Footwear is a key industry in many countries, mainly due to the large number of people employed throughout its production process in addition to those involved in its commercialization. Consequently, production has historically shifted from country to country, across continents, to wherever unskilled workers would accept lower wages. After all, basic manufacturing skills are easy to learn or transfer from one place to another. An abundance of raw materials is a second key factor, and the combination of both gives a competitive edge; this is exemplified by the rise of the current leading player, China.Footnote 1 The industry is mature and stable, with global retail sales estimated by Euromonitor at US$375 billion for the year 2013, and with more than 21 billion pairs of shoes manufactured every year.Footnote 2

Shoemaking is important to Mexico and crucial to the local manufacturers based around the city of León, in the State of Guanajuato. Historically, the town has centered its economic activities on the production of leather and shoes. Although thousands of artisans and small shops are still in business, reduced numbers of companies have surfaced over the years, creating large enterprises, with a few multinational companies in the making. Two of those, Grupo Flexi (also known by its registered trademark, “Flexi”) and Fábricas de Calzado Andrea SA de CV (also known by its registered trademark, “Andrea”), overshadow their competitors and are extending their activities overseas. Both are among the largest manufacturers of shoes nationwide, but their strategies, managerial skills, company values, and business trajectories show different paths towards becoming global.

In this chapter, we show how both companies followed different routes in striving for success within Mexican borders and beyond. Flexi and Andrea offer a view of the internationalization of companies in a market without a clear leader; therefore, we have an example of MultiLatinas different from the most renowned cases of Pemex, Cemex, Bimbo, or industrial groups, thus presenting the opportunity to analyze how smaller enterprises may become multinational corporations. In fact, contrary to the popular image of a multinational company as a large corporation with facilities in many countries, the commonly accepted definition also includes enterprises of smaller size, as long as they have some added value operations in foreign markets.Footnote 3

Although both organizations are part of the same industry and belong to the same local cluster, they present some important differences. Flexi is more focused on the manufacturing process and is one of the largest shoemakers in Mexico; its road to internationalization has been slow and at first reactive to conditions in global markets. Andrea, on the other hand, has shown more rapid growth leveraged on marketing strategies. This is a sales-driven organization with manufacturing capacity that has targeted the sophisticated US market as the first step to internationalization. Flexi relies on product quality and full control of its operations, while Andrea proves to be a more agile organization. The former is a valid example of the many companies following a well-thought-out plan for international expansion, with reduced exposure to the hazards of global competition. The latter presents a more appealing illustration to new ventures that are willing to address demanding consumers at once, even without previous experience abroad. Both routes have similarities but yield different results.

Ultimately, the lesson to be learned may apply to the many enterprises in similar industries in developing economies: going international is a hard choice, but it may also be the decision that could set a company apart from its competitors. In the cases of Flexi and Andrea, the internationalization process brought organizational changes, improved manufacturing capabilities, and, above all, changed managerial vision, making clear the importance of being constantly alert in order to remain competitive in global markets.

Footwear: A Global Industry

Footwear is among the most important global consumer industries, as well as one of the more peculiar. Understanding the industry requires an examination of its value chain and the threats and opportunities imposed by globalization. Therefore, in this section, we present the main factors that make footwear a unique and globalized industry.

A Look at the Industry

At first glance, the footwear industry may appear to be the simple manufacturing and selling of shoes, but there are many other sectors associated with those activities. The industry is dynamic and has overcome profound changes over the last few decades in technology, machinery, input materials, and distribution. Shoemaking is already a global process, with changes in the buying experience as well.Footnote 4

The value chain for the footwear industry is also becoming more complex and geographically dispersed,Footnote 5 with global competitors sourcing in different countries of Asia, manufacturing in Mexico, and marketing their products in Europe, as done by Nike, Crocs, and many other leading brands. Innovation has shaken the selection of the basic raw materials, as well as the entire manufacturing and marketing processes; furthermore, the diversity of products requires different industrial processes and creates a dependency upon new business models.Footnote 6

The industry faces important challenges due to rapid changes in demand, strong competition on the supply side, and a high degree of globalization. Footwear is fashion-influenced and, consequently, product life cycles are shorter and the risk of being left out of the consumer preference is always present. Fragmentation of suppliers is evident, while the need for improvements in technology, strategic intelligence, and agile supply chains imposes higher capital investments on large corporations; those are gaining leverage on the distribution channels, but without reaching a full leadership position. Retailers, on the other hand, continue widening their range of operations, favoring their own brands while new business models are created. Although the changes described are common to many industries, in the specific case of footwear the importance is amplified by the impact on employment, protectionism, and the extension of the whole global chain into an increasing number of countries.

The International Perspective

Over the years, the dominant position of developed countries has shifted to China, India, Vietnam, Brazil, and other emerging economies, including Mexico. The population is a key factor in determining the size of the consumer market, but disposable income creates an important distortion. American consumers, for instance, purchase a total number of pairs each year that is similar to the number purchased in heavily populated countries such China or India. Trade flows show Europe to be the continent importing the largest number of pairs, followed by North America. In fact, many consumers in wealthy markets consider shoes as fashion items, with per capita expenditures in the hundreds of dollars in some countries. This is the point of convergence between footwear and the fashion and apparel industry, which is a much larger industry with a market size of US$1.7 trillion and 75 million people employed during 2012, when combining both industries, according to the World Trade Organization’s (WTO) statistical data.Footnote 7

The footwear industry involves complicated dynamics of international trade. Repeatedly, nations make their debut on the global rankings, while production sites and markets change or even reverse the logistics of the flow of raw materials and finished products. Bitter rivals may suddenly become each other’s suppliers or customers, and e-business dissolves national borders. Another key element of this industry is the dependency on a few raw materials, mainly leather, which reaches approximately one-half of the aggregate cost of materials.

