I

The performance and dynamics of the banking sector during the Great Depression have attracted increasing attention from financial historians. While a substantial body of research has examined commercial banks’ performance within national economies and domestic financial systems,Footnote 1 another strand of the literature has focused on their involvement in international finance, their exposure to cross-border risks, and their role in propagating global instability (Accominotti Reference ACCOMINOTTI2012, Reference ACCOMINOTTI2019; Postel‐Vinay and Collet Reference POSTEL‐VINAY and COLLET2024). Positioned at the crossroads of local credit structures and global financial markets, commercial banks not only facilitated the international circulation of capital and trade; they also became, once the crisis erupted, key channels for the transmission and amplification of economic disruptions worldwide.

The interconnections between national banking systems and global financial networks became most apparent in 1931. When Austria’s Creditanstalt collapsed in May, banking panics spread to Germany and Hungary, thus intensifying the pressure that was already undermining financial sectors in Italy, the Netherlands and Spain. This cascade of events pushed European banking systems to the brink of collapse and contributed to deepening the ongoing recession (Wicker Reference WICKER1996; James Reference JAMES2001; Feinstein et al. Reference FEINSTEIN1995). Moreover, banking distress became intertwined with monetary instability, which triggered currency crises and prompted the introduction of capital controls (Bernanke and James Reference BERNANKE, JAMES and Hubbard1991; Albers Reference ALBERS2020). This precipitated the breakdown of the international monetary order, as one country after another was forced to abandon the gold standard – beginning with Germany in July, followed by the United Kingdom in September, and many others afterwards (Eichengreen Reference EICHENGREEN1996; Accominotti Reference ACCOMINOTTI, Battilossi, Cassis and Yago2020). The global financial crisis of 1931 thus brought international capital movements to an abrupt halt; it marked the end of the expansionary era and ushered in what has been termed the ‘mother of all sudden stops’ (Accominotti and Eichengreen Reference ACCOMINOTTI and EICHENGREEN2016).

This article examines the nexus between the European banking crises of 1931 and Argentina’s economic developments during the Great Depression, a relationship that has been largely neglected so far. Argentina offers a valuable case to study the transmission of global banking shocks to the periphery, for several reasons. By the late 1920s, the country occupied a distinctive position: an emerging economy whose financial system displayed levels of development comparable to, and in some respects exceeding, those of several European nations (Diaz-Alejandro Reference DIAZ-ALEJANDRO and Thorp1984; Marichal Reference MARICHAL2022). On the eve of the Great Depression, Argentina’s commercial banks held greater total assets and higher deposits per capita than those in the Netherlands, Belgium, Germany and Hungary – all countries that had experienced severe banking distress and contagion.Footnote 2 Argentina was also a main destination for European capital; it was highly integrated into international financial markets and deeply intertwined with global trade and banking networks (Stone Reference STONE1968, Reference STONE1999; Edelstein Reference EDELSTEIN1982). Finally, the prominence of foreign banks within its domestic system – which were remarkable both for their scale and for the diversity of nationalities they represented, including institutions from several countries engulfed by the 1931 crisis (Jones Reference JONES1993; Marichal Reference MARICHAL2024) – offers a unique lens for tracing and assessing the propagation of banking turmoil across borders, and how this redefined financial linkages between countries at the core and on the periphery.Footnote 3

To examine these issues, this study focuses on the presence and operations of European banks in Argentina. Rather than looking at the transmission of the crisis through global markets and macroeconomic linkages, it analyses how financial distress in Europe was mediated through transnational organizations. Headquartered in Europe but deeply embedded in Argentina’s financial system via its overseas affiliates, these institutions were important intermediaries in trade and capital flows that connected Argentine finance to the main money markets of London, Paris, Berlin and beyond.Footnote 4 The study draws on a diverse body of sources: annual balance sheets published in The Bankers’ Almanac, monthly reports from the Monitor de Sociedades Anónimas and the Boletín Oficial de la República Argentina, and qualitative archival materials from the Bank of London and South America and the Banque Française et Italienne pour l’Amérique du Sud, held respectively in London and Milan. Additional documentation from the Bank for International Settlements (BIS) and the Deutsche Überseeische Bank complements this evidence, to allow a detailed reconstruction of how European banks in Argentina experienced and responded to the shocks of 1931. While the primary focus is on European institutions, the situation of North American and Canadian banks is also considered; this provides a suitable comparative benchmark, given their different organizational structures and the distinct financial conditions prevailing in their home countries.

The article contributes to the historiography of interwar banking and the Great Depression in Argentina. To date, the literature has largely examined the Argentine banking system in aggregate terms, focusing on its overall stability, deposit and lending trends, and the performance of domestic and foreign institutions, as well as the role of the Banco de la Nación Argentina (BNA) and its lender-of-last-resort policies (see Della Paolera and Taylor Reference DELLA PAOLERA and TAYLOR2001, Reference DELLA PAOLERA and TAYLOR2012). Other studies have provided detailed cases and analyses of individual institutions in distress – such as the Banco Español del Río de la Plata and the Banco Francés del Río de la Plata – or explored the internal political and regulatory dynamics of specific banks (see Regalsky Reference REGALSKY2010, Reference REGALSKY, Rougier and Sember2018, Reference REGALSKY, Regalsky and Rougier2023; Iglesias Reference IGLESIAS2012; Regalsky and Iglesias Reference REGALSKY and IGLESIAS2015, Reference REGALSKY and IGLESIAS2019; Sember Reference SEMBER, Rougier and Sember2018; Newland Reference NEWLAND2020). These works share a predominant focus on domestic developments, with limited consideration of the contemporaneous banking upheavals taking place overseas. This article takes a different approach, and assesses domestic economic dynamics in Argentina in interconnection with banking developments in European financial centres. This perspective is particularly relevant, given that financial shocks and policy shifts in core countries have historically affected trajectories at the periphery. The focus on European banks complements and extends recent work by Alvarez and Nodari (2025), which highlights that variability in bank-level distress in Argentina was closely linked to episodes of international financial instability.

The condition of the Argentine banking system during the Great Depression was strongly influenced by major institutional reforms and financial arrangements. In particular, the creation of the Central Bank in 1935, and the bank rescue programme implemented through the Instituto Movilizador de Inversiones Bancarias (IMIB), have been widely associated with the need to restructure and clean up the balance sheet of the BNA, whose lending and rediscount practices had seemingly heightened systemic fragility (see, for instance, Della Paolera and Taylor Reference DELLA PAOLERA and TAYLOR2001, ch. 8; Della Paolera and Taylor Reference DELLA PAOLERA and TAYLOR2003). In this context, domestic banks have often been portrayed as a primary source of risk and vulnerability; in contrast to foreign banks, which appeared more stable due to their access to funding from headquarters, stronger capitalization levels and more conservative loan portfolios (Della Paolera and Taylor Reference DELLA PAOLERA and TAYLOR2001). In this article, we challenge that interpretation by demonstrating that the problems in Europe triggered significant liquidity issues for the Argentine affiliates of foreign banks; in some cases, they required financial support from local monetary authorities. Furthermore, we argue that the European banking crises of 1931 led to substantial changes in the lending strategies of foreign banks’ Argentine affiliates – an adjustment that created an enduring recessionary pressure on the domestic economy, which persisted throughout the Great Depression of the 1930s.

The remainder of the article is organized as follows. The next section outlines the historical context of the Argentine banking sector, and foreign banks’ position and role during the Great Depression. Section III examines the condition of the European head offices in the aftermath of the 1931 banking crisis, while Section IV turns to their Argentine affiliates. Section V analyses the banks’ reactions and responses to the international crisis, the resulting adjustments in their balance sheets, and their recourse to financial assistance from national monetary authorities. Section VI explores the medium-term consequences of these changes, particularly in the cash-holding and lending strategies of European banks, as well as other potential factors that may have shaped their portfolio management decisions. The article concludes by discussing the broader implications of the main findings for Argentina’s interwar banking history, and for the historiography of domestic financial and monetary instability during the Great Depression.

II

The Great Depression reached Argentina in the late 1920s, with recovery beginning in 1932 and the economy returning to its 1929 level by the mid 1930s. Despite the country’s deep integration into the global economy, the economic downturn was relatively mild and short-lived by both Latin American and international standards.Footnote 5 Between 1929 and 1932, domestic real output contracted by about 14 per cent; compared with, for instance, 30 per cent in Chile over the same years, or 28.5 per cent in the United States from 1929 to 1933 (Della Paolera and Taylor Reference DELLA PAOLERA and TAYLOR1999; Gerchunoff and Llach Reference GERCHUNOFF and LLACH2018). Deflation, unemployment and sharp declines in manufacturing, investment and consumption – the hallmarks of the Great Depression – were less severe in Argentina, and by 1933 the country had already avoided the most devastating consequences of the external shocks and the global crisis in international trade and capital markets.

Naturally, Argentina’s banking sector was closely tied to its economic trajectory and crisis dynamics during this period. The rapid expansion of deposits and lending that had characterized the system since 1925 came to a halt at the end of the decade, and began to contract as the country was plunged into the Great Depression. In 1930, when the domestic economy entered recession, bank lending continued to grow despite the decline in deposits that had already started in 1929. Between 1931 and 1932, with Argentina’s GDP falling by a cumulative 10 per cent, both deposits and lending moved in the same direction, contracting by 11 and 10 per cent, respectively. These figures continued to decline, though more moderately, over the following two years, even as economic activity began to recover. In the context of global depression, shrinking international trade, domestic deflation and mounting difficulties in the agricultural sector, the normal funding and lending operations of banks were severely affected. Moreover, the banking system itself came under considerable strain, which prompted the monetary authorities to use rediscounts and other forms of financial assistance to safeguard stability (Prados Arrarte Reference PRADOS ARRARTE1944).

