Refine search

Actions for selected content:

3876 results in Optimization

AN ANALYTICAL APPROXIMATION FORMULA FOR THE PRICING OF CREDIT DEFAULT SWAPS WITH REGIME SWITCHING

- Part of

-

- Journal:

- The ANZIAM Journal / Volume 63 / Issue 2 / April 2021

- Published online by Cambridge University Press:

- 02 September 2021, pp. 143-162

-

- Article

- Export citation

SPECTRALLY ACCURATE OPTION PRICING UNDER THE TIME-FRACTIONAL BLACK–SCHOLES MODEL

- Part of

-

- Journal:

- The ANZIAM Journal / Volume 63 / Issue 2 / April 2021

- Published online by Cambridge University Press:

- 25 August 2021, pp. 228-248

-

- Article

- Export citation

-

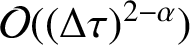

We propose a Legendre–Laguerre spectral approximation to price the European and double barrier options in the time-fractional framework. By choosing an appropriate basis function, the spectral discretization is used for the approximation of the spatial derivatives of the time-fractional Black–Scholes equation. For the time discretization, we consider the popular

$L1$ finite difference approximation, which converges with order

$L1$ finite difference approximation, which converges with order  $\mathcal {O}((\Delta \tau )^{2-\alpha })$ for functions which are twice continuously differentiable. However, when using the

$\mathcal {O}((\Delta \tau )^{2-\alpha })$ for functions which are twice continuously differentiable. However, when using the  $L1$ scheme for problems with nonsmooth initial data, only the first-order accuracy in time is achieved. This low-order accuracy is also observed when solving the time-fractional Black–Scholes European and barrier option pricing problems for which the payoffs are all nonsmooth. To increase the temporal convergence rate, we therefore consider a Richardson extrapolation method, which when combined with the spectral approximation in space, exhibits higher order convergence such that high accuracies over the whole discretization grid are obtained. Compared with the traditional finite difference scheme, numerical examples clearly indicate that the spectral approximation converges exponentially over a small number of grid points. Also, as demonstrated, such high accuracies can be achieved in much fewer time steps using the extrapolation approach.

$L1$ scheme for problems with nonsmooth initial data, only the first-order accuracy in time is achieved. This low-order accuracy is also observed when solving the time-fractional Black–Scholes European and barrier option pricing problems for which the payoffs are all nonsmooth. To increase the temporal convergence rate, we therefore consider a Richardson extrapolation method, which when combined with the spectral approximation in space, exhibits higher order convergence such that high accuracies over the whole discretization grid are obtained. Compared with the traditional finite difference scheme, numerical examples clearly indicate that the spectral approximation converges exponentially over a small number of grid points. Also, as demonstrated, such high accuracies can be achieved in much fewer time steps using the extrapolation approach.

AN ANALYTICAL OPTION PRICING FORMULA FOR MEAN-REVERTING ASSET WITH TIME-DEPENDENT PARAMETER

- Part of

-

- Journal:

- The ANZIAM Journal / Volume 63 / Issue 2 / April 2021

- Published online by Cambridge University Press:

- 23 August 2021, pp. 178-202

-

- Article

- Export citation

PRICING TIMER OPTIONS: SECOND-ORDER MULTISCALE STOCHASTIC VOLATILITY ASYMPTOTICS

- Part of

-

- Journal:

- The ANZIAM Journal / Volume 63 / Issue 2 / April 2021

- Published online by Cambridge University Press:

- 23 August 2021, pp. 249-267

-

- Article

- Export citation

FINITE MATURITY AMERICAN-STYLE STOCK LOANS WITH REGIME-SWITCHING VOLATILITY

- Part of

-

- Journal:

- The ANZIAM Journal / Volume 63 / Issue 2 / April 2021

- Published online by Cambridge University Press:

- 19 August 2021, pp. 163-177

-

- Article

- Export citation

LOCALIZED RADIAL BASIS FUNCTIONS FOR NO-ARBITRAGE PRICING OF OPTIONS UNDER STOCHASTIC ALPHA–BETA–RHO DYNAMICS

- Part of

-

- Journal:

- The ANZIAM Journal / Volume 63 / Issue 2 / April 2021

- Published online by Cambridge University Press:

- 19 August 2021, pp. 203-227

-

- Article

- Export citation

OPTION PRICING UNDER THE FRACTIONAL STOCHASTIC VOLATILITY MODEL

- Part of

-

- Journal:

- The ANZIAM Journal / Volume 63 / Issue 2 / April 2021

- Published online by Cambridge University Press:

- 13 August 2021, pp. 123-142

-

- Article

- Export citation

A NOTE ON THE AXISYMMETRIC DIFFUSION EQUATION

- Part of

-

- Journal:

- The ANZIAM Journal / Volume 63 / Issue 3 / July 2021

- Published online by Cambridge University Press:

- 21 July 2021, pp. 333-341

-

- Article

- Export citation

-

We consider the explicit solution to the axisymmetric diffusion equation. We recast the solution in the form of a Mellin inversion formula, and outline a method to compute a formula for

$u(r,t)$ as a series using the Cauchy residue theorem. As a consequence, we are able to represent the solution to the axisymmetric diffusion equation as a rapidly converging series.

$u(r,t)$ as a series using the Cauchy residue theorem. As a consequence, we are able to represent the solution to the axisymmetric diffusion equation as a rapidly converging series.

OPTIMAL PORTFOLIO AND CONSUMPTION FOR A MARKOVIAN REGIME-SWITCHING JUMP-DIFFUSION PROCESS

- Part of

-

- Journal:

- The ANZIAM Journal / Volume 63 / Issue 3 / July 2021

- Published online by Cambridge University Press:

- 21 July 2021, pp. 308-332

-

- Article

- Export citation

Design Optimization using MATLAB and SOLIDWORKS

-

- Published online:

- 17 July 2021

- Print publication:

- 29 April 2021

-

- Textbook

- Export citation

ANZ VOLUME 63 ISSUE 1 COVER AND BACK MATTER

-

- Journal:

- The ANZIAM Journal / Volume 63 / Issue 1 / January 2021

- Published online by Cambridge University Press:

- 30 June 2021, pp. b1-b6

-

- Article

-

- You have access

- Export citation

ANZ VOLUME 63 ISSUE 1 COVER AND FRONT MATTER

-

- Journal:

- The ANZIAM Journal / Volume 63 / Issue 1 / January 2021

- Published online by Cambridge University Press:

- 30 June 2021, pp. f1-f2

-

- Article

-

- You have access

- Export citation

Advanced Optimization for Process Systems Engineering

-

- Published online:

- 11 June 2021

- Print publication:

- 25 March 2021

-

- Textbook

- Export citation

ASYMMETRICAL CELL DIVISION WITH EXPONENTIAL GROWTH

- Part of

-

- Journal:

- The ANZIAM Journal / Volume 63 / Issue 1 / January 2021

- Published online by Cambridge University Press:

- 04 June 2021, pp. 70-83

-

- Article

- Export citation

ANALYSIS OF CELL TRANSMISSION MODEL FOR TRAFFIC FLOW SIMULATION WITH APPLICATION TO NETWORK TRAFFIC

- Part of

-

- Journal:

- The ANZIAM Journal / Volume 63 / Issue 1 / January 2021

- Published online by Cambridge University Press:

- 18 May 2021, pp. 84-99

-

- Article

- Export citation

SLOW-BURNING INSTABILITIES OF DUFORT–FRANKEL FINITE DIFFERENCING

- Part of

-

- Journal:

- The ANZIAM Journal / Volume 63 / Issue 1 / January 2021

- Published online by Cambridge University Press:

- 30 April 2021, pp. 23-38

-

- Article

- Export citation

9 - Truss Analysis

-

- Book:

- Design Optimization using MATLAB and SOLIDWORKS

- Published online:

- 17 July 2021

- Print publication:

- 29 April 2021, pp 209-234

-

- Chapter

- Export citation

5 - Unconstrained Optimization: Algorithms

-

- Book:

- Design Optimization using MATLAB and SOLIDWORKS

- Published online:

- 17 July 2021

- Print publication:

- 29 April 2021, pp 79-125

-

- Chapter

- Export citation

EFFICIENT COMPUTATION OF COORDINATE-FREE MODELS OF FLAME FRONTS

- Part of

-

- Journal:

- The ANZIAM Journal / Volume 63 / Issue 1 / January 2021

- Published online by Cambridge University Press:

- 29 April 2021, pp. 58-69

-

- Article

- Export citation

14 - Finite Element Analysis in 3D

-

- Book:

- Design Optimization using MATLAB and SOLIDWORKS

- Published online:

- 17 July 2021

- Print publication:

- 29 April 2021, pp 332-342

-

- Chapter

- Export citation