The Mexican Footwear Industry

Mexican shoemakers are becoming more integrated into the global footwear industry, but the Mexican industry has some distinctive insights. It is important to consider the roots of shoemaking activities in the country, the present outlook, the importance of geographical concentration of producers, and the nature of the main competitors. The information from this section will cover those points.

Historical Evolution

In the early eighties, due to the import substitution program that lasted from 1940 to 1984, the makers of many products could easily obtain a captive share in Mexico, and sometimes even a monopolistic position. The absence of competitors paved the road for shoemakers; paradise lasted for many years until the nation joined the international commercial arena.Footnote 8 In fact, between 1985 and 1994 the nation started a unilateral commercial liberalization program; by 1986 it joined the GATT and a new flow of imports had an impact on the local footwear industry. By 1994, when the North American Free Trade Agreement (NAFTA) allowed free trade of most manufactured merchandise among Mexico, Canada, and the USA, the local industry was suddenly facing much larger competitors, superior in marketing, technology, and operations expertise. Pressed by many nations, by September 2001 the country had to vote in favor of the admission of The People’s Republic of China into the WTO. Mexican manufacturers from different industries were troubled by the thought of competing at arm’s length with Chinese companies.Footnote 9 Trade associations attempted to stop unfair competition, but without visible results, while the government had little interest in protecting a decaying industry, particularly not at the expense of a commercial dispute with the Asian nation.

Although global players continue to challenge Mexican shoemakers, the local footwear industry has overcome the challenge of having to share its market with foreign competition. Production by the year 2013 reached 244 million pairs, and the country ranked once again among the top ten exporters worldwide.Footnote 10 Furthermore, its contribution to employment, total GDP, and manufacturing added value remained constant between 2008 and 2012, as shown in Table 9.1.

Table 9.1 Mexican shoe industry, 2008–12

| Shoe Industry Mexico | 2008 | 2009 | 2010 | 2011 | 2012 |

|---|---|---|---|---|---|

| Production (Mex$ million) | 12,889 | 12,548 | 13,449 | 13,192 | 13,558 |

| % Annual growth | −4.45% | −2.65% | 7.19% | −1.92% | 2.77% |

| % Total GDP | 0.11% | 0.11% | 0.11% | 0.10% | 0.1% |

| Trade balance, US$ million | −291 | −203 | −254 | −306 | −293 |

| Exports, US$ million | 260 | 259 | 329 | 411 | 520 |

| Imports, US$ million | 552 | 461 | 583 | 718 | 813 |

| % Total exports | 0.09% | 0.11% | 0.11% | 0.12% | 0.14% |

| % Manufacturing exports | 0.11% | 0.14% | 0.13% | 0.15% | 0.17% |

| Manufacturing employment | 47,470 | 45,589 | 47,955 | 47,550 | 48,389 |

| % Manufacturing employment | 1.46% | 1.54% | 1.56% | 1.5% | 1.5% |

Source: Adapted from Mexico’s Ministry of Economy (Secretaría de Economía, 2013).

Present Outlook

A brief analysis of the local footwear industry shows a fragmented industry, strong competition among dominant retail groups and a few major manufacturers, and reduced buying power from consumers.Footnote 11 Large manufacturers have the upper hand on the supply side, even though they are negligible in number (probably around 2 percent of the total industrial base), as compared with the thousands of small and medium enterprises (SMEs), out of the estimated 7,398 shoe-manufacturing units.Footnote 12 The little regulation also favors atomization of production, since entry and exit barriers are minimal; labor legislation and environmental protection are two issues of concern, but laws are either not too stringent or not properly enforced, especially in the case of smaller companies. Those enterprises also benefit from the lack of brand recognition, although at the expense of downward pressure on pricing.Footnote 13

Even though few companies are export-oriented, total sales abroad reached approximately 26 million pairs in 2012, with revenues of US$520 million. In spite of these positive figures, there is a trade deficit in this industry, with imports of 68 million pairs to satisfy the demand for less expensive products from a growing population. Vietnam is the leading exporter to Mexico, with 33 percent of total value, followed by China and Indonesia, with 17 percent each. Mexican shoes, though, have a significantly higher added value than less expensive shoes imported from Asia. A breakdown of Mexican exports per country indicates an overwhelming concentration in the US market, roughly 80 percent of value and quantity.Footnote 14

Geographical Concentration

The industry in Mexico presents a high degree of geographical concentration, with approximately 68 percent of production located in the state of Guanajuato, 18 percent in the state of Jalisco, and 13 percent near Mexico City and the neighboring State of Mexico. The reason behind such concentration is explained by a historical presence in some locations of skilled artisans and suppliers specializing in their own lines of products, such as men’s and children’s shoes in León, women’s shoes in Jalisco, and athletic shoes around Mexico City.Footnote 15

León, known as the capital city of the footwear industry, is the most important urban area in the state of Guanajuato and ranks fifth in population in the country, with more than 1.5 million people, a number of thriving industries, and a large number of family-owned businesses. Its inhabitants have made their living making shoes over many decades and entrepreneurs have been there since early times when merchants and artisans from northern Mexico established themselves within the boundaries of modern León.

