I. Introduction

Taxation plays a crucial role in resource allocation in society and has a significant impact on firms’ operating, investing, and financing decisions (Slemrod (Reference Slemrod, Cnossen and Sinn2003)). In the United States, the political ideologies of politicians, legislators, and members of the judiciary can have a profound effect on tax policy. On the conventional liberal-to-conservative political spectrum, liberals tend to favor increasing tax revenue, especially by taxing businesses, whereas conservatives often prefer to lower taxes, favoring corporations (Howard (Reference Howard2005), (Reference Howard2010)), see also the model assumptions in Dixit and Londregan (Reference Dixit and Londregan1998), Roemer (Reference Roemer1999), and Krasa and Polborn (Reference Krasa and Polborn2014)). The judicial branch is vital to the enforcement of tax policy, as it connects the executive and legislative branches of tax enforcement by interpreting tax laws to resolve disputes between taxpayers and the Internal Revenue Service (IRS). Legal research suggests that liberal judges are more likely than conservative judges to rule in favor of the government in corporate tax lawsuits (Staudt, Epstein, and Wiedenbeck (Reference Staudt, Epstein and Wiedenbeck2006)). In this study, we investigate whether judges’ political ideology affects corporate tax planning, with the aim of providing insights into the role of the judicial branch in corporate decision-making.Footnote 1

U.S. tax laws are ambiguous due to their complex nature and lawmakers’ divergent political views (Mashaw (Reference Mashaw1985), Logue (Reference Logue2005), and Kopczuk (Reference Kopczuk and Sawicky2006)). While firms assert that their tax strategies comply with the letter of the law, many of these strategies are challenged by the IRS, which argues that they provide firms with tax benefits not intended by Congress (Blank (Reference Blank2009), Lawsky (Reference Lawsky2009)). When firms and the IRS cannot agree, firms may file lawsuits in federal courts. Federal judges then make rulings based on their interpretation of the relevant tax laws.

As courts are the ultimate recourse for resolving firm–IRS disputes, judges’ ideology not only affects the parties engaged in tax litigation but also looms over the entire tax collection process. In the U.S. common law system, judicial decisions in the Courts of Appeals and the Supreme Court become case law (i.e., they have binding constraints on subsequent cases) and thus affect the expected costs and benefits for other firms of using similar tax strategies in the future. The literature also suggests that judges’ ideology can have a significant impact on settlement negotiations between the IRS and firms (Internal Revenue Manual (IRM)), Guttman (Reference Guttman1993), Fogel (Reference Fogel2003), and Blank and Staudt (Reference Blank and Staudt2012)) and on IRS audit attention (Howard and Nixon (Reference Howard and Nixon2003)). We, therefore, expect firms under the jurisdiction of more liberal judges to engage in less aggressive tax planning, particularly through firms’ evaluation of the net benefits of tax planning.

All federal judges are appointed by the U.S. president. As presidents almost always appoint judges whose ideology reflects that of their political party (Dorsen (Reference Dorsen2006), Federal Judicial Center (FJC) (2006)), we follow prior research in using the partisanship of the appointing president to identify judges’ ideology (Sunstein, Schkade, and Ellman (Reference Sunstein, Schkade and Ellman2004)). That is, we label judges appointed by a Democratic president as liberal and those appointed by a Republican president as conservative. Within the federal courts, we focus on judges in the Courts of Appeals (i.e., the Circuit Courts), as these courts have the most significant influence on corporate tax planning.Footnote 2 Empirically, we calculate each circuit’s judge ideology as the probability that a randomly selected three-judge panel from the circuit is dominated by liberal judges (Huang, Hui, and Li (Reference Huang, Hui and Li2019)). As changes in a court’s judge ideology depend only on judge turnover and the party of the appointing president, these changes are arguably exogenous to corporate tax planning decisions. For instance, firms’ economic conditions are unlikely to determine judges’ eligibility to retire or the partisanship of the president that appoints judges. In sum, this measure takes advantage of variation in judges’ departures and appointments, which occur at different times across circuits, for empirical identification.

We begin by analyzing the relation between judge ideology and tax case outcomes to validate the influence of ideology in the Circuit Courts and to corroborate the proposed mechanism through which ideology affects firms’ tax planning. Using a manually collected sample of 328 corporate tax cases decided by the Circuit Courts between 1996 and 2016, we find that panels with a majority of liberal judges are 21.3% more likely to rule in favor of the IRS than panels with a majority of conservative judges, after controlling for these judges’ senior status, aptitude, and gender, as well as for circuit and year fixed effects.

Using the federal GAAP effective tax rate (hereafter, federal ETR) as a proxy for firms’ aggressiveness in federal tax planning, we find that firms engage in less aggressive tax planning when judges in the Circuit Court with jurisdiction over the firm are more liberal. This finding is consistent with the notion that a more liberal judge ideology increases the expected cost of aggressive tax planning. The deterrent effect is economically significant: A 1-standard-deviation increase in the liberal judge ideology of the Circuit Court is associated with an increase of 0.61 percentage points in the federal ETR, which amounts to a $1.65 million increase in the annual federal tax expense for the average firm in our sample (which has a mean pretax domestic income of $270.87 million).

We then conduct three sets of cross-sectional analyses to explore the mechanism through which judge ideology affects tax planning. Intuitively, the effect of judge ideology should be stronger when tax planning is more likely to attract disputes and when these disputes impose higher costs on firms. We measure firms’ likelihood of tax disputes through i) their use of uncertain and thus judiciary-sensitive tax strategies, including cross-border income shifting, Domestic Production Activities Deduction (DPAD), and R&D tax credits (Klassen and Laplante (Reference Klassen and Laplante2012), Lester and Rector (Reference Lester and Rector2016), De Simone, Mills, and Stomberg (Reference De Simone, Mills and Stomberg2019)) and ii) the degree of IRS tax enforcement risk faced by firms (Hoopes, Mescall, and Pittman (Reference Hoopes, Mescall and Pittman2012), Fox and Wilson (Reference Fox and Wilson2023)). We proxy for the costs of potential tax disputes using an indicator of consumer-brand status, as these companies face greater reputational fallout from tax controversies (Graham, Hanlon, Shevlin, and Shroff (Reference Graham, Hanlon, Shevlin and Shroff2014), Dyreng, Hoopes, and Wilde (Reference Dyreng, Hoopes and Wilde2016)). Our findings are consistent with our prediction. We find that the effect of judge ideology on federal ETR is more pronounced among firms that engage in judiciary-sensitive tax strategies, those with a greater likelihood of being audited by the IRS, those receiving more attention from the IRS, and those with consumer brands.

Next, we examine whether judge ideology influences firms’ financial outcomes through its effect on tax planning. We focus specifically on two outcomes, R&D investment and firm valuation, both of which are of significant interest to the finance audience and highly sensitive to tax strategies (e.g., Desai and Dharmapala (Reference Desai and Dharmapala2006), Akcigit and Stantcheva (Reference Akcigit, Stantcheva, Goolsbee and Jones2020)). The results of mediation tests suggest that liberal judge ideology reduces firms’ R&D investments and firm valuation by deterring tax planning. These findings suggest that the ideological stance of judges can have a broad influence on corporate financial outcomes, highlighting the importance of judicial discretion in shaping corporate behavior beyond the legal domain.

We include several additional analyses to ensure the robustness of our results and to yield further insights. Our findings are unchanged across alternative samples and model specifications, such as further including financial firms, the use of firm fixed effects, alternative standard errors adjustments, Fama–MacBeth regressions, an instrumental variable approach, and a placebo test. We also find stronger effects among firms with greater tax planning capacity, consistent with their ability to adjust strategies quickly in response to changes in the regulatory environment. To further explore whether judge characteristics moderate the effect of judge ideology, we analyze judges’ qualifications, experience, age, and gender. We find that liberal ideology has a stronger deterrent effect in circuits with female judges. This pattern is consistent with prior evidence that women, on average, exhibit greater conservatism and risk aversion than men in tax-related contexts (Powell and Ansic (Reference Powell and Ansic1997), Francis, Hasan, Wu, and Yan (Reference Francis, Hasan, Wu and Yan2014)), which may amplify the influence of liberal ideology in discouraging aggressive tax strategies.

Our article makes several important contributions to the literature. The first concerns the economic determinants of corporate tax planning (Allingham and Sandmo (Reference Allingham and Sandmo1972), Andreoni, Erard, and Feinstein (Reference Andreoni, Erard and Feinstein1998), and Slemrod (Reference Slemrod2007)). Prior studies examine the effect of tax enforcement on tax evasion (Slemrod and Yitzhaki (Reference Slemrod, Yitzhaki, Auerbach and Feldstein2002), Almunia and Lopez-Rodriguez (Reference Almunia and Lopez-Rodriguez2018), and Slemrod (Reference Slemrod2019)), focusing on actions by the legislative branch, such as the passage of a new tax law or the modification of existing ones (e.g., Auerbach (Reference Auerbach2018), Slemrod (Reference Slemrod2018), Garrett and Serrato (Reference Garrett and Serrato2019), and Hanlon, Hoopes, and Slemrod (Reference Hanlon, Hoopes and Slemrod2019)), and by the executive branch (i.e., the IRS) (Reinganum and Wilde (Reference Reinganum and Wilde1988), Mills (Reference Mills1998), Hoopes et al. (Reference Hoopes, Mescall and Pittman2012), Bozanic, Hoopes, Thornock, and Williams (Reference Bozanic, Hoopes, Thornock and Williams2017), Kubick, Lockhart, Mills, and Robinson (Reference Kubick, Lockhart, Mills and Robinson2017), DeBacker, Heim, and Tran (Reference DeBacker, Heim, Tran and Yuskavage2018), Ayers, Seidman, and Towery (Reference Ayers, Seidman and Towery2019), and Nessa, Schwab, Stomberg, and Towery (Reference Nessa, Schwab, Stomberg and Towery2020)). While both the IRS and the judiciary play key roles in tax enforcement, their roles and responsibilities differ considerably. The IRS actively detects and prosecutes tax underpayments and serves as the representative of the federal government. In contrast, the judiciary is an independent branch that should remain impartial in resolving disputes between taxpayers and the IRS. Its status as the final arbiter of tax disputes and its ability to establish precedents constrain the power of the IRS and influence future IRS enforcement. Our study is the first to show that the judicial branch, through its critical role in interpreting tax law, has a significant influence on corporate tax planning.

Second, we contribute to the growing body of research examining the role of the judiciary in corporate finance decisions and outcomes. Prior studies establish the relation between judge ideology and corporate financial disclosures (Huang et al. (Reference Huang, Hui and Li2019), Huang, Rahman, Lee, and Gu (Reference Huang, Rahman, Lee and Gu2026)). The finance, economics, and accounting literature also well documents the importance of taxation in shaping R&D investment (e.g., Mukherjee, Singh, and Žaldokas (Reference Mukherjee, Singh and Žaldokas2017), Akcigit and Stantcheva (Reference Akcigit, Stantcheva, Goolsbee and Jones2020), Williams and Williams (Reference Williams and Williams2021), Goldman, Lampenius, Radhakrishnan, Stenzel, and de Almeida (Reference Goldman, Lampenius, Radhakrishnan, Stenzel and de Almeida2024), and Cowx (Reference Cowx2025)) and firm valuation (Desai and Dharmapala (Reference Desai and Dharmapala2006), Desai, Dyck, and Zingales (Reference Desai, Dyck and Zingales2007)). Building on this foundation, our analyses show that the ideological orientation of the judiciary influences corporate decisions and valuation processes by shaping tax strategies. This finding not only highlights the critical role of tax planning in financial outcomes but also offers the novel insight that judge ideology is a significant factor in this relation. Our research thus connects the fields of taxation, legal studies, and finance, providing valuable insights for academia, practitioners, and regulators into how judge ideology interacts with corporate financial outcomes.

