1. Introduction

In this article, all stochastic quantities are defined on a complete probability space  $(\Omega, \mathcal{F}, (\mathcal{F}_t)_{t\geq0}, P)$. The filtration

$(\Omega, \mathcal{F}, (\mathcal{F}_t)_{t\geq0}, P)$. The filtration  $(\mathcal{F}_t)_{t\geq0}$ is right-continuous, and all stochastic processes throughout the article are adapted.

$(\mathcal{F}_t)_{t\geq0}$ is right-continuous, and all stochastic processes throughout the article are adapted.

After the global financial crisis triggered by the collapse of Lehman Brothers, the International Monetary Fund, the Bank for International Settlements, and the Financial Stability Board cooperated to establish an initial framework for evaluating the systemic importance of financial institutions in 2,009. In this framework, systemic risk was defined as “[the] risk of disruption to financial services that (i) [is] caused by an impairment of all or parts of the financial system and (ii) has the potential to have serious negative consequences for the real economy.” From the viewpoint of policymakers, risk measures are vital for developing a comprehensive and efficient regulatory framework to manage systemic risk and enhance financial stability. Based on this, numerous scholars have proposed a series of systemic risk measures, such as Value-at-Risk (VaR), Conditional Tail Expectation (CTE), Contagion Risk (CR), Expected shortfall (ES), and Joint Expected Shortfall (JES), as demonstrated in works such as [Reference Cai, Einmahl, de Haan and Zhou3, Reference Hua and Joe15, Reference Ji, Tan and Yang16, Reference Li, Luo and Yao23], [Reference Landsman, Makov and Tomer19] and [Reference Zhou, Dhaene and Yao31]. In practice, when there are various dependence structures among individual risks, calculating the analytical expressions of systemic risk measures becomes challenging. Therefore, many researchers have shifted their focus to investigating asymptotic expressions with the help of Extreme Value Theory, as shown in works such as [Reference Asimit, Furman, Tang and Vernic1, Reference Chen and Liu4, Reference Fu and Liu9, Reference Fu, Ni and Chen10, Reference Hao and Tang14, Reference Liu and Yang24] and [Reference Tang27]. A significant point to note is that the systemic risk measures mentioned above have traditionally been studied within a static framework. Thus, recent research has extended these measures into continuous-time risk models, as demonstrated by [Reference Li22]. Inspired by [Reference Guo and Wang11], we assume that for any integer  $k\in[1,d]$, the loss process

$k\in[1,d]$, the loss process  $L_k(t)$ of the k-th line of business can be modeled by

$L_k(t)$ of the k-th line of business can be modeled by

\begin{align}

L_k(t)=\sum_{i=1}^{N_k(t)}X_{ki}e^{-\xi(\tau_{ki})},

\end{align}

\begin{align}

L_k(t)=\sum_{i=1}^{N_k(t)}X_{ki}e^{-\xi(\tau_{ki})},

\end{align} where d denotes the total number of lines of business, Xki describes the i-th loss in the k-th line of business whose arrival times τki constitute a loss-number process  $N_k(t)$, and

$N_k(t)$, and  $\xi(t)$ denotes a general càdlàg process, which measures the exposure to common macroeconomic factors. Consequently, the aggregate loss process S(t) can be expressed as follows:

$\xi(t)$ denotes a general càdlàg process, which measures the exposure to common macroeconomic factors. Consequently, the aggregate loss process S(t) can be expressed as follows:

\begin{align}

S(t)=\sum_{k=1}^{d}L_k(t)=\sum_{k=1}^{d}\sum_{i=1}^{N_k(t)}X_{ki}e^{-\xi(\tau_{ki})} .

\end{align}

\begin{align}

S(t)=\sum_{k=1}^{d}L_k(t)=\sum_{k=1}^{d}\sum_{i=1}^{N_k(t)}X_{ki}e^{-\xi(\tau_{ki})} .

\end{align} For a general risk variable X, its VaR at level  $0 \lt q \lt 1$ is defined by

$0 \lt q \lt 1$ is defined by  $VaR_X(q)=\inf\{s\in\mathbb{R}: P(X\leq s)\geq q\}$. Motivated by relations (1.3) and (1.4) in [Reference Chen and Liu4], in the context of ES capital allocations, for any integer

$VaR_X(q)=\inf\{s\in\mathbb{R}: P(X\leq s)\geq q\}$. Motivated by relations (1.3) and (1.4) in [Reference Chen and Liu4], in the context of ES capital allocations, for any integer  $k\in[1,d]$, we introduce two risk measures based on our multivariate continuous-time risk model: the systemic expected shortfall

$k\in[1,d]$, we introduce two risk measures based on our multivariate continuous-time risk model: the systemic expected shortfall  $SES_k(t,q)$ and the marginal expected shortfall

$SES_k(t,q)$ and the marginal expected shortfall  $MES_k(t,q)$, as described below:

$MES_k(t,q)$, as described below:

\begin{align}&SES_k(t,q)=\mathbb{E}\left((L_k(t)-A_k(t,q))_+~|~S(t) \gt A(t,q)\right),

\end{align}

\begin{align}&SES_k(t,q)=\mathbb{E}\left((L_k(t)-A_k(t,q))_+~|~S(t) \gt A(t,q)\right),

\end{align}and

\begin{align}&MES_k(t,q)=\mathbb{E}\left(L_k(t)~|~S(t) \gt A(t,q)\right),

\end{align}

\begin{align}&MES_k(t,q)=\mathbb{E}\left(L_k(t)~|~S(t) \gt A(t,q)\right),

\end{align} where the capital allocation of the k-th line of business  $A_k(t,q)$ and the total capital allocation

$A_k(t,q)$ and the total capital allocation  $A(t,q)$ can be described by

$A(t,q)$ can be described by

\begin{align}&A_k(t,q)=\mathbb{E}\left(L_k(t)~|~S(t) \gt VaR_S(t,q)\right),

\end{align}

\begin{align}&A_k(t,q)=\mathbb{E}\left(L_k(t)~|~S(t) \gt VaR_S(t,q)\right),

\end{align}and

\begin{align}&A(t,q)=\sum_{k=1}^{d}A_k(t,q)=\mathbb{E}\left(S(t)~|~S(t) \gt VaR_S(t,q)\right).

\end{align}

\begin{align}&A(t,q)=\sum_{k=1}^{d}A_k(t,q)=\mathbb{E}\left(S(t)~|~S(t) \gt VaR_S(t,q)\right).

\end{align} Here and throughout the article, we use  $x_+=x\mathbb{I}_{\{x\geq0\}}$, where

$x_+=x\mathbb{I}_{\{x\geq0\}}$, where  $\mathbb{I}_A$ denotes the indicator function of an event A.

$\mathbb{I}_A$ denotes the indicator function of an event A.

The multivariate continuous-time risk model (1.1) that includes a general càdlàg process highlights the shared financial environment and the correlations among individual businesses. The general càdlàg processes are a class of stochastic processes characterized by right continuity and left limits, with significant applications in mathematics, finance, and engineering. The càdlàg processes are often determined by some important investment return processes such as the fractional Brownian motions, the Vasicek model, the Cox–Ingersoll–Ross model (CIR), and the Heston model, as shown in [Reference Cheng, Konstantinides and Wang6, Reference Guo and Wang11] and [Reference Guo and Wang12]. As indicated by Section 5 of [Reference Cheng, Konstantinides and Wang6] and Section 3 of [Reference Fu and Li8], it is evident that when a general càdlàg process is determined by the classical geometric Brownian motion or the Vasicek model, the value of the general càdlàg process at each time point can be directly calculated. Nevertheless, it is not practical to calculate the value of the general càdlàg process at each time point directly when the general càdlàg process is determined by more complex models such as the CIR model or the Stochastic Volatility model et al. In addition, it is emphasized in Section 3 of [Reference Guo and Wang11] that calculating the expectation related to the general càdlàg process is a challenging task. Consequently, these limitations restrict the application of the general càdlàg process in current risk theory.

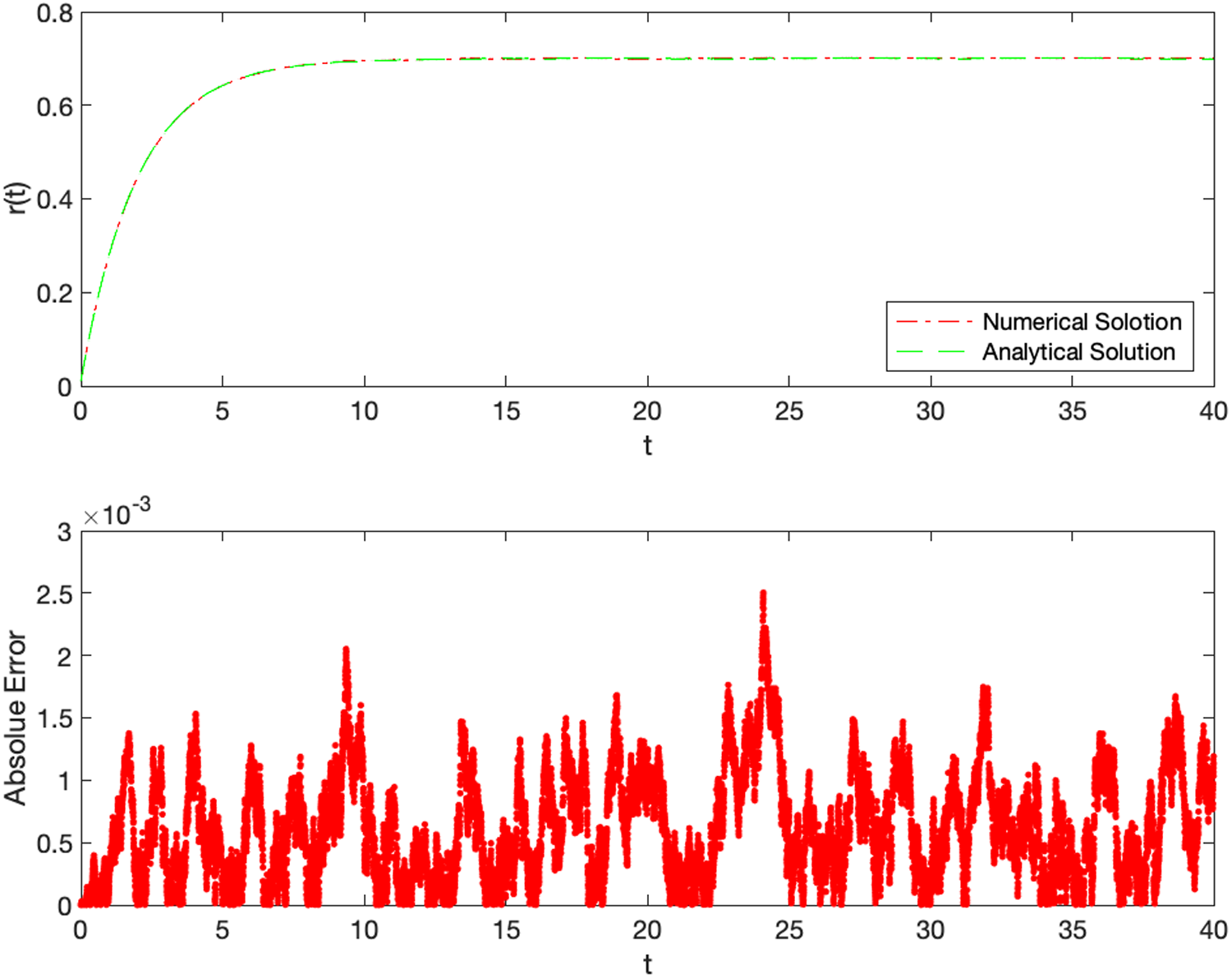

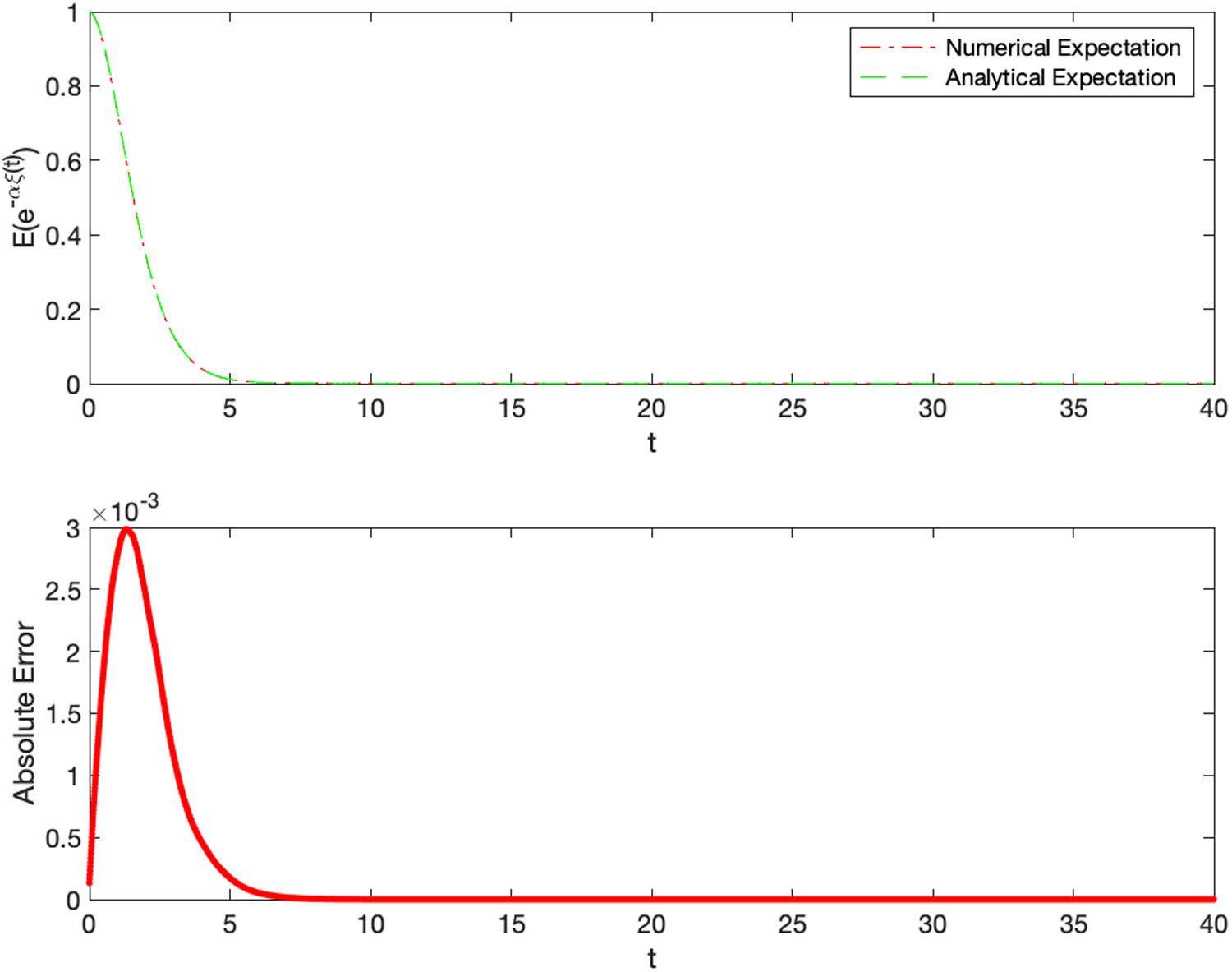

A key point to mention is that the càdlàg process often connects with some complex and specific stochastic differential equations (SDEs). To overcome the challenge of direct calculation, we employ the explicit order 3.0 weak scheme, which is widely used for solving SDEs. A significant point to note is that the explicit order 3.0 weak scheme does not involve derivatives of the drift and diffusion coefficients, which allows us to approximate the values of the càdlàg process at discrete time points in a more convenient way. Additionally, the explicit order 3.0 weak scheme can be also viewed as an alternative method for approximating the expectation related to the general càdlàg process. Therefore, this numerical method contributes to verifying moment condition related to the general càdlàg process from a numerical standpoint and to understanding the sensitivity of parameters. Owing to these advantages, we believe that the explicit order 3.0 weak scheme extends the applicability of the general càdlàg process in the field of risk theory. For detailed information on the explicit order 3.0 weak scheme, we refer the reader to [Reference Kloeden and Platen17, Reference Platen25], among others.