There are different factors at the root of the footwear industry in León but, arguably, “the four pillars” are the clustering of activities, direct commercialization of the products, entrepreneurial skills, and trade associations. The first factor is very evident, as demonstrated by a myriad of tanneries, or tenerías, and small shoe-making shops, or picas, usually with fewer than ten employees. Although work is done with little machinery, in aggregate those small shops supply many thousands of shoes daily. The second factor, direct selling of shoes, is almost as old as the manufacturing of the product and has been present in León for many years, especially at the tianguis or informal markets. The third pillar is the entrepreneurial culture, which seems to be inherited by people from León. Companies are constantly created by those who learn how to use the tools of the trade. Finally, trade associations are paramount to the industry’s success, especially as they are capable of securing the support of government entities at the local and federal level. Cámara de la Industria del Calzado del Estado de Guanajuato (CICEG), a trade organization with more than one thousand members, is leading those efforts, especially by being the organizer of SAPICA, a trade show that attracts hundreds of qualified buyers from around the globe by exhibiting the local offering. The main supporting entities are ProMéxico, the federal entity devoted to foster trade, foreign investment, and the internationalization of Mexican enterprises; and the Coordinadora del Fomento al Comercio Exterior (COFOCE), a governmental organization for the promotion of trade in the State of Guanajuato. The above-mentioned four pillars could be considered the cornerstones of the industry’s success in León, but other factors are helping the city, such as a frenzy of logistical activities at Guanajuato Puerto Interior, an inland port that serves the shoe industry by providing logistics support to exporters, and the role of universities, among others.

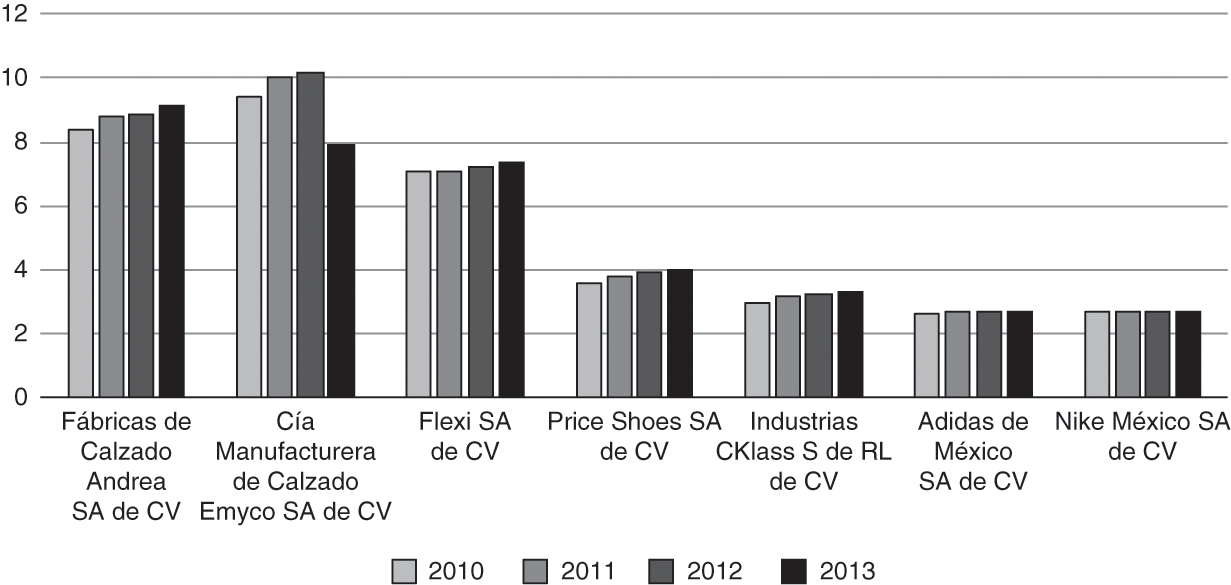

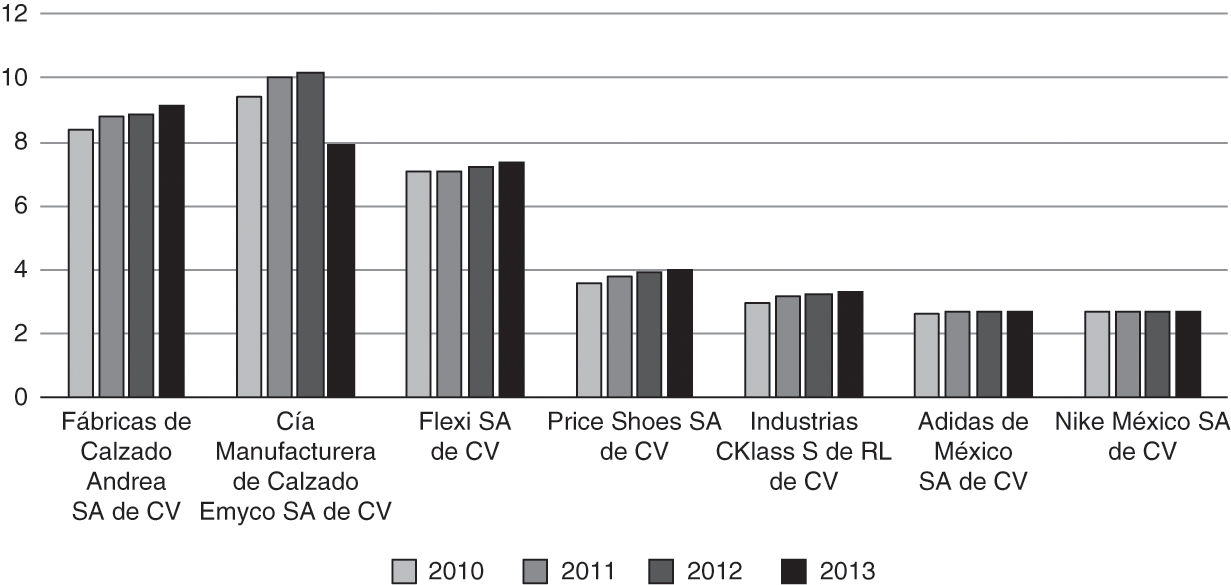

Competitors

In terms of market share, three Mexican companies hold similar percentages: Andrea at 9 percent, Emyco at 8 percent, and Flexi at 7 percent, while the rest of the competitors have minimal representation. Figure 9.1 provides a picture of the main competitors by National Brand Owner (NBO).

