9 United Kingdom

9.1 Introduction to the case study

Like other OECD1 and EU countries, the UK now has a mature broadband market with penetration above 80% of households2. This places the UK ninth in the OECD and sixth in the EU league tables of broadband adoption. Today, the average headline access data rate is around 9.4 Mbit/s, however, the two principal network operators, BT and Virgin Media, have upgraded their networks to offer access data rates of up to 100 Mbit/s in the more densely populated areas of the country. The UK government had the objective of all households having access to at least 2 Mbit/s by 2012, which might be considered unambitious.

Where the UK differs from other countries is that it was the first country to adopt ʻequivalence of inputʼ (EOI) and ʻfunctional separationʼ of the incumbent operator, BT, to enhance competition in the broadband market. The functional separation of BT came about as a result of a set of Undertakings3 signed between BT and the regulator, Ofcom, in 2005, following the Telecoms Strategic Review (TSR). The purpose of EOI and functional separation was to deter BT, which was the dominant provider of unbundled local loops and wholesale broadband access, from discriminating against its retail competitors. At the time of the TSR discrimination, in particular non-price discrimination, was considered a major roadblock to the development of a dynamic broadband market. Such behaviour by the dominant firm may be hard to detect by entrants and regulators, and it may have been the expectation, rather than the experience, of discrimination that concerned rival operators. Nevertheless, Ofcom stated in its second TSR document that competing operators who rely on BT for access ʻhave experienced twenty years of:

Slow product development;

Inferior quality wholesale products;

Poor transactional process; and

A general lack of transparency.ʼ4

Since the adoption of the Undertakings in the UK, other countries, notably Sweden, New Zealand and Australia, have also adopted versions of functional separation, while Italy introduced a form of functional separation in 2002 (see Chapter 10). In 2009 the European Union adopted a revised Framework Directive in which functional separation was included as an exceptional remedy that national regulatory authorities (NRAs) could impose on firms with significant market power (SMP) if all other remedies had not corrected competition problems5.

This case study, therefore, concentrates on Ofcom’s Telecoms Strategic Review and the resulting Undertakings. Section 9.2 describes the state of the broadband market prior to the adoption of the Undertakings in 2005. Section 9.3 examines the TSR, setting out the background to the review; summarising the responses from some of the players in the market; and finally describing the key remedies of equivalence of input (EOI) and ʻfunctional separationʼ defined in the Undertakings. Section 9.4 describes the market today and shows how both the retail and wholesale broadband markets have evolved since the Undertakings. Section 9.5 presents the case conclusions.

9.2 The broadband market before 2005

Broadband was first made commercially available in the United Kingdom in April 1999 by the two cable operators, NTL and Telewest6, although BT did not launch a commercial DSL service until July 2000. BT was relatively late in launching commercial DSL compared with its counterparts in other European countries.

By the first quarter of 2005 (just before the implementation of the Undertakings), penetration had reached 7.25 million lines, 31% of households. The rate of growth was beginning to accelerate, as can be seen in Figure 9.1.

Figure 9.1 Broadband penetration, UK, 2002–2005

Table 9.1 shows the launch date of cable and DSL in the five largest EU member states together with the penetration level by June 2005, by which time the UK had the second-highest level of penetration in this group of countries.

Table 9.1 Broadband launch dates and penetration, UK

At the time, the market was dominated by ISPs who resold BT’s bitstream products. These firms accounted for 46% of all broadband customers. BT and the two cable companies had 1.8 million and 2.1 million customers respectively. The share of the market taken by LLU was very small: just 39,500 customers. The average data rate of broadband access was a little over 1 Mbit/s7.

At the retail level, the market was relatively competitive. No firm had a market share greater than around 24%, which compared well with countries such as France and Germany, where France Telecom and Deutsche Telekom had retail market shares closer to 50%. However, at the wholesale level there was a very different picture. As most retailers relied on BT’s infrastructure to provide services, BT had a wholesale market share of around 70%.

Although the retail market was competitive, the overwhelming reliance of competitors on bitstream products for access meant that they had little if any opportunity to differentiate their products from BT’s. In essence BT set all the parameters of service quality from access data rate to repair times and there was no ability for its rivals to provide a higher quality services. Therefore, BT’s competitors could only compete by charging a lower price, and so needed to have lower retail costs.

Further, BT’s dominant position in the wholesale market and its presence in the retail market led to the potential to discriminate against its downstream rivals, although no such discrimination was ever proven. Discrimination can take either price or non-price forms. Price discrimination refers to the charging of a different price for an essential input to internal and external customers, without any cost-based justification. External customers are usually charged the higher price and so are unable to compete with the vertically integrated firm. Non-price discrimination refers to providing lower quality of service to external customers compared with the integrated firm’s own retail business. Longer installation times, longer repair times and slower product development are all examples of non-price discrimination. This behaviour is designed to advantage the integrated firm and harm its rivals8.

Starting in April 2003, Ofcom’s predecessor, Oftel, conducted an ex ante review of the wholesale broadband access (WBA) market. This review, conducted under the Communications Act 2003, which implemented the European Union’s Common Regulatory Framework (CRF)9, found BT to have significant market power (SMP) in the WBA market and Oftel therefore imposed a number of ex ante obligations on BT in the relevant market. The obligations that a national regulatory authority (NRA) may impose on firms with SMP on the relevant market are set out in Articles 9–15 of the Access Directive (AD).

Two obligations imposed on BT by Oftel are particularly important for the purposes of this case study. First, BT was under an obligation of ʻNo undue discriminationʼ. How the Communications Act 2003 and Oftel interpreted this obligation is central to understanding the actions that Ofcom took as a result of the TSR.

Article 10AD describes the obligation of non-discrimination and consists of two paragraphs:

1. A national regulatory authority may, in accordance with the provisions of Article 8, impose obligations of non-discrimination, in relation to interconnection and/or access.

2. Obligations of non-discrimination shall ensure, in particular, that the [SMP] operator applies equivalent conditions in equivalent circumstances to other undertakings providing equivalent services, and provides services and information to others under the same conditions and of the same quality as it provides for its own services, or those of its subsidiaries or partners.

