I. Introduction

Researchers have found that debt is essential for funding innovations across diverse contexts, including publicly traded companies (Mann (Reference Mann2018)) and startups (Robb and Robinson (Reference Robb and Robinson2014), Davis, Morse, and Wang (Reference Davis, Morse and Wang2020)). Furthermore, empirical studies have shown that debt fosters innovation and that improved debt financing accelerates innovation and cultivates innovation novelty for firms (Benfratello, Schiantarelli, and Sembenelli (Reference Benfratello, Schiantarelli and Sembenelli2008), Amore, Schneider, and Žaldokas (Reference Amore, Schneider and Žaldokas2013), and Chava, Oettl, Subramanian, and Subramanian (Reference Chava, Oettl, Subramanian and Subramanian2013)), whereas credit market disruptions hinder innovation (Hombert and Matray (Reference Hombert and Matray2017), Granja and Moreira (Reference Granja and Moreira2023)).

This body of empirical evidence presents a puzzle in light of the conventional view that debt may not be desirable for financing innovation. Early work argues that debt contracts might not be well-suited for financing innovation due to the uncertainty surrounding research and development (R&D) outcomes, which can lead to credit rationing and premature liquidation (Stiglitz (Reference Stiglitz1985), Atanassov, Nanda, and Seru (Reference Atanassov, Nanda and Seru2007)). For practitioners engaged in innovation and its financing, however, it is crucial to distinguish between uncertainty (or ambiguity) and risk. The significant asymmetry of innovation payoffs further poses challenges to aligning fixed-obligation debt with innovation incentives (Manso (Reference Manso2011)). In addition, the intangible nature of R&D constrains collateral value and reduces the debt capacity of innovative firms (Hall and Lerner (Reference Hall, Lerner, Hall and Rosenberg2010)). Lastly, why debt can foster innovation remains an open question.

To address this question, we integrate the distinctive features of innovation returns into a framework for financing a growth option, originally developed by Sundaresan and Wang (Reference Sundaresan and Wang2007) and Sundaresan, Wang, and Yang (Reference Sundaresan, Wang and Yang2015). We distinguish risk—characterized by a single known probability distribution—from ambiguity, which is characterized by model uncertainty represented by a set of plausible distributions. In our setting, an entrepreneur makes joint decisions regarding when to initiate an innovation project and how to finance it. Once launched, the project generates cash flows characterized by both jumps and ambiguity—key features of innovation returns that distinguish them from conventional investments, as highlighted by Kerr, Nanda, and Rhodes-Kropf (Reference Kerr, Nanda and Rhodes-Kropf2014) and Kerr and Nanda (Reference Kerr and Nanda2015). While jumps are intrinsic to the cash flow dynamics under the objective measure, ambiguity reflects the entrepreneur’s subjective beliefs (Seo (Reference Seo2009), Baillon, Huang, Selim, and Wakker (Reference Baillon, Huang, Selim and Wakker2018)). The entrepreneur can finance the project either entirely with equity (all-equity financing) or with an optimal mix of equity and debt (optimal financing), the latter leveraging the tax benefits of debt while accounting for bankruptcy costs. Both the entrepreneur and external financiers are ambiguity-averse, making decisions under worst-case scenarios.

Our model highlights the central role of debt in fostering innovation through an investment acceleration mechanism. This mechanism emerges from the dynamic interaction between optimal investment timing, capital structure, and cash flow uncertainty. Under complete information, our model jointly and endogenously determines financing and investment decisions in a first-best equilibrium, without relying on exogenous financing constraints.

To ensure analytical tractability, we model innovation cash flows using the double-exponential jump diffusion process introduced by Kou (Reference Kou2002). This process not only captures the leptokurtic features commonly observed in asset and innovation returns but also allows for a closed-form characterization of the first-passage time distribution. Since both the investment and default options are path-dependent and their values hinge critically on first-passage probabilities, this tractability offers a distinct advantage over alternative jump-size specifications.

We extend the original recursive multiple priors utility (RMPU) framework developed by Chen and Epstein (Reference Chen and Epstein2002) to incorporate both diffusion and jump ambiguity. In the RMPU framework, agents possess a set of equivalent priors (probability measures) characterized by Itô diffusions and maximize utility under the worst-case prior. The state process under an alternative prior differs only in its drift, thereby altering the first moment only. However, this framework falls short when analyzing innovation as a driving force behind investment and financing choices, because diffusion increments are symmetric and normally distributed.

In this pursuit, we build on the mathematical framework of Quenez and Sulem (Reference Quenez and Sulem2013), (Reference Quenez and Sulem2014) to model agents’ multiple priors on innovation-driven cash flows as a set of equivalent Lévy processes. Under both drift and jump ambiguity, the density generator for an alternative prior consists of two components: one for Brownian risk and another for the Poisson random measure. Under jump ambiguity, the state process deviates from the reference measure not just in the mean but across the entire distribution. Solving the optimal stopping problem under such conditions is analytically challenging, particularly in determining the worst-case measure. To address this, we apply the theories of backward stochastic differential equations (BSDEs) with jumps (Quenez and Sulem (Reference Quenez and Sulem2013), (Reference Quenez and Sulem2014)) to derive the worst-case measure and closed-form solutions for optimal investment and financing decisions.

We use detection-error probabilities to calibrate ambiguity and compute relative entropy growth to quantify the contributions of diffusion ambiguity and jump ambiguity, building on Anderson, Hansen, and Sargent (Reference Anderson, Hansen and Sargent2003), Maenhout (Reference Maenhout2006), and Aït-Sahalia and Matthys (Reference Aït-Sahalia and Matthys2019). Under ambiguity, the worst-case measure is considered reasonable when it is statistically difficult to distinguish from the reference measure. Relative entropy growth measures the statistical distance between two priors. In the model, the total relative entropy growth is comprised of two additive components driven by diffusion and jump ambiguity. In the context of innovation, it is important to examine the influence of the two types of ambiguity. For instance, in high-tech sectors where innovations often exhibit radical characteristics, the role of jump ambiguity is naturally magnified, whereas traditional sectors are expected to show the opposite feature.

We show that the investment acceleration benefit of debt for project value arises from the interaction between two effects: the reduction in the investment threshold and the passage time effect—the time it takes for cash flows to reach a target level from below. Under optimal financing, firms invest at a lower cash flow level rather than waiting to reach the higher threshold required under all-equity financing, as the net tax benefit of debt offsets the difference.Footnote 1 This lower threshold leads to earlier investment in expectation, thereby increasing the project’s expected net present value. Moreover, we demonstrate that the passage time effect amplifies this value gain in a power-law fashion.

Innovation projects, which typically involve greater ambiguity, benefit more from the investment acceleration effect of debt. Although ambiguity raises the investment thresholds, delays investment, and lowers project values under both financing scenarios, optimal financing mitigates these adverse effects.Footnote 2 On one hand, ambiguity reduces optimal leverage and hence the net tax benefit of debt, narrowing the threshold gap between optimal and all-equity financing. Nevertheless, this gap shrinks at a diminishing rate. On the other hand, ambiguity strengthens the passage time effect by further delaying investment under all-equity financing. The combination of a slowly declining threshold gap and an increasingly dominant power effect explains why the investment acceleration benefit of debt is amplified under greater ambiguity.

Moreover, our analysis reveals that the fostering effect of debt is particularly pronounced when innovative firms have limited historical data for gauging ambiguity. This result helps explain why young startups, which typically lack extensive track records, often favor debt financing. This observation is consistent with empirical evidence from Robb and Robinson (Reference Robb and Robinson2014), Davis et al. (Reference Davis, Morse and Wang2020), and Chava et al. (Reference Chava, Oettl, Subramanian and Subramanian2013). Additionally, we find that the fostering effect of debt is especially significant for radical innovations when jump ambiguity is the primary concern. This finding aligns with Benfratello et al. (Reference Benfratello, Schiantarelli and Sembenelli2008), who show that high-tech firms benefit greatly from increased credit availability, given their focus on radical innovations capable of generating substantial jumps in returns.

Our theoretical results on the elevated investment threshold and reduced project scale under ambiguity contribute to the broader literature on investment under uncertainty, pioneered by Bloom (Reference Bloom2009).Footnote 3 Recent studies, including Gulen and Ion (Reference Gulen and Ion2016) and Campello, Cortes, d’Almeida, and Kankanhalli (Reference Campello, Cortes, d’Almeida and Kankanhalli2022), document that heightened economic policy uncertainty suppresses corporate investment. As recent research (e.g., Aït-Sahalia, Matthys, Osambela, and Sircar (Reference Aït-Sahalia, Matthys, Osambela and Sircar2025)) uses the economic policy uncertainty index as a proxy for ambiguity, these findings align well with the prediction of our model that ambiguity delays investment. In addition, our result that greater ambiguity leads to smaller optimal project scales echoes the findings of Campello, Kankanhalli, and Kim (Reference Campello, Kankanhalli and Kim2024), who show that firms respond to elevated uncertainty by delaying both investment and disinvestment, particularly when sunk costs are high. Taken together, these empirical patterns reinforce our theoretical insight that ambiguity discourages large-scale commitments in uncertain environments.

Existing real option models focus on diffusion ambiguity only, for example, see Nishimura and Ozaki (Reference Nishimura and Ozaki2007) and Miao and Wang (Reference Miao and Wang2011). These models do not consider jump ambiguity, nor do they investigate financing choices, as we do in our paper. Dicks and Fulghieri (Reference Dicks and Fulghieri2021) develop a theory of innovation waves and investor sentiment tied to ambiguity. Coiculescu, Izhakian, and Ravid (Reference Coiculescu, Izhakian and Ravid2024) treat innovation as real options and find that ambiguity negatively impacts R&D, while risk has a positive effect. A recent and closely related study by Geelen, Hajda, and Morellec (Reference Geelen, Hajda and Morellec2022) develops a Schumpeterian growth model with endogenous R&D and financing choices, demonstrating that debt fosters innovation and growth at the aggregate level, similar to our findings. They attribute this effect to the tax benefit of debt. Different from this study, our model emphasizes the interaction between debt financing and jump ambiguity, a defining feature of innovation returns.

II. The Model

Our baseline model combines the irreversible investment framework of McDonald and Siegel (Reference McDonald and Siegel1986) with the EBIT-based capital structure model of Goldstein, Ju, and Leland (Reference Goldstein, Ju and Leland2001). Sundaresan and Wang (Reference Sundaresan and Wang2007) and Sundaresan et al. (Reference Sundaresan, Wang and Yang2015) formally analyze the joint implications of these models and extend them further. We adopt their assumptions but introduce jump risk into the baseline model. Our main contribution is to examine the effects of ambiguity about both the drift and the jump intensity and size distribution.

