Introduction

This paper examines the fiscal health of Northern Cyprus’s pension system, emphasising the concerning trend of increasing pension deficits. These deficits indicate a structural problem affecting the system’s sustainability and integrity. With Northern Cyprus aspiring to join the EU, addressing these imbalances is imperative.

The Social Security Pension System in Northern Cyprus plays a crucial role in providing income support to the retired elderly, particularly during inflationary periods. This system is designed to be inflation-indexed, meaning that pensions are adjusted to keep pace with rising prices. This mechanism ensures that retirees’ purchasing power is preserved, making indexed social security pensions an important buffer against the eroding effects of inflation and the uncertainty of highly variable inflation rates faced by many retirees. Since 2010, the mean annual rate of inflation has been 27% with a high standard deviation of 28%. This extreme volatility in the purchasing power of retired people’s fixed nominal sources of income is an issue that any responsible government needs to mitigate. Such volatility means that people need to secure an investment return that approximately matches the inflation rate to maintain their purchasing power. It is not just about compensating for the current rates of inflation, but also about managing the perceived risk that comes with inflation’s unpredictability.

No policy instruments are available to Northern Cyprus to control the rate of inflation. It does not have its own currency, with the Turkish Lira (TL) being used in most day-to-day transactions. Significant government financial support is received from Turkey, and this is also paid in TL. Hence, the only action that the government can take is to try its best to mitigate the effects of inflation on its residents. To mitigate the impact of inflation, the salaries of public servants are generally indexed to reflect the rate of inflation experienced. Private employers also tend to adjust the salaries of their employees over time for the cumulative inflation. Firms and individuals are allowed to hold their financial assets in a range of hard currencies. For sources of retirement income, however, only the publicly sponsored Social Security Pension System is adjusted to reflect the current rate of inflation in the economy. This system covers both public and private employees as well as the self-employed. As a pay-as-you-go system (PAYG), it receives contributions from current employees to the system, and these are used to pay the pension payments of those who are retired.

The Provident Fund in Northern Cyprus is a mandatory savings scheme for employees, separate from the Social Security Pension System. The Provident Fund is a defined contribution pension system that is contributed to by both employees and employers. The required contributions by both employees and employers are 4% each of the declared income of the employees, and is designed to pay out a lump sum payment to an employee upon retirement. The contributions collected by the Provident Fund are largely invested in the securities and other liabilities of the government of Northern Cyprus. Hence, it is the government that ultimately determines the return that contributors receive on the funds they invest by periodically setting the interest rate on this fund. Unfortunately, the design of the Provident Fund lacks adequate inflation protection for the funds contributed, resulting in a real value loss during high inflation periods. This contrasts with the Social Security Pension System’s adjustment of pensions for inflation, underscoring the latter’s importance in protecting retirees’ purchasing power and well-being.

The importance of this issue cannot be overstated, as it touches upon the very fabric of social welfare and economic stability. The pension system, designed as a means of social security, is now posing an economic conundrum that requires immediate and thoughtful policy intervention. The following analysis is set against a backdrop of fiscal imbalances, with the aim of distilling the complexities of the pension system into actionable insights. It is imperative to understand that the conclusions drawn herein are not mere academic musings but are deeply rooted in the socio-economic realities of Northern Cyprus, with far-reaching implications for its populace and governance.

In this paper, we offer a detailed analysis of the Social Security Pension System of Northern Cyprus, proposing solutions to ensure its fiscal sustainability and equity. By examining this specific case, we aim to provide insights that can be applied to other countries facing similar challenges. The key recommendation is to move towards strengthening the institutional arrangements for the financing systems of inflation-adjusted pensions, to protect retirees’ purchasing power in high-inflation environments. This approach ensures that current workers’ contributions will fund retirees’ pensions, while keeping pace with inflation and maintaining retirees’ standard of living.

Literature review, historical context, challenges, and reforms

The economic environment in many developing and transitioning countries has been marked by high or fluctuating inflation rates, which have had a significant impact on the sustainability and effectiveness of their social security pension systems. Countries such as Argentina, Turkey, Venezuela, Brazil, Russia, Poland, Hungary, and Romania have faced similar challenges to those of Northern Cyprus, grappling with pension deficits exacerbated by economic instability (Dedák and Fiser Reference Dedák and Fiser2024; Lukyanets et al Reference Lukyanets, Okhrimenko and Egorova2021; Mesa-Lago Reference Mesa-Lago2021). For instance, Argentina, Turkey, and Venezuela have seen pension values eroded by high inflation, while Russia, Poland, Hungary, and Romania have struggled with demographic shifts and economic volatility that strain their pension systems (Jenkins Reference Jenkins1993; OECD 2021; OECD 2023).

In the past five years, several reform measures have been undertaken by the EU and other countries to reduce governments’ future contingent liability for funding public sector pensions and to provide long-term sustainability to their pension systems. Due to increases in life expectancy, a key element of the reforms has been to increase the age of retirement and/or to increase the number of years of service for a full pension. Such reforms have been taken in France, Belgium, Sweden, Denmark, Romania, the Netherlands, and Spain (Bravo et al Reference Bravo, Ayuso and El Mekkaoui2025; Hinrichs Reference Hinrichs2021; OECD 2023). In addition, there has been a move by governments to take a smaller role in providing pensions for their residents. For example, the Netherlands and Greece have shifted their public pension systems from a defined benefit system to one where defined contribution plans play an increasing role. Lithuania has significantly reduced the fiscal costs of its public pension system by stopping matching private contributions to private pension funds. Other countries such as Ireland, Greece, France and Spain have increased the required rates of contribution. Some others, such as France, have moved to strengthen the level of the minimum pensions provided while capping the size of the pension that can be obtained through the public pension system (OECD 2024).

A common issue across these countries is the reliance on government budgets to finance pension deficits, which poses a major risk to fiscal stability. This dependency creates a vulnerability where pension systems are subject to the broader economic policy decisions of the government. This dependency often leads to unsustainable practices and financial strain during economic downturns. A social security pension system should be designed to remain stable during fiscal crises; otherwise, the burden will fall on retirees.

The Social Security Pension System of Northern Cyprus has undergone significant reforms over the years aimed at harmonising the retirement benefits of public and private sector workers and addressing sustainability concerns. The earliest legislation was the 1976 Kıbrıs Türk Sosyal Sigortalar Yasası (Law 16/1976), which catered to self-employed individuals and private sector employees. This was followed by the 1977 Emeklilik Müessesesi Yasası (Law 26/1977) for civil servants, and the 1987 Emeklilik Yasası (Law 39/1987), which established the Emekli Sandığı Fonu, a fund for civil servants. Historically, the pension system in Northern Cyprus has faced sustainability issues. The Social Insurance Fund, established in 1977, was in surplus until the late 1990s. However, the state often did not pay its contributions, leading to a depletion of reserves and growing deficits. By 2006, the pension deficit stood at 7.27% of gross domestic product (GDP), partly due to early retirements under lenient conditions and the failure of the state to contribute its share (Cevik Reference Cevik2008). Before these reforms, Northern Cyprus’s pension system faced numerous challenges characterised by fiscal imbalances and inequities. Altiok and Jenkins (Reference Altiok and Jenkins2013a) highlight the structural inefficiencies and the growing fiscal burden of the civil service pension scheme. The scheme, largely unfunded, was plagued by issues such as early retirement, generous benefits, and a lack of actuarial fairness, leading to a significant strain on public finances.