The CRF was transposed into UK law by the Communications Act 2003, which entered into force on July 23rd 2003. The non-discrimination obligation is set out in Section 87(6)(a) which allows the regulator to impose ʻa condition requiring the dominant provider not to discriminate unduly against particular persons, or against a particular description of persons, in relation to matters connected with network access to the relevant network or with the availability of the relevant facilities.ʼ

In neither the EU Directive nor the UK law is discrimination banned outright. Article 10AD requires only that the operator ʻapplies equivalent conditions in equivalent circumstancesʼ whilst UK law proscribes the dominant provider from ʻunduly discriminatingʼ.

In a document discussing how it intended to impose access obligations under the new regulations, the then-regulator, Oftel, gave guidance as to its interpretation of non-discrimination.10 Perhaps the most significant section is 3.8, which reads:

Non-discrimination’ does not necessarily mean that there should be no differences in treatment between undertakings, rather that any differences should be objectively justifiable, for example by:

a) differences in underlying costs, or

b) no material adverse effect of competition.

In section 3.11 Oftel says that it would find differences in underlying costs to be a valid justification for making different products available on different terms to different parties.

The implication of the above is that BT could legitimately treat external customers differently from its own downstream business if such different treatment was objectively justifiable. Such a difference in treatment would not technically be discriminatory, although it may feel that way to a competing operator.

In 2005 Ofcom, which replaced Oftel as the regulator in 2004, set out guidelines for how it would investigate potential cases of discrimination on competition grounds11. It described undue discrimination as ʻwhen an SMP provider does not reflect relevant differences between (or does not reflect relevant similarities in) the circumstances of customers in the transaction conditions it offers, and where such behaviour could harm competitionʼ (page 7). Ofcom then provides the example of the SMP operator providing different levels of reliability to customers in similar circumstances at the same price ʻand this was capable of harming competition between the two customersʼ. ʻCustomersʼ here includes the downstream division of the vertically integrated SMP provider that competes with an external customer.

Material harm to competition is therefore a critical element of the meaning of discrimination as defined in UK law.

Although BT was never found to have behaved in such a manner, nevertheless and as we shall discuss later, the problem of discrimination became central to Ofcom’s Telecoms Strategic Review and led directly to the obligation in the Undertakings of ʻequivalence of inputʼ.

The second relevant obligation imposed on BT was accounting separation, which is described in Article 11 AD:

A national regulatory authority may, in accordance with the provisions of Article 8, impose obligations for accounting separation in relation to specified activities related to interconnection and/or access.

In particular, a national regulatory authority may require a vertically integrated company to make transparent its wholesale prices and its internal transfer prices inter alia to ensure compliance where there is a requirement for non-discrimination under Article 10 or, where necessary, to prevent unfair cross-subsidy.

The need for accounting separation was described by the Director General of Oftel in his 2003 consultation on financial reporting in which he states:

Financial reporting is an essential part of regulation. As an economic regulator, the Director frequently requires high quality financial information from regulated companies. This is because certain obligations placed on regulated companies require rigorous and effective monitoring in order to ensure compliance and, in the case of non-compliance, allow the Director to take appropriate action.12

One of the specific reasons given for the need for cost accounting is that the SMP operator can demonstrate its compliance with the non-discrimination obligation (para. 2.3). This view is supported by the European Regulators Group (ERG):

Accounting separation should ensure that a vertically integrated company makes transparent its wholesale prices and its internal transfer prices especially where there is a requirement for non-discrimination.13

The ERG makes it clear that the accounting separation obligation exists to counter price discrimination, where an SMP operator charges a higher price externally than it does internally. It is also an instrument to make transparent any inappropriate cross-subsidy, for example between a product subject to competition and a monopoly product allowing the dominant firm to appear to be reducing its costs, and therefore prices, in competitive markets whilst raising them in monopoly markets. Cave and Martin describe the central benefit of accounting separation:

Separate accounting with identical interconnection and internal transfer prices provides the regulator ex post with information about the profitability of wholesale services, and enables him or her to detect abuse of monopoly power in the bottleneck facility by observing and comparing rates of return earned on ‘wholesale’ and ‘retail’ activity.14

Accounting separation has three problems. First, if an upstream monopolist faces different costs to serve its internal and external customers then it may legitimately charge different prices. Secondly, the regulated firm has an incentive to assign costs strategically by over-allocating costs to monopoly parts of the business and reducing costs in the competitive areas. Finally, accounting separation provides no transparency for non-price discrimination. The upstream monopolist still has the incentive to harm its rivals and detection is still difficult.

It is this third problem which was of most concern to competitive operators, and eventually to Ofcom. Whilst accounting separation could make transparent, and therefore deter, price discrimination, it was of no use in preventing non-price discrimination.

9.3 The Telecoms Strategic Review

9.3.1 The market before the review

The UK first introduced competition in the telecoms market in 1984 with the licensing of Mercury Communications as the sole competitor to BT in domestic markets. In return Mercury entered into commitments to develop a domestic trunk network, but relied on BT for local access, except in some business districts. It used the Cable & Wireless international network for overseas calls. In 1985, Oftel determined interconnection prices between the two firms that were initially favourable to Mercury, as a method of supporting entry.

In 1991, following the UK government’s review of the duopoly, this period of ʻmanaged competitionʼʼ drew to an end as other firms were permitted to enter the market. The end of the duopoly allowed cable companies, until then permitted to offer telephony only in partnership with Mercury or BT, to enter the market providing infrastructure-based competition to BT, which was Oftel’s preferred form of competition.

A further policy designed to support infrastructure competition was differential access prices for service-based and infrastructure-based competitors. The former had to buy inputs from BT at discounted retail prices, whilst the latter could buy at lower wholesale rates that were the same as BT charged internally15.

By the time of the review, the UK telecoms market was more competitive than most other markets at the retail level. BT had a market share of around 25% in the retail broadband market, 82% of exchange lines and 60% of fixed traffic16. BT’s strength in the calls market came from ʻother callsʼ (including calls to free dial-up internet access), which accounted for 47% of all minutes and in which BT had a 70% market share. By contrast, BT had only a 34% share of international call minutes, although such calls were only a small part of the market (just 2.3%).