Yet, the severity and underpinnings of banking difficulties remain a matter of debate. Although according to Raúl Prebisch – Argentina’s most influential economist and policymaker of the 1930s – the banking system stood on the verge of collapse (Prebisch Reference PREBISCH1991), latter historiography has offered more nuanced interpretations. Diaz-Alejandro (Reference DIAZ-ALEJANDRO and Thorp1984) and Bulmer-Thomas (Reference BULMER-THOMAS2003), for instance, suggest that banking problems and deposit withdrawals in Argentina were modest and did not generate major strains. Della Paolera and Taylor (Reference DELLA PAOLERA and TAYLOR2001), by contrast, emphasize the presence of serious distress in the early 1930s, which culminated in a systemic crisis in 1934, underscoring the fragile condition of domestic banks, and the decisive role this played in the creation of the central bank in 1935. Along these lines, Nakamura and Zarazaga (Reference NAKAMURA, ZARAZAGA, Paolera and Taylor2003) document a persistent and uninterrupted decline in both bank share prices and returns between 1929 and 1935, while Francis and Newland (Reference FRANCIS and NEWLAND2021) find that the banking sector operated under relatively sound profitability during the Great Depression. Adding to this picture, Gomez (Reference GOMEZ2018) highlights the divergent performance of domestic and foreign banks; Alvarez and Nodari (Reference ALVAREZ and NODARI2024) further explore this distinction using more granular, bank-level data, to show that foreign banks’ credit lines fell more sharply than the industry average, and remained depressed throughout the 1930s.

Figure 1 plots changes in the ratio of cash holdings to deposits against changes in loan portfolios for individual banks between 1931 and 1933. Two main patterns emerge from the chart. First, there is a negative association between reserve ratios and lending activity, meaning that the banks that increased their cash holdings the most and/or lost deposits were also those that curtailed their lending portfolios most sharply. Second, foreign and domestic banks form two distinct clusters. While domestic banks (blue dots) are relatively dispersed around the origin of the chart, foreign banks are heavily concentrated in the upper-left quadrant. This shows that, unlike their domestic counterparts, all foreign banks reduced their lending portfolios; but also that the magnitude of the contraction was significantly greater, ranging from 30 to as much as 60 per cent. At the same time, foreign banks display a marked rise in cash-to-deposit ratios, which is particularly evident among European institutions. This pattern suggests an adjustment mechanism among foreign banks, linking liquidity hoarding, deposit withdrawals and lending retrenchment – a dynamic that the article will explore in greater detail as a potential unique recessionary pressure on the Argentine domestic economy during the Great Depression.

Relationship between cash holdings and bank lending, 1930–3

Figure 1 Long description

The scatter plot illustrates the relationship between changes in cash-to-deposit ratios and changes in lending portfolios for individual banks between 1930 and 1933. The horizontal axis represents the change in the lending portfolio between 1930 and 1933, ranging from negative 60 percent to positive 60 percent. The vertical axis represents the change in cash-to-deposit ratios in 1933 compared to 1930, ranging from negative 60 percent to positive 30 percent. The plot shows two distinct clusters: domestic banks, represented by blue dots, are dispersed around the origin, while foreign banks, represented by red diamonds, are concentrated in the upper-left quadrant. This indicates that foreign banks reduced their lending portfolios more significantly, with changes ranging from 30 to 60 percent and displayed a marked rise in cash-to-deposit ratios. Notable banks include The National City Bank of New York and The First National Bank of Boston, which are positioned in the lower-left quadrant, indicating a decrease in both lending and cash-to-deposit ratios. The plot highlights a negative correlation between reserve ratios and lending activity, with foreign banks showing a greater contraction in lending and an increase in cash holdings.

Foreign banks were an important part of Argentina’s banking system.Footnote 6 They encompassed a variety of institutions and nationalities, with branch networks spread across the nation (see Figure 2). In 1930, the Bank of London and South America (BOLSA) and the Anglo-South American Bank (Anglo) stood out as the leading foreign banks, with assets of US$298 million and 216 million, respectively, and branch networks extending all the way down the Patagonian coast and Cuyo for BOLSA, and the northeast for Anglo. Among German banks, the German Transatlantic Bank (GTB) held US$162 million in assets across five branches in the central region, while the German Bank of South America (GBSA) maintained US$111.8 million in its Buenos Aires branch. Other European banks included the French–Italian Bank for South America (Sudameris) with US$69 million and two branches, followed by the Italian–Belgian Bank (IBB) and the Holland Bank for South America (HBSA) at similar levels (with US$43 and 40 million, respectively); both were located in Buenos Aires. Figure 2 illustrates how the City of Buenos Aires and its surrounding areas concentrated the bulk of the branches, serving as the primary locus of European banking activity in the country.Footnote 7 From North America, the First National Bank of Boston and the National City Bank of New York held assets for US$158.2 and 100.2 million, respectively, while the Royal Bank of Canada accumulated US$50.7 million; all three also operated primarily from Buenos Aires.Footnote 8

Branch network of European banks in Argentina in 1930

Figure 2 Long description

The map shows the branch locations of European banks in Argentina in 1930. It includes an inset focusing on the Buenos Aires area. The banks are represented by different colored dots: Bank of London and South America (BOLSA) in red, Anglo-South American Bank (Anglo) in blue, German Transatlantic Bank (GTB) in green, German Bank of South America (GBSA) in purple, French and Italian Bank for South America (Sudameris) in light blue, Italo-Belgian Bank (IBB) in orange and Holland Bank for South America (HBSA) in pink. The map highlights the concentration of branches in Buenos Aires and other regions such as the Patagonian coast, Cuyo and the northeast. The inset provides a detailed view of the dense network of branches in and around Buenos Aires, indicating its importance as a financial hub.

The institutional arrangement as joint-stock multinational corporations – otherwise known as free-standing companies – was a common, distinguishing feature of these European banks.Footnote 9 Headquartered in Europe, they had been established by raising capital through the issuance of shares in the stock exchanges of the main financial centres where the head offices were based, but with the specific purpose of operating abroad. To do so, a separately capitalized bank was set up in the host country, which could then open several branches or affiliates at their destination, depending on its business strategy. In most cases, these banks were initiated and owned by leading commercial banks in their home countries (see Table 1). For instance, Dresdner Bank and Deutsche Bank, two major Berlin banks, were the main owners of GBSA and GTB, respectively. Lloyds Bank held over 99 per cent of BOLSA’s shares, while Anglo had been linked to Colonel John Thomas North (the ‘Nitrate King’) from its founding in 1890. HBSA belonged to the Rotterdamsche Bank and the Nederlandsche Handel-Maatschappij (NHM), and Sudameris to Banca Commerciale Italiana (Comit), Société Générale and Paribas.Footnote 10 Finally, IBB was owned by Credito Italiano (CI), the other major Italian bank, with the participation of several Belgian banks.

European banks in Argentina in 1930 (assets and capital in millions of US$)

Table 1 Long description

The table compares seven European banks operating in Argentina in 1930, listing head-office assets and capital, head-office city and main shareholders, plus Argentine affiliate assets, capital, and branch counts; all money figures are in millions of US dollars. At head office, the Anglo-South American Bank has the highest assets at 394.4, followed by the Bank of London and South America at 305.0; the Holland Bank of South America is smallest at 29.6. Head-office capital is highest for Anglo at 27.4 and BOLSA at 17.2, while Sudameris and the Italo-Belgian Bank are lowest at 3.9 each. In Argentina, BOLSA has the largest affiliate assets at 298.0, ahead of Anglo at 216.6; the smallest affiliate assets are for the Italo-Belgian Bank at 43.0 and the Holland Bank of South America at 40.2. Branch networks are concentrated in BOLSA with 19 and Anglo with 20, while most others have five or fewer branches, including single-branch operations for the German Bank of South America and the Italo-Belgian Bank. The German banks are headquartered in Berlin with major shareholders Deutsche Bank for GTB and Dresdner Bank for GBSA; Sudameris is linked to major French and Italian shareholders, and HBSA is linked to Dutch banking groups. Figures reflect positions just before the early 1930s banking turmoil, so they should be read as pre-crisis snapshots rather than outcomes.

Note: Total assets of the HO of the National City Bank of New York, the First National Bank of Boston and the Royal Bank of Canada totalled 2078.3, 718.5 and 874.3 million dollars, respectively. The year 1930 was chosen as it represents the last full year before the 1931 European banking crisis, showing banks’ pre-crisis positions.

Source: The Bankers’ Almanac 1931 and Boletín Oficial (various issues).

The banks’ headquarters and overseas affiliates were legally autonomous and maintained separate capital bases, yet they remained financially and managerially interconnected. In general, head offices were relatively small in staff and business volume compared to their overseas networks, but maintained effective control of activities abroad.Footnote 11 At home, head offices were seldom engaged in retail banking (domestic lending or deposit taking); they focused mainly on international activities, especially trade finance and foreign exchange. They managed the European end of trade finance between their home countries and Latin America, actively participated in wholesale money markets, oversaw the investment portfolios (largely kept in Europe) and handled dividend payments. In contrast, Argentine affiliates combined these international and foreign exchange functions with retail operations, in order to serve local clients, railways, electricity companies, trams, insurance firms and other foreign enterprises, as well as extending credit to municipalities and the state.Footnote 12 Through these operations, the overseas affiliates and home offices became connected through reciprocal financial ties such as interbank deposits and business accounts.Footnote 13

The relationship between Argentine affiliates and their headquarters also extended to personnel. Beyond institutional factors and internal procedures that regulated banking activities overseas, home offices exerted influence and control by appointing nationals to key directorial positions at the affiliates. Data on the composition of the boards of directors of European banks in Argentina (as of 1927) show that all members were foreigners, and specifically from the banks’ countries of origin (Lluch and Salvaj Reference LLUCH, SALVAJ, David and Westerhuis2014). The boards of GBSA and GTB, for instance, consisted of three and two German nationals, respectively. In the case of Sudameris, the four board members were French, and the other banks also were managed by foreigners. The absence of Argentine representation on the boards, and the dominance of directors from the banks’ countries of origin, reflects the extent to which the affiliates’ strategic direction and operations responded to European rather than domestic considerations. As Geoffrey Jones explains for the case of British banks, they ‘made very effective use of socialization strategies to control their overseas branches, which reduced the need for a large head office to monitor staff’.Footnote 14

III

The spring and summer of 1931 were marked by a wave of panics and exchange difficulties in Europe. After the collapse of Creditanstalt in Austria in May 1931, liquidity problems and bank failures emerged in Hungary and Germany over the following months (for an overview, see James Reference JAMES2001). In July, some major German banks, such as the Danatbank, went bankrupt, while others were brought to the brink of collapse; this led to the temporary suspension of the entire banking system, the introduction of foreign-exchange controls and the suspension of the free convertibility of the Reichsmark (see Schnabel Reference SCHNABEL2004). The German crisis, and the measures adopted to deal with it, brought significant pressures in other countries: in the case of the UK, it propelled a run on sterling, and the eventual suspension of the gold standard by British authorities in September 1931 (Accominotti Reference ACCOMINOTTI2012, Reference ACCOMINOTTI2019).