Altiok and Jenkins (Reference Altiok and Jenkins2015) discuss the broader context of the Social Security Pension System, emphasising the disparities in benefits and contributions across different sectors. Their study suggests that before the reform, the structure of the laws and regulations governing the operation of the Social Security Pension System was marred by a lack of innovation and fiscal prudence, leading to social inequity and financial unsustainability.

The 2008 Sosyal Güvenlik Yasası (Law 73/2007), affecting both civil servants and private sector employees from 1 January 2008, standardised social security contributions at 9% for employees, with employers adding 11%, and mandated a 6% government contribution. These contributions add up to 26% of an employee’s gross income and were earmarked as follows: 16.5% (12.5% employee and employer and 4% government) for social security pensions, 6.5% for health, 1.5% for unemployment benefits, 1% for maternity, and 0.5% for workers’ accident compensation. This reform was critical for addressing fiscal and demographic challenges. It increased the retirement age and revised the benefit formula for the social security pensions to counter manipulation and inflation, fostering fiscal sustainability and aligning the system with international norms. Also included in this reform was the imposition of a 25-year minimum work requirement for full pension rights. All the critical items of this reform were analysed by Altiok and Jenkins (Reference Altiok and Jenkins2018).

Altiok and Jenkins (Reference Altiok and Jenkins2013b) explore the post-reform scenario, analysing how the changes affected the generosity of the social security system. Their study finds that while the reform has indeed reduced some of the system’s generosity, it has also brought about a more equitable and sustainable framework. The article emphasises the need for ongoing adjustments to ensure the system’s responsiveness to demographic and economic changes.

The 2012 amendment to the Sosyal Güvenlik Yasası included private sector employees who were employed before 2008 and were previously under the 1976 law. This amendment was part of ongoing efforts to address disparities and financial sustainability challenges in the pension system. This reform was aimed at creating a more equitable and sustainable pension system in Northern Cyprus, reducing public sector pension benefits and aligning retirement ages and conditions across sectors.

The 2008 and 2012 reforms in Northern Cyprus marked progress towards fiscal sustainability and equity in the pension system, aligning it with international norms. Despite these efforts, challenges persist with unresolved fiscal sustainability and imbalances between contributions and benefits.

Altiok and Jenkins (Reference Altiok and Jenkins2018) highlight the continuous need for reform to address these issues and secure the system’s long-term health. This study highlights the need for structural reforms that shield pension systems from the volatility of government budgets and presents specific recommendations. However, to date, no analysis has been undertaken to quantitatively construct a pathway of social security pension reform that would correct for the deficit in the social security system. This is the gap in the literature which this study aims to fill. The analysis indicates that by establishing dedicated funding mechanisms and stable pension formulas, countries can enhance the transparency, trust and long-term financial stability of their social security pension systems. The lessons drawn from Northern Cyprus’s experience are pertinent for policymakers in other regions, providing a framework for addressing the dual challenges of maintaining fiscal sustainability and protecting retirees’ incomes amidst inflationary fluctuations.

Research methodology

The methodology employed in this analysis follows two approaches. We employ standard public sector cash accounting to estimate the current level of the social security deficit, which is defined as the difference between current contributions and current pension payments. This approach is in stark contrast with the derivation of the quantitative estimates of the amount of subsidy received over the lifetime of different pension labour force cohorts. In these cases, detailed pension actuarial methods are employed. This involves the estimation of the present values (PVs) of the contributions made over the working life of these different cohorts. To calculate these PVs, we first estimate the amounts of contributions using the legal structure of the Social Security Pension System for the different levels of individual earnings. Second, a discount rate is required that reflects the financial cost of funds to the public sector. A real discount rate of 3% is employed (Jenkins Reference Jenkins1993), as this is the standard used in most actuarial estimations of the PV of pension assets and liabilities. To estimate the PV of the liabilities of the pension system created when people retire, we must use life expectancy estimates at different ages of retirement. The life expectancy tables used in this analysis are those of the World Health Organization (2023).

Our hypothesis is that, if the support ratio remains at the current level, parametric reforms such as increasing the age of retirement will not be sufficient to eliminate the deficit of the Social Security Pension System. If that is the case, then the only way to reduce the pension financing deficit is either to reduce the level of pensions being paid currently and in the future, or to increase the level of contributions being paid by current contributors to fund the current pension payments. Reducing the level of pensions being received by current retirees would be legally impossible and politically destabilising. A solution to the deficit issues that deals with both the current and future deficits is required. Hence, the investigation began to determine if the current ratio of the fiscal social security pension deficit would be approximately equal to the ratio of the PV of fiscal subsidy accrued over the lifetime of an individual to the PV of the pensions received. Furthermore, this study considered not only the social security system but also the Provident Fund, which was implemented as a defined contribution pension fund whose purpose was to complement the defined benefit Social Security Pension System. With the results of the quantitative analysis, we are then able to design a set of structural reforms that will eliminate both the current rate of social security pension deficit and the long-term fiscal subsidy. An analysis is being undertaken to see if this can be done by reallocating the contributions of employees and their employers without significantly raising the overall rate of contributions above their current levels.

Two aspects of the problem

When examining the financial situation regarding the Social Security Pension System, we need to consider two aspects of the problem. First, there is the immediate budgetary challenge of raising the funds from current contributors in any given year to meet the financial obligations to the current pension recipients. These individuals were promised certain amounts of income after retirement, which the government has an obligation to pay. The second aspect of the analysis is to investigate whether the structure of the pension system is designed so that over the lifetime of the participants, their contributions made while working would be sufficient to cover the costs of the payout of the pension benefits after retirement if they were invested and earned interest. This is an indication of the intergenerational fairness of the PAYG pension system.

The problem with a PAYG Social Security Pension System is one of contribution rates (CRs) and demographics – specifically, the ratio of contributing workers to retired pensioners. Another aspect is fairness: whether participants contribute enough during their working years to justify their expected pension benefits upon retirement, and whether the system’s design requires a subsidy from taxpayers to fulfil its pension promises. These issues are analysed further in this article.

