5 Belgium: Flanders

Preamble: Flanders in Belgium

Belgium is a small but complex country, bounded by several states and for a small part by the North Sea. Its surface, only 30,500 km2, covers a variety of landscapes, a coastal plain in the north-west, a plateau in the centre and the forested Ardennes uplands in the southern part of the country. Although small, the country is split into three different communities based on language and culture: the Dutch-speaking community in the north (about 60% of the population), the French-speaking (40%) in the south and a small area of German-speaking people (about 74,000 people) in the east of Belgium. Apart from this division, Belgium consists out of three regions: Flanders, Wallonia and the Brussels Capital Region located geographically between the former two (Belgium, 2011).

This complex geographical and cultural partition clearly has its political consequences. There are many different levels of political authority in Belgium. Next to the federal government, every community and region has its own council (legislative body) and government (executive body). Belgium is a monarchy with a King who is the Head of State, but who does not exercise any personal authority. The ministers of the federal government, communities and regions are fully responsible for signing new laws in their own field. For the telecommunications sector, the National Regulatory Authority, BIPT, is a federal institute, and responsible for all that concerns the telecommunications networks. On the other hand, the legal institutes for media (media regulator) fall under the responsibility of the communities, since these bodies regulate content and are therefore language-driven. Thirdly, there is the competition authority, which is federal but separate, a part of the Ministry of Economic Affairs.

With a total population of 10,951,665 (at 1 January 2011), Belgium is a densely populated state. The population density is considerably higher in the region of Flanders (about 460 people/km2 in 2010) than in Wallonia (about 205 people/km2 in 2010) (Eurostat, 2011).

The Belgian economy is mainly based on services, transport and trade (73% of the working population) (CIA, 2011). The share of industry (25% of the working population) keeps decreasing. The main industrial zones are currently located near the harbour cities of Antwerp, Bruges and Ghent. In Wallonia, the most important industrial sites are located along the two largest rivers: the Sambre and the Meuse. Agriculture is limited in Belgium (only 2% of the working population). Because of its central position in Europe, Belgium (especially its capital Brussels) is a very attractive location for central offices of international companies. This central position also requires Belgium to own a well-developed transportation infrastructure. There is an extensive network of highways, railways and waterways. Belgium has five international airports, among them the two large airports in Zaventem and Charleroi, and a number of international harbours, among which is the harbour of Antwerp, the second largest in Europe.

By the end of the 1980s, badly planned economic policies resulted in a public debt of 120% of the Gross Domestic Product (GDP). In the following period, the Belgian government made sure that every major decision fitted in the overall goal of reducing this major debt. By the end of 2006, the public debt was reduced to 100% and to 90% in 2008. Due to the financial crisis in recent years, this public debt has risen again to 99.7% in 2011 (CIA, 2011). All three major banks in Belgium suffered heavily from this crisis and the government was forced to intervene financially to prevent severe damage.

It is important to note that this paper focuses only on Flanders. As can be derived from this short introduction, the differences between Flanders and Wallonia are significant, both in the development of the telecom sector and in the emergence of different actors. The authors therefore chose to devote the remainder of this chapter to the development of telecommunications in the region of Flanders only. The focus will be on the development of fixed broadband, in particular infrastructure-based competition between the PSTN operator and the CATV-cable operator.

5.1 Introduction: the dual road of telephone and analogue television network development

Telecommunications started a long time ago but developed faster and faster as time went by, from communicating by means of carrier pigeons in the Middle Ages, over telegraph systems at the beginning of the 19th century to telephone networks deployed at the end of the 19th century, while cable networks for broadcast services emerged in the 1950s. This section provides a brief overview of the development of copper and coaxial cable networks, since, in Flanders, they are now both used to offer broadband connectivity.

5.1.1 The development of the copper network

Introduction to communication services in Belgium (1879–1930)

The first telephone line was installed by the Belgian telegraph service at the Parliament in 1879. The first telephone call between two cities (Brussels and Antwerp) took place in 1884 and the first international conversation (with France) in 1886. The first commercial exploitation was set up by a subsidiary of the International Bell Telephone Company (IBTC) (Dienst Pers en Informatie, 1982). This subsidiary, the N.V. Bell Telephone Manufacturing Company, was founded in 1882 with the aim of introducing public telephony in Europe (Vanden Berghen, Reference Vanden Berghen2012). In 1886, the Belgian state granted Bell the installation of the first local telephone network in Ostend.

The networks owned by Bell worked fine in the densely populated cities, but did not succeed in connecting people in the rural areas. Additionally, the private ownership of the various local networks made it difficult to interconnect them. In 1893, the Belgian state bought back the concessions and thereby regained control of the various local networks. In 1896, the Belgian state decided to establish a public company that received total control of the telephone sector. The company started by taking over the remaining private networks; the final goal was to provide telephone service throughout the entire country. By 1913, the major part of Belgium had access to telephones, principally through public booths installed in most railway stations and post offices (Wikipedia, 2011).

Monopolistic situation: RTT (1930–1991)

With the outbreak of the First World War, the Belgian authorities had to deal with great financial trouble and could no longer support the public telephone company. This led to an abrupt suspension of telecommunication services in Belgium. In order to avoid losing facilities due to lack of financial means in the future, a new company was founded under the name of RTT (Regie Telegraaf en Telefonie) in 1930, which inherited a subscriber base of about 225,000 customers. This public company still owned the monopoly over the whole telephone network, but was set up as an autonomous institution, no longer depending on the funding provided by the authorities. Competition was out of the question, as all threats of entry and substitute products were locked out by law, which determined that the RTT not only had the monopoly of owning and exploiting the copper network but also the sole rights to offering services and equipment. Its independence soon appeared to be primarily theoretical, as the economic crisis of the 1930s caused the RTT to become involved in the industrial and employment policy of the state. To reduce the high unemployment rate, the RTT was forced to create jobs through the expansion and total automation of the Belgian telephone network. In the period from 1930 to the beginning of the Second World War, the RTT succeeded in increasing its customer base by almost one third, reaching a subscriber base of more than 300,000 customers.

During World War II, the Belgian telephone network experienced serious damage and parts of its lines were destroyed. The RTT lost more than 70,000 subscribers. To support the fast developing economy, that characterized the period after the Second World War, the state decided to intervene financially to give a boost to the telecommunication sector. The growing number of subscribers (from 350,000 in 1946 to 522,000 in 1951 and 1,049,000 in 1965) stimulated the RTT to invest heavily in its network. As a consequence, the Belgian telephone network became one of the most developed and most progressive at the time1.

But this boom had its negative side. At the end of the 1960s, the saturation of the market put a stop to the increasing revenue trend, and losses started to accumulate. Then, in 1973, the civil engineer Paul Demaegt, an RTT employee, revealed that Germain Baudrain, the administrative director of RTT at the time, no longer put up the construction and decoration of RTT-buildings out to public tender, but awarded it to private enterprises in which the director himself owned shares. This led to an augmentation of the RTT’s losses. Although the telecom network remained well maintained, questions about the RTT’s efficiency arose. Customers (especially business subscribers) started to realize that the prices they were paying were too high for the quality of service they received. This awareness also arose in other countries, was a major cause for regulatory intervention and provided the justification for serious restructuring of the sector during the 1980s and 1990s.

Towards the liberalization of the Belgian market (1991–1998)

The first legislation concerning the use of the telephone was published in 1896, with the monopolization of the network and the foundation of the first public company. The first real Telecommunications Law appeared in 1930, together with the formation of the RTT. This law remained relatively unchanged for about sixty years, as nothing fundamentally changed concerning the monopolistic situation of the RTT.