A. The Baseline Model without Ambiguity

1. The Project

An entrepreneur has access to an innovation project that, once initiated, generates an earnings before interest and taxes (EBIT) flow

$ X(t):= X\left(t,\omega \right) $

defined on a probability space (

$ X(t):= X\left(t,\omega \right) $

defined on a probability space (

$ \Omega, \mathcal{F},{Q}^0) $

endowed with a standard complete filtration

$ \Omega, \mathcal{F},{Q}^0) $

endowed with a standard complete filtration

$ \mathbf{F}=\{{\mathcal{F}}_t|t\ge 0\} $

satisfying the “usual conditions.” We assume that the EBIT process is exogenous and independent of the entrepreneur’s investment decision. We specify

$ \mathbf{F}=\{{\mathcal{F}}_t|t\ge 0\} $

satisfying the “usual conditions.” We assume that the EBIT process is exogenous and independent of the entrepreneur’s investment decision. We specify

$ {Q}^0 $

to be the risk-neutral probability measure, in line with the traditional EBIT-based capital structure model of Goldstein et al. (Reference Goldstein, Ju and Leland2001).Footnote 4 Under

$ {Q}^0 $

to be the risk-neutral probability measure, in line with the traditional EBIT-based capital structure model of Goldstein et al. (Reference Goldstein, Ju and Leland2001).Footnote 4 Under

$ {Q}^0 $

,

$ {Q}^0 $

,

$ X(t) $

follows a geometric Lévy process:

$ X(t) $

follows a geometric Lévy process:

$$ \frac{dX(t)}{X\left({t}^{-}\right)}=\mu dt+\sigma dW(t)+{\int}_{\mathrm{\mathbb{R}}}\iota \left(t,u\right)\tilde{N}\left( dt, du\right), $$

$$ \frac{dX(t)}{X\left({t}^{-}\right)}=\mu dt+\sigma dW(t)+{\int}_{\mathrm{\mathbb{R}}}\iota \left(t,u\right)\tilde{N}\left( dt, du\right), $$

where

$ W(t) $

is a standard Brownian motion,

$ W(t) $

is a standard Brownian motion,

$ \tilde{N}\left( dt, du\right) $

is a compensated Poisson random measure given by

$ \tilde{N}\left( dt, du\right) $

is a compensated Poisson random measure given by

$$ \tilde{N}\left( dt, du\right)=N\left( dt, du\right)-\nu (du) dt, $$

$$ \tilde{N}\left( dt, du\right)=N\left( dt, du\right)-\nu (du) dt, $$

with

$ \nu (du):= \unicode{x1D53C}\left[N\left(1, du\right)\right] $

being the Lévy measure, and

$ \nu (du):= \unicode{x1D53C}\left[N\left(1, du\right)\right] $

being the Lévy measure, and

$ \iota \left(t,u\right) $

being a square-integrable predictable process with respect to

$ \iota \left(t,u\right) $

being a square-integrable predictable process with respect to

$ \nu (du) $

. It is worth noting that the specification of a compensated Poisson random measure under the risk-neutral reference measure follows the same rational expectation equilibrium pricing rule as in Goldstein et al. (Reference Goldstein, Ju and Leland2001).Footnote 5 Additionally, we assume that

$ \nu (du) $

. It is worth noting that the specification of a compensated Poisson random measure under the risk-neutral reference measure follows the same rational expectation equilibrium pricing rule as in Goldstein et al. (Reference Goldstein, Ju and Leland2001).Footnote 5 Additionally, we assume that

$ X(0)=x>0 $

,

$ X(0)=x>0 $

,

$ \mu $

,

$ \mu $

,

$ \sigma $

, and

$ \sigma $

, and

$ r $

are constants with

$ r $

are constants with

$ \mu <r $

and

$ \mu <r $

and

$ r $

being the risk-free rate.

$ r $

being the risk-free rate.

We specify the jump component as a compound Poisson process with intensity

$ \lambda <+\infty $

and assume a double exponential distribution for the jump size (i.e.,

$ \lambda <+\infty $

and assume a double exponential distribution for the jump size (i.e.,

$ X(t) $

follows a double exponential jump-diffusion process, first introduced by Kou (Reference Kou2002)). Specifically, we can write the jump component explicitly as

$ X(t) $

follows a double exponential jump-diffusion process, first introduced by Kou (Reference Kou2002)). Specifically, we can write the jump component explicitly as

$$ \iota \left(t,u\right)={e}^u-1,\hskip1em \mathrm{and}\hskip1em \nu (du)=\lambda f(du), $$

$$ \iota \left(t,u\right)={e}^u-1,\hskip1em \mathrm{and}\hskip1em \nu (du)=\lambda f(du), $$

where the jump size density

$ f $

is given by

$ f $

is given by

$$ {f}_u=p{\eta}_1{e}^{-{\eta}_1u}{\mathbf{1}}_{u\ge 0}+q{\eta}_2{e}^{\eta_2u}{\mathbf{1}}_{u<0},\hskip1em {\eta}_1>1,{\eta}_2>0,p,q\ge 0,p+q=1 $$

$$ {f}_u=p{\eta}_1{e}^{-{\eta}_1u}{\mathbf{1}}_{u\ge 0}+q{\eta}_2{e}^{\eta_2u}{\mathbf{1}}_{u<0},\hskip1em {\eta}_1>1,{\eta}_2>0,p,q\ge 0,p+q=1 $$

in which

$ \mathbf{1} $

is an indicator function. In the specification,

$ \mathbf{1} $

is an indicator function. In the specification,

$ p $

and

$ p $

and

$ q $

are the conditional probabilities of upward and downward jumps, respectively, and

$ q $

are the conditional probabilities of upward and downward jumps, respectively, and

$ 1/{\eta}_1 $

and

$ 1/{\eta}_1 $

and

$ -1/{\eta}_2 $

are the conditional mean log jump sizes of positive and negative jumps, respectively. This model specification has two merits. First, as shown by Kou and Wang (Reference Kou and Wang2004), it allows for analytical solutions to valuation problems with American-style perpetual options.Footnote 6 This property is crucial to our analyses of joint investment and financing decisions in the real options model. Second, the specification has the appealing feature of modeling positive and negative jumps separately, which generates a rich set of priors, as will be shown later.

$ -1/{\eta}_2 $

are the conditional mean log jump sizes of positive and negative jumps, respectively. This model specification has two merits. First, as shown by Kou and Wang (Reference Kou and Wang2004), it allows for analytical solutions to valuation problems with American-style perpetual options.Footnote 6 This property is crucial to our analyses of joint investment and financing decisions in the real options model. Second, the specification has the appealing feature of modeling positive and negative jumps separately, which generates a rich set of priors, as will be shown later.

2. Financing

We assume that the project requires external funding, as available cash is insufficient. Taxation on project cash flows at rate

$ \phi \in \left(0,1\right) $

motivates firms to issue debt for tax shielding. The entrepreneur chooses between all equity financing and optimal financing, aiming to determine the optimal equity-debt mix.Footnote 7 Drawing on the established literature (e.g., Leland (Reference Leland1998), Goldstein et al. (Reference Goldstein, Ju and Leland2001)), we analyze debt contracts with perpetual coupon payments

$ \phi \in \left(0,1\right) $

motivates firms to issue debt for tax shielding. The entrepreneur chooses between all equity financing and optimal financing, aiming to determine the optimal equity-debt mix.Footnote 7 Drawing on the established literature (e.g., Leland (Reference Leland1998), Goldstein et al. (Reference Goldstein, Ju and Leland2001)), we analyze debt contracts with perpetual coupon payments

$ C $

in a time-homogeneous context. Debt issuance reduces tax by

$ C $

in a time-homogeneous context. Debt issuance reduces tax by

$ \phi C $

but also exposes the firm to potential bankruptcy costs.

$ \phi C $

but also exposes the firm to potential bankruptcy costs.

We begin with the all-equity financing case. The equity value at the

$ {\mathrm{\mathcal{F}}}_0 $

-measurable random investment time

$ {\mathrm{\mathcal{F}}}_0 $

-measurable random investment time

$ {\tau}_I\ge 0 $

is

$ {\tau}_I\ge 0 $

is

$$ {V}_e\left({\tau}_I\right)={\unicode{x1D53C}}_{\tau_I}\left[{\int}_{\tau_I}^{\infty }{e}^{-r\left(t-{\tau}_I\right)}\left(1-\phi \right)X(t) dt-I\right], $$

$$ {V}_e\left({\tau}_I\right)={\unicode{x1D53C}}_{\tau_I}\left[{\int}_{\tau_I}^{\infty }{e}^{-r\left(t-{\tau}_I\right)}\left(1-\phi \right)X(t) dt-I\right], $$

where the constant

$ I>0 $

denotes the investment cost. At time 0, the entrepreneur chooses the optimal stopping time

$ I>0 $

denotes the investment cost. At time 0, the entrepreneur chooses the optimal stopping time

$ {\tau}_I^e $

to initiate the project; hence, her value function at time 0 is

$ {\tau}_I^e $

to initiate the project; hence, her value function at time 0 is

$$ {V}_e(0)=\underset{\tau_I}{\sup}\;{\unicode{x1D53C}}_0\left[{e}^{-r{\tau}_I}{V}_e\left({\tau}_I\right)\right]={\unicode{x1D53C}}_0\left[{e}^{-r{\tau}_I^e}{V}_e\left({\tau}_I^e\right)\right]. $$

$$ {V}_e(0)=\underset{\tau_I}{\sup}\;{\unicode{x1D53C}}_0\left[{e}^{-r{\tau}_I}{V}_e\left({\tau}_I\right)\right]={\unicode{x1D53C}}_0\left[{e}^{-r{\tau}_I^e}{V}_e\left({\tau}_I^e\right)\right]. $$

In the case of optimal financing, the entrepreneur can issue debt at the time of investment,

$ {\tau}_I $

, to take advantage of the tax benefits associated with debt. Default occurs later, at the stopping time

$ {\tau}_I $

, to take advantage of the tax benefits associated with debt. Default occurs later, at the stopping time

$ {\tau}_D $

under the assumption of optimal default, a standard assumption in the literature (Sundaresan and Wang (Reference Sundaresan and Wang2007), Strebulaev and Whited (Reference Strebulaev and Whited2012), and Sundaresan et al. (Reference Sundaresan, Wang and Yang2015)). As per the traditional trade-off theory of capital structure (e.g., Leland (Reference Leland1994), Goldstein et al. (Reference Goldstein, Ju and Leland2001)), default triggers liquidation under the absolute priority rule, with a fraction

$ {\tau}_D $

under the assumption of optimal default, a standard assumption in the literature (Sundaresan and Wang (Reference Sundaresan and Wang2007), Strebulaev and Whited (Reference Strebulaev and Whited2012), and Sundaresan et al. (Reference Sundaresan, Wang and Yang2015)). As per the traditional trade-off theory of capital structure (e.g., Leland (Reference Leland1994), Goldstein et al. (Reference Goldstein, Ju and Leland2001)), default triggers liquidation under the absolute priority rule, with a fraction

$ \alpha \in \left(0,1\right) $

of the asset value lost in the liquidation process. This assumption is standard in models that balance the benefits of debt (via tax shields) with the costs of potential default and liquidation. Figure 1 illustrates the timelines for both financing choices.

$ \alpha \in \left(0,1\right) $

of the asset value lost in the liquidation process. This assumption is standard in models that balance the benefits of debt (via tax shields) with the costs of potential default and liquidation. Figure 1 illustrates the timelines for both financing choices.

The timeline in Figure 1 illustrates the investment option and potential default under debt financing.

