I. Introduction

Share repurchase programs have become the cornerstone of corporate payout policies, with corporations worldwide returning over $1.2 trillion via stock buybacks in 2019 alone, primarily through open-market repurchase programs (OMR).Footnote 1 An OMR gives the firm the right, but not the obligation, to buy back its shares on the open market.Footnote 2 Evidence suggests that managers use this discretion and their private information to execute buybacks at favorable prices (e.g., Ikenberry et al. (Reference Ikenberry, Lakonishok and Vermaelen2000), Brockman and Chung (Reference Brockman and Chung2001), Cook, Krigman, and Leach (Reference Cook, Krigman and Leach2004), and Dittmar and Field (Reference Dittmar and Field2015)). Traditionally, the literature asserts that such informed buybacks hurt shareholders.Footnote 3 A recent Wall Street Journal article summarizes this view:

managers who know the stock is cheap use open-market repurchases to secretly buy back shares, boosting the value of their long-term equity. Although continuing public shareholders also profit from this indirect insider trading, selling public shareholders lose by a greater amount, reducing investor returns in aggregate.Footnote 4

Such concerns have contributed to a move toward repurchase structures with less managerial discretion, such as accelerated share repurchases (Chemmanur, Cheng, Wu, and Zhang (Reference Chemmanur, Cheng, Zhang and Wu2022)) and 10b5-1 plans (Bonaime, Harford, and Moore (Reference Bonaime, Harford and Moore2020)).

This article challenges the conventional wisdom—that informed buybacks inherently harm shareholders—by showing that this premise rests on the incomplete assumption that only the manager is informed. Prior studies of buybacks and adverse selection focus on settings where the firm is the sole informed party (e.g., Barclay and Smith (Reference Barclay and Smith1988), Oded (Reference Oded2005), Bond and Zhong (Reference Bond and Zhong2016), Kumar, Langberg, Oded, and Sivaramakrishnan (Reference Kumar, Langberg, Oded and Sivaramakrishnan2017), and Bond, Yuan, and Zhong (Reference Bond, Yuan and Zhong2025)). In practice, firms compete against other parties—hedge funds, proprietary traders, and informed institutions—for trading profits.Footnote 5 In this richer setting, the effects of buybacks depend critically on how they are executed. Buybacks that reflect the manager’s private information compete against outside speculators, reducing their trading profits. But buybacks also affect the firm’s per-share value: buying undervalued shares generates gains while buying overvalued shares generates losses, amplifying the sensitivity of per-share value to fundamentals and making speculators’ private information more valuable for trading. Sufficiently informed buybacks benefit shareholders in aggregate because the competitive discipline dominates; uninformed buybacks harm them because they provide no competitive discipline while amplifying the value of speculators’ information. This analysis suggests that the recent shift toward mechanical buyback execution, intended to protect shareholders from informed insider trading, may have unintended negative consequences.

I formalize this argument in a trading model featuring a manager who executes buybacks on behalf of the firm, an outside speculator who trades for personal profit, and shareholders whose unpredictable liquidity needs create noise in the market. At

$ t=0 $

, the firm can authorize a buyback program. At

$ t=1 $

, the firm can authorize a buyback program. At

$ t=1 $

, both the manager and the speculator observe private signals about the firm’s fundamentals. The manager decides whether to execute the authorized buyback; the speculator decides whether to buy. Competitive Kyle (Reference Kyle1985)-type market makers observe aggregate order flow and set prices. At

$ t=2 $

, both the manager and the speculator observe private signals about the firm’s fundamentals. The manager decides whether to execute the authorized buyback; the speculator decides whether to buy. Competitive Kyle (Reference Kyle1985)-type market makers observe aggregate order flow and set prices. At

$ t=2 $

, the firm’s fundamentals become public, and accounts are settled.

, the firm’s fundamentals become public, and accounts are settled.

In my framework, the informativeness of buybacks refers to the extent to which their execution tracks the manager’s private information. For instance, when the manager buys back shares only when she knows fundamentals are high, buybacks are fully informed. When she buys regardless of what she knows, buybacks are uninformed.

Buybacks introduce two countervailing forces. The first is a competition effect. When the manager executes buybacks in an informed way, her trades make the aggregate order flow more informative about firm fundamentals. The resulting improvement in price discovery compresses the speculator’s trading profits—he can no longer buy undervalued shares as cheaply. The competition effect is a classic feature of models with multiple informed traders, but prior buyback research overlooks it by assuming only the manager is informed.Footnote 6

The second is a dispersion effect. Unlike the speculator’s trades, buybacks affect the firm’s per-share value. In good states, when fundamentals are high, the buyback of undervalued shares generates trading gains that increase the firm’s per-share value. In bad states, when fundamentals are low, the buyback of overvalued shares incurs trading losses that decrease per-share value. These state-dependent gains and losses increase the dispersion of the firm’s per-share value across different realizations of its fundamentals—higher in good states, lower in bad states. The increased sensitivity of the firm’s per-share value to its fundamentals makes the speculator’s private information more valuable for trading.

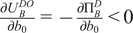

Less informed buybacks weaken the competition effect—order flow becomes less revealing when buybacks occur, even when fundamentals are low—while strengthening the dispersion effect: they are more likely to occur in bad states, generating trading losses that push per-share value further below fundamentals. I show that buybacks reduce the speculator’s trading profits—and thereby benefit shareholders in aggregate—if and only if they are sufficiently informed. Uninformed buybacks unambiguously harm shareholders: they provide no competitive discipline against the speculator while maximizing the value dispersion that makes speculative trading profitable. This result offers a new perspective on the idea that buybacks stabilize markets, with firms acting as “buyers of last resort” (Hong, Wang, and Yu (Reference Hong, Wang and Yu2008)). While uninformed buybacks can support the firm’s short-term stock price, the trading losses they generate when fundamentals are weak further depress the firm’s per-share value once fundamentals become known.

Whether buybacks are, in fact, informed is an equilibrium outcome. As is common in applied models of corporate decision-making (e.g., Stein (Reference Stein1989), Holmstrom and Tirole (Reference Holmstrom and Tirole1993)), the manager maximizes a weighted combination of the firm’s interim stock price and long-term value—reflecting, for instance, compensation contracts tied to both short- and long-term performance. The manager’s equilibrium strategy depends on her incentives. A manager focused on long-term value executes informed buybacks, while a manager concerned with short-term price performance may buy back overvalued shares to inflate the interim price. Beyond managerial incentives, constraints on informativeness can also arise from legitimate corporate objectives—such as offsetting dilution from equity compensation or distributing excess cash—that push toward consistent execution regardless of fundamentals.

While the aggregate effects of buybacks depend on informativeness, they mask important heterogeneity across shareholders. I distinguish shareholders by their exposure to liquidity shocks. Liquidity-insulated shareholders—insiders, blockholders, and long-horizon institutions—hold until firm fundamentals are revealed. They benefit from informed buybacks because they capture buyback gains without bearing adverse-selection costs, a phenomenon that Fried (Reference Fried2013) refers to as “insider trading via the firm.” In contrast, liquidity-exposed shareholders—those who may need to sell before fundamentals are revealed—face a trade-off. Informed buybacks transfer wealth to liquidity-insulated shareholders, but they also reduce the profits the speculator earns at their expense. Which effect dominates depends on the prevalence of informed speculation. When speculation is rare, they prefer less informed buybacks, recovering the standard argument against informed buybacks in the prior literature (e.g., Barclay and Smith (Reference Barclay and Smith1988)). When speculation is prevalent, liquidity-exposed shareholders benefit from informed buybacks. This result is consistent with findings from Hillert, Maug, and Obernberger (Reference Hillert, Maug and Obernberger2016), who show that more informed buybacks can improve rather than harm liquidity.

The authorization decision, therefore, depends on ownership composition and governance. When insiders control the board, they always authorize buybacks. When liquidity-exposed shareholders have influence, they oppose buybacks when informed speculation is rare, but support authorization when speculation is prevalent and they anticipate sufficiently informed execution.

This analysis helps explain documented patterns. Buyback authorizations are procyclical (e.g., Jagannathan, Stephens, and Weisbach (Reference Jagannathan, Stephens and Weisbach2000), Dittmar and Dittmar (Reference Dittmar and Dittmar2008)) and more common for firms with liquid shares (e.g., Brockman, Howe, and Mortal (Reference Brockman, Howe and Mortal2008)). The model rationalizes both patterns: conditions of strong expected fundamentals and high liquidity increase the anticipated informativeness of buyback execution, making authorization more attractive to liquidity-exposed shareholders.