Current funding challenge of social security pensions

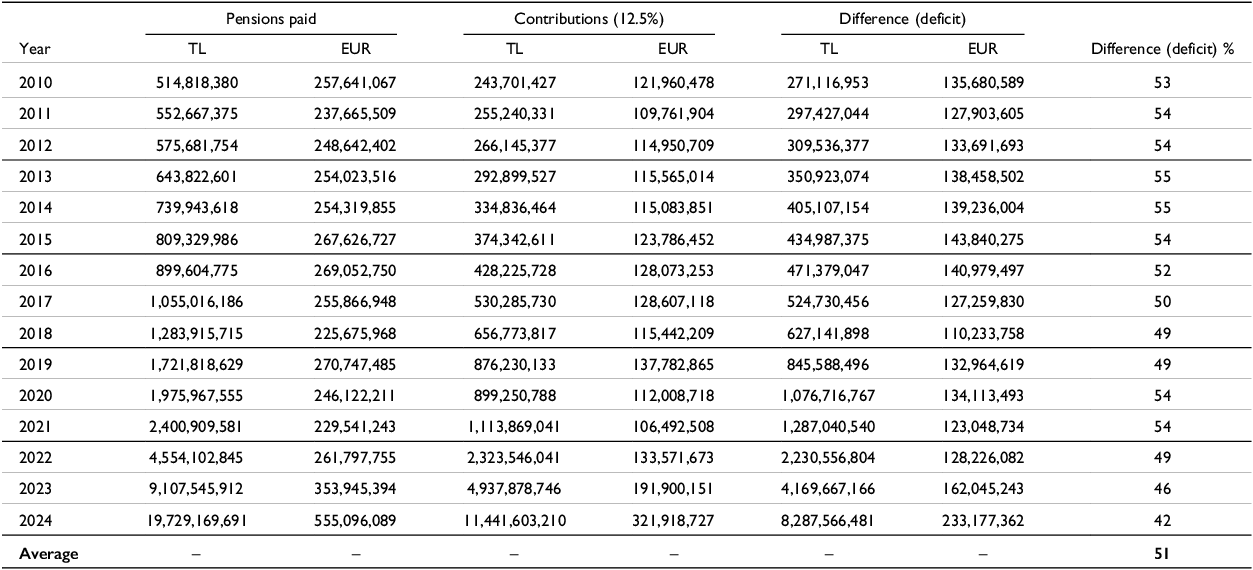

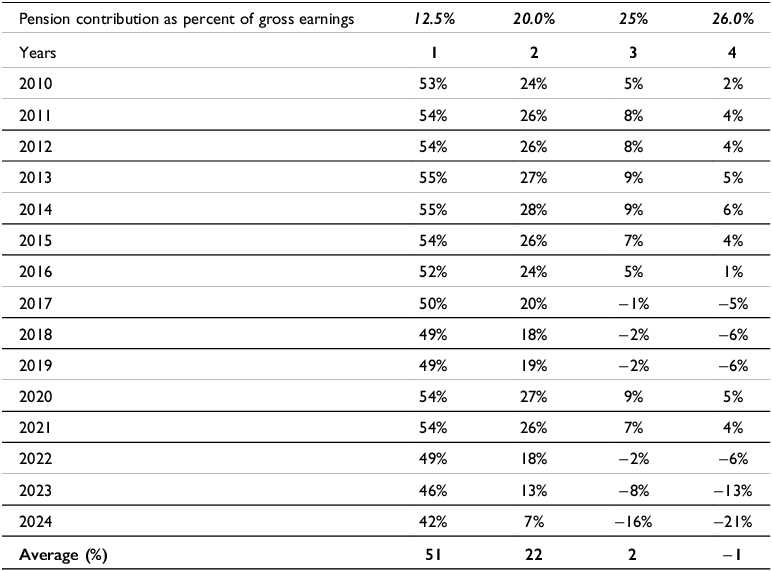

The Northern Cyprus pension system faces a fiscal challenge, with a consistent deficit. 51% of pension payments exceed the combined 12.5% contributions from employees and employers (Table 1), signalling a structural issue that undermines sustainability. This misalignment necessitates urgent reforms to secure the system’s future, underscoring the pressing need for a financial strategy that reduces reliance on the general budget and ensures long-term viability.

Disparity between pension contributions and payouts in northern Cyprus (TL and EUR). Converted to EUR at the average exchange rate of the relevant year

The disparities between current contributions and current pension payments were acute throughout the whole period from 2010 to 2024, as reported in Table 1. In 2024, total contributions amounted to 11.4 billion TL (321.9 million EUR) while the total pensions paid out amounted to 19.7 billion TL (555.1 million EUR). The deficit, amounting to 8.3 billion TL (233.2 million EUR), or 42% of the total pension payments in that year, illustrates the magnitude of the imbalance. In the same year, the total budget for education was about 9.9 billion TL (278.5 million EUR). It is also worth mentioning that this deficit figure represents the burden on the budget resulting solely from the Social Security Pension System. Taken together with the deficit of the civil servant pension system, which no longer accepts new entrants, and which is financed almost entirely from the general budget, the severity of the pension problem becomes more obvious.

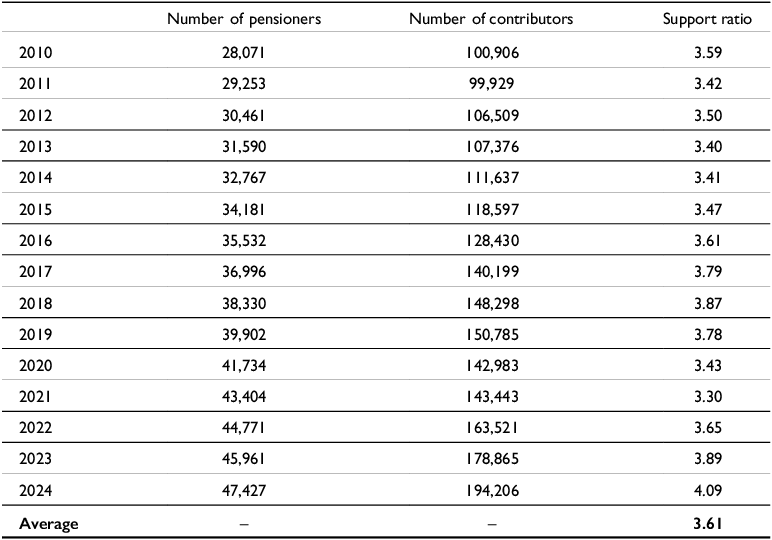

The average support ratio, which measures the number of workers contributing to the pension of one retiree, was 3.61 between 2010 and 2024, underpinning the demographic challenge of a working population required to support a retiree cohort. If the CR is not increased, the current support ratio of 4.09 in 2024 would need to increase to 7.06, necessitating a rise in the number of contributors from 194,206 to 334,876, a surge of 1.72 times the current figures, to achieve a zero-deficit scenario. The support ratios between the years 2010 and 2024 are presented in Table 2 below.