Given the above, the firm value at the investment time

$ {\tau}_I $

is

$ {\tau}_I $

is

$$ {V}_{\ast}\left({\tau}_I\right)=E\left({\tau}_I\right)+D\left({\tau}_I\right)-I, $$

$$ {V}_{\ast}\left({\tau}_I\right)=E\left({\tau}_I\right)+D\left({\tau}_I\right)-I, $$

where

$ D\left({\tau}_I\right) $

is the entrepreneur’s valuation of debt, and

$ D\left({\tau}_I\right) $

is the entrepreneur’s valuation of debt, and

$ E\left({\tau}_I\right) $

is the value of (leveraged) equity, given by

$ E\left({\tau}_I\right) $

is the value of (leveraged) equity, given by

$$ {\displaystyle \begin{array}{c}E\left({\tau}_I\right)=\underset{\tau_D\ge {\tau}_I}{\sup}\;{\unicode{x1D53C}}_{\tau_I}\left[{\int}_{\tau_I}^{\tau_D}{e}^{-r\left(t-{\tau}_I\right)}\left(1-\phi \right)\left(X(t)-C\right) dt\right]\\ {}={\unicode{x1D53C}}_{\tau_I}\left[{\int}_{\tau_I}^{\tau_D^{\ast }}{e}^{-r\left(t-{\tau}_I\right)}\left(1-\phi \right)\left(X(t)-C\right) dt\right].\end{array}} $$

$$ {\displaystyle \begin{array}{c}E\left({\tau}_I\right)=\underset{\tau_D\ge {\tau}_I}{\sup}\;{\unicode{x1D53C}}_{\tau_I}\left[{\int}_{\tau_I}^{\tau_D}{e}^{-r\left(t-{\tau}_I\right)}\left(1-\phi \right)\left(X(t)-C\right) dt\right]\\ {}={\unicode{x1D53C}}_{\tau_I}\left[{\int}_{\tau_I}^{\tau_D^{\ast }}{e}^{-r\left(t-{\tau}_I\right)}\left(1-\phi \right)\left(X(t)-C\right) dt\right].\end{array}} $$

The above indicates that the equity value is the discounted net profit received by equity holders until default. At default, equity holders recover nothing. As is standard in the trade-off theory of capital structure, we assume that the entrepreneur maximizes equity value by choosing the default policy

$ {\tau}_D $

. However, when choosing the optimal debt policy

$ {\tau}_D $

. However, when choosing the optimal debt policy

$ {C}^{\ast } $

, she maximizes firm value

$ {C}^{\ast } $

, she maximizes firm value

$ {V}_{\ast}\left({\tau}_I\right) $

, incorporating her expectation of debt value

$ {V}_{\ast}\left({\tau}_I\right) $

, incorporating her expectation of debt value

$ D\left({\tau}_I\right) $

.Footnote 8 In a symmetric rational expectation equilibrium, the entrepreneur’s valuation of debt,

$ D\left({\tau}_I\right) $

.Footnote 8 In a symmetric rational expectation equilibrium, the entrepreneur’s valuation of debt,

$ D\left({\tau}_I\right) $

, equals debt investors’ valuation and is given by

$ D\left({\tau}_I\right) $

, equals debt investors’ valuation and is given by

$$ D\left({\tau}_I\right)={\unicode{x1D53C}}_{\tau_I}\left[{\int}_{\tau_I}^{\tau_D^{\ast }}{e}^{-r\left(t-{\tau}_I\right)} Cdt+\left(1-\alpha \right){\int}_{\tau_D^{\ast}}^{\infty }{e}^{-r\left(t-{\tau}_I\right)}\left(1-\phi \right)X(t) dt\right]. $$

$$ D\left({\tau}_I\right)={\unicode{x1D53C}}_{\tau_I}\left[{\int}_{\tau_I}^{\tau_D^{\ast }}{e}^{-r\left(t-{\tau}_I\right)} Cdt+\left(1-\alpha \right){\int}_{\tau_D^{\ast}}^{\infty }{e}^{-r\left(t-{\tau}_I\right)}\left(1-\phi \right)X(t) dt\right]. $$

The first term inside the conditional expectation operator is the present value of the coupon collected while the firm remains solvent. The second term is the present value of the asset value recovered upon liquidation in bankruptcy.

Since

$ {\tau}_D^{\ast } $

and

$ {\tau}_D^{\ast } $

and

$ {C}^{\ast } $

depend on

$ {C}^{\ast } $

depend on

$ {\tau}_I^{\ast } $

, these three decision variables are jointly determined at time 0 by maximizing the discounted firm value at investment.

$ {\tau}_I^{\ast } $

, these three decision variables are jointly determined at time 0 by maximizing the discounted firm value at investment.

$$ {V}_{\ast }(0)=\underset{\tau_I,{\tau}_D>{\tau}_I,C}{\sup}\;{\unicode{x1D53C}}_0\left[{e}^{-r{\tau}_I}{V}_{\ast}\left({\tau}_I\right)\right]=\underset{\tau_I,{\tau}_D>{\tau}_I,C}{\sup}\;{\unicode{x1D53C}}_0\left[{e}^{-r{\tau}_I}{\unicode{x1D53C}}_{\tau_I}\left[{V}_{\ast}\left({\tau}_I\right)\right]\right], $$

$$ {V}_{\ast }(0)=\underset{\tau_I,{\tau}_D>{\tau}_I,C}{\sup}\;{\unicode{x1D53C}}_0\left[{e}^{-r{\tau}_I}{V}_{\ast}\left({\tau}_I\right)\right]=\underset{\tau_I,{\tau}_D>{\tau}_I,C}{\sup}\;{\unicode{x1D53C}}_0\left[{e}^{-r{\tau}_I}{\unicode{x1D53C}}_{\tau_I}\left[{V}_{\ast}\left({\tau}_I\right)\right]\right], $$

where the second equality follows from the property of conditional expectations, and the optimization is subject to the default policy determined in (4).

B. The Set of Priors

Agents face ambiguity about the EBIT reference model in equation (1) and consider “close” alternative models. With ambiguity aversion, they opt for worst-case EBIT dynamics. To capture jump ambiguity, we extend the utility framework of Chen and Epstein (Reference Chen and Epstein2002) to allow for uncertainty in both jump intensity and size distribution. Our extension builds on the general results of Quenez and Sulem (Reference Quenez and Sulem2013), (Reference Quenez and Sulem2014), who provide the comparison theorem for BSDEs under Lévy processes and general results for related optimal stopping problems under ambiguity.

Let

$ \Theta $

denote the set of density generators. Each density generator

$ \Theta $

denote the set of density generators. Each density generator

$ \theta \in \Theta $

is binary (i.e.,

$ \theta \in \Theta $

is binary (i.e.,

$ \theta =\left({\theta}_W,{\theta}_N\right) $

, where

$ \theta =\left({\theta}_W,{\theta}_N\right) $

, where

$ {\theta}_W $

is for the Brownian motion and

$ {\theta}_W $

is for the Brownian motion and

$ {\theta}_N $

for the jump component). For each

$ {\theta}_N $

for the jump component). For each

$ \theta \in \Theta $

, let

$ \theta \in \Theta $

, let

$ {Z}^{\theta }(t) $

be the solution to the (forward) SDE:

$ {Z}^{\theta }(t) $

be the solution to the (forward) SDE:

$$ {dZ}^{\theta }(t)={Z}^{\theta}\left({t}^{-}\right)\left(-{\theta}_W(t) dW(t)-{\int}_{\mathrm{\mathbb{R}}}{\theta}_N\Big(t,u\Big)d\tilde{N}( dt, du\Big)\right), $$

$$ {dZ}^{\theta }(t)={Z}^{\theta}\left({t}^{-}\right)\left(-{\theta}_W(t) dW(t)-{\int}_{\mathrm{\mathbb{R}}}{\theta}_N\Big(t,u\Big)d\tilde{N}( dt, du\Big)\right), $$

for

$ t\in \left[0,T\right] $

with

$ t\in \left[0,T\right] $

with

$ {Z}^{\theta }(0)=1 $

. For

$ {Z}^{\theta }(0)=1 $

. For

$ {\theta}_W(t) $

, we adopt the

$ {\theta}_W(t) $

, we adopt the

$ \kappa $

-ignorance specification of Chen and Epstein (Reference Chen and Epstein2002) (i.e.,

$ \kappa $

-ignorance specification of Chen and Epstein (Reference Chen and Epstein2002) (i.e.,

$ {\theta}_W(t)\in \left[-\kappa, \kappa \right],0<\kappa <\infty $

). Based on the technical requirements in Quenez and Sulem (Reference Quenez and Sulem2013), (Reference Quenez and Sulem2014), we specify

$ {\theta}_W(t)\in \left[-\kappa, \kappa \right],0<\kappa <\infty $

). Based on the technical requirements in Quenez and Sulem (Reference Quenez and Sulem2013), (Reference Quenez and Sulem2014), we specify

$ {\theta}_N\left(t,u\right) $

as:

$ {\theta}_N\left(t,u\right) $

as:

$$ {\displaystyle \begin{array}{ll}& {\theta}_N\left(t,u\right)=1-{e}^{\theta_{N,1}(t)u}{\mathbf{1}}_{u\ge 0}-{e}^{\theta_{N,2}(t)u}{\mathbf{1}}_{u<0},\\ {}& {\theta}_{N,1}(t)\in \left[-{M}_1,0\right],\hskip1em {\theta}_{N,2}(t)\in \left[0,{M}_2\right],\hskip1em \mathrm{and}\hskip1em {M}_1,{M}_2>0.\end{array}} $$

$$ {\displaystyle \begin{array}{ll}& {\theta}_N\left(t,u\right)=1-{e}^{\theta_{N,1}(t)u}{\mathbf{1}}_{u\ge 0}-{e}^{\theta_{N,2}(t)u}{\mathbf{1}}_{u<0},\\ {}& {\theta}_{N,1}(t)\in \left[-{M}_1,0\right],\hskip1em {\theta}_{N,2}(t)\in \left[0,{M}_2\right],\hskip1em \mathrm{and}\hskip1em {M}_1,{M}_2>0.\end{array}} $$

This specification for

$ {\theta}_N\left(t,u\right) $

follows from the jump-size distribution in equation (2), and we discuss its implications after constructing the set of priors.

$ {\theta}_N\left(t,u\right) $

follows from the jump-size distribution in equation (2), and we discuss its implications after constructing the set of priors.

To construct the set of priors, we define a probability measure

$ {Q}^{\theta } $

on

$ {Q}^{\theta } $

on

$ {\mathrm{\mathcal{F}}}_T $

, equivalent to

$ {\mathrm{\mathcal{F}}}_T $

, equivalent to

$ {Q}^0 $

for

$ {Q}^0 $

for

$ \theta \in \Theta $

as

$ \theta \in \Theta $

as

$$ {\unicode{x1D53C}}^{\theta}\left[{\mathbf{1}}_A\right]=\unicode{x1D53C}\left[{\mathbf{1}}_A{Z}_T^{\theta}\right],\hskip1em A\in {\mathrm{\mathcal{F}}}_T. $$

$$ {\unicode{x1D53C}}^{\theta}\left[{\mathbf{1}}_A\right]=\unicode{x1D53C}\left[{\mathbf{1}}_A{Z}_T^{\theta}\right],\hskip1em A\in {\mathrm{\mathcal{F}}}_T. $$

Hence, under

$ {Q}^{\theta } $

,

$ {Q}^{\theta } $

,

$$ {dW}^{\theta }(t)= dW(t)+{\theta}_W(t) dt, $$

$$ {dW}^{\theta }(t)= dW(t)+{\theta}_W(t) dt, $$

which represents the Brownian risk, and

$$ {\tilde{N}}^{\theta}\left( dt, du\right)=\tilde{N}\left( dt, du\right)+{\theta}_N\left(t,u\right)\nu (du) dt=N\left( dt, du\right)-\left(1-{\theta}_N\left(t,u\right)\right)\nu (du) dt, $$

$$ {\tilde{N}}^{\theta}\left( dt, du\right)=\tilde{N}\left( dt, du\right)+{\theta}_N\left(t,u\right)\nu (du) dt=N\left( dt, du\right)-\left(1-{\theta}_N\left(t,u\right)\right)\nu (du) dt, $$

which is a compensated Poisson random measure by Girsanov’s theorem; see Øksendal and Sulem ((Reference Øksendal and Sulem2019), Chapter 1.4). Taken together, under