Third, we contribute to the literature on tax disputes and litigation. Although Staudt et al. (Reference Staudt, Epstein and Wiedenbeck2006) examine how judge ideology influences corporate tax litigation outcomes, they focus on cases heard by the Supreme Court. We are the first to document how Circuit Court judge ideology affects rulings on corporate tax cases. Furthermore, as most corporate tax disputes are settled between the firm and the IRS before a case is filed in court (Gerdes, Langdon, and Louthan (Reference Gerdes, Langdon and Louthan2001), IRS (2017)), our evidence based on firms’ ex ante actions (i.e., tax-planning strategies) helps to reveal the full effect of the judicial branch on corporate taxation.

II. Background and Literature Review

A. Government and Corporate Tax Planning

Corporate tax planning, which includes all transactions that affect a firm’s explicit tax liability, is an important issue for businesses and governments and attracts widespread attention from politicians and the media (Dyreng, Hanlon, and Maydew (Reference Dyreng, Hanlon and Maydew2008), Hanlon and Heitzman (Reference Hanlon and Heitzman2010), Dyreng et al. (Reference Dyreng, Hoopes and Wilde2016), and Chen, Schuchard, and Stomberg (Reference Chen, Schuchard and Stomberg2019)). In its report on the tax gap, the IRS estimated that corporate underreporting worth $37 billion occurred annually between 2014 and 2016, suggesting an underreporting rate of 12%. Unsurprisingly, therefore, researchers in accounting, finance, economics, and law make significant efforts to understand the determinants of corporate tax planning (e.g., Shackelford and Shevlin (Reference Shackelford and Shevlin2001), Slemrod (Reference Slemrod2007), Hanlon and Heitzman (Reference Hanlon and Heitzman2010), and Wilde and Wilson (Reference Wilde and Wilson2018)).

Numerous political science studies investigate the influence of the legislative branch, including governors, state legislators (Alt and Lowry (Reference Alt and Lowry1994), Poterba (Reference Poterba1994), Reed (Reference Reed2006), and Besley, Persson, and Sturm (Reference Besley, Persson and Sturm2010)), and key congressional committees (Young, Reksulak, and Shughart (Reference Young, Reksulak and Shughart2001), Baloria and Klassen (Reference Baloria and Klassen2018)), on corporate tax collection. They find that the dynamics of these political bodies (e.g., their competition, partisanship, and representation) explain the variation in local tax rates and IRS enforcement efforts. The literature also examines the influence of the executive branch (i.e., the IRS), which administers tax laws by translating these laws into detailed rules, regulations, and procedures and then enforcing them via audits. These studies generally find that firms engage in less aggressive tax planning when IRS enforcement increases, including when the expected probability of an IRS audit is higher and when a nearby IRS office employs industry specialists (Hoopes et al. (Reference Hoopes, Mescall and Pittman2012), Kubick et al. (Reference Kubick, Lockhart, Mills and Robinson2017)).Footnote 3

The third government branch (i.e., the judiciary) interprets tax laws and resolves tax disputes between the IRS and taxpayers through its rulings. Given that courts are the ultimate recourse for tax disputes, judges’ ideology directly affects tax case rulings and also looms over the entire tax collection process, including settlement negotiations (IRM, Guttman (Reference Guttman1993), and Fogel (Reference Fogel2003)) and IRS audits (Howard and Nixon (Reference Howard and Nixon2003)). Despite the importance of the judicial branch in tax collection, the potential effects of the judiciary on corporate tax planning remain underexplored.

B. Political Ideology and Tax Collection

When considering disputes between firms and the government, those related to tax are arguably among the most important and controversial, because of their widespread potential impacts. As stated by Howard ((Reference Howard2005), p. 146), “the collection and distribution of revenue is the single most important and politically charged issue that any government must confront. Who or what should pay and how much, and who or what should receive this revenue and how much, are inescapably political questions charged with ideological overtones.” The traditional liberal–conservative distinction suggests that liberal ideology favors the government, whereas conservative ideology favors firms in tax disputes (Howard (Reference Howard2002), (Reference Howard2005), and Howard and Nixon (Reference Howard and Nixon2002)). For instance, the Republican Party platform states that “Republicans advocate lower taxes, reasonable regulation, and smaller, smarter government” (Republican National Committee (2004), (2008)).

Ample evidence indicates that ideological preferences affect all three government branches in tax matters. For example, Republican presidents and congressmen are far more likely than their Democratic counterparts to favor tax cuts. Analyzing presidential State of the Union addresses, Bagchi (Reference Bagchi2016) finds that 81.2% of tax policy statements made by Republican presidents are in favor of tax cuts, compared with 44.8% of such statements made by Democratic presidents. During the legislation of the two Bush tax cuts in 2001 and 2003 and the Tax Cuts and Jobs Act of 2017, most members of Congress cast their votes along party lines.Footnote 4 Furthermore, Democrat-controlled Congresses allocate larger budgets and more resources for IRS personnel (Scholz and Wood (Reference Scholz and Wood1998), Bagchi (Reference Bagchi2016)). Anecdotally, from 2011 to 2018, congressional Republicans repeatedly cut IRS budgets, leading to a one-third decrease in IRS enforcement staff (Kiel and Eisinger (Reference Kiel and Eisinger2018)). As a result, the IRS generally conducts fewer corporate audits under a Republican regime than under a Democratic one.

In the judiciary branch, both legal and political science studies find that ideology is among the most important personal attributes of judges in terms of its influence on civil liberties and economic lawsuit outcomes (Johnston (Reference Johnston1976), Tate (Reference Tate1981), Segal and Cover (Reference Segal and Cover1989), and Staudt et al. (Reference Staudt, Epstein and Wiedenbeck2006)).Footnote 5 Due to liberals’ pro-government tendencies, liberal judges are expected to be more likely than conservative judges to rule in favor of the government in corporate tax lawsuits. Consistent with this conjecture, Staudt et al. (Reference Staudt, Epstein and Wiedenbeck2006) find that liberal justices in the Supreme Court are more likely to vote in favor of the government in tax cases than are conservative justices.Footnote 6

C. How Judge Ideology Affects Corporate Tax Planning

Tax planning is by nature forward-looking and requires managers and tax directors to consider the expected costs and benefits of a tax strategy when determining whether to adopt it and, if it is adopted, how aggressively to pursue it.Footnote 7 This assessment requires managers to assess the expected outcome if the strategy is challenged, that is, the court ruling if the dispute goes to trial or the settlement amount if the case is settled, as well as the likelihood of an IRS challenge, all of which are influenced by judge ideology.

First, liberal judges are more likely than conservative judges to rule against firms (in favor of the IRS), which reduces the expected net benefits of aggressive tax planning that may end up before the court. After losing tax cases, firms pay taxes and penalties, and both firms and managers face reputational damage arising from unfavorable media coverage and negative publicity (Graham et al. (Reference Graham, Hanlon, Shevlin and Shroff2014), Dyreng et al. (Reference Dyreng, Hoopes and Wilde2016), and Chen et al. (Reference Chen, Schuchard and Stomberg2019)). Furthermore, because judicial precedents are either binding or persuasive when deciding subsequent cases with similar issues or facts under the common law system, current judge ideology can affect firms’ tax planning decisions through the litigation outcomes of recent cases (Heitzman and Ogneva (Reference Heitzman and Ogneva2019), Donelson, Glenn, and Yust (Reference Donelson, Glenn and Yust2022), and Nesbitt, Outslay, and Persson (Reference Nesbitt, Outslay and Persson2023)).

Second, judge ideology can have a significant impact on the negotiations between the taxpayer and the IRS and therefore on settlement outcomes. During negotiations between a firm and the IRS, both sides are likely to consider judicial attributes, such as judges’ ideology and biases, when estimating the lawsuit outcome should the dispute reach court (see Section IA.1 of the Supplementary Material for details of the settlement negotiation). As noted by Blank and Staudt ((Reference Blank and Staudt2012), p. 1665), “the parties negotiate in the shadow of litigation” throughout the tax dispute process. The IRS explicitly requires its officers to review the strengths and weaknesses of the respective positions taken in the case and to propose a settlement and penalties based on the “hazards of litigation,” that is, the likelihood that the IRS will prevail in a lawsuit (IRM, Fogel (Reference Fogel2003)).Footnote 8 Judges can even play a direct role in guiding the parties to reach an agreement by offering a tentative view on how they may rule in the case.Footnote 9

Third, research finds that the IRS is more likely to audit firms when judges are more liberal, which suggests that judge ideology can affect IRS enforcement actions. For instance, using state-level audit data from 1960 to 1988, Howard and Nixon (Reference Howard and Nixon2003) document that when a Court of Appeals has more liberal judges, the IRS’s audit attention in states that are under that court’s jurisdiction shifts away from individuals and toward corporate taxpayers. This observation is consistent with the findings of Nessa et al. (Reference Nessa, Schwab, Stomberg and Towery2020), which suggest that the IRS allocates more resources to taxpayer positions that are supported by weaker facts and more likely to be settled in the IRS’s favor. Thus, to the extent that IRS enforcement actions are affected by judge ideology, current judge ideology can have a significant effect on firms’ tax planning. In sum, we argue that, given its effects on tax dispute outcomes and IRS audits, judge ideology is likely to influence firms’ tax planning through their evaluation of the net benefits of aggressive tax planning.Footnote 10

III. Variable Measurement and Sample Description

A. Variable Measurement

The U.S. federal court hierarchy that handles the vast majority of tax cases consists of four courts spanning three levels: two trial courts, the Tax Court and the District Courts; intermediate appeals courts, the Circuit Courts; and the highest court in the federal judiciary, the Supreme Court (see Figure 1 and Section IA.1 of the Supplementary Material for details). We do not focus on the Supreme Court, because it rarely hears tax cases (Hoffman, Raabe, and Maloney (Reference Hoffman, Raabe, Young, Nellen, Maloney and Boyd2017)). Of the three remaining courts, we expect the Circuit Courts to exert the most significant influence on corporate tax planning for two reasons. First, Tax Court and District Court decisions are subject to mandatory review by the Circuit Courts if the losing party appeals. Thus, Tax Court and District Court judges consider the ideology of the Circuit Court judges when deciding cases (Schanzenbach and Tiller (Reference Schanzenbach and Tiller2007), Randazzo (Reference Randazzo2008)). Second, Circuit Court decisions are binding in the trial courts within their jurisdictions. That is, both the Tax Court and District Courts must follow the case precedents set by the Circuit Court that has jurisdiction over the case.Footnote 11 As Cross ((Reference Cross2007), p. 2) argues, “In large measure, it is the Circuit Courts that create U.S. law. They represent the true iceberg, of which the Supreme Court is but the most visible tip. The Circuit Courts play by far the greatest legal policymaking role in the United States judicial system.”

Figure 1 displays the procedure for tax disputes in the federal judicial system. Section IA.1 of the Supplementary Material provides a detailed explanation.