The framework also illuminates payout policy. The literature highlights several advantages of buybacks over dividends—such as tax efficiency (Grullon and Michaely (Reference Grullon and Michaely2002)), the ability to adjust payout without signaling negative information (Jagannathan et al. (Reference Jagannathan, Stephens and Weisbach2000)), and usefulness in offsetting dilution from equity compensation (Kahle (Reference Kahle2002))—that are maximized by consistent execution regardless of fundamentals. Such uninformed execution generates the dispersion effect that harms liquidity-exposed shareholders. Dividends, by contrast, reduce per-share value equally in good and bad states—the firm has less cash regardless of fundamentals—creating no dispersion effect. This distinction presents a trade-off: firms seeking to maximize the benefits of buybacks must execute consistently, but consistent execution is uninformed execution, which amplifies the profitability of informed speculation at the expense of liquidity-exposed shareholders. The secular shift from dividends to buybacks (e.g., Kahle and Stulz (Reference Kahle and Stulz2021)) may, therefore, have distributional consequences for shareholders with different liquidity exposures, beyond the tax and flexibility considerations typically emphasized in the literature.

A. Related Literature

This article connects to several strands of literature. One strand examines open-market repurchases as a payout policy. Researchers have proposed many explanations for the popularity of these programs, including tax advantages (Grullon and Michaely (Reference Grullon and Michaely2002), Moser (Reference Moser2007)), financial flexibility (Stephens and Weisbach (Reference Stephens and Weisbach1998), Guay and Harford (Reference Guay and Harford2000), Jagannathan et al. (Reference Jagannathan, Stephens and Weisbach2000), and Bonaime, Hankins, and Harford (Reference Bonaime, Hankins and Harford2014)), mitigation of agency conflicts (Oded (Reference Oded2011), Caton, Goh, Lee, and Linn (Reference Caton, Goh, Lee and Linn2016)), and signaling (Oded (Reference Oded2005), Bhattacharya and Jacobsen (Reference Bhattacharya and Jacobsen2016)). See Bonaime and Kahle (Reference Bonaime, Kahle and Denis2024) for a recent comprehensive survey.

Since Barclay and Smith (Reference Barclay and Smith1988), the notion that informed buybacks impose adverse-selection costs has played an important role in this literature. This view arises naturally when the manager is the sole informed party: her buyback trades profit at the expense of less informed shareholders (e.g., Fried (Reference Fried2013), Babenko, Tserlukevich, and Wan (Reference Babenko, Tserlukevich and Wan2020)). Prior work views informed buybacks as a cost that shareholders reluctantly accept to access other benefits of repurchase programs. My framework suggests that shareholders might welcome informed buybacks—not merely tolerate them—because they provide competitive discipline against outside speculators. This article also complements recent theoretical analyses that study buybacks in richer environments, though still featuring only one informed party. Bond and Zhong (Reference Bond and Zhong2016) investigate dynamic tender-offer buybacks under persistent asymmetric information. Bond, Yuan, and Zhong (Reference Bond, Yuan and Zhong2025) develop a unified signaling framework for share issues and buybacks that explains the asymmetry in transaction methods. Campello, Matta, and Saffi (Reference Campello, Matta and Saffi2026) examine how buybacks interact with manipulation incentives and short-selling frictions when prices affect real investment.

Another strand is the literature on the real effects of financial markets (Dow and Gorton (Reference Dow and Gorton1997), see Bond, Edmans, and Goldstein (Reference Bond, Edmans and Goldstein2012) for a survey), which emphasizes how prices affect firm value by guiding investment decisions. Here, buybacks affect per-share value directly through trading gains and losses. Because buybacks alter the profitability of informed trading, they can interact with feedback effects in settings where prices guide real decisions.

Finally, my analysis relates to the literature that investigates trading in Kyle (Reference Kyle1985)-type frameworks with multiple informed parties. Research consistently finds that additional informed traders decrease existing speculators’ profits (e.g., Admati and Pfleiderer (Reference Admati and Pfleiderer1988), Holden and Subrahmanyam (Reference Holden and Subrahmanyam1992), and Back, Cao, and Willard (Reference Back, Cao and Willard2000)).Footnote 7 This competition effect completely characterizes how additional informed parties affect trading dynamics in conventional trading models. My analysis reveals that buybacks generate a dispersion effect absent from standard informed trading—one that can dominate the competition effect when buybacks are uninformed—demonstrating that buybacks by the firm differ from informed trading by outside speculators in important ways.

II. Model

The model spans three dates (

$ t=0,t=1,t=2 $

) and features risk-neutral economic agents: the firm’s shareholders, a manager who executes buybacks on behalf of the firm, an outside speculator who trades for personal profit, and market makers who clear the market. The firm has assets in place that generate a payoff of

$ A $

) and features risk-neutral economic agents: the firm’s shareholders, a manager who executes buybacks on behalf of the firm, an outside speculator who trades for personal profit, and market makers who clear the market. The firm has assets in place that generate a payoff of

$ A $

at

$ t=2 $

at

$ t=2 $

that can be high (

$ A=1 $

that can be high (

$ A=1 $

) or low (

$ A=0 $

) or low (

$ A=0 $

) with probabilities

$ \theta $

) with probabilities

$ \theta $

and

$ 1-\theta $

and

$ 1-\theta $

, respectively. The parameter

$ \theta \in \left(0,1\right) $

, respectively. The parameter

$ \theta \in \left(0,1\right) $

—the probability that firm fundamentals are high—captures the firm’s ex ante quality. The firm is financed entirely by equity and has one share outstanding at

$ t=0 $

—the probability that firm fundamentals are high—captures the firm’s ex ante quality. The firm is financed entirely by equity and has one share outstanding at

$ t=0 $

.

.

At

$ t=0 $

, the firm’s shareholders can authorize a buyback program.Footnote

8 If authorized, the program gives the manager the discretion to buy back

$ x<1-\theta $

, the firm’s shareholders can authorize a buyback program.Footnote

8 If authorized, the program gives the manager the discretion to buy back

$ x<1-\theta $

shares on behalf of the firm at

$ t=1 $

shares on behalf of the firm at

$ t=1 $

. The parameter restriction on

$ x $

. The parameter restriction on

$ x $

ensures that there is a unique equilibrium trading strategy for the manager.Footnote

9 Let

$ k=\frac{x}{1-x} $

ensures that there is a unique equilibrium trading strategy for the manager.Footnote

9 Let

$ k=\frac{x}{1-x} $

denote the scale of the buyback program, measuring shares repurchased relative to shares remaining. If shareholders do not authorize a buyback program at

$ t=0 $

denote the scale of the buyback program, measuring shares repurchased relative to shares remaining. If shareholders do not authorize a buyback program at

$ t=0 $

, the manager cannot buy back shares at

$ t=1 $

, the manager cannot buy back shares at

$ t=1 $

. In contrast with conventional signaling models of stock buybacks, the authorization at

$ t=0 $

. In contrast with conventional signaling models of stock buybacks, the authorization at

$ t=0 $

conveys no information about the firm’s fundamentals because it takes place before insiders (e.g., the manager) receive private information, consistent with empirical evidence and institutional practice.Footnote

10

conveys no information about the firm’s fundamentals because it takes place before insiders (e.g., the manager) receive private information, consistent with empirical evidence and institutional practice.Footnote

10

Trading at

$ t=1 $

takes place in a market characterized by a discrete-trade version of the Kyle (Reference Kyle1985) framework, in which participants trade in increments of

$ x $

takes place in a market characterized by a discrete-trade version of the Kyle (Reference Kyle1985) framework, in which participants trade in increments of

$ x $

shares. Shareholders who experience liquidity needs at

$ t=1 $

shares. Shareholders who experience liquidity needs at

$ t=1 $

submit an order of

$ {q}_Z $

submit an order of

$ {q}_Z $

shares, with

$ {q}_Z $

shares, with

$ {q}_Z $

taking values

$ -x $

taking values

$ -x $

and

$ 0 $

and

$ 0 $

with equal probability. These liquidity-driven trades are independent of firm fundamentals (

$ A $

with equal probability. These liquidity-driven trades are independent of firm fundamentals (

$ A $

).

).