Figure 9.1 National Brand Owner (NBO) company shares of footwear by percentage value, 2010–13

Andrea started as a little shop in 1973 and later ventured into selling through leaflets. After seven years, it built a plant in León and spread all over the nation.Footnote 16 Andrea has been adding new product lines and is becoming the industry leader.Footnote 17 Emyco started in 1926, and during the sixties and seventies signed licensing agreements to produce international brands, also selling those in the national market. From this collaborative experience with American companies, Emyco obtained state-of-the-art technology and gained a quality image associated with the Hush Puppies and Florsheim brands.Footnote 18 Ever since, Emyco has been one of the leading manufacturers, with a yearly production of more than four million pairs, owning over 100 stores throughout the country.Footnote 19

Flexi is a family-owned group that started in León in 1935 and expanded vertically during the seventies. The company produces over thirteen million pairs a year, and is also the leading exporter, with a large number of its own stores both locally and in different foreign markets.Footnote 20 No other competitor is of a similar size, but there are other important local players. C-Klass and Prices Shoes, both based in the Guadalajara area, are rivals to Andrea in selling through catalogs, while Grupo Cuadra has gained international recognition in the exotic leather segment. Cuadra started operations in León in 1991 and after two years was able to export boots; soon after, the group started its own network of high fashion stores around the country and is presently expanding into the USA.Footnote 21

Flexi and Andrea

As previously stated, León is home to a concentration of leading shoe makers in Mexico. Two of those, Flexi and Andrea, are especially important because of their size, impact on employment, technology use, and marketing efforts, among other factors. In this section, we present an overview of the history of both companies, as well as their internationalization process.

The Rise of Flexi

In 1935, Mr. Roberto Plasencia Gutiérrez (“Don Roberto”) started his own shop, as was often done in León, and many years later, during the sixties, it became Flexi, a shoe-making company with modern serial production. By 1973 Flexi started to export shoes under its own brand name,Footnote 22 and by 1988 its private brand, Flexi Country, gained popularity in the local market and also became an international success. The firm employs approximately 4,600 people at four different plants, with a direct presence in foreign markets and a strong reputation for quality.

Leadership has not been an issue over the years; the founder of Flexi was successfully replaced by his own son, also known as Don Roberto (Plasencia Saldaña). The first Don Roberto was the founding father, but the next one was remarkable as well. By 1963, the son took full responsibility for consolidating the organization as a business group. By 2015, a third Don Roberto (Plasencia Torres) was taking over the leadership of the company, backed by a great deal of experience in marketing and sales within the organization.

Although the personalities of the leaders were of great importance to Flexi, the fact is that the organization followed a clear path; at the core of the business model there is a value proposition for quality and comfort, backed by Flexi’s leadership in product design and manufacturing according to high-quality standards and advanced technology.Footnote 23 The Flexi brand was born in 1965, but it was probably the launch of the Flexi Country brand in 1988 that demonstrated to Don Roberto that good quality alone was not sufficient to reach broader markets. The company was betting on promotion and communication with the client, and nowadays it also shares information with the customer base through its own website and popular social networking services, while it conveys information to the market through advertising in printed and digital media. Flexi is capable of reaching customers in sophisticated markets such as the USA, Japan, Canada, and the European Union, as well as countries in Latin America and Asia, using its own network of 326 stores and international distributors, either directly or through its e-commerce system.Footnote 24 Over 4,000 major clients, including a few department stores, support wholesales all across the local market and abroad.Footnote 25 Table 9.2 shows a timeline with important landmarks in the history of the company.

Table 9.2 The road to success for Flexi

Note: Data from Euromonitor 2014 and corporate data from Flexi.

Key activities for Flexi are related to the production and distribution of shoes, a process where innovation and manufacturing techniques based upon quality control systems are of utmost importance. In the whole process of reaching customers, Flexi relies on key partners, mainly foreign suppliers of raw materials and a network of thirteen local companies that carry out maquiladora production, as well as outsourcing from four companies in Vietnam.Footnote 26 At the bottom of the structure, there is a system for tracking new fashion trends, improving quality standards, and administrating its own store chain, as well as managing marketing, logistics, and corporate social responsibility programs.Footnote 27 This structure is funded by the revenues generated from the sale of more than 13 million pairs a year through its own store chain, exports, and wholesales through authorized distributors.Footnote 28 Flexi is a privately held company and therefore does not report financial data or information about its foreign export activities or sales from subsidiaries.