$ {Q}^{\theta } $

,

$ {Q}^{\theta } $

,

$ X(t) $

is given by

$ X(t) $

is given by

$$ \frac{dX(t)}{X\left({t}^{-}\right)}={\displaystyle \begin{array}{l}\left(\mu -{\theta}_W(t)\sigma -{\int}_{\mathrm{\mathbb{R}}}\left({e}^u-1\right){\theta}_N\left(t,u\right)\nu (du)\right) dt+\sigma {dW}^{\theta }(t)\\ {}+\hskip2px {\int}_{\mathrm{\mathbb{R}}}\left({e}^u-1\right){\tilde{N}}^{\theta}\left( dt, du\right).\end{array}} $$

$$ \frac{dX(t)}{X\left({t}^{-}\right)}={\displaystyle \begin{array}{l}\left(\mu -{\theta}_W(t)\sigma -{\int}_{\mathrm{\mathbb{R}}}\left({e}^u-1\right){\theta}_N\left(t,u\right)\nu (du)\right) dt+\sigma {dW}^{\theta }(t)\\ {}+\hskip2px {\int}_{\mathrm{\mathbb{R}}}\left({e}^u-1\right){\tilde{N}}^{\theta}\left( dt, du\right).\end{array}} $$

Our method of distorting the reference measure can attenuate the impact of positive or negative jumps, depending on the monotonicity of the entrepreneur’s value function in the state variable. If the value function increases with the state variable, as in the baseline model without ambiguity, the worst-case measure leads to the smallest unconditional probability and mean size for positive jumps, and the largest values for negative jumps—all constrained within the set of priors. To see this, equation (5) shows that

$ {N}^{\theta}\left( dt, du\right) $

has a Lévy measure

$ {N}^{\theta}\left( dt, du\right) $

has a Lévy measure

$ {\nu}^{\theta }(du)=\left(1-{\theta}_N\left(t,u\right)\right)\nu (du) $

under

$ {\nu}^{\theta }(du)=\left(1-{\theta}_N\left(t,u\right)\right)\nu (du) $

under

$ {Q}^{\theta } $

. We can express

$ {Q}^{\theta } $

. We can express

$ {\nu}^{\theta }(du) $

as

$ {\nu}^{\theta }(du) $

as

$$ {\nu}^{\theta }(du)={\lambda}_t^{\theta }{f}_t^{\theta }(du), $$

$$ {\nu}^{\theta }(du)={\lambda}_t^{\theta }{f}_t^{\theta }(du), $$

where

$ {\lambda}_t^{\theta } $

is the distorted jump intensity given by

$ {\lambda}_t^{\theta } $

is the distorted jump intensity given by

$$ {\lambda}_t^{\theta }=\lambda {\int}_{\mathrm{\mathbb{R}}}\left(1-{\theta}_N\left(t,u\right)\right){f}_u du=\lambda \left(\frac{p{\eta}_1}{\eta_1-{\theta}_{N,1}(t)}+\frac{q{\eta}_2}{\eta_2+{\theta}_{N,2}(t)}\right), $$

$$ {\lambda}_t^{\theta }=\lambda {\int}_{\mathrm{\mathbb{R}}}\left(1-{\theta}_N\left(t,u\right)\right){f}_u du=\lambda \left(\frac{p{\eta}_1}{\eta_1-{\theta}_{N,1}(t)}+\frac{q{\eta}_2}{\eta_2+{\theta}_{N,2}(t)}\right), $$

and the distorted jump size density is given by

$$ {\displaystyle \begin{array}{c}{f}_{u,t}^{\theta }=\frac{\left(1-{\theta}_N\left(t,u\right)\right){f}_u}{\int_{\mathrm{\mathbb{R}}}\left(1-{\theta}_N\left(t,u\right)\right){f}_u du}\\ {}={p}_t^{\theta}\left({\eta}_1-{\theta}_{N,1}(t)\right){e}^{-\left({\eta}_1-{\theta}_{N,1}(t)\right)u}{\mathbf{1}}_{u\ge 0}+{q}_t^{\theta}\left({\eta}_2+{\theta}_{N,2}(t)\right){e}^{\left({\eta}_2+{\theta}_{N,2}(t)\right)u}{\mathbf{1}}_{u<0},\end{array}} $$

$$ {\displaystyle \begin{array}{c}{f}_{u,t}^{\theta }=\frac{\left(1-{\theta}_N\left(t,u\right)\right){f}_u}{\int_{\mathrm{\mathbb{R}}}\left(1-{\theta}_N\left(t,u\right)\right){f}_u du}\\ {}={p}_t^{\theta}\left({\eta}_1-{\theta}_{N,1}(t)\right){e}^{-\left({\eta}_1-{\theta}_{N,1}(t)\right)u}{\mathbf{1}}_{u\ge 0}+{q}_t^{\theta}\left({\eta}_2+{\theta}_{N,2}(t)\right){e}^{\left({\eta}_2+{\theta}_{N,2}(t)\right)u}{\mathbf{1}}_{u<0},\end{array}} $$

with

$ {p}_t^{\theta } $

and

$ {p}_t^{\theta } $

and

$ {q}_t^{\theta } $

being the distorted probabilities of upward and downward jumps given by

$ {q}_t^{\theta } $

being the distorted probabilities of upward and downward jumps given by

$$ {\displaystyle \begin{array}{l}{p}_t^{\theta }=\frac{p{\eta}_1\left({\eta}_2+{\theta}_{N,2}(t)\right)}{p{\eta}_1\left({\eta}_2+{\theta}_{N,2}(t)\right)+q{\eta}_2\left({\eta}_1-{\theta}_{N,1}(t)\right)},\ \mathrm{and}\\ {}{q}_t^{\theta }=\frac{q{\eta}_2\left({\eta}_1-{\theta}_{N,1}(t)\right)}{p{\eta}_1\left({\eta}_2+{\theta}_{N,2}(t)\right)+q{\eta}_2\left({\eta}_1-{\theta}_{N,1}(t)\right)}.\end{array}} $$

$$ {\displaystyle \begin{array}{l}{p}_t^{\theta }=\frac{p{\eta}_1\left({\eta}_2+{\theta}_{N,2}(t)\right)}{p{\eta}_1\left({\eta}_2+{\theta}_{N,2}(t)\right)+q{\eta}_2\left({\eta}_1-{\theta}_{N,1}(t)\right)},\ \mathrm{and}\\ {}{q}_t^{\theta }=\frac{q{\eta}_2\left({\eta}_1-{\theta}_{N,1}(t)\right)}{p{\eta}_1\left({\eta}_2+{\theta}_{N,2}(t)\right)+q{\eta}_2\left({\eta}_1-{\theta}_{N,1}(t)\right)}.\end{array}} $$

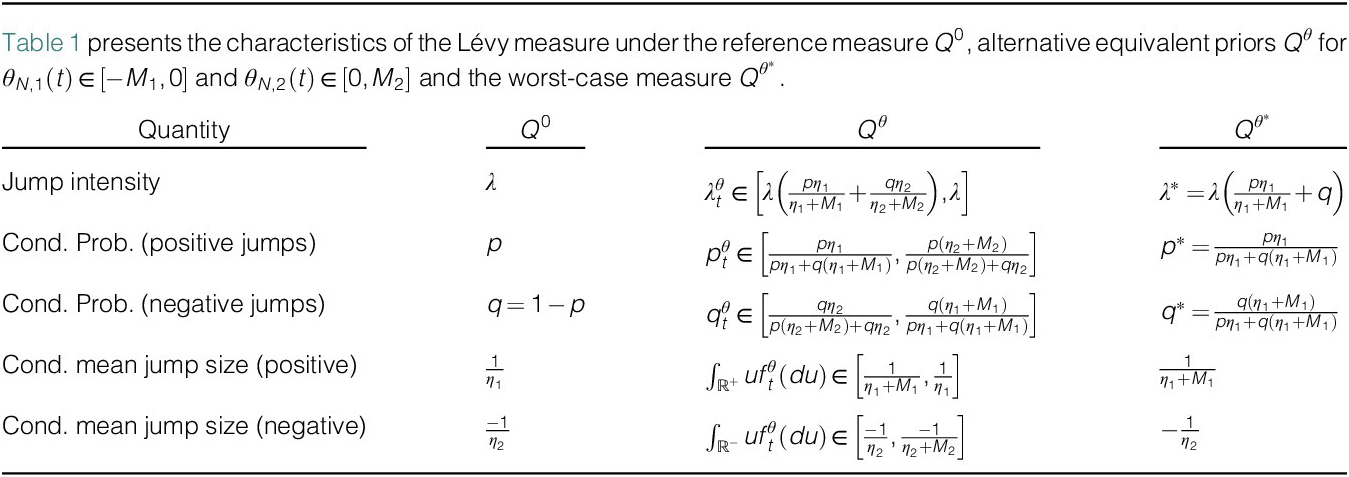

Table 1 summarizes the Lévy measures for

$ {N}^{\theta}\left( dt, du\right) $

under the set of priors specified

$ {N}^{\theta}\left( dt, du\right) $

under the set of priors specified

$ {\theta}_{N,1}(t)\in \left[-{M}_1,0\right] $

and

$ {\theta}_{N,1}(t)\in \left[-{M}_1,0\right] $

and

$ {\theta}_{N,2}(t)\in \left[0,{M}_2\right] $

. In the extreme case where only positive jumps occur (

$ {\theta}_{N,2}(t)\in \left[0,{M}_2\right] $

. In the extreme case where only positive jumps occur (

$ p=1 $

), the jump intensity ranges from

$ p=1 $

), the jump intensity ranges from

$ \left[{\lambda \eta}_1/\left({\eta}_1+{M}_1\right),\lambda \right] $

, with the conditional probability of positive jumps fixed at 1. If the worst-case scenario corresponds to

$ \left[{\lambda \eta}_1/\left({\eta}_1+{M}_1\right),\lambda \right] $

, with the conditional probability of positive jumps fixed at 1. If the worst-case scenario corresponds to

$ {\theta}_{N,1}(t)=-{M}_1 $

(or 0) for all

$ {\theta}_{N,1}(t)=-{M}_1 $

(or 0) for all

$ t\ge 0 $

, the jump intensity is minimized (or maximized). A similar observation holds for the other extreme case (

$ t\ge 0 $

, the jump intensity is minimized (or maximized). A similar observation holds for the other extreme case (

$ q=1 $

).

$ q=1 $

).