The major cause of change resulted from the publishing of the Green Paper on the development of the common market for telecommunication services and equipment (European Commission, 1987). This paper aimed at initiating discussions in Europe concerning the development of a common market for telecommunications. Also, the decreasing satisfaction of Belgian customers made the authorities realize that change was needed. On 21 March 1991, the proposals from the Green Paper were incorporated in Belgian law (Belgium, 1991), which led to the foundation of two institutions: Belgacom, an autonomous telecommunications operator with a monopoly in the copper telephone network and the BIPT (Belgian Institute for Postal Services & Telecommunications), a regulatory authority.

Belgian Institute for Postal services and Telecommunications (BIPT)

The BIPT is the Belgian National Regulatory Authority, positioned as an independent institution. The role of the Ministry of Telecommunications is limited to selecting and assigning (by means of a Royal Decree) the executive board members every six years. BIPT funds itself using revenues from the management of licenses and numbering. Its main responsibilities include (BIPT, 2011):

– correct application of the laws concerning telecommunications (radio, television, telephone and Internet services) and postal services;

– oversight of the transition of the necessary European directives into Belgian law (although this obligation is to be shifted to the Directorate-General (DG) Telecom of the Ministry of Economic Affairs);

– management of scarce resources, i.e., the radio frequency spectrum and the numbering space;

– mediation when differences between telecom operators occur;

– granting of licenses to new entrants.

To prevent conflicts of interest between the telecom operators and the BIPT, the latter is forbidden to practise commercial activities.

At the same time, another institution was founded next to the BIPT: the Office of the Ombudsman for Telecommunications (Ombudsdienst Telecommunicatie, 2011). This organization serves as a mediator between customers and telecom operators. It is a completely different institution, independent of the operators, authorities and regulators. Whenever a customer has a complaint concerning an operator, if this customer cannot come to an agreement with the operator, he or she can turn to the Ombudsman for intervention.

Every year, the organization submits a report on the major complaints. This report can be seen as a representation of the Belgian customer’s demands and complaints, which can be used to further improve the existing infrastructures and services.

Belgacom

The Law of 1991 aimed to transform the Belgian market in order to make it more receptive to competition. Belgacom was created as a successor of the RTT and still owned the entire Belgian telephone network. The main difference between the RTT and Belgacom concerned the degree of monopoly. The RTT had the monopoly of exploiting the whole telephone network, while Belgacom only inherited the monopoly on ʻpublic telecommunicationsʼ. The Law of 1991 defined public telecommunications as (Belgium, 1991):

– construction, maintenance, modernization and operation of public telecommunications infrastructure;

– exploitation of the reserved services (including telephone and telegraph service, provisioning of fixed links) for third parties;

– construction, maintenance and operation of the publicly accessible establishments located on the public domain and intended for telecommunications.

In 1994, the Bangemann Report from the European Commission provided the official recognition for the complete liberalization of the European telecommunications market. As a response to this report, the government decided to privatize Belgacom in that same year by selling 50% -1 of its shares to the ADSB Consortium, consisting of Ameritech, Tele Danmark and Singapore Telecom, plus three Belgian financial institutions: Sofina, Dexia and KBC. The other 50% + 1 share stayed in the possession of the Belgian authorities, the state thus remaining the major shareholder. The state believed this privatization to be necessary to counter competition from international rivals, because of the attractive position of Belgacom as the only telecom operator in a country in the centre of Europe, but also to be able to face the competition to emerge from the domestic CATV operators, as the European directives authorized the ‘commercial exploitation of non-reserved services on alternative infrastructures’. Next to reducing the threat of entry, the Belgian state used the proceeds from this privatization to reduce the huge public debt the country had to deal with at that time.

1994 was also the year of the foundation of the first Belgian mobile network: Proximus. This network and the old analogue Mob2 system were transferred later that year to a separate subsidiary, Belgacom Mobile. Belgacom owned 75% of shares; the other 25% was in the hands of US-based Air Touch which was acquired by Vodafone in 1999. Today, Belgacom again owns 100% of the shares. As mentioned in the introduction to this chapter, we will not explore the development of the mobile market in further detail. Only the facts that are important in relation to the actors in the fixed broadband market and the services offered will be addressed.

Belgacom entered the Internet market in 1996 with the acquisition of 25% of the shares of Skynet, a company providing Internet services that was founded in 1995. Before 1995, it was principally the academic world that made use of the Internet through the research network, BELNET, that could be used free of charge by the Belgian universities thanks to funding from the federal government. Belgacom acquired the remaining 75% of Skynet shares two years later. The subsidiary Belgacom Skynet was officially born, and customers could gain access to narrowband Internet using dial-up.

5.1.2 The development of the cable network

Introduction to cable services in Belgium

The distribution of television channels by cable networks originated in the United States of America in 1947. Belgium was the first country on the European mainland that established cable distribution networks in the early 1950s. The first cable lines were installed in large apartment buildings where the residents invested jointly in one antenna and distributed the signals using cable. Soon, some of those networks were combined into inter-municipal networks, sometimes with the participation of a private firm. The initiator was NV Coditel, which set up a cable network in Saint-Servais (close to Namur, in the Walloon region) in 1960. Liège, Verviers and Visé were connected to the network in the following years. The regions of Brussels and Flanders followed the lead of Coditel with the foundation of similar companies in their regions. The number of subscribers grew rapidly: more than 50% of Belgian viewers had subscribed by 1976 and about 88% in 1985 (De Bens, Reference De Bens1986). There are several reasons for this boost. First of all, cabling was promising in both densely populated and rural areas. Urban areas with lots of inhabitants gave the cable companies the advantages of economies of scale, while the poor antenna-reception in the rural areas formed a good incentive for the roll-out of a more reliable cable network. Another important motive included the linguistic duality in Belgium. The Dutch-speaking part was interested in receiving foreign TV-channels from the Netherlands and, analogously, the French-speaking part wanted to watch French TV-shows and movies. Last but not least, cable networks also served an aesthetic purpose: once homes were connected to the cable network, the jungle of antennas could be removed.

Because of the large difference in content between the Flemish and Walloon television services, the authorities decided to put the regulations and legislations for cable networks – and television in general – under the responsibility of the communities (media regulators). It is important to note that although the cable operators were autonomous companies, a formal approval from the RTT was necessary for the establishment and exploitation of any cable network, irrespective of size. By 1996, thirty-eight cable companies with a total subscription base of 95% of households made Belgium the world’s leading country for cable coverage. Despite the large number of cable companies, competition wasn’t present at the time, as every cable company operated only in its own geographical region.

The demand for more programs and channels caused serious expansion campaigns during the 1980s and 1990s, each time increasing the available bandwidth per user and thereby enhancing the quantity and quality of the services offered. Starting in the 1990s, local companies merged in order to be able to keep up with the required investments and to improve the services. Only a couple of big companies remained, mainly based on geographical coverage. After a series of important mergers, driven by both public and private actors, only one cable company remained in Flanders: Telenet. The interactions leading to the current shape and status of the cable company were important for the market structure and development of broadband in Flanders; hence, they are the case’s focus in the next section.