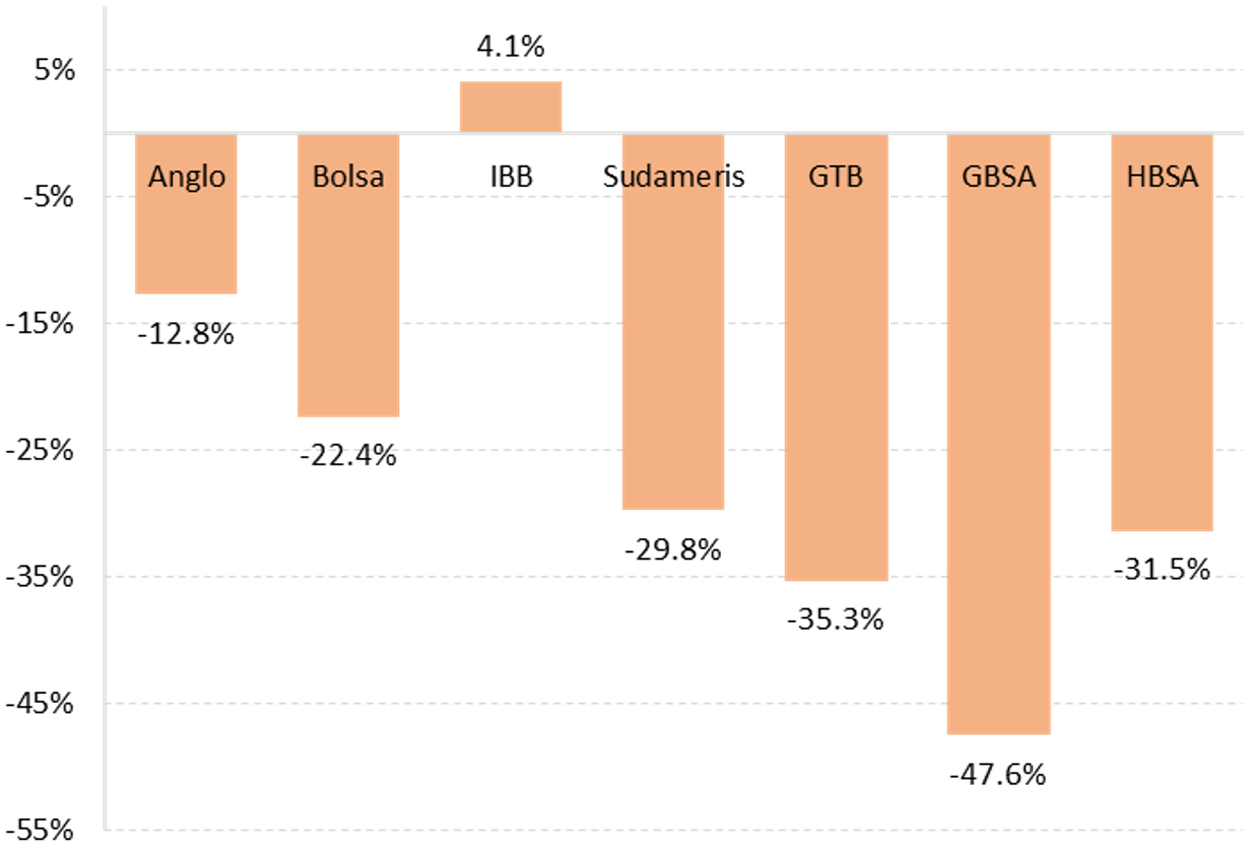

Figure 3 shows the change in total assets and liabilities of the head offices of European banks operating in Argentina in 1931. The chart highlights the striking scale of the adjustments, with most institutions experiencing sharp contractions in their balance sheets. With the exception of IBB – which registered a modest increase – all others recorded significant declines. German banks were the most severely affected: GBSA’s assets and liabilities in Berlin fell by nearly half, while those of GTB dropped by 35.3 per cent. HBSA in Amsterdam and Sudameris in Paris likewise experienced substantial reductions, with balance sheets shrinking by about one-third in a year. Among the British banks headquartered in London, BOLSA registered the steepest fall, with a 22.4 per cent contraction, and by mid 1931 it had already closed two of its Latin American branches in Antofagasta and Santiago, Chile. Anglo, despite showing the smallest contraction at 12.8 per cent, faced acute financial difficulties in London. Indeed, after withdrawing from Uruguay, the head office came under severe strain and approached British authorities for assistance; it was eventually rescued by the Bank of England in September 1931 (see Accominotti Reference ACCOMINOTTI2012, pp. 26–7; Miller Reference MILLER, Llorca-Jaña, Miller and Barría2019).

Annual change in total assets and liabilities of the head offices in Europe in 1931

The challenges in 1931 were not confined to the head offices alone, as their domestic parent institutions also faced major problems and financial pressure. The Dresdner and Deutsche Banks, owners of GBSA and GTB, respectively, were badly affected by the crisis; they suffered heavy withdrawals of deposits and were eventually bailed out by the Reich and Reichsbank (along with the Danatbank).Footnote 15 CI and Comit in Italy, the main shareholders of IBB and Sudameris, respectively, also faced severe liquidity problems, and both signed secret agreements with the Treasury and the Bank of Italy for emergency assistance in 1931 (see Battilossi Reference BATTILOSSI2009). In the Netherlands, while no panics and widespread banking failures were observed, the situation of some banks was far from sound and stable. The Rotterdamsche Bank – major shareholder of HBSA, the Nederlandsche Handel-Maatschappij (NHM) and other major banks – lost significant volumes of deposits during the year. On the contrary, the situation of Lloyds in London, owner of BOLSA, remained quite stable despite the banking turmoil; although it closed 1931 with losses for the first time in decades, and undertook some changes to improve its financial position (Joslin Reference JOSLIN1963). Banking problems also reached France and Belgium, and affected to different degrees the activities of Paribas, Société Générale and the Belgian banks with shares in Sudameris and IBB.

The breakdown of international money markets was at the heart of the 1931 financial crisis and global contagion. The standstill agreements and capital controls implemented to address the central European banking and currency crises severely disrupted the bill of exchange and acceptance markets, which were essential for the international flow of liquidity across banks and countries. On the one hand, under the standstill agreements signed with Austria in June and October, and with Germany and Hungary in July 1931, foreign creditor banks committed to maintaining (i.e. freezing) their deposits and interbank credit lines with the banking systems of these countries. The instauration of new foreign exchange restrictions prevented banks and importers that had borrowed through bills of exchange or money market facilities from repaying their obligations; this created market tensions and payment difficulties for those who had guaranteed these instruments in other countries. In the case of London merchant banks, as Accominotti (Reference ACCOMINOTTI2012) has demonstrated, exposure to standstill agreements and deposit withdrawals were closely linked, with the banks most involved in Central Europe suffering the greatest losses.

Archival information on the negotiations of the standstill agreements in Austria, Germany and Hungary reveal the direct exposure of the European overseas banks’ shareholders. The Creditanstalt standstill, formalized in mid June 1931, was at the centre of the banking problems in Europe; it compelled several of the parent banks as signatories to immobilize significant portions of their assets. The three principal owners of Sudameris – Comit, Paribas and Société Générale – had losses amounting to approximately US$2 million.Footnote 16 Lloyds Bank, overseeing BOLSA, was required to freeze US$250,000. Similarly, the Dutch institutions, Rotterdamsche Bank and Nederlandsche Handel-Maatschappij, both stakeholders in HBSA, participated in the Creditanstalt agreement, with combined commitments totalling US$600,000.Footnote 17 Dresdner Bank and Deutsche Bank, the main stakeholders of GBSA and GTB, incurred respective losses of US$900,000 and US$200,000.Footnote 18 Finally, IBB’s CI and Banque Belge pour l’Étranger were also entangled in the crisis, freezing US$ 200,000 in assets.Footnote 19 The ripple effects of the Creditanstalt standstill were soon compounded by the subsequent German and Hungarian agreements, signed by mid July, in which most of these shareholder banks were also involved (see Bussière Reference BUSSIÈRE1992; Cottrell Reference COTTRELL1997; Stanciu Reference STANCIU2020).

