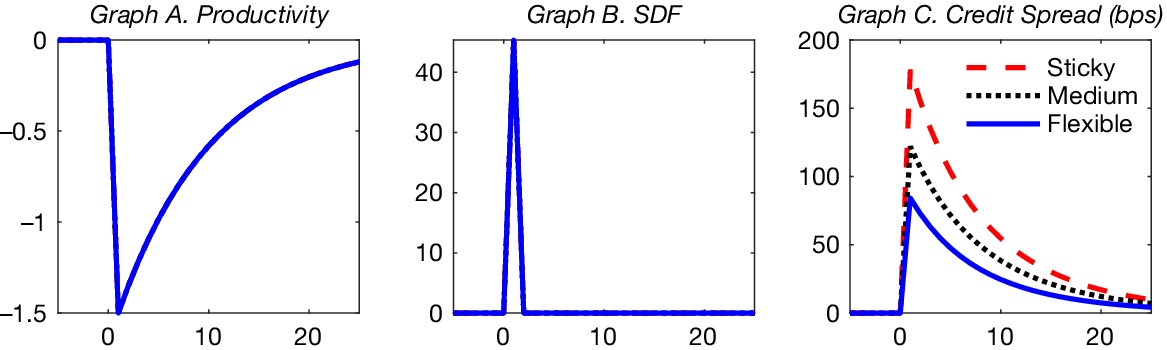

Figure 3 presents the results. Following the aggregate shock (Graph A), expected real marginal costs rise persistently for all firms, reducing firm valuations and widening credit spreads. Flexible-price firms can partially offset the shock by raising prices, whereas sticky-price firms cannot reoptimize and must absorb the full cost increase, leading to larger valuation losses and sharper credit spread increases for sticky firms (Graph C). Importantly, since recessions are associated with a higher price of risk, as reflected in the SDF (Graph B), the debt of sticky-price firms not only carries greater average credit risk, but also earns a larger risk premium. In short, sticky-price firms are more exposed to both idiosyncratic (Figure 2) and aggregate productivity shocks, making them riskier.

Figure 3 illustrates how an aggregate productivity shock (Graph A) impacts the stochastic discount factor (Graph B) and credit spreads (Graph C) using the impulse-response functions for three types of firms: Sticky-price firms (dashed red), medium flexible-price firms (dotted black), and flexible-price firms (solid blue). Price flexibility is governed by

$ \theta $

, which is set to 0 for flexible firms, 0.5 for medium firms, and 1 for sticky firms. The shock, that is, a surprise decline in productivity

$ \theta $

, which is set to 0 for flexible firms, 0.5 for medium firms, and 1 for sticky firms. The shock, that is, a surprise decline in productivity

$ {\varepsilon}_{\mu }<0 $

, occurs at the end of

$ {\varepsilon}_{\mu }<0 $

, occurs at the end of

$ t=0 $

, after financing decisions are made. Impulse-response functions are averaged across the distribution of idiosyncratic shocks. The

$ t=0 $

, after financing decisions are made. Impulse-response functions are averaged across the distribution of idiosyncratic shocks. The

$ y $

-axis reports the magnitude of the productivity shock (Graph A), the value of the SDF (Graph B), and credit spreads in basis points (Graph C); the

$ y $

-axis reports the magnitude of the productivity shock (Graph A), the value of the SDF (Graph B), and credit spreads in basis points (Graph C); the

$ x $

-axis shows the number of periods from the shock.

$ x $

-axis shows the number of periods from the shock.