Flexi: Going International

Flexi went through several different stages throughout its internationalization process, as described by the import/export director and the international sales director and summarized in the next paragraphs.Footnote 29 The process started in 1985 when many Mexican companies were approached by global brands to outsource their production. The lack of opportunities in the national market was a driving force for Flexi, as well as many other enterprises, to look for opportunities elsewhere. Nevertheless, production specifically for export markets started after 1994, when NAFTA favored the import of better raw materials at reduced prices and the export of finished products processed under the PITEX program, an export promotion tool designed to favor direct investment in Mexico through fiscal concessions to local and foreign companies producing for export markets. A sour end to the maquiladora boom came as the Mexican shoe industry started to lose international competitiveness and could no longer face Chinese and Asian manufacturers. During those years, the country was lagging behind in technology and product quality, while input prices continued to rise. Worsening conditions were difficult to ignore, but few people were as outspoken as Don Roberto Plasencia, who gave a warning to the local shoe industry. According to his view: “in a world of global competition, it is difficult to sleep quietly. What happens in any corner of the world has an impact in distant places. I see this as an opportunity: yes, we need to be cautious, but we also need to be confident in our own strength.”Footnote 30

That was the appropriate timing for the enterprise to devise its own international strategy, relying on the Flexi brand. By 2001, the organization had created “Brand Positioning in International Markets Plan,” a document that would set the compass for international expansion. The plan was flexible enough to privilege domestic sales while looking for opportunities in new markets. Following this plan, Flexi ventured into Central American countries such as Costa Rica (seven stores), Guatemala (six stores), Honduras (three stores), and El Salvador (two stores); Costa Rica has been the market with the strongest presence, and the entry into each country did not follow a straight timeline. The second major move was to enter the US market through a strategic alliance with a Mexican catalog sales company specializing in cowboy boots. Although it was a positive experience, Flexi tried afterward to concentrate on marketing its own brand through its own sales channels. On a third stage, Flexi reached a number of spread-out markets, such as Canada, countries in the Middle East, and Japan. The opening in 2009 of a distribution center near the local airport provided a backbone for exports and international distribution; in fact, the center allows for an inventory of two million pairs and is technologically advanced.

Flexi’s success has made previous roadmaps to international expansion obsolete. The brand is present in major international trade shows, which allows for better international recognition. While the organization contemplates a further advance in Europe and Asia, its presence in Central American countries keeps growing steadily. Flexi is the leading brand in Costa Rica, while Panama, Nicaragua, and Peru are the immediate targets for wholesaling. The US market, though, has proven to be the new frontier. After a good response to a virtual shoe shop, Flexi opened its first three retail stores and has opened three more under its own brand and property. The stores are located in shopping malls in Texas and Oklahoma.

The expansion will continue: management has found an ideal formula, blending a pleasant shopping experience through the Internet while offering physical stores that reassure the customer about the design and quality of the product. Although future plans for the USA have not been disclosed, Flexi is positioning its brand in such a competitive market. In only two years, the company has more than doubled the number of stores in Guatemala, Costa Rica, El Salvador, and the USA, reaching 24 stores overall outside Mexico. There is a mixed approach to ownership of the stores: in the USA, the stores are fully owned by Flexi, whereas in other countries the organization looks for partners with expertise in the local market.Footnote 31

The Rise of Andrea

Andrea started operations in 1973 in Mexico City, as a large shop. Roberto Ruiz is the CEO, but his public appearances are infrequent at best, and it is hard to find a directory of the company or the organizational chart. Very early on, he came out with the idea of selling shoes directly through leaflets and catalogs; sales increased exponentially and consequently, Andrea needed a large plant to satisfy demand. In 1980, management chose to build the new facilities at the León cluster; this was a major turning point in the history of Andrea that led to its becoming a strong shoe-making company.

The direct selling system continued in parallel with the new manufacturing activities, and by 1990 Andrea started geographical expansion through the opening of its own chain of stores, first in Mexico and then in the USA. In 2005, the company expanded its product lines with the Mia brand of lingerie. One year later, Andrea created new brand names for men’s shoes, such as Forastero, created specifically for the American market. In 2007, the company launched a new line of beauty products for women and a line of blue jeans. Table 9.3 shows a timeline with important landmarks in the history of the company.

Table 9.3 The road to success for Andrea

| Year | Domestic Market | International Impact |

|---|---|---|

| 1973 | Production starts in Mexico City | |

| 1976 | From sales to local shoe stores to leaflet sales | |

| 1980 | First plant in León and corporate offices | |

| 1990 | Sales spread nationwide with stores in nine towns | |

| 1993 | First shoe catalog using celebrities and more fashionable products | |

| 1998 | New distribution center provides higher capacity for national sales expansion | |

| 2001 | Product line expansion into lingerie with the Mia brand | First outlet in Chula Vista, California |

| 2005 | New line expansion with IU cosmetics and beauty care products and Andrea Jeans | Ferrato and Forastero brands designed for the American market |

| 2006 | ||

| 2007 | ||

| 2011 | E-commerce with HotSALE | |

| 2013 | Credipag, proprietary credit system | 17 international stores |

| 2015 | Special product launch for the 40th anniversary | Exports to Brazil, Colombia, Guatemala, Argentina, and Spain |

| 145 stores in Mexico |

Note: Information from Andrea web page and additional sources.

Over the last 40 years, Andrea has built an unusual organization. It is hard to define its true nature: the core business is still footwear, but the firm is targeting different segments with a growing array of products, especially in apparel and fashion. The many thousands of sales associates (more than 180,000) make Andrea a major player in direct marketing in its home country, with the potential to compete with different product offerings. Direct marketing has granted many people a very desirable value proposition, which is to start their own business with the potential to sell products from a diversity of product lines. The system, called “Estrellas Andrea” (or in English, Andrea Stars), is complex and looks to provide a number of increasing benefits to loyal associates and forge a feeling of partnership with them. They create “a network of friends, family, and acquaintances through samples of products, where profits are given by the sales volume of each person.”Footnote 32 Andrea Stars purchase catalogs at marginal prices, which they use, in turn, to show available products to their customers. They can purchase those products with discounts that range from 20 to 30 percent, with additional bonuses that range from 3 to 15 percent, once they reached pre-established quotas. They pick up the product at the nearest point of sale, deliver it to the customer, and secure payment. In addition to the sales network, there is a distribution chain with 145 stores in Mexico and 17 in the USA, all supported by telemarketing and customer care programs.

