Internationalisation can have six economic effects on the competitive advantage of any firm: adding volume and growth, reducing cost, differentiating and increasing willingness to pay, increasing industry attractiveness, normalising risk and generating knowledge and other resources.Footnote 1

Adding volume and growth is one of the key drivers of competitive advantage and most multinational organisations cite this as the main reason behind their internationalisation. EMBRAER’s expansion into China, for example, was driven by optimistic expectations of the growth in regional and business air transport in the region. In 2015, as many as 130 planes were forecast to leave EMRAER’s Chinese factory; however, only 2 were delivered and EMRAER was rumoured to be considering shutting down its Chinese operations, after the dramatic slump in Chinese business aviation that followed the government’s crackdown on corporate corruption.Footnote 2 Cost reduction was the driver behind Marcopolo’s expansion into Egypt; the Brazilian bus body manufacturer made the move to lower the cost of serving its markets in North Africa, the Middle East and Europe.Footnote 3 The Brazilian cosmetics company Natura boosted its differentiation and customers’ willingness to pay by opening a flagship store in Paris, trading its traditional direct sales model off against the reputational benefit of having a store in the world capital of cosmetics. Competitive advantage can also be derived from increased industry attractiveness. The Mexican company CEMEX exploited this masterfully when internationalising in Colombia and Venezuela, where it captured more than 70% of the installed market capacity. By internationalising, CEMEX also normalised its risk, as the construction industry that drives the cement business is characterised by uncorrelated national cycles. The company also benefitted from the development of new knowledge and integrated it into the ‘CEMEX way’.

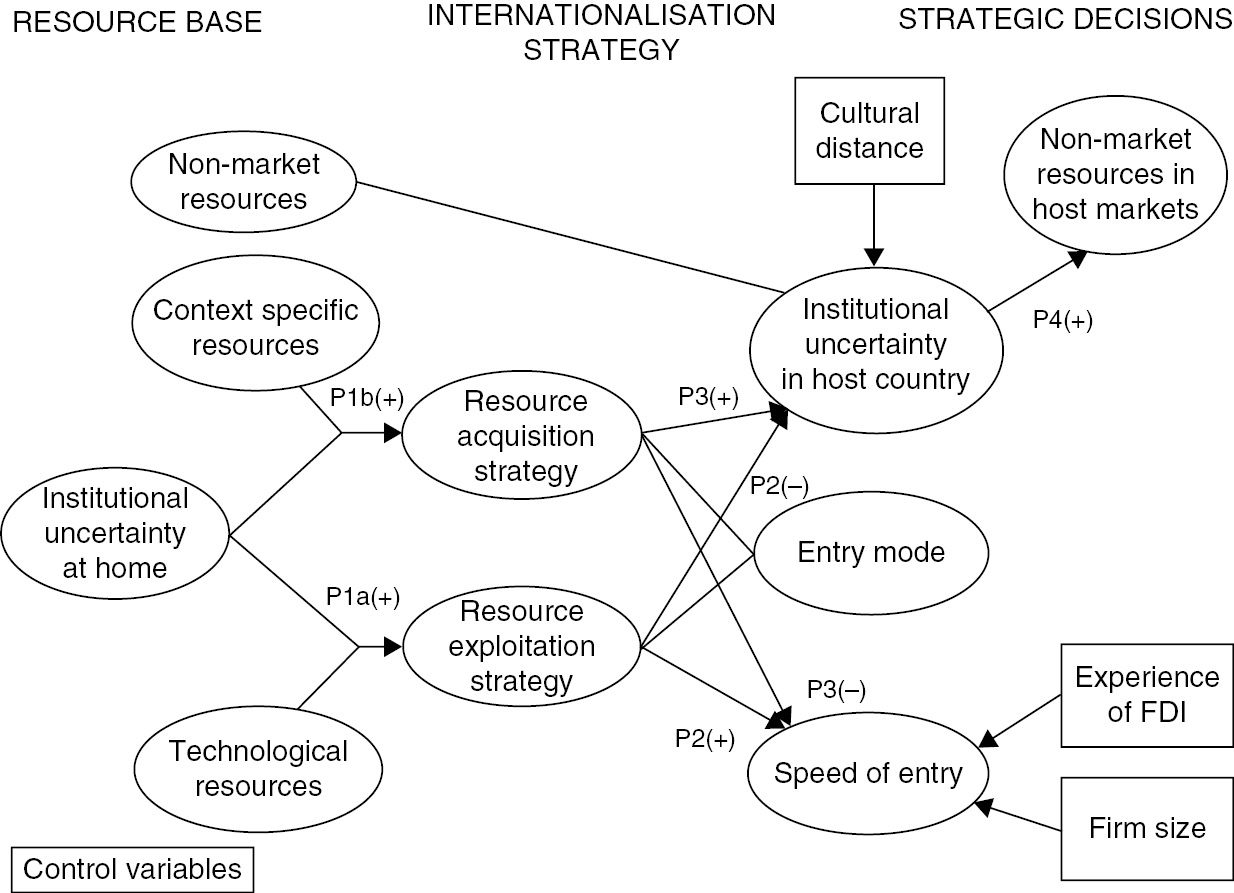

These six drivers of internationalisation give rise to the distinct strategies that multinationals use to mobilise their resources to create economic value. It is important to understand how the nature of home-based resources conditions the implementation of resource exploitation and resource acquisition strategies in an environment characterised by general institutional uncertainty, which is focused on as the most significant structural factor in the region. From this resource-based perspective, resource exploitation and resource acquisition are the two generic approaches to internationalisation and their desirability depends on the characteristics of the resources that lead to the consolidation of the competitive advantage at home.

In essence, the varying degrees of reliance on technological and context-specific resources in domestic environments with significant institutional uncertainty create dissimilar opportunities for multilatinas and influence the choices they make during the internationalisation process.

For firms whose domestic competitive advantage is predominantly reliant on technological resources, which are more easily transferred across borders, political instability and government intervention in their home market might stimulate the process of internationalisation to countries with a lower level of institutional uncertainty. Faced with challenges or deteriorating conditions of institutional uncertainty at home, these multilatinas can take the opportunity to move abroad to exploit their domestic technological resources in products and processes similar to those used in the home market. This gives them the potential to benefit from enhanced profitability,Footnote 4 increased economies of scaleFootnote 5 and possibly fewer competitive pressures,Footnote 6 besides the normalisation of risk. Exploitation of their strategically important domestic resources is feasible because technological resources are highly redeployable and their value is preserved or even increased across markets.Footnote 7

On the other hand, multilatinas that compete domestically, relying predominantly on context-specific resources, such as brands and supplier networks, find it impossible to redeploy their assets as these are non-fungible and embedded in the context. Of course, under the pressure of institutional uncertainty, all business operations face greater risk, whatever the nature of their assets. This risk has to be taken into account when analysing the process of internationalisation of all kinds of emerging country multinationals.Footnote 8 For example, if firms base their competitive advantage at home on strong relations with local communities, as is the case of many oil and gas companies in Latin America, they might lose their competitiveness if national institutions intervene to alter the balance in these relationships. The temptation for different government institutions to shift the division of gains between indigenous groups and oil and gas companies, as in Colombia in 2016, substantially increases the risk of doing business in these contexts; companies are exposed to short- and long-term incentives, which ultimately lead to an even more adverse business environment. In the short run, and given the sunk-cost nature of the investment, companies have an incentive to compensate local communities above and beyond the level initially agreed. In the long run, however, this can lead to the exponential escalation of ex-post rent-seeking by communities that were not even part of the initial negotiations with the oil and gas companies, triggering a bandwagon effect. This ultimately reduces the attractiveness of the local environment and creates incentives for companies to find alternative locations abroad. Knowledge that is useful for dealing with specific but critical institutional details cannot usually be reapplied within other institutional frameworks without substantial adaptationFootnote 9 and learning. For this reason, multilatinas, whose competitiveness is based on context-specific resources at home, invest abroad following a resources acquisition strategy in the host country,Footnote 10 unable to benefit from much of the home market advantages they have built.

Resource acquisition strategy increases firms’ resources through investments abroad.Footnote 11 The rationale of this strategy is that resources that are new for the firm are acquired abroad to substitute for the internal development of resources or capabilities. Multilatinas that compete at home on the basis of context-specific resources need to acquire additional new resources when engaging in foreign direct investment (FDI) because of the non-fungibility of context-specific resources.Footnote 12

A local supplier network that has been useful for a firm building advantages at home has low added value abroad because it represents a resource that was developed for and with a specific group of partners that are embedded in the home market. To compete successfully abroad, this firm would need to develop new networks with a different group of stakeholders in the host markets. These examples, and current research, suggest that context-specific resources might lose their value or even create disadvantages when deployed across contexts.Footnote 13 Therefore, multilatinas that compete successfully at home by relying on context-specific resources developed under conditions of institutional uncertainty take a resource acquisition approach to FDI.