Support ratios (2010–2024)

To achieve a zero-deficit scenario without increasing the CR, a large influx of young immigrant workers who are registered in the social security system would be crucial in the short term. This would entail not only expanding the workforce but also ensuring that these new entrants are integrated into the formal economy. Moreover, it is imperative to ensure that all working individuals, both native and immigrant, are duly registered and actively contributing to the pension system. The unregistered or informal employment sector poses a significant challenge in this regard, as individuals in this sector do not contribute to the pension fund. Strengthening labour market regulations and enhancing enforcement are critical steps in this direction. These measures would not only increase the number of contributors but may also, if coupled with several structural reforms, ensure the sustainability of pension payouts.

The COVID-19 pandemic in 2020 and 2021 led to elevated unemployment and economic downturns, reducing pension contributions and exacerbating system deficits. By 2024, the level of employment had largely recovered, and the level of the deficit fell to 42%, which was less than the 15-year average of 51%. This situation underscores the vulnerability of pension systems to macroeconomic shocks, particularly those affecting employment.

The Provident Fund, as a government-managed defined contribution pension scheme, offers tax-deductible contributions and tax-free withdrawals at retirement. This scheme is mandatory for employees and employers, yet optional and notably unused by the self-employed despite its favourable tax treatment compared to similar schemes like the 401(k) in the USA or RRSPs in Canada. This lack of voluntary engagement underscores its ineffectiveness as a retirement savings vehicle.

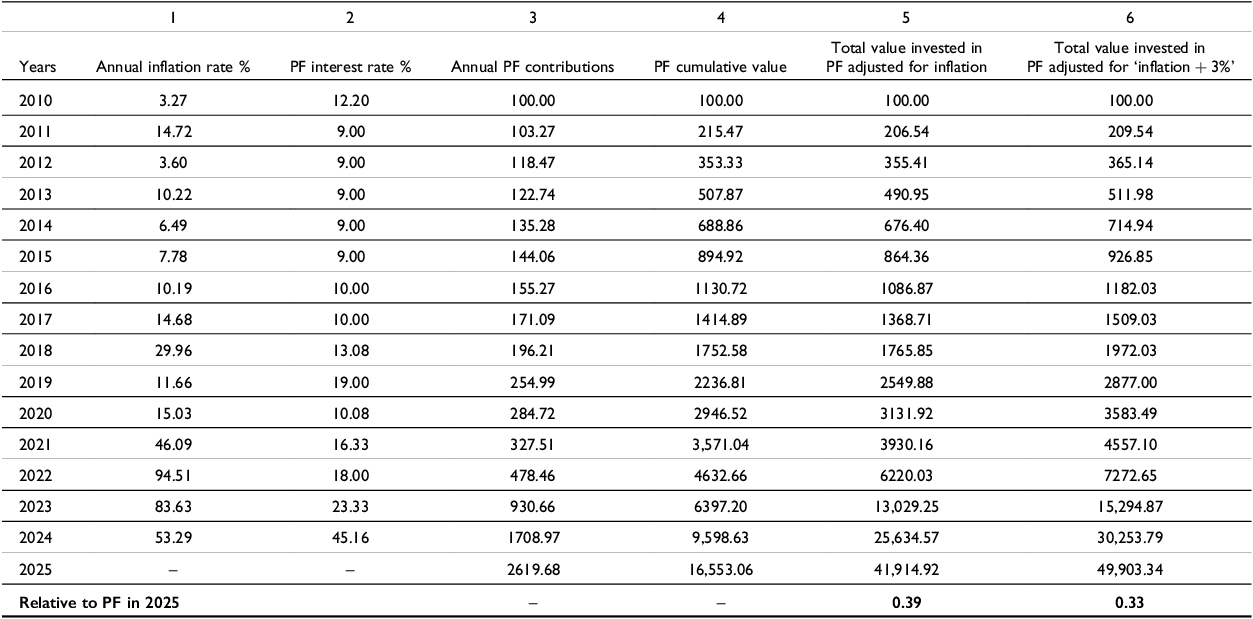

Table 3 below presents a comparative analysis of investment returns in the Provident Fund against other inflation-protected investments over a period of 15 years (2010–2024). It shows the value of a series of annual cumulations of the Provident Fund, with its government-set interest rates, over 15 years and compares this to two alternative situations. Firstly, the outcome if these contributions had been invested in an inflation-indexed account earning a zero real interest rate and secondly, if they had been invested in an inflation-indexed account earning a real interest rate of 3%.

Comparative analysis of provident fund returns in northern Cyprus (TL) vs. Inflation-adjusted investments (2010–2024)

Note: PF indicates Provident Fund.

In this simulation, an annual contribution is made each year to the Provident Fund from 2010 to 2024. This contribution is set at 100 TL (48 EUR when converted at the 1 January 2010 exchange rate) in 2010, and the amount contributed is then increased with the annual rate of inflation each year until 2024. Column 3, ‘Annual PF contributions’, reflects these yearly contributions.

The second column in Table 3 represents the Provident Fund interest rate in Northern Cyprus, serving as an indicator of the potential growth of retirement savings. The fourth column shows the cumulative values of the Provident Fund over time by investing 100 TL annually into the fund. By 2025, this investment accumulates to 16,553.06 TL (449 EUR), a stark contrast to the cumulative value of the other two benchmarks used for evaluating the relative investment performance. Column 5 serves as a baseline for understanding the real return on investments. If the annual contributions of 100 TL per year starting in 2010 were adjusted annually only for inflation, the cumulated amount would have grown to 41,914.92 TL (1,139 EUR) by 2025.

By 2025, the Provident Fund’s real value for an individual was just 39% of what it could have been if it had been adjusted for inflation annually. Because the balances in the Provident Fund are denominated in TL, the periodic episodes of high inflation experienced by Turkey and Northern Cyprus erode the real value of the fund’s balances held by individuals.

The situation is much worse if the alternative asset being held to finance retirement earned a real rate of return of 3% above the rate of inflation. For example, Turkish government-issued bonds denominated in $US during this period have yielded a real rate of return of more than 3%. The same has been experienced by those individuals who purchased land in Northern Cyprus during this period. Such alternative assets earning a real rate of return of 3% would have a cumulative value of 49,903.34 TL (1,356 EUR), while the cumulative value of the funds invested into the Provident Fund would have yielded only 33% of this amount (Table 3, column 6).

In Northern Cyprus, there are many small plots of land and apartments, which people buy as an asset to provide protection against the erosion of the value of their savings by inflation. Given the increased attractiveness of Northern Cyprus as a place for people to purchase holiday homes, such investments in land have proven to be a very high-return investment. In contrast, investments in the Provident Fund have yielded only negative real returns.