In previous research on systemic risk measures, the study of dependent losses has primarily focused on two different aspects: asymptotic independence and asymptotic dependence. For instance, [Reference Liu and Yang24] utilized Extreme Value Theory to investigate the asymptotic expressions of systemic risk measures with asymptotically independent losses. Common asymptotically independent structures include pairwise strong quasi-asymptotic independence, Gaussian copula, and the Johnson-Kotz iterated Farlie-Gumbel-Morgenstern copula, as discussed by [Reference Fu and Li8, Reference Guo, Wang and Yang13], [Reference Li20] and [Reference Li21]. Similarly, [Reference Hao and Tang14] has examined the asymptotic relationships of CTE with asymptotically dependent losses. Examples of asymptotically dependent structures can be found in [Reference Asimit, Furman, Tang and Vernic1, Reference Chen and Yuan5, Reference Konstantinides and Li18] and [Reference Li22]. In this article, we explore extremes for  $SES_k(t,q)$ and

$SES_k(t,q)$ and  $MES_k(t,q)$ within a framework that considers wide dependence structures among losses, concluding pairwise strong quasi-asymptotic independence and multivariate regular variation.

$MES_k(t,q)$ within a framework that considers wide dependence structures among losses, concluding pairwise strong quasi-asymptotic independence and multivariate regular variation.

The current article extends the existing works on systemic risk measures in four main aspects. First, compare with [Reference Li22] that explores the extremes for systemic risk measures in a multivariate continuous-time risk model with a constant interest rate, we introduce a general càdlàg process into the multivariate continuous-time risk model. Since the general càdlàg process lacks independent and stationary incremental properties, it adds great difficulty to the theoretical proof, but it also makes the  $SES_k(t,q)$ and

$SES_k(t,q)$ and  $MES_k(t,q)$ more practical. Our results reveal that the general càdlàg process has a significant impact on the

$MES_k(t,q)$ more practical. Our results reveal that the general càdlàg process has a significant impact on the  $SES_k(t,q)$ and

$SES_k(t,q)$ and  $MES_k(t,q)$. Second, we propose a mild moment assumption for the general càdlàg process. This assumption can be easily satisfied by selecting appropriate model parameters when the general càdlàg process is determined by some investment return processes, such as the fractional Brownian motions, the Vasicek model, the CIR model, and the Heston model. In addition, compared to [Reference Cheng, Konstantinides and Wang6] and [Reference Guo and Wang11], who verify the conditions associated with the general càdlàg process from a theoretical viewpoint, our numerical findings suggest that this moment assumption is well-founded from a numerical standpoint. Third, we note that during the European sovereign debt crisis, the high levels of debt in several European countries, along with the interconnectedness of European banks, created a contagion effect that posed a threat to the stability of the entire Eurozone and had widespread impacts on global financial markets. In this context, we explore the extremes for

$MES_k(t,q)$. Second, we propose a mild moment assumption for the general càdlàg process. This assumption can be easily satisfied by selecting appropriate model parameters when the general càdlàg process is determined by some investment return processes, such as the fractional Brownian motions, the Vasicek model, the CIR model, and the Heston model. In addition, compared to [Reference Cheng, Konstantinides and Wang6] and [Reference Guo and Wang11], who verify the conditions associated with the general càdlàg process from a theoretical viewpoint, our numerical findings suggest that this moment assumption is well-founded from a numerical standpoint. Third, we note that during the European sovereign debt crisis, the high levels of debt in several European countries, along with the interconnectedness of European banks, created a contagion effect that posed a threat to the stability of the entire Eurozone and had widespread impacts on global financial markets. In this context, we explore the extremes for  $SES_k(t,q)$ and

$SES_k(t,q)$ and  $MES_k(t,q)$ under the framework of dependence structures, namely pairwise strong quasi-asymptotic independence and multivariate regular variation. Our results indicate that the influence of the pairwise strong quasi-asymptotically independence structure among losses on the

$MES_k(t,q)$ under the framework of dependence structures, namely pairwise strong quasi-asymptotic independence and multivariate regular variation. Our results indicate that the influence of the pairwise strong quasi-asymptotically independence structure among losses on the  $SES_k(t,q)$ and

$SES_k(t,q)$ and  $MES_k(t,q)$ is minimal, while the property of multivariate regular variation among losses significantly impacts the

$MES_k(t,q)$ is minimal, while the property of multivariate regular variation among losses significantly impacts the  $SES_k(t,q)$ and

$SES_k(t,q)$ and  $MES_k(t,q)$. Finally, we note that operational risks and large insurance losses are identified as having heavy tails, and that in the 2,008 financial crisis, extreme risks are shown to be contagious. Based on this, we aim to discuss the interplay of dependence structures and heavy-tailedness with the help of the explicit order 3.0 weak scheme. Our numerical studies demonstrate that while the asymptotic dependence structure among losses plays a role in

$MES_k(t,q)$. Finally, we note that operational risks and large insurance losses are identified as having heavy tails, and that in the 2,008 financial crisis, extreme risks are shown to be contagious. Based on this, we aim to discuss the interplay of dependence structures and heavy-tailedness with the help of the explicit order 3.0 weak scheme. Our numerical studies demonstrate that while the asymptotic dependence structure among losses plays a role in  $SES_k(t,q)$ and

$SES_k(t,q)$ and  $MES_k(t,q)$, the heavy-tailed property has a more substantial effect.

$MES_k(t,q)$, the heavy-tailed property has a more substantial effect.

In the rest of this article, Section 2 introduces the mild moment condition, as well as dependence structures. Section 3 states our main results. Section 4 proves the main results after introducing some useful lemmas. Section 5 applies the explicit order 3.0 weak scheme to perform numerical studies.

2. Preliminaries and assumptions

2.1. Preliminaries

Throughout this article, C represents a generic constant, which may vary with the context. Hereafter, all limit relations are for  $x\rightarrow\infty$ or

$x\rightarrow\infty$ or  $q\uparrow 1$ unless stated otherwise. For two positive functions

$q\uparrow 1$ unless stated otherwise. For two positive functions  $a(\cdot )$ and

$a(\cdot )$ and  $b(\cdot )$, we write

$b(\cdot )$, we write  $a(x)\lesssim b(x)$ if

$a(x)\lesssim b(x)$ if  $\limsup\limits_{x\rightarrow\infty}\frac{a(x)}{b(x)}\leq 1$;

$\limsup\limits_{x\rightarrow\infty}\frac{a(x)}{b(x)}\leq 1$;  $a(x) \gt rsim b(x)$ if

$a(x) \gt rsim b(x)$ if  $\liminf\limits_{x\rightarrow\infty}\frac{a(x)}{b(x)}\geq 1$; and

$\liminf\limits_{x\rightarrow\infty}\frac{a(x)}{b(x)}\geq 1$; and  $a(x)\sim b(x)$ if

$a(x)\sim b(x)$ if  $\lim\limits_{x\rightarrow\infty}\frac{a(x)}{b(x)}=1$. Also, we write

$\lim\limits_{x\rightarrow\infty}\frac{a(x)}{b(x)}=1$. Also, we write  $a(x)\asymp b(x)$ if

$a(x)\asymp b(x)$ if  $0 \lt \liminf\limits_{x\rightarrow\infty}\frac{a(x)}{b(x)} \lt \limsup\limits_{x\rightarrow\infty}\frac{a(x)}{b(x)} \lt \infty$. Furthermore, for two positive bivariate functions

$0 \lt \liminf\limits_{x\rightarrow\infty}\frac{a(x)}{b(x)} \lt \limsup\limits_{x\rightarrow\infty}\frac{a(x)}{b(x)} \lt \infty$. Furthermore, for two positive bivariate functions  $a(\cdot,\cdot)$ and

$a(\cdot,\cdot)$ and  $b(\cdot,\cdot)$ satisfying

$b(\cdot,\cdot)$ satisfying  $0\leq L_1\leq \liminf_{x\rightarrow\infty}\inf_{t\in\Delta}\frac{a(x,t)}{b(x,t)}\leq \limsup_{x\rightarrow\infty}\sup_{t\in\Delta}\frac{a(x,t)}{b(x,t)}\leq L_2 \lt \infty,~\Delta\neq\emptyset$. We say the relation

$0\leq L_1\leq \liminf_{x\rightarrow\infty}\inf_{t\in\Delta}\frac{a(x,t)}{b(x,t)}\leq \limsup_{x\rightarrow\infty}\sup_{t\in\Delta}\frac{a(x,t)}{b(x,t)}\leq L_2 \lt \infty,~\Delta\neq\emptyset$. We say the relation  $a(x,t)\asymp b(x,t)$ holds uniformly for all

$a(x,t)\asymp b(x,t)$ holds uniformly for all  $t\in\Delta$ if

$t\in\Delta$ if  $0 \lt L_1\leq L_2 \lt \infty$;

$0 \lt L_1\leq L_2 \lt \infty$;  $a(x,t)\lesssim b(x,t)$ holds uniformly for all

$a(x,t)\lesssim b(x,t)$ holds uniformly for all  $t\in\Delta$ if

$t\in\Delta$ if  $L_2\leq1$;

$L_2\leq1$;  $a(x,t) \gt rsim b(x,t)$ holds uniformly for all

$a(x,t) \gt rsim b(x,t)$ holds uniformly for all  $t\in\Delta$ if

$t\in\Delta$ if  $L_1\geq1$; and

$L_1\geq1$; and  $a(x,t)\sim b(x,t)$ holds uniformly for all

$a(x,t)\sim b(x,t)$ holds uniformly for all  $t\in\Delta$ if

$t\in\Delta$ if  $L_1=L_2=1$. The vectors are denoted by bold letters and assumed to be d-dimensional, as for example,

$L_1=L_2=1$. The vectors are denoted by bold letters and assumed to be d-dimensional, as for example,  $\boldsymbol{a}=(a_1,a_2,\ldots,a_d)$. Furthermore, we denote

$\boldsymbol{a}=(a_1,a_2,\ldots,a_d)$. Furthermore, we denote  $\boldsymbol{1}=(1,1,\ldots,1)$. For for any integer

$\boldsymbol{1}=(1,1,\ldots,1)$. For for any integer  $k\in[1,d]$, the notation Ik denotes the unit vector whose k-th component is 1, so

$k\in[1,d]$, the notation Ik denotes the unit vector whose k-th component is 1, so  $\boldsymbol{1}=\sum_{k=1}^{d}\boldsymbol{I}_{k}$ is obtained.

$\boldsymbol{1}=\sum_{k=1}^{d}\boldsymbol{I}_{k}$ is obtained.

At first, we recall some related classes of heavy-tailed distributed functions (distribution function). By definition, a distribution function belongs to the class of dominated variation, denoted by  $F\in \mathcal{D}$, if F has an ultimate right tail and for any

$F\in \mathcal{D}$, if F has an ultimate right tail and for any  $y\in(0,1)$,

$y\in(0,1)$,

\begin{equation*}

\limsup_{x\rightarrow\infty}\frac{\overline{F}(xy)}{\overline{F}(x)} \lt \infty.

\end{equation*}

\begin{equation*}

\limsup_{x\rightarrow\infty}\frac{\overline{F}(xy)}{\overline{F}(x)} \lt \infty.

\end{equation*} An important subclass of the class  $\mathcal{D}$ is the class

$\mathcal{D}$ is the class  $\mathcal{R}_{-\alpha}$ of regularly varying functions specified by

$\mathcal{R}_{-\alpha}$ of regularly varying functions specified by

\begin{equation*}

\lim_{x\rightarrow\infty}\frac{\overline{F}(xy)}{\overline{F}(x)}=y^{-\alpha},~\mathrm{for}~y \gt 0.

\end{equation*}

\begin{equation*}

\lim_{x\rightarrow\infty}\frac{\overline{F}(xy)}{\overline{F}(x)}=y^{-\alpha},~\mathrm{for}~y \gt 0.

\end{equation*} For any distribution  $F\in \mathcal{R}_{-\alpha}$ with α > 0, Theorem 1.5 of [Reference Bingham, Goldie and Teugels2] ensures that

$F\in \mathcal{R}_{-\alpha}$ with α > 0, Theorem 1.5 of [Reference Bingham, Goldie and Teugels2] ensures that

\begin{align}

\lim_{x\rightarrow\infty} \sup_{y\in[b,\infty)} \left|\frac{\overline{F}(xy)}{\overline{F}(x)}-y^{-\alpha}\right|=1,

\end{align}

\begin{align}

\lim_{x\rightarrow\infty} \sup_{y\in[b,\infty)} \left|\frac{\overline{F}(xy)}{\overline{F}(x)}-y^{-\alpha}\right|=1,

\end{align} holds for arbitrarily fixed  $0 \lt b \lt \infty$. According to Karamata’s Theorem, if

$0 \lt b \lt \infty$. According to Karamata’s Theorem, if  $F\in\mathcal{R}_{-\alpha}$ for some α > 1, then,

$F\in\mathcal{R}_{-\alpha}$ for some α > 1, then,

\begin{align*}

\lim_{x\rightarrow\infty}\frac{\int_{x}^{\infty}\overline{F}(y)dy}{x\overline{F}(x)}=\frac{1}{\alpha-1}.