Before trading begins at

$ t=1 $

, the speculator observes the realized value of fundamentals with probability

$ \phi \in \left(0,1\right) $

, the speculator observes the realized value of fundamentals with probability

$ \phi \in \left(0,1\right) $

, capturing the notion that speculators are imperfectly informed. The speculator’s trading strategy specifies an order

$ {q}_S\in \left\{0,x\right\} $

, capturing the notion that speculators are imperfectly informed. The speculator’s trading strategy specifies an order

$ {q}_S\in \left\{0,x\right\} $

that depends on his private information about firm fundamentals.Footnote

11 He trades to maximize his expected trading profits.

that depends on his private information about firm fundamentals.Footnote

11 He trades to maximize his expected trading profits.

Prior to trading, the manager perfectly observes the realized value of fundamentals. The manager’s buyback strategy specifies the probability with which she executes the buyback program—defined as submitting a buy order of

$ {q}_B=x $

—conditional on her private information about firm fundamentals. The manager executes buybacks to maximize

$ \unicode{x1D53C}\left[\omega P+V\right] $

—conditional on her private information about firm fundamentals. The manager executes buybacks to maximize

$ \unicode{x1D53C}\left[\omega P+V\right] $

, where

$ P $

, where

$ P $

is the firm’s stock price at

$ t=1 $

is the firm’s stock price at

$ t=1 $

,

$ V $

,

$ V $

is the firm’s per-share value at

$ t=2 $

is the firm’s per-share value at

$ t=2 $

, and

$ \omega \ge 0 $

, and

$ \omega \ge 0 $

captures her concern for the interim stock price. For instance, the manager may have a linear compensation contract that increases with the firm’s stock price at

$ t=1 $

captures her concern for the interim stock price. For instance, the manager may have a linear compensation contract that increases with the firm’s stock price at

$ t=1 $

and

$ t=2 $

and

$ t=2 $

as in Holmstrom and Tirole (Reference Holmstrom and Tirole1993).Footnote

12 Insider trading restrictions prevent the manager from trading using her personal account at

$ t=1 $

as in Holmstrom and Tirole (Reference Holmstrom and Tirole1993).Footnote

12 Insider trading restrictions prevent the manager from trading using her personal account at

$ t=1 $

.

.

Deep-pocketed market makers observe the aggregate order flow

$ q={q}_B+{q}_S+{q}_Z $

. Competition among many market makers implies that they set prices to break even in expectation. For brevity, I refer to market makers collectively as the market.

. Competition among many market makers implies that they set prices to break even in expectation. For brevity, I refer to market makers collectively as the market.

At

$ t=2 $

, the fundamentals of the firm become public information. The market makers settle accounts. The firm is liquidated, with proceeds distributed pro rata to holders of its outstanding shares.Footnote

13 Table 1 summarizes the timing of the model.

, the fundamentals of the firm become public information. The market makers settle accounts. The firm is liquidated, with proceeds distributed pro rata to holders of its outstanding shares.Footnote

13 Table 1 summarizes the timing of the model.

TABLE 1 Long description

Starting at the top, t equals 0 marks the firm’s decision to authorize a buyback program or not. The next section, t equals 1, contains three rows: first, the manager and speculator receive private information; second, the manager, speculator, and shareholders with liquidity needs submit orders simultaneously; third, competitive market makers set a price based on aggregate order flow and clear the market. The final section, t equals 2, also has three rows: first, the firm’s fundamentals become public information; second, accounts are settled; third, the firm is liquidated and proceeds are distributed pro rata to holders of outstanding shares.

The trading equilibrium at

$ t=1 $

consists of three components: a pricing rule, the speculator’s trading strategy, and the manager’s buyback strategy. In equilibrium, the market sets prices equal to the firm’s expected per-share value at

$ t=2 $

consists of three components: a pricing rule, the speculator’s trading strategy, and the manager’s buyback strategy. In equilibrium, the market sets prices equal to the firm’s expected per-share value at

$ t=2 $

conditional on aggregate order flow and the anticipated strategies of the other parties. The speculator chooses his trading strategy to maximize expected profits given the pricing rule, the manager’s strategy, and his private information. The manager selects her buyback strategy to maximize a weighted combination of the firm’s stock price at

$ t=1 $

conditional on aggregate order flow and the anticipated strategies of the other parties. The speculator chooses his trading strategy to maximize expected profits given the pricing rule, the manager’s strategy, and his private information. The manager selects her buyback strategy to maximize a weighted combination of the firm’s stock price at

$ t=1 $

and the per-share value at

$ t=2 $

and the per-share value at

$ t=2 $

, given the pricing rule, the speculator’s strategy, and her private information.

, given the pricing rule, the speculator’s strategy, and her private information.

III. Buybacks and Trading Outcomes

This section analyzes how a stock buyback program affects trading outcomes at

$ t=1 $

. I begin by characterizing the benchmark trading equilibrium without buybacks (denoted with subscript

$ 0 $

. I begin by characterizing the benchmark trading equilibrium without buybacks (denoted with subscript

$ 0 $

):

):

Lemma 1. In the absence of a buyback program, the equilibrium pricing rule is

and the speculator buys

$ x $

shares if and only if he learns that firm fundamentals are high (

$ A=1 $

shares if and only if he learns that firm fundamentals are high (

$ A=1 $

).

).

The results of Lemma 1 follow the standard logic of Kyle-type informed trading frameworks. The presence of noise trading implies that the expected market-clearing price is strictly between

$ 0 $

and

$ 1 $

and

$ 1 $

both when

$ A=1 $

both when

$ A=1 $

and

$ A=0 $

and

$ A=0 $

. Hence, the speculator strictly prefers to buy upon learning

$ A=1 $

. Hence, the speculator strictly prefers to buy upon learning

$ A=1 $

and to abstain otherwise. The market makers’ equilibrium pricing rule reflects this trading strategy, increasing with the aggregate order flow.

and to abstain otherwise. The market makers’ equilibrium pricing rule reflects this trading strategy, increasing with the aggregate order flow.

Lemma 1 implies that the speculator’s expected trading profit (

$ \Pi $

) in this benchmark is

) in this benchmark is

As is standard in such informed trading frameworks, the speculator’s expected trading profits increase with his private information (

$ \phi $

), the volatility of the firm’s fundamentals (

$ \theta \left(1-\theta \right) $

), the volatility of the firm’s fundamentals (

$ \theta \left(1-\theta \right) $

), and the volatility of noise trade (

$ x $

), and the volatility of noise trade (

$ x $

). More uncertainty about fundamentals amplifies potential mispricing and, in turn, trading profits. Additional noise trade allows him to take larger positions without revealing his information.

). More uncertainty about fundamentals amplifies potential mispricing and, in turn, trading profits. Additional noise trade allows him to take larger positions without revealing his information.

A. Trading Equilibrium with Buybacks

This section analyzes the implications of a buyback program for trading outcomes. The authorization of a buyback program at

$ t=0 $

makes the firm an active participant in the market for its shares, with the manager effectively becoming another informed trader at

$ t=1 $

makes the firm an active participant in the market for its shares, with the manager effectively becoming another informed trader at

$ t=1 $

. In this section, I assume that the manager executes buybacks with probability

$ {b}_1=1 $

. In this section, I assume that the manager executes buybacks with probability

$ {b}_1=1 $

when firm fundamentals are high (

$ A=1 $

when firm fundamentals are high (

$ A=1 $

) and with probability

$ {b}_0\in \left[0,1\right] $

) and with probability

$ {b}_0\in \left[0,1\right] $

when fundamentals are low (

$ A=0 $

when fundamentals are low (

$ A=0 $

). Section IV shows that such a buyback strategy is indeed optimal for a manager who maximizes a weighted combination of the firm’s stock price at

$ t=1 $

). Section IV shows that such a buyback strategy is indeed optimal for a manager who maximizes a weighted combination of the firm’s stock price at

$ t=1 $

and the per-share value at

$ t=2 $

and the per-share value at

$ t=2 $

.Footnote

14 One interpretation of the buyback strategy is that the manager executes a fraction

$ {b}_0 $

.Footnote

14 One interpretation of the buyback strategy is that the manager executes a fraction

$ {b}_0 $

of the program in an uninformed manner—buying

$ x $

of the program in an uninformed manner—buying

$ x $

shares regardless of fundamentals—and the remaining fraction

$ 1-{b}_0 $

shares regardless of fundamentals—and the remaining fraction

$ 1-{b}_0 $

in an informed manner—buying only when fundamentals are high. Under this interpretation,

$ 1-{b}_0 $

in an informed manner—buying only when fundamentals are high. Under this interpretation,

$ 1-{b}_0 $

measures the informativeness of buybacks. As

$ {b}_0 $

measures the informativeness of buybacks. As

$ {b}_0 $

increases, the difference in the execution probabilities in good and bad states narrows, and buybacks become less informative. Buybacks are fully uninformed when

$ {b}_0=1 $

increases, the difference in the execution probabilities in good and bad states narrows, and buybacks become less informative. Buybacks are fully uninformed when

$ {b}_0=1 $

: the manager buys with the same probability in good and bad states, so buybacks carry no information about fundamentals.

: the manager buys with the same probability in good and bad states, so buybacks carry no information about fundamentals.