As Circuit Courts assign each case to a randomly selected three-judge panel, we measure judge ideology as the probability of the panel being dominated by Democratic presidents’ appointees (Liberal Circuit). We obtain the name of the president who appointed each judge from the FJC. While using the partisanship of the appointing presidents to measure federal judge ideology aligns with prior empirical legal studies (Sunstein et al. (Reference Sunstein, Schkade and Ellman2004)), it is important to note that judges may not always strictly adhere to party lines on tax issues and that judicial behavior can be influenced by factors beyond political affiliation, which can introduce noise into the measure.

Following the literature, we include both active and senior judges in the circuit (Huang et al. (Reference Huang, Hui and Li2019)). As firms that sue the IRS in a District Court must file their cases in the district where they are headquartered (28 U.S.C. $1402(a)(2) (2006)), we assign each firm-year observation to the corresponding courts based on the firm’s historical headquarters location. We calculate each court’s ideology at the end of the first month of the firm’s fiscal year, as this is likely to be when managers make tax-planning decisions. In doing so, we measure the current judge ideology that affects the outcomes of recent tax cases with similar strategies and reflects firms’ expectations of judge ideology in potential future tax disputes (Heitzman and Ogneva (Reference Heitzman and Ogneva2019), Donelson et al. (Reference Donelson, Glenn and Yust2022), and Nesbitt et al. (Reference Nesbitt, Outslay and Persson2023)).Footnote 12

To validate our measure, we examine the relation between judge ideology and the outcomes of corporate tax cases in the Circuit Courts. We manually collect detailed information—including the docket number, docket year, appellant identity, case outcome, judge’s name, tax year of the litigated tax position, and lower court from which the appeal was taken—on 328 Circuit Court cases involving disputes between the IRS and corporate taxpayers decided from 1996 to 2016 using the Westlaw Classic database. Of these cases, 156, 116, and 56 originate from appeals of decisions by the District Courts, the Tax Court, and the Court of Federal Claims, respectively. We estimate a probit model in which the dependent variable is whether the court rules in favor of the IRS, and the key independent variable is an indicator of whether at least two judges on the three-judge panel were appointed by Democratic presidents. We control for lower court type and judges’ senior status, ability, and gender, obtained from the FJC and Google searches, and include circuit and decision year fixed effects. The results, presented in Table IA.2 in the Supplementary Material, show that panels with a liberal majority are 21.3% more likely to rule in favor of the IRS than panels with a conservative majority, confirming the significant influence of judge ideology on corporate tax case outcomes in the Circuit Courts.

Our main measure of corporate tax planning is the federal ETR (Fed ETR Dom), defined as total federal tax expense divided by pretax domestic income. As federal judge ideology should only affect corporate tax obligations related to the federal government, we use total federal tax expense as the numerator to exclude amounts related to state and foreign tax issues and use pretax domestic income as the denominator to focus on domestic tax planning. A higher value of Fed ETR Dom indicates that the firm incurs a greater federal tax expense per dollar of pretax domestic income, indicating less aggressive domestic tax planning.

B. Sample Description

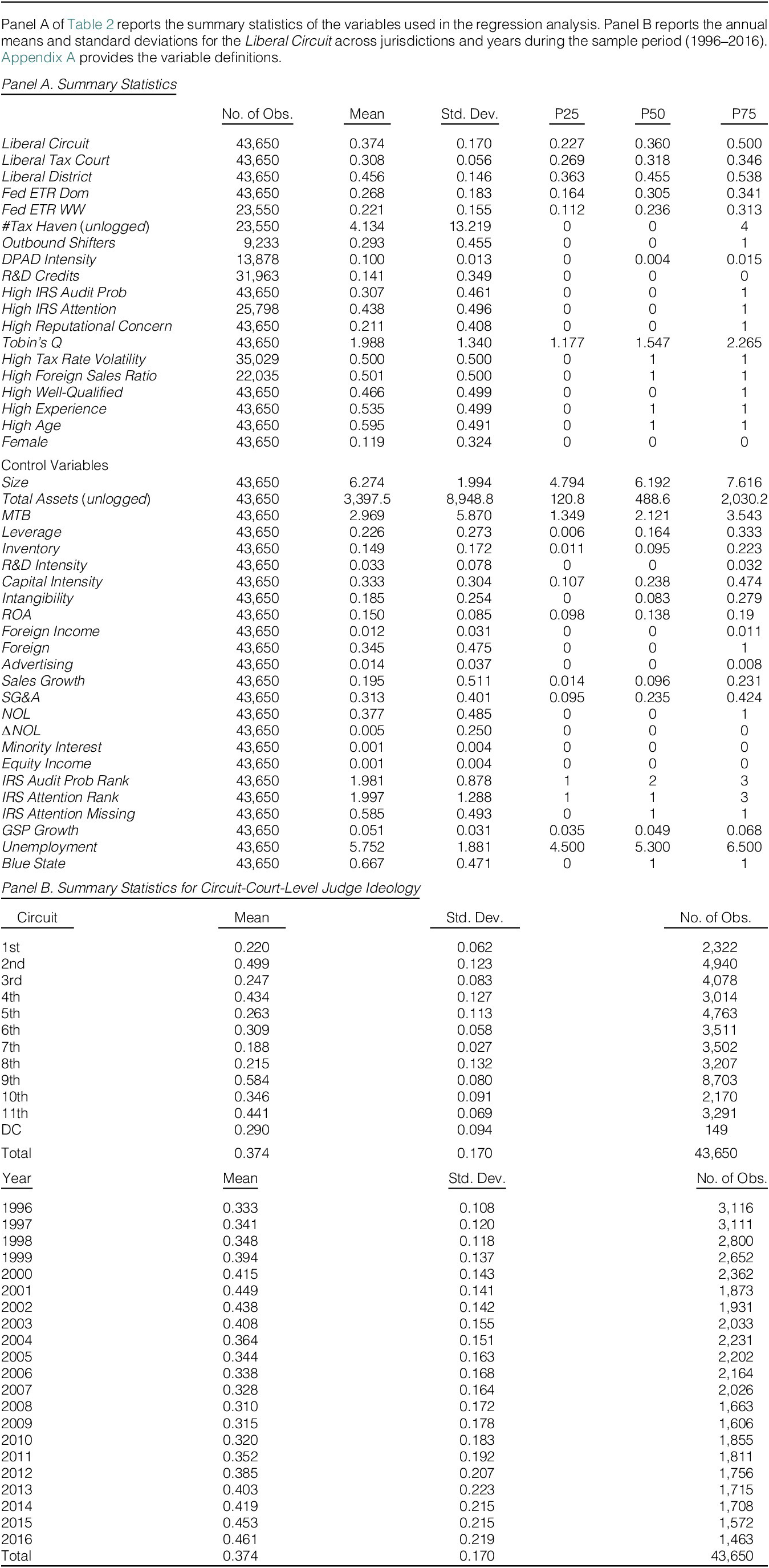

Table 1 reports the sample selection procedures for our main tests. Our sample includes firm-year observations in Compustat from 1996 to 2016.Footnote 13 We begin the sample period in 1996 because firm filings from the Securities and Exchange Commission (SEC)’s EDGAR system, from which we extract firms’ historical headquarters locations, have sparse coverage before 1996. We require firms to be incorporated in the United States and headquartered in a U.S. state so that they are subject to U.S. income tax, and we can determine which courts have jurisdiction over them. We exclude financial firms and further eliminate firm-year observations if they are missing the data necessary to construct the variables in our tests. Our main sample includes 43,650 firm-year observations from 5,766 unique firms. Some tests have smaller sample sizes due to additional data requirements.

Panel A of Table 2 presents the descriptive statistics of the variables included in the main regression. The mean and median Fed ETR Dom are 0.268 and 0.305, respectively. An average firm-year in our sample has total assets of $3,398 million, an MTB of 2.97, and leverage of 22.6% (of total assets). Of the sample firm-years, 34.5% report positive foreign income and 37.7% report a loss carryforward. The descriptive statistics are consistent with those reported in previous studies (e.g., Dyreng, Hanlon, and Maydew (Reference Dyreng, Hanlon and Maydew2010), Hoopes et al. (Reference Hoopes, Mescall and Pittman2012), and Rego and Wilson (Reference Rego and Wilson2012)).

Panel B of Table 2 presents the means and standard deviations of judge ideology across circuits and over time. The statistics show substantial variation across jurisdictions, with an average cross-sectional standard deviation of 0.17. During the sample period, the Second, Fourth, Ninth, and Eleventh Circuits are, on average, more liberal, and the First, Seventh, and Eighth Circuits are more conservative. The majority of changes in judge composition are driven by judge deaths, with the remainder due to retirements, resignations, and reappointments. As such, we consider judges’ departures to be largely exogenous to contemporaneous factors, including firm characteristics and tax policy.Footnote 14 In addition, because judge departures and appointments occur at different times across circuits, court ideology does not always move in tandem. For example, from 2006 to 2012, the Seventh and Eighth Circuits became more conservative, while the First, Second, and Ninth Circuits became more liberal. In Table IA.3 in the Supplementary Material, we tabulate the number of judge changes by ideology in each circuit-year.

This combination of cross-sectional and time-series variations in judge ideology enables us to study the impact of the judicial branch on corporate tax planning while maintaining adequate statistical power.

IV. Judge Ideology and Corporate Tax Planning

A. Judge Ideology and Federal GAAP ETR

To examine the relation between judge ideology and tax planning, we use OLS to estimate the following model:

$$ {\displaystyle \begin{array}{c} Fed\hskip0.52em ETR\hskip0.52em Dom=a+{b}_1\cdot Liberal\ Circuit+ Controls\\ {}\hskip12.5em +\hskip0.3em MSA\hskip0.52em FE+ Industry\times Year\hskip0.42em FE+\varepsilon .\end{array}} $$

$$ {\displaystyle \begin{array}{c} Fed\hskip0.52em ETR\hskip0.52em Dom=a+{b}_1\cdot Liberal\ Circuit+ Controls\\ {}\hskip12.5em +\hskip0.3em MSA\hskip0.52em FE+ Industry\times Year\hskip0.42em FE+\varepsilon .\end{array}} $$

As outlined in Section II.C, we predict that firms engage in less aggressive federal tax planning when they are in a circuit with a more liberal ideology (i.e., a positive coefficient on circuit judge ideology, b 1). We follow prior research in controlling for a number of firm characteristics associated with tax planning (e.g., Dyreng, Hanlon, and Maydew (Reference Dyreng, Hanlon and Maydew2010), Hoopes et al. (Reference Hoopes, Mescall and Pittman2012), and Rego and Wilson (Reference Rego and Wilson2012)), including firm size (Size); market-to-book ratio (MTB); leverage (Leverage); asset intensity (Inventory, R&D, Capital Intensity, and Intangibility); pretax profitability (ROA); income from foreign operations (Foreign Income); multinationality (Foreign); advertising expenditure (Advertising); an indicator of loss carried forward (NOL); the change in NOL (ΔNOL); sales growth (Sales Growth); selling, general, and administrative expenditures (SG&A); minority interest (Minority Interest); and income or loss reported under the equity method (Equity Income). We include the IRS audit probability (IRS Audit Prob Rank) to control for the average IRS enforcement level faced by firms in a certain size group in a given year (Hoopes et al. (Reference Hoopes, Mescall and Pittman2012)). We also include IRS attention (IRS Attention Rank) to control for firm-specific scrutiny imposed by the IRS in a given year, based on the IRS’s downloads of firm filings from EDGAR (Hoopes et al. (Reference Hoopes, Mescall and Pittman2012), Bozanic et al. (Reference Bozanic, Hoopes, Thornock and Williams2017), and Fox and Wilson (Reference Fox and Wilson2023)).Footnote 15

To mitigate concerns that our observed effects are confounded by local economic and political factors, we control for state-level economic growth, unemployment rate, and an indicator variable for blue states, defined based on the voting percentage for the Democratic candidate in the last presidential election. Appendix A provides detailed definitions of the variables. Finally, we include metropolitan statistical area (MSA) fixed effects to account for unobservable time-invariant differences across geographic regions, including economic, demographic, and political characteristics, and industry-by-year fixed effects to control for differences in tax planning across industries and changes in regulatory and political environments over time, such as those driven by changes in the president, the IRS, or Congress or by the passage of new federal tax laws (Hoopes et al. (Reference Hoopes, Mescall and Pittman2012), Bagchi (Reference Bagchi2016), and Nessa et al. (Reference Nessa, Schwab, Stomberg and Towery2020)).