5.1.3 Case focus: the Flemish initiatives leading to the founding and survival of Telenet

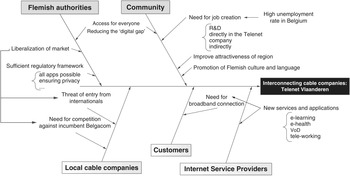

In Flanders, the project ʻMultimedia in Vlaanderenʼ (Van Batselaer et al., Reference Van Batselaer, Lobet-Maris and Pierson1997) was aimed at developing an information society in Flanders2. This project was presented by the Flemish government in April 1996 and based on domestic studies as well as conclusions from European and international studies. The objectives of this project were multi-fold (Van den Brande, Reference Van den Brande1996), see also Figure 5.1:

– conversion of the Flemish cable infrastructure into an interactive broadband network offering broadcast, telecommunication and multimedia services;

– creation of a stable regulatory institution and legislation based on competition;

– promotion of research and development in the sector of information technology;

– assignment of an exemplary role to the Flemish government in the set-up of pilot projects;

– creation of additional jobs.

The objective of this project was to create new applications and to lay the foundation of an information society in Flanders, as well as to create a united cable company as a competitor to Belgacom in Flanders. The policy plan of 1996 gave some examples of future applications, some of which are now commonly used: e-learning, e-working, e-shopping, e-administration, video-on-demand, e-health and many more.

The major consequence of the project was the foundation of Telenet Vlaanderen, set up to interconnect and potentially unite the independent Flemish cable companies to achieve an interactive broadband network offering broadcast and telecommunications, as well as multimedia services to all citizens. This foundation provided a good fit within the project ʻTelenet in Vlaanderenʼ, the major sub-project of ʻMultimedia in Vlaanderenʼ.

The reasons for this project were twofold. On the one hand, the infrastructure was insufficiently used, although Flanders possessed one of the densest cable networks in the world. The legal restrictions imposed upon the cable networks (every action in the cable sector must be approved by the RTT) limited the application possibilities. At the time, there were many small cable companies, each covering their own region with their own infrastructure but lacking interconnection between the different regions and infrastructures. On the other hand, with the liberalization of the telecom market of January 1998 (authorized by the European Commission) on the horizon, a need arose for competition with the incumbent Belgacom and other possible international entrants.

A thorough feasibility study performed by the GIMV (Gewestelijke InvesteringsMaatschappij voor Vlaanderen, a European venture capitalist with public funds and experience in private equity (GIMV, 1998)), estimated the investment costs at BEF50 billion (about EUR 1.25 billion). A starting capital of BEF17 billion (about EUR 420,000) was provided by a consortium of four large partners in the Telenet Holding: MediaOne (25%), the Flemish inter-municipal corporations (35%), GIMV (20%) and a financial consortium with representatives of the Flemish media and several financial groups (20%). A major part of this total investment was invested in rolling out an extensive fibre backbone of about 635 km in order to connect the individual networks of the various cable companies, which was completed in July 1997. Through the use of switching centres and by making the amplifiers in the coaxial network bi-directional, two-way traffic became possible, thereby enabling many additional applications, as such creating a playing field for innovation.

As a consequence of the ʻMultimedia in Vlaanderenʼ project, a set of new enterprises arose from the merger of the former local cable companies. Apart from the foundation of Telenet itself, 1996 was characterized by the creation of UPC Belgium (United Pan-Europe Communications Belgium), founded as a joint venture of Philips and UIH (United International Holding), with US-based Liberty Global and UPC Broadband as major stakeholders. Its network took over the existing networks in seven communes of Brussels (Etterbeek, Ganshoren, Jette, Koekelberg, Schaerbeek, Berchem-Holy-Agathe and Forest) and three communes of Flanders (Heverlee, Kessel-Lo and Leeuwen). Another cable company, Interkabel Vlaanderen, resulted from the merger of three local ʻintercommunalesʼ: Interelectra (province of Limburg and the Antwerp city of Laakdal), PBE (region of Hageland in the province of Vlaams-Brabant), WVEM (regions of Diskmuide en Wevelgem in the province of West-Vlaanderen, region Halle-Vilvoorde in the province of Vlaams-Brabant and the cities of Beerse and Vosselaar in the province of Antwerp) and Integan (region of Antwerp and city of Essen). Interkabel Vlaanderen offered broadband services, cable television and INDI, a digital television platform.

Although the business plan for Telenet was ambitious, the first Internet access offer, branded Pandora (launched in August 1997), was too expensive (about EUR 50 per month), leading to a delay of the expected boom in uptake and very high debts. Furthermore, Telenet (Pandora) only received revenues from offering additional services; the network revenues stayed with the network owners (privately owned and geographically divided ‘intercommunales’). In 2002, the newly appointed CEO, Duco Sickinghe, changed the strategy of the company. By buying into the intercommunales (UPC Belgium in 20063, Interkabel Vlaanderen in 20084) in return for a share in the larger Telenet, he could refinance the entire operation, using the ensured revenues from the network (cable TV revenues previously destined for the intercommunales) as collateral. Through the takeover of about 850,000 customers of UPC and Interkabel, Telenet acquired the fourth and final important part of the Flemish cable network. This strategic move prevented Belgacom from entering the cable infrastructure business, and therefore made Telenet a full competitor on the infrastructure level using its HFC (Hybrid Fibre Coaxial) architecture.

Apart from the strategy change, the Belgian NRA, BIPT, had an important influence on the business case for Telenet: that is, an interconnection agreement signed with Belgacom on the application of asymmetric regulation on termination fees to the advantage of Telenet meant a large extra income for Telenet, and saved the company to some extent (as without this measure, Telenet might have gone bankrupt). Some even considered this asymmetric regulation as an indirect subsidy from Belgacom to Telenet, justified in the context of creating a level playing field in telecoms in Flanders. Although this justification may be subject to discussion, it led to the current duopoly situation where Belgacom and Telenet compete for broadband customers.

5.2 Case description: From narrowband to broadband in Flanders – a duopoly market

Although the European telecom reform aimed at introducing more competition by allowing new entrants to compete on the copper network of the incumbent, it largely resulted in a competitive duopoly between the incumbent operator Belgacom and the cable operator Telenet. This section will describe the evolution and the most important events in the development of broadband (Internet), while focusing on the tit-for-tat competition between copper and cable. A summary of the most important events for both operators is given in Figure 5.2 and Figure 5.4, respectively. Although this paper focuses on the development of fixed broadband markets, we also include a timeline for mobile communications because all operators offer quadruple play services (including television, Internet and fixed and mobile telephony).

Figure 5.2 Timeline presenting the most important events in the history of Belgacom

5.2.1 Belgacom in a competitive setting

Starting 1 January 1998, the Belgian telecom market was completely liberalized, whereby Belgacom was obliged to open up its network to new entrants. Local Loop Unbundling (LLU) was legislated in October 2000, allowing access to the network of the incumbent from 1 January 2001 onwards. Belgacom first issued a Reference Unbundling Offer (RUO) in December 2000, which was reviewed and rejected by the BIPT several times. The publication of the documents was found inadequate and the standard contracts contained a number of clauses that formed a serious obstruction to new entrants (as stated in the review of Belgacom’s Reference LLU Offer, 12-03-2001 (BIPT, 12/03/2001; 14/03/2001). The final BRUO-proposal (Belgacom’s RUO) was approved by the BIPT in March 2001 and included rental possibilities on three levels: full LLU, line sharing and sub-loop unbundling. Bitstream access was granted a few months later through a separate reference offer. The Belgian market became not only officially but also practically open to OLOs (Other Licensed Operators).

Because of this newly introduced competition, Belgacom had to improve its applications and services in order to maintain its strong position on the telecom market. Figure 5.2 provides an overview of the most important events that characterized Belgacom’s history. In the following paragraphs we will discuss these events.