A buyback program changes the trading equilibrium in important ways. The following lemma characterizes the new trading equilibrium with buybacks (denoted with subscript

$ B $

):

):

Lemma 2. Given a stock buyback program and the manager’s buyback execution strategy

$ \left({b}_1=1,{b}_0\right) $

, the equilibrium pricing rule is

, the equilibrium pricing rule is

and the speculator buys

$ x $

shares if and only if he learns that firm fundamentals are high (

$ A=1 $

shares if and only if he learns that firm fundamentals are high (

$ A=1 $

).Footnote

15

).Footnote

15

A stock buyback program introduces two economic forces to trading at

$ t=1 $

. First, it affects the market’s inferences about firm fundamentals by altering the information content of the order flow. This informed execution of buybacks makes the order flow more revealing, improving price discovery and lowering informed trading profits. This competition effect is a robust feature of trading frameworks with multiple informed parties. Second, the program generates buyback profits and losses that make the firm’s per-share value more sensitive to its fundamentals. This dispersion effect is unique to the buyback setting.

. First, it affects the market’s inferences about firm fundamentals by altering the information content of the order flow. This informed execution of buybacks makes the order flow more revealing, improving price discovery and lowering informed trading profits. This competition effect is a robust feature of trading frameworks with multiple informed parties. Second, the program generates buyback profits and losses that make the firm’s per-share value more sensitive to its fundamentals. This dispersion effect is unique to the buyback setting.

1. Competition Effect

A buyback program introduces the firm’s manager as an additional informed trader who may execute buybacks in ways that affect the informativeness of the order flow. To see this clearly, consider how the market updates its beliefs about the firm’s fundamentals (

$ A $

) based on the observed order flow (

$ q $

) based on the observed order flow (

$ q $

):

$ \hat{\theta}(q)=\mathit{\Pr}\left(A=1|q\right) $

):

$ \hat{\theta}(q)=\mathit{\Pr}\left(A=1|q\right) $

. In the benchmark without buybacks, the market’s posterior belief is

. In the benchmark without buybacks, the market’s posterior belief is

With buybacks, the market’s posterior belief becomes

One measure of market informativeness is the difference between the market’s expected posterior belief in the two fundamental states:

. A larger

$ \Delta \hat{\theta} $

. A larger

$ \Delta \hat{\theta} $

indicates that the order flow better discriminates between high (

$ A=1 $

indicates that the order flow better discriminates between high (

$ A=1 $

) and low fundamentals (

$ A=0 $

) and low fundamentals (

$ A=0 $

), with

$ \Delta \hat{\theta}=1 $

), with

$ \Delta \hat{\theta}=1 $

corresponding to the case where the market perfectly infers the firm’s fundamentals from the order flow. Comparing equations (4) and (5) yields the following result:

corresponding to the case where the market perfectly infers the firm’s fundamentals from the order flow. Comparing equations (4) and (5) yields the following result:

Lemma 3. Relative to the benchmark, a buyback program improves market informativeness (

$ \Delta {\hat{\theta}}_B>\Delta {\hat{\theta}}_0 $

) if buybacks are informed (

$ {b}_0<1 $

) if buybacks are informed (

$ {b}_0<1 $

). The improvement increases with buyback informativeness.

). The improvement increases with buyback informativeness.

When buybacks are uninformed (

$ {b}_0=1 $

), they simply shift the distribution of the order flow—increasing it by

$ x $

), they simply shift the distribution of the order flow—increasing it by

$ x $

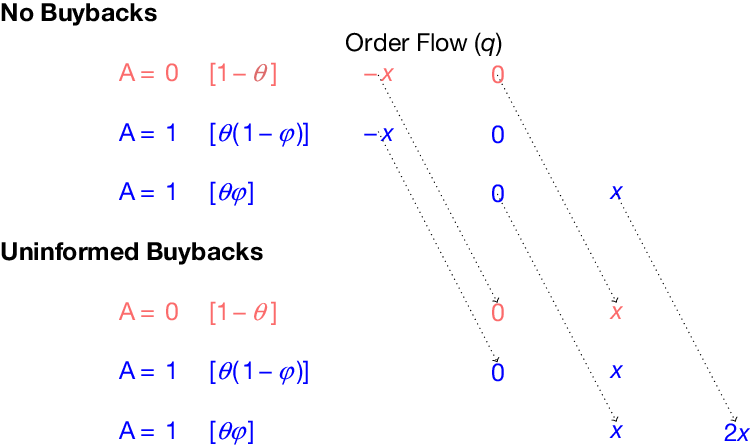

—across all fundamental states, as shown in Figure 1. This shift does not affect the information content of the order flow, leaving market informativeness unchanged (

$ \Delta {\hat{\theta}}_B=\Delta {\hat{\theta}}_0 $

—across all fundamental states, as shown in Figure 1. This shift does not affect the information content of the order flow, leaving market informativeness unchanged (

$ \Delta {\hat{\theta}}_B=\Delta {\hat{\theta}}_0 $

).

).

The upper portion of Figure 1 shows the distribution of the order flow (

$ q $

) across different firm fundamentals (

$ A $

) across different firm fundamentals (

$ A $

) in the absence of a buyback program. The lower portion shows how uninformed buybacks (

$ 1-{b}_0=0 $

) in the absence of a buyback program. The lower portion shows how uninformed buybacks (

$ 1-{b}_0=0 $

) shift the distribution of the order flow to the right by

$ x $

) shift the distribution of the order flow to the right by

$ x $

units in all states, leaving the informativeness of the order flow unchanged. Bracketed terms report the probabilities of the corresponding rows.

units in all states, leaving the informativeness of the order flow unchanged. Bracketed terms report the probabilities of the corresponding rows.

FIGURE 1 Long description

The chart is divided into two horizontal panels. The top panel, labeled No Buybacks, lists three rows for A equals 0 and A equals 1, each with bracketed probabilities in red. For A equals 0, the probability is open bracket 1 minus theta close bracket, and order flow q is negative x or 0. For A equals 1, the first row has probability open bracket theta times open parenthesis 1 minus phi close parenthesis close bracket, and order flow q is negative x or 0. The second A equals 1 row has probability open bracket theta phi close bracket, and order flow q is 0 or x. Dotted lines connect each probability to its corresponding order flow value. The bottom panel, labeled Uninformed Buybacks, repeats the same three rows for A with identical probabilities, but the order flow q values are shifted rightward: for A equals 0, q is 0 or x; for the first A equals 1 row, q is 0 or x; for the second A equals 1 row, q is x or 2 x. Dotted lines again connect each probability to its new order flow values, illustrating a uniform rightward shift in order flow across all states.

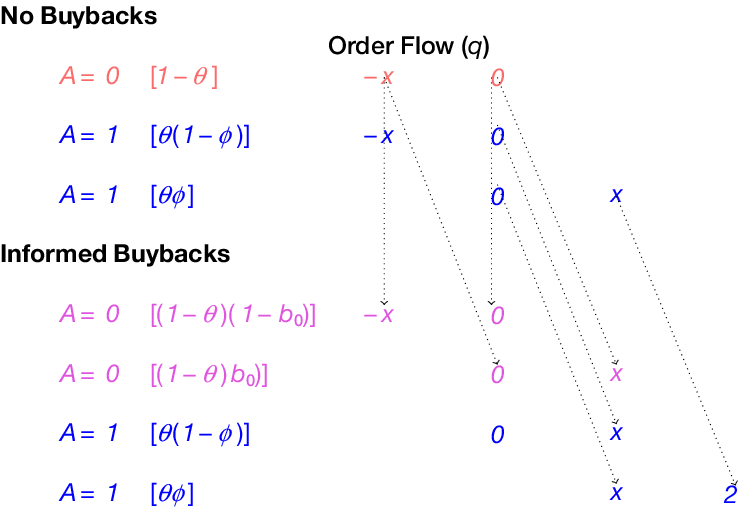

In contrast, informed buybacks (

$ 1-{b}_0>0 $

) make the order flow more revealing of firm fundamentals. As illustrated in Figure 2, informed buybacks are more likely to shift the order flow distribution rightward when firm fundamentals are high (

$ A=1 $

) make the order flow more revealing of firm fundamentals. As illustrated in Figure 2, informed buybacks are more likely to shift the order flow distribution rightward when firm fundamentals are high (

$ A=1 $

) than when they are low (

$ A=0 $

) than when they are low (

$ A=0 $

). This state-contingent shift makes high-order flows more indicative of high fundamentals, and low-order flows more indicative of low fundamentals. The more informative the buybacks (i.e., higher

$ 1-{b}_0 $

). This state-contingent shift makes high-order flows more indicative of high fundamentals, and low-order flows more indicative of low fundamentals. The more informative the buybacks (i.e., higher

$ 1-{b}_0 $

), the greater the improvement in market informativeness.