Internationalisation strategies and strategic decisions

The strategic decisions related to the where, when and how of internationalisation are contingent on following a strategy of resource exploitation or resource acquisition. Technological resources that are essential to competitiveness at home are redeployable, so firms should not face significant delays when taking them abroad. For these firms, the time elapsing between discovering an investment opportunity and establishing operations abroad will be relatively short.Footnote 14 Faster speed of investment also allows multilatinas to escape from increasing institutional threats in their home market and reduces the risk of losing their advantage there. Even though contexts with a low degree of institutional uncertainty are more business-friendly and effectively protect technological resources, multilatinas might face late-entrant disadvantages in them. The redeployability of technological resources makes the prospect of initiating business operations in conditions of higher institutional uncertainty feasible, despite the fact that they are likely to offer fewer risk reduction opportunities.

In essence, countries with strong formal institutions, where the rules of the game are stable and predictable, are attractive for multilatinas that aim to exploit their technological resources by obtaining exclusive, enforceable rights to them, but this frequently comes with the disadvantages of serious competition and late entry. Nevertheless, even institutionally uncertain host environments can be opportunistic choices, as the redeployability of technological resources allows them to be transferred away at a relatively low cost if necessary.Footnote 15

Resource exploiters can benefit from a variety of entry formats. Greenfield investment is the most efficient way to transfer valuable resources between countries while minimising negotiation costsFootnote 16 and benefitting from economies of scale. Resource exploiters seek to replicate abroad the combination of core technological resources and competences they have used successfully in their home markets and usually need only complementary (non-essential) resources in the host country.Footnote 17 These emerging multinationals do not have a strong incentive to pay a premium price for a firm already positioned in the host market as they expect to be able to compete there successfully using their own resources. Compared to joint ventures and acquisitions, greenfield investments allow multilatinas to retain full ownership of the resources that are sources of advantage.Footnote 18 However, greenfield projects have an important disadvantage when it comes to speed of execution. If multilatinas pick host markets on the basis of the redeployability of their critical resources, the speed of relocation is likely to be an important decision variable. In this case, acquisitions have the advantage of faster execution, besides offering a more attractive market structure by eliminating a local competitor. The choice between greenfield investment and acquisition as entry strategies is a choice between tighter control of key competitive assets and speed of relocation. This represents an important trade-off. In light of the evidence that the internationalisation of emerging multinationals is an opportunity-driven, time-sensitive process, speed is seen as the decisive advantage of acquisition as an entry strategy for resource exploiting multilatinas. This choice of entry mode is analysed with data in Chapter 12.

In short, the resource exploitation strategy is, conceptually, positively related to investments in countries with low institutional uncertainty (where), speedy FDI (when) and choice of greenfield as an entry mode (how), as it provides the most control over the valuable resources but is the least expeditious mode of international entry.

The strategic decisions of firms that base their home advantage on context-specific resources are different from those of firms that base their advantage on technological resources.Footnote 19 The former have to build them up from scratch in every host market. As a result, firms that rely on context-specific resources at home draw their advantage not so much from the home-based resources themselves but from their experience of having built them in an uncertain institutional environment. Therefore, multilatinas in the process of building context-specific resources abroad might actually enjoy an advantage from investing in countries with similarly uncertain institutional environments. By selecting host markets with high levels of institutional uncertainty multilatinas reduce the cost of learning how to do business in the host country because they can take advantage of the similarities across institutional settings between the home and host country.Footnote 20 Because context-specific resources are essential for business success but are also unique for each market, their development depends on substantial local learning, which is time-intensive. After identifying business opportunities in a given host market, multilatinas that pursue a resource acquisition strategy are likely to take time to plan their subsequent steps carefully, unlike firms that pursue a resource exploitation strategy. The availability of local partners can accelerate this learning process. On the other hand, multilatinas that make foreign investments to build new context-specific resources benefit from entry modes that allow them to control the resources needed. If they have a choice and are not forced into a joint venture by the host regulators,Footnote 21 multilatinas are likely to prefer controlling their operations in the host market rather than sharing ownership with a partner because misalignment of goals between the different parties might limit access to the resources required to build market advantages.Footnote 22 It is a well-known fact that joint ventures are very difficult to manage because of the structural complexity they exhibit.Footnote 23 Resource acquisitive multilatinas need to decide between entering a market through acquisition or through greenfield investment, which has the disadvantage that it does not readily provide much-needed context-specific resources.

Briefly, the resource acquisition strategy is conceptually positively related to the selection of countries with high levels of institutional uncertainty (where), negatively related to the speed of FDI (when) and positively related to the acquisition entry mode (how) because of the readily available and valuable context-specificity of the resources in the host market.

Non-market resources and the internationalisation of multilatinas

The approach to internationalisation also depends on how multilatinas deal with the non-market forces entrenched in the social, political and legal structures that impact on their relationships with relevant stakeholders in both home and host countries.Footnote 24 To deal effectively with these environmental pressures, multilatinas develop non-market resources and competences in order to reconcile them with the companies’ objectives. Sometimes the use of a specific kind of resource is not motivated by the desire to align a company’s strategy or structure with the environment but to align the external context with the firm’s objectives.Footnote 25 For instance, firms have reportedly used favours or political connections to improve their efficiency, unlock markets, influence regulation, handicap rivals and obtain competitive advantage at home and in foreign markets.Footnote 26

Non-market forces differ widely across countries.Footnote 27 The non-market environment in developed markets is characterised by highly structured and stable social, political and legal frameworks. These features reduce the uncertainty of firms operating in these environments because the rules of game are highly predictable. Non-market forces in emerging markets, on the other hand, are highly unstable. The uncertainty and unpredictability of these environments are especially critical because they significantly increase the difficulty of doing business.Footnote 28 For example, in China and Brazil trust and reciprocity are seen as the rules of game that support business activitiesFootnote 29 and they sometimes function as substitutes for strong formal institutions like legal systems or enforceable contracts.

Because multilatinas face volatile non-market environments at home, they have developed non-market resources and competences rooted in the informal and cultural-cognitive frameworks of their home countries to survive and prosper.Footnote 30 Non-market resources are tangible and intangible assets and competences that firms develop to shape the external forces that surround their business activities. As such these resources are highly context-specific because their development and use by multilatinas are the result of deep understanding of the non-market context at home and of a careful identification of the appropriate mechanisms to shape the social, political or legal pressures that act on them.Footnote 31

Multilatinas can benefit from the availability of non-market resources when investing abroad for two main reasons. First, theoretical and empirical analyses suggest that emerging multinationals use both legal (e.g. negotiation) and illegal (e.g. bribery) non-market resources to shape their home market environments. Developing an extraordinarily rich repertoire of context-specific, even illegal, resources means multilatinas have great internal flexibility and the capacity to adapt to the local environment. Competitors that come from less institutionally uncertain places do not need to develop the same level of sensitivity.

Second, firms have a natural drive to replicate abroad ways of doing business that are successful in their home markets. The ability to use non-market resources, together with this tendency, can give multilatinas one more competitive lever in other highly uncertain institutional contexts. The use of non-market resources abroad will therefore depend on the level of institutional uncertainty in the host country, turning non-market resources into a prospective competitive tool. A multilatina’s decision to enter a market with a high level of institutional uncertainty leverages the value of existing non-market resources, while entering a market with higher level of institutional certainty does not affect the value of any context-specific assets. In other words, multilatinas’ choice of host markets with higher institutional uncertainty is positively related to their use of non-market resources at home.

Although it might seem intuitive that strong regulatory mechanisms will reduce the feasibility of using some non-market resources (e.g. bribery) in markets with strong institutions, there is another important reason why multilatinas are deterred from using them when entering institutionally and economically developed markets and that is the need to gain legitimacy in the eyes of important stakeholders in the host market.Footnote 32 The use of resources that are considered inappropriate in these contexts reduces the chances of emerging multinationals being perceived as legitimate and reaching their long-term goals. Additionally, although non-market resources could probably be used everywhere (after all, corruption is present to a greater or lesser degree in all countries), multilatinas have to recognise the context-specific nature of non-market resources.