9.3.2 The review

As early as 2002 some players in the telecoms market began to lobby for a strategic review of telecoms regulation and the break-up of BT17. Those who argued for a review believed that the market was being held back by the vertically integrated nature of BT and that separation would increase dynamic competition in retail markets. They argued that investment by competitors was being held back because they expected BT to use its integrated structure to sabotage any product development by rivals, thus preventing investors from earning a reasonable return on any investment. It was not necessary for BT actually to have harmed its rivals for them to change their behaviour; all that was required was an expectation of discrimination to deter investment. Although there is little hard evidence to support the claim that investment was being held back, the very low uptake of LLU can be seen as backing up the claim. In July 2004, there were just 13,000 LLU lines out of a total of 4.4 million broadband access lines.

Ofcom launched the TSR in April 2004 with a first phase consultation document18 in which it set out the purpose of the TSR as to:

assess the options for enhancing value and choice in the UK telecommunications sector. It will have a particular focus on assessing the prospects for maintaining and developing effective competition in the UK telecoms markets, while also considering investment and innovation

Ofcom set out its analysis of the sector looking both at the level of competition at the time and towards the future with an analysis of technology trends. Stakeholders were asked ʻfive fundamental questionsʼ and sixteen more detailed questions. The five fundamental questions were:

In relation to the interests of citizen-consumers, what are the key attributes of a well-functioning telecoms market?

Where can effective and sustainable competition be achieved in the UK telecoms market?

Is there scope for a significant reduction in regulation, or is the market power of incumbents too entrenched?

How can Ofcom incentivise efficient and timely investment in next generation networks?

At varying times since 1984, the case has been made for structural or operational separation of BT, or the delivery of full functional equivalence. Are these still relevant questions?

In the Phase 1 consultation document, Ofcom found a mixed picture of benefits to UK consumers. It found, for example, that whilst there was plenty of competition in the fixed voice market, most of this was based on service provision and that BT still provided most access infrastructure, despite Oftel’s policy of infrastructure competition. Similarly, BT dominated the broadband access market at wholesale level, although the retail market was competitive19. Ofcom’s overall conclusion, therefore, was that the 20 years of competition prior to the TSR resulted in only partial benefits for UK consumers in both residential and business markets.

Responses were received from over eighty interested parties, including fixed and mobile operators, consumer representative organizations, independent experts and individuals with no affiliation. Although the responses were wide ranging, a central theme to emerge was the problem of discrimination and the ineffectiveness of the legal/regulatory regime to prevent such behaviour. Some operators went further and argued that both Article 10AD and the UK law allowed dominant operators to discriminate by not providing equivalent products in equivalent circumstances.

In its response to the TSR, Cable & Wireless, then the UK’s second-largest fixed line operator and which had absorbed Mercury Communications in 1997, stated:

By far the biggest issue for this review is the problem of discrimination as regulating to prevent discrimination remains the key unsolved problem of regulation. Although there are existing regulatory rules and structures to deal with the problem of discrimination, in practice they have been ineffective in preventing BT from favouring its own operations.

The examples of such discrimination are endless. In the world of broadband, BT was allowed to create an LLU20product which was prohibitively expensive, not industrialised and not fit-for-purpose, which meant that it was entirely unsuitable for mass-market take-up. The result is that there is currently virtually no competition in broadband based on LLU. In the world of narrowband voice, there is a similar story to tell. The basic monopoly access network building blocks to narrowband competition, such as call origination, carrier pre-selection and wholesale line rental have all been made available to BT’s competitors on sub-standard terms, such that the cost base of competitors, and the maximum functionality they can offer to customers, are compromised. Again, the result is that BT has been permitted to retain an artificially high market share in narrowband voice to the detriment of innovation and of end-users.21

Energis, another competitor to BT which has subsequently been acquired by Cable & Wireless, discussed the problem of ʻundue discriminationʼ. It stated:

Oftel’s approach to equivalence (in common with many regulators in telecommunications around the world) took as its starting point a formal requirement for equal treatment (or non-discrimination) and then engaged in a series of compromises based on equivalence of outcome to produce the detail of regulatory decisions.

The essence of this approach can be seen in the debate over the use of the term ‘undue’ discrimination. This approach embedded the concept of ‘due’ discrimination in the regulatory regime, allowing differences between the systems that BT used to supply itself, and competitors, where there were ‘objectively justifiable’ differences. The problem with that approach is that it assumed that Oftel would be effectively empowered to distinguish between ‘due’ and ‘undue’ discrimination. While in many cases this approach seems to have worked, in other markets, that hasn’t been the case.22

Energis was established in 1992 by the national electricity transportation network, National Grid. It used National Grid’s network to develop a fibre-optic trunk network which formed the basis of its offering to business customers. Energis, through its subsidiary PlanetOnline, worked with the electronics retailer Dixons to create Freeserve, an Internet service provider (ISP) providing free dial-up Internet access based on an 0800 number. At its peak in 2000, Energis had a stock market valuation of £10 billion, however in July 2002 it was placed into receivership and was acquired by Cable & Wireless in 2005 for a little under £600 million.

The essence of these responses was that preventing discrimination was not enough when the obligation of ʻno undue discriminationʼ allowed justifiably different treatment by the dominant firm of its own downstream business and that of its competitors and allowed different treatment when there was no material effect on competition.

Cable & Wireless’s example of LLU provides a good example. LLU allows competitive operators to rent the copper local loop that runs between the local exchange and the customer premises. The LLU customer needs to install its own equipment in the local exchange to allow broadband signals to be sent over the local loop. It can then sell that service to consumers. BT, like other incumbent operators in their own countries, does not use LLU to provide broadband access themselves. So BT’s retail division was buying a different product from its competitors23.

There was a similar concern with narrowband or traditional voice access products. The externally supplied product is known as wholesale line rental (WLR) and allows a downstream competitor to rent from BT a local exchange line conditioned for voice services. BT itself did not use WLR to provide voice services at the time of the TSR.