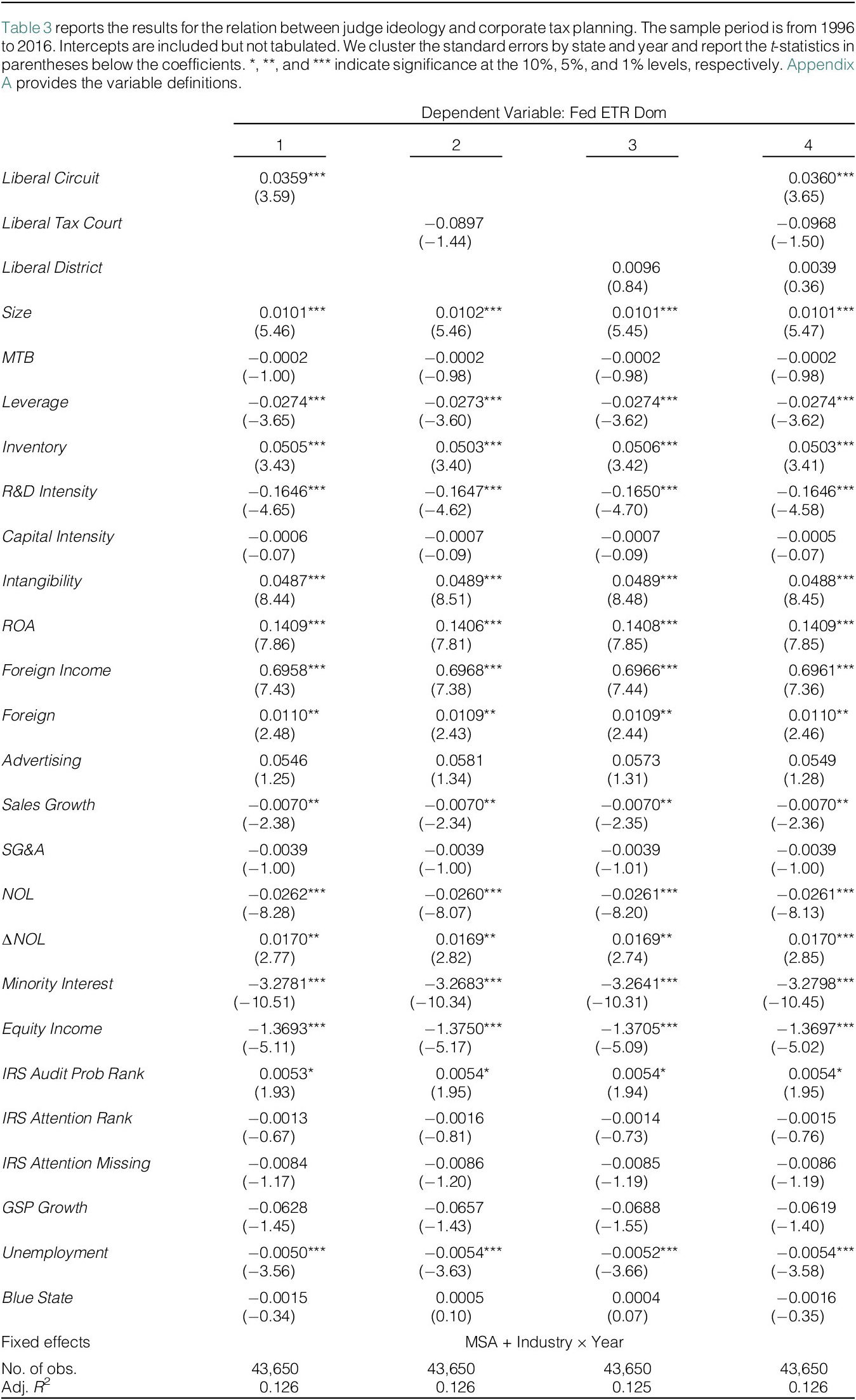

Table 3 presents the regression results for the relation between Fed ETR Dom and circuit judge ideology. Column 1 shows that the coefficient on Liberal Circuit is positive and significant (0.0359, t = 3.59), consistent with our expectation that firms are less aggressive in their federal tax planning when circuit judges are more liberal. In terms of economic significance, a 1-standard-deviation increase in Liberal Circuit is associated with an increase in Fed ETR Dom of 0.61 percentage points. For the average firm in our sample (with a mean annual pretax domestic income of $270.87 million), the estimated effect amounts to a $1.65 million increase in the annual total federal tax expense. The results for the control variables are generally consistent with those reported in the literature (e.g., Dyreng, Hanlon, and Maydew (Reference Dyreng, Hanlon and Maydew2010), Hoopes et al. (Reference Hoopes, Mescall and Pittman2012)). For example, we find that Fed ETR Dom is negatively associated with Leverage, R&D Intensity, NOL, and Minority Interest and positively associated with Size, Inventory, Intangibility, and IRS Audit Prob Rank. Footnote 16

In columns 2 and 3, we replace Liberal Circuit with the judge ideology in the Tax and District Courts, respectively, as measured by the percentage of judges appointed by a Democratic president. We do not find evidence that judge ideology in the two lower courts affects tax planning (the coefficients on Liberal Tax Court and Liberal District are not significant). The nonsignificant result for the Liberal Tax Court can be attributed to a lack of cross-sectional variation in judge ideology in the Tax Court. District Court judges’ lack of influence is consistent with prior studies’ finding that judge ideology is less important in District Court decisions than in Circuit and Tax Court decisions (Howard (Reference Howard2005), (Reference Howard2010), Huang, Hui, and Zheng (Reference Huang, Hui and Zheng2025)) due to District Court judges’ lack of tax expertise and incentives to avoid reversals, as well as the constraints imposed by Circuit Courts (Randazzo (Reference Randazzo2008), Choi, Gulati, and Posner (Reference Choi, Gulati and Posner2012), and Franke et al. (Reference Franke, Huang, Li and Wang2024)). In column 4, we include all three judge ideology measures in one model and obtain similar results. In subsequent analyses, we omit the Liberal Tax Court and the Liberal District because of their insignificant effects.Footnote 17

Overall, our findings are consistent with the prediction that in making tax planning decisions, firms consider judge ideology at the Circuit Court level: They are less aggressive when Circuit Court judges are more liberal.

B. Judge Ideology and Federal GAAP ETR: Cross-Sectional Tests

We conduct a series of cross-sectional analyses to provide evidence of the mechanisms through which judge ideology affects tax planning. If firms consider judges’ political leanings when constructing tax strategies due to expected tax litigation costs, we expect the effect to be stronger when tax planning is more likely to attract disputes and when such disputes impose higher costs on firms. Empirically, we measure firms’ likelihood of tax disputes using i) the extent to which they employ uncertain tax strategies, which are more likely to be challenged, and ii) the degree of IRS tax enforcement risk they face. We proxy for the costs associated with potential tax disputes using an indicator of whether firms operate in a consumer-brand industry.

1. Tax Dispute Likelihood

First, we examine the effect of judge ideology on a subset of more uncertain tax strategies. As these strategies are more likely to be challenged by the IRS and are thus more likely to be the subject of a tax dispute than other tax strategies, we refer to them as judiciary-sensitive tax strategies. We expect judge ideology to have stronger effects if firms use these strategies, and we test this prediction using equation (2):

$$ {\displaystyle \begin{array}{c} Fed\hskip0.52em ETR\hskip0.52em Dom\hskip0.42em \left( Fed\hskip0.52em ETR\hskip0.52em WW\right)=a+{b}_1\times Liberal\ Circuit\times Tax\hskip0.52em Strategy\\ {}\hskip24.5em +\hskip0.4em {b}_2\times Liberal\ Circuit+{b}_3\times Tax\hskip0.52em Strategy\\ {}\hskip19em +\hskip0.4em Controls+ MSA\hskip0.52em FE+ Industry\\ {}\hskip6.72em \times Year\hskip0.52em FE+\varepsilon .\end{array}}\hskip0.24em $$

$$ {\displaystyle \begin{array}{c} Fed\hskip0.52em ETR\hskip0.52em Dom\hskip0.42em \left( Fed\hskip0.52em ETR\hskip0.52em WW\right)=a+{b}_1\times Liberal\ Circuit\times Tax\hskip0.52em Strategy\\ {}\hskip24.5em +\hskip0.4em {b}_2\times Liberal\ Circuit+{b}_3\times Tax\hskip0.52em Strategy\\ {}\hskip19em +\hskip0.4em Controls+ MSA\hskip0.52em FE+ Industry\\ {}\hskip6.72em \times Year\hskip0.52em FE+\varepsilon .\end{array}}\hskip0.24em $$

Our variable of interest is the coefficient on the interaction term Liberal Circuit × Tax Strategy (b1), which captures the incremental effect of circuit judge ideology on tax planning for firms that engage in judiciary-sensitive tax strategies. We examine three types of tax strategies, cross-border income shifting, DPAD, and R&D tax credits, as prior literature suggests that firms frequently report these strategies in Uncertain Tax Position filings to the IRS (Klassen and Laplante (Reference Klassen and Laplante2012), Lester and Rector (Reference Lester and Rector2016), Towery (Reference Towery2017), and De Simone et al. (Reference De Simone, Mills and Stomberg2019)).

We use two methods to identify firms that are likely to have engaged in cross-border income shifting. First, we consider the use of tax haven operations (#Tax Haven) by multinational firms (Klassen and Laplante (Reference Klassen and Laplante2012), Bennedsen and Zeume (Reference Bennedsen and Zeume2018), and Gómez-Cram and Olbert (Reference Gómez-Cram and Olbert2023)), as reported in Exhibit 21 of firms’ 10-K filings (Dyreng, Lindsey, Markle and Shackelford (Reference Dyreng, Lindsey, Markle and Shackelford2015), Chen and Lin (Reference Chen and Lin2017)). Second, we classify outbound income shifting firms as those with a lower average foreign tax rate than the U.S. statutory rate and an abnormally high foreign return on sales, following prior research (Collins, Kemsley, and Lang (Reference Collins, Kemsley and Lang1998), Klassen and Laplante (Reference Klassen and Laplante2012)). Table 2 indicates that the mean number of material subsidiaries in tax havens is 4.13, and approximately 29.3% of firm-years are identified as outbound income shifters.