\end{align*}

\begin{align*}

\lim_{x\rightarrow\infty}\frac{\int_{x}^{\infty}\overline{F}(y)dy}{x\overline{F}(x)}=\frac{1}{\alpha-1}.

\end{align*} In addition, a distribution function F is said to be long-tailed, denoted by  $F\in\mathcal{L}$, if F has an ultimate right tail and for any

$F\in\mathcal{L}$, if F has an ultimate right tail and for any  $b\in\mathbb{R}$,

$b\in\mathbb{R}$,

\begin{align*}

\lim_{x\rightarrow\infty}\frac{\overline{F}(x+b)}{\overline{F}(x)}=1.

\end{align*}

\begin{align*}

\lim_{x\rightarrow\infty}\frac{\overline{F}(x+b)}{\overline{F}(x)}=1.

\end{align*} Next, we introduce the upper and lower Matuszewska indices:  $J_{F}^{+}=-\lim_{y\rightarrow\infty}\frac{\log{\overline{F_*}(y)}}{\log{y}} $ and

$J_{F}^{+}=-\lim_{y\rightarrow\infty}\frac{\log{\overline{F_*}(y)}}{\log{y}} $ and  $J_{F}^{-}=-\lim_{y\rightarrow\infty}\frac{\log{\overline{F^*}(y)}}{\log{y}}$, where

$J_{F}^{-}=-\lim_{y\rightarrow\infty}\frac{\log{\overline{F^*}(y)}}{\log{y}}$, where  $ \overline{F_*}(y)=:\liminf_{x\rightarrow\infty}\frac{\overline{F}(xy)}{\overline{F}(x)}$ and

$ \overline{F_*}(y)=:\liminf_{x\rightarrow\infty}\frac{\overline{F}(xy)}{\overline{F}(x)}$ and  $\overline{F^*}(y)=:\limsup_{x\rightarrow\infty}\frac{\overline{F}(xy)}{\overline{F}(x)}$. Generally,

$\overline{F^*}(y)=:\limsup_{x\rightarrow\infty}\frac{\overline{F}(xy)}{\overline{F}(x)}$. Generally,  $0\leq{J_{F}^{-}}\leq{J_{F}^{+}}\leq\infty$. Especially, if

$0\leq{J_{F}^{-}}\leq{J_{F}^{+}}\leq\infty$. Especially, if  $F\in \mathcal{D}$, then

$F\in \mathcal{D}$, then  ${J_{F}^{+}} \lt \infty$, and if

${J_{F}^{+}} \lt \infty$, and if  $F\in \mathcal{R}_{-\alpha}$ with α > 0, then

$F\in \mathcal{R}_{-\alpha}$ with α > 0, then  ${J_{F}^{-}}={J_{F}^{+}}={\alpha}$.

${J_{F}^{-}}={J_{F}^{+}}={\alpha}$.

Lastly, we introduce two different dependence structures: Definition 2.1, which is a well-known asymptotic independence structure, and Definition 2.2, which is a common asymptotic dependence structure.

Definition 2.1.

Let Y 1, Y 2, … be non-negative random variables. We say that Y 1, Y 2, … are pairwise strong quasi-asymptotically independent (pSQAI), if, for any i ≠ j,

\begin{align*}

\lim_{\min\{y_i,~y_j\}\rightarrow\infty}P(Y_i \gt y_i~|~Y_j \gt y_j)=0.

\end{align*}

\begin{align*}

\lim_{\min\{y_i,~y_j\}\rightarrow\infty}P(Y_i \gt y_i~|~Y_j \gt y_j)=0.

\end{align*}For more details on pSQAI, see [Reference Li20].

Definition 2.2.

For a non-negative random vector  $(Y_1, \ldots, Y_d)$, assume that there exists some α > 0, a distribution function

$(Y_1, \ldots, Y_d)$, assume that there exists some α > 0, a distribution function  $G\in \mathcal{R}_{-\alpha}$, and some Radon measure υ, which satisfies that for any Borel set Q away from 0,

$G\in \mathcal{R}_{-\alpha}$, and some Radon measure υ, which satisfies that for any Borel set Q away from 0,  $\upsilon~(Q) \gt 0$ and assigns zero mass to the boundary

$\upsilon~(Q) \gt 0$ and assigns zero mass to the boundary  $\partial Q$, such that the following vague convergence holds as

$\partial Q$, such that the following vague convergence holds as  $x\longrightarrow\infty$:

$x\longrightarrow\infty$:

\begin{equation}

\frac{P\left(\frac{(Y_1,Y_2,\ldots, Y_d)}{x}\in\cdot\right)}{\overline{G}(x)}\rightarrow \upsilon(\cdot).

\end{equation}

\begin{equation}

\frac{P\left(\frac{(Y_1,Y_2,\ldots, Y_d)}{x}\in\cdot\right)}{\overline{G}(x)}\rightarrow \upsilon(\cdot).

\end{equation} In the context of Definition 2.2, we write  $(Y_1,Y_2,\ldots, Y_d)\in MRV_d(\alpha, G, \upsilon)$. For any Borel set Q away from 0, the measure υ exhibits the following property of homogeneity:

$(Y_1,Y_2,\ldots, Y_d)\in MRV_d(\alpha, G, \upsilon)$. For any Borel set Q away from 0, the measure υ exhibits the following property of homogeneity:

\begin{align}

\upsilon(yQ)=y^{-\alpha}\upsilon(Q),~\mathrm{for~any}~y \gt 0.

\end{align}

\begin{align}

\upsilon(yQ)=y^{-\alpha}\upsilon(Q),~\mathrm{for~any}~y \gt 0.

\end{align} Besides, if  $\upsilon((\boldsymbol{1},\boldsymbol{\infty}]) \gt 0$, then we have

$\upsilon((\boldsymbol{1},\boldsymbol{\infty}]) \gt 0$, then we have

\begin{align}

\lim_{x\rightarrow\infty}\frac{P\left(\bigcap_{k=1}^{d}\{Y_k \gt b_kx\}\right)}{\overline{G}(x)}=\upsilon((\boldsymbol{b},\boldsymbol{\infty}]) \gt 0, \mathrm{for~any~\boldsymbol{b}~away~from~\boldsymbol{0}},

\end{align}

\begin{align}

\lim_{x\rightarrow\infty}\frac{P\left(\bigcap_{k=1}^{d}\{Y_k \gt b_kx\}\right)}{\overline{G}(x)}=\upsilon((\boldsymbol{b},\boldsymbol{\infty}]) \gt 0, \mathrm{for~any~\boldsymbol{b}~away~from~\boldsymbol{0}},

\end{align}and

\begin{align}

\lim_{x\rightarrow\infty}\frac{P(Y_k \gt x)}{\overline{G}(x)}=\upsilon((\boldsymbol{I}_k,\boldsymbol{\infty}]) \gt 0,~\mathrm{for~any~integer}~k\in[1,d].

\end{align}

\begin{align}

\lim_{x\rightarrow\infty}\frac{P(Y_k \gt x)}{\overline{G}(x)}=\upsilon((\boldsymbol{I}_k,\boldsymbol{\infty}]) \gt 0,~\mathrm{for~any~integer}~k\in[1,d].

\end{align} Relation (2.5) indicates that  $Y_1,Y_2$,…, and Yd have regularly varying tails and are mutually tail-equivalent. From relations (2.4) and (2.5), if

$Y_1,Y_2$,…, and Yd have regularly varying tails and are mutually tail-equivalent. From relations (2.4) and (2.5), if  $Y_1,Y_2$,…, and Yd have a joint distribution exhibiting multivariate regular variation with some Radon measure υ such that

$Y_1,Y_2$,…, and Yd have a joint distribution exhibiting multivariate regular variation with some Radon measure υ such that  $\upsilon((\boldsymbol{1},\boldsymbol{\infty}]) \gt 0$, we have for any

$\upsilon((\boldsymbol{1},\boldsymbol{\infty}]) \gt 0$, we have for any  $1\leq i \lt j\leq d$,

$1\leq i \lt j\leq d$,

\begin{align*}

\lim_{x\rightarrow\infty}\frac{P(Y_i \gt x,Y_j \gt x)}{P(Y_i \gt x)}= \lim_{x\rightarrow\infty}\frac{P(Y_i \gt x,Y_j \gt x)}{\overline{G}(x)}\frac{\overline{G}(x)}{P(Y_i \gt x)}\geq \frac{\upsilon((\boldsymbol{I},\boldsymbol{\infty}])}{\upsilon((\boldsymbol{I}_i,\boldsymbol{\infty}])} \gt 0.

\end{align*}

\begin{align*}

\lim_{x\rightarrow\infty}\frac{P(Y_i \gt x,Y_j \gt x)}{P(Y_i \gt x)}= \lim_{x\rightarrow\infty}\frac{P(Y_i \gt x,Y_j \gt x)}{\overline{G}(x)}\frac{\overline{G}(x)}{P(Y_i \gt x)}\geq \frac{\upsilon((\boldsymbol{I},\boldsymbol{\infty}])}{\upsilon((\boldsymbol{I}_i,\boldsymbol{\infty}])} \gt 0.

\end{align*}Thus, these random variables are pairwise asymptotically dependent. For more details on multivariate regular variation, see [Reference Chen and Yuan5, Reference Konstantinides and Li18] and [Reference Li22].

2.2. Assumptions

Here, we present some conditions that are used throughout the article.

(i) Let’s assume that N(t),  $N_1(t)$,

$N_1(t)$,  $\ldots$, and

$\ldots$, and  $N_d(t)$ are renewal counting processes with corresponding renewal functions

$N_d(t)$ are renewal counting processes with corresponding renewal functions  $\lambda(t)$,

$\lambda(t)$,  $\lambda_1(t)$,

$\lambda_1(t)$,  $\ldots$,

$\ldots$,  $\lambda_d(t)$ and loss inter-arrival times

$\lambda_d(t)$ and loss inter-arrival times  $\theta_{i}, \theta_{1i}, \ldots, \theta_{di}$,

$\theta_{i}, \theta_{1i}, \ldots, \theta_{di}$,  $i\in\mathbb{N}^+$, respectively. For any two distinct integers i and j, we suppose that

$i\in\mathbb{N}^+$, respectively. For any two distinct integers i and j, we suppose that  $N_i(t)$ and

$N_i(t)$ and  $N_j(t)$ are mutually independent, as are the arrival times

$N_j(t)$ are mutually independent, as are the arrival times  $\tau_{i\cdot}$ and

$\tau_{i\cdot}$ and  $\tau_{j\cdot}$.

$\tau_{j\cdot}$.

(ii) For any integer  $k\in[1,d]$, we assume that losses

$k\in[1,d]$, we assume that losses  $\{X_{ki},i\in\mathbb{N}^+\}$ along the k-th line are non-negative and identically distributed with a generic random variable Xk, distributed by Fk.

$\{X_{ki},i\in\mathbb{N}^+\}$ along the k-th line are non-negative and identically distributed with a generic random variable Xk, distributed by Fk.

(iii) We assume the loss frequencies  $\{N_{k}(t), k=1,2,\ldots,d\}$, the losses

$\{N_{k}(t), k=1,2,\ldots,d\}$, the losses  $\{X_{ki}, k=1,2,\ldots,d, i\in \mathbb{N}^+\}$ and the general càdlàg process are mutually independent.

$\{X_{ki}, k=1,2,\ldots,d, i\in \mathbb{N}^+\}$ and the general càdlàg process are mutually independent.

Next, let us introduce the moment condition for the general càdlàg process.

Assumption 2.1.

Assume there exists a constant κ such that for any  $\omega\in[0,\kappa)$,

$\omega\in[0,\kappa)$,  $l\in(0, \kappa]$ and integer

$l\in(0, \kappa]$ and integer  $k\in[1,d]$, the following relation holds

$k\in[1,d]$, the following relation holds

\begin{align*}

\sum_{i=1}^{\infty}i^{\omega}\mathbb{E}\left(e^{-l\xi(\tau_{ki})}\right) \lt \infty.

\end{align*}

\begin{align*}

\sum_{i=1}^{\infty}i^{\omega}\mathbb{E}\left(e^{-l\xi(\tau_{ki})}\right) \lt \infty.

\end{align*}Remark 2.1.

Here, we choose several specific instances of the general càdlàg process to illustrate that Assumption 2.1 can be readily met.

(i) Let the general càdlàg process be a Lèvy process with characteristic triplet  $(\gamma,\sigma^2,\nu_0)$, where γ is a real-valued constant in

$(\gamma,\sigma^2,\nu_0)$, where γ is a real-valued constant in  $(-\infty,\infty),~\sigma$ is a non-negative constant, and ν 0 represents a Lèvy measure on

$(-\infty,\infty),~\sigma$ is a non-negative constant, and ν 0 represents a Lèvy measure on  $(-\infty,\infty)$ satisfying

$(-\infty,\infty)$ satisfying  $\nu_0(\{0\})=0$ and

$\nu_0(\{0\})=0$ and  $\int_{-\infty}^{\infty}\min(y^2,1)\nu_0(dy) \lt \infty$. Define the Laplace exponent of the Lèvy process as

$\int_{-\infty}^{\infty}\min(y^2,1)\nu_0(dy) \lt \infty$. Define the Laplace exponent of the Lèvy process as  $\phi(s)=\log \mathbb{E}(e^{-s\xi(1)}),s\in(-\infty,\infty)$. If

$\phi(s)=\log \mathbb{E}(e^{-s\xi(1)}),s\in(-\infty,\infty)$. If  $\phi(s) \lt \infty$, then, for all

$\phi(s) \lt \infty$, then, for all  $t\geq0$, we can obtain

$t\geq0$, we can obtain  $\mathbb{E}(e^{-s\xi(t)})=e^{t\phi(s)}$. For more details of the Lèvy process, we refer the reader to [Reference Cont and Tankov7] and [Reference Sato26]. Assume there exists a constant κ such that

$\mathbb{E}(e^{-s\xi(t)})=e^{t\phi(s)}$. For more details of the Lèvy process, we refer the reader to [Reference Cont and Tankov7] and [Reference Sato26]. Assume there exists a constant κ such that  $\phi(\kappa) \lt 0$, it is easy to verify that

$\phi(\kappa) \lt 0$, it is easy to verify that  $\phi(s)$ is convex in s, and finite. Since

$\phi(s)$ is convex in s, and finite. Since  $\phi(0) = 0$, we see that the condition

$\phi(0) = 0$, we see that the condition  $\phi(\kappa) \lt 0$ implies that

$\phi(\kappa) \lt 0$ implies that  $\phi(s) \lt 0$ for all

$\phi(s) \lt 0$ for all  $s\in (0, \kappa]$. Additionally, suppose that for any integer

$s\in (0, \kappa]$. Additionally, suppose that for any integer  $k\in[1,d]$,

$k\in[1,d]$,  $N_k(t)$ is a renewal counting process. Therefore, it is obvious that for any

$N_k(t)$ is a renewal counting process. Therefore, it is obvious that for any  $\omega\in[0,\kappa)$,

$\omega\in[0,\kappa)$,  $l\in(0, \kappa]$ and integer

$l\in(0, \kappa]$ and integer  $k\in[1,d]$,

$k\in[1,d]$,

\begin{align*}

\sum_{i=1}^{\infty}i^{\omega}\mathbb{E}\left(e^{-l\xi(\tau_{ki})}\right)=\sum_{i=1}^{\infty}i^{\omega}\mathbb{E}\left(e^{\tau_{ki}\phi(l)}\right)=\sum_{i=1}^{\infty}i^{\omega}\left(\mathbb{E}\left(e^{\theta_{k1}\phi(l)}\right)\right)^i \lt \infty.