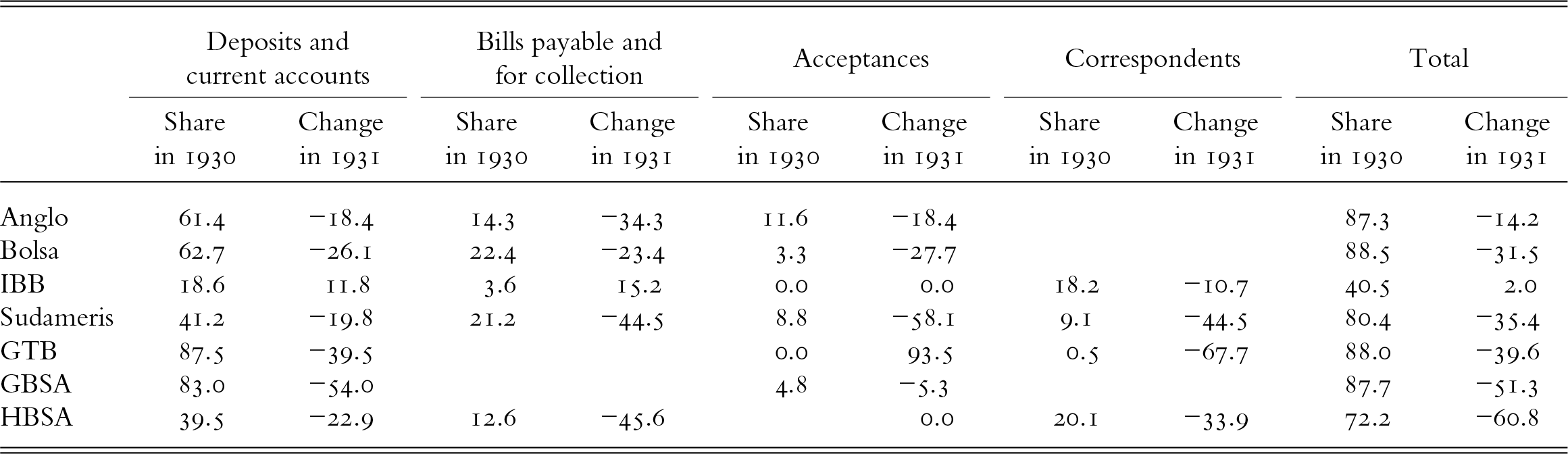

The disruption in the European money markets was especially problematic for international banks with a large involvement in wholesale liquidity; this was the case for the headquarters of European overseas banks. Table 2 presents their main fundraising accounts as a share of total liabilities in 1930, and their percentage change in 1931. The figures make clear the extent to which head offices relied on wholesale banking instruments, and how dramatically they contracted in 1931.Footnote 20 Money market instruments accounted for 72 per cent of the balance sheet of the HBSA, 80 per cent for Sudameris, and as much as 87–88.5 per cent for Anglo, BOLSA, GTB and GBSA. Notably, the share for IBB – the only one not to suffer a contraction of its balance sheet in 1931 – was much lower, representing only 40 per cent of total liabilities. Moreover, unlike its counterparts, IBB’s deposits and bills of exchange accounts increased in 1931. It is important to note that, since retail banking was not the primary activity for the head offices (as previously mentioned), the deposit and current accounts displayed in Table 2 consisted largely of interbank deposits or short-term credit lines from other banks and financial institutions. Given the highly volatile nature of this type of transaction and its sensitivity to shocks, when the crisis hit, the regular flow of wholesale liquidity in the interbank market deteriorated, with banks shortening the term of the credit lines and/or directly withdrawing their interbank deposits.

Main fundraising accounts of the head offices, 1930–1 (percentage)

Table 2 Long description

The table reports each head office’s percentage share in 1930 and the change in 1931 for five fundraising account types: deposits and current accounts, bills payable and for collection, acceptances, correspondents, and the total. Total share in 1930 is highest for GTB at 88.0, Bolsa at 88.5, Anglo at 87.3, and GBSA at 87.7, while IBB is lowest at 40.5. In 1931, total share falls for Anglo by 14.2 points, Bolsa by 31.5, Sudameris by 35.4, GTB by 39.6, GBSA by 51.3, and HBSA by 60.8; IBB is the only bank with a small increase of 2.0 points. Deposits and current accounts are especially concentrated in GTB at 87.5 and GBSA at 83.0 in 1930, but both drop sharply in 1931, by 39.5 and 54.0 points respectively. Bills payable and for collection are reported for Anglo, Bolsa, IBB, Sudameris, and HBSA, and all of these show declines in 1931 except IBB, which increases by 15.2 points. Acceptances are modest for most banks in 1930, with Sudameris at 8.8 and Anglo at 11.6, and Sudameris shows the largest decline in 1931 at 58.1 points; GTB is an outlier with a large increase from a zero base. Correspondents data are only present for IBB, Sudameris, GTB, and HBSA, and all four decline in 1931, with GTB dropping by 67.7 points. Some cells are blank, so comparisons by account type are incomplete for banks without reported values.

Sources: The Bankers’ Almanac (various issues).

The situation of BOLSA and GTB in the wake of the standstill agreement illustrates the dynamics affecting both supply and demand in a distressed interbank market, in which the head offices of European overseas banks were heavily involved. At the London Conference of 20–23 July 1931, BOLSA – which had been progressively reducing its deposits at Deutsche Bank, Dresdner Bank and Danatbank – agreed, under pressure from the Bank of England, to roll over and renew short-term credits to the struggling German banks; this effectively halted its withdrawals and helped to stabilize their financial position. The committed deposits were £1,800,000, £900,000 and over £500,000, respectively, and represented about three-quarters of BOLSA’s capital base.Footnote 21 GTB faced a parallel but more severe challenge: its interbank deposits and credit lines, which accounted for as much as 87.5 per cent of its funding base (see Table 2), deteriorated significantly. Moreover, not only did these funds contract by 40 per cent in 1931, but their term structure shortened sharply: over half of GTB’s deposits and current accounts (52.9 per cent) were due within seven days, with an additional 13.3 per cent due within three months.Footnote 22 This contrast highlights the acute tensions in the international interbank market, and underscores how it had become an increasingly unstable and vulnerable source of funding for borrowing banks.

On the asset side, the composition of the portfolio illustrates how the banks deployed the funds obtained from interbank wholesale sources. BOLSA and Anglo were heavily involved in trade finance, with bills of exchange and advances forming up to 83 per cent and 61 per cent of their total claims, respectively. Investments in securities and other assets constituted the primary allocation of funds for IBB and, to a much lesser extent, Anglo, accounting for 57 per cent and 15 per cent of their assets, respectively. Bills of exchange and advances represented 41.4, 31.2, 30.9 and 28.5 per cent of the assets of Sudameris, GTB, GBSA and HBSA, respectively, while current accounts with the banks represented 24.8, 51.5, 42.5 and 32.2 per cent; this underscores their participation on the supply side of wholesale markets. Yet, as shown in Table 2, deposits and current accounts on the liability side exceeded those on the asset side, while the opposite was true for bill of exchange facilities. This means that these banks acted as net borrowers in the interbank deposit markets, and net lenders in the bill of exchange markets. In other words, they borrowed from other banks through short-term credit lines to fund trade finance operations. When the central European crisis struck, causing an interbank funding squeeze, the banks reduced their assets to meet shrinking liabilities, which led most of these accounts to decline.

IV

Given European banking’s central role in international commercial and financial relationships, the problems in this sector entailed significant repercussions overseas. As the head offices struggled with funding challenges and shrinking balance sheets, their boards adopted adjustment measures affecting the operations undertaken in Latin America, where much of their business was concentrated. A major consequence of the crisis was the restructuring and retrenchment of their international banking networks. Between 1929 and 1931, BOLSA and Sudameris each closed five overseas branches, four of which were in Latin America for BOLSA, and one for Sudameris. Anglo and GTB closed, respectively, three and one Latin American branches, while other banks – IBB, HBSA and GBSA – maintained their networks unchanged. None of these closures affected branches in Argentina, and BOLSA even opened a new branch in the country during 1930.Footnote 23 Yet, like their headquarters and parent institutions, the balance sheets of the Argentine affiliates underwent significant changes in the wake of the 1931 international banking crisis.

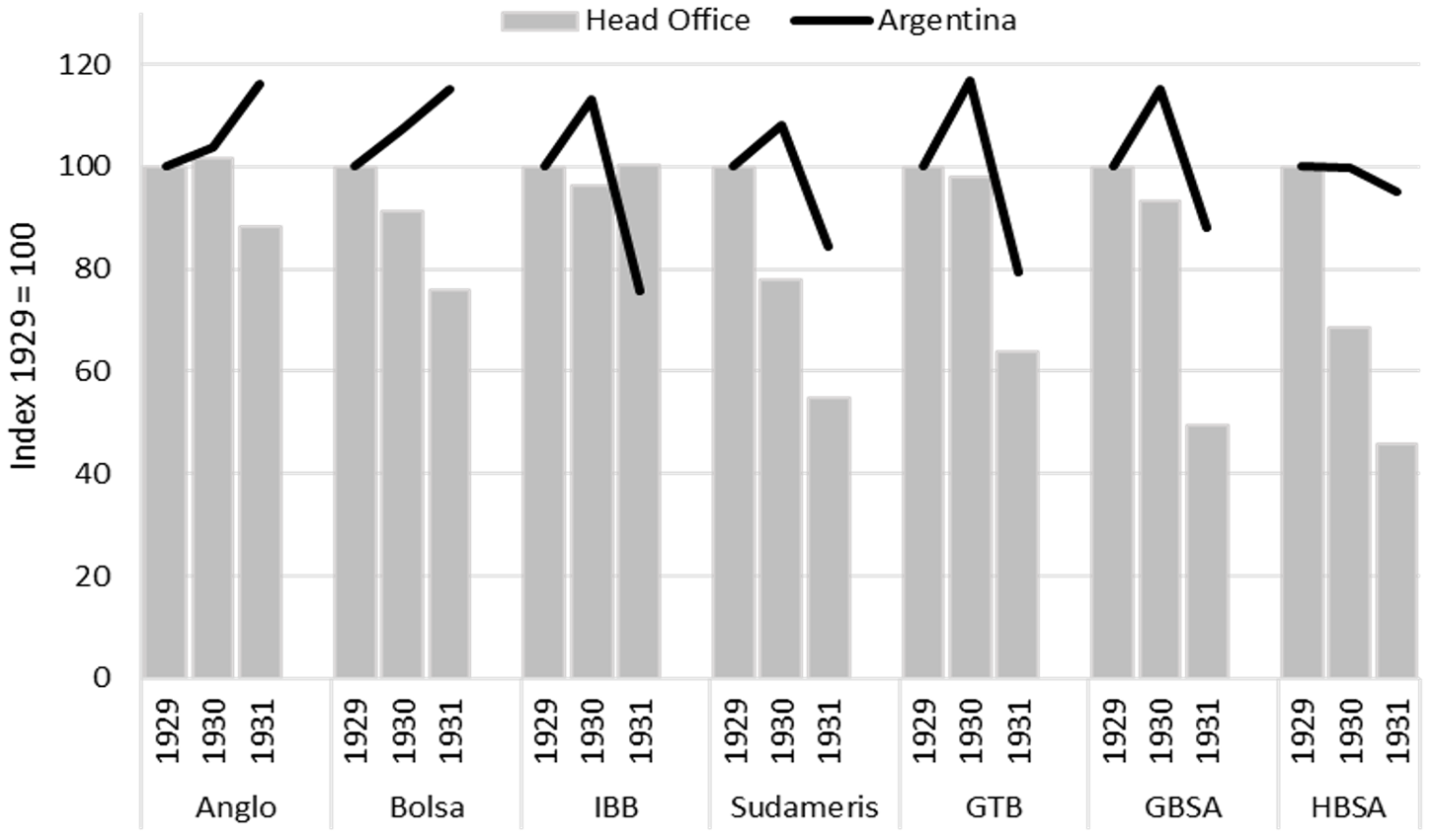

Figure 4 shows the evolution of assets and liabilities of both the head offices and their Argentine affiliates between 1929 and 1931. The chart highlights the distinct impact and dynamics of the crisis in Argentina, compared to Europe. Unlike their European head offices, the balance sheets of the banks in Argentina expanded in 1930, only to begin contracting the following year. For British banks, the Argentine affiliates’ total assets grew in 1931, as they absorbed business from their former counterparts in Uruguay and Chile that were being closed. IBB contracted in Argentina, even as its head office expanded in Antwerp. Among the rest, GTB was hit hardest, with a 32 per cent decline in 1931. GBSA, Sudameris and HBSA followed, with decreases of 23.6, 21.9 and 4.6 per cent, respectively. While these declines were significant, they were far less severe than those suffered in Europe. Notably, while European balance sheets had already begun contracting in 1930, the downturn in Argentina only commenced in 1931.