For the DPAD, we first identify firms that use it by searching their annual reports for related words and phrases (Lester (Reference Lester2019)). We then measure the intensity of DPAD usage, which we refer to as DPAD Intensity, based on the size of qualifying activities, following the methodology described in Ohrn (Reference Ohrn2018). Concerning R&D tax credits, we define an indicator variable (R&D Credit) that equals 1 if a firm mentions claiming R&D tax credits in its annual report for a given year, and 0 otherwise.Footnote 18 As shown in the summary statistics in Table 2, approximately 14.1% of the sample firms disclose the use of R&D tax credits.

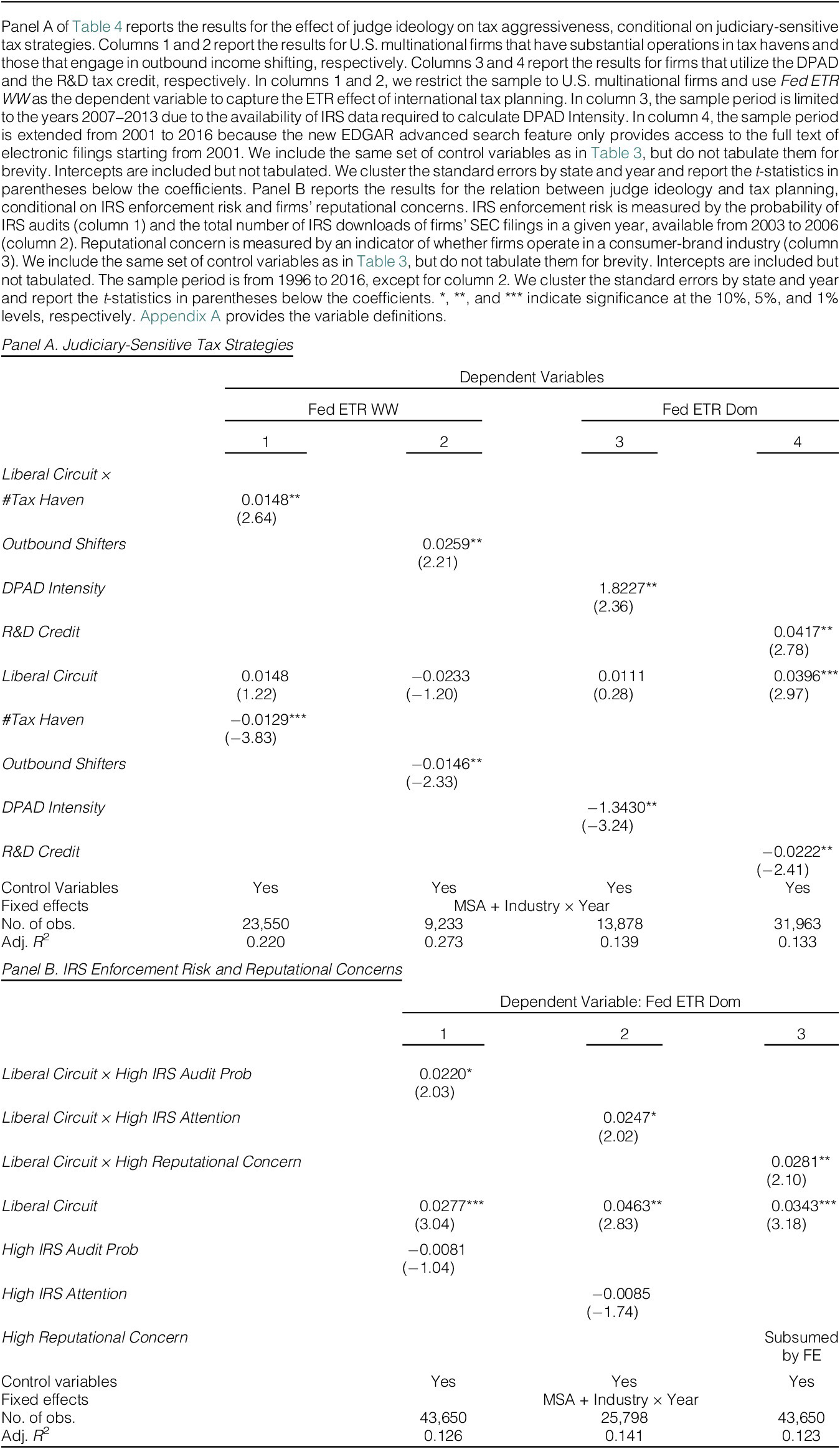

Table 4 reports the results of estimating equation (2). In Panel A, we first analyze how liberal judge ideology affects the magnitude of federal tax savings associated with cross-border tax planning.Footnote 19 Column 1 presents the results for firms’ tax haven operations (#Tax Haven). We find that the coefficient on Liberal Circuit × #Tax Haven is positive and significant (0.0148, t = 2.64), suggesting that the deterrent effect of liberal judge ideology is stronger for firms with more extensive tax haven operations. In column 2, we observe a positive and statistically significant coefficient (0.0259, t = 2.21) for Liberal Circuit × Outbound Shifters, indicating that the effect of judge ideology on tax planning strengthens when firms conduct outbound income shifting.

Columns 3 and 4 show that the coefficients on the interaction terms (Liberal Circuit × DPAD Intensity and Liberal Circuit × R&D Credit) are positive and statistically significant (1.8227 and 0.0417, respectively), at the 5% significance level. These findings support our prediction that firms that use more DPAD and R&D tax credits are more concerned about liberal judge ideology in tax planning.Footnote 20 In summary, our findings in this section demonstrate that judge ideology’s effect on aggressive tax planning is particularly strong when firms engage in judiciary-sensitive tax strategies.

2. IRS Enforcement Risk

We examine IRS enforcement risk in the second set of cross-sectional tests. During a tax audit, the IRS makes a detailed examination of the taxpayer’s return, seeks justification for and verification of the reported income and expenditures, and determines whether the taxpayer complied with the tax code. When the IRS enforcement risk is high, firms should weigh judge ideology more heavily in their tax decisions for two reasons. First, IRS scrutiny increases both the likelihood of a tax dispute and the amount of tax deficiencies, and consequently, the chance of tax litigation in courts. Second, when the IRS devotes more resources to enforcement, it increases its focus on more challenging cases that it is less certain of winning (Nessa et al. (Reference Nessa, Schwab, Stomberg and Towery2020)). Such cases are more ambiguous, which gives judges more room to exercise their discretion and increases the potential impact of judges’ ideology.

Following prior research, we employ two approaches to assess firms that are exposed to higher IRS enforcement risk. First, we consider IRS audit probability, measured as the number of face-to-face corporate audits that the IRS conducts in fiscal year t for a firm size (asset) group, divided by the total number of Form 1120 tax returns filed in the previous year for that firm size group (Hoopes et al. (Reference Hoopes, Mescall and Pittman2012), Bauer, Fang, and Pittman (Reference Bauer, Fang and Pittman2021)). Second, we consider the IRS’s attention, measured as the number of times during year t that a computer with an IRS IP address downloaded any SEC filings from EDGAR for a given firm (Bozanic et al. (Reference Bozanic, Hoopes, Thornock and Williams2017), Fox and Wilson (Reference Fox and Wilson2023)). Unlike IRS audit probability, which is constant for all firms within each asset size and year group, IRS attention is specific to each firm-year. To facilitate interpretation of the results, we define two variables, High IRS Audit Prob and High IRS Attention, to denote firm-years with above-median IRS audit probability and IRS attention, respectively.

To test our prediction, we re-estimate equation (1) while including the IRS enforcement risk and its interaction with Liberal Circuit, with the interaction as our variable of interest. Table 4 Panel B reports the results. In column 1, the coefficient on Liberal Circuit × High IRS Audit Prob is positive and statistically significant (0.0220, t = 2.03), consistent with judge ideology’s much stronger effect (79% = 0.0220/0.0277) for firms with high (vs. low) IRS audit probability. In column 2, the coefficient for the interaction term (Liberal Circuit × High IRS Attention) is likewise positive and statistically significant (0.0247, t = 2.02). This result indicates that, as with IRS audit probability, judge ideology has a more pronounced effect when firms face high (vs. low) IRS attention. Overall, these findings suggest that the impact of liberal judge ideology on tax planning is more substantial when firms face greater IRS enforcement risks, supporting the notion of a complementary relationship between the judicial and executive branches.

3. Reputational Concern

In the third set of cross-sectional tests, we investigate how costs associated with reputational concerns influence the deterrent effect associated with liberal judge ideology. Firms that depend more heavily on a strong brand image are more concerned about the reputational damage from tax controversies. This pattern aligns with prior research indicating that firms with prominent consumer brands tend to engage in less tax avoidance (Austin and Wilson (Reference Austin and Wilson2017)) and that companies respond to public pressure by reducing their international tax avoidance activities (Dyreng et al. (Reference Dyreng, Hoopes and Wilde2016)). Additionally, Graham et al. (Reference Graham, Hanlon, Shevlin and Shroff2014) surveyed tax executives and found that approximately 70% believe that firm reputation significantly influences their tax planning decisions. We thus expect firms with heightened reputational concerns to be more likely to be deterred by liberal judge ideology in tax planning.

To empirically test this prediction, we define a variable High Reputational Concern to indicate firms in consumer-brand industries (based on the Fama–French 48 industry classification) and include this variable and its interaction with Liberal Circuit in equation (1). The results are reported in column 3. Consistent with our expectations, the interaction terms are significant and positive, suggesting that the deterrent effect of liberal judge ideology is stronger for firms with higher reputational concerns from tax disputes. The magnitude of the estimated coefficient indicates that firms in consumer-brand industries are more than twice as sensitive to judge ideology in tax planning than firms in other industries.

Taken together, the cross-sectional tests highlight that the influence of judge ideology on tax planning operates through firms’ anticipation of tax litigation costs. Firms become more cautious in their tax strategies when the likelihood and potential costs of disputes are higher, demonstrating that judicial ideology shapes corporate behavior by altering the perceived risks of aggressive tax planning.

V. Judge Ideology, Tax Planning, and Firms’ Financial Outcomes

Building on the finding that firms consider judge ideology in tax planning, we examine whether this influence extends to firms’ financial outcomes. Specifically, we examine its impact on two key financial outcomes widely studied in the finance literature: R&D investment and firm value.

A. Judge Ideology, Tax Planning, and R&D Investment

We focus on R&D investment for two reasons. First, R&D plays a critical role in driving technological progress and economic growth. Recognizing the importance of fostering innovation to maintain competitive advantages and promote sustainable development, governments worldwide implement various tax policies, such as R&D tax credits, deductions, and incentives, to encourage firms to increase their R&D investments.Footnote 21 Second, R&D investment is highly sensitive to taxation. Extensive research shows that tax incentives influence firms’ decisions on where to locate intellectual property (Bartelsman and Beetsma (Reference Bartelsman and Beetsma2003), Dischinger and Riedel (Reference Dischinger and Riedel2011), Karkinsky and Riedel (Reference Karkinsky and Riedel2012), Baumann, Boehm, Knoll, and Riedel (Reference Baumann, Boehm, Knoll and Riedel2020), and Ciaramella (Reference Ciaramella2023)). Relatedly, tax policies, including changes in tax rates and enforcement, have a strong influence on corporate R&D investment. For instance, Rao (Reference Rao2016) estimates that a 10% reduction in the user cost of R&D through tax credits increases a firm’s research intensity, measured as the ratio of R&D spending to sales, by 19.8% in the short run. Similarly, Mukherjee et al. (Reference Mukherjee, Singh and Žaldokas2017) find that increases in state-level corporate income tax rates lead to a decline in R&D investment. Moreover, the risk of IRS scrutiny can discourage R&D activities and reduce the effectiveness of tax incentives in promoting innovation (Williams and Williams (Reference Williams and Williams2021), Goldman et al. (Reference Goldman, Lampenius, Radhakrishnan, Stenzel and de Almeida2024), and Cowx (Reference Cowx2025)).