Measuring the where, when and how of internationalisation

We developed a questionnaire to test our observations about the behaviour of multilatinas (Table 11.1). This was an iterative process, from conception through development to discussions with executives and experts and vice versa. After identifying the key constructs for the study, validated measurements used in previous research were selected. When such measures were not available, a set of items were developed to captured the essence of the constructs. By following this procedure multi-item scales with content validity were created.Footnote 33

Table 11.1 Indicators of the measurement model

| Resources acquisition strategy: By investing in the host country (thereafter p1) your company was looking for (1= strongly disagree; 7 = strongly agree): | |

|---|---|

| Acq_1 | Acquire complementary physical, human and organisational resources to improve its competitive ability. |

| Acq_2 | Access quickly newly physical, human and organisational resources to compete at par with competitors. |

| Acq_3 | Acquire new physical, human and organisational resources to create advantage over competitors. |

| Resources exploitation strategy: Investing in p1 your company was looking for (1= strongly disagree; 7 = strongly agree): | |

|---|---|

| Exp_1 | By investing in p1 your company was looking for ways to compete in a similar way that it did at home. |

| Exp_2 | The physical, human and organisational resources that your company used to create advantages at (p1) were transferred from the country of origin to the host country. |

| Exp_3 | The physical, human and organisational resources that your company used to create advantages at (p1) were very similar to the resources used at home. |

| Technological resources: To what extent each of the following resources and competences was source of competitive advantage over competitors at your home country when your company decided to invest in (selected host country) (1 = not at all 7 = completely) | |

|---|---|

| Tec_1 | Advanced production technologies |

| Tec_2 | Own research and development (R&D) |

| Tec_3 | Patents obtained or acquired by your company |

| Context specific resources: To what extent each of the following resources and competences was source of competitive advantage over competitors in your home country when your company decided to invest in (p1) (1 = not at all 7 = completely) | |

|---|---|

| Loc_1 | Managerial knowledge of global markets |

| Loc_2 | Brands |

| Loc_3 | Supply chain networks developed by your company |

| Loc_4 | Low cost of labour |

| Loc_5 | Access to raw material related to natural resources |

| Loc_6 | Market knowledge |

| Loc_7 | Qualified labour in your home country |

| Institutional uncertainty at home: When your company decided to invest in (selected host country), in the home country (1= strongly disagree; 7 = strongly agree): | |

|---|---|

| IUH_1 | The government regulated the prices that affect the industry. |

| IUH_2 | The risk of imitation was high because of low protection of property rights in your country. |

| IUH_3 | The government regulated the ownership in your industry. |

| IUH_4 | The corruption in the public sector was low. |

| IUH_5 | The political instability was high. |

| IUH_6 | The laws of protection to property rights were applied rigorously. |

| IUH_7 | Was easy to get illegal copies of your products. |

| Institutional uncertainty in the host country: When your company decided to invest in (selected country), the government of (selected country) (1= strongly disagree; 7 = strongly agree): | |

|---|---|

| IDH_1 | ... required from foreign investors to transfer technology to national companies. |

| IDH_2 | ... limited the foreign ownership in the industry. |

| IDH_3 | ... regulated the prices that affect the industry. |

| IDH_4 | ....(selected country) was a country with high political stability. |

| Non-market resources: Do you think that investors in p1 (1= never; 7 = very frequently)...? | |

|---|---|

| NMR_1 | Ask favours from influential decision-makers in the host country to achieve the business objectives of their companies. |

| NMR_2 | Engage in negotiations with the regulatory agencies of (p1) to obtain favourable conditions for their business. |

| NMR_3 | Offer money to government employees or regulators to obtain favourable conditions for business. |

| NMR_4 | Offer gifts to influential decision-makers in p1 to obtain favourable conditions for business. |

| NMR_5 | Respect the legal norms of the host country despite the negative effect on the business goals of their company. |

| Speed of investment | (a) In which month and year did your company discover the investment opportunity in the host country? (b) In which month and year did your company start the legal procedures to initiate the investment in the host country? |

| Entry mode | Your company invested in (selected host country) through (a) acquisition; (b) joint venture with another company; (c) greenfield. |

| Market choice | Name of the host country in which your company invested. |

| Size | What was the number of employees of your company in the year of the investment decision. |

| Experience | Number of years since the first FDI of the company. |

When the first draft of the questionnaire was finalised, four experts in internationalisation and questionnaire development reviewed the draft.Footnote 34 After four rounds of discussions, a pilot study was performed, giving the questionnaire to a group of twenty-five executives enrolled in a top regional EMBA program. The draft was revised and updated at every stage of the development process.

Main variables

Our measurement model has thirty-four items that account for three exogenous and six endogenous constructs. All exogenous constructs are represented by multi-item measures: competitive advantage built on context-specific resources (seven items); competitive advantage built on technological resources (three items); and institutional uncertainty at home (seven items). Likewise, multi-item scales are applied for four endogenous constructs: resource exploitation strategy (three items); resource acquisition strategy (three items); and non-market resources (five items).

Host market choice is a special case of multi-item variable. Although research takes into account numerous aspects of a country (e.g. market size and competition), of specific interested is the institutional uncertainty of host markets. Managerial perceptions of institutional features determine whether or not a country is attractive to companies looking to exploit their technological resources or acquire new context-specific resources.Footnote 35 Items of institutional uncertainty at home and in the host country differ; while institutional uncertainty at home is related to threats to resources as a source of advantage, institutional uncertainty in the host country is related to the threats to the FDI process.

It is easier to achieve high levels of predictive validity by using multi-item measures.Footnote 36 For example, resource acquisition strategy gives firms speedy access to complementary resources to increase their competitive abilities.Footnote 37 In Table 11.1, these three elements are captured independently by Acq-1, Acq-2 and Acq-3, and jointly reflect the reliance of multilatinas on a resource acquisition strategy. The same reasons guided the development of the remaining constructs of interest. Two simple endogenous constructs (speed of investment and entry mode) are measured by a single item.

We use a measure based on the kinds of resources that constitute the base of competitive advantage to assess competitiveness derived from technological and context-specific resources. In this way, a common criticism of the resource-based view that resources are defined too broadly was overcome. Because of the scarcity of analysis to identify specific resources involved in the internationalisation of multilatinas,Footnote 38 a list of ten tangible and intangible resources was created based on previous research.Footnote 39 The logic behind this was to capture the degree to which multilatinas are involved in competition at home based on technological or context-specific resources (see Tec_1, Tec_2, Tec_3, Loc_1, Loc_2, Loc_3, Loc_4, Loc_5, Loc_6 and Loc_7 in Table 11.1).

Competitive strategies based on context-specific and technological resources are measured with a seven-point Likert scale. High scores for reliance on a specific resource suggest that it is perceived as a source of competitive advantage for the firm. Responses related to institutional uncertainty at home and in the host country are measured in the same way. High scores for a specific item indicate that managers perceived that item to be a strong indicator of institutional (un)certainty at home or in the host market.

Resource exploitation and resource acquisition strategies are also measured with seven-point Likert scales. Higher scores indicate greater reliance on a specific strategy. Information about non-market resources was collected in the same way. Items with higher scores are the most common non-market resources.

Speed of investment is measured by the number of days between two points in timeFootnote 40: the month and year in which the firm undertook legal steps related to investment in the host country minus the month and year of the discovery of the investment opportunity. The higher the value of this variable, the less speedy the internationalisation process is.

Entry mode is measured using a categorical variable indicating whether the firm entered a selected host market through an acquisition, a joint venture or a greenfield investment.

Control variables

Besides these main variables, information about three control variables that are widely recognised in the literature as relevant factors in the internationalisation process were incorporated: size of the firm, experience in foreign markets and the cultural distance between home and host markets.

There is empirical evidence that small firms are less prone to invest abroad through cooperative ventures than large firms because they are highly vulnerable to losing their technical core.Footnote 41 Besides entry mode, small and large firms also differ in speed of investment. For instance, large firms might have a resource base (e.g. knowledge, a management team experienced in international markets and new technologies) that facilitates faster decision-making.Footnote 42 In the same vein, firms with no international experience are more likely to choose entry modes with low or shared risks (e.g. joint venture). Conversely, firms with greater international experience might prefer acquisition or greenfield investment.Footnote 43 Experience in international markets also provides firms with superior knowledge that could accelerate decision-making and implementation during internationalisation.

Finally, cultural proximity is an important driver of market choice. When they choose familiar settings, organisations limit costs they would otherwise incur by moving into unfamiliar territory.Footnote 44 There appears to be a strong relationship between perceived risk and entry mode.Footnote 45 In fact, cultural distance between home and host market is a factor that increases perceived risk:Footnote 46 when distance increases, firms are more prone to choose entry modes that reduce perceived risk and slow down the decision-making investment process. For instance, when faced with high cultural distance firms might prefer to acquire targets with established routines and networks to reduce the risk of failure. Similarly, firms might prefer to form joint ventures to bypass the risk in the host market.Footnote 47 Alternatively, where there is low cultural distance firms might prefer greenfield investment to ease the design of global strategies and speed up the decision-making process. The survey items and the scale used to measure main and control variables are reported in Table 11.1. Chapter 12 presents the empirical results involving the variables described here.

