1.1 Unicorns, Their Origin and Impact on Emerging Economies

Until a few years ago the term ‘unicorn’ held no meaning for those participating in entrepreneurial ecosystems around the world. A unicorn was just a mythical creature with a horn on its head, found in legends and children’s books. Today, however, it refers to a status most start-ups aspire to achieve. In the context of technology-driven companies, the term ‘unicorn’ refers to privately held start-ups that have reached a valuation of US$1 billion or more.

The concept of a unicorn company emerged in the early 2010s, and the phenomenon has since become a prominent part of the tech and venture capital landscape and culture. Technically, the term ‘unicorn’ was first coined by the venture capitalist Aileen Lee in a Reference Lee2013 TechCrunch article (Lee, Reference Lee2013). Lee used the term to describe the exceptional occurrence of start-ups that achieved valuations of US$1 billion or above, denoting them as creatures as unusual as the mythical unicorns. Lee has received very little credit for her linguistic discovery since then, despite how the term ‘unicorn’ has become an essential part of the start-up lexicon, symbolising the potential for exponential growth and success in the digital age.

The phenomenon gained attention as more and more tech-based and digital start-ups achieved billion-dollar valuations. The availability of venture capital (VC) and the disruptive potential of digital technologies in various industries were the main drivers of unicorn proliferation. With the number of unicorns increasing at a fast pace, questions about their business models, profitability and sustainability continue to abound. Many of these companies have suffered from growing pains during their transition from a rapid growth to profitability focus, while national and city governments around the world have greeted them with optimism, some even scrambling to lure them in. Unicorns hold the promise of attracting talent, boosting investment and raising the prestige of the cities where they are headquartered. However, when it comes to public policy, measures far beyond tax breaks have proved necessary for successfully pursuing unicorns (BBC Future, 2023). Unicorns also became part of the pulse of global powers over data access, analytics and control over storytelling, dominant narratives and artificial intelligence (AI). Unicorns have turned themselves into a symbol of innovation and disruption in the tech industry and beyond. They continue to attract significant attention from investors as well as the media, political forces and the general public, becoming symbols of economic power, national pride, political and social influence, technological dominance and even fear.

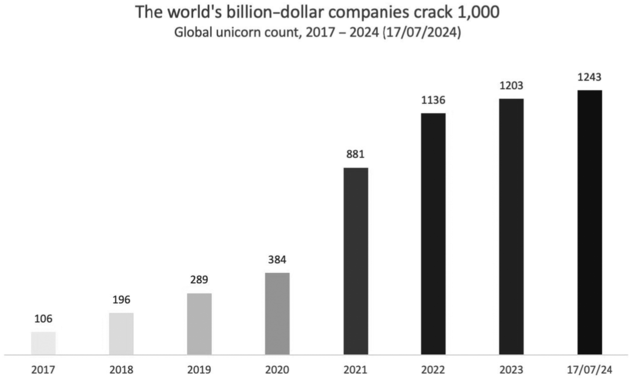

Over time, the definition of a unicorn has evolved to include promising high-growth companies with valuations approaching (but still below) US$1 billion, called ‘soonicorns’ (see Chapter 9); unicorns with valuations exceeding US$10 billion, known as ‘decacorns’; and even higher categories, such as ‘hectocorns’ for those valued over US$100 billion. There were fifty-three reported unicorns with a valuation of over US$10 billion in the world in 2025 (CB Insights, 2025). The value of unicorns is generally based on how investors and venture capitalists expect them to grow and consolidate industries, so their value comes down to longer-term forecasting and expectations. Unicorns’ valuations have little to do with how they perform financially in the short-term, and many of these companies rarely generate any profits during their first few years of existence. The number of unicorns has risen and the number of unicorn companies around the world in 2022 hit the one thousand mark (see Figure 1.1).

Global unicorn count 2017–2024.

Figure 1.1 Long description

The bar chart illustrates the global unicorn count of billion-dollar companies from 2017 to July 17, 2024. The x-axis represents years, while the y-axis represents the number of unicorns. The bars, which darken progressively, depict steady growth in unicorn numbers over time. The data are as follows: 2017: 106 unicorns. 2018: 196 unicorns. 2019: 289 unicorns. 2020: 384 unicorns. 2021: 881 unicorns, marking a sharp increase. 2022: 1,136 unicorns, surpassing 1,000 for the first time. 2023: 1,203 unicorns. July 17, 2024: 1,243 unicorns. The trend indicates a rapid expansion in unicorn companies, particularly from 2020 onwards.