The exceptional growth of Andrea is based on offering products of acceptable quality, affordable price, and deferred small payments, while its promotional strategies make it easier for the sales force to reach the customer base. Billboards and printed advertising in magazines and its own catalogs have made Andrea a well-recognized brand. In 2013, the firm dropped the use of celebrities in favor of using normal models, with an increase in mass media publicity.Footnote 33 Andrea has seen a strong growth in sales value, reaching Mex$13.6 billion (equivalent to US$1 billion) in 2013, Mex$12.2 billion during 2012, and Mex$11 billion for the year 2011. Revenues come from different sources, mainly women’s footwear, men’s footwear, women’s underwear, and children’s footwear.

Although Andrea made changes in its product offerings, the most relevant strategic moves involve production strategies and retail operations, along with bold actions to increase brand recognition and geographical extension. Production, in fact, is based on outsourcing from 35 factories in León, Guadalajara, and Mexico City, with some imports from Asia.Footnote 34 Another area of importance to management is social media; in fact, an analysis of the corporate Facebook page over the first three months of the year 2014 showed satisfaction among users, with few complaints and widespread agreement with the content generated by Andrea, especially those messages with images and little text.Footnote 35

Retail is the key to further growth; customers have access to the company’s own brands as well as to additional leading brands at the many different points of sale. Stores give support to direct marketing activities and changes are expected in the immediate future, such as an Internet-based selling platform that presumably will be the backbone for further expansion in local and international markets in a more distant future. The company is venturing into e-commerce by offering products directly through its own web page and by participating in nationwide coordinated events in Mexico such as the Hot Sale, a four-day online shopping event that attempts to replicate Cyber Monday.Footnote 36

The organization has also been successful in financial terms, and it generates different revenue streams. A large percentage of sales are in cash or on short-term financing, which gives the company the potential to invest in new outlets, and Andrea Stars’ purchases for their own personal use add more cash to the main selling activities. Andrea has developed its own proprietary payment system called Credipag, which offers sales associates the ability to receive immediate payments through debit or credit cards, with the option of deferring payments with no interest charges for up to three months and easy financing for up to six months. No other competitors have a similar system, which clearly gives Andrea a competitive edge in a segment of the market where many customers have limited access to credit or even basic banking services. Andrea is a privately held company and therefore it does not report financial data or information about its foreign export activities or sales from subsidiaries.

Andrea: Going International

Most probably, the internationalization of Andrea came as a part of its expansion frenzy in Mexico. The growing number of outlets, the increasing number of Andrea Stars, and their ties to compatriots on the other side of the border paved the road to the US market. At first, sales were made through the so-called paisanos, first-generation Mexican residents in the neighboring country; Andrea was appealing to the Hispanic community, where the brand was identified as fully Mexican. In fact, as of today, the corporate websites for American consumers address potential buyers and distributors in Spanish, without an English version. Only specific instructions for Andrea Stars and directions for locating stores are translated into English; even the name Estrellas Andrea is used, instead of the easy translation into Andrea Stars. The major difference, though, lies in the technology supporting sales in the American market: Andrea Stars have access through the Digital Ordering Kiosk, the Internet Ordering Systems, and the Automatic Telephone Ordering System. The return policy is also more generous.

In 2001, Andrea opened an outlet in Chula Vista, California; by 2014, there were 17 fully owned stores in the USA, covering the states of Arizona, Colorado, Georgia, Illinois, Nevada, and Texas. California has the strongest presence, and the cities serviced by Andrea range from small ones, such as Santa Clara, to large metropolitan areas, such as Greater Los Angeles or Chicago. The common denominator, though, is the presence of large Hispanic populations. In addition to the points of sale, Andrea operates its own logistic systems with eight warehouses distributed on both sides of the border.

Andrea operates in the USA through different companies, such as Andrea West USA LLC in the city of San Diego, California, and Andrea Apparels, which also acts as a distributor of Mexican footwear brands and provides logistics support for other direct marketing organizations.Footnote 37 Nowadays the organization is looking at different markets, such as Asia, where it analyzes the possibilities of extending its direct-selling model to China.Footnote 38

Lessons for International Managers

In this section, we compare the internationalization processes of Flexi and Andrea, sharing the lessons that both enterprises may offer to managers in developing countries. Those lessons are intended for business people planning to expand into foreign countries, mainly in Latin America. In fact, many companies in the region need to deal with non-supportive governments, fierce competition with firms of similar size, and well-established foreign brands. Nevertheless, the lessons may also be valuable for enterprises worldwide, especially those trying to reach consumers in highly competitive markets such as the USA.