\end{align*}

\begin{align*}

\sum_{i=1}^{\infty}i^{\omega}\mathbb{E}\left(e^{-l\xi(\tau_{ki})}\right)=\sum_{i=1}^{\infty}i^{\omega}\mathbb{E}\left(e^{\tau_{ki}\phi(l)}\right)=\sum_{i=1}^{\infty}i^{\omega}\left(\mathbb{E}\left(e^{\theta_{k1}\phi(l)}\right)\right)^i \lt \infty.

\end{align*} (ii) When the general càdlàg process is determined by the fractional Brownian motion, the Vasicek model, the CIR model or the Heston model, it is evident from Section 3 of [Reference Guo and Wang11] that there exist constants κ and η satisfying  $\eta \gt \kappa[\omega]/l-1+2\kappa/l \gt 0$, such that the following condition holds,

$\eta \gt \kappa[\omega]/l-1+2\kappa/l \gt 0$, such that the following condition holds,

\begin{equation}

\int_{0}^{\infty}\max\{s^{\eta},1\}\mathbb{E}(e^{-\kappa\xi(s)})ds \lt \infty,

\end{equation}

\begin{equation}

\int_{0}^{\infty}\max\{s^{\eta},1\}\mathbb{E}(e^{-\kappa\xi(s)})ds \lt \infty,

\end{equation} where  $\omega\in[0,\kappa)$,

$\omega\in[0,\kappa)$,  $l\in(0, \kappa]$ and [A] denotes the integer part of A. Assume that for any integer

$l\in(0, \kappa]$ and [A] denotes the integer part of A. Assume that for any integer  $k\in[1,d]$,

$k\in[1,d]$,  $N_k(t)$ is a homogeneous Poisson counting process with arrival times

$N_k(t)$ is a homogeneous Poisson counting process with arrival times  $\tau_{ki},~i\in\mathbb{N}^+$. Consequently, the inter-arrival times θki follow an exponential distribution with parameter λk. Note that τki is a gamma random variable satisfying

$\tau_{ki},~i\in\mathbb{N}^+$. Consequently, the inter-arrival times θki follow an exponential distribution with parameter λk. Note that τki is a gamma random variable satisfying

\begin{align}P(\tau_{ki}\in ds)=\frac{s^{i-1}\lambda_k^i}{(i-1)!}e^{-\lambda_ks}ds.

\end{align}

\begin{align}P(\tau_{ki}\in ds)=\frac{s^{i-1}\lambda_k^i}{(i-1)!}e^{-\lambda_ks}ds.

\end{align} Thus, we have that for any δ > 0,  $\omega\in[0,\kappa)$,

$\omega\in[0,\kappa)$,  $l\in(0, \kappa]$ and integer

$l\in(0, \kappa]$ and integer  $k\in[1,d]$,

$k\in[1,d]$,

\begin{align*}

&\sum_{i=1}^{\infty}i^{\omega}\mathbb{E}\left(e^{-l\xi(\tau_{ki})}\right)\\

&=\sum_{i=1}^{\infty}i^{\omega}\int_{0}^{\infty}\mathbb{E}\left(e^{-l\xi(s)}\right)\frac{s^{i-1}\lambda_k^i}{(i-1)!}e^{-\lambda_ks}ds\\

&\leq C \int_{0}^{\infty}\max\{s^{[\omega]+1},1\}\mathbb{E}\left(e^{-l\xi(s)}\right)ds\\

&\leq C \left(\int_{0}^{2}\max\{s^{[\omega]+1},1\}\left(\mathbb{E}\left(e^{-\kappa\xi(s)}\right)\right)^{l/\kappa}ds+\int_{2}^{\infty}\frac{s^{[\omega]+2-l/\kappa}log^{1+\delta}s}{s^{1-l/\kappa}log^{1+\delta}s}\left(\mathbb{E}\left(e^{-\kappa\xi(s)}\right)\right)^{l/\kappa}ds\right)\\

&\leq C\left(\int_{0}^{2}\mathbb{E}\left(e^{-\kappa\xi(s)}\right)ds\right)^{l/\kappa}\\

&+\left(\int_2^{\infty}s^{\kappa[\omega]/l-1+2\kappa/l}log^{(1+\delta)\kappa/l}s\mathbb{E}\left(e^{-\kappa\xi(s)}\right)ds\right)^{l/\kappa} \left(\int_{2}^{\infty}s^{-1}log^{-(1+\delta)\kappa/(\kappa-l)}sds\right)^{1-l/\kappa}\\

&\leq C\left(\left(\int_0^2\mathbb{E}\left(e^{-\kappa\xi(s)}\right)ds\right)^{l/\kappa}+\left(\int_{2}^{\infty}s^{\eta}\mathbb{E}\left(e^{-\kappa\xi(s)}\right)ds\right)^{l/\kappa}\right) \lt \infty,

\end{align*}

\begin{align*}

&\sum_{i=1}^{\infty}i^{\omega}\mathbb{E}\left(e^{-l\xi(\tau_{ki})}\right)\\

&=\sum_{i=1}^{\infty}i^{\omega}\int_{0}^{\infty}\mathbb{E}\left(e^{-l\xi(s)}\right)\frac{s^{i-1}\lambda_k^i}{(i-1)!}e^{-\lambda_ks}ds\\

&\leq C \int_{0}^{\infty}\max\{s^{[\omega]+1},1\}\mathbb{E}\left(e^{-l\xi(s)}\right)ds\\

&\leq C \left(\int_{0}^{2}\max\{s^{[\omega]+1},1\}\left(\mathbb{E}\left(e^{-\kappa\xi(s)}\right)\right)^{l/\kappa}ds+\int_{2}^{\infty}\frac{s^{[\omega]+2-l/\kappa}log^{1+\delta}s}{s^{1-l/\kappa}log^{1+\delta}s}\left(\mathbb{E}\left(e^{-\kappa\xi(s)}\right)\right)^{l/\kappa}ds\right)\\

&\leq C\left(\int_{0}^{2}\mathbb{E}\left(e^{-\kappa\xi(s)}\right)ds\right)^{l/\kappa}\\

&+\left(\int_2^{\infty}s^{\kappa[\omega]/l-1+2\kappa/l}log^{(1+\delta)\kappa/l}s\mathbb{E}\left(e^{-\kappa\xi(s)}\right)ds\right)^{l/\kappa} \left(\int_{2}^{\infty}s^{-1}log^{-(1+\delta)\kappa/(\kappa-l)}sds\right)^{1-l/\kappa}\\

&\leq C\left(\left(\int_0^2\mathbb{E}\left(e^{-\kappa\xi(s)}\right)ds\right)^{l/\kappa}+\left(\int_{2}^{\infty}s^{\eta}\mathbb{E}\left(e^{-\kappa\xi(s)}\right)ds\right)^{l/\kappa}\right) \lt \infty,

\end{align*}where in the first step, we use relation (2.7), in the second step, we utilize the fact that for any non-negative constant n, the following relation holds

\begin{align*}

\sum_{i=1}^{\infty}i^{n}\frac{s^{i-1}\lambda_k^i}{(i-1)!}e^{-\lambda_ks}\leq \begin{cases}

C \max\{s^n,1\},&n=0,1,2,\ldots\\

C \max\{s^{[n]+1},1\},&\mathrm{else},

\end{cases}

\end{align*}

\begin{align*}

\sum_{i=1}^{\infty}i^{n}\frac{s^{i-1}\lambda_k^i}{(i-1)!}e^{-\lambda_ks}\leq \begin{cases}

C \max\{s^n,1\},&n=0,1,2,\ldots\\

C \max\{s^{[n]+1},1\},&\mathrm{else},

\end{cases}

\end{align*} in the third and fourth steps, we apply H $\ddot{\mathrm{o}}$lder’s inequality, and in the last step, we use relation (2.6).

$\ddot{\mathrm{o}}$lder’s inequality, and in the last step, we use relation (2.6).

(iii) Suppose that there exists a constant κ such that

\begin{align} \mathbb{E}\left(e^{-\kappa\xi(t)}\right)\sim\varphi(\kappa)e^{\vartheta(\kappa)t}, \mathrm{as}~t\rightarrow\infty,

\end{align}

\begin{align} \mathbb{E}\left(e^{-\kappa\xi(t)}\right)\sim\varphi(\kappa)e^{\vartheta(\kappa)t}, \mathrm{as}~t\rightarrow\infty,

\end{align} where the function  $\varphi(\kappa) \gt 0$ is bounded for any fixed κ, and the function

$\varphi(\kappa) \gt 0$ is bounded for any fixed κ, and the function  $\vartheta(\kappa) \lt 0$. Additionally, it is assumed that there exists a constant T such that for sufficiently large

$\vartheta(\kappa) \lt 0$. Additionally, it is assumed that there exists a constant T such that for sufficiently large  $H' \gt 0$,

$H' \gt 0$,

\begin{align} \sup_{t\in [0, T]}\mathbb{E}\left(e^{-\kappa\xi(t)}\right) \lt H'.

\end{align}

\begin{align} \sup_{t\in [0, T]}\mathbb{E}\left(e^{-\kappa\xi(t)}\right) \lt H'.

\end{align} Section 4 of [Reference Cheng, Konstantinides and Wang6] implies that when the general càdlàg process is determined by the Vasicek model, the CIR model or the Heston model, the conditions (2.8) and (2.9) can be satisfied. Furthermore, assume that for any integer  $k\in[1,d]$,

$k\in[1,d]$,  $N_k(t)$ is a renewal counting process. Thus, it can be shown that there exists a large T 0 such that for any

$N_k(t)$ is a renewal counting process. Thus, it can be shown that there exists a large T 0 such that for any  $\omega\in[0,\kappa)$,

$\omega\in[0,\kappa)$,  $l\in(0, \kappa]$ and integer

$l\in(0, \kappa]$ and integer  $k\in[1,d]$, the following relation holds

$k\in[1,d]$, the following relation holds

\begin{align*}

\sum_{i=1}^{\infty}i^{\omega}\mathbb{E}\left(e^{-l\xi(\tau_{ki})}\right)&

\leq \sum_{i=1}^{\infty}i^{\omega}\left(\mathbb{E}\left(e^{-\kappa\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}\leq T_0\}}\right)+\mathbb{E}\left(e^{-\kappa\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki} \gt T_0\}}\right)\right)^{l/\kappa}\\

&\leq C\sum_{i=1}^{\infty}i^{\omega}\left(H' P(\tau_{ki}\leq T_0)+\varphi(\kappa)\mathbb{E}\left(e^{\vartheta(\kappa)\tau_{ki}}\right)\right)^{l/\kappa}\\

&\leq C\sum_{i=1}^{\infty}i^{\omega}\left( \left(P(\theta_{k1}\leq T_0)\right)^i+\left(\mathbb{E}\left(e^{\vartheta(\kappa)\theta_{k1}}\right)\right)^{i}\right)^{l/\kappa}\\

&\leq C\sum_{i=1}^{\infty}i^{\omega}\left( \left(P(\theta_{k1}\leq T_0)\right)^{il/\kappa}+\left(\mathbb{E}\left(e^{\vartheta(\kappa)\theta_{k1}}\right)\right)^{il/\kappa}\right) \lt \infty,

\end{align*}

\begin{align*}

\sum_{i=1}^{\infty}i^{\omega}\mathbb{E}\left(e^{-l\xi(\tau_{ki})}\right)&

\leq \sum_{i=1}^{\infty}i^{\omega}\left(\mathbb{E}\left(e^{-\kappa\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}\leq T_0\}}\right)+\mathbb{E}\left(e^{-\kappa\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki} \gt T_0\}}\right)\right)^{l/\kappa}\\

&\leq C\sum_{i=1}^{\infty}i^{\omega}\left(H' P(\tau_{ki}\leq T_0)+\varphi(\kappa)\mathbb{E}\left(e^{\vartheta(\kappa)\tau_{ki}}\right)\right)^{l/\kappa}\\

&\leq C\sum_{i=1}^{\infty}i^{\omega}\left( \left(P(\theta_{k1}\leq T_0)\right)^i+\left(\mathbb{E}\left(e^{\vartheta(\kappa)\theta_{k1}}\right)\right)^{i}\right)^{l/\kappa}\\

&\leq C\sum_{i=1}^{\infty}i^{\omega}\left( \left(P(\theta_{k1}\leq T_0)\right)^{il/\kappa}+\left(\mathbb{E}\left(e^{\vartheta(\kappa)\theta_{k1}}\right)\right)^{il/\kappa}\right) \lt \infty,

\end{align*} where in the first step, we use H $\ddot{\mathrm{o}}$lder’s inequality, in the second step, we apply relations (2.8) and (2.9), and in the fourth step, we use Cr inequality.

$\ddot{\mathrm{o}}$lder’s inequality, in the second step, we apply relations (2.8) and (2.9), and in the fourth step, we use Cr inequality.

Remark 2.2.

Under the conditions of Assumption 2.1 with  $N_1(t)=N_2(t)=\cdots=N(t)$, by H

$N_1(t)=N_2(t)=\cdots=N(t)$, by H $\ddot{\mathrm{o}}$lder’s inequality, we have that for any

$\ddot{\mathrm{o}}$lder’s inequality, we have that for any  $l_1,l_2\in(0,\kappa/2)$,

$l_1,l_2\in(0,\kappa/2)$,

\begin{align*}

\mathbb{E}\left(e^{-l_1\xi(\tau_i)}e^{-l_2\xi(\tau_j)}\right)\leq \left(\mathbb{E}\left(e^{-2l_1\xi(\tau_i)}\right)\right)^{1/2}\left(\mathbb{E}\left(e^{-2l_2\xi(\tau_j)}\right)\right)^{1/2} \lt \infty,~i\neq j.