Unicorns often embody experimentation and novel practices in business operations as they introduce unique technology-enabled business models and fast-paced growth and scale up. Attaining unicorn status epitomises a pinnacle of distinction, acknowledging the prowess of start-ups in pioneering technologies, devising viable strategies to captivate venture capital and other resources and a capacity to scale up. The international reach of unicorns underscores the globalisation of technology and entrepreneurship, capitalises on the dynamic tech landscape and connectivity and brings their societal and cultural implications across local contexts both in the Global North and South to the fore. Unicorns’ successes and failures also hold important lessons for a wide range of stakeholders in the business, entrepreneurship and technology sectors, as well as in the public sphere. They have become particularly important for CEOs of large corporations looking to defend their turf and/or build new revenue streams, bolster resilience and court venture capital resources (Berger de León et al., Reference Berger de León, Königsfeld, Leypoldt and Vollhardt2022). They are equally important to policymakers, who strive to understand and direct the economic and social change triggered by the phenomenon of digitalisation and technological transformation that unicorns accelerate (Si et al., Reference Si, Hall and Klein Leichman2023).

Unicorns are special because of their potential to disrupt traditional business models by relying on one or more enablers of exponential growth. These can include proprietary innovation, first-mover advantage, digital technology scalability, user-centric processes, network effects, access to capital, global reach, agility, strong branding and entrepreneurial drive, among others. For the Global South’s emerging economies, unicorns are also a driver of hope and optimism. They hold the promise of leapfrogging over the educational, infrastructure, institutional and other shortcomings of their local contexts via innovative digital and technology solutions. As of 2023, emerging economies were responsible for more than 50 per cent of the world’s economic growth (CFI Team, 2023). The increasing number of unicorns from the Global South presage a scenario of increased influence and prosperity of emerging economies even though many unknowns still remain before such a prospect can become a reality.

Entrepreneurial ecosystems from the Global South differ in their capacity to enable local innovation-driven start-ups to reach unicorn status and harness their transformational potential. The most prominent entrepreneurial ecosystems as of 2023 included China, India, Southeast Asia, Eastern Europe and Russia, Latin America, the Middle East and Africa. The remainder of this chapter offers a succinct overview of the birthplaces of unicorns from emerging markets and sets the scene for the in-depth analysis offered in the subsequent chapters, which highlight the defining features of specific entrepreneurial ecosystems and signature unicorns.

1.2 The Birthplaces of Unicorns and Soonicorns from the Global South

1.2.1 China

China has shifted economically, politically and culturally since the late twentieth century. After Deng Xiaoping’s reforms, the Asian country transitioned towards a more open market economy and prioritised its exporting competitiveness. State institutions promoted the sophistication of the economy and the creation of strong innovation capacity, giving rise to technology-driven innovative ventures. Thus, the technological progress of the twenty-first century and the Chinese government’s efforts to promote the transition to a knowledge-based economy boosted the creation, funding and growth of innovative start-ups, many of which attained unicorn status (see Chapter 11).

The Chinese entrepreneurial ecosystem has become the second most relevant in the world in terms of the number of unicorns, behind only the United States (see Chapter 5). There were 162 Chinese unicorns in May 2023, mostly headquartered in big industrial hubs such as Beijing and Shanghai and pertaining to the following industries: healthtech (10 per cent), AI (10 per cent), e-commerce (9 per cent), semiconductors (9 per cent), software-as-a-service (SaaS) (6 per cent) and enterprise services (6 per cent) (Slotta, Reference Slotta2023). Among the most prominent Chinese unicorns were ByteDance (Beijing, 2012; media and entertainment), SHEIN (Shenzhen, 2008; consumer and retail) and Xiaohongshu (Shanghai, 2013; media and entertainment). According to CB Insights (2024), ByteDance and SHEIN were the first and the third highest valued unicorns in the world in 2023. ByteDance had an impressive valuation of US$225 billion, US$75 billion more than the second most valued global unicorn, SpaceX (USA). SHEIN had a valuation of US$66 billion, while Xiaohongshu was the 12th most-valued global unicorn with a US$20 billion valuation (CB Insights, 2024) (see Figure 1.2).

Top twelve most valuable global unicorns.

Figure 1.2 Long description

The table displays the names of global unicorns and their valuations in billions of U S dollars. The companies are arranged from highest to lowest valuation: ByteDance: U S D 225 billion, Space X: U S D 150 billion, OpenA I: U S D 80 billion, SHEIN: U S D 66 billion, Stripe: U S D 70 billion, Databricks: U S D 43 billion, Canva: U S D 25.4 billion, Revolut: U S D 33 billion, Epic Games: U S D 22.5 billion, Fanatics: U S D 31 billion, Chime: U S D 25 billion, and x A I: U S D 24 billion.