Evolution of total assets and liabilities of head offices and Argentina’s affiliates, 1929–31

Figure 4 Long description

The bar graph plots index values for head offices and Argentina affiliates across six banks. The y-axis is labeled Index 1929 equals 100 and ranges from 0 to 120. The x-axis lists six banks: Anglo, Bolsa, IBB, Sudameris, GTB and GBSA, plus HBSA. Each bank has three grouped sets of vertical bars corresponding to the years 1929, 1930 and 1931. Within each year group, two bars appear side by side representing the two series in the legend: Head Office and Argentina. The 1929 baseline value for all bars is set at 100. For Anglo, the Head Office bars remain near or above 100 across all three years, while the Argentina bars show a rise in 1930 followed by a drop in 1931 to approximately 80. For Bolsa, both series start at 100 in 1929, with Argentina rising above 100 in 1930 and falling below 100 in 1931 to near 80. For IBB, the Head Office bars rise above 100 in 1930 and remain elevated in 1931, while the Argentina bars decline below 100 by 1931. For Sudameris, both series start at 100, with Argentina remaining near 100 in 1930 before falling to approximately 80 in 1931. For GTB, the Argentina bars drop sharply in 1931 to approximately 65 to 70, representing one of the largest declines visible in the graph. For GBSA, Argentina bars fall to near 75 in 1931. For HBSA, the Argentina bars show a comparatively smaller decline in 1931, remaining closer to 95. Head Office bars across most banks remain at or above 100 in 1930 and show smaller changes in 1931 compared to the Argentina series.

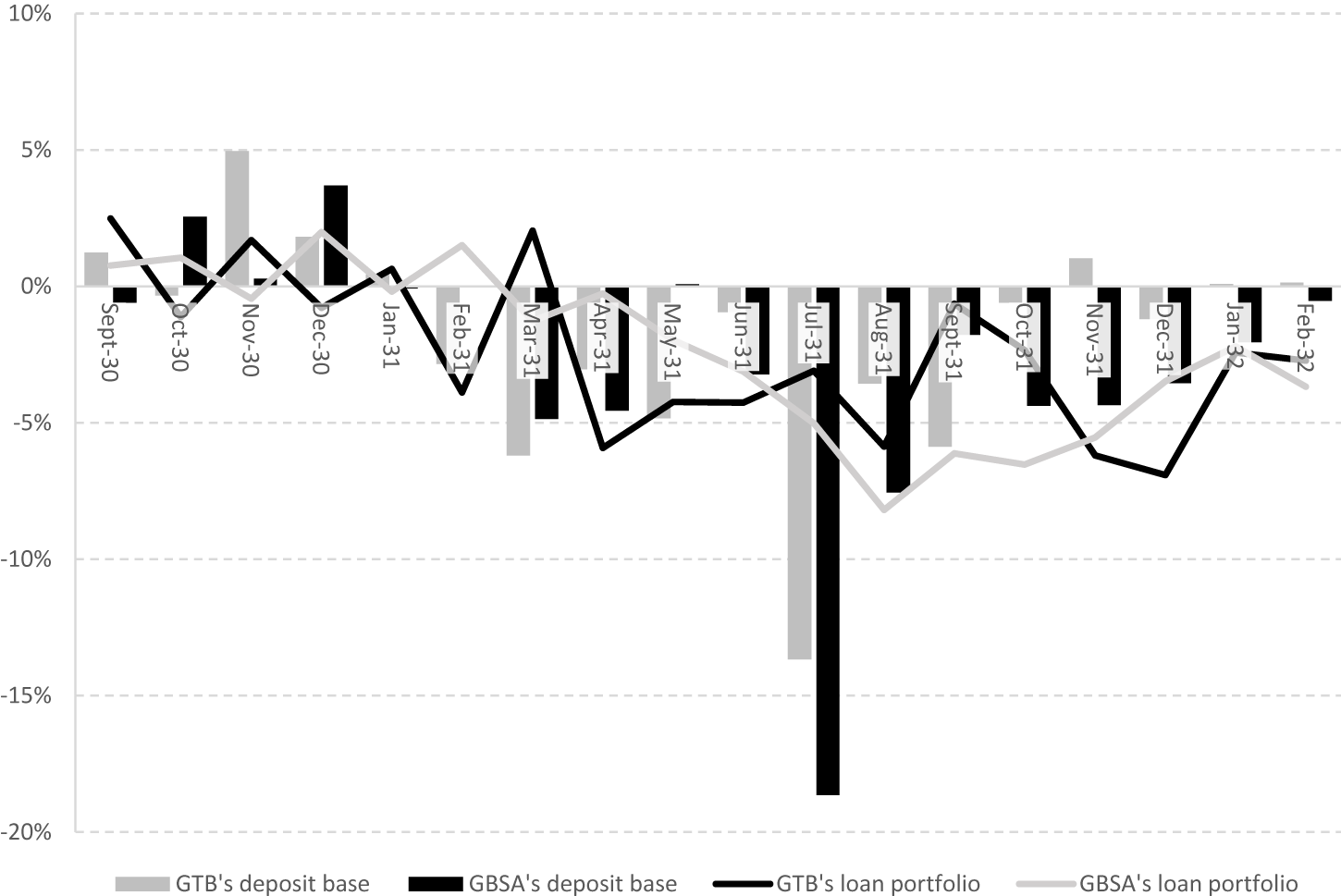

To examine the potential connection between banking dynamics in Europe and Argentina, Figure 5 plots the evolution of the deposit bases of the two German banks. The chart displays the monthly percentage changes in deposits at the Argentine affiliates of GTB and GBSA, whose European head offices experienced major balance sheet contractions in 1931. Total deposits with the GTB, which had been declining since February, dropped sharply by 13.7 per cent in July and continued to fall, accumulating a 35.2 per cent decline by the end of the year. GBSA underwent a similar trend, but with even heavier losses: an 18.6 per cent fall in July 1931, ending up with a 43 per cent drop by the year’s end. This illustrates a close synchronization of deposit behaviour in Argentina with developments in Europe, with both banks experiencing the largest withdrawals at the peak of Germany’s banking and financial crisis. Importantly, the lending portfolio began to retrench immediately after the downturn in deposits, as can be observed in Figure 5, with total declines of about 34.6 and 33.8 per cent by the end of the year, respectively. The timing and scope of these contractions suggest that the retrenchment of lending was a response and resulted from the banks’ need to liquidate assets to meet their liabilities.

Monthly percentage change of deposits and loans of the GTB and GBSA in Argentina, September 1930 – February 1932

Figure 5 Long description

The vertical axis shows percent values from negative 20 percent to 10 percent, with labeled ticks at 10 percent, 5 percent, 0 percent, negative 5 percent, negative 10 percent, negative 15 percent and negative 20 percent. The horizontal axis shows months labeled: Sept-30, Oct-30, Nov-30, Dec-30, Jan-31, Feb-31, Mar-31, Apr-31, May-31, Jun-31, Jul-31, Aug-31, Sept-31, Oct-31, Nov-31, Dec-31, Jan-32, Feb-32. A legend lists four series: GTB′s deposit base, GBSA′s deposit base, GTB′s loan portfolio, GBSA′s loan portfolio. GTB′s deposit base is shown with vertical bars. The bar at Nov-30 reaches about 5 percent. The bar at Mar-31 reaches about negative 6 percent. The bar at Jul-31 reaches about negative 14 percent. The bar at Nov-31 is about 1 percent. Other GTB deposit bars are near 0 percent to negative 6 percent across the remaining months. GBSA′s deposit base is shown with vertical bars. The bar at Jan-31 is about 4 percent. The bar at Mar-31 is about negative 5 percent. The bar at Apr-31 is about negative 4 percent. The bar at Aug-31 reaches about negative 19 percent. Other GBSA deposit bars are near 0 percent to about negative 4 percent across the remaining months. GTB′s loan portfolio is shown with a line. It is near 2 percent at Sept-30, near 0 percent at Oct-30, near 2 percent at Nov-30, near negative 1 percent at Dec-30, near 1 percent at Jan-31, near negative 4 percent at Feb-31, near 2 percent at Mar-31, near negative 6 percent at Apr-31, near negative 4 percent at May-31, near negative 4 percent at Jun-31, near negative 3 percent at Jul-31, near negative 6 percent at Aug-31, near negative 1 percent at Sept-31, near negative 4 percent at Oct-31, near negative 6 percent at Nov-31, near negative 7 percent at Dec-31, near negative 3 percent at Jan-32 and near negative 3 percent at Feb-32. GBSA′s loan portfolio is shown with a line. It is near 1 percent at Sept-30, near 1 percent at Oct-30, near 0 percent at Nov-30, near 2 percent at Dec-30, near 0 percent at Jan-31, near 2 percent at Feb-31, near 0 percent at Mar-31, near negative 1 percent at Apr-31, near negative 2 percent at May-31, near negative 2 percent at Jun-31, near negative 5 percent at Jul-31, near negative 8 percent at Aug-31, near negative 6 percent at Sept-31, near negative 6 percent at Oct-31, near negative 5 percent at Nov-31, near negative 4 percent at Dec-31, near negative 2 percent at Jan-32 and near negative 4 percent at Feb-32.