), the greater the improvement in market informativeness.

The upper portion of Figure 2 shows the distribution of the order flow (

$ q $

) across different firm fundamentals (

$ A $

) across different firm fundamentals (

$ A $

) in the absence of buybacks. The lower portion illustrates how informed buybacks improve the informativeness of the order flow by shifting the distribution of the order flow to the right more when the firm’s fundamentals are high (

$ A=1 $

) in the absence of buybacks. The lower portion illustrates how informed buybacks improve the informativeness of the order flow by shifting the distribution of the order flow to the right more when the firm’s fundamentals are high (

$ A=1 $

) than when they are low (

$ A=0 $

) than when they are low (

$ A=0 $

). Bracketed terms report the probabilities of the corresponding rows.

). Bracketed terms report the probabilities of the corresponding rows.

FIGURE 2 Long description

The table is divided into two sections. The upper section, labeled No Buybacks, lists three rows for firm fundamentals: A equals 0 with probability one minus theta, A equals 1 with probability theta times open parenthesis one minus phi close parenthesis, and A equals 1 with probability theta phi. Each row connects by dotted lines to order flow q values: minus x, 0, and x. The lower section, labeled Informed Buybacks, has four rows: A equals 0 with probability open bracket one minus theta close bracket times open bracket one minus b sub 0 close bracket, A equals 0 with probability open bracket one minus theta close bracket b sub 0, A equals 1 with probability theta times open parenthesis one minus phi close parenthesis, and A equals 1 with probability theta phi. These connect to order flow values minus x, 0, x, and 2 x. Dotted lines indicate how probabilities map to order flow outcomes, with more mass shifted to higher order flow values under Informed Buybacks, especially when A equals 1.

Informed buybacks that closely track the firm’s fundamentals erode the speculator’s informational advantage by making the order flow more revealing. In other words, informed buybacks compete against the speculator’s informed trades.

These results parallel the classic literature on competing informed traders (e.g., Admati and Pfleiderer (Reference Admati and Pfleiderer1988), Holden and Subrahmanyam (Reference Holden and Subrahmanyam1992), Foster and Viswanathan (Reference Foster and Viswanathan1993), and Back et al. (Reference Back, Cao and Willard2000)), where additional informed parties enhance price informativeness and compress existing traders’ profits. However, a crucial distinction emerges: in conventional models, informed traders use private accounts and personally bear their trading gains and losses. While their activities alter the firm’s ownership composition, they do not directly affect per-share value.Footnote 16 Consequently, the competition effect completely captures the impact of introducing an additional informed trader.

In my framework, however, the additional informed trader is the manager acting on behalf of the firm. Her buyback trades affect not only the information content of order flow but also the distribution of per-share value through realized trading gains and losses—introducing the novel dispersion effect analyzed next.

2. Dispersion Effect

Buyback activity generates trading gains and losses that accrue to the firm’s remaining shareholders. Consequently, with buybacks, the firm’s per-share value at

$ t=2 $

becomes

$ V=A+T $

becomes

$ V=A+T $

, where

$ A $

, where

$ A $

represents the fundamental payoff from the firm’s assets and

$ T $

represents the fundamental payoff from the firm’s assets and

$ T $

captures the per-share gains and losses from the firm’s trading activity.

captures the per-share gains and losses from the firm’s trading activity.

The impact of buybacks on the firm’s per-share value at

$ t=2 $

depends on whether its shares are under- or overvalued at

$ t=1 $

depends on whether its shares are under- or overvalued at

$ t=1 $

. When fundamentals are high relative to the market-clearing price at

$ t=1 $

. When fundamentals are high relative to the market-clearing price at

$ t=1 $

(

$ A>{P}_B $

(

$ A>{P}_B $

), the firm buys back undervalued shares, generating trading gains that increase per-share value at

$ t=2 $

), the firm buys back undervalued shares, generating trading gains that increase per-share value at

$ t=2 $

from

$ A $

from

$ A $

to

$ {V}_H $

to

$ {V}_H $

(i.e.,

$ T>0 $

(i.e.,

$ T>0 $

):

):

where

$ k=\frac{x}{1-x} $

is the scale of the buyback program. Conversely, when fundamentals are low relative to the market-clearing price at

$ t=1 $

is the scale of the buyback program. Conversely, when fundamentals are low relative to the market-clearing price at

$ t=1 $

(

$ A<{P}_B $

(

$ A<{P}_B $

), the firm buys back overvalued shares, generating trading losses that decrease per-share value at

$ t=2 $

), the firm buys back overvalued shares, generating trading losses that decrease per-share value at

$ t=2 $

from

$ A $

from

$ A $

to

$ {V}_L $

to

$ {V}_L $

(i.e.,

$ T<0 $

(i.e.,

$ T<0 $

):

):

Unlike the trades of speculators, buybacks tend to increase the firm’s per-share value when its fundamentals are high (

$ A=1 $

) and decrease the firm’s per-share value when its fundamentals are low (

$ A=0 $

) and decrease the firm’s per-share value when its fundamentals are low (

$ A=0 $

). As a result, buybacks amplify the sensitivity of the firm’s per-share value to its fundamentals—the dispersion effect.

Footnote

17

). As a result, buybacks amplify the sensitivity of the firm’s per-share value to its fundamentals—the dispersion effect.

Footnote

17

To quantify this effect, consider the dispersion in the firm’s expected per-share value between good (

$ A=1 $

) and bad (

$ A=0 $

) and bad (

$ A=0 $

) states:

$ \Delta V=E\left[V|A=1\right]-E\left[V|A=0\right] $

) states:

$ \Delta V=E\left[V|A=1\right]-E\left[V|A=0\right] $

. In the benchmark without buybacks, this measure simply equals the fundamental spread in asset payoffs:

$ \Delta {V}_0=1 $

. In the benchmark without buybacks, this measure simply equals the fundamental spread in asset payoffs:

$ \Delta {V}_0=1 $

. With buybacks, the dispersion becomes

. With buybacks, the dispersion becomes

where

$ {\overline{T}}_G $

and

$ {\overline{T}}_L $

and

$ {\overline{T}}_L $

are the magnitudes of the expected trading gains and losses from executing buybacks when the firm’s fundamentals are high (

$ A=1 $

are the magnitudes of the expected trading gains and losses from executing buybacks when the firm’s fundamentals are high (

$ A=1 $

) and low (

$ A=0 $

) and low (

$ A=0 $

), respectively.

), respectively.

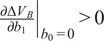

Lemma 4. Relative to the benchmark, a buyback program strictly increases the dispersion of the firm’s per-share value (

$ \Delta {V}_B>\Delta {V}_0 $

). The dispersion in per-share value decreases with the informativeness of buybacks

$ \left(\frac{\mathrm{\partial \Delta }{V}_B}{\partial {b}_0}>0\right) $

). The dispersion in per-share value decreases with the informativeness of buybacks

$ \left(\frac{\mathrm{\partial \Delta }{V}_B}{\partial {b}_0}>0\right) $

.

.

Buybacks increase the dispersion of the firm’s per-share value: they tend to raise per-share value when fundamentals are high and reduce it when fundamentals are low. Less informed buybacks amplify value dispersion through two channels. First, they incur larger trading losses in bad states (

$ A=0 $

), further suppressing value. Second, they make the order flow less informative, which increases the profitability of good-state buybacks, further boosting value in good states (

$ A=1 $

), further suppressing value. Second, they make the order flow less informative, which increases the profitability of good-state buybacks, further boosting value in good states (

$ A=1 $

).

).

The competition effect of buybacks improves market informativeness and reduces information asymmetry about the firm’s fundamentals among market participants. The dispersion effect works in the opposite direction—the increased sensitivity of the firm’s per-share value to its fundamentals makes any residual private information more valuable for trading. These changes have important economic consequences, as they determine both the efficiency of market prices and the distribution of trading gains between the speculator and the firm’s shareholders.

B. Speculator’s Profits

This section explores how buybacks shape trading outcomes, focusing on the speculator’s expected trading profits. Because these gains come at the expense of shareholders with liquidity needs, they are essential for evaluating how buybacks affect shareholder welfare.

To begin, consider the following measure of price discovery:

$ \Delta P=\unicode{x1D53C}\left[P|A=1\right]-\unicode{x1D53C}\left[P|A=0\right] $

. It captures how much market prices differ across fundamental states, with higher values indicating that prices better reflect the firm’s underlying value. In the benchmark without buybacks, price discovery coincides with market informativeness because the firm’s per-share value only depends on the fundamental payoff of its assets (

$ A $

. It captures how much market prices differ across fundamental states, with higher values indicating that prices better reflect the firm’s underlying value. In the benchmark without buybacks, price discovery coincides with market informativeness because the firm’s per-share value only depends on the fundamental payoff of its assets (

$ A $

):

$ \Delta {P}_0=\Delta {\hat{\theta}}_0 $

):

$ \Delta {P}_0=\Delta {\hat{\theta}}_0 $

. With buybacks, price discovery involves learning both about fundamentals and about buyback trading gains, which are jointly determined.