C. Innovation with All-Equity Financing under Ambiguity

With the set of priors, the entrepreneur’s value function under all-equity financing at the investment time

$ {\tau}_I $

and under a candidate measure

$ {\tau}_I $

and under a candidate measure

$ {Q}^{\theta } $

is

$ {Q}^{\theta } $

is

$$ {V}_e\left({\tau}_I;\theta \right)={\unicode{x1D53C}}_{\tau_I}^{\theta}\left[{\int}_{\tau_I}^{\infty }{e}^{-r\left(t-{\tau}_I\right)}\left(1-\phi \right)X(t) dt-I\right]. $$

$$ {V}_e\left({\tau}_I;\theta \right)={\unicode{x1D53C}}_{\tau_I}^{\theta}\left[{\int}_{\tau_I}^{\infty }{e}^{-r\left(t-{\tau}_I\right)}\left(1-\phi \right)X(t) dt-I\right]. $$

At time 0, she chooses the optimal investment time

$ {\tau}_I^e $

to start the project. The ambiguity-averse entrepreneur chooses the worst-case measure

$ {\tau}_I^e $

to start the project. The ambiguity-averse entrepreneur chooses the worst-case measure

$ {Q}^{\theta^{\ast }} $

from the set of priors. As long as

$ {Q}^{\theta^{\ast }} $

from the set of priors. As long as

$ {Q}^{\theta^e}\left\{{\tau}_I^{\ast }<+\infty \right\}=1 $

, her value function at time 0 is

$ {Q}^{\theta^e}\left\{{\tau}_I^{\ast }<+\infty \right\}=1 $

, her value function at time 0 is

$$ {V}_e\left(0;{\tau}_I^e,{\theta}^{\ast}\right)=\underset{\tau_I\ge 0}{\sup}\;\underset{Q^{\theta }}{\operatorname{inf}}\;{\unicode{x1D53C}}_0^{\theta}\left[{e}^{-r{\tau}_I}{V}_e\left({\tau}_I;\theta \right)\right]. $$

$$ {V}_e\left(0;{\tau}_I^e,{\theta}^{\ast}\right)=\underset{\tau_I\ge 0}{\sup}\;\underset{Q^{\theta }}{\operatorname{inf}}\;{\unicode{x1D53C}}_0^{\theta}\left[{e}^{-r{\tau}_I}{V}_e\left({\tau}_I;\theta \right)\right]. $$

It is necessary to discuss a few technical details of the optimal stopping problem under ambiguity, given by equations (6) and (7). First, Quenez and Sulem (Reference Quenez and Sulem2014) prove that the nonlinear expectation in (7) admits the minmax relation. Thus, we can first solve the minimum expectation problem to find the worst-case measure

$ {Q}^{\theta^{\ast }} $

and then solve the optimal stopping problem for

$ {Q}^{\theta^{\ast }} $

and then solve the optimal stopping problem for

$ {\tau}_I^{\ast } $

under

$ {\tau}_I^{\ast } $

under

$ {Q}^{\theta^{\ast }} $

. Because the minimum expectation problem involves the application of Girsanov’s theorem and the comparison theorem for BSDEs under Lévy processes and because

$ {Q}^{\theta^{\ast }} $

. Because the minimum expectation problem involves the application of Girsanov’s theorem and the comparison theorem for BSDEs under Lévy processes and because

$ {Q}^{\theta^{\ast }} $

exists for any horizon in our model, we can solve the optimal stopping problem under

$ {Q}^{\theta^{\ast }} $

exists for any horizon in our model, we can solve the optimal stopping problem under

$ {Q}^{\theta^{\ast }} $

for the infinite horizon. Second, Quenez and Sulem (Reference Quenez and Sulem2013) show that the minimum expectation is dynamically consistent:

$ {Q}^{\theta^{\ast }} $

for the infinite horizon. Second, Quenez and Sulem (Reference Quenez and Sulem2013) show that the minimum expectation is dynamically consistent:

$$ \underset{Q^{\theta }}{\operatorname{inf}}\;{\unicode{x1D53C}}_0^{\theta}\left[{e}^{-r{\tau}_I}{V}_e\left({\tau}_I;\theta \right)\right]=\underset{Q^{\theta^{\prime }}}{\operatorname{inf}}\;{\unicode{x1D53C}}_0^{\theta^{\prime }}\left[\underset{Q^{\theta^{{\prime\prime} }}}{\operatorname{inf}}\;{\unicode{x1D53C}}_{\tau_I}^{\theta^{{\prime\prime} }}\left[{e}^{-r{\tau}_I}{V}_e\left({\tau}_I;\left\{{\theta}^{\prime },{\theta}^{{\prime\prime}}\right\}\right)\right]\right]. $$

$$ \underset{Q^{\theta }}{\operatorname{inf}}\;{\unicode{x1D53C}}_0^{\theta}\left[{e}^{-r{\tau}_I}{V}_e\left({\tau}_I;\theta \right)\right]=\underset{Q^{\theta^{\prime }}}{\operatorname{inf}}\;{\unicode{x1D53C}}_0^{\theta^{\prime }}\left[\underset{Q^{\theta^{{\prime\prime} }}}{\operatorname{inf}}\;{\unicode{x1D53C}}_{\tau_I}^{\theta^{{\prime\prime} }}\left[{e}^{-r{\tau}_I}{V}_e\left({\tau}_I;\left\{{\theta}^{\prime },{\theta}^{{\prime\prime}}\right\}\right)\right]\right]. $$

where

$ {\theta}^{\prime } $

and

$ {\theta}^{\prime } $

and

$ {\theta}^{{\prime\prime} } $

deliver density generators for the decision intervals

$ {\theta}^{{\prime\prime} } $

deliver density generators for the decision intervals

$ \left[0,{\tau}_I\right] $

and

$ \left[0,{\tau}_I\right] $

and

$ \left[{\tau}_I,T\right] $

with

$ \left[{\tau}_I,T\right] $

with

$ T\le +\infty $

, respectively. Dynamic consistency provides analytical convenience in that the worst-case density generators for

$ T\le +\infty $

, respectively. Dynamic consistency provides analytical convenience in that the worst-case density generators for

$ \left[0,{\tau}_I\right] $

and

$ \left[0,{\tau}_I\right] $

and

$ \left[{\tau}_I,T\right] $

coincide with that for

$ \left[{\tau}_I,T\right] $

coincide with that for

$ \left[0,T\right] $

. Hence, it suffices to begin with the following to find the worst-case measure:

$ \left[0,T\right] $

. Hence, it suffices to begin with the following to find the worst-case measure:

$$ {V}_e\left(0;{\tau}_I,{\theta}^{\ast}\right)=\underset{Q^{\theta }}{\operatorname{inf}}\;{\unicode{x1D53C}}_0^{\theta}\left[{e}^{-r{\tau}_I}{V}_e\left({\tau}_I;\theta \right)\right],\hskip1em \mathrm{for}\hskip0.42em \mathrm{any}\hskip0.42em {\tau}_{\mathrm{I}}. $$

$$ {V}_e\left(0;{\tau}_I,{\theta}^{\ast}\right)=\underset{Q^{\theta }}{\operatorname{inf}}\;{\unicode{x1D53C}}_0^{\theta}\left[{e}^{-r{\tau}_I}{V}_e\left({\tau}_I;\theta \right)\right],\hskip1em \mathrm{for}\hskip0.42em \mathrm{any}\hskip0.42em {\tau}_{\mathrm{I}}. $$

Proposition 1. The density generator that gives the minimum expectation in (8) is

$ {\theta}^{\ast }=\left({\theta}_W^{\ast },{\theta}_N^{\ast}\right)=\left(\kappa, 1-{e}^{-{M}_1u}{\boldsymbol{1}}_{u\ge 0}-{\boldsymbol{1}}_{u<0}\right) $

for all

$ {\theta}^{\ast }=\left({\theta}_W^{\ast },{\theta}_N^{\ast}\right)=\left(\kappa, 1-{e}^{-{M}_1u}{\boldsymbol{1}}_{u\ge 0}-{\boldsymbol{1}}_{u<0}\right) $

for all

$ t\in \left[0,T\right] $

.

$ t\in \left[0,T\right] $

.

In the Supplementary Material, we provide the proof, which relies on dynamic consistency and the comparison theorem for BSDEs under the Lévy process.

An immediate implication is that under

$ {Q}^{\theta^{\ast }} $

,

$ {Q}^{\theta^{\ast }} $

,

$ X(t) $

follows the process

$ X(t) $

follows the process

$$ \frac{dX(t)}{X\left({t}^{-}\right)}={\mu}^{\theta^{\ast }} dt+\sigma {dW}^{\theta^{\ast }}(t)+{\int}_{\mathrm{\mathbb{R}}}\left({e}^u-1\right){\tilde{N}}^{\theta^{\ast }}\left( dt, du\right) $$

$$ \frac{dX(t)}{X\left({t}^{-}\right)}={\mu}^{\theta^{\ast }} dt+\sigma {dW}^{\theta^{\ast }}(t)+{\int}_{\mathrm{\mathbb{R}}}\left({e}^u-1\right){\tilde{N}}^{\theta^{\ast }}\left( dt, du\right) $$

where

$$ {\displaystyle \begin{array}{c}{\mu}^{\theta^{\ast }}=\mu -\kappa \sigma -{\int}_{\mathrm{\mathbb{R}}}\left({e}^u-1\right)\left(1-{e}^{-{M}_1u}{\mathbf{1}}_{u\ge 0}-{\mathbf{1}}_{u<0}\right)\nu (du)\\ {}=\mu +\underset{\mathrm{drift}\ \mathrm{ambiguity}\ \mathrm{discount}<0}{\underbrace{\left(-\kappa \sigma \right)}}+\underset{\mathrm{jump}\ \mathrm{ambiguity}\ \mathrm{discount}<0}{\underbrace{\left(-\frac{\lambda p}{\left({\eta}_1-1\right)}+\frac{\lambda p{\eta}_1}{\left({\eta}_1+{M}_1-1\right)\left({\eta}_1+{M}_1\right)}\right)}}.\end{array}} $$

$$ {\displaystyle \begin{array}{c}{\mu}^{\theta^{\ast }}=\mu -\kappa \sigma -{\int}_{\mathrm{\mathbb{R}}}\left({e}^u-1\right)\left(1-{e}^{-{M}_1u}{\mathbf{1}}_{u\ge 0}-{\mathbf{1}}_{u<0}\right)\nu (du)\\ {}=\mu +\underset{\mathrm{drift}\ \mathrm{ambiguity}\ \mathrm{discount}<0}{\underbrace{\left(-\kappa \sigma \right)}}+\underset{\mathrm{jump}\ \mathrm{ambiguity}\ \mathrm{discount}<0}{\underbrace{\left(-\frac{\lambda p}{\left({\eta}_1-1\right)}+\frac{\lambda p{\eta}_1}{\left({\eta}_1+{M}_1-1\right)\left({\eta}_1+{M}_1\right)}\right)}}.\end{array}} $$

The distorted process above indicates that drift ambiguity and jump ambiguity reduce the perceived mean return by

$ \kappa \sigma $

and

$ \kappa \sigma $

and

$ \lambda p/\left({\eta}_1-1\right)-\lambda p{\eta}_1/\left({\eta}_1+{M}_1-1\right)\left({\eta}_1+{M}_1\right) $

, respectively.

$ \lambda p/\left({\eta}_1-1\right)-\lambda p{\eta}_1/\left({\eta}_1+{M}_1-1\right)\left({\eta}_1+{M}_1\right) $

, respectively.

Before turning to the detailed discussion of

$ X(t) $

under

$ X(t) $

under

$ {Q}^{\theta^{\ast }} $

, it is important to note that jump ambiguity distortions remain independent of drift ambiguity. This property arises from the independence of the Brownian and jump terms in line with the Itô-Lévy Decomposition. In essence, the relative importance of the two drift distortions depends on the entrepreneur’s relative concern with diffusion ambiguity versus jump ambiguity.

$ {Q}^{\theta^{\ast }} $

, it is important to note that jump ambiguity distortions remain independent of drift ambiguity. This property arises from the independence of the Brownian and jump terms in line with the Itô-Lévy Decomposition. In essence, the relative importance of the two drift distortions depends on the entrepreneur’s relative concern with diffusion ambiguity versus jump ambiguity.