Referring back to the legal definitions of discrimination, BT could well argue that differences between internal and external cost and terms were justified and that therefore they were not discriminating under the definition of ʻundue discriminationʼ.

However, such a defence was unnecessary as no discrimination cases were successfully brought against BT: indeed Ofcom did not find explicit evidence of discrimination during its review. What became clear, however, was that competing communications providers (CPs) lacked confidence in a system that allowed BT to duly discriminate as evidenced by the paragraphs from the Cable & Wireless and Energis responses quoted above. The expectation of different treatment was enough to change the behaviour of downstream competitors.

On 18 November 2004, Ofcom issued its Phase 2 consultation document.24 This reviewed the comments received from the first phase and put forward specific proposals for future regulation of the electronic communications market.

Central to Ofcom’s analysis in Phase 2 was the concept of ʻenduring economic bottlenecksʼ (para. 1.17) which it described as those areas of the network where ʻeffective, infrastructure based competition is unlikely to emerge in the medium termʼ. In possibly the most damning paragraph in the Phase 2 consultation, Ofcom said that competing operators who rely on BT for access ʻhave experienced twenty years of:

Slow product development;

Inferior quality wholesale products;

Poor transactional process; and

A general lack of transparency.ʼ

Ofcom concluded that the ʻno undue discriminationʼ remedy by itself had proved inadequate to address the competition problems caused by economic bottlenecks and that a stronger remedy was needed. It partially laid the blame at the door of its predecessor, Oftel.

Oftel’s approach might be characterized as accepting certain differences of outcome which arise from the existence of asymmetrical inputs for BT’s downstream businesses and those of third parties, provided these were not material or deliberately or perversely created by BT to impede competition. Oftel worked to ensure that wholesale products specifically designed by BT under regulatory pressure were as close to being fit-for-purpose as possible. But clearly this approach has not resolved the continuing problems of lack of equality of access in a number of areas. Firstly, BT faces weak incentives to comply and, as a result, the achievement of fit-for-purpose products which BT itself has no interest in using or selling has required a high degree of regulatory intervention. Secondly, the process permits differences between the treatment of BT’s wholesale customers and its own retail activities which, while relatively insignificant in isolation, constitute significant disadvantages when taken in combination.

In the last sentence of this quote, Ofcom discusses what has been referred to as ʻcumulative materialityʼ. This is the idea that it is possible for there to be many minor differences between an internal and an external wholesale product which, when each difference is taken alone, appear unimportant but which when they have a cumulative impact can result in a significant disadvantage for the external customer.

9.3.3 Equivalence of input

Ofcom’s principal proposal arising from the TSR was to strengthen the non-discrimination remedy by requiring what it termed ʻreal equality of accessʼ which would prevent BT having justifiable reasons for providing different services internally and externally. This would require ʻequivalenceʼ at the product level and clear behavioural changes by BT.

At the product level, Ofcom stated that equality of access implies BT’s wholesale customers should have access to:

the same or a similar set of regulated wholesale products as BT’s own retail activities;

at the same prices as BT’s own retail activities; and

using the same or similar transactional processes as BT’s own retail activities. (para. 1.36)

Ofcom termed these characteristics of equality of access ʻequivalence of inputʼ. One purpose of the proposal was to strengthen the incentives for BT to provide fit-for-purpose wholesale products without intrusive regulation.

Ofcom also stated that it was important that there is equivalence throughout the product development process and product life cycle. It implied that BT’s wholesale customers have the same ability as BT’s retail activities to introduce changes or have problems addressed.

The final stage of the TR was the issuing by Ofcom of a ʻStatementʼ including a set of undertakings by BT in lieu of a reference under the Enterprise Act 200225. Paragraph 2 (Definitions and Interpretation) of Annex A sets out what is meant by Equivalence of Input

ʻEquivalence of Inputsʼ or ʻEOIʼ means that BT provides, in respect of a particular product or service, the same product or service to all Communications Providers (including BT) on the same timescales, terms and conditions (including price and service levels) by means of the same systems and processes, and includes the provision to all Communications Providers (including BT) of the same Commercial Information about such products, services, systems and processes. In particular, it includes the use by BT of such systems and processes in the same way as other Communications Providers and with the same degree of reliability and performance as experienced by other Communications Providers.

Since the signing of the original Undertakings a number of amendments have been introduced and brought together in a consolidated version. In this consolidated version ʻsameʼ is helpfully defined as meaning ʻexactly the sameʼ.

Whereas the non-discrimination requirement left room for some degree of ambiguity, the definition of EOI makes it clear that BT must provide exactly the same products internally and externally under the same conditions, etc.

The list of products to which EOI was applied is set out in paragraph 3.1 of the Undertakings. These are:

These products existed at the time of the TSR and were offered by BT in the wholesale market. Thus it can be argued that they had to be reverse engineered to be offered under EOI terms.

However, the Undertakings also commit BT to providing certain (at the time) future services on an EOI basis (para. 3.1). These are listed as:

a) Wholesale Extension Service Access Product;

b) Wholesale Extension Service Backhaul Product;

c) Wholesale End-to-End Ethernet Service;

d) IP based Bitstream Network Access products that are the successors to IPStream or DataStream; and

e) A successor product to Wholesale Line Rental if:

i) such a product is provided using BT’s NGN, based on Multi-Service Access Node (MSAN) access; and

ii) BT is determined by Ofcom to have SMP in a Network Access market or markets which includes that product.

Looking further to what was in 2005 the future, the Undertakings place certain obligations on BT regarding the provision of next-generation networks (NGN). Section 11 of the Undertakings makes it clear that BT will provide network access to its NGN on an EOI basis.

The Undertakings seek to ensure that BT designs-inequivalence of inputs into future products. Thus whilst there may have been a cost associated in ensuring that ʻoldʼ products were made fit for EOI, new products should not incur the same costs.

Ofcom also introduced the concept of ʻequivalence of outcomeʼ which was a weaker form of equivalence, more akin to non-discrimination, and was applied to products that at the time were expected to become redundant as they were overtaken by new services such as those listed above.