It is clear from the above analysis that the Provident Fund is a public institution that should be abolished in its present form. It serves primarily as an instrument to allow the government, through the effects of inflation, to erode the pension savings of employees. Contributions to the Provident Fund have been largely borrowed by the government at negative real interest rates and not paid back. This method of investing through the Provident Fund comes at a cost to the retiring participants of the scheme.

It is not surprising that the self-employed completely avoid contributing to the Provident Fund. This analysis, however, provides some clues as to the direction that reforms of both the Social Security Pension System and the Provident Fund might take to create a single sustainable public pension system in Northern Cyprus.

Table 4 reports on an extended analysis of the existing and alternative contribution strategies for financing the Social Security Pension System in Northern Cyprus. To understand their impact on the pension fund deficit, a simulation is made using the actual pension benefits and contributions from 2010 to 2024 as the basis for the analysis. This table utilises basic information from Table 1, focusing on the pension deficits that would have existed under different CRs.

Contribution rates vs. pension deficits: A 12-Year analysis in northern Cyprus

Table 4, column 1, reports on the annual deficits as a percentage of the total pension benefits paid out over the year. Over the 15-year period, the pension system consistently operated at a deficit, ranging from 42% to 55% under the standard 12.5% CR. This indicates a persistent gap between the funds required to sustain pension payouts and the contributions received. Other than the COVID years, 2021 and 2022, there was a slight reduction in the deficit after 2016. This is due to the reduction in average pension benefits received per recipient as the proportion of the population of retirees with pensions determined by the new formula increased.

In Table 4, column 2, the entire 20% social security contribution (9% from the employee and 11% from the employer for all the social security programmes) is assumed to be allocated to financing the pension component of social security. This, in fact, has been the way the government has been financing a major part of the social security pension benefits for some years. Even when all the 20% contributions that employees and employers make to the social security system are applied to finance the pensions, the average deficit is still equal to 22% of the benefit payments made over this period (Table 4, column 2).

As a result of the diversion of funding from the public health care system, the ability of the public sector health system to meet the demand for such services from the residents of Northern Cyprus has been significantly eroded. In response to this gap between the demand and the public supply of health services, a much better-quality private health care system has developed, largely through an increase in the number of private hospitals and clinics. These private hospitals, which are of varying quality, operate on a fee-for-service basis. Only poor individuals and households depend primarily on the public health care system for health services.

The data further demonstrate a troubling trend: even with a hypothetical allocation of the full 20% contribution toward pensions, there would still exist a deficit, albeit a reduced one. This persistent deficit, while smaller, continues to highlight the inadequacies of the current funding model. The sustainability of the Social Security Pension System is not guaranteed with such ad hoc financing.

Some stakeholders argue that a perceived pension deficit is mitigated with the government’s 6% additional pension contribution, as shown in Table 4 column 4, reducing the deficit from 52% to −1%. However, this 6% transfer from general taxation, though legislated, still burdens the state’s budget, masking the pension system’s inability to be self-sustaining. The need for government funding to balance the pension system indicates an operational deficit, especially after reallocating funds from health and unemployment insurance to pensions.

It is imperative to acknowledge the true financial state of the pension system, which requires a reform that addresses both its structural deficits and its long-term viability without relying on external government contributions that may mask the system’s financial health. The importance of the public Social Security Pension System in providing income support to retirees in such an inflationary environment cannot be overemphasised. It is critical that the funding of this system be properly institutionalised in a way that is transparent and sustainable for future generations of retirees.

We propose merging the Provident Fund with the Social Security Pension System to address budgetary issues. Currently, employees and employers each contribute 4% of gross income to this government-administered, tax-deductible fund. Upon reaching age 55, employees can withdraw their contributions and interest tax-free. However, the government, not future retirees, benefits from these funds, borrowing at rates below inflation. Our proposal suggests no change to the existing or historical cumulative balances held in the Provident Fund. The existing balances would be paid out according to the existing laws and regulations. Hence, this will not impose a greater burden on the finances of the government.

A possible way to fund the Social Security Pension System is to increase to 25% the combined rate of employees’ and employers’ contributions and those of the self-employed to the social security system. The results presented in Table 3, column 3, suggest that this rate could potentially eliminate the pension system’s deficit. This outcome is likely, as the deficit has been falling slightly since 2015 (except for the Covid years) due to the application of the new pension formulas to new retirees.

The current combined rate of contributions to the Social Security Pension System and the Provident Fund of 28% can be restructured in three different ways to enhance the system’s sustainability.

-

1. Increase pension contributions from 12.5% to 25% of gross employee income eliminates the current 8% required contributions to the Provident Fund and raise the retirement age to 65 years old. By increasing the pension contributions to 25% of gross income in combination with an increase in the retirement age to 65, the sustainability of the Social Security Pension System’s financial health is guaranteed (Table 4, column 3). This approach focuses solely on enhancing the primary source of pension funding.

-

2. Integrate unemployment insurance and the Social Security Pension System (total CR of 28%). Here, we propose increasing pension contributions to 25% of gross income and adding a 3% premium for unemployment insurance, totalling 28%. This unemployment insurance provides additional security, helping maintain stability for employees during periods of joblessness and contributing to the overall resilience of the social security system.

-

3. Increase Social Security Pension System contributions while placing 3% of contributions into a reformed Provident Fund that only invests in hard currency assets (total 28%). Another alternative is to increase the pension contributions to 25% of gross income, plus a 3% Provident Fund contribution. The Provident Fund would then be invested in hard currency financial assets that are denominated in dollars or euros. This strategy hedges against local currency devaluation and inflation, ensuring more stable and potentially higher returns for the fund.

In each of these scenarios, while there is an increase in total contributions to the Social Security Pension System, the overall income deductions for the contributions made toward retirement either remain the same or are reduced. These reforms aim to guarantee the solvency and sustainability of the Social Security Pension System without reducing the take-home pay of employees. Each approach offers a unique solution to the pension system’s challenges, focusing on bolstering funding through increased social security pension contributions while providing additional financial security measures or more strategic investment options.

All these proposals imply a uniform CR for all, including the self-employed, who currently pay 18.5% without the Provident Fund. This increase aims to bolster government revenue, even if the Provident Fund component is dissolved, by enhancing social security contributions to a flat rate of 25%, thereby restructuring the pension system to better withstand inflationary pressures and provide more substantial retirement benefits.

According to the Organization for Economic Co-operation and Development (OECD 2021), participation in pension schemes is compulsory in 34 member nations, encompassing both the public and private sectors. These countries typically feature pension systems where contributions are more directly linked to the pension system. Within this cohort, 11 nations – Austria, Czechia, Denmark, Finland, Germany, Iceland, Italy, Lithuania, Luxembourg, Slovenia, and Turkey – extend their pension contributions to cover disability or invalidity benefits. As of 2020, the average effective CR for pensions at the average income level in these countries was 18.2%. Italy has the distinction of having the highest mandatory CR, at 33%. Other countries with notably high CR, between approximately 26% and 28%, include Czechia, France, and Greece.