Broadband Internet: network upgrades

In order to stay competitive, a prime requirement is to have a competitive network. After emergence of the public Internet and dial-up use in 1995, the real story of commercial broadband Internet using the PSTN network of Belgacom begins in 1998, with the execution of a pilot project for the testing of ADSL (asymmetric digital subscriber line), ʻthe high-data rate access roads to the information highwayʼ. The project included 1,000 customers in several large Belgian cities (Antwerp, Brussels, Leuven, Liège, Mechelen, Ghent and Charleroi). Belgacom predicted that, by using this new technology, transferring information at data rates up to 8 Mbit/s (download) and 600 kbit/s (upload) per user would become everyday reality in the near future.

Because of the success of the pilot project (80% of the test public approved of the possibilities of the service and agreed to recommend it), Belgacom Skynet was one of the first operators (world-wide) to introduce ADSL commercially in April 1999. Soon, ADSL covered 30 to 35% of Belgacom’s telephone customers. The intention was to achieve coverage of 70% by the end of 2000. This objective was exceeded when in November 2000, ADSL services were available to 75% of Belgian population. By the end of 2002, the coverage was almost complete when 98% of the inhabitants had access to ADSL services (Belgacom, 15/01/2003), making Belgium the leader in Europe. In 2010, DSL coverage had reached 99.85% of the Belgian population. In terms of uptake, Belgacom had 517,000 subscribers by the end of 2002, an increase of 290,000 since the end of 2001. This number doubled again in the next two years, reaching the milestone of 1 million in 2004 (Belgacom, 25/02/2004). By June 2011, Belgacom had 1,835,000 subscribers.

Not only did technical measures give rise to network upgrades and expansion of uptake; at the end of 2008, the acquisition of Scarlet, a Dutch telecom company specialized in low-cost Internet offers, increased the market share of Belgacom by 5%. Both the BIPT and the OLOs reacted quite negatively to this acquisition; however, IBPT approved the acquisition on the condition that Scarlet’s backbone was sold. Not only did this take-over increase Belgacom’s market share but it also allowed Belgacom to offer a low-cost brand (although Scarlet is fully owned by Belgacom, the name is retained) (De Tijd, 09/09/Reference Tijd2008).

In 2002, Belgacom launched SDSL (Symmetric DSL), which provides a fast Internet connection with the same maximum available data rates in both directions (up and down). SDSL was primarily developed for business customers. The need for higher data rates made Belgacom explore the opportunities of fibre deployment within the scope of the Broadway project that was launched in 2004. This project aimed at upgrading the network to a combined copper and fibre network. The goal was to connect the central offices to the street cabinets using optical fibre (the so-called Fibre-to-the-Cabinet, FttC) and to roll out a VDSL platform between the street cabinets and the end users. The VDSL technology was introduced commercially on 2 November 2004 and by investing EUR 103 million in 2006, VDSL coverage of 45% was reached by the end of that year. This VDSL technology offered data rates up to 8 Mbit/s download and 400 kbit/s upload by the beginning of 2005. Because the equipment vendor Alcatel Lucent no longer supported the particular VDSL technology (incompatible with ADSL and too much spectral noise) and because the need for higher data rates was urgent due to the introduction of digital television, Belgacom implemented ADSL2+ in 2005 as a temporary solution until the new VDSL2 standard would be ready at the end of 2007. By 2009, a total investment of about EUR 500 million had led to the deployment of 14,000 km of fibre, connecting 17,000 ROPs (Remote Optical Platforms) representing a FttC coverage of about 70%. Thanks to the early investments in the Broadway project and the high ranking of the VDSL2-coverage (second place in Europe in 2009), Belgacom received the 2009 Innovations Award from Global Telecommunications Business (Belgacom, 29/10/2004; 09/09/2009).

Because of the increasing demand for higher bandwidths and in order to stay competitive vis-à-vis the cable operator Telenet, Belgacom decided to invest further in applications using optical fibre. The first tests concerning Fibre-to-the-Home (FttH), bringing the optical fibre into the living room of the customer, were executed in Rochefort in 2008 and extended to Sint-Truiden and La Louvière in 2009 (Belgacom, 09/09/2009) but no commercial deployment was envisaged yet.

On the one hand, Belgacom was deploying VDSL2 to all its customers, having reached a national coverage of 78.9% at the end of 2011, aiming for 85% by the end of 2013. On the other hand, Belgacom recognized the limitations of VDSL2, and therefore already communicated their ʻGet to fast, fasterʼ strategy (Belgacom, 27/09/2011). In a partnership with Alcatel-Lucent, Belgacom aims at maximizing the VDSL2 throughput by using the new state-of-the-art vectoring technology. VDSL2 vectoring is a noise-cancelling technology that will allow the use of VDSL2 at its theoretical data rates, which will allow rates of 100 Mbit/s and beyond to be transmitted on copper cables. Belgacom opted for this upgrade because it will bring high data rate broadband to the end-consumer in a fast and cost effective way. Tests of VDSL2 vectoring started at the end of 2012.

Apart from vectoring, other technological upgrades on VDSL are possible to boost bandwidth capabilities. In VDSL bonding, two physical twisted pairs to each customer are used instead of one, which almost doubles the data rate. However, as there are few spare copper pairs in Belgium, it is unlikely that this upgrade can be implemented for every customer. Phantoming adds a third – virtual – twisted pair, which would bring data rates up to 200 Mbit/s to each individual household5. Combining all options (bonding, phantoming and vectoring) would allow the DSL network to offer data rates of about 300 Mbit/s (Alcatel-Lucent, 2010, 2011).

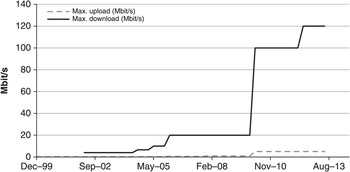

The graph in Figure 5.3 provides an overview of the most important changes concerning the available data rates for residential users.

Broadband Internet: applications and services

Next to the gradual upgrading of its network and the extensions towards mobile services and digital television offerings, Belgacom also extended its services over the years into different fields. In 1998, for example, Belgacom launched its own website www.belgacom.be. The main purpose of this site was to clearly communicate (new) applications and services and their prices to (potential) customers. The faster ADSL connections provided a passage to the development of new applications. In 2003, Skynet’s Internet access activities were transferred to Belgacom to optimize service provisioning. Since then, Skynet is appointed to develop the new activities of the Belgacom Group, such as the further expansion of the portal site Skynet.be, broadband video, 50 years of television, vrtnieuws.net and Big Brother, legal downloading of music with the Skynet Music Club, the publishing of personal blogs, etc.

Within the concept of providing ʻICT for everyoneʼ, Belgacom participated in a number of governmental projects. In 2003, for instance, Belgacom was one of the partners in the Private PC initiative. The objective of this project was to boost PC penetration through new legislation that provided tax benefits for companies that equip their employees with a home computer and Internet connection, (Belgacom, 16/05/2003). At the beginning of 2004, Belgacom launched ʻTeleworking Plug and Workʼ. The application is a hardware solution that can be plugged into the ADSL Ethernet modem, making it possible for the teleworker to access corporate data over the Internet in a secure manner (Belgacom, 09/01/2004).

Another important acquisition involved Telindus, a company founded in 1969 which offered ICT services and solutions to the corporate and public sector. Its headquarters were located in Heverlee (close to Leuven). By taking over several foreign companies, it had grown into an international company with establishments in Thailand and China. Telindus was taken over by Belgacom at the beginning of 2006, after a hostile bidding war with France Télécom, among others. Telindus became a subsidiary of Belgacom and kept operating under its own name. After reviewing Telindus’s position in each country where it operated, Belgacom decided to retain only the operations in six countries: Belgium, the Netherlands, France, Luxembourg, Great Britain and Spain (Broens, 30/09/Reference Broens2008).