. With buybacks, price discovery involves learning both about fundamentals and about buyback trading gains, which are jointly determined.

Lemma 5. Price discovery improves with the informativeness of buybacks

$ \left(\frac{\mathrm{\partial \Delta }{P}_B}{\partial {b}_0}<0\right) $

.

.

At first glance, this result may seem puzzling. The analysis in Section III.A.2 shows that less informed buybacks generate more dispersion in per-share value, suggesting that prices should also diverge more across fundamental states. However, price discovery depends not only on the actual dispersion of per-share value, but also on what the market can infer from the order flow. Section III.A.1 shows that less informed buybacks decrease the information content of the order flow. This effect dominates, and a more informed execution of buybacks improves price discovery.

Recall that

$ {q}_S $

denotes the speculator’s order. His expected trading profit can be expressed as

denotes the speculator’s order. His expected trading profit can be expressed as

where the last equality follows from the market-clearing condition (

$ \unicode{x1D53C}\left[V-P\right]=0 $

). The speculator profits to the extent that his trades covary positively with the deviation of per-share value from price—that is, he gains by buying when the firm’s shares are undervalued and abstaining when they are overvalued.

). The speculator profits to the extent that his trades covary positively with the deviation of per-share value from price—that is, he gains by buying when the firm’s shares are undervalued and abstaining when they are overvalued.

To build intuition, consider the limiting case with

$ \phi \to 1 $

, where the speculator is almost always informed. Recall that the speculator buys (

$ {q}_S=x $

, where the speculator is almost always informed. Recall that the speculator buys (

$ {q}_S=x $

) if and only if he learns that firm fundamentals are high (

$ A=1 $

) if and only if he learns that firm fundamentals are high (

$ A=1 $

). In this case, the speculator almost always observes fundamentals, so his order (

$ {q}_S $

). In this case, the speculator almost always observes fundamentals, so his order (

$ {q}_S $

) is nearly perfectly correlated with

$ A $

) is nearly perfectly correlated with

$ A $

, implying that

, implying that

and

This decomposition in equation (11) reveals the tension between the two effects of buybacks. The competition effect improves price discovery (

$ \Delta {P}_B>\Delta {P}_0 $

), compressing the speculator’s informational advantage. The dispersion effect increases the spread in per-share value across fundamental states (

$ \Delta {V}_B>\Delta {V}_0 $

), compressing the speculator’s informational advantage. The dispersion effect increases the spread in per-share value across fundamental states (

$ \Delta {V}_B>\Delta {V}_0 $

), making his private information about firm fundamentals more valuable for trading. Buybacks reduce the speculator’s expected trading profit relative to the benchmark if and only if the competition effect dominates the dispersion effect.

), making his private information about firm fundamentals more valuable for trading. Buybacks reduce the speculator’s expected trading profit relative to the benchmark if and only if the competition effect dominates the dispersion effect.

In the more general case with

$ \phi \in \left(0,1\right) $

, the speculator is not always informed. As a result, his trades are not perfectly correlated with firm fundamentals, and the expression for his expected trading profit does not decompose cleanly into value dispersion and price discovery components. Intuitively, what matters is how value and prices vary across the speculator’s trading decisions, not just across fundamental states. Nevertheless, the same economic forces apply: the dispersion effect raises the stakes for informed trading, while the competition effect erodes the speculator’s informational advantage. The following proposition formalizes these results:

, the speculator is not always informed. As a result, his trades are not perfectly correlated with firm fundamentals, and the expression for his expected trading profit does not decompose cleanly into value dispersion and price discovery components. Intuitively, what matters is how value and prices vary across the speculator’s trading decisions, not just across fundamental states. Nevertheless, the same economic forces apply: the dispersion effect raises the stakes for informed trading, while the competition effect erodes the speculator’s informational advantage. The following proposition formalizes these results:

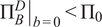

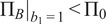

Proposition 1. Relative to the benchmark, a buyback program strictly decreases the speculator’s expected trading profit if and only if buybacks are sufficiently informed: there exists a threshold

$ {\overline{b}}_0\in \left(0,1\right) $

such that

$ {\Pi}_B<{\Pi}_0\iff {b}_0<{\overline{b}}_0 $

such that

$ {\Pi}_B<{\Pi}_0\iff {b}_0<{\overline{b}}_0 $

.

.

An immediate implication of Proposition 1 is that uninformed buybacks (

$ {b}_0=1 $

) unambiguously increase the speculator’s expected trading profits. Uninformed buybacks maximize the dispersion effect while contributing nothing to the competition effect. The speculator benefits from the increased value dispersion without facing any additional competition for trading profits.

) unambiguously increase the speculator’s expected trading profits. Uninformed buybacks maximize the dispersion effect while contributing nothing to the competition effect. The speculator benefits from the increased value dispersion without facing any additional competition for trading profits.

The results in this section characterize how buybacks affect the speculator’s expected trading profits, which, in turn, reveal how they affect the aggregate payoffs of the firm’s existing shareholders. For this analysis, the level of informed speculation (

$ \phi $

) affects the magnitude of changes but not the qualitative conclusions. However, when analyzing how buybacks affect different types of shareholders, the level of informed speculation becomes qualitatively important as well. Section III.C explores these welfare implications.

) affects the magnitude of changes but not the qualitative conclusions. However, when analyzing how buybacks affect different types of shareholders, the level of informed speculation becomes qualitatively important as well. Section III.C explores these welfare implications.

C. Heterogeneous Shareholder Welfare

A central concern in the literature is that informed buybacks transfer wealth from outside shareholders to insiders—a phenomenon Fried (Reference Fried2013) calls “insider trading via the firm” (see also Barclay and Smith (Reference Barclay and Smith1988), Fried (Reference Fried2005), Buffa and Nicodano (Reference Buffa and Nicodano2008), and Babenko, Tserlukevich, and Wan (Reference Babenko, Tserlukevich and Wan2020) for similar arguments). The mechanism underlying this wealth transfer is not insider status per se, but rather that insiders typically hold their shares until firm value is realized, whereas outside shareholders may need to sell beforehand to satisfy liquidity needs. Hence, this section examines how a buyback program affects shareholders with different exposures to liquidity shocks.

So far, the analysis has been agnostic about how the firm’s ownership is structured. To connect to the literature on wealth transfers between insiders and outside shareholders, I consider two types of investors who initially own the firm: liquidity-exposed and liquidity-insulated, denoted with superscript

$ E $

and

$ I $

and

$ I $

, respectively. Liquidity-exposed shareholders own a fraction

$ x $

, respectively. Liquidity-exposed shareholders own a fraction

$ x $

of the firm; their liquidity needs at

$ t=1 $

of the firm; their liquidity needs at

$ t=1 $

are the source of noise trade in the model.Footnote

18 Liquidity-insulated shareholders own the remaining

$ 1-x $

are the source of noise trade in the model.Footnote

18 Liquidity-insulated shareholders own the remaining

$ 1-x $

shares and hold their position until

$ t=2 $

shares and hold their position until

$ t=2 $

. These two groups represent the extremes of liquidity exposure. The payoffs of shareholders with intermediate exposures can be obtained as convex combinations of the payoffs of these two groups, providing insight into heterogeneous welfare effects—including for insiders and outside shareholders as conventionally defined.

. These two groups represent the extremes of liquidity exposure. The payoffs of shareholders with intermediate exposures can be obtained as convex combinations of the payoffs of these two groups, providing insight into heterogeneous welfare effects—including for insiders and outside shareholders as conventionally defined.

In the benchmark, the firm’s expected per-share value at

$ t=2 $

equals

$ \theta $

equals

$ \theta $

, the expected fundamental payoff of its assets. The expected payoff of liquidity-insulated shareholders is

$ {U}_0^I=\left(1-x\right)\theta $

, the expected fundamental payoff of its assets. The expected payoff of liquidity-insulated shareholders is

$ {U}_0^I=\left(1-x\right)\theta $

. The expected payoff of liquidity-exposed shareholders is

$ {U}_0^E= x\theta -{\Pi}_0 $

. The expected payoff of liquidity-exposed shareholders is

$ {U}_0^E= x\theta -{\Pi}_0 $

. Because of their liquidity needs at

$ t=1 $

. Because of their liquidity needs at

$ t=1 $

, the speculator’s trading profits come at their expense.

, the speculator’s trading profits come at their expense.