The difference between the ex post remedy of non-discrimination applied ex ante and the design of the specific ex ante remedy is central to an understanding of the Undertakings and their impact on the UK telecommunications market.

EOI was and remains a radical change from the ʻno undue discriminationʼ requirement placed on BT in markets where it has SMP. Under the non-discrimination approach, BT did not have to design-in to existing products and processes the equality of treatment of internal and external customers. Each could use a different product and process and differences between the two could be justified, allowing BT to charge different prices or to impose other non-price terms.

BT, or indeed any other incumbent firm, could legitimately argue that its network was built for use by a single integrated firm and was not designed for access by other networks. It was designed to carry calls from the calling party to the receiving party (end-to-end calling) and not to pick up calls or deliver calls to other (national) networks. Therefore, BT could argue that it faced lower costs to deliver a call end-to-end on its own network than to carry calls to or from an interconnected network. Likewise it could argue that it could provide different order-processing systems internally and externally.

Therefore, under the definition of non-discrimination adopted by Ofcom, its treatment of internal and external customers differently was objectively justifiable and therefore not unduly discriminatory. Nevertheless, industry participants and Ofcom determined that the competition policy principle of non-discrimination was not sufficient to stimulate effective and sustainable competition downstream of the economic bottleneck and so a stronger, specifically ex ante remedy was required to overcome the incentive to discriminate.

That remedy, equivalence of input (EOI), requires equal treatment to be designed into products. BT’s commitment in the Undertakings is to provide the ʻsameʼ product, timescales and information with the same degree of reliability. BT is also expected to respond to requests for new services from wholesale customers using the same process: i.e., it should not distinguish between a request from BT Retail and external customers.

There has been no legal testing of equivalence but it would seem unlikely from the unequivocal wording of the Undertakings that BT could claim external customers were not in an ʻanalogous situationʼ to their internal customers.

Equivalence can therefore be regarded as a specifically ex ante approach to redress incentives for discrimination, whereas the ʻno undue discriminationʼ obligation was an ex post remedy applied ex ante.

9.3.4 Functional separation

In the Undertakings, BT also agreed to a change its organization form and incentives for managers. The new organization form became known as ʻfunctional separationʼ though the term itself is not used in the Undertakings. BT made a significant number of commitments, the three most important and relevant of which were to establish:

a separate Access Services business unit with a separate brand name: One of the first deliverables from BT was the establishment of Openreach, a new business unit separated from the rest of BT with responsibility for providing the majority of the input equivalent wholesale products. Although not explicit within the Undertakings, it was a perceived aim of BT, through establishing Openreach, to develop a different culture which treated all of its customers in an equivalent manner. The introduction of Openreach ensured that there was a ʻcleanʼ interface with all the operators competing in the downstream markets and greater transparency for monitoring compliance with the Undertakings;

a Code of Practice for employees: it was obviously essential that the detailed set of commitments made in the Undertakings was understood clearly by the employees affected and so a simple code of practice was needed, backed up by training and support services for employees;

an Equality of Access Board (EAB): this body provided an independent means to monitor the implementation and administration of the Undertakings, to ensure that BT remains compliant with its commitments. Although it is a body internal to BT, its independence comes from the fact that three of its five directors are required to be independent of BT.

The purpose of these organisational changes was to remove the incentive to discriminate and so to facilitate the implementation of equivalence of input. Openreach managers have a set of incentives that are not connected to the overall performance of BT, but only to the performance of Openreach. In theory at least, this should encourage managers only to consider their own division, rather than the effect of their decisions on the profitability of other divisions or the business overall.

9.3.5 Parallel actions

The signing and implementation of the Undertakings were not the only actions taken by Ofcom to attempt to stimulate the take up of LLU and therefore change the competitive dynamics in the UK market. Two other actions were important: Ofcom’s review of the wholesale local access market (WLAM) and the setting up of the Office of Telecoms Adjudication (OTA).

In May 2004, Ofcom began its market review of the WLAM in line with its obligations under the CRF. The review defined the market on technologically neutral grounds such that both copper local loops and the cable access networks fell in the same market definition. Ofcom found BT to have SMP in the relevant market and so imposed a number of ex anteremedies designed to ensure access to local loops by third parties on fair and reasonable terms.

For the purposes of this case study, the most important obligation placed on BT was that of cost orientation. Condition FA3 of the formal Notification required that BT provide network access for a price that was ʻreasonably derived from the costs of provision based on a forward looking long run incremental cost (LRIC) approach and allowing an appropriate mark up for the recovery of common costs including an appropriate return on capital employed.ʼ

To establish the appropriate cost oriented price, Ofcom also investigated BT’s weighted average cost of capital (WACC) calculating a separate WACC for BT’s low-risk local access network business and the rest of the company, and the value of BT’s copper network. Both these consultations provided Ofcom with evidence that allowed it to reduce the price of both fully- and partly- unbundled local loops.

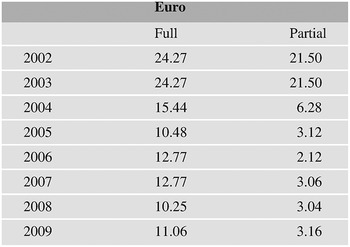

Table 9.2 shows the development of the price of fully- and partially-unbundled loops from 2002–200926. The data show a sharp decline in the monthly rental average cost of the first year between 2003 and 2005 with some fluctuation of charges since then but at prices between one-half and two-thirds of the 2005 price.

Table 9.2 Cost of LLU, UK, 2002–2009

The substantial reduction in the price of unbundled local loops would clearly have a significant impact on the economics of unbundling for competitive operators and may well have been at least as important as the functional separation of BT in encouraging investment by competitors.

The second parallel development was the establishment of the Office of Telecom Adjudicator (OTA) in 2005, now superseded by OTA2. The principal purpose of the OTA was to ensure that the processes for LLU and other ʻcurrent generationʼ access products (for example, wholesale line rental) were industrialised and ʻfit for purposeʼ. It was technically independent of both Ofcom and the industry although its accommodation was provided by Ofcom and its members were representatives of BT and its competitors.