In 2011, Belgacom signed an agreement with the Spanish company FON, which represents the world’s largest Wi‑Fi community: over 4 million customers share their wireless access points with other users, and this on a worldwide scale (Belgacom, 14/11/2011). The principle of this sharing lies in setting up two access points using the client’s Wi-Fi modem: one (main) access point for private use, one (lower-capacity) access point for other customers of the FON community. The service is free for all customers of Belgacom; they only have to subscribe online to give ‘visitors’ access to their own modems, and to receive the username and password with which to use the connectivity provided by other FON users. In this way, Belgacom’s customers have free access to all FON enabled Wi-Fi connection points, both inside Belgium and abroad.

In 2011, by concluding a contract with Deezer, a music streaming company, Belgacom was the first operator in Belgium able to offer free and unlimited access to over 13 million songs. The service is offered for free to anyone owning a Generation Pack subscription, or for EUR 4.99 per month for other Belgacom customers (Belgacom, 08/12/2011).

Finally, Belgacom introduced ʻInternet Everywhereʼ in 2012, allowing its customers to opt for a single subscription to be connected everywhere, through the fixed network or using Wi‑Fi at home, through the Wi-Fi FON spots or the 3G Proximus network (Belgacom, 28/03/2012).

Mobile communications and digital television

Along with exploiting the network for the use of fixed telephony and Internet, Belgacom started conducting trials for the offering of digital television in November 2004. Belgacom TV was introduced commercially in June of 2005. Using both the earlier VDSL and the ADSL2+ technology deployed thereafter, Belgacom TV was accessible to 79.5% of Belgian households at the end of that year. In June 2009, Belgacom TV had 589,000 subscribers, around 12% of households.

In May 2005, Belgacom acquired the rights to broadcast the Belgian Jupiler Football League (Belgacom, 09/05/2005) thereby setting a hard deadline for the launch of their new digital television services. Only some important matches would be broadcast using the public broadcast channels (VRT and RTBF); all additional material would be distributed exclusively on Belgacom’s digital television platform. The monopoly rights gave Belgacom an important strategic advantage over Telenet. Because those rights are not exclusive anymore, Belgacom launched ʻBelgacom 11+ʼ, a new channel exclusive to Belgacom subscribers, broadcasting UEFA, Spanish and Portuguese soccer league matches (Belgacom, 02/07/2012).

Belgacom entered the mobile market in 1994 under the Proximus brand (see also Section 5.1.1). Although Belgacom had offered 3G services under the same Proximus brand for some time, the acquisition of a license for operation in the 1.8 GHz and the 2.6 GHz bands (acquired for EUR 20.22 million in November 2011) allowed Belgacom to be the first Belgian operator to offer 4G services. 4G was introduced commercially in 8 Belgian cities in November 2012, and extended to 17 cities by March 2013. Nowadays, Belgacom is a quadruple-play operator offering broadband Internet fixed telephony, mobile telephony, digital television and Internet access through 3G and 4G.

This multi-medium platform comprising fixed broadband, worldwide Wi-Fi access through FON and the mobile network of Proximus is used by Belgacom not only in its packaged offers (see ʻInternet everywhereʼ as described above) but also in its services. In July 2011, Belgacom launched its field test of ʻTV everywhereʼ, allowing its clients to watch TV on all their devices using the nearest available Internet source (fixed, Wi-Fi, 3G/4G) (Belgacom, 20/08/2013). After a trial period of about one year, Belgacom officially launched the service in September 2008. It is now offered for free to customers subscribed to a ʻmaxi packʼ, and for EUR 4.95 per month to other customers.

5.2.2 Telenet: an infrastructure-based competitor with similar offers

Starting in 1998, a duopoly of Belgacom and Telenet now dominates the telecommunications market in Flanders. Both companies upgraded their networks and services gradually, in order to counter the competitive pressure. This paragraph focuses on the evolution of Telenet, the Flemish cable operator. Comparison to the corresponding services offered by Belgacom is made where possible. An overview of the applications and services offered by Telenet, as well as a summary of the most important upgrades is shown in Figure 5.4.

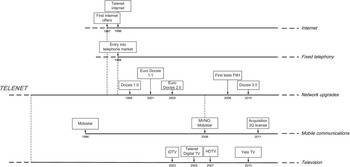

Figure 5.4 Timeline showing the most important events in the history of Telenet

Broadband Internet: network upgrades

Figure 5.5 shows the evolution of the data rates offered by Telenet. To provide its services, Telenet uses a HFC network, which consists of fibre backbones and coaxial access in the areas served. To provide broadband access, Telenet uses the DOCSIS (Data over Cable Service Interface Specification) technology. The first version of this technology (DOCSIS 1.0) was developed in 1997 by CableLabs for the US market. To match the European cable frequency spectrum, the standard was adapted and the Euro-DOCSIS technology was born. The first upgrade (DOCSIS 1.1) was launched in 2001. Now, Telenet uses the European version of DOCSIS 3.0, which allows them to offer a download data rate of 100 Mbit/s and more (Boonefaes, Reference Boonefaes2005–2006; CableLabs, 2011).

Over the years, Telenet launched various new products, each time increasing the data rates. The first telecom product was launched in 1998 under its ‘Home’, ‘Do’ and ‘Young’ packages. Telenet Internet XL came to the market in September 2000, providing a downstream rate of 1 Mbit/s and an upstream rate of 256 kbit/s, thereby doubling their previous offer. In 2002, Telenet Internet XL offered download data rates up to 4 Mbit/s, while Euro-DOCSIS 2.0, introduced in 2003 as part of Telenet ExpressNet, enabled an upgrade to 10 Mbit/s. Download data rates increased to 20 Mbit/s in the fall of 2005. In 2010 followed the introduction of DOCSIS 3.0 with a download rate of 100 Mbit/s and an upload of 4 Mbit/s.

In March 2010, Telenet launched ‘Digital Wave 2015’, a project aimed at improving the existing network over the next five years, with an investment of about EUR 30 million every year. Through the roll-out of an extensive fibre network, Telenet wants to promote the transformation of Flanders into a digital and networked economy. Along with the transformation of the network itself, Telenet aims to develop a number of new applications, such as remote medical services, call centre video assistance over the Internet, 3D television, video on demand, mobile television, new file-sharing and synchronization and e-government (Telenet, 3/03/2010). Telenet keeps upgrading its network by gradually reducing the size of the service areas (SAs). An SA is the part of the network that connects the end-customers to the first local collection point through the use of coaxial cables. From the collection point onward only fibre cables are used.

Since the available data rates offered by Telenet nowadays are much higher than those of Belgacom, the motivation to upgrade towards FttH is weaker. Telenet, however, did intend to keep up the current level of investment in their network, within the scope of the Digital Wave 2015 project. They are currently expanding their DOCSIS 3.0 technology (using channel bonding to increase data rates to over 100 Mbit/s) to all customers, and keep on increasing the available bandwidth by reducing the size of their service areas. These projects allowed Telenet to increase the data rates again in June 2012, to a maximum download rate of 120 Mbit/s and upload of 5 Mbit/s for residential customers (Telenet, 7/06/2012). Plans for deploying FttH have not been announced so far.