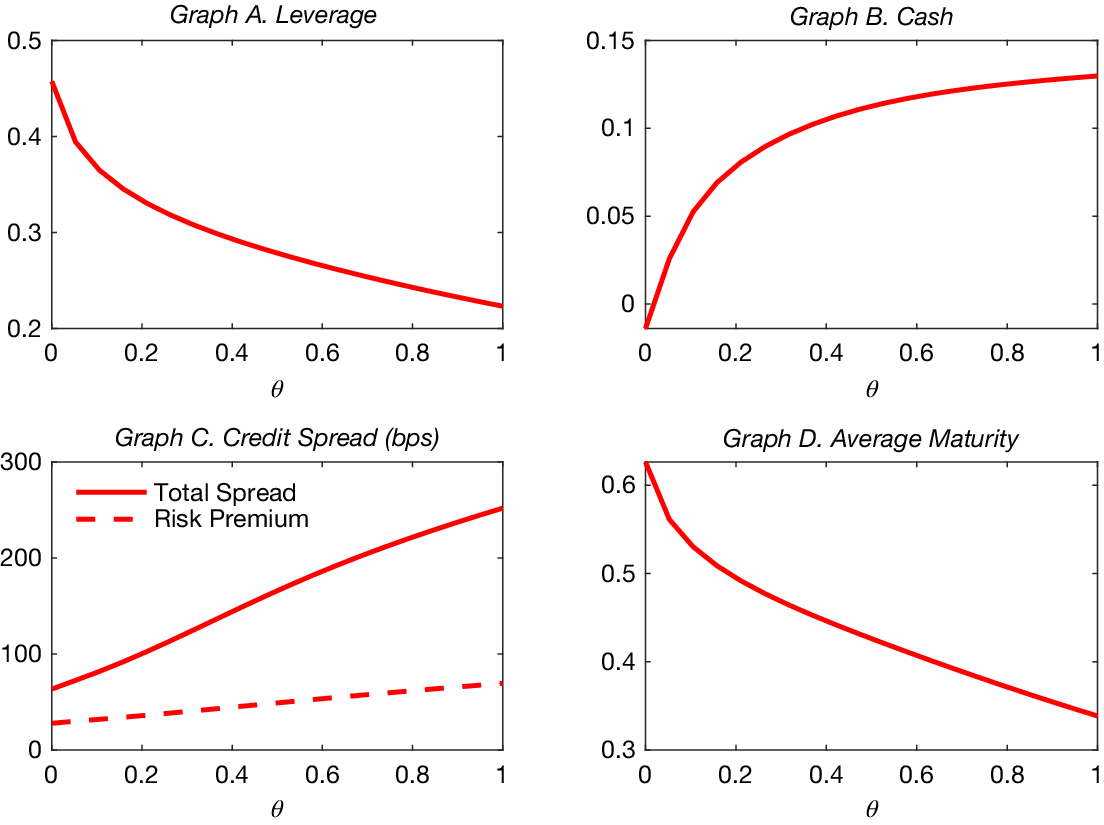

Anticipating greater risk exposure, firms adjust their financing decisions based on price flexibility. Figure 4 plots optimal financing policies and equilibrium credit spreads at

$ t=0 $

as a function of

$ t=0 $

as a function of

$ \theta $

, yielding novel, testable predictions. Sticky-price firms (higher

$ \theta $

, yielding novel, testable predictions. Sticky-price firms (higher

$ \theta $

) are riskier and thus issue less, and more expensive, debt, resulting in lower leverage (Graph A), consistent with D’Acunto et al. (Reference D’Acunto, Liu, Pflueger and Weber2018). Although one might expect sticky-price firms to hold less cash (Bolton et al. (Reference Bolton, Chen and Wang2014)), they instead hold more precautionary cash in equilibrium to offset elevated credit and rollover risk (Graph B).

$ \theta $

) are riskier and thus issue less, and more expensive, debt, resulting in lower leverage (Graph A), consistent with D’Acunto et al. (Reference D’Acunto, Liu, Pflueger and Weber2018). Although one might expect sticky-price firms to hold less cash (Bolton et al. (Reference Bolton, Chen and Wang2014)), they instead hold more precautionary cash in equilibrium to offset elevated credit and rollover risk (Graph B).

Hypothesis 1. Sticky-price firms have higher cash holdings than flexible-price firms.

Figure 4 illustrates the model-implied effects of price rigidity on key firm outcomes: Leverage (Graph A), cash-to-assets (Graph B), the total credit spread and credit risk premium at issuance (Graph C), and average debt maturity (Graph D). Leverage is defined as

$ {b}^S+{b}^L $

, cash-to-assets as

$ {b}^S+{b}^L $

, cash-to-assets as

$ {b}^S-{x}_0 $

, the credit spread is computed for long-term debt, and the average maturity is given by

$ {b}^S-{x}_0 $

, the credit spread is computed for long-term debt, and the average maturity is given by

$ {b}^S\times 1+{b}^L\times 2 $

. Price rigidity is governed by the parameter

$ {b}^S\times 1+{b}^L\times 2 $

. Price rigidity is governed by the parameter

$ \theta $

. The plots are based on firm optimal decisions computed over a range of price stickiness levels (

$ \theta $

. The plots are based on firm optimal decisions computed over a range of price stickiness levels (

$ \theta $

ranging from 0 to 1), with the model simulated for 10,000 periods following a burn-in of 2000 periods.

$ \theta $

ranging from 0 to 1), with the model simulated for 10,000 periods following a burn-in of 2000 periods.

The higher riskiness of sticky-price firms is reflected in higher credit spreads, which include a greater credit risk premium due to their greater countercyclicality (Graph C).

Hypothesis 2. Sticky-price firms have higher credit spreads and risk premium than flexible-price firms.

Since long-term creditors are repaid only if the firm survives two periods, long-term debt is more sensitive to default risk. As a result, sticky-price firms rely more on short-term debt to capture the tax benefits of debt financing, reducing average maturity (Graph D).

Hypothesis 3. Sticky-price firms have lower average debt maturity than flexible-price firms.

Debt covenants allow long-term creditors to restructure outstanding debt upon a covenant violation, thereby reducing credit risk. Given their greater cash flow uncertainty and higher credit risk, sticky-price firms are likely to benefit more from tighter covenants than flexible-price firms. In effect, covenants function similarly to shorter debt maturity by limiting creditors’ exposure to default risk. This logic leads to a fourth testable predictionFootnote 8:

Hypothesis 4. Sticky-price firms have tighter covenants than flexible-price firms.