Importantly, beyond reducing drift, jump ambiguity also distorts jump intensity and the size distribution. For instance, the conditional mean for positive jumps (in log units) reaches its minimum at

$ 1/{\eta}_1^{\ast } $

, where

$ 1/{\eta}_1^{\ast } $

, where

$ {\eta}_1^{\ast }={\eta}_1+{M}_1 $

, while the conditional mean of negative jumps (in log units) attains its maximum at

$ {\eta}_1^{\ast }={\eta}_1+{M}_1 $

, while the conditional mean of negative jumps (in log units) attains its maximum at

$ -1/{\eta}_2^{\ast } $

, with

$ -1/{\eta}_2^{\ast } $

, with

$ {\eta}_2^{\ast }={\eta}_2 $

. The conditional probability of positive jumps reaches its minimum at

$ {\eta}_2^{\ast }={\eta}_2 $

. The conditional probability of positive jumps reaches its minimum at

$ {p}^{\ast }=p{\eta}_1/\left(p{\eta}_1+q\left({\eta}_1+{M}_1\right)\right) $

, and that of negative jumps achieves its maximum at

$ {p}^{\ast }=p{\eta}_1/\left(p{\eta}_1+q\left({\eta}_1+{M}_1\right)\right) $

, and that of negative jumps achieves its maximum at

$ {q}^{\ast }=q\left({\eta}_1+{M}_1\right)/\left(p{\eta}_1+q\left({\eta}_1+{M}_1\right)\right) $

. The jump intensity in the worst-case scenario does not attain either its maximum or minimum value but instead equals

$ {q}^{\ast }=q\left({\eta}_1+{M}_1\right)/\left(p{\eta}_1+q\left({\eta}_1+{M}_1\right)\right) $

. The jump intensity in the worst-case scenario does not attain either its maximum or minimum value but instead equals

$ {\lambda}^{\ast }=\lambda \left(p{\eta}_1/\left({\eta}_1+{M}_1\right)+q\right) $

.

$ {\lambda}^{\ast }=\lambda \left(p{\eta}_1/\left({\eta}_1+{M}_1\right)+q\right) $

.

These worst-case parameters are summarized in Table 1. The interpretation of these results follows from our earlier discussion of Table 1, where we considered the monotonicity of the value function with respect to the state variable. Specifically, the parameter

$ {\lambda}^{\ast } $

takes an interior value, as the distortion minimizes the unconditional probability of positive jumps while maximizing that of negative jumps.

$ {\lambda}^{\ast } $

takes an interior value, as the distortion minimizes the unconditional probability of positive jumps while maximizing that of negative jumps.

The expression for

$ X(t) $

under

$ X(t) $

under

$ {Q}^{\theta^{\ast }} $

reveals that jump ambiguity distorts the entire distribution of

$ {Q}^{\theta^{\ast }} $

reveals that jump ambiguity distorts the entire distribution of

$ X(t) $

, whereas drift ambiguity distorts the mean only. This is evident by examining the moment generating function of

$ X(t) $

, whereas drift ambiguity distorts the mean only. This is evident by examining the moment generating function of

$ Y(t)=\ln \left(X(t)/X(0)\right) $

as

$ Y(t)=\ln \left(X(t)/X(0)\right) $

as

$$ {\unicode{x1D53C}}^{\theta^{\ast }}\left[{e}^{vY(t)}\right]={e}^{t{\phi}^{\theta^{\ast }}(v)}, $$

$$ {\unicode{x1D53C}}^{\theta^{\ast }}\left[{e}^{vY(t)}\right]={e}^{t{\phi}^{\theta^{\ast }}(v)}, $$

where

$$ {\phi}^{\theta^{\ast }}(v)={\displaystyle \begin{array}{l}\frac{1}{2}{\sigma}^2{v}^2+\left({\mu}^{\theta^{\ast }}-\frac{1}{2}{\sigma}^2-{\lambda}^{\ast}\left(\frac{p{\eta}_1^{\ast }}{\eta_1^{\ast }-1}+\frac{q^{\ast }{\eta}_2^{\ast }}{\eta_2^{\ast }+1}-1\right)\right)v+\hskip2px {\lambda}^{\ast}\left(\frac{p^{\ast }{\eta}_1^{\ast }}{\eta_1^{\ast }-v}+\frac{q^{\ast }{\eta}_2^{\ast }}{\eta_2^{\ast }+v}-1\right).\end{array}} $$

$$ {\phi}^{\theta^{\ast }}(v)={\displaystyle \begin{array}{l}\frac{1}{2}{\sigma}^2{v}^2+\left({\mu}^{\theta^{\ast }}-\frac{1}{2}{\sigma}^2-{\lambda}^{\ast}\left(\frac{p{\eta}_1^{\ast }}{\eta_1^{\ast }-1}+\frac{q^{\ast }{\eta}_2^{\ast }}{\eta_2^{\ast }+1}-1\right)\right)v+\hskip2px {\lambda}^{\ast}\left(\frac{p^{\ast }{\eta}_1^{\ast }}{\eta_1^{\ast }-v}+\frac{q^{\ast }{\eta}_2^{\ast }}{\eta_2^{\ast }+v}-1\right).\end{array}} $$

It follows immediately that the variance of

$ Y(t) $

is

$ Y(t) $

is

$$ {\unicode{x1D53C}}^{\theta^{\ast }}\left[{\left(Y(t)-{\unicode{x1D53C}}^{\theta^{\ast }}\left[Y(t)\right]\right)}^2\right]={\sigma}^2t+2{\lambda}^{\ast}\left(\frac{p^{\ast }}{{\left({\eta}_1^{\ast}\right)}^2}+\frac{q^{\ast }}{{\left({\eta}_2^{\ast}\right)}^2}\right)t. $$

$$ {\unicode{x1D53C}}^{\theta^{\ast }}\left[{\left(Y(t)-{\unicode{x1D53C}}^{\theta^{\ast }}\left[Y(t)\right]\right)}^2\right]={\sigma}^2t+2{\lambda}^{\ast}\left(\frac{p^{\ast }}{{\left({\eta}_1^{\ast}\right)}^2}+\frac{q^{\ast }}{{\left({\eta}_2^{\ast}\right)}^2}\right)t. $$

In contrast to drift ambiguity, jump ambiguity has a significant effect on the variance of

$ Y(t) $

and higher moments, which we demonstrate numerically in Section III.B.

$ Y(t) $

and higher moments, which we demonstrate numerically in Section III.B.

After finding the worst-case measure, we solve for the optimal investment policy and the value function in equation (7). Here, we can gain analytical tractability of the double exponential jump-diffusion process for optimal stopping problems. The following proposition characterizes the optimal investment policy and the associated value function under all-equity financing.

Proposition 2. Let

$ {\eta}_1^{\ast }={\eta}_1+{M}_1 $

and

$ {\eta}_1^{\ast }={\eta}_1+{M}_1 $

and

$ {\eta}_2^{\ast }={\eta}_2 $

. For

$ {\eta}_2^{\ast }={\eta}_2 $

. For

$ X(0)=x $

, the value function

$ X(0)=x $

, the value function

$ {V}_e\left(0;{\tau}_I^e,{\theta}^{\ast}\right) $

in (7) has the solution

$ {V}_e\left(0;{\tau}_I^e,{\theta}^{\ast}\right) $

in (7) has the solution

$$ {V}_e\left(0;{\tau}_I^e,{\theta}^{\ast}\right)={\displaystyle \begin{array}{l}{A}_0{X}_I^e\left[{c}_{1,1}{\left(\frac{X_I^e}{x}\right)}^{-{\beta}_1}+{c}_{2,1}{\left(\frac{X_I^e}{x}\right)}^{-{\beta}_2}\right]-\hskip2px I\left[{c}_{1,0}{\left(\frac{X_I^e}{x}\right)}^{-{\beta}_1}+{c}_{2,0}{\left(\frac{X_I^e}{x}\right)}^{-{\beta}_2}\right],\end{array}} $$

$$ {V}_e\left(0;{\tau}_I^e,{\theta}^{\ast}\right)={\displaystyle \begin{array}{l}{A}_0{X}_I^e\left[{c}_{1,1}{\left(\frac{X_I^e}{x}\right)}^{-{\beta}_1}+{c}_{2,1}{\left(\frac{X_I^e}{x}\right)}^{-{\beta}_2}\right]-\hskip2px I\left[{c}_{1,0}{\left(\frac{X_I^e}{x}\right)}^{-{\beta}_1}+{c}_{2,0}{\left(\frac{X_I^e}{x}\right)}^{-{\beta}_2}\right],\end{array}} $$

where the optimal stopping time satisfies

$ {\tau}_I^e={\operatorname{inf}}_t\;\left\{X(t)\ge {X}_I^e\right\} $

, and the optimal investment boundary

$ {\tau}_I^e={\operatorname{inf}}_t\;\left\{X(t)\ge {X}_I^e\right\} $

, and the optimal investment boundary

$ {X}_I^e $

is given by

$ {X}_I^e $

is given by

$$ {A}_0{X}_I^e=\underset{option\ multiplier>1}{\underbrace{\frac{\beta_1{\beta}_2}{\left({\beta}_1-1\right)\left({\beta}_2-1\right)}\frac{\eta_1^{\ast }-1}{\eta_1^{\ast }}}}I,\hskip1em {A}_0=\underset{value\ multiplier}{\underbrace{\frac{1-\phi }{r-{\mu}^{\theta^{\ast }}}}}. $$

$$ {A}_0{X}_I^e=\underset{option\ multiplier>1}{\underbrace{\frac{\beta_1{\beta}_2}{\left({\beta}_1-1\right)\left({\beta}_2-1\right)}\frac{\eta_1^{\ast }-1}{\eta_1^{\ast }}}}I,\hskip1em {A}_0=\underset{value\ multiplier}{\underbrace{\frac{1-\phi }{r-{\mu}^{\theta^{\ast }}}}}. $$

Here,

$ {\beta}_1 $

,

$ {\beta}_1 $

,

$ {\beta}_2 $

,

$ {\beta}_2 $

,

$ {\beta}_3 $

,

$ {\beta}_3 $

,

$ {\beta}_4 $

are constants satisfying

$ {\beta}_4 $

are constants satisfying

$ -\infty <-{\beta}_4<-{\eta}_2^{\ast }<-{\beta}_3<0<{\beta}_1<{\eta}_1^{\ast }<{\beta}_2<\infty $

and are the four roots of the equation

$ -\infty <-{\beta}_4<-{\eta}_2^{\ast }<-{\beta}_3<0<{\beta}_1<{\eta}_1^{\ast }<{\beta}_2<\infty $

and are the four roots of the equation

$ G\left(\beta \right)=r $

, with

$ G\left(\beta \right)=r $

, with

$$ G\left(\beta \right)=\frac{1}{2}{\sigma}^2{\beta}^2+\left[{\mu}^{\theta^{\ast }}-\frac{1}{2}{\sigma}^2-{\lambda}^{\ast}\left(\frac{p^{\ast }{\eta}_1^{\ast }}{\eta_1^{\ast }-1}+\frac{q^{\ast }{\eta}_2^{\ast }}{\eta_2^{\ast }+1}-1\right)\right]\beta +{\lambda}^{\ast}\left(\frac{p^{\ast }{\eta}_1^{\ast }}{\eta_1^{\ast }-\beta }+\frac{q^{\ast }{\eta}_2^{\ast }}{\eta_2^{\ast }+\beta }-1\right). $$

$$ G\left(\beta \right)=\frac{1}{2}{\sigma}^2{\beta}^2+\left[{\mu}^{\theta^{\ast }}-\frac{1}{2}{\sigma}^2-{\lambda}^{\ast}\left(\frac{p^{\ast }{\eta}_1^{\ast }}{\eta_1^{\ast }-1}+\frac{q^{\ast }{\eta}_2^{\ast }}{\eta_2^{\ast }+1}-1\right)\right]\beta +{\lambda}^{\ast}\left(\frac{p^{\ast }{\eta}_1^{\ast }}{\eta_1^{\ast }-\beta }+\frac{q^{\ast }{\eta}_2^{\ast }}{\eta_2^{\ast }+\beta }-1\right). $$