The original OTA was established to ʻfacilitate swift implementation of the processes necessary to enable competitors to gain access to BT’s local loop on an equivalent basis to that enjoyed by BT’s own businesses. The Telecommunications Adjudicator will also be able to bring all parties together to find a prompt mediated resolution of working-level implementation disputes.ʼ

OTA2 has a slightly different objective: ʻOTA2 will facilitate the swift implementation of processes where necessary to enable a wider range of Communications Providers and End Users to benefit from clear and focused improvements, in particular where multi-lateral engagement is necessary.ʼ

The OTA2 website sets out a six point ʻvisionʼ:

the OTA2 will champion end user issues;

Communications Providers will benefit from a competitive telecommunications infrastructure based on Openreach products that has no operational barriers to success;

there will be implementation (as quickly as is reasonably possible) of new product functionality, features and services relating to In-scope Products that will be seamlessly introduced;

migrations between broadband and narrowband products of both BT and other Communications Providers will be seamless, timely and with minimal interruption to service for end users;

dips in operational quality performance of In-scope Products provided by Openreach will be unusual and will be proactively managed by Openreach to ensure the least impact on Communications Providers and end users; and

participation by Communications Providers in the OTA2 Scheme will be widespread and representative.

Although OTA2 mentions end users in its objectives, the scheme participants are all drawn from the supply side of the market with no user representatives. The main scheme participants are the larger communications providers: BT, Openreach, BSkyB, Cable & Wireless, Everything Everywhere, Exponential-e, Global Crossing, O2, Scottish and Southern, TalkTalk Group and Virgin Media. Smaller communications providers are represented through the Federation of Communications Services.

Equivalence of inputs and functional separation, reduced LLU prices and the OTA can be seen as a three-pronged strategy to encourage the development of LLU as the principal wholesale product for broadband access. It may not be possible to separate the effectiveness of any one part of the strategy and of course it may be that the three together were critical to ensure increased adoption of LLU. In the next section of this case study we examine the UK broadband market today, at both the retail and wholesale levels.

9.4 The broadband market today

9.4.1 The retail market

Broadband penetration has increased substantially since July 2005 and now stands at 22.1 million lines or 83.7% of households27. This level of household penetration places the UK ninth in the OECD countries and 6th in the EU, behind Sweden, the Netherlands, Denmark, Finland and Luxembourg. South Korea, Iceland and Norway also have higher levels of household penetration than the UK.

Figure 9.2 below extends Figure 9.1 to cover the period 2002–2013. A comparison of the rate of growth of broadband lines in the UK before and after the Undertakings shows no significant difference: diffusion of broadband continues to show the classic ʻSʼ shaped growth. There appears to be a slowdown in the growth of broadband in the wake of the 2008 financial crisis, with growth resuming in late 2010.

Figure 9.2 Broadband Penetration, UK, 2002–2013

The retail broadband market has also seen substantial consolidation amongst suppliers. The four largest suppliers (BT, Sky, TalkTalk and Virgin Media) now have a combined market share in excess of 90%. At the time of the Undertakings, neither Sky nor TalkTalk was a significant player in the retail market, so both have entered the market on the back of an improved climate for LLU.

Sky’s market growth has been largely organic, benefiting from its strong position in the Pay-TV market to cross sell broadband to its existing customer base. TalkTalk Group, by contrast, has been acquisitive, acquiring the UK customer bases of AOL and Tiscali.

Table 9.3 shows various acquisitions that have taken place in the market over the period 2006–2009.

Table 9.3 Selected ISP mergers, UK, 2006–2013

Ofcom explains the spate of mergers and acquisitions in the sector by the increased need for scale as a result of the increase in the uptake of LLU. For each unbundled exchange, the unit costs fall with each additional subscriber, meaning that scale is important for an ISP operator to be profitable, compared with using wholesale bitstream products from BT.

Whilst consumers’ choice of supplier may have diminished since 2006, consumers have benefited from an increase in the average connection speeds available.

Figure 9.3 shows the average actual broadband data rates for the period 2009–2013, which has grown steadily from 4 Mbit/s in 2009 to over 14 Mbit/s in 2013. Between 2012 and 2013 there was an exceptionally large increase in actual access data rates as more customers signed up to ʻsuperfastʼ broadband products based on fibre to the cabinet or DOCSIS3.

Figure 9.3 Average broadband connection data rates, UK, 2009–2013

This increase in average connection data rates has largely been driven by the upgrade of DSL lines from ADSL to ADSL2+ and by the upgrade of the Virgin Media cable network to DOCSIS3.

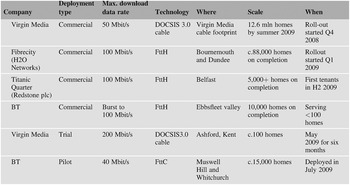

Table 9.4 below shows a selection of super-fast broadband implementations and trials as identified by Ofcom in July 2009.

Table 9.4 Selected super-fast broadband implementations and trials, UK, July 2009

Since July 2009, there have been a number of further announcements, in particular by BT and Virgin Media.

In October 2010, Virgin Media announced plans to upgrade to 100 Mbit/s from December 2010 with the entire network being upgraded by mid-201229. In March 2011, Virgin Media announced that its 100 Mbit/s service had passed one million homes and was on track to meet the 2012 deadline. In November 2013, Virgin Media announced plans to increase the access data rate to over 150 Mbit/s to all of the 12.5 million homes its network passes in 201430.

BT has responded to Virgin Media’s various upgrades, and arguably to political pressure, by launching Fibre to the Home (FttH) and Fibre to the Cabinet (FttC) products, which it retails under the brand ʻInfinityʼ. This fibre based service provides access data rates of up to 40 Mbit/s. Infinity was first trialled in exchanges in London, Cheshire and Glasgow and in January 2014 was available in around 1,900 local exchange areas covering over 75% of UK homes31.

In January 2013, according to the EC Broadband Scorecard, 14.5% of broadband lines provided data rates of 30 Mbit/s up to 99 Mbit/s, while 0.9% provided data rates of 100 Mbit/s or above.