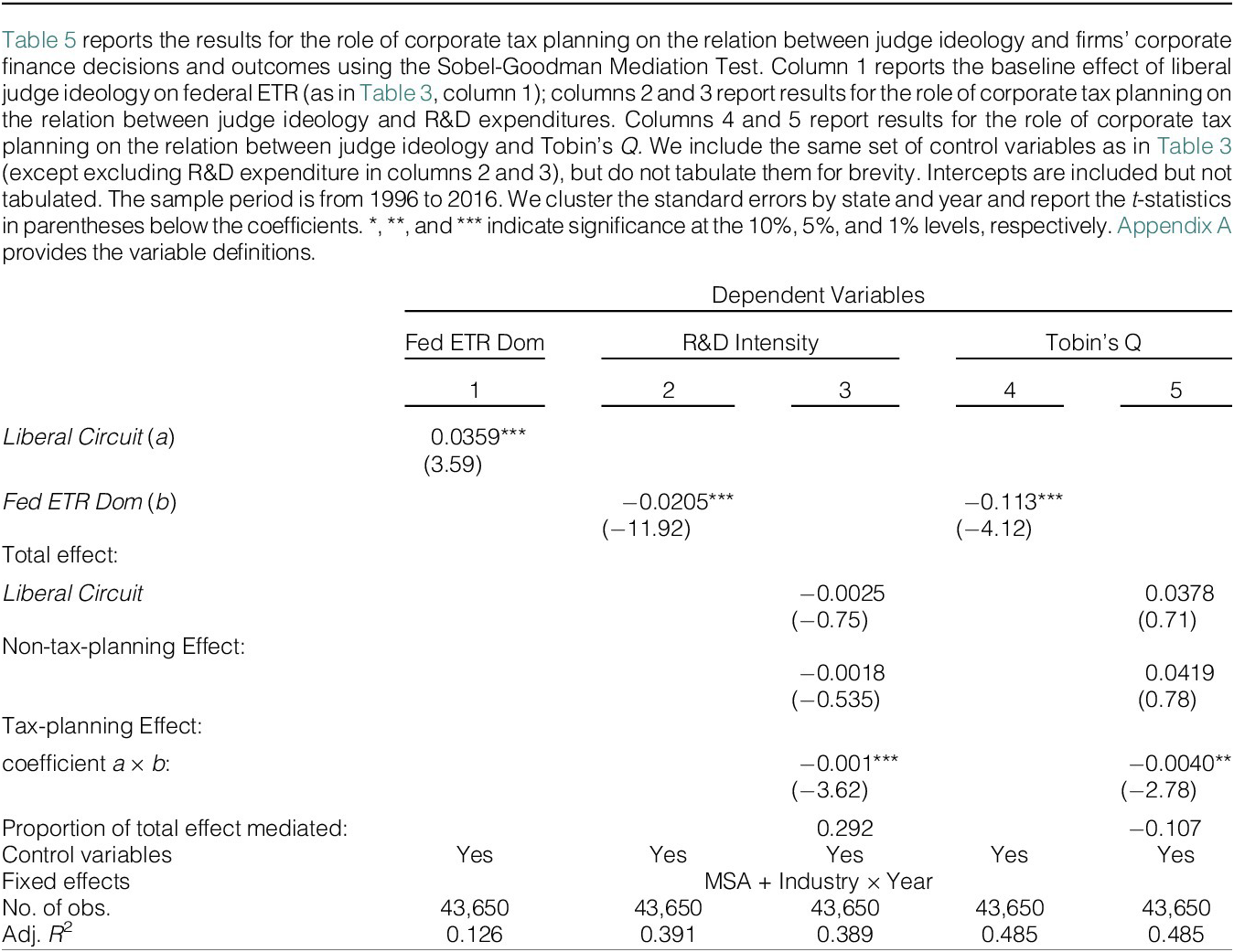

We examine whether liberal judge ideology discourages R&D investment by deterring tax planning, as proxied by Fed ETR, using the Sobel-Goodman mediation test. Following prior research (e.g., Mukherjee et al. (Reference Mukherjee, Singh and Žaldokas2017), Cowx (Reference Cowx2025)), we measure R&D investment through R&D expenditures (R&D Intensity).

The results are presented in Table 5. Column 1 reproduces the relation between liberal judge ideology and Fed ETR (as reported in Table 3, column 1). In column 2, we observe a significant and negative relation between Fed ETR and R&D Intensity, indicating that higher corporate income tax burden impedes R&D investment, consistent with prior research (Mukherjee et al. (Reference Mukherjee, Singh and Žaldokas2017)). Most importantly, the indirect effect of liberal judge ideology on R&D investment through tax planning is negative and significant at the 1% level, suggesting that liberal judge ideology reduces R&D investment by constraining tax planning. Column 3 shows that the direct, non-tax-related effect of liberal judge ideology on R&D investment is not statistically significant. The estimates imply that this indirect pathway, mediated by tax planning deterrence, accounts for approximately 29.2% of the total effect of liberal judge ideology on R&D investment. These results underscore the role of judicial enforcement beyond IRS scrutiny in influencing corporate innovation investment through the tax planning channel (Williams and Williams (Reference Williams and Williams2021), Goldman et al. (Reference Goldman, Lampenius, Radhakrishnan, Stenzel and de Almeida2024), and Cowx (Reference Cowx2025)).

B. Judge Ideology, Tax Planning, and Firm Value

Having demonstrated that liberal judge ideology significantly influences corporate R&D investment by deterring tax planning, we now turn to its implications for firm value. The traditional view suggests that tax planning enhances firm value by generating tax savings and increasing after-tax cash flows (Desai and Dharmapala (Reference Desai and Dharmapala2006), Desai et al. (Reference Desai, Dyck and Zingales2007)). In contrast, the agency perspective emphasizes potential risks, arguing that aggressive tax planning may facilitate managerial rent extraction, which could reduce or even offset the benefits of tax savings (Desai and Dharmapala (Reference Desai and Dharmapala2006), Desai et al. (Reference Desai, Dyck and Zingales2007), and Bennedsen and Zeume (Reference Bennedsen and Zeume2018)). However, Blaylock (Reference Blaylock2016) finds no evidence of managerial rent extraction associated with aggressive tax planning in U.S. firms, indicating that tax planning in this context should primarily enhance firm value through tax savings.

To investigate whether liberal judge ideology reduces firm value through its impact on tax planning, we again analyze both indirect and direct effects using a mediation analysis framework. Following prior research, we measure firm value using Tobin’s Q (Desai and Dharmapala (Reference Desai and Dharmapala2006), Bennedsen and Zeume (Reference Bennedsen and Zeume2018)). In column 4 of Table 5, we observe a significant and negative relation between Fed ETR and Tobin’s Q (at the 1% level), aligning with findings in prior studies that more aggressive tax planning (lower ETR) increases firm value through additional tax savings.

The indirect effect of liberal judge ideology on firm value through tax planning is negative and significant (−0.004, significant at the 5% level), consistent with the notion that liberal judge ideology reduces firm value by constraining tax planning. In column 5, we find that the coefficient of Liberal Circuit is positive but statistically insignificant, suggesting that the total effect of judge ideology on firm value is inconclusive.Footnote 22 Nevertheless, the estimated coefficients indicate that this indirect effect, mediated through tax planning, accounts for 10.7% of the overall effect of liberal judge ideology on firm value.Footnote 23

In summary, our results suggest that liberal judge ideology, by restricting corporate tax planning, negatively impacts both firms’ R&D investments and overall firm value. These results emphasize the broader economic significance of judicial ideology in shaping corporate decision-making, innovation, and financial performance.

VI. Additional Analyses

A. Judge Ideology and Federal GAAP ETR: Robustness Tests

We conduct a battery of robustness tests to ensure that our main results are not sensitive to alternative samples, fixed effects, and model specifications, and are not driven by endogeneity or spurious correlations. The results are reported in Table IA.5 in the Supplementary Material. In column 1, we include financial firms in the sample, and the results remain consistent. Column 2 replaces the high-dimensional Industry × Year fixed effects with separate Industry and Year fixed effects, while column 3 replaces MSA fixed effects with firm fixed effects to control for unobserved firm-specific characteristics that may influence tax planning. Across these variations, our main results remain robust.

To address concerns about cross-correlation in residuals, we apply Newey-West (Reference Newey and West1987) standard errors with a 3-year lag in column 4 to correct for potential serial correlation and heteroscedasticity. The results remain similar. In column 5, we use the Fama and MacBeth (Reference Fama and MacBeth1973) approach, which relies on cross-sectional variations. While the mean of the yearly coefficients (0.0297, t = 4.46) is slightly lower than the OLS estimate (0.0359 in column 1 of Table 3), it remains statistically significant at the 1% level.

To further address endogeneity concerns, we adopt an instrumental variable approach. We use the number of judges eligible for retirement in the next 5 years within the Circuit Court where the firm is headquartered (Eligible-to-Retire) as an instrument. Under Section 371(c) of Title 28 of the U.S. Code, federal judges may retire or take senior status once they meet the “Rule of 80,” when the sum of their age plus years of service equals at least 80. Column 6 presents a positive and significant (at the 1% level) coefficient on Eligible-to-Retire in the first-stage regression, confirming the relevance of the instrument. In the second-stage regression (column 7), using the predicted Liberal Circuit, the coefficient remains significant and positive, demonstrating that our primary findings are not driven by endogeneity.

Finally, we conduct a placebo test to rule out the possibility of spurious correlations. We randomly reassign the value of Liberal Circuit within each circuit across the sample years and re-estimate equation (1) to obtain a counterfactual coefficient on Liberal Circuit. Repeating this procedure 3000 times, we plot the distribution of these counterfactual estimates in Figure IA.6 in the Supplementary Material. Only one of the counterfactual estimates exceeds the magnitude of our baseline result, yielding a Fisher p-value of 0.0003. This indicates that our findings are unlikely to be driven by randomness.