Broadband Internet: Applications and public service

In March 2003, Telenet launched XboxLive, an online-gaming service from Microsoft, for its high-speed cable Internet customers. Telenet also took over the activities of Hypertrust in February 2006. Hypertrust, founded in May 2000, was the first European organization that offered secure communication and storage services on the Internet under the slogan ʻYour content in actionʼ (Finance.nl, 22/07/2003). Telenet also entered the advertising business in July 2008, with the founding of a new Media Sales House, in cooperation with ‘Concentra en Var’ – the advertising department of the VRT (the Flemish public broadcast channel). The objective of this new independent entity was the acquisition of advertising and the development of a centralized advertising platform with extended segmentation possibilities (Telenet, 2/07/2008).

Telenet also offers mobile Internet to its customers through Wi-Fi hotspots. The first 120 hotspots were set up in 2003. In May 2006, Telenet reached an agreement with Signpost to launch ʻStudent Hotspotʼ (Telenet, 31/05/2006). The objective of this product is to provide all students and academics with access to all Telenet hotspots (in public locations like airports, restaurants, railway stations etc.) in Belgium and Luxembourg for rather low tariffs (EUR 7.95 per month). Telenet further adopted the principle of Wi-Fi–sharing under their Wi-Free brand (Telenet, 14/12/2011). They have several services using this principle. Their hotspot network allows Telenet subscribers to freely access these hotspots, which are Wi-Fi access points in public locations. In Belgium and Luxembourg, 1200 of those locations already exist. In 2011, Telenet extended the offer to ʻHome spotsʼ, in which customers share part of their own bandwidth with other customers (the principle is basically the same as used by Belgacom). When finished (if all customers’ modems are updated), this gives Telenet subscribers access to over 0.5 million extra Wi-Fi access points by the end of summer 2012 (Telenet, 27/02/2012). A recent article confirms the realization of this target: in January 2013, Telenet customers had access to about 700,000 Wi-Fi homespots and about 1200 hotspots (Vief, 29/01/2013).

Mobile communications and digital television

A first test project for interactive digital television (iDTV) was started by Telenet in 2003, in cooperation with Interkabel (which in the meantime has been acquired by Telenet) and some Flemish broadcasters. In 2005, hardly three months after Belgacom’s TV launch, Telenet introduced Telenet Digital TV, including extra services such as an electronic programme guide, request for missed shows and Prime, a set of movie channels. Prime is the former Canal+ Vlaanderen which Telenet took over in 2003. In December 2007, Telenet was the first to introduce digital TV in high definition (HD). To lower entry barriers, customers of Telenet can obtain the HD digicorder on a rental basis.

Following the launch of the Yelo app in 2010 (making it possible to watch TV on your smartphone or tablet), Telenet launched ʻYelo TVʼ in the fall of 2012 and commercialized it beginning 2013. Yelo TV allows Telenet’s customers to watch their favourite content (live or recorded) on any screen in the house (TV screen, tablet, smartphone, laptop, etc.).

Telenet didn’t limit its services to the fixed market for long. On 13 February 2006, Telenet signed a partnership agreement with Mobistar, one of the most important Belgian providers of mobile telephony. Telenet thus became an MVNO (Mobile Virtual Network Operator) and created the possibility of quadruple play (broadband Internet fixed telephone line, digital television and mobile phone). The first bundled offers (one bill for all requested services) were sold in August of that same year. With the contracting of Alcatel-Lucent for the deployment of mobile network elements on 16 July 2009, Telenet became the first European cable operator that is also a full MVNO6. On 27 June 2011, Telenet, together with Tecteo (the Walloon cable operator), acquired a license to operate in the 3G-spectrum band (Telenet, 27/06/2011). This acquisition of the radio spectrum license improved Telenet’s position on the mobile market, as well as on the telecommunications market in general, as this ‘mobile extension’ gave Telenet the opportunity to offer more competitive services and prices. Although Telenet ran tests for 4G (Telenet, 17/06/2010), they did not participate in the 4G auction. Instead Telenet concluded a contract renewal with Mobistar as full MVNO; the agreement between Telenet and Mobistar was prolonged until 2017, which also implies that the 3G license was never used. In May 2012 BIPT argued that the 3G-license should be used within a term of seven months to avoid losing the license (Blyaert, 15/05/Reference Blyaert2012). In June 2013 BIPT imposed an administrative penalty of EUR 5000 on Telenet (and the Walloon cable operator Tecteo) for not using the 3G-license. They were given a 6-month period to comply (BIPT, 2013b).

5.3 Case analysis: Does the duopoly setting with tit-for-tat competition suffice to realize the Digital Agenda targets?

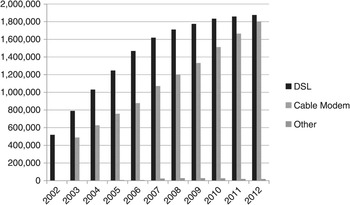

For a very long period, telephone service provision in Belgium has been characterized by a monopoly regime and it was the imminent threat of competition, supported by the pressure from Europe, that prompted the Flemish government to start a project through which the telecom market structure in Flanders would radically change. Telenet was founded and became the key competitor for the incumbent Belgacom in the Flemish fixed broadband market (Figure 5.6) and, as such, stimulated competition, innovation and price reduction. By describing concrete examples and events, this section will analyse the dynamics of the Flemish broadband market and provide insights into the road to reach Europe’s Digital Agenda targets.

Figure 5.6 Broadband subscriptions, Belgium, 2002–2012

5.3.1 Marketing strategies: focus on own strengths

From the previous section it is clear that, although there are some smaller niche players present, the fixed broadband market in Flanders is dominated by Belgacom and Telenet, each having a close-to-100% coverage with their networks (DSL and DOCSIS, respectively). However, since the available data rates on those networks differ significantly (maximum download data rates for residential users are 30 Mbit/s for Belgacom versus 120 Mbit/s for Telenet), both players market their offers using different key services and promotions.

Since mid-2012 Telenet focuses its marketing strategy on data rates and simplicity, for both the fixed and mobile markets. In July 2012, Telenet launched King and Kong, two straightforward tariff schemes for its mobile customers. Both are bundles including voice, SMS and mobile data for a fixed amount per month. To attract or convince fixed Telenet customers, discounts are given. In June 2013 Telenet launched a similar offer for its fixed services: Whop and Whoppa bundles including digital television, VoIP telephony and fixed and Wi-Fi Internet through their Wi-Free hotspots. Their advertising emphasizes the high data rates reached (Whoppa: ʻfor whom fast isn’t fast enoughʼ) and the inclusion of all services into one simple and transparent bundle.

Belgacom, as a quadruple-play operator, goes one step further in bundling its services. Because Proximus is a subsidiary of Belgacom, they are able to offer both mobile and fixed Internet in one package: the ʻGeneration packʼ. Various options exist, for different download limits, voice and SMS usages, etc. Telenet could follow the same strategy by making use of its full MVNO contract but has not taken this path so far.

Another field of competition is the broadcasting of football matches. Although Belgacom long had the monopoly on the Jupiler Pro League Football (the main football competition in Belgium), this right is not exclusive anymore. Both Telenet and Belgacom now try to attract customers with their football channels, Telenet even promising 2,222 live goals on its Sporting Telenet channel for the upcoming season, or a refund of all subscription fees.