Another testable implication from Figure 3 is that debt prices of sticky-price firms should be more sensitive to productivity shocks. However, such shocks are difficult to identify empirically. To address this point, we turn to alternative exogenous shocks in the model that are arguably easier to isolate in the data: Monetary policy and volatility shocks.

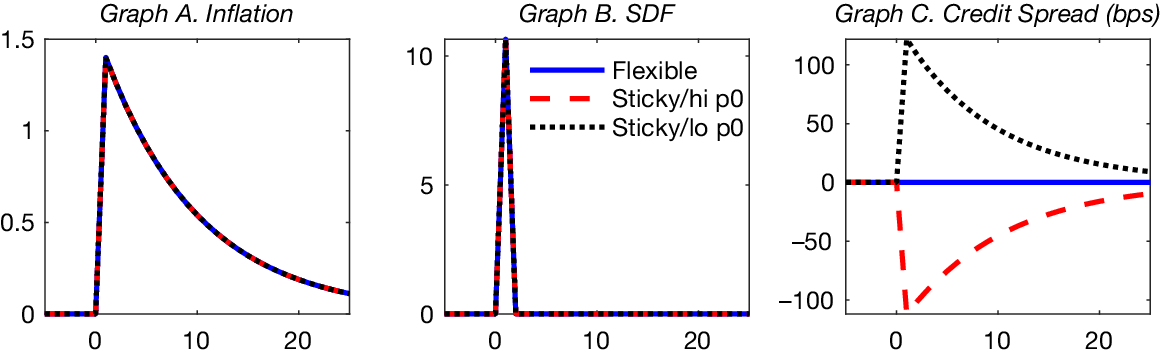

Figure 5 illustrates the response of credit spreads to a surprise MPS (

$ {\varepsilon}_{rt}>0 $

) that raises inflation (Graph A) and, in turn, increases nominal marginal costs. Because inflation is bad news for expected consumption, the SDF rises on impact (Graph B). Flexible-price firms adjust output prices immediately, passing the inflation on to customers and leaving their credit spreads largely unchanged (solid blue line, Graph C). Sticky-price firms, unable to reoptimize prices, are directly affected. For firms currently overpricing relative to the flexible-firm optimum (dashed red line), inflation reduces the price wedge, improves valuations, and narrows spreads. Conversely, for underpricing firms (dotted black line), inflation pushes prices further from optimality, lowering valuations and widening spreads. While the direction of the effect differs by firm type, the magnitude of the response is consistently greater for sticky-price firms.Footnote

9 This asymmetry motivates our next prediction:

$ {\varepsilon}_{rt}>0 $

) that raises inflation (Graph A) and, in turn, increases nominal marginal costs. Because inflation is bad news for expected consumption, the SDF rises on impact (Graph B). Flexible-price firms adjust output prices immediately, passing the inflation on to customers and leaving their credit spreads largely unchanged (solid blue line, Graph C). Sticky-price firms, unable to reoptimize prices, are directly affected. For firms currently overpricing relative to the flexible-firm optimum (dashed red line), inflation reduces the price wedge, improves valuations, and narrows spreads. Conversely, for underpricing firms (dotted black line), inflation pushes prices further from optimality, lowering valuations and widening spreads. While the direction of the effect differs by firm type, the magnitude of the response is consistently greater for sticky-price firms.Footnote

9 This asymmetry motivates our next prediction:

Hypothesis 5. The magnitude of the change in credit spreads in response to a MPS is lower for flexible-price firms than for sticky-price firms.

Figure 5 compares the impulse responses of inflation (Graph A), the stochastic discount factor (Graph B), and credit spreads (Graph C) to a MPS for three types of firms: Flexible-price firms (solid blue), sticky-price firms with a high initial price at

$ t=0 $

(red dashed), and sticky-price firms with a low initial price at

$ t=0 $

(red dashed), and sticky-price firms with a low initial price at

$ t=0 $

(black dotted). Price flexibility is governed by

$ t=0 $

(black dotted). Price flexibility is governed by

$ \theta $

, set to 0 for flexible firms and 1 for sticky firms. Differences in

$ \theta $

, set to 0 for flexible firms and 1 for sticky firms. Differences in

$ {p}_0 $

are generated using a persistent process; high- and low-price firms are defined by initial prices

$ {p}_0 $

are generated using a persistent process; high- and low-price firms are defined by initial prices

$ {p}_0 $

that are 25% above and 10% below the steady state, respectively, at the time of the shock. The shock – a surprise increase in inflation – is introduced at the end of period

$ {p}_0 $

that are 25% above and 10% below the steady state, respectively, at the time of the shock. The shock – a surprise increase in inflation – is introduced at the end of period

$ t=0 $

, after financing decisions have been made. Impulse-response functions are averaged across the distribution of idiosyncratic shocks. The

$ t=0 $

, after financing decisions have been made. Impulse-response functions are averaged across the distribution of idiosyncratic shocks. The

$ y $