\end{align*}

\begin{align*}

\mathbb{E}\left(e^{-l_1\xi(\tau_i)}e^{-l_2\xi(\tau_j)}\right)\leq \left(\mathbb{E}\left(e^{-2l_1\xi(\tau_i)}\right)\right)^{1/2}\left(\mathbb{E}\left(e^{-2l_2\xi(\tau_j)}\right)\right)^{1/2} \lt \infty,~i\neq j.

\end{align*}Indeed, the relation above is essential in the proof of Theorem 3.2, as evident in Lemmas 4.10-4.11.

3. Main results

Now, we are ready to state our main theorems. In the Theorem 3.1, we explore the extremes for systemic risk measures  $SES_k(t,q)$ and

$SES_k(t,q)$ and  $MES_k(t,q)$ under asymptotic independence structure. In the Theorem 3.2, we investigate the extremes for systemic risk measures

$MES_k(t,q)$ under asymptotic independence structure. In the Theorem 3.2, we investigate the extremes for systemic risk measures  $SES_k(t,q)$ and

$SES_k(t,q)$ and  $MES_k(t,q)$ under asymptotic dependence structure.

$MES_k(t,q)$ under asymptotic dependence structure.

Theorem 3.1.

Consider the  $SES_k(t,q)$ and

$SES_k(t,q)$ and  $MES_k(t,q)$ defined by (1.3) and (1.4) with Assumption 2.1. Suppose that random variables X11, X12, …,

$MES_k(t,q)$ defined by (1.3) and (1.4) with Assumption 2.1. Suppose that random variables X11, X12, …,  $X_{d1}$, … are pSQAI. For any integer

$X_{d1}$, … are pSQAI. For any integer  $k\in[1,d]$, assume that there exists a representing distribution F satisfying

$k\in[1,d]$, assume that there exists a representing distribution F satisfying  $\lim_{x\rightarrow\infty}\frac{\overline{F}_k(x)}{\overline{F}(x)}=: b_k\in(0,\infty)$.

$\lim_{x\rightarrow\infty}\frac{\overline{F}_k(x)}{\overline{F}(x)}=: b_k\in(0,\infty)$.

(i) Suppose that  $F\in\mathcal{D}\cap\mathcal{L}$ with

$F\in\mathcal{D}\cap\mathcal{L}$ with  $\kappa \gt 2\max\{J_{F_1}^+,\ldots,J_{F_d}^+\}$ and

$\kappa \gt 2\max\{J_{F_1}^+,\ldots,J_{F_d}^+\}$ and  $\min\{J_{F_1}^-,\ldots,J_{F_d}^-\} \gt 1$. For any integer

$\min\{J_{F_1}^-,\ldots,J_{F_d}^-\} \gt 1$. For any integer  $k\in[1,d]$ and any fixed

$k\in[1,d]$ and any fixed  $t\in(0,\infty]$ satisfying

$t\in(0,\infty]$ satisfying  $P(\max\{\tau_{11},\ldots,\tau_{d1}\}\leq t) \gt 0$, if as

$P(\max\{\tau_{11},\ldots,\tau_{d1}\}\leq t) \gt 0$, if as  $q\uparrow1$,

$q\uparrow1$,  $VaR_S(t,q)$ diverges to

$VaR_S(t,q)$ diverges to  $\infty$, then, the following relations hold

$\infty$, then, the following relations hold

\begin{align}

SES_k(t,q)&\sim\frac{A(t,q)\left(1-D_k(t,1)\right)\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt A(t,q)\right)\lambda_k(ds)}{\sum_{k=1}^{d}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt A(t,q)\right)\lambda_k(ds)}\nonumber\\

&+\frac{A(t,q)\int_{1}^{\infty}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt A(t,q)y\right)\lambda_k(ds)dy}{\sum_{k=1}^{d}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt A(t,q)\right)\lambda_k(ds)},

\end{align}

\begin{align}

SES_k(t,q)&\sim\frac{A(t,q)\left(1-D_k(t,1)\right)\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt A(t,q)\right)\lambda_k(ds)}{\sum_{k=1}^{d}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt A(t,q)\right)\lambda_k(ds)}\nonumber\\

&+\frac{A(t,q)\int_{1}^{\infty}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt A(t,q)y\right)\lambda_k(ds)dy}{\sum_{k=1}^{d}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt A(t,q)\right)\lambda_k(ds)},

\end{align}and

\begin{align}

MES_k(t,q)&\sim\frac{A(t,q)\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt A(t,q)\right)\lambda_k(ds)}{\sum_{k=1}^{d}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt A(t,q)\right)\lambda_k(ds)}\nonumber\\

&+\frac{A(t,q)\int_{1}^{\infty}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt A(t,q)y\right)\lambda_k(ds)dy}{\sum_{k=1}^{d}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt A(t,q)\right)\lambda_k(ds)},

\end{align}

\begin{align}

MES_k(t,q)&\sim\frac{A(t,q)\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt A(t,q)\right)\lambda_k(ds)}{\sum_{k=1}^{d}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt A(t,q)\right)\lambda_k(ds)}\nonumber\\

&+\frac{A(t,q)\int_{1}^{\infty}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt A(t,q)y\right)\lambda_k(ds)dy}{\sum_{k=1}^{d}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt A(t,q)\right)\lambda_k(ds)},

\end{align}where

\begin{align*}

&D_k(t,1)\\

&=\lim_{q\uparrow1}\frac{\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt VaR_S(t,q)\right)\lambda_k(ds)+\int_{1}^{\infty}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt VaR_S(t,q)y\right)\lambda_k(ds)dy}{\sum_{k=1}^{d}\left(\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt VaR_S(t,q)\right)\lambda_k(ds)+\int_{1}^{\infty}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt VaR_S(t,q)y\right)\lambda_k(ds)dy\right)}.

\end{align*}

\begin{align*}

&D_k(t,1)\\

&=\lim_{q\uparrow1}\frac{\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt VaR_S(t,q)\right)\lambda_k(ds)+\int_{1}^{\infty}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt VaR_S(t,q)y\right)\lambda_k(ds)dy}{\sum_{k=1}^{d}\left(\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt VaR_S(t,q)\right)\lambda_k(ds)+\int_{1}^{\infty}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt VaR_S(t,q)y\right)\lambda_k(ds)dy\right)}.

\end{align*} (ii) Assume  $F\in\mathcal{R}_{-\alpha}$ with

$F\in\mathcal{R}_{-\alpha}$ with  $\alpha\in(1,\kappa/2)$. For any integer

$\alpha\in(1,\kappa/2)$. For any integer  $k\in[1,d]$ and any fixed

$k\in[1,d]$ and any fixed  $t\in(0,\infty]$ satisfying

$t\in(0,\infty]$ satisfying  $P(\max\{\tau_{11},\ldots,\tau_{d1}\}\leq t) \gt 0$, we have

$P(\max\{\tau_{11},\ldots,\tau_{d1}\}\leq t) \gt 0$, we have

\begin{align}

SES_k(t,q)&\sim \frac{\alpha b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)}{(\alpha-1)\left(\sum_{k=1}^{d}b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)\right)^{1-\frac{1}{\alpha}}}\nonumber\\

&\times\left(\frac{\alpha}{\alpha-1}-\frac{b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)}{\sum_{k=1}^{d}b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)}\right)VaR_X(q),

\end{align}

\begin{align}

SES_k(t,q)&\sim \frac{\alpha b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)}{(\alpha-1)\left(\sum_{k=1}^{d}b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)\right)^{1-\frac{1}{\alpha}}}\nonumber\\

&\times\left(\frac{\alpha}{\alpha-1}-\frac{b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)}{\sum_{k=1}^{d}b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)}\right)VaR_X(q),

\end{align}and

\begin{align}&MES_k(t,q)\sim\frac{\alpha^2b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)}{(\alpha-1)^2\left(\sum_{k=1}^{d}b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)\right)^{1-\frac{1}{\alpha}}}VaR_X(q).

\end{align}

\begin{align}&MES_k(t,q)\sim\frac{\alpha^2b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)}{(\alpha-1)^2\left(\sum_{k=1}^{d}b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)\right)^{1-\frac{1}{\alpha}}}VaR_X(q).

\end{align} Actually, when  $F\in\mathcal{R}_{-\alpha}$, from relation (4.28), it is clear that the condition “as

$F\in\mathcal{R}_{-\alpha}$, from relation (4.28), it is clear that the condition “as  $q\uparrow1$,

$q\uparrow1$,  $VaR_S(t,q)$ diverge to

$VaR_S(t,q)$ diverge to  $\infty$.” in Theorem 3.1(i) can be directly satisfied. Consequently, we remove this condition in Theorem 3.1(ii).

$\infty$.” in Theorem 3.1(i) can be directly satisfied. Consequently, we remove this condition in Theorem 3.1(ii).

Theorem 3.2.

Consider the  $SES_k(t,q)$ and

$SES_k(t,q)$ and  $MES_k(t,q)$ defined by (1.3) and (1.4) with Assumption 2.1. Let

$MES_k(t,q)$ defined by (1.3) and (1.4) with Assumption 2.1. Let  $N_1(t)=\cdots=N_d(t)=N(t)$. Suppose that

$N_1(t)=\cdots=N_d(t)=N(t)$. Suppose that  $\{(X_1,X_2,\ldots,X_d),(X_{1i},X_{2i},\ldots,X_{di}),i\in\mathbb{N}^+\}$ is a sequence of independent and identically distributed random vectors with

$\{(X_1,X_2,\ldots,X_d),(X_{1i},X_{2i},\ldots,X_{di}),i\in\mathbb{N}^+\}$ is a sequence of independent and identically distributed random vectors with  $(X_1,X_2,\ldots,X_d)\in MRV_{d}(\alpha,F,\upsilon)$,

$(X_1,X_2,\ldots,X_d)\in MRV_{d}(\alpha,F,\upsilon)$,  $\alpha\in(1,\kappa/2)$ such that

$\alpha\in(1,\kappa/2)$ such that  $\upsilon((\boldsymbol{1},\boldsymbol{\infty}]) \gt 0$. Then, for any integer

$\upsilon((\boldsymbol{1},\boldsymbol{\infty}]) \gt 0$. Then, for any integer  $k\in[1,d]$ and any fixed

$k\in[1,d]$ and any fixed  $t\in(0,\infty]$ satisfying

$t\in(0,\infty]$ satisfying  $P(\tau_{1}\leq t) \gt 0$, the following relations hold

$P(\tau_{1}\leq t) \gt 0$, the following relations hold

\begin{align}&SES_k(t,q)\sim\frac{\alpha\left(\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda(ds)\right)^{\frac{1}{\alpha}}\left[(\alpha-1)\int_{B(k,\alpha)}^{1}V_k(y,1)dy+\upsilon(\Upsilon_k)\right]}{(\alpha-1)^2\left(\upsilon\left(\Delta\right)\right)^{1-\frac{1}{\alpha}}}VaR_X(q),

\end{align}

\begin{align}&SES_k(t,q)\sim\frac{\alpha\left(\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda(ds)\right)^{\frac{1}{\alpha}}\left[(\alpha-1)\int_{B(k,\alpha)}^{1}V_k(y,1)dy+\upsilon(\Upsilon_k)\right]}{(\alpha-1)^2\left(\upsilon\left(\Delta\right)\right)^{1-\frac{1}{\alpha}}}VaR_X(q),

\end{align}and

\begin{align}MES_k(t,q)\sim\frac{\alpha\left(\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda(ds)\right)^{\frac{1}{\alpha}}\left[(\alpha-1)\int_{0+}^{1}V_k(y,1)dy+\upsilon(\Upsilon_k)\right]}{(\alpha-1)^2\left(\upsilon\left(\Delta\right)\right)^{1-\frac{1}{\alpha}}}VaR_X(q),

\end{align}

\begin{align}MES_k(t,q)\sim\frac{\alpha\left(\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda(ds)\right)^{\frac{1}{\alpha}}\left[(\alpha-1)\int_{0+}^{1}V_k(y,1)dy+\upsilon(\Upsilon_k)\right]}{(\alpha-1)^2\left(\upsilon\left(\Delta\right)\right)^{1-\frac{1}{\alpha}}}VaR_X(q),

\end{align}where

\begin{align}

&\Upsilon_k=\left\{(x_1,x_2,\ldots,x_d)\in\mathbb{R}_{+}^{d}:~x_k \gt 1\right\},~~~\Delta=\left\{(x_1,x_2,\ldots,x_d)\in\mathbb{R}_{+}^{d}:~\sum_{l=1}^{d}x_l \gt 1\right\},\nonumber\\

&V_k(y,1)=\upsilon\left((x_1,x_2,\ldots,x_d)\in\mathbb{R}_{+}^{d}:~x_k \gt y,~\sum_{l=1}^{d}x_l \gt 1\right),~\mathrm{for}~y\in(0,1],~~~~~~~~

\end{align}

\begin{align}

&\Upsilon_k=\left\{(x_1,x_2,\ldots,x_d)\in\mathbb{R}_{+}^{d}:~x_k \gt 1\right\},~~~\Delta=\left\{(x_1,x_2,\ldots,x_d)\in\mathbb{R}_{+}^{d}:~\sum_{l=1}^{d}x_l \gt 1\right\},\nonumber\\

&V_k(y,1)=\upsilon\left((x_1,x_2,\ldots,x_d)\in\mathbb{R}_{+}^{d}:~x_k \gt y,~\sum_{l=1}^{d}x_l \gt 1\right),~\mathrm{for}~y\in(0,1],~~~~~~~~

\end{align}and

\begin{align*}

B(k,\alpha)=\frac{(\alpha-1)\int_{0+}^{1}V_k(y,1)dy+\upsilon(\Upsilon_k)}{\alpha \upsilon\left(\Delta\right)}.

\end{align*}

\begin{align*}

B(k,\alpha)=\frac{(\alpha-1)\int_{0+}^{1}V_k(y,1)dy+\upsilon(\Upsilon_k)}{\alpha \upsilon\left(\Delta\right)}.