We use structural equation modelling (SEM) to estimate structural coefficients that reflect relationships between the constructs described in Chapter 11 rather than between directly observable variables.Footnote 1 This technique offers two main advantages: first, SEM allows the simultaneous estimation of multiple dependent and independent variables. In particular, we analyse simultaneously the strategy followed by multilatinas (resource exploitation or resource acquisition), specific strategic decisions (where, when and how) and their reliance on non-market resources. Second, SEM allows us to use multiple indicators of latent constructs to improve the content validity of the scales. These advantages have been widely acknowledged in the literature on international business.Footnote 2

Common bias variance

As with all self-reported data, there is a risk of method variance in the use of SEM,Footnote 3 that is, variance attributable to the method of measurement rather than to the constructs themselves. The fact that we collected independent and dependent variables from the same executive could create bias in the respondent that might provide alternative explanations for the observed relationships among the constructs.Footnote 4 To guard against this risk we built two procedural remedies into the design of the questionnaire. First, we guaranteed the anonymity of the respondents; and second, the questionnaire was tested and adjusted to reduce the risk of bias of complicated syntax or misunderstanding.

We also conducted a Harmon one-factor test.Footnote 5 In this test all variables of interest are studied using the factor analysis method and the unrotated factor solution is examined to determine the number of factors necessary to account for the data variance. The basic assumption of this technique is that if a substantial amount of common method variance is present, either (a) a single factor will emerge from the factor analysis, or (b) one general factor will account for the majority of the covariance among the measures.Footnote 6 The results of this test show the presence of seven factors with eigenvalues greater than 1, explaining 90.3% of the variance, which implies that common method effects are not a likely contaminant of the results observed in our research.

Non-response bias

We used three tests to analyse if there were differences between multilatinas that participated in the study and those that did not. First, we compared sales and net income in 2011 and did not find significant differences between the two groups of firms in relation to either variable. Second, we tested for a relationship between the country of origin and the decision to participate in the study. A chi-square test showed that this relationship does not exist (X2 = 10.468; p = 0.234). We obtained a weaker result when we analysed the relationship between the economic sector of the firms and participation in the study but we rejected the existence of bias at the generally accepted level (X2 = 46.867; p = 0.087). This evidence shows that participation in the study was random and without a systematic bias.

The where, when and how model

Our baseline structural model is presented in Figure 12.1. According to this model, we expect that the interaction between context-specific resources and institutional uncertainty at home relate positively to a resource acquisition strategy. Similarly, a resource acquisition strategy is positively related to investment in countries with high institutional uncertainty and negatively related to speed of investment. We expect that companies that follow a resource acquisition strategy for internationalisation will choose acquisition as their preferred mode of entry as it will provide them with context-specific resources without the complications associated with joint ventures. According to the model, the interaction between institutional uncertainty at home and reliance on technological resources is positively related to a resource exploitation strategy. This strategy is negatively related to investment in countries with high institutional uncertainty and positively related to speed of investment. We expect multilatinas that follow a resource exploitation strategy to prefer greenfield as an entry mode but also to undertake acquisitions in order to speed up the internationalisation process. The data reveal the dominant rationale that multilatinas follow. Investment in countries with high institutional uncertainty is related to the use of non-market resources. Finally, and following previous studies, firm size and experience with foreign direct investment (FDI) are related to speed of investment and included as control variables. Cultural distance is related to the selection of countries with low institutional development as an additional control variable.

Data analysis

There were two stages to our data analysis. First, we analysed the structural relationships between the main constructs (except for entry mode) as described in Figure 12.1, using partial least squares path modelling (PLS-SEM). We then estimated a separate multinomial logistic model to study the relationship between firm strategies and entry mode. This model was needed because in its basic form PLS-SEM requires metric data and the use of dummy variables (such as entry modes) distorts the basis of the method.Footnote 7

PLS-SEM path modelling

PLS path modelling (PLS-SEM) is a variance-based structural equation technique that differs from covariance-based structural equation modelling (CB-SEM) in its objectives and method of estimation.Footnote 8 First, while PLS-SEM seeks to minimise the unexplained variance of constructs, CB-SEM is a confirmatory approach that aims to minimise the difference between the covariance matrix implied by the model and the sample covariance matrix. Second, while PLS-SEM makes estimations based on ordinary least squares (OLS) regressions, CB-SEM makes estimations based on maximum likelihood. Third, unlike CB-SEM, PLS-SEM does not use a specific factor analytic technique (e.g. exploratory or confirmatory) because PLS-SEM relies on predetermined networks of relationships between constructs as well as between constructs and their measures.Footnote 9 The choice of method depends on the characteristics of the research, especially the research aim (prediction or theory testing) and model complexity (e.g. number of relationships and recursive or non-recursive relationships).

We have theoretical and practical reasons to prefer PLS-SEM. At the theoretical level, our aim is to predict and explore a set of relationships between variables in an under-analysed context (multilatinas’ internationalisation strategies). Second, we analyse a complex set of relationships among variables in order to understand the strategic internationalisation decisions made by multilatinas. The nature of this research, added to the complexity of the model, make PLS-SEM a more suitable method than traditional CB-SEM methods, which are limited by theoretical and methodological assumptions.

There are also practical reasons for using PLS-SEM instead of CB-SEM. First, like many studies in social sciences, we have a relatively small sample (sixty-two observations). Although this sample size is way off the 150–400 range required to apply maximum likelihood estimation methods in a CB-SEM,Footnote 10 it is large enough to predict R2 between 0.25 and 0.50 with a statistical power of 80%.Footnote 11

Additional practical reasons to choose PLS are that we mix single and multi-item measures making no distributional assumptions, although in the data there are no major problems of skewedness or kurtosis. Simultaneously, recursive models (single loops) and reflective measures are used. Finally, no additional model specifications such as co-variation between error terms are applied. For these theoretical and practical reasons, PLS path modelling is the most appropriate technique for data analysis in our case.Footnote 12

Multinomial logit model

We used a multinomial logit model (MLM) to test our theoretical predictions about the relationship between multilatinas’ internationalisation strategies and their preferred entry mode. MLM is widely used because it lends itself to the analysis of dichotomous choices while testing the significance of each variable leading to the choice.Footnote 13

An MLM assumes independence from irrelevant alternatives (IIA), which means that the relative probability of choosing two alternatives does not depend on the availability or characteristics of other alternatives. This represents the main difference between MLM and multinomial probit models.Footnote 14 To test this assumption, we performed Hausman and Small-Hsiao tests, which support the distinction (independence) between the three entry modes and justify the use of MLM over a multinomial probit model.Footnote 15 In order to estimate the equation system required to calculate MLM, we arbitrarily made greenfield entry mode the reference option.Footnote 16 We then estimated the relative probability of a choice compared to the greenfield option. The parameter vectors, β, were estimated by maximum likelihood function using the STATA 12 software package.

Results

In this section, we present the results of the PLS-SEM model and discuss the characteristics of MLM. Table 12.1 displays the correlation matrix, which shows that some variables have correlations greater than 0.709; however, because these cases involve items measuring the same construct, it is not considered to be a problem. Table 12.2 contains a detailed description of the sample.