The simultaneous and concomitant deposit withdrawals in the Argentine affiliates, the head office banks in Germany and their shareholder banks suggest the presence of a broader, common phenomenon. This raises questions about causality: were the problems originating in Germany and spreading to Argentina, or vice versa? While an in-depth analysis of contagion and the causal chain linking these financial difficulties is beyond the scope of this article, it is difficult to believe that issues faced by relatively small actors on the periphery could have sparked the systemic problems that endangered the stability of Germany’s banking system. Indeed, according to historical accounts of the German banking crisis, the causes lie in factors largely unrelated to the situation in Argentina, which indicates that the chain of effects probably flowed in the opposite direction. Chronologically, while the Dresdner and Deutsche Banks began losing deposits as early as the mid 1930s, and the balance sheets of GBSA and GTB contracted in 1930, the erosion of deposits in the Argentine affiliates only began later, in 1931. It is more plausible that the difficulties faced by the Dresdner and Deutsche Banks, along with their affiliates GTB and GBSA in Germany, had a subsequent impact on their Argentine subsidiaries rather than the reverse, as they were interconnected through interbank operations (see the next section).

To varying degrees, the rest of the European banks operating in Argentina also faced deposit losses in 1931. Apart from the German banks, the most affected were IBB and HBSA, with Sudameris impacted to a lesser extent; this reflected the problems encountered in Central Europe, along with the Italian and Dutch banking systems. After a period of relative stability at around 32 million pesos moneda nacional ($ m/n), the deposit base of the IBB contracted by 7 per cent in June and an additional 15 per cent in July; it continued to decline over the following months, accumulating a total fall of 30 per cent by the end of 1931. HBSA, which had expanded its deposits from about $ m/n 17 million in 1927 to $ m/n 23 million by the mid 1930s, began a steady decline in November 1930, which continued throughout 1931, shrinking by up to 32 per cent that year. In contrast to IBB and HBSA, Sudameris did not experience bank-run-like behaviour; it exhibited a more moderate decline, which appeared to be part of a longer-term trend that had started well before the European crises. After peaking at $ m/n 65.5 million in May 1928, deposits progressively declined, with losses of 9.1 and 8.4 per cent in November and December 1929; they stabilized in 1930, and then resumed their decline in 1931, culminating in a total loss of 20 per cent for the year.

The circumstances of British banks in Argentina were distinct from those encountered by their continental European counterparts. In the case of BOLSA, the deposit base had been expanding consistently from early 1929 until March 1931, and remained relatively stable throughout the rest of the year. Deposit fluctuations were evident, ranging from a 3.4 per cent contraction in April to a 3.7 per cent expansion in December, but BOLSA closed 1931 with a deposit base 6.4 per cent higher. Anglo experienced a less favourable deposit trend, though it fared significantly better than the other European banks. Its deposits declined slightly at the beginning of the year, recovered by September, then fell again by 3.1 per cent in October and a further 4.8 per cent by the end of the year. The financial challenges in London in 1931, particularly the pressure on sterling, along with the difficulties faced by the head offices, were not fully mirrored in the behaviour of their Argentine affiliates’ deposits. While Anglo’s deposit base contracted between September and December, coinciding with the aftermath of the abandonment of the gold standard and the head office’s appeal to the Bank of England, the decline was moderate and did not persist over the following months.Footnote 24

Nevertheless, the lack of bank runs, or of significant deposit declines, does not necessarily indicate that British banks in Argentina were in a completely sound condition. Anglo’s well-known exposure to the Chilean nitrate industry caused problems (Miller Reference MILLER, Llorca-Jaña, Miller and Barría2019), and BOLSA faced its own challenges. A 1932 report on BOLSA, by Lloyds Bank executives Sir Alexander R. Murray and Mr F. A. Beane, identified several critical concerns. In 1931–2, for instance, the bank made provisions of $ m/n 11 million, thus eroding the consistent profits of approximately $ m/n 22 million it had earned over the previous decade. Additionally, while the Argentine network as a whole produced positive results, certain offices – such as those in Bahía Blanca, Mendoza, Paraná and Posadas – incurred significant losses. The report notes that the bank’s strategy in 1929 and 1930 seemed to have been ‘to attract additional deposits by offering higher rates, and to encourage our managers to lend out more freely, not only such funds as they themselves had available, but also to borrow for that purpose from Buenos Aires Branch’. The report goes on to observe that ‘the longer history of many of the branches shews evidence of risky and hazardous banking resulting in losses which the last two years of depressed trade have accentuated and brought to light’.Footnote 25

Despite variations in deposit behaviour among European banks’ Argentine affiliates in 1931, a consistent pattern was the reduction in lending portfolios. Like the German banks, their counterparts from the UK and other parts of continental Europe also shifted their lending practices. During 1931, the credit portfolios of HBSA, Sudameris and IBB decreased by 27.8, 31.7, and 41.7 per cent, respectively – a substantial contraction, which often outpaced the reduction in deposits. British banks exhibited a similar trend, though their lending portfolios declined at more moderate rates of 14.3 and 19.5 per cent, respectively. A key distinction, however, lies in the fact that for GTB and GBSA – as well as for other banks to a lesser degree – the reduction in lending corresponded with a contraction in deposits. In the case of BOLSA, the reduced lending occurred despite an increase in its deposit base, while at Anglo, the contraction in lending was 2.3 times larger than the reduction in deposits. This shows that, regardless of changes in their deposit levels, banks responded to the European banking crisis by choosing not to renew credit lines; they acted cautiously due to the uncertain financial climate, as we discuss in detail below.

V

The disruptions that the 1931 financial crisis inflicted on banking activities had significant implications for the balance sheet management strategies, both in Europe and overseas. To face the retrenchment of deposits and interbank credit lines, a first reaction by head offices and the affiliates was to contract their credit portfolio, as was previously shown. Adjustments to lending were not always enough; in such cases they turned to other elements on the assets side that they could liquidate, such as securities or positive balances with other financial institutions, and to new sources of funding or financial assistance from lenders of last resort. Importantly, through their internal debit and credit accounts (as well as with their correspondents abroad), the head offices and foreign affiliates could move liquidity across borders to meet their liabilities, and secure their financial position and funding needs in the host countries.

The actions undertaken by the head offices of the most affected banks in Europe, and the changes in their balance sheets, illustrate these points.Footnote 26 GTB, for instance, made recourse to reserve funds, which slightly increased in 1930 and then halved in 1931, while simultaneously liquidating 36 per cent of its securities and investment portfolio. HBSA used all its reserves and liquidated the holdings of Treasury stocks, along with 18 and 52 per cent of its investments in 1931 and 1932, respectively. GBSA did not draw on its reserves, but it also reduced its portfolio investments (by 40 per cent), and increased branch accounts in the liabilities from nil to RM 1.5 million. Sudameris, for its part, barely reduced its investment portfolio, and addressed the declining liabilities entirely through its cash holdings and its balances with its correspondents. In the cases of BOLSA and Anglo, while the former managed to meet its needs with its reserve funds, the latter encountered serious liquidity problems and was finally assisted by the Bank of England, as mentioned previously.Footnote 27 IBB, which did not suffer a contraction of its balance sheet in 1930, also liquidated some investments and adjusted its balances with correspondents.

The effects on the management of internal funding between head offices and overseas branches were substantial; these differed significantly across institutions. Table 3 shows the Argentine branches’ internal accounts with their head offices and foreign affiliates, recorded on both the asset and liability sides as of the end of 1930 and 1931. It also displays the net position, calculated as the difference between assets and liabilities, which reflects whether the Argentine branches had a surplus (positive net position) or a deficit (negative net position) with their overseas counterparts. A positive net position indicates that the Argentine affiliates were providing funds to the international network, or acting as net suppliers to the head office and other foreign affiliates. Conversely, a negative net position means that the Argentine affiliates were net debtors to their overseas counterparts, effectively borrowing from them. The figures clearly show significant changes in 1931, both in the absolute size of the accounts and in shifts in the net position. These changes varied from bank to bank, which reflects the differing conditions faced by the head offices in Europe and their Argentine affiliates – as well as those in other countries.

Argentine branches account for head office and affiliates overseas, 1930–1 (thousands of pesos moneda nacional ($ m/n))

Table 3 Long description

The table reports assets, liabilities, and resulting net position for seven Argentine branches in 1930 and 1931, with amounts in thousands of pesos moneda nacional. In 1930, Anglo had the largest assets at 6,647.2 and a strong net position of 3,241.6, while IBB had the weakest net position at negative 5,505.6 due to liabilities of 7,167.7 against assets of 1,662.1. In 1931, Anglo strengthened further to the highest net position at 7,371.3, driven by assets of 8,342.9 and low liabilities of 971.6. GTB and GBSA both reversed from positive net positions in 1930, at 2,906.4 and 3,019.6, to negative net positions in 1931, at negative 2,680.0 and negative 1,434.1. Bolsa improved from a modest net position of 379.5 in 1930 to 1,860.2 in 1931 as liabilities fell from 5,558.9 to 3,369.7. IBB and Sudameris moved from negative net positions in 1930, at negative 5,505.6 and negative 92.8, to positive net positions in 1931, at 1,753.6 and 1,418.9. HBSA remained negative in both years, improving slightly from negative 1,228.1 to negative 1,065.2. Comparisons should be read as year specific snapshots, since the table does not explain causes such as exchange rates, accounting changes, or restructuring.

Source: Boletín Oficial (various issues).

The two German banks in Argentina, which were among the most affected by the financial crisis of 1931, exhibited similar behaviour. By the end of 1930, their claims on the head office and foreign affiliates were more than three times greater than their liabilities to them, resulting in positive balances of $ m/n 2.9 million for GTB and $ m/n 3 million for GBSA. This suggests that the Argentine affiliates were helping to finance their overseas counterparts’ liquidity needs, and those of branches elsewhere. However, in 1931, the situation reversed, with both banks significantly cutting their claims on the head office and foreign affiliates, while increasing their liabilities to them. As a result, the net position turned negative, which signals that throughout 1931, the Argentine affiliates had become net borrowers through internal funding channels. In other words, the head offices and foreign affiliates appear to have started providing financial assistance to the Argentine branches, to help them manage the decline in deposits. Nevertheless, it is important to recognize the limited role of these internal funding flows within the broader context of balance sheet changes, as the net positions accounted for merely 1.6 to 2.7 per cent of total assets on the balance sheets of GTB and GBSA in 1930 and 1931, respectively.