\end{align*} Indeed, all of our results (3.3)–(3.6) are presented in a concise form of  $C\times VaR_X(q)$, where C is a constant unrelated to q, reflecting the combined effects of the general càdlàg process and heavy-tailed property of losses. In the case of Theorem 3.1, the influence of the dependence structure among losses on the

$C\times VaR_X(q)$, where C is a constant unrelated to q, reflecting the combined effects of the general càdlàg process and heavy-tailed property of losses. In the case of Theorem 3.1, the influence of the dependence structure among losses on the  $SES_k(t,q)$ and

$SES_k(t,q)$ and  $MES_k(t,q)$ is minimal, but it is crucial in Theorem 3.2. This indicates that the asymptotic dependence structure among losses has a significant impact on the systemic risk measures.

$MES_k(t,q)$ is minimal, but it is crucial in Theorem 3.2. This indicates that the asymptotic dependence structure among losses has a significant impact on the systemic risk measures.

Corollary 3.1.

(i) For any integer  $k\in[1,d]$, we assume

$k\in[1,d]$, we assume  $N_k(t)$ is a homogeneous Poisson counting process with parameter λk. Under the remaining conditions of Theorem 3.1(ii), for any integer

$N_k(t)$ is a homogeneous Poisson counting process with parameter λk. Under the remaining conditions of Theorem 3.1(ii), for any integer  $k\in[1,d]$ and any fixed

$k\in[1,d]$ and any fixed  $t\in(0,\infty]$ satisfying

$t\in(0,\infty]$ satisfying  $P(\max\{\tau_{11},\ldots,\tau_{d1}\}\leq t) \gt 0$, the following relations hold,

$P(\max\{\tau_{11},\ldots,\tau_{d1}\}\leq t) \gt 0$, the following relations hold,

\begin{align*}

SES_k(t,q)&\sim\frac{\alpha b_k\lambda_k\left[\alpha\sum_{k=1}^{d}b_k\lambda_k-(\alpha-1)b_k\lambda_k\right]\left[\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)ds\right]^{\frac{1}{\alpha}}}{(\alpha-1)^2\left(\sum_{k=1}^{d}b_k\lambda_k\right)^{2-\frac{1}{\alpha}}}VaR_X(q),

\end{align*}

\begin{align*}

SES_k(t,q)&\sim\frac{\alpha b_k\lambda_k\left[\alpha\sum_{k=1}^{d}b_k\lambda_k-(\alpha-1)b_k\lambda_k\right]\left[\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)ds\right]^{\frac{1}{\alpha}}}{(\alpha-1)^2\left(\sum_{k=1}^{d}b_k\lambda_k\right)^{2-\frac{1}{\alpha}}}VaR_X(q),

\end{align*}and

\begin{align*}

MES_k(t,q)\sim\frac{\alpha^2b_k\lambda_k\left[\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)ds\right]^{\frac{1}{\alpha}}}{(\alpha-1)^2\left(\sum_{k=1}^{d}b_k\lambda_k\right)^{1-\frac{1}{\alpha}}}VaR_X(q).

\end{align*}

\begin{align*}

MES_k(t,q)\sim\frac{\alpha^2b_k\lambda_k\left[\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)ds\right]^{\frac{1}{\alpha}}}{(\alpha-1)^2\left(\sum_{k=1}^{d}b_k\lambda_k\right)^{1-\frac{1}{\alpha}}}VaR_X(q).

\end{align*} (ii) Assume that N(t) is a homogeneous Poisson counting process with parameter λ. Under the remaining conditions of Theorem 3.2, for any integer  $k\in[1,d]$ and any fixed

$k\in[1,d]$ and any fixed  $t\in(0,\infty]$ satisfying

$t\in(0,\infty]$ satisfying  $P(\tau_{1}\leq t) \gt 0$, the following relations hold,

$P(\tau_{1}\leq t) \gt 0$, the following relations hold,

\begin{align*}

SES_k(t,q)&\sim\frac{\alpha\left(\lambda\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)ds\right)^{\frac{1}{\alpha}}\left[(\alpha-1)\int_{B(k,\alpha)}^{1}V_k(y,1)dy+\upsilon(\Upsilon_k)\right]}{(\alpha-1)^2\left(\upsilon\left(\Delta\right)\right)^{1-\frac{1}{\alpha}}}VaR_X(q),

\end{align*}

\begin{align*}

SES_k(t,q)&\sim\frac{\alpha\left(\lambda\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)ds\right)^{\frac{1}{\alpha}}\left[(\alpha-1)\int_{B(k,\alpha)}^{1}V_k(y,1)dy+\upsilon(\Upsilon_k)\right]}{(\alpha-1)^2\left(\upsilon\left(\Delta\right)\right)^{1-\frac{1}{\alpha}}}VaR_X(q),

\end{align*}and

\begin{align*}

MES_k(t,q)\sim\frac{\alpha\left(\lambda\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)ds\right)^{\frac{1}{\alpha}}\left[(\alpha-1)\int_{0+}^{1}V_k(y,1)dy+\upsilon(\Upsilon_k)\right]}{(\alpha-1)^2\left(\upsilon\left(\Delta\right)\right)^{1-\frac{1}{\alpha}}}VaR_X(q).

\end{align*}

\begin{align*}

MES_k(t,q)\sim\frac{\alpha\left(\lambda\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)ds\right)^{\frac{1}{\alpha}}\left[(\alpha-1)\int_{0+}^{1}V_k(y,1)dy+\upsilon(\Upsilon_k)\right]}{(\alpha-1)^2\left(\upsilon\left(\Delta\right)\right)^{1-\frac{1}{\alpha}}}VaR_X(q).

\end{align*}Remark 3.1.

A Financial institution needs to allocate an available capital amount Q across various business lines, and assign a proportional capital Qk to each business unit such that  $Q=\sum_{k=1}^dQ_k$. As discussed in Section 3.2 of [Reference Zhou, Dhaene and Yao31], for any integer

$Q=\sum_{k=1}^dQ_k$. As discussed in Section 3.2 of [Reference Zhou, Dhaene and Yao31], for any integer  $k\in[1,d]$, the CTE capital allocation rule is

$k\in[1,d]$, the CTE capital allocation rule is

\begin{align*}

\mathcal{Q}_k&=\mathcal{Q}\frac{A_k(t,q)}{A(t,q)}=\mathcal{Q}\frac{\mathbb{E}(L_k(t)~|~S(t) \gt VaR_S(t,q))}{\mathbb{E}(S(t)~|~S(t) \gt VaR_S(t,q))}.

\end{align*}

\begin{align*}

\mathcal{Q}_k&=\mathcal{Q}\frac{A_k(t,q)}{A(t,q)}=\mathcal{Q}\frac{\mathbb{E}(L_k(t)~|~S(t) \gt VaR_S(t,q))}{\mathbb{E}(S(t)~|~S(t) \gt VaR_S(t,q))}.

\end{align*} (i) Under the conditions of Theorem 3.1(ii), for any integer  $k\in[1,d]$, applying relation (4.27) yields that

$k\in[1,d]$, applying relation (4.27) yields that

\begin{align*}

\mathcal{Q}_k

&\sim\mathcal{Q}\frac{b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)}{\sum_{k=1}^{d}b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)}.

\end{align*}

\begin{align*}

\mathcal{Q}_k

&\sim\mathcal{Q}\frac{b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)}{\sum_{k=1}^{d}b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)}.

\end{align*} (ii) Under the conditions of Theorem 3.2, for any integer  $k\in[1,d]$, using relation (4.32) gives that

$k\in[1,d]$, using relation (4.32) gives that

\begin{align*}

\mathcal{Q}_k

\sim\mathcal{Q}\frac{\left[(\alpha-1)\int_{0+}^{1}V_k(y,1)dy+\upsilon(\Upsilon_k)\right]}{\sum_{k=1}^{d}\left[(\alpha-1)\int_{0+}^{1}V_k(y,1)dy+\upsilon(\Upsilon_k)\right]}.

\end{align*}

\begin{align*}

\mathcal{Q}_k

\sim\mathcal{Q}\frac{\left[(\alpha-1)\int_{0+}^{1}V_k(y,1)dy+\upsilon(\Upsilon_k)\right]}{\sum_{k=1}^{d}\left[(\alpha-1)\int_{0+}^{1}V_k(y,1)dy+\upsilon(\Upsilon_k)\right]}.

\end{align*} Next, we give for Theorem 3.2 a specific example, in which the constant before  $VaR_X(q)$ can be calculated explicitly.

$VaR_X(q)$ can be calculated explicitly.

Remark 3.2.

Consider a special case where the economic system only has two lines of businesses (i.e., d = 2). Let the loss Xi follows a Pareto distribution

\begin{equation} F_i(x)=1-\left(\frac{\gamma_i}{x+\gamma_i}\right)^{\alpha},~\mathrm{for}~x \gt 0~\mathrm{and}~\gamma_i \gt 0,~i=1,2.

\end{equation}

\begin{equation} F_i(x)=1-\left(\frac{\gamma_i}{x+\gamma_i}\right)^{\alpha},~\mathrm{for}~x \gt 0~\mathrm{and}~\gamma_i \gt 0,~i=1,2.

\end{equation} We assume that the survival copula of  $(X_1,X_2)$ is an Archimedean one with a regularly varying generator function

$(X_1,X_2)$ is an Archimedean one with a regularly varying generator function  $\psi(\cdot)$, such that relation

$\psi(\cdot)$, such that relation

\begin{align*}

\lim_{u\rightarrow0^+}\frac{\psi(yu)}{\psi(u)}=y^{-\beta},

\end{align*}

\begin{align*}

\lim_{u\rightarrow0^+}\frac{\psi(yu)}{\psi(u)}=y^{-\beta},

\end{align*} holds for any y > 0 and β > 0. According to [Reference Asimit, Furman, Tang and Vernic1], we can obtain that  $(X_1,X_2)\in MRV_2(\alpha,F_1,\upsilon)$ with the measure υ satisfying for any

$(X_1,X_2)\in MRV_2(\alpha,F_1,\upsilon)$ with the measure υ satisfying for any  $(y_1,y_2)\in[0,\infty]^2\setminus{\{(0,0)\}}$,

$(y_1,y_2)\in[0,\infty]^2\setminus{\{(0,0)\}}$,

\begin{equation} \upsilon\left((y_1,\infty]\times(y_2,\infty]\right)=\left(y_1^{\alpha\beta}+\vartheta^{-\beta} y_2^{\alpha\beta}\right)^{-\frac{1}{\beta}}=:H(y_1,y_2),~~\beta \gt 0,

\end{equation}

\begin{equation} \upsilon\left((y_1,\infty]\times(y_2,\infty]\right)=\left(y_1^{\alpha\beta}+\vartheta^{-\beta} y_2^{\alpha\beta}\right)^{-\frac{1}{\beta}}=:H(y_1,y_2),~~\beta \gt 0,

\end{equation} where  $\vartheta=\big(\frac{\gamma_2}{\gamma_1}\big)^{\alpha}$. We write

$\vartheta=\big(\frac{\gamma_2}{\gamma_1}\big)^{\alpha}$. We write

\begin{align}

H^{(1)}(y_1,y_2)=-\frac{\partial H(y_1,y_2)}{\partial y_1}=\alpha \left(y_1^{\alpha\beta}+\vartheta^{-\beta}y_2^{\alpha\beta}\right)^{-1-1/\beta}y_1^{\alpha\beta-1}.

\end{align}

\begin{align}

H^{(1)}(y_1,y_2)=-\frac{\partial H(y_1,y_2)}{\partial y_1}=\alpha \left(y_1^{\alpha\beta}+\vartheta^{-\beta}y_2^{\alpha\beta}\right)^{-1-1/\beta}y_1^{\alpha\beta-1}.

\end{align}Relations (3.9)-(3.10) imply that

\begin{align}\int_{0+}^{1}V_1(y,1)dy&=\int_{0+}^{1}\int_{x}^{1}\upsilon(dy,(1-y,\infty])dx\nonumber\\

&=\int_{0}^{1}\int_{x}^{1}H^{(1)}(y,1-y)dydx\nonumber\\

&=\int_{0}^{1}\int_{x}^{1}\alpha \left(y^{\alpha\beta}+\vartheta^{-\beta}(1-y)^{\alpha\beta}\right)^{-1-1/\beta}y^{\alpha\beta-1}dydx,

\end{align}

\begin{align}\int_{0+}^{1}V_1(y,1)dy&=\int_{0+}^{1}\int_{x}^{1}\upsilon(dy,(1-y,\infty])dx\nonumber\\

&=\int_{0}^{1}\int_{x}^{1}H^{(1)}(y,1-y)dydx\nonumber\\

&=\int_{0}^{1}\int_{x}^{1}\alpha \left(y^{\alpha\beta}+\vartheta^{-\beta}(1-y)^{\alpha\beta}\right)^{-1-1/\beta}y^{\alpha\beta-1}dydx,

\end{align}and

\begin{align} \upsilon\left(\Delta\right)&=\upsilon\left((1,\infty]\times(0,\infty]\right)+\int_{0}^{1}\upsilon(dy,(1-y,\infty])\nonumber\\

&=1+\int_{0}^{1}\alpha \left(y^{\alpha\beta}+\vartheta^{-\beta}(1-y)^{\alpha\beta}\right)^{-1-1/\beta}y^{\alpha\beta-1}dy,

\end{align}

\begin{align} \upsilon\left(\Delta\right)&=\upsilon\left((1,\infty]\times(0,\infty]\right)+\int_{0}^{1}\upsilon(dy,(1-y,\infty])\nonumber\\

&=1+\int_{0}^{1}\alpha \left(y^{\alpha\beta}+\vartheta^{-\beta}(1-y)^{\alpha\beta}\right)^{-1-1/\beta}y^{\alpha\beta-1}dy,