9.4.2 Broadband services

With the growth in the average access data rate has come a change in how the Internet is used. One of the most important applications that demands high bandwidth is ʻcatch-up TVʼ, through services such as BBC i-player, and the equivalent from the other TV channels, which has enjoyed particularly strong growth. In March 2013, there were 272 million requests for TV and radio programmes on BBC i-Player, up from 78 million in 200932. Equivalent data on ITV Player were not available.

BT has also entered the TV market offering IPTV over its FttC/H network. In 2013 BT secured the rights to show Champions League football matches live with a bid of over £800 million putting it squarely in competition with Sky’s and Virgin Media’s TV offerings. In fact, over 2013 there has been a noticeable shift in the locus of competition in broadband markets from Internet access to TV, with products such as ʻSky plusʼ and Virgin Media’s TiVo becoming increasingly popular.

9.4.3 The wholesale market

Whilst there have been many changes in the retail market, it is perhaps the wholesale market that has seen most change since the Undertakings were signed.

In 2006, 2010 and 2013, Ofcom conducted market reviews of the wholesale broadband access (WBA) market . This market lies at the intermediate level between the wholesale local access market (WLAM) and the retail broadband market (RBM). Whereas BT and Virgin Media self-supply the whole broadband value chain, most other ISPs operate only in the WBAM or retail market. LLU operators enter at the WBA level, buying unbundled local loops as their input, while retail ISPs enter at the retail level, buy bitstream access either from BT or an LLU provider that operates in the WBA market, as illustrated in Figure 9.4. It should though be noted that most LLU operators also buy bitstream access from BT in areas where it is uneconomic for them to place their own equipment in exchanges and purchase unbundled loops.

Figure 9.4 Broadband market structure, UK, 2013

Legend: WNIA: Wholesale Network Infrastructure Access (Market 4 in the EC 2007 Recommendation); WBA: Wholesale Broadband Access (Market 5); RBA: Retail Broadband Access (not included in the 2007 Recommendation); VM: Virgin Media (the cable operator).

When Ofcom’s predecessor, Oftel, first reviewed the WBAM in 2003, it was only able to identify one national market33 and Oftel found BT to have SMP in that market. By the time Ofcom reviewed the market again in 2006 and 2010, it found there to be three geographic markets based on the number of LLU operators plus Virgin Media present in exchange area. According to the 2010 market definition the three markets are defined as:

Market 1: exchanges where only BT is present (11.7% of premises);

Market 2: exchanges where two Principal Operators (POs) are present or forecast and exchanges where three POs are present or forecast but where BTs share is greater than or equal to 50 per cent (10.0% of premises); and

Market 3: exchanges where four or more POs are present or forecast and exchanges where three POs are present or forecast but where BTs share is less than 50 per cent (77.6% of premises).

In the final statement Ofcom found BT to have SMP in Markets one and two, but no firm was found to have SMP in Market 3. This means that in exchange areas covering more than three quarters of all premises, BT is no longer dominant. Although the market definitions and size of the markets was somewhat different in the 2006 WBAM review, the finding of SMP was the same.

By 2013, the market had developed yet further and Ofcom found only two markets:

Market A: exchange areas where there are no more than two Principal Operators (POs) present or forecast to be present, which accounts for 9.6% of UK premises.

Market B: exchange areas where there are three or more POs present or forecast to be present, which accounts for 89.7% of UK premises34.

This finding is a major change from the 2003 market review. Ofcom found that effectively competitive markets were operating below the retail level and thus the retail market in some 90% of the UK was not dependent on regulation at the wholesale level, albeit it is dependent on regulation at the LLU level.

This change in the market structure, and thus the finding of SMP, has come about because ISPs have substituted LLU for bitstream or wholesale access. TalkTalk Group now has over 2,700 exchanges enabled, covering some 24 million homes within 5 km from the exchange, 97% of all households. Sky has enabled over 2,300 exchanges covering 23.3 million homes within 5 km35.

Figure 9.5 shows the number of wholesale copper access lines, i.e., those not offered by BT, by type: resale, bitstream and LLU. Resale lines peaked in January 2007 as LLU began to take an increasing share of the market. Until January 2006 almost no customers accessed broadband via LLU, but by January 2008 LLU was the most popular single method of wholesale copper access and by July 2010 two-thirds of wholesale copper access lines were via LLU. In July 2010 some 29% of all retail access lines were via LLU, whilst bitstream and resale combined reached around 22%.

Figure 9.5 Wholesale copper access methods, UK, 2002–2009

Over the same period, cable’s share of the market has declined from 59% to 20%. In part, this decline is due to BT extending its broadband availability to around 99% of homes whilst cable still only reaches about 55% of homes: BT’s larger physical reach ensures that twisted copper wire has been able to gain a larger market share.

What we have seen in the UK therefore is a dramatic change in the nature of competition from one based on a mix of cable and the reselling of BT’s bitstream products, to one where LLU has a significant and growing market share with unbundled loops largely replacing bitstream.

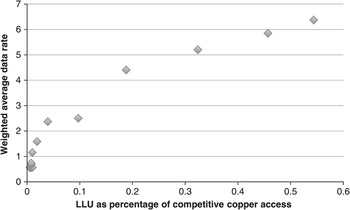

This change in the wholesale market is important as LLU allows ISPs considerably more control over their own products. Whilst care should always be taken over simple correlations, especially over time, Figure 9.6 shows a strong correlation between LLU as a share of all competitive copper access lines and the weighted average access data rate enjoyed by users. However, it should be noted that the greatest percentage increase in access data rates happen when LLU had only a very low market share (less than 10%).

9.6 Relationship between LLU and average access data rate, UK, 2002–2008

9.5 Conclusions

During the decade 2000–2010, the UK broadband market has experienced substantial changes. Cable broadband was launched in 1999 and a DSL version with a wholesale variant was not available until 2000. The few customers who took up broadband could only get access data rates of 512 kbit/s. Today, over 80% of households have a fixed broadband connection and the market is still growing, although the rate of growth has slowed. Access data rates of up to 100 Mbit/s are available to all households passed by the Virgin Media network and rates of at least 40 Mbit/s to around 85% of households passed by the BT FttH/C network.