The success of the Chinese entrepreneurial ecosystem in promoting start-up growth and unicorn creation has been attributed to strong government relationships, strategic alliances and founders with unique backgrounds and capabilities (Jinzhi & Carrick, Reference Jinzhi and Carrick2019). Notably, the Chinese government has been a fundamental ally, consistently channelling substantial investments into start-up ventures through a myriad of federal, provincial and local investment initiatives. Spanning dozens of direct and indirect programmes, these initiatives furnished nascent companies with crucial resources. Such support mechanisms have been instrumental in catalysing the emergence of thousands of high-growth start-ups (He et al., Reference He, Lu and Qian2019).

Besides direct funding, the government has used regulation and policy elements to promote investments. The active involvement of the Chinese government profoundly shaped the evolution of the Chinese venture capital community. This influence was exerted through regulatory frameworks that govern the operations of VC entities, as well as through direct interventions such as the establishment of government guidance funds that compete alongside traditional VCs. Additionally, the government participates in VC funds as limited partners, injecting capital into the ecosystem, further influencing its trajectory and sheltering it against geopolitical risks (Chen et al., Reference Chen, Gong and Li2024). Tax deduction has also been an influential regulatory element. The Chinese government implemented significant alterations to tax policies in 2017 and 2018, facilitating a deduction of 70 per cent of the invested capital from taxable income for VC investors (Ho & Lu, Reference Ho and Lu2019). In addition to financial support, human and social capital are two of the most important building blocks for new technology-based companies as they are at the core of competitive advantage; thus, science and education were identified as fundamental drivers of entrepreneurial ecosystem growth (Jinzhi & Carrick, Reference Jinzhi and Carrick2019). China’s results in this domain have been remarkable as it overtook the United States in terms of the total number of science publications, according to data from the US National Science Foundation (Tollefson, Reference Tollefson2018).

Amid geopolitical tensions between the United States and China, China managed to add fifty-six new unicorns in 2023, while the US added seventy (Global Unicorn Index, 2024). Globally, the decline of initial public offerings (IPOs) drives some of this growth, as ventures await the best moment to go public. Most of the Chinese ventures focus on AI, semiconductors and new energy, which attracted VC attention despite a negative trend in global VC investments and the increasing geopolitical uncertainty since 2022. This is especially relevant for such technologies which are sensitive to considerations of state interest.

1.2.2 India

India has also emerged as a prominent leader in the Global South start-up space, currently ranking as the country with the third largest number of start-ups, second only to the United States and China. Yet, a smaller number of Indian start-up ventures have attained unicorn status; the total number of Indian unicorns in 2023 was reported at eighty-three, one less than in 2022 (The Economic Times, 2023a). Since 2017, the number of government recognised start-ups in India has experienced rapid growth, climbing from 6,000 to over 113,000 by 2023 (DPIIT, 2024). In addition, the number of unicorns, which was one in 2010, reached 111 in 2023, with a total market valuation exceeding US$345 billion (Jain, Reference Jain2024). Almost all Indian unicorns are digital businesses as only a few non-digital Indian start-ups have managed to attain unicorn status (Forbes India, 2024).

Start-up activity is primarily concentrated in India’s major entrepreneurial hubs, which become homes for the Indian unicorns; Bengaluru, New Delhi and Mumbai accounted for 85 per cent of the country’s start-ups in 2022. These ecosystems, populated with dynamic information technology and business process outsourcing companies, also capture 85 per cent of all start-up investment in the country.

Several driving factors have been key to India’s prominent place in the global unicorn landscape. The vast and expanding Indian domestic market has been critical to the demand for the products and services offered by Indian unicorns. With 834.29 million people with internet access and 600 million smartphone users, India offers a significant digital market, especially in sectors such as e-commerce, fintech and consumer services. Secondly, India stands out as one of the countries with the largest number of STEM (science, technology, engineering and mathematics) graduates globally, with 34 per cent of students opting for careers in these fields according to data from UNESCO (United Nations Educational, Scientific and Cultural Organization) (Leap, 2024). The abundance of cost-competitive technical talent has been a crucial asset to the local entrepreneurial ecosystem, with elite educational institutions such as the Indian Institute of Technology playing a significant role. With over 27,000 active start-ups in the tech space, abundant and competent technical talent has been a driver for growth and innovation (The Economic Times, 2023b). A steady flow of venture capital also played a positive role; until 2022 cumulative investment in tech start-ups in India had reached US$446 billion (Investment in India, 2024). The government has provided targeted support through programmes such as Startup India and Digital India. Initiatives such as Aadhar and the Jan Dhan-Aadhar-Mobile (JAM) banking system have democratised access to financial services and stimulated demand. Recently, geopolitical tensions and trade disputes between China and the USA have created additional opportunities for Indian technology companies. There has been a surge in foreign investments in the Indian entrepreneurial ecosystem which international VCs perceived as less risky than the Chinese equivalent. From a geopolitical perspective, it appears that strengthening US–India technology relations could continue driving foreign investment in Indian research and development (R&D) capabilities.