Table 12.1 Correlations

| Tec_1 | Tec_2 | Loc_1 | Loc_2 | Loc_3 | Loc_4 | Loc_5 | Acq_1 | Acq_2 | Acq_3 | Exp_1 | Exp_2 | Exp_3 | IUH_1 | IUH_2 | IUH_3 | NMR_1 | NMR_2 | NMR_3 | IDH_1 | IDH_2 | IDH_3 | Speed | Cul_Dis | ExpFDI | Size | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Tec_1 | 1 | |||||||||||||||||||||||||

| Tec_2 | 0.636** | 1 | ||||||||||||||||||||||||

| Loc_1 | 0.414** | 0.293* | 1 | |||||||||||||||||||||||

| Loc_2 | 0.431** | 0.386** | 0.076 | 1 | ||||||||||||||||||||||

| Loc_3 | 0.461** | 0.252* | 0.772** | 0.181 | 1 | |||||||||||||||||||||

| Loc_4 | 0.338** | 0.327** | 0.19 | –0.018 | 0.204 | 1 | ||||||||||||||||||||

| Loc_5 | 0.1630 | 0.251* | 0.034 | 0.064 | 0.048 | 0.667** | 1 | |||||||||||||||||||

| Acq_1 | 0.460** | 0.338** | 0.254* | 0.430** | 0.278* | 0.268* | 0.201 | 1 | ||||||||||||||||||

| Acq_2 | 0.403** | 0.144 | 0.16 | 0.321* | 0.211 | –0.025 | –0.121 | 0.168 | 1 | |||||||||||||||||

| Acq_3 | 0.457** | 0.281* | 0.121 | 0.421** | 0.169 | 0.175 | 0.130 | 0.739** | 0.294* | 1 | ||||||||||||||||

| Exp_1 | 0.127 | 0.155 | –0.002 | –0.010 | 0.011 | –0.098 | –0.029 | 0.040 | –0.044 | 0.007 | 1 | |||||||||||||||

| Exp_2 | 0.241 | 0.213 | 0.276* | –0.013 | 0.146 | 0.172 | 0.218 | 0.118 | –0.127 | –0.034 | 0.383** | 1 | ||||||||||||||

| Exp_3 | 0.142 | 0.201 | 0.147 | 0.008 | 0.104 | –0.148 | –0.169 | –0.016 | 0.157 | –0.076 | 0.741** | 0.218 | 1 | |||||||||||||

| IUH_1 | 0.204 | 0.056 | 0.103 | –0.123 | 0.025 | 0.038 | 0.008 | 0.042 | 0.050 | 0.005 | 0.194 | 0.134 | 0.328** | 1 | ||||||||||||

| IUH_2 | 0.106 | –0.092 | 0.017 | –0.106 | –0.064 | –0.030 | –0.081 | –0.001 | 0.009 | –0.002 | 0.146 | 0.230 | 0.246 | 0.683** | 1 | |||||||||||

| IUH_3 | 0.194 | 0.120 | 0.01 | 0.163 | –0.096 | 0.082 | 0.093 | 0.101 | 0.049 | 0.167 | 0.160 | 0.372** | 0.210 | 0.440** | 0.736** | 1 | ||||||||||

| NMR_1 | 0.038 | 0.029 | 0.187 | –0.082 | 0.102 | 0.030 | –0.043 | 0.317* | –0.019 | 0.120 | 0.275* | 0.160 | 0.259* | 0.209 | 0.286* | 0.237 | 1 | |||||||||

| NMR_2 | 0.274* | 0.230 | –0.016 | 0.140 | 0.043 | 0.127 | 0.126 | 0.274* | 0.183 | 0.256* | 0.353** | 0.078 | 0.274* | 0.191 | 0.056 | 0.050 | 0.243 | 1 | ||||||||

| NMR_3 | 0.013 | 0.034 | –0.06 | –0.070 | –0.058 | 0.199 | 0.114 | 0.159 | –0.035 | 0.090 | 0.110 | –0.073 | –0.036 | –0.018 | –0.069 | –0.095 | 0.355** | 0.629** | 1 | |||||||

| IDH_1 | 0.200 | 0.166 | 0.225 | 0.179 | 0.188 | 0.202 | 0.184 | 0.671** | –0.032 | 0.029 | 0.103 | 0.213 | 0.093 | 0.100 | 0.067 | 0.055 | 0.391** | 0.169 | 0.17 | 1 | ||||||

| IDH_2 | 0.065 | 0.109 | 0.23 | 0.077 | 0.185 | –0.010 | –0.022 | 0.292* | –0.031 | 0.072 | 0.273* | 0.072 | 0.279* | 0.086 | 0.085 | 0.092 | 0.606** | 0.100 | –0.032 | 0.386** | 1 | |||||

| IDH_3 | 0.293* | 0.279* | 0.145 | 0.198 | 0.176 | 0.038 | 0.072 | 0.195 | 0.076 | 0.153 | 0.241 | 0.146 | 0.256* | 0.271* | 0.198 | 0.156 | 0.233 | 0.656** | 0.161 | 0.143 | 0.359** | 1 | ||||

| Speed | 0.239 | 0.079 | 0.073 | 0.178 | 0.265* | 0.189 | 0.086 | 0.270* | 0.259* | 0.171 | –0.221 | –0.092 | –0.202 | 0.126 | 0.130 | 0.043 | 0.015 | 0.137 | 0.221 | 0.270* | 0.056 | 0.168 | 1 | |||

| Cul_Dis | 0.193 | 0.181 | –0.020 | 0.044 | 0.014 | 0.220 | 0.162 | 0.096 | 0.021 | 0.232 | –0.005 | 0.034 | –0.073 | 0.044 | –0.064 | 0.099 | –0.127 | 0.143 | 0.013 | –0.079 | 0.053 | 0.258* | 0.087 | 1 | ||

| ExpFDI | 0.352** | 0.278* | 0.086 | 0.21 | 0.090 | 0.223 | 0.091 | 0.101 | –0.026 | 0.046 | –0.046 | 0.196 | –0.022 | 0.090 | –0.056 | –0.043 | –0.08 | 0.227 | 0.219 | 0.072 | –0.101 | 0.139 | 0.274* | 0.086 | 1 | |

| Size | 0.131 | 0.159 | 0.106 | –0.068 | 0.105 | 0.301* | 0.083 | –0.012 | 0.008 | 0.097 | –0.110 | 0.006 | –0.178 | –0.267* | –0.325** | –0.198 | –0.022 | –0.017 | 0.073 | –0.151 | –0.014 | –0.094 | –0.212 | 0.094 | 0.195 | 1 |

| Variable | Mean | Std dev. | Min | Max |

|---|---|---|---|---|

| Tec_1 | 4.806452 | 1.772640 | 1 | 7 |

| Tec_2 | 5.322581 | 1.989927 | 1 | 7 |

| Loc_1 | 5.161290 | 1.538506 | 1 | 7 |

| Loc_2 | 4.822581 | 2.336624 | 1 | 7 |

| Loc_3 | 4.935484 | 1.871888 | 1 | 7 |

| Loc_4 | 3.290323 | 1.464186 | 1 | 6 |

| Loc_5 | 3.661290 | 2.318447 | 1 | 7 |

| Acq_1 | 3.612903 | 1.334963 | 1 | 6 |

| Acq_2 | 4.838710 | 1.839401 | 1 | 7 |

| Acq_3 | 4.725806 | 1.917729 | 1 | 7 |

| Exp_1 | 5.032258 | 1.773833 | 1 | 7 |

| Exp_2 | 4.516129 | 1.808377 | 1 | 7 |

| Exp_3 | 4.790323 | 1.527208 | 1 | 7 |

| IUH_1 | 3.000000 | 1.764867 | 1 | 7 |

| IUH_2 | 2.451613 | 1.522266 | 1 | 7 |

| IUH_3 | 2.500000 | 1.097688 | 1 | 5 |

| NMR_1 | 2.403226 | 1.419532 | 1 | 6 |

| NMR_2 | 3.887097 | 1.942660 | 1 | 7 |

| NMR_3 | 2.677419 | 1.565763 | 1 | 6 |

| IDH_1 | 2.177419 | 1.760441 | 1 | 7 |

| IDH_2 | 3.000000 | 2.268819 | 1 | 7 |

| IDH_3 | 4.064516 | 2.296619 | 1 | 7 |

| Speed | 5.161290 | 1.074191 | 3 | 8 |

| Cul_Dis | 2.720048 | 1.459097 | –0.5259 | 4.5985 |

| ExpFDI | 2.679097 | 0.837856 | 0 | 4.4188 |

| lnemplead | 8.535660 | 1.367483 | 5.2983 | 11.8845 |

Quality assessment of the PLS-SEM model

Following our analysis of the relationships between exogenous and endogenous constructs, we took a two-step analytical approach, assessing the outer model first, then the inner model.Footnote 17 The inner model specifies the relationships between unobserved or latent variables, while the outer model specifies relationships between a latent variable and its observed or manifested components. In CB-SEM these are referred to as measurement and structural models, respectively.Footnote 18 The reason for this two-step approach is that the quality of the measures (e.g. the reliability and validity of the measurement model) is required to guarantee that the results of the structural model can be used to draw valid conclusions.

We use a number of indicators to analyse the reliability, internal consistency, discriminant validity and predictive power of the model. To assess the quality of these measures and to estimate the relationships between latent constructs we use SmartPLS 2.0 software.Footnote 19 This has recently been used in several management, strategy and marketing studies that apply PLS-SEM.Footnote 20

Analysis of the indicators’ reliability and the internal consistency of the scales shows that ten indicators did not reach the threshold of loads and statistical significance. This first analytical stage allowed us to eliminate two items related to non-market resources, one item related to institutional uncertainty in the host country, four items related to institutional uncertainty at home, two items related to context-specific resources and one item related to technological resources. The process of item elimination at this stage did not affect content validity.