Figure 6 shows the monthly evolution of GTB’s and GBSA’s net positions with their head offices and foreign affiliates, along with correspondent banks overseas, between December 1930 and December 1931.Footnote 28 The chart highlights how the positive balance with head offices and foreign affiliates gradually diminished throughout 1931, eventually turning negative by the end of the year. This trend contrasts with the banks’ net positions with overseas correspondents: while both banks had negative balances in 1930, the deficits steadily decreased, and in the case of GTB even shifted to a positive balance by the end of 1931. Thus, unlike in their internal accounts, the Argentine affiliates were net borrowers from correspondent banks overseas in 1930, but this funding source progressively decreased over the course of 1931. The close inverse relationship between these two net balances suggests that clearing actions were taking place between the Argentine affiliates, head offices, and other creditor and debtor banks, through these internal debit and credit accounts. It appears that a payment triangulation was in place, and that positive balances with the head offices and foreign affiliates were used to reimburse and repay the Argentine affiliates’ foreign correspondents.

Accounts with head offices and foreign affiliates vis-à-vis correspondents overseas, January–December 1931

Figure 6 Long description

The scatter plot illustrates the relationship between the net balance with correspondents overseas and the net balance with head office and foreign affiliates, both expressed as percentages of total assets. The horizontal axis represents the net balance with correspondents overseas, ranging from negative 5.0 percent to positive 1.0 percent. The vertical axis represents the net balance with head office and foreign affiliates, ranging from negative 5.0 percent to positive 2.0 percent. Two series are shown: GTB and GBSA, differentiated by color. GTB data points generally show a positive trend, moving from negative to positive values over time, while GBSA data points show a negative trend. Clusters are visible, with GTB points concentrated around the positive end of the horizontal axis and GBSA points more spread out. The plot reveals that GTB′s net balance with correspondents overseas improved over time, while GBSA′s balance decreased. This comparison highlights the differing financial strategies or conditions of the two entities over the period.

The internal accounts of British banks, whose deposit bases in Argentina were among the less affected, followed a different pattern. Both BOLSA and Anglo held positive net positions in 1930, and substantially increased the net lending to their head offices and foreign affiliates in 1931. This shift was primarily due to a decrease in liabilities rather than a rise in assets. For BOLSA, claims on the head office and foreign affiliates stayed relatively stable, while liabilities fell by nearly 40 per cent. Anglo saw even larger changes, with claims increasing by 25 per cent and liabilities dropping by 71 per cent. In the case of BOLSA, these adjustments – particularly the reduction in liabilities – aligned with the board’s instructions to foreign branches to reduce their reliance on head offices and return part of their capital loans to London; this will be discussed in the following section. For both banks, the Argentine affiliates functioned as net suppliers of funds to their counterparts abroad, thus effectively transferring liquidity through internal channels. However, like the German banks, the weight of these accounts on the affiliates’ balance sheets was modest: up to 1.9 per cent for BOLSA, and 4 per cent for Anglo.

IBB was the bank whose internal accounts had the greatest weight on its balance sheets. In 1930, claims on and liabilities to the head offices of foreign affiliates constituted 3.7 per cent and 16.1 per cent of its Argentine branch balance sheet, respectively; however, by the end of 1931, these figures reversed to 12.8 per cent and 6.7 per cent. This reflects a shift from borrowing as much as 12.3 per cent of its balance sheet from its overseas counterparts, to lending them about 6.1 per cent – a change driven primarily by an increase in assets, alongside a substantial reduction in liabilities. Conversely, Sudameris demonstrated the least dependence on internal channels, with less than 1 per cent of its balance sheet attributed to interactions with head offices and foreign affiliates in 1930; although this share grew by 1931, and the net position shifted from negative to positive (see Table 3). Finally, for HBSA, there were almost no claims with head offices and foreign affiliates, while liabilities represented about 3 per cent of its balance sheet in both 1930 and 1931. The net position remained negative (meaning that the Argentine branch operated as net borrower), with slight variations in absolute terms or relative to the balance sheets.

Even with these adjustments, the affiliates struggled to balance their assets and liabilities; in many cases, they required support from local authorities. At this time, Argentina did not yet have a central bank, and the responsibilities of the lender of last resort fell to BNA through its rediscount policies (Della Paolera and Taylor Reference DELLA PAOLERA and TAYLOR2001; Gomez Reference GOMEZ2018).Footnote 29 Figure 7 plots the rediscount lines from BNA to the European banks: their trajectory directly mirrors the timing of the European crisis and the mounting difficulties of the Argentine affiliates throughout 1931. German banks were the most significant rediscounting entities, especially following the outbreak of the crisis in Germany in July 1931. Moreover, in the case of GTB, the balance sheets show increases in liabilities to the Caja de Conversión of $ m/n 7.0, 4.7 and 2.3 million in April, May and June, respectively; this suggests that the bank was also borrowing directly from the Conversion Office.Footnote 30 To a much lesser extent, Sudameris also engaged in rediscounting towards the end of the year, while HBSA and IBB resorted to smaller amounts, and Anglo and BOLSA did not. Importantly, the rediscounts by these European banks increased not only in absolute terms, but also in relation to the total rediscounts’ portfolio of the BNA, reaching about 10 per cent in November 1931. This suggests that the liquidity problems following the outbreak of the European banking crisis were relatively more concentrated in European banks, as other banks did not increase their recourse to rediscounts to the same extent. In the case of German banks, the amounts rediscounted closely matched what they were losing in deposits.

Rediscounts of European affiliates with Banco de la Nacion

Figure 7 Long description

The graph displays rediscounts of European banks and total rediscounts to the banking sector. The x-axis represents time from the end of 1929 to the end of 1930, marked as YE (Year End) and mid-year points. The left y-axis shows thousands of pesos moneda nacional (m/n) ranging from 0 to 30000, while the right y-axis shows rediscounts as a percentage from 0 to 12 percent. The legend identifies five entities: HBSA, Sudameris, IBB, OBSA and GTB, along with a dashed line representing rediscounts of European banks as a percentage of total rediscounts. The area graph shows a rise in rediscounts, peaking at YE 1930. The dashed line indicates a similar trend, peaking at around 10 percent. Key points include a significant increase in rediscounts from mid-1930 to YE 1930, with GTB showing the highest values. The graph highlights the correlation between rediscounts in pesos and their percentage of total rediscounts.

VI

The international financial meltdown of 1931 marked a turning point in the lending policies and liquidity management strategies of European banks in Argentina. Within a context of heightened uncertainty, European banks operating overseas adopted more conservative approaches as the world headed into the Great Depression. Banks that were struggling to secure interbank credit lines in Europe, or facing deposit erosion in Argentina, had little choice but to adjust their credit portfolios. Yet this shift was also evident in banks with more stable or even growing deposits. Furthermore, the reduced lending by banks in trouble persisted even after the immediate effects of the European financial crises had passed and their deposit bases began to recover. As restrictions on international capital flows and the collapse of global trade loomed, European banks continued to scale back lending, and focused instead on strengthening their financial condition.

Improving the liquidity position of Latin American affiliates became a priority for the European banks’ headquarters. The cases of BOLSA and Sudameris, the two banks whose deposit bases in Argentina were among the least affected in 1931, are the most telling examples of this change. Despite BOLSA’s relatively stable (and even growing) deposit base, by early September the board of directors in London advised branch managers to reduce lending. Following the United Kingdom’s abandonment of the gold standard, the headquarters instructed overseas branches to operate within their own resources and minimize the strain on the head office. The board also imposed a strict requirement to ‘the cash high – in many cases 50% of liabilities – quickly cabling any manager that failed to come into line’ (Joslin Reference JOSLIN1963, p. 250). Memorandums sent to Argentina stressed that ‘a strong financial position must continue to be your first consideration’;Footnote 31 a directive that led to a 60 per cent increase in cash holdings and a rise in the cash-to-deposit ratio from 20 to 30 per cent. Moreover, telegrams to overseas branches added that ‘it would be advisable that South American and New York agencies should gradually return to Head Office part of agencies’ capital loans’.Footnote 32

Internal documents and reports from Sudameris reveal similar reactions and dynamics. As the Austrian banking crisis spread across Central Europe and threatened the solvency of its main shareholder Comit, the director of Sudameris, Giuseppe Zuccoli, returned from a financial mission in Latin America and implemented some precautionary measures.Footnote 33 By the end of May, as debates about approving a banking standstill agreement for the Creditanstalt were reaching their peak in London, the Comit board advised their overseas affiliates to be more cautious in renewing existing credits – as, according to Italian bankers, the ‘world crisis obliged [them] to restrict operations with the rest of the world’.Footnote 34 Sudameris aligned with this cautious approach, instructing Argentine branches to ‘avoid every risk, avoid every credit immobilization and realize all the profits’.Footnote 35 Headquarters directed affiliates not to renew the most important trade credit lines to South America upon their maturity, and to reduce their acceptances in circulation.Footnote 36 Additionally, while the board had previously agreed to increase the Argentine affiliates’ capital, the decision was suspended in order to avoid taking further risks and to reduce the exposure in Latin America, given the instability and the extent of the crisis’ spread in Europe.Footnote 37

The situation of German banks in Argentina – which were among the most affected ones – illustrates the extent to which this phenomenon persisted long after 1931. As Figure 8 shows, for GBSA, deposits collapsed abruptly in mid 1931, but began to recover the following year and continued to expand thereafter. Lending, however, kept falling through late 1932, before stabilizing at a lower level. The renewed inflow of deposits was not channelled into new loans but instead accumulated as cash reserves; this reflects a deliberate strategy to strengthen liquidity. GTB displays a similar pattern: although its deposits stabilized after 1931, its loan portfolio kept shrinking for nearly two more years. With deposits down 35 per cent in 1931, loans dropped by more than 50 per cent between 1930 and 1933 – thus falling below late 1920s levels, and never recovering. Like GBSA, GTB used deposit inflows primarily to build up liquidity, through maintaining higher cash balances on its books instead of resuming credit expansion. Alvarez and Nodari (Reference ALVAREZ and NODARI2024) show that this liquidity hoarding and credit retrenchment in the post-1931 period was not unique to German banks, but a common response among European institutions. The introduction of capital controls and restrictions on profit repatriation for foreign companies have been suggested as possible drivers of this behaviour, but evidence remains inconclusive, and the topic warrants further investigation.