To compare the deficits in Northern Cyprus and other countries, it is worth mentioning that the pension systems in some European countries are also facing significant financial challenges, as highlighted by Hervé and Monika (Reference Hervé and Monika2023) and Gillet and Vasse (Reference Gillet and Vasse2022). In France, pension spending constitutes approximately 14% of GDP and the current deficit in the pension system is 2% of GDP. In Northern Cyprus, social security pension spending alone (excluding civil service pension) is around 6% of GDP, and the pension deficit being financed by the government is around 3% of GDP. This provides an indication of the relative imbalance between current pension payments and contributions in the Social Security Pension System in Northern Cyprus relative to EU countries.

The other major components of the social security system are the publicly supplied health services and the income support to individuals with very low incomes or disabilities. It would be more equitable to have such current expenditures financed out of the value-added tax system. This system has a much broader base as it is applied to the current consumption expenditures of residents rather than simply the wages and incomes of employees and the self-employed.

Several studies have addressed the problems with the financing of health care through social security or pension contributions. The World Bank (2014) emphasises the importance of how countries finance health care and its impact on the performance and outcomes of health systems. It discusses different methods of mobilising revenues for health care and the role of public and private insurance in health financing. The World Bank’s interventions in health financing across various countries are outlined, highlighting the complexity of health financing and its separation from other social welfare mechanisms such as pensions.

Holzmann (Reference Holzmann2012) addresses the changing dynamics of global pension systems and their reforms, driven by various factors including economic crises and demographic changes. The focus here is on the pension systems themselves, with discussions on reforms across different pension pillars. It provides a context for understanding how pension systems are distinct entities that face unique challenges, separate from health care financing. Dorfman and Palacios (Reference Dorfman and Palacios2012) review the World Bank’s framework for analysing pension programmes, focusing on challenges such as coverage, adequacy, and sustainability. They highlight the distinct objectives and challenges of pension systems, reinforcing the idea that health care financing might require a different approach.

In numerous US states, policymakers have actively tried to diminish the liabilities associated with public pensions and retiree health benefits, driven by substantial underfunding issues. These alterations have the potential to impact decisions regarding social security claims and workforce participation by modifying the benefits gained from continued employment. Ni and Podgursky (Reference Ni and Podgursky2016) and Salinas (Reference Salinas2017) are examples of studies that have utilised administrative records from states that have undergone modifications in retirement or health care benefits. These studies specifically investigate how such changes influence employment trends in the public sector.

Long-term structural fairness of the Social Security Pension System

The second dimension of the Social Security Pension System is its long-term intergenerational fairness. The central question is whether the recipients of the pension system have paid enough into the system in the contributory phase when they were working to warrant the amount of pension benefits they are receiving.

To conduct this analysis, one needs to employ an actuarial model of the pension system that can be used to evaluate the impact of the different variables and parameter values used in the design of the pension system. Such a model is discussed briefly below.

The model

In our analysis, we employed the Altiok and Jenkins (Reference Altiok and Jenkins2015) actuarial model, a sophisticated tool developed to assess the Social Security Pension System of Northern Cyprus, focusing on financial sustainability and social equity. This model integrates demographic (age, gender, life expectancy), economic (wage growth, inflation rates), and pension system parameters (replacement rate, retirement age) to project the system’s future viability. Key outcomes include estimates of pension contributions and benefits’ PV, potential system deficits or surpluses, the impact of demographic changes, and the effectiveness of pension reforms. These insights are critical for evaluating policy reforms aimed at ensuring the pension system’s long-term sustainability and fairness. For further technical details, the original paper by Altiok and Jenkins (Reference Altiok and Jenkins2015) is recommended.

The key features of Northern Cyprus’s Social Security Pension System

The Social Security Pension System in Northern Cyprus, reformed in 2008 and refined in 2012, has several key features:

Benefit Formula: The actual monthly pension amount a retiree receives at the point of retirement is determined by multiplying the average wage declared in the country one year prior to retirement by the replacement rate (RR). The RR is calculated as follows: 2.5% per year for the first 15 years, and an additional 2% each year beyond this.

Retirement Age: Previously, under the Civil Servants Pension Scheme and Social Insurance Scheme, retirement was possible at or even below the age of 50, with the average retirement age being 55 for both civil servants and private sector workers. The new Social Security Pension System has increased the retirement age for new entrants to a minimum of 60, which is a step toward sustainability, though it is still below the EU average of 64.3 for men and 63.5 for women (Yanatma Reference Yanatma2023).

Contribution Rate (CR): The CR is 12.5% of the monthly gross salary for all new civil servants employed after 2012 and for all private sector employees.

Replacement Rate and Calculation of Pension Benefits: The 2008 reform partially addressed the issue of the generous RR of the Civil Servants Pension Scheme and the Social Insurance System applicable to private employees. For civil servants, the RR was 55.79% of the final year’s income. For social insurance for private sector workers, the RR was 70% of the highest four years out of the last seven years’ income. This formula, which weighed the incomes of only the four best years of the last seven years of working, meant that the Social Insurance System was subject to manipulation and abuse.

The new system calculates pensionable income in an innovative way to prevent manipulation and account for inflation. The declared incomes of a contributor are calculated annually relative to the average income of all contributors in that year throughout their working life. The overall average of these ratios, excluding the final year’s income before retirement, is multiplied by an RR. This rate is formulated by multiplying the first 15 years of service by 2.5% and adding 2% for each additional year of service.

For the analysis in calculating the average RR or required CR, the sets of both male and female contributors are broken down into equal groups, each with an equal number of individuals. There are those who retire at age 60, having contributed for 25 years, those who retire at age 60, having contributed for 30 years, and those who retire at age 65, having contributed for 35 years.

Results

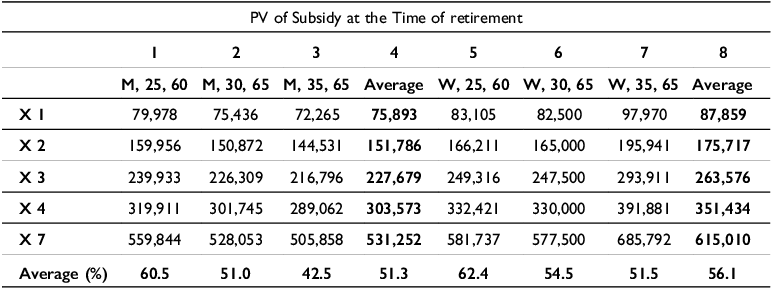

The pension system’s gender dynamics and the impact of lifetime earnings on subsidies become evident when examining the PV of subsidies at retirement, excluding widows’ payments. In the analysis reported in Tables 5 and 6, a real discount rate of 3% is used. This is a rate frequently used in the actuarial estimations of pension plan sustainability. The results presented in Table 5 delineate scenarios based on different service years and retirement ages for both men and women. The deficit figures presented in Table 5 are in Euros for stability against Turkish Lira inflation using the January 2023 exchange rate of 20.00 TL/EUR. The life expectancy tables published by the World Health Organization for Cyprus were used in making the estimations in PV terms presented in Table 5.