The reliability and internal consistency of the indicators was studied again for the variables retained in the analysis. All the scales showed internal consistency and all the indicators reached the loads and required threshold significance. The only exception was the scale of context-specific resources, which showed relatively low levels of internal consistency, with two items showing statistically non-significant loads.

Further analysis of this result revealed that context-specific resources could be divided into two groups: created and endowed location-specific resources.Footnote 21 Created resources require human intervention at the firm level; in our case, they relate to brands, networks, market knowledge or managerial teams. Endowed resources do not require any human intervention and include abundant low-cost labour and access to raw materials and other natural resources. Consequently, the original model was revised to accommodate these two groups. Because we had made no theoretical predictions about a finer taxonomy of resources, we performed an exploratory analysis to study the relation between endowed resources and the strategy multilatinas follow abroad. Specifically, we introduced a new interaction between endowed resources and institutional uncertainty at home to analyse the relationship with both a resources acquisition strategy and a resources exploitation strategy. The relationships of created resources were explored only for the case of resource acquisition because these resources are context-specific and their characteristics make them difficult to exploit abroad. The revised model is shown in Figure 12.2.

Figure 12.2 Revised model with endowed and created context-specific resources.

The internal reliability of the model was examined by inspecting the Cronbach’s alphas and composite reliability (CR). All constructs had alpha values above 0.6 except institutional uncertainty at home. The alpha value of this scale was α = 0.55, which is slightly lower than 0.6. However, the CR values of this scale (CR = 0.8987) show that the three items measured the perceived institutional uncertainty at home country sufficiently well. Similarly, the CR values of the rest of the constructs were between 0.7665 and 0.904, confidently surpassing the threshold of 0.7.Footnote 22 These results confirmed that the internal consistency of the applied scales was acceptable (see Table 12.3).

Table 12.3 Internal reliability of the structural model

| Scale | Composite reliability | Cronbach’s alpha |

|---|---|---|

| Acquisition strategy | 0.8173 | 0.6669 |

| Created resources | 0.7665 | 0.6105 |

| Cultural distance | 1 | 1 |

| Endowed resources | 0.9047 | 0.8002 |

| Experience of FDI | 1 | 1 |

| Exploitation strategy | 0.8408 | 0.7083 |

| Institutional development in host country | 0.7717 | 0.5576 |

| Institutional uncertainty in home country | 0.8987 | 0.8302 |

| Non-market resources | 0.8 | 0.6747 |

| Firm size | 1 | 1 |

| Speed of investment | 1 | 1 |

| Technological resources | 0.8995 | 0.7776 |

Indicator reliability was examined by measuring the outer loadings on all items in the model. The absolute standardised outer loadings ranged from 0.449 to 0.950 (see Table 12.4). There are four items with scores below 0.7: Xmin = 0.449 for the resource acquisition strategy; X min = 0.594 for the resource exploitation strategy; X min = 0.670 for institutional uncertainty at home, and Xmin = 0.661 for created resources. The items with low loads were not deleted because they form part of multi-item scales: their deletion would not improve the composite reliability of the scales but would harm the content validity of the measures. Generally, these results confirmed the reliability of the measurements used to study the internationalisation of multilatinas.

Table 12.4 Indicators of reliability of the structural model

| Constructs | Indicators | Outer weights | p-value |

|---|---|---|---|

| Acquisition strategy | Acq_1 | 0.919 | 0.000 |

| Acq_2 | 0.449 | 0.047 | |

| Acq_3 | 0.898 | 0.000 | |

| Exploitation strategy | Exp_1 | 0.915 | 0.000 |

| Exp_2 | 0.594 | 0.000 | |

| Exp_3 | 0.863 | 0.000 | |

| Institutional development in host market | IDH_1 | 0.670 | 0.000 |

| IDH_2 | 0.783 | 0.000 | |

| IDH_3 | 0.729 | 0.000 | |

| Institutional uncertainty in home country | IUH_1 | 0.813 | 0.000 |

| IUH_2 | 0.925 | 0.000 | |

| IUH_3 | 0.853 | 0.000 | |

| Created resources | Loc_1 | 0.661 | 0.003 |

| Loc_2 | 0.761 | 0.000 | |

| Loc_3 | 0.745 | 0.001 | |

| Endowed resources | Loc_4 | 0.950 | 0.000 |

| Loc_5 | 0.866 | 0.000 | |

| Non-market resources | NMR_1 | 0.802 | 0.000 |

| NMR_2 | 0.762 | 0.003 | |

| NMR_3 | 0.702 | 0.002 | |

| Technological resources | Tec_1 | 0.890 | 0.000 |

| Tec_2 | 0.918 | 0.000 | |

| Speed | Speed (Ln) | 1.000 | 1.000 |

| Firm size | No. Emplead (Ln) | 1.000 | 1.000 |

| Cultural distance | Cul_Dis (Ln) | 1.000 | 1.000 |

| Experience of FDI | ExpFDI (Ln) | 1.000 | 1.000 |

We also assessed convergent validity by measuring the average variance extracted (AVE).Footnote 23 All constructs show AVE values greater than the 0.5 threshold (AVEmin = 0.52 for competition based on created resources). These results indicate that all constructs, on average, explain more than half of the variance of their indicators. This implies the existence of sufficient convergent validity of all the measures (see Table 12.5).

Table 12.5 Convergent validity and predictive power of the structural model

| Scale | AVEa | R square |

|---|---|---|

| Acquisition strategy | 0.6175 | 0.3342 |

| Created resources | 0.5234 | |

| Cultural distance | 1 | |

| Endowed resources | 0.8263 | |

| Experience of FDI | 1 | |

| Exploitation strategy | 0.645 | 0.3533 |

| Institutional development in host country | 0.5308 | 0.2438 |

| Institutional uncertainty in home country | 0.7479 | |

| Non-market resources | 0.5722 | 0.3541 |

| Firm size | 1 | |

| Speed of investment | 1 | 0.2989 |

| Technological resources | 0.8174 |

a Average variance extracted.

Table 12.5 also contains details about the predictive power of the model. This aspect is analysed using R2. Using the PLS Algorithm function in SmartPLS 2.0, we computed the R2 statistics of the five endogenous constructs in the model. The R2 values of resource exploitation strategy, resource acquisition strategy, institutional uncertainty in the host country, non-market resources and speed of investment were 0.35, 0.33, 0.24, 0.35 and 0.30, respectively These values are greater than the acceptable threshold of 0.1.Footnote 24

Finally, we examined discriminant validity using the square root of AVE and cross-loadings. As shown in Table 12.6, the values of the square root of AVE for each construct are greater than the highest correlation between that construct and the others.Footnote 25 Furthermore, we assessed discriminant validity by comparing the loading values of each indicator with the cross-loadings with other reflective indicators. The indicator loadings were all higher than the cross-loadings, suggesting satisfactory discriminant validity in the model.

Table 12.6 Path coefficients in the structural model

| Variables | Acquisition strategy | Exploitation strategy | Institutional uncertainty in host country | Speed of investment | Non-market resources |

|---|---|---|---|---|---|

| Created resources | 0.4732*** (4.4262) | ||||

| Created resources x Institutional uncertainty at home | –0.1789 (0.7573) | ||||

| Endowed resources x Institutional uncertainty in home country | –0.0942 (0.5652) | 0.2355** (2.3089) | |||

| Technological resources x Institutional uncertainty in home country | 0.285** (2.447) | ||||

| Acquisition strategy | 0.3394*** (2.9171) | 0.2781** (1.9942) | |||

| Cultural distance | 0.0862 (0.6518) | ||||

| Exploitation strategy | 0.3111*** (2.7862) | –0.2779** (2.3698) | |||

| Size | –0.098 (0.9234) | –0.3208*** (3.3804) | |||

| Experience of FDI | 0.3256*** (3.097) | ||||

| Institutional uncertainty in host country | 0.5951*** (10.5661) | ||||

Testing predictions of where and when

We introduced the interaction between institutional uncertainty at home and technological, created and endowed resources in PLS-SEM as a product term.Footnote 26 To test our predictions, we examined the significance of the path coefficient estimates for the twelve paths in the model, including three related to control variables and two to exploratory relationships. We use a bootstrap technique, which produces more reasonable standard error estimatesFootnote 27 and we performed 5,000 re-samplings with sixty-two observations in each. Table 12.6 contains the estimates of the path coefficients of the structural model.