Two Ways to Reach International Markets

The internationalization processes of Flexi and Andrea cannot be separated from the rise of the local shoe industry in León; in fact, it would be hard to understand the success of either organization if it did not fall under the umbrella of the local cluster. Although shoe companies had been exporting for decades, only a slow process of adjusting to foreign competition, developing skills, and building their business models allowed both companies to emerge with the new breed of Mexican MultiLatinas. The context was as critical as ever: during the eighties, a flock of foreign purchasing agents visited León. They were astonished by the low costs and the skills of artisans; eventually, they started the maquiladora process, which in turn allowed shoemakers to grow and look at international opportunities.Footnote 39

The time was ripe for Andrea and Flexi to go international since they had already built the muscle for serving foreign markets. As we can see in Table 9.4, both organizations have some similarities. They employ a relatively similar number of people, taking into consideration that Andrea Stars are not employees, and almost match each other’s market share. In addition, both organizations use some of the same promotional strategies and focus their business on shoe making and the marketing of their own products. The differences, though, are evident in terms of the relationship with the customer base: Flexi meets the customer in 302 outlets spread nationwide, while Andrea offers only half that number of points of sale. Flexi brings the customer a high-quality product at a fair price, while Andrea offers average quality at a relatively higher price, which includes generous commissions to the sales associates that are technically treated as discounts on the final price of the products.

Table 9.4 Flexi and Andrea: comparison inside and outside Mexico

| Inside Mexico | Outside Mexico | ||||

|---|---|---|---|---|---|

| Features | Flexi | Andrea | Internationalization | Flexi | Andrea |

| Experience in local market | Since 1935 | Since 1973 | Experience (first exports) | 1988 | 2003 |

| Employees | 4,600 | 3,000 | Markets served | Multimarket: Costa Rica (7)*, US (6), Guatemala (6), Honduras (3), El Salvador (2) | Single market: USA (17) |

| Market share | 7% | 9% | |||

| Distribution channels | Department stores, independent distributors, own store chain | Sales associates and own store chain | Distribution | Own store chain, web platform, authorized distributors | Own store chain and sales associates, eight distribution centers in the USA |

| Outlets | 302 | 145 | Outlets | 24 | 17 |

| Promotional strategies | Outdoor advertising, printed media, points of sale, web platform | Outdoor advertising, printed media, personal promotion, web platform | Trade shows | Very active | Only purchasing and sourcing activities |

| Brand (perception) | High quality, fair price | Average quality, slightly overpriced | Commercial missions | Active | Seldom |

| Innovation strategies | Product, design, and quality | Marketing and finance | Online platform | Same for Mexico and USA, in English, local stores information, communication, and content | Web page slightly different from Mexico, mainly in Spanish |

| Online platform | Sales, product information, and social media | Customer service and specific sales promotions, social media | Sophisticated ordering systems: digital ordering kiosk, Internet ordering system, and automatic telephone ordering system | ||

| Ownership | Family owned | Partners | |||

| Product offering | Footwear, men’s and women’s, and limited supply of accessories | Footwear, men’s, women’s, children’s, bags, clothing, beauty products, and cosmetics | Central America: same as Mexico, except for local store information and contact | ||

| Payments | Cash and credit card for customers and trade credit to distributors | Direct credit to sales associates and proprietary payment system | |||

Note: Information from Andrea web page and additional sources.

* the number in parenthesis indicates the total number of stores per country, 2014.

The differences are even more important in terms of international vision. While Flexi ventured first into markets of lesser importance, Andrea went straight ahead into the American market. Flexi worked patiently, building a network of stores exclusively promoting its own brand, whereas Andrea made changes to the product offering, adjusting to consumer tastes in the Hispanic market. Flexi tried different formulas, such as partnerships or alliances in the US, until it decided to proceed with direct ownership of the outlets; Andrea, on the other hand, never agreed to share control of the operation.

Flexi shows the benefits of sticking to a brand name, controlling every step of the operation, and cautiously following a roadmap from the easier markets to the hardest market. Andrea’s example, on the other hand, shows a way to achieve international success for those companies with more aggressive marketing strategies. This is a sales-driven organization, like many others that become successful in a short time, with a different business model, making products more appealing to local customers in different markets. Flexi offers uncompromised quality, while Andrea gets closer to the customer, turning sales associates into buyers and later on into business partners. In both cases, management runs a tight ship and leadership is transferred through generations. Business plans are carefully followed, although Andrea seems to be more capable of making major turns, such as in the case of entering foreign markets. Andrea, indeed, shows how to generate incremental business through networking, splitting profits with thousands of associates, and reaching out to specific demographic groups such as the Mexican migrant population in the USA; customers are Spanish-speaking people already established on the other side of the border, independent of their legal status.

Andrea and Flexi, both in national and foreign markets, do not relinquish control of their operations. Flexi has a reputation for strict quality control during the manufacturing process, while Andrea focuses more on controlling the sales process, even in minute detail. Both companies ventured into other markets after local success. Flexi has been open to the world for many years, actively participating in trade shows and commercial missions, with permanent representation in local institutions fostering exports. Andrea, on the other hand, sends its own purchasing representatives to major footwear events. They do not exhibit products; they strike deals, mainly for input materials.

As previously stated, both organizations reached the US market following different paths: Flexi ventured in after many years of experience in fragmented markets, while Andrea entered the same country without relevant international experience. Much of the information for this chapter was collected through interviews, but the reasoning behind Andrea’s decision to go international remains unclear. Apparently, it was not a deliberate strategy, but happened naturally, mirroring the flow of people, products, and ideas between the bordering countries. Flexi, on the other hand, designed a plan for internationalization; in fact, it had to back up on a number of occasions because of macroeconomic factors, financial obstacles, or a partner’s decisions. In the end, the organization learned the lessons and changed course. Changes in leadership had a profound impact in Flexi, but not in Andrea. Both companies had their own landmarks tied to changes in production, marketing strategies, and technology improvements.