In summary, our robustness tests confirm that the effect of judge ideology on federal tax planning is consistent across alternative empirical specifications and is not driven by endogeneity or spurious correlations.Footnote 24

B. Judge Ideology and Federal GAAP ETR: Additional Variations

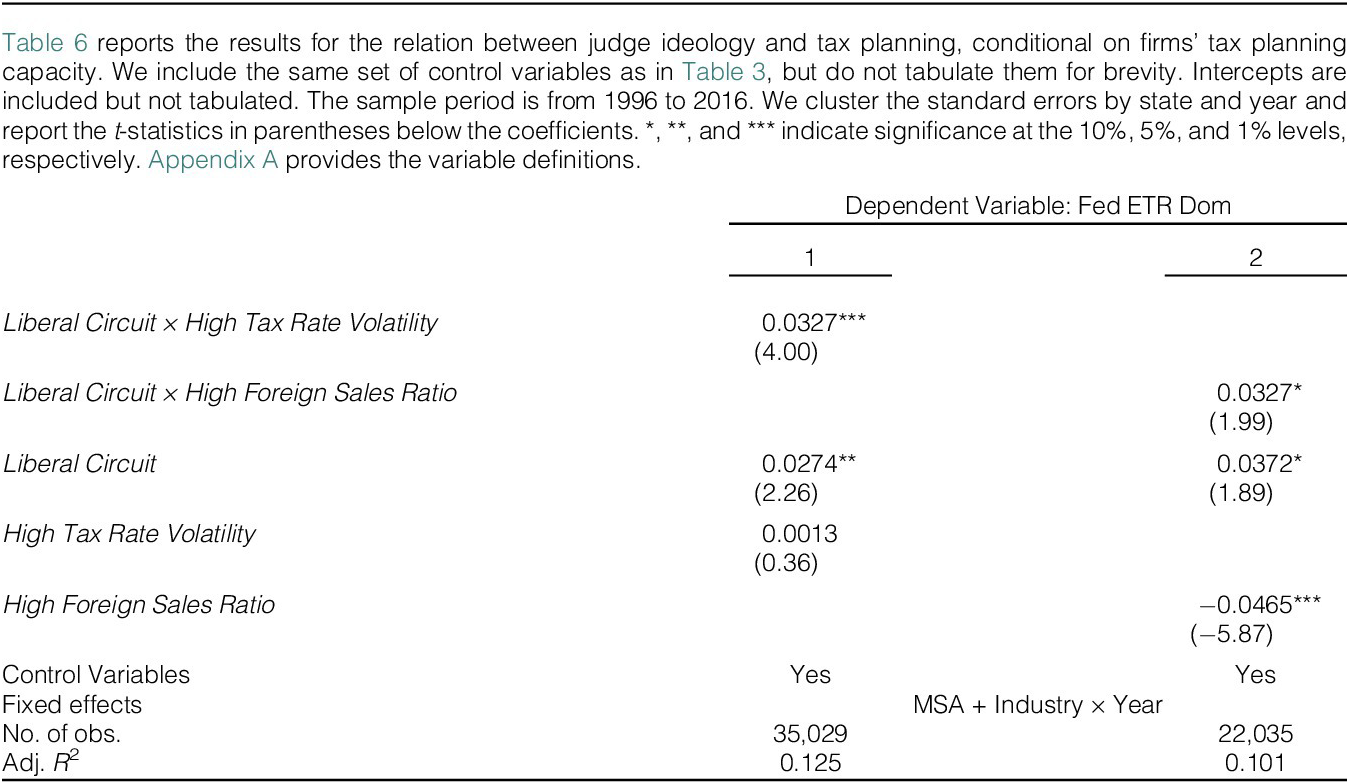

Our final set of tests examines whether the sensitivity of corporate tax policies to judge ideology depends on firms’ existing tax planning capacity and judge characteristics. By definition, firms with higher tax planning capacity are those with greater potential to lower their ETR, offering more flexibility to adjust and optimize tax strategies. Such firms often have complex organizational structures and legal arrangements, such as subsidiaries or special-purpose entities, that can be restructured as needed. Additionally, these firms typically possess substantial financial resources, enabling them to invest in new tax planning strategies or to make modifications without significant constraints. This enhanced tax planning capacity translates into greater agility, allowing these firms to swiftly adjust their tax strategies in response to increased regulatory scrutiny. Thus, we expect the influence of judge ideology to be more pronounced for firms with higher tax planning capacity.

We use two measures of tax planning capacity. The first is an indicator variable, High Tax Volatility, for firms with above-median volatility in ETR, as these firms are likely to have greater potential to enhance their tax outcomes through strategic adjustments (Guenther, Matsunaga, and Williams (Reference Guenther, Matsunaga and Williams2017)). The second measure is an indicator of an above-median ratio of foreign sales to total sales (High Foreign Sales Ratio), as firms generating a larger share of sales from foreign jurisdictions are more likely to have cross-border tax planning opportunities (Dyreng, Lindsey, Markle, and Shackelford (Reference Dyreng, Lindsey, Markle and Shackelford2015), Dyreng et al. (Reference Dyreng, Hoopes and Wilde2016)).Footnote 25

To test our prediction, we re-estimate equation (1), incorporating the high tax planning capacity indicators and their interactions with Liberal Circuit, our variable of interest. The results, presented in Table 6, show that the interaction terms are significant and positive. These findings are consistent with our expectation that the deterrent effect of liberal judge ideology is more pronounced for firms with high (vs. low) tax planning capacity. In terms of economic significance, the estimated coefficients indicate that the deterrent effect on firms with high tax planning capacity is about twice as strong as that on firms with low tax planning capacity.

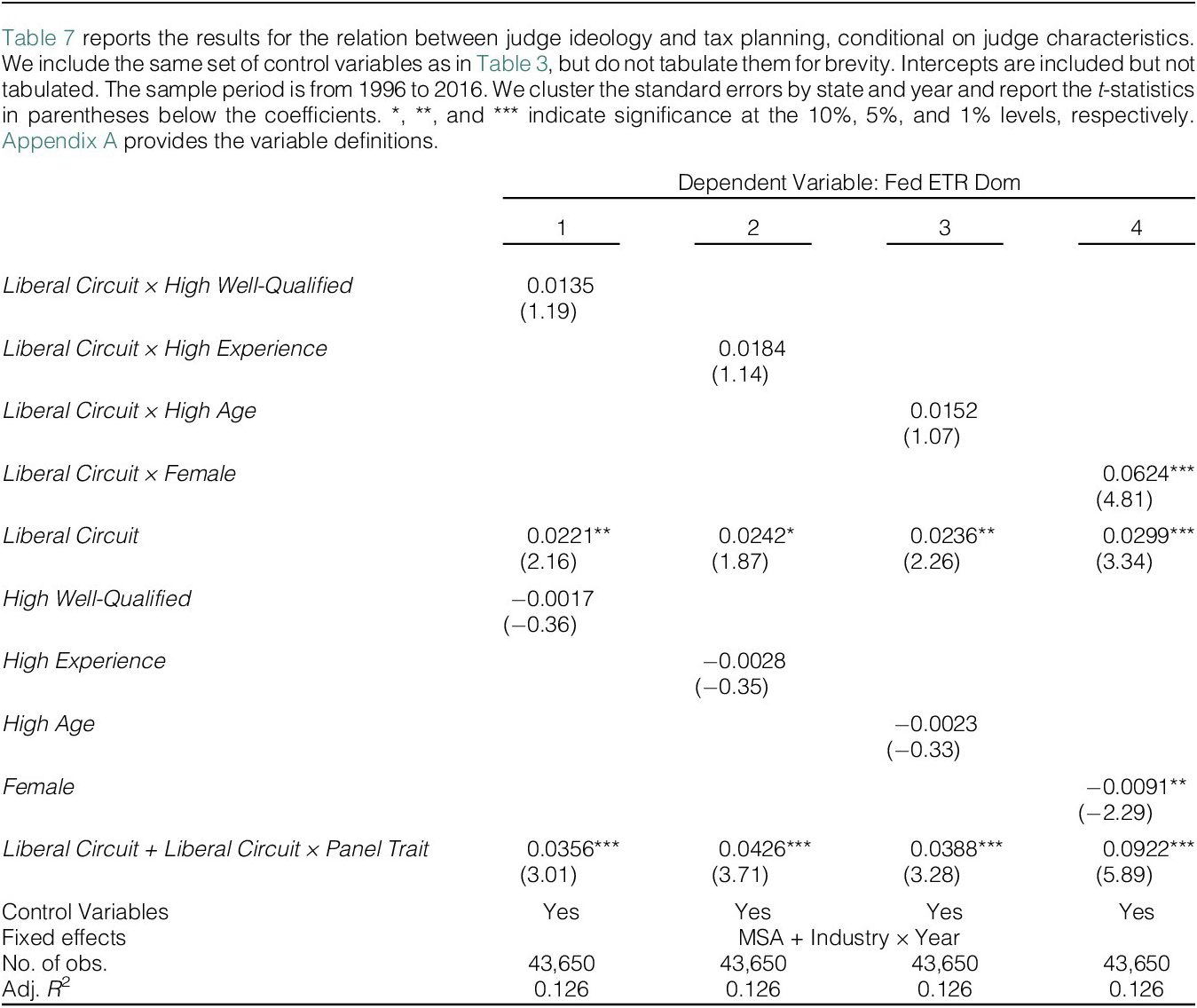

To further explore whether judge characteristics moderate the effect of judge ideology on corporate tax planning, we examine the roles of judge qualification, experience, age, and gender. We define four circuit-year-level indicator variables: High Well-Qualified, High Experience, High Age, and Female. The first three variables equal 1 if the circuit-year’s proportion of well-qualified judges, average judge experience, and average judge age exceed their respective sample medians (i.e., 0.61, 16 years, and 66.8 years, respectively). Female equals 1 if at least one female judge serves in the circuit during the year, and 0 otherwise. In our sample, about 12% of circuit-year observations have at least one female judge.

We re-estimate equation (1), incorporating these indicators and their interactions with Liberal Circuit. The results, presented in Table 7, indicate that the interaction terms for High Well-Qualified, High Experience, and High Age (columns 1–3) are statistically insignificant. These findings align with the theoretical ambiguity regarding how judicial expertise and experience influence the relation between judge ideology and corporate tax planning (Howard (Reference Howard2005)). On the one hand, more experienced judges may have greater discretion in their rulings, potentially amplifying the effect of their ideology. On the other hand, experienced judges may possess deeper knowledge of tax regulations, which could lead them to rely less on discretion, thereby mitigating the influence of ideology.

Interestingly, as shown in column 4, we find that the interaction between Female and Liberal Circuit is significant and positive, suggesting that female liberal judges have a stronger deterrent effect on corporate tax planning than male liberal judges. Prior research indicates that female decision-makers often adopt more conservative or risk-averse approaches to financial decision-making, as highlighted by scholars such as Powell and Ansic (Reference Powell and Ansic1997) and evidence of female CFOs’ levels of tax aggressiveness (Francis et al. (Reference Francis, Hasan, Wu and Yan2014)). Our findings thus extend this literature by demonstrating that conservative stances by female judges may complement liberal ideology in deterring aggressive tax strategies.Footnote 26

VII. Conclusion

Ideological preferences play a powerful role in shaping U.S. tax policy, yet little is known about how judge ideology impacts corporate tax planning. Using the political party of the appointing president as a proxy for judicial ideology, we find that more liberal judges are associated with less aggressive corporate tax planning, as measured by firms’ federal ETR. This effect is economically significant and robust across multiple specifications. Further analysis demonstrates that the deterrent effect of liberal judge ideology is stronger in scenarios where tax litigation imposes higher costs on firms, such as when they employ judicially sensitive tax strategies, face heightened IRS enforcement, or are exposed to reputational risks. Additionally, we find that liberal judge ideology influences firms’ R&D investments and valuation, underscoring the broader economic consequences of judicial decisions beyond tax compliance.

This study is the first to empirically examine the relation between the judicial branch and corporate tax planning, a critical corporate decision shaped by competing liberal and conservative views on tax enforcement. By focusing on the judiciary, we provide a novel perspective that complements research on the roles of the legislative and executive branches in shaping corporate taxation. Our findings also highlight the judiciary’s often-overlooked role as an active participant in the regulatory environment, particularly in areas where legal interpretation and discretion significantly influence corporate behavior.