However, India faces important challenges regarding the exponential growth prospects of its technology-driven ventures. The valuations of companies that went public in 2021 fell by more than 50 per cent in 2022 and smaller IPOs, in the US$300 million range, were anticipated to become more common than multibillion-dollar IPOs. This hinted towards a possible wave of premature IPOs that could be potentially destructive for ventures and the entrepreneurial ecosystem in general. A quick and sizable rebound of 72 per cent was reported in IPO activity in 2023 (Chadha, Reference Chadha2024). At the same time, as many as fifty-five (74 per cent) out of the seventy-four unicorns, analysed by Inc42, incurred a cumulative operating loss of US$5.9 billion in 2022 (Agarwal, Reference Agarwal2023). Nevertheless, the Indian entrepreneurial ecosystem has been moving to a more mature stage, with companies focusing on profitability and value creation within specific niches. Despite these challenges, the fundamental factors behind the growth of the start-up ecosystem in India remain robust. The digital revolution in India is in its early stages, with great potential for growth in internet, smartphones, e-commerce and financial services (see Chapter 6).

India came third in the list of countries with the highest number of new unicorns in 2024 (Global Unicorn Index, 2024). The emergence of new unicorns in India appears to be more sensitive to the declining trend in global venture investments than in China. The hopes for the transformational impact of Indian unicorn ventures are strongly linked to the overall growth of the Indian economy.

1.2.3 Southeast Asia

The countries from Southeast Asia, albeit smaller than China and India, have shown remarkable potential for scaling up their technology-driven ventures into unicorns (see Chapter 7). A convergence of factors have propelled the valuation of unicorns including the widespread adoption of smartphones, the rapid digitalisation catalysed by the COVID-19 pandemic, a burgeoning middle class and intensified initiatives by regional governments for fostering digital economies (Yean, Reference Yean2023). Private equity played a key role as the market allegedly reached a high of US$25 billion in 2021 (Yean, Reference Yean2023). The Asian Development Bank (ADB) has also supported the region’s entrepreneurial ecosystems. For example, in 2022 a project in Indonesia partially funded by the ADB focused on building technology parks to promote research and innovation (ADB, 2022). This project made funding available for technological solutions that could complement the development of scalable start-ups. Still, the region’s entrepreneurial ecosystems manifested their vulnerability as the US$25 billion invested in high-growth ventures in 2021 decreased to US$13 million the following year, a decline attributed to global uncertainties, rising interest rates and less attractive exit conditions (Yean, Reference Yean2023).

The Startup Genome 2023 global start-up ecosystem ranking accounts for a number of parameters including the number of exits, the value of the ecosystem and the success of start-ups. The ranking testified to the capacity of Southeast Asia for supporting its ventures in attaining unicorn status, a capacity that is far from equal among countries. Globally, Singapore came in eighth place, while Indonesia ranked 41st, Malaysia 43rd, Thailand 52nd, Vietnam 58th and the Philippines 59th. The Tech Collective counted forty-two newly minted unicorns in 2022: twenty-five unicorns in Singapore, sixteen in Indonesia, four in Vietnam, three in Thailand and two in Malaysia and the Philippines (Tech Collective, 2023). As of 2023 the region’s most prominent unicorns included J&T Express (Indonesia, 2015; Industrials), HyalRoute (Singapore, 2015; Industrials) and Traveloka (Indonesia, 2012; Consumer & Retail). J&T Express was the region’s highest-valued unicorn at US$20 billion (CB Insights, 2024) and it was the 13th highest-valued unicorn in the world. HyalRoute has a valuation of US$3.5 billion and Traveloka – US$3 billion (CB Insights, 2024).

Fintech was the industry with the highest numbers of unicorns from the region, mostly influenced by the relatively disproportionate impact of Singapore among the ASEAN (Association of Southeast Asian Nations) countries and its traditionally strong financial industry. More than 40 per cent of Singapore’s unicorns were in finance-related sectors (including insurance) and e-commerce. The latter accounted for the largest share of unicorns in Indonesia (Yean, Reference Yean2023). Growing smartphone usage, young demographics, increased private equity funding and a growing middle class have all enhanced the prominence of fintech unicorns (Tech Collective, 2023). In Indonesia, 51 per cent of citizens had no access to banking or financial services in 2023, while the underbanked, defined as people with access but who choose to use alternative financial services, accounted for 26 per cent of a population of 275 million people (Yean, Reference Yean2023).

The success of Singapore, the birthplace of the majority Southeast Asian unicorns, would have been impossible without long-standing government support. One example of strategic government intervention was developed in 2017 when the Singaporean government started to develop in-house technical solutions and purchase services from technology start-ups through its Smart Nation Initiative, rather than offering grants to support them (Dekker & Okano-Heijmans, Reference Dekker and Okano-Heijmans2020: 20). With this and many other programmes and initiatives, the government of Singapore has promoted innovation and digitalisation and helped Singapore obtain a first-mover advantage in the region as a unicorn powerhouse.