The constants

$ {c}_{1,0},{c}_{2,0},{c}_{1,1} $

and

$ {c}_{1,0},{c}_{2,0},{c}_{1,1} $

and

$ {c}_{2,1} $

are given by

$ {c}_{2,1} $

are given by

$$ {c}_{1,0}=\frac{\eta_1^{\ast }-{\beta}_1}{\beta_2-{\beta}_1}\frac{\beta_2}{\eta_1^{\ast }},{c}_{2,0}=\frac{\beta_2-{\eta}_1^{\ast }}{\beta_2-{\beta}_1}\frac{\beta_1}{\eta_1^{\ast }},{c}_{1,1}=\frac{\eta_1^{\ast }-{\beta}_1}{\beta_2-{\beta}_1}\frac{\beta_2-1}{\eta_1^{\ast }-1},{c}_{2,1}=\frac{\beta_2-{\eta}_1^{\ast }}{\beta_2-{\beta}_1}\frac{\beta_1-1}{\eta_1^{\ast }-1}. $$

$$ {c}_{1,0}=\frac{\eta_1^{\ast }-{\beta}_1}{\beta_2-{\beta}_1}\frac{\beta_2}{\eta_1^{\ast }},{c}_{2,0}=\frac{\beta_2-{\eta}_1^{\ast }}{\beta_2-{\beta}_1}\frac{\beta_1}{\eta_1^{\ast }},{c}_{1,1}=\frac{\eta_1^{\ast }-{\beta}_1}{\beta_2-{\beta}_1}\frac{\beta_2-1}{\eta_1^{\ast }-1},{c}_{2,1}=\frac{\beta_2-{\eta}_1^{\ast }}{\beta_2-{\beta}_1}\frac{\beta_1-1}{\eta_1^{\ast }-1}. $$

The investment payoff at

$ {\tau}_I^e $

is

$ {\tau}_I^e $

is

$ {A}_0X\left({\tau}_I^e\right)-I $

. In equation (9), the term

$ {A}_0X\left({\tau}_I^e\right)-I $

. In equation (9), the term

$ {A}_0{X}_I^e $

represents the equity value at

$ {A}_0{X}_I^e $

represents the equity value at

$ {\tau}_I^e $

(in the absence of overshooting) and admits a Gordon growth-like interpretation.Footnote 9 The value multiplier (VM) reflects the project’s value when

$ {\tau}_I^e $

(in the absence of overshooting) and admits a Gordon growth-like interpretation.Footnote 9 The value multiplier (VM) reflects the project’s value when

$ X(t)=1 $

, and it decreases as ambiguity increases. On the right-hand side, the equity value is expressed in terms of the cost

$ X(t)=1 $

, and it decreases as ambiguity increases. On the right-hand side, the equity value is expressed in terms of the cost

$ I $

and the option multiplier (OM), which accounts for the effect of uncertainty on the investment decision. Here, uncertainty includes both diffusion and jump risks, characterized by the primitive parameters of the double-exponential jump-diffusion process, as well as drift and jump ambiguity.

$ I $

and the option multiplier (OM), which accounts for the effect of uncertainty on the investment decision. Here, uncertainty includes both diffusion and jump risks, characterized by the primitive parameters of the double-exponential jump-diffusion process, as well as drift and jump ambiguity.

Remark 1. Jump ambiguity reduces the project value by lowering the investment payoff at

$ {\tau}_I^e $

, raising the cash flow threshold

$ {\tau}_I^e $

, raising the cash flow threshold

$ {X}_I^e $

, and extending the expected threshold hitting time

$ {X}_I^e $

, and extending the expected threshold hitting time

$ {\tau}_I^e $

.

$ {\tau}_I^e $

.

An immediate observation from the inequality:

$$ \frac{\beta_2}{\beta_2-1}I<{A}_0{X}_I^e<\frac{\beta_1}{\beta_1-1}I, $$

$$ \frac{\beta_2}{\beta_2-1}I<{A}_0{X}_I^e<\frac{\beta_1}{\beta_1-1}I, $$

is that as jump ambiguity

$ {M}_1\to \infty $

,

$ {M}_1\to \infty $

,

$ {\beta}_2 $

approaches infinity, causing the lower bound of

$ {\beta}_2 $

approaches infinity, causing the lower bound of

$ {A}_0{X}_I^e $

to decrease monotonically toward

$ {A}_0{X}_I^e $

to decrease monotonically toward

$ I $

. Although the limit of

$ I $

. Although the limit of

$ {\beta}_1 $

is harder to deduce, it is evident that the upper bound also decreases monotonically with

$ {\beta}_1 $

is harder to deduce, it is evident that the upper bound also decreases monotonically with

$ {M}_1 $

. We conjecture that both bounds eventually converge, reducing the OM to 1 and driving the equity value at

$ {M}_1 $

. We conjecture that both bounds eventually converge, reducing the OM to 1 and driving the equity value at

$ {\tau}_I^e $

to the net present value (NPV) threshold,

$ {\tau}_I^e $

to the net present value (NPV) threshold,

$ I $

.

$ I $

.

We deduce that

$ {X}_I^e $

increases with

$ {X}_I^e $

increases with

$ {M}_1 $

. While the effect of

$ {M}_1 $

. While the effect of

$ {M}_1 $

on

$ {M}_1 $

on

$ {X}_I^e $

is not immediately clear due to the simultaneous decrease in both the OM and VM, we can infer the relationship by comparing their rates of change. Computing

$ {X}_I^e $

is not immediately clear due to the simultaneous decrease in both the OM and VM, we can infer the relationship by comparing their rates of change. Computing

$ \partial {X}_I^e/\partial {M}_1 $

is technically challenging, but the decline in

$ \partial {X}_I^e/\partial {M}_1 $

is technically challenging, but the decline in

$ {\mu}^{\theta^{\ast }} $

with

$ {\mu}^{\theta^{\ast }} $

with

$ {M}_1 $

follows a rate bounded by

$ {M}_1 $

follows a rate bounded by

$ \tilde{C}/{M}_1^2 $

, leading the VM to decrease at the same rate, where

$ \tilde{C}/{M}_1^2 $

, leading the VM to decrease at the same rate, where

$ \tilde{C}>0 $

denotes an arbitrary constant. Moreover, the upper and lower bounds for

$ \tilde{C}>0 $

denotes an arbitrary constant. Moreover, the upper and lower bounds for

$ {A}_0{X}_I^e $

decrease at a rate bounded by

$ {A}_0{X}_I^e $

decrease at a rate bounded by

$ \tilde{C}/{M}_1 $

. Thus, we numerically verify that

$ \tilde{C}/{M}_1 $

. Thus, we numerically verify that

$ {X}_I^e $

increases with

$ {X}_I^e $

increases with

$ {M}_1 $

at a rate bounded by

$ {M}_1 $

at a rate bounded by

$ \tilde{C}/{M}_1 $

.

$ \tilde{C}/{M}_1 $

.

Lastly, we anticipate that the expected investment time,

$ {\tau}_I^e $

, also increases with

$ {\tau}_I^e $

, also increases with

$ {M}_1 $

for two reasons. First, investment occurs when

$ {M}_1 $

for two reasons. First, investment occurs when

$ X(t) $

reaches

$ X(t) $

reaches

$ {X}_I^e $

from below, and under

$ {X}_I^e $

from below, and under

$ {Q}^{\theta^{\ast }} $

,

$ {Q}^{\theta^{\ast }} $

,

$ X(t) $

has the least upward potential, leading to a longer average time to reach any given level compared to

$ X(t) $

has the least upward potential, leading to a longer average time to reach any given level compared to

$ {Q}^0 $

. Second, since

$ {Q}^0 $

. Second, since

$ {X}_I^e $

is higher under

$ {X}_I^e $

is higher under

$ {Q}^{\theta^{\ast }} $

than under

$ {Q}^{\theta^{\ast }} $

than under

$ {Q}^0 $

, the expected hitting time is further extended, reinforcing the delay in investment.

$ {Q}^0 $

, the expected hitting time is further extended, reinforcing the delay in investment.

Remark 2. Under a fixed cash flow threshold policy, ambiguity induces the firm to undertake smaller innovation projects.

A fixed cash flow threshold policy is to invest when

$ X(t)\ge \overline{X} $

for the first time, where

$ X(t)\ge \overline{X} $

for the first time, where

$ \overline{X} $

is a fixed level.Footnote 10 In this case, the optimality condition (9) implies that the firm can maximize its equity value by choosing

$ \overline{X} $

is a fixed level.Footnote 10 In this case, the optimality condition (9) implies that the firm can maximize its equity value by choosing

$ I $

optimally, satisfying

$ I $

optimally, satisfying

$ {I}_e^{\ast }=\overline{X}\times VM/ OM $

. As discussed above, jump ambiguity lowers the VM at a rate bounded by

$ {I}_e^{\ast }=\overline{X}\times VM/ OM $

. As discussed above, jump ambiguity lowers the VM at a rate bounded by

$ \tilde{C}/{M}_1^2 $

and the OM at a rate bounded by

$ \tilde{C}/{M}_1^2 $

and the OM at a rate bounded by

$ \tilde{C}/{M}_1 $

. Hence,

$ \tilde{C}/{M}_1 $

. Hence,

$ {I}_e^{\ast } $

decreases with

$ {I}_e^{\ast } $

decreases with

$ {M}_1 $

at a rate bounded by

$ {M}_1 $

at a rate bounded by

$ \tilde{C}/{M}_1 $

.

$ \tilde{C}/{M}_1 $

.

Remark 2 parallels the insight of Campello and Kankanhalli (Reference Campello, Kankanhalli and Denis2024), who show that greater uncertainty reduces investment size in a two-period framework with mean-preserving spread.Footnote 11 Our approach differs from that of Campello and Kankanhalli (Reference Campello, Kankanhalli and Denis2024), as in that model the ambiguity-neutral decision maker evaluates uncertainty through second-order stochastic dominance, whereas our continuous-time framework explicitly incorporates both diffusion and jump risks together with ambiguity.

D. Innovation with Optimal Financing

1. Optimal Default under Ambiguity

Because of the property

$ {Q}^{\theta^{\ast }}\{{\tau}_I^{\ast }<+\mathrm{\infty}\}=1 $

in the all-equity financing case and dynamic consistency, we can first solve for the entrepreneur’s optimal default decision and then the optimal coupon to determine the optimal capital structure. Under the worst-case measure

$ {Q}^{\theta^{\ast }}\{{\tau}_I^{\ast }<+\mathrm{\infty}\}=1 $

in the all-equity financing case and dynamic consistency, we can first solve for the entrepreneur’s optimal default decision and then the optimal coupon to determine the optimal capital structure. Under the worst-case measure

$ {Q}^{\theta^{\ast }} $

(Proposition 3),

$ {Q}^{\theta^{\ast }} $

(Proposition 3),

$ {Q}^{\theta^{\ast }}\{{\tau}_D^{\ast }<+\mathrm{\infty}\}=1 $

holds for our parameter requirements, and thus the levered equity value at

$ {Q}^{\theta^{\ast }}\{{\tau}_D^{\ast }<+\mathrm{\infty}\}=1 $

holds for our parameter requirements, and thus the levered equity value at

$ {\tau}_I $

follows:

$ {\tau}_I $

follows:

$$ E\left({\tau}_I;{\tau}_D^{\ast },{\theta}^{\ast },C\right)=\underset{\tau_D\ge {\tau}_I}{\sup}\;\underset{Q^{\theta }}{\operatorname{inf}}\;{\unicode{x1D53C}}_{\tau_I}\left[{\int}_{\tau_I}^{\tau_D}{e}^{-r\left(t-{\tau}_I\right)}\left(1-\phi \right)\left(X(t)-C\right) dt\right]. $$

$$ E\left({\tau}_I;{\tau}_D^{\ast },{\theta}^{\ast },C\right)=\underset{\tau_D\ge {\tau}_I}{\sup}\;\underset{Q^{\theta }}{\operatorname{inf}}\;{\unicode{x1D53C}}_{\tau_I}\left[{\int}_{\tau_I}^{\tau_D}{e}^{-r\left(t-{\tau}_I\right)}\left(1-\phi \right)\left(X(t)-C\right) dt\right]. $$

Without ambiguity, the problem reduces to the baseline model in equation (4).