Ultimately, this study underscores the importance of judicial ideology as a key factor influencing corporate tax policies and strategic decisions, including innovation and investment decisions. As debates over judicial appointments and tax enforcement continue, our findings provide timely insights into the broader economic implications of judicial decision-making. By connecting perspectives from finance, economics, law, and political science, this study deepens understanding of how political ideology shapes corporate behavior and the regulatory landscape in both meaningful and lasting ways.

Appendix A. Variable Definitions

- Liberal Circuit

-

The probability of a three-judge panel randomly selected from a Circuit Court having at least two judges appointed by Democratic presidents; that is,

$ \left[C\left(x,3\right)+C\left(x,2\right)\times C\left(y-x,1\right)\right]/C\left(y,3\right) $

, where y is the total number of judges in the Circuit Court and x is the number of judges in the Circuit Court appointed by Democratic presidents.

$ C\left(a,b\right) $

is the number of combinations of selecting b objects from a distinct objects. For each firm-year observation, we use the Liberal Circuit measure of the firm’s headquarters at the beginning of the fiscal year. Historical headquarters data are extracted from firms’ 10-K and 10-Q filings. We obtain data on Circuit Court judges’ appointing presidents from the FJC website.

$ \left[C\left(x,3\right)+C\left(x,2\right)\times C\left(y-x,1\right)\right]/C\left(y,3\right) $

, where y is the total number of judges in the Circuit Court and x is the number of judges in the Circuit Court appointed by Democratic presidents.

$ C\left(a,b\right) $

is the number of combinations of selecting b objects from a distinct objects. For each firm-year observation, we use the Liberal Circuit measure of the firm’s headquarters at the beginning of the fiscal year. Historical headquarters data are extracted from firms’ 10-K and 10-Q filings. We obtain data on Circuit Court judges’ appointing presidents from the FJC website. - Liberal Tax Court

-

The percentage of judges in the Tax Court that were first appointed by Democratic presidents. For each firm-year observation, we use the Liberal Tax Court at the beginning of the fiscal year. We obtain the Tax Court judges’ appointing presidents from the website of the U.S. Tax Court.

- Liberal District

-

The percentage of judges in a District Court appointed by Democratic presidents. For each firm-year observation, we use the Liberal District measure of the firm’s headquarters at the beginning of the fiscal year. Historical headquarters information is extracted from firms’ 10-K and 10-Q filings. We obtain District Court judges’ appointing presidents from the FJC website.

- Fed ETR Dom

-

The federal total tax expense divided by the PIDOM in year t, with the nonmissing federal total tax expense (TXFED + TXDFED) or the PIDOM, winsorized at 0 and 1. For observations missing both the PIDOM and foreign pretax income (PIFO), we replace the missing PIDOM with the pretax income (PI). Observations with a negative denominator are set as missing.

- Fed ETR WW

-

The federal total tax expense divided by the worldwide PI in year t, with the nonmissing federal total tax expense (TXFED + TXDFED) or PI, winsorized at 0 and 1. Observations with a negative denominator are set as missing.

- #Tax Haven

-

The natural logarithm of 1 plus the total number of material subsidiaries located in a tax haven jurisdiction (Dyreng et al. (Reference Dyreng, Hoopes and Wilde2016)).

- Outbound Shifters

-

An indicator variable that equals 1 if the firm-year is classified as outbound income shifting, and 0 otherwise (Collins et al. (Reference Collins, Kemsley and Lang1998), Klassen and Laplante (Reference Klassen and Laplante2012)). Firms are classified as outbound income shifters if they meet both of the following criteria: i) they have an incentive to move income from the U.S. to foreign jurisdictions, that is, their average foreign tax rate is lower than the U.S. statutory rate; and ii) the firm-year residual from an income shifting regression (Klassen and Laplante (Reference Klassen and Laplante2012)) is positive, indicating that their actual foreign return on sales exceeds the predicted foreign return on sales.

- DPAD Intensity

-

The estimated Qualifying Production Activity Income (QPAI) for the industry-asset class-year multiplied by the DPAD deduction rate, which equals 3% in 2005–2006, 6% in 2007–2009, and 9% from 2010 onward (Ohrn (Reference Ohrn2018)).

The SOI Corporate Source Book provides corporate tax return data on taxable income and the DPAD, both of which are aggregated by the 12 asset classes and by the NAICS industry from 2005 to 2013. Following Ohrn (Reference Ohrn2018), for each asset class-industry-year, we first calculate the Qualified Production Activities Income (QPAI) by grossing up the total DPAD using the phase-in DPAD rate (i.e., 3% in 2005–2006, 6% in 2007–2009, and 9% from 2010 onward). We then calculate the QPAI percentage (QPAI Percent), which is obtained by dividing the QPAI by the income before the DPAD (i.e., the sum of the QPAI and taxable income). Finally, we multiply QPAI Percent with the phase-in DPAD rate to define DPAD Intensity, which varies across approximately 8640 (= 80 × 12 × 9) industry-size-year bins during the 2005–2013 sample period.

- R&D Credit

-

An indicator variable that equals 1 if the firm mentions an R&D tax credit in its annual financial statements in year t, and 0 otherwise (Hoopes (Reference Hoopes2018)).

- High IRS Audit Prob

-

An indicator variable that equals 1 for firm-years with above-median IRS audit probability, and 0 otherwise. The IRS audit probability is the number of face-to-face corporate audits the IRS completes in fiscal year t for size (asset) group k that the IRS assigns the firm to, divided by the number of corporate tax returns (Form 1120) filed in calendar year t – 1 for firm size group k (Hoopes et al. (Reference Hoopes, Mescall and Pittman2012)). IRS Audit Prob Rank ranges from 1 to 4.

- High IRS Attention

-

An indicator variable that equals 1 for firm-years with above-median IRS attention, and 0 otherwise. IRS attention is defined as the number of times during year t that a computer with an IRS IP address downloaded any SEC filings from EDGAR for the firm (Bozanic et al. (Reference Bozanic, Hoopes, Thornock and Williams2017), Fox and Wilson (Reference Fox and Wilson2023)). The data on IRS attention are obtained from Professor Zackery Fox’s website, covering fiscal years 2003–2016.

- High Reputational Concern

-

An indicator variable that equals 1 if the firm belongs to one of the following industry categories based on the Fama–French 48 Industry Classification: Food Products (2); Candy and Soda (3); Recreation (6); Consumer Goods (9); Apparel (10); Automobiles and Trucks (23); Personal Services (33); Retail (42); and Restaurants, Hotels, Motels (43).

- Tobin’s Q

-

The ratio of i) the sum of the book value of assets plus the difference between the market value and the book value of equity (calculated as AT + PRCC_F × CSHO – CEQ), to ii) the book value of assets (AT).

- High Tax Rate Volatility

-

An indicator variable that equals 1 if the firm’s volatility of Fed ETR Dom exceeds the sample median in a given year, and 0 otherwise. The firm’s federal ETR volatility (Tax Rate Volatility) is measured by the standard deviation of its federal ETR over the previous 5 years (from t – 5 to t – 1).

- High Foreign Sales Ratio

-

An indicator variable that equals 1 if the firm’s Foreign Sales Ratio exceeds the sample median for that year, and 0 otherwise. The firm’s Foreign Sales Ratio is measured by foreign sales to total sales. This analysis is restricted to multinational firms, that is, those with nonzero foreign sales.

- High Well-Qualified

-

An indicator variable that equals 1 if the ratio of well-qualified judges to total judges in the circuit-year exceeds the median, and 0 otherwise.

- High Experience

-

An indicator variable that equals 1 if the average years of experience of judges in the circuit-year exceed the median, and 0 otherwise.

- High Age

-

An indicator variable that equals 1 if the average age of judges in the circuit–year exceeds the median, and 0 otherwise.

- Female

-

An indicator variable that equals 1 if there is at least one female judge in the circuit-year, and 0 otherwise.

Control Variables

- Size

-

Natural logarithm of total assets (AT).

- MTB

-

Market-to-book ratio, calculated as PRCC_F × CSHO/CEQ.

- Leverage

-

Long-term debt (DLTT) scaled by the lagged AT; set to 0 if missing.

- Inventory

-

Inventory (INVT) scaled by the lagged AT; set to 0 if missing.

- R&D Intensity

-

R&D expenditures (XRD) scaled by the lagged AT; set to 0 if missing.

- Capital Intensity

-

Property, plant, and equipment (PPENT) scaled by the lagged AT; set to 0 if missing.

- Intangibility

-

Intangible assets (INTAN) scaled by the lagged AT; set to 0 if missing.

- ROA

-

Operating income before depreciation and amortization (OIBDP) scaled by the lagged AT.

- Foreign Income

-

PIFO scaled by the lagged AT.

- Foreign

-

An indicator variable that equals 1 if the PIFO is positive, and 0 otherwise.

- Advertising

-

Advertising expenditures (XAD) scaled by the lagged AT; set to 0 if missing.

- Sales Growth

-

Annual growth in sales (SALE) between years t – 1 and t.

- SG&A

-

Selling, general, and administrative expenses (XSGA) scaled by the lagged AT.

- NOL

-

An indicator variable that equals 1 if the firm has a net operating loss carry-forward (TLCF), and 0 otherwise.

- ∆NOL

-

The difference in the TLCF between years t and t–1, scaled by the lagged AT; set to 0 if missing.

- Minority Interest

-

Income (loss) attributable to MII scaled by the lagged AT.

- Equity Income

-

Equity income in earnings (ESUB) scaled by the lagged AT.

- IRS Audit Prob Rank

-

The quartile rank of the firm’s IRS audit probability in year t. The IRS audit probability is the number of face-to-face corporate audits the IRS completes in fiscal year t for size (asset) group k that the IRS assigns the firm to, divided by the number of corporate tax returns (Form 1120) filed in calendar year t – 1 for firm size group k (Hoopes et al. (Reference Hoopes, Mescall and Pittman2012)). IRS Audit Prob Rank ranges from 1 to 4.

- IRS Attention Rank

-

The quartile rank of the firm’s IRS attention in year t. IRS attention is defined as the number of times during year t that a computer with an IRS IP address downloaded any SEC filings from EDGAR for the firm (Bozanic et al. (Reference Bozanic, Hoopes, Thornock and Williams2017), Fox and Wilson (Reference Fox and Wilson2023)). For observations with missing IRS download data, we set the number of downloads to zero. The data on IRS attention are obtained from Professor Zackery Fox’s website, covering fiscal years 2003–2016.

- IRS Attention Missing

-

An indicator for missing IRS download data in year t.

- GSP Growth

-

Gross state product growth rate from year t – 1 to year t.

- Unemployment

-

State unemployment rate in year t.

- Blue State

-

An indicator variable that equals 1 if a state is identified as a “blue” state, and 0 otherwise. We define a blue state as one where the Democratic share of total votes exceeded the Republican share of total votes in the most recent presidential election.

Supplementary Material

To view supplementary material for this article, please visit http://doi.org/10.1017/S0022109026102622.

Funding Statement

The authors acknowledge the financial support provided by the Hong Kong University of Science and Technology, University of Hong Kong, Singapore Management University, and University of California at Irvine. Huang gratefully acknowledges the financial support received from the National Natural Science Foundation of China (Grant/Award Number 72172079).

Open access

Open access