Pension subsidies in northern Cyprus (EUR, January 2023 price level, 1 EURO = 20 TL) with 1% increase in real wages and age earning Premium (AEP)

Notes: PV = Present value, AEP = Age Earning Premium (1.83% real for men and 1.47% real for women).

Contribution rate adjustments to attain fiscal equilibrium in the pension system with 1% increase in real wages and age earning premium (AEP)

Note: CR = Contribution rate, RR = Replacement rate.

These estimates also incorporate an annual real growth rate in wages of 1% per year. This means that the starting real wage for new entrants into the labour force grows at 1% a year. In addition, wages over the career of the individual also increase annually due to increased work experience. The growth rates in real wages as people obtain more work experience in Northern Cyprus have been estimated from labour force wage data at 1.83% per year for men and 1.47% per year for women.

Table 5, column 1 shows that for men with 25 years of service retiring at 60 the subsidy – a measure of the PV of the pension system’s payments upon the date of retirement relative to the PV of individual’s contributions at this same point in time – ranges from a deficit of 79,978 EUR for someone declaring a minimum wage income during their contributory period to a subsidy of 559,844 EUR at a declared income of seven times the minimum wage. Women, on average, receive a higher subsidy, reflecting their longer life expectancy and, implicitly, the longer duration of pension payments. In Table 5, two further estimates of the PV of the pension deficit are made for men and women retiring at age 65. In one case (column 2 and column 6), the individuals have worked for 30 years, in the second scenario (column 3 and column 7), the individuals have worked for 35 years. Moving the retirement age from age 60 to 65 will certainly help to reduce the deficit, but it is far from a complete solution to the deficit problem. In the case reported in Table 5, raising both the retirement age to 65 and the required number of years worked from 25 to 30 reduces the deficit by 9.5% for men and 7.9% for women. If the required number of years of work is increased from 30 to 35 years, the deficit would decrease by 8.5% for men and 3.0% for women.

The average subsidy over the three scenarios for men is 51.3% of the pension income they receive, while for women it is 56.1% (Table 5, columns 4 and 8). These rates of subsidy are quite close to the average annual budgetary deficit (51%) experienced by the pension accounts of the social security system over the past 15 years. While a number of countries have increased the age of retirement as a major component of their pension reforms, in Northern Cyprus, the gap between the rate of contribution and the pension benefits received is too far out of balance. An increase in the age of retirement to 65 and an increase in the number of years an employee is expected to work would, in total, only reduce the amount of the deficit by 30% (from 60.5 to 42.5) for men and 18% (from 62.4 to 51.5) for women. A more fundamental reform of how pension benefits are financed is required.

This analysis reveals that the current Social Security Pension System in Northern Cyprus is characterised by significant subsidies that vary by gender and income level. The findings suggest that reforms aimed at addressing these inequities, possibly through a restructuring of contribution levels and a re-evaluation of benefit formulas, are imperative to maintain the system’s financial viability while ensuring fairness across different demographics.

Importantly, the proximity of the current contribution deficit to the long-term deficit for individuals unveils a unique opportunity. This closeness suggests that some solutions might simultaneously address both the immediate fiscal challenges and the long-term sustainability issues. For example, a recalibrated CR that addresses the current shortfall could also be structured to align with the lifetime contributions required for sustainable long-term payouts. This dual-purpose approach would not only resolve the immediate financial strain but also lay the groundwork for a more equitable and enduring pension system. Such a strategy would require careful analysis to balance short-term fiscal needs with long-term actuarial fairness, ensuring that the system remains solvent and equitable for both current and future retirees.

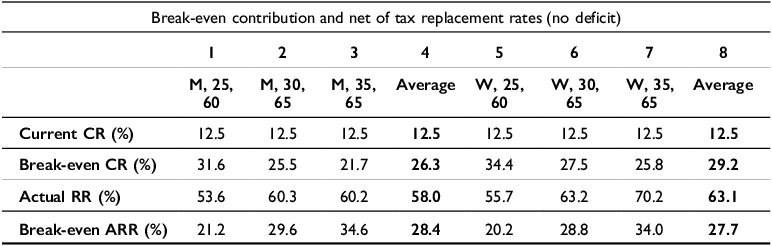

Table 6 illustrates the break-even CR and the break-even RR that give zero-deficit outcomes. An examination of the break-even CR necessary to eliminate the pension deficit reveals a stark contrast between the current and required rates to maintain sustainability. If we consider raising the retirement age from 60 to 65 while raising the number of years of service to 30 years, the required CR would be 25.5% for males and 27.5% for females. If the increase of retirement age were also accompanied by 35 years of contributions, which is the most likely scenario for the social security system, the standard CR of 12.5% falls significantly short of the break-even rate of 21.7% for males, which would be needed to maintain the system without a deficit over the long term (Table 6, column 3). For women retiring at age 65 with 35 years of service, the required CR is 25.8% (Table 6, column 7). Combining both men and women over all the two scenarios where the retirement age is raised to 65 years old would require a CR of exactly 25%. This suggests that a reform that would increase the retirement age to 65 and approximately double the current contributions is needed to both stabilise the budgetary impact of the system and to ensure a basic level of long-term fairness in the system.

When the CR is 12.5%, the current RRs as a percentage of the net of tax income for the three scenarios range between 53.6% and 60.2 % for men and from 55.7% to 70.2% for women. To align the RR with the current CR of 12.5%, it would need to be drastically reduced to between approximately 20% to 35% for both men and women (Table 3, row 4).

This is comparable to the RR of the Canadian pension plan (33%), which has approximately the same CR (11.9%) as the one levied in Northern Cyprus. In the case of Canada, the pension benefits accumulate at slightly more than 1% a year, while for Northern Cyprus the promised annual pension benefits cumulate at a rate of between 2% and 2.5% of the income earned in each year employed.

These findings point out the trade-offs that policymakers face. First, they can increase the CR to about 25% while eliminating the inefficient Provident Fund system. This would ensure pension stability without any net cost to the participants in the Social Security Pension System. However, the Ministry of Finance will need to find alternative sources of funding from those they now obtain by plundering the contributions of the participants of the Provident Fund. Second, the authorities could maintain the CR at 12.5%, which would necessitate a considerable reduction in pension benefits, and hence the RR, at least over time. This second alternative would lead to public discontent.