1.2.4 Eastern Europe and Russia

Eastern Europe’s former socialist bloc countries, along with Russia, had exhibited an impressive performance regarding unicorn and new venture creation before 2022. According to Crunchbase (CB Insights, 2024), the region directly or indirectly generated a record number of unicorns and even decacorns in 2021 and kept appealing to tech investors. For example, Miro secured a US$400 million investment from leading US investors, boosting its valuation to US$17.5 billion. Originally founded in Perm, Russia in 2011, the visual collaboration company relocated to California. That year, Grammarly, born in Kiev in 2009, reached a valuation of US$13 billion. TradingView, a social network and charting platform for financial markets from Russia, hit a US$3 billion valuation. InDriver, a ride-hailing app founded in Russia in 2012, announced its US$1.23 billion valuation. In addition, PandaDoc from Belarus became a unicorn, closing a large series C round (an advanced stage of capital raising); Russian-founded global graphene nanotube leader OCSiAl reached a US$2 billion valuation; Nexters, a Russian-founded game development company, went public on the Nasdaq through a special purpose acquisition company (SPAC) merger valued at US$1.9 billion; and People.ai, of Ukrainian origin, reached a valuation of US$1.1 billion.

Further west, a similarly prolific period of unicorn creation also took place. The years 2021 and 2022 were particularly robust for billion-dollar companies in Central and Eastern Europe (CEE), with over half of them emerging during this period. As the ecosystem evolved, it garnered increased attention from international investors, fostering more cross-border collaborations between regional venture capital firms (Groszkowska, Reference Groszkowska2023). Consequently, both the amount and proportion of funding directed towards late-stage start-ups grew significantly. This surge in mega-rounds fuelled the rise of local unicorns. In 2021 alone, fifteen new unicorns were born, followed by eight more in 2022. By the end of the third quarter in 2022, the region had produced a total of forty-four unicorns (Groszkowska, Reference Groszkowska2023), including Rimac Automobili (Croatia), Nord Security (Lithuania), Glia (Estonia), Payhawk (Bulgaria), Productboard (Czechia), and Veriff (Estonia). A point worth highlighting is that the scaling process of these unicorns included relocation outside their country of origin, while their back-office operations remained closely linked to the country/region of origin. Many promising start-ups and entrepreneurs have relocated internationally, posing a brain drain in the region.

Many of these unicorns concentrate on digital technologies that need relatively limited capital investment. Consequently, they typically secure smaller amounts of funding and at a later stage compared to their Western counterparts, frequently reaching profitability faster than unicorns from other regions. Naturally, investment companies specialising in high-tech ventures from this part of the world emerged. Examples include the United Venture Company and NRG Ventures.

Somewhat unexpectedly, according to the Startup Ecosystem Index by StartupBlink (2024), Moscow ranked first in Eastern Europe and 32nd globally in 2024, despite the ongoing armed conflict. As of 2022, Russia’s population stood at around 143.44 million people, with Moscow being the largest metropolis, boasting 12.5 million inhabitants (Statista, 2023). Specifically, Russia’s unicorn companies have enjoyed a burgeoning presence in high-tech industries, encompassing aerospace, nuclear technology, information technology and biotechnology. To bolster innovation and entrepreneurship, the government established the Skolkovo Foundation in 2010, focusing on supporting the development and commercialisation of advanced technologies both within Russia and beyond (WIPO, 2020). The Foundation aspired to be a leading innovation hub specialising in biomedicine, energy, nuclear technologies and space technologies. Additionally, the TechnoSpark deeptech start-up studio in New Moscow was built to foster innovation in areas like robotics and renewable energy. Some Russian universities played an important role in integrating entrepreneurial education into academia, providing expert support and business training to aspiring entrepreneurs.

The armed conflict between Russia and Ukraine started in March 2022 and this profoundly changed the region’s entrepreneurial and economic prospects. The case of Yandex (see Chapter 13) exemplifies how geopolitical factors such as sanctions and politics become determinant for the evolution of a unicorn. This case highlights the power of digital technology over the modern-day global power balance. Global geopolitical tensions mould the business environment and strategies of technology companies in a dramatic and immediate way. This underscores the significance of resilience and adaptability for unicorns navigating challenging geopolitical landscapes.

Moreover, geopolitical tensions exert a substantial impact on talent retention and brain drain within the start-ups and unicorns, and such risks must be carefully assessed in a world in flux.