Evolution of the main balance sheet accounts of the GBSA, 1925–35

The analysis developed so far has emphasized the 1931 European banking crisis’ adverse impact on the lending portfolios of European banks in Argentina, but other factors may also have contributed to this outcome. In particular, the sharp decline in international trade as the world entered the Great Depression, coupled with the widespread adoption of protectionist policies during the 1930s, could have also influenced foreign banks’ lending behaviour.Footnote 38 Trade finance was a core activity of these institutions, and the collapse of global trade may help to explain why European banks’ lending in Argentina remained subdued long after the crisis’ immediate effects had passed. Moreover, since these banks were also active within the internal market, the broader conditions of the Argentine economy may have affected their balance sheets as well. In fact, although it is difficult to assess the precise weight of domestic business in their portfolios, booking records and board minutes reveal the presence of local companies and domestic clients. Sudameris, for example, maintained revolving credit lines with firms such as Compañía Italo Argentina de Electricidad, Molinos Harineros y Elevadores de Granos SA and Valsechi Hermanos & Cia.Footnote 39 Similarly, BOLSA extended credit to Azucarera Argentina SA and Di Tella Limitada, and Anglo to regional companies including SA Bodegas y Viñedos Domingo Tomba, SA Bodegas Arizu and SA Vitivinícola de Mendoza, among others.Footnote 40

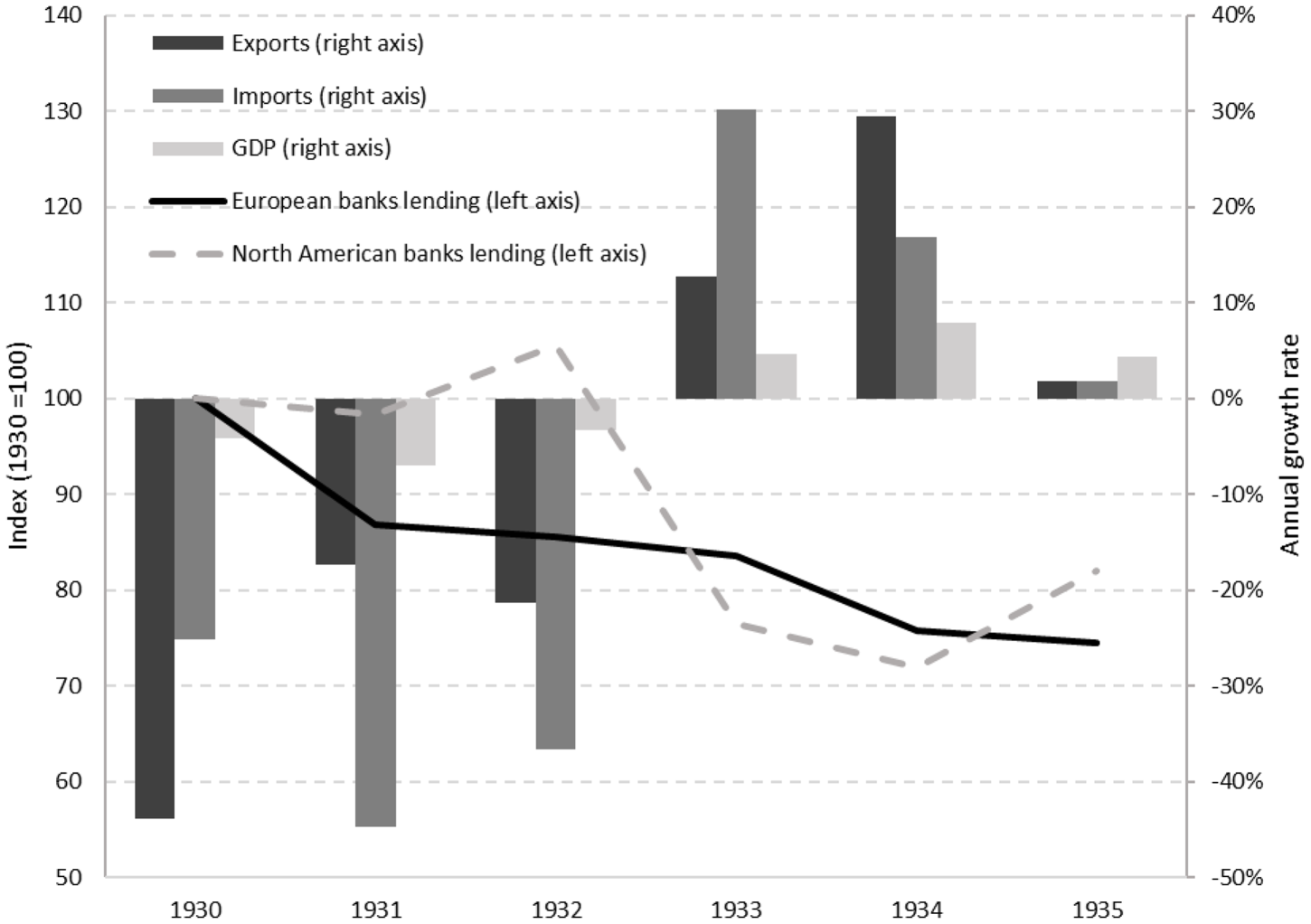

While a detailed examination of these factors is beyond the scope of this article, Figure 9 offers some insight into their potential relationship. It plots the evolution of the loan portfolios of foreign banks in Argentina against annual changes in GDP, exports and imports between 1930 and 1935. The chart shows that after an initial contraction of 13.1 per cent in 1931, European banks’ lending continued to decline, albeit at a slower pace, over the following years. By 1935, their loan portfolios were 25 per cent below 1930 levels. The domestic economy and international trade, however, followed a different trajectory: after contracting sharply for three consecutive years between 1930 and 1932, they began to recover in 1933 and expanded steadily thereafter.Footnote 41 This suggests that although the initial decline in output and trade may have weakened credit demand, the subsequent recovery failed to spur renewed financial activity; this points instead to supply-side factors as the main driver of foreign banks’ lending behaviour. It is worth noting, however, that this reflects only the aggregate trend; thus, a proper understanding of lending performance would require examining sectoral patterns and the distribution of credit across European banks.

Evolution of foreign banks’ lending and Argentine international trade and GDP, 1929–35

Figure 9 Long description

A mixed bar and line graph with years 1930, 1931, 1932, 1933, 1934 and 1935 on the horizontal axis. The left vertical axis is labeled “Index 1929 equals 100” and shows values from 50 to 140. The right vertical axis is labeled “Annual change” and shows values from negative 50 percent to 40 percent. Legend entries: Exports (right axis), Imports (right axis), GDP (right axis), European banks lending (left axis), North American banks lending (left axis). European banks lending (left axis) is a solid line. It is at 100 in 1930, about 90 in 1931, about 90 in 1932, about 85 in 1933, about 75 in 1934 and about 75 in 1935. North American banks lending (left axis) is a dashed line. It is at 100 in 1930, about 105 in 1931, about 100 in 1932, about 75 in 1933, about 70 in 1934 and about 80 in 1935. Exports (right axis) bars: 1930 about negative 45 percent; 1931 about negative 10 percent; 1932 about negative 25 percent; 1933 about 5 percent; 1934 about 30 percent; 1935 about 2 percent. Imports (right axis) bars: 1930 about negative 25 percent; 1931 about negative 45 percent; 1932 about negative 35 percent; 1933 about 30 percent; 1934 about 20 percent; 1935 about 3 percent. GDP (right axis) bars: 1930 about negative 10 percent; 1931 about negative 5 percent; 1932 about negative 10 percent; 1933 about 5 percent; 1934 about 10 percent; 1935 about 5 percent.

Importantly, Figure 9 highlights the contrasting behaviour of North American banks. Unlike their European counterparts, these banks kept their loan portfolios relatively stable between 1930 and 1932, but registered a sharp contraction of 27.5 per cent in 1933; after this, lending remained broadly at that lower level through 1935. While a deeper analysis would be required to explain this distinct pattern, the North American banks’ different strategies and business models may have played a role. As several strands of the literature suggest, although trade finance and foreign exchange operations were also central to US banks’ activities abroad, their business scope tended to be broader than that of their European counterparts.Footnote 42 The case of the Buenos Aires branch of National City Bank is illustrative in this regard. Bridges (Reference BRIDGES2024) has stressed, for instance, that the branch served as a ‘concierge service for US businessman looking to expand trading opportunities overseas’. It also experimented with small-scale consumer lending and credit programmes with immigrants – initiatives to explore new market segments (see Bridges Reference BRIDGES2024, p. 90). Moreover, the implicit backing of the US government (and the Federal Reserve System), which had supported the internationalization of national banks as part of broader foreign policy objectives – the so-called dollar diplomacy – might have contributed to shielding them from local political risks and external shocks.

In fact, the activities of New York banks in the US proved strikingly resilient to the European banking crisis of 1931. While the collapse of the Creditanstalt shook numerous European countries and forced the United Kingdom to abandon the gold standard, banks in New York City – the central money market of the United States – continued to operate largely ‘as usual’ (Richardson and Van Horn Reference RICHARDSON and VAN HORN2018). The National City Bank of New York and the First National Bank of Boston, in particular, experienced no major disruptions in their domestic or international activities, and their Argentine (and broader Latin American) branches remained comparatively insulated from the turmoil not only in Europe, but also in other parts of the United States. While backing from the Federal Reserve may have played a role, these banks had greater legal and operational flexibility than their European counterparts; they were also, as is widely noted in the literature, far better capitalized. A similar situation prevailed in Canada, where the combination of a nationwide branch banking system, effective government regulation and a distinctive asset structure helped sustain the Canadian banking sector’s stability throughout the 1930s, as well as that of the leading domestic institution, the Royal Bank of Canada (Drummond Reference DRUMMOND, James, Lindgren and Teichova1991).

VII

This article has examined the connection between the European banking crisis of 1931 and the Argentine economy during the Great Depression, a dimension that has received little scholarly attention to date. By analysing the structure and evolution of the balance sheet accounts of the foreign banks’ Argentine affiliates in relation to the condition of their European head offices, the study reveals a close interrelationship and dynamic between banking developments in Europe and the behaviour of the Argentine deposits, lending portfolios, and reserve holdings.