Figure 12.3 contains the results of the hypotheses testing. The path coefficient from the product term of technological resources and institutional uncertainty at home to resources exploitation strategy is 0.285 and it is statistically significant at standard levels (t = 2.447, p < 0.05). This supports our prediction that multilatinas that rely on technological resources in their home markets, and perceive high institutional uncertainty at home, follow a resource exploitation strategy for internationalisation (see Chapter 11). The path coefficients from the resource exploitation strategy to the speed of investment and institutional uncertainty in the host country are −0.2779 (t = 2.3698; p < 0.05) and 0.3111 (t = 2.7862; p < 0.05), respectively. These results show that multilatinas that invest abroad to exploit their resources spend less time between discovering an investment opportunity and beginning legal procedures to invest. Also, these multilatinas invest in countries that have high institutional uncertainty. This result is consistent with the conjecture that a resource exploitation strategy is positively related to investments in countries with low institutional uncertainty, speedy FDI and the choice of acquisition as an entry mode (see Chapter 11). This evidence also shows that when following a resource exploitation strategy, multilatinas are driven more by available opportunities abroad and less by the desire to keep resources better protected in a more predictable institutional environment. This means that the conjecture related to the choice of host markets does not find empirical support, raising important questions about the rationale behind the internationalisation of multilatinas relying on technological resources. Certainly, the nature of these resources and (above all) their redeployability make them less vulnerable to institutional threats, which opens many host market opportunities for multilatinas that follow this particular internationalisation approach.

Figure 12.3 Prediction testing and statistical significance.

The path coefficient from the resource acquisition strategy to the speed of investment and the selection of countries with high institutional uncertainty are 0.2781 (t = 1.9942; p < 0.05) and 0.3394 (t = 2.9171; p < 0.05), respectively. This result supports the conjecture, that a resource acquisition strategy is positively related to the selection of countries with high levels of institutional uncertainty, negatively related to speed of FDI and positively related to the acquisition entry mode (see Chapter 11).

The path coefficient from institutional uncertainty in the host country to the use of non-market resources is 0.5951 (t = 10.5661; p < 0.000). This result supports the idea that multilatinas’ choice of host markets with higher institutional uncertainty is positively related to their use of non-market resources at home (see Chapter 11).

To test the robustness of these results, we also estimated the model using POLCON,Footnote 28 an objective measure of political constraints to political changes (or limitations to political discretion) based on the number and preferences of political actors with veto power within the political structure of a country. We did not find a statistically significant relationship between this new objective proxy of institutional quality and the strategies of resource exploitation and acquisition. Neither did we find a statistically significant relationship between this variable and the use of non-market resources. These results also suggest that there is no correlation between the objective (POLCON) and subjective (self-reported perceptions of top managers in multilatinas) measures of institutional uncertainty. The lack of correlation between objective and subjective measures of institutional and environmental variables is not new in the field of social studies.Footnote 29 In our view, the result also corroborates the appropriateness of using managerial cognitive representations as measures of institutional uncertainty to analyse the internationalisation strategies of multilatinas.

We also tested the emergent relations between variables. The coefficient path from the product term of endowed resources and institutional uncertainty at home is −0.0942 (t = 0.5652; p < 0.574) to resource acquisition strategy and 0.2355 (t = 2.3089, p < 0.05) to resource exploitation strategy. These findings suggest that multilatinas that compete on the basis of endowed resources in markets with high institutional uncertainty invest abroad following the logic of resource exploitation. Apparently, the fungibility of endowed natural resources creates opportunities for companies to undertake internationalisation strategies that rely on resource exploitation.

On the other hand, the coefficient path from the product term of created context-specific resources and institutional uncertainty at home to resource acquisition strategy is −0.1789 (t = 0.7573; p < 0.452), implying a statistically non-significant relationship between these constructs. However, the coefficient from created resources to resource acquisition strategy is 0.4732 (t = 4.4262; p < 0.000), suggesting that multilatinas that build their advantage on created context-specific resources go abroad to acquire new resources irrespective of the uncertainty of the institutional environment at home. The statistically significant relationships are shown graphically in Figure 12.4.

Figure 12.4 Graphical analysis of MLM for entry mode (full sample, resource exploitation strategy).

Considering control variables, firm size shows a positive relationship with speed of investment (β = −0.3208; t = 3.3804; p < 0.001). In other words, larger multilatinas are quicker to invest abroad. The experience of multilatinas on international markets, however, shows a negative relationship with speed of investment. For our sample, greater international experience (more years) correlates with an increase in the time (number of days) between the discovery of an investment opportunity and investment abroad (β = 0.3256; t = 3.097; p < 0.005). Cultural distance does not show any relationship to the selection of a host market (β = 0.0862; t = 0.6518; p < 0.517).

The final finding might seem surprising because the literature recognises cultural proximity as an important driver of market choice. For instance, Gomes and Ramaswamy assert that by choosing familiar settings organisations limit the costs they would otherwise incur if they move into unfamiliar territories.Footnote 30 The absence of a statistically significant relationship could occur for at least two reasons. First, the dimensions of cultural distance that we use in our research, following HofstedeFootnote 31 and Kogut and Singh,Footnote 32 sometimes have the opposite effect on the FDI process. For instance, Tang shows that some dimensions used by Hofstede, such as differences in individualism, encourage FDI flows between two countries while other dimensions, such as differences in power distance, impede bilateral FDI flows.Footnote 33 Because we focus on the aggregate cultural distance such effects are not accounted for and their opposite effects cancel out. Second, it is possible that market choice is influenced by aspects beyond cultural dissimilarities. For instance, the literature states that geographical distance and differences in administrative and economic frameworks are more significant than cultural dissimilarity for the success of international market entry.Footnote 34 To test for this possibility we substituted cultural distance by the CAGE distance, accounting for the cultural (C), administrative (A), geographic (G) and economic (E) distances between each pair of home-host countries, and re-ran the model.

The result of this estimation was a positive relation between the CAGE distance and the choice of host markets with high perceived institutional uncertainty. That is, the perception of high institutional uncertainty in the host market relates positively to geographical distance, cultural and administrative differences and the absence of economic or commercial links between the home and host countries. The strongest effect is exhibited by geographical distance, which is at the core of the powerful gravity models of cross-country trade flows.Footnote 35 When we inspected the joint effect of the cultural, administrative and economic factors, we confirmed the initial result of no correlation between these distances and the perceived institutional uncertainty of the host market.

Testing predictions of how: a multinomial logit model

To analyse the relationship between multilatinas’ internationalisation strategies in foreign markets and choice of entry mode, we computed a single score for each latent construct – one for the resource acquisition strategy and one for the exploitation strategy. Because both strategies are measured with three indicators we estimated an unweighted average of the original variables that define each one.Footnote 36 There are several reasons why this is a suitable approach. First, because the indicator variables are measured with the same continuous scale and are highly correlated, their use could create collinearity problems in the regression analysis. Second, the use of highly correlated indicators does not increase the variance of the dependent variable. Finally, this approach has been used in strategic management research.Footnote 37

In the MLM the dependent variable is measured by a nominal variable that has a value of 1 = greenfield entry mode, 2 = acquisition entry mode, and 3 = joint venture entry mode. As well as the independent variables resource acquisition and exploitation strategies, we use three control variables: firm size, firm experience in foreign markets and cultural distance between home and host country. The results of the model estimation are shown in Table 12.7.

Table 12.7 Multinomial logit model of entry mode

| Variable | Acquisition entry mode | Joint venture entry mode |

|---|---|---|

| Cultural distance | 0.268 | –0.225 |

| (0.267) | (0.222) | |

| Experience of FDI | 0.393 | 0.232 |

| (0.429) | (0.382) | |

| Size (Ln employees) | 0.345 | –0.081 |

| (0.261) | (–0.249) | |

| Acquisition strategy | –0.119 | –0.247 |

| (0.268) | (0.50) | |

| Exploitation strategy | 0.568** | 0.241 |

| (0.275) | (0.246) | |

| Log-likelihood | – 60.842 | |

| Nagelkerke’s pseudo R2 | 0.235 | |

Note: N = 62; standard errors in parentheses; ** p < 0.05.

The results of the MLM (Table 12.7) do not support the suggested positive relationship between exploitation strategy and choice of greenfield entry mode. Also, the results do not show a statistically significant relationship between resource exploitation strategy and joint venture as entry mode. The results show that multilatinas that follow a resource exploitation strategy are more likely to select acquisition as an entry mode rather than greenfield (β =0.647; p < 0.05). In our sample, multilatinas do not exhibit a preferred entry mode when they follow a strategy of resource acquisition, as the coefficients show no statistical significance at the accepted levels. The control variables are also non-significant.