\end{align} Similarly, we can get explicit relation of  $B(k,\alpha)$,

$B(k,\alpha)$,  $\int_{0+}^{1}V_2(y,1)dy$,

$\int_{0+}^{1}V_2(y,1)dy$,  $\int_{B(k,\alpha)}^{1}V_1(y,1)dy$ and

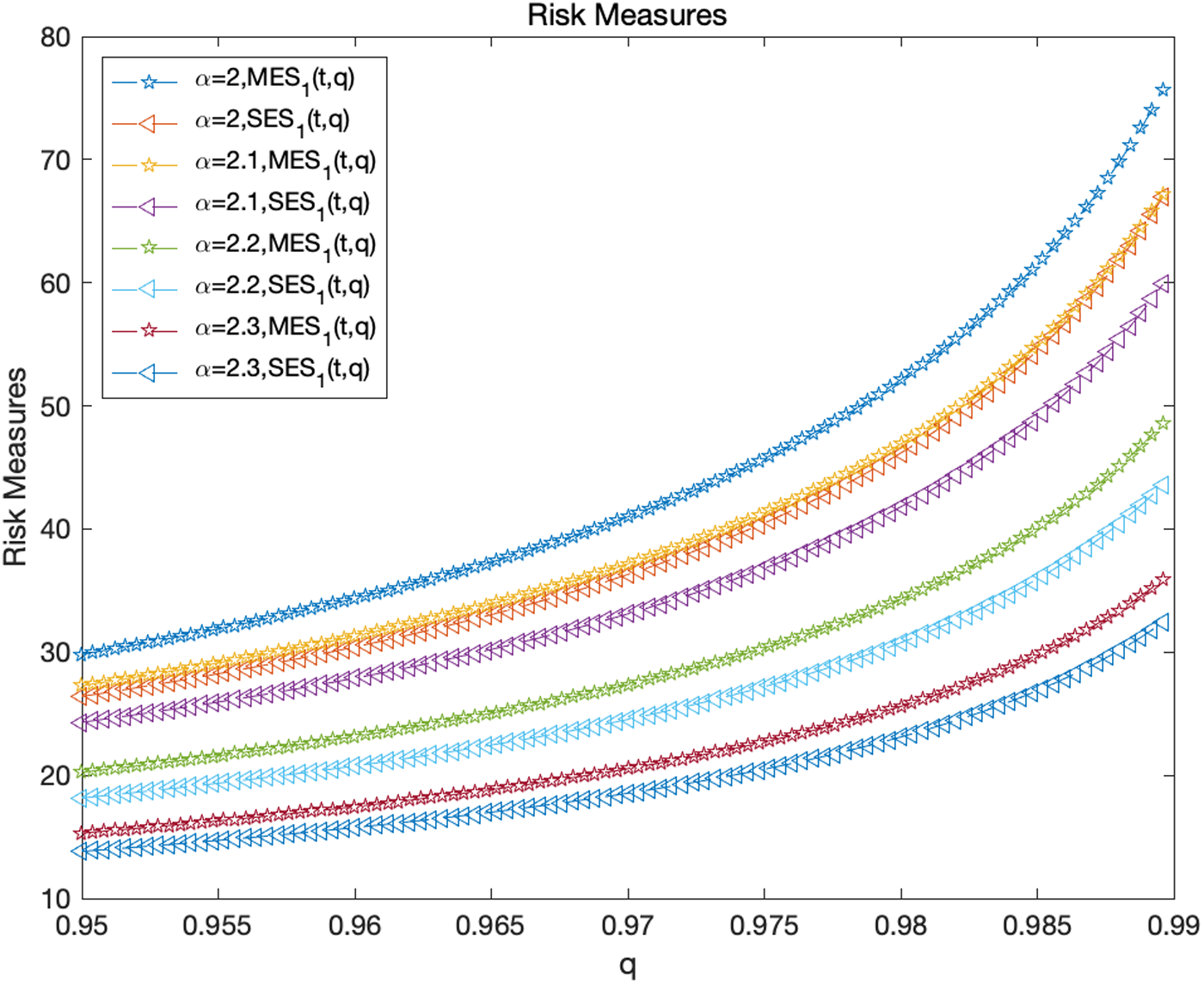

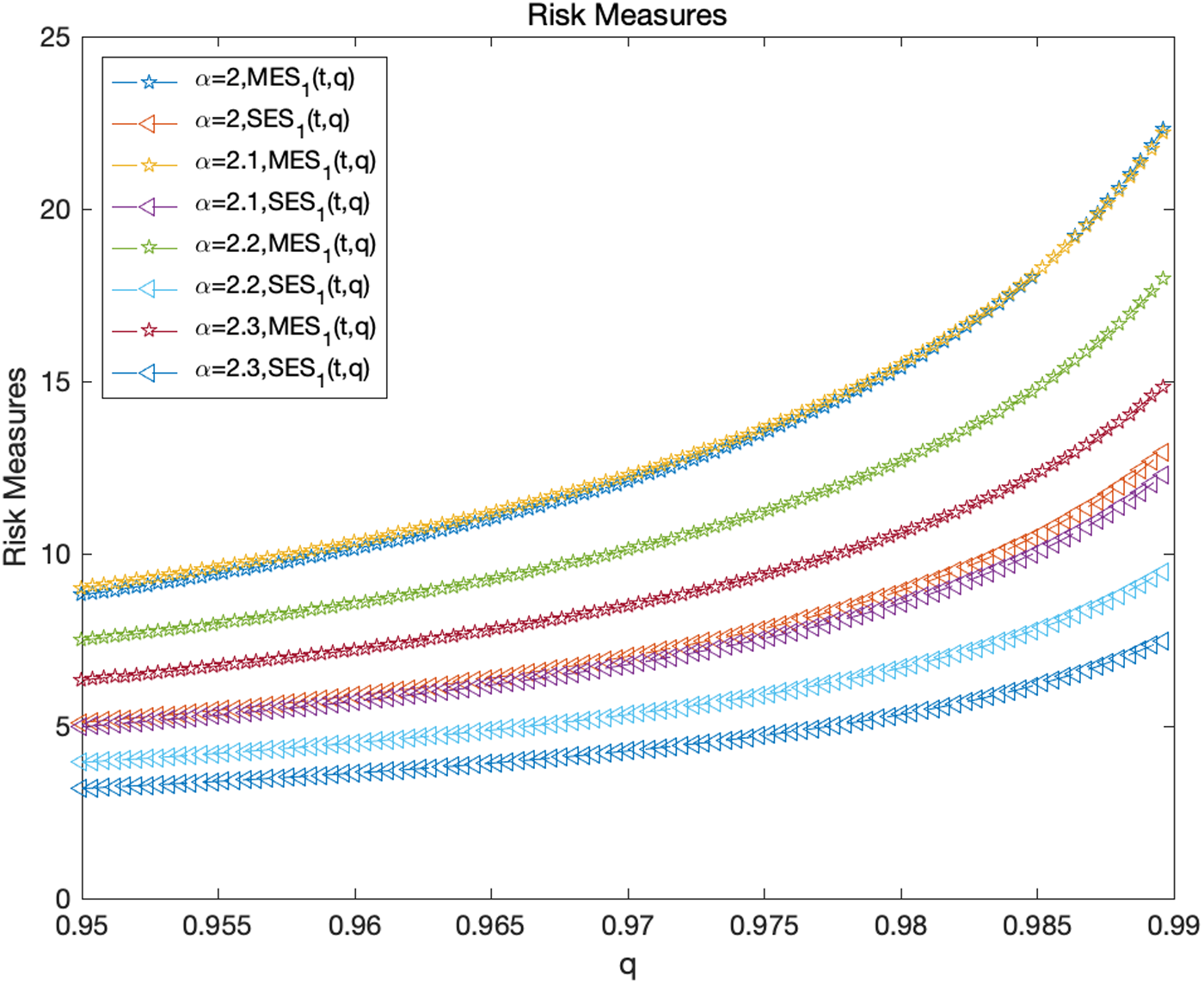

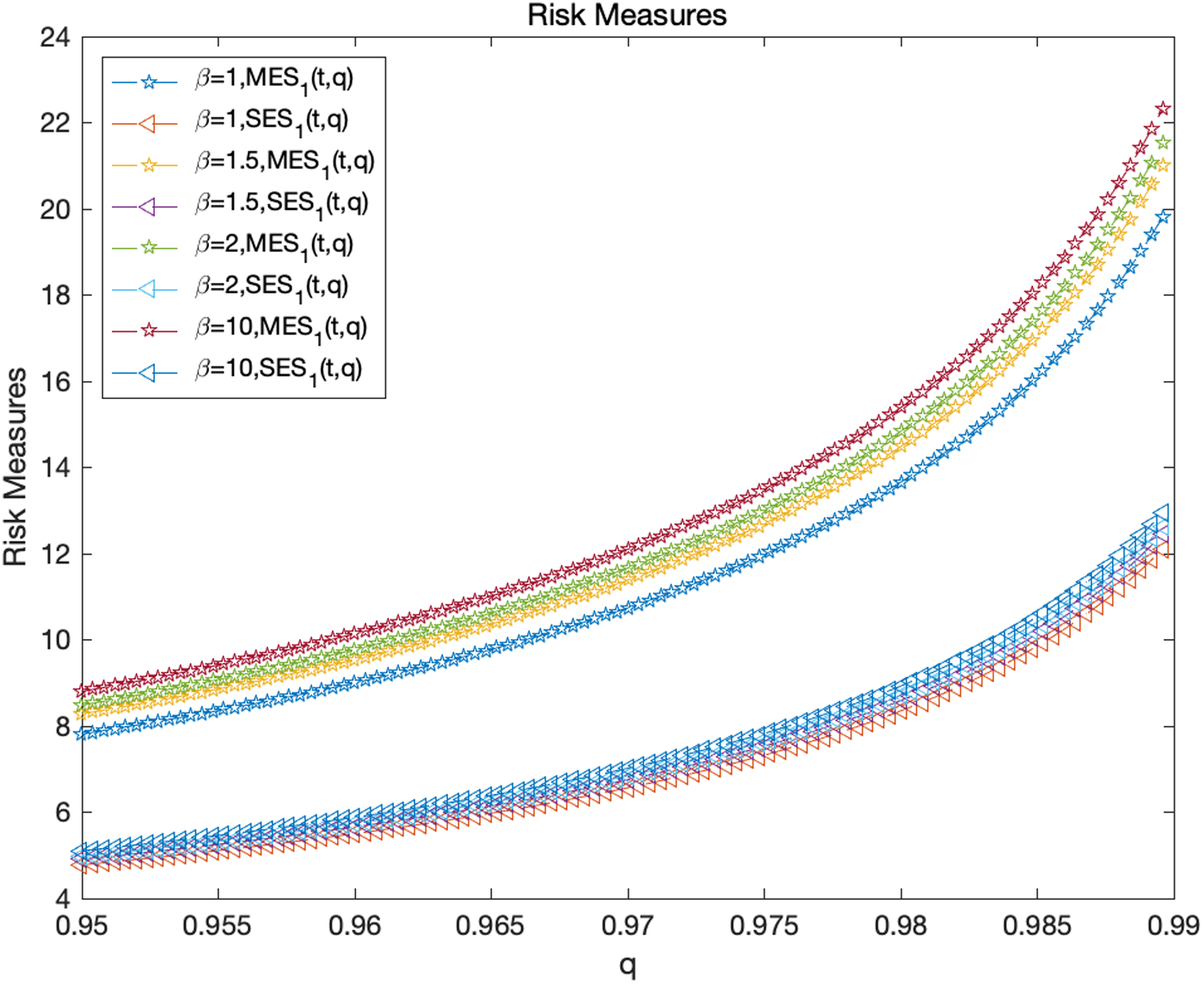

$\int_{B(k,\alpha)}^{1}V_1(y,1)dy$ and  $\int_{B(k,\alpha)}^{1}V_2(y,1)dy$. Thus, we have the ability to compute relations on the right side of Theorem 3.2. Formally speaking, the results in relations (3.11)-(3.12) are challenging to calculate directly. However, leveraging MATLAB software, we present the numerical calculation results in Section 5.

$\int_{B(k,\alpha)}^{1}V_2(y,1)dy$. Thus, we have the ability to compute relations on the right side of Theorem 3.2. Formally speaking, the results in relations (3.11)-(3.12) are challenging to calculate directly. However, leveraging MATLAB software, we present the numerical calculation results in Section 5.

4. Proof of main results

In this section, we provide detailed proof of the main results. Section 4.1 proves Theorem 3.1, supported by three key lemmas. In Section 4.2, we prove Theorem 3.2 with the aid of three lemmas.

Additionally, we introduce some results essential for proving Theorems 3.1 and 3.2. For a distribution function F, with some simple adjustments on Proposition 2.2 in [Reference Bingham, Goldie and Teugels2], we see that for any fixed  $0 \lt p_1 \lt J_F^{-}$ and

$0 \lt p_1 \lt J_F^{-}$ and  $J_F^{+} \lt p_2 \lt \infty$, there exist positive constants C 1, C 2, D 1 and D 2 such that

$J_F^{+} \lt p_2 \lt \infty$, there exist positive constants C 1, C 2, D 1 and D 2 such that

\begin{eqnarray}

\frac{\overline{F}(xy)}{\overline{F}(x)}\leq C_1 y^{-{p_1}},~~~~~~\mathrm{and}~~~~~~~~\frac{\overline{F}(u)}{\overline{F}(uv)}\leq C_2 v^{p_2},

\end{eqnarray}

\begin{eqnarray}

\frac{\overline{F}(xy)}{\overline{F}(x)}\leq C_1 y^{-{p_1}},~~~~~~\mathrm{and}~~~~~~~~\frac{\overline{F}(u)}{\overline{F}(uv)}\leq C_2 v^{p_2},

\end{eqnarray} hold for all  $xy\geq x \geq D_1$ and

$xy\geq x \geq D_1$ and  $uv\geq u\geq D_2$. It is easy to see that

$uv\geq u\geq D_2$. It is easy to see that

\begin{eqnarray}

x^{-p}=o\left(\overline{F}(x)\right),~\mathrm{for~any}~p \gt J_F^{+}.\

\end{eqnarray}

\begin{eqnarray}

x^{-p}=o\left(\overline{F}(x)\right),~\mathrm{for~any}~p \gt J_F^{+}.\

\end{eqnarray}Lemma 4.1. Let Y and Z be two independent random variables, where Y is distributed by  $F\in\mathcal{D}\cap\mathcal{L}$ and Z is non-negative and nondegenerate at 0 satisfying

$F\in\mathcal{D}\cap\mathcal{L}$ and Z is non-negative and nondegenerate at 0 satisfying  $\mathbb{E}(Z^p) \lt \infty$ for some

$\mathbb{E}(Z^p) \lt \infty$ for some  $p \gt J_F^{+}$. Then, the distribution of the product YZ belongs to the class

$p \gt J_F^{+}$. Then, the distribution of the product YZ belongs to the class  $\mathcal{D}\cap\mathcal{L}$ and

$\mathcal{D}\cap\mathcal{L}$ and  $P(YZ \gt x)\asymp\overline{F}(x)$.

$P(YZ \gt x)\asymp\overline{F}(x)$.

Proof. See Lemma 4.1 in [Reference Wang and Tang29].

Lemma 4.2. Let Y and Z be two independent random variables, where Y is distributed by F. If  $F\in \mathcal{D}$ with

$F\in \mathcal{D}$ with  $J_F^- \gt 0$, and Z is non-negative and nondegenerate at 0, then, for arbitrarily fixed

$J_F^- \gt 0$, and Z is non-negative and nondegenerate at 0, then, for arbitrarily fixed  $0 \lt p_1 \lt J_{F}^-\leq J_{F}^+ \lt p_2 \lt \infty$, there exists a positive constant C irrespective to Z such that for large x,

$0 \lt p_1 \lt J_{F}^-\leq J_{F}^+ \lt p_2 \lt \infty$, there exists a positive constant C irrespective to Z such that for large x,

\begin{eqnarray*}

&&P(YZ \gt x\mid Z)\leq C \overline{F}(x)\max\{Z^{p_1}, Z^{p_2}\}.