5.3.2 Regulatory setting: unbundling obligation and the new telecom law

Unbundling obligation

1998 was the year of the liberalization of the European telecom market. The incumbent Belgacom was obliged to open up its network to new entrants. Belgacom remained owner of the network but had to provide network access to other operators. The consequence of this liberalization was the rise of many new OLOs (Other Licensed Operators) in the following years (e.g., British Telecom, MCI, Colt, Versatel, Coditel, Tele2, Dommel, EDPnet, Mobistar, Eleven, Scarlet). This fragmentation of the market in the field of the copper network stood in great contrast to the intense concentration of the market in the cable network. This is an important observation: while Belgacom was obliged to open up its network, the cable companies were asked to form a united cable network.

However, the fragmentation of the market remained limited, as the new entrants had to combine the significant investments attached to the start-up of a new company with the need to offer low prices to attract customers. New entrants had to offer cheaper and/or better products than the incumbent, because they had to overcome customer loyalty for the existing brands. More firms in the market made the competitors play each other off by using aggressive pricing to attract more customers. This on-going price pressure made it hard for the new entrants to survive, forcing some to end their activities (e.g., Eleven) or to sell their activities to another operator (e.g., Versatel, Tele2, Scarlet).

Other operators managed to develop a customer base of significant size. An excellent example here is the operator Schedom, which provides a cheap Internet connection for urban subscribers under the brand name Dommel. Its success is implicit in the selection of the market segment. By focusing only on urban, densely populated areas (including many students and gamers), Schedom can keep its line prices low (Dommel, 2011). Other operators, like Scarlet, were taken over by Belgacom, although Scarlet remains an autonomous subsidiary (Scarlet, 2011).

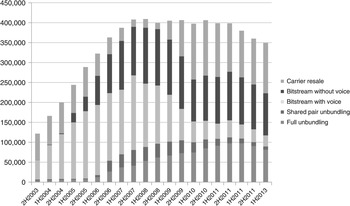

The impact of the unbundling obligation remained marginal until the BIPT lowered LLU prices in 2006.7 The scale of the alternative operators was by then large enough to climb further on the ladder of investment and to invest in unbundling. These investments were stopped in 2008 when the economic crisis hit and when Belgacom announced that it intended to close down 10% of its MDFs (Main Distribution Frames) as a consequence of the move to an all-IP infrastructure and VDSL deployments in the sub-loop. Because the planned closure impacted 40% of the unbundled lines, the BIPT intervened with additional obligations8 to guarantee a fair return on investments for the alternative operators, but the investments in unbundling never recovered. See also Figure 5.7. Carrier resale has gained in volume due to take-overs (Scarlet by Belgacom, LLU network Base by Mobistar) and to the move from ADSL2+ to VDSL2 (no subloop unbundling).

Figure 5.7 The use of wholesale access, Belgium, 2H 2003 – 1H 2013

Although Telenet long enjoyed a monopoly on the cable network and services, the CRC (Conference of Media Regulators) and the Belgian NRA (BIPT) published a proposal for opening up the cable network in 2010. This proposal was transformed into a formal decision on 1 July 2011, in which the authorities regulated Telenet and the other cable operators and created an obligation to provide wholesale access to analogue television and broadband Internet services, as well as opening up the digital television platform. Telenet responded stating that regulating analogue TV is not useful because of the declining number of subscribers and that regulating digital TV is not necessary, as in that market there is enough competition from different platforms (cable, IPTV, satellite, DTT and Internet TV). They furthermore argued that regulating the most important competitor to the SMP incumbent would definitely not enhance the infrastructure-based competition the European Commission favours (Telenet, 18/07/2011, 21/06/2011, 21/12/2010, 26/05/2011). Notwithstanding the arguments Telenet put forward, they were all rejected by the regulators. The regulators and operators are now defining the implementation of the decisions; a final decision from the Court is expected for end 2013 (Belgacom, 2013a). The CRC has already approved the qualitative elements of the decision, calling for Telenet to provide the access within a six-month period after the official request (either through impress payment or signed letter of intent) of the alternative operator (CRC, 2013). However, a final outcome of the court case is not expected before mid-2014 (Telenet, 2013).

Concerning the current LLU and bitstream access regulation of Belgacom’s network, the BIPT is also re-evaluating its models for calculating the price caps, following the European guideline to stabilize the prices for copper lines between EUR 8 and EUR 10 per month, as such increasing the flexibility for the deployment of fibre-based networks. As mentioned above, these caps were set in 2010, and remained unchanged until 2012.

The new telecom law (2012)

In July 2012, a new telecom law was voted in Parliament, focusing on transparency, competition promotion and (universal) service obligation. The law requires customer protection by obliging the operator to be transparent in their communication with their clients and by allowing customers to change operators for free. Every contract can be modified or terminated by the client after a period of six months, without needing to specify a (legal) reason. Finally, the law includes a quality of service obligation, whereby the BIPT can enforce a minimum quality level when certain requirements are not being met. With this law, the Belgian telecom market should comply with, if not exceed, the requirements set by the European Commission.

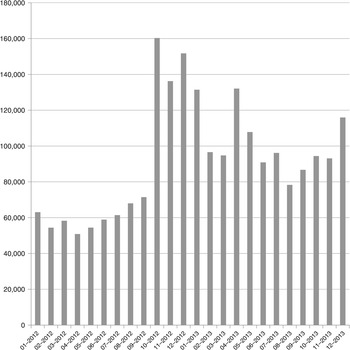

The effect of the telecom law became visible quickly after it was put into force at the beginning of October 2012. The number of ported mobile numbers rose from 71,000 in September to 160,000 in October of that same year (see Figure 5.8). Although the effect slowed down later in the year (136,000 in November, 151,000 in December), it remains significant and demonstrates the impact of telecom regulation in Belgium. This strong increase in ported mobile numbers can be fully attributed to the new telecom law, but certainly also finds a cause in the launch of the competitive King and Kong subscriptions by Telenet, strategically positioned two months before the implementation of the telecom law.

Figure 5.8 Ported mobile numbers per month, Belgium, 2012–2013

The effect on the fixed market was lower, but still significant, with a net increase of about 9,000 ported numbers (an average of 29,038 ported numbers per month before versus an average of 38,131 after the implementation date).

VDSL vectoring or VDSL unbundling?

A final regulatory intervention worth mentioning is the recent withdrawal of the VDSL sub-loop unbundling requirement by the BIPT (CRC, 2011). For VDSL vectoring to function properly (i.e., to effectively cancel out cross-talk) the copper lines connected to the DSLAMs should be handled as one bundle, which would imply the bundle is controlled by the same operator.9 Moreover, the business case for sub-loop unbundling is less attractive as the aggregation point moves lower into the network; hence, it does not attract many OLOs, BIPT has decided to withdraw this obligation in order to stimulate the commercial deployment of VDSL vectoring, thereby ensuring the competitiveness of Belgacom’s DSL with Telenet’s DOCSIS network. Because of the withdrawal of sub-loop unbundling, in the same decision the BIPT enhanced the obligation to provide bitstream by adding multicast functionality and allowing more differentiation possibilities for active access at local and regional level.10

5.3.3 External influences: blocking of 4G by Apple

Besides the regulatory influences, there are some other external influences affecting the telecom market in Flanders and Belgium, including the competitive interplay between the market parties. One salient example of this kind of influence is the impact of Apple blocking 4G access on iPhones. Although the recently launched iPhone 5 supports 4G functionality, it has not been activated in Belgium. Belgacom communicated the following: ʻ4G functionality is currently not activated on these devices making it impossible to use the Proximus 4G network. Apple will decide when 4G will be available for their devices on our network. This also applies to the 4G network of other operators.ʼ (Belgacom, 2013b).