Using the same approach as in Section II.C, we begin by finding the density generator that delivers the worst-case measure:

$$ E\left({\tau}_I;{\tau}_D,{\theta}^{\ast },C\right)=\underset{Q^{\theta }}{\operatorname{inf}}\;{\unicode{x1D53C}}_{\tau_I}\left[{\int}_{\tau_I}^{\tau_D}{e}^{-r\left(t-{\tau}_I\right)}\left(1-\phi \right)\left(X(t)-C\right) dt\right]. $$

$$ E\left({\tau}_I;{\tau}_D,{\theta}^{\ast },C\right)=\underset{Q^{\theta }}{\operatorname{inf}}\;{\unicode{x1D53C}}_{\tau_I}\left[{\int}_{\tau_I}^{\tau_D}{e}^{-r\left(t-{\tau}_I\right)}\left(1-\phi \right)\left(X(t)-C\right) dt\right]. $$

Proposition 3. The density generator that gives the minimum expectation in (13) is

$ {\theta}^{\ast }=\left({\theta}_W^{\ast },{\theta}_N^{\ast}\right)=\left(\kappa, 1-{e}^{-{M}_1u}{\boldsymbol{1}}_{u\ge 0}-{\boldsymbol{1}}_{u<0}\right) $

for all

$ {\theta}^{\ast }=\left({\theta}_W^{\ast },{\theta}_N^{\ast}\right)=\left(\kappa, 1-{e}^{-{M}_1u}{\boldsymbol{1}}_{u\ge 0}-{\boldsymbol{1}}_{u<0}\right) $

for all

$ t\in \left[{\tau}_I,T\right] $

.

$ t\in \left[{\tau}_I,T\right] $

.

Proposition 3 establishes that the worst-case measure is the same under both optimal financing and all-equity financing. This result follows because, in both cases, equity holders receive net profit, and their main concern under ambiguity is that the perceived EBIT profile is the least favorable.

Given that we have determined the worst-case prior for equity holders, we can then solve for the optimal default timing

$ {\tau}_D^{\ast } $

and the value function. The results are summarized in the proposition below.

$ {\tau}_D^{\ast } $

and the value function. The results are summarized in the proposition below.

Proposition 4. Let

$ {\beta}_3 $

,

$ {\beta}_3 $

,

$ {\beta}_4 $

,

$ {\beta}_4 $

,

$ {\mu}^{\theta^{\ast }} $

,

$ {\mu}^{\theta^{\ast }} $

,

$ {\eta}_1^{\ast } $

,

$ {\eta}_1^{\ast } $

,

$ {\eta}_2^{\ast } $

, and

$ {\eta}_2^{\ast } $

, and

$ {A}_0 $

be the same as in Proposition 2. The levered equity value

$ {A}_0 $

be the same as in Proposition 2. The levered equity value

$ E\left({\tau}_I;{\tau}_D^{\ast },{\theta}^{\ast },C\right) $

in (12) has the following expression.

$ E\left({\tau}_I;{\tau}_D^{\ast },{\theta}^{\ast },C\right) $

in (12) has the following expression.

$$ {\displaystyle \begin{array}{c}E\left({\tau}_I;{\tau}_D^{\ast },{\theta}^{\ast },C\right)={A}_0X\left({\tau}_I\right)-\frac{\left(1-\phi \right)C}{r}\left[1-{d}_{1,0}{\left(\frac{X_D^{\ast }}{X\left({\tau}_I\right)}\right)}^{\beta_3}-{d}_{2,0}{\left(\frac{X_D^{\ast }}{X\left({\tau}_I\right)}\right)}^{\beta_4}\right]\\ {}\hskip1.05em -{A}_0{X}_D^{\ast}\left[{d}_{1,1}{\left(\frac{X_D^{\ast }}{X\left({\tau}_I\right)}\right)}^{\beta_3}+{d}_{2,1}{\left(\frac{X_D^{\ast }}{X\left({\tau}_I\right)}\right)}^{\beta_4}\right],\end{array}} $$

$$ {\displaystyle \begin{array}{c}E\left({\tau}_I;{\tau}_D^{\ast },{\theta}^{\ast },C\right)={A}_0X\left({\tau}_I\right)-\frac{\left(1-\phi \right)C}{r}\left[1-{d}_{1,0}{\left(\frac{X_D^{\ast }}{X\left({\tau}_I\right)}\right)}^{\beta_3}-{d}_{2,0}{\left(\frac{X_D^{\ast }}{X\left({\tau}_I\right)}\right)}^{\beta_4}\right]\\ {}\hskip1.05em -{A}_0{X}_D^{\ast}\left[{d}_{1,1}{\left(\frac{X_D^{\ast }}{X\left({\tau}_I\right)}\right)}^{\beta_3}+{d}_{2,1}{\left(\frac{X_D^{\ast }}{X\left({\tau}_I\right)}\right)}^{\beta_4}\right],\end{array}} $$

where

$$ {d}_{1,0}=\frac{\eta_2^{\ast }-{\beta}_3}{\beta_4-{\beta}_3}\frac{\beta_4}{\eta_2^{\ast }},{d}_{2,0}=\frac{\beta_4-{\eta}_2^{\ast }}{\beta_4-{\beta}_3}\frac{\beta_3}{\eta_2^{\ast }},{d}_{1,1}=\frac{\eta_2^{\ast }-{\beta}_3}{\beta_4-{\beta}_3}\frac{\beta_4+1}{\eta_2^{\ast }+1},{d}_{2,1}=\frac{\beta_4-{\eta}_2^{\ast }}{\beta_4-{\beta}_3}\frac{\beta_3+1}{\eta_2^{\ast }+1}, $$

$$ {d}_{1,0}=\frac{\eta_2^{\ast }-{\beta}_3}{\beta_4-{\beta}_3}\frac{\beta_4}{\eta_2^{\ast }},{d}_{2,0}=\frac{\beta_4-{\eta}_2^{\ast }}{\beta_4-{\beta}_3}\frac{\beta_3}{\eta_2^{\ast }},{d}_{1,1}=\frac{\eta_2^{\ast }-{\beta}_3}{\beta_4-{\beta}_3}\frac{\beta_4+1}{\eta_2^{\ast }+1},{d}_{2,1}=\frac{\beta_4-{\eta}_2^{\ast }}{\beta_4-{\beta}_3}\frac{\beta_3+1}{\eta_2^{\ast }+1}, $$

and the optimal default policy is

$ {\tau}_D^{\ast }={\operatorname{inf}}_t\left\{X(t)\le {X}_D^{\ast}\right\} $

with the optimal default boundary

$ {\tau}_D^{\ast }={\operatorname{inf}}_t\left\{X(t)\le {X}_D^{\ast}\right\} $

with the optimal default boundary

$ {X}_D^{\ast } $

given by

$ {X}_D^{\ast } $

given by

$$ {A}_0{X}_D^{\ast }=\underset{option\ multiplier<1}{\underbrace{\frac{\beta_3{\beta}_4\left({\eta}_2^{\ast }+1\right)}{\left({\beta}_3+1\right)\left({\beta}_4+1\right){\eta}_2^{\ast }}}}\frac{\left(1-\phi \right)C}{r}. $$

$$ {A}_0{X}_D^{\ast }=\underset{option\ multiplier<1}{\underbrace{\frac{\beta_3{\beta}_4\left({\eta}_2^{\ast }+1\right)}{\left({\beta}_3+1\right)\left({\beta}_4+1\right){\eta}_2^{\ast }}}}\frac{\left(1-\phi \right)C}{r}. $$

At default, under liquidation bankruptcy, equity holders lose the firm, valued at

$ {A}_0{X}_D^{\ast } $

—the left-hand side of equation (15). At the same time, they cease paying the tax deductible perpetual coupons, valued at

$ {A}_0{X}_D^{\ast } $

—the left-hand side of equation (15). At the same time, they cease paying the tax deductible perpetual coupons, valued at

$ \left(1-\phi \right)C/r $

. Thus, the NPV rule dictates that default occurs when

$ \left(1-\phi \right)C/r $

. Thus, the NPV rule dictates that default occurs when

$ {A}_0X(t)=\left(1-\phi \right)C/r $

for the first time. However, defaulting at the NPV threshold is suboptimal because equity holders have the option to inject additional equity to delay default, anticipating a future rebound in

$ {A}_0X(t)=\left(1-\phi \right)C/r $

for the first time. However, defaulting at the NPV threshold is suboptimal because equity holders have the option to inject additional equity to delay default, anticipating a future rebound in

$ X(t) $

. Therefore, the optimal default threshold is set below the NPV threshold, discounted by the OM, which reflects the factors discussed earlier in relation to

$ X(t) $

. Therefore, the optimal default threshold is set below the NPV threshold, discounted by the OM, which reflects the factors discussed earlier in relation to

$ {X}_I^{\ast } $

in Proposition 2.Footnote 12

$ {X}_I^{\ast } $

in Proposition 2.Footnote 12

Remark 3. Jump ambiguity has a secondary effect on optimal default boundary

$ {X}_D^{\ast } $

.

$ {X}_D^{\ast } $

.

For

$ {X}_D^{\ast } $

, we can establish its lower and upper bounds as follows:

$ {X}_D^{\ast } $

, we can establish its lower and upper bounds as follows:

$$ \frac{\beta_3+1}{\beta_3}\frac{\left(1-\phi \right)C}{r}<{A}_0{X}_D^{\ast }<\frac{\beta_4+1}{\beta_4}\frac{\left(1-\phi \right)C}{r}. $$

$$ \frac{\beta_3+1}{\beta_3}\frac{\left(1-\phi \right)C}{r}<{A}_0{X}_D^{\ast }<\frac{\beta_4+1}{\beta_4}\frac{\left(1-\phi \right)C}{r}. $$

Since

$ {\theta}_{N,2}=0 $

under

$ {\theta}_{N,2}=0 $

under

$ {Q}^{\theta^{\ast }} $

, jump ambiguity governed by

$ {Q}^{\theta^{\ast }} $

, jump ambiguity governed by

$ {M}_1 $

does not significantly affect

$ {M}_1 $

does not significantly affect

$ {\beta}_3 $

and

$ {\beta}_3 $

and

$ {\beta}_4 $

, implying that the bounds for

$ {\beta}_4 $

, implying that the bounds for

$ {A}_0{X}_D^{\ast } $

do not converge in the same way as the bounds for

$ {A}_0{X}_D^{\ast } $

do not converge in the same way as the bounds for

$ {A}_0{X}_I^{\ast } $

. As a result, the influence of jump ambiguity on

$ {A}_0{X}_I^{\ast } $

. As a result, the influence of jump ambiguity on

$ {X}_D^{\ast } $

stems primarily from the interaction between the VM and

$ {X}_D^{\ast } $

stems primarily from the interaction between the VM and

$ {C}^{\ast } $

, the endogenously determined optimal coupon. This suggests that both the OM and the default boundary are less sensitive to jump ambiguity than their counterparts for investment.

$ {C}^{\ast } $

, the endogenously determined optimal coupon. This suggests that both the OM and the default boundary are less sensitive to jump ambiguity than their counterparts for investment.

2. Optimal Financing Choice