1.2.5 Middle East and North Africa (MENA)

The Middle East and North Africa region has witnessed a surge of technology-driven entrepreneurship, especially in industries such as e-commerce, transportation, logistics and fintech. From 2023 it featured about 100 Israeli-founded (but not necessarily headquartered in Israel) unicorns and ten unicorns across the other countries in the region: four in the UAE, three in Egypt and three in the Kingdom of Saudi Arabia (see Chapter 9).

Although family-owned small and medium businesses that coexist with multinational corporations have traditionally dominated the regional economies, the region has been taking steps to build vibrant entrepreneurial ecosystems, attracting entrepreneurs and investors from around the globe. With a young and tech-savvy population, supportive government policies and a growing venture capital community, the Middle East and North Africa (MENA) region offers opportunities for technology innovation and ambitious business scaling. According to the Global Start-up Ecosystem Report 2024, Israel is the biggest regional player because Tel Aviv is a consolidated hub for technological innovation. The city globally ranks in fourth place for the performance of its entrepreneurial ecosystem. In 2023, eighty-eight Israeli unicorns were headquartered in the USA, which put Israel into a class of its own, given the very high degree of integration between its entrepreneurial ecosystem and that of the US, which is the most advanced (Si et al., Reference Si, Hall and Klein Leichman2023). Unlike those of any other country from the MENA region, Israeli unicorns develop deeptech solutions in AI, big data, analytics, cybersecurity and life sciences.

The MENA region is one of the most diverse in terms of the stage of development and maturity of the countries’ entrepreneurial ecosystems, their priorities and ambitions. For example, Dubai hosts a large and diverse expat community boasting a high concentration of technological innovators and entrepreneurs. Egypt has benefited from venture capital funding, government policies geared towards technology-based start-up creation and a growing network of technology incubators and global accelerators that have started to show positive effects. In the Kingdom of Saudi Arabia, the Ministry of Communications and Information Technology, Mohammed bin Salman Foundation ‘Misk’ and the National Information Technology Development Programme launched a joint national programme (Saudi Unicorns) to empower and support high-growth technology start-ups. These different national efforts are meant to support the attainment of unicorn status for an increasing number of high-growth ventures. Here are some examples:

Swvl is a transportation unicorn created in Egypt in 2018 and later headquartered in Dubai. It focuses on tech-enabled mass transit solutions, particularly bus trips (Rasmal, 2022). Kitopi was created in Dubai and has a presence in sixteen countries with over 6,700 employees (Forbes, 2022). This unicorn raised US$450 million in a Series C round and offers ‘ghost kitchen’ services, using digital technology to transform supply chains, logistics and delivery for some 100 restaurant brands across the Middle East (Rasmal, 2022). Created in Egypt, Fawry is a fintech company that surpassed the US$2 billion valuation mark in under two years. As an e-payment company, it allows payments of bills for obligations and external services such as traffic fines and water bills. Lastly, Careem was a Dubai-based ride-hailing service with presence in more than fourteen countries. It was acquired by Uber in 2020 for US$3.1 billion, which marked the biggest tech deal in the Middle East as of 2023 (Forbes, 2022).

The rise in MENA unicorn cases has been driven by one main structural strength: more than 55 per cent of the region’s population is under the age of thirty and very active in the digital domain. The finance, logistics and real estate sectors are expected to be particularly well suited for a technological disruption and surge in the number of unicorns (Wamda, 2022).

1.2.6 Latin America and the Caribbean

Latin America and the Caribbean have a very strong entrepreneurial tradition compared to other regions, although their firms are small and less likely to grow or innovate (Lederman et al., Reference Lederman, Messina, Pianknagura and Rigolini2014). In the age of digital transformation, unicorns are expected to change this, despite a few structural limitations that have persisted and weakened the regional entrepreneurial ecosystems. For example, access to digital infrastructure is limited across this vast and rugged region. More than 60 per cent of the population of Latin America and the Caribbean lack access to quality digital infrastructure (Martínez et al., Reference Martínez, Iglesias and García2020). Education quality and human development in general have made some advancements. Against this backdrop, venture capital was at US$3.9 billion in 2023, down from an all-time-high of US$20.1 billion in 2021 (dealroom.com, 2024).

It is important to stress the role that Latin American governments have played in promoting the growth of technology-driven start-ups by stimulating innovation, entrepreneurship and ultimately the attainment of their unicorn status. Governments have long been interested in fostering innovation. However, arguably, some long-standing policies such as tax subsidies have not had enough bite (Gonzáles & Hernandez, Reference Gonzales and Hernández2021). Tax subsidies for research and development, for example, are hardly relevant as most innovative technology-driven start-ups do not generate profits until years after their innovations occur. Although there have been some efforts to promote time-enduring policies that benefit entrepreneurial activity, there is still a long road ahead.