In January 2013 Apple updated the iOS operating system, allowing iPads to surf on the 4G-network but ignored the iPhone. Proximus, the mobile brand of Belgacom, was not aware, nor notified of Apple’s plan and believes it to be a pure commercial decision (Stevens, Reference Stevens2013). Mobistar, on the other hand, is listed as a provider allowed to offer 4G on the iPhone, but they have no 4G network operational yet.

5.4 Realizing the Digital Agenda targets

Concerning the 100% coverage goal of 30 Mbit/s or more, set out by the Digital Agenda for Europe, 98% was reached by the end of 2011: 85% of households via VDSL, 95.5% via the DOCSIS 3.0 technology. Belgium is the leader when it comes to the uptake of high data rate broadband. At the end of 2012, the penetration of fixed broadband amounted to 17.5% of households (Figure 5.9), The second goal, reaching 50% uptake of high-data rate broadband (>=100 Mbit/s) by 2020 is, however, further away: an uptake of 3.4% was reached by the end of 2012.

Figure 5.9 Penetration of fixed broadband ≥30 Mbit/s in Europe, 2012 (in percentage of households)

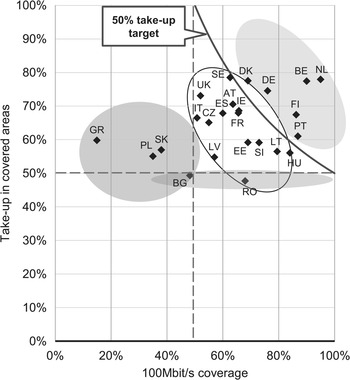

Forecasts, however, are optimistic for Belgium. According to Akama, Belgium ranks tenth globally with observed average data rates of 6.1 Mbit/s and ranks sixth on observed peak data rates of 26.7 Mbit/s (Akamai, 2012). Analysys Mason communicated that Belgium is one of six countries that should reach the 50% uptake goal of high-data rate broadband by 2020 (Figure 5.10). Furthermore, although total revenues in the telecom market decreased in 2012, the percentage of revenues re-invested increased to 17.4%.

Figure 5.10 Forecast likelihood of reaching 100 Mbit/s by 2020, EU

However, the road to reach these targets differs strongly from other countries sharing the same goals. Belgacom communicated its VDSL vectoring strategy to achieve the goals set out in the Digital Agenda to the European Commission (European Commission, 2011), while FttH is more common in other countries. In Belgium, FttH coverage remains small: 0.2% at the end of 2011. Therefore, Belgacom commented that the Commission should assure ʻtechnological neutrality when considering investments in broadband infrastructure in view of reaching the Digital Agendaʼ. They stated that there is too much focus on FttH, while the developments by Alcatel-Lucent clearly indicate that the targets can also be reached with gradual upgrades of VDSL.

Whereas Belgacom reaches data rates of 30 Mbit/s and more, Telenet is far ahead, offering data rates up to 120 Mbit/s using their DOCSIS 3.0 technology, which is available to 95.5% of households.

Although neither operator opts for a revolutionary FttH deployment, the opportunities and possibilities for such a rollout are still being examined by the NRA (Laroy, Reference Laroy2009). This examination includes thorough cost analyses, assessing the relative weight of the trenching costs versus the service provisioning and operational costs, investigating opportunities of synergetic rollout with other utility network owners, as well as assessing the impact of public-private partnerships involving the local municipalities following examples such as the Netherlands. The Belgian NRA proposes to harmonize and standardize the right of way, to stimulate sharing of infrastructure (e.g. empty ducts), to investigate the opportunities of decreasing the price for the last mile (e.g. by allowing aerial deployment or micro-trenching), etc.

5.5 Conclusions and reflections

The status of broadband coverage and uptake in Belgium is at the top of the league in Europe. The country has reached the 2013 goals of the Digital Agenda already. Six of the fifteen ICT goals set in the Digital Agenda for Europe for 2015 were already met in mid-2013 (FOD Economie, 25/06/2013). Positive points are the percentage of broadband connections (58% of the fixed connections have data rates over 30 Mbit/s, 12% are ultrafast broadband with data rates greater than 100 Mbit/s), and widespread computer (98%) and Internet (97%) use. However, there is still room for improvement: the prices for multiple-play offers, as well as for smartphone use (voice, SMS and data), were significantly higher than the European average in 2012 and, although enterprises want to hire ICT experts, they experience difficulties in filling the vacancies.

Although the duopoly between incumbent DSL and DOCSIS operators has brought relatively fast broadband to Flemish consumers, the dominant market position of both players and the lack of more competition keep prices high for end-users. These dominant players rule the price settings and pace of network upgrades, as the barrier to market entry appears to be too high. This phenomenon is especially visible in the fixed market, where the infrastructure assets are important. In the mobile market, competition is fiercer; entry is largely controlled by radio spectrum regulation and through license auctions. Supported by the new telecom law of 2012 (see Section 5.3.2), competition has increased and prices have been significantly reduced over the last year.

Considering the Digital Agenda goals set out by Europe, Belgium is well on the way to reaching them, as multiple sources confirm. However, these goals will most probably be reached without much FttH deployment. Although Belgium holds a leading position in Europe, it is still far behind in comparison to Asian countries such as Korea and Japan. The question then rises as to how important FttH deployment is in the realization of the Digital Agenda for 2020. While its deployment may not be as urgent, will it be inevitable at some point in the future?

Another concern lies with the uptake: although both prominent market players are at the forefront, each with its own technology, the uptake of the high-end subscriptions remains rather low. Should the NRA intervene more to reduce consumer prices, or focus more on raising awareness about the opportunities and possible new applications high-data rate broadband will entail?

References

1 In 1965, Belgium counted 9,428,100 inhabitants. Assuming three people per household, almost one-third of all Belgian households were directly connected to the network.

2 Such a government-driven project cannot be identified in the Walloon region of Belgium.

3 In November 2006 UPC Belgium was taken over by Telenet with, as major advantage for Telenet, the expansion of its geographical region to Brussels and an increase of its subscribers by about 42,000. Starting from 9 July 2007, Telenet offered all its services to the former customers of UPC Belgium.

4 In November 2007 the press reported that Interkabel Vlaanderen and Telenet had concluded a policy agreement on the takeover of distribution of analogue and digital television (INDI) from Interkabel by Telenet. The other large telecom operator in Belgium, Belgacom, reacted by instituting legal proceedings, stating that the auction should be a public one. On 10 June 2008 Belgacom made an offer of EUR 420 million, but this wasn’t sufficient to persuade Interkabel, which decided to accept a final offer of EUR 427 million from Telenet on 28 June 2008 (Van Leemputten, 28/06/Reference Van Leemputten2008; Telenet, 1/10/2008). It is important to note here the role of the competition authority, which watched the development closely: given the complementarity of the coverage of Telenet and Interkabel, there was no problem about the takeover, but this would have been a concern if Belgacom had won the bid.

5 However, there is a lot of skepticism around the phantoming concept, as there are no successful field test results available yet.

6 A full MVNO (Mobile Virtual Network Operator) owns all necessary end-equipment to provide mobile connectivity, and only leases the use of antennas and spectrum from a ‘real’ mobile operator. This allows more flexibility in terms of product offerings and ranges than the light MVNO.

7 BIPT decision of 29 November 2006 on blocks and tie cable tariffs.

8 Decision of 12 November 2008 concerning the addendum NGN/NGA complementing the market analysis of 10 January 2008.

9 In recent publications it is argued that vectoring could work effectively in an unbundled environment.

10 This enhanced form of bitstream is also called Virtual Unbundled Local Access (VULA).