It has often been suggested that the solution to the current budgetary deficits of the Social Security Pension System is to force private sector employees to declare a higher percentage of their employment income to the social security system and hence increase current contributions. The analysis of this policy option underscores a systemic challenge: if wage declarations are forced to increase, the immediate inflow of contributions improves the current state of the pension fund. However, this is a double-edged sword: while higher declared incomes would yield higher contributions now, this will lead to significantly larger pension obligations later, potentially creating an even more unsustainable systemic problem when these individuals retire.

In essence, the strategy of encouraging higher wage declarations to address the current underfunding of the pension system could inadvertently guarantee future financial instability. This paradox highlights the need for a strategic approach that balances immediate fiscal needs with long-term pension liabilities. The increase in short-term contributions based on increasing declared incomes may provide temporary relief but could exacerbate the subsidy burden in the long run, especially as the population ages and more retirees draw on the system at higher subsidy levels.

The analysis of subsidies based on varying wage declarations reveals a crucial aspect of pension economics: the intergenerational transfer of fiscal responsibilities. Policymakers must consider the repercussions of today’s contribution policies on tomorrow’s pension payouts. A sustainable pension system requires not only adjustments to current contributions but also a forward-looking strategy that anticipates future demographic shifts and economic conditions.

In summary, the results of this analysis confirm our hypothesis that changes solely in the parameters of the social security system related to delaying the age of retirement will not solve the current and future fiscal deficit of this pension system. This has been a common element of pension reforms in the OECD countries. While it is also needed in the Northern Cyprus system, it is not sufficient to address the fiscal problem. Furthermore, reallocating the contributions made to the defined contribution Provident Fund to finance the Social Security Pension System and freezing the Provident Fund will address both the current and future deficits facing the Social Security Pension System. In addition, it would eliminate the risk of inflation eroding the savings of employees who have, until now, been required to make contributions to the Provident Fund. These results also show that this reallocation of contributions would give retired employees an acceptable rate of income replacement that is inflation-protected.

The situation at this time in Northern Cyprus is very similar to the situation facing many of the transitional countries, such as Hungary, Poland, Slovakia, Bulgaria, Croatia, Estonia, Latvia, Lithuania, and North Macedonia, in the early years of this century (Ortiz et al Reference Ortiz, Durán-Valverde, Urban, Wodsak and Yu2019; Sokhey Reference Sokhey2018). Many transitional countries in the 1990s instituted mandatory contributions to defined contribution pension funds that invested in financial assets, mainly of the private sector. This was referred to as the second tier of the pension system in these countries. In the period following 2010, these countries largely eliminated this requirement and transferred the assets to support the financing of the public sector pension system. The populations of these countries felt more secure with an enhanced public sector pension system that provided inflation-protected benefits rather than relying on the performance of their investments in private assets to finance their retirement. In most of these countries, when the individuals were given the option, they chose to opt out of the private pension plans and moved their private pension assets to support a public sector guaranteed option. While each of these countries has its own institutional peculiarities, the basic situation is the same as that now facing the members of the pension system in Northern Cyprus. There is a public pension system that, until the present time, has provided reliable inflation-protected pension benefits, while at the same time, the assets in the defined contribution plan have been poorly managed and underperforming. The proposed solutions for Northern Cyprus parallel the policies implemented by the transitional countries. These countries transferred the funding of the defined contribution component to strengthen the sustainability of the public defined benefit pensions component, which is preferred by the pension participants.

Conclusion and policy implications

The pension system in Northern Cyprus faces significant challenges, which manifest in the form of structural deficits and sustainability concerns. The analysis reveals that over the last 15 years, the system has operated under a substantial fiscal strain, with an average subsidy of 50% for pensions, evidencing a mismatch between contributions and payouts.

This subsidy is not uniformly distributed across different income groups. Lower-income groups receive smaller subsidies in absolute euro terms, highlighting an inequitable burden distribution that further entrenches socio-economic disparities among the elderly population.

To move toward a more equitable and sustainable path, a reform of the Social Security Pension System financing is imperative. It must address the immediate fiscal imbalances and lay the groundwork for a pension system that is robust enough to withstand demographic changes, economic fluctuations, and the evolving needs of society. Due to the periodic bouts of high rates of inflation, there is a great need for a publicly supported pension system that protects the elderly from the financial losses to savings caused by inflation.

The proposed reforms that address these objectives are as follows:

Reform of the financing of the Social Security Pension System and increasing the Retirement Age: The proposal is to direct all components of current social security contributions (including health, unemployment insurance and others) plus 5% of gross income that is currently contributed to the Provident Fund (for a total rate of contributions of 25%) towards social security pension funding. In addition, it is recommended to increase the retirement age to 65 to reflect the increase in life expectancy of the population. This approach not only addresses the immediate concern of funding current pension payments but would also move the system toward a state of long-term financial equilibrium and sustainability.

By equating the PV of contributions with the PV of pension payouts, this strategy offers a more equitable system where individuals’ contributions are more closely aligned with their eventual pension benefits. A key element of this reform is that the proposed adjusted financing formula, coupled with the pay-as-you-go system of financing, would protect the pension income of the retired population from real losses due to inflation.

Reform of the Provident Fund: Given the erosion of the Provident Fund’s value due to inflation, the recommendation is to eliminate the Provident Fund. This would enable individuals to decide how to save for their future, potentially through more reliable and profitable options.

Redistribution of Government Contributions: The government contributions and subsidies currently given to the pension system should be focused on the vulnerable, retired poor, both in terms of income support as well as health care.

Reforms to achieve Fairness of income support in retirement: The proposed reforms deal with the unfairness of the subsidies; by eliminating the subsidies, high-income groups are no longer receiving a greater subsidy out of general revenues than lower-income groups. However, there are those in society who, for various reasons, are not eligible for a large enough social security pension, or perhaps receive no pension, for them to live a life out of poverty. To avoid creating adverse incentives for those contributing to social security pensions, it is better not to try to cross-subsidise different groups of individuals through the social security system. Such basic income support for the impoverished aged is best paid for through general taxation.

The implications of this research extend well beyond the immediate context of Northern Cyprus, providing a critical lens through which to view the sustainability and fairness of pension systems globally. As nations worldwide confront aging populations and the resultant pension pressures, the lessons drawn from Northern Cyprus’s reform initiatives offer valuable insights into the dynamics of pension management, reform, and policy adaptation in response to fiscal and demographic challenges. By integrating these insights into the broader discourse on pension sustainability and social security reforms, this study contributes to a more comprehensive understanding of how pension systems can be designed to be both resilient and equitable.

Competing interests

None.

Open access

Open access