In a search for alternatives to support the development of start-ups, venture accelerators have been created to boost the number and potential of early stage start-ups (Herman Rodríguez, Reference Herman Rodríguez2015). Some of the ventures that benefited from these instruments managed to attain unicorn status, and by 2023 the region had potentiated the growth of forty-nine unicorns: twenty-five from Brazil, ten from Argentina, two from Chile, two from Colombia and one from Uruguay (see Chapter 8).

Three of the most impactful unicorns from Latin America in 2023 were Nubank (Brazil, 2013; fintech), Rappi (Colombia, 2015; super app) and Mercado Libre (Argentina, 1999; marketplace). The region suffered an extreme drop in venture capital availability in 2020 triggered by the COVID-19 pandemic. In spite of this, it managed to reach record levels in 2021, indicative of high variability and dependence on foreign VC.

Brazil stands as a compelling example of a thriving start-up ecosystem (see Chapter 12). It is one of the Latin American countries with the highest rate of entrepreneurial creation (Statista, 2023). São Paulo, a major global tech start-up hub and Brazil’s largest city, found itself at number twenty-six in the global ranking in 2024, earning the distinction of being the top-ranked ecosystem from Latin America and the only one featured among the global top 30 (Global Startup Ecosystem Report, 2023). Other Brazilian cities such as Rio de Janeiro and Florianópolis have also been rapidly developing their own tech start-up communities, benefiting from the government’s legal framework for start-ups.

São Paulo’s start-up ecosystem is much more developed than that of most Latin American cities and has positioned itself as an innovative leader in the region. Factors that have enabled this include its status as the largest economy in Latin America, which allows it to have a large local digital market, and the possibility of benefiting from strengthened accelerators and incubators. For example, the accelerator ‘Latitud’, a platform that supports early-stage founders with training through a selective scholarship programme, offers tailored resources for local start-ups like Latitud Go. It has already invested in more than ninety companies in the region (BBVA, 2022). As a result, the city is home to twelve of the country’s seventeen unicorns. It is also remarkable that the combination of public and private support networks, entrepreneurship hubs and talent without borders has given rise to the solid start-up ecosystem of São Paulo, mature enough to withstand future challenges.

Latin American countries have experienced rapid growth in terms of internet access and enjoy high concentrations of internet users and daily digital content use, with an average of 9.3 hours per day (Atlantico, 2023). The region has all the necessary potential to facilitate exponential growth for digital and technology-driven ventures, and it is home to 650 million people. Therefore, efforts must continue in order to move forward to a more robust digital ecosystem while reducing the country’s extreme socioeconomic inequality.

1.2.7 Africa

Africa’s innovation, technology, entrepreneurship and start-up landscape has experienced a remarkable transformation thanks to digital connectivity and young demographics prone to experimentation and innovation. Observers have noted that entrepreneurship in Africa has experienced an exponential upsurge (Helaly, Reference Helaly2023). The World Economic Forum (WEF) named seven African tech start-ups among the 100 most promising technology pioneers of 2022 (Disrupt Africa, 2023). Among these were Alerzo (Nigeria, 2020; on-demand inventory distribution and financial services), Dove Air (South Africa; urban air mobility technology, 2020) and Vendease (Nigeria; marketplace, 2020).

Africa’s technological infrastructure has been undergoing a transformation as governments are taking proactive steps to support business efforts related to innovation and the knowledge economy, benefiting from the digitalisation trend (see Chapter 10). The COVID-19 pandemic sharply accelerated African digital innovation, and demand for more and better digital infrastructure increased across the continent. Industry-related regulatory policy changes made in countries of sub-Saharan Africa during the pandemic emphasised digital accessibility (Feydeau et al., Reference Feydeau, Menski and Perry2022). The result was a rise in the consumption of online services, increased connectivity and the proposal of new, more ambitious approaches to public policies, in the hope that new technologies could provide a leapfrogging opportunity for Africa. African governments are taking proactive steps to support entrepreneurial endeavours, and they have a growing interest in leveraging the region’s economic growth with the opportunities offered by technology to boost new business (Business Insider Africa, 2023). Infrastructure development, policy reforms and initiatives to promote digital literacy contribute to the enabling environment for start-ups to flourish. International organisations and private investors also recognise the potential of African businesses and provide support through funding and mentorship programmes.

West Africa attracted the largest proportion of venture capital deal volume in Africa in 2022: 30 per cent. Nigeria was the most active country by volume at 22 per cent and drove up this overall proportion. The most attractive sectors included fintech, health tech, agritech. Most investors in Africa were international, with African investors representing just 23 per cent (Venture Capital in Africa Report, 2022). Of all VC deals in 2022, 78 per cent were in technology-enabled companies operating across a variety of sectors plus fintechs. These absorbed 31 per cent of the deal volume and 42 per cent of the deal value. Besides Nigeria, where Lagos is the African leader in entrepreneurial ecosystems value and early-stage financing, South Africa, Mauritius and Kenya are emerging as promising entrepreneurial hubs.