With buybacks, the firm’s expected per-share value at

$ t=2 $

becomes

$ \theta +\unicode{x1D53C}\left[T\right] $

becomes

$ \theta +\unicode{x1D53C}\left[T\right] $

, where

$ \unicode{x1D53C}\left[T\right] $

, where

$ \unicode{x1D53C}\left[T\right] $

is the expected per-share trading gains of its buyback program. The expected payoff of liquidity-insulated shareholders becomes

$ {U}_B^I=\left(1-x\right)\left(\theta +\unicode{x1D53C}\left[T\right]\right) $

is the expected per-share trading gains of its buyback program. The expected payoff of liquidity-insulated shareholders becomes

$ {U}_B^I=\left(1-x\right)\left(\theta +\unicode{x1D53C}\left[T\right]\right) $

.

.

Lemma 6. The expected per-share trading gain of the buyback program is positive (

$ \unicode{x1D53C}\left[T\right]\ge 0 $

) and increases with the informativeness of buybacks

$ \left(\frac{\partial \unicode{x1D53C}\left[T\right]}{\partial {b}_0}<0\right) $

) and increases with the informativeness of buybacks

$ \left(\frac{\partial \unicode{x1D53C}\left[T\right]}{\partial {b}_0}<0\right) $

.

.

An informed manager who executes buybacks based on her private information about firm fundamentals earns trading profits in expectation: she is more likely to buy back shares when they are undervalued than when they are overvalued. The more buybacks reflect the manager’s private information, the larger the expected profits from buybacks.

Because the firm’s liquidity-insulated shareholders hold their shares until

$ t=2 $

, they avoid adverse-selection trading costs at

$ t=1 $

, they avoid adverse-selection trading costs at

$ t=1 $

. Instead, they benefit from the trading gains generated by informed buybacks. Lemma 6, therefore, implies that liquidity-insulated shareholders are always weakly better off with a buyback program, strictly so if buybacks are informed (

$ {b}_0<1 $

. Instead, they benefit from the trading gains generated by informed buybacks. Lemma 6, therefore, implies that liquidity-insulated shareholders are always weakly better off with a buyback program, strictly so if buybacks are informed (

$ {b}_0<1 $

). This result echoes a concern emphasized by Barclay and Smith (Reference Barclay and Smith1988) and others in the literature: informed buybacks benefit those who hold their shares until firm fundamentals are revealed at the expense of those who may need to sell earlier. This traditional perspective implies that liquidity-exposed shareholders prefer less informed buybacks to limit this wealth transfer. Whether this conclusion holds, however, depends on the prevalence of informed speculation (

$ \phi $

). This result echoes a concern emphasized by Barclay and Smith (Reference Barclay and Smith1988) and others in the literature: informed buybacks benefit those who hold their shares until firm fundamentals are revealed at the expense of those who may need to sell earlier. This traditional perspective implies that liquidity-exposed shareholders prefer less informed buybacks to limit this wealth transfer. Whether this conclusion holds, however, depends on the prevalence of informed speculation (

$ \phi $

) in the market.

) in the market.

To see why, note that buybacks present a more complex trade-off for liquidity-exposed shareholders because they affect two wealth transfers: one to liquidity-insulated shareholders and another to the speculator. With buybacks, the expected payoff of liquidity-exposed shareholders is

The first term (

$ x\theta $

) is the fundamental value of the liquidity-exposed shareholders’ stake. The second term (

$ \left(1-x\right)\unicode{x1D53C}\left[T\right] $

) is the fundamental value of the liquidity-exposed shareholders’ stake. The second term (

$ \left(1-x\right)\unicode{x1D53C}\left[T\right] $

) reflects a wealth transfer to liquidity-insulated shareholders, who capture a fraction of the expected buyback gains without incurring trading costs. The final term (

$ {\Pi}_B $

) reflects a wealth transfer to liquidity-insulated shareholders, who capture a fraction of the expected buyback gains without incurring trading costs. The final term (

$ {\Pi}_B $

) is the wealth transfer to the speculator, whose informed trades profit at the expense of liquidity-exposed shareholders. One can interpret the last two terms as the reduction in the expected payoff of liquidity-exposed shareholders due to illiquidity.

) is the wealth transfer to the speculator, whose informed trades profit at the expense of liquidity-exposed shareholders. One can interpret the last two terms as the reduction in the expected payoff of liquidity-exposed shareholders due to illiquidity.

More informative buybacks have two opposing effects on this payoff. They increase the wealth transfer to liquidity-insulated shareholders, but also decrease the wealth transfer to the speculator. In general, the net effect is ambiguous and can be nonmonotonic.

However, we can characterize the effects when informed speculation (

$ \phi $

) is sufficiently rare or sufficiently prevalent. When informed speculation is sufficiently rare, liquidity-exposed shareholders face limited adverse-selection trading costs in the benchmark, so the benefit of reducing the speculator’s profits is small. In this case, the wealth transfer to liquidity-insulated shareholders dominates, and liquidity-exposed shareholders prefer less informative buybacks.

) is sufficiently rare or sufficiently prevalent. When informed speculation is sufficiently rare, liquidity-exposed shareholders face limited adverse-selection trading costs in the benchmark, so the benefit of reducing the speculator’s profits is small. In this case, the wealth transfer to liquidity-insulated shareholders dominates, and liquidity-exposed shareholders prefer less informative buybacks.

Proposition 2. When informed speculation is sufficiently rare (

$ \phi <\underline{\phi} $

), the expected payoff of liquidity-exposed shareholders decreases with the informativeness of buybacks

$ \left(\frac{\partial {U}_B^E}{\partial {b}_0}>0\right) $

), the expected payoff of liquidity-exposed shareholders decreases with the informativeness of buybacks

$ \left(\frac{\partial {U}_B^E}{\partial {b}_0}>0\right) $

.

.

This result aligns with the conventional view in the literature, which abstracts from informed speculation and concludes that liquidity-exposed shareholders prefer less informed buybacks to limit the wealth transfer to liquidity-insulated shareholders, such as insiders. Proposition 2 shows that this conclusion holds when informed speculation is sufficiently rare—including the limiting case of

$ \phi \to 0 $

implicitly assumed in many prior studies.

implicitly assumed in many prior studies.

When informed speculation is sufficiently prevalent, the opposite can occur. Liquidity-exposed shareholders face substantial adverse-selection costs in the benchmark, so the benefit from reduced speculator profits can more than offset the wealth transfer to liquidity-insulated shareholders.

Proposition 3. When informed speculation is sufficiently prevalent (

$ \phi >\overline{\phi} $

), the expected payoff of liquidity-exposed shareholders increases with the informativeness of buybacks

$ \left(\frac{\partial {U}_B^E}{\partial {b}_0}<0\right) $

), the expected payoff of liquidity-exposed shareholders increases with the informativeness of buybacks

$ \left(\frac{\partial {U}_B^E}{\partial {b}_0}<0\right) $

.

.

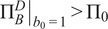

Proposition 3 suggests that the firm can use informed buybacks to protect its liquidity-exposed shareholders from adverse-selection trading costs, consistent with the findings of Wiggins (Reference Wiggins1994), who documents that the adverse-selection component of the bid–ask spread tends to widen before the authorization of a buyback program and narrow afterward. More recently, Hillert, Maug, and Obernberger (Reference Hillert, Maug and Obernberger2016) conclude that “the information content of repurchases is not associated with a deterioration of liquidity […] higher information content seems to be associated with improvements and not with deterioration in liquidity at the time repurchases were executed.”

The preceding analysis might suggest that uninformed buybacks are benign—they minimize wealth transfers to insiders while avoiding the complications of informed execution. They are not:

Corollary 1. Relative to the benchmark without buybacks (Lemma 1), a buyback program strictly lowers the expected payoff of the firm’s liquidity-exposed shareholders when buybacks are uninformed (

$ {b}_0=1 $

) and informed speculation is present (

$ \phi >0 $

) and informed speculation is present (

$ \phi >0 $

).

).

At first glance, Corollary 1 may seem puzzling. Uninformed buybacks—which are always executed regardless of firm fundamentals—neither make nor lose money in expectation. Why should they harm liquidity-exposed shareholders?

The crux of the result is that the speculator’s informed trading induces a correlation between the liquidity trades of liquidity-exposed shareholders and the profitability of buybacks. The presence of informed speculative trading (

$ \phi >0 $

) results in an equilibrium pricing rule that increases with order flow even when buybacks are uninformed. When liquidity-exposed shareholders sell to meet liquidity needs, they simultaneously reduce their stake in the firm and push down the price at which buybacks are executed. Consequently, they are less likely to retain shares in states where buybacks generate gains. Even though uninformed buybacks break even in expectation, liquidity-exposed shareholders receive a disproportionately small share of the gains and bear a disproportionately large share of the losses. This correlation causes liquidity-exposed shareholders to incur net losses from uninformed buybacks. Such a channel is absent in conventional models without buybacks, where informed speculation affects only the price at which liquidity-exposed shareholders sell, not the per-share value of the shares they retain.