MultiLatinas Entering the American Market

The experience offered by the two Mexican shoe companies could be of value to enterprises of other nationalities expanding from their home ground, in particular to the American market. The US market is one that few Mexican companies dare to enter with a direct presence. On the positive side, the Hispanic market accounts for 16.9 percent of the US population. It is a $1.5 trillion market, considering only disposable income, which is more than the GDP of the vast majority of the countries in the world.Footnote 40 It is also a peculiar market where Spanish is spoken along with English or vice versa, which means that companies with the required language and cultural capabilities have a natural advantage. Their commercial message may reach the nostalgia market in second- or third-generation Mexican American families that have much larger purchasing power. On the negative side, the market has plenty of restrictions, rules, and regulations to abide by that only costly legal specialists can handle properly. Insurance is a must, and the legal system is completely different from Mexico’s, as are the distribution channels, sales territories, and financial or fiscal issues.Footnote 41 Those are perilous waters for naïve exporters or investors, but Andrea had no hesitations and was determined to extend its commercial success against all odds. Flexi followed suit, but only once it felt prepared.

Organizations from different parts of the world might be tempted, as in the case of Flexi, to proceed cautiously through minor neighboring markets until ready to face major competitors in the US. Although this is a preferred path for many companies, it might not be in tune with modern times. In fact, managers looking to become global players will have to face the difficulties associated with serving sophisticated buyers immediately, leaving aside tortuous itineraries through minor markets. The opportunities are not limited to Mexican enterprises, as globalization favors the marketing of products or services from every corner of the planet.

Another important lesson for international managers relates to the double-edged sword of dealing with Asian countries, mainly China. On the one hand, sourcing from those countries reduces manufacturing costs; on the other hand, it is the easiest way to open the door to foreign competition. Mexican shoemakers tried to stay away from those competitors, focusing their efforts on demanding trade barriers from their government. In the specific cases of China and Vietnam, the result of such strategies had doubtful results; to some, those barriers kept the Mexican shoe industry alive for a number of years, while others point to a different reality, namely, the overwhelming presence of Chinese and Vietnamese shoes in the local market.

Conclusions

In the previous section, we presented some suggestions that may be valuable for international business people. Those lessons may apply to different situations, although the recommendations were intended for decision-makers in developing markets, especially in Latin America. There is much more to learn from Flexi and Andrea; both organizations reacted to: a) a similar environment, Mexico; b) the same industry, shoe manufacturing; and c) the same local competitive environment, the city of Leon. The main decisions, though, were dependent upon the use of technology, funding for the operation and expansion projects, the commitment to innovation, and organizational decision making. Those differences were more difficult to perceive while Flexi and Andrea were conducting business within the same market. In fact, they never became fierce competitors, as each company was addressing its own customer base. Indeed, the divergence became notorious when both organizations ventured into foreign markets. That was the point in time when the differences in their fundamental values and strategies showed two distinct enterprises. Flexi follows a more conservative approach to doing business while offering fair value to the customer. Andrea, on the other hand, is constantly seeking new ways to please the consumer, with a more appealing proposal at the expense of quality.

Flexi and Andrea are not ordinary organizations, but there are many other companies in Mexico with the potential to venture into foreign countries, especially in the shoe industry. Those companies will have to decide upon the entry mode to other markets. Some will consider Central America as the first step to internationalization; after all, those territories are unappealing to most of the largest MNEs, there are no language or cultural barriers, purchasing power is relatively similar, and the geographical proximity has a positive impact. That was the roadmap followed by Flexi. Andrea, instead, was looking at the American market at the outset of its intentions of selling abroad.

Entering the American market was a matter of choice for Flexi and Andrea, but presumably, Mexican companies going international in the future will face no similar dilemma. By the year 2050, the Hispanic market in the USA will reach 128.8 million people – more than the entire population of Japan – with immense disposable income. Much wealth is already being transferred from Mexico to the northern side of the border, which means increasing investments and business opportunities. Startup companies are already multiplying in Mexico, looking at opportunities in Silicon Valley or the most sophisticated segments in the USA. Andrea may offer a great example to those ventures, with the hint of innovative business models. The lesson may apply, as well, to enterprises in other developing countries, and the same reasoning is valid when looking at other developed markets.

Are Mexican companies at a disadvantage when going overseas? The issue has been a subject of debate and there are many different answers. The label “Hecho en México,” or “Made in Mexico,” may have a good or bad impact depending on the product promoted. Some people may be reluctant to fly on an airplane fully assembled in Mexico, but the label works positively in some industries. In reality, the national automotive industry is in the top rankings for quality and safety, while the incipient aerospace industry is attracting many manufacturers. In the shoe industry opinions vary widely, although the fact is that Mexican shoes lack international recognition.Footnote 42 Few brands are even known to foreign consumers, but a positive effect can be seen in Latin American nations. In some of those, especially in Central America, the country is perceived as an industrial giant, even technologically advanced.Footnote 43 Is the perception of Made in Mexico changing after the success of Flexi or Andrea? Most probably the effect is negligible. However, as implied by the comments about the potential of the US market, the “Hecho en México” label can be beneficial to brands well positioned in the home country. Andrea, in fact, spends very little in advertising north of the border, since prospects are already familiar with its name. Flexi addresses the customer base in the USA by focusing on quality, and not so much by looking at the nostalgia market.

Although Flexi and Andrea followed different paths of internationalization, both companies reveal paths to success in a foreign land. Their efforts are showing new alternatives to other shoemakers while offering valuable lessons to organizations looking for opportunities abroad. Managers at the many companies wishing to compete globally may find reassurance about their projects when looking at how both enterprises were capable of surmounting obstacles in their home country, competing with well-positioned brands, and establishing their own facilities in a highly competitive market. In the end, Flexi and Andrea tell us the same story: facing competition away from home is harsh, but going international may create the divide that sets successful organizations apart.