Until 2005 the broadband market was relatively undynamic: other than Virgin Media, BT’s rivals relied on BT’s wholesale bitstream products which meant that they could not differentiate the service quality they offered customers. Local loop unbundling (LLU) had hardly been taken up in 2005, with just a few tens of thousands of lines unbundled. However, access via bitstream meant that barriers to entry were low and so the retail market was fragmented compared with many other countries which had a retail market dominated by the incumbent operator.

The market today is very different. LLU is now prevalent throughout the country and the level of competition in the WBA market is such that Ofcom has been able to find exchange areas covering some 90% of the population free from a firm with significant market power. This change has largely come about because Ofcom forced through three key regulatory changes in 2005: EOI and the functional separation of BT; reduced LLU prices and the creation of the OTA with a brief to make LLU work.

Since that time we can see a ʻvirtuous circleʼ evolving as LLU-based ISPs installed more advanced DSLAMs, based on ADSL2+ and ADSL Max, allowing them to offer access data rates of up to 24 Mbit/s. Both BT and Virgin Media have responded to this competitive pressure by investing in FttC/H and DOCSIS3.0 respectively, allowing them to offer ʻsuper-fastʼ broadband. As higher data access rates have become available, Internet usage has changed to take advantage of this higher bandwidth, with catch-up TV being a particularly popular application.

The rate of diffusion of broadband amongst UK consumers appears to have been hardly affected by the regulatory changes of 2005. However, there have been a number of fundamental changes in the structure of the market and the quality of services available to consumers since 2005.

The regulatory reforms introduced by Ofcom in 2005 can be said to mark the watershed between the relatively undynamic early days of broadband and the more dynamic second half of the decade. What cannot be concluded with any degree of certainty is the effect any individual reform had or whether it was the package of the three reforms together that helped change the market. The much-heralded reform of EOI and functional separation may have been necessary but there is insufficient evidence to know whether it would have been sufficient in the absence of lower prices and the OTA. What can be concluded with certainty, however, is that UK consumers today enjoy the advantages of a highly competitive market, much higher data access rates and a lower price per Mbit/s than their predecessors did in 2000 or indeed 2005.

1 Organisation for Economic Co-operation and Development (OECD).

2 Source: Ofcom, ‘Telecommunications Market Data Update, Q2 2013.

3 Ofcom Final statements on the Strategic Review of Telecommunications, and undertakings in lieu of a reference under the Enterprise Act 2002, 22 September 2005.

4 Ofcom Strategic Review of Telecommunications: Phase 2 Consultation Document, (para. 1.19).

5 Directive 2002/19/EC of the European Parliament and of the Council of 7 March 2002 on access to, and interconnection of, electronic communications networks and associated facilities (Access Directive) as amended by Directive 2009/140/EC, Article 13a.

6 These two companies have since merged to form Virgin Media.

7 Source: Ofcom, author’s calculation.

8 There has been substantial academic analysis on the incentives of vertically integrated firms with upstream market to harm their rivals in downstream markets. For a good discussion in the context of the UK telecoms sector, see , and (2006), Regulating for non-price discrimination: The case of UK fixed telecoms, in Competition and Regulation in Network Industries 2006 (3).

9 The CRF is a set of five Directives designed to establish a consistent regulatory process across the EU based on the principles of competition law, although with market investigations, or ʻreviewsʼ conducted ex ante.

10 Oftel (2002) Imposing Access Obligations under the new EU Directives,sections 3.4–3.11.

11 (2005) Undue discrimination by SMP providers: How Ofcom will investigate potential contraventions on competition grounds of Requirements not to unduly discriminate imposed on SMP providers.

12 (2003) Financial Reporting Obligations in SMP Markets: A consultation on accounting separation and cost accounting, para. 2.1.

13 (2003) ERG Common Position on the approach to Appropriate remedies in the new regulatory framework, page 49.

14 M. Cave and I. Martin (1994), The costs and benefits of accounting separation Telecommunications Policy 18 (1), 12–20.

15 For a more detailed analysis of competition before the TSR, see and (1996) Entry, Competition and Regulation in UK Telecommunications, Oxford Review of Economic Policy,12 (4), 100–121.

16 Source: Ofcom Telecoms Market Data Tables, Q2 2005.

17 Notably Cable & Wireless, for whom the author worked as a consultant on a project related to the separation of BT.

18 (2004) Strategic Review of Telecommunications: Phase 1 Consultation Document.

19 Ibid, page 22.

20 Local Loop Unbundling.

21 Cable & Wireless Response to the Ofcom ʻStrategic Review of Telecommunications Phase 1 consultation documentʼ.

22 Energis Response to the Ofcom ʻStrategic Review of Telecommunications Phase 1ʼconsultation document.

23 Ofcom also agreed with this statement by C&W. In the Phase 2 consultation document it said ʻWe believe that similar stories could be told about carrier pre-selection, wholesale line rental, partial private circuits and indirect access in their early daysʼ (para. 6.3).

24 Ofcom Strategic Review of Telecommunications: Phase 2 Consultation Document.

25 Ofcom (2005) ʻStatementʼ (see note 3).

26 Data source: European Commission Implementation Reports 2003–2009. These prices are shown in euro in the Implementation Report. Prices have been converted to Sterling and then back to euro using the average exchange rate for the period.

27 Source: Ofcom, Telecommunications Market Data Update, Q2 2013.

28 Note: Sky acquired only O2?s domestic UK broadband business and not the mobile network.

29 Virgin Media press release 27 October 2010.

30 Virgin Media Press Release 11 November 2013.

31 Source: SamKnows. Website www.samknows.com checked 24 January 2014.

32 Source: BBC i-player Monthly Performance Pack, March 2013.

33 For historic reasons the city of Kingston upon Hull in northeast England has never been part of the BT network. Therefore Oftel in fact found two geographic markets, ʻthe Hull areaʼ and the rest of the UK. For the purposes of this case study, however, we shall ignore the Hull area.

34 Source: Ofcom, Review of wholesale broadband access markets 1 August 2013. The Hull area accounts for the remaining 1.3% of households.

35 Source: www.samknows.com.