\end{eqnarray*}

\begin{eqnarray*}

&&P(YZ \gt x\mid Z)\leq C \overline{F}(x)\max\{Z^{p_1}, Z^{p_2}\}.

\end{eqnarray*}Proof. Following the proof of Lemma 4.1 in [Reference Wang and Tang29], we can get this lemma.

Lemma 4.3. Assume that the random variables Y1, …, and Yd are real-valued and independent random variables, distributed by F1, …, and Fd, respectively, and that the random weights Z1, …, and Zd are non-negative, not degenerate at 0, and arbitrary dependent on each other, but independent of Y1, …, and Yd. If  ${F}_i\in \mathcal{D}\cap\mathcal{L}$ and

${F}_i\in \mathcal{D}\cap\mathcal{L}$ and  $\mathbb{E}(Z_i^{\beta_i}) \lt \infty$ for some

$\mathbb{E}(Z_i^{\beta_i}) \lt \infty$ for some  $\beta_i \gt J_{F_i}^+$ and all

$\beta_i \gt J_{F_i}^+$ and all  $i=1,\ldots,d$, then the following relation holds,

$i=1,\ldots,d$, then the following relation holds,

\begin{eqnarray}

&&P\left(\sum_{i=1}^{d}Y_iZ_i \gt x\right)\sim\sum_{i=1}^{d}P(Y_iZ_i \gt x).

\end{eqnarray}

\begin{eqnarray}

&&P\left(\sum_{i=1}^{d}Y_iZ_i \gt x\right)\sim\sum_{i=1}^{d}P(Y_iZ_i \gt x).

\end{eqnarray}Proof. See Theorem 3 of [Reference Tang and Yuan28].

Lemma 4.4. Let Y1, …, and Yd be d real-valued random variables with distribution function  ${F}_i\in\mathcal{D}$ for

${F}_i\in\mathcal{D}$ for  $1\leq i\leq d$, and Z1, …, and Zd be another d non-negative random variables independent of Y1, …, and Yd such that

$1\leq i\leq d$, and Z1, …, and Zd be another d non-negative random variables independent of Y1, …, and Yd such that  $\mathbb{E}(Z_i^p) \lt \infty, 1\leq i\leq d$, for some

$\mathbb{E}(Z_i^p) \lt \infty, 1\leq i\leq d$, for some  $p \gt \max\{J_{F_1}^+,\ldots,J_{F_d}^+\}$. If Y1, …, and Yd are pSQAI, then

$p \gt \max\{J_{F_1}^+,\ldots,J_{F_d}^+\}$. If Y1, …, and Yd are pSQAI, then  $Y_1Z_1$, …, and

$Y_1Z_1$, …, and  $Y_dZ_d$ are pSQAI, respectively.

$Y_dZ_d$ are pSQAI, respectively.

Proof. See Theorem 2.2 of [Reference Li20].

Lemma 4.5. Let Y1, …, and Yd be d real-valued and pSQAI random variables with survival functions  ${F}_i\in\mathcal{D}\cap\mathcal{L}$ for

${F}_i\in\mathcal{D}\cap\mathcal{L}$ for  $1\leq i\leq d$, and Z1, …, and Zd be another d non-negative random variables, independent of Y1, …, and Yd, such that

$1\leq i\leq d$, and Z1, …, and Zd be another d non-negative random variables, independent of Y1, …, and Yd, such that  $\mathbb{E}(Z_i^p) \lt \infty, 1\leq i\leq d$, for some

$\mathbb{E}(Z_i^p) \lt \infty, 1\leq i\leq d$, for some  $p \gt \max\{J_{F_1}^+,\ldots,J_{F_d}^+\}$. Then, relation (4.3) holds.

$p \gt \max\{J_{F_1}^+,\ldots,J_{F_d}^+\}$. Then, relation (4.3) holds.

Proof. See Theorem 2.3 of [Reference Li20].

4.1. Proof of Theorem 3.1

Next, we present three key lemmas (i.e., Lemmas 4.6-4.8) in the proof of Theorem 3.1.

Lemma 4.6. (i) Under the conditions of Theorem 3.1(i), for any fixed  $t\in(0,\infty]$ satisfying

$t\in(0,\infty]$ satisfying  $P(\max\{\tau_{11},\ldots,\tau_{d1}\}\leq t) \gt 0$, we can obtain,

$P(\max\{\tau_{11},\ldots,\tau_{d1}\}\leq t) \gt 0$, we can obtain,

\begin{align}

P(S(t) \gt x)\sim\sum_{k=1}^{d}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt x\right)\lambda_k(ds).

\end{align}

\begin{align}

P(S(t) \gt x)\sim\sum_{k=1}^{d}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt x\right)\lambda_k(ds).

\end{align} (ii) Under the conditions of Theorem 3.1(ii), for any fixed  $t\in(0,\infty]$ satisfying

$t\in(0,\infty]$ satisfying  $P(\max\{\tau_{11},\ldots,\tau_{d1}\}\leq t) \gt 0$, we can obtain

$P(\max\{\tau_{11},\ldots,\tau_{d1}\}\leq t) \gt 0$, we can obtain

\begin{align}

P(S(t) \gt x)\sim\sum_{k=1}^{d}b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)\overline{F}(x).

\end{align}

\begin{align}

P(S(t) \gt x)\sim\sum_{k=1}^{d}b_k\int_{0}^{t}\mathbb{E}\left(e^{-\alpha\xi(s)}\right)\lambda_k(ds)\overline{F}(x).

\end{align}Proof. (i) By Assumption 2.1 and Lemma 4.5, choosing a large M, we can obtain

\begin{align}

P(S(t) \gt x)& \gt rsim\sum_{k=1}^{d}\left(\sum_{i=1}^{\infty}-\sum_{i=M+1}^{\infty}\right)P(X_{ki}e^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}} \gt x)=:J_1-J_2.

\end{align}

\begin{align}

P(S(t) \gt x)& \gt rsim\sum_{k=1}^{d}\left(\sum_{i=1}^{\infty}-\sum_{i=M+1}^{\infty}\right)P(X_{ki}e^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}} \gt x)=:J_1-J_2.

\end{align}For J 1, it is obvious that

\begin{align}

J_1=\sum_{k=1}^{d}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt x\right)\lambda_k(ds).

\end{align}

\begin{align}

J_1=\sum_{k=1}^{d}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt x\right)\lambda_k(ds).

\end{align} For  $0 \lt p_1 \lt \min\{J_{F_1}^-,\ldots,J_{F_d}^-\} \lt \max\{J_{F_1}^+,\ldots,J_{F_d}^+\} \lt p_2 \lt \kappa/2$, it follows from Assumption 2.1, Lemma 4.2 and the condition of tail equivalence (i.e.,

$0 \lt p_1 \lt \min\{J_{F_1}^-,\ldots,J_{F_d}^-\} \lt \max\{J_{F_1}^+,\ldots,J_{F_d}^+\} \lt p_2 \lt \kappa/2$, it follows from Assumption 2.1, Lemma 4.2 and the condition of tail equivalence (i.e.,  $\lim_{x\rightarrow\infty}\frac{\overline{F}_k(x)}{\overline{F}(x)}=b_k,~k=1,2,\ldots,d$) that there exists a large enough M such that for any small enough ϵ,

$\lim_{x\rightarrow\infty}\frac{\overline{F}_k(x)}{\overline{F}(x)}=b_k,~k=1,2,\ldots,d$) that there exists a large enough M such that for any small enough ϵ,

\begin{align}

J_2\leq C\sum_{k=1}^{d}\sum_{i=M+1}^{\infty}\left[\mathbb{E}\left(e^{-p_1\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}}\right)+\mathbb{E}\left(e^{-p_2\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}}\right)\right]\overline{F}_k(x)\leq C\epsilon \overline{F}(x).

\end{align}

\begin{align}

J_2\leq C\sum_{k=1}^{d}\sum_{i=M+1}^{\infty}\left[\mathbb{E}\left(e^{-p_1\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}}\right)+\mathbb{E}\left(e^{-p_2\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}}\right)\right]\overline{F}_k(x)\leq C\epsilon \overline{F}(x).

\end{align} On the one hand, choosing a constant M, using Assumption 2.1, Lemma 4.1 and the condition of tail equivalence gives that for any integer  $k\in[1,d]$ and any fixed

$k\in[1,d]$ and any fixed  $t\in(0,\infty]$ satisfying

$t\in(0,\infty]$ satisfying  $P(\max\{\tau_{11},\ldots,\tau_{d1}\}\leq t) \gt 0$,

$P(\max\{\tau_{11},\ldots,\tau_{d1}\}\leq t) \gt 0$,

\begin{align}

& \int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt x\right)\lambda_k(ds)\geq \sum_{i=1}^{M}P\left(X_ke^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}} \gt x\right)\geq C \overline{F}(x).

\end{align}

\begin{align}

& \int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt x\right)\lambda_k(ds)\geq \sum_{i=1}^{M}P\left(X_ke^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}} \gt x\right)\geq C \overline{F}(x).

\end{align}On the other hand, choosing a large constant M, by Assumption 2.1, Lemma 4.1, the condition of tail equivalence and (4.8), we get,

\begin{align*}

\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt x\right)\lambda_k(ds)&\leq \sum_{i=1}^{M}P\left(X_ke^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}} \gt x\right)+\sum_{i=M+1}^{\infty}P\left(X_ke^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}} \gt x\right)\\ &\leq C \overline{F}(x).

\end{align*}

\begin{align*}

\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt x\right)\lambda_k(ds)&\leq \sum_{i=1}^{M}P\left(X_ke^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}} \gt x\right)+\sum_{i=M+1}^{\infty}P\left(X_ke^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}} \gt x\right)\\ &\leq C \overline{F}(x).

\end{align*} Thus, we can obtain that for any integer  $k\in[1,d]$ and any fixed

$k\in[1,d]$ and any fixed  $t\in(0,\infty]$ satisfying

$t\in(0,\infty]$ satisfying  $P(\max\{\tau_{11},\ldots,\tau_{d1}\}\leq t) \gt 0$, the following relation holds

$P(\max\{\tau_{11},\ldots,\tau_{d1}\}\leq t) \gt 0$, the following relation holds

\begin{align}

& \int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt x\right)\lambda_k(ds) \asymp \overline{F}(x).

\end{align}

\begin{align}

& \int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt x\right)\lambda_k(ds) \asymp \overline{F}(x).

\end{align} A combination of the arbitrariness of ϵ, (4.6)-(4.8) and (4.10) gives the lower bound of (4.4) immediately. Choosing a  $\delta\in(0,1)$ and a large M satisfying

$\delta\in(0,1)$ and a large M satisfying  $\sum_{i=M+1}^{\infty}\frac{1}{i^2} \lt 1$, we can get

$\sum_{i=M+1}^{\infty}\frac{1}{i^2} \lt 1$, we can get

\begin{align}

&P(S(t) \gt x)\nonumber\\

&\leq P\left(\sum_{k=1}^{d}\sum_{i=1}^{M}X_{ki}e^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}} \gt \delta x\right)+P\left(\sum_{k=1}^{d}\sum_{i=M+1}^{\infty}X_{ki}e^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}} \gt (1-\delta) x\right).

\end{align}

\begin{align}

&P(S(t) \gt x)\nonumber\\

&\leq P\left(\sum_{k=1}^{d}\sum_{i=1}^{M}X_{ki}e^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}} \gt \delta x\right)+P\left(\sum_{k=1}^{d}\sum_{i=M+1}^{\infty}X_{ki}e^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}} \gt (1-\delta) x\right).

\end{align} Denote the two probabilities on (4.11) by K 1 and K 2, respectively. There exists some positive function g(x) satisfying as  $x\rightarrow\infty$,

$x\rightarrow\infty$,  $g(x)\rightarrow\infty$ and

$g(x)\rightarrow\infty$ and  $\frac{g(x)}{x}\rightarrow0$. Obviously, let

$\frac{g(x)}{x}\rightarrow0$. Obviously, let  $g(x)=\frac{x}{lnx}$ which satisfies the assumption condition. Take

$g(x)=\frac{x}{lnx}$ which satisfies the assumption condition. Take  $\max\{J_{F_1}^+,\ldots,J_{F_d}^+\}+\epsilon_1 \lt p \lt \kappa$ for some

$\max\{J_{F_1}^+,\ldots,J_{F_d}^+\}+\epsilon_1 \lt p \lt \kappa$ for some  $\epsilon_1 \gt 0$. By Assumption 2.1, (4.1) and Lemma 4.5, we have

$\epsilon_1 \gt 0$. By Assumption 2.1, (4.1) and Lemma 4.5, we have

\begin{align}

K_1&\sim \sum_{k=1}^{d}\sum_{i=1}^{M}P\left(X_{ki}e^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}} \gt \delta x\right)\nonumber\\

&\leq \sum_{k=1}^{d}\sum_{i=1}^{M}P\left(e^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}} \gt g(x)\right)+\sum_{k=1}^{d}\sum_{i=1}^{M}\int_{0}^{g(x)}P\left(X_{ki} \gt \frac{\delta x}{y}\right)P\left(e^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}}\in dy\right)\nonumber\\

&\lesssim\delta^{-p}\sum_{k=1}^{d}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt x\right)\lambda_k(ds)+o(1)\overline{F}(x),

\end{align}

\begin{align}

K_1&\sim \sum_{k=1}^{d}\sum_{i=1}^{M}P\left(X_{ki}e^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}} \gt \delta x\right)\nonumber\\

&\leq \sum_{k=1}^{d}\sum_{i=1}^{M}P\left(e^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}} \gt g(x)\right)+\sum_{k=1}^{d}\sum_{i=1}^{M}\int_{0}^{g(x)}P\left(X_{ki} \gt \frac{\delta x}{y}\right)P\left(e^{-\xi(\tau_{ki})}\mathbb{I}_{\{\tau_{ki}

\leq t\}}\in dy\right)\nonumber\\

&\lesssim\delta^{-p}\sum_{k=1}^{d}\int_{0}^{t}P\left(X_ke^{-\xi(s)} \gt x\right)\lambda_k(ds)+o(1)\overline{F}(x),

\end{align} where in the third step, we use the fact that when  $g(x)=\frac{x}{lnx}$, the following relation holds due to Markov’s inequality, Assumption 2.1 and (4.2),