) results in an equilibrium pricing rule that increases with order flow even when buybacks are uninformed. When liquidity-exposed shareholders sell to meet liquidity needs, they simultaneously reduce their stake in the firm and push down the price at which buybacks are executed. Consequently, they are less likely to retain shares in states where buybacks generate gains. Even though uninformed buybacks break even in expectation, liquidity-exposed shareholders receive a disproportionately small share of the gains and bear a disproportionately large share of the losses. This correlation causes liquidity-exposed shareholders to incur net losses from uninformed buybacks. Such a channel is absent in conventional models without buybacks, where informed speculation affects only the price at which liquidity-exposed shareholders sell, not the per-share value of the shares they retain.

The stock buyback literature often emphasizes how informed buybacks can hurt liquidity-exposed shareholders (e.g., Barclay and Smith (Reference Barclay and Smith1988), Brockman and Chung (Reference Brockman and Chung2001), Buffa and Nicodano (Reference Buffa and Nicodano2008), Fried (Reference Fried2013), and Babenko et al. (Reference Babenko, Tserlukevich and Wan2020)). This conventional view suggests that firms could protect them by committing not to use the manager’s private information when executing buybacks. The analysis in this section shows that this view is incomplete. While informed buybacks do transfer wealth to liquidity-insulated shareholders, uninformed buybacks are not a neutral alternative. They subject liquidity-exposed shareholders to additional adverse-selection costs arising from the speculator’s informed trades. In fact, when informed speculation is sufficiently prevalent, informed buybacks can actually benefit liquidity-exposed shareholders by reducing the speculator’s profits (Proposition 3). The desirability of informed versus uninformed buybacks thus depends critically on the level of informed speculation already present in the market.

IV. Manager’s Buyback Strategy

This section examines the optimal buyback strategy of a manager who maximizes

$ \unicode{x1D53C}\left[\omega P+V\right] $

, where

$ P $

, where

$ P $

is the firm’s stock price at

$ t=1 $

is the firm’s stock price at

$ t=1 $

,

$ V $

,

$ V $

is the firm’s per-share value at

$ t=2 $

is the firm’s per-share value at

$ t=2 $

, and

$ \omega \ge 0 $

, and

$ \omega \ge 0 $

captures her concern for the firm’s interim stock price. When

$ \omega =0 $

captures her concern for the firm’s interim stock price. When

$ \omega =0 $

, the manager only cares about the firm’s per-share value at

$ t=2 $

, the manager only cares about the firm’s per-share value at

$ t=2 $

. As

$ \omega $

. As

$ \omega $

increases, she places greater emphasis on the interim stock price. In the limiting case as

$ \omega \to \infty $

increases, she places greater emphasis on the interim stock price. In the limiting case as

$ \omega \to \infty $

, her objective is driven entirely by the interim stock price.

, her objective is driven entirely by the interim stock price.

Recall that the manager’s buyback strategy specifies the probability with which she executes buybacks when firm fundamentals are high (

$ {b}_1 $

) and when they are low (

$ {b}_0 $

) and when they are low (

$ {b}_0 $

). When firm fundamentals are high (

$ A=1 $

). When firm fundamentals are high (

$ A=1 $

), executing buybacks is a dominant strategy for the manager. Buying back

$ x $

), executing buybacks is a dominant strategy for the manager. Buying back

$ x $

shares strictly increases the expected market-clearing stock price at

$ t=1 $

shares strictly increases the expected market-clearing stock price at

$ t=1 $

and generates trading profits that raise the per-share value at

$ t=2 $

and generates trading profits that raise the per-share value at

$ t=2 $

. Hence, when the manager learns that firm fundamentals are high, she executes buybacks with certainty (

$ {b}_1^{\ast }=1 $

. Hence, when the manager learns that firm fundamentals are high, she executes buybacks with certainty (

$ {b}_1^{\ast }=1 $

).

).

However, when firm fundamentals are low (

$ A=0 $

), the manager faces a trade-off. Executing buybacks increases the expected market-clearing stock price at

$ t=1 $

), the manager faces a trade-off. Executing buybacks increases the expected market-clearing stock price at

$ t=1 $

—because the equilibrium pricing rule is increasing in order flow—but generates trading losses that reduce per-share value at

$ t=2 $

—because the equilibrium pricing rule is increasing in order flow—but generates trading losses that reduce per-share value at

$ t=2 $

. The optimal buyback strategy depends on her concern about the interim stock price (

$ \omega $

. The optimal buyback strategy depends on her concern about the interim stock price (

$ \omega $

):

):

Proposition 4. Upon learning that firm fundamentals are high, the manager executes buybacks with certainty (

$ {b}_1^{\ast }=1 $

). Upon learning that firm fundamentals are low, she executes buybacks with probability

$ {b}_0^{\ast } $

). Upon learning that firm fundamentals are low, she executes buybacks with probability

$ {b}_0^{\ast } $

:

:

where

$ 0<\underline{\omega}<\overline{\omega} $

.Footnote

19

.Footnote

19

When the manager places little weight on the interim stock price (

$ \omega <\underline{\omega} $

), she never buys back overvalued shares. For intermediate values (

$ \omega \in \left[\underline{\omega},\overline{\omega}\right] $

), she never buys back overvalued shares. For intermediate values (

$ \omega \in \left[\underline{\omega},\overline{\omega}\right] $

), the probability of buyback execution increases continuously with

$ \omega $

), the probability of buyback execution increases continuously with

$ \omega $

as the manager becomes increasingly inclined to inflate the stock price by buying back overvalued shares. When her concerns about the interim stock price are strong (

$ \omega >\overline{\omega} $

as the manager becomes increasingly inclined to inflate the stock price by buying back overvalued shares. When her concerns about the interim stock price are strong (

$ \omega >\overline{\omega} $

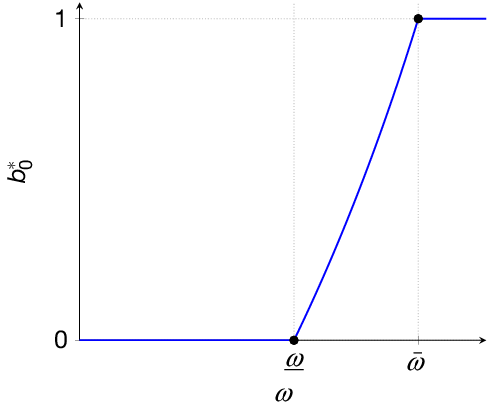

), she buys back shares regardless of firm fundamentals. Figure 3 illustrates this relationship. These predictions align with the evidence that managers facing stronger short-term incentives execute more value-destroying buybacks (e.g., Cheng, Harford, and Zhang (Reference Cheng, Harford and Zhang2015), Almeida, Fos, and Kronlund (Reference Almeida, Fos and Kronlund2016), and Edmans, Fang, and Huang (Reference Edmans, Fang and Huang2022)).

), she buys back shares regardless of firm fundamentals. Figure 3 illustrates this relationship. These predictions align with the evidence that managers facing stronger short-term incentives execute more value-destroying buybacks (e.g., Cheng, Harford, and Zhang (Reference Cheng, Harford and Zhang2015), Almeida, Fos, and Kronlund (Reference Almeida, Fos and Kronlund2016), and Edmans, Fang, and Huang (Reference Edmans, Fang and Huang2022)).

Proposition 5. The informativeness of buybacks increases with expected fundamentals (

$ \theta $

) and the scale of the buyback program (

$ k $

) and the scale of the buyback program (

$ k $

), and decreases with the prevalence of informed speculation (

$ \phi $

), and decreases with the prevalence of informed speculation (

$ \phi $

).

).

Figure 3 illustrates the relationship between the manager’s optimal buyback decision and her concern for the interim stock price. For low

$ \omega <\underline{\omega} $

, the manager never executes the buyback, for intermediate

$ \omega \in \left[\underline{\omega},\overline{\omega}\right] $

, the manager never executes the buyback, for intermediate

$ \omega \in \left[\underline{\omega},\overline{\omega}\right] $

, she executes with an interior probability, and for high

$ \omega >\overline{\omega} $

, she executes with an interior probability, and for high

$ \omega >\overline{\omega} $

, she executes the buyback with certainty. Hence, the informativeness of buybacks worsens with

$ \omega $

, she executes the buyback with certainty. Hence, the informativeness of buybacks worsens with

$ \omega $

.

.

FIGURE 3 Long description