Nigeria emerges as a reference point for start-up development due to a combination of factors that have boosted its entrepreneurial ecosystem. The country has experienced a surge in investment both from local and international sources, reflecting the growing confidence in its start-up ecosystem. The presence of dynamic tech hubs and incubators, such as Lagos’ YabaCon Valley, provides essential support, mentorship and resources for budding entrepreneurs (Hayden, Reference Hayden2022).

Africa reportedly had seven unicorns in 2024: the Nigerian Interswitch, a digital payment and commerce solution and the oldest African unicorn; Flutterwave, a Nigerian application programming interface (API)-driven platform, aggregating payment gateways across Africa; Opay, a mobile payments platform; Wave, a full-stack digital mobile money wallet initially focused on Francophone Africa; Andela, a talent marketplace; Chipper Cash, a cross-border, peer-to-peer money transfer platform; and MNT-Halan, a money lending fintech (Today Africa, 2024).

The world increasingly looks towards innovation and start-ups as drivers of economic growth and transformation. As this happens, Africa hopes to seize the opportunity to not only bridge the digital divide but also become a remarkable success story due to its tech and start-up ecosystems.

1.3 The Importance of Unicorns from Emerging Economies

Emerging economies are characterised by low to middle income per capita and not fully consolidated and competitive industrial sectors. In terms of investment opportunities, emerging markets distinguish themselves by their high returns and low covariance with global market factors, among other things (Goetzmann & Jorion, Reference Goetzmann and Jorion1999). Emerging economies were responsible for more than 50 per cent of the world’s economic growth in 2023 (CFI Team, 2023). This strong growth translates into huge potential for business opportunities, including unicorns and technology-driven start-ups with exponential transformational impact.

The interconnectedness experienced in the 2000s is partly responsible for this growth and, thus, the emergence of start-ups and unicorns in the Global South. The world experienced a peak in globalisation between 2007 and 2011 in terms of trade and foreign investment. Two of the main factors that drove this increasing interdependence among nations were technology developments and the reduction of communication and transportation costs (Witt, Reference Witt2019). The increase in trade, foreign investment and communications created opportunities for many emerging economies. In the specific case of unicorns, these companies were created under one of two logics. The first meant taking things that work somewhere and adapting them to work under the unique conditions of the Global South. The second involved building new and better ways of doing things to solve local, regional and global problems. The high degree of interconnectedness, enhanced access to capital and expansion of the technological frontier all contributed to the emergence and increase in the number of unicorns from the Global South.

This chapter has presented a brief overview of the concept of unicorns and explained what makes them unique. On one hand, they are relevant because new technologies and lower costs have allowed scalable and competitive technology-based services to solve specific problems that are intrinsic to the locations in which they are created. These types of new companies offer improved, more attractive solutions or inclusive solutions for traditionally underserved segments. On the other hand, unicorns in emerging markets are different from other companies because, due to the unique conditions of the Global South under which they are created, the need to add value has brought about innovations that lead to disruption in various sectors. Chapter 2 further enriches and expands on these ideas presenting a theoretical framework. Chapter 3 and Chapter 4 focus on understanding the geography and main features of unicorns at a global level. Furthermore, from Chapter 5 to Chapter 13 we zoom into the key determinants of entrepreneurial ecosystems and their unicorns across the emerging economies of the Global South: Latin America, MENA, Eastern Europe and Russia, Africa, India, China, and Southeast Asia. Chapter 14 concludes by systematising the key insights, posing new research questions and outlining a future research agenda.

COVID-19 played a key role in accelerating technological developments in many of these regions. Specific locations stand as central nodal elements in the process of unicorn creation in the Global South among which São Paulo (Brazil), Lagos (Nigeria), Beijing (China) and Singapore (Southeast Asia) stand out. In such places, governments play a key role in enhancing the conditions for start-up creation and unicorn scale up through targeted policies, tax regulation or direct financing to compensate for some of the disadvantages and complement some of the natural advantages of the emerging economies. These advantages can include sizable markets, entrepreneurial spirit, VC capital availability, human talent and training, and a community of determined entrepreneurs. Unicorns from emerging economies have a transformational role in the public and private discourse on human progress and prosperity. The growing number of start-ups founded and located in emerging markets represents a change in how these economies add value. They change the focus from commodity extraction to technology-based services, igniting economic growth, business opportunities, job creation, services exports and other ways of connecting the entrepreneurial ecosystems of the Global South to the global knowledge-based economy. Such a perspective brings hope and new-found confidence to millions of young and creative minds around the world. There is nothing more transformational and important to study and understand than the human spirit that brings change to the world on the wings of a unicorn.