In Table 12.7, Nagelkerke’s pseudo R2 is reported as a goodness-of-fit measure, reflecting the cumulative strength of the model. It can be interpreted similarly to the R2 in linear regression and as such it provides an estimate of the model’s substantive significance.Footnote 38 In general, pseudo R2 such as Nagelkerke’s R2 tend to be lower than real R2 values, where values between 0.2 and 0.4 are considered acceptable.Footnote 39 In our case, Nagelkerke’s Pseudo R2 is 0.235, suggesting a moderate relationship between the predictors and the dependent variable.

Figure 12.4 contains a more detailed analysis of these results. A close look at graph 4a in Figure 12.4 shows that reliance on the resource exploitation strategy increases the probability of choosing acquisition as an entry mode. Similarly, graph 4b shows that reliance on exploitation strategy reduces the likelihood of choosing greenfield entry mode. Finally, graph 4c shows that reliance on a resource exploitation strategy is not related to changes in the likelihood of choosing a joint venture as entry mode. Graph 4d presents the marginal effect of the variables on each of the three entry modes, greenfield, acquisition and joint venture. If the marginal effects are small, the entry modes will be bundled very close together. The greater the effect of a particular entry mode, the farther the option will be from the origin of the coordinate system.Footnote 40 In our case, graph 4d quantifies changes in the likelihood of choosing a specific entry mode if the measure of resource exploitation strategy changes by one standard deviation. Specifically, the graph shows that increasing the measure of exploitation strategy by one standard deviation increases the likelihood of choosing acquisition as an entry mode by 11%, while the likelihood of choosing greenfield falls by 10%, and joint venture by 1%.

The MLM results, on the other hand, do not offer evidence for a statistically significant relationship between resource acquisition strategy and any kind of entry mode. This finding suggests that there is no preference for acquisition over other entry modes.

Following this line of argument, we investigated statistically the interaction effect of business group affiliation on the relation between a resources acquisition strategy and entry mode. Business groups own 53% of the firms included in our sample. The results of the MLM, including the moderator effect, are summarised in Table 12.8. The interaction effect of a resource acquisition strategy and belonging to a business group is negatively and significantly correlated to acquisition entry mode (β = −1.930, p < 0.05) and joint venture entry mode (β = −1.746, p < 0.05). These findings show a strong preference for greenfield entry over acquisition and joint venture among multilatinas that invest abroad following a resources acquisition strategy. Nagelkerke’s Pseudo R2 is 0.375, which shows a moderate relationship between the independent and dependent variables.

Table 12.8 MLM of entry mode with business group effect

| Variable | Acquisition entry mode | Joint venture entry mode |

|---|---|---|

| Cultural distance | 0.271 | –0.280 |

| (0.295) | (0.241) | |

| Experience of FDI | 0.557 | 0.358 |

| (0.471) | (0.412) | |

| Size (Ln employees) | 0.332 | –0.089 |

| (0.295) | (0.287) | |

| Acquisition strategy | 0.526 | 0.369 |

| (0.394) | (0.341) | |

| Exploitation strategy | 0.535* | 0.207 |

| (0.305) | (0.262) | |

| Business group | 6.53** | 6.41** |

| (2.52) | (2.618) | |

| Resource acquisition strategy x Business group | –1.563** | –1.457** |

| (0.640) | (0.580) | |

| Log-likelihood | –55.537 | |

| Nagelkerke’s pseudo R2 | 0.375 | |

Note: N = 62; standard error in parentheses; * p < 0.1; ** p < 0.05.

We further explore the statistical significance of the relationship between greenfield entry mode and the interaction term between a resource acquisition strategy and business group affiliation following the procedure described in this chapter.Footnote 41 We converted the model into a dichotomous model (greenfield = 1; 0 = otherwise) and computed the algorithm of Norton, Wang and Ai.Footnote 42 This algorithm computes the correct marginal effect of a change in the predicted probability that y = 1 (entry mode = greenfield) for a change in the independent variables involved in the interaction. We also included the control variables.

The empirical results confirm a statistically significant relationship between greenfield entry mode and the interaction term of resource acquisition strategy and business group affiliation. The x-axis of graph 5a in Figure 12.5 shows the predicted probabilities and the y-axis the interaction effect. Figure 12.5 also shows the marginal effect computed by the linear method and the corrected interaction effect computed by the applied algorithm.

Figure 12.5 Greenfield entry mode, resource acquisition strategy and business group affiliation.

Our evidence implies that multilatinas that follow a resources acquisition strategy and are affiliated to a business group are more likely to use greenfield entry mode than acquisition or joint venture. The selection of greenfield could be feasible in these cases owing to the longer timespan over which resource acquisition strategy develops. Also, business groups provide their affiliates with the tangible and intangible resources needed to internationalise. In our sample, the preference for greenfield is reinforced by the fact that multilatinas invest in their natural markets at short geographical distances,Footnote 43 environments in which context-specific resources share a substantial degree of similarity.Footnote 44 As a result of investment in proximate markets, there might not be radical differences in the characteristics of the resources that firms or their business groups control at home and the resources that multilatinas can acquire abroad.Footnote 45

If they have the time and the resources, multilatinas might actually prefer to spend time and effort building a new set of tangible and/or intangible assets in the host country instead of buying them. Acquisition means that multilatinas frequently have to buy more resources than they require. This makes internal development more attractive than buying or sharing resources with partners abroad. Internal development assures that firms’ resources fit their own needs perfectly. This is especially relevant when a greenfield investment is an extension of a previous entry in the same market. In our sample, the FDI 72% of the companies were undertaking was reinvestment in the same country. Internal development of resources also allows firms to consolidate and optimise the investments associated with their international strategies.

Figure 12.6 shows a detailed graphical analysis of entry modes for multilatinas following a resource acquisition strategy of internationalisation. Graph 6a implies that an increasing reliance on resource acquisition reduces the likelihood that multilatinas owned by business groups will opt for acquisition as an entry mode. At the same time, increasing reliance on resource acquisition increases the likelihood that stand-alone firms will enter through acquisitions. Stand-alone firms have fewer restrictions and fewer opportunities to create synergies across foreign markets than firms affiliated to business groups. The strategic decisions about internationalisation made by stand-alone multilatinas are not under the control of a higher-order entity that shapes the decision-making process, but neither can they rely on a large pool of internal resources. As graph 6b in Figure 12.6 shows, the more focused on a resource acquisition strategy stand-alone multilatinas become, the less likely they are to use a greenfield entry mode. For firms affiliated to business groups, increased focus on resource acquisition is positively related to an increase in the likelihood of using greenfield entry mode. The absence of economies of scope or synergies that characterise stand-alone multilatinas could explain why this relationship is reversed in their case. Finally, graph 6d illustrates changes in the likelihood of choosing a specific entry mode if the interaction of a resource acquisition strategy and business group affiliation changes by one standard deviation. The graph shows that in this case the likelihood of choosing a greenfield entry mode increases by 75%, the likelihood of choosing acquisition diminishes by 39% and the likelihood of choosing joint venture diminishes by 38%.

Figure 12.6 Graphical analysis of the MLM estimation for entry mode and belonging to a business group (resource acquisition strategy, full sample).

In sum, there seems to be a pattern of internationalisation of multilatinas that is shaped by the nature of their organisational assets as well as the conditions of the home and host countries’ institutional environment. This pattern is consistent with ideas and predictions offered by the existing literature on international business but it has never been characterised as fully as we have done in this book. Chapter 13 examines the lessons that emerge from the careful data analysis presented so far.

The natures of the resources that make multilatinas successful at home affect the approach these companies follow in their internationalisation strategies. The fact that multilatinas come from institutionally uncertain environments affects their behaviour abroad.

Multilatinas and resource exploitation strategy

Multilatinas that compete on the basis of their technological resources invest abroad to exploit those resources when managers perceive high institutional uncertainty at home. In particular, multilatinas that have advanced production and R&D technologies at home and perceive high risks of imitation, governmental intervention in prices and threats to ownership rights invest abroad to exploit the technologies that have been successful at home. In this way these multilatinas use their technological resources abroad to create similar advantages to those that they had at home and diversify the risk related to domestic institutional uncertainty.

For example, economic and political uncertainty led many Brazilian companies to increase their investments abroad during the early 2000s.Footnote 1 One of these firms was Marcopolo, the bus body builder, which opened high added value operations in several locations around the world, including China and India. The purpose of these investments was to compensate for the loss of competitiveness of the Brazilian economy and the associated threats of political and electoral crises.Footnote 2 Investments in foreign markets allowed Marcopolo to exploit its technological knowledge by building new production facilities, gaining access to new markets while